While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if...

|

|

|

- Corey Thompson

- 7 years ago

- Views:

Transcription

1 Monopoly

2 Cause of monopoly

3 While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes there are significant barriers to enter the market.

4 Microsoft has the market power for Windows operating system. The market price charged by each legal copy of the Windows operating system exceeds the mariginal costs of production. Why the price is not even higher? Because people wouldn t buy Although monopolies can control prices of their good, their profits are not unlimited!

5 The fundamental cause of monopoly is barriers to entry. Barriers to entry have three sources: Ownership of a key resource. The government gives a single firm the exclusive right to produce some good. Costs of production make a single producer more efficient than a large number of producers.

6 Although exclusive ownership of a key resource is a potential source of monopoly, in practice monopolies rarely arise for this reason. Nowadays, resources are owned by many people. Many goods are traded internationally and the scope of their markets is worldwide.

7 Governments may restrict entry by giving a single firm the exclusive right to sell a particular good in certain markets. Patent and copyright laws are two important examples of how government creates a monopoly to serve the public interest.

8 An industry is a natural monopoly when a single firm can supply a good or service to an entire market at a smaller cost than could two or more firms. A natural monopoly arises when there are economies of scale over the relevant range of output.

9 Copyright 2004 South-Western Cost Average total cost 0 Quantity of Output

10 Monopoly versus Competition Monopoly Is the sole producer Faces a downward-sloping demand curve Is a price maker Reduces price to increase sales Competitive Firm Is one of many producers Faces a horizontal demand curve Is a price taker Sells as much or as little at the same price

11 Copyright 2004 South-Western (a) A Competitive Firm s Demand Curve (b) A Monopolist s Demand Curve Price Price Demand Demand 0 Quantity of Output 0 Quantity of Output

12 The company was founded in 1888 by Cecil Rhodes: in 1871, he found a 83.5 carat diamond on Kimberley, South Africa he invested the profits into buying up small mining operators In 1888, he founded De Beers, as a result of merge He was the sole owner of all diamond mining operations in South Africa.

13 In 1889, Rhodes got an agreement with the London-based Diamond Syndicate, which agreed to purchase a fixed quantity of diamonds at an agreed price. in 1902, De Beers controlled 90% of the world's diamond production.

14 the only way to increase the value of diamonds is to make them scarce, that is to reduce production. E. Oppenheimer (later chair of the company) It controlled prices by: purchasing and stockpiling diamonds produced by other manufacturers convincing independent producers to join its single channel monopoly flooding the market with diamonds similar to those of producers who refused to join the cartel.

15 The end of the monopoly: In 2000, producers in Russia, Canada and Australia decided to distribute diamonds outside of the De Beers channel. Rising awareness of blood diamonds that forced De Beers to limit sales to its own mined products. De Beers market share fell from 90% in the 1980s to less than 40% in 2012.

16 Is a Microsoft truly the monopolist? Large market share Behavior Limits the access to documentation, which enables developing of competitive software Sell jointly Internet Explorer with an operating system Exclusionary agreements

17 Microsoft: Settled anti-trust litigation in the U.S. in 2001 Fined 493 million euros by the European Commission in 2004 Fined 1.35 Billion USD in 2008 for noncompliance with the 2004 rule. Is the Microsoft truly the monopolist or very strong competitor?

18 Polish mail (Poczta Polska) Deutsche Telekom: former state monopoly, still partially state owned, currently monopolizes high-speed VDSL broadband network Warsaw underground

19 Decision process

20 Total Revenue Average Revenue Marginal Revenue TR AR TR Q Q P Q P Q MR TR Q 1 1/ E P P Q

21 Copyright 2004 South-Western

22 A Monopoly s Marginal Revenue A monopolist s marginal revenue is always less than the price of its good. The demand curve is downward sloping. When a monopoly drops the price to sell one more unit, the revenue received from previously sold units also decreases.

23 A Monopoly s Marginal Revenue When a monopoly increases the amount it sells, it has two effects on total revenue (P Q). The output effect more output is sold, so Q is higher. The price effect price falls, so P is lower.

24 Copyright 2004 South-Western Price $ Marginal revenue Demand (average revenue) Quantity of Water

25 A monopoly maximizes profit by producing the quantity at which marginal revenue equals marginal cost. It then uses the demand curve to find the price that will induce consumers to buy that quantity.

26 Copyright 2004 South-Western Costs and Revenue Monopoly price and then the demand curve shows the price consistent with this quantity. B 1. The intersection of the marginal-revenue curve and the marginal-cost curve determines the profit-maximizing quantity... A Average total cost Marginal cost Demand Marginal revenue 0 Q Q MAX Q Quantity

27 Comparing Monopoly and Competition For a competitive firm, price equals marginal cost. P = MR = MC For a monopoly firm, price exceeds marginal cost. P > MR = MC

28 Profit equals total revenue minus total costs. Profit = TR - TC Profit = (TR/Q - TC/Q) Q Profit = (P - ATC) Q

29 Copyright 2004 South-Western Costs and Revenue Marginal cost Monopoly price E B Monopoly profit Average total cost Average total cost D C Demand Marginal revenue 0 Q MAX Quantity

30 The monopolist will receive economic profits as long as price is greater than average total cost.

31 Two type of market structures observed: Monopoly: patent laws give the monopoly on sale drugs for some time Competition: when the patent runs out, any firm may produce and sell the drug During the life of the patent the price is above the marginal cost When the patent runs out, new firms enter the market and the price falls

32 Copyright 2004 South-Western Costs and Revenue Price during patent life Price after patent expires Marginal revenue Demand Marginal cost 0 Monopoly quantity Competitive quantity Quantity

33 Suppose, a company is a monopolist and faces the downward sloping demand curve P D 100 2Q The company has the following cost structure TC 10 40Q Q How much will the firm produce? At what cost and price? What are the firm profits? 2

34 Consumer and producer surplus

35 Welfare economics is the study of how the allocation of resources affects economic wellbeing. Buyers and sellers receive benefits from taking part in the market. The equilibrium in a market maximizes the total welfare of buyers and sellers.

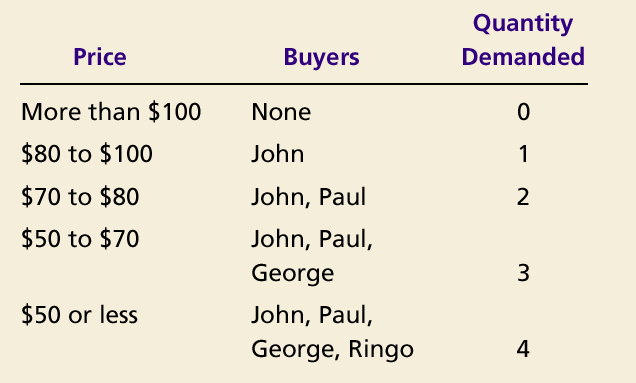

36 Equilibrium in the market results in maximum benefits, and therefore maximum total welfare for both the consumers and the producers of the product.

37 Consumer surplus measures economic welfare from the buyer s side. Producer surplus measures economic welfare from the seller s side.

38 Willingness to pay is the maximum amount that a buyer will pay for a good. It measures how much the buyer values the good or service.

39 Consumer surplus is the buyer s willingness to pay for a good minus the amount the buyer actually pays for it.

40 Copyright 2004 South-Western

41 The market demand curve depicts the various quantities that buyers would be willing and able to purchase at different prices.

42

43 Copyright 2003 Southwestern/Thomson Learning Price of Album $100 John s willingness to pay 80 Paul s willingness to pay 70 George s willingness to pay 50 Ringo s willingness to pay Demand Quantity of Albums

44 Copyright 2003 Southwestern/Thomson Learning Price of Album (a) Price = $80 $100 John s consumer surplus ($20) Demand Quantity of Albums

45 Copyright 2003 Southwestern/Thomson Learning Price of Album $ (b) Price = $70 John s consumer surplus ($30) Paul s consumer surplus ($10) 50 Total consumer surplus ($40) Demand Quantity of Albums

46 The area below the demand curve and above the price measures the consumer surplus in the market.

47 Copyright 2003 Southwestern/Thomson Learning (a) Consumer Surplus at Price P Price A Consumer surplus P 1 B C Demand 0 Q 1 Quantity

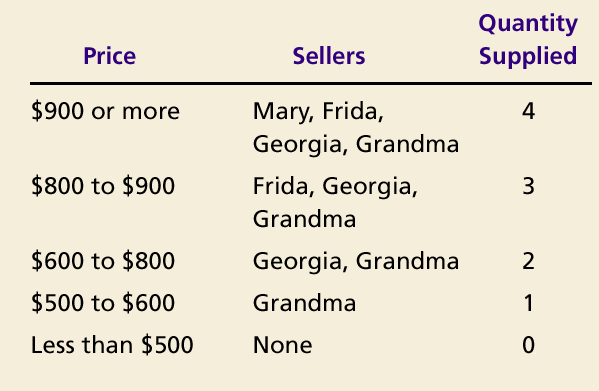

48 Copyright 2003 Southwestern/Thomson Learning (b) Consumer Surplus at Price P Price A P 1 Initial consumer surplus B C Consumer surplus to new consumers P 2 D Additional consumer surplus to initial consumers E F Demand 0 Q 1 Q 2 Quantity

49 Consumer surplus, the amount that buyers are willing to pay for a good minus the amount they actually pay for it, measures the benefit that buyers receive from a good as the buyers themselves perceive it.

50 Producer surplus is the amount a seller is paid for a good minus the seller s cost. It measures the benefit to sellers participating in a market.

51 Copyright 2004 South-Western

52 Just as consumer surplus is related to the demand curve, producer surplus is closely related to the supply curve.

53

54

55 The area below the price and above the supply curve measures the producer surplus in a market.

56 (a) Price = $600 Price of House Painting Supply $ Grandma s producer surplus ($100) Quantity of Houses Painted Copyright 2003 Southwestern/Thomson Learning

57 Price of House Painting $ Total producer surplus ($500) (b) Price = $800 Supply Georgia s producer surplus ($200) Grandma s producer surplus ($300) Quantity of Houses Painted Copyright 2003 Southwestern/Thomson Learning

58 Copyright 2003 Southwestern/Thomson Learning (a) Producer Surplus at Price P Price Supply P 1 B Producer surplus C A 0 Q 1 Quantity

59 Copyright 2003 Southwestern/Thomson Learning (b) Producer Surplus at Price P Price Additional producer surplus to initial producers Supply P 2 D E F P 1 B Initial producer surplus C Producer surplus to new producers A 0 Q 1 Q 2 Quantity

60 Consumer surplus and producer surplus may be used to address the following question: Is the allocation of resources determined by free markets in any way desirable?

61 Consumer Surplus = Value to buyers Amount paid by buyers and Producer Surplus = Amount received by sellers Cost to sellers

62 Total surplus = Consumer surplus + Producer surplus or Total surplus = Value to buyers Cost to sellers

63 Efficiency is the property of a resource allocation of maximizing the total surplus received by all members of society.

64 In addition to market efficiency, a social planner might also care about equity the fairness of the distribution of well-being among the various buyers and sellers.

65 Copyright 2003 Southwestern/Thomson Learning Price A D Supply Equilibrium price Consumer surplus Producer surplus E B Demand C 0 Equilibrium Quantity quantity

66 Three Insights Concerning Market Outcomes Free markets allocate the supply of goods to the buyers who value them most highly, as measured by their willingness to pay. Free markets allocate the demand for goods to the sellers who can produce them at least cost. Free markets produce the quantity of goods that maximizes the sum of consumer and producer surplus.

67 Because the equilibrium outcome in a competitive market is an efficient allocation of resources, the social planner can leave the market outcome as he/she finds it.

68 Market Power If a market system is not perfectly competitive, market power may result. Market power can cause markets to be inefficient because it keeps price and quantity from the equilibrium of supply and demand.

69 Deadweight loss

70 In contrast to a competitive firm, the monopoly charges a price above the marginal cost. From the standpoint of consumers, this high price makes monopoly undesirable. However, from the standpoint of the owners of the firm, the high price makes monopoly very desirable.

71 Copyright 2004 South-Western Price Marginal cost Value to buyers Cost to monopolist Cost to monopolist Value to buyers Demand (value to buyers) 0 Quantity Value to buyers is greater than cost to seller. Efficient quantity Value to buyers is less than cost to seller.

72 Deadweight loss: is the total surplus lost due to monopoly pricing Because a monopoly sets its price above marginal cost, it places a wedge between the consumer s willingness to pay and the producer s cost. This wedge causes the quantity sold to fall short of the social optimum.

73 Copyright 2004 South-Western Price Deadweight loss Marginal cost Monopoly price Marginal revenue Demand 0 Monopoly quantity Efficient quantity Quantity

74 The Inefficiency of Monopoly The monopolist produces less than the socially efficient quantity of output. Some consumers would buy the good in a competitive market but will not buy under monopolistic pricing

75 The deadweight loss caused by a monopoly is similar to the deadweight loss caused by a tax. The difference between the two cases is that the government gets the revenue from a tax, whereas a private firm gets the monopoly profit. The deadweight loss is however not a result of the monopoly profit monopoly profits are not a social problem

76 Government responds to the problem of monopoly in one of four ways. Making monopolized industries more competitive. Regulating the behavior of monopolies. Turning some private monopolies into public enterprises. Doing nothing at all.

77 Antitrust laws are a collection of statutes aimed at curbing monopoly power. Antitrust laws give government various ways to promote competition. They allow government to prevent mergers. They allow government to break up companies. They prevent companies from performing activities that make markets less competitive.

78 Prevent mergers: Microsoft and Intuit in Breaks up companies: Polish railways (PKP) were divided into a set of smaller companies (2001) AT&T telecommunications company was divided into 8 smaller companies (1984) Prevents companies from performing activities that make markets less competitive.

79 Government may regulate the prices that the monopoly charges. The allocation of resources will be efficient if price is set to equal marginal cost. When the company is a natural monopoly than it has a decreasing average cost then AC<MC The firm will exit the market (suffers losses)

80 Copyright 2004 South-Western Price Average total cost Regulated price Loss Average total cost Marginal cost Demand 0 Quantity

81 In practice, regulators will allow monopolists to keep some of the benefits from lower costs in the form of higher profit, a practice that requires some departure from marginal-cost pricing. Examples: Electricity prices Gas prices

82 Rather than regulating a natural monopoly that is run by a private firm, the government can run the monopoly itself. Examples: Railway trucks Postal Services

83 Government can do nothing at all if the market failure is deemed small compared to the imperfections of public policies.

84 Lets consider the previous example with a company characterized by P D 100 2Q TC 10 40Q Q What is the efficient scale of production? What is the deadweight loss? Suppose, the company profits are transferred to consumers. Does it change the deadweight loss? 2

85 Examples and effects on the deadweight loss.

86 Price discrimination is the business practice of selling the same good at different prices to different customers, even though the costs for producing for the two customers are the same.

87 Suppose, we run a Publishing company that has a monopoly for selling a novel No printing costs Fixed cost to the author: $2 million for exclusive rights to publish Demand Price Sale Income Profits 30$ $ Decision: set the price $30

88 Deadweight loss: potential readers do not buy the book Suppose, the two types of customers lives in two countries: Europa (willing to pay $30) US (wiling to pay $5) When it charges two different prices, the company can have $ profit Country Price Sale Income EU 30$ US 5$

89 Price discrimination is not possible when a good is sold in a competitive market since there are many firms all selling at the market price. In order to price discriminate, the firm must have some market power. Perfect Price Discrimination Perfect price discrimination refers to the situation when the monopolist knows exactly the willingness to pay of each customer and can charge each customer a different price.

90 The price discrimination is a rational behavior of a monopolist Increase the profits It requires separation of consumers according to their willingness to pay No arbitrage Price discrimination can rise the economic welfare (reduces the deadweight loss)

91 Copyright 2004 South-Western (a) Monopolist with Single Price Price Monopoly price Profit Consumer surplus Deadweight loss Marginal cost Marginal revenue Demand 0 Quantity sold Quantity

92 Copyright 2004 South-Western (b) Monopolist with Perfect Price Discrimination Price Profit Marginal cost Demand 0 Quantity sold Quantity

93 Examples of Price Discrimination Movie tickets Airline prices Discount coupons Quantity discounts

94 How prevalent are the problems of monopolies? Monopolies are common. Most firms have some control over their prices because of differentiated products. Firms with substantial monopoly power are rare. Few goods are truly unique.

95 A monopoly is a firm that is the sole seller in its market. It faces a downward-sloping demand curve for its product. A monopoly s marginal revenue is always below the price of its good.

96 Like a competitive firm, a monopoly maximizes profit by producing the quantity at which marginal cost and marginal revenue are equal. Unlike a competitive firm, its price exceeds its marginal revenue, so its price exceeds marginal cost.

97 A monopolist s profit-maximizing level of output is below the level that maximizes the sum of consumer and producer surplus. A monopoly causes deadweight losses similar to the deadweight losses caused by taxes.

98 Policymakers can respond to the inefficiencies of monopoly behavior with antitrust laws, regulation of prices, or by turning the monopoly into a government-run enterprise. If the market failure is deemed small, policymakers may decide to do nothing at all.

99 Monopolists can raise their profits by charging different prices to different buyers based on their willingness to pay. Price discrimination can raise economic welfare and lessen deadweight losses.

Monopoly WHY MONOPOLIES ARISE

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

Chapter 15: Monopoly WHY MONOPOLIES ARISE HOW MONOPOLIES MAKE PRODUCTION AND PRICING DECISIONS

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Learning Objectives. Chapter 6. Market Structures. Market Structures (cont.) The Two Extremes: Perfect Competition and Pure Monopoly

The Two Extremes: Perfect Competition and Pure Monopoly") Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

CONSUMER SURPLUS. Consumers, Producers and the Efficiency of Markets

In this chapter, look for the answers these questions: What is consumer? How is it related the demand curve? What is producer? How is it related the supply curve? Do markets produce a desirable allocation

In this chapter, look for the answers these questions: What is consumer? How is it related the demand curve? What is producer? How is it related the supply curve? Do markets produce a desirable allocation

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 14 - Monopoly Fall 2010 Herriges (ISU) Ch. 14 Monopoly Fall 2010 1 / 35 Outline 1 Monopolies What Monopolies Do 2 Profit Maximization for the Monopolist 3

Econ 101: Principles of Microeconomics Chapter 14 - Monopoly Fall 2010 Herriges (ISU) Ch. 14 Monopoly Fall 2010 1 / 35 Outline 1 Monopolies What Monopolies Do 2 Profit Maximization for the Monopolist 3

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition

, 2 nd Edition") CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

Common in European countries government runs telephone, water, electric companies.

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) A major characteristic of monopoly is A) a single seller of a product. B) multiple sellers of a product. C) two sellers of a product. D) a few sellers

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) A major characteristic of monopoly is A) a single seller of a product. B) multiple sellers of a product. C) two sellers of a product. D) a few sellers

Pricing and Output Decisions: i Perfect. Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Thus MR(Q) = P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).

= P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).") A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

Chapter 7: Market Structures Section 1

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

Monopolistic Competition

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

1. Supply and demand are the most important concepts in economics.

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

At the end of Chapter 18, you should be able to answer the following:

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Econ 202 Exam 3 Practice Problems

Econ 202 Exam 3 Practice Problems Principles of Microeconomics Dr. Phillip Miller Multiple Choice Identify the choice that best completes the statement or answers the question. Chapter 13 Production and

Econ 202 Exam 3 Practice Problems Principles of Microeconomics Dr. Phillip Miller Multiple Choice Identify the choice that best completes the statement or answers the question. Chapter 13 Production and

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

N. Gregory Mankiw Principles of Economics. Chapter 15. MONOPOLY

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition.

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

c. Given your answer in part (b), what do you anticipate will happen in this market in the long-run?

, what do you anticipate will happen in this market in the long-run?") Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Monopoly. Monopoly Defined

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

The Efficiency of Markets. What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society?

The Efficiency of Markets What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society? We need to look at the benefits to consumers and producers.

The Efficiency of Markets What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society? We need to look at the benefits to consumers and producers.

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.)

") CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

Monopolistic Competition

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

Final Exam 15 December 2006

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Imperfect Competition. Oligopoly. Types of Imperfectly Competitive Markets. Imperfect Competition. Markets With Only a Few Sellers

Imperfect Competition Oligopoly Chapter 16 Imperfect competition refers to those market structures that fall between perfect competition and pure monopoly. Copyright 2001 by Harcourt, Inc. All rights reserved.

Imperfect Competition Oligopoly Chapter 16 Imperfect competition refers to those market structures that fall between perfect competition and pure monopoly. Copyright 2001 by Harcourt, Inc. All rights reserved.

ECON 600 Lecture 5: Market Structure - Monopoly. Monopoly: a firm that is the only seller of a good or service with no close substitutes.

I. The Definition of Monopoly ECON 600 Lecture 5: Market Structure - Monopoly Monopoly: a firm that is the only seller of a good or service with no close substitutes. This definition is abstract, just

I. The Definition of Monopoly ECON 600 Lecture 5: Market Structure - Monopoly Monopoly: a firm that is the only seller of a good or service with no close substitutes. This definition is abstract, just

Final Exam (Version 1) Answers

Answers") Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

MPP 801 Monopoly Kevin Wainwright Study Questions

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

chapter: Solution Solution Monopoly 1. Each of the following firms possesses market power. Explain its source.

S197-S28_Krugman2e_PS_Ch14.qxp 9/16/8 9:22 PM Page S-197 Monopoly chapter: 14 1. Each of the following firms possesses market power. Explain its source. a. Merck, the producer of the patented cholesterol-lowering

S197-S28_Krugman2e_PS_Ch14.qxp 9/16/8 9:22 PM Page S-197 Monopoly chapter: 14 1. Each of the following firms possesses market power. Explain its source. a. Merck, the producer of the patented cholesterol-lowering

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

Figure: Computing Monopoly Profit

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

SUPPLY AND DEMAND : HOW MARKETS WORK

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

Economics Chapter 7 Review

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

Econ 201 Final Exam. Douglas, Fall 2007 Version A Special Codes 00000. PLEDGE: I have neither given nor received unauthorized help on this exam.

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Chapter 7: Market Structure in Government and Nonprofit Industries. Soft Drinks. What is a Market? Do NFPs Compete? Some NFPs Compete Directly

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

Principle of Microeconomics Econ 202-506 chapter 13

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Monopoly Quantity & Price Elasticity Welfare. Monopoly Chapter 24

Monopol monopl.gif (GIF Image, 289x289 pixels) Chapter 24 http://i4.photobu Motivating Questions What price and quantit does a monopol choose? What are the welfare effects of monopol? What are the effects

Monopol monopl.gif (GIF Image, 289x289 pixels) Chapter 24 http://i4.photobu Motivating Questions What price and quantit does a monopol choose? What are the welfare effects of monopol? What are the effects

Profit Maximization. 2. product homogeneity

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

A Detailed Price Discrimination Example

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

MONOPOLIES HOW ARE MONOPOLIES ACHIEVED?

Monopoly 18 The public, policy-makers, and economists are concerned with the power that monopoly industries have. In this chapter I discuss how monopolies behave and the case against monopolies. The case

Monopoly 18 The public, policy-makers, and economists are concerned with the power that monopoly industries have. In this chapter I discuss how monopolies behave and the case against monopolies. The case

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits.

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Exam Prep Questions and Answers

Exam Prep Questions and Answers Instructions: You will have 75 minutes for the exam. Do not cheat. Raise your hand if you have a question, but continue to work on the exam while waiting for your question

Exam Prep Questions and Answers Instructions: You will have 75 minutes for the exam. Do not cheat. Raise your hand if you have a question, but continue to work on the exam while waiting for your question

Economics Chapter 7 Market Structures. Perfect competition is a in which a large number of all produce.

Economics Chapter 7 Market Structures Perfect competition is a in which a large number of all produce. There are Four Conditions for Perfect Competition: 1. 2. 3. 4. Barriers to Entry Factors that make

Economics Chapter 7 Market Structures Perfect competition is a in which a large number of all produce. There are Four Conditions for Perfect Competition: 1. 2. 3. 4. Barriers to Entry Factors that make

Econ 101, section 3, F06 Schroeter Exam #4, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #4, Red Choose the single best answer for each question. 1. Profit is defined as a. net revenue minus depreciation. *. total revenue minus total cost. c. average

Econ 101, section 3, F06 Schroeter Exam #4, Red Choose the single best answer for each question. 1. Profit is defined as a. net revenue minus depreciation. *. total revenue minus total cost. c. average

D) Marginal revenue is the rate at which total revenue changes with respect to changes in output.

Marginal revenue is the rate at which total revenue changes with respect to changes in output.") Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

BEE2017 Intermediate Microeconomics 2

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

BEE2017 Intermediate Microeconomics 2 Dieter Balkenborg Sotiris Karkalakos Yiannis Vailakis Organisation Lectures Mon 14:00-15:00, STC/C Wed 12:00-13:00, STC/D Tutorials Mon 15:00-16:00, STC/106 (will

Figure 1, A Monopolistically Competitive Firm

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

Examples on Monopoly and Third Degree Price Discrimination

1 Examples on Monopoly and Third Degree Price Discrimination This hand out contains two different parts. In the first, there are examples concerning the profit maximizing strategy for a firm with market

1 Examples on Monopoly and Third Degree Price Discrimination This hand out contains two different parts. In the first, there are examples concerning the profit maximizing strategy for a firm with market

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

Economics 100 Exam 2

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Rutgers University Economics 102: Introductory Microeconomics Professor Altshuler Fall 2003

Rutgers University Economics 102: Introductory Microeconomics Professor Altshuler Fall 2003 Answers to Problem Set 11 Chapter 16 2. a. If there were many suppliers of diamonds, price would equal marginal

Rutgers University Economics 102: Introductory Microeconomics Professor Altshuler Fall 2003 Answers to Problem Set 11 Chapter 16 2. a. If there were many suppliers of diamonds, price would equal marginal

How To Understand The Market Structure Of A Monopoly

Monopoly 1 1. Types of market structure 2. The diamond market 3. Monopoly pricing 4. Why do monopolies exist? 5. The social cost of monopoly power 6. Government regulation 2 Announcements We are going

Monopoly 1 1. Types of market structure 2. The diamond market 3. Monopoly pricing 4. Why do monopolies exist? 5. The social cost of monopoly power 6. Government regulation 2 Announcements We are going

1 of 14 11/5/2013 4:33 PM

1 of 14 11/5/2013 4:33 PM Market power is A characteristic of all market structures. The ability to alter the market price of a product. Most common for competitive firms. Enjoyed by all firms at high

1 of 14 11/5/2013 4:33 PM Market power is A characteristic of all market structures. The ability to alter the market price of a product. Most common for competitive firms. Enjoyed by all firms at high

chapter >> Consumer and Producer Surplus Section 3: Consumer Surplus, Producer Surplus, and the Gains from Trade

chapter 6 >> Consumer and Producer Surplus Section 3: Consumer Surplus, Producer Surplus, and the Gains from Trade One of the nine core principles of economics we introduced in Chapter 1 is that markets

chapter 6 >> Consumer and Producer Surplus Section 3: Consumer Surplus, Producer Surplus, and the Gains from Trade One of the nine core principles of economics we introduced in Chapter 1 is that markets

CHAPTER 9: PURE COMPETITION

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs:

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Maximising Consumer Surplus and Producer Surplus: How do airlines and mobile companies do it?

Maximising onsumer Surplus and Producer Surplus: How do airlines and mobile companies do it? This is a topic that has many powerful applications in understanding economic policy applications: (a) the impact

Maximising onsumer Surplus and Producer Surplus: How do airlines and mobile companies do it? This is a topic that has many powerful applications in understanding economic policy applications: (a) the impact

Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry s output.

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

UNIVERSITY OF CALICUT MICRO ECONOMICS - II

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

N. Gregory Mankiw Principles of Economics. Chapter 14. FIRMS IN COMPETITIVE MARKETS

N. Gregory Mankiw Principles of Economics Chapter 14. FIRMS IN COMPETITIVE MARKETS Solutions to Problems and Applications 1. A competitive market is one in which: (1) there are many buyers and many sellers

N. Gregory Mankiw Principles of Economics Chapter 14. FIRMS IN COMPETITIVE MARKETS Solutions to Problems and Applications 1. A competitive market is one in which: (1) there are many buyers and many sellers

4. Market Structures. Learning Objectives 4-63. Market Structures

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

MODULE 62: MONOPOLY & PUBLIC POLICY

MODULE 62: MONOPOLY & PUBLIC POLICY Schmidty School of Economics 1 LEARNING TARGETS I CAN Ø Compare & Contrast the effect that perfect competition and monopoly has upon society's welfare. Ø Explain how

MODULE 62: MONOPOLY & PUBLIC POLICY Schmidty School of Economics 1 LEARNING TARGETS I CAN Ø Compare & Contrast the effect that perfect competition and monopoly has upon society's welfare. Ø Explain how

Oligopoly and Strategic Pricing

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

Market is a network of dealings between buyers and sellers.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly.

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

Managerial Economics

Managerial Economics Unit 3: Perfect Competition, Monopoly and Monopolistic Competition Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012 Winter-Ebmer, Managerial Economics: Unit 3 1

Managerial Economics Unit 3: Perfect Competition, Monopoly and Monopolistic Competition Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012 Winter-Ebmer, Managerial Economics: Unit 3 1

OLIGOPOLY. Nature of Oligopoly. What Causes Oligopoly?

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

Lecture 10 Monopoly Power and Pricing Strategies

Lecture 10 Monopoly Power and Pricing Strategies Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Origins of Monopoly 2 Monopolistic Behaviours 3 Limits of Monopoly Power 4 Price Discrimination

Lecture 10 Monopoly Power and Pricing Strategies Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Origins of Monopoly 2 Monopolistic Behaviours 3 Limits of Monopoly Power 4 Price Discrimination

Pure Competition urely competitive markets are used as the benchmark to evaluate market

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

Course: Economics I. Author: Ing. Martin Pop

Course: Economics I Author: Ing. Martin Pop Contents Introduction 1. Characteristics of imperfect competition. The main causes of imperfect competition 2. Equilibrium firms in imperfect competition 3.

Course: Economics I Author: Ing. Martin Pop Contents Introduction 1. Characteristics of imperfect competition. The main causes of imperfect competition 2. Equilibrium firms in imperfect competition 3.

Lab 12: Perfectly Competitive Market

Lab 12: Perfectly Competitive Market 1. Perfectly competitive market 1) three conditions that make a market perfectly competitive: a. many buyers and sellers, all of whom are small relative to market b.

Lab 12: Perfectly Competitive Market 1. Perfectly competitive market 1) three conditions that make a market perfectly competitive: a. many buyers and sellers, all of whom are small relative to market b.

Name Eco200: Practice Test 2 Covering Chapters 10 through 15

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

Variable Cost. Marginal Cost. Average Variable Cost 0 $50 $50 $0 -- -- -- -- 1 $150 A B C D E F 2 G H I $120 J K L 3 M N O P Q $120 R

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Employment and Pricing of Inputs

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

4 THE MARKET FORCES OF SUPPLY AND DEMAND

4 THE MARKET FORCES OF SUPPLY AND DEMAND IN THIS CHAPTER YOU WILL Learn what a competitive market is Examine what determines the demand for a good in a competitive market Chapter Overview Examine what

4 THE MARKET FORCES OF SUPPLY AND DEMAND IN THIS CHAPTER YOU WILL Learn what a competitive market is Examine what determines the demand for a good in a competitive market Chapter Overview Examine what

LABOR UNIONS. Appendix. Key Concepts

Appendix LABOR UNION Key Concepts Market Power in the Labor Market A labor union is an organized group of workers that aims to increase wages and influence other job conditions. Craft union a group of

Appendix LABOR UNION Key Concepts Market Power in the Labor Market A labor union is an organized group of workers that aims to increase wages and influence other job conditions. Craft union a group of

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Learning Objectives. After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to:

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive