Recent amendments in Schedule VI to the Companies Act, 1956

|

|

|

- Marcus Harrell

- 7 years ago

- Views:

Transcription

1 Bombay Chartered Accountants Society Recent amendments in Schedule VI to the Companies Act, 1956 CA. P. R. Ramesh 4th May 2011

2 Agenda History and Applicability. Format. Major Highlights. Comparison with the existing. Points and Issues. 1

3 History and Applicability The 1956 Act. Original Notification for Schedule VI dated 21 st March, Formulation of NACAS Convergence to IFRS. Discussions with ICAI on format etc. Present Notification dated 28 th February,

4 History cont d The MCA Site: The format uploaded. The applicability period mentioned as For the financial year Deletion of the applicability line. Revised applicability period mentioned as effective from Notification issued dated 28 th February, The 35 Accounting Standards. 3

5 History cont d 4

6 Format 5

7 Format cont d 6

8 Format cont d 7

9 Format cont d 8

10 Format cont d 9

11 Format cont d 10

12 Format cont d 11

13 Format cont d 12

14 Format cont d 13

15 Format cont d 14

16 Major Highlights Compliance with the Act and/or Accounting Standards: Requirements of the Act and/or Standards will override the related requirement of Schedule VI. Disclosures as required by Accounting Standards: Additional disclosures specified in the Accounting Standards shall be made in the notes to accounts or by way of additional statement unless required to be disclosed on the face of the Financial Statements. 15

17 Major Highlights - cont d Other Disclosures: All other disclosures as required by the Companies Act shall be made in the notes to accounts in addition to the requirements set out in the Revised Schedule VI 16

18 Major Highlights - cont d Notes to Accounts: Shall contain information in addition to that presented in the Financial Statements and shall provide where required : narrative descriptions or disaggregation of items recognized in those statements and information about items that do not qualify for recognition in those statements. 17

19 Major Highlights - cont d Cross Reference: Each item on the face of the Balance Sheet and Statement of Profit and Loss shall be cross-referenced to any related information in the notes to accounts. Balance to be maintained between: providing excessive detail that may not assist users; and not providing important information as a result of too much aggregation 18

20 Major Highlights - cont d Presentation of figures: Where Turnover: o o < Rs. 100 crores = Figures to be in nearest hundreds, thousands, lakhs or millions or decimals thereof. > Rs. 100 crores = Figures to be in nearest lakhs or millions or crores or decimals thereof. Once a unit of measurement is used, it should be used uniformly in the Financial Statements 19

21 Major Highlights - cont d Figures of previous period: The corresponding amounts (comparatives) for the immediately preceding reporting period for all items shown in the Financial Statements including notes shall also be given. o Terms used: Confusion between comparative figures and corresponding figures As per Accounting Standards. 20

22 Major Highlights - cont d Disclosure requirements: These are minimum requirements. Requirements of industry/sector, Accounting Standards, Companies Act etc. to be considered for disclosure on the face of the Financials Statements. 21

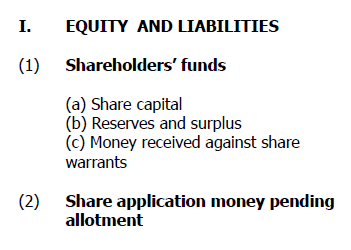

23 Major Highlights - cont d Balance Sheet: Heading changed to Equities and Liabilities from Sources of Funds ; and to Assets from Application of Funds New Line Items - Liabilities: Money received against Share Warrants Share Application Money pending allotment Trade Payables Separate headings for classifying Noncurrent and Current Liabilities. 22

24 Major Highlights - cont d Balance Sheet: New Line Items - Assets: o o o o Intangible Assets under development Trade Receivables Separate headings for classifying Noncurrent and Current Assets. Cash and cash equivalents. 23

25 Major Highlights - cont d Balance Sheet: Concept of Current (assets and liabilities): o o o o Expected to realize in or is intended for sale or consumption in the Normal Operating Cycle It is held primarily for the purpose of being traded Expected to be realized within 12 months after the reporting date It is cash and cash equivalents unless there are restrictions from being exchanged or used to settle a liability for atleast 12 months after the reporting date. 24

26 Major Highlights - cont d Balance Sheet: Concept of Current (assets and liabilities): o The Company s Normal Operating Cycle: An operating cycle is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Where the normal operating cycle cannot be identified, it is assumed to have a duration of 12 months. o To classify as current liabilities, the company must not have an unconditional right to defer settlement of liability for atleast 12 months after the reporting date. 25

27 Major Highlights - cont d Other changes in disclosures: Share Capital: Shares in respect of each class in the company held by its holding company or its ultimate holding company including shares held by or by subsidiaries or associates of the holding company or the ultimate holding company in aggregate. Number of shares held by each shareholder in excess of 5 % together with their names. 26

28 Major Highlights - cont d Reserves and Surplus: Surplus i.e. balance in Statement of Profit and Loss disclosing allocations and appropriations such as dividend, bonus shares and transfer to/from reserves etc. o P&L Appropriation account to be disclosed under Reserves and Surplus. Debit balance of P&L A/c to be shown as a negative figure under the head Surplus. 27

29 Major Highlights - cont d Long-term and Short-term borrowings: Loans and advances from related parties. Period and amount of continuing default as on the balance sheet date in repayment of loans and interest, shall be specified separately in each case. 28

30 Major Highlights - cont d Long-term and Short-term provisions: Provision for employee benefits. Others (specify nature). 29

31 Major Highlights - cont d Other Current liabilities: Current maturities of long-term debt Current maturities of finance lease obligations; Interest accrued but not due on borrowings Interest accrued and due on borrowings; Income received in advance Unpaid dividends 30

32 Major Highlights - cont d Other Current liabilities: Application money received for allotment of securities and due for refund and interest accrued thereon. o o Share application money includes advances towards allotment of share capital. The period for which the share application money has been pending beyond the period for allotment as mentioned in the document inviting application for shares along with the reason for such share application money being pending shall be disclosed. 31

33 Major Highlights - cont d Other Current liabilities: Unpaid matured deposits and interest accrued thereon Unpaid matured debentures and interest accrued thereon Other payables (specify nature); 32

34 Major Highlights - cont d Tangible and Intangible Assets: Movement between opening and closing balances to be given. Details of reduction by way of reduction of capital, revaluation etc. to be given by way of a note. 33

35 Major Highlights - cont d Non-current investments: Includes Investment Property Under each classification, details shall be given of names of the bodies corporate, indicating separately whether such bodies are (i) subsidiaries (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities The nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid). 34

36 Major Highlights - cont d Long-term loans and advances: Capital Advances; Security Deposits; Loans and advances to related parties (giving details thereof); Other loans and advances (specify nature). 35

37 Major Highlights - cont d Inventories: Raw materials; Work-in-progress; Finished goods; Stock-in-trade (in respect of goods acquired for trading); Stores and spares; Loose tools; Others (specify nature). Goods-in-transit shall be disclosed under the relevant sub-head of inventories. 36

38 Major Highlights - cont d Others: The amount of dividends proposed to be distributed to equity and preference shareholders for the period and the related amount per share shall be disclosed separately. Arrears of fixed cumulative dividends on preference shares shall also be disclosed separately. o Thus proposed dividend is not to be provided for in the financial statements? 37

39 Major Highlights - cont d Profit and Loss: Now known as Profit and Loss Statement for the year ended. Format specified in new Schedule. Exceptional and extraordinary items need to be disclosed separately on the face of the Statement of Profit and Loss. The details of the same as also of any prior period items should be disclosed in the notes. 38

40 Major Highlights - cont d Profit and Loss: Profit / loss before and after tax from discontinuing operations and the tax expense from discontinuing operations need to be disclosed separately on the face of the Statement of Profit and Loss. The items to be disclosed under Revenue from Operations have been specifically indicated for both finance companies and others. 39

41 Major Highlights - cont d Profit and Loss: Employee Benefits expense should be disclosed separately as: Salaries and wages Contribution to provident and other funds Expense on ESOP and ESPP Staff welfare expenses 40

42 Major Highlights - cont d Profit and Loss: Payments to auditor as: a. Auditor b. For taxation matters c. For company law matters d. For management services e. For other services f. For reimbursement of expenses 41

43 Major Highlights - cont d Profit and Loss: Any item of income or expenditure which exceeds one percent of the revenue from operations or Rs. 1,00,000 whichever is higher should be disclosed separately. Broad heads shall be decided taking into account the concept of materiality and presentation of true and fair view of financial statements. 42

44 Comparison between the existing Schedule VI Particulars Old Schedule VI Revised Schedule VI Authority Form of Balance Sheet Form of Profit and Loss Account Headings in Balance Sheet Profit and Loss Appropriation Account Provisions of Schedule VI will prevail over Accounting Standards Both horizontal and vertical form were allowed No format specified for Profit and Loss Account Sources of funds and Application of funds Opening surplus, proposed dividend and transfer to/ from reserves were shown in Profit and Loss Appropriation Account Provisions of Accounting Standards will prevail over Schedule VI Only vertical form of Balance Sheet has been specified in the revised Schedule VI Form of Profit and Loss Account specified under Part II Equities and Liabilities and Assets Transfer from/ to reserves to be shown under the heading Reserves & Surplus only. No requirement of separate Profit and Loss Appropriation Account. 43

45 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Proposed Dividend Quantitative Details Proposed Dividend required to be provided for Quantitative details of Raw materials, purchases, stocks and turnover to be given for each class of goods. Also licensed and installed capacity and production quantity to be given for manufacturing companies Proposed Dividend to be disclosed in notes No quantitative details required. Limited requirements for disclosure for CIF and FOB values etc. 44

46 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Rounding off of Figures appearing in financial statement Turnover of less than Rs. 100 Crs - R/off to the nearest Hundreds, thousands or decimal thereof Turnover of Rs. 100 Crs or more but less than Rs. 500 Crs - R/off to the nearest Hundreds, thousands, lakhs or millions or decimal thereof Turnover of Rs. 500 Crs or more - R/off to the nearest Hundreds, thousands, lakhs, millions or crores, or decimal thereof Turnover of less than Rs. 100 Crs - R/off to the nearest Hundreds, thousands, lakhs or millions or decimal thereof Turnover of Rs. 100 Crs or more - R/off to the nearest lakhs, millions or crores, or decimal thereof 45

47 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Share Capital No requirement to disclose separately bonus shares issued during last 5 years. Also no requirement for details of shareholders holding more than 5% of shares In addition to the disclosure requirements of old Schedule VI following additional disclosures are also required Number of bonus shares/ shares allotted without payment being received in cash/ shares bought back during last 5 years Names and number of shares held by shareholders holding more than 5 percent of total shares 46

48 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Net Working Capital Fixed Assets Current assets & Liabilities are shown together under application of funds. The net working capital appears on balance sheet. There was no bifurcation required in to tangible & intangible assets. Capital advances used to be shown under the Head Capital Work in Progress under Fixed Assets Assets & Liabilities are to be bifurcated in to current & Non-current and to be shown separately. Hence, net working capital will not be appearing in Balance sheet. Fixed assets to be shown under non-current assets and have to be bifurcated in to Tangible & intangible assets. Capital advances to be shown under the head Long term Loans and Advances 47

49 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Borrowings Short term & long term borrowings are grouped together under the head Loan funds sub-head Secured / Unsecured Long term borrowings to be shown under non-current liabilities and short term borrowings to be shown under current liabilities with separate disclosure of secured / unsecured loans. Period and amount of continuing default as on the balance sheet date in repayment of loans and interest to be separately specified Deposits Lease deposits are part of loans & advances Lease deposits to be disclosed as long term loans & advances under the head non-current assets 48

50 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Investments Both current & non-current investments to be disclosed under the head investments Current and non-current investments are to be disclosed separately under current assets & non-current assets respectively. Loans & Advances Deferred Tax Assets / Liabilities Loans & Advance are disclosed along with current assets Loans & Advance to subsidiaries & others to be disclosed separately. Deferred Tax assets / liabilities to be disclosed separately Loans & Advances to be broken up in long term & short term and to be disclosed under non-current & current assets respectively. Loans & Advance from related parties & others to be disclosed separately. Deferred Tax assets / liabilities to be disclosed under non-current assets / liabilities as the case may be. 49

51 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Cash & Bank Balances Profit & Loss (Debit Balance) Bank balance to be bifurcated in scheduled banks & others P&L debit balance to be separately disclosed in the Balance Sheet. No such bifurcation required. Bank balances in relation to earmarked balances, held as margin money against borrowings, deposits with more than 12 months maturity, each of these to be shown separately. Debit balance of Profit and Loss Account to be shown as negative figure under the head Surplus. Therefore, Reserve & Surplus can have a negative balance. 50

52 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Sundry Debtors Other current liabilities Separate line item Disclosure criteria Debtors outstanding for more than six months from invoice date to be shown separately No specific mention for separate disclosure of Current maturities of long term debt No specific mention for separate disclosure of Current maturities of finance lease obligation any item under which expense exceeds one per cent of the total revenue of the company or Rs. 5,000 which ever is higher; shall be disclosed separately Debtors outstanding for more than six months from the date they became due to be shown separately Current maturities of long term debt to be disclosed under other current liabilities. Current maturities of finance lease obligation to be disclosed. any item of income / expense which exceeds one per cent of the revenue from operations or Rs. 1,00,000, which ever is higher; to be disclosed separately 51

53 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Expense classification Finance Cost Foreign exchange gain / loss Function wise & nature wise Finance cost to be classified in fixed loans & other loans Gain / Loss on foreign currency transaction to be shown under finance cost Expenses in Statement of Profit and Loss to be classified based on nature of expenses Finance cost shall be classified as interest expense, other borrowing costs & Gain / Loss on foreign currency transaction & translation Gain / Loss on foreign currency transaction to be separated into finance costs and other expenses 52

54 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI Purchases TDS amount on Interest, royalty received Managerial Remuneration and Commission The purchase made and the opening & closing stock, giving break up in respect of each class of goods traded in by the company and indicating the quantities thereof. TDS amount was required to be shown for Interest income etc. Payment to directors and detailed calculation under section 198 was required to be disclosed Goods traded in by the company to be disclosed in broad heads in notes. Disclosure of quantitative details of goods is diluted. Goods-in-transit to be separately disclosed. No requirement of disclosing TDS amounts separately No disclosure requirements for Managerial Remuneration 53

55 Comparison (Cont d) Particulars Old Schedule VI Revised Schedule VI ESOP expenses No requirement to show separately as part of Employee Benefits expense Part III- Interpretation Terms provision, reserve, capital reserve, quoted investment etc. were defined Expense on Employee Stock Option Scheme (ESOP) and Employee Stock Purchase Plan (ESPP) to be shown separately as part of Employee Benefits expense No such specific definitions. Part IV- Balance Sheet Abstract Details of company registration number, capital raised, Balance Sheet details, products etc. were required to be attached with financials No such requirement. 54

56 Points and Issues Status of roll-out of converged Accounting Standards. Reclassification of Previous Year/Period figures. Computation of Net-working capital for finance. Ageing for receivables to be calculated from due date of payment. 55

57 Points and Issues Implementation Issues: Legality of the amendment. Can Sch VI be amended in isolation without any notifications? Substantial efforts required by companies to recast and auditors to audit previous reporting period s figures Challenges faced whilst preparing consolidated financial statements as per revised Sch VI for entities which have a large number of subsidiaries, associates and joint ventures in such a short duration. 56

58 Points and Issues Share Capital (Para 6A) Disclosure of shareholding of each shareholder holding more than 5% of share capital will result in making the disclosure voluminous and the annual report bulkier Challenges in getting information from Depository Participants, GDR / ADR custodians Reserves and Surplus (Para 6B) Lack of clarity whether proposed dividend needs to be provided for. 57

59 Points and Issues Long-term borrowing (Para 6C) Lack of clarity whether the long-term borrowings will get covered for the purposes of determining limits u/s 293(1)(d). Lack of clarity whether Advances and Deposits need to be treated as borrowings Non-Current Investments (Para 6K) Clarification required for nature and definition of Controlled Special Purpose Entity 58

60 Points and Issues Long-term Loans and Advance (Para 6L) Capital Advance whether should be considered as a Long-term Advance or as part of Capital Work-In-Progress. Trade Receivable Ageing based on due date of invoice Vs based on issue date of invoice. Will require significant systemic changes. 59

61 Points and Issues Status of recent notifications for exemptions from certain disclosures (quantitative etc.). Disclosure under the MSME Act. Changes required in ERP systems and Hyperion accounting packages. First step of a mind-set change. 60

62 Thank You

Webcast on Revised Schedule VI. CA. Pankajj Goel

Webcast on Revised Schedule VI CA. Pankajj Goel Overview Background and Applicability Significant Features Major Changes Structure of Revised Schedule VI Form of Balance Sheet Statement of Profit and Loss

Webcast on Revised Schedule VI CA. Pankajj Goel Overview Background and Applicability Significant Features Major Changes Structure of Revised Schedule VI Form of Balance Sheet Statement of Profit and Loss

Welcome to workshop on revised schedule VI. K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Rev Re i v sed e Scheduled VI Dhinal Shah Charte Chart re r d Accoun Accoun a t nt

Revised Scheduled VI Dhinal Shah Chartered Accountant Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards

Revised Scheduled VI Dhinal Shah Chartered Accountant Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards

NEW SCHEDULE VI (SECTION 221)

") NEW SCHEDULE VI (SECTION 221) The Schedule VI has been revised by MCA and is applicable for all Balance Sheet made after 31st March, 2011. The Format has done away with earlier two options of format of

NEW SCHEDULE VI (SECTION 221) The Schedule VI has been revised by MCA and is applicable for all Balance Sheet made after 31st March, 2011. The Format has done away with earlier two options of format of

B S R & Co. Revised Schedule VI Key changes and issues

B S R & Co. Revised Schedule VI Key changes and issues 19 th march2013 Introduction Overall approach Interim Financial Reporting Clause 41 application Key changes related to balance sheet Agenda Key changes

B S R & Co. Revised Schedule VI Key changes and issues 19 th march2013 Introduction Overall approach Interim Financial Reporting Clause 41 application Key changes related to balance sheet Agenda Key changes

SUPPLEMENT ON REVISED SCHEDULE VI

SUPPLEMENT ON REVISED SCHEDULE VI TABLE OF CONTENTS Contents Page no. Introduction to Revised Schedule VI 3 Comparative analysis between Revised and old Schedule VI 6 Format of Revised Schedule VI 9 Supplement

SUPPLEMENT ON REVISED SCHEDULE VI TABLE OF CONTENTS Contents Page no. Introduction to Revised Schedule VI 3 Comparative analysis between Revised and old Schedule VI 6 Format of Revised Schedule VI 9 Supplement

SUPPLEMENT ON REVISED SCHEDULE VI

SUPPLEMENT ON REVISED SCHEDULE VI ICSI House, 22, Institutional Area, Lodi Road, New Delhi 110 003 Ph. : 45341000, 41504444 Fax : 24626727 E-mail : info@icsi.edu; Website : www.icsi.edu C O N T E N T S

SUPPLEMENT ON REVISED SCHEDULE VI ICSI House, 22, Institutional Area, Lodi Road, New Delhi 110 003 Ph. : 45341000, 41504444 Fax : 24626727 E-mail : info@icsi.edu; Website : www.icsi.edu C O N T E N T S

Revised Schedule VI to the Companies Act

Revised Schedule VI to the Companies Act Applicable w. e. f. Financial Year : 2011 2012 1 st & 2 nd Floor, H.K. House, Ashram Road, Ahmedabad 380009 Insight into Schedule VI There is a need to change almost

Revised Schedule VI to the Companies Act Applicable w. e. f. Financial Year : 2011 2012 1 st & 2 nd Floor, H.K. House, Ashram Road, Ahmedabad 380009 Insight into Schedule VI There is a need to change almost

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

Exposure Draft Ind AS-compliant Schedule III to the Companies Act, 2013 For companies other than Non-Banking Finance companies (NBFCs)

") Exposure Draft Ind AS-compliant Schedule III to the Companies Act, 2013 For companies other than Non-Banking Finance companies (NBFCs) (Last Date for comments: January 20, 2015) Issued by Accounting Standards

Exposure Draft Ind AS-compliant Schedule III to the Companies Act, 2013 For companies other than Non-Banking Finance companies (NBFCs) (Last Date for comments: January 20, 2015) Issued by Accounting Standards

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231 A view of financial and non financial elements as may be presented in set of financial statements. Content Page [010000] Filing

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231 A view of financial and non financial elements as may be presented in set of financial statements. Content Page [010000] Filing

ACCOUNTING AND AUDITING UPDATE

ACCOUNTING AND AUDITING UPDATE This February heading 2012 style is set in Univers bold 27.5pt on 30pt Revised Schedule VI This paragraph style is set at 12pt with 16pt leading and 8pt space after. Also

ACCOUNTING AND AUDITING UPDATE This February heading 2012 style is set in Univers bold 27.5pt on 30pt Revised Schedule VI This paragraph style is set at 12pt with 16pt leading and 8pt space after. Also

5N PLUS INC. Condensed Interim Consolidated Financial Statements (Unaudited) For the three month periods ended March 31, 2016 and 2015 (in thousands

For the three month periods ended March 31, 2016 and 2015 (in thousands") Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Indian Accounting Standard (Ind AS) 27. Consolidated and Separate Financial Statements

27. Consolidated and Separate Financial Statements") Indian Accounting Standard (Ind AS) 27 Consolidated and Separate Financial Statements Contents Paragraphs Scope 1-3 Definitions 4-8 Presentation of Consolidated Financial 9-11 Statements Scope of Consolidated

Indian Accounting Standard (Ind AS) 27 Consolidated and Separate Financial Statements Contents Paragraphs Scope 1-3 Definitions 4-8 Presentation of Consolidated Financial 9-11 Statements Scope of Consolidated

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

Problems on Balance Sheet of a Company as per Revised Schedule III of the Companies Act 2013

Problems on Balance Sheet of a Company as per Revised Schedule III of the Companies Act 2013 FORMAT OF BALANCE SHEET BALANCE SHEET of.company Limited as on 31 st March. Particulars Note No. Amount (Rs.)

Problems on Balance Sheet of a Company as per Revised Schedule III of the Companies Act 2013 FORMAT OF BALANCE SHEET BALANCE SHEET of.company Limited as on 31 st March. Particulars Note No. Amount (Rs.)

Acal plc. Accounting policies March 2006

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Acal plc Accounting policies March 2006 Basis of preparation The consolidated financial statements of Acal plc and all its subsidiaries have been prepared in accordance with International Financial Reporting

Large Company Limited. Report and Accounts. 31 December 2009

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Small Company Limited. Report and Accounts. 31 December 2007

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

Registered number 123456 Small Company Limited Report and Accounts 31 December 2007 Report and accounts Contents Page Company information 1 Directors' report 2 Accountants' report 3 Profit and loss account

Financial Statements Presentation under Companies Act, 2013: Practitioner s Perspective

Financial Statements Presentation under Companies Act, 2013: Practitioner s Perspective Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF&SMP) The Institute of Chartered

Financial Statements Presentation under Companies Act, 2013: Practitioner s Perspective Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF&SMP) The Institute of Chartered

Financial Statements

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

IFrS. Disclosure checklist. July 2011. kpmg.com/ifrs

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

Oracle (OFSS) Processing Services Limited. Directors Report

Processing Services Limited. Directors Report") Directors Report Dear Members, Your Directors take pleasure in bringing you the Sixth Annual Report of your Company along with the Audited Accounts of the Company for the financial year from April 01,

Directors Report Dear Members, Your Directors take pleasure in bringing you the Sixth Annual Report of your Company along with the Audited Accounts of the Company for the financial year from April 01,

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002 Unaudited Unaudited Note Turnover 2 5,576 5,803 Other net losses (1) (39) 5,575 5,764 Direct costs and operating expenses (1,910)

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the six months ended June 30, 2002 Unaudited Unaudited Note Turnover 2 5,576 5,803 Other net losses (1) (39) 5,575 5,764 Direct costs and operating expenses (1,910)

Small Company Limited. Abbreviated Accounts. 31 December 2007

Registered number 123456 Small Company Limited Abbreviated Accounts 31 December 2007 Abbreviated Balance Sheet as at 31 December 2007 Notes 2007 2006 Fixed assets Intangible assets 2 Tangible assets 3

Registered number 123456 Small Company Limited Abbreviated Accounts 31 December 2007 Abbreviated Balance Sheet as at 31 December 2007 Notes 2007 2006 Fixed assets Intangible assets 2 Tangible assets 3

NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS

NAS 01 NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 PURPOSE OF FINANCIAL STATEMENTS 5 Responsibility for financial statements 6 Components

NAS 01 NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 PURPOSE OF FINANCIAL STATEMENTS 5 Responsibility for financial statements 6 Components

IFRS. Disclosure checklist. August 2012. kpmg.com/ifrs

IFRS Disclosure checklist August 2012 kpmg.com/ifrs Contents About this publication 1 What s new? 2 The Checklist 3 1. General presentation 3 1.1 Presentation of financial statements 3 1.2 Changes in equity

IFRS Disclosure checklist August 2012 kpmg.com/ifrs Contents About this publication 1 What s new? 2 The Checklist 3 1. General presentation 3 1.1 Presentation of financial statements 3 1.2 Changes in equity

Principal Accounting Policies

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

1. Basis of Preparation The accounts have been prepared in accordance with Hong Kong Financial Reporting Standards ( HKFRS ). The accounts have been prepared under the historical cost convention as modified

SUMMARY OF CONSOLIDATED BUSINESS RESULTS for the nine months ended December 31, 2012

SUMMARY OF CONSOLIDATED BUSINESS RESULTS for the nine months ended December 31, 2012 February 8, 2013 ARRK Corporation 2-2-9 Minami Hommachi, Chuo-ku, Osaka, 541-0054, JAPAN 1. Consolidated financial results

SUMMARY OF CONSOLIDATED BUSINESS RESULTS for the nine months ended December 31, 2012 February 8, 2013 ARRK Corporation 2-2-9 Minami Hommachi, Chuo-ku, Osaka, 541-0054, JAPAN 1. Consolidated financial results

PRELIMINARY RESULTS FOR HALF YEAR ENDED 30 SEPTEMBER 2015

Page 1 PRELIMINARY RESULTS FOR HALF YEAR ENDED 30 SEPTEMBER 2015 Reporting Period 6 months to 30 September 2015 Reporting Period 6 months to 30 September 2014 Amount NZ$ 000 Percentage Change % Revenue

Page 1 PRELIMINARY RESULTS FOR HALF YEAR ENDED 30 SEPTEMBER 2015 Reporting Period 6 months to 30 September 2015 Reporting Period 6 months to 30 September 2014 Amount NZ$ 000 Percentage Change % Revenue

Lonmin Plc Adoption of International Financial Reporting Standards. Unaudited Restatement of Accounts

Lonmin Plc Adoption of International Financial Reporting Standards Unaudited Restatement of Accounts Financial highlights Relatively limited impacts on profitability for the year to 30 September 2005 under

Lonmin Plc Adoption of International Financial Reporting Standards Unaudited Restatement of Accounts Financial highlights Relatively limited impacts on profitability for the year to 30 September 2005 under

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

Consolidated balance sheet

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 (2Q FY2011)

") November 8, 2011 Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 () Name of the company: Iwatani Corporation Share traded: TSE, OSE, and NSE first sections Company

November 8, 2011 Overview of Business Results for the 2nd Quarter of Fiscal Year Ending March 31, 2012 () Name of the company: Iwatani Corporation Share traded: TSE, OSE, and NSE first sections Company

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Results For The Financial Year Ended 31 December 2014 Unaudited Financial Statements and Dividend Announcement

Financial Statements and Related Announcement::Full Yearly Results http://infopub.sgx.com/apps?a=cow_corpannouncement_content&b=announcem... Page 1 of 1 2/27/2015 Financial Statements and Related Announcement::Full

Financial Statements and Related Announcement::Full Yearly Results http://infopub.sgx.com/apps?a=cow_corpannouncement_content&b=announcem... Page 1 of 1 2/27/2015 Financial Statements and Related Announcement::Full

GOODYEAR (THAILAND) PUBLIC COMPANY LIMITED FINANCIAL STATEMENTS 31 DECEMBER 2011

PUBLIC COMPANY LIMITED FINANCIAL STATEMENTS 31 DECEMBER 2011") GOODYEAR (THAILAND) PUBLIC COMPANY LIMITED FINANCIAL STATEMENTS 31 DECEMBER 2011 AUDITOR S REPORT To the Shareholders of Goodyear (Thailand) Public Company Limited I have audited the accompanying statements

GOODYEAR (THAILAND) PUBLIC COMPANY LIMITED FINANCIAL STATEMENTS 31 DECEMBER 2011 AUDITOR S REPORT To the Shareholders of Goodyear (Thailand) Public Company Limited I have audited the accompanying statements

Mantas India Private Limited. Directors Report

Mantas India Private Limited Directors Report Dear Members, Your Directors take pleasure in bringing you the Annual Report of your Company along with the Audited Accounts for the financial year from April

Mantas India Private Limited Directors Report Dear Members, Your Directors take pleasure in bringing you the Annual Report of your Company along with the Audited Accounts for the financial year from April

Jones Sample Accounts Limited. Company Registration Number: 04544332 (England and Wales) Report of the Directors and Unaudited Financial Statements

Report of the Directors and Unaudited Financial Statements") Company Registration Number: 04544332 (England and Wales) Report of the Directors and Unaudited Financial Statements Period of accounts Start date: 1st June 2008 End date: 31st May 2009 Contents of the

Company Registration Number: 04544332 (England and Wales) Report of the Directors and Unaudited Financial Statements Period of accounts Start date: 1st June 2008 End date: 31st May 2009 Contents of the

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Preliminary Final report

Appendix 4E Rule 4.3A Preliminary Final report AMCOR LIMITED ABN 62 000 017 372 1. Details of the reporting period and the previous corresponding period Reporting Period: Year Ended Previous Corresponding

Appendix 4E Rule 4.3A Preliminary Final report AMCOR LIMITED ABN 62 000 017 372 1. Details of the reporting period and the previous corresponding period Reporting Period: Year Ended Previous Corresponding

5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT I. GENERAL PROVISIONS II. KEY DEFINITIONS

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

<NAME OF THE BROKERING FIRM> STATEMENT OF FINANCIAL POSITION AS AT <.>

ASSETS STATEMENT OF FINANCIAL POSITION AS AT NOTES ANNEXURE 4 NON CURRENT ASSETS PROPERTY, PLANT & EQUIPMENT 1 INTANGIBLE ASSETS 2 INVESTMENT IN SUBSIDIARIES 3 INVESTMENT

ASSETS STATEMENT OF FINANCIAL POSITION AS AT NOTES ANNEXURE 4 NON CURRENT ASSETS PROPERTY, PLANT & EQUIPMENT 1 INTANGIBLE ASSETS 2 INVESTMENT IN SUBSIDIARIES 3 INVESTMENT

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

Condensed Consolidated Statement of Comprehensive Income For the second quarter ended 30 September 2013 (Unaudited)

") Condensed Consolidated Statement of Comprehensive Income For the second quarter ended 30 September 2013 (Unaudited) Group Individual Quarter ended Unaudited Unaudited 30 Sep 2012 (Company No: 591898-H)

Condensed Consolidated Statement of Comprehensive Income For the second quarter ended 30 September 2013 (Unaudited) Group Individual Quarter ended Unaudited Unaudited 30 Sep 2012 (Company No: 591898-H)

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS. Actuarial Gains and Losses, Group Plans and Disclosures

08 TCL Multimedia Technology Holdings Limited INTERIM RESULTS NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 1. Basis of preparation The Directors are responsible for the preparation of the Group

08 TCL Multimedia Technology Holdings Limited INTERIM RESULTS NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 1. Basis of preparation The Directors are responsible for the preparation of the Group

NOTICE OF NO AUDITOR REVIEW OF INTERIM FINANCIAL STATEMENTS

Condensed Interim Consolidated Financial Statements of THE BRICK LTD. For the three months ended March 31, 2013 NOTICE OF NO AUDITOR REVIEW OF INTERIM FINANCIAL STATEMENTS Under National Instrument 51-102,

Condensed Interim Consolidated Financial Statements of THE BRICK LTD. For the three months ended March 31, 2013 NOTICE OF NO AUDITOR REVIEW OF INTERIM FINANCIAL STATEMENTS Under National Instrument 51-102,

Summary of Significant Accounting Policies FOR THE FINANCIAL YEAR ENDED 31 MARCH 2014

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

46 Unless otherwise stated, the following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements. The Company and

C. A. FINAL FINANCIAL REPORTING VALUE ADDED STATEMENT

C. A. FINAL FINANCIAL REPORTING VALUE ADDED STATEMENT Q.1. X Ltd. had been preparing value added statement for the past five years. The personnel manager of company has suggested that a value added incentive

C. A. FINAL FINANCIAL REPORTING VALUE ADDED STATEMENT Q.1. X Ltd. had been preparing value added statement for the past five years. The personnel manager of company has suggested that a value added incentive

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

Second Quarter Unaudited Financial Statements for the Period Ended 30 June 2012 `

(Company Registration No : 195800035D) Second Quarter Unaudited Financial Statements for the Period Ended 30 June 2012 ` 1(a) (i) The following statements in the form presented in the group s most recently

(Company Registration No : 195800035D) Second Quarter Unaudited Financial Statements for the Period Ended 30 June 2012 ` 1(a) (i) The following statements in the form presented in the group s most recently

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL BROKERAGE FIRMS AND MANAGEMENT COMPANIES I. GENERAL PROVISIONS

APPROVED by Order No. VAS-6 of 12 May 2006 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL

APPROVED by Order No. VAS-6 of 12 May 2006 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014 covering the period from 01-07-2013 to 30-09-2013 Publication date: 14 November 2013

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014 covering the period from 01-07-2013 to 30-09-2013 Publication date: 14 November 2013

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Treatment of Various Items under Revised Schedule VI of the Companies Act, 1956

Treatment of Various Items under Revised Schedule VI of the Companies Act, 1956 IMPORTANT NOTE Detail of each entry (item) in the Balance Sheet and Statement of Profit and Loss is to be given by way of

Treatment of Various Items under Revised Schedule VI of the Companies Act, 1956 IMPORTANT NOTE Detail of each entry (item) in the Balance Sheet and Statement of Profit and Loss is to be given by way of

Closing Announcement of First Quarter of the Fiscal Year Ending March 31, 2009

Member of Financial Accounting Standards Foundation Closing Announcement of First Quarter of the Fiscal Year Ending March 31, 2009 Name of Listed Company: Arisawa Mfg. Co., Ltd. Listed on the 1st Section

Member of Financial Accounting Standards Foundation Closing Announcement of First Quarter of the Fiscal Year Ending March 31, 2009 Name of Listed Company: Arisawa Mfg. Co., Ltd. Listed on the 1st Section

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

OOREDOO Q.S.C. CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS 30 SEPTEMBER 2015

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS 30 SEPTEMBER 2015 CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS As at and for the nine months ended 2015 CONTENTS Page (s) Independent auditors

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS 30 SEPTEMBER 2015 CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS As at and for the nine months ended 2015 CONTENTS Page (s) Independent auditors

Diploma in International Financial Reporting Standards (IFRSs)

") Chartered Accountants Ireland Diploma in International Financial Reporting Standards (IFRSs) Objective This Diploma is designed to provide qualified Chartered Accountants with the opportunity to enhance

Chartered Accountants Ireland Diploma in International Financial Reporting Standards (IFRSs) Objective This Diploma is designed to provide qualified Chartered Accountants with the opportunity to enhance

Accounting for ESOP. IPCC Paper 5: Advanced Accounting Chapter 4. CA. Shruthi BN, Bangalore

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS (1) Consolidated Quarterly Balance Sheets September 30, 2014 and March 31, 2014 Supplementary Information 2Q FY March 2015 March 31, 2014 September 30, 2014

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS (1) Consolidated Quarterly Balance Sheets September 30, 2014 and March 31, 2014 Supplementary Information 2Q FY March 2015 March 31, 2014 September 30, 2014

None of the Directors had an interest in the shares of the company at any time during the year.

EMAMI BANGLADESH LIMITED DIRECTORS REPORT FOR THE PERIOD 01 st APRIL 2014 TO 31 st MARCH 2015 The directors present their report and the financial statements for the period 1 st April 2014 to 31 st March

EMAMI BANGLADESH LIMITED DIRECTORS REPORT FOR THE PERIOD 01 st APRIL 2014 TO 31 st MARCH 2015 The directors present their report and the financial statements for the period 1 st April 2014 to 31 st March

$ 2,035,512 98,790 6,974,247 2,304,324 848,884 173,207 321,487 239,138 (117,125) 658,103

658,103") FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

1. Basis of Preparation. 2. Summary of Significant Accounting Policies. Principles of consolidation. (a) Foreign currency translation.

Foreign currency translation.") Nitta Corporation and Subsidiaries Notes to Consolidated Financial Statements March 31, 1. Basis of Preparation The accompanying consolidated financial statements of Nitta Corporation (the Company ) and

Nitta Corporation and Subsidiaries Notes to Consolidated Financial Statements March 31, 1. Basis of Preparation The accompanying consolidated financial statements of Nitta Corporation (the Company ) and

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

ČEZ, a. s. FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015

ČEZ, a. s. FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015 PRELIMINARY UNAUDITED ACCOUNTS Prepared as of March 14, 2016 ČEZ, a. s. BALANCE

ČEZ, a. s. FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS OF DECEMBER 31, 2015 PRELIMINARY UNAUDITED ACCOUNTS Prepared as of March 14, 2016 ČEZ, a. s. BALANCE

Volex Group plc. Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement. 1.

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

International Accounting Standard 1 Presentation of Financial Statements

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

Appendix 5B. Mining exploration entity quarterly report. Quarter ended ( current quarter ) 108 476 384 30 September 2015

108 476 384 30 September 2015") Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity Aurelia Metals

Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity Aurelia Metals

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET. ASSETS Unaudited Current Audited Previous Dipnot I- Current Assets

ASSETS Unaudited Current Audited Previous Dipnot I- Current Assets A- Cash and Cash Equivalents 14 2.364.314.943 2.304.904.212 1- Cash 14 38.784 18.864 2- Cheques Received 3- Banks 14 1.961.058.269 1.937.834.876

ASSETS Unaudited Current Audited Previous Dipnot I- Current Assets A- Cash and Cash Equivalents 14 2.364.314.943 2.304.904.212 1- Cash 14 38.784 18.864 2- Cheques Received 3- Banks 14 1.961.058.269 1.937.834.876

Report and Non-Statutory Accounts

Report and Non-Statutory Accounts 31 December Registered No CR - 117363 Cayman Islands Registered office: PO Box 309 GT, Ugland House, South Church Street, George Town, Grand Cayman, Cayman Islands Report

Report and Non-Statutory Accounts 31 December Registered No CR - 117363 Cayman Islands Registered office: PO Box 309 GT, Ugland House, South Church Street, George Town, Grand Cayman, Cayman Islands Report

Exposure Draft. Guidance Note on Accounting for Derivative Contracts

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

PENSONIC HOLDINGS BERHAD (300426-P) (Incorporated in Malaysia) CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE QUARTER ENDED 31 AUGUST 2015

(Incorporated in Malaysia) CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE QUARTER ENDED 31 AUGUST 2015") CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE QUARTER ENDED 31 AUGUST 2015 CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE QUARTER ENDED 31 AUGUST 2015 (Unaudited) Individual Quarter

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE QUARTER ENDED 31 AUGUST 2015 CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE QUARTER ENDED 31 AUGUST 2015 (Unaudited) Individual Quarter

CEMATRIX CORPORATION Consolidated Financial Statements (in Canadian dollars) September 30, 2015

September 30, 2015") Consolidated Financial Statements September 30, 2015 Management s Responsibility for Financial Reporting and Notice of No Auditor Review of the Interim Consolidated Financial Statements for the Three and

Consolidated Financial Statements September 30, 2015 Management s Responsibility for Financial Reporting and Notice of No Auditor Review of the Interim Consolidated Financial Statements for the Three and

DIRECTORS REPORT TO THE MEMBERS

DIRECTORS REPORT TO THE MEMBERS Your Directors present their Fourth Report together with the audited accounts of the Company for the year ended 31 st March, 2013. FINANCIAL HIGHLIGHTS Particulars For the

DIRECTORS REPORT TO THE MEMBERS Your Directors present their Fourth Report together with the audited accounts of the Company for the year ended 31 st March, 2013. FINANCIAL HIGHLIGHTS Particulars For the

Presentation of Items of Other Comprehensive Income. (Amendments to SB-FRS 1)

") STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 1 Presentation of Items of Other Comprehensive Income (Amendments to SB-FRS 1) This standard applies for annual periods beginning on or after 1 July

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 1 Presentation of Items of Other Comprehensive Income (Amendments to SB-FRS 1) This standard applies for annual periods beginning on or after 1 July

Model financial statements for the year ended 30 June 2011

Model financial statements for the year ended Illustrative example of general purpose financial statements prepared in accordance with the Financial Reporting Act 1993, the Companies Act 1993, applying

Model financial statements for the year ended Illustrative example of general purpose financial statements prepared in accordance with the Financial Reporting Act 1993, the Companies Act 1993, applying

International Accounting Standard 12 Income Taxes

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

Consolidated Financial Results for Six Months Ended September 30, 2007

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET ASSETS

ASSETS ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ I- Current Assets Audited Current Audited Previous Period Period Notes 31/12/2015 31/12/2014 A- Cash and Cash Equivalents 14 2.304.904.212 1.606.048.714 1- Cash

ASSETS ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ I- Current Assets Audited Current Audited Previous Period Period Notes 31/12/2015 31/12/2014 A- Cash and Cash Equivalents 14 2.304.904.212 1.606.048.714 1- Cash

Half Year Financial Statement And Announcement for the Period Ended 31/12/2010

AUSSINO GROUP LTD Company Registration No.: 199100323H Half Year Financial Statement And Announcement for the Period Ended 31/12/2010 PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2

AUSSINO GROUP LTD Company Registration No.: 199100323H Half Year Financial Statement And Announcement for the Period Ended 31/12/2010 PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2

ABN 17 006 852 820 PTY LTD (FORMERLY KNOWN AS AQUAMAX PTY LTD) DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015

DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015") DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015 In accordance with a resolution of the Directors dated 16 December 2015, the Directors of the Company have pleasure in reporting on the Company for

DIRECTORS REPORT FOR THE YEAR ENDED 30 SEPTEMBER 2015 In accordance with a resolution of the Directors dated 16 December 2015, the Directors of the Company have pleasure in reporting on the Company for

For personal use only

ASX RELEASE 21 March 2012 Market Update February 2012 The Report on Cash Flows for the month of February 2012, provided in accordance with Listing Rule 4.7B(d), is attached. Debt Facility The Company confirms

ASX RELEASE 21 March 2012 Market Update February 2012 The Report on Cash Flows for the month of February 2012, provided in accordance with Listing Rule 4.7B(d), is attached. Debt Facility The Company confirms

CAPITAL GROUP CENTRUM NOWOCZESNYCH TECHNOLOGII SPÓŁKA AKCYJNA

CAPITAL GROUP CENTRUM NOWOCZESNYCH TECHNOLOGII SPÓŁKA AKCYJNA MID-YEAR CONDENSED CONSOLIDATED FINANCIAL STATEMENT OF THE CAPITAL GROUP CNT S.A. AND MID-YEAR CONDENSED SEPARATE FINANCIAL STATEMENT OF CNT

CAPITAL GROUP CENTRUM NOWOCZESNYCH TECHNOLOGII SPÓŁKA AKCYJNA MID-YEAR CONDENSED CONSOLIDATED FINANCIAL STATEMENT OF THE CAPITAL GROUP CNT S.A. AND MID-YEAR CONDENSED SEPARATE FINANCIAL STATEMENT OF CNT

Acerinox, S.A. and Subsidiaries. Consolidated Annual Accounts 31 December 2014. Consolidated Directors' Report 2014. (With Auditors Report Thereon)

") Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2014 Consolidated Directors' Report 2014 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2014 Consolidated Directors' Report 2014 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

462 IBN18 (MAURITIUS) LIMITED. IBN18 (Mauritius) Limited

LIMITED. IBN18 (Mauritius) Limited") 462 IBN18 (MAURITIUS) LIMITED IBN18 (Mauritius) Limited IBN18 (MAURITIUS) LIMITED 463 Independent Auditors Report Independent Auditors Report to the member of IBN18 (Mauritius) Limited Report on the Financial

462 IBN18 (MAURITIUS) LIMITED IBN18 (Mauritius) Limited IBN18 (MAURITIUS) LIMITED 463 Independent Auditors Report Independent Auditors Report to the member of IBN18 (Mauritius) Limited Report on the Financial

Consolidated Financial Statements

Consolidated Financial Statements Consolidated Income Statement for the year ended 30 June Consolidated Financial Statements Notes $'000 $'000 Revenue from continuing operations 437,459 336,460 Employee

Consolidated Financial Statements Consolidated Income Statement for the year ended 30 June Consolidated Financial Statements Notes $'000 $'000 Revenue from continuing operations 437,459 336,460 Employee

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

The Awa Bank, Ltd. Consolidated Financial Statements. The Awa Bank, Ltd. and its Consolidated Subsidiaries. Years ended March 31, 2011 and 2012

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2011 and 2012 Consolidated Balance Sheets (Note 1) 2011 2012 2012 Assets Cash and due from banks (Notes 3 and 4) \ 230,831 \

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2011 and 2012 Consolidated Balance Sheets (Note 1) 2011 2012 2012 Assets Cash and due from banks (Notes 3 and 4) \ 230,831 \

2 FSA002 Income statement

2 FSA002 Income statement This data item provides the PRA with information on the main sources of income and expenditure for a firm. It should be completed on a cumulative basis for the firm's current

2 FSA002 Income statement This data item provides the PRA with information on the main sources of income and expenditure for a firm. It should be completed on a cumulative basis for the firm's current