BUS312A/612A Financial Reporting I. Homework & Statements of Income and Retained Earnings Chapter 4

|

|

|

- Kathryn Sophie Oliver

- 7 years ago

- Views:

Transcription

1 BUS312A/612A Financial Reporting I Homework & Statements of Income and Retained Earnings Chapter 4

2 E4-2 (Income Statement Items) Presented below are certain account balances of Viel Co. at December 31, 2014, the end of its first year of operations. Sales revenue $310,000 Cost of goods sold 140,000 Selling & Admin. Expenses 50,000 Gain on sale of plant assets 30,000 Unrealized gain on available-for-sale investments 10,000 Interest expense $ 6,000 Loss on discontinued operations 12,000 Allocation to noncontrolling interest 40,000 Dividends declared and paid 5,000 Compute the following: (a) income from operations, (b) net income, (c) net income attributable to Viel Company s controlling shareholders, (d) comprehensive income, and (e) retained earnings balance at December 31, 2014.

3

4 Alt. E4-3 (Income Statement Items) Presented below are certain account balances of Paczki Products Co. Rental revenue $ 6,500 Interest expense 12,700 Beginning retained earning 114,400 Ending retained earnings 134,000 Dividend revenue 71,000 Sales returns 12,400 Allocation to noncontrolling interest 17,000 Sales discounts $ 7,800 Selling expenses 99,400 Sales revenue 390,000 Income tax expense 31,000 Cost of goods sold 184,400 Administrative expenses 82,500 From the foregoing, compute the following: (a) total net revenue, (b) net income, (c) dividends declared during the current year, and income attributable to controlling stockholders.

5

6 E4-4 Single step Income Statement Fire destroyed L Jones Inc. financial records. Prepare an income statement for 2014 in singlestep form using the data the controller kept. 1. The beginning merchandise inventory was $92,000 and decreased 20% during the current year. 2. Sales discounts amount to $17, ,000 shares of common stock were outstanding the entire year. 4. Interest expense was $20,000 for the year. 5. The income tax rate is 30%. 6. Cost of goods sold amounts to $500, Administrative expenses are 20% of cost of goods sold but only 8% of gross sales. 8. Four-fifths of the operating expenses relate to sales activities.

7

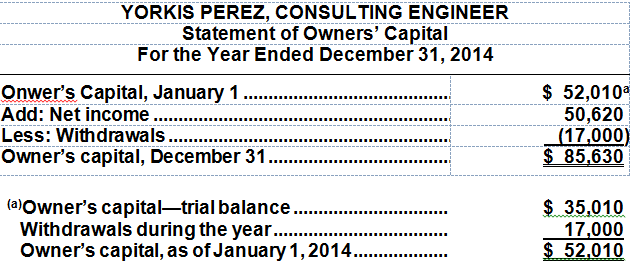

8 P3-6 Adjusting Entries and Financial Statements Cash $29,500 Accounts Receivable 49,600 Allowance for Bad Debts $ 750 Inventory 1,960 Prepaid Insurance 1,100 Equipment 25,000 Accumulated Depreciation- Equipment 6,250 Notes Payable 7,200 Owner s Capital 35,010 Service Revenue 100,000 Rent Expense 9,750 Salaries and Wages Expense 30,500 Utilities Expense 1,080 Office Expense 720 $149,210 $149, Fees received in advance from clients $6, Services performed for clients that were not recorded by December 31, $4, Bad debt expense for the year $1, Insurance expired during the year $ Equipment is being depreciated at 10% per year. 6. Perez gave bank a 90 day, 10% note for $7,200 on December 1, Rent of the building is $750 per month. The rent for 2014 has been paid, as has that for January Office salaries and wages earned but unpaid at December 31, $2,510.

9 1. Fees received in advance from clients $6, Services performed for clients that were not recorded by December 31, $4, Bad debt expense for the year $1, Insurance expired during the year $ Equipment is being depreciated at 10% per year. 6. Perez gave bank a 90 day, 10% note for $7,200 on December 1, Rent of the building is $750 per month. The rent for 2014 has been paid, as has that for January Office salaries and wages earned but unpaid at December 31, $2,510.

10

11

12 E4-5 (Multiple-step and Single-step) 2014 information for P. Bride Co. ($000 omitted). Administrative expense Officers salaries $ 4,900 Depreciation of furniture and equipment 3,960 Cost of goods sold 60,570 Rental revenue 17,230 Selling expense Delivery expense 2,690 Sales commissions 7,980 Depreciation of sales equipment 6,480 Sales revenue 96,500 Income tax expense 9,070 Interest expense 1,860 a) Multiple-step income statement for Shares outstanding = 40,550 ($000 omitted). b) Single-step income statement for c) Which one is best? Discuss.

13

14 Alt. E4-6 (Multiple-step and Extraordinary Items) The following balances were taken from the books of MCA Corp. on December 31, Interest revenue $ 86,000 Cash 51,000 Sales 1,380,000 Accounts receivable 150,000 Prepaid Insurance 20,000 Sales returns and allowances 150,000 Allowance for doubtful accounts 7,000 Sales discounts 45,000 Land 100,000 Equipment 200,000 Building 140,000 Cost of goods sold 621,000 Assume the total effective tax rate on all items is 34%. Accumulated depreciation-equipment $ 40,000 Accumulated depreciation-building 28,000 Notes receivable 155,000 Selling expenses 194,000 Accounts payable 170,000 Bonds payable 100,000 Administrative and general expenses 97,000 Accrued liabilities 32,000 Interest expense 60,000 Notes payable 100,000 Loss from earthquake damage (extraordinary item) 150,000 Common stock 500,000 Retained earnings 21,000 Prepare a multiple-step income statement; 100,000 shares of common stock outstanding during the year.

15

16 E4-14 (Change in Accounting Principle) Tim Mattke Company began operations in 2012 and for simplicity reasons, adopted weighted-average pricing for inventory. In 2014, in accordance with other companies in its industry, Mattke changed its inventory pricing to FIFO. The pretax income data is reported below. Year EBIT Weighted-Average EBIT FIFO 2012 $370,000 $395, , , , ,000 Instructions (a) (b) (c) What is Mattke s net income for 2014? Assume a 35% tax rate in all years. Compute the cumulative effect of the change in accounting principle. Show the comparative income statements for the company, beginning with income before income tax, as presented on the 2014 income statement.

17

the one statement format, and (b) the two statement format.")

18 E4-15 (Comprehensive Income) Carter Corporation reported the following for 2014: net sales $1,200,000; cost of goods sold $750,000; selling and administrative expenses $320,000; unrealized holding gain on available-for sale securities $18,000. Prepare a statement of comprehensive income, using (a) the one statement format, and (b) the two statement format. Ignore income taxes and earnings per share).

19 Alt. E4-16 (Comprehensive Income) Reither Co. reports the following for 2014: sales revenue $700,000; COGS $500,000; operating expenses $80,000; and an unrealized holding loss on available-for-sale securities of $60,000. It declared and paid a cash dividend of $10,000 in January 1, 2014 balances in common stock $350,000; accumulated other comprehensive income $80,000; retained earnings $90,000. No stock issued in 2014.

20 Alt. CA4-6 (Classification of Income Statement Items) What section of the income statement or retained earnings statement should these items be classified? Explain. 1. A merchandising company incorrectly overstated its ending inventory two years ago. Inventory for all other periods is correctly computed. 2. An automobile dealer sells for $137,000 a rare 1930 S type Invicta which it purchased for $21, years ago. The Invicta is the only such display item the dealer owns. 3. A drilling company extended the estimated useful life of drilling equipment from 9 to 15 years. As a result, depreciation for the current year was materially lowered. 4. A retail outlet changed its computation for bad debt expense from 1% to.5% of sales because of changes in its customer clientele. 5. A mining concern sells a foreign subsidiary engaged in uranium mining, although it (the seller) continues to engage in uranium mining in other countries. 6. A steel company changes from the average-cost to FIFO inventory costing. 7. A company, at great expense, prepared a major proposal for a government loan, which is not approved. 8. A water pump manufacturer has had large losses resulting from a strike by its employees early in the year. 9. Depreciation for a prior period was incorrectly understated by $950,000. The error was discovered in the current year. 10. A sheep rancher suffered a major loss because the state required that all sheep be killed to halt the spread of a rare disease. Such a situation has not occurred in the state for 20 years. 11. A food distributor that sells to supermarket chains and fast-food restaurants (two distinguishable classes of customers) decides to discontinue the division that sells to supermarkets.

21 CA4-3 (Earnings Management) The controller for Kelly Corporation is preparing the company s income statement at year-end. He notes that the company has lost a considerable sum on the sale of some equipment it had decided to replace. Since the company has sold equipment routinely in the past, he knows the losses cannot be reported as extraordinary. He does not want to highlight it as a material loss since he feels that will reflect poorly on him and the company. He reasons that if the company had recorded more depreciation during the assets lives, the losses would not be so great. Since depreciation is included among the company s operating expenses, he wants to report the losses along with the company expenses, where he hopes it will not be noticed. Instructions (a) What are the ethical issues involved? (b) What should the controller do?

22 Classification in the Balance Sheet Question The correct order to present current assets is a. Cash, accounts receivable, prepaid items, inventories. b. Cash, accounts receivable, inventories, prepaid items. c. Cash, inventories, accounts receivable, prepaid items. d. Cash, inventories, prepaid items, accounts receivable. Order of Liquidity

23 Statement of Cash Flows Question In preparing a statement of cash flows, which of the following transactions would be considered an investing activity? a. Sale of equipment at book value b. Sale of merchandise on credit c. Declaration of a cash dividend d. Issuance of bonds payable at a discount receivable.

24 IFRS SELF-TEST QUESTION Current assets under IFRS are listed generally: a. by importance. b. in the reverse order of their expected conversion to cash. c. by longevity. d. alphabetically.

25 IFRS SELF-TEST QUESTION Companies that use IFRS: a. may report all their assets on the statement of financial position at fair value. b. are not allowed to net assets (assets 2 liabilities) on their statement of financial positions. c. may report noncurrent assets before current assets on the statement of financial position. d. do not have any guidelines as to what should be reported on the statement of financial position.

26 IFRS SELF-TEST QUESTION A company has purchased a tract of land and expects to build a production plant on the land in approximately 5 years. During the 5 years before construction, the land will be idle. Under IFRS, the land should be reported as: a. land expense. b. property, plant, and equipment. c. an intangible asset. d. a long-term investment.

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

a. $ 65,000. b. $ 80,000. c. $130,000. d. $145,000.

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

注 意 1. 本 試 題 卷 共 50 題, 總 分 100 分 第 01-15 題, 每 題 1.75 分, 合 計 26.25 分 ; 第 16-35 題, 每 題 2 分, 合 計 40 分 ; 第 36-50 題, 每 題 2.25 分, 合 計 33.75 答 錯 不 倒 扣 2. 請 將 答 案 按 試 題 題 號, 依 序 填 入 答 案 卡 1.FastForward had cash

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試 7 月 12 日 14:00~15:30 商 學 群 組 二 年 級 科 目 : 會 計 學 ( 共 七 頁 第 一 頁 ) 可 使 用 計 算 機, 惟 僅 限 不 具 可 程 式 及 多 重 記 憶 者 一 MULTIPLE CHOICE QUESTIONS: (50%) 誠 實 是 我 們 珍 視 的 美 德, 我 們 喜

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試 7 月 12 日 14:00~15:30 商 學 群 組 二 年 級 科 目 : 會 計 學 ( 共 七 頁 第 一 頁 ) 可 使 用 計 算 機, 惟 僅 限 不 具 可 程 式 及 多 重 記 憶 者 一 MULTIPLE CHOICE QUESTIONS: (50%) 誠 實 是 我 們 珍 視 的 美 德, 我 們 喜

PROFESSOR S NAME ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8)

") COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

1. Operating, Investment and Financial Cash Flows

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

1. Operating, Investment and Financial Cash Flows Solutions Problem 1 During 2005, Myears Oil Co. had gross sales of $1 000,000, cost of goods sold of $400,000, and general and selling expenses of $300,000.

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

SOLUTIONS. Learning Goal 15

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

How To Calculate A Trial Balance For A Company

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

THE BASIC MODEL The accounting information system is designed to collect and organize data into information that is useful for stakeholders. The Accounting Equation The basic accounting equation is what

Section A: Questions On Fill In The Blanks

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

Section A : 26 FILL IN THE BLANK Section B : 10 TRUE OR FALSE QUESTIONS Section C : 11 Multiple Choice Questions Section A: Questions Fill In The Blanks the right column please insert the items from which

SANYO TRADING COMPANY LIMITED. Financial Statements

Financial Statements Year Ended September 30, 2014 English translation from original Japanese-language documents Balance Sheets As of September 30, 2014 ASSETS Current Assets Cash and deposits US$ 18,509,007

Financial Statements Year Ended September 30, 2014 English translation from original Japanese-language documents Balance Sheets As of September 30, 2014 ASSETS Current Assets Cash and deposits US$ 18,509,007

EXERCISES. Does not normally require adjustment. Normally requires adjustment (AE).

.") EXERCISES Ex. 3 1 1. Prepaid expense 2. Accrued revenue 3. Unearned revenue 4. Accrued expense 5. Unearned revenue 6. Prepaid expense 7. Accrued expense 8. Accrued expense Ex. 3 2 Account Accounts Receivable...

EXERCISES Ex. 3 1 1. Prepaid expense 2. Accrued revenue 3. Unearned revenue 4. Accrued expense 5. Unearned revenue 6. Prepaid expense 7. Accrued expense 8. Accrued expense Ex. 3 2 Account Accounts Receivable...

B Exercises 4-1. (d) Intangible assets. (i) Paid-in capital in excess of par.

Intangible assets. (i) Paid-in capital in excess of par.") B Exercises E4-1B (Balance Sheet Classifications) Presented below are a number of balance sheet accounts of Castillo Inc. (a) Trading Securities. (h) Warehouse in Process of Construction. (b) Work in Process.

B Exercises E4-1B (Balance Sheet Classifications) Presented below are a number of balance sheet accounts of Castillo Inc. (a) Trading Securities. (h) Warehouse in Process of Construction. (b) Work in Process.

Financial Statements Tutorial

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS (1) Consolidated Quarterly Balance Sheets September 30, 2014 and March 31, 2014 Supplementary Information 2Q FY March 2015 March 31, 2014 September 30, 2014

3. CONSOLIDATED QUARTERLY FINANCIAL STATEMENTS (1) Consolidated Quarterly Balance Sheets September 30, 2014 and March 31, 2014 Supplementary Information 2Q FY March 2015 March 31, 2014 September 30, 2014

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

Chapter 21 The Statement of Cash Flows Revisited

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 21 The Statement of Cash Flows Revisited AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Statement of Cash Flows

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

PREPARING THE STATEMENT OF CASH FLOWS: THE INDIRECT METHOD OF REPORTING CASH FLOWS FROM OPERATING ACTIVITIES The work sheet method described in the text book is not the recommended approach. We will provide

BUS312A/612A Financial Reporting I. Homework 9.10.2014 & 9.15.2014 The Accounting Cycle Review Chapter 3

BUS312A/612A Financial Reporting I Homework 9.10.2014 & 9.15.2014 The Accounting Cycle Review Chapter 3 E3-1 (Transaction Analysis-Service Company) During the first month of operations of her business

BUS312A/612A Financial Reporting I Homework 9.10.2014 & 9.15.2014 The Accounting Cycle Review Chapter 3 E3-1 (Transaction Analysis-Service Company) During the first month of operations of her business

ACER INCORPORATED AND SUBSIDIARIES. Consolidated Balance Sheets

Consolidated Balance Sheets June 30, 2015, December 31, 2014, and (June 30, 2015 and 2014 are reviewed, not audited) Assets 2015.6.30 2014.12.31 2014.6.30 Current assets: Cash and cash equivalents $ 36,400,657

Consolidated Balance Sheets June 30, 2015, December 31, 2014, and (June 30, 2015 and 2014 are reviewed, not audited) Assets 2015.6.30 2014.12.31 2014.6.30 Current assets: Cash and cash equivalents $ 36,400,657

Dr. M. D. Chase Advanced Accounting Exam 1AA Page 1 of 9

Advanced Accounting Exam 1AA Page 1 of 9 MARK THE LETTER OF THE BEST ANSWER ON YOUR SCANTRON FORM. 1. A business combination is accounted for appropriately as a pooling of interests. Costs of furnishing

Advanced Accounting Exam 1AA Page 1 of 9 MARK THE LETTER OF THE BEST ANSWER ON YOUR SCANTRON FORM. 1. A business combination is accounted for appropriately as a pooling of interests. Costs of furnishing

Account Numbering. By separating each account by several numbers, many new accounts can be added between any two while maintaining the logical order.

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014)

") Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014) 28/4/2014 Name of registrant: ShinMaywa Industries, Ltd. Stock Exchange Listed: Tokyo Code number: 7224 (URL: http://www.shinmaywa.co.jp

Consolidated Financial Results for Fiscal Year 2013 (April 1, 2013 March 31, 2014) 28/4/2014 Name of registrant: ShinMaywa Industries, Ltd. Stock Exchange Listed: Tokyo Code number: 7224 (URL: http://www.shinmaywa.co.jp

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

ACCOUNTING 105 CONCEPTS REVIEW

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated)

") Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

Summary of Financial Report for the FY ending March 2015 (Non-Consolidated) April 30, 2015 Listed Company Name: Japan Tissue Engineering Co., Ltd. Listed Securities Exchange: JQ Stock Code: 7774 URL http://www.jpte.co.jp

Accounting Skills Assessment Practice Exam Page 1 of 10

NAU ACCOUNTING SKILLS ASSESSMENT PRACTICE EXAM & KEY 1. A company received cash and issued common stock. What was the effect on the accounting equation? Assets Liabilities Stockholders Equity A. + NE +

NAU ACCOUNTING SKILLS ASSESSMENT PRACTICE EXAM & KEY 1. A company received cash and issued common stock. What was the effect on the accounting equation? Assets Liabilities Stockholders Equity A. + NE +

GBA 521 Midterm Review Dr. Markelevich

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

GBA 521 Midterm Review Dr. Markelevich Multiple Choice (3 points for each question) Identify the letter of the choice that best completes the statement or answers the question. Wynn Corp. Wynn Corp. reported

The Statement of Cash Flows

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

CHAPTER The Statement of Cash Flows OBJECTIVES After careful study of this chapter, you will be able to: 1. Define operating, investing, and financing activities. 2. Know the categories of inflows and

CHAPTER 22. Accounting Changes and Error Analysis 4, 6, 7, 8, 9, 12, 13, 15

CHAPTER 22 Accounting Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics 1. Differences between change in principle, change in estimate, change in entity, errors. Questions 4,

CHAPTER 22 Accounting Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics 1. Differences between change in principle, change in estimate, change in entity, errors. Questions 4,

Statement of Cash Flows: Reporting and Analysis

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Statement of Cash Flows: Reporting and Analysis Statement of Cash Flows: Reporting and Analysis Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings ANSWERS TO QUESTIONS 1. Adjusting entries are made at the end of the accounting period to record all revenues and expenses that

Chapter 4 Adjustments, Financial Statements, and the Quality of Earnings ANSWERS TO QUESTIONS 1. Adjusting entries are made at the end of the accounting period to record all revenues and expenses that

GENERAL LIGHTING CORPORATION Income Statement For the Year Ended December 31, 2013

Chapter 4 Exercises and Problems Exercise 4 2 Requirement 1 GENERAL LIGHTING CORPORATION Income Statement Revenues and gains: Sales... $2,350,000 Rental revenue... 80,000 Total revenues and gains... 2,430,000

Chapter 4 Exercises and Problems Exercise 4 2 Requirement 1 GENERAL LIGHTING CORPORATION Income Statement Revenues and gains: Sales... $2,350,000 Rental revenue... 80,000 Total revenues and gains... 2,430,000

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

Consolidated Financial Results for the nine months of Fiscal Year 2010

Consolidated Financial Results for the nine months of Fiscal Year 2010 (Fiscal Year 2010: Year ending March 31, 2010) Noritake Co., Limited Company Name Stock Exchange Listings Tokyo, Nagoya Code Number

Consolidated Financial Results for the nine months of Fiscal Year 2010 (Fiscal Year 2010: Year ending March 31, 2010) Noritake Co., Limited Company Name Stock Exchange Listings Tokyo, Nagoya Code Number

1. This exam contains 12 pages. Please make sure your copy is not missing any pages.

Name Solution Key Section ACCOUNTING 15.501 SPRING 2003 FINAL EXAM EXAM GUIDELINES 1. This exam contains 12 pages. Please make sure your copy is not missing any pages. 2. The exam must be completed within

Name Solution Key Section ACCOUNTING 15.501 SPRING 2003 FINAL EXAM EXAM GUIDELINES 1. This exam contains 12 pages. Please make sure your copy is not missing any pages. 2. The exam must be completed within

02.Murray Company debited Prepaid Insurance for $960 on July 1, 1998 for a one-year

八 十 八 學 年 度 會 計 學 考 古 題 題 目 難 易 的 順 序 ( 難 易 ) 為 : I III II I Multiple Choice (74%) 01.The purchase of office equipment for $15,000 cash a. is a cash outflow from financing activities. b. is a cash outflow

八 十 八 學 年 度 會 計 學 考 古 題 題 目 難 易 的 順 序 ( 難 易 ) 為 : I III II I Multiple Choice (74%) 01.The purchase of office equipment for $15,000 cash a. is a cash outflow from financing activities. b. is a cash outflow

ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET J.M. TULL SCHOOL OF ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET

ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET J.M. TULL SCHOOL OF ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET Important: PRINT your response (A,B,C,D or E) that best completes the statement

ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET J.M. TULL SCHOOL OF ACCOUNTING ENTRANCE EXAMINATION PRACTICE QUESTION SET Important: PRINT your response (A,B,C,D or E) that best completes the statement

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Exam 1 chapters 1-4 Needles 10ed

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

Consolidated balance sheet

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

83 Consolidated balance sheet December 31 Non-current assets Goodwill 14 675.1 978.4 Other intangible assets 14 317.4 303.8 Property, plant, and equipment 15 530.7 492.0 Investment in associates 16 2.5

Consolidated Financial Statements (For the fiscal year ended March 31, 2013)

") Consolidated Financial Statements (For the fiscal year ended ) Consolidated Balance Sheets Current assets: Cash and deposits Other Assets Notes receivable, accounts receivable from completed construction

Consolidated Financial Statements (For the fiscal year ended ) Consolidated Balance Sheets Current assets: Cash and deposits Other Assets Notes receivable, accounts receivable from completed construction

> DO IT! Chapter 13. Classification of Cash Flows. Cash from Operating Activities D-1. Solution. Action Plan

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

Chapter 13 > DO IT! Classification of Cash Flows Identify the three types of activities used to report all cash inflows and outflows. Report as operating activities the cash effects of transactions that

RAPID REVIEW Chapter Content

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

Accounting 500 4A Balance Sheet Page 1

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

Sample Test for entrance into Acct 3110 and Acct 3310

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

CHAPTER 4. Income Statement and Related Information 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 18, 28, 31, 32, 33 11, 19, 23, 24 13, 14, 15, 16, 27, 29

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. If the assets owned by a business total $100,000 and liabilities total $70,000, stockholders' equity totals $30,000.

Rallis Page 1 Name: _ Date: 1. If the assets owned by a business total $100,000 and liabilities total $70,000, stockholders' equity totals $30,000. A) True B) False 2. If total liabilities decreased by

Rallis Page 1 Name: _ Date: 1. If the assets owned by a business total $100,000 and liabilities total $70,000, stockholders' equity totals $30,000. A) True B) False 2. If total liabilities decreased by

EXERCISES. The cash from operating activities detail is provided as follows for class discussion:

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

EXERCISES Ex. 14 1 There were net additions, such as depreciation and amortization of intangible assets of $389 million, to the net loss reported on the income statement to convert the net loss from the

Items Disclosed via the Internet Concerning the Notice of. Convocation of the 117th Annual General Meeting of Shareholders

To our shareholders: Items Disclosed via the Internet Concerning the Notice of Convocation of the 117th Annual General Meeting of Shareholders Notes to Consolidated Financial Statements Notes to Non-consolidated

To our shareholders: Items Disclosed via the Internet Concerning the Notice of Convocation of the 117th Annual General Meeting of Shareholders Notes to Consolidated Financial Statements Notes to Non-consolidated

TRANSACTIONS ANALYSIS EXAMPLE. Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations:

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

TRANSACTIONS ANALYSIS EXAMPLE Maxwell Partners Medical Diagnostic Services report the following information for 2011, their first year of operations: 1. Billings to clients for services provided: $350,000

Accounting 201 Comprehensive Practice Exam 2C Page 1

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

國 立 體 育 學 院 九 十 六 學 年 度 學 士 班 轉 學 考 試 試 題

國 立 體 育 學 院 九 十 六 學 年 度 學 士 班 轉 學 考 試 試 題 會 計 學 ( 本 試 題 共 8 頁 ) 注 意 :1 答 案 一 律 寫 在 答 案 卷 上, 否 則 不 予 計 分 2 請 核 對 試 卷 准 考 證 號 碼 與 座 位 號 碼 三 者 是 否 相 符 3 試 卷 彌 封 處 不 得 汚 損 破 壞 4 行 動 電 話 或 呼 叫 器 等 通 訊 器 材 不

國 立 體 育 學 院 九 十 六 學 年 度 學 士 班 轉 學 考 試 試 題 會 計 學 ( 本 試 題 共 8 頁 ) 注 意 :1 答 案 一 律 寫 在 答 案 卷 上, 否 則 不 予 計 分 2 請 核 對 試 卷 准 考 證 號 碼 與 座 位 號 碼 三 者 是 否 相 符 3 試 卷 彌 封 處 不 得 汚 損 破 壞 4 行 動 電 話 或 呼 叫 器 等 通 訊 器 材 不

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000)

") Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

Investments Advance to subsidiary company 81,000

EXERCISE 7-3 (10 15 minutes) Current assets Accounts receivable Customers Accounts (of which accounts in the amount of $40,000 have been pledged as security for a bank loan) $79,000 Installment accounts

EXERCISE 7-3 (10 15 minutes) Current assets Accounts receivable Customers Accounts (of which accounts in the amount of $40,000 have been pledged as security for a bank loan) $79,000 Installment accounts

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Gold Run Snowmobile. Adjusting Entries and Closing Entries For The Quarter Ended December 31. Final Project Evaluation. 5 th Edition.

Gold Run Snowmobile 5 th Edition Adjusting Entries and Closing Entries For The Quarter Ended December 31 and the Final Project Evaluation Page 1 ADJUSTING ENTRIES FOR THE QUARTER Using a copy of the December

Gold Run Snowmobile 5 th Edition Adjusting Entries and Closing Entries For The Quarter Ended December 31 and the Final Project Evaluation Page 1 ADJUSTING ENTRIES FOR THE QUARTER Using a copy of the December

PART 5. External Reporting and Performance Evaluation. Statements of financial performance and position. Statement of cash flows 19

PART 5 External Reporting and Performance Evaluation Statements of financial performance and position 18 Statement of cash flows 19 Analysis and interpretation of financial statements 20 CHAPTER 18 Statements

PART 5 External Reporting and Performance Evaluation Statements of financial performance and position 18 Statement of cash flows 19 Analysis and interpretation of financial statements 20 CHAPTER 18 Statements

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Course pack Accounting 202 Chapter 13: Cash Flow Statement

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

Course pack Accounting 202 Chapter 13: Cash Flow Statement Value Chapter Included 13 Purpose of Cash Flow Understand Operating, Investing, Financing activities Prepare a Cash Flow Statement indirect only

KYODO PRINTING CO., LTD. and Consolidated Subsidiaries

KYODO PRINTING CO., LTD. and Consolidated Subsidiaries Interim Consolidated Financial Statements (Unaudited) for the, Interim Consolidated Balance Sheets, as compared with March 31, (Unaudited) ASSETS,

KYODO PRINTING CO., LTD. and Consolidated Subsidiaries Interim Consolidated Financial Statements (Unaudited) for the, Interim Consolidated Balance Sheets, as compared with March 31, (Unaudited) ASSETS,

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

(2)Adoptions of simplified accounting methods and accounting methods particular to the presentation of quarterly financial statements: None

Adoptions of simplified accounting methods and accounting methods particular to the presentation of quarterly financial statements: None") Financial Statement for the Six Months Ended September 30, 2015 Name of listed company: Mipox Corporation Stock Code: 5381 (URL http://www.mipox.co.jp) Name and Title of Representative: Jun Watanabe, President

Financial Statement for the Six Months Ended September 30, 2015 Name of listed company: Mipox Corporation Stock Code: 5381 (URL http://www.mipox.co.jp) Name and Title of Representative: Jun Watanabe, President

Balance Sheet. 15.501/516 Accounting Spring 2004. Professor S.Roychowdhury. Sloan School of Management Massachusetts Institute of Technology

Balance Sheet 15.501/516 Accounting Spring 2004 Professor S.Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 09, 2003 1 Some residual administrative matters Access web

Balance Sheet 15.501/516 Accounting Spring 2004 Professor S.Roychowdhury Sloan School of Management Massachusetts Institute of Technology Feb 09, 2003 1 Some residual administrative matters Access web

Chapter 9, Problem 7 Closing inventory profits Before Tax After tax 40% tax

Chapter 9, Problem 7 Cost of 70% of Simon 900,000 Book value of Simon Common stock 550,000 Retained earnings Jan. 1 400,000 Net income to April 1 (¼ 200,000) 50,000 1,000,000 70% 700,000 Purchase discrepancy

Chapter 9, Problem 7 Cost of 70% of Simon 900,000 Book value of Simon Common stock 550,000 Retained earnings Jan. 1 400,000 Net income to April 1 (¼ 200,000) 50,000 1,000,000 70% 700,000 Purchase discrepancy

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

Summary of Consolidated Financial Results for the Six Months Ended September 30, 2013

November 6, 2013 Summary of Consolidated Financial Results for the Six Months Ended Name of Company Listed: Stock Exchange Listings: Nippon Paper Industries Co., Ltd. Tokyo Code Number: 3863 URL: Representative:

November 6, 2013 Summary of Consolidated Financial Results for the Six Months Ended Name of Company Listed: Stock Exchange Listings: Nippon Paper Industries Co., Ltd. Tokyo Code Number: 3863 URL: Representative:

Accounting, CPT Chapter 6 CA PRATHAP SS

Accounting, CPT Chapter 6 CA PRATHAP SS INTRODUCTION Preparation of Final Accounts is the last phase of the Accounting Process. INTRODUCTION The process of accounting starts from Transaction then entered

Accounting, CPT Chapter 6 CA PRATHAP SS INTRODUCTION Preparation of Final Accounts is the last phase of the Accounting Process. INTRODUCTION The process of accounting starts from Transaction then entered

University of Waterloo Final Examination. Term: Fall Year: 2005. Core Concepts of Accounting Information

University of Waterloo Final Examination Term: Fall Year: 2005 Student Name Solution UW Student ID Number Course Abbreviation and Number AFM 101 Course Title Core Concepts of Accounting Information Section(s)

University of Waterloo Final Examination Term: Fall Year: 2005 Student Name Solution UW Student ID Number Course Abbreviation and Number AFM 101 Course Title Core Concepts of Accounting Information Section(s)

Consolidated Financial Statements 2009

Consolidated Financial Statements 2009 (April 1, 2009 - March 31, 2010) Senkon Logistics Co., Ltd. CONSOLIDATED BALANCE SHEET ASSETS (As of March 31,2009) (As of March 31,2010) Current assets Cash and

Consolidated Financial Statements 2009 (April 1, 2009 - March 31, 2010) Senkon Logistics Co., Ltd. CONSOLIDATED BALANCE SHEET ASSETS (As of March 31,2009) (As of March 31,2010) Current assets Cash and

MASTER BUDGET - EXAMPLE

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

MASTER BUDGET - EXAMPLE Sales IN UNITS for the previous two months (of last quarter), as well as the sales forecast for next quarter are as follows: Sales Budget Units May sales (ACTUAL) 20 June sales

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

PART 1. BASIC CONCEPTS AND ACCOUNTING MODEL

CHAPTER 1 PART 1. BASIC CONCEPTS AND ACCOUNTING MODEL OBJECTIVES The objectives of this part are: To introduce a definition of accounting, the need for accounting information, and the various accounting

CHAPTER 1 PART 1. BASIC CONCEPTS AND ACCOUNTING MODEL OBJECTIVES The objectives of this part are: To introduce a definition of accounting, the need for accounting information, and the various accounting

Accounting Is a Language. Financial Accounting: The Balance Sheet BALANCE SHEET. Accounting Information. Assets. Balance Sheet: Layout

Accounting Is a Language Financial Accounting: The Balance Sheet Richard S. Barr Purpose: providing information Financial Statements Summarize accounting information Examples We need to know what the numbers

Accounting Is a Language Financial Accounting: The Balance Sheet Richard S. Barr Purpose: providing information Financial Statements Summarize accounting information Examples We need to know what the numbers

Chapter 13 Financial Statements and Closing Procedures

Chapter 13 - Financial Statements and Closing Procedures Chapter 13 Financial Statements and Closing Procedures TEACHING OBJECTIVES 13-1) Prepare a classified income statement from the worksheet. 13-2)

Chapter 13 - Financial Statements and Closing Procedures Chapter 13 Financial Statements and Closing Procedures TEACHING OBJECTIVES 13-1) Prepare a classified income statement from the worksheet. 13-2)

Long Island University C.W. Post GBA 521. Final Exam - review

Long Island University C.W. Post GBA 521 Name: _ (Last name) (First name) Date: _ Final Exam - review Multiple Choice Following are 14 multiple choice questions, worth 3 points each. Clearly identify the

Long Island University C.W. Post GBA 521 Name: _ (Last name) (First name) Date: _ Final Exam - review Multiple Choice Following are 14 multiple choice questions, worth 3 points each. Clearly identify the

Examination: 11052 Financial Accounting Summer Term 2008 Examiner: Prof. Dr. Barbara Schöndube-Pirchegger Examination questions: 3

Examination: 11052 Financial Accounting Summer Term 2008 Examiner: Prof. Barbara Schöndube-Pirchegger Examination questions: 3 Name: Matriculation number: The following aids can be used: a calculator in

Examination: 11052 Financial Accounting Summer Term 2008 Examiner: Prof. Barbara Schöndube-Pirchegger Examination questions: 3 Name: Matriculation number: The following aids can be used: a calculator in

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Total shares at the end of ten years is 100*(1+5%) 10 =162.9.

10 =162.9.") FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

Glossary of Accounting Terms Peter Baskerville

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

ZAMIL INDUSTRIAL INVESTMENT COMPANY (SAUDI JOINT STOCK COMPANY)

") ZAMIL INDUSTRIAL INVESTMENT COMPANY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS REPORT (LIMITED REVIEW) FOR THE THREE MONTHS AND NINE MONTHS PERIODS ENDED SEPTEMBER 30, NOTES TO THE INTERIM

ZAMIL INDUSTRIAL INVESTMENT COMPANY INTERIM CONSOLIDATED FINANCIAL STATEMENTS AND AUDITORS REPORT (LIMITED REVIEW) FOR THE THREE MONTHS AND NINE MONTHS PERIODS ENDED SEPTEMBER 30, NOTES TO THE INTERIM

Vol. 1, Chapter 5 The Balance Sheet

Vol. 1, Chapter 5 The Balance Sheet Problem 1: Solution Assets Construction in progress Cash advance to affiliated co. Petty cash Trade receivables Building Cash surrender value of life insurance Notes

Vol. 1, Chapter 5 The Balance Sheet Problem 1: Solution Assets Construction in progress Cash advance to affiliated co. Petty cash Trade receivables Building Cash surrender value of life insurance Notes

Consolidated and Non-Consolidated Financial Statements

May 13, 2016 Consolidated and Non-Consolidated Financial Statements (For the Period from April 1, 2015 to March 31, 2016) 1. Summary of Operating Results (Consolidated) (April 1,

May 13, 2016 Consolidated and Non-Consolidated Financial Statements (For the Period from April 1, 2015 to March 31, 2016) 1. Summary of Operating Results (Consolidated) (April 1,

2. The balance in a deferred revenue account represents an amount that is Earned Collected a. Yes Yes b. Yes No c. No Yes d. No No.

Multiple choice (36%, 2%each): 1. Failure to record the expired amount of prepaid rent expense would not a. understate expense. b. overstate net income. c. overstate owners' equity. d. understate liabilities.

Multiple choice (36%, 2%each): 1. Failure to record the expired amount of prepaid rent expense would not a. understate expense. b. overstate net income. c. overstate owners' equity. d. understate liabilities.

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital