Bank Reconciliation Class. Presenter: Emilia Tito Staff Accountant Auditing & Property Records

|

|

|

- Osborne Bridges

- 8 years ago

- Views:

Transcription

1 Bank Reconciliation Class Presenter: Emilia Tito Staff Accountant Auditing & Property Records

2 Introduction Administrators are asked to attend the bank reconciliation class because they are responsible for reviewing and signing the Bank Reconciliation statement, as well as, the Principal s monthly financial report. To have good internal control over the school s assets, the school administrator is responsible for understanding and verifying the financial data on the monthly reconciliations.

3 Objectives 1. To know the processes used to post interest and service charges monthly. 2. Be familiar with the reports required to prepare the bank reconciliation statements. 3. Learn the processes used for outstanding checks and NSF checks using the NSF log. 4. As an administrator know what questions to ask. 5. To do a bank reconciliation using the general ledger, the bank statement and previous month s bank reconciliation statement.

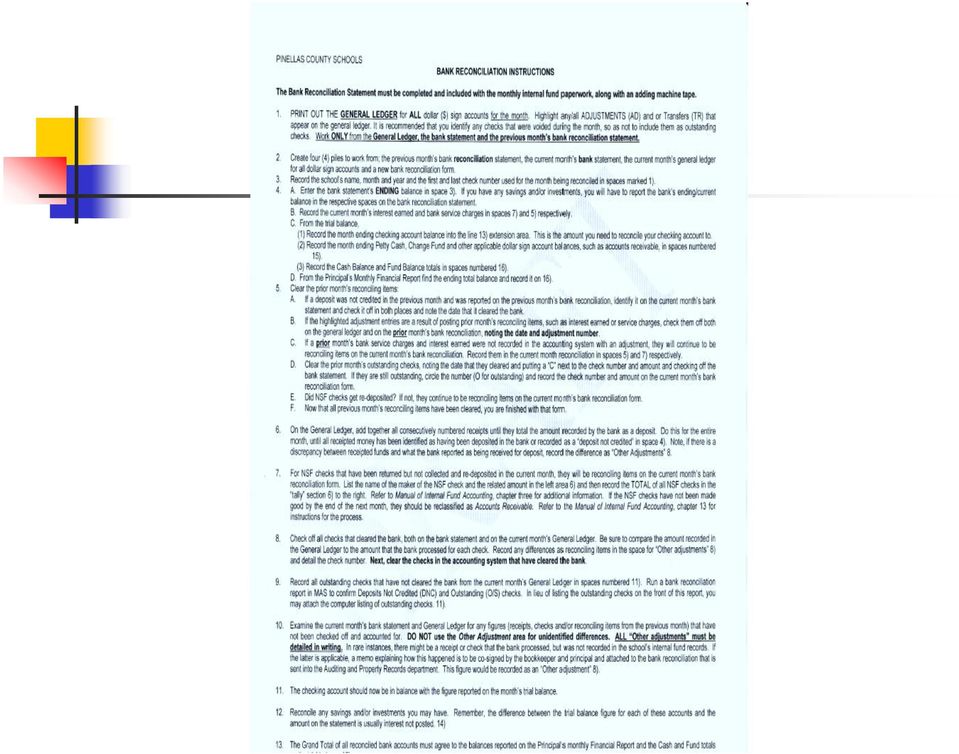

4 Financial reports due to Auditing by the 12 th of each month Summary of Principal s monthly Trial Balance Bank statement Bank reconciliation statement with adding machine tape to support all amounts listed and make sure the other adjustments are identified. General ledger- needs to be sent to Auditing if you are a new bookkeeper or out of balance. See Chapter 10 of the Manual of Internal Fund Accounting book for more information.

5

6

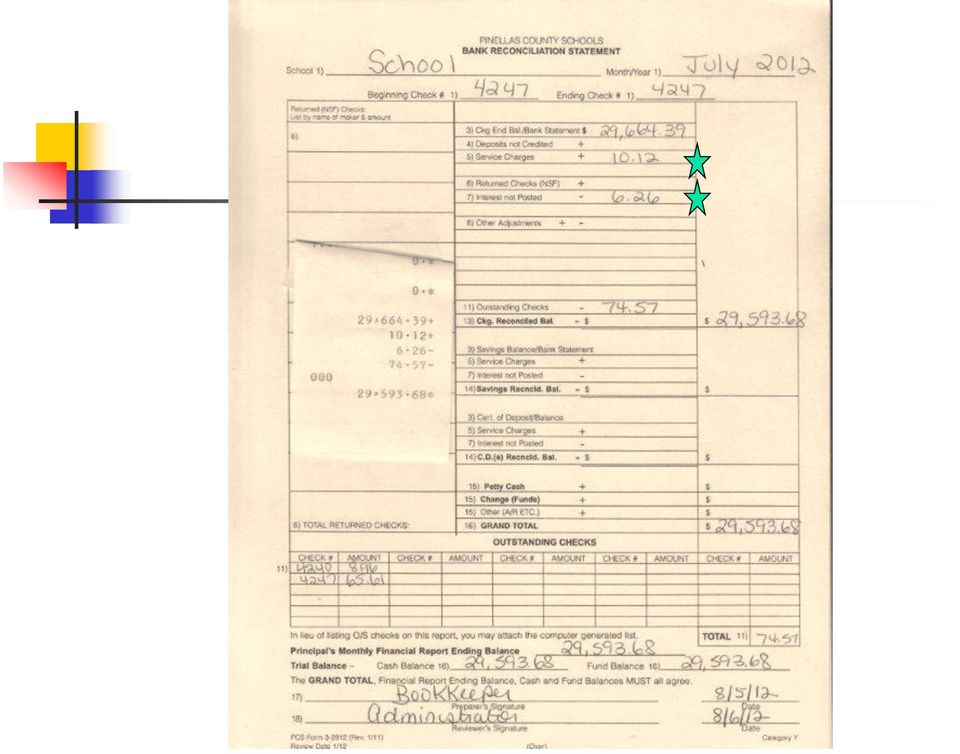

- Are the other adjustments on the bank reconciliation there for a reason? Need explanation.")

7 Important to ASK QUESTIONS. -The prior month s other adjustments getting FIXED or do they need to be carried over? - Interest and service charges (are they being posted to the GL?) - Are the other adjustments on the bank reconciliation there for a reason? Need explanation. - Deposits in transit (is it on the next month s bank statement or is it being carried over month to month? ) Make sure the reports and numbers on the bank reconciliation statement match the supporting documents. All amounts listed must be supported with sufficient documentation.

- Directions from the back of the Bank Reconciliation Statement on how to balance the financials.")

8 Exercise 1- Reconciling August Exercise packets should include: - Bank Statement for the month of August - Completed Bank Reconciliation Statement for the month of July - Blank Bank Reconciliation Statement (will be used for the August bank reconciliation) - Directions from the back of the Bank Reconciliation Statement on how to balance the financials. - General ledger for the month of August - Trial balance for the month of August - Principal s monthly for the month of August

9

10

11

12

13

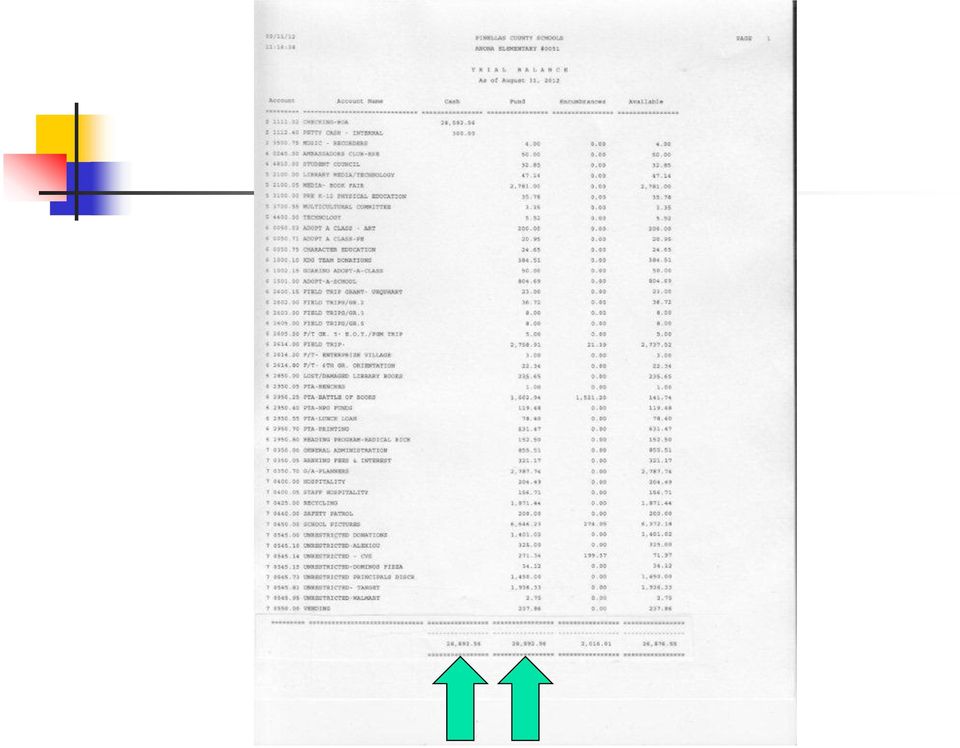

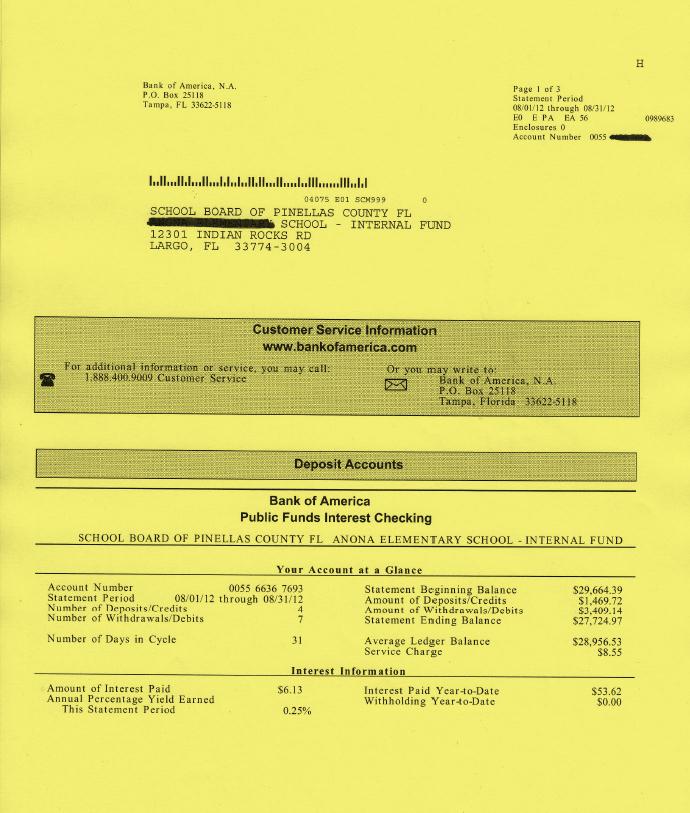

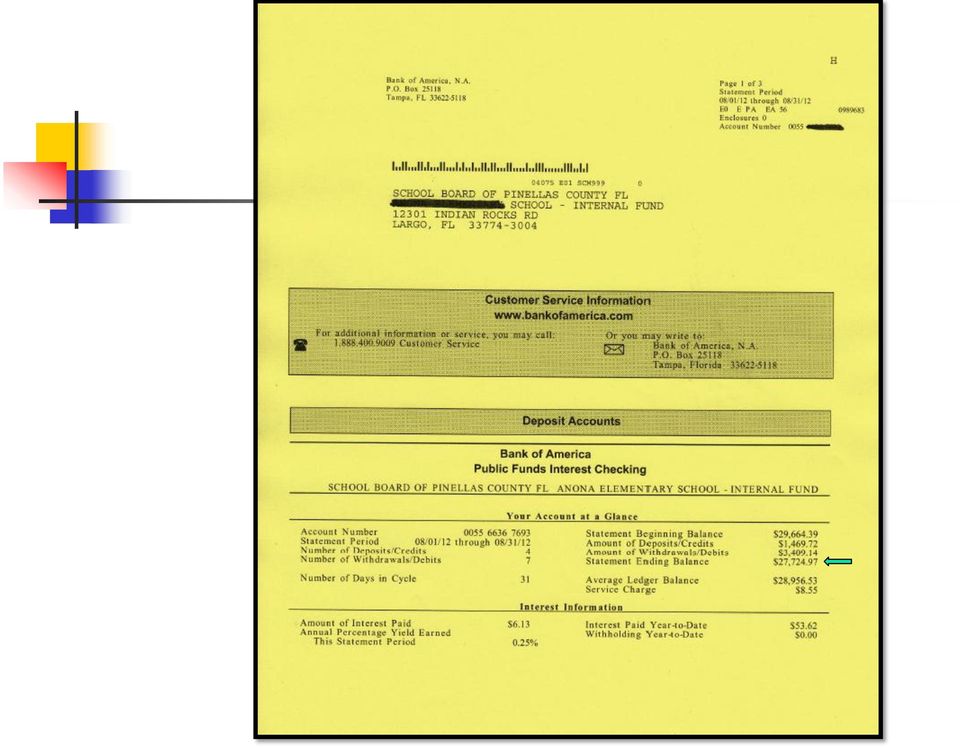

14 School Aug , , , ,892.56

15

16

17

18

19 Dep not CR

20

21 School Aug , , , ,892.56

22

23

24 School Aug , , , ,892.56

25 School Aug , , , , , ,

26 Banking tips 1 - Principals must contact the Director of Auditing if you would like to change banks. - If a Principal or an administrator is moving to another location please write a letter to the director of Auditing on letterhead with the name of your current school, check signers of your current school(old), ask to delete your name from the list of school signers and add the new principal or admin. and list their name, list your account number and sign with your original signature. - Your check stock should state the following: * void after 6 months * two signatures required(cannot be two support personnel)

27 Banking tips 2 - NEVER pre-sign checks - Checks should be stored in the safe when not in use. - Voided checks should be put with the disbursement packets in numerical order. - Unused bank bags and voided bank bags should be in a locked cabinet. - A school can have only one checking account. - All BOA users must have on line access to statements and transaction information on cash pro. It may be challenging to pick up your certificate or reset your password, but we will work with you. Please contact Emilia Tito in Auditing if you need access.

28 Banking tips 3 - BOA users if you need any checks, deposit slips or a deposit stamp please contact: Harland Clarke You should all be getting a faxed confirmation with every deposit made from your bank. - If you have any problems with your bank statement, a deposit or a check that has cleared please dedicatedservice101@bankofamerica.com - See additional information in Chapter 3 Manual of Internal Fund Accounting book.

29 Clearing checks Checks should be cleared in MANATEE each month using the bank statement- this should be part of the monthly reconciling process. Go in MANATEE: Disbursement > Bank Reconciliation > Edit/clear checks Never change the amount of the check in MANATEE during the clearing check process, fix with an adjustment afterwards. Not clearing your checks is an audit item and can cause problems when you back up daily and monthly.

30 Stale dated checks (outstanding checks) If a check has not cleared the bank in 2 3 months, contact the company or individual to whom the check was written to and inquire if the check has been lost or misplaced. If the check is under (and over 360 days old) the principal may approve the check to be voided in the MAS system. If the check is or more, a disbursement packet needs to be completed and sent to the Cash Mgmt. Dept. and the check needs to be voided. Stale dated checks not processed in a timely manner is an audit item. Read Chapter 3 Manual of Internal Fund Accounting for detailed instructions.

31 Voided checks Do not alter or hand write on any check(s) Write VOID across the spoiled check Physically cut out the signature area of the check Keep voided checks with disbursement packets. On the general ledger, a voided check has brackets around it on the disbursement side. Read Chapter 3 Manual of Internal Fund Accounting for more information.

32 NSF checks (returned checks) Start a No Check list to prevent repeat offenders. Do not re-deposit an NSF check - collect cash or a money order. Use a separate deposit slip for the cash or money order collected, may be put in a bank bag with another deposit. Do not include in the bank bag total. On the bank reconciliation statement (left side) where it says name of maker - list last name of the check owner and the amount. Collecting service charges is up to the Principal. Make sure you send checks for or more to the state attorney s office for collection. Process an adjustment to record an NSF check as an accounts receivable. Not following up on your NSF checks in a timely manner is an audit item. Refer to Chapter 3 and Chapter 13 Manual of Internal Fund Accounting book

33 NSF checks continued Procedures for un-collected returned checks states if the check has not been redeemed and re deposited by the end of the following month an adjustment must be made to reclassify as an accounts receivable prior to preparing the bank reconciliation.

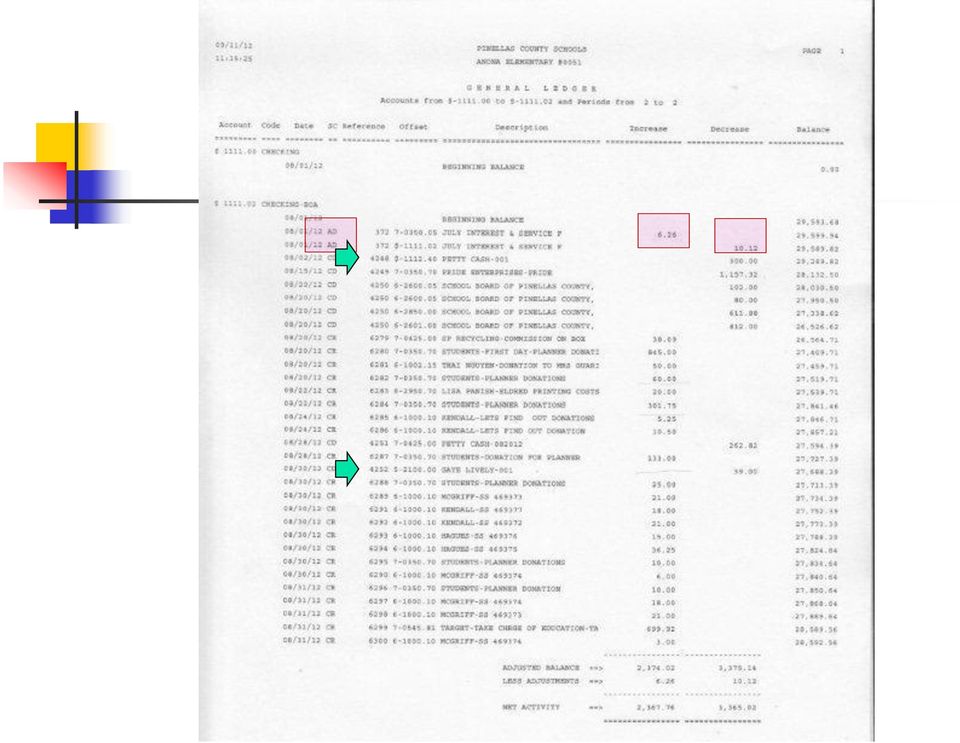

34 Adjustments 1 Make sure you use the proper codes 3431-interest, 0720-service charges Make sure you post the service charges and interest to the correct account May combine service charges and interest into one adjustment- the adjustment will have at least 4 lines of coding. On your bank reconciliation statement make sure to fill out a detailed explanation as to why there is a reconciling item (adjustment). Adjustments should have their own folder - signed, in numerical order and with backup attached. SUGGESTION: have a separate internal purchase requisition attached to each monthly service chg./interest adjustment -less likely to forget & not mandatory.

35 Adjustments 2 Post the service charges & interest each month or else it s an audit item if you carry it month to month. See Chapter 13 of the Manual of Internal Fund Accounting book for more info on adjustments Adjustments should be signed by both the administrator and the bookkeeper with supporting documentation. If your account is in the negative can TR funds from either GA or unrestricted donations.

36 When not in balance 1: Print the general ledger for only the cash accounts. Make sure the service charges and interest were posted properly. You will need your previous month s bank statement and previous month s bank reconciliation and a current month s general ledger with the adjustments highlighted. Were the other adjustments (reconciling items) on the previous months bank reconciliation either posted to MANATEE or adjusted by the bank? If not, they will need to be brought over to the current month s reconciliation. Use the general ledger to obtain deposits not credited amount; to identify and compare all deposit amounts and disbursement amounts to the bank statement; and to identify any adjustments made.

37 When not in balance 2: Make sure you run the trial balance and principals monthly reports on the same date/time and that the reports have the same totals. Transpositions - divisible by 9 Make sure you are carrying over outstanding checks from the previous month. The bank reconciliation reviewer (principal or another administrator assigned) needs to double check each figure on the bank reconciliation statement to the supporting documentation reports. Send required reports (trial balance and principal s monthly) on time every month with a copy of the bank statement to Auditing by the 12 th of the month. If the bank reconciliation statement is not completed or not balanced attach a note stating that the bank reconciliation statement will be sent in later when balanced.

- Directions from the back of the Bank Reconciliation Statement on how to balance the financials.")

38 Exercise 2- reconciling June Exercise packets should include: - Bank Statement for the month of June - Completed Bank Reconciliation Statement for the month of MAY - Blank Bank Reconciliation Statement (will be used for the June bank reconciliation) - Directions from the back of the Bank Reconciliation Statement on how to balance the financials. - General ledger for the month of June - Trial balance for the month of June - Principal s monthly for the month of June

39 3.99

40 School June ,

41

42

43 School June , , , ,257.90

44 See NSF Log to see If any cks clrd Is it on June s bank stmt? On the general ledger? Have the checks cleared the bank?

45

46 May bank reconciliation May bank reconciliation June bank reconciliation

47

48 Added from June bank stmt School Sewell Lowell June , May May , , ,257.90

49 Ck 300 clrd Wrong amt Voided check

50

51 Added from June bank stmt School Sewell Lowell June , May May -.35 ck#300 clrd wr amt , , ,

52 difference Deposits not credited

53 / / / / / / NSF redep

54 Added from June bank stmt School Sewell Lowell June , May May -.35 ck#300 cleared wrong amt /6/08 deposit error Adding machine tape , , signed signed 74, , ,

55 Conclusion Information is available: Clearing checks, what is sent in monthly, NSF packets, adjustments for service charges & interest, transaction codes or stale dated check packets. **Remember if you have any trouble balancing your bank reconciliation first ask your reviewer to double check your figures after you have attempted to use the general ledger and have read the instructions carefully that are on the back of the bank reconciliation statement.

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

FS-06-SF3 School Funds Receipt Log; FS-04-SF2 Schools Funds Payment Request; FS-04-SF1 School Funds: Advance of Funds

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Account Sub Account Account Name Receipts Disbursements $ 1111.0X N/A Checking $ 55.00 7-0350.05 0720 Bank Fees & Interest $ 55.00

EXAMPLES OF ADJUSTMENTS A. To record a bank service charge (for example: monthly service fee, charge for new checks ordered or for an NSF (returned item fee (not the amount of the NSF check)). Bank Charge

EXAMPLES OF ADJUSTMENTS A. To record a bank service charge (for example: monthly service fee, charge for new checks ordered or for an NSF (returned item fee (not the amount of the NSF check)). Bank Charge

NEXTGEN TRAINING TRANSACTIONS. I. Vendor Maintenance. Purchase Order Entry. Invoice Entry. Cash Disbursements. V. Journal Entry Cash Receipts

TRANSACTIONS I. Vendor Maintenance II. Purchase Order Entry III. Invoice Entry NEXTGEN TRAINING IV. Cash Disbursements V. Journal Entry Cash Receipts Janet Cowart VI. VII. Queries/Reports Bank Statement

TRANSACTIONS I. Vendor Maintenance II. Purchase Order Entry III. Invoice Entry NEXTGEN TRAINING IV. Cash Disbursements V. Journal Entry Cash Receipts Janet Cowart VI. VII. Queries/Reports Bank Statement

Internal Accounts Fiscal Year 2013 Year-End at a Glance

Internal Accounts Fiscal Year 2013 Year-End at a Glance Purchase Requisition Input - last day to input for: Petty Cash requisition District reimbursement All other requisitions Critial Needs Purchase Request-

Internal Accounts Fiscal Year 2013 Year-End at a Glance Purchase Requisition Input - last day to input for: Petty Cash requisition District reimbursement All other requisitions Critial Needs Purchase Request-

NEXTGEN BUDGETARY ACCOUNTING TRAINING

NEXTGEN BUDGETARY ACCOUNTING TRAINING TRANSACTIONS I. Vendor Maintenance II. III. IV. Requisition Entry - Routing Purchase Order Entry Accounts Payable - Invoice Entry V. Accounts Payable - Cash Disbursements

NEXTGEN BUDGETARY ACCOUNTING TRAINING TRANSACTIONS I. Vendor Maintenance II. III. IV. Requisition Entry - Routing Purchase Order Entry Accounts Payable - Invoice Entry V. Accounts Payable - Cash Disbursements

Accounting. Chapter 6

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

Chapter Five: Cash Receipts

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

Chapter Five: Cash Receipts A. Policies Overview In order to maintain good controls over accounting, the Central Office is responsible for depositing all cash and checks into the operating account. Cash

Chapter 13 Bank Reconciliations

Chapter 13 Bank Reconciliations The Bank Reconciliation module of school cash allows Treasurers to quickly perform bank reconciliations and print month-end reports for the Principal s review and approval.

Chapter 13 Bank Reconciliations The Bank Reconciliation module of school cash allows Treasurers to quickly perform bank reconciliations and print month-end reports for the Principal s review and approval.

Department of Human Services Client Trust Fund 7290 Trust Accounting System Procedures

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

CASH HANDLING POLICY

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

Agency Escrow Accounting Standards.

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Accounts Payable. Best Practices: Existing Control: Control Gap: Controls Evaluation and Gap Analysis. Purchasing

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

CALCASIEU PARISH SCHOOL BOARD SCHOOL ACTIVITY FUNDS EPES ACCOUNTING PROCEDURES MANUAL

CALCASIEU PARISH SCHOOL BOARD SCHOOL ACTIVITY FUNDS EPES ACCOUNTING PROCEDURES MANUAL TABLE OF CONTENTS CPSB SAF EPES Procedures Manual START UP 4 Log in 4 Main Screen 5 Exit 5 UTILITIES 5 Preferences

CALCASIEU PARISH SCHOOL BOARD SCHOOL ACTIVITY FUNDS EPES ACCOUNTING PROCEDURES MANUAL TABLE OF CONTENTS CPSB SAF EPES Procedures Manual START UP 4 Log in 4 Main Screen 5 Exit 5 UTILITIES 5 Preferences

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

Cash Receipts Internal Controls

3 3 Start If gift is stock If gift is credit card If gift is cash/check Mail opened, checks stamped FDO Community Foundation, totals logged & verified 1 Administrative Assistant & mail verifier Cash Receipts

3 3 Start If gift is stock If gift is credit card If gift is cash/check Mail opened, checks stamped FDO Community Foundation, totals logged & verified 1 Administrative Assistant & mail verifier Cash Receipts

CR-370 CASH RECEIPTS

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

How To Reconcile Account Balance In Gpa

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

Accounting software & data

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

Accounting software & data Accounting software and data should reside at church or be webbased where the data base can be accessed by multiple users Multiple people should be trained on software Software

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

efunds User Guide For School Office Employees

efunds User Guide For School Office Employees Table of Contents Introduction & Login Procedure... 1 Welcome to efunds: Main Screen... 3 General Ledger... 3 Receive Money... 3 Pay Bills... 3 Bank Reconciliation...

efunds User Guide For School Office Employees Table of Contents Introduction & Login Procedure... 1 Welcome to efunds: Main Screen... 3 General Ledger... 3 Receive Money... 3 Pay Bills... 3 Bank Reconciliation...

ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

AgencyPro. Cash Accounting Workflow

AgencyPro Cash Accounting Workflow This document is a supplemental accounting guide to reiterate the general processes outlined during the first accounting training. Some of the outlined processes differ

AgencyPro Cash Accounting Workflow This document is a supplemental accounting guide to reiterate the general processes outlined during the first accounting training. Some of the outlined processes differ

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

ACCRUAL ACCOUNTING WORKFLOW

ACCRUAL ACCOUNTING WORKFLOW TABLE OF CONTENTS COMPANY ACCOUNT NUMBERS... 2 POLICY ENTRY... 2 Agency Bill... 2 Direct Bill... 3 Transaction Detail... 3 CLIENT PAYMENTS... 4 Agency Billed Payment... 4 Direct

ACCRUAL ACCOUNTING WORKFLOW TABLE OF CONTENTS COMPANY ACCOUNT NUMBERS... 2 POLICY ENTRY... 2 Agency Bill... 2 Direct Bill... 3 Transaction Detail... 3 CLIENT PAYMENTS... 4 Agency Billed Payment... 4 Direct

to Create an Item How to Create an Item School Cash Suite Frequently Asked Questions

to Create an Item How to Create an Item School Cash Suite Frequently Asked Questions Update: August 2014 Version 4.7.0 Table of Contents General Activities... 5 1 How can I access help within the program?:...

to Create an Item How to Create an Item School Cash Suite Frequently Asked Questions Update: August 2014 Version 4.7.0 Table of Contents General Activities... 5 1 How can I access help within the program?:...

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

CASH RECONCILIATION & INTERNAL CONTROLS

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

Job Ready Assessment Blueprint. Accounting-Advanced. Test Code: 3900 / Version: 01

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

Blue Bear/SchoolBooks Transfers, Adjustments & Bank Reconciliation QR Guide

Transfers and Adjustments Transfer Entry Use Transfers to move money between fund accounts (non-cash accounts). Transfers do not change the cash balance of any bank account. The Transfer Entry Both the

Transfers and Adjustments Transfer Entry Use Transfers to move money between fund accounts (non-cash accounts). Transfers do not change the cash balance of any bank account. The Transfer Entry Both the

- 1 - School Based Funds Reference Guide

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Monthly Closing & Reconciliations. Presented by Bronwyn Duprey

Monthly Closing & Reconciliations Presented by Bronwyn Duprey Introduction Data Flow File Types Reconciling within an application Reconciling applications to General Ledger STO Reconciliation Tools Other

Monthly Closing & Reconciliations Presented by Bronwyn Duprey Introduction Data Flow File Types Reconciling within an application Reconciling applications to General Ledger STO Reconciliation Tools Other

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

Sayre School Accounting and Financial Policies and Procedures Manual

Sayre School Accounting and Financial Policies and Procedures Manual Approved May 15, 2003 Updated 2009 Updated Summer 2011 Access to Records It is the policy of the school to allow the public to inspect

Sayre School Accounting and Financial Policies and Procedures Manual Approved May 15, 2003 Updated 2009 Updated Summer 2011 Access to Records It is the policy of the school to allow the public to inspect

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

CASH: CHECK CONTROLS C-173-15 ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS. Contents. I. Introduction 2

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

Example Accounting/Financial Policies

Example Accounting/Financial Policies TABLE OF CONTENTS INTERNAL CONTROLS... 2 ACCESS TO RECORDS BY MEMBERS... 3 ACCOUNTING COMPUTER FILE BACK-UP PROCEDURE... 3 ACCOUNTING METHOD... 3 AUDIT COMMITTEE...

Example Accounting/Financial Policies TABLE OF CONTENTS INTERNAL CONTROLS... 2 ACCESS TO RECORDS BY MEMBERS... 3 ACCOUNTING COMPUTER FILE BACK-UP PROCEDURE... 3 ACCOUNTING METHOD... 3 AUDIT COMMITTEE...

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Agenda. Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8. Objective. Cash Receipts. Cash Receipts, Payments, & Banking Procedures

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

Cash Receipts, Payments, & Banking Procedures Agenda Lecture Chapter 9 Quiz Chapter 8 Exercises & Problem Chapter 8 Cash Receipts, Payments, & Banking Procedures Objective Cash Receipts 1.cash receipts

Cash Operations Manual - Cash Receipts

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

A. DEFINITION OF CASH Cash Operations Manual - Cash Receipts The term "cash" as used in this manual, refers to U.S. currency and coin, checks drawn on U.S. banks and written in U.S. dollar values (including

06-06 08-06. 4-H Club Officer Handbook. Treasurer

06-06 08-06 4-H Club Officer Handbook Treasurer Treasurer Congratulations! Your fellow club members have selected you to lead them through a successful 4-H year as Treasurer. In case you may have some

06-06 08-06 4-H Club Officer Handbook Treasurer Treasurer Congratulations! Your fellow club members have selected you to lead them through a successful 4-H year as Treasurer. In case you may have some

Monitoring of controls Information System Control procedures

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

Wisconsin Department of Safety & Professional Services

Mail To: P.O. Box 8935 Madison, WI 53708-8935 1400 E. Washington Avenue Madison, WI 53703 FAX #: (608) 261-7083 Phone #: (608) 266-2112 E-Mail: dsps@wi.gov Website: http://dsps.wi.gov DIVISION OF PROFESSIONAL

Mail To: P.O. Box 8935 Madison, WI 53708-8935 1400 E. Washington Avenue Madison, WI 53703 FAX #: (608) 261-7083 Phone #: (608) 266-2112 E-Mail: dsps@wi.gov Website: http://dsps.wi.gov DIVISION OF PROFESSIONAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

How To Use A Bankbook On A Pc Or Macbook With A Credit Card (For A Credit Union)

") EPES School Accounting BASIC ACCOUNTING and Purchase Orders for Windows Copyrighted by Educational Programs and Software, Inc. 2000 This documentation may not be copied without written consent from EPES

EPES School Accounting BASIC ACCOUNTING and Purchase Orders for Windows Copyrighted by Educational Programs and Software, Inc. 2000 This documentation may not be copied without written consent from EPES

Internal Controls: Best Practices for Political Campaigns in New York City

Internal Controls: Best Practices for Political Campaigns in New York City This document describes standard financial controls and procedures that can help you protect and manage your campaign s assets

Internal Controls: Best Practices for Political Campaigns in New York City This document describes standard financial controls and procedures that can help you protect and manage your campaign s assets

Reconciling a Bank Statement

Reconciling a Bank Statement 1. Under Data Adjustments Receipt add interest Claim take out bank charges 2. Under Check Recon Reconcile Bank Statement a. Always do trial first b. Fill in information, then

Reconciling a Bank Statement 1. Under Data Adjustments Receipt add interest Claim take out bank charges 2. Under Check Recon Reconcile Bank Statement a. Always do trial first b. Fill in information, then

S5: Bank Reconciliation Start to Finish

S5: Bank Reconciliation Start to Finish Welcome To Bank Reconciliation Introductions If you have questions not covered: Write them down on a Questions Form and drop in a Connections Box Ask them at Round

S5: Bank Reconciliation Start to Finish Welcome To Bank Reconciliation Introductions If you have questions not covered: Write them down on a Questions Form and drop in a Connections Box Ask them at Round

BANK ACCOUNTS SUPPLEMENTAL INFORMATION School District of Okaloosa County. I. General Provisions

I. General Provisions A. Depositories in which internal funds are kept must be qualified public depositories, approved by the School Board, and are required to furnish the same type of security for deposits

I. General Provisions A. Depositories in which internal funds are kept must be qualified public depositories, approved by the School Board, and are required to furnish the same type of security for deposits

Amicus Small Firm Accounting: Frequently Asked Questions

Amicus Small Firm Accounting: Frequently Asked Questions Questions Administration... 3 1 How do I add another user account? 3 2 How are passwords set up and how are they used? 3 3 What does "Reset User

Amicus Small Firm Accounting: Frequently Asked Questions Questions Administration... 3 1 How do I add another user account? 3 2 How are passwords set up and how are they used? 3 3 What does "Reset User

Checking Accounts. Open, Manage, and Reconcile

Checking Accounts Open, Manage, and Reconcile 1. What is a checking account? A checking account is opened at a bank or other financial institution. Banks offer several different types of checking accounts.

Checking Accounts Open, Manage, and Reconcile 1. What is a checking account? A checking account is opened at a bank or other financial institution. Banks offer several different types of checking accounts.

Chapter 8. Internal Control. Chapter 8-1

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

How To Account For A Wing

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

for Sage 100 ERP Bank Reconciliation Overview Document

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Financial Accounting. John J. Wild. Sixth Edition. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Paw Paw Public Schools. Business Office. Procedures Manual

Paw Paw Public Schools Business Office Procedures Manual Updated August 2013-1 - TABLE OF CONTENTS Section 1 General Section 2 Cash Management Section 3 Expenditures Purchasing Section 4 Expenditures Accounts

Paw Paw Public Schools Business Office Procedures Manual Updated August 2013-1 - TABLE OF CONTENTS Section 1 General Section 2 Cash Management Section 3 Expenditures Purchasing Section 4 Expenditures Accounts

INTERNAL CONTROLS IC INTERNAL SELF-ASSESSMENT IMPREST CHECKING (BANK) ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS

ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS") ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

PROCEDURES FOR SCHOOL COUNCIL FUNDS

PROCEDURES FOR SCHOOL COUNCIL FUNDS August 2013 Index Part 1 Part 2 PSAB and School Board Reporting Ontario Regulation 612/00... 1 School Council Financial Reporting (PSAB)... 2 Administrative Procedures

PROCEDURES FOR SCHOOL COUNCIL FUNDS August 2013 Index Part 1 Part 2 PSAB and School Board Reporting Ontario Regulation 612/00... 1 School Council Financial Reporting (PSAB)... 2 Administrative Procedures

TRUST ACCOUNT. Record Keeping Guide ARKANSAS REAL ESTATE COMMISSION

TRUST ACCOUNT Record Keeping Guide ARKANSAS REAL ESTATE COMMISSION December 2014 The Arkansas Real Estate Commission provides this information as a sample guide about real estate Trust Account maintenance.

TRUST ACCOUNT Record Keeping Guide ARKANSAS REAL ESTATE COMMISSION December 2014 The Arkansas Real Estate Commission provides this information as a sample guide about real estate Trust Account maintenance.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVISED DATE 08/13 CASH HANDLING

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

BUSINESS SERVICES DIVISION PROCEDURES MANUAL CASH HANDLING REVISED DATE 08/13 When handling money, internal controls ensure resources are guarded against waste, loss, and misuse. Basic principles of internal

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011. DIVISION: Finance & Administration. TITLE: Cash Operations Policy and Procedures. DATE: July 15, 2011

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS THROUGHOUT THE MONTH Montana Clerks, Treasurers & Finance Officers Institute ~ May 2014 Darla Erickson, Local Government Services

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS THROUGHOUT THE MONTH Montana Clerks, Treasurers & Finance Officers Institute ~ May 2014 Darla Erickson, Local Government Services

FISCAL POLICIES AND PROCEDURES

FISCAL POLICIES AND PROCEDURES SECTION 1.1 FINANCIAL RECORDS AND REPORTING Colorado Nonprofit Association's fiscal period begins January 1 and ends December 31. The financial records of the organization

FISCAL POLICIES AND PROCEDURES SECTION 1.1 FINANCIAL RECORDS AND REPORTING Colorado Nonprofit Association's fiscal period begins January 1 and ends December 31. The financial records of the organization

GENERAL PAYROLL CONTROLS Dates in scope:

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

GENERAL PAYROLL CONTROLS Risk # Risk Expected Control Step # Testing Documents/Info Needed 1 Unauthorized initial pay rate 2 Unauthorized/unsupported deductions (statutory deductions and benefits). Initial

Guides for County Office Fiscal Management

Guides for County Office Fiscal Management UNIVERSITY OF GEORGIA CAES March 3, 2014 Authored by: Timothy Gray Table of Contents: Page 1. Bank Reconciliations 2 2. Spot Checking for CECs..3-4 3. Checkout

Guides for County Office Fiscal Management UNIVERSITY OF GEORGIA CAES March 3, 2014 Authored by: Timothy Gray Table of Contents: Page 1. Bank Reconciliations 2 2. Spot Checking for CECs..3-4 3. Checkout

Cash Receipts, Cash Payments, and Banking Procedures

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

9-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Cash Receipts, Cash Payments, and Banking Procedures Section 1: Cash Receipts Section Objectives 1. Record cash receipts in a cash

School Accounting Made Easy. The how to guide of the Activity Accounting and Purchase Order Programs.

Accounting & P.O. Manual School Accounting Made Easy. The how to guide of the Activity Accounting and Purchase Order Programs. Walk through of Activity Accounting32 Purchase Orders Includes Screen Shots

Accounting & P.O. Manual School Accounting Made Easy. The how to guide of the Activity Accounting and Purchase Order Programs. Walk through of Activity Accounting32 Purchase Orders Includes Screen Shots

SUBJECT: Cash Handling Policy. Forest Preserve District of Cook County: Employee Handbook Rules of Conduct

POLICY PROCEDURE GUIDELINES POLICY NUMBER: 04.30.00. SUBJECT: Cash Handling Policy PAGE NUMBER: 1 of 7 Adopted: 7/6/2015 Latest Revision: 12/8/2015 Next Review: 04.30.00. POLICY STATEMENT 04.30.01. PURPOSE

POLICY PROCEDURE GUIDELINES POLICY NUMBER: 04.30.00. SUBJECT: Cash Handling Policy PAGE NUMBER: 1 of 7 Adopted: 7/6/2015 Latest Revision: 12/8/2015 Next Review: 04.30.00. POLICY STATEMENT 04.30.01. PURPOSE

USC Care Medical Group, Inc. LAWSON ACCOUNTS RECEIVABLE -- NON PATIENT CLINICAL REVENUE

USC Care Medical Group, Inc. LAWSON ACCOUNTS RECEIVABLE -- NON PATIENT CLINICAL REVENUE Melody Tuw, Mylam Le, Derrick Hsu 5/3/2010 NON PATIENT BILLING REVENUE Policy Statement The USC Care Finance Department

USC Care Medical Group, Inc. LAWSON ACCOUNTS RECEIVABLE -- NON PATIENT CLINICAL REVENUE Melody Tuw, Mylam Le, Derrick Hsu 5/3/2010 NON PATIENT BILLING REVENUE Policy Statement The USC Care Finance Department

Oregon State University Cash Handling Training Cover your assets!

Oregon State University Cash Handling Training Cover your assets! Why training on Cash Handling? Each year OSU processes over $700 million to help fulfill its teaching, research, and public service mission.

Oregon State University Cash Handling Training Cover your assets! Why training on Cash Handling? Each year OSU processes over $700 million to help fulfill its teaching, research, and public service mission.

Sage 100 Year-End Closing Procedures

SWK technologies, inc. Tech Tips SWK Technologies, Inc. Sage 100 Year-End Closing Procedures SWK TECHNOLOGIES, INC. 5 Regent Street Suite 520 Livingston NJ 07039 backup before period end Make sure that

SWK technologies, inc. Tech Tips SWK Technologies, Inc. Sage 100 Year-End Closing Procedures SWK TECHNOLOGIES, INC. 5 Regent Street Suite 520 Livingston NJ 07039 backup before period end Make sure that

FINANCIAL POLICIES INDEX

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

Independent School District of Boise City. Elementary Checking Account Procedures

Independent School District of Boise City Elementary Checking Account Procedures Printed March 2012 TABLE OF CONTENTS ELEMENTARY SCHOOL FUNDS... 1 I. INTRODUCTION... 1 II. DESCRIPTION OF ACCOUNTS... 2

Independent School District of Boise City Elementary Checking Account Procedures Printed March 2012 TABLE OF CONTENTS ELEMENTARY SCHOOL FUNDS... 1 I. INTRODUCTION... 1 II. DESCRIPTION OF ACCOUNTS... 2

Important Disclaimer. Copyright Information

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

FORM 31. (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT

LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT") FORM 31 (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT Instructions 1. This form must be filed within six months from the end of the law firm financial year. 2. If space is insufficient,

FORM 31 (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT Instructions 1. This form must be filed within six months from the end of the law firm financial year. 2. If space is insufficient,

Chapter 7 Trustee. Internal Control Questionnaire

Chapter 7 Trustee Instructions for the trustee: The purpose of the (ICQ) is to provide the United States Trustee with an understanding of the internal controls and financial record keeping and reporting

Chapter 7 Trustee Instructions for the trustee: The purpose of the (ICQ) is to provide the United States Trustee with an understanding of the internal controls and financial record keeping and reporting

Omni Getting Started Manual. switched on accounting

Omni Getting Started Manual switched on accounting Omni Getting Started Table of Contents Install & Register... 3 Install and Register... 3 Omni Programs... 3 Users... 4 Creating Companies... 5 Create

Omni Getting Started Manual switched on accounting Omni Getting Started Table of Contents Install & Register... 3 Install and Register... 3 Omni Programs... 3 Users... 4 Creating Companies... 5 Create

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

INTERNAL ACCOUNTS PROCEDURES Provided by the Business Division

INTERNAL ACCOUNTS PROCEDURES Provided by the Business Division IAP 12.20.2013 Table of Contents Introduction... 7 There are two kinds of funds available to schools.... 7 New school secretaries and bookkeepers....

INTERNAL ACCOUNTS PROCEDURES Provided by the Business Division IAP 12.20.2013 Table of Contents Introduction... 7 There are two kinds of funds available to schools.... 7 New school secretaries and bookkeepers....

HOW TO DO AN INTERNAL AUDIT COMPONENT ASSOCIATION FINANCES

HOW TO DO AN INTERNAL AUDIT OF COMPONENT ASSOCIATION FINANCES Prepared by Lisa Farragut 2000/2001 CAMT Treasurer (California) What is an internal audit? An internal audit is a formal examination of the

HOW TO DO AN INTERNAL AUDIT OF COMPONENT ASSOCIATION FINANCES Prepared by Lisa Farragut 2000/2001 CAMT Treasurer (California) What is an internal audit? An internal audit is a formal examination of the

Pullen Memorial Financial Policies, Forms, & Procedures. (As of June 18, 2012)

") Pullen Memorial Financial Policies, Forms, & Procedures (As of June 18, 2012) Bank Accounts Policy 1. Pullen Memorial Church maintains one primary checking account. Both budget and nonbudget funds shall

Pullen Memorial Financial Policies, Forms, & Procedures (As of June 18, 2012) Bank Accounts Policy 1. Pullen Memorial Church maintains one primary checking account. Both budget and nonbudget funds shall

We recommend that you create seven binders: one each for each SAGE PRO module you own:

We recommend that you create seven binders: one each for each SAGE PRO module you own: General Ledger Inventory Control Accounts Receivable Accounts Payable Order Entry Purchase Orders Payroll If you have

We recommend that you create seven binders: one each for each SAGE PRO module you own: General Ledger Inventory Control Accounts Receivable Accounts Payable Order Entry Purchase Orders Payroll If you have

ACCOUNTS PAYABLE/PURCHASING CLERK JOB DESCRIPTION

JOB DESCRIPTION Employee performs responsible work involving the application of bookkeeping principles which require independent judgment and initiative. Employee also follows standard accounting procedures

JOB DESCRIPTION Employee performs responsible work involving the application of bookkeeping principles which require independent judgment and initiative. Employee also follows standard accounting procedures

DEKALB COUNTY, GEORGIA

DEKALB COUNTY, GEORGIA DEKALB COUNTY SHERIFF'S OFFICE MANAGEMENT REPORT FOR YEAR ENDED DECEMBER 31,2014 PREPARED BY FINANCE- INTERNAL AUDIT DIVISION Page Left Intentionally Blank Finance Department Internal

DEKALB COUNTY, GEORGIA DEKALB COUNTY SHERIFF'S OFFICE MANAGEMENT REPORT FOR YEAR ENDED DECEMBER 31,2014 PREPARED BY FINANCE- INTERNAL AUDIT DIVISION Page Left Intentionally Blank Finance Department Internal

FINANCIAL INFORMATION SYSTEM. Managing Cash Receipts

FINANCIAL INFORMATION SYSTEM Managing Cash Receipts August 2007 Agenda Definition of Cash Receipts Responsibility for Processing Processing Departments Maintaining Cash Security Making Timely Deposit General

FINANCIAL INFORMATION SYSTEM Managing Cash Receipts August 2007 Agenda Definition of Cash Receipts Responsibility for Processing Processing Departments Maintaining Cash Security Making Timely Deposit General

Business Busines Swit S ch Kit wit

Business Switch Kit Switching banks sounds like a lot of work, which is probably why you re staying at your old bank even if you re not satisfied. But what if switching was really easy? We put together

Business Switch Kit Switching banks sounds like a lot of work, which is probably why you re staying at your old bank even if you re not satisfied. But what if switching was really easy? We put together

Stated below are the SCIRE activity level control objectives for purchasing and accounts payable.

SCIRE PURCHASING AND ACCOUNTS PAYABLE AND SUMMARY The goals of the purchasing function at SCIRE are to achieve open, competitive and costeffective buying, while adhering to external funding sources for

SCIRE PURCHASING AND ACCOUNTS PAYABLE AND SUMMARY The goals of the purchasing function at SCIRE are to achieve open, competitive and costeffective buying, while adhering to external funding sources for

Cash, Petty Cash, Change Funds, and Credit Cards

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

Research Subject Incentive Payment Procedures. University Financial Services. Business Requirements. 1. Stakeholders & Business Units

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

JEFFERSON COUNTY PUBLIC SCHOOLS ACTIVITY FUND ACCOUNTING MANUAL

JEFFERSON COUNTY PUBLIC SCHOOLS ACTIVITY FUND ACCOUNTING MANUAL INTRODUCTION This Activity Fund Accounting Manual has been prepared by the Jefferson County Public School staff to serve as an instructional

JEFFERSON COUNTY PUBLIC SCHOOLS ACTIVITY FUND ACCOUNTING MANUAL INTRODUCTION This Activity Fund Accounting Manual has been prepared by the Jefferson County Public School staff to serve as an instructional

Cash Handling Questionnaire

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

How To Manage School Money

PREFACE This Accounting Manual is a Year 2010 revision of the Caddo Parish School Board Intra-School Accounting Procedures. The purpose of this manual is to provide uniform procedures for the financial

PREFACE This Accounting Manual is a Year 2010 revision of the Caddo Parish School Board Intra-School Accounting Procedures. The purpose of this manual is to provide uniform procedures for the financial

Accounting Policies and Procedures Manual (Sample)

") Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash

Accounting Policies and Procedures Manual (Sample) Table of Contents Introduction General Business Office Staff Revenues and Cash Receipts Sources of Revenues Collecting Offerings Posting Revenues Cash