Injury Prevention. Loss Control. Compliance.

|

|

|

- Isabella Campbell

- 8 years ago

- Views:

Transcription

1 Injury Prevention. Loss Control. Compliance. GDI Your Workers Compensation Partner Our agency can deliver the strategies, tools and resources that will help you manage and understand common workers compensation issues and concerns. Our Tools for Success Our agency can help you build solid loss control and safety programs to help you stay on top of your biggest risk management and compliance challenges. Statutes for Your State We can provide you with the most important workers compensation information for your state. Most statutes change annually based on inflation, and we stay on top of these changes for you. Controlling Your MOD We have informational documents to assist you in understsanding and controlling your MOD. Safety Programs and Policies Your industry has risks and we have the programs and policies that outline how to control those safety risks to keep your employees injury-free on the job. Fight Fraud Workers compensation fraud is commonplace. We can instruct you on how to prevent fraud in your workplace. Workers Compensation Made Simple Understanding workers compensation and how employees may be eligible can be confusing. Educate your employees with our easy-to-understand resources. Stay Virtually Connected We deliver documents on command and have OSHA recordkeeping capabilities, all from the convenience of your unique Web-based client portal. These tools allow you to access and share valuable resources, including employee newsletters, industry resources and connecting to peers in your industry. Grant Davis GDI Insurance Agency, Inc. 801 Geer Road Turlock, CA Phone Web site

2 Table of Contents TOP 10 WAYS TO CONTROL YOUR MOD... 3 UNDERSTANDING YOUR WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR WORKERS COMPENSATION FRAUD: 15 WARNING SIGNS... 6 FIGHTING WC FRAUD IN THE WORKPLACE... 7 FINANCIAL IMPACT OF WORKERS COMPENSATION INJURIES PRESENTATION ACCIDENT COSTS, TIP OF THE ICEBERG FINANCIAL IMPACT OF INDIRECT CLAIMS COSTS SAFETY BUDGET WORKSHEET SAFETY PROGRAMS AND THE IMPACT TO YOUR BOTTOM LINE WORKERS COMPENSATION: HURT ON THE JOB? QUICK GUIDE TO WORKERS COMPENSATION PAYROLL STUFFER WORKERS COMPENSATION AUDIT CHECKLIST

3 Top 10 Ways to Control Your Mod Your experience modification factor, or mod, is an important component used in calculating your workers compensation premium. If you can control your mod, you can control your price so we ve gathered some top tips designed to positively impact your bottom line. 1. Investigate accidents immediately and thoroughly. Take corrective action to eliminate hazards. Be aware of fraud. 2. Report all claims to carrier immediately. Alert carrier to any serious, potentially serious, or suspect claims. Frequently monitor the status of the claim and communicate with the adjuster to resolve as quickly as possible. 3. Take an aggressive approach to providing light duty to all injured employees upon their release from treatment. Supervise light duty employees to assure their conformance with restrictions 4. In serious cases that involve lost time, communicate with the claims adjuster so that they recognize your interest in returning the injured employee back to gainful employment. 5. Set safety performance goals for persons with supervisory responsibility. Success in achieving safety goals should be used as one measure during performance appraisals. 6. Develop a written safety program and train employees in their responsibilities for safety. Incorporate a disciplinary policy into the program, one that holds employees accountable for breaking the rules or rewards them for correctly following safety procedures. 7. Frequently communicate with employees, on a formal and informal basis, regarding the importance of safety. 8. Make safety a priority. Senior management must be visible in the safety effort and must support improvement. 9. Evaluate accident history and near-misses at least monthly. Look for trends in experience and take corrective action on worst problems first, as soon as the problems manifest themselves. 10. Hire us to ensure success! For more information, contact your broker representative. 3

4 Coverage Insights Understanding Your Workers Compensation Experience Modification Factor The key to calculating a workers compensation premium is the experience modification factor, also known as your mod. Understanding your company s mod and the data used to obtain it provides you with the information necessary to determine how to keep your workers compensation premium under control. Who calculates the mod factor? Most states use the National Council on Compensation Insurance (NCCI) to collect data and calculate the experience modification factor. NCCI is a private corporation funded by member insurance companies. However, the following states have their own governmentrun rating bureaus that are separate from the NCCI: California, Delaware, Indiana, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Carolina, Pennsylvania, Texas and Wisconsin. How is a mod calculated? Calculating the experience modification factor is complex, but the underlying theory and purpose of the formula is straightforward. Your company s actual losses are compared to its expected losses by industry type. The formula incorporates factors that take into account company size, unexpected large losses and the difference between loss frequency and loss severity to achieve a balance between fairness and accountability. How does my mod affect my premiums? The mod factor represents either a credit or debit that is applied to your workers compensation premium. A mod factor greater than 1.0 is a debit mod, which means that losses are worse than expected and a surcharge will be added to your premium. A mod factor less than 1.0 is a credit mod, which means the losses are better than expected, resulting in a discounted premium. What is the experience rating period? The mod is calculated using loss and payroll data for an experience rating period. The experience rating period typically includes data for three policy years, excluding the most recently completed year. For example, for a mod factor calculated on January 1, 2010, data would be used for the January 1, , January 1, and January 1, policy periods. The data for the January 1, would be excluded. Time period used in Workers Compensation Experience Rating Experience Rating Period Data Excluded Rating Year 1/1/2006 1/1/2007 1/1/2008 1/1/2009 1/1/2010 Claims Costs For Each Policy Period Mod Calculated Mod Applied Payroll data by state and class code Three years of data is used to provide a more accurate reflection of the losses, smoothing out the impact of any bad or good year of losses. 4

5 The actual loss data is separated into primary and excess pools. Primary losses, which are the first $5,000 of every loss, measure frequency. Excess losses or amounts more than $5,000 measure severity. The formula penalizes loss frequency by including all loss amounts in the calculation. The reason for this is that these types of claims can be controlled through proactive loss control programs. Losses in excess of $5,000 are capped at levels that vary by state. This minimizes the impact that any single claim can have on your premium. In approved states, medical-only claims figures are reduced by 70 percent. Expected losses are then calculated by using your payroll data by state and class code, and applying the Expected Loss Ratio (ELR). The ELR is provided by each state rating bureau. These figures are also broken down into expected primary losses and expected excess losses. How do your losses compare? The final mod calculation compares your actual primary and excess loss figures to those expected for a company of the same size and industry type. To understand how workers compensation losses to your business compare to state industry averages, contact GDI Insurance Agency, Inc. to review your experience modification worksheet. How can you control your mod? Your mod factor has a direct impact on your workers compensation premium. The key to controlling your insurance costs is through accident prevention. - The mod is calculated based on data reported to the rating bureau by past insurers. Incorrect or incomplete data can cause incorrect mod factors. Review the loss and payroll data to make sure the calculation is complete and accurate. - Losses remain in the experience rating formula for three years. The experience modification factor is influenced more by small, frequent losses than by large, infrequent ones. - Develop a sound safety program, return to work program and prevention procedures to reduce loss frequency. - An effective self-inspection and accident investigation program are critical to managing claim frequency. - Implement an active claims management program to manage outstanding reserves and focus on efficiently resolving open claims. - Report all claims to your carrier immediately. - Take an aggressive approach to providing light duty to all injured employees upon their release from treatment. - Set safety performance goals for supervisory roles. Success in achieving safety goals should be used as one measure during performance appraisals. - Train employees on their responsibilities for safety, and enforce conformance with these responsibilities. - Frequently communicate with employees, on a formal and informal basis, regarding the importance of safety. How can your experience rating save you money? Establishing a proactive safety program is an effective way to reduce losses, which impacts your mod and workers compensation premium. Contact us today. We have the loss control experience to help you advance safety and control your workers compensation premium. This Coverage Insights is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional for appropriate advice. Photography Outdoor Office V154 Getty Images, Inc. Source: Insurance Information Institute. Reprinted with permission. 5

6 Workers Compensation Fraud 15 Warning Signs The WC (workers' compensation) insurance system is a no-fault method of paying workers for medical expenses and wage losses due to on-the-job injuries. While the majority of WC claims are truthful, the National Insurance Crime Bureau reports that billions of dollars of false claims are submitted each year. To help you detect possible WC fraud, experience shows a claim may be fraudulent if two or more of the following factors are present: 1. Monday Morning: The alleged injury occurs either first thing Monday morning, or late on a Friday afternoon but not reported until Monday. 2. Employment Change: The reported accident occurs immediately before or after a strike, a layoff, the end of a big project, or at the conclusion of seasonal work. 3. Job Termination: If an employee files a post-termination claim: Was the alleged injury reported by the employee prior to termination? Did the employee exhaust their unemployment benefits prior to claiming workers compensation benefits? 4. History of Changes: The claimant has a history of frequently changing physicians, addresses and places of employment. 5. Medical History: The employee has a pre-existing medical condition that is similar to the alleged work injury. 6. No Witnesses: The accident has no witnesses, and the employee's own description does not logically support the cause of injury. 7. Conflicting Descriptions: The employee's description of the accident conflicts with the medical history or First Report of Injury. 8. History of Claims: The claimant has a history of numerous suspicious or litigated claims. 9. Treatment is Refused: The claimant refuses a diagnostic procedure to confirm the nature or extent of an injury. 10. Late Reporting: The employee delays reporting the claim without a reasonable explanation. 11. Hard to Reach: You have difficulty contacting a claimant at home, when they are allegedly disabled. 12. Moonlighting: Does the employee have another paying job or do volunteer work? 13. Unusual Coincidence: There is an unusual coincidence between the employee s alleged date of injury and their need for personal time off. 14. Financial Problems: The employee has tried to borrow money from co-workers or the company, or requested pay advances. 15. Hobbies: The employee has a hobby that could cause an injury similar to the alleged work injury. Remember, these warning signs are simply indicators. If you are suspicious of a claim, alert your Insurance Carrier. 6

7 Fighting WC Fraud in the Workplace According to OSHA, companies that treat their workers fairly and with concern have the fewest job injuries and fraudulent WC (workers compensation) claims. As a supervisor, here are the top 10 proactive things you can do to fight WC fraud in the workplace. 1. Educate your employees. Employees should understand both their rights concerning legitimate WC claims and the penalties for fraudulent ones. Hold a safety meeting on the topic, and use posters, flyers and payroll stuffers to advance your fraud message. And don t be afraid to promote your tough stance against fraud by informing employees that all suspicious claims will be investigated and prosecuted. 2. Maintain a safe work environment. Initiate a formal Safety or Injury Prevention Program to minimize safety hazards. 3. Implement a Return to Work program. Experience shows that injured workers recover faster when they return to work. Returning to regular work usually occurs more quickly when transitional or modified duty is offered to the injured employee. 4. Keep in touch. Employees who feel valued are less likely to cheat the system. Keep in touch with an injured employee and make it clear you re looking forward to having them back at work as soon as they have their doctor s approval. 5. Partner with a reputable medical provider. Partner with a reputable medical clinic to serve as your company s primary provider to ensure workplace injuries are treated by a trustworthy physician. 6. Establish reporting procedures. Employees and supervisors should be familiar with reporting procedures, and keep accident forms on hand. Also, stress the importance of reporting injuries promptly. 7. Investigate immediately. If an accident occurs, investigate the accident while memories are still fresh. Separately talk to each witness and co-worker about the injury. Be sure to relay any suspicions about the incident to your claims adjuster. 8. Conduct exit interviews. You should document the work-related activities of employees who are about to be laid off or fired. Conduct exit interviews that include questions about the employee s physical condition and any on-the-job accidents or injuries that have not been reported. This may help to deter fraudulent claims or refute future false claims. 9. Be cautious. Fraud is a serious accusation that if not handled properly could put you in the middle of a lawsuit for libel or slander. Give your company the added protection by working with your claims carrier to validate your suspicions, and to determine if the incident should be reported to the appropriate authorities. 10. Be honest. Honesty works both ways. Don t knowingly provide false or misleading information with regard to entitlement to WC benefits in order to discourage an injured worker from pursuing a claim. 7 Fraud hits you where it hurts: your bottom line. Learn the top 10 things you can do to fight workers compensation fraud in the workplace. This flyer is for general informational purposes only, and is not intended as medical or legal advice. Photography Building Supply V130 Getty Images, Inc. Content Zywave, Inc. All rights reserved.

8 8

9 9

10 10

11 11

12 Safety Budget Worksheet From To 1. Supervisor/manager -Training, Continuing Ed/Development $0.00 -Special courses or seminars $ Employee training Rate Hours -Formal safety training $ $0 -Toolbox talks $ $0 3. Safety Committee Number of EE's Rate Hours -Employee time 0 $ $0.00 -Management $ $0.00 -Outside resource $ $0.00 -Training $ $ New Hire Orientation Number of New Hires Rate Hours -Employee time 0 $ $0.00 -Management $ $0.00 -Outside resource $ $ Safety Coordinator -Full Time/Part Time Compensation & Benefits $0.00 -Travel $0.00 -Subscriptions and membership fees $ Safety Coordinator $ Personal Protective Equipment Number of EE's Cost/Equipment/EE -New Equipment 0 $0.00 $0.00 -Replacement Orders 0 $0.00 $

13 8. First Aid Supplies Number of Kits Cost -Full Kits 0 $0.00 $0.00 -Replacement Orders 0 $0.00 $ Physicals, Audiograms, Post injury drug tests -Audiogram Equipment $ Personnel time to conduct audiogram $ $ Post Injury Drug Testing Fees $ $ Facility Capital Improvements for Safety -Fire protection and utilities $0.00 -Building renovations/additions $0.00 -New equipment purchase $ Maintenance and repair - existing equipment/facility -Equipment $0.00 -Building $ Outside consulting and inspection services $0.00 TOTAL $0.00 Prepared by: 13

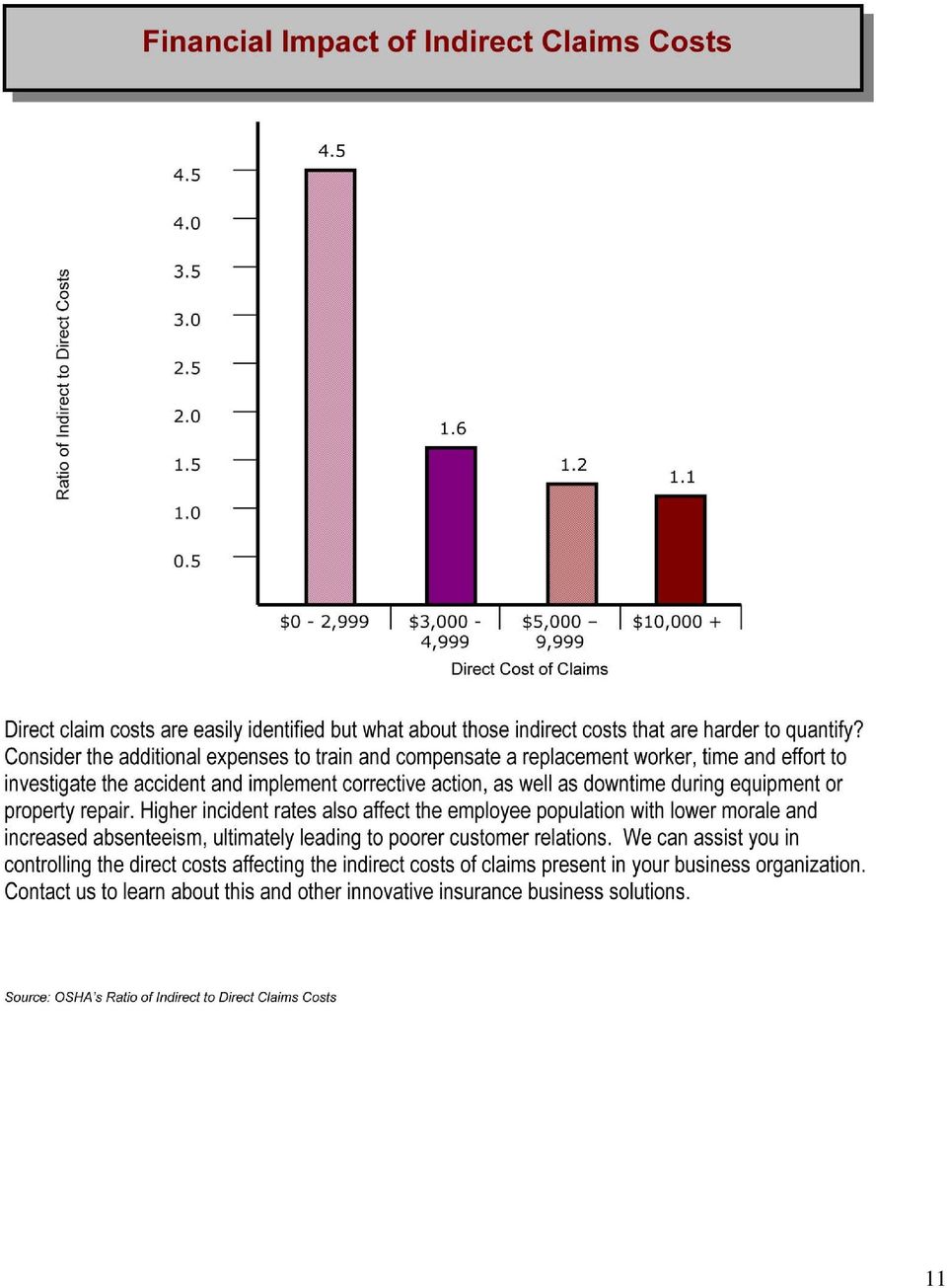

14 Risk Insights Safety Programs and the Impact to Your Bottom Line If you could save your company money, improve productivity and increase employee morale, would you? According to the Occupational Safety and Health Administration (OSHA), workplaces that establish safety and health management systems can reduce their injury and illness costs by 20 to 40 percent. Safe environments also improve employee morale, which positively impacts productivity and service. When it comes to the costs associated with safety, consider the following statistics from OSHA: It is estimated that employers pay almost $1 billion per week for direct workers compensation costs alone; this comes straight out of company profits. Injuries and illnesses increase workers compensation and retraining costs. Lost productivity from injuries and illnesses costs companies roughly $63 billion each year. In today s business environment, these safety-related costs can be the difference between reporting a profit or a loss. Measuring the Cost of Safety Demonstrating the value of safety to management is often a challenge because the return on investment (ROI) can be cumbersome to measure. Your goal in measuring safety is to balance your investment vs. the return expected. Where do you begin? According to the International Risk Management Institute s (IRMI), there are many different approaches to measuring the cost of safety, depending on your goal. Defining your goal helps you to determine what costs to track and how complex your tracking will be. For example, you may want to capture certain data simply to determine what costs to build into the price of a product or service, or you may want to track your company s total cost of safety to show increased profitability, which would include more specific data collection like safety wages and benefits, operational costs (such as safety training expenses), insurance costs, etc. Since measuring can be time consuming, general cost formulas are available. A Stanford study conducted by Levitt and Samuelson places safety costs at two and a half percent of costs, and a study published by The Economist Intelligence Unit (EIU) estimates general safety costs at about eight percent of payroll. If it s important for your organization to measure safety as it relates to profitability, more accurate tracking should be done. For measuring data, safety costs can be divided into two categories: 1. Direct or hard costs, which include: - Safety wages - Operational costs - Insurance premiums and/or attorney s fees - Accidents and incidents - Fines and/or penalties 2. Indirect or soft costs, which go beyond those recorded on paper, such as: - Accident investigation - Repairing damaged property - Administrative expenses - Worker stress in the aftermath of an accident resulting in lost productivity, low employee morale and increased absenteeism 14

15 - Training and compensating replacement workers - Developing a poor reputation, which translates to difficulty in attracting skilled workers, losing business share, etc. When calculating soft costs, minor accidents are considered to be about four times greater than direct costs, and serious accidents about 10 to 15 times greater, especially if the accident generates OSHA fines and/or litigation costs. Considering the statistics, safety experts believe that there is direct correlation between safety and a company s profit. We are committed to helping you establish a strong safety, health and environmental program that protects both your workers and your bottom line. Contact us today at to learn more about our value-added services. According to IRMI, just the act of measuring costs will drive improvement. In theory, those providing the data become more aware of the costs and begin managing them. This supports the common business belief that what gets measured gets managed. And, as costs go down, what gets rewarded gets repeated. How Can You Show ROI? OSHA studies indicate that for every $1 invested in effective safety programs, $4 to $6 may be saved as illnesses, injuries and fatalities decline. With a good safety program in place, your costs will naturally decrease. It is important to determine what costs to measure to establish benchmarks, which can then be used to demonstrate the value of safety over time. Also, keep in mind, your total cost of safety is just one part of managing your total cost of risk. When safety is managed and monitored, it can also help drive down your total cost of risk. Safety as a Core Business Strategy Industry studies report that companies who focus on safety as a core business strategy come out ahead. Consider the following as reported in Return on Investment (ROI) for Safety, Health and Environmental (SH&E) Management Programs, by the American Society of Safety Engineers: - A coal mining company in West Virginia reduced its workers compensation rate of $1.28 per $100 payroll vs. its competitor s rate of $ Implementation of an OSHA consultation program reduced losses at a forklift manufacturing operation from $70,000 to $7,000 per year. - A fall protection program implementation reduced one employer s accident costs by 96 percent -- from $4.25 to $0.18 per person-hour. - Implementation of an improved safety and health program reduced Service master s workers compensation costs by $2.4 million over a two-year period. 15

16 Safety and health tips for your work, home and life brought to you by the insurance and safety specialists. Workers Compensation: Hurt on the Job? Put these FAQs to work for you Workers compensation benefits are available to employees who are unable to work as a result of either a work-related accident or illness. If you are injured on the job and medically authorized to take time off from work, you will be reimbursed for lost wages (typically a percentage of your regular wages) and all medical expenses related to your treatment and rehabilitation. When should I report an accident? If you are injured, notify your supervisor immediately to file a report. This will initiate the process for receiving workers compensation benefits. How will I be reimbursed? Lost time compensation is payable during the time period in which you are authorized by your treating doctor to be off from work. [EMPLOYERS: MANUALLY ENTER WC INFO HERE] What is an independent medical exam (IME)? An IME is an exam by a medical professional other than the doctor who conducted your initial exam. An insurance carrier or employer is entitled to require an IME to confirm the original physician s diagnosis and treatment plan. What happens if I do not comply with my treatment plan? Non-compliance with recommended medical treatment, therapy, or returnto-work plans may jeopardize your workers compensation benefits. How are disputes handled? Workers, employers, and insurance carriers are permitted to file an application for a hearing to resolve If injured on the job... disputes. Legal disputes can be settled by stipulation, arbitration, or proceeding with the formal hearing. When should I return to work? You, your doctor, and your employer will coordinate a return-to-work plan that helps you return to your regular job or a modified duty position as quickly as possible. Notify your supervisor immediately. A late accident report could adversely affect the health and workers compensation you receive. This flyer is for informational purposes only. Photography Getty Images, Inc. All rights reserved. Content Zywave, Inc. 16

17 Quick Guide to Workers Compensation Benefits are payable to employees who sustain a work-related injury or illness. Prompt reporting of all accidents will prevent delays in receiving benefits. Coverage includes: Payment of medical bills associated with the work-related injury Reimbursement of costs for prescription medication Lost time compensation payable at [ENTER STATE- SPECIFIC %] of average weekly wage Contact your supervisor or HR department for more information. Quick Guide to Workers Compensation Benefits are payable to employees who sustain a work-related injury or illness. Prompt reporting of all accidents will prevent delays in receiving benefits. Coverage includes: Payment of medical bills associated with the work-related injury Reimbursement of costs for prescription medication Lost time compensation payable at [ENTER STATE- SPECIFIC %] of average weekly wage Contact your supervisor or HR department for more information. Quick Guide to Workers Compensation Benefits are payable to employees who sustain a work-related injury or illness. Prompt reporting of all accidents will prevent delays in receiving benefits. Coverage includes: Payment of medical bills associated with the work-related injury Reimbursement of costs for prescription medication Lost time compensation payable at [ENTER STATE- SPECIFIC %] of average weekly wage Contact your supervisor or HR department for more information. 17

18 WORKERS COMPENSATION AUDIT CHECKLIST Unlike the estimated premium originally used to calculate your workers compensation insurance premium, an annual premium audit determines the accurate costs for the policy period. There can be vast differences between the estimated and actual premiums, so the audit process is extremely important. To bypass audit errors that tend to inflate workers compensation premiums, utilize this checklist. BEFORE THE AUDITOR ARRIVES: Set up an appointment with the auditor and obtain a name and phone number in case you need to change your appointment. If you do need to cancel and reschedule, do so promptly. Assign an employee as the auditor s primary contact person. This individual should be familiar with all of the company s departments and employees. This individual should have knowledge of the payroll records that the auditor will be examining. The contact person should review the prior year s billing statements and auditor s worksheets (if requested in the past) to understand the issues that may arise again. Make sure that your records document the actual gross payroll spent by each employee in different workplace exposures if employees are involved in a variety of operations. Do not estimate payroll. Gross payroll should be provided with monthly and quarterly or year-to-date totals by employee and department. The type of work performed and the job duties by each person must be shown. This includes officers, members, sole proprietors and partners. If your records do not break down payroll by different workplace exposures, the auditor will classify it under the most expensive classification applicable. Consolidate the payroll verification records including 941's, 940, W-3, Unemployment Tax Reports or Schedule C. You may also want to assist the auditor by highlighting pre-tax wages that will be subject to premium. Have workers compensation documentation including certificates of insurance for 1099 independent or subcontractors showing that they have their own insurance (if applicable). If you do not have this information, get it before the auditor arrives. Otherwise, the auditor will charge your company the premium charge for this exposure. Review payroll documents to highlight overtime pay for the auditor so he/she can discount it back to normal pay (allowed in most states workers compensation rules). The auditor does not have the time to perform the premium portion of your overtime pay, so records should be easily readable so he/she can do their job efficiently. 18

19 Review the classification codes assigned to your job contacts. Some individual jobs may be subject to different codes. If the auditor cannot locate this information, he/she will need to review your invoices. WHEN THE AUDITOR ARRIVES: Give the auditor a well-lit, comfortable place to do his/her work, preferably onsite. If you must conduct the audit offsite, make sure your contact person is available for questions. Provide payroll records (as mentioned previously), which include payroll tax records (state and federal), your cash disbursement journal/checkbook, job contacts and general ledger. Once the audit is complete, ask for a copy of the auditor s worksheets. This document is not normally provided but will be upon request. These documents provide you with information concerning how the audit was conducted, how payroll numbers were derived and what codes were used. Designate someone from the company to receive the audit worksheets, as it contains confidential payroll information. AFTER THE AUDIT PROCESS: Review the audit billing statement carefully and compare that document to your original policy. Balance the total audited payroll figures to the documentation provided. Check for any significant changes between the total payroll shown on the policy and the actual figures provided. Compare the payroll by classification code on the policy to that on the audit. The payroll by classification codes shown on the audit should not contain any significant fluctuations in comparison to the policy. Compare the experience modification factor on the original policy to the one shown on the audit. Make sure the auditor applied the factor for the audited period. Review the rates charged for each classification code. There should be no significant changes between the rates on the audit versus the original rates on the policy. There should be no changes to the Schedule Credit or Debit from the original policy. Contact the auditor to discuss any questions that arise or make any necessary revisions. 19

, which include payroll tax records (state and federal), your cash disbursement journal/checkbook, job contacts and general ledger.")

Corporate Consulting Services, Ltd. Workers Compensation in Today s Environment

Corporate Consulting Services, Ltd. Workers Compensation in Today s Environment 2014 Corporate 2014 Corporate Consulting Consulting Services, Services, Ltd. Ltd. Forces Impacting Workers Compensation Today

Corporate Consulting Services, Ltd. Workers Compensation in Today s Environment 2014 Corporate 2014 Corporate Consulting Consulting Services, Services, Ltd. Ltd. Forces Impacting Workers Compensation Today

Fraud. Baldomero Gonzalez. Our reputation for excellence is no accident. TM

Fraud Baldomero Gonzalez Workers Compensation Fraud It is estimated that ten percent of all claims, nearly $31 billion dollars, is paid annually in fraudulent workers compensation claims. Workers compensation

Fraud Baldomero Gonzalez Workers Compensation Fraud It is estimated that ten percent of all claims, nearly $31 billion dollars, is paid annually in fraudulent workers compensation claims. Workers compensation

Workers Compensation Claim Fraud

Workers Compensation Claim Fraud Small businesses don t have to be insurance experts to realize the many potential benefits associated with taking a strategic approach to workers compensation and risk

Workers Compensation Claim Fraud Small businesses don t have to be insurance experts to realize the many potential benefits associated with taking a strategic approach to workers compensation and risk

Quick Guide to Workers Compensation

Quick Guide to Workers Compensation What Is Workers Compensation Insurance? Workers compensation insurance covers businesses for their statutory and legal obligations for employee expenses that are a direct

Quick Guide to Workers Compensation What Is Workers Compensation Insurance? Workers compensation insurance covers businesses for their statutory and legal obligations for employee expenses that are a direct

Quick Guide to Workers Compensation for Small Business

Quick Guide to Workers Compensation for Small Business Do I Need Workers Compensation Coverage? Generally speaking, businesses must obtain workers compensation coverage if they have employees that are

Quick Guide to Workers Compensation for Small Business Do I Need Workers Compensation Coverage? Generally speaking, businesses must obtain workers compensation coverage if they have employees that are

Workers Compensation Optimal Claims Management

OVERALL OBJECTIVE - ECM seeks to provide a consultative relationship in which we work with our clients to influence and improve their Risk Management Process. Following are a few suggestions regarding

OVERALL OBJECTIVE - ECM seeks to provide a consultative relationship in which we work with our clients to influence and improve their Risk Management Process. Following are a few suggestions regarding

Managing the Care and Return to Work of Injured Workers (and controlling your Workers Compensation Costs)

") Managing the Care and Return to Work of Injured Workers (and controlling your Workers Compensation Costs) This Guide was developed to provide you with valuable information regarding our managed care program,

Managing the Care and Return to Work of Injured Workers (and controlling your Workers Compensation Costs) This Guide was developed to provide you with valuable information regarding our managed care program,

Volunteer Return to Work

Volunteer Return to Work Volunteer Modified Duty Handbook Workers Compensation Fund toll-free: 1.800.446.2667 web: www.wcfgroup.com Although preventing injuries is the best way to control workers compensation

Volunteer Return to Work Volunteer Modified Duty Handbook Workers Compensation Fund toll-free: 1.800.446.2667 web: www.wcfgroup.com Although preventing injuries is the best way to control workers compensation

I ve been hurt at work. What do I do / to whom must I give notice of my accident and by what date?

WORKER: I ve been hurt at work. What do I do / to whom must I give notice of my accident and by what date? In general, you must give your employer or your supervisor written notice within 15 days after

WORKER: I ve been hurt at work. What do I do / to whom must I give notice of my accident and by what date? In general, you must give your employer or your supervisor written notice within 15 days after

STRATEGIES FOR MANAGING WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTORS

STRATEGIES FOR MANAGING WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTORS Introduction The National Council on Compensation Insurance (NCCI) recently announced its plan to modify how a company s Experience

STRATEGIES FOR MANAGING WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTORS Introduction The National Council on Compensation Insurance (NCCI) recently announced its plan to modify how a company s Experience

Workers Compensation Strategies That Will Positively Influence Your Bottom Line

GDI INSURANCE AGENCY, INC S MONEY-SAVING WORKERS COMPENSATION TIPS Workers Compensation Strategies That Will Positively Influence Your Bottom Line Provided by: GDI Insurance Agency, Inc. 801 Geer Road

GDI INSURANCE AGENCY, INC S MONEY-SAVING WORKERS COMPENSATION TIPS Workers Compensation Strategies That Will Positively Influence Your Bottom Line Provided by: GDI Insurance Agency, Inc. 801 Geer Road

Manage Your Experience Modification Rate

Dave Smith & Co Inc Manage Your Experience Modification Rate Average View Of Insurance Why the Ex Mod is a Poor Safety Measure and What you Can Do About It Actual What Is The EMR? Workers Compensation

Dave Smith & Co Inc Manage Your Experience Modification Rate Average View Of Insurance Why the Ex Mod is a Poor Safety Measure and What you Can Do About It Actual What Is The EMR? Workers Compensation

WORKERS COMPENSATION QUICK FACTS

The Workers' Compensation Handbook // 1 WORKERS COMPENSATION QUICK FACTS Workers Compensation Quick Facts contains general information about the workers compensation system in New Mexico, to provide employers

The Workers' Compensation Handbook // 1 WORKERS COMPENSATION QUICK FACTS Workers Compensation Quick Facts contains general information about the workers compensation system in New Mexico, to provide employers

AN EMPLOYER S GUIDE TO WORKERS COMPENSATION IN NEW JERSEY

AN EMPLOYER S GUIDE TO WORKERS COMPENSATION IN NEW JERSEY I. WHAT IS WORKERS COMPENSATION?... 2 II. WORKERS COMPENSATION BENEFITS... 3 III. INSURANCE REQUIREMENTS... 4 Types of Coverage Definition of Employee

AN EMPLOYER S GUIDE TO WORKERS COMPENSATION IN NEW JERSEY I. WHAT IS WORKERS COMPENSATION?... 2 II. WORKERS COMPENSATION BENEFITS... 3 III. INSURANCE REQUIREMENTS... 4 Types of Coverage Definition of Employee

Anne M. Noonan, Commissioner, Vermont Department of Labor WORKERS COMPENSATION FRAUD STUDY AND REPORT

Memorandum To: From: House Committee on Commerce and Economic Development; Senate Economic Development, Housing and General Affairs Anne M. Noonan, Commissioner, Vermont Department of Labor Date: 1/15/2015

Memorandum To: From: House Committee on Commerce and Economic Development; Senate Economic Development, Housing and General Affairs Anne M. Noonan, Commissioner, Vermont Department of Labor Date: 1/15/2015

Manage Your EMR: Why Ex Mods Are A Poor Safety Measurement And What You Can Do About It!

Dave Smith & Company Manage Your EMR: Why Ex Mods Are A Poor Safety Measurement And What You Can Do About It! The EMR (Workers Compensation Insurance Experience Modification Rating) continues to be used

Dave Smith & Company Manage Your EMR: Why Ex Mods Are A Poor Safety Measurement And What You Can Do About It! The EMR (Workers Compensation Insurance Experience Modification Rating) continues to be used

Workers Compensation Frequently Asked Questions

Workers Compensation Frequently Asked Questions Injured Workers Employers Adjusters/Attorneys/Insurers Vocational Rehabilitation Injured Workers What do I do if my employer has failed to file a claim?

Workers Compensation Frequently Asked Questions Injured Workers Employers Adjusters/Attorneys/Insurers Vocational Rehabilitation Injured Workers What do I do if my employer has failed to file a claim?

Sixty Best Practices In Sixty Minutes

Sixty Best Practices In Sixty Minutes Midwest Employers Casualty Company Jacque Jones, Regional Sales Vice President Anjie Severo, Client Services Account Manager Topics for Discussion What are Best Practices

Sixty Best Practices In Sixty Minutes Midwest Employers Casualty Company Jacque Jones, Regional Sales Vice President Anjie Severo, Client Services Account Manager Topics for Discussion What are Best Practices

Utah Labor Commission Industrial Accidents Division. Employers Guide to. Workers Compensation

2015 2016 Utah Labor Commission Industrial Accidents Division E m p l o y e r s G u i d e Employers Guide to Workers Compensation Utah Labor Commission Industrial Accidents Division Employers Guide to

2015 2016 Utah Labor Commission Industrial Accidents Division E m p l o y e r s G u i d e Employers Guide to Workers Compensation Utah Labor Commission Industrial Accidents Division Employers Guide to

EMPLOYER S GUIDE WORKERS COMPENSATION

EMPLOYER S GUIDE TO WORKERS COMPENSATION State of New Hampshire Department of Labor State Office Park South 95 Pleasant Street Concord, New Hampshire 03301 (603) 271-3176 INTRODUCTION This booklet has

EMPLOYER S GUIDE TO WORKERS COMPENSATION State of New Hampshire Department of Labor State Office Park South 95 Pleasant Street Concord, New Hampshire 03301 (603) 271-3176 INTRODUCTION This booklet has

WORKER S COMPENSATION TREATMENT AUTHORIZATION FORM

FLORIDA TECH EMPLOYEE ACCIDENT/ INJURY REPORT Contact Financial Affairs @ 674-7297 OR 8885 IMMEDIATELY regarding an Employee's Injury. Employee AND Supervisor must complete this report. EMPLOYEE INFORMATION

FLORIDA TECH EMPLOYEE ACCIDENT/ INJURY REPORT Contact Financial Affairs @ 674-7297 OR 8885 IMMEDIATELY regarding an Employee's Injury. Employee AND Supervisor must complete this report. EMPLOYEE INFORMATION

Texas Mutual Insurance Company. The Employer s Guide to Workers Comp

Texas Mutual Insurance Company The Employer s Guide to Workers Comp 2013-2014 Table of Contents n Workers Comp: What Is It, and Why Do You Need it? 1 n Legal protection for you 1 n Medical and income benefits

Texas Mutual Insurance Company The Employer s Guide to Workers Comp 2013-2014 Table of Contents n Workers Comp: What Is It, and Why Do You Need it? 1 n Legal protection for you 1 n Medical and income benefits

Workers Compensation. Are Costs Controllable?

Workers Compensation Are Costs Controllable? Your WC Risk Costs Has your WC premium gone down in recent years? Has your WC premium stayed the same? Has your WC premium gone up in recent years? Are you

Workers Compensation Are Costs Controllable? Your WC Risk Costs Has your WC premium gone down in recent years? Has your WC premium stayed the same? Has your WC premium gone up in recent years? Are you

Employer s Handbook. Workers Compensation

Employer s Handbook Workers Compensation Workers Compensation 101 Table of Contents Contact Information. 3 What is Workers Compensation?... 4-5 What is your role?... 6-7 Workers Compensation Benefits 8-9

Employer s Handbook Workers Compensation Workers Compensation 101 Table of Contents Contact Information. 3 What is Workers Compensation?... 4-5 What is your role?... 6-7 Workers Compensation Benefits 8-9

Benefits Guide. Information for the Injured Worker

Benefits Guide Information for the Injured Worker The purpose of this benefits guide is to help you learn what to expect if you ever need workers compensation benefits. Recovering from a work injury can

Benefits Guide Information for the Injured Worker The purpose of this benefits guide is to help you learn what to expect if you ever need workers compensation benefits. Recovering from a work injury can

WORKERS' COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS

WORKERS' COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION LOG NUMBER * INSURED

WORKERS' COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION LOG NUMBER * INSURED

An Injured Workers Guide to the Workers Compensation Process Table of Contents

An Injured Workers Guide to the Workers Compensation Process Table of Contents I. Claim Information A. General Information 1. What is workers compensation? 2. How do I know if I qualify for Workers Compensation?

An Injured Workers Guide to the Workers Compensation Process Table of Contents I. Claim Information A. General Information 1. What is workers compensation? 2. How do I know if I qualify for Workers Compensation?

Wisconsin Contractors Institute. Worker s Compensation Laws

Wisconsin Contractors Institute Worker s Compensation Laws For more information: Website: www.wicontractorsinstitute.com Email: questions@wicontractorsinstitute.com Phone: 262-293-6850 Chapter 5 - Wisconsin

Wisconsin Contractors Institute Worker s Compensation Laws For more information: Website: www.wicontractorsinstitute.com Email: questions@wicontractorsinstitute.com Phone: 262-293-6850 Chapter 5 - Wisconsin

SAFETY IN THE WORKPLACE By Sharon A. Stewart. January 28, 2005. The Occupational Safety and Health Act (OSHA) includes a General Duty Clause

includes a General Duty Clause") SAFETY IN THE WORKPLACE By Sharon A. Stewart January 28, 2005 The Occupational Safety and Health Act (OSHA) includes a General Duty Clause requiring employers to "furnish a place of employment which is

SAFETY IN THE WORKPLACE By Sharon A. Stewart January 28, 2005 The Occupational Safety and Health Act (OSHA) includes a General Duty Clause requiring employers to "furnish a place of employment which is

WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR. For All That Matters

WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR For All That Matters WHAT S A WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR? Your Work Comp Experience Modification Factor (E-Mod) is a primary

WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR For All That Matters WHAT S A WORKERS COMPENSATION EXPERIENCE MODIFICATION FACTOR? Your Work Comp Experience Modification Factor (E-Mod) is a primary

The Employers Guide to. Pennsylvania s Workers Compensation Law

The Employers Guide to Pennsylvania s Workers Compensation Law Table of Contents About this Guide. 3 The Pennsylvania Workers Compensation Act: An Overview for the Pennsylvania Employer....4 Your Duties

The Employers Guide to Pennsylvania s Workers Compensation Law Table of Contents About this Guide. 3 The Pennsylvania Workers Compensation Act: An Overview for the Pennsylvania Employer....4 Your Duties

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION LOG NUMBER * INSURED

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION LOG NUMBER * INSURED

WORKERS COMPENSATION CLAIM KIT. Workers Compensation That Works...With You and For You.

WORKERS COMPENSATION CLAIM KIT Workers Compensation That Works...With You and For You. CNA ASAP Now, One Phone Call, Fax or E-mail Can Get Results ASAP, 24 Hours a Day, Seven Days a Week Toll Free: 877-CNA-ASAP

WORKERS COMPENSATION CLAIM KIT Workers Compensation That Works...With You and For You. CNA ASAP Now, One Phone Call, Fax or E-mail Can Get Results ASAP, 24 Hours a Day, Seven Days a Week Toll Free: 877-CNA-ASAP

Employee Injury/Illness Reporting and Managed Return to Work. April 15, 2011 HR 23. Human Resources Responsible Key Business

Managed Return to Work Date Effective April 15, 2011 City Manager Revision Date Effective Code Number HR 23 Human Resources Responsible Key Business Objective: The City of Charlotte seeks to ensure the

Managed Return to Work Date Effective April 15, 2011 City Manager Revision Date Effective Code Number HR 23 Human Resources Responsible Key Business Objective: The City of Charlotte seeks to ensure the

Workers Compensation Policy and Procedure

EL PASO COUNTY DEPARTMENT OF HUMAN RESOURCES Workers Compensation Policy and Procedure Revised Date: March 21, 2016 I. Purpose The County of El Paso provides workers compensation benefits for incidental

EL PASO COUNTY DEPARTMENT OF HUMAN RESOURCES Workers Compensation Policy and Procedure Revised Date: March 21, 2016 I. Purpose The County of El Paso provides workers compensation benefits for incidental

Provided By Touchstone Consulting Group Workers Compensation Employer Penalties

Provided By Touchstone Consulting Group Workers Compensation Employer New Jersey s workers compensation laws determine the benefits available to employees who are injured in the course and scope of employment.

Provided By Touchstone Consulting Group Workers Compensation Employer New Jersey s workers compensation laws determine the benefits available to employees who are injured in the course and scope of employment.

Better Employee Management

Better Employee Management Eight Critical Areas for Small-Business Success This white paper is an overview of eight building blocks of an effective small-business HR program: payroll, employee communications,

Better Employee Management Eight Critical Areas for Small-Business Success This white paper is an overview of eight building blocks of an effective small-business HR program: payroll, employee communications,

Workers Compensation Program Review and Approval Authority

July 2003 Workers Compensation Program Review and Approval Authority Prepared and Edited by: Assistant Director Date UM Workers Compensation Manager Date Reviewed and Approved by: Chair - UM E, H & S Operations

July 2003 Workers Compensation Program Review and Approval Authority Prepared and Edited by: Assistant Director Date UM Workers Compensation Manager Date Reviewed and Approved by: Chair - UM E, H & S Operations

TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION

TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified per the signed attached quotation, to become effective on, at 12:01 AM

TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified per the signed attached quotation, to become effective on, at 12:01 AM

RISK CONTROL. Workers compensation best practices risk management guide. Risk Management Guide

Risk Management Guide RISK CONTROL REDUCE RISK. PREVENT LOSS. SAVE LIVES. Workers compensation costs are escalating rapidly. In fact, statistics reveal that the direct cost of work place injuries in 1999

Risk Management Guide RISK CONTROL REDUCE RISK. PREVENT LOSS. SAVE LIVES. Workers compensation costs are escalating rapidly. In fact, statistics reveal that the direct cost of work place injuries in 1999

An Employer s Guide. To Workers Compensation

An Employer s Guide To Workers Compensation March 2003 www.ndworkerscomp.com Dear Policyholder, North Dakota Workers Compensation (NDWC) is dedicated to providing an efficient, high-quality, and easy-to-use

An Employer s Guide To Workers Compensation March 2003 www.ndworkerscomp.com Dear Policyholder, North Dakota Workers Compensation (NDWC) is dedicated to providing an efficient, high-quality, and easy-to-use

Workers Compensation 101. Dave Young EMC Insurance Companies

Workers Compensation 101 Dave Young EMC Insurance Companies Outline I. Brief history of Workers Compensation Insurance II. What does Workers Compensation do? III. Calculation of the Workers Compensation

Workers Compensation 101 Dave Young EMC Insurance Companies Outline I. Brief history of Workers Compensation Insurance II. What does Workers Compensation do? III. Calculation of the Workers Compensation

The Insurance Coverage Law Information Center

The following article is from National Underwriter s latest online resource, FC&S Legal: The Insurance Coverage Law Information Center. The Insurance Coverage Law Information Center EXPERIENCE, EXPERTISE,

The following article is from National Underwriter s latest online resource, FC&S Legal: The Insurance Coverage Law Information Center. The Insurance Coverage Law Information Center EXPERIENCE, EXPERTISE,

Essex Insurance Company P.O. Box 22778, Oklahoma City, OK 73123 800.800.4007 Fax: 405.840.5432

PO Box 22778, Oklahoma City, OK 73123 8008004007 Fax: 4058405432 TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified per the

PO Box 22778, Oklahoma City, OK 73123 8008004007 Fax: 4058405432 TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified per the

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION CLAIM NUMBER * INSURED

WORKERS COMPENSATION - FIRST REPORT OF INJURY OR ILLNESS EMPLOYER (NAME & ADDRESS INCL ZIP) CARRIER / ADMINISTRATOR CLAIM NUMBER * REPORT PURPOSE CODE * JURISDICTION * JURISDICTION CLAIM NUMBER * INSURED

E-COMP, The National Workers Compensation Program. Workers Compensation Training, For the Employer

E-COMP, The National Workers Compensation Program Workers Compensation Training, For the Employer Introduction Workers compensation is a benefit mandated by laws in all 48 of the 50 states (Texas and New

E-COMP, The National Workers Compensation Program Workers Compensation Training, For the Employer Introduction Workers compensation is a benefit mandated by laws in all 48 of the 50 states (Texas and New

BUDGET & FISCAL AFFAIRS COMMITTEE

BUDGET & FISCAL AFFAIRS COMMITTEE WORKERS COMPENSATION PROGRAM COMPLIANCE REQUIREMENTS DIRECTOR, OMAR C. REID April 30, 2013 Workers Compensation Fraud Overview Our Philosophy Common Types of Fraud Employee

BUDGET & FISCAL AFFAIRS COMMITTEE WORKERS COMPENSATION PROGRAM COMPLIANCE REQUIREMENTS DIRECTOR, OMAR C. REID April 30, 2013 Workers Compensation Fraud Overview Our Philosophy Common Types of Fraud Employee

Essex Insurance Company P.O. Box 22778, Oklahoma City, OK 73123 Phone: 800.800.4007 Fax: 405.840.5432

P.O. Box 22778, Oklahoma City, OK 73123 Phone: 800.800.4007 Fax: 405.840.5432 TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified

P.O. Box 22778, Oklahoma City, OK 73123 Phone: 800.800.4007 Fax: 405.840.5432 TEXAS NON-SUBSCRIBER OCCUPATIONAL ACCIDENT INSURANCE POLICY APPLICATION Application is hereby made for coverage (s), as specified

An Analysis of Workers Compensation Outreach Materials. to combat insurance fraud

An Analysis of Workers Compensation Outreach Materials to combat insurance fraud April 1999 I N T R O D U C T I O N In 1997 the coalition s Workers Compensation Task Force made a series of recommendations

An Analysis of Workers Compensation Outreach Materials to combat insurance fraud April 1999 I N T R O D U C T I O N In 1997 the coalition s Workers Compensation Task Force made a series of recommendations

Claims Management. Our Claims Management Mission. Claims Management Team

Claims Management Our Claims Management Mission To provide the highest level of customer service, proactive claims management, and loss control strategies that will reduce the cost of risk, increase customer

Claims Management Our Claims Management Mission To provide the highest level of customer service, proactive claims management, and loss control strategies that will reduce the cost of risk, increase customer

WORKERS' COMPENSATION INSURANCE

Office of Information Technology Maine Employer s Mutual Insurance Company s (MEMIC) Rates The Bureau s website includes the following link to MEMIC s rates, charged per $100 of payroll for all classifications:

Office of Information Technology Maine Employer s Mutual Insurance Company s (MEMIC) Rates The Bureau s website includes the following link to MEMIC s rates, charged per $100 of payroll for all classifications:

Department of Labor & Industries Program Compliance Audit

Department of Labor & Industries Program Compliance Audit FIRM INTERVIEW WORKSHEET Firm Name: Firm Number: Name of Facility: 1. PERSONAL SERVICE LABOR CONTRACTS (RCW 51.08.180): Do you have any individuals

Department of Labor & Industries Program Compliance Audit FIRM INTERVIEW WORKSHEET Firm Name: Firm Number: Name of Facility: 1. PERSONAL SERVICE LABOR CONTRACTS (RCW 51.08.180): Do you have any individuals

Important Information

16 An Employee s Guide to the South Dakota Workers Compensation System Division of Labor and Management Phone: (605) 773-3681 www.sdjobs.org Department of Labor and Regulation 700 Governors Drive Pierre,

16 An Employee s Guide to the South Dakota Workers Compensation System Division of Labor and Management Phone: (605) 773-3681 www.sdjobs.org Department of Labor and Regulation 700 Governors Drive Pierre,

The County of Scotland Transitional Duty Policy

The County of Scotland Transitional Duty Policy A. PURPOSE This policy defines the County of Scotland s Transitional Duty Program for employees who are injured on the job. B. POLICY/MISSION STATEMENT It

The County of Scotland Transitional Duty Policy A. PURPOSE This policy defines the County of Scotland s Transitional Duty Program for employees who are injured on the job. B. POLICY/MISSION STATEMENT It

INDUSTRIAL COMMISSION OF ARIZONA

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

POLICYHOLDER / CERTIFICATEHOLDER. Policy Number(s): 1) 2) Social Security Number: Date of Birth: / / Male Female

: 1) 2) Social Security Number: Date of Birth: / / Male Female") CLAIM FORM AND INSTRUCTIONS If you have any questions regarding benefits available, or how to file your claim, or if you would like to appeal any determination, please contact our Customer Care Center

CLAIM FORM AND INSTRUCTIONS If you have any questions regarding benefits available, or how to file your claim, or if you would like to appeal any determination, please contact our Customer Care Center

Who Administers the Workers Compensation Program and Related Responsibilities?

What is Workers Compensation? Who Administers the Workers Compensation Program and Related Responsibilities? Who is Eligible for Workers Compensation? What Coverage is Provided? What is a Compensable Injury?

What is Workers Compensation? Who Administers the Workers Compensation Program and Related Responsibilities? Who is Eligible for Workers Compensation? What Coverage is Provided? What is a Compensable Injury?

Managed Care Program

Summit Workers Compensation Managed Care Program KENTUCKY How to obtain medical care for a work-related injury or illness. Welcome Summit s workers compensation managed-care organization (Summit MCO) is

Summit Workers Compensation Managed Care Program KENTUCKY How to obtain medical care for a work-related injury or illness. Welcome Summit s workers compensation managed-care organization (Summit MCO) is

FILING WORKERS COMPENSATION CLAIMS IN IDAHO

Claims contact information First Report of Injury forms ReportClaim@IdahoSIF.org General e-mail ClaimsIM@IdahoSIF.org FILING WORKERS COMPENSATION CLAIMS IN IDAHO Provider inquiries 208-332-2169 or 800-334-2370

Claims contact information First Report of Injury forms ReportClaim@IdahoSIF.org General e-mail ClaimsIM@IdahoSIF.org FILING WORKERS COMPENSATION CLAIMS IN IDAHO Provider inquiries 208-332-2169 or 800-334-2370

Workers Compensation Flight Attendant Rights By: Debora Sutor

Workers Compensation Flight Attendant Rights By: Debora Sutor Dear American Eagle Flight Attendant, Following an unusual increase in the amount of workers compensation inquiries AFA has received recently,

Workers Compensation Flight Attendant Rights By: Debora Sutor Dear American Eagle Flight Attendant, Following an unusual increase in the amount of workers compensation inquiries AFA has received recently,

Workers Compensation Solutions from CNA. www.cna.com

Workers Compensation Solutions from CNA www.cna.com A commitment to your employees A commitment to your company Take a look around your company. Chances are, your workplace has changed in the past 10 years.

Workers Compensation Solutions from CNA www.cna.com A commitment to your employees A commitment to your company Take a look around your company. Chances are, your workplace has changed in the past 10 years.

The ACCG Claims Office staff is here to help you. Please feel free to call us with your questions and concerns.

1 WELCOME This handbook contains information prepared by the Association County Commissioners of Georgia - Group Self-Insurance Workers Compensation Fund (ACCG - GSIWCF) to assist employees and management

1 WELCOME This handbook contains information prepared by the Association County Commissioners of Georgia - Group Self-Insurance Workers Compensation Fund (ACCG - GSIWCF) to assist employees and management

OASIS GROUP. Workers Compensation Claims Call Center. Workers Compensation Injury Reporting Guide

OASIS GROUP Workers Compensation Claims Call Center Workers Compensation Injury Reporting Guide Workers Compensation Injury Reporting Oasis Risk Department 2601 Cattlemen Road Suite 300 Sarasota, FL 34232

OASIS GROUP Workers Compensation Claims Call Center Workers Compensation Injury Reporting Guide Workers Compensation Injury Reporting Oasis Risk Department 2601 Cattlemen Road Suite 300 Sarasota, FL 34232

(404) 919-9756 david@davidbrauns.com www.davidbrauns.com

919-9756 david@davidbrauns.com www.davidbrauns.com") You are probably reading this guide because you were recently in an automobile accident. Now you are faced with some difficulties. The tasks of managing your care and your insurance claim can be confusing

You are probably reading this guide because you were recently in an automobile accident. Now you are faced with some difficulties. The tasks of managing your care and your insurance claim can be confusing

Introduction to Workers Compensation

2013 Risk Management Seminar Putting Safety to Work Introduction to Workers Compensation To Begin Introduction to the Claims Department My goals and objectives Agenda Claims Management Philosophy The Roles

2013 Risk Management Seminar Putting Safety to Work Introduction to Workers Compensation To Begin Introduction to the Claims Department My goals and objectives Agenda Claims Management Philosophy The Roles

The 411 on Connecticut Injuries at Work and Workers Compensation

52 Holmes Avenue Waterbury, CT 06710 (203) 753-7300 The 411 on Connecticut Injuries at Work and Workers Compensation www.welcomelawfirm.com JWelcome@WelcomeLawFirm.com Injured at Work? What now? If you

52 Holmes Avenue Waterbury, CT 06710 (203) 753-7300 The 411 on Connecticut Injuries at Work and Workers Compensation www.welcomelawfirm.com JWelcome@WelcomeLawFirm.com Injured at Work? What now? If you

What to Do When an Accident Occurs - Work Comp Procedures

What to Do When an Accident Occurs - Work Comp Procedures Immediate Response Non-emergency Respond with onsite first aid/cpr responders. Employee must select a physician from the Panel of Physicians form

What to Do When an Accident Occurs - Work Comp Procedures Immediate Response Non-emergency Respond with onsite first aid/cpr responders. Employee must select a physician from the Panel of Physicians form

POLICYHOLDER / CERTIFICATEHOLDER. Policy Number(s): 1) 2) Social Security Number: Date of Birth: / / Male Female

: 1) 2) Social Security Number: Date of Birth: / / Male Female") CLAIM FORM AND INSTRUCTIONS If you have any questions regarding our determination of your claim, or if you would like to appeal any determination, please contact our Customer Care Center at 1-800-348-4489

CLAIM FORM AND INSTRUCTIONS If you have any questions regarding our determination of your claim, or if you would like to appeal any determination, please contact our Customer Care Center at 1-800-348-4489

Breaking Down Work Comp Premium

3. 4. Missouri Employers Mutual Understand How it Can Add Up to Savings For more information: www.mem-ins.com 1.800.442.0593 These recommendations were developed from national standards and sources believed

3. 4. Missouri Employers Mutual Understand How it Can Add Up to Savings For more information: www.mem-ins.com 1.800.442.0593 These recommendations were developed from national standards and sources believed

The Tooher Ferraris Insurance Group Property & Casualty Resource

Tooher Ferraris Insurance Group Property & Casualty Resource Table of Contents Compliance...1 State-Specific Regulatory Information...1 State & Federal Safety Guides...1 Workers Compensation Statutes...2

Tooher Ferraris Insurance Group Property & Casualty Resource Table of Contents Compliance...1 State-Specific Regulatory Information...1 State & Federal Safety Guides...1 Workers Compensation Statutes...2

The forms must be completed by a qualified person and signed with their occupational title as per its respective form.

Your ability to work and generate income is your greatest asset. If a disability ever left you unable to work, a combination of increased expenses and loss of income could create financial difficulties.

Your ability to work and generate income is your greatest asset. If a disability ever left you unable to work, a combination of increased expenses and loss of income could create financial difficulties.

Robert Bell Insurance Brokers, Inc. Property & Casualty Resource Library

Robert Bell Insurance Brokers, Inc. Property & Casualty Resource Library Table of Contents Service and Renewal tools...1 Strategic Plans...1 Servicing Tools...1 Renewal Tools...1 Compliance...1 State-Specific

Robert Bell Insurance Brokers, Inc. Property & Casualty Resource Library Table of Contents Service and Renewal tools...1 Strategic Plans...1 Servicing Tools...1 Renewal Tools...1 Compliance...1 State-Specific

Employer s Guide to Workers Compensation

Employer s Guide to Workers Compensation 2 ABOUT PINNACOL ASSURANCE Mission statement To provide assured protection to Colorado employers and their greatest asset their employees. Who we are For more than

Employer s Guide to Workers Compensation 2 ABOUT PINNACOL ASSURANCE Mission statement To provide assured protection to Colorado employers and their greatest asset their employees. Who we are For more than

POLICYHOLDER. Policy No.(s): Waiver of Premium (include life policies) Routine Pregnancy

: Waiver of Premium (include life policies) Routine Pregnancy") CLAIM FORM AND INSTRUCTIONS If you have any questions regarding our determination of your claim, or if you would like to appeal any determination, please contact our Customer Care Center at 1-800-348-4489

CLAIM FORM AND INSTRUCTIONS If you have any questions regarding our determination of your claim, or if you would like to appeal any determination, please contact our Customer Care Center at 1-800-348-4489

Occupational Math: How Safety Professionals / Risk Managers Contributions Affect the Bottom-Line

Occupational Math: How Safety Professionals / Risk Managers Contributions Affect the Bottom-Line Cathi L. Marx, ALCM, COSS, CHS-V President Aspen Risk Management Group First Things First: Question:Should

Occupational Math: How Safety Professionals / Risk Managers Contributions Affect the Bottom-Line Cathi L. Marx, ALCM, COSS, CHS-V President Aspen Risk Management Group First Things First: Question:Should

System-Wide Workers' Compensation HR Policy No: 6.08 Page 1 of 6

System-Wide Workers' Compensation HR Policy No: 6.08 Page 1 of 6 Policy No: 6.08 Subject: Supercedes: Effective: January 1, 1999 Reviewed: July 1, 2009 Workers' Compensation All existing corporate and

System-Wide Workers' Compensation HR Policy No: 6.08 Page 1 of 6 Policy No: 6.08 Subject: Supercedes: Effective: January 1, 1999 Reviewed: July 1, 2009 Workers' Compensation All existing corporate and

Workers Compensation. Inside this Brief. Background Brief on. History in Oregon 1990 Reforms. 1995 Reforms. Management-Labor Advisory Committee

Background Brief on September 2012 Inside this Brief History in Oregon 1990 Reforms 1995 Reforms Management-Labor Advisory Committee Claims Process Medical Service Providers Fatality Benefits Staff and

Background Brief on September 2012 Inside this Brief History in Oregon 1990 Reforms 1995 Reforms Management-Labor Advisory Committee Claims Process Medical Service Providers Fatality Benefits Staff and

Virginia Workers Compensation Commission

Virginia Workers Compensation Commission Employer Guide to Virginia Workers Compensation 11 What is Workers Compensation? Workers Compensation is a mandatory insurance requirement for most employers. It

Virginia Workers Compensation Commission Employer Guide to Virginia Workers Compensation 11 What is Workers Compensation? Workers Compensation is a mandatory insurance requirement for most employers. It

ACCIDENT INSURANCE CLAIM

ACCIDENT INSURANCE CLAIM ReliaStar Life Insurance Company A member of the ING family of companies Administered by: Key Benefit Administrators, Inc., P.O. Box 1238 Fort Mill, SC 29716 Phone: 866-225-8704,

ACCIDENT INSURANCE CLAIM ReliaStar Life Insurance Company A member of the ING family of companies Administered by: Key Benefit Administrators, Inc., P.O. Box 1238 Fort Mill, SC 29716 Phone: 866-225-8704,

Workers Compensation Claim Kit PRAIRIE STATE INSURANCE COOPERATIVE

Workers Compensation Claim Kit PRAIRIE STATE INSURANCE COOPERATIVE A CMI, A York Risk Services Company, publication November 1, 2013 Table of Contents About CMI.... 1 To Report a Claim... 1 The Importance

Workers Compensation Claim Kit PRAIRIE STATE INSURANCE COOPERATIVE A CMI, A York Risk Services Company, publication November 1, 2013 Table of Contents About CMI.... 1 To Report a Claim... 1 The Importance

Investigating Workers Compensation Claims and Complying with Wage and Hour Law

Investigating Workers Compensation Claims and Complying with Wage and Hour Law Noel C. Shepard 614-559-7223 nshepard@fbtlaw.com Adam R. Hanley 614-559-7238 ahanley@fbtlaw.com Investigating Workers Compensation

Investigating Workers Compensation Claims and Complying with Wage and Hour Law Noel C. Shepard 614-559-7223 nshepard@fbtlaw.com Adam R. Hanley 614-559-7238 ahanley@fbtlaw.com Investigating Workers Compensation

Controlling WWWWoer Workers Compensation Claims

Premiums paid here, stay here to keep Wisconsin strong. Controlling WWWWoer Workers Compensation Claims Presented By: Sheila K. McGraw Director of Claims To The: Wisconsin Towns Associations Annual Convention

Premiums paid here, stay here to keep Wisconsin strong. Controlling WWWWoer Workers Compensation Claims Presented By: Sheila K. McGraw Director of Claims To The: Wisconsin Towns Associations Annual Convention

Thank you for choosing CNA

Thank you for choosing CNA As every employer knows, workers compensation is a significant cost of doing business, not only in actual dollars, but in lost work days and reduced productivity. In order to

Thank you for choosing CNA As every employer knows, workers compensation is a significant cost of doing business, not only in actual dollars, but in lost work days and reduced productivity. In order to

Humana short-term income protection claim form

Humana short-term income protection claim form 1-866-836-6144 Instructions Please read and follow the instructions carefully. 1. If this is the initial claim for benefit payments for this disability, please

Humana short-term income protection claim form 1-866-836-6144 Instructions Please read and follow the instructions carefully. 1. If this is the initial claim for benefit payments for this disability, please

EMPLOYEE FACTS IMPORTANT WORKERS COMPENSATION INFORMATION FOR FLORIDA S WORKERS

EMPLOYEE FACTS IMPORTANT WORKERS COMPENSATION INFORMATION FOR FLORIDA S WORKERS Please visit our website at www.fldfs.com/wc where you will find extensive information such as publications, a number of

EMPLOYEE FACTS IMPORTANT WORKERS COMPENSATION INFORMATION FOR FLORIDA S WORKERS Please visit our website at www.fldfs.com/wc where you will find extensive information such as publications, a number of

Policy and Procedures

Policy and Procedures Return to SafeworksIllinois.com articles Subject: Return To Work Policy 1. Table of Contents 1 2. Purpose.2 3. Policy....2 4. Procedures..3 4.1 Reporting an Injury.3 4.2 Medical Treatment

Policy and Procedures Return to SafeworksIllinois.com articles Subject: Return To Work Policy 1. Table of Contents 1 2. Purpose.2 3. Policy....2 4. Procedures..3 4.1 Reporting an Injury.3 4.2 Medical Treatment

An Employee s Guide to the Missouri Workers Compensation System

An Employee s Guide to the Missouri Workers Compensation System Missouri Department of Labor and Industrial Relations Division of Workers Compensation Important Information You may want to put names and

An Employee s Guide to the Missouri Workers Compensation System Missouri Department of Labor and Industrial Relations Division of Workers Compensation Important Information You may want to put names and

11/15/2010. Money Saving Secrets to Reduce Workers Compensation Costs. New Jersey Medicaid Case Mix Reimbursement and your Facility Insurance

Presented by: Elio Vecchiarelli, CIC Money Saving Secrets to Reduce Workers Compensation Costs www.niagroup.com New Jersey Medicaid Case Mix Reimbursement and your Facility Insurance As of July 1, 2010

Presented by: Elio Vecchiarelli, CIC Money Saving Secrets to Reduce Workers Compensation Costs www.niagroup.com New Jersey Medicaid Case Mix Reimbursement and your Facility Insurance As of July 1, 2010

19. Injury, Accident, and Loss Reporting

19. Injury, Accident, and Loss Reporting Overview This section discusses the following topics: Where to Report Claims Reporting Workers Compensation Illnesses and Injuries Reporting Automobile Accidents

19. Injury, Accident, and Loss Reporting Overview This section discusses the following topics: Where to Report Claims Reporting Workers Compensation Illnesses and Injuries Reporting Automobile Accidents

Effective Injury Management Program AN EMPLOYER S GUIDE. Captain John Parker photo

Effective Injury Management Program AN EMPLOYER S GUIDE Captain John Parker photo How Well Does Your Company Manage Employee Injuries? Do you have procedures in place to assure prompt reporting of claims

Effective Injury Management Program AN EMPLOYER S GUIDE Captain John Parker photo How Well Does Your Company Manage Employee Injuries? Do you have procedures in place to assure prompt reporting of claims

EMR as Qualifier to Bid on Construction Projects

EMR as Qualifier to Bid on Construction Projects July 14, 2011 Introduction This white paper discusses the use of the experience rating modification (commonly referred to as EMR in the construction trades)

EMR as Qualifier to Bid on Construction Projects July 14, 2011 Introduction This white paper discusses the use of the experience rating modification (commonly referred to as EMR in the construction trades)

Disability Benefit Claim Form

Transamerica Worksite Marketing P.O. Box 8043 Little Rock, AR 72203-8043 Phone: 800-251-7254 (7:00 a.m. 5:00 p.m. CST) Fax: 866-586-6528 Disability Benefit Claim Form Instructions to submit claim 1) The

Transamerica Worksite Marketing P.O. Box 8043 Little Rock, AR 72203-8043 Phone: 800-251-7254 (7:00 a.m. 5:00 p.m. CST) Fax: 866-586-6528 Disability Benefit Claim Form Instructions to submit claim 1) The

Accident Claim Filing Instructions

Accident Claim Filing Instructions The offering Company(ies) listed below, severally or collectively, as the content may require, are referred to in this authorization as We or Humana. Life, Specified

Accident Claim Filing Instructions The offering Company(ies) listed below, severally or collectively, as the content may require, are referred to in this authorization as We or Humana. Life, Specified

Workers Compensation Cost Data

Workers Compensation Cost Data Edward M. Welch Workers Compensation Center School of Labor and Industrial Relations Michigan State University E-mail: welche@msu.edu Web Page: http://www.lir.msu.edu/wcc/

Workers Compensation Cost Data Edward M. Welch Workers Compensation Center School of Labor and Industrial Relations Michigan State University E-mail: welche@msu.edu Web Page: http://www.lir.msu.edu/wcc/

Act Now! GIVE YOUR FAMILY PEAK PROTECTION. Group Long Term Disability Insurance Conversion Plan Enrollment Kit

Act Now! You must apply within 60 days of termination GIVE YOUR FAMILY PEAK PROTECTION Group Long Term Disability Insurance Conversion Plan Enrollment Kit Customer Service Center 888-262-6873 Monday through

Act Now! You must apply within 60 days of termination GIVE YOUR FAMILY PEAK PROTECTION Group Long Term Disability Insurance Conversion Plan Enrollment Kit Customer Service Center 888-262-6873 Monday through

SOLE PROPRIETORS UNDER THE WISCONSIN WORKER S COMPENSATION ACT

SOLE PROPRIETORS UNDER THE WISCONSIN WORKER S COMPENSATION ACT Department of Workforce Development Worker s Compensation Division Bureau of Insurance Programs 201 E. Washington Ave., Rm. C100 P.O. Box

SOLE PROPRIETORS UNDER THE WISCONSIN WORKER S COMPENSATION ACT Department of Workforce Development Worker s Compensation Division Bureau of Insurance Programs 201 E. Washington Ave., Rm. C100 P.O. Box

Information for Worker s Compensation Clients

Information for Worker s Compensation Clients Overview of the Worker s Compensation Act Indiana Worker s Compensation cases are governed by a State law known as the Worker s Compensation Act. The legislature

Information for Worker s Compensation Clients Overview of the Worker s Compensation Act Indiana Worker s Compensation cases are governed by a State law known as the Worker s Compensation Act. The legislature

1. Employee Benefits: Workers' Compensation provides both medical and indemnity benefit payments for and to eligible employees.

Policies of the University of North Texas Health Science Center 05.803 Worker s Compensation Insurance Chapter 05 Human Resources Policy Statement. The University of North Texas Health Science Center at

Policies of the University of North Texas Health Science Center 05.803 Worker s Compensation Insurance Chapter 05 Human Resources Policy Statement. The University of North Texas Health Science Center at