ABA Staff Analysis: Interim Rule Amending Regulation Z (Summary Information Regarding Interest Rates and Payment Changes)

|

|

|

- Vernon Bryant

- 8 years ago

- Views:

Transcription

1 ABA Staff Analysis: Interim Rule Amending Regulation Z (Summary Information Regarding Interest Rates and Payment Changes) SUMMARY: The Board is publishing interim rule changes and soliciting comments for amendments to Regulation Z, which implements the Truth in Lending Act (TILA). The new interim rule implements Congressional directives contained in the Mortgage Disclosure Improvement Act of 2008 (MDIA), which amended TILA to add new timing requirements and consumer protections in home-secured transactions. 1 Under this interim rule, creditors that extend credit secured by real property or a dwelling must disclose summarized information about interest rates and payment changes. The interest rate and payment summary tables replace the payment schedule previously required as part of the TILA disclosure for mortgage transactions. The interim rule mandates that such summaries be presented in tabular format. The rule adds a statement informing consumers that they are not guaranteed to be able to refinance their loans in the future. EFFECTIVE DATES: This interim rule is effective [insert date that is 30 days after the date of publication in the Federal Register]. The Board clarifies that compliance with its requirements is optional until January 30, In order to comply with the time deadlines imposed by MDIA, the new rule requirements are mandatory for transactions for which an application for credit is received by the creditor on or after January 30, The Board is also soliciting comments n this interim rule, which must be received on or before [insert date that is 60 days after the date of publication in the Federal Register]. The Board states that it is issuing an interim rule, rather than a final rule, because it intends to conduct additional testing of this and other disclosure requirements, and may revise these interim provisions further in light of further testing results. SCOPE: The Board s interim rule applies to closed-end credit transactions secured by real property or a dwelling, and excludes loans secured interests in timeshare plans. The rule therefore requires interest rate and payment summary tables for all transactions secured by real property or a dwelling, including fixed-rate, fixed-payment mortgages. Reverse Mortgages: Under the interim rules, reverse mortgages are subject to Section (s) and (t), but they will be excluded from the definition of a negative amortization mortgage. Timeshares: Loans secured by interests in timeshare plans are not subject to new Section (s) and (t), but would be subject to Section (g) requiring an exact payment schedule to be disclosed in accordance with the provisions of that section. RULE CONTENT: For full understanding of the new disclosures mandated under the interim rule, readers must examine the model forms set forth by the Board under Appendix H to the regulations. These model forms are reproduced below, as an attachment to this summary. 1 The MDIA is contained in Sections 2501 through 2503 of the Housing and Economic Recovery Act of 2008, Pub.L , enacted on July 30, The Board implemented an initial these MDIA requirements in final rules published on May 19, 2009, and effective July 30, See 74 FR (May 19, 2009).

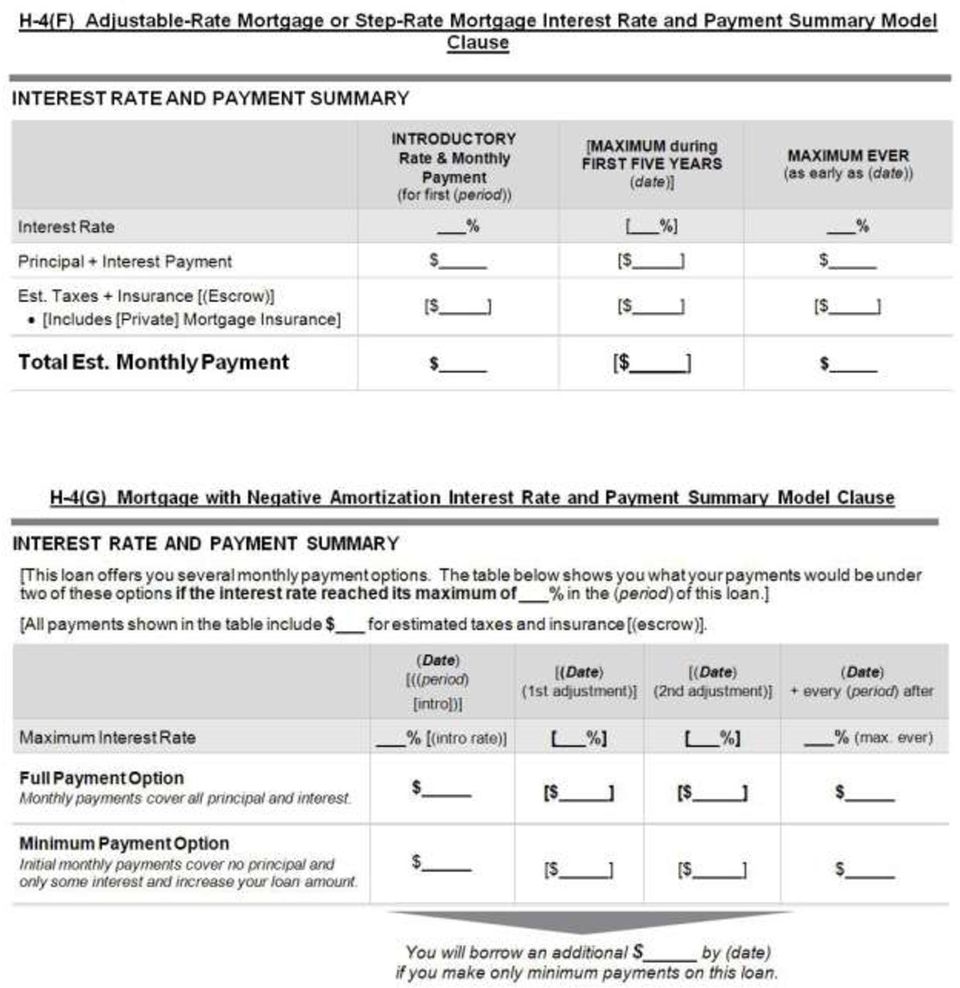

2 Interest Rate and Payment Summary: The Board is adopting a new Section (s) that will replace the current payment schedule disclosure for closed-end consumer credits (found in Section (g)) with a new interest rate and payment summary table for a transaction secured by real property or a dwelling. Section (g) will remain in place, but will apply only to loans that are not secured by real property or a dwelling; that section is therefore amended to exclude property or dwelling-secured transactions from its coverage. The Board crafted the interim rules in a manner that permits their application to all types of loan products. The precise detail and presentation of the disclosure will vary upon the specific characteristics of the particular loan product. Since the application of these new rules to actual products can vary according to the details of the individual products, the interim rule and accompanying commentaries provide various sets of examples to properly illustrate the correct application of the new provisions. The new Section (s) requires creditors to disclose the contract interest rate, regular periodic payment, and balloon payment if applicable. Creditors must provide the information about interest rates and payments in the form of a table, and creditors are not permitted to include other, unrelated information in the table. For all amortizing loans, creditors must separately itemize an estimate of the amount for taxes and insurance if the creditor will establish an escrow account. Under (s)(1), the table must be in a minimum 10-point font to ensure that it is clear and conspicuous. (TILA s current font and size requirements generally state that no minimum type size is mandated for the disclosures.) The regulatory elements applicable to the various combinations of interest rate products are as follow Amortizing Loans (18(s)(2)(i)) For a fixed-rate mortgage with no scheduled payment increases or balloon payments, the creditor discloses only one interest rate. Creditors must disclose the interest rate applicable at consummation. Fixed-rate loans with payment increases require the creditor to disclose the interest rate along with each payment increase, even if the interest rate does not change. o Section (s)(2)(i)(C) provides that, where payment increases will not coincide with an interest rate adjustment, the creditor must include a column that discloses the interest rate that would apply at the time the adjustment is scheduled to occur, and the date on which the increase would occur. For a fixed-rate mortgage, the creditor shows the same interest rate twice. For adjustable-rate or step-rate amortizing loans, the rule requires up to three interest rates and corresponding periodic payments, including the maximum possible interest rate and payment. Section 128(b)(2)(C) requires creditors to disclose examples of payment increases, including the maximum possible payment, for adjustable-rate mortgages and other mortgages where payments may vary. o o Section (s)(2)(i)(B)(1), requires disclosure of the interest rate at consummation and the period of time until the first adjustment, labeled as introductory rate and monthly payment. Section (s)(2)(i)(B)(2) requires disclosure of the maximum possible rate at any time during the first five years after consummation, even if that is not the first adjustment, and the earliest date that rate may apply.

3 o o Section (s)(2)(i)(B)(3) requires creditors to disclose the maximum interest rate that could apply at any time, and the earliest date on which that rate could apply, as required by TILA Section 128(b)(2)(C). Section (s)(2)(i)(C) provides that, where payment increases will not coincide with an interest rate adjustment, the creditor must include a column that discloses the interest rate that would apply at the time the adjustment is scheduled to occur, and the date on which the increase would occur. In such instances, creditors must include a column that discloses the interest rate that will apply at the time of the increase, the date the increase is scheduled to occur, and an appropriate description such as first increase or first adjustment, as appropriate. Negative Amortizing Loans (18(s)(2)(ii)) For negative amortization loans, for which any scheduled payment may cause the principal balance to increase, Section (s)(2)(ii) requires disclosure of the interest rate applicable at consummation. For ARM loans that do not provide any limitations on interest rate increases ( caps ), the creditor must disclose the rate applicable at consummation and assume that the interest rate reaches the maximum at the next adjustment. Section (s)(6) requires a statement of the amount of the increase in the loan s principal balance if the consumer makes only minimum payments and the earliest month and year in which the minimum payment will recast to a fully amortizing payment, assuming that the interest-rate reaches its maximum at the earliest possible time. o To further inform consumers, this section requires a statement directly above the summary table explaining that the loan offers payment options. The explanation preceding the table also must state the maximum possible interest rate and the smallest number of months or years in which the interest rate could reach its maximum. Introductory Rate Disclosure for Amortizing Adjustable-Rate Mortgages (18(s)(2)(iii)) In instances of adjustable-rate mortgages that have an introductory or teaser rate set below the sum of the index and margin used for later adjustments, Section (s)(2)(iii) requires o An explanation of the introductory rate below the table; o Disclosure of the introductory rate, how long it will last, and that the interest rate will increase at the first scheduled adjustment even if market rates do not increase; o The fully indexed rate that otherwise would apply at consummation. The Board clarifies that for early disclosures required to be delivered within three business days after receipt of an application (under (a)(1)), the fully-indexed rate disclosed under Section (s)(2)(iii)(C) may be based on the index in effect at the time the disclosure is provided. This is set forth in Comment 18(s)(2)(iii)(C)-1. Principal, Interest Payments, and Escrows (18(s)(3)(i)) Section (s)(3)(i) requires disclosure of the principal and interest payment that corresponds to each interest rate disclosed under Section (s)(2)(i). Under Section (s)(3)(i), if all regular periodic payments include principal and interest, each disclosed

(2)(i)(C) provides that, where payment increases will not coincide with an interest rate adjustment, the creditor must include a column that discloses the interest rate that would apply at the")

4 payment amount must be listed in a single row in the table with a description such as principal and interest. Section (s)(3)(i)(C) provides that, if an escrow account will be established, the creditor must disclose the estimated payment amount for taxes and insurance, including any mortgage insurance. The rules provide that the escrow amount must include mortgage insurance premiums even if they are not escrowed. o The Board has determined that escrow payments are an important piece of consumer information, and under these new rules, for purposes of transactions secured by real property or a dwelling, creditors may no longer opt to exclude escrow accounts as provided in existing Section (g). o The Board is further considering whether taxes and insurance estimates should be o included even when no escrow account is established. Comment 18(s)(3)(i)(C)-1 clarifies the types of taxes and insurance that are required to be included in the estimate. Include amounts for property taxes and mortgage-related insurance items required by the creditor, such as insurance against loss of or damage to property, or against liability arising out of the ownership or use of the property, or insurance protecting the creditor against the consumer's default or other credit loss. Exclude premiums for credit insurance, debt suspension and debt cancellation agreements. Note that payment amounts under (s)(3)(i) should reflect the consumer s mortgage insurance payments until the date on which the creditor must automatically terminate coverage under applicable law. Payment amounts under (s)(3)(i) should reflect the consumer s mortgage insurance payments. This amount is included whether or not the loan carries an escrow account. The mortgage insurance premiums must be calculated until the date on which the creditor must automatically terminate coverage under applicable law (even though the consumer may have a right to request that the insurance be cancelled earlier). Section (s)(3)(i)(D) requires disclosure of the total estimated monthly payment, which includes the sum of the principal and interest payments (required under Section (s)(3)(i)(A) or (B)), and the estimated taxes and insurance payments required to be disclosed (under Section (s)(3)(i)(C)). Payments for Negative Amortization Loans (18(s)(4)) For each interest rate disclosed under (s)(2)(ii) for a negative amortization loan, the creditor must disclose payments in two separate rows, as follows o First row shows the fully amortizing payment for each interest rate; o Second row shows the minimum required payment for each rate, until the recast point. At the recast point, the minimum payment row shows the fully amortizing payment. The interest rate and payment summary would display only two payment options, even if the terms of the legal obligation provide for others the option to make minimum payments that result in negative amortization, and the option to make fully amortizing payments.

5 Under Section (s)(4)(i)(C), creditor must provide a statement that the minimum payment will cover only some of the accrued interest and none of the principal and will cause the principal balance to increase. Section (s)(4)(ii) requires disclosure of the fully amortizing payment that will be required at recasts (when minimum payments no longer are permitted and fully amortizing payments are required). This payment amount must reflect the maximum possible interest rate that will be applicable at that time, based on the contract terms. Section (s)(4)(iii) requires disclosure of the fully amortizing payment, assuming that the consumer makes only fully amortizing payments beginning at consummation. The fully amortizing payment row must be completed for each interest rate required to be disclosed. Balloon Payments (18(s)(5)) In instances of balloon notes, Section (s)(5)(i) provides that the balloon payment must be disclosed in the last row of the table rather than in a column, unless it coincides with an interest rate adjustment or other payment increase such as the expiration of an interest-only option. If a balloon coincides with an interest rate adjustment or other payment increase, the balloon payment is disclosed in the table as that payment increase. Section (s)(5)(i) provides that a payment is a balloon payment if it is more than twice the amount of other payments. MDIA Refinancing Warning MDIA amended TILA to require creditors to disclose for variable rate transactions, in conspicuous type size and format, that there is no guarantee that the consumer will be able to refinance the transaction to lower the interest rate or monthly payments ( MDIA refinancing warning ) U.S.C. 1638(b)(2)(C)(ii). To implement this change, the Board is adding new provisions under Section (t). Section (t)(1) requires creditors to disclose a statement that there is no guarantee that the consumer will be able to refinance the loan to obtain a lower interest rate and payment. o The Board is expanding the scope of this requirement to include fixed-rate transactions secured by a dwelling, as well as transactions secured by real property without a dwelling. Section (t)(2) provides format requirements for the MDIA refinancing warning. The statement must be made in a form substantially similar to Model Clause H-4(K) in Appendix H.

(4)(ii) requires disclosure of the fully amortizing payment that will be required at recasts (when minimum payments no longer are permitted and fully amortizing payments are required).")

6 Model Forms and Clauses The interim rule sets forth model clauses to illustrate the new requirements under this regulation. Model Clause H-4(E) illustrates the interest rate and payment summary table required under Section (s) for a fixed-rate mortgage transaction. Model Clause H-4(F) illustrates the table for an adjustable-rate or a step-rate mortgage transaction. Model Clause H-4(G) illustrates the table for a mortgage transaction with negative amortization. Model Clause H-4(H) illustrates the table for a fixed-rate loan with interest-only terms. Model Clause H-4(I) illustrates the introductory rate disclosure required by Section (s)(2)(iii) if an adjustable-rate mortgage has an introductory rate. Model Clause H-4(J) illustrates the balloon payment disclosure required by Section (s)(5) for a mortgage with a balloon payment term. Model Clause H-4(K) illustrates the no-guarantee-to-refinance statement required by Section (t). The model forms and clauses are set forth below. * * * * *

illustrates the table for a fixed-rate loan with interest-only terms. Model Clause H-4(I) illustrates the introductory rate disclosure required by Section 226.")

7

8 H-4(I) Introductory Rate Model Clause Introductory Rate Notice You have a discounted introductory rate of % that ends after (period). In the (period in sequence), even if market rates do not change, this rate will increase to %. H-4(J) Balloon Payment Model Clause Final Balloon Payment due (date): $ H-4(K) No-Guarantee-to-Refinance Statement Model Clause There is no guarantee that you will be able to refinance to lower your rate and payments. * * * * *

Balloon Payment Model Clause Final Balloon Payment due (date): $ H-4(K) No-Guarantee-to-Refinance")

Comment Call (10-16)

") Comment Call (10-16) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Compliance & General Counsel Date: October 20, 2010 RE: Regulation Z Interim Final Rule and Request for Comment

Comment Call (10-16) To: From: All Affiliated Credit Union CEOs Veronica Madsen Director of Compliance & General Counsel Date: October 20, 2010 RE: Regulation Z Interim Final Rule and Request for Comment

Federal Reserve System

Friday, September 24, 2010 Part II Federal Reserve System 12 CFR Part 226 Regulation Z; Truth in Lending; Proposed Rules, Interim Rule, Final Rules VerDate Mar2010 16:23 Sep 23, 2010 Jkt 220001 PO

Friday, September 24, 2010 Part II Federal Reserve System 12 CFR Part 226 Regulation Z; Truth in Lending; Proposed Rules, Interim Rule, Final Rules VerDate Mar2010 16:23 Sep 23, 2010 Jkt 220001 PO

Regulatory Practice Letter

RPL Number 10-17 Financial Services Regulatory Practice Regulatory Practice Letter ADVISORY Amendments to Mortgage Loan Provisions under Regulation Z Executive Summary The Federal Reserve Board ( Fed )

RPL Number 10-17 Financial Services Regulatory Practice Regulatory Practice Letter ADVISORY Amendments to Mortgage Loan Provisions under Regulation Z Executive Summary The Federal Reserve Board ( Fed )

REGULATORY ALERT NATIONAL CREDIT UNION ADMINISTRATION 1775 DUKE STREET, ALEXANDRIA, VA 22314. DATE: January 2014 NO.: 14-RA-03

REGULATORY ALERT NATIONAL CREDIT UNION ADMINISTRATION 1775 DUKE STREET, ALEXANDRIA, VA 22314 DATE: January 2014 NO.: 14-RA-03 TO: SUBJECT: ENCL: ACTION: Federally Insured Credit Unions Mortgage Servicing

REGULATORY ALERT NATIONAL CREDIT UNION ADMINISTRATION 1775 DUKE STREET, ALEXANDRIA, VA 22314 DATE: January 2014 NO.: 14-RA-03 TO: SUBJECT: ENCL: ACTION: Federally Insured Credit Unions Mortgage Servicing

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS)

(CLOSED-END HOME MORTGAGE TRANSACTIONS)") QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

How To Determine The Maximum Loan Amount In The United States

6. In Supplement I to Part 1026 Official Interpretations: A. Under Section 1026.25 Record Retention: i. Under 25(a) General rule, paragraph 2 is revised. ii. 25(c) Records related to certain requirements

6. In Supplement I to Part 1026 Official Interpretations: A. Under Section 1026.25 Record Retention: i. Under 25(a) General rule, paragraph 2 is revised. ii. 25(c) Records related to certain requirements

TILA-RESPA INTEGRATED DISCLOSURE

TILA-RESPA INTEGRATED DISCLOSURE Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau Version log The Bureau updates this guide on a periodic basis to reflect finalized

TILA-RESPA INTEGRATED DISCLOSURE Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau Version log The Bureau updates this guide on a periodic basis to reflect finalized

2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules

and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules") JUNE 7, 2013 2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules SMALL ENTITY COMPLIANCE GUIDE 1 Please refer to our proposed

JUNE 7, 2013 2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules SMALL ENTITY COMPLIANCE GUIDE 1 Please refer to our proposed

The Federal Register published the proposed rule on August 23, 2012.

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CFPB Issues Much Anticipated Final Rules: Ability to Repay, Qualified Mortgages, Escrow Requirements and Homeownership Counseling The Consumer Financial Protection Bureau ( CFPB ) issued their much anticipated

CFPB Proposes New Mortgage Disclosure Rules

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act.

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

Early Summary of Ability to Repay and Qualified Mortgage Rules under Dodd-Frank Wall Street Reform and Consumer Protection Act January 11, 2013 OVERVIEW - On January 10, 2013, the Consumer Financial Protection

2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules

and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules") JANUARY 8, 2014 2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules SMALL ENTITY COMPLIANCE GUIDE 1 Version Log The Bureau updates

JANUARY 8, 2014 2013 Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Mortgage Servicing Final Rules SMALL ENTITY COMPLIANCE GUIDE 1 Version Log The Bureau updates

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate.

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

TILA-RESPA INTEGRATED DISCLOSURE

TILA-RESPA INTEGRATED DISCLOSURE Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau Version log The Bureau updates this guide on a periodic basis to reflect finalized

TILA-RESPA INTEGRATED DISCLOSURE Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau Version log The Bureau updates this guide on a periodic basis to reflect finalized

CUNA s HOEPA (Home Ownership and Equity Protection Act) CHART (revised 10/22/2013)

CHART (revised 10/22/2013)") What: CFPB s new HOEPA requirements, 12 CFR 1026 Subpart E. HOEPA was initially enacted in 1994 as an amendment to Truth in Lending to address abusive practices in refinancing and home equity mortgage

What: CFPB s new HOEPA requirements, 12 CFR 1026 Subpart E. HOEPA was initially enacted in 1994 as an amendment to Truth in Lending to address abusive practices in refinancing and home equity mortgage

TILA-RESPA. Guide to the Loan Estimate and Closing Disclosure forms. Consumer Financial Protection Bureau

TILA-RESPA Integrated Disclosure Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau What s inside 1. Introduction...6 1.1 What is the purpose of this guide?...

TILA-RESPA Integrated Disclosure Guide to the Loan Estimate and Closing Disclosure forms Consumer Financial Protection Bureau What s inside 1. Introduction...6 1.1 What is the purpose of this guide?...

Rules and Regulations

23289 Rules and Regulations Federal Register Vol. 74, No. 95 Tuesday, May 19, 2009 This section of the FEDERAL REGISTER contains regulatory documents having general applicability and legal effect, most

23289 Rules and Regulations Federal Register Vol. 74, No. 95 Tuesday, May 19, 2009 This section of the FEDERAL REGISTER contains regulatory documents having general applicability and legal effect, most

Regulatory Practice Letter February 2013 RPL 13-07

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

DISCLAIMER. Page - 1 - of 17

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

RESPA and TILA Mortgage Servicing Final Rules

This summary is provided by the Minnesota Credit Union Network for informational purposes only, and is intended to provide credit unions with the general regulatory requirements and effective dates for

This summary is provided by the Minnesota Credit Union Network for informational purposes only, and is intended to provide credit unions with the general regulatory requirements and effective dates for

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013 On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued a final rule that carries out changes

NEW CFPB RULES FOR HIGH COST MORTGAGES AND HOMEOWNERSHIP COUNSELING February 3, 2013 On January 10, 2013, the Consumer Financial Protection Bureau ( CFPB ) issued a final rule that carries out changes

Mon. ICBA Summary of the Military Lending Act Updated Regulation. August 2015. Month Year. Contact:

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

ICBA Summary of the Military Lending Act Updated Regulation August 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org www.icba.org ICBA Summary

2013 Home Ownership and Equity Protection Act (HOEPA) Rule

Rule") MAY 2, 2013 2013 Home Ownership and Equity Protection Act (HOEPA) Rule SMALL ENTITY COMPLIANCE GUIDE The Bureau recently finalized changes to this rule. The revisions amend the final rule issued January

MAY 2, 2013 2013 Home Ownership and Equity Protection Act (HOEPA) Rule SMALL ENTITY COMPLIANCE GUIDE The Bureau recently finalized changes to this rule. The revisions amend the final rule issued January

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43)

") The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

The CFPB s Ability-to-Repay Regulation Z Rules: (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this CompNOTES only covers

CCE Consumer Compliance Examination. Truth in Lending. Comptroller s Handbook. October 2008 CCE-TIL

CCE-TIL Comptroller of the Currency Administrator of National Banks Truth in Lending Comptroller s Handbook October 2008 CCE Consumer Compliance Examination Truth in Lending Table of Contents Introduction

CCE-TIL Comptroller of the Currency Administrator of National Banks Truth in Lending Comptroller s Handbook October 2008 CCE Consumer Compliance Examination Truth in Lending Table of Contents Introduction

CFPB Proposes Comprehensive Mortgage Servicing Regulations

August 2012 CFPB Proposes Comprehensive Mortgage Servicing Regulations On August 9, 2012, the Consumer Financial Protection Bureau (CFPB) issued two notices of proposed rulemaking (NPRs) 1 implementing

August 2012 CFPB Proposes Comprehensive Mortgage Servicing Regulations On August 9, 2012, the Consumer Financial Protection Bureau (CFPB) issued two notices of proposed rulemaking (NPRs) 1 implementing

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43)

") The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

The CFPB s Qualified Mortgage Requirements from the ATR/QM Final Rule (12 CFR 1026.43) This has been updated to include changes from the CFPB final rule issued on September 13, 2013. In addition, this

Interim Rule Under Regulation Z Implementing New Tabular Disclosure Requirements for Truth In Lending Consumer Disclosures (DocketNumber.

Weiner Brodsky Sidman Kider P C. November 23, 2010 Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th and Constitution Avenue, Northwest Washington, D C 2 0 5 5 1 Re: Interim

Weiner Brodsky Sidman Kider P C. November 23, 2010 Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th and Constitution Avenue, Northwest Washington, D C 2 0 5 5 1 Re: Interim

Advertising, Consumer protection, Mortgages, Reporting and recordkeeping

List of Subjects in 12 CFR Part 1026 Advertising, Consumer protection, Mortgages, Reporting and recordkeeping requirements, Truth in Lending. Authority and Issuance For the reasons set forth in the preamble,

List of Subjects in 12 CFR Part 1026 Advertising, Consumer protection, Mortgages, Reporting and recordkeeping requirements, Truth in Lending. Authority and Issuance For the reasons set forth in the preamble,

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK FIS REGULATORY ADVISORY SERVICES

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

Regulation Z. Background and Summary

Regulation Z Truth in Lending Introduction Background and Summary The Truth in Lending Act (TILA), 15 USC 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub.

Regulation Z Truth in Lending Introduction Background and Summary The Truth in Lending Act (TILA), 15 USC 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub.

CORRESPONDENT Compliance Manual. Instructions to Complete the TRID Loan Estimate

CORRESPONDENT Compliance Manual Instructions to Complete the TRID Loan Estimate Compliance Department 9/14/2015 2015 Impac Mortgage Corp. NMLS #128231. www.nmlsconsumeraccess.org. Rates, fees and programs

CORRESPONDENT Compliance Manual Instructions to Complete the TRID Loan Estimate Compliance Department 9/14/2015 2015 Impac Mortgage Corp. NMLS #128231. www.nmlsconsumeraccess.org. Rates, fees and programs

New Mortgage Rules Update

New Mortgage Rules Update 1 OBJECTIVES To provide information regarding the new mortgage rules, in particular: Ability-to-Repay/Qualified Mortgages; Mortgage Loan Origination Compensation; High-Cost Loans

New Mortgage Rules Update 1 OBJECTIVES To provide information regarding the new mortgage rules, in particular: Ability-to-Repay/Qualified Mortgages; Mortgage Loan Origination Compensation; High-Cost Loans

Financial Regulatory Reform: The New Rules on Loan Originator Compensation

Financial Regulatory Reform: The New Rules on Loan Originator Compensation 1 Introduction NOTICE: This information is not intended to be used as legal advice to any person or entity. The information contained

Financial Regulatory Reform: The New Rules on Loan Originator Compensation 1 Introduction NOTICE: This information is not intended to be used as legal advice to any person or entity. The information contained

CUNA s COMPLIANCE HIGHLIGHTS

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

Truth in Lending 1 Examination Objectives

Truth in Lending 1 Examination Objectives 1. To appraise the quality of the financial institution s compliance management system for the Truth in Lending Act and Regulation Z (12 CFR part 1026). 2. To

Truth in Lending 1 Examination Objectives 1. To appraise the quality of the financial institution s compliance management system for the Truth in Lending Act and Regulation Z (12 CFR part 1026). 2. To

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

AN ACT Codification District of Columbia Official Code 2001 Edition IN THE COUNCIL OF THE DISTRICT OF COLUMBIA 2008 Winter Supp. West Group Publisher To amend the Mortgage Lender and Broker Act of 1996

AN ACT Codification District of Columbia Official Code 2001 Edition IN THE COUNCIL OF THE DISTRICT OF COLUMBIA 2008 Winter Supp. West Group Publisher To amend the Mortgage Lender and Broker Act of 1996

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

Know The Rules Truth in Lending and Florida Compliance

Know The Rules Truth in Lending and Florida Compliance Continuing Education for Florida Mortgage Professionals www.bookmarkeducation.com Know The Rules Truth in Lending and Florida Compliance A considerable

Know The Rules Truth in Lending and Florida Compliance Continuing Education for Florida Mortgage Professionals www.bookmarkeducation.com Know The Rules Truth in Lending and Florida Compliance A considerable

Regulation Z. Background and Summary

Regulation Z Truth in Lending Introduction Background and Summary The Truth in Lending Act (TILA), 15 USC 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub.

Regulation Z Truth in Lending Introduction Background and Summary The Truth in Lending Act (TILA), 15 USC 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub.

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS AND MORTGAGE COMPANIES 4CCR 725-3

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS AND MORTGAGE COMPANIES 4CCR 725-3 8-1-1 MORTGAGE LOAN ORIGINATOR ADVERTISING Pursuant to and in compliance with Title

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS AND MORTGAGE COMPANIES 4CCR 725-3 8-1-1 MORTGAGE LOAN ORIGINATOR ADVERTISING Pursuant to and in compliance with Title

Know Before You Owe Mortgage Disclosure Rule Construction Lending

Know Before You Owe Mortgage Disclosure Rule Construction Lending Outlook Live Webinar March 1, 2016 Nick Hluchyj Senior Counsel Office of Regulations Kristin Switzer Regulatory Implementation Analyst

Know Before You Owe Mortgage Disclosure Rule Construction Lending Outlook Live Webinar March 1, 2016 Nick Hluchyj Senior Counsel Office of Regulations Kristin Switzer Regulatory Implementation Analyst

V 1.1. V. Lending TILA. Truth in Lending Act. Introduction

Truth in Lending Act Introduction The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented

Truth in Lending Act Introduction The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented

Regulation Z Checklist

Regulation Z Checklist Open-End Credit 1. Are the credit and charge card early disclosures provided on or with all applications for credit and charge cards? (12 CFR 226.5a(a)) 2. Do the early disclosures

Regulation Z Checklist Open-End Credit 1. Are the credit and charge card early disclosures provided on or with all applications for credit and charge cards? (12 CFR 226.5a(a)) 2. Do the early disclosures

Truth in Lending Act

Comptroller s Handbook CC-TILA Consumer Compliance (CC) Truth in Lending Act December 2014 Office of the Comptroller of the Currency Washington, DC 20219 Contents Introduction...1 Background and Summary...

Comptroller s Handbook CC-TILA Consumer Compliance (CC) Truth in Lending Act December 2014 Office of the Comptroller of the Currency Washington, DC 20219 Contents Introduction...1 Background and Summary...

Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay

June 2011 Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay BY KEVIN L. PETRASIC, HELEN Y. LEE & AMANDA M. JABOUR Comments

June 2011 Uncertainty Regarding Fed Proposal and CFPB Action on Minimum Underwriting Standards for Consideration of a Consumer s Ability to Repay BY KEVIN L. PETRASIC, HELEN Y. LEE & AMANDA M. JABOUR Comments

Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14

Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14") Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14 General Loan Type 1994 TILA amendments apply to homeowners that already owned their homes and

Comparison of Section 32(HOEPA) Regulation; Current Rules vs. January 10, 2014 CFPB Changes As of 10/16/14 General Loan Type 1994 TILA amendments apply to homeowners that already owned their homes and

Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014

& Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014") Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014 General Consumer Loan Type Not Applicable HPML (12 CFR 1026.35) A closed-end consumer

Comparison of Section 35(HPML) & Section 32(HOEPA) Regulations Including CFPB 2013 & 2014 Updates As of 01/07/2014 General Consumer Loan Type Not Applicable HPML (12 CFR 1026.35) A closed-end consumer

Implications of the Federal Right of Rescission for Lenders and Borrowers

Implications of the Federal Right of Rescission for Lenders and Borrowers An Interactive Day of Building an Effective Community Response to Foreclosures in Wisconsin December 12, 2007 Disclaimer The views

Implications of the Federal Right of Rescission for Lenders and Borrowers An Interactive Day of Building an Effective Community Response to Foreclosures in Wisconsin December 12, 2007 Disclaimer The views

CFPB issues ability-to-repay and qualified mortgage rules

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

1 FEBRUARY 4, 2013 CFPB issues ability-to-repay and qualified mortgage rules By Raymond J. Gustini, Lloyd H. Spencer, Tiana M. Butcher, Courtney L. Lindsay II, and Pierce Han No standard is perfect, but

House of Representatives

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

House of Representatives General Assembly File No. 44 February Session, 2002 Substitute House Bill No. 5073 House of Representatives, March 18, 2002 The Committee on Banks reported through REP. DOYLE of

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35)

") TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

The CFPB Finalizes New Mortgage Servicing Rules

A DV I S O RY April 2013 The CFPB Finalizes New Mortgage Servicing Rules On January 17, 2013, the Consumer Financial Protection Bureau (CFPB) finalized rules implementing the mortgage loan servicing requirements

A DV I S O RY April 2013 The CFPB Finalizes New Mortgage Servicing Rules On January 17, 2013, the Consumer Financial Protection Bureau (CFPB) finalized rules implementing the mortgage loan servicing requirements

Private Education Loans

Truth in Lending Act Rules for Private Education Loans Please note that the following material is presented only for educational purposes and constitutes only the opinions of the presenter. The material

Truth in Lending Act Rules for Private Education Loans Please note that the following material is presented only for educational purposes and constitutes only the opinions of the presenter. The material

MRS Title 9-A 8-103. Definitions and rules of construction

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

9-A 8-103. Definitions and rules of construction The text included in this publication was prepared by the Maine Bureau of Financial Institutions and is current through July 15, 2008. It is a version that

Truth in Lending. Regulation Z. Background. Organization of Regulation Z. Applicability

Regulation Z Truth in Lending Background Regulation Z (12 CFR 226) implements the Truth in Lending Act (TILA) (15 USC 1601 et seq.), which was enacted in 1968 as title I of the Consumer Credit Protection

Regulation Z Truth in Lending Background Regulation Z (12 CFR 226) implements the Truth in Lending Act (TILA) (15 USC 1601 et seq.), which was enacted in 1968 as title I of the Consumer Credit Protection

Bankruptcy - What is a CFPB Mortgage Servicer and How Does it Work?

Impact of the CFPB Mortgage Servicing Rules on Your Bankruptcy Practice Thomas E. Hoffman John Rao National Consumer Law Center 2013 CFPB Mortgage Servicing Rules Dodd-Frank Act of 2010 amended RESPA and

Impact of the CFPB Mortgage Servicing Rules on Your Bankruptcy Practice Thomas E. Hoffman John Rao National Consumer Law Center 2013 CFPB Mortgage Servicing Rules Dodd-Frank Act of 2010 amended RESPA and

209 CMR: DIVISION OF BANKS AND LOAN AGENCIES

209 CMR 32.00: TRUTH IN LENDING Section GENERAL 32.01: Purpose and Scope 32.02: Definitions and Rules of Construction 32.03: Exempt Transactions 32.04: Finance Charges OPEN END CREDIT 32.05: General Disclosure

209 CMR 32.00: TRUTH IN LENDING Section GENERAL 32.01: Purpose and Scope 32.02: Definitions and Rules of Construction 32.03: Exempt Transactions 32.04: Finance Charges OPEN END CREDIT 32.05: General Disclosure

by: Stephen King, JD, AMLP

Community Bank Audit Group Dodd-Frank Lending Issues June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf & Company, P.C. Today s Agenda

Community Bank Audit Group Dodd-Frank Lending Issues June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf & Company, P.C. Today s Agenda

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C.

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C. 20007 (202) 295-4500 (202) 337-5502 www.sftlaw.com A DETAILED SUMMARY OF THE CFPB S FINAL

CLIENT AND FRIENDS BANKING UPDATE SILVER, FREEDMAN & TAFF, L.L.P. 3299 K STREET, N.W., SUITE 100, WASHINGTON, D.C. 20007 (202) 295-4500 (202) 337-5502 www.sftlaw.com A DETAILED SUMMARY OF THE CFPB S FINAL

INFOBYTES SPECIAL ALERT: DETAILED ANALYSIS OF CFPB S FINAL ESCROW RULE

INFOBYTES SPECIAL ALERT: DETAILED ANALYSIS OF CFPB S FINAL ESCROW RULE FEBRUARY 15, 2013 On January 10, 2013, the Consumer Financial Protection Bureau (the Bureau ) issued its final rule (the Rule or Escrow

INFOBYTES SPECIAL ALERT: DETAILED ANALYSIS OF CFPB S FINAL ESCROW RULE FEBRUARY 15, 2013 On January 10, 2013, the Consumer Financial Protection Bureau (the Bureau ) issued its final rule (the Rule or Escrow

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Financial Services Update Special Alert

Financial Services Update Special Alert August 16, 2010 Federal Reserve Issues Final Rules Regarding Loan Originator Compensation Practices On August 16, 2010, the Federal Reserve announced final rules

Financial Services Update Special Alert August 16, 2010 Federal Reserve Issues Final Rules Regarding Loan Originator Compensation Practices On August 16, 2010, the Federal Reserve announced final rules

The Consumer Financial Protection Bureau (Bureau) is issuing a final rule to implement

is issuing a final rule to implement") SUMMARY OF THE ABILITY-TO-REPAY AND QUALIFIED MORTGAGE RULE AND THE CONCURRENT PROPOSAL The Consumer Financial Protection Bureau (Bureau) is issuing a final rule to implement laws requiring mortgage lenders

SUMMARY OF THE ABILITY-TO-REPAY AND QUALIFIED MORTGAGE RULE AND THE CONCURRENT PROPOSAL The Consumer Financial Protection Bureau (Bureau) is issuing a final rule to implement laws requiring mortgage lenders

ESCROW REQUIREMENTS UNDER TILA

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

Overview Escrow Requirements Reg. Z High Cost Mortgage and Counseling - Reg. Z & X Ability to Repay & Qualified Mortgages Reg. Z & X Mortgage Servicing Reg. Z & X Loan Originator Compensation Reg. Z Copies

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices FIS Regulatory Advisory Services www.fisregulatoryservices.com New Servicing i Rules under Regulation Z Periodic

New Servicing Rules under Regulation Z Periodic Statements & Adjustable Rate Mortgages Notices FIS Regulatory Advisory Services www.fisregulatoryservices.com New Servicing i Rules under Regulation Z Periodic

STATE OF RHODE ISLAND DEPARTMENT OF BUSINESS REGULATION DIVISION OF BANKING 233 RICHMOND STREET, SUITE 231 PROVIDENCE, RHODE ISLAND 02903

TABLE OF CONTENTS STATE OF RHODE ISLAND DEPARTMENT OF BUSINESS REGULATION DIVISION OF BANKING 233 RICHMOND STREET, SUITE 231 PROVIDENCE, RHODE ISLAND 02903 BANKING REGULATION 3 HOME LOAN PROTECTION ACT

TABLE OF CONTENTS STATE OF RHODE ISLAND DEPARTMENT OF BUSINESS REGULATION DIVISION OF BANKING 233 RICHMOND STREET, SUITE 231 PROVIDENCE, RHODE ISLAND 02903 BANKING REGULATION 3 HOME LOAN PROTECTION ACT

General. Definitions. Current examination

Questions and Answers Regarding Joint Interagency Statement of Policy for Administrative Enforcement of the Truth in Lending Act Reimbursement Issued by the FFIEC on July 11, 1980, and Revised July 1998

Questions and Answers Regarding Joint Interagency Statement of Policy for Administrative Enforcement of the Truth in Lending Act Reimbursement Issued by the FFIEC on July 11, 1980, and Revised July 1998

V 1.1. V. Lending TILA. Truth in Lending Act 1. Introduction

Truth in Lending Act 1 Introduction The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented

Truth in Lending Act 1 Introduction The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented

Understanding Regulation Z: A Concise Analysis of the Amendments. Alla A. Vaynrub, CFA Director

Understanding Regulation Z: A Concise Analysis of the Amendments Alla A. Vaynrub, CFA Director 1 888 250 4400 Executive Summary Regulation Z, implementing Truth in Lending Act (TILA), has long been considered

Understanding Regulation Z: A Concise Analysis of the Amendments Alla A. Vaynrub, CFA Director 1 888 250 4400 Executive Summary Regulation Z, implementing Truth in Lending Act (TILA), has long been considered

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-457 HOUSE BILL 1222 AN ACT TO UPDATE THE RATE SPREAD AND HIGH-COST HOME LOANS STATUTES, AND TO MAKE A CONFORMING CHANGE TO THE EMERGENCY

UNDERSTANDING THE LOAN ESTIMATE

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

Upon completion you will be able to:

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

.") Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

How To Serve A Mortgage In The United States

Break Out Session: Mortgage Loan Servicing and Administration 2 Agenda Mortgage Servicing Rules (Real Estate Settlement Procedures Act [RESPA] and Truth in Lending Act [TILA]) Effective Date: Applications

Break Out Session: Mortgage Loan Servicing and Administration 2 Agenda Mortgage Servicing Rules (Real Estate Settlement Procedures Act [RESPA] and Truth in Lending Act [TILA]) Effective Date: Applications

CFPB Laws and Regulations

Laws and Regulations Truth in Lending Act 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The, implemented

Laws and Regulations Truth in Lending Act 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The, implemented

CFPB Mortgage Amendments. Get Caught Up!

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

Regulation Z Truth in Lending Act 1

Regulation Z Truth in Lending Act 1 Background The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The

Regulation Z Truth in Lending Act 1 Background The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The

The federal government and all state governments have enacted

4 C h a p t e r 4 Federal Lending Legislation In This Chapter The federal government and all state governments have enacted numerous laws that affect various aspects of the real estate industry. As a mortgage

4 C h a p t e r 4 Federal Lending Legislation In This Chapter The federal government and all state governments have enacted numerous laws that affect various aspects of the real estate industry. As a mortgage

Break Out Session: Mortgage Loan Underwriting and Pricing

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Truth in Lending Act 1

Truth in Lending Act 1 The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented by

Truth in Lending Act 1 The Truth in Lending Act (TILA), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The TILA, implemented by

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions David A. Elliott Partner Richard C. Keller Partner OUTLINE Section 1032(f)

CFPB Loan Disclosure Rules: Know Before You Owe Mortgage Forms The New Requirements and Their Impact on Financial Institutions David A. Elliott Partner Richard C. Keller Partner OUTLINE Section 1032(f)

Federal Reserve Issues Proposed Ability-to-Repay Rule

April 28, 2011 Federal Reserve Issues Proposed Ability-to-Repay Rule By Joseph Gabai On April 19, 2011, the Federal Reserve Board ( Board ) issued a proposed rule to implement ability-to-repay requirements

April 28, 2011 Federal Reserve Issues Proposed Ability-to-Repay Rule By Joseph Gabai On April 19, 2011, the Federal Reserve Board ( Board ) issued a proposed rule to implement ability-to-repay requirements

TITLE X PRIVATE STUDENT LOAN IMPROVEMENT

122 STAT. 3478 PUBLIC LAW 110 315 AUG. 14, 2008 (E) MINORITY BUSINESS. The term minority business includes HUBZone small business concerns (as defined in section 3(p) of the Small Business Act (15 U.S.C.

122 STAT. 3478 PUBLIC LAW 110 315 AUG. 14, 2008 (E) MINORITY BUSINESS. The term minority business includes HUBZone small business concerns (as defined in section 3(p) of the Small Business Act (15 U.S.C.

brochure, you are entitled to a refund of any fee you may have already paid.

HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity Line of Credit Plan. You should read it carefully

HOME EQUITY EARLY DISCLOSURE IMPORTANT TERMS OF OUR HOME EQUITY LINE OF CREDIT PLAN This disclosure contains important information about our Home Equity Line of Credit Plan. You should read it carefully

TABLE OF CONTENTS. SCENARIO #1 FIXED PURCHASE. Page 2. Loan Estimate.. Page 3. Closing Disclosure. Page 12. SCENARIO #2 TOLERANCE CURE Page 22

TRID CASE BOOK TABLE OF CONTENTS SCENARIO #1 FIXED PURCHASE. Page 2 Loan Estimate.. Page 3 Closing Disclosure. Page 12 SCENARIO #2 TOLERANCE CURE Page 22 SCENARIO #3 FIXED REFINANCE Page 25 Loan Estimate...

TRID CASE BOOK TABLE OF CONTENTS SCENARIO #1 FIXED PURCHASE. Page 2 Loan Estimate.. Page 3 Closing Disclosure. Page 12 SCENARIO #2 TOLERANCE CURE Page 22 SCENARIO #3 FIXED REFINANCE Page 25 Loan Estimate...

Dodd Frank Mortgage Reform 2014

Dodd Frank Mortgage Reform 2014 Business Partner Deck v1 12.16.13 Overview RULE EFFECTIVE DATE Loan Originator Compensation - TILA Loans closed and paid on or after 1/01/14 Ability to Repay/Qualified Mortgages

Dodd Frank Mortgage Reform 2014 Business Partner Deck v1 12.16.13 Overview RULE EFFECTIVE DATE Loan Originator Compensation - TILA Loans closed and paid on or after 1/01/14 Ability to Repay/Qualified Mortgages

NORTH AMERICAN TITLE COMPANY Like Clockwork. www.nat.com/cfpb

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

The New Mortgage Servicing Rules. FMS East Coast Regional Conference September 17, 2013

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

CFPB Mortgage Servicing Standards

www.pwc.com/consumerfinance www.pwcregulatory.com CFPB Mortgage Servicing Standards An analysis of the Consumer Financial Protection Bureau s Real Estate Settlement Procedures Act (Regulation X) and Truth

www.pwc.com/consumerfinance www.pwcregulatory.com CFPB Mortgage Servicing Standards An analysis of the Consumer Financial Protection Bureau s Real Estate Settlement Procedures Act (Regulation X) and Truth

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Truth in Lending Act 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321).

Consumer Laws and Regulations Truth in Lending Act 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321).

4/20/2015. Dodd Frank Sections 1411 and 1412. Defines pretty specifically the terms and dimensions of each. On this one, you can't blame the CFPB

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

Federal Banking Law Reporter Regulations, Regulation, 12 CFR 1026.35, Requirements for higher-priced mortgage loans.

Federal Banking Law Reporter Regulations, Regulation, 12 CFR 1026.35, Requirements for higher-priced mortgage loans. Click to open document in a browser The following text of Section 1026.35 is effective

Federal Banking Law Reporter Regulations, Regulation, 12 CFR 1026.35, Requirements for higher-priced mortgage loans. Click to open document in a browser The following text of Section 1026.35 is effective

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Truth in Lending 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The,

Consumer Laws and Regulations Truth in Lending 1 The Truth in Lending Act (), 15 U.S.C. 1601 et seq., was enacted on May 29, 1968, as title I of the Consumer Credit Protection Act (Pub. L. 90-321). The,

How To Get A Home Equity Line Of Credit

WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before making a decision, however,

WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT If you are in the market for credit, a home equity plan is one of several options that might be right for you. Before making a decision, however,

HOME EQUITY LINES OF CREDIT

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

Chapter 2d Utah High Cost Home Loan Act

Chapter 2d Utah High Cost Home Loan Act 61-2d-101 Title. This chapter is known as the "Utah High Cost Home Loan Act." 61-2d-102 Definitions. As used in this part: (1) "Accelerate" means a demand for immediate

Chapter 2d Utah High Cost Home Loan Act 61-2d-101 Title. This chapter is known as the "Utah High Cost Home Loan Act." 61-2d-102 Definitions. As used in this part: (1) "Accelerate" means a demand for immediate