Dr. Claes A. Belfrage School of Management University of Liverpool

|

|

|

- Crystal Roberts

- 8 years ago

- Views:

Transcription

1 Challenges for strengthening Mercosul financial integration lessons from the European experience Dr. Claes A. Belfrage School of Management University of Liverpool

2 Acknowledgements, Disclaimers and concessions Thanks! The argument and recommendations of this report are not necessarily representative of BCB or SGT4. And, it certainly isn t representative of the ECB or the European Commission... Europeanist Learning about the Mercosul You are experts on Mercosul, so I will assume more knowledge of Mercosul than European Union

3 Outline Core Argument Questions Arising Report Overview Analytical framework Historical Background Current Situation in European financial integration Current Situation in Mercosul financial integration Current Problems in Europe: the High Wire Act of Sustaining the Euro Recent Developments in financial integration: European (partial) politicisation and Political Limits in Mercosul Lessons learnt: 10 Policy Recommendations

politicisation and Political Limits in Mercosul Lessons learnt: 10 Policy")

4 Core Argument Overarching Question: What can Mercosul learn from the experience(s) of financial integration in Europe? European Union and Mercosul have long histories and prehistories In both regions, financial integration have shorter histories Yet, financial integration has been positioned at the core of the larger projects of integration (FSAP and LSAP) Both aimed at the creation of regional financial markets through liberalisation However, crudely measured, similarities end there

Both aimed at the creation of regional financial markets through liberalisation However, crudely measured,")

5 Core Argument Europe approached financial integration enthusiastically and confidently emphasising market-making over market control. Burnt by the debt crisis and a series of finance-related crises in the 1980s and 1990s, and constrained by retained national autonomy, Mercosul was more cautious. While each region was hit by crises around the Millennium (Brazil- 98, Argentina-2001/2 and tech-stock bubble in parts of Europe), only Mercosul seems to have learnt their lessons: 1. Financial markets serve important purposes in the capitalist economy, but they are inherently unstable. 2. They require careful regulation and supervision. 3. Because of their instability, crises will happen despite careful regulation and supervision. The (countercyclical) policy tools have to be in the toolkit to deal with them so that their impact on the real economy is limited.

6 Core Argument In a proper electrical system, there are circuit-breakers and back-up systems. Mercosul had/has those. Europe did not/are trying to construct them. Financial liberalisation in Europe was private-led. In Mercosul, it was publicled. Private-led liberalisation leads to lax regulation/supervision. Outsourcing regulation to private bodies (e.g. Credit rating agencies) is oxymoronic. Market self-regulation is a bad idea. Still, this was not just as a result of purposeful by design, but also as unintended outcome of broader integration process. Europe had undertaken monetary integration (EMU). Mercosul had not. Europe saw it as a great facilitator of integration. Enviously looking at the EU, Mercosul was keen (esp. Brazil), hesitated and could not agree on its design. As intended, the Eurosystem served as a transmission belt for monetary policy. It also, through financial integration (esp. wholesale banking sector), became, albeit clearly not the expected outcome, the transmission belt for build-up of imbalances in the system between core and periphery (artificial interest rates). Free-riding should have been impossible thanks to macroeconomic convergence norms and rules (GSP). These proved inadequate. Even Germany and France broke them. Moral hazard was institutionalised!

. Mercosul had not. Europe saw it as a great facilitator of integration. Enviously looking at the EU, Mercosul was keen (esp.")

7 Core Argument Now, Europe is in a vicious cycle of recurring crises, as there are not enough circuit-breakers: No regional recapitalisation funds No fiscal integration to secure welfare systems No political integration ECB-imposed taboo around countercyclical growth policies (e.g. Europe2020)(inflation and potential credit crisis) Policy-makers, regulators and supervisors play catch-up with the financial markets they have been involved in integrating. Bailouts, bailins and bailiffs : It is a tragic story of Europeans paying for bailouts and now also bail-ins as well as having to endure austerity policies to satisfy illegitimate bailiffs (Troika). A political high-wire act performed without sufficient legitimacy, but the consequences (break-up) are too severe to ponder. Mercosul, despite its successes in containing crisis, faces challenges in financial integration with diverging policy preferences and structural obstacles (Brazil- Argentina, Paraguay and Venezuela).

are too severe to ponder.")

8

9 Questions Arising Mercosul, with a degree of gleefulness, looks on and learns lessons from the European experience. Yet, are of course also affected by it through reduced demand, tendential overheating and speculative flows of hot money. Will Europe successfully carry out the high wire act? What are the different scenarios imaginable in a break-up? Smaller Eurozone of core economies and economic disaster in the peripheral ones? How can Mercosul financial integration move further given its current stalemate? How much further does Mercosul want to go in liberalising and integrating, however cautiously, regional financial markets? What would be required for a single Mercosul financial market without a common currency to function with minimal systemic risk? Through 10 policy-recommendations, this report points to possible solutions to assure minimal systemic risk and that financial markets serve the public interest of Mercosul.

10 Report Overview 1. Introduction 2. Methodology 3. Period 1: Early Financial Integration 4. Period 2: Accelerating Financial Market Integration 5. Period 3: Crisis Response: Supervising Financial Markets 6. Conclusion and Policy Recommendations

11 Methodology Real methodological challenges arising from the study: 1. Radically different contexts of financial integration 2. While parallels are in place, different integration processes (EU neoliberalisation and Mercosul cautious liberalisation) 3. Processes are path-dependent and complex 4. Quantitative comparative analysis is therefore problematic 5. Language and unavailability of Mercosul documentation in English 6. Field interviews in Europe, document analysis and BCB Telephone conferences.

12 Analytical Framework Direction, purpose and content of policy and regulation ( technical ) Heterodox International Political Economy approach enabling consideration of the interaction of regional processes with global and local contexts States are essential for the construction and sustaining of markets. But, states are neither simple transmission belts of dominant social forces nor a black box of perfect cohesiveness. It is relatively autonomous, pervaded by historical social relations. Policy-making and Regulation/Supervision can be located on continuum from public-led to private-led Processual Complentarity: Financial integration is (in)compatible with other integration processes and overall regional growth strategy Concepts used to understand broader growth strategies: (neo- )liberalisation, Keynesianism and Developmentalism Regulation is a complex term. It is (increasingly) hard to distinguish from supervision. What is its relationship to e.g. liberalisation? Deregulation? All regulatory processes are related to what was before and always involve Este documento the state, não representa therefore necessariamente re-regulation. a opinião do Banco Central do Brasil.

compatible with other integration processes")

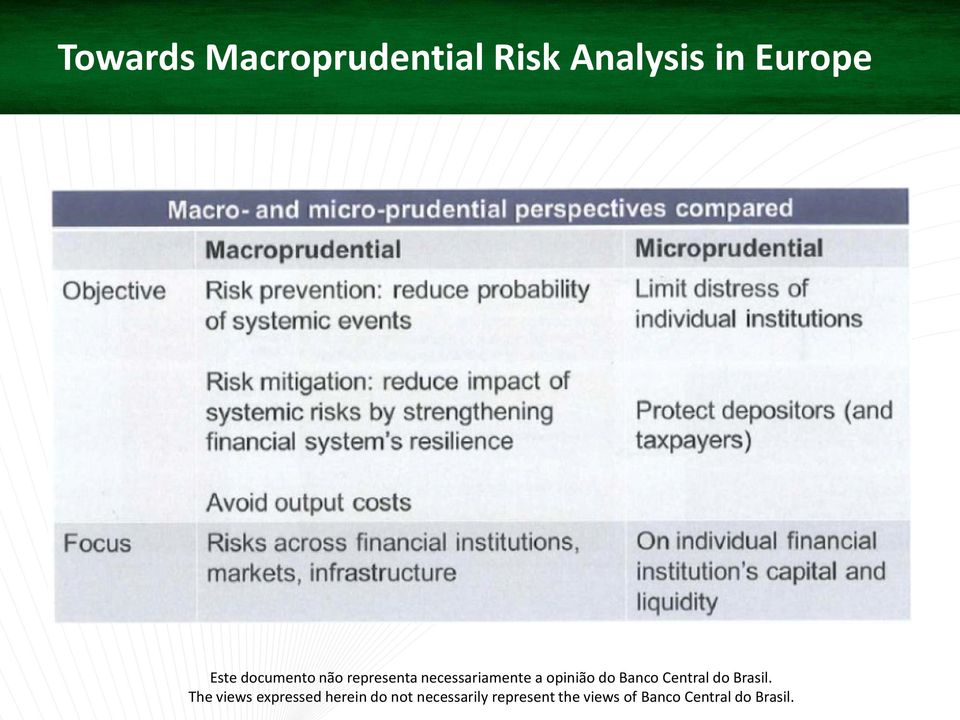

13 Analytical framework Negative and positive integration Against the historical background of focus on microprudential risk analysis, the framework emphasises macroprudential such. Financial fragility and amplification risk (Hyman Minsky) are key in a financial system. Internal (regional/local) and external (insertion into global political economy and international negotiations) dimensions of integration Path-dependent and path-breaking policy

and external (insertion into global political economy and international negotiations)")

14 Periodisation of financial integration 1. Pre-1998 Financial Integration The European Coal and Steel Community and European Economic Community The Latin American Free Trade Area The European Monetary System and the European Exchange Rate Mechanism The Latin American Integration Association The Single European Act The Treaty of Asuncion (Mercosul), the Montevideo Protocol and fixed exchange rate systems (Convertibility and Real Plans) Maastricht and the European Economic and Monetary Union Crises and Booms

, the Montevideo Protocol and fixed exchange rate systems (Convertibility")

15 Periodisation of Financial integration /8 Accelerating Financial Market Integration The Lisbon Strategy Giovannini Barriers Financial Services Action Plan The Lamfalussy Process Basel II and the Capital Requirements Directive(s) Mercosul developments (Social Democratic Shift, cautious liberalisation acknowledgement of asymmetric benefits of Mercosul - FOCEM)

Mercosul developments (Social Democratic Shift, cautious")

16 Periodisation of financial integration Crisis Response: Supervising Financial Markets G20, Bailout and Eurocrisis TARGET II (payment system)(special focus) TARGETIISECURITIES Economic Policy Governance and the European Stability Mechanism European Systemic Risk Board (special focus) European Banking Authority and the European Banking Union European Securities and Markets Authority European Insurance and Occupational Authority Mercosul developments (remit for technical work achieved, bur further integration faces limits in terms of political will)

17 ECB Liquidity Provision and Target2

18 Target2 Imbalances post-crisis

19 The New Financial Stability Governance System

20 Towards Macroprudential Risk Analysis in Europe

21 Current Situation in European financial integration The wholesale interbank market is quite integrated in that the infrastructure is there, but national barriers remain. Money markets are non-existing Retail market integration is limited Monetary integration is only partial. What is in place is a currency union rather than a monetary union. Banking union is desperately needed here to prevent national ringfencing of liquidity. Big differences in securities and solvency laws remain. Here, there is a lack of common securities law. Moreover, all Giovannini barriers are not removed. Integration in this area is currently at a tipping point of resistance to harmonisation. Bonds and listed derivatives markets are less integrated than equity markets. There has been an opening up of pan-european equity trading, but trading has not meaningfully expanded because there is a lack of harmonisation.

22 On the European Financial Integration Horizon Completion of technical implementation of FSAP Deepened operationalisation of new financial governance infrastructure Banking Union Target2Securities Implementation of Pay Structure Directive In related macroeconomic convergence policy area, deepened operationalisation of European Semester, Fiscal integration Macroprudential analysis and systemic crisis fighting (Greece, Spain, Italy, Portugal, Cyprus,...France)

23 Current Situation in Mercosul financial integration Intergovernmental circuit-breakers Willingness to adopt Keynesian-style countercyclical expansionary policy to deal with inevitable crises Lack of monetary integration, but payment system (SML) between Argentina and Brazil (Uruguay negotiations) Strong internal market, partly facilitated by a significant credit expansion... Greater policy autonomy has been created through trade diversification and a reconsideration of internationally dominant policy regimes. This has given the region the freedom to respond in this more effective manner to the crisis. However, limited degree of integration in the region and the historical flexibility towards suspensions of integration agreements is also a cause of tension. 1. Argentina s recent reversion to a more protectionist stance in policy-making, but also Brazil s. 2. Financial integration policy must remain focused on the regulation and supervision of systemic risk despite pressures to deviate from this path. 3. Paraguay suspension and Venezuelan accession are considerable challenges

24 Mercosul financial integration On the short-term horizon Analysis of Mercosul asymmetries on Financial Services concerning National Treatment (NT) and the Market Access (MA). Analysis of obstacles to the progress of effective Financial integration, identification of possible alternatives and resolutions to the identified problems Developing a Technical Cooperation plan in order to foster the financial integration process Constructing a template that addresses the financial regulators requirements to be used in all financial integration processes or financial services negotiations involving Mercosul Writing of a full report on the use of Mercosul currencies on the other Mercosul countries Presentation of a plan for full incorporation of SGT-4 regulations by Venezuela (incl. comparative tables).

25 Conclusion: 10 Policy Recommendations Policy recommendations political and usually stay clear Even when appearing to be technical, they always have consequences benefiting some at the expense of others. (Pareto optimality is rare.) For Mercosul as a whole For individual member states as best practice Typically left imprecise

26 1. Counter Pro-cyclicality in the Financial System by Strengthening Macroprudential Analysis ( Amplification Risk )

27 2. Create Lobby Groups to Represent the Public Interest in Financial Integration (Purpose of integration: longterm (non- HFT), sustainable growth, profitability/public interest, anti-transfer of credit risk, credit access)

28 3. Regulation Needs to be Performed by Public Bodies; Rating Agencies Should Not be Regulators

29 4. Create Mercosul Supervisory Colleges for Cross-border Financial Institutions

30 5. Create a Regional Recapitalisation Fund for Cross-border Financial Institutions

31 6. Prevent the Emergence of Financial Institutions that Are Too Big to Fail

32 7. Ensure the Appropriate Incentives and Time Horizons for Managers of Financial Institutions

33 8. (Continue to) Develop Payment Systems in Local Currency (SML), but be careful with the consequences of monetary integration (OCA) for financial integration and beyond

34 9. Brazil Has to Be a Benevolent (FOCEM+) and Financially Responsible Hegemon (credit expansion)

35 10. (Continue to) Play a confident role in international fora for standard-setting with regard to regulation and supervision and prioritise bottom-up harmonisation

Report on the convenience and risks of currency internationalization and the wider trade of Mercosul Countries assets (including currency) abroad

abroad") Os documentos não representam um posicionamento oficial do SGT-4 nem do Banco Central do Brasil. Report on the convenience and risks of currency internationalization and the wider trade of Mercosul Countries

Os documentos não representam um posicionamento oficial do SGT-4 nem do Banco Central do Brasil. Report on the convenience and risks of currency internationalization and the wider trade of Mercosul Countries

The state of the EU crisis: possible scenarios. Johannes Jäger

The state of the EU crisis: possible scenarios Johannes Jäger 1 The state of the EU crisis: possible scenarios 1. The crisis at the surface 2. Theoretical perspective: political economy 3. Causes and dynamics

The state of the EU crisis: possible scenarios Johannes Jäger 1 The state of the EU crisis: possible scenarios 1. The crisis at the surface 2. Theoretical perspective: political economy 3. Causes and dynamics

Managing the Fragility of the Eurozone. Paul De Grauwe University of Leuven

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 80 70 UK Spain 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 80 70 UK Spain 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008

Accountability of central banks and supervisory bodies what should be the remit of auditors at EU and national level

Claes Norgren Auditor General Version 20141009 Accountability of central banks and supervisory bodies what should be the remit of auditors at EU and national level Keynote speech by Auditor General Mr

Claes Norgren Auditor General Version 20141009 Accountability of central banks and supervisory bodies what should be the remit of auditors at EU and national level Keynote speech by Auditor General Mr

Is the Eurocrisisover? Paul De Grauwe London School of Economics

Is the Eurocrisisover? Paul De Grauwe London School of Economics Outline of presentation Legacy of the sovereign debt crisis Design failures of Eurozone Redesigning the Eurozone Towards a political union?

Is the Eurocrisisover? Paul De Grauwe London School of Economics Outline of presentation Legacy of the sovereign debt crisis Design failures of Eurozone Redesigning the Eurozone Towards a political union?

Mario Draghi: Europe and the euro a family affair

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Arnout H. E. M. Wellink. President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

discussion Paper 2014: Finance for jobs, growth and infrastructure in the EU

The Anglo-Italian Financial Services Dialogue discussion Paper 2014: Finance for jobs, growth and infrastructure in the EU ROME, 24 OCTOBER 2014 contents 1. Introduction 3 2. Policy Summary 4 3. Ensuring

The Anglo-Italian Financial Services Dialogue discussion Paper 2014: Finance for jobs, growth and infrastructure in the EU ROME, 24 OCTOBER 2014 contents 1. Introduction 3 2. Policy Summary 4 3. Ensuring

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank. The euro area Prospects and challenges

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank The euro area Prospects and challenges Speech at the Fundacao Getulio Vargas in Sao Paulo Monday, 5 October 2015 Seite 1 von 12 Inhalt 1 Introduction...

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank The euro area Prospects and challenges Speech at the Fundacao Getulio Vargas in Sao Paulo Monday, 5 October 2015 Seite 1 von 12 Inhalt 1 Introduction...

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker Abstract This paper argues the euro zone requires a government banker that manages the bond market

Europe s Financial Crisis: The Euro s Flawed Design and the Consequences of Lack of a Government Banker Abstract This paper argues the euro zone requires a government banker that manages the bond market

CONTENTS MARZO-ABRIL 2000 NUMERO 784 186

FERNANDEZ RODRIGUEZ, Vicente Javier Euro Exchange Rate Policy: Institutional and Economic Issues Abstract: The present paper describes the institutional aspects of euro exchange rate policy. The first

FERNANDEZ RODRIGUEZ, Vicente Javier Euro Exchange Rate Policy: Institutional and Economic Issues Abstract: The present paper describes the institutional aspects of euro exchange rate policy. The first

International Monetary and Financial Committee

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

Understanding Financial Consolidation

Keynote Address Roger W. Ferguson, Jr. Understanding Financial Consolidation I t is my pleasure to speak with you today, and I thank Bill McDonough and the Federal Reserve Bank of New York for inviting

Keynote Address Roger W. Ferguson, Jr. Understanding Financial Consolidation I t is my pleasure to speak with you today, and I thank Bill McDonough and the Federal Reserve Bank of New York for inviting

Stability in the Eurozone: Challenges and Solutions

Stability in the Eurozone: Challenges and Solutions Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance IMFS Working Lunch, Frankfurt (Main), 15 July

Stability in the Eurozone: Challenges and Solutions Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance IMFS Working Lunch, Frankfurt (Main), 15 July

Annotated Agenda of the Sherpa meeting. Main features of Contractual Arrangements and Associated Solidarity Mechanisms

Annotated Agenda of the Sherpa meeting 21-11-2013 Main features of Contractual Arrangements and Associated Solidarity Mechanisms At their meeting on 26 November the Sherpas are invited to discuss: General

Annotated Agenda of the Sherpa meeting 21-11-2013 Main features of Contractual Arrangements and Associated Solidarity Mechanisms At their meeting on 26 November the Sherpas are invited to discuss: General

How to improve financial stability and resilience of systemically important financial institutions after the crisis?

How to improve financial stability and resilience of systemically important financial institutions after the crisis? EBA Policy Research Workshop How to regulate and resolve systemically important banks

How to improve financial stability and resilience of systemically important financial institutions after the crisis? EBA Policy Research Workshop How to regulate and resolve systemically important banks

Overcoming the Crisis

Overcoming the Crisis Klaus Regling, Managing Director, ESM Bank of Greece Athens, 10 July 2014 Reasons for the crisis The crisis was caused by a very specific mix of circumstances: Excessive deficit/debt

Overcoming the Crisis Klaus Regling, Managing Director, ESM Bank of Greece Athens, 10 July 2014 Reasons for the crisis The crisis was caused by a very specific mix of circumstances: Excessive deficit/debt

The European Banking and Capital Markets Unions: Challenges and Risks

Foundation for European Progressive Studies Fondazione Italianieuropei The European Banking and Capital Markets Unions: Challenges and Risks Remarks by Fabio Panetta Deputy Governor of the Bank of Italy

Foundation for European Progressive Studies Fondazione Italianieuropei The European Banking and Capital Markets Unions: Challenges and Risks Remarks by Fabio Panetta Deputy Governor of the Bank of Italy

The EMU and the debt crisis

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

A European Unemployment Insurance Scheme

A European Unemployment Insurance Scheme Necessary? Desirable? Optimal? Grégory Claeys, Research Fellow, Bruegel Zsolt Darvas, Senior Fellow, Bruegel Guntram Wolff, Director, Bruegel July, 2014 Key messages

A European Unemployment Insurance Scheme Necessary? Desirable? Optimal? Grégory Claeys, Research Fellow, Bruegel Zsolt Darvas, Senior Fellow, Bruegel Guntram Wolff, Director, Bruegel July, 2014 Key messages

European Monetary Union Chapter 20

European Monetary Union Chapter 20 1. Theory of Optimum Currency Areas 2. Background for European Monetary Union 1 Theory of Optimum Currency Areas 1.1 Economic benefits of a single currency Monetary effi

European Monetary Union Chapter 20 1. Theory of Optimum Currency Areas 2. Background for European Monetary Union 1 Theory of Optimum Currency Areas 1.1 Economic benefits of a single currency Monetary effi

Oversight of payment and settlement systems

Oversight of payment and settlement systems The efficiency of the financial system depends on the smooth functioning of various payment and settlement systems, because all financial transactions are performed

Oversight of payment and settlement systems The efficiency of the financial system depends on the smooth functioning of various payment and settlement systems, because all financial transactions are performed

The Contribution of Trade in Financial Services to Economic Growth and Development

The Contribution of Trade in Financial Services to Economic Growth and Development 26 June 2012 Mina Mashayekhi Head Trade Negotiations and Commercial Diplomacy Branch, DITC/UNCTAD Outline 1. Financial

The Contribution of Trade in Financial Services to Economic Growth and Development 26 June 2012 Mina Mashayekhi Head Trade Negotiations and Commercial Diplomacy Branch, DITC/UNCTAD Outline 1. Financial

STRENGTHENING MACRO AND MICRO-PRUDENTIAL SUPERVISION IN EU CANDIDATES AND POTENTIAL CANDIDATES

April 2012 STRENGTHENING MACRO AND MICRO-PRUDENTIAL SUPERVISION IN EU CANDIDATES AND POTENTIAL CANDIDATES A programme funded by the European Union Project Summary (not for publication) A programme implemented

April 2012 STRENGTHENING MACRO AND MICRO-PRUDENTIAL SUPERVISION IN EU CANDIDATES AND POTENTIAL CANDIDATES A programme funded by the European Union Project Summary (not for publication) A programme implemented

Implications of the SSM for the Nordic banking sector. Stefan Ingves, June 5 2014

Implications of the SSM for the Nordic banking sector Stefan Ingves, June 5 2014 Financial trilemma Financial stability Financial integration National supervision Arrangements for cross-border cooperation

Implications of the SSM for the Nordic banking sector Stefan Ingves, June 5 2014 Financial trilemma Financial stability Financial integration National supervision Arrangements for cross-border cooperation

How To Be Cheerful About 2012

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

2012: Deeper into crisis or the long road to recovery? Bart Van Craeynest Hoofdeconoom Petercam Bart.vancraeynest@petercam.be 1 2012: crises looking for answers Global slowdown No 2008-0909 rerun Crises

Lecture 10: International banking

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

Lecture 10: International banking The sessions so far have focused on banking in a domestic context. In this lecture we are going to look at the issues which arise from the internationalisation of banking,

European perspective

Fiscal policy challenges from a European perspective Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance Federal Ministry of Finance, Germany Banco

Fiscal policy challenges from a European perspective Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance Federal Ministry of Finance, Germany Banco

COMPLETING AND STRENGTHENING THE EMU. Italian contribution, May 2015

COMPLETING AND STRENGTHENING THE EMU Italian contribution, May 2015 1. State of play The depth of the economic and financial crisis and its long-lasting impact highlight fundamental unresolved issues related

COMPLETING AND STRENGTHENING THE EMU Italian contribution, May 2015 1. State of play The depth of the economic and financial crisis and its long-lasting impact highlight fundamental unresolved issues related

Klicken Sie, um das Titelformat. zu bearbeiten. The Eurocrisis: new challenges for the EU s. economic policy. Thomas Westphal. 23th of February 2015

The Eurocrisis: new challenges for the EU s Klicken Sie, um das Titelformat economic policy zu bearbeiten Thomas Westphal Klicken Director Sie, General um das European Format Policy des Untertitel-Masters

The Eurocrisis: new challenges for the EU s Klicken Sie, um das Titelformat economic policy zu bearbeiten Thomas Westphal Klicken Director Sie, General um das European Format Policy des Untertitel-Masters

Masaaki Shirakawa: Insurance companies and the financial system a central bank perspective

Masaaki Shirakawa: Insurance companies and the financial system a central bank perspective Keynote address by Mr Masaaki Shirakawa, Governor of the Bank of Japan, at the 18th Annual Conference of the International

Masaaki Shirakawa: Insurance companies and the financial system a central bank perspective Keynote address by Mr Masaaki Shirakawa, Governor of the Bank of Japan, at the 18th Annual Conference of the International

List of legislative acts

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

Ministry of Finance > PO Box 20201 2500 EE Den Haag The Netherlands. Date 20 January 2013 Subject Policy Priorities Eurogroup Presidency

Ministry of Finance > PO Box 20201 2500 EE Den Haag The Netherlands Euro area Ministers of Finance Date 20 January 2013 Subject Policy Priorities Eurogroup Presidency Dear Minister, As you are aware, I

Ministry of Finance > PO Box 20201 2500 EE Den Haag The Netherlands Euro area Ministers of Finance Date 20 January 2013 Subject Policy Priorities Eurogroup Presidency Dear Minister, As you are aware, I

Basel 3: A new perspective on portfolio risk management. Tamar JOULIA-PARIS October 2011

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

Basel 3: A new perspective on portfolio risk management Tamar JOULIA-PARIS October 2011 1 Content 1. Basel 3 A complex regulatory framework With possible unintended consequences 2. Consequences on Main

WHITE PAPER NO. III. Why a Common Eurozone Bond Isn t Such a Good Idea

CENTER FOR FINANCIAL STUDIES WHITE PAPER NO. III JULY 2009 Why a Common Eurozone Bond Isn t Such a Good Idea Otmar Issing Europe s World, Brussels, Belgium Center for Financial Studies Goethe-Universität

CENTER FOR FINANCIAL STUDIES WHITE PAPER NO. III JULY 2009 Why a Common Eurozone Bond Isn t Such a Good Idea Otmar Issing Europe s World, Brussels, Belgium Center for Financial Studies Goethe-Universität

TEXTS ADOPTED Provisional edition

European Parliament 2014-2019 TEXTS ADOPTED Provisional edition P8_TA-PROV(2016)0063 European Central Bank annual report for 2014 European Parliament resolution of 25 February 2016 on the European Central

European Parliament 2014-2019 TEXTS ADOPTED Provisional edition P8_TA-PROV(2016)0063 European Central Bank annual report for 2014 European Parliament resolution of 25 February 2016 on the European Central

FINANCIAL STABILITY ISSUES FOR SMALL STATES. Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data

FINANCIAL STABILITY ISSUES FOR SMALL STATES Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data Disclaimer: Any views expressed are only the author s s own and do not

FINANCIAL STABILITY ISSUES FOR SMALL STATES Mirko Mallia Assistant Executive Financial Stability Surveillance, Assessment and Data Disclaimer: Any views expressed are only the author s s own and do not

União Bancária: A nova fronteira da regulação financeira na UE

The functioning of the Banking Union Pedro Duarte Neves Vice-Governor Lisboa, 25 January 2016 União Bancária: A nova fronteira da regulação financeira na UE 1. Lessons from the crisis 2. Regulatory and

The functioning of the Banking Union Pedro Duarte Neves Vice-Governor Lisboa, 25 January 2016 União Bancária: A nova fronteira da regulação financeira na UE 1. Lessons from the crisis 2. Regulatory and

Preparing for Next Steps on Better Economic Governance in the Euro Area

Preparing for Next Steps on Better Economic Governance in the Euro Area Analytical Note Jean-Claude Juncker in close cooperation with Donald Tusk, Jeroen Dijsselbloem and Mario Draghi Informal European

Preparing for Next Steps on Better Economic Governance in the Euro Area Analytical Note Jean-Claude Juncker in close cooperation with Donald Tusk, Jeroen Dijsselbloem and Mario Draghi Informal European

Position Paper. on the

Position Paper on the Communication from the European Commission to the European Parliament and the Council on Strengthening the Social Dimension of the Economic and Monetary Union (COM (2013) 690) from

Position Paper on the Communication from the European Commission to the European Parliament and the Council on Strengthening the Social Dimension of the Economic and Monetary Union (COM (2013) 690) from

DSF POLICY BRIEFS No. 1/ February 2011

DSF POLICY BRIEFS No. 1/ February 2011 Risk Based Deposit Insurance for the Netherlands Dirk Schoenmaker* Summary: During the recent financial crisis, deposit insurance cover was increased across the world.

DSF POLICY BRIEFS No. 1/ February 2011 Risk Based Deposit Insurance for the Netherlands Dirk Schoenmaker* Summary: During the recent financial crisis, deposit insurance cover was increased across the world.

Market Fragmentation and Recession of 2015

Seminarreihe Aktuelle volkswirtschaftliche Fragen im Rahmen von internationaler Wirtschaft und Europäischer Integration Seminar 1: Neue Erkenntnisse der Außenwirtschaftstheorie von Ricardo bis Melitz mit

Seminarreihe Aktuelle volkswirtschaftliche Fragen im Rahmen von internationaler Wirtschaft und Europäischer Integration Seminar 1: Neue Erkenntnisse der Außenwirtschaftstheorie von Ricardo bis Melitz mit

A full report of our recent meeting will be distributed to all the delegations. Let me briefly summarize some of the most salient conclusions.

Statement by the Executive Secretary of the Economic Commission for Latin America and the Caribbean, ECLAC, Dr. José Antonio Ocampo, in the name of Regional Commissions of the United Nations It is a great

Statement by the Executive Secretary of the Economic Commission for Latin America and the Caribbean, ECLAC, Dr. José Antonio Ocampo, in the name of Regional Commissions of the United Nations It is a great

EU economic. governance. Strong economic rules to manage the euro and economic and monetary union. istockphoto/jon Schulte.

EU economic governance Strong economic rules to manage the euro and economic and monetary union Economic and istockphoto/jon Schulte Responding to the sovereign debt crisis important reforms of EU economic

EU economic governance Strong economic rules to manage the euro and economic and monetary union Economic and istockphoto/jon Schulte Responding to the sovereign debt crisis important reforms of EU economic

The Benefits of a Working European Retail Market for Financial Services

EFR Study Benefits of a Working EU Market for Financial Services 1 Friedrich Heinemann Mathias Jopp The Benefits of a Working European Retail Market for Financial Services Report to European Financial

EFR Study Benefits of a Working EU Market for Financial Services 1 Friedrich Heinemann Mathias Jopp The Benefits of a Working European Retail Market for Financial Services Report to European Financial

Overcoming the Debt Crisis and Securing Growth- Irreconcilable Challenges for the Euro-zone?

Franco-German Conference Overcoming the Debt Crisis and Securing Growth- Irreconcilable Challenges for the Euro-zone? Cinzia Alcidi, CEPS May 3, 2010, Paris Outline: General post crisis background Debt

Franco-German Conference Overcoming the Debt Crisis and Securing Growth- Irreconcilable Challenges for the Euro-zone? Cinzia Alcidi, CEPS May 3, 2010, Paris Outline: General post crisis background Debt

* * * BIS central bankers speeches 1

Luis M Linde: Situation of and challenges facing the European and Spanish banking industry following the start-up of the Single Supervisory Mechanism (SSM) Opening address by Mr Luis M Linde, Governor

Luis M Linde: Situation of and challenges facing the European and Spanish banking industry following the start-up of the Single Supervisory Mechanism (SSM) Opening address by Mr Luis M Linde, Governor

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors Washington, June 3, 2015 1. The financial crisis highlighted severe weaknesses and excesses in the

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors Washington, June 3, 2015 1. The financial crisis highlighted severe weaknesses and excesses in the

Financial Architecture and Banking Systems

Financial Architecture and Banking Systems Financial and Private Sector Development Financial Systems Practice The World Bank Group Our Mission The Financial Architecture and Banking Systems Service Line

Financial Architecture and Banking Systems Financial and Private Sector Development Financial Systems Practice The World Bank Group Our Mission The Financial Architecture and Banking Systems Service Line

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels Governor Carlos Costa Six years since the onset of the financial crisis in 2008, output levels in the EU are below those observed before the crisis.

Keynote Speech, EIB/IMF Meeting, 23 October, Brussels Governor Carlos Costa Six years since the onset of the financial crisis in 2008, output levels in the EU are below those observed before the crisis.

European Sovereign Debt Crisis Policy Proposal Presented by the French Republic 9 November 2012

European Sovereign Debt Crisis Policy Proposal Presented by the French Republic 9 November 2012 The European Redemption Pact We propose the enactment of the European Redemption Pact, with several amendments.

European Sovereign Debt Crisis Policy Proposal Presented by the French Republic 9 November 2012 The European Redemption Pact We propose the enactment of the European Redemption Pact, with several amendments.

ISSUES PAPER ON COMPLETING THE ECONOMIC AND MONETARY UNION. Introduction. The European Council of 29 June 2012 concluded the following:

ISSUES PAPER ON COMPLETING THE ECONOMIC AND MONETARY UNION Introduction The European Council of 29 June 2012 concluded the following: "The report "Towards a Genuine Economic and Monetary Union" presented

ISSUES PAPER ON COMPLETING THE ECONOMIC AND MONETARY UNION Introduction The European Council of 29 June 2012 concluded the following: "The report "Towards a Genuine Economic and Monetary Union" presented

Supervisor in the Institutional and Sectoral Oversight Division; Supervisor in the Analysis and Methodological Support Division.

Position Details Supervisors, DG/MS III Reference 2016-012-EXT S Function The European Central Bank (ECB) is seeking professionals with experience in the prudential supervision of credit institutions,

Position Details Supervisors, DG/MS III Reference 2016-012-EXT S Function The European Central Bank (ECB) is seeking professionals with experience in the prudential supervision of credit institutions,

Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability

: A proposal for a layered scheme with limited joint liability") Jan Pieter Krahnen - Jörg Rocholl Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability White Paper Series No. 10 Designing the

Jan Pieter Krahnen - Jörg Rocholl Designing the funding side of the Single Resolution Mechanism (SRM): A proposal for a layered scheme with limited joint liability White Paper Series No. 10 Designing the

The role of the G20. Central Bank of Argentina. Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011

The role of the G20 Central Bank of Argentina Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011 Agenda Agenda 1. G20 Objectives for 2011 a) Macroeconomic Policy Coordination

The role of the G20 Central Bank of Argentina Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011 Agenda Agenda 1. G20 Objectives for 2011 a) Macroeconomic Policy Coordination

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

Press release Press enquiries: +41 61 280 8188 press@bis.org www.bis.org Ref no: 35/2010 12 September 2010 Group of Governors and Heads of Supervision announces higher global minimum capital standards

Executive Summary In light of the i2010 initiative, the Commission has adopted initiatives to further develop the Single European Information Space a Single Market for the Information Society. However,

Executive Summary In light of the i2010 initiative, the Commission has adopted initiatives to further develop the Single European Information Space a Single Market for the Information Society. However,

Be prepared Four in-depth scenarios for the eurozone and for Switzerland

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

www.pwc.ch/swissfranc Be prepared Four in-depth scenarios for the eurozone and for Introduction The Swiss economy is cooling down and we are currently experiencing unprecedented levels of uncertainty in

Banking Regulation. Pros and Cons

Certificate in Social Banking Money and Society Banking Regulation Pros and Cons Professor Dr. Gregor Krämer Chair for Banking, Finance, and Accounting Alanus University of Arts and Social Sciences, Alfter,

Certificate in Social Banking Money and Society Banking Regulation Pros and Cons Professor Dr. Gregor Krämer Chair for Banking, Finance, and Accounting Alanus University of Arts and Social Sciences, Alfter,

Committee on Payment and Settlement Systems. Central bank oversight of payment and settlement systems

Committee on Payment and Settlement Systems Central bank oversight of payment and settlement systems May 2005 Copies of publications are available from: Bank for International Settlements Press & Communications

Committee on Payment and Settlement Systems Central bank oversight of payment and settlement systems May 2005 Copies of publications are available from: Bank for International Settlements Press & Communications

Delegations will find attached the draft Council conclusions on a Capital Markets Union, as prepared by the Economic and Financial Committee.

Council of the European Union Brussels, 16 June 2015 (OR. en) 9852/15 EF 110 ECOFIN 473 SURE 14 UEM 223 NOTE From: To: Subject: General Secretariat of the Council Permanenet Representatives Committee (Part

Council of the European Union Brussels, 16 June 2015 (OR. en) 9852/15 EF 110 ECOFIN 473 SURE 14 UEM 223 NOTE From: To: Subject: General Secretariat of the Council Permanenet Representatives Committee (Part

Vítor Constâncio: A European solution for crisis management and bank resolution

Vítor Constâncio: A European solution for crisis management and bank resolution Speech by Mr Vítor Constâncio, Vice-President of the European Central Bank, at Sveriges Riksbank and ECB Conference on Bank

Vítor Constâncio: A European solution for crisis management and bank resolution Speech by Mr Vítor Constâncio, Vice-President of the European Central Bank, at Sveriges Riksbank and ECB Conference on Bank

New Plan Aims to End European Debt Crisis

New Plan Aims to End European Debt Crisis AP EU heads of state at their summit meeting in Brussels This story comes from VOA Special English, Voice of America's daily news and information service for English

New Plan Aims to End European Debt Crisis AP EU heads of state at their summit meeting in Brussels This story comes from VOA Special English, Voice of America's daily news and information service for English

Currency and exchange rate regime options

1 Currency and exchange rate regime options 1.1 Introduction In the near future, Icelanders must make important decisions concerning the framework for the currency and monetary policy, the structure of

1 Currency and exchange rate regime options 1.1 Introduction In the near future, Icelanders must make important decisions concerning the framework for the currency and monetary policy, the structure of

Recommendation for a COUNCIL RECOMMENDATION. on the 2015 National Reform Programme of Portugal

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 271 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Portugal and delivering a Council opinion on the 2015 Stability

EUROPEAN COMMISSION Brussels, 13.5.2015 COM(2015) 271 final Recommendation for a COUNCIL RECOMMENDATION on the 2015 National Reform Programme of Portugal and delivering a Council opinion on the 2015 Stability

Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Fabrizio Aurilia, the Insurance Review (Italy)

") Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Fabrizio Aurilia, the Insurance Review (Italy) 1. Since EIOPA was established, how has the role of European supervision of the insurance

Interview with Gabriel Bernardino, Chairman of EIOPA, conducted by Fabrizio Aurilia, the Insurance Review (Italy) 1. Since EIOPA was established, how has the role of European supervision of the insurance

Portugal Programme Assessment

1 Portugal Programme Assessment European Commission, DG ECFIN 15 May, 2014 2 Root causes of Portugal's initial imbalances and need for assistance Macroeconomic imbalances Low GDP and productivity for more

1 Portugal Programme Assessment European Commission, DG ECFIN 15 May, 2014 2 Root causes of Portugal's initial imbalances and need for assistance Macroeconomic imbalances Low GDP and productivity for more

Monetary integration. Giovanni Di Bartolomeo Sapienza University of Rome

Monetary integration Giovanni Di Bartolomeo Sapienza University of Rome The Gold Standard Before World War I, nearly all of the world economy was on the gold standard A government would define a unit of

Monetary integration Giovanni Di Bartolomeo Sapienza University of Rome The Gold Standard Before World War I, nearly all of the world economy was on the gold standard A government would define a unit of

Introduction This book discusses the emergence of a multi-polar currency system. The first chapter examines the implications of the creation of the Euro and its role as a global currency in today s multi-polar

Introduction This book discusses the emergence of a multi-polar currency system. The first chapter examines the implications of the creation of the Euro and its role as a global currency in today s multi-polar

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014 Cohesion Policy and economic governance: complementing each other Background paper September

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014 Cohesion Policy and economic governance: complementing each other Background paper September

Euro Zone s Economic Outlook and What it Means for the United States

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

WELCOME TO THE WEBINAR WEBINAR LINK: HTTP://FRBATL.ADOBECONNECT.COM/ECONOMY/ DIAL-IN NUMBER (MUST USE FOR AUDIO): 855-377-2663 ACCESS CODE: 71032685 Euro Zone s Economic Outlook and What it Means for the

Will it ever fly? Stockholm, May 12, 2011. Robert Bergqvist Chief Economist, SEB Group robert.bergqvist@seb.se Tel: +4670 445 1404

Will it ever fly? Stockholm, May 12, 2011 Robert Bergqvist Chief Economist, SEB Group robert.bergqvist@seb.se Tel: +4670 445 1404 1 2 2010 1997 1997 The future of the euro Three questions that need an

Will it ever fly? Stockholm, May 12, 2011 Robert Bergqvist Chief Economist, SEB Group robert.bergqvist@seb.se Tel: +4670 445 1404 1 2 2010 1997 1997 The future of the euro Three questions that need an

UK Response to the Commission Green Paper on Capital Markets Union BUILDING A STRONG CAPITAL MARKETS UNION

UK Response to the Commission Green Paper on Capital Markets Union BUILDING A STRONG CAPITAL MARKETS UNION The UK welcomes the opportunity to respond to this consultation. Creating a Capital Markets Union

UK Response to the Commission Green Paper on Capital Markets Union BUILDING A STRONG CAPITAL MARKETS UNION The UK welcomes the opportunity to respond to this consultation. Creating a Capital Markets Union

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

FINANCIAL STABILITY FORUM. FSF Principles for Cross-border Cooperation on Crisis Management

FSF Principles for Cross-border Cooperation on Crisis Management 2 April 2009 Preface These high-level principles for cross-border cooperation on crisis management have been developed and endorsed by the

FSF Principles for Cross-border Cooperation on Crisis Management 2 April 2009 Preface These high-level principles for cross-border cooperation on crisis management have been developed and endorsed by the

GROUP OF TEN REPORT ON CONSOLIDATION IN THE FINANCIAL SECTOR

GROUP OF TEN REPORT ON CONSOLIDATION IN THE FINANCIAL SECTOR January 2001 The present publication can be obtained through the websites of the BIS, the IMF and the OECD: www.bis.org www.imf.org www.oecd.org

GROUP OF TEN REPORT ON CONSOLIDATION IN THE FINANCIAL SECTOR January 2001 The present publication can be obtained through the websites of the BIS, the IMF and the OECD: www.bis.org www.imf.org www.oecd.org

Prudential Lessons from the Global Financial Crisis

Prudential lessons from the Global Financial Crisis A speech delivered to Financial Institutions of NZ 2012 Remuneration Forum in Auckland On 3 May 2012 By Grant Spencer, Deputy Governor, Reserve Bank

Prudential lessons from the Global Financial Crisis A speech delivered to Financial Institutions of NZ 2012 Remuneration Forum in Auckland On 3 May 2012 By Grant Spencer, Deputy Governor, Reserve Bank

Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Ignazio Visco: Rebalancing trade and capital flows

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

the actions of the party who is insured. These actions cannot be fully observed or verified by the insurance (hidden action).

.") Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

Moral Hazard Definition: Moral hazard is a situation in which one agent decides on how much risk to take, while another agent bears (parts of) the negative consequences of risky choices. Typical case:

Vice-President Jyrki Katainen Euro changeover conference 25 September 2014, Vilnius. Introduction. Distinguished Guests, Ladies and Gentlemen,

Vice-President Jyrki Katainen Euro changeover conference 25 September 2014, Vilnius Introduction Distinguished Guests, Ladies and Gentlemen, It is a great pleasure to be here in Vilnius today to mark this

Vice-President Jyrki Katainen Euro changeover conference 25 September 2014, Vilnius Introduction Distinguished Guests, Ladies and Gentlemen, It is a great pleasure to be here in Vilnius today to mark this

A. Introduction. 1. Motivation

A. Introduction 1. Motivation One issue for currency areas such as the European Monetary Union (EMU) is that not necessarily one size fits all, i.e. the interest rate setting of the central bank cannot

A. Introduction 1. Motivation One issue for currency areas such as the European Monetary Union (EMU) is that not necessarily one size fits all, i.e. the interest rate setting of the central bank cannot

ISSUES IN THE REGULATION OF ANNUITIES MARKETS

ISSUES IN THE REGULATION OF ANNUITIES MARKETS E Philip Davis Brunel University West London e_philip_davis@msn.com www.geocities.com/e_philip_davis groups.yahoo.com/group/financial_stability Abstract Annuities

ISSUES IN THE REGULATION OF ANNUITIES MARKETS E Philip Davis Brunel University West London e_philip_davis@msn.com www.geocities.com/e_philip_davis groups.yahoo.com/group/financial_stability Abstract Annuities

The Impact of Bank Capital Regulation on Financing the Economy

IW policy paper 27/2015 Contributions to the political debate by the Cologne Institute for Economic Research The Impact of Bank Capital Regulation on Financing the Economy Comments on the Public Consultation

IW policy paper 27/2015 Contributions to the political debate by the Cologne Institute for Economic Research The Impact of Bank Capital Regulation on Financing the Economy Comments on the Public Consultation

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES. Hamid Raza PhD Student, Economics University of Limerick Ireland

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

Council Conclusions on Finance for Growth and the Long-term Financing of the European Economy. ECOFIN Council meeting Brussels, 9 December 2014

Council of the European Union PRESS EN COUNCIL CONCLUSIONS Brussels, 9 December 2014 Council Conclusions on Finance for Growth and the Long-term Financing of the European Economy ECOFIN Council meeting

Council of the European Union PRESS EN COUNCIL CONCLUSIONS Brussels, 9 December 2014 Council Conclusions on Finance for Growth and the Long-term Financing of the European Economy ECOFIN Council meeting

ACCESS TO FINANCE. of SMEs in the euro area, European Commission and European Central Bank (ECB), November 2013.

, November 2013.") ACCESS TO FINANCE Improving access to finance is essential to restoring growth and enhancing competitiveness. Investment and innovation are not possible without adequate financing. Difficulties in accessing

ACCESS TO FINANCE Improving access to finance is essential to restoring growth and enhancing competitiveness. Investment and innovation are not possible without adequate financing. Difficulties in accessing

Stress Tests as a Policy Tool: The European Experience During the Crisis

Stress Tests as a Policy Tool: The European Experience During the Crisis Athanasios Orphanides MIT Frankfurt, 6 June 2014 1 GDP per capita in the US and the euro area 105 105 100 100 Index 2007Q4=100 95

Stress Tests as a Policy Tool: The European Experience During the Crisis Athanasios Orphanides MIT Frankfurt, 6 June 2014 1 GDP per capita in the US and the euro area 105 105 100 100 Index 2007Q4=100 95

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

How To Get A Better Deal On A Euro Bond

21 st ASSIOM FOREX Congress Speech by the Governor of the Bank of Italy Ignazio Visco Milan, 7 February 2015 The positive signs emerging from the global economy are still accompanied by marked uncertainty.

21 st ASSIOM FOREX Congress Speech by the Governor of the Bank of Italy Ignazio Visco Milan, 7 February 2015 The positive signs emerging from the global economy are still accompanied by marked uncertainty.

A Shared European Policy Strategy for Growth, Jobs, and Stability

A Shared European Policy Strategy for Growth, Jobs, and Stability February 2016 The European project is suffering an unparalleled crisis: the policy reaction to the economic recession and large unemployment

A Shared European Policy Strategy for Growth, Jobs, and Stability February 2016 The European project is suffering an unparalleled crisis: the policy reaction to the economic recession and large unemployment

COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT. Accompanying the document. Proposal for a

EUROPEAN COMMISSION Brussels, XXX SEC(2011) 1227 COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT

EUROPEAN COMMISSION Brussels, XXX SEC(2011) 1227 COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT

The EU budget and SMEs

Briefing The EU budget and SMEs Background information for the BUDG Committee Public Hearing on "The EU budget and SMEs" on 15 July 2015 in the European Parliament in Brussels Introduction Small and medium-sized

Briefing The EU budget and SMEs Background information for the BUDG Committee Public Hearing on "The EU budget and SMEs" on 15 July 2015 in the European Parliament in Brussels Introduction Small and medium-sized

January 2015. Eurogas Views on the Energy Union and Enhancing Supply Security

January 2015 Eurogas Views on the Energy Union and Enhancing Supply Security Eurogas is the association representing the European gas wholesale, retail and distribution sectors. Founded in 1990, its members

January 2015 Eurogas Views on the Energy Union and Enhancing Supply Security Eurogas is the association representing the European gas wholesale, retail and distribution sectors. Founded in 1990, its members

CONSOLIDATION IN THE FINANCIAL SECTOR

GROUP OF TEN CONSOLIDATION IN THE FINANCIAL SECTOR Summary Report January 2001 This publication can be obtained through the websites of the BIS, the IMF and the OECD: www.bis.org www.imf.org www.oecd.org

GROUP OF TEN CONSOLIDATION IN THE FINANCIAL SECTOR Summary Report January 2001 This publication can be obtained through the websites of the BIS, the IMF and the OECD: www.bis.org www.imf.org www.oecd.org

China's debt - latest assessment SUMMARY

China's debt - latest assessment SUMMARY China s debt-to-gdp ratio continues to increase despite the slowing economy. A convincing case can be made that the situation is manageable: the rate of credit

China's debt - latest assessment SUMMARY China s debt-to-gdp ratio continues to increase despite the slowing economy. A convincing case can be made that the situation is manageable: the rate of credit

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

FROM GOVERNMENT DEFICIT TO DEBT: BRIDGING THE GAP

FROM GOVERNMENT DEFICIT TO DEBT: BRIDGING THE GAP Government deficit and debt are the primary focus of fiscal surveillance in the euro area, and reliable data for these key indicators are essential for

FROM GOVERNMENT DEFICIT TO DEBT: BRIDGING THE GAP Government deficit and debt are the primary focus of fiscal surveillance in the euro area, and reliable data for these key indicators are essential for

The Eurozone and Greece: A Client Update

DIMENSIONAL FUND ADVISORS Special Posting The Eurozone and Greece: A Client Update June 2012 Events in the Eurozone, particularly Greece s future participation in the currency union, have been the overwhelming

DIMENSIONAL FUND ADVISORS Special Posting The Eurozone and Greece: A Client Update June 2012 Events in the Eurozone, particularly Greece s future participation in the currency union, have been the overwhelming