Submitted electronically via Open to Comments page on IFRS Foundation website

|

|

|

- Jonathan Park

- 8 years ago

- Views:

Transcription

1 Submitted electronically via Open to Comments page on IFRS Foundation website IFRS Foundation IASB 30 Canon street London, EC4M 6XH United Kingdom Amsterdam, 20 November 2012 Ref: B Subject: Eumedion s response to IASB s Request for Information on Post-Implementation Review: IFRS 8 Operating Segments Dear Sirs, Madams, Eumedion welcomes the opportunity to respond to IASB s request for information on the postimplementation review of IFRS 8. By way of background, Eumedion is the Dutch based corporate governance forum for institutional investors. Our 70 Dutch and non-dutch participants together have more than EUR 1 trillion assets under management. They invest for their clients and their beneficiaries in listed companies worldwide. Our views therefore represent a perspective of users of financial statements. The comments submitted in this response are to complement the comments and views discussed in the meeting of 14 September 2012 where representatives of IASB, EFRAG and ESMA jointly discussed IFRS 8 with a group of participants of Eumedion. We regard the potential relevance of segment reporting as very high for investors. Our answers do not only highlight a number of issues, but also contain some suggestions for improvements to the standard. 1

2 Answers to the questions in the Request for Information Question 1: Are you comparing IFRS 8 with IAS 14 or with a different, earlier segment-reporting Standard that is specific to your jurisdiction? In providing this information, please tell us: (a) what your current job title is; (b) what your principal jurisdiction is; and (c) whether your jurisdiction or company is a recent adopter of IFRSs. Eumedion is a corporate governance platform with a focus on the largest 75 listed companies incorporated in the Netherlands, although our participants tend to invest in many jurisdictions. The Netherlands is not a recent adopter of IFRS. Question 2: What is your experience of the effect of the IASB s decision to identify and report segments using the management perspective? Investors: please focus on whether our initial assessment - that the management perspective would allow you to better understand the business - was correct. What effect has IFRS 8 had on your ability to understand the business and to predict results? IAS 14, the preceding standard, relied on segmentation based on risk and return characteristics. Risk and return characteristics typically are factors that tend to be in line with the perspective of investors. If risk and return characteristics are significantly different between two activities, we would tend to prefer a separate operating segment for each activity even though through the eyes of management they may be managed as one; and reversely, if risk and return characteristics are not significantly different between two activities, we would tend to prefer the activities to be aggregated into a single segment, even though through the eyes of management they may be dissimilar. Segment reporting is more useful if the output can be compared with previous years, not just the previous year. We believe that the risk and return assessment for segment definition in the preceding standard is more likely to result in a more stable segment definition than the through the eyes of management perspective in IFRS 8. If there is no significant change in the risk and return characteristics of the segments, in many cases, we would prefer a company to keep the segment definitions identical, even if there is a change in how management manages its business segments. Matrix segmentation (introduced by IFRS 8) reduced usefulness We believe matrix segmentation, where the segments are a mix of different types of segments (for example geographical and business segments mixed in one table), tends to reduce usefulness for investors: 2

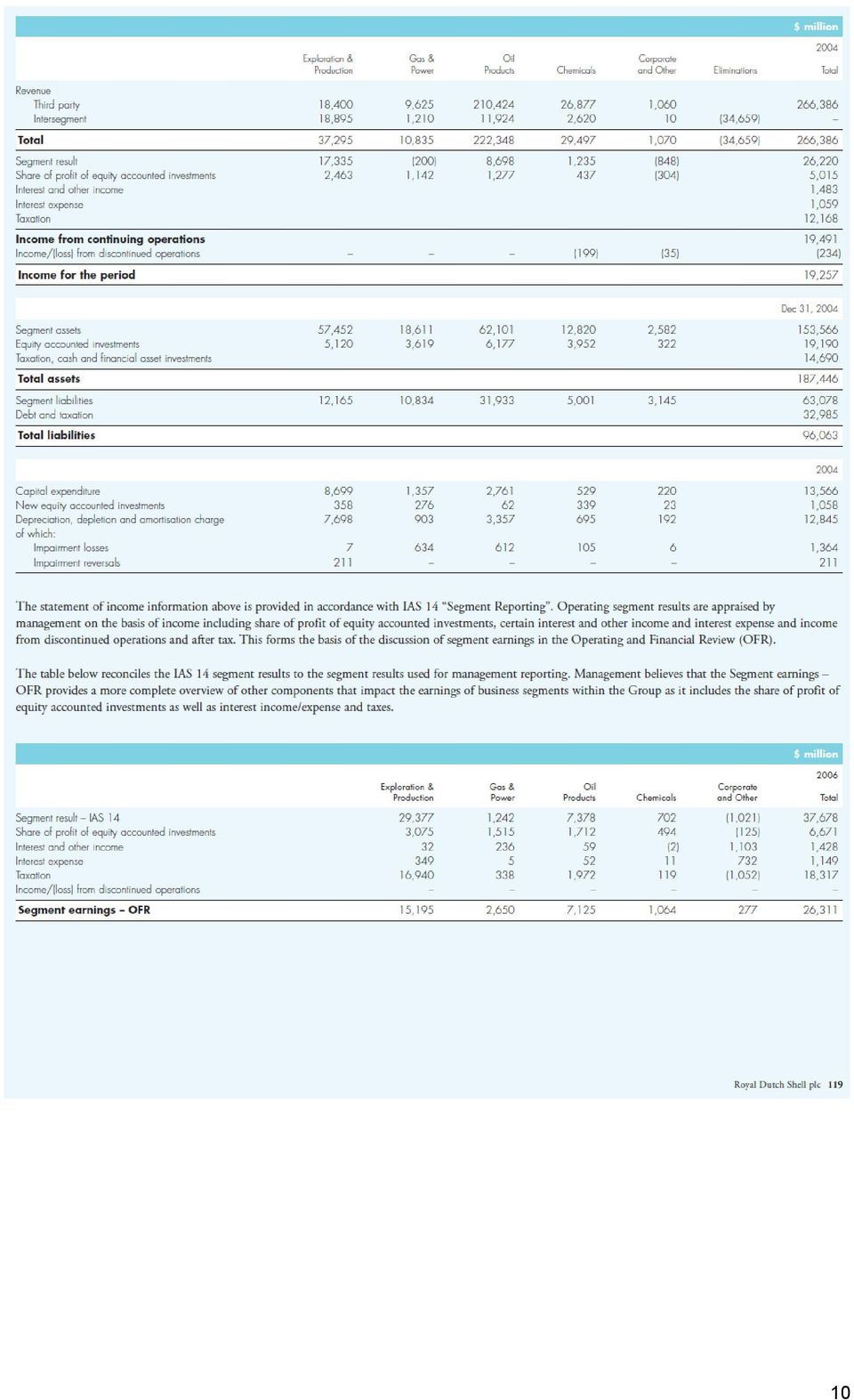

3 Segment reporting is more useful if the output can be compared with direct competitors. Matrix segmentation tends to result in very company specific output that is significantly more difficult, if not impossible, to compare amongst direct competitors. We have reason to believe that matrix segment reporting also more often results in changes, making multi-year comparison more difficult. Through the eyes of management perspective too often results in lack of granularity in segment definition There is a wide variety of quality in segment definition. Unfortunately, too often the segment definition is not granular enough for investors. We observed many companies distinguishing only two operating segments. Some companies provide a higher, and more useful, granularity outside the annual report. For example, the listed company Royal Dutch Shell provides such higher granularity not only in investor presentations, but also in an Investor s handbook and in quarterly updated Excel files. A disadvantage of only having a higher granularity in the investor material and not in the annual report is that such information tends to fall outside the scope of an external audit. In general, the terms used in investor presentations by companies often are not as clearly defined as the line-items in the annual report. Royal Dutch Shell reported five operating segments under IAS 14 in Although the introduction of IFRS 8 initially increased the number of segments in 2007, in 2009 a change in how management views the company reduced the number of operating segments to only 3 1 ; this clearly resulted in a less useful segment reporting in the annual report for investors. The fact that some companies have reduced the number of operating segments is not necessarily an enforcement issue, as the reduction in usefulness may be inherent to the standard s management perspective. In general, Eumedion worries that the significant discretion management has to define and redefine segments through the eyes of management, has resulted in a standard where possible sub-par reporting is too difficult for external auditors and public enforcers to act on. We believe that the management perspective introduced by IFRS 8 for segment definition did not contribute to improved understanding of the business by investors. Question 3: How has the use of non-ifrs measurements affected the reporting of operating segments? Investors: please comment on the effect that the use of non-ifrs measurements has had on your ability to understand the operating risks involved in managing a specific business and the operating performance of that business. It would be particularly helpful if you can provide examples from published financial statements to illustrate your observations and enable us to understand the effects that you describe. 1 Appendix: Royal Dutch Shell segment reporting 2006 versus

4 Reconciliation to IFRS numbers We believe non-ifrs line items in segment reporting could provide, and often does provide useful information to investors. However, in practice we observe a high number of companies that present line items that are identical to the line items in the primary statements. We believe many investors are not aware that the through the eyes of management perspective effectively allows management to allocate certain charges to an other/eliminations segment to an extent that may be well beyond what is true and fair from an investor perspective, and still claim full compliance with the standard. Since the net effect of such a practice is nil, it remains undetected in the column that reconciles the numbers to IFRS. Therefore, investors remain uncertain how useful the presented segment reporting really is. We also observe many instances where the column that would provide a reconciliation from through the eyes of management to the IFRS numbers, is missing. As this will be interpreted by many investors that the reported line item is IFRS compliant in all of the individual columns, a revised standard could explicitly require such compliance with IFRS if a reporting entity chooses not to include such column. Another suggestion we would like to make to the IASB is the following: a reporting entity should only be allowed to use line items mentioned in the IFRS primary financial statements if the IFRS definition is consistently used for the entire line item in the segment reporting. If a company chooses to deviate from measurement used in the primary statements, the name of the line item displayed should be accompanied by the word adjusted. If a company chooses to report an adjusted line item, it should also include the unadjusted line item, as measured in the primary statements. We observe a number of companies where the reconciliation is an integral part of an other or eliminations column. We believe this is an enforcement issue, and not necessarily a problem of the standard, as the standard clearly disallows such practice. Question 4: How has the requirement to use internally-reported line items affected financial reporting? Investors: please focus on how the reported line items that you use have changed. Please also comment on which line items are/would be most useful to you, and why, and whether you are receiving these. We support companies to continue to report non-ifrs line items. It allows companies to provide industry or even company specific performance indicators that can add to the insight of investors. As discussed before, we consider it best practice that if a reporting entity chooses to report adjusted IFRS line items, the unadjusted IFRS line items should also be included as a separate line in the segment report. 4

5 Although certain line items are relevant in many cases (like revenues, operating profit, depreciation & amortisation, capital expenditures), there are very few line items that are universally relevant for all industries. We believe IFRS 8 should not specify individual line items for operating segments, as there are too few that are truly universally relevant in this context. Question 5: How have the disclosures required by IFRS 8 affected you in your role? Investors: please provide examples from published operating segment information to illustrate your assessment of the disclosures relating to operating segments. Do you now receive better information that helps you to understand the company s business? Please also comment on the specific disclosure requirements of IFRS 8 for example, those relating to the identification and aggregation of operating segments; the types of goods and services attributed to reportable segments; and the reconciliations that are required. It would also be useful to indicate whether you regularly request other types of segment disclosures. In addition to our answer to question 2, we prefer a standard that requires companies to report both a business, and a geographical breakdown. Unfortunately, we observe quite a number of companies providing a geo breakdown only, where we would have preferred a business breakdown. Only in a rare case where the mix of businesses is very similar across all geographies, for example because the company predominantly sells a single product, a more detailed geographical breakdown together with a less detailed business breakdown may provide sufficient insight to investors as well. In most other cases, line items like margins per country will remain difficult to interpret as differences between countries could be dominated by unknown differences in business mix. We would support a standard that, in addition to a business breakdown, also requires a basic geographical breakdown by destination, and if significantly different also by origin. Impact of partial ownership of subsidiaries The group structure is highly relevant for analysts, also in the context of segment reporting. Unfortunately, disclosure on group structure is too often overlooked by companies 2. IFRS 8 did not improve segment disclosure on this important topic. In this respect, through the eyes of management has in most cases not resulted in more useful information for investors. There are examples of companies that are clearly aware of the relevance of partial ownership of subsidiaries. One of them is Vivendi SA. Vivendi includes in the segment reporting paragraph the following overview (page 19 of the consolidated financial statements 3 ): 2 On 29 October 2012, the Netherlands Authority Financial Markets published a report on the quality of disclosure on noncontrolling interest by Dutch companies:

6 As the operating segment information relates to fully consolidated numbers, these numbers are based on the (often fictitious) assumption that all of the subsidiaries are fully owned. If this is not the case, investors need insight in what proportion of the reported segment reporting numbers is attributable to the common shareholders, i.e. excluding the amounts attributable to external shareholders. The term proportionate share represents the common shareholders proportionate share of the fully consolidated numbers. If all of the subsidiaries are fully owned, the proportionate shares are identical to the fully consolidated amounts. Eumedion requests IASB to revise IFRS 8 to provide insight in proportionate shares. The segment reporting of companies that fully consolidate partly owned subsidiaries should include a column for each segment to indicate what percentage of the reported number is attributable to the common shareholder. The picture below explains the format we envisage for the German listed company Fresenius SE & Co.KGaA: The percentages can be displayed between the columns as demonstrated in the third table (please note: only if the percentages are significantly different from 100%). 6

7 Question 6: How were you affected by the implementation of IFRS 8? Investors: please focus on whether the way in which you use financial reports has changed as a result of applying IFRS 8. Please explain to us what that effect was and the consequences of any changes to how you analyse data or predict results. We do not believe IFRS 8 has changed the way analysts analyse companies. However, the answers to the previous questions highlighted multiple issues with IFRS 8, that are likely to have resulted in analysts having to spent more time trying to get to the same level of insight, and/or settle for less insight for their economic decision making. In general, both outcomes result in additional costs and/or uncertainty not only for the asset manager, but also for the assets owners and beneficiaries. If you would like to discuss our views in further detail, please do not hesitate to contact us. Our contact person is Martijn Bos (martijn.bos@eumedion.nl, ). Yours sincerely, Rients Abma Executive Director Eumedion PO Box AX AMSTERDAM 7

8 Appendix: Royal Dutch Shell segment reporting 2006 versus 2011 Annual report Royal Dutch Shell 2006, under IAS 14 Page 112: NEW ACCOUNTING STANDARDS AND INTERPRETATIONS <..> IFRS 8 Operating Segments is effective from January 1, 2009, although early adoption by the Group is under consideration. The standard replaces IAS 14 Segment Reporting and converges with US GAAP. Adoption will simplify the way in which segment information is disclosed in the Consolidated Financial Statements as the Group currently complies with both IFRS and US GAAP requirements. 8

9 9

10 10

11 11

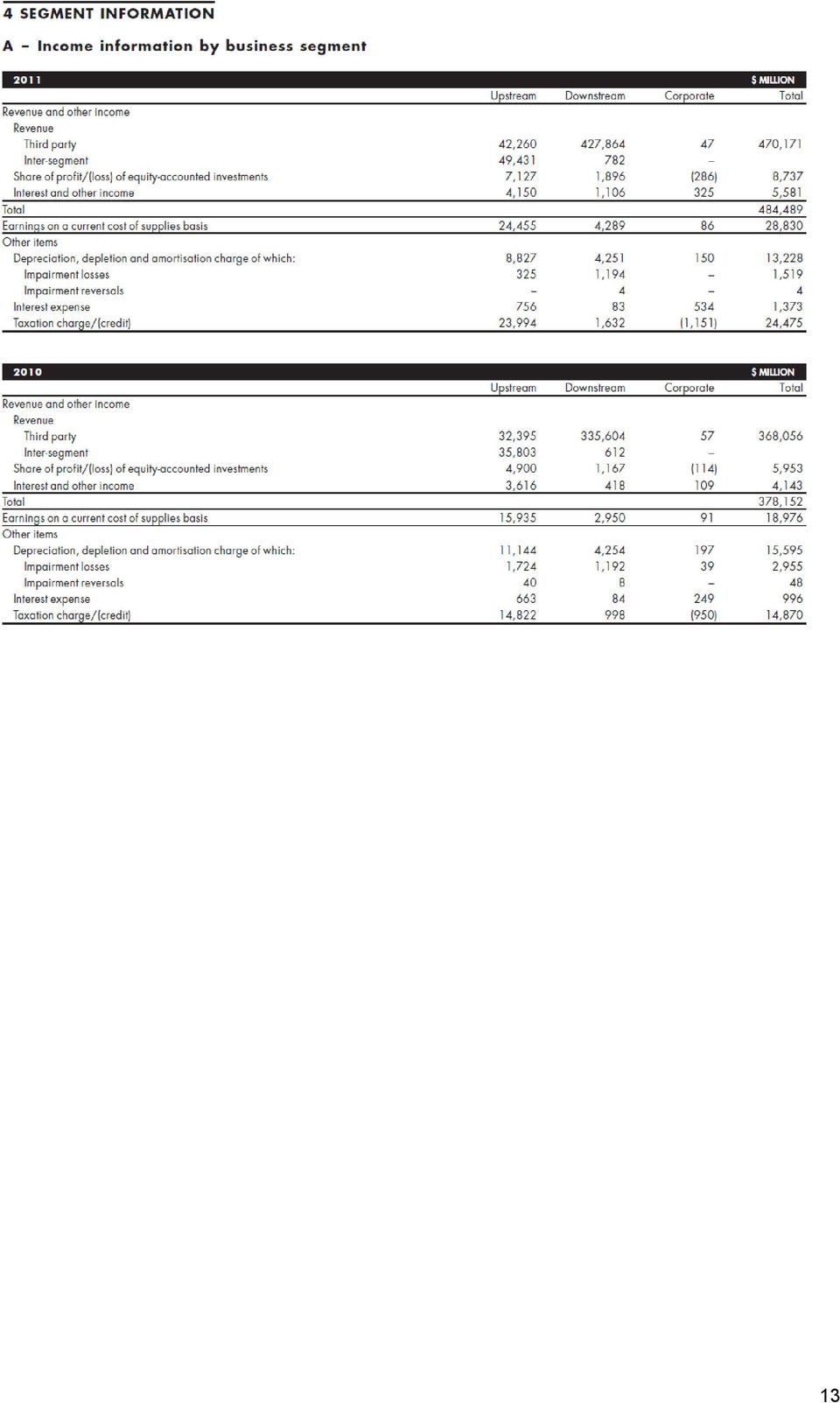

12 Royal Dutch Shell Annual report 2011 Nature of operations and segmental reporting Shell is engaged in the principal aspects of the oil and gas industry in more than 80 countries and reports its business through three segments. Upstream combines the operating segments Upstream International and Upstream Americas, which have similar characteristics and are engaged in searching for and recovering crude oil and natural gas; the liquefaction and transportation of gas; the extraction of bitumen from oil sands that is converted into synthetic crude oil; and wind energy. Downstream is engaged in manufacturing; distribution and marketing activities for oil products and chemicals; in alternative energy (excluding wind); and CO2 management. Corporate represents the key support functions, comprising holdings and treasury, headquarters, central functions and Shell s self-insurance activities. Integrated within the Upstream and Downstream segments are Shell s trading activities. 12

13 13

14 14

15 15

16 Investor presentation on full year 2011 results alyst_presentation.pdf 16

Full consolidation of partly owned subsidiaries requires additional disclosure

Full consolidation of partly owned subsidiaries requires additional disclosure Capital Markets Advisory Committee, 17 October 2012 Martijn Bos, Policy advisor accounting & audit martijn.bos@eumedion.nl

Full consolidation of partly owned subsidiaries requires additional disclosure Capital Markets Advisory Committee, 17 October 2012 Martijn Bos, Policy advisor accounting & audit martijn.bos@eumedion.nl

Position Paper. Full consolidation of partly owned subsidiaries requires additional disclosure

Position Paper Full consolidation of partly owned subsidiaries requires additional disclosure 1. Introduction Many entities control one or more partly owned subsidiaries 1. International Financial Reporting

Position Paper Full consolidation of partly owned subsidiaries requires additional disclosure 1. Introduction Many entities control one or more partly owned subsidiaries 1. International Financial Reporting

Re.: IASB Request for Information Post-implementation Review: IFRS 3 Business Combinations

Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom 28 May 2014 540/636 Dear Mr Hoogervorst Re.: IASB Request for Information Post-implementation

Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom 28 May 2014 540/636 Dear Mr Hoogervorst Re.: IASB Request for Information Post-implementation

Submitted by e-mail. Amsterdam, 15 March 2013. Dear Mr. Gunn,

James Gunn, Technical Director International Auditing and Assurance Standards Board (IAASB) 545 Fifth Avenue, 14 th Floor New York, New York 10017 USA Submitted by e-mail Subject: IAASB Exposure Draft

James Gunn, Technical Director International Auditing and Assurance Standards Board (IAASB) 545 Fifth Avenue, 14 th Floor New York, New York 10017 USA Submitted by e-mail Subject: IAASB Exposure Draft

Comment on Exposure Draft ED/2013/10 Equity Method in Separate Financial Statements

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref :RJ-IASB 448 C Direct dial : (+31) 20 301 0391 Date :Amsterdam, 4 February 2014 Re :Comment on Exposure

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref :RJ-IASB 448 C Direct dial : (+31) 20 301 0391 Date :Amsterdam, 4 February 2014 Re :Comment on Exposure

Comment on Exposure Draft 2014-4 Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref : IASB 455 C Direct dial : Tel.: (+31) 20 301 0391 / Fax: (+31) 20 301 0302 Date : Amsterdam, December 22

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref : IASB 455 C Direct dial : Tel.: (+31) 20 301 0391 / Fax: (+31) 20 301 0302 Date : Amsterdam, December 22

International Financial Reporting Standard 8 Operating Segments

EC staff consolidated version as of 21 June 2012, EN EU IFRS 8 FOR INFORMATION PURPOSES ONLY International Financial Reporting Standard 8 Operating Segments Core principle 1 An entity shall disclose information

EC staff consolidated version as of 21 June 2012, EN EU IFRS 8 FOR INFORMATION PURPOSES ONLY International Financial Reporting Standard 8 Operating Segments Core principle 1 An entity shall disclose information

Re: Exposure Draft Annual Improvements to IFRSs 2011 2013 Cycle

18 February 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Exposure Draft Annual Improvements to IFRSs 2011 2013 Cycle On behalf of the

18 February 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Exposure Draft Annual Improvements to IFRSs 2011 2013 Cycle On behalf of the

Eumedion response to the IAASB Framework for Audit Quality

James Gunn, Technical Director International Auditing and Assurance Standards Board 545 Fifth Avenue, 14 th Floor New York, New York 10017 USA Submitted by e-mail Subject: Eumedion response to the IAASB

James Gunn, Technical Director International Auditing and Assurance Standards Board 545 Fifth Avenue, 14 th Floor New York, New York 10017 USA Submitted by e-mail Subject: Eumedion response to the IAASB

Third LAC Tax Policy Forum

Third LAC Tax Policy Forum Cooperative Compliance - a business perspective Wilbert Huijbens; Tax Manager; Shell International BV Montevideo, Uruguay; DEFINITIONS AND CAUTIONARY NOTE Resources: Our use

Third LAC Tax Policy Forum Cooperative Compliance - a business perspective Wilbert Huijbens; Tax Manager; Shell International BV Montevideo, Uruguay; DEFINITIONS AND CAUTIONARY NOTE Resources: Our use

A practical guide to segment reporting. September 2008

A practical guide to segment reporting September 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides

A practical guide to segment reporting September 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides

Comments on the Request for Information Post-implementation Review: IFRS 3 Business Combinations

The Japanese Institute of Certified Public Accountants 4-4-1, Kudan-Minami, Chiyoda-ku, Tokyo 102-8264 JAPAN Phone: +81-3-3515-1130 Fax: +81-3-5226-3355 e-mail: kigyokaikei@jicpa.or.jp http://www.hp.jicpa.or.jp/english/

The Japanese Institute of Certified Public Accountants 4-4-1, Kudan-Minami, Chiyoda-ku, Tokyo 102-8264 JAPAN Phone: +81-3-3515-1130 Fax: +81-3-5226-3355 e-mail: kigyokaikei@jicpa.or.jp http://www.hp.jicpa.or.jp/english/

Consultation Paper ESMA Guidelines on Alternative Performance Measures

Tel +44 (0)20 7694 8871 8 Salisbury Square Fax +44 (0)20 7694 8429 London EC4Y 8BB mark.vaessen@kpmgifrg.com david.littleford@kpmg.co.uk United Kingdom Mr Steven Maijoor Chairman European Securities and

Tel +44 (0)20 7694 8871 8 Salisbury Square Fax +44 (0)20 7694 8429 London EC4Y 8BB mark.vaessen@kpmgifrg.com david.littleford@kpmg.co.uk United Kingdom Mr Steven Maijoor Chairman European Securities and

Exposure Draft of Financial Instruments with characteristics of equity

10 September 2008 Sir David Tweedie Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: Exposure Draft of Financial Instruments with characteristics

10 September 2008 Sir David Tweedie Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: Exposure Draft of Financial Instruments with characteristics

Draft Comment Letter

Draft Comment Letter Comments should be submitted by 5 September 2014 to commentletters@efrag.org [Date] International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam,

Draft Comment Letter Comments should be submitted by 5 September 2014 to commentletters@efrag.org [Date] International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam,

BUSINESS COMBINATIONS PHASE II

International Accounting Standards Board BUSINESS COMBINATIONS PHASE II Project summary, feedback and effect analysis January 2008 International Accounting Standards Board Business Combinations Phase

International Accounting Standards Board BUSINESS COMBINATIONS PHASE II Project summary, feedback and effect analysis January 2008 International Accounting Standards Board Business Combinations Phase

Adopting the consolidation suite of standards

IFRS PRACTICE ISSUES Adopting the consolidation suite of standards Transition to IFRSs 10, 11 and 12 January 2013 kpmg.com/ifrs Contents Simplifications provide relief 1 1. Extent of relief depends on

IFRS PRACTICE ISSUES Adopting the consolidation suite of standards Transition to IFRSs 10, 11 and 12 January 2013 kpmg.com/ifrs Contents Simplifications provide relief 1 1. Extent of relief depends on

For your convenience, we have also attached an appendix with the draft comment letter of EFRAG.

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref: RJ-IASB 438 B Direct dial: Tel.: (+31) 20 301 0391 / Fax: (+31) 20 301 0302 Date: Amsterdam, 21st of March

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Our ref: RJ-IASB 438 B Direct dial: Tel.: (+31) 20 301 0391 / Fax: (+31) 20 301 0302 Date: Amsterdam, 21st of March

International Financial Reporting Standard 8 Operating Segments

International Financial Reporting Standard 8 Operating Segments Core principle 1 An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects

International Financial Reporting Standard 8 Operating Segments Core principle 1 An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects

FEE Response to Request for Information - Post Implementation Review: IFRS 3 Business Combinations

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 19 May 2014 Ref.: ACC/AKI/HBL/PGI/SRO Dear Chairman, Re: FEE Response

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 19 May 2014 Ref.: ACC/AKI/HBL/PGI/SRO Dear Chairman, Re: FEE Response

Eumedion response to the consultation questions on IIRC <IR> draft framework

To: The International Integrated Reporting Council (IIRC) Submitted via http:/www.theiirc.org/consultationdraft2013/feedback/ The Hague, 3 July 2013 Our reference: B13.28 Subject: Eumedion response to

To: The International Integrated Reporting Council (IIRC) Submitted via http:/www.theiirc.org/consultationdraft2013/feedback/ The Hague, 3 July 2013 Our reference: B13.28 Subject: Eumedion response to

IPSAS 7 INVESTMENTS IN ASSOCIATES

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

Rechnungslegungs Interpretations Accounting Interpretations Committee

AIC c/o DRSC e.v. Zimmerstr. 30 10969 Berlin Telefon +49 (0)30 206412-12 Telefax +49 (0)30 206412-15 E-Mail info@drsc.de Mr Robert Garnett Chairman of the IFRS Interpretations Committee (IFRS IC) 30 Cannon

AIC c/o DRSC e.v. Zimmerstr. 30 10969 Berlin Telefon +49 (0)30 206412-12 Telefax +49 (0)30 206412-15 E-Mail info@drsc.de Mr Robert Garnett Chairman of the IFRS Interpretations Committee (IFRS IC) 30 Cannon

Investments in Associates and Joint Ventures

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

Singapore Illustrative Financial Statements 2013

Singapore Illustrative Financial Statements 2013 About KPMG KPMG is one of the world s leading networks of professional services firms. With more than 152,000 professionals worldwide, KPMG member firms

Singapore Illustrative Financial Statements 2013 About KPMG KPMG is one of the world s leading networks of professional services firms. With more than 152,000 professionals worldwide, KPMG member firms

ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS

Exposure Draft ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS Comments to be received by 24 October 2003 ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED

Exposure Draft ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED OPERATIONS Comments to be received by 24 October 2003 ED 4 DISPOSAL OF NON-CURRENT ASSETS AND PRESENTATION OF DISCONTINUED

INFORMATION FOR OBSERVERS. Project: Earnings Per Share Treasury stock method (Agenda Paper 3)

") 30 Cannon Street, London EC4M 6XH, United Kingdom International Phone: +44 (0)20 7246 6410, Fax: +44 (0)20 7246 6411 Accounting Standards Email: iasb@iasb.org Website: http://www.iasb.org Board This document

30 Cannon Street, London EC4M 6XH, United Kingdom International Phone: +44 (0)20 7246 6410, Fax: +44 (0)20 7246 6411 Accounting Standards Email: iasb@iasb.org Website: http://www.iasb.org Board This document

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations

EC staff consolidated version as of 21/06/2012, FOR INFORMATION PURPOSES ONLY EN IFRS 5 International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations Objective

EC staff consolidated version as of 21/06/2012, FOR INFORMATION PURPOSES ONLY EN IFRS 5 International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations Objective

Financial Statement Presentation. Introduction. Staff draft of an exposure draft

Financial Statement Presentation Staff draft of an exposure draft Introduction The project on financial statement presentation is a joint project of the International Accounting Standards Board (IASB)

Financial Statement Presentation Staff draft of an exposure draft Introduction The project on financial statement presentation is a joint project of the International Accounting Standards Board (IASB)

Comment letter from FSR to the IASB Exposure Draft ED/2009/2 Income Tax

Foreningen af Statsautoriserede Revisorer Kronprinsessegade 8, 1306 København K. Telefon 33 93 91 91 Telefax nr. 33 11 09 13 e-mail: fsr@fsr.dk Internet: www.fsr.dk International Accounting Standards Board

Foreningen af Statsautoriserede Revisorer Kronprinsessegade 8, 1306 København K. Telefon 33 93 91 91 Telefax nr. 33 11 09 13 e-mail: fsr@fsr.dk Internet: www.fsr.dk International Accounting Standards Board

AOSSG comments on IASB Request for Information Post-Implementation Review of IFRS 3 Business Combinations

22 July 2014 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH UNITED KINGDOM Dear Hans AOSSG comments on IASB Request for Information Post-Implementation

22 July 2014 Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH UNITED KINGDOM Dear Hans AOSSG comments on IASB Request for Information Post-Implementation

Illustrative financial statements

IFRS Illustrative financial statements October 2012 kpmg.com/ifrs 1 Contents What s new 2 About this publication 3 Independent auditors report on consolidated financial statements 5 Consolidated financial

IFRS Illustrative financial statements October 2012 kpmg.com/ifrs 1 Contents What s new 2 About this publication 3 Independent auditors report on consolidated financial statements 5 Consolidated financial

c/o KAMMER DER WIRTSCHAFTSTREUHÄNDER SCHOENBRUNNER STRASSE 222 228/1/6 A-1120 VIENNA AUSTRIA TEL +43 (1) 81173 228 FAX +43 (1) 81173 100 E-MAIL WEB

81173 228 FAX +43 (1) 81173 100 E-MAIL WEB") c/o KAMMER DER WIRTSCHAFTSTREUHÄNDER SCHOENBRUNNER STRASSE 222 228/1/6 A-1120 VIENNA AUSTRIA Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United

c/o KAMMER DER WIRTSCHAFTSTREUHÄNDER SCHOENBRUNNER STRASSE 222 228/1/6 A-1120 VIENNA AUSTRIA Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United

IFRS industry insights

IFRS Global Office Issue 2, June 2011 IFRS industry insights Joint arrangements in the energy and resources industry The most significant change will likely be the removal of the option to proportionately

IFRS Global Office Issue 2, June 2011 IFRS industry insights Joint arrangements in the energy and resources industry The most significant change will likely be the removal of the option to proportionately

IPSAS 7 INVESTMENTS IN ASSOCIATES

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

DRAFT COMMENT LETTER Comments should be sent to Commentletters@efrag.org by 6 July 2010

DRAFT COMMENT LETTER Comments should be sent to Commentletters@efrag.org by 6 July 2010 XX July 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/ Madam

DRAFT COMMENT LETTER Comments should be sent to Commentletters@efrag.org by 6 July 2010 XX July 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/ Madam

IASB. Request for Views. Effective Dates and Transition Methods. International Accounting Standards Board

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

Module 14 Investments in Associates

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 14 Investments in Associates IFRS Foundation: Training Material for the IFRS for SMEs including the full text

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 14 Investments in Associates IFRS Foundation: Training Material for the IFRS for SMEs including the full text

Re: IASB Discussion Paper Financial Instruments with Characteristics of Equity

Date Le Président Fédération Avenue d Auderghem 22-28/8 des Experts 1040 Bruxelles 29 September 2008 Comptables Tél. 32 (0) 2 285 40 85 Européens Fax: 32 (0) 2 231 11 12 AISBL E-mail: secretariat@fee.be

Date Le Président Fédération Avenue d Auderghem 22-28/8 des Experts 1040 Bruxelles 29 September 2008 Comptables Tél. 32 (0) 2 285 40 85 Européens Fax: 32 (0) 2 231 11 12 AISBL E-mail: secretariat@fee.be

INFORMATION FOR OBSERVERS. Project: IAS 39 and Business Combinations (Agenda Paper 7E)

") 30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This observer note

30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This observer note

International Financial Reporting Bulletin

Issue 1/2006 BDO International 17 January 2006 Status: Final Effective date: Immediate Accounting impact: May affect the classification of investments as being in subsidiaries International Financial Reporting

Issue 1/2006 BDO International 17 January 2006 Status: Final Effective date: Immediate Accounting impact: May affect the classification of investments as being in subsidiaries International Financial Reporting

Snapshot: Offsetting Financial Assets and Financial Liabilities

January 2011 Exposure Draft Snapshot: Offsetting Financial Assets and Financial This snapshot is an introduction to a proposed International Financial Reporting Standard (IFRS) on offsetting financial

January 2011 Exposure Draft Snapshot: Offsetting Financial Assets and Financial This snapshot is an introduction to a proposed International Financial Reporting Standard (IFRS) on offsetting financial

Draft Comment Letter

Draft Comment Letter Comments should be submitted by 22 October 2015 to commentletters@efrag.org International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom [Date] Dear Sir/Madam,

Draft Comment Letter Comments should be submitted by 22 October 2015 to commentletters@efrag.org International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom [Date] Dear Sir/Madam,

Investments in Associates and Joint Ventures

IFAC Board Exposure Draft 50 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Investments in Associates and Joint Ventures This Exposure Draft 50, Investments

IFAC Board Exposure Draft 50 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Investments in Associates and Joint Ventures This Exposure Draft 50, Investments

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IFRS Viewpoint. What s the issue? Common control business combinations

IFRS Viewpoint Common control business combinations Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each issue will focus on an area where

IFRS Viewpoint Common control business combinations Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each issue will focus on an area where

Module 6 Statement of Changes in Equity and Statement of Income and Retained Earnings

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 6 Statement of Changes in Equity and Statement of Income and Retained Earnings IFRS Foundation: Training Material

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 6 Statement of Changes in Equity and Statement of Income and Retained Earnings IFRS Foundation: Training Material

2 This Standard shall be applied by all entities that are investors with joint control of, or significant influence over, an investee.

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

105 SHELL ANNUAL REPORT AND FORM 20-F 2013 CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 1 BASIS OF PREPARATION The Consolidated Financial Statements of Royal Dutch Shell

105 SHELL ANNUAL REPORT AND FORM 20-F 2013 CONSOLIDATED FINANCIAL STATEMENTS NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 1 BASIS OF PREPARATION The Consolidated Financial Statements of Royal Dutch Shell

Module 5 Statement of Comprehensive Income and Income Statement

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 5 Statement of Comprehensive Income and Income Statement IFRS Foundation: Training Material for the IFRS for

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 5 Statement of Comprehensive Income and Income Statement IFRS Foundation: Training Material for the IFRS for

Subject: Eumedion s response to IASB s Exposure Draft 2015/3 Conceptual Framework for Financial

To the members of the International Accounting Standards Board Submitted electronically Subject: Eumedion s response to IASB s Exposure Draft 2015/3 Conceptual Framework for Financial Ref: B15.23 Reporting

To the members of the International Accounting Standards Board Submitted electronically Subject: Eumedion s response to IASB s Exposure Draft 2015/3 Conceptual Framework for Financial Ref: B15.23 Reporting

FINANCIAL POSITION SHARE-BASED PAYMENT EPS UNIT OF ACCOUNT DISCLOSURES HELD-FOR-SALE PENSION FINANCIAL POSITION PRESENTATION

PERFORMANCE BUSINESS COMBINATIONS OPERATING SEGMENTS CASH FLOWS GOING CONCERN UNCONSOLIDATED STRUCTURED ENTITIES FINANCIAL POSITION GOODWILL ESTIMATES OFFSETTING OCI PROFIT OR LOSS PRESENTATION DISCLOSURES

PERFORMANCE BUSINESS COMBINATIONS OPERATING SEGMENTS CASH FLOWS GOING CONCERN UNCONSOLIDATED STRUCTURED ENTITIES FINANCIAL POSITION GOODWILL ESTIMATES OFFSETTING OCI PROFIT OR LOSS PRESENTATION DISCLOSURES

Re: Exposure Draft of Proposed Amendments to IAS 37 Provisions, Contingent Liabilities and Contingent Assets and IAS 19 Employee Benefits

TP PT PT Members Organización Internacional de Comisiones de Valores International Organisation of Securities Commissions Organisation internationale des commissions de valeurs Organização Internacional

TP PT PT Members Organización Internacional de Comisiones de Valores International Organisation of Securities Commissions Organisation internationale des commissions de valeurs Organização Internacional

In depth A look at current financial reporting issues

inform.pwc.com In depth A look at current financial reporting issues A fresh look at IFRS 8, Operating segments March 2015 No. INT2015-14 At a glance 1 Why it s important 1 Operating segments 2 Reportable

inform.pwc.com In depth A look at current financial reporting issues A fresh look at IFRS 8, Operating segments March 2015 No. INT2015-14 At a glance 1 Why it s important 1 Operating segments 2 Reportable

FEE comments on Separate Financial Statements Discussion Paper

Ms Françoise Flores TEG Chair EFRAG Square de Meeûs 35 B-1000 BRUXELLES E-mail: commentletters@efrag.org 15 January 2015 Ref.: ACC/PFK/PGI/SRO Dear Ms Flores, Re: FEE comments on Separate Financial Statements

Ms Françoise Flores TEG Chair EFRAG Square de Meeûs 35 B-1000 BRUXELLES E-mail: commentletters@efrag.org 15 January 2015 Ref.: ACC/PFK/PGI/SRO Dear Ms Flores, Re: FEE comments on Separate Financial Statements

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

Drafting the Proposal of a Share-Based Payment Transactions

2 April 2015 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Exposure Draft Classification and Measurement of Share-based Payment Transactions

2 April 2015 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Re: Exposure Draft Classification and Measurement of Share-based Payment Transactions

Exposure Draft: Post-implementation Review: IFRS-3 Business Combinations

IASB International Accounting Standards Board IFRS International Financial Reporting Standard Mainzer Landstrasse 47a DE 60329 Frankfurt am Main Contact: Laura Compte Direct number: +49 69 26 4848 300

IASB International Accounting Standards Board IFRS International Financial Reporting Standard Mainzer Landstrasse 47a DE 60329 Frankfurt am Main Contact: Laura Compte Direct number: +49 69 26 4848 300

MASUPARIA GOLD CORPORATION

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS THREE MONTHS ENDED DECEMBER 31, 2011 and 2010 (expressed in Canadian Dollars) NOTICE TO READERS Under National Instrument 51-102, Part 4.3 (3)(a), if

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS THREE MONTHS ENDED DECEMBER 31, 2011 and 2010 (expressed in Canadian Dollars) NOTICE TO READERS Under National Instrument 51-102, Part 4.3 (3)(a), if

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12)

") New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 October 2010 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 October 2010 other than consequential amendments

Disclosure of Interests in Other Entities

IFAC Board Exposure Draft 52 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Disclosure of Interests in Other Entities This Exposure Draft 52, Disclosure

IFAC Board Exposure Draft 52 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Disclosure of Interests in Other Entities This Exposure Draft 52, Disclosure

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

CONTACT(S) Kazuhiro Sakaguchi ksakaguchi@ifrs.org +44 (0)20 7246 6930

Kazuhiro Sakaguchi ksakaguchi@ifrs.org +44 (0)20 7246 6930") STAFF PAPER IFRS Interpretations Committee Meeting January 2013 Project Paper topic IAS 28 Investments in Associates and Joint Ventures/IFRS 3 Business Combinations Acquisition of an interest in an associate

STAFF PAPER IFRS Interpretations Committee Meeting January 2013 Project Paper topic IAS 28 Investments in Associates and Joint Ventures/IFRS 3 Business Combinations Acquisition of an interest in an associate

Non-current Assets Held for Sale and Discontinued Operations

HKFRS 5 Revised June November 2014 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations

HKFRS 5 Revised June November 2014 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations

2. This paper supplements Agenda Paper 2A Outreach and comment letter analysis for this meeting. This paper does not ask any questions.

IASB Agenda ref 2B STAFF PAPER REG IASB Meeting Project Insurance contracts Paper topic Feedback from users of financial statements January 2014 CONTACT(S) Izabela Ruta iruta@ifrs.org +44 (0)20 7246 6957

IASB Agenda ref 2B STAFF PAPER REG IASB Meeting Project Insurance contracts Paper topic Feedback from users of financial statements January 2014 CONTACT(S) Izabela Ruta iruta@ifrs.org +44 (0)20 7246 6957

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

IFRIC DRAFT INTERPRETATION DI/2010/1 STRIPPING COSTS IN THE PRODUCTION PHASE OF A SURFACE MINE

Mr Kevin Stevenson Chairman Australian Accounting Standards Board PO Box 204, Collins Street WEST VICTORIA 8007 By Email: standard@aasb.gov.au 8 November 2010 Dear Kevin Grant Thornton Australia Limited

Mr Kevin Stevenson Chairman Australian Accounting Standards Board PO Box 204, Collins Street WEST VICTORIA 8007 By Email: standard@aasb.gov.au 8 November 2010 Dear Kevin Grant Thornton Australia Limited

IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities

September 2011 (updated July 2013) Effect analysis IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities The IASB s approach to effect analysis Before we issue

September 2011 (updated July 2013) Effect analysis IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities The IASB s approach to effect analysis Before we issue

IFRS Interpretations Committee Update

International Financial Reporting Standards GPF meeting, Nov 2014 Agenda Paper 2 IFRS Interpretations Committee Update The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards GPF meeting, Nov 2014 Agenda Paper 2 IFRS Interpretations Committee Update The views expressed in this presentation are those of the presenter, not necessarily

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Mar 30, Mar 29, 2014 2015 Net system sales 1,030.0 1,246.5 Net service and field option sales 366.5 403.4 Total net

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Mar 30, Mar 29, 2014 2015 Net system sales 1,030.0 1,246.5 Net service and field option sales 366.5 403.4 Total net

08FR-003 Business Combinations IFRS 3 revised 11 January 2008. Key points

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

IFRS News. Special Edition. A consolidation exception for investment entities

IFRS News Special Edition December 2012 Many commentators have long believed that consolidating the financial statements of an investment entity and its investees does not provide the most useful information.

IFRS News Special Edition December 2012 Many commentators have long believed that consolidating the financial statements of an investment entity and its investees does not provide the most useful information.

Mr Roger Marshall Acting President EFRAG Board European Financial Reporting Advisory Group (EFRAG) 35 Square de Meeüs 1000 Brussels Belgium

35 Square de Meeüs 1000 Brussels Belgium") * esma European Securities and Markel:s Authority *** The Chair 19 November2015 ESMA/2015/1739 Mr Roger Marshall Acting President EFRAG Board European Financial Reporting Advisory Group (EFRAG) 35 Square

* esma European Securities and Markel:s Authority *** The Chair 19 November2015 ESMA/2015/1739 Mr Roger Marshall Acting President EFRAG Board European Financial Reporting Advisory Group (EFRAG) 35 Square

IFrS. Disclosure checklist. July 2011. kpmg.com/ifrs

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

Accounting for Interests in Joint Operations structured through Separate Vehicles Consultation of the IFRS Interpretations Committee by the IASB

STAFF PAPER IFRS Interpretations Committee Meeting 12 13 November 2013 IASB: May, Sep 2013 Project Paper topic Accounting for Interests in Joint Operations structured through Separate Vehicles Consultation

STAFF PAPER IFRS Interpretations Committee Meeting 12 13 November 2013 IASB: May, Sep 2013 Project Paper topic Accounting for Interests in Joint Operations structured through Separate Vehicles Consultation

IFRS IN PRACTICE. IAS 36 Impairment of Assets (December 2013)

") IFRS IN PRACTICE IAS 36 Impairment of Assets (December 2013) 2 IFRS IN PRACTICE - IAS 36 IMPAIRMENT OF ASSETS (DECEMBER 2013) IFRS IN PRACTICE - IAS 36 IMPAIRMENT OF ASSETS (DECEMBER 2013) 3 INTRODUCTION

IFRS IN PRACTICE IAS 36 Impairment of Assets (December 2013) 2 IFRS IN PRACTICE - IAS 36 IMPAIRMENT OF ASSETS (DECEMBER 2013) IFRS IN PRACTICE - IAS 36 IMPAIRMENT OF ASSETS (DECEMBER 2013) 3 INTRODUCTION

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Six months ended, Jun 29, Jun 28, Jun 29, Jun 28, 2014 2015 2014 2015 Net system sales 1,243.0 1,134.5 2,273.0 2,381.0

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Six months ended, Jun 29, Jun 28, Jun 29, Jun 28, 2014 2015 2014 2015 Net system sales 1,243.0 1,134.5 2,273.0 2,381.0

Ref: B15.01 Eumedion response draft revised OECD principles on corporate governance

Organisation for Economic Co-operation and Development (OECD) Corporate Governance Committee 2, rue André Pascal 75775 Paris Cedex 16 France The Hague, 2 January 2015 Ref: B15.01 Subject: Eumedion response

Organisation for Economic Co-operation and Development (OECD) Corporate Governance Committee 2, rue André Pascal 75775 Paris Cedex 16 France The Hague, 2 January 2015 Ref: B15.01 Subject: Eumedion response

5N PLUS INC. Condensed Interim Consolidated Financial Statements (Unaudited) For the three month periods ended March 31, 2016 and 2015 (in thousands

For the three month periods ended March 31, 2016 and 2015 (in thousands") Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Insurance Contracts Project Update

International Financial Reporting Standards Insurance Contracts Project Update March 2015 The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS

International Financial Reporting Standards Insurance Contracts Project Update March 2015 The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS

International Financial Reporting Standards

Audit International Financial Reporting Standards IFRS 8 Operating Segments A disclosure checklist An IAS Plus guide February 2007 Audit.Tax.Consulting.Financial Advisory. Contacts Global IFRS leadership

Audit International Financial Reporting Standards IFRS 8 Operating Segments A disclosure checklist An IAS Plus guide February 2007 Audit.Tax.Consulting.Financial Advisory. Contacts Global IFRS leadership

IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities

May 2011 (updated January 2012) Project Summary and Feedback Statement IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities At a glance We, the International

May 2011 (updated January 2012) Project Summary and Feedback Statement IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities At a glance We, the International

International Accounting Standard 28 Investments in Associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

CONTACT(S) Michelle Sansom michellesansom@ifrs.org +44 (0)20 7246 6963

Michelle Sansom michellesansom@ifrs.org +44 (0)20 7246 6963") Agenda Ref 3A STAFF PAPER IASB Meeting Project The Equity Method of Accounting Paper topic Project scope CONTACT(S) Michelle Sansom michellesansom@ifrs.org +44 (0)20 7246 6963 June 2014 This paper has

Agenda Ref 3A STAFF PAPER IASB Meeting Project The Equity Method of Accounting Paper topic Project scope CONTACT(S) Michelle Sansom michellesansom@ifrs.org +44 (0)20 7246 6963 June 2014 This paper has

90 Statement of directors responsibilities. Independent auditor s reports 91 Group income statement 96 Group statement of comprehensive income 97

Financial statements 90 Statement of directors responsibilities 91 Consolidated financial statements of the BP group Independent auditor s reports 91 Group income statement 96 Group statement of comprehensive

Financial statements 90 Statement of directors responsibilities 91 Consolidated financial statements of the BP group Independent auditor s reports 91 Group income statement 96 Group statement of comprehensive

Endorsement of IFRS 8 Operating Segments Analysis of potential Impacts (API)

") EUROPEAN COMMISSION Internal Market and Services DG FREE MOVEMENT OF CAPITAL, COMPANY LAW AND CORPORATE GOVERNANCE Accounting Brussels, 30 May 2007 F3/RB D(2007) Endorsement of IFRS 8 Operating Segments

EUROPEAN COMMISSION Internal Market and Services DG FREE MOVEMENT OF CAPITAL, COMPANY LAW AND CORPORATE GOVERNANCE Accounting Brussels, 30 May 2007 F3/RB D(2007) Endorsement of IFRS 8 Operating Segments

FINANCIAL STATEMENT PRESENTATION

Staff Draft of Exposure Draft IFRS X FINANCIAL STATEMENT PRESENTATION 1 July 2010 This staff draft of an exposure draft has been prepared by the staff of the IASB and the US FASB for the boards joint project

Staff Draft of Exposure Draft IFRS X FINANCIAL STATEMENT PRESENTATION 1 July 2010 This staff draft of an exposure draft has been prepared by the staff of the IASB and the US FASB for the boards joint project

IFRIC Update From the IFRS Interpretations Committee

IFRIC Update From the IFRS Interpretations Committee May 2014 Welcome to the IFRIC Update IFRIC Update is the newsletter of the IFRS Interpretations Committee (the Interpretations Committee ). All conclusions

IFRIC Update From the IFRS Interpretations Committee May 2014 Welcome to the IFRIC Update IFRIC Update is the newsletter of the IFRS Interpretations Committee (the Interpretations Committee ). All conclusions

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

IFRS 15 Revenue from Contracts with Customers

May 2014 International Financial Reporting Standard IFRS 15 Revenue from Contracts with Customers International Financial Reporting Standard 15 Revenue from Contracts with Customers IFRS 15 Revenue from

May 2014 International Financial Reporting Standard IFRS 15 Revenue from Contracts with Customers International Financial Reporting Standard 15 Revenue from Contracts with Customers IFRS 15 Revenue from

Practical guide to IFRS Combined and carve out financial statements

pwc.com/ifrs Practical guide to IFRS Combined and carve out financial statements Contents Introduction 1 Step by step approach to the preparation of combined financial 2 statements in accordance with IFRS

pwc.com/ifrs Practical guide to IFRS Combined and carve out financial statements Contents Introduction 1 Step by step approach to the preparation of combined financial 2 statements in accordance with IFRS

DRAFT COMMENT LETTER. Comments should be sent to Commentletter@efrag.org by 21 August 2009

XX August 2009 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom DRAFT COMMENT LETTER Comments should be sent to Commentletter@efrag.org by 21 August 2009 Dear Sir

XX August 2009 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom DRAFT COMMENT LETTER Comments should be sent to Commentletter@efrag.org by 21 August 2009 Dear Sir

Comments on the Exposure Draft Equity Method: Share of Other Net Asset Changes (Proposed amendments to IAS 28)

") March 22, 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Comments on the Exposure Draft Equity Method: Share of Other Net Asset Changes (Proposed

March 22, 2013 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir/Madam, Comments on the Exposure Draft Equity Method: Share of Other Net Asset Changes (Proposed

DISCLOSURES ANNUAL EPS CASH FLOWS CGU JUDGEMENT. Guide to annual financial statements Illustrative disclosures CURRENT ASSOCIATE GOING CONCERN

PERFORMANCE BUSINESS COMBINATIONS OPERATING SEGMENTS CASH FLOWS GOING CONCERN PROFIT OR LOSS DISCLOSURES UNCONSOLIDATED STRUCTURED ENTITIES FINANCIAL POSITION PRESENTATION SIGNIFICANT PROPERTY ACQUISITION

PERFORMANCE BUSINESS COMBINATIONS OPERATING SEGMENTS CASH FLOWS GOING CONCERN PROFIT OR LOSS DISCLOSURES UNCONSOLIDATED STRUCTURED ENTITIES FINANCIAL POSITION PRESENTATION SIGNIFICANT PROPERTY ACQUISITION

IFRS 15: an overview of the new principles of revenue recognition

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

Developing and Reporting Supplementary Financial Measures Definition, Principles, and Disclosures

IFAC Board Exposure Draft February 2014 Professional Accountants in Business Committee International Good Practice Guidance Developing and Reporting Supplementary Financial Measures Definition, Principles,

IFAC Board Exposure Draft February 2014 Professional Accountants in Business Committee International Good Practice Guidance Developing and Reporting Supplementary Financial Measures Definition, Principles,

Consolidated Financial Statements

AASB Standard AASB 10 August 2011 Consolidated Financial Statements Obtaining a Copy of this Accounting Standard This Standard is available on the AASB website: www.aasb.gov.au. Alternatively, printed

AASB Standard AASB 10 August 2011 Consolidated Financial Statements Obtaining a Copy of this Accounting Standard This Standard is available on the AASB website: www.aasb.gov.au. Alternatively, printed

Financial Instruments on Display. Illustrative Disclosures and Guidance on IFRS 7 September 2009

Financial Instruments on Display Illustrative Disclosures and Guidance on IFRS 7 September 2009 Financial Instruments on Display 3 Introduction IFRS 7 Financial Instruments: Disclosures (IFRS 7) is not

Financial Instruments on Display Illustrative Disclosures and Guidance on IFRS 7 September 2009 Financial Instruments on Display 3 Introduction IFRS 7 Financial Instruments: Disclosures (IFRS 7) is not

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Nine months ended, Sep 28, Sep 27, Sep 28, Sep 27, 2014 2015 2014 2015 Net system sales 884.5 975.3 3,157.5 3,356.3

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Nine months ended, Sep 28, Sep 27, Sep 28, Sep 27, 2014 2015 2014 2015 Net system sales 884.5 975.3 3,157.5 3,356.3

ED 10 Consolidated Financial Statements

December 2008 ED 10 EXPOSURE DRAFT ED 10 Consolidated Financial Statements Comments to be received by 20 March 2009 Exposure Draft ED 10 CONSOLIDATED FINANCIAL STATEMENTS Comments to be received by 20

December 2008 ED 10 EXPOSURE DRAFT ED 10 Consolidated Financial Statements Comments to be received by 20 March 2009 Exposure Draft ED 10 CONSOLIDATED FINANCIAL STATEMENTS Comments to be received by 20