Statement of Cash Flows and Articulation

|

|

|

- Darren Hawkins

- 7 years ago

- Views:

Transcription

1 Chapter 5 Statement of Cash Flows and Articulation 1. Important companion of the income statement 2. Three main categories of the cash flow statement: operating, investing, and financing 3. Cash flows from operations using either the direct or the indirect method 4. Prepare a complete statement of cash flows 5. Analysis of a firm s financial strength from perspective of cash flows 6. Articulation of the three primary financial statements 7. Forecasted statement of cash flows 5-1

2 1. Describe the circumstances in which the cash flow statement is a particularly important companion of the income statement. What Good is a Cash Flow Statement? We need the cash flow statement because: Sometimes earnings fail. Everything is on one page. It is used as a forecasting tool. 5-2

3 Sometimes Earnings Fail The Big Loss Scenario When a company reports large noncash expenses such as: - write-offs - depreciation - provisions for future obligations earnings may give a gloomier picture of current operations than warranted. (continued) 5-3

4 The Rapid Growth Scenario Rapidly growing firms use large amounts of cash to expand inventory. Cash collections on the growing accounts receivable often lag behind the need to pay creditors. Reported earnings may be positive, but operations are actually consuming rather than generating cash. 5-4

5 The Reality Check Scenario Companies entering phases in which it is critical that reported earnings look good, accounting assumptions can be stretched Just before making a large loan application Just before the initial public offering of stock Just before being bought out by another company Cash flow from operations, which is not impacted by accrual assumptions, provides an excellent reality check for earnings. 5-5

6 Everything is on One Page The cash flow statement includes information on operating, investing, and financing activities. Everything you ever wanted to know about a company s performance for the year is summarized in this one statement. (continued) 5-6

7 It is Used as a Forecasting Tool A pro forma cash flow statement is a prediction of what the actual cash flow statement will look like in future years if the operating, investing, and financing plans are implemented. 5-7

8 2. Outline the structure of and information reported in the three main categories of the cash flow statement: operating, investing, and financing Statement of Cash Flows A statement of cash flows explains the change during the period in cash and cash equivalents. What is this? 5-8

9 Cash Equivalent A cash equivalent is a short-term, highly liquid investment that can be converted easily into cash. To qualify as a cash equivalent, an item must be: 1. Readily convertible into cash 2. So near to its maturity that there is insignificant risk of changes in value due to changes in interest rates 5-9

10 Three Categories of Cash Flows Operating activities include those transactions and events that enter into the determination of net income. Cash receipts from selling goods or from providing services. Receipts from Interest, dividends, and similar items. Payments to purchase inventory and to pay wages, taxes, and similar expenses. 5-10

11 (continued) 5-11

12 Three Categories of Cash Flows The primary investing activities are the purchase and sale of land, buildings, equipment, and other assets not generally held for resale. In addition, investing activities include those transactions and events that involve the purchase and sale of financial instruments not intended for trading purposes, as well as making and collecting loans. (continued) 5-12

13 (continued) 5-13

14 Three Categories of Cash Flows Financing activities include those transactions and events whereby resources are obtained from, or repaid to, owners (equity financing) and creditors (debt financing): Cash proceeds from issuing stocks or bonds. Payments to reacquire stock (treasury stock) or to retire bonds. Payment of dividends. (continued) 5-14

15 (concluded) 5-15

16 Cash Flow Patterns Most companies (73% in the United States in 2006) generate positive cash flow from operations. In normal times, most companies use cash to expand or enhance long-term assets, so cash from investing activities is usually negative (83% of the time in the United States in 2006). No general statement can be made about cash flow from financing activities. (continued) 5-16

17 5-17

18 Noncash Investing and Financing Activities Noncash investing and financing activities affect an entity s financial position but not the entity s cash flow. Examples include: Equipment purchased with a note payable Land acquired by issuing stock Significant transactions should be disclosed separately. These transactions do NOT appear in the statement of cash flows. 5-18

19 Cash Flow Categories Under IAS 7 The provisions of IAS 7, Statement of Cash Flows, are more flexible than the U.S. rules contained in SFAS No. 95. Here is a summary of these differences: 5-19

20 3. Compute cash flow from operations using either the direct or the indirect method 5-20

21 5-21

22 Operating Activities: Direct Method The direct method is essentially a reexamination of each income statement item with the objective of reporting how much cash was received or disbursed in association with the item. To prepare the operating section, each income statement item must be adjusted for the effects of accruals. 5-22

23 Operating Activities: Indirect Method The indirect method begins with net income as reported on the income statement and adjusts the accrual amount for any items that do not affect cash flow. Both the direct and indirect methods produce identical results that is, the same amount of net cash provided by (or used in) operations. (continued) 5-23

24 Operating Activities: Indirect Method The adjustments for the indirect method are of three basic types: Revenues and expenses that do not involve cash inflow or outflow. Gains and losses associated with investing or financing activities. Adjustments for changes in current operating assets and liabilities that indicate noncash sources of revenues and expenses. 5-24

25 Operating Activities 5-25

26 Operating Activities: Direct Method Sales and Cash Collected from Customers Beginning accounts receivable $ 40 + Sales 150 = Cash available for collection $190 Ending accounts receivable 60 = Cash collected from customers $130 (continued) 5-26

27 Operating Activities: Direct Method Cost of Goods Sold and Cash Paid for Inventory Ending inventory $ 75 + Cost of goods sold 80 = Required inventory $155 Beginning inventory 100 = Inventory purchased this year $ 55 (continued) 5-27

28 Operating Activities: Direct Method Wages Expense and Cash Paid for Wages Beginning wages payable $ 7 + Wages expense 25 = Total obligation to employees $32 Ending wages payable 10 = Cash paid for wages $22 (continued) 5-28

29 Operating Activities: Direct Method Depreciation Expense 5-29

30 Operating Activities: Indirect Method Sales The $20 increase in accounts receivable means that cash collected is $20 less than the $150 the sales number indicates. So, the necessary adjustment is to subtract the $20 to show that $130 was collected on account. (continued) 5-30

31 Operating Activities: Indirect Method Cost of Goods Sold The $25 decrease in inventory means that although cost of good sold of $80 is included in the income statement, less cash was used to purchase inventory than suggested add $25 to net income. (continued) 5-31

32 Operating Activities: Indirect Method Wages Expense The $3 increase in wages payable indicates that only $22 of the $25 expense was paid in cash. The $3 increase in wages payable is added to net income. (continued) 5-32

33 Operating Activities: Indirect Method Depreciation Expense The $30 depreciation expense is a noncash expense. Because it was subtracted in computing net income, it must be added back to net income because it was deducted from net income to determine the accrual net income. (continued) 5-33

34 Operating Activities: Indirect Method Note the same net cash from operating activities as calculated using the direct method. 5-34

35 Important Depreciation is not a source of cash. Because you added depreciation back to net income as an adjustment using the indirect method does not mean that there is an inflow of cash. However, depreciation does lower the amount of income taxes paid. One advantage of the indirect method is that it highlights how cash flow can be improved in the short run by adjusting operating procedures. 5-35

36 Comparison of Direct and Indirect Methods Direct Method The shaded area is reported in the Operating Activities section of the statement of cash flows. (continued) 5-36

37 Comparison of Direct and Indirect Methods Indirect Method With the indirect method, only net income and the adjustments are reported. The Operating Activities section of the statement of cash flows includes the shaded information above. (continued) 5-37

38 5-38

39 5-39

40 4. Prepare a complete statement of cash flows and provide the required supplemental disclosures Preparing a Complete Statement of Cash Flows Basic information to prepare the three sections of the cash flow statement comes from the balance sheet and income statement, as follows: Operating income statement adjusted for changes in current operating assets and liabilities. Investing changes in long-term assets. Financing changes in long-term liabilities and owners equity. 5-40

41 Preparing a Complete Statement of Cash Flows Step 1: Compute How Much the Cash Balance Changed During the Year The statement of cash flow is not complete until the sum of cash from operating, investing, and financing activities exactly matches the total change in the cash balance during the year. (continued) 5-41

42 Cash increased $10 during the year. (continued) 5-42

43 Preparing a Complete Statement of Cash Flows Step 2: Convert the Income Statement from an Accrual-Basis to a Cash-Basis Summary of Operations This is done in three steps: (a) Eliminate expenses that do not involve the outflow of cash, such as depreciation expense. (continued) 5-43

44 (continued) 5-44

45 Preparing a Complete Statement of Cash Flows Step 2: Continued (b) Eliminate gains and losses associated with investing or financing activities to avoid counting these items twice. (continued) 5-45

46 Replace with new 5-7 (continued) 5-46

47 Preparing a Complete Statement of Cash Flows Step 2: Continued (c) Adjust for changes in the balances of current operating assets and operating liabilities. (continued) 5-47

48 (continued) 5-48

49 (continued) 5-49

50 (continued) 5-50

51 (continued) 5-51

52 (continued) 5-52

53 Because an interest payable account does not exist, we can safely assume that all interest expense was paid for in cash. Therefore, there is no need for an adjustment. 5-53

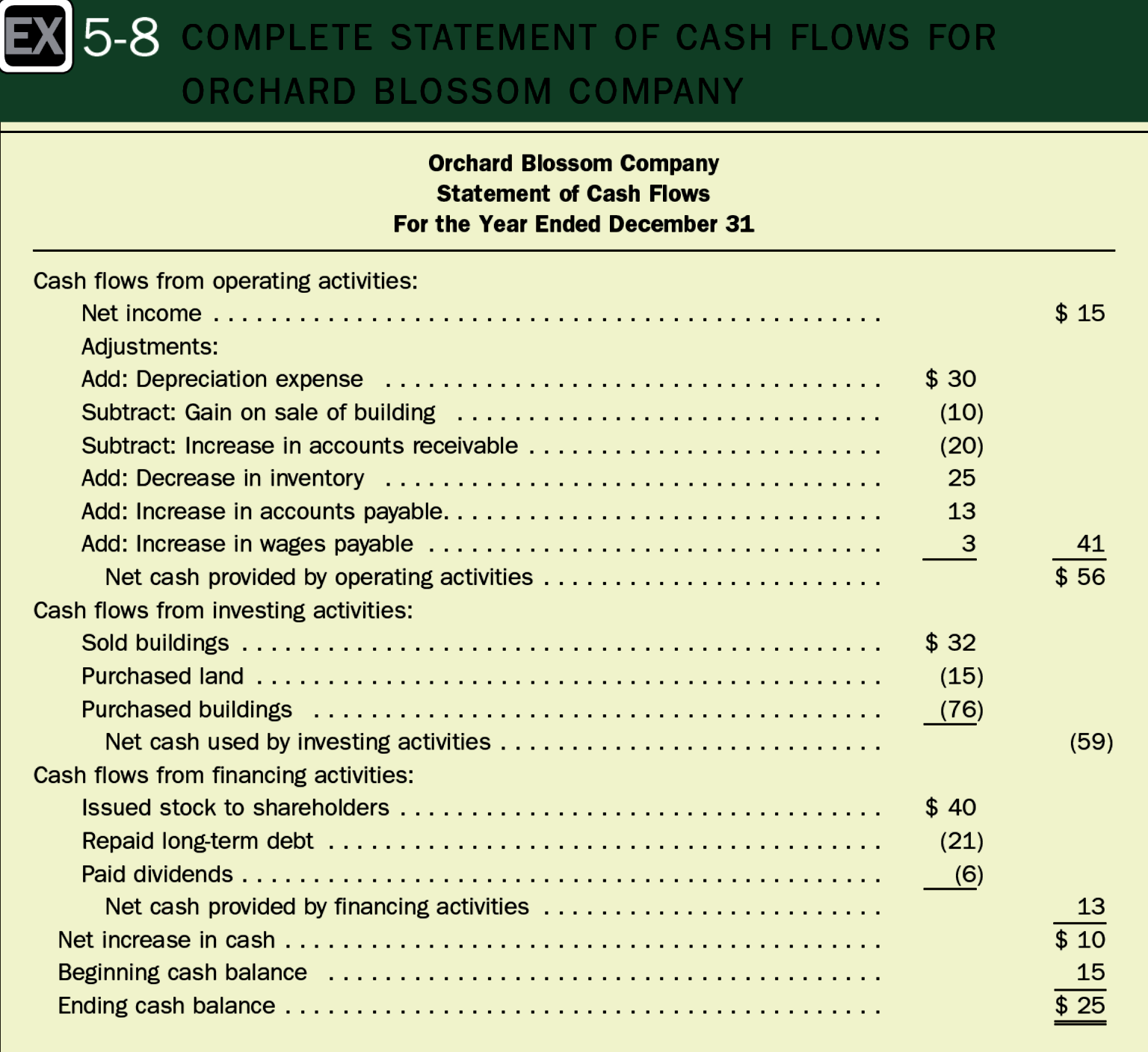

54 Preparing a Complete Statement of Cash Flows Step 3: Analyze the Long-Term Assets to Identify the Cash Flow Effects of Investing Activities. Orchard Blossom reports two long-term asset accounts: Land and Buildings. (continued) 5-54

55 Investing Activities Cash Inflow Sale of plant assets Sale of securities, other than trading securities Collection of principal on loans Cash Outflow Purchase of plant assets Purchase of securities, other than trading securities Making of loans with other entities (continued) 5-55

56 Investing Activities The land account increased by $15 during the year. Because there is no indication of a land sale, we conclude that the $15 represents the price of new land purchased during the year. (continued) 5-56

57 Investing Activities The building account increased $40 during the year. In the absence of any other information, this increase would suggest that Orchard Blossom purchased buildings with a cost of $40. However, additional (continued) 5-57

58 Investing Activities information above is available that indicates that buildings were sold for $32. The $32 cash proceeds from the sale is a cash inflow from investing activities. (continued) 5-58

59 Investing Activities Cash proceeds (given) $32 Book value ($36 $14) 22 Gain on sale of building $10 (continued) 5-59

60 Investing Activities Known (continued) 5-60

61 Investing Activities Building(s) costing $76 must have been purchased during the year. 5-61

62 Preparing a Complete Statement of Cash Flows Step 4: Analyze the Long-Term Debt and Stockholders Equity Accounts to Determine the Cash Flow Effects of Any Financing Transactions. (continued) 5-62

63 Financing Activities Cash Inflow Issuance of own stock Borrowings Cash Outflow Dividend payments Repaying principal on borrowing Treasury stock purchase 5-63

64 Financing Activities We can infer that Orchard Blossom repaid $21 in long-term loans during the year. (continued) 5-64

65 Financing Activities Retained earnings increased by $9. We know there was a $15 net income, so we can use a T- account to determine the amount of the dividend. The $40 ($100 $60) increase in Orchard Blossom s paid-in capital account during the year represents a cash inflow from the issuance of new shares of stock. This cash inflow is reported as part of cash from financing activities. 5-65

during the year.")

66 Financing Activities The $6 debit, or squeeze figure, has to be the dividends declared (and we will assume paid) during the year. 5-66

67 Preparing a Complete Statement of Cash Flows Step 5: Prepare a Formal Statement of Cash Flows. Based on our analyses of the income statement and balance sheet accounts, we have identified all inflows and outflow of cash for Orchard Blossom for the year, and we have categorized those cash flows based on the type of activity. (continued) 5-67

68 5-68

69 Preparing a Complete Statement of Cash Flows Step 6: Prepare Supplemental Disclosure. FASB ASC Topic 230 requires separate disclosure of the cash paid for interest and for income taxes during the year. o Cash paid for interest and income taxes o Noncash investing and financing activities 5-69

70 5. Assess a firm s financial strength by analyzing the relationships among cash flows from operating, investing, and financing activities and by computing financial ratios based on cash flow data Cash Flow Patterns It is possible to gain useful insights about a company by analyzing the relationships among the three cash flow categories. Exhibit 5-9 on Slides 5-71 and 5-72 shows the eight different possible patterns. 5-70

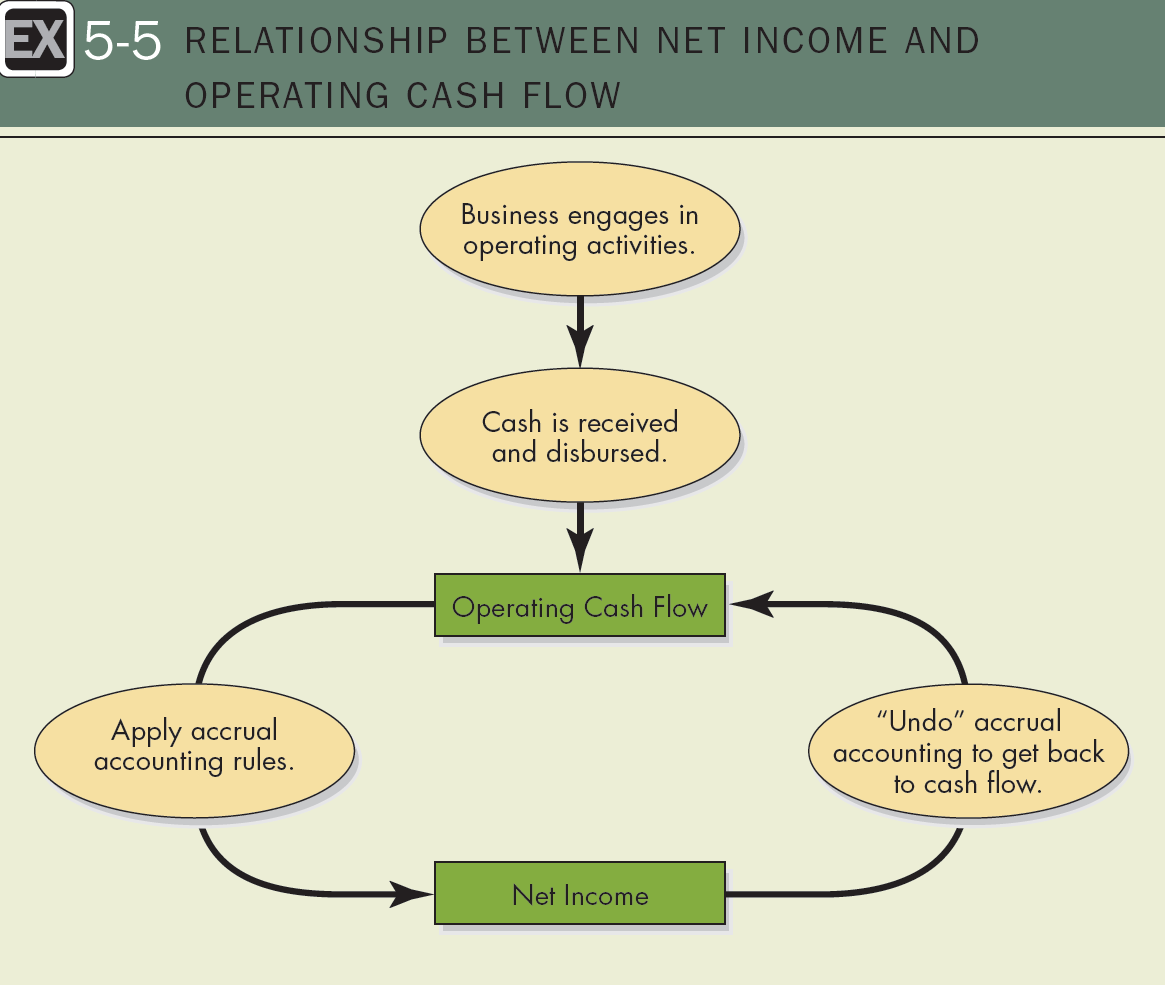

71 (continued) 5-71

72 5-72

73 5-73

74 Cash Flow to Net Income Ratio Cash-flow-to-netincome ratio Cash Flow Ratios = Cash from operations Net income Measure of earnings quality Tends to be greater than 1 Should remain fairly stable for the years for a specific company 5-74

75 Cash Flow Ratios Cash flow adequacy ratio = Cash Flow Adequacy Ratio A cash cow is a business that is generating enough cash from operations to completely pay for all new plant and equipment purchases with cash left over to repay loans or distribute to owners. This ratio indicates whether a business is a cash cow. Cash from operations Capital expenditures and acquisitions (continued) 5-75

76 Cash Flow Ratios Cash Flow Adequacy Ratio 5-76

77 Cash Flow Ratios Cash Times Interest Earned Cash times interest earned ratio = Cash from operations + Interest paid + Taxes paid Interest expense Measures interest-paying ability Generally, a higher ratio indicates more solvency (continued) 5-77

78 Cash Flow Ratios Cash Times Interest Earned 5-78

79 6. Demonstrates how the three primary financial statements tie together, or articulate, in a unified framework Articulation: How the Financial Statements Tie Together In an accounting context, articulation means that the three primary financial statements are not isolated lists of numbers but are an integrated set of reports on a company s financial health. (continued) 5-79

80 $6 5-80

81 7. Use knowledge of how the three primary financial statements tie together to prepare a forecasted statement of cash flows Forecasted Statement of Cash Flows 1. Compute the change in cash. 2. Convert the income statement from an accrual basis to a cash basis. 3. Analyze the long-term asset accounts. 4. Analyze the long-term debt and stockholders equity accounts. 5. Prepare the statement of cash flows. 6. Disclose any significant noncash activities. 5-81

82 5-82

83 5-83

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

The Statement of Cash Flows

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

THE STATEMENT OF CASH FLOWS

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, luciancernusca_ro@yahoo.com Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, luciancernusca_ro@yahoo.com Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

Chapter 14. 1 Copyright 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

Chapter 14 1 Identify the purposes of the statement of cash flows Distinguish among operating, investing, and financing cash flows Prepare the statement of cash flows by the indirect method Identify noncash

T-Account Approach to Preparing a Statement of Cash Flows Indirect Method

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

266 Part 1 E M Foundations of Financial Accounting With these adjustments to the income statement, we can now present the operating activities section of the statement of cash flows using either the direct

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

Analyzing the Statement of Cash Flows

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Analyzing the Statement of Cash Flows Operating Activities NACM Upstate New York Credit Conference 2015 By Ron Sereika, CCE,CEW NACM 1 Objectives of this Educational Session u Show how the statement of

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

The Income Statement and Statement of Cash Flows

THE STATEMENT OF CASH FLOWS Purpose of the Statement of Cash Flows The purpose of the statement of cash flows is to identify the sources and uses of cash and the change in cash from the beginning to the

THE STATEMENT OF CASH FLOWS Purpose of the Statement of Cash Flows The purpose of the statement of cash flows is to identify the sources and uses of cash and the change in cash from the beginning to the

Section A: Questions On Fill In The Blanks

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Statement of Cash Flow

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

> DO IT! Chapter 13. Classification of Cash Flows. Cash from Operating Activities D-1. Solution. Action Plan

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

how to prepare a cash flow statement

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

business builder 4 how to prepare a cash flow statement zions business resource center zions business resource center 2 how to prepare a cash flow statement A cash flow statement is important to your business

Statement of Cash Flows

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

HOSP 2110 (Management Acct) Learning Centre Statement of Cash Flows The Statement of Cash Flows (or cash flow statement) is one of the main financial statements used by investors. It shows the cash generated

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

Statement of Cash Flows: Reporting and Analysis

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

Statement of Cash Flows

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Course pack Accounting 202 Chapter 13: Cash Flow Statement

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

The Cash Flow Statement and Decisions

CHAPTER THIRTEEN The Cash Flow Statement and Decisions Review Previous chapters examined the information provided by the income statement, balance sheet, and statement of changes Where in This owners Chapter

CHAPTER THIRTEEN The Cash Flow Statement and Decisions Review Previous chapters examined the information provided by the income statement, balance sheet, and statement of changes Where in This owners Chapter

Statement of Cash Flows. Study Objectives

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of the product

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

FINANCIAL ACCOUNTING WEEK 12 STATEMENT OF CASH FLOWS. A. Understand the basic structure and format of the statement of cash flows.

FINANCIAL ACCOUNTING WEEK 12 STATEMENT OF CASH FLOWS I. LEARNING OBJECTIVES - STATEMENT OF CASH FLOWS A. Understand the basic structure and format of the statement of cash flows. B. Distinguish cash flows

FINANCIAL ACCOUNTING WEEK 12 STATEMENT OF CASH FLOWS I. LEARNING OBJECTIVES - STATEMENT OF CASH FLOWS A. Understand the basic structure and format of the statement of cash flows. B. Distinguish cash flows

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

Chpater-4: Solutions to Problems

Chpater-4: Solutions to Problems P4-1. Depreciation LG 1; Basic Year Depreciation Schedule Percentages Cost(1) from Table 4.2 (2) Depreciation [(1) (2)] (3) Asset A 1 $17,000 33% $ 5,610 2 $17,000 45 7,650

Chpater-4: Solutions to Problems P4-1. Depreciation LG 1; Basic Year Depreciation Schedule Percentages Cost(1) from Table 4.2 (2) Depreciation [(1) (2)] (3) Asset A 1 $17,000 33% $ 5,610 2 $17,000 45 7,650

Midterm Fall 2012 Solution

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Cash Flow Statement. Introduction. Introd. Contd. Chapter 4

Cash Flow Statement Chapter 4 Introduction Management and other interested external parties have always recognized the need for a cash flow statement but it was never required until the FASB (Financial

Cash Flow Statement Chapter 4 Introduction Management and other interested external parties have always recognized the need for a cash flow statement but it was never required until the FASB (Financial

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

Chapter. Statement of Cash Flows For Single Company

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Chapter 4 Statement of Cash Flows For Single Company 4.1 Single company statement of cash flows Statement of cash flows are primary financial statements and are required along side the income statement

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Financial Reporting & Analysis Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Determining cash flows from operations Using the indirect method, cash flow from operations is computed

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Cash Flow Analysis. 15.511 Corporate Accounting Summer 2004. Professor SP Kothari. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

The Basic Framework of Budgeting

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

Master Budgeting 1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

CHAPTER 5. Examining the Balance Sheet and Statement of Cash Flows 2 4, 5 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 12, 13, 14, 15, 16

CHAPTER 5 Examining the Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles,

CHAPTER 5 Examining the Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles,

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital

CHAE Review. Capital Leases & Forms of Business

CHAE Review Financial Statements, Capital Leases & Forms of Business This is a complete review of the two volume text book, Certified Hospitality Accountant Executive Study Guide, as published by The Educational

CHAE Review Financial Statements, Capital Leases & Forms of Business This is a complete review of the two volume text book, Certified Hospitality Accountant Executive Study Guide, as published by The Educational

Short Term Finance and Planning. Sources and Uses of Cash

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

3,000 3,000 2,910 2,910 3,000 3,000 2,940 2,940

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A Simple Model. Cash Flow Statement

An introduction to the cash flow statement in the context of building a financial model. This series introduces the financial statements in the context of a financial model. Cash Flow Statement NOTES TO

An introduction to the cash flow statement in the context of building a financial model. This series introduces the financial statements in the context of a financial model. Cash Flow Statement NOTES TO

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Vol. 1, Chapter 7 The Statement of Cash Flows

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

Vol. 1, Chapter 7 The Statement of Cash Flows Problem 1: Solution Transaction # Identification 1 Operating 2 Investing 3 Noncash transaction 4 Financing 5 Noncash transaction 6 Operating 7 Investing 8

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

STATEMENT OF CHANGES IN FINANCIAL POSITION

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

Home Page - Statement of Changes in Financial Position STATEMENT OF CHANGES IN FINANCIAL POSITION by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Financial Statement Analysis: An Introduction

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

MIDTERM EXAMINATION. Afaaq_tariq@yahoo.com. Fall 2009

MIDTERM EXAMINATION Afaaq_tariq@yahoo.com Fall 2009 FIN621- Financial Statement Analysis Asslam O Alikum FIN621- Financial Statement Analysis (Session 3) solved by Afaaq n Shani Bhai with reference n numerical

MIDTERM EXAMINATION Afaaq_tariq@yahoo.com Fall 2009 FIN621- Financial Statement Analysis Asslam O Alikum FIN621- Financial Statement Analysis (Session 3) solved by Afaaq n Shani Bhai with reference n numerical

MASTER BUDGET - EXAMPLE

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

Cash Flow Statements

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

ACC 120 PRINCIPLES OF FINANCIAL ACCOUNTING

ACC 120 PRINCIPLES OF FINANCIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites ENG 090, and RED 090 or DRE 098; MAT 070 or DMA 010, 020, 030, 040, or satisfactory score on placement test Corequisites: None

ACC 120 PRINCIPLES OF FINANCIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites ENG 090, and RED 090 or DRE 098; MAT 070 or DMA 010, 020, 030, 040, or satisfactory score on placement test Corequisites: None

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements. Fall 2015 Comp Week 5

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements Fall 2015 Comp Week 5 CODE: CA$H Administrative Stuff Send an email to trentnelson@college.harvard.edu if you have not been added

ACCOUNTING III Cash Flow Statement & Linking the 3 Financial Statements Fall 2015 Comp Week 5 CODE: CA$H Administrative Stuff Send an email to trentnelson@college.harvard.edu if you have not been added

Cash Flow Analysis. 15.501/516 Accounting Spring 2004. Professor S. Roychowdhury. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

Cash Flow Analysis 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology Mar 1/3, 2004 1 About The Exam March 10 th a week from today.

Accounting 500 4A Balance Sheet Page 1

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures

THE POWER OF CASH FLOW RATIOS

THE POWER OF CASH FLOW RATIOS By Frank R, Urbancic, DBA, CPA Professor and Chair Department of Accounting Mitchell College of Business University of South Alabama Mobile, Alabama 36688 (251) 460-6733 FAX

THE POWER OF CASH FLOW RATIOS By Frank R, Urbancic, DBA, CPA Professor and Chair Department of Accounting Mitchell College of Business University of South Alabama Mobile, Alabama 36688 (251) 460-6733 FAX

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

IGAS 3. Cash Flow Statements. Government Accounting Standards Advisory Board. Contents

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Farm Financial Management

Farm Financial Management Your Farm Income Statement How much did your farm business earn last year? There are many ways to answer this question. A farm income statement (sometimes called a profit and

Farm Financial Management Your Farm Income Statement How much did your farm business earn last year? There are many ways to answer this question. A farm income statement (sometimes called a profit and

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 13 1. Corporate Organization: a. Application for incorporation. b. State grants Charter or Articles of Incorporation. c. By-laws: rules and procedures of

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 13 1. Corporate Organization: a. Application for incorporation. b. State grants Charter or Articles of Incorporation. c. By-laws: rules and procedures of

National Black Law Journal UCLA

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

Accounting Guideline

Accounting Guideline GAP 2 Cash Flow Statements All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic,

Accounting Guideline GAP 2 Cash Flow Statements All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic,

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Preparation Of The Statement Of Cash Flows In Accordance With IAS 7

Preparation Of The Statement Of Cash Flows In Accordance With IAS 7 Ephraim Hudson Mazvidza Matavire, Tawanda Dzama Abstract: International Accounting Standard (IAS) 1: Presentation of financial statements,

Preparation Of The Statement Of Cash Flows In Accordance With IAS 7 Ephraim Hudson Mazvidza Matavire, Tawanda Dzama Abstract: International Accounting Standard (IAS) 1: Presentation of financial statements,

Preparing Agricultural Financial Statements

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records