Boston Medical Center Policy and Procedure Manual

|

|

|

- Melvin Watts

- 8 years ago

- Views:

Transcription

Monitoring Policy and Procedure Purpose: To provide guidance to Research Administrators,")

1 Policy #: Issued: October 2001 Reviewed: Revised: March 2015 Section: 39 Research Subcontract (Subrecipient) Monitoring Policy and Procedure Purpose: To provide guidance to Research Administrators, Principal Investigators and Research Operations staff on conducting risk assessment and appropriate ongoing monitoring of federal subrecipients in order to comply with federal subrecipient monitoring requirements as it relates to Boston Medical Center s (BMC) subrecipients. To define risk assessment to ensure proper classification of subrecipients as either Higher or Lower risk, and to ensure appropriate selection and implementation of monitoring methods tailored to particular subawards. Policy Statement: It is the policy of BMC that all federally sponsored projects follow the federal OMB Uniform Guidance regarding the monitoring of subrecipients. BMC monitors the programmatic and administrative performance of its federal subrecipients based upon the pre-award assessment of risk and will take appropriate action in the event of subrecipient noncompliance. Application: This policy applies to all federal subrecipient relationships, including those relationships with for-profit and foreign entities, as well as all other entities qualifying as exempt from 2 CFR Part 200, subpart F, regardless of funding source. Exceptions: n-federal subrecipient relationships Procedure: I. Pre-Award Subrecipient Risk Assessment The BMC Grants and Contracts Office will perform an initial risk assessment for all new subrecipients receiving federal subawards, with subsequent annual risk assessments conducted in January of each year for all subrecipients who will continue to receive federal funding. 1

subrecipients.")

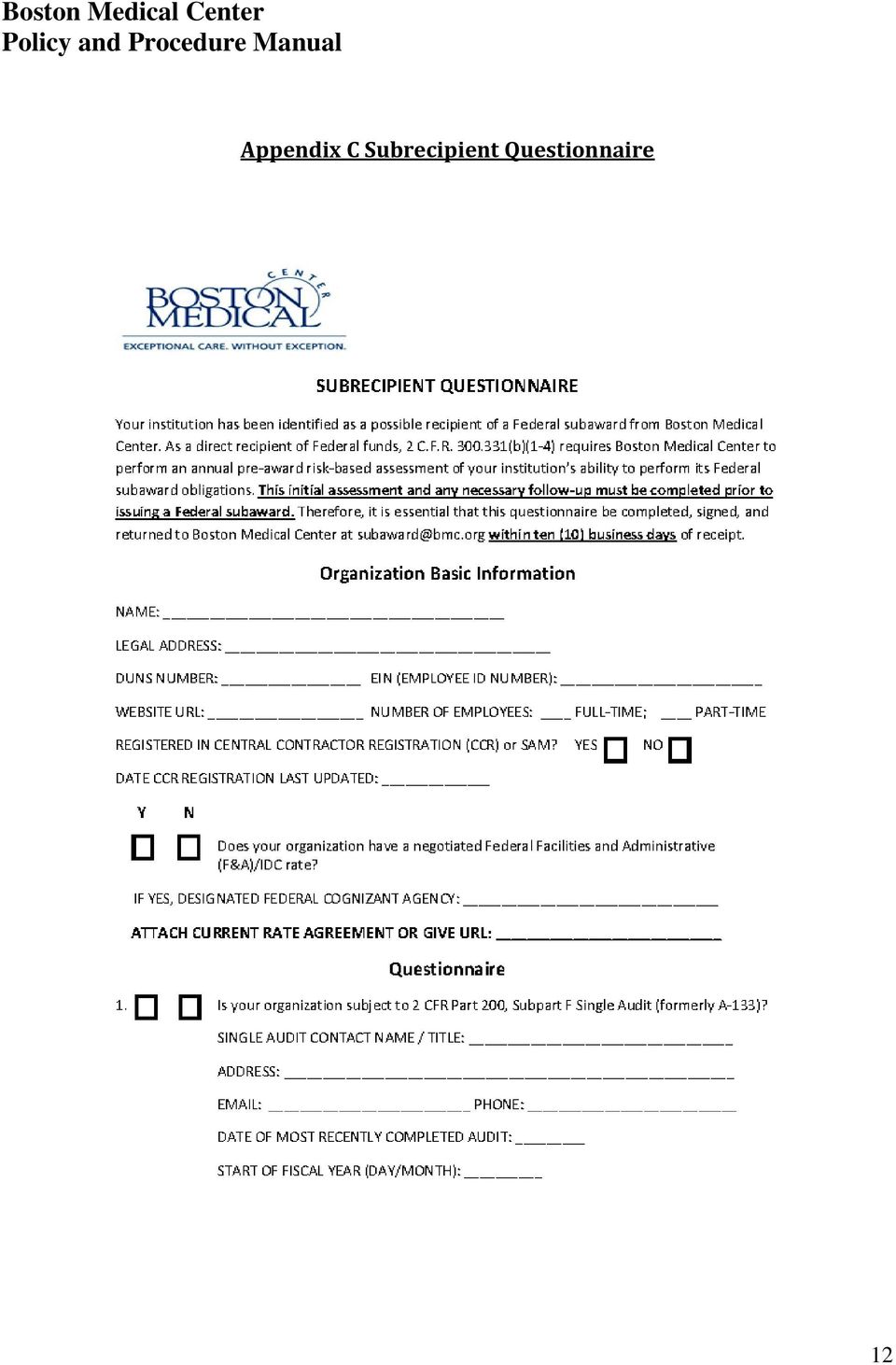

2 Upon receiving a Just-in-Time (JIT) notification from a federal awarding agency, the Pre-Award Grant Specialist (GS) will review the submitted grant proposal to determine whether it references the use of any subrecipients for the project. For proposals indicating subrecipients, the GS will communicate with the PI or Research Administrator (RA) to verify which subrecipient(s) the PI intends to use if awarded. The GS will then query the SAM subrecipient database to determine whether subrecipients verified by the PI have submitted a signed Subrecipient Questionnaire (Appendix C), a single audit report (2 CFR Part 200, Subpart F report) or audited financials, and a federal negotiated IDC rate agreement, in the previous twelve (12) months. The GS will coordinate with the PI or RA to ensure that a Questionnaire is ed to any subrecipients that have not submitted a Questionnaire or any of these documents in the last twelve (12) months. Once the Questionnaire is returned, the Contract Specialist (CS) enters the subrecipient information into the database, updating previously entered information as needed. The SAM database tracks subrecipient-monitoring data, including: Basic organizational data and contact information for each federal subrecipient; Data obtained from responses to Subrecipient Questionnaires; Data and comments from initial pre-award risk assessment and subsequent annual reviews of subrecipient single audits or other financial statements; The current classification of subrecipients as either Higher or Lower Risk; tations summarizing BMC management decisions based on risk assessment or based on reported audit deficiencies relating to BMC subawards. Initial Risk Assessment and Monitoring Decision The BMC Research Attorney will review the information obtained from the Subrecipient Questionnaire (Appendix C), any requested supplemental documentation, and publicly available debarment/ suspension/exclusion information. After review and assessment of the information, subrecipients will be assigned to one (1) of two (2) risk categories, Lower or Higher. The initial classification is made based on the matrix criteria below (Table 1). The presence of any Higher Risk characteristics will cause a subrecipient to be assigned to the Higher Risk category until the next annual risk review, or until the subrecipient submits adequate documentation of completed corrective action, as applicable. Table 1 First-Level Risk Assessment Decision Matrix Financial Review Lower Risk Characteristics Higher Risk Entities with Single Audit Low-risk auditee Unmodified auditor opinion Characteristics Modified auditor opinion 2

, a single audit report (2")

3 material weaknesses going-concern issue material noncompliance with laws Material weaknesses Going-concern issues Material noncompliance with laws Financial Statements Annual audited financials t annually audited Federal Award Experience? Financial Systems / Controls? Segregated financial duties? Provides backup for expenses? Foreign entity Single Audit or Annually Audited Financials Only unaudited financials or financials unavailable Compliance Review Lower Risk Characteristics Higher Risk Characteristics Debarment/Suspension OIG Exclusions Check Neither institution nor key personnel debarred or suspended Subrecipient institution not listed in OIG Exclusions database Adverse OIG actions, including exclusion, suspension Subrecipients assigned to the Lower Risk category in the initial risk assessment still remain subject to normal subrecipient monitoring, including: 1) a review of subrecipient invoices by PIs and departmental RAs to ensure that all expenses submitted are both allowable under the federal award and in line with the technical progress of the subaward (see Allowable Costs for Research, BMC Policy# ); 2) terms included in the Memorandum of Agreement and tice of Award (NOA) that communicate flow-down requirements and authorizations applicable to the subrecipient by federal laws and the provisions of the federal award; and 3) submission by the PI or PI delegate of a Subrecipient Performance Form (Appendix B) each year for each subcontract as part of the Pre-Award Office s federal non-competing renewal review. Subrecipients determined to be Higher Risk are evaluated again on a project-specific basis prior to the issuing of the subaward to determine the appropriate level of post-award monitoring and what special conditions, if any, should be added to the subcontract agreement beyond normal 3

4 subrecipient monitoring. The Grants and Contracts Office also performs annual single-audit collection and review for all subrecipients (both Higher and Lower) pursuant to 2 CFR Part 200, Subpart F. Whenever the Grants and Contracts Office receives a request to issue a subcontract from a federal activity during the course of the year, the Contract Specialist will check the subrecipient database to verify that a risk assessment has been performed. If no assessment information is in the database or no risk assessment has been performed in the previous twelve (12) months, the Contract Specialist will immediately send a Subrecipient Questionnaire (Appendix C) to the subrecipient and will notify the Research Attorney that a risk assessment is required. Project Specific Monitoring for Higher Risk Subrecipients For all subrecipients categorized as Higher Risk, BMC will require heightened subaward monitoring. To determine the level of monitoring, the Grants and Contracts office will review each Higher Risk subrecipient on a project- specific basis. Certain weaknesses in subrecipient systems, controls and policies may have no practical impact on a particular subaward (e.g., lack of research-equipment inventory policy, where a federal subaward involves no equipment purchases). A context-specific management decision regarding additional monitoring will consider factors including: Dollar amount of the subaward Complexity of subaward project, in view of technical and compliance requirements Whether subrecipient has successfully managed similar federally funded projects Whether subrecipient has successfully performed other federal subawards from BMC Relative strengths/weaknesses of subrecipient s existing financial systems, controls and policies in the context of performing the particular subaward PI s experience with, and assessment of, subrecipient s ability to perform the project Other considerations relevant to assessing the subrecipient s ability to perform Immediately after the determination is made that a subrecipient is Higher Risk, the Research Attorney will contact the PI and RA to discuss the risk assessment in light of project requirements. Based on communications with the PI and the other factors just noted above, prior to issuing a federal subcontract the Research Attorney will recommend a monitoring plan suggesting special conditions or additional post-award monitoring, if and as appropriate. Once the monitoring plan is approved by the Director, Grants and Contracts and/or the Associate Director/Research Finance, the Research Attorney will record and summarize the plan and factors considered in the SAM database, and communicate the plan back to the PI. The Contract Specialist will then add any necessary special-condition or post-award monitoring language to the MOA/MOAA template and communicate those special conditions or added monitoring requirements to the PI. The PI shall be responsible for ensuring that the subrecipient complies fully with all special conditions and additional monitoring requirements, if any. 4

months, the Contract Specialist will immediately send a Subrecipient Questionnaire")

5 For Higher Risk subrecipients, at a minimum, the PI will be required to certify to subrecipient satisfactory performance every six (6) months using the Subrecipient Performance Form. The PI is responsible for collecting and reviewing any interim technical reports, financial expenditure reports, or detailed invoice backup (e.g., receipts, time sheets) that may be required as part of a monitoring plan or special-conditions, if any. Copies of these documents must also be sent by the PI or their delegate to the appropriate Research Financial Analyst (RFA) for the project file. Other special contract conditions may include: Requiring payments as reimbursements rather than advance payments; Requiring itemized invoices; Withholding authority to proceed to the next phase until receipt of evidence of acceptable performance within a given period of performance; Requiring additional, more detailed financial reports at appropriate intervals; Requiring additional project monitoring as needed; and Requiring the subrecipient to obtain technical or management assistance. Other monitoring methods may include: Initiating performance reports when required; reviewing and monitoring subrecipient program budgets, and evaluating financial performance against technical performance; (terms and conditions written into subcontract to be monitored by PI) Evaluating corrective action plans for Subpart F audit deficiencies pertaining to BMC subawards (Research Attorney responsibility); Contacting the subrecipient regularly during the award period and addressing any inquiries concerning the federally funded program; (PI responsibility) Performing site visits to observe program operations and to review financial records (Research Operations responsibility); Offering technical assistance to subrecipients as needed to help ensure compliance as well as successful programmatic performance (Research Operations responsibility); and Other monitoring methods, as authorized and appropriate. BMC will consider appropriate sanctions against federal subrecipients it determines are noncompliant with federal statutes, regulations or the terms and conditions of a federal award. Such sanctions may include: Temporarily withholding cash payments pending correction of the deficiency by the nonfederal entity or more severe enforcement action by BMC; Denying both use of funds and any applicable matching credit for all or part of the cost of the activity or action not in compliance; Wholly or partly suspend or terminate the federal subaward; Withhold issuing additional subawards to the subrecipient; and Taking other remedies that may be legally available to BMC. 5

6 II: Single Audit (2 CFR 200 Subpart F) Annual Report Review BMC must verify that every subrecipient is audited as required by 2 CFR Part 200, Subpart F when it is expected that the subrecipient s federal awards expended during the respective fiscal year equaled or exceeded $750,000. In accordance with good business practices, BMC also requires a copy of annual audited financials or other annual financial statements or compilations from subrecipients who receive federal funding but are not covered by Subpart F, including forprofit or foreign subrecipients. Single Audit Review and Management Decision The Research Attorney reviews a subrecipient s single audit or other financial statements to determine whether it contains findings or raises risk concerns pertaining to the performance of a BMC subaward (e.g., a going-concern notation in an independent audit). Instances of noncompliance or material weaknesses documented in the audit are noted in the SAM database. The Research Attorney reports each instance of findings pertaining to BMC federal sub-awards to the Associate Director of Research Finance for a management decision as required by 2 CFR 200, Subpart F. The BMC PI is also notified of any findings pertaining to their federally funded program. The subrecipient s Corrective Action Plan is also reviewed by the Research Attorney and the Director, Grants and Contracts. To monitor the implementation of Corrective Action Plans, the Research Attorney may ask the subrecipient for progress updates, for additional documentation, or for permission to perform site visits. If no progress is apparent after a year, appropriate sanctions will be imposed against the noncompliant subrecipient as noted above, including but not limited to suspension of further funding until compliance is satisfactorily attained. Appropriate sanctions will be determined on a case-by-case basis in a management decision by BMC Research Operations after consulting with the BMC PI. The Research Attorney notes and summarizes any management decision and associated sanctions or follow-up in the tracking database. Federal research subrecipients are identified at Fiscal Year-end from information in Lawson and the SAM database. BMC Research Operations maintains a tracking system to note any audit deficiencies pertaining to BMC subawards and the CS or Researh Attorney obtains follow-up reports from the subrecipients as needed to verify that they have implemented timely and appropriate corrective action for such findings. Single Audit Collection Process To verify subrecipient compliance with Subpart F, and to obtain up-to-date Single Audits for annual subrecipient monitoring, the Contract Specialist will query the Federal Audit Clearinghouse ( FAC ) three times a year: in April, July and October and download audit reports. 6

7 Subrecipients whose Single Audits have not been uploaded into the FAC in accordance with their reported fiscal-year deadlines will be contacted by letter (Appendix A). BMC requires this documentation, regardless of Subpart F exemption status, to verify that exempt subrecipients prepare and, as appropriate, have annual financials audited independently. Subsequent requests are sent at 45-day intervals after the first request. The Contract Specialist assists the Research Attorney by following up via phone calls or s. Subrecipient tracking entries are reviewed and updated as necessary by the Research Attorney based on information collected in the Subpart F Review process to update the presence or absence of Higher Risk characteristics according to the initial risk assessment matrix above. Subrecipients may be assigned to the appropriate risk category at any time information is obtained warranting a reclassification. Responsibility: Principal Investigators Research Administrators Research Operations Staff Forms: a Subpart F Request Letter, Appendix A b Subrecipient Performance Form, Appendix B c Subrecipient Questionnaire, Appendix C Other Related Policies: Subcontracting (BMC as Prime) References: Title 2 CFR , , , 2 CFR Part 200 Subpart F Audit Requirements Section: 39 Research Policy.: Title: Subcontract (Subrecipient) Monitoring Policy and Procedure Initiated by: Grants and Contracts Contributing Departments: N/A 7

8 DATE Mr./Ms. Addressee Title Organization Address City, ST Zipcode Appendix A Single Audit Request Letter Re: Single Audit (2 CFR Part 200, Subpart F) Subrecipient Monitoring for FY 2014 As a federal pass-through entity, Boston Medical Center (BMC) must monitor your institution s compliance with 2 CFR Part 200, Subpart F (formerly OMB A-133). According to our records, your institution received a federal subaward(s) for our fiscal year ending in 2014 (10/1/2013 9/30/2014). Please have an authorized individual at your institution complete this form, attach appropriate documentation, and certify your institution s status by signing at the bottom. 1. We have not yet completed our Subpart F Single Audit for the fiscal year ending We expect our audit to be completed on / / (mm/dd/yyyy) and will: (a) Upload the full Single Audit Report to the Federal Audit Clearinghouse; or (b) Provide BMC a full copy within 30 days of completion, including a copy of our responses to audit findings and corrective action plan, if any. 2. We have completed our Subpart F audit for the fiscal year ending (a) Enclosed please find a copy of our Single Audit report, including a copy of our responses to audit findings and corrective action plan, if any. (b) Our Audit is available on the Internet at URL:. 3. We are not subject to Subpart F because (check one): a) we did not expend $750,000 or more in federal funds; b) we are a for-profit entity; or c) we are a non-u.s. entity. Enclosed is a copy of our most recent audited financial statement, end-of-year statement or compilation, documenting accounting compliance standards and controls. It is the policy of BMC to require all subrecipients of federal funds to submit copies of annual financial or accounting compliance documentation even without findings pertaining to BMC grants or when exempt from Subpart F. Please your documentation and this form to my attention at subaward@bmc.org or by regular mail to the address above. Please call xxxx with any questions concerning this request. Signature: Date: Name: Title: Phone: 8

for our fiscal year ending in 2014 (10/1/2013 9/30/2014).")

9 Sincerely, XXXXXXX Contract Specialist 9

10 Appendix B Subrecipient Performance Form Account number: Date: Project Title: BMC Principal Investigator: Program Administrator: Subrecipient (subcontractor): Performance Dates: from to Budget Dollars: $ 1. Does the Subrecipient (subcontractor/subawardee) invoice in a timely manner? 1a. List the backup documentation that was supplied by the subcontractor/subrecipient to substantiate the amount billed (e.g., time sheets, copies of invoices for lab supplies, etc.): 2. Are the amounts invoiced reasonable based on the technical progress of the project? 3. Is the Subrecipient satisfactorily performing the Scope of Work? 4. Are the reports/deliverables (if applicable) satisfactory? 5. [ Higher Risk federal subrecipients only]: Has the Subrecipient fully complied with all Special Conditions and/or additional monitoring requirements of the subaward agreement? 10

11 If you answered to any of these questions, please describe your plan of action to remedy the situation. I certify 1) that the information submitted above is accurate to the best of the my knowledge; 2) that any false, fictitious, or fraudulent statements or claims may subject me (the Principal Investigator) to criminal, civil, or administrative penalties; and 3) that I (the Principal Investigator) accept the responsibility for the scientific conduct of my project s subrecipients. PI Signature: 11

that I (the Principal Investigator) accept the responsibility for the scientific conduct of my project s")

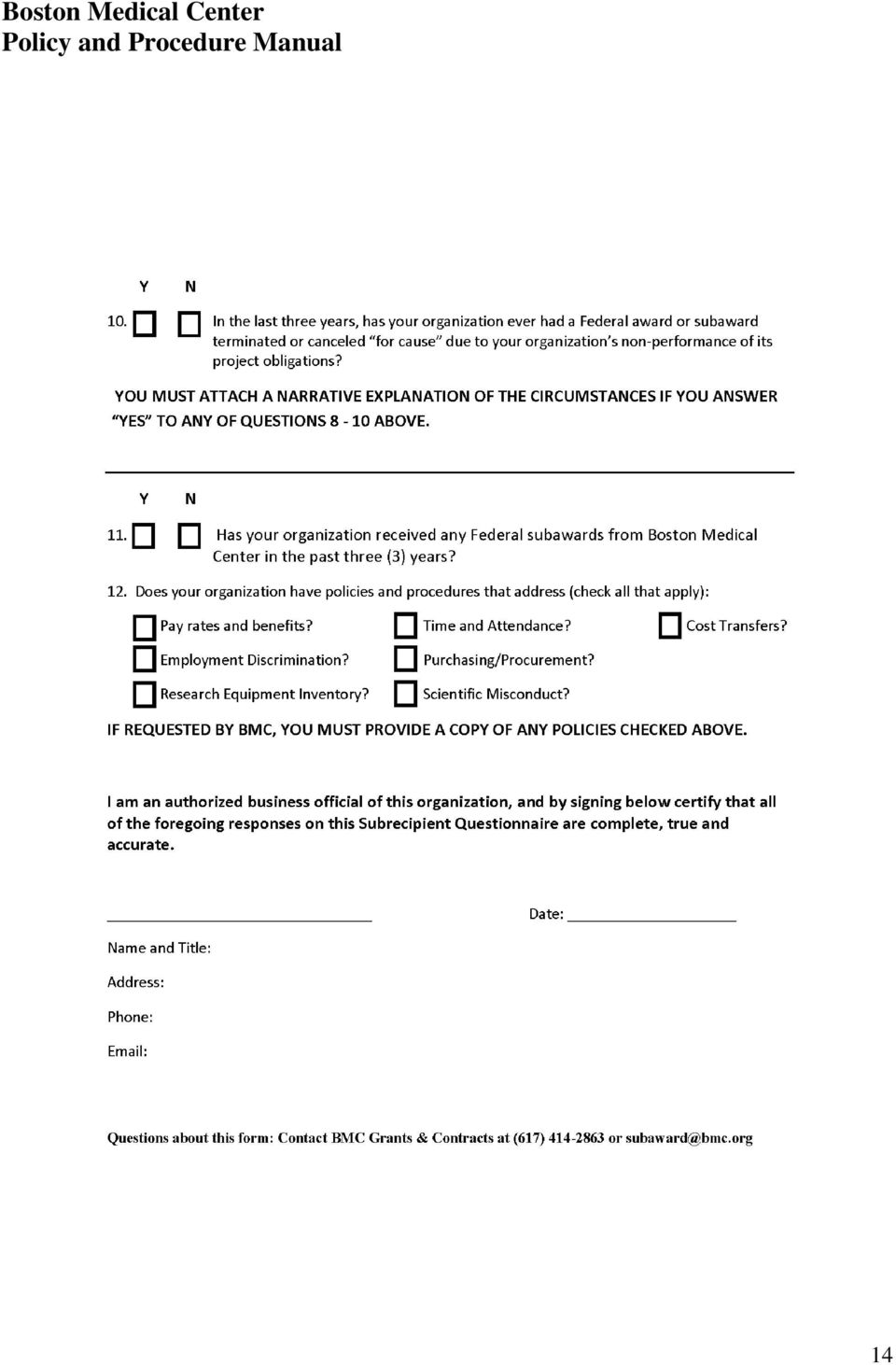

12 Appendix C Subrecipient Questionnaire 12

13 13

14 14

15 15

ADMINISTRATIVE PRACTICE LETTER

Page 1 of 9 Index Purpose of Guidelines Policy Who is Responsible Definitions and Terms Responsibilities and Procedures o Audit Requirements o For-profit Recipients and Audit Requirements o Roles and Responsibilities

Page 1 of 9 Index Purpose of Guidelines Policy Who is Responsible Definitions and Terms Responsibilities and Procedures o Audit Requirements o For-profit Recipients and Audit Requirements o Roles and Responsibilities

SUBRECIPIENT COMMITMENT FORM

Guidance on how to complete this form is found at: http://spo.berkeley.edu/forms/subaward/subrecipient_instructions.html. SECTION A: UC Berkeley Proposal Information Name of UC Berkeley PI: Prime Sponsor:

Guidance on how to complete this form is found at: http://spo.berkeley.edu/forms/subaward/subrecipient_instructions.html. SECTION A: UC Berkeley Proposal Information Name of UC Berkeley PI: Prime Sponsor:

EPA Policy on Assessing Capabilities of Non-Profit Applicants for Managing Assistance Awards

Classification No.: 5700.8 Approval Date: 02/23/2009 Review Date: 02/23/2012 1. PURPOSE. EPA Policy on Assessing Capabilities of Non-Profit Applicants for Managing Assistance Awards This Order establishes

Classification No.: 5700.8 Approval Date: 02/23/2009 Review Date: 02/23/2012 1. PURPOSE. EPA Policy on Assessing Capabilities of Non-Profit Applicants for Managing Assistance Awards This Order establishes

RULES OF THE AUDITOR GENERAL

RULES OF THE AUDITOR GENERAL CHAPTER 10.650 FLORIDA SINGLE AUDIT ACT AUDITS NONPROFIT AND FOR-PROFIT ORGANIZATIONS EFFECTIVE 9-30-15 RULES OF THE AUDITOR GENERAL CHAPTER 10.650 TABLE OF CONTENTS Rule Description

RULES OF THE AUDITOR GENERAL CHAPTER 10.650 FLORIDA SINGLE AUDIT ACT AUDITS NONPROFIT AND FOR-PROFIT ORGANIZATIONS EFFECTIVE 9-30-15 RULES OF THE AUDITOR GENERAL CHAPTER 10.650 TABLE OF CONTENTS Rule Description

SUBRECIPIENT CERTIFICATION FORM

Our records indicate that your organization is currently being considered for receipt of a subaward under sponsored project funds awarded to the University of Washington. Please check all applicable Certifications

Our records indicate that your organization is currently being considered for receipt of a subaward under sponsored project funds awarded to the University of Washington. Please check all applicable Certifications

Thompson Publishing Group, Inc. Audio Conference June 6, 2006 Troubleshooting Subrecipient Monitoring: Review of Pass-Through Entity Responsibilities

What is Monitoring? A definition from the Department of Health and Human Services Grants Policy Directive: Monitoring - A process whereby the programmatic and business management performance aspects of

What is Monitoring? A definition from the Department of Health and Human Services Grants Policy Directive: Monitoring - A process whereby the programmatic and business management performance aspects of

1/25/2016. Uniform Guidance Subpart D Administrative Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Guidance Subpart D Administrative Requirements 1 Why This Session Is Needed Changes impact grant operations and policies Changes to recipient and subrecipient responsibilities 2 Lesson Overview

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards AT 2 CFR 200 November 11, 2014 WHAT S CHANGING AND WHEN? Grants Reform Office of Management and Budget Circulars

How To Audit A Federal Program

Circular No. A-133 Revised to show changes published in the Federal Register June 27, 2003 and June 26, 2007 Audits of States, Local Governments, and Non-Profit Organizations Accompanying Federal Register

Circular No. A-133 Revised to show changes published in the Federal Register June 27, 2003 and June 26, 2007 Audits of States, Local Governments, and Non-Profit Organizations Accompanying Federal Register

Policy on Subcontracts

Policy on Subcontracts BACKGROUND A subcontract is a contract awarded to another institution by the primary recipient (prime) of a contract or grant. It is also known as a subaward, subagreement, or consortium

Policy on Subcontracts BACKGROUND A subcontract is a contract awarded to another institution by the primary recipient (prime) of a contract or grant. It is also known as a subaward, subagreement, or consortium

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

Audit Unit Policy 16 th Revision April 2006. Floyd Blodgett, Education Accounting and Auditing Analyst

Audit Unit Policy 16 th Revision April 2006 Floyd Blodgett, Education Accounting and Auditing Analyst This document describes the process by which the Vermont Department of Education (VTDOE) conducts its

Audit Unit Policy 16 th Revision April 2006 Floyd Blodgett, Education Accounting and Auditing Analyst This document describes the process by which the Vermont Department of Education (VTDOE) conducts its

Procedures and Guidelines for External Grants and Sponsored Programs

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

Definitions: Procedures and Guidelines for External Grants and Sponsored Programs 1. Grant and Contract Financial Administration Office (Grants Office): The office within the Accounting Operations Area

H:\Cost\OMB\OMB completed templates\subpart F-Audit Requirements\Subpart F Audit Req Word Docs\Uniform-Guidance-Section_200.

H:\Cost\OMB\OMB completed templates\subpart F-Audit Requirements\Subpart F Audit Req Word Docs\Uniform-Guidance-Section_200.512 - Fund Accounting.docx 200.512 Report submission. (a) General. (1) The audit

H:\Cost\OMB\OMB completed templates\subpart F-Audit Requirements\Subpart F Audit Req Word Docs\Uniform-Guidance-Section_200.512 - Fund Accounting.docx 200.512 Report submission. (a) General. (1) The audit

Audit Report. Division of Mental Health and Developmental Services Substance Abuse Prevention and Treatment Agency

LA12-15 STATE OF NEVADA Audit Report Division of Mental Health and Developmental Services Substance Abuse Prevention and Treatment Agency 2012 Legislative Auditor Carson City, Nevada Audit Highlights Highlights

LA12-15 STATE OF NEVADA Audit Report Division of Mental Health and Developmental Services Substance Abuse Prevention and Treatment Agency 2012 Legislative Auditor Carson City, Nevada Audit Highlights Highlights

How To Manage Money At The Purdue Plant

Account Management Guidelines for SPS Funds (4XXXXXXX) Summary In order to achieve maximum utilization of Purdue resources, the Account Management Guidelines are used as a working document to provide more

Account Management Guidelines for SPS Funds (4XXXXXXX) Summary In order to achieve maximum utilization of Purdue resources, the Account Management Guidelines are used as a working document to provide more

AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS Daniel R. Levinson Inspector General June 2006 OEI-07-04-00460

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS Daniel R. Levinson Inspector General June 2006 OEI-07-04-00460

A Guide to Sub-recipient Monitoring

A Guide to Sub-recipient Monitoring 1 SPONSORED PROJECTS OFFICE UNIVERSITY OF CALIFORNIA, BERKELEY PAM MILLER, DIRECTOR SPO WOULD BE HAPPY TO BRING THIS PRESENTATION TO INDIVIDUAL UNITS. CONTACT PAM MILLER

A Guide to Sub-recipient Monitoring 1 SPONSORED PROJECTS OFFICE UNIVERSITY OF CALIFORNIA, BERKELEY PAM MILLER, DIRECTOR SPO WOULD BE HAPPY TO BRING THIS PRESENTATION TO INDIVIDUAL UNITS. CONTACT PAM MILLER

Chapter VI Fiscal Procedures

Chapter VI Fiscal Procedures VI. Fiscal Procedures 6-2 A. In-house Grant Payment and Federal Reimbursement Voucher Process 6-2 i. Review Process 6-2 Table 11. TSO Sub-grantee and State Agency Claim Review

Chapter VI Fiscal Procedures VI. Fiscal Procedures 6-2 A. In-house Grant Payment and Federal Reimbursement Voucher Process 6-2 i. Review Process 6-2 Table 11. TSO Sub-grantee and State Agency Claim Review

How To Write A Prepaid Expense Policy For Maricopa County

Category: Issued: 09/2008 Initiated by: Department of Finance Approved by: Maricopa County Board of Supervisors & Special Districts Revised: A. Purpose The purpose of the Maricopa County Prepaid Expense

Category: Issued: 09/2008 Initiated by: Department of Finance Approved by: Maricopa County Board of Supervisors & Special Districts Revised: A. Purpose The purpose of the Maricopa County Prepaid Expense

APPLIED SCIENCE COOPERATIVE AGREEMENT STANDARD OPERATING PROCEDURES FOR PTRs, GRANTS & TECHNOLOGY TRANSFER STAFF

APPLIED SCIENCE COOPERATIVE AGREEMENT STANDARD OPERATING PROCEDURES FOR PTRs, GRANTS & TECHNOLOGY TRANSFER STAFF Purpose: This standard operating procedure assists the Applied Science personnel in performing

APPLIED SCIENCE COOPERATIVE AGREEMENT STANDARD OPERATING PROCEDURES FOR PTRs, GRANTS & TECHNOLOGY TRANSFER STAFF Purpose: This standard operating procedure assists the Applied Science personnel in performing

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds National Science Foundation Office of Inspector General March 31, 2006 OIG 06-1-008 XXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Howard University Needs To Improve Internal Controls Over Management of NSF Grant Funds National Science Foundation Office of Inspector General March 31, 2006 OIG 06-1-008 XXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ATTACHMENT B FEDERAL CERTIFICATIONS FOOD SERVICE MANAGEMENT COMPANIES AND PUBLIC SCHOOLS

The undersigned states that: ATTACHMENT B FEDERAL CERTIFICATIONS FOOD SERVICE MANAGEMENT COMPANIES AND PUBLIC SCHOOLS 1. He or she is the duly authorized representative of the Vendor named below; 2. He

The undersigned states that: ATTACHMENT B FEDERAL CERTIFICATIONS FOOD SERVICE MANAGEMENT COMPANIES AND PUBLIC SCHOOLS 1. He or she is the duly authorized representative of the Vendor named below; 2. He

EPA RESEARCH AND RELATED AGENCY SPECIFIC REQUIREMENTS (June 2009)

") EPA RESEARCH AND RELATED AGENCY SPECIFIC REQUIREMENTS (June 2009) Environmental Protection Agency Home Page http://www.epa.gov EPA Grants Information http://www.epa.gov/epahome/grants.htm National Center

EPA RESEARCH AND RELATED AGENCY SPECIFIC REQUIREMENTS (June 2009) Environmental Protection Agency Home Page http://www.epa.gov EPA Grants Information http://www.epa.gov/epahome/grants.htm National Center

Appendix 1 CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES. Criminal Justice Commission Contract Management Policies and Procedures

CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES SNYOPSIS: The CJC was created by a Palm Beach County ordinance in 1988. It has 21 public sector members representing local, state, and federal criminal justice

CJC CONTRACT MANAGEMENT POLICIES AND PROCEDURES SNYOPSIS: The CJC was created by a Palm Beach County ordinance in 1988. It has 21 public sector members representing local, state, and federal criminal justice

Audit of Grants Management at Dakota State University

Audit of Grants Management at Dakota State University National Science Foundation Office of the Inspector General February 28, 2005 OIG 05-6004 Memorandum Report Audit of Grants Management at Dakota State

Audit of Grants Management at Dakota State University National Science Foundation Office of the Inspector General February 28, 2005 OIG 05-6004 Memorandum Report Audit of Grants Management at Dakota State

Department of Financial Services Division of Accounting & Auditing

STATE OF FLORIDA CONTRACT AND GRANT USER GUIDE Department of Financial Services Division of Accounting & Auditing - 1 - TABLE OF CONTENTS PAGE INTRODUCTION.. 3 CHAPTER 1 PLANNING... 4 CHAPTER 2 PROCUREMENT...

STATE OF FLORIDA CONTRACT AND GRANT USER GUIDE Department of Financial Services Division of Accounting & Auditing - 1 - TABLE OF CONTENTS PAGE INTRODUCTION.. 3 CHAPTER 1 PLANNING... 4 CHAPTER 2 PROCUREMENT...

EPA General Terms and Conditions Effective December 26, 2014

EPA General Terms and Conditions Effective December 26, 2014 1. Introduction The recipient and any sub-recipient must comply with the applicable EPA general terms and conditions outlined below. These terms

EPA General Terms and Conditions Effective December 26, 2014 1. Introduction The recipient and any sub-recipient must comply with the applicable EPA general terms and conditions outlined below. These terms

GAO FEDERAL STUDENT LOAN PROGRAMS. Opportunities Exist to Improve Audit Requirements and Oversight Procedures. Report to Congressional Committees

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

RULES OF THE AUDITOR GENERAL

RULES OF THE AUDITOR GENERAL CHAPTER 10.550 LOCAL GOVERNMENTAL ENTITY AUDITS EFFECTIVE 9-30-15 RULES OF THE AUDITOR GENERAL CHAPTER 10.550 TABLE OF CONTENTS Rule Description Page Section No. PREFACE TO

RULES OF THE AUDITOR GENERAL CHAPTER 10.550 LOCAL GOVERNMENTAL ENTITY AUDITS EFFECTIVE 9-30-15 RULES OF THE AUDITOR GENERAL CHAPTER 10.550 TABLE OF CONTENTS Rule Description Page Section No. PREFACE TO

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

DHHS POLICIES AND PROCEDURES

DHHS POLICIES AND PROCEDURES Section IV: General Administration Revision History: Original Effective Date: 7/1/00 Purpose The purpose of this policy is to clarify the monitoring functions for the Department

DHHS POLICIES AND PROCEDURES Section IV: General Administration Revision History: Original Effective Date: 7/1/00 Purpose The purpose of this policy is to clarify the monitoring functions for the Department

2000.04 REV-2 CHG-17 1-1

CHAPTER 1. GENERAL AUDIT GUIDANCE 1-1. Purpose. This audit guide is to assist the independent auditor (auditor) in performing audits of profit-motivated entities that are subject to the U.S. Department

CHAPTER 1. GENERAL AUDIT GUIDANCE 1-1. Purpose. This audit guide is to assist the independent auditor (auditor) in performing audits of profit-motivated entities that are subject to the U.S. Department

GUIDANCE - Subrecipient and Vendor Determinations Federal Funds

Date of Issue: July 21, 2008 Office of Issuance: AWI FG 063 Reference: Final Subrecipient/Vendor Guidance GUIDANCE - Subrecipient and Vendor Determinations Federal Funds OF INTEREST TO: Workforce Florida

Date of Issue: July 21, 2008 Office of Issuance: AWI FG 063 Reference: Final Subrecipient/Vendor Guidance GUIDANCE - Subrecipient and Vendor Determinations Federal Funds OF INTEREST TO: Workforce Florida

ATSU Financial Management Plan for Administration of Grants and Contracts

ATSU Financial Management Plan for Administration of Grants and Contracts Overview ATSU is committed to maintaining a financial management system that provides accurate, current, and full disclosure of

ATSU Financial Management Plan for Administration of Grants and Contracts Overview ATSU is committed to maintaining a financial management system that provides accurate, current, and full disclosure of

10/30/2015. Procurement Under the New Requirements. Why This Session Is Needed. Lesson Overview & Module Objectives. Changes to conflict of interest

Requirements Procurement under the New Requirements 1 1 Why This Session Is Needed New provisions in Uniform Guidance Changes to conflict of interest requirements in Uniform Guidance Distinctions between

Requirements Procurement under the New Requirements 1 1 Why This Session Is Needed New provisions in Uniform Guidance Changes to conflict of interest requirements in Uniform Guidance Distinctions between

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT #

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT # This Cost Reimbursable Subaward Agreement is entered into in order to specify the terms and conditions under which Florida Atlantic University,

FLORIDA ATLANTIC UNIVERSITY COST-REIMBURSABLE SUBAWARD AGREEMENT # This Cost Reimbursable Subaward Agreement is entered into in order to specify the terms and conditions under which Florida Atlantic University,

Grants Management Training. Office of Federal Programs August 19, 2015

Training Office of Federal Programs August 19, 2015 MS State Board of Education s Vision and Mission Vision To create a world-class educational system that gives students the knowledge and skills to be

Training Office of Federal Programs August 19, 2015 MS State Board of Education s Vision and Mission Vision To create a world-class educational system that gives students the knowledge and skills to be

Budgets and Financial Monitoring Tools and Tips. January 21, 2014

Budgets and Financial Monitoring Tools and Tips January 21, 2014 Overview Setting the stage with regulatory framework Circulars and general ideas and principles behind them Changes to OMB with the recently

Budgets and Financial Monitoring Tools and Tips January 21, 2014 Overview Setting the stage with regulatory framework Circulars and general ideas and principles behind them Changes to OMB with the recently

Changes in Financial Management of Sponsored Projects: - Subawards and Contracts - Subaccounts - Closeouts

Changes in Financial Management of Sponsored Projects: - Subawards and Contracts - Subaccounts - Closeouts Impact of Uniform Guidance and New Subaccount Payment Procedures Presentation 1 8/28 & 9/3/2014

Changes in Financial Management of Sponsored Projects: - Subawards and Contracts - Subaccounts - Closeouts Impact of Uniform Guidance and New Subaccount Payment Procedures Presentation 1 8/28 & 9/3/2014

Research Master Trial Agreement

November 2010 FDP Institution/Organization ("Prime Recipient") (National Coordinating Center ( NCC ) Institution/Organization ("Subrecipient") (Regional Coordinating Center ( RCC ) Name: University of

November 2010 FDP Institution/Organization ("Prime Recipient") (National Coordinating Center ( NCC ) Institution/Organization ("Subrecipient") (Regional Coordinating Center ( RCC ) Name: University of

HACKENSACK UNIVERSITY MEDICAL CENTER Research Department Policies and Procedures Manual

Policy Name: Research Grant Submissions Process HACKENSACK UNIVERSITY MEDICAL CENTER Research Department Policies and Procedures Manual Policy #: SPO_003 Effective Date: 01/01/2009 Page 1 of 9 GENERAL

Policy Name: Research Grant Submissions Process HACKENSACK UNIVERSITY MEDICAL CENTER Research Department Policies and Procedures Manual Policy #: SPO_003 Effective Date: 01/01/2009 Page 1 of 9 GENERAL

http://agnis/sites/amsissuances/shared%20documents/201.1.htm

Page 1 of 11 Directive 201.1 11/4/91 ASSISTANCE DOCUMENTS AND MEMORANDUMS OF UNDERSTANDING TABLE OF CONTENTS Page I. PURPOSE... 2 II. REPLACEMENT HIGHLIGHTS... 2 III. POLICY... 2 IV. DEFINITIONS... 2 V.

Page 1 of 11 Directive 201.1 11/4/91 ASSISTANCE DOCUMENTS AND MEMORANDUMS OF UNDERSTANDING TABLE OF CONTENTS Page I. PURPOSE... 2 II. REPLACEMENT HIGHLIGHTS... 2 III. POLICY... 2 IV. DEFINITIONS... 2 V.

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL Date: January 31, 2012 To: Mary F. Santonastasso, Director Division of Institution and Award Support

NATIONAL SCIENCE FOUNDATION 4201 Wilson Boulevard ARLINGTON, VIRGINIA 22230 OFFICE OF INSPECTOR GENERAL Date: January 31, 2012 To: Mary F. Santonastasso, Director Division of Institution and Award Support

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY*

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY* The Department of Justice (DOJ) Office of the Inspector General (OIG) conducted

AUDIT OF THE MACOMB COUNTY SHERIFF S OFFICE EQUITABLE SHARING PROGRAM ACTIVITIES MOUNT CLEMENS, MICHIGAN EXECUTIVE SUMMARY* The Department of Justice (DOJ) Office of the Inspector General (OIG) conducted

Guide to Subrecipient/Subgrantee Payments vs. Vendor/Con tractor Payments General distinctions:

U.S. Office of Management and Budget (OMB) Circular A-133 requires grant-awarding entities to determine whether an arrangement resulting from a particular award that the awarding entity makes to another

U.S. Office of Management and Budget (OMB) Circular A-133 requires grant-awarding entities to determine whether an arrangement resulting from a particular award that the awarding entity makes to another

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL. January 25, 2016

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Sacramento Audit Region January 25, 2016 Dr. Mitchell D. Chester Commissioner Massachusetts Department of Elementary and

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Sacramento Audit Region January 25, 2016 Dr. Mitchell D. Chester Commissioner Massachusetts Department of Elementary and

A8.900 Extramurally Funded Research and Non-Research Grants and Contracts

Prepared by Contracts and Grants Management Office. This replaces Administrative Procedure No. A8.948, dated July 1988. A8.948 August 1993 A8.900 Extramurally Funded Research and Non-Research Grants and

Prepared by Contracts and Grants Management Office. This replaces Administrative Procedure No. A8.948, dated July 1988. A8.948 August 1993 A8.900 Extramurally Funded Research and Non-Research Grants and

200.110 Effective/applicability date

Administrative Changes Kris Rhodes, Director 200.110 Effective/applicability date Final rule issued 12/26/2013 Federal agencies submit drafts implementing regulations to OMB by June 2014 Uniform implementation

Administrative Changes Kris Rhodes, Director 200.110 Effective/applicability date Final rule issued 12/26/2013 Federal agencies submit drafts implementing regulations to OMB by June 2014 Uniform implementation

Frequently Asked Questions Updated: September 2015

Frequently Asked Questions Updated: September 2015 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Frequently Asked Questions Updated: September 2015 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

OMB. Uniform Guidance

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

AN INTRODUCTION TO FINANCIAL MANAGEMENT FOR GRANT RECIPIENTS National Historical Publications and Records Commission National Archives www.archives.gov/nhprc June 17, 2015 Table of Contents USE OF THE

Report of independent certified public accountants in accordance with Government Auditing Standards and Circular A-133 State of Hawaii, Department of

Report of independent certified public accountants in accordance with Government Auditing Standards and Circular A-133 State of Hawaii,, June 30, 2004 2 C O N T E N T S REPORT OF INDEPENDENT CERTIFIED

Report of independent certified public accountants in accordance with Government Auditing Standards and Circular A-133 State of Hawaii,, June 30, 2004 2 C O N T E N T S REPORT OF INDEPENDENT CERTIFIED

Procurement Standards 2 CFR 200.317-326

2 CFR 200 Uniform Guidance Procurement Standards Kris Rhodes, Director Sponsored Project Services 1 Procurement Standards 2 CFR 200.317-326 200.317 Procurement by states 200.318 General procurement standards

2 CFR 200 Uniform Guidance Procurement Standards Kris Rhodes, Director Sponsored Project Services 1 Procurement Standards 2 CFR 200.317-326 200.317 Procurement by states 200.318 General procurement standards

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit Audit Period: December 1, 2009 to February 12, 2010 Report number Issuance date: March 9, 2010 Contents

Environmental Protection Agency Clean Water and Drinking Water State Revolving Funds ARRA Program Audit Audit Period: December 1, 2009 to February 12, 2010 Report number Issuance date: March 9, 2010 Contents

Workers Compensation Commission

Audit Report Workers Compensation Commission March 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

Audit Report Workers Compensation Commission March 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

Proactive CPA and Consulting Firm

THE TOR PROJECT, INC. AND AFFILIATE CONSOLIDATED FINANCIAL STATEMENTS AND REPORTS REQUIRED FOR AUDITS IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS AND OMB CIRCULAR A-133 DECEMBER 31, 2013 AND 2012

THE TOR PROJECT, INC. AND AFFILIATE CONSOLIDATED FINANCIAL STATEMENTS AND REPORTS REQUIRED FOR AUDITS IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS AND OMB CIRCULAR A-133 DECEMBER 31, 2013 AND 2012

ENFORCEMENT INITIATIVES RELATING TO FEDERAL RESEARCH GRANTS

American Health Lawyers Association Legal Issues Affecting Academic Medical Centers and Other Teaching Institutions ENFORCEMENT INITIATIVES RELATING TO FEDERAL RESEARCH GRANTS Paul W. Shaw K&L Gates LLP

American Health Lawyers Association Legal Issues Affecting Academic Medical Centers and Other Teaching Institutions ENFORCEMENT INITIATIVES RELATING TO FEDERAL RESEARCH GRANTS Paul W. Shaw K&L Gates LLP

West Shore Community College. Year Ended June 30, 2013. Single Audit Act Compliance

West Shore Community College Year Ended June 30, 2013 Single Audit Act Compliance West Shore Community College Table of Contents Page Independent Auditors Report on the Schedule of Expenditures of Federal

West Shore Community College Year Ended June 30, 2013 Single Audit Act Compliance West Shore Community College Table of Contents Page Independent Auditors Report on the Schedule of Expenditures of Federal

Hazardary Subrecipient Costs For Yale University and Roger Williams Hospital

$ G *4f*rara DEPARTMENT OF'HEALTH & HUMAN SERVICES AUG 7 2006 Report Number: A-01-06-01 501 Mr. Stephan W. Lenhardt Vice President for Management and Fiscal Affairs and Treasurer University of Massachusetts'

$ G *4f*rara DEPARTMENT OF'HEALTH & HUMAN SERVICES AUG 7 2006 Report Number: A-01-06-01 501 Mr. Stephan W. Lenhardt Vice President for Management and Fiscal Affairs and Treasurer University of Massachusetts'

GRANTS MANAGEMENT. After completing the module, you will have a working knowledge of the:

MODULE 4 LEARNING OBJECTIVES: GRANTS MANAGEMENT After completing the module, you will have a working knowledge of the: Components of grants management Reporting requirements Financial regulations Administrative

MODULE 4 LEARNING OBJECTIVES: GRANTS MANAGEMENT After completing the module, you will have a working knowledge of the: Components of grants management Reporting requirements Financial regulations Administrative

PITTSBURG UNIFIED SCHOOL DISTRICT

PITTSBURG UNIFIED SCHOOL DISTRICT New Construction and Modernization Projects PRE-QUALIFICATION PROGRAM QUESTIONNAIRE FOR PROJECTS $20 MILLION AND OVER TABLE OF CONTENTS PAGE NO. GENERAL INFORMATION.......i

PITTSBURG UNIFIED SCHOOL DISTRICT New Construction and Modernization Projects PRE-QUALIFICATION PROGRAM QUESTIONNAIRE FOR PROJECTS $20 MILLION AND OVER TABLE OF CONTENTS PAGE NO. GENERAL INFORMATION.......i

UNIVERSITY OF NORTH FLORIDA Office for Research and Sponsored Programs (ORSP) COLLECTION PROCEDURES

COLLECTION PROCEDURES") UNIVERSITY OF NORTH FLORIDA Office for Research and Sponsored Programs (ORSP) COLLECTION PROCEDURES I. Overview II. Definitions III. Who is Affected by This Procedure IV. Procedures V. Appendix I. OVERVIEW

UNIVERSITY OF NORTH FLORIDA Office for Research and Sponsored Programs (ORSP) COLLECTION PROCEDURES I. Overview II. Definitions III. Who is Affected by This Procedure IV. Procedures V. Appendix I. OVERVIEW

AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

JULY 26, 2012 AUDIT REPORT OFFICE OF AUDITS AUDIT OF NASA GRANTS AWARDED TO THE PHILADELPHIA COLLEGE OPPORTUNITY RESOURCES FOR EDUCATION OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

offlceofinspectorgeneral OfficeofAudithvices DEPARTMENT OFHEALTE%HUMAN SERVICES REGION IV P. 0. BOX 2047 ATLAMA, GEORGIA 30301

Date: From: Subject: To: offlceofinspectorgeneral OfficeofAudithvices DEPARTMENT OFHEALTE%HUMAN SERVICES REGION IV P. 0. BOX 2047 ATLAMA, GEORGIA 30301 Regional Inspector General for Audit Services, Region

Date: From: Subject: To: offlceofinspectorgeneral OfficeofAudithvices DEPARTMENT OFHEALTE%HUMAN SERVICES REGION IV P. 0. BOX 2047 ATLAMA, GEORGIA 30301 Regional Inspector General for Audit Services, Region

This document has been archived. The Why and When list at the AAPD Archive identifies why the document has been archived and where current guidance

This document has been archived. The Why and When list at the AAPD Archive identifies why the document has been archived and where current guidance may be found. Internal users may also access the OAA

This document has been archived. The Why and When list at the AAPD Archive identifies why the document has been archived and where current guidance may be found. Internal users may also access the OAA

Public Act No. 15-162

Public Act No. 15-162 AN ACT CONCERNING A STUDENT LOAN BILL OF RIGHTS. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. (NEW) (Effective October 1, 2015)

Public Act No. 15-162 AN ACT CONCERNING A STUDENT LOAN BILL OF RIGHTS. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. (NEW) (Effective October 1, 2015)

AUDIT GUIDE FOR RECIPIENTS AND AUDITORS

AUDIT GUIDE FOR RECIPIENTS AND AUDITORS FOREWORD Under the Legal Services Corporation (LSC) Act, LSC provides financial support to organizations that furnish legal assistance to eligible clients. Section

AUDIT GUIDE FOR RECIPIENTS AND AUDITORS FOREWORD Under the Legal Services Corporation (LSC) Act, LSC provides financial support to organizations that furnish legal assistance to eligible clients. Section

Homeland Security National Training Program

Office of State and Local Government Coordination and Preparedness Office for Domestic Preparedness Homeland Security National Training Program Grant Application Guidance Kit I. Background The Office for

Office of State and Local Government Coordination and Preparedness Office for Domestic Preparedness Homeland Security National Training Program Grant Application Guidance Kit I. Background The Office for

GRANT AND CONTRACT ACCOUNTING GRANT REVIEW TOOLKIT POST AWARD PROCESS

The below information is a brief overview of the Post Award Process that Grant and Contract Accounting follows in its post award administration of awarded sponsored projects. Please note that this overview

The below information is a brief overview of the Post Award Process that Grant and Contract Accounting follows in its post award administration of awarded sponsored projects. Please note that this overview

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM 60.20 Policy Name: Closing Sponsored Awards General Policy and Procedure Overview: The University of Missouri receives

University of Missouri System Accounting Policies and Procedures Policy Number: APM 60.20 Policy Name: Closing Sponsored Awards General Policy and Procedure Overview: The University of Missouri receives

Master Document Audit Program. Version 4.7, dated November 2015 B-1 Planning Considerations

Activity Code 10110 Version 4.7, dated November 2015 B-1 Planning Considerations A-133 Audit Audit Specific Independence Determination Members of the audit team and internal specialists consulting on this

Activity Code 10110 Version 4.7, dated November 2015 B-1 Planning Considerations A-133 Audit Audit Specific Independence Determination Members of the audit team and internal specialists consulting on this

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations PART I. Article 1. Administrative Information and

Air Force Research Laboratory Grants Terms and Conditions September 2009 Awards to International Educational Institutions and Non-Profit Organizations PART I. Article 1. Administrative Information and

Document Management Policy and Procedure

Office of Research and Sponsored Programs Issued: January, 2008 PURPOSE This document outlines the policy and procedures governing the retention and destruction of records within the Office of Research

Office of Research and Sponsored Programs Issued: January, 2008 PURPOSE This document outlines the policy and procedures governing the retention and destruction of records within the Office of Research

SECTION 3 OVERVIEW FOR RECIPIENTS OF HUD HOUSING & COMMUNITY DEVELOPMENT FUNDING

SECTION 3 OVERVIEW FOR RECIPIENTS OF HUD HOUSING & COMMUNITY DEVELOPMENT FUNDING Why HUD Enforces Section 3? Each year the U.S. Department of Housing and Urban Development invests billions of federal dollars

SECTION 3 OVERVIEW FOR RECIPIENTS OF HUD HOUSING & COMMUNITY DEVELOPMENT FUNDING Why HUD Enforces Section 3? Each year the U.S. Department of Housing and Urban Development invests billions of federal dollars

Federal Single Audit Act Update

Federal Single Audit Act Update Presented By: James Halleran, CPA Partner June 16, 2015 What We Will Cover Background and Effective Dates Key Points of the Uniform Guidance for Federal Awards Key Points

Federal Single Audit Act Update Presented By: James Halleran, CPA Partner June 16, 2015 What We Will Cover Background and Effective Dates Key Points of the Uniform Guidance for Federal Awards Key Points

WAGNER-PEYSER ACT (W-PA) ANNUAL FUNDING AGREEMENT (Including Mod 0, initial Notice of Obligation) PY 2014/FY 2015

ANNUAL FUNDING AGREEMENT (Including Mod 0, initial Notice of Obligation) PY 2014/FY 2015") 28 Attachment J WAGNER-PEYSER ACT (W-PA) ANNUAL FUNDING AGREEMENT (Including Mod 0, initial Notice of Obligation) PY 2014/FY 2015 Grant Number: (To be completed by DOL) CFDA #17.207 Employment Service/Wagner-Peyser

28 Attachment J WAGNER-PEYSER ACT (W-PA) ANNUAL FUNDING AGREEMENT (Including Mod 0, initial Notice of Obligation) PY 2014/FY 2015 Grant Number: (To be completed by DOL) CFDA #17.207 Employment Service/Wagner-Peyser

WorkLink Workforce Investment Board (effective July 1, 2015 WorkLink Workforce Development Board)

") WorkLink Workforce Investment Board (effective July 1, 2015 WorkLink Workforce Development Board) Workforce Innovation & Opportunity Act Website Maintenance, Updates, & SEO Hosting Request for Quotes (RFQ)

WorkLink Workforce Investment Board (effective July 1, 2015 WorkLink Workforce Development Board) Workforce Innovation & Opportunity Act Website Maintenance, Updates, & SEO Hosting Request for Quotes (RFQ)

February 15, 2006. The Honorable Joshua B. Bolten Director Office of Management and Budget 725 17 th Street, NW Washington, DC 20503

February 15, 2006 The Honorable Joshua B. Bolten Director Office of Management and Budget 725 17 th Street, NW Washington, DC 20503 Dear Director Bolten: This letter transmits the Corrective Action Plan

February 15, 2006 The Honorable Joshua B. Bolten Director Office of Management and Budget 725 17 th Street, NW Washington, DC 20503 Dear Director Bolten: This letter transmits the Corrective Action Plan

CMS DID NOT ALWAYS MANAGE AND OVERSEE CONTRACTOR PERFORMANCE

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL CMS DID NOT ALWAYS MANAGE AND OVERSEE CONTRACTOR PERFORMANCE FOR THE FEDERAL MARKETPLACE AS REQUIRED BY FEDERAL REQUIREMENTS AND CONTRACT

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL CMS DID NOT ALWAYS MANAGE AND OVERSEE CONTRACTOR PERFORMANCE FOR THE FEDERAL MARKETPLACE AS REQUIRED BY FEDERAL REQUIREMENTS AND CONTRACT

Risk Assessment and Subrecipient Monitoring

Risk Assessment and Subrecipient Monitoring Portia Garvey, Assistant Director, Preaward Services Research Office Research 0 Risk Assessment and Subrecipient Monitoring Research Learning Objectives Understand

Risk Assessment and Subrecipient Monitoring Portia Garvey, Assistant Director, Preaward Services Research Office Research 0 Risk Assessment and Subrecipient Monitoring Research Learning Objectives Understand

Uniform Guidance Training #1 Implementation at VCU

Uniform Guidance Training #1 Implementation at VCU Annie Publow, CRA, MFA Director of Sponsored Programs, Government/NonProfit Support Mark Roberts Director of Grants & Contracts Accounting Uniform Guidance

Uniform Guidance Training #1 Implementation at VCU Annie Publow, CRA, MFA Director of Sponsored Programs, Government/NonProfit Support Mark Roberts Director of Grants & Contracts Accounting Uniform Guidance

Question and Answers 42 CFR Part 93

Question and Answers 42 CFR Part 93 These questions and answers are intended to: (1) Assist institutional research integrity officers (RIOS), compliance officers, institutional counsel, and other institutional

Question and Answers 42 CFR Part 93 These questions and answers are intended to: (1) Assist institutional research integrity officers (RIOS), compliance officers, institutional counsel, and other institutional

NSF Grants Conference March 2013. William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation

NSF Grants Conference March 2013 William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation Assistant Inspector General for Audit Inspector General (IG)

NSF Grants Conference March 2013 William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation Assistant Inspector General for Audit Inspector General (IG)

Post-Award Administration. Office of Research Administration

Post-Award Administration Office of Research Administration Post-Award Administration The purpose of this booklet is to help you become familiar with the common issues and transactions associated with

Post-Award Administration Office of Research Administration Post-Award Administration The purpose of this booklet is to help you become familiar with the common issues and transactions associated with

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

Policy Statement The University is committed to ensuring that effort reports completed in connection with sponsored projects are accurate.

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Effort Reporting: Certifying Effort on Sponsored Projects Scope This document sets forth the University s policy on certification of effort expended on sponsored project awards administered by Alabama

Office of the Clerk of Circuit Court Baltimore City, Maryland

Audit Report Office of the Clerk of Circuit Court Baltimore City, Maryland May 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Baltimore City, Maryland May 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

STATE OF FLORIDA VOLUNTARY PREKINDERGARTEN EDUCATION PROGRAM SPECIALIZED INSTRUCTIONAL SERVICES PROVIDER AGREEMENT

STATE OF FLORIDA VOLUNTARY PREKINDERGARTEN EDUCATION PROGRAM SPECIALIZED INSTRUCTIONAL SERVICES PROVIDER AGREEMENT, Rule 6M-8.500, F.A.C. Call the Office Early Learning at 1-866-357-3239 for assistance

STATE OF FLORIDA VOLUNTARY PREKINDERGARTEN EDUCATION PROGRAM SPECIALIZED INSTRUCTIONAL SERVICES PROVIDER AGREEMENT, Rule 6M-8.500, F.A.C. Call the Office Early Learning at 1-866-357-3239 for assistance

Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE)

and Tax Counseling for the Elderly (TCE)") Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) Grant Application Process Overview May 5, 2015 What We are Going to Cover Grant objectives Differences between grants Grant

Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) Grant Application Process Overview May 5, 2015 What We are Going to Cover Grant objectives Differences between grants Grant

.110-9 Effective Dates and Consistent Implementation (Federal)... 9.110-10 Effective Dates and Consistent Implementation (States)... 9.

... 9.110-10 Effective Dates and Consistent Implementation (States)... 9.") Frequently Asked Questions For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The following are frequently

Frequently Asked Questions For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The following are frequently

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT If the Order involves funds from a Federal government contract or funds from a

Attachment II FLOW-DOWN CLAUSES APPLICABLE TO PURCHASE ORDERS INVOLVING FUNDS FROM A FEDERAL GOVERNMENT CONTRACT OR GRANT If the Order involves funds from a Federal government contract or funds from a

CASH MANAGEMENT POLICIES AND PROCEDURES HANDBOOK

F-1 CASH MANAGEMENT POLICIES AND PROCEDURES HANDBOOK APPENDIX F. PROMPT PAYMENT REQUIREMENTS Section 1.0 General This appendix to the Handbook establishes Department of Commerce policies and procedures

F-1 CASH MANAGEMENT POLICIES AND PROCEDURES HANDBOOK APPENDIX F. PROMPT PAYMENT REQUIREMENTS Section 1.0 General This appendix to the Handbook establishes Department of Commerce policies and procedures

SBIR/STTR Post Award Frequently Asked Questions

SBIR/STTR Post Award Frequently Asked Questions FedConnect 1. We have not received notification that our company s grant has been awarded. If our grant has been awarded, how do we access our assistance

SBIR/STTR Post Award Frequently Asked Questions FedConnect 1. We have not received notification that our company s grant has been awarded. If our grant has been awarded, how do we access our assistance

RULES OF THE STATE OF FLORIDA DEPARTMENT OF ELDER AFFAIRS AGING RESOURCE CENTERS CHAPTER 58B-1

RULES OF THE STATE OF FLORIDA DEPARTMENT OF ELDER AFFAIRS AGING RESOURCE CENTERS CHAPTER 58B-1 58B-1.001 Definitions. In addition to the definitions included in Chapter 430, F.S., the following terms shall

RULES OF THE STATE OF FLORIDA DEPARTMENT OF ELDER AFFAIRS AGING RESOURCE CENTERS CHAPTER 58B-1 58B-1.001 Definitions. In addition to the definitions included in Chapter 430, F.S., the following terms shall

RESPONDING TO SUBPOENAS AND REQUESTS FOR EXPERT WITNESS SERVICES. I. Purpose 1. II. Scope

SMITHSONIAN DIRECTIVE 113, July 24, 2012 RESPONDING TO SUBPOENAS AND REQUESTS FOR EXPERT WITNESS SERVICES I. Purpose 1 II. Scope 1 III. Roles and Responsibilities 3 IV. Policy 4 V. Definitions 5 5 I. Purpose

SMITHSONIAN DIRECTIVE 113, July 24, 2012 RESPONDING TO SUBPOENAS AND REQUESTS FOR EXPERT WITNESS SERVICES I. Purpose 1 II. Scope 1 III. Roles and Responsibilities 3 IV. Policy 4 V. Definitions 5 5 I. Purpose

RELOCATION ASSISTANCE SERVICES SPECIFICATIONS (LUMP SUM)

") RELOCATION ASSISTANCE SERVICES SPECIFICATIONS (LUMP SUM) A. PROJECT DESCRIPTION The Local Public Agency (LPA) will receive proposals for Relocation Assistance Services for: Project: CN: Location: The work

RELOCATION ASSISTANCE SERVICES SPECIFICATIONS (LUMP SUM) A. PROJECT DESCRIPTION The Local Public Agency (LPA) will receive proposals for Relocation Assistance Services for: Project: CN: Location: The work

Grants Manual. Approved by Board of County Commissioners March 24, 2016

Grants Manual Approved by Board of County Commissioners March 24, 2016 Prepared by Grants and Special Projects Department 6495 Caroline Street Milton, FL 32570 Table of Contents CHAPTER 1: PURPOSE, SCOPE,

Grants Manual Approved by Board of County Commissioners March 24, 2016 Prepared by Grants and Special Projects Department 6495 Caroline Street Milton, FL 32570 Table of Contents CHAPTER 1: PURPOSE, SCOPE,

Contractor Purchasing System Review (CPSR)

") Contractor Purchasing System Review (CPSR) Presentation References FAR 44.3 and DFARS 244.3 -- Contractors Purchasing Systems Reviews Consent to Subcontract FAR 44.2 2 What is a CPSR Contractor purchasing

Contractor Purchasing System Review (CPSR) Presentation References FAR 44.3 and DFARS 244.3 -- Contractors Purchasing Systems Reviews Consent to Subcontract FAR 44.2 2 What is a CPSR Contractor purchasing

MINNESOTA DEPARTMENT OF HEALTH MASTER GRANT CONTRACT FOR COMMUNITY HEALTH BOARDS

MINNESOTA DEPARTMENT OF HEALTH MASTER GRANT CONTRACT FOR COMMUNITY HEALTH BOARDS DRAFT for Discussion Only 8.22.14 THIS MASTER GRANT CONTRACT, and amendments and supplements thereto, is between the State

MINNESOTA DEPARTMENT OF HEALTH MASTER GRANT CONTRACT FOR COMMUNITY HEALTH BOARDS DRAFT for Discussion Only 8.22.14 THIS MASTER GRANT CONTRACT, and amendments and supplements thereto, is between the State