Standard Operating Procedures Manual SOPs Finance Reconciliation and Year End closing Presented to: Independent Elections Commission (IEC) Funded and

|

|

|

- Rachel Walters

- 7 years ago

- Views:

Transcription

")

1 Standard Operating Procedures Manual SOPs Finance Reconciliation and Year End closing Presented to: Independent Elections Commission (IEC) Funded and Supported By United Nations Development Programme (UNDP) Kabul- Afghanistan Date: March 2016/ Hoot 1394 Prepared by: BDO- Jordan & SH 1

2 Issue date Hoot 1394/ March 2016 Department Finance SOP No. F-03 Revision No. and date NEW Implemented By Accounting & Finance Department Review authority No. of pages 17 Signature/ stamp 1. Objective and Scope To reconcile expenditures with AFMIS report; and To present a complete and final reporting on the transactions of a ministry/independent agency. The report includes appropriations, prime allotments, all payments, commitments, and remaining unspent balances This SOP will cover the following areas: a) T-8 Bank Reconciliation Report b) M-91 Qatia Report 2. Terms, Definitions & Abbreviations M2: Cash Purchase order (using for petty cash purchases) M3: Purchase order (using for all purchases except petty cash) M7: Goods Received Note (GNR) M10: Advance Request form (both for petty cash other Advance) M12: Advance Acquittal form M16a: Salary Payment Voucher M16b: Expenses Payment Voucher T-8: Bank Reconciliation Report M-91: Qatia Report (year End closing report) GD: General Directorate CEO: Chief Executive Officer IEC: Independent Election Commission of Afghanistan SOP: Standard Operating Procedure AFN: Afghani GRN: Goods Received Note GoIRA: Government of Islamic Republic of Afghanistan PFEML: Public Finance & Expenditure Management Law CoA: Chart of Accounts GOCA: General Officer of Cash Accounting TSA: Treasury Single Account 3. Tasks, Responsibilities and Accountability Task Authorized Responsible 2

3 T-8 Bank Reconciliation Report CEO Cashier & GOCA Preparing M-91 Qatia Report CEO GOCA 4. Operating procedure a) T-8 Bank Reconciliation Report All Mustofiats and line ministries/independent agencies are required on a monthly basis to reconcile any bank statements/ AFMIS report with accounting transactions. They do this by preparing a T 8 Form using the M 30 Bank Ledger as the source and comparing it to the Treasury for review. The T 8 Form provides summary information on a bank account records including opening and closing balances, deposits, withdrawals, and unpresented checks (These are checks that have been issued by the Treasury or Mustofiat but have not been cashed). It also details banking transactions that have not been recorded in the budget unit s accounting records. Any discrepancies identified in the T 8 form between bank transactions and accounting records must be reviewed and promptly fixed. Corrections in the General Ledger are processed by preparing the M 33 Journal Voucher and recording the adjustment in AFMIS. If adjustments to bank records are required, then the Treasury will send a letter to DAB detailing the discrepancy and request the appropriate transfer of funds. Journal Vouchers and Correcting Entries: All correcting entries of accounting transactions are process through the use of the M 33 Journal Voucher Form. It can be used to change any account including corrections to expenditures, revenues or advances. Treasury or Mustofiat personnel will prepare the M 33 Form and then enter the information in AFMIS. They will file the copy. Expenditure Reconciliation: After the budget section of primary budgetary units complete their reconciliations with Qatia Unit, the bookkeeping unit of primary budget units will receive their twelve (12) month expenditure report from Treasury prepared from AFMIS. Budget units will then reconcile this report with their maintained M 20 ledgers. If there no differences then the primary budget unit will send a signed report to the Qatia Unit verifying that AFMIS information reconciles with their ledger accounts. If differences exist between the M 20 Ledger and AFMIS, the discrepancies should be reported to Reconciliation Unit of Treasury. The Reconciliation Unit will review the discrepancies and make correction entries as required. 3

4 M30 Bank Ledger: The M 30 Bank Ledger is used to keep a running balance of transactions in a Mustofiat expenditure or revenue bank account. It records all credits and debits from bank transfers, disbursements or revenue deposits. All Mustofiats should maintain the M 30 Bank Ledger for each of their bank accounts. (See Appendix D 38 with detailed instructions on how to prepare the M 30 Bank Ledger.) Error! Reference source not found.bank Reconciliation process Flow provides a graphical presentation of the process. b) M-91 Qatia Report All line ministries and independent agencies at the end of each fiscal year close their ledgers and accounts and prepare M-91 Qatia Reports, which is then reconciled by Treasury and used to create a consolidated M-91 Report (Qatia) for the whole government. The M-91 Report includes summary information on ministry/independent agency appropriations, adjustments, allotments, expenditures, commitments and liquidations, prepayments/advances and acquittals including remaining allotment and appropriations balances. The budget and accounting information is categorized by major object expenditure code. The source data of the M-91 Qatia Report is the final Consolidated M-22 Monthly Status of Allotment Report by Primary Budget Unit of the fiscal year and the M-38a Budget Control Ledger maintained by the line ministries and independent agencies. These two documents are segregated by either allotment or appropriation and thus are also categorized by major object expenditure code. As an intermediate step transfer M-22 and M-38a data into the M-91 worksheet to consolidate data by major object code. Thus, one M-91 worksheet will be used for each major object code. 4

5 Annex 1: Bank Reconciliation Process Flow 5

6 5. Related Documents T-8 Bank Reconciliation Ministry of Finance - Treasury Department Form T- 8 - Bank Reconciliation Statement Section A: (This Section shall be filled by Accounting Office) 1. Budget Unit 2. Bank Name 3. Bank Account No. 4. Month 5. Year 6. Bank Unit Records a. Opening Bank Balance Amount b. Total Receipts c. Total Withdrawals d. Closing Bank Balance 7. Deduct: Unpresented Checks Date Check No. Issued To Amount 8. Total Unpresented Checks 9. Subtotal (Closing Bank Balance - Total Unpresented Checks) 10. Add/Deduct: Entries Not in Bookkeeping Entry No. Entry Details Amount 11. Total of Entries Not in Bookkeeping 12. Balance as per Payment Unit Records (Subtotal +/- Entries not in Bookkeeping) Section B: Review and Authorization 13. Payment Manager (Sign & Date) 14. Bank Manager (Sign & Date) 15. Authorizing Authority (Sign & Date) 6

7 T-8 Instructions Purpose: To reconcile expenditures with bank statements Prepare an original and one (1) copy as follows: Section A: (This section shall be filled by Bookkeeping Office) 1. Unit Enter the name of the organizational unit to which the T-8 Form applies. 2. Bank Name Enter the name of the bank used by the unit. 3. Bank Account No. Enter the bank account number which is being reconciled. 4. Month Enter the month of the T-8 reconciliation. 5. Year Enter the year of the T-8 reconciliation. 6. Bank Unit Records Record information related to cash deposits and withdrawals from the budget unit bank account. a. Opening Bank Balance Enter the opening bank balance of the based on the closing bank balance of the T-8 Form from the previous month. b. Total Receipts Enter total receipts that have been deposited in the bank account with a deposit date in the month. c. Total Withdrawals Enter total withdrawals that have been taken from the bank account with a deposit date in the month. d. Closing Bank Balance Calculate the Closing Bank Balance by adding Total Receipts and Opening Bank Balance and subtracting Closing Bank Balance. 7. Deduct: not presented Cheques Provide information related to Cheques that have been written but not yet presented to the bank for cashing. a. Date Enter the date of the not presented Cheque. b. Cheque No. Enter the Cheque number of the not presented Cheque. c. Issue to Enter the name of the person to which the Cheque was presented. d. Amount Enter the amount of the not presented Cheque. 8. Total not presented Cheques Sum the Amount of all the not presented Cheques listed in Field Subtotal (Closing Bank Balance Total not presented Cheques) Subtract Field 8 - Total not presented Cheques from the Field 6d - Closing Bank Balance. 10. Add/Deduct: Entries Not in Bookkeeping In this section add or deduct any bank transactions (withdrawals/deposits) that are known not to be in accounting ledger. a. Entry No. Enter the entry no. of the bank transaction. b. Entry Details Enter details related to the bank transaction. c. Amount Enter the amount of the bank transaction not in bookkeeping 11. Total of Entries Not in Bookkeeping Sum the Amount of entries not in bookkeeping listed in Field Balance as per Payment Unit Records (Subtotal +/-Entries not in Bookkeeping) Add Field 11 - Total of Entries Not in Bookkeeping to Field 9 - Subtotal. 7

8 Section B: Review and Authorization 13. Payment Manager (Sign & Date) This space is for the Payment Manager to sign and date after filling out the Form. 14. Bank Manager (Sign & Date) This space is for the bank manager to sign and date to verify the accuracy of the Form. 15. Authorizing Authority (Sign & Date) This space is for the Authorizing Authority at the Mustofiat to sign and date in order to approve the final T-8 Form. AFMIS: None Distribution: Original Bookkeeping Office/Mustofiat Copy Treasury/Mustofiat 8

9 M-30 Bank Ledger: 9

10 M 30 Instructions: Purpose: To record bank transactions for Mustofiats bank accounts and track balances Maintain the ledger as follows: 1) Ministry/Org. Enter the name of the organization/ministry to which the ledger applies. 2) Location Name & Code Enter the location name and four (4) digit location code of the office where the bank account is managed. 3) Bank Account No. Enter the bank account number which the ledger is tracking. 4) Bank Name Enter the bank name of the account. 5) Bank Reconciliation Period Enter the period of time that the M 30 Bank Ledger is recording by adding a from date and To date. 6) Date 7) Checks Received Provide information related to checks receiver or electronic transfers received. a. Check No. Enter the check number or transaction code for electronic transfers. b. Amount Enter the amount of the check or electronic transfer. 8) Checks Paid a. Check No. Enter the check number or transaction code for electronic transfers. b. M 16 No. Enter the M 16 Form serial number which was used to process the check or electronic transfer. c. Amount Enter the amount of the check or electronic transfer. d. Expiration Date Enter the expiration of the check disbursed by Treasury. 9) Balance Maintain a running balance of the bank account. Each time a transaction or check is posted to the ledger update the balance either by debiting or crediting it by the amount of the Check Received or Check Paid. AFMIS Transactions: None Distribution: Original Bookkeeping Office/Mustofiat 10

11 M-33 Journal voucher: 11

12 M 33 Instructions: Purpose: To record accounting transactions not specifically provided for by other accounting records (adjustment). Prepare an original as follows: Section A: (This Section is to be filled by the Bookkeeping Office) 1) Journal Voucher No. Enter a Journal Voucher serial number beginning with 1 prefixed by the ministry number. 2) Doc Name & Ref No. Enter the serial number of the M 16 Form or M 29 Form from the original transaction this Journal Voucher will be modifying. 3) Original EV No. Enter the electronic voucher number of the original transaction this Journal Voucher will be modifying. 4) Fiscal Year Enter the fiscal year in which the original transaction occurred. 5) Post Date Enter the posting date of the Journal Voucher transaction. 6) Coding Block Enter each section of the expenditure coding block to which transactions in the Journal Voucher will apply. a. Org. (4) Insert the four (4) digits Sub-organization Code of the ministry. b. Project (6) Insert the six (6) digits Project Code. c. Program (5) Insert the five (5) digits Program Code. d. Fund (5) Insert the five (5) digit Fund Component. e. Location (4) Insert the four (4) digit District Code. f. Object (5) Insert the five (5) digits Object Code. 7) Amount a. Debit Enter the debit amount of the transaction to be processed referenced by the coding block. b. Credit Enter the credit amount of the transaction to be processed referenced by the coding block. 8) Total Sum the total debits and credits for the referenced coding blocks. 9) Remarks Enter any additional comments describing the Journal Voucher transactions. Section B: Review and Authorization 10) Authorizing Authority (Sign & Date) This space is provided to the appropriate authorizing authority to sign and date in order to approve the Journal Voucher. AFMIS Transactions: The debits and credits should be posted in the appropriate AFMIS Module using the account recorded in Field 6 Coding Block. Distribution: Original Treasury 12

13 13

14 Detailed M91 Worksheet 14

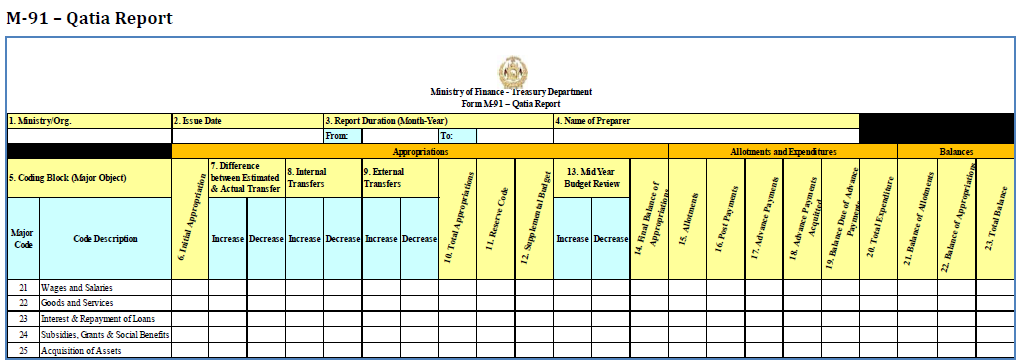

15 M-91 Instructions Purpose: To present a complete and final reporting on the transactions of a ministry/independent agency. The report includes appropriations, prime allotments, sub allotments to provinces, internal transfer, External transfer, Midyear budget review, Expenditures, commitments, and remaining unspent balances This form is the summary shape of yearly financial reporting (M91), in addition the organization can attached the detailed report with it as per the requirement Prepare an original and one (1) copy as follows: 1) Ministry/Org. Enter the name of the line ministry/independent agency to which the Qatia applies. 2) Issue Date Enter the date the report is completed. 3) Report Duration (Month-Year) Enter the duration (start & end) of year and month of the Final Accounting Report Form. 4) Name of Preparer - Enter the name of the individual who prepared the Final Accounting Report. 5) Coding Block (Major Object) Enter two (2) digit object code blocks will be pre populated data for the Final Accounting Report. 6) Initial Appropriation Enter the appropriation given to the line ministry/independent agency at the beginning of the year. 7) Difference between Estimated and Actual Transfers(Development Budget Only) a. Increases Enter the total increases of the differences between estimated transfer of funds from prior allotments and actual transfers. b. Decreases - Enter the decreases of the differences between estimated transfer of funds from prior allotments and actual transfers 8) Internal Transfers a. Increases Enter the total increases in internal transfers of funds between appropriations of the line ministry/independent agency. b. Decreases - Enter the total decreases in internal transfers of funds between appropriations of the line ministry/independent agency. 9) External Transfers a. Increases Enter the total appropriations received from other line ministries/independent agencies. b. Decreases - Enter the total appropriations transferred to other line ministries/independent agencies. 10) Total Appropriations - Calculate total appropriations as the sum of Field 6 Initial Appropriation, Field 7 Difference between Estimated and Actual Transfers, and Field 8 Internal Transfers, and Field 9 External Transfers. 15

16 11) Reserve Code (Development Budget Only) Enter any funds that were transferred to the line ministry/independent agency from the reserve funds used to make foreign exchange disbursements. 12) Supplemental Budget Enter any additional appropriations received from supplemental budgets enacted by Parliament. 13) Mid-Year Budget Review a. Increases Enter the total of any increases in appropriations as a result of the mid-year budget review. b. Decreases Enter the total of any decreases in appropriations as a result of the mid-year budget review. 14) Final Balance of Appropriations Calculate the Final Balance of Appropriations as the sum of Field 10 Total Appropriation, Field 11 Reserve Code, and Field 12 Supplemental Budget, and Field 13 Mid Year Budget Review. 15) Allotments Enter the amount of allotments received by the line ministry/independent agency. 16) Post Payments Enter total value post payments made by the line ministry/independent agency. 17) Advance Payments Enter the total value advance payments made by the line ministry/independent agency. 18) Advance Payment Acquittals Enter the total value of prepayments that were acquitted. 19) Balance Due of Advance Payments Calculate the Balance of Due Advance Payments by subtracting Field 18 - Advance Payment Acquittals from the Field 17 - Advance Payments. 20) Total Expenditures Calculate total expenditures by line ministry/independent agency as the sum of Field 16 - Post Payments and Field 18 Advance Payment Acquittals. 21) Balance of Allotments Calculate Balance of Allotments by subtracting Field 20 - Total Expenditures from Field 15 - Allotments. 22) Balance of Appropriations Calculate Balance from Appropriations by subtracting Field 11 - Allotments from Field 14 Final Balance of Appropriations. 23) General Balance Calculate the General Balance as the sum of Field 21 Balance of Allotments and Field 22 - Balance from Appropriations. AFMIS Transactions: None Distribution: Original Bookkeeping Office Copy Treasury 6. References 16

17 Accounting Manual 1.26 of GoIRA Financial Regulations Developed pursuant to Public Finance and Expenditure Management Law, Gazette #893 CoA ( Chart of Accounts) 7. Attachments M-38a T-8 M30 M-33 M-91 17

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

Public Finance and Expenditure Management Law

Public Finance and Expenditure Management Law Chapter one General provisions Article one. The basis This law has been enacted in consideration of Article 75, paragraph 4 of the Constitution of Afghanistan

Public Finance and Expenditure Management Law Chapter one General provisions Article one. The basis This law has been enacted in consideration of Article 75, paragraph 4 of the Constitution of Afghanistan

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES AND ECONOMIC DEVELOPMENT TECHNICAL ASSISTANCE Comptroller OFFICE OF THE STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT SERVICES & ECONOMIC

ACCOUNTING ASSISTANT

MICHIGAN DEPARTMENT OF CIVIL SERVICE JOB SPECIFICATION ACCOUNTING ASSISTANT JOB DESCRIPTION Employees in this job correct, process and reconcile a wide variety of accounting documents such as invoices,

MICHIGAN DEPARTMENT OF CIVIL SERVICE JOB SPECIFICATION ACCOUNTING ASSISTANT JOB DESCRIPTION Employees in this job correct, process and reconcile a wide variety of accounting documents such as invoices,

District and Provincial Treasuries will pay the following accounts:

SECTION 8: PROCESSING PAYMENTS AND ACCOUNTS All claims for payments for a Local-level Government shall be processed either in a District/Provincial Treasury or at a Cash Office situated in the vicinity

SECTION 8: PROCESSING PAYMENTS AND ACCOUNTS All claims for payments for a Local-level Government shall be processed either in a District/Provincial Treasury or at a Cash Office situated in the vicinity

LODGE AUDIT PROGRAM. A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by

LODGE AUDIT PROGRAM A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by Committee on Finance & Update by the Grand Secretary 2009 Most Worshipful Grand Lodge

LODGE AUDIT PROGRAM A guide to conducting an audit of Lodge and Building Association Financial Records. Prepared by Committee on Finance & Update by the Grand Secretary 2009 Most Worshipful Grand Lodge

Monitoring of controls Information System Control procedures

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

Chapter 7 Define internal control Organizational plan and all the related measures to: Congress passed SOX after the Enron and WorldCom scandals 3 4 6 Monitoring of controls Information System Control

INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL CONTROL OVER CASH RECEIPTS

Internal Control over the followings is included in the syllabus: INTERNAL CONTROL OVER SALES INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL

Internal Control over the followings is included in the syllabus: INTERNAL CONTROL OVER SALES INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL

LEHMAN COLLEGE: DEPARTMENTAL RETENTION SCHEDULE 11/8/2013 ACCOUNTS PAYABLE. List of cost center codes for all College expenditures

AP-1 Appropriations of Expenditure Codes List of cost center codes for all College expenditures 6 years after superseded or obsolete General 9[9] b AP-2 Metrics Reports Reports prepared for the VP of Administration

AP-1 Appropriations of Expenditure Codes List of cost center codes for all College expenditures 6 years after superseded or obsolete General 9[9] b AP-2 Metrics Reports Reports prepared for the VP of Administration

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

What are the elements of an accounting system?

What are the elements of an accounting system? An accounting system is comprised of accounting records (checkbooks, journals, ledgers, etc.) and a series of processes and procedures assigned to staff,

What are the elements of an accounting system? An accounting system is comprised of accounting records (checkbooks, journals, ledgers, etc.) and a series of processes and procedures assigned to staff,

Vouchers for Reproductive Health Services Project

Vouchers for Reproductive Health Services Project Vouchers for Reproductive Health Services Project ( VMA ) Address: PO Box 585 # 40 F, Corner Street 167 & 426, Sangkat Toul Tom Poung II, Khan Chamkar

Vouchers for Reproductive Health Services Project Vouchers for Reproductive Health Services Project ( VMA ) Address: PO Box 585 # 40 F, Corner Street 167 & 426, Sangkat Toul Tom Poung II, Khan Chamkar

Financial Reporting for Schools. Financial Services Division

Financial Reporting for Schools Financial Services Division Published by the Communications Division for Financial Services Division Department of Education and Early Childhood Development Melbourne November

Financial Reporting for Schools Financial Services Division Published by the Communications Division for Financial Services Division Department of Education and Early Childhood Development Melbourne November

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

Financial Accounting: Assets FA 2 Module 6. Handouts. Current financial assets And current liabilities. Presented by: Laura Dallas, CGA

Accounting: Assets FA 2 Module 6 Handouts Current financial assets And current liabilities Presented by: Laura Dallas, CGA Note: this information is prepared from the best information I have available

Accounting: Assets FA 2 Module 6 Handouts Current financial assets And current liabilities Presented by: Laura Dallas, CGA Note: this information is prepared from the best information I have available

Financial Accounting. John J. Wild. Sixth Edition. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 06 Reporting and Analyzing Cash and Internal Controls Conceptual

DoD Financial Management Regulation Volume 12, Chapter 8 + August 2002

SUMMARY OF MAJOR CHANGES TO DOD 7000.14-R, VOLUME 12, CHAPTER 8 FOREIGN NATIONAL EMPLOYEES SEPARATION PAY ACCOUNT, DEFENSE New and revised instructions are indicated by a + placed immediately before the

SUMMARY OF MAJOR CHANGES TO DOD 7000.14-R, VOLUME 12, CHAPTER 8 FOREIGN NATIONAL EMPLOYEES SEPARATION PAY ACCOUNT, DEFENSE New and revised instructions are indicated by a + placed immediately before the

Office of the CONTROLLER GENERAL OF ACCOUNTS CGA Complex, G-5/2, ISLAMABAD

Office of the CONTROLLER GENERAL OF ACCOUNTS CGA Complex, G-5/2, ISLAMABAD The Accountant General Pakistan Revenue, ISLAMABAD No.AC-II/1-39/08-Vol-V/632 Dated: September 24, 2008 Subject:- REVISED PROCEDURE

Office of the CONTROLLER GENERAL OF ACCOUNTS CGA Complex, G-5/2, ISLAMABAD The Accountant General Pakistan Revenue, ISLAMABAD No.AC-II/1-39/08-Vol-V/632 Dated: September 24, 2008 Subject:- REVISED PROCEDURE

PRESCRIBED CODING SYSTEM

Revised 2/1/2004 SECTION H PRESCRIBED CODING SYSTEM All school districts shall utilize the prescribed coding system as detailed in Sections H, I, J, K, L and M of this manual. This coding system must be

Revised 2/1/2004 SECTION H PRESCRIBED CODING SYSTEM All school districts shall utilize the prescribed coding system as detailed in Sections H, I, J, K, L and M of this manual. This coding system must be

AUSTIN INDEPENDENT SCHOOL DISTRICT INTERNAL AUDIT DEPARTMENT PAYROLL AUDIT PROGRAM

PAYROLL GENERAL: The Payroll Department is responsible for processing all District payrolls and compliance with all rules and regulations pertaining to and/or resulting from payroll operations which includes

PAYROLL GENERAL: The Payroll Department is responsible for processing all District payrolls and compliance with all rules and regulations pertaining to and/or resulting from payroll operations which includes

- 1 - School Based Funds Reference Guide

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

EVERYTHING YOU WANTED TO KNOW ABOUT MID-YEAR & YEAR- END FINANCIALS

EVERYTHING YOU WANTED TO KNOW ABOUT MID-YEAR & YEAR- END FINANCIALS Rev. 11/2015 1 of 7 TABLE OF CONTENTS Introduction... 3 Getting Started. 3 Filling out the Troop/Group Finance Report... 4 Submitting

EVERYTHING YOU WANTED TO KNOW ABOUT MID-YEAR & YEAR- END FINANCIALS Rev. 11/2015 1 of 7 TABLE OF CONTENTS Introduction... 3 Getting Started. 3 Filling out the Troop/Group Finance Report... 4 Submitting

Flow Chart of Financial Monitoring & Planning in WebSAMS version 2.0

Financial Monitoring & Planning (FMP) School Management School Level and Session to be retrieved from School Management Module School Accounting Information Accounting Year Maintenance Chart of Account

Financial Monitoring & Planning (FMP) School Management School Level and Session to be retrieved from School Management Module School Accounting Information Accounting Year Maintenance Chart of Account

Accounting for Cash. College Accounting. Heintz & Parry CASH INTERNAL CONTROL OPENING A CHECKING ACCOUNT

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Assertion Control objectives Controls Tests of controls Occurrence and existence

Internal Control over Payroll Assertion Control objectives Controls Tests of controls Occurrence and existence Payment is made only to bona fide employees of the entity. Segregation of duties between HR

Internal Control over Payroll Assertion Control objectives Controls Tests of controls Occurrence and existence Payment is made only to bona fide employees of the entity. Segregation of duties between HR

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

Mango s Health Check. How healthy is financial management in your not-for-profit organisation?

How healthy is financial management in your not-for-profit organisation? Version 3 2009 Mango 2nd Floor East, Chester House, George Street, Oxford OX1 2AU Phone +44 (0)1865 423818 Fax +44 (0)1865 423560

How healthy is financial management in your not-for-profit organisation? Version 3 2009 Mango 2nd Floor East, Chester House, George Street, Oxford OX1 2AU Phone +44 (0)1865 423818 Fax +44 (0)1865 423560

GRAP Implementation Guide for Municipalities

GRAP Implementation Guide for Municipalities TOPIC 2.3: BANK ACCOUNTS AND CASH This section of the manual sets out the FSOP s that need to be executed by the municipality regarding Bank Balances and Cash.

GRAP Implementation Guide for Municipalities TOPIC 2.3: BANK ACCOUNTS AND CASH This section of the manual sets out the FSOP s that need to be executed by the municipality regarding Bank Balances and Cash.

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

Financial Regulations and Rules

Financial Regulations and Rules Contents Regulation 1. Applicability... 276 Rule 101.1. Applicability and authority... 276 Rule 101.2. Responsibility... 277 Regulation 2. The financial period... 277 Regulation

Financial Regulations and Rules Contents Regulation 1. Applicability... 276 Rule 101.1. Applicability and authority... 276 Rule 101.2. Responsibility... 277 Regulation 2. The financial period... 277 Regulation

FORM 31. (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT

LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT") FORM 31 (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT Instructions 1. This form must be filed within six months from the end of the law firm financial year. 2. If space is insufficient,

FORM 31 (Rule 179) LAW SOCIETY OF YUKON LAW FIRM AND ACCOUNTANT S REPORT Instructions 1. This form must be filed within six months from the end of the law firm financial year. 2. If space is insufficient,

COMPTROLLER OF ACCOUNTS

COMPTROLLER OF ACCOUNTS Ministry of Finance Government of the Republic of Trinidad Tobago Accounting Manual Prepared by the Financial Management Branch, Treasury Division, Ministry of Finance TABLE OF

COMPTROLLER OF ACCOUNTS Ministry of Finance Government of the Republic of Trinidad Tobago Accounting Manual Prepared by the Financial Management Branch, Treasury Division, Ministry of Finance TABLE OF

Process diagram. Legend of symbols. Functional process. Information flow

Names of departments or organizational entities responsible for carrying out the process Process diagram Legend of symbols Functional process Process Description Information flow Data base/data store Information

Names of departments or organizational entities responsible for carrying out the process Process diagram Legend of symbols Functional process Process Description Information flow Data base/data store Information

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Reconciling the Bank Statement

PrinciplesofAccounting HelpLesson #6 Reconciling the Bank Statement By Laurie L. Swanson Cash is one of the most important assets a business owns. Cash is the primary asset used to acquire other assets

PrinciplesofAccounting HelpLesson #6 Reconciling the Bank Statement By Laurie L. Swanson Cash is one of the most important assets a business owns. Cash is the primary asset used to acquire other assets

Great Aycliffe Town Council. Purchase Ordering and Payment for Goods and Services Policy

Great Aycliffe Town Council Purchase Ordering and Payment for Goods and Services Policy Finance Section April 2013 1.0 Introduction 1.1 This policy sets out the Council s arrangements for ordering, receiving,

Great Aycliffe Town Council Purchase Ordering and Payment for Goods and Services Policy Finance Section April 2013 1.0 Introduction 1.1 This policy sets out the Council s arrangements for ordering, receiving,

COMPTROLLER OF ACCOUNTS CIRCULAR NO. 13 DATED 2010 SEPTEMBER 01 TO: ALL PERMANE NT SECRETARIES AND HEADS OF DEPARTMENTS SUBJECT:

FM: 3/2/187 COMPTROLLER OF ACCOUNTS CIRCULAR NO. 13 DATED 2010 SEPTEMBER 01 TO: ALL PERMANE NT SECRETARIES AND HEADS OF DEPARTMENTS SUBJECT: UPGRADE OF THE CHEQUE WRITING SYSTEM AND MATTERS RELATING THERETO

FM: 3/2/187 COMPTROLLER OF ACCOUNTS CIRCULAR NO. 13 DATED 2010 SEPTEMBER 01 TO: ALL PERMANE NT SECRETARIES AND HEADS OF DEPARTMENTS SUBJECT: UPGRADE OF THE CHEQUE WRITING SYSTEM AND MATTERS RELATING THERETO

FINANCIAL POLICIES INDEX

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the

INTERNATIONAL DIPLOMA PROGRAM ON BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the MODERN PRACTICAL METHODS OF ACCOUNTING Trained and competent bookkeeping

INTERNATIONAL DIPLOMA PROGRAM ON BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the MODERN PRACTICAL METHODS OF ACCOUNTING Trained and competent bookkeeping

ACCT 652 Accounting. Review of last week. Should you always take discounts? 5/17/15. ACCT652 Week 4 1

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

ACCT 652 Accounting Week 4 Special Journals, Cash, and Internal Controls Some slides Times Mirror Higher Education Division, Inc. Used by permission Michael D. Kinsman, Ph.D. Review of last week Some highlights

Introduction to Disbursement Services

Introduction to Disbursement Services Purpose Disbursement Services is a service unit within the University business organization, reporting to the Controller. The department's responsibility is to monitor,

Introduction to Disbursement Services Purpose Disbursement Services is a service unit within the University business organization, reporting to the Controller. The department's responsibility is to monitor,

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity National Assembly RESOLUTION of the NATIONAL ASSEMBLY of the Lao People s Democratic Republic No.025/NA On the Adoption of

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity National Assembly RESOLUTION of the NATIONAL ASSEMBLY of the Lao People s Democratic Republic No.025/NA On the Adoption of

Finance Procedure 2.11 PURCHASING & ACCOUNTS PAYABLE PROCEDURE CENTRAL OFFICE

Finance Procedure 2.11 PURCHASING & ACCOUNTS PAYABLE PROCEDURE CENTRAL OFFICE FP2.11 Version 003 Sept14 1.0 INTRODUCTION This procedure sets out the finance processes and responsibilities for administering

Finance Procedure 2.11 PURCHASING & ACCOUNTS PAYABLE PROCEDURE CENTRAL OFFICE FP2.11 Version 003 Sept14 1.0 INTRODUCTION This procedure sets out the finance processes and responsibilities for administering

Level 1 Certificate in Book-Keeping

LCCI International Qualifications Level 1 Certificate in Book-Keeping Syllabus Effective for examinations to be held after 1 Jan 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email.

LCCI International Qualifications Level 1 Certificate in Book-Keeping Syllabus Effective for examinations to be held after 1 Jan 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email.

This policy applies to all employees who hold or use petty cash funds, including the security, disbursement, reimbursement and use of these funds.

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

BUTTE COUNTY 4 H YOUTH DEVELO0PMENT PROGRAM FINANCIAL FORMS

4 H Financial Forms These forms were revised from the California State 4 H Treasurer's Manual (4H1035, rev 5/2003). Please note this workbook contains the below worksheets without formulas. Form 5.1 Mid

4 H Financial Forms These forms were revised from the California State 4 H Treasurer's Manual (4H1035, rev 5/2003). Please note this workbook contains the below worksheets without formulas. Form 5.1 Mid

LOCAL TRAINING INITIATIVE

Training Standards System LOCAL TRAINING INITIATIVE BOOKS OF ACCOUNT AND RECORD KEEPING Best Practice Guidelines Page 1 of 13 The LTI must comply with public procurement guidelines when purchasing goods

Training Standards System LOCAL TRAINING INITIATIVE BOOKS OF ACCOUNT AND RECORD KEEPING Best Practice Guidelines Page 1 of 13 The LTI must comply with public procurement guidelines when purchasing goods

CASH RECONCILIATION & INTERNAL CONTROLS

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

Introduction to Governmental Accounting

Introduction to Governmental Accounting Karin Slater, CPFO Montrose County School District RE-1J February 25, 2016 Introductions Introduction to Governmental Accounting Name Entity or Government Position

Introduction to Governmental Accounting Karin Slater, CPFO Montrose County School District RE-1J February 25, 2016 Introductions Introduction to Governmental Accounting Name Entity or Government Position

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

The Business Center Handbook

201-201 The Business Center Handbook Revised /201 The Business Center Handbook The Business Center at Education Service Center Region utilizes a business model that streamlines and facilitates sound business

201-201 The Business Center Handbook Revised /201 The Business Center Handbook The Business Center at Education Service Center Region utilizes a business model that streamlines and facilitates sound business

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

CASH: CASH CONTROLS C-173 ACCOUNTING MANUAL Page 1. Contents. I. Introduction 2. II. General Description of Cash Operations 2

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL. TOPIC: Section 11 Institution Accounting 2.1 EFFECTIVE DATE: 06/01/1983

MANUAL. TOPIC: Section 11 Institution Accounting 2.1 EFFECTIVE DATE: 06/01/1983") STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: EFFECTIVE DATE: 06/01/1983 TITLE: Store Inventory

STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: EFFECTIVE DATE: 06/01/1983 TITLE: Store Inventory

1. SEGREGATION OF DUTIES IS ESSENTIAL

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

The way a church handles money can present a positive or negative witness. Churches need to be diligent in handling money to encourage integrity and positive Biblical stewardship. Every step should be

Invoicing Internal Procedure

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects

Loyal Order of Moose Fraternal Education

Loyal Order of Moose Fraternal Education This booklet presents accounting and tax information that may or may not be right for your specific Fraternal Unit. In view of the complex, individual, and specific

Loyal Order of Moose Fraternal Education This booklet presents accounting and tax information that may or may not be right for your specific Fraternal Unit. In view of the complex, individual, and specific

for Sage 100 ERP Bank Reconciliation Overview Document

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Section 2: The Bookkeeping Process (Module 3)

") Section 2: The Bookkeeping Process Dermott Crofton dcrofton@sd62.bc.ca 1 This Section of the Course Bookkeeping Process Double Entry Bookkeeping Rules of Debits and Credits The T-Account Representing transactions

Section 2: The Bookkeeping Process Dermott Crofton dcrofton@sd62.bc.ca 1 This Section of the Course Bookkeeping Process Double Entry Bookkeeping Rules of Debits and Credits The T-Account Representing transactions

CHAPTER XII DOUBLE ENTRY ACCOUNTING SYSTEM

12-1 CHAPTER XII DOUBLE ENTRY ACCOUNTING SYSTEM SECTION A - ACCOUNTING BASIS The accounting basis for recording transactions will vary according to the purpose for which each fund is established. Generally,

12-1 CHAPTER XII DOUBLE ENTRY ACCOUNTING SYSTEM SECTION A - ACCOUNTING BASIS The accounting basis for recording transactions will vary according to the purpose for which each fund is established. Generally,

Accounting Policies & Procedures Manual

Accounting Policies & Procedures Manual Updated and Approved: 1 CAWST Accounting Policies & Procedures Index 1. Accounting Policies APL100 Financial statement concepts and accountability APL210 Cash and

Accounting Policies & Procedures Manual Updated and Approved: 1 CAWST Accounting Policies & Procedures Index 1. Accounting Policies APL100 Financial statement concepts and accountability APL210 Cash and

1.8 PETTY CASH Produced by Plymouth Schools Accountancy Team 72 Updated August 2008

1.8 PETTY CASH 72 PETTY CASH To proceed with the issue of petty cash expenditure reimbursements we suggest that the Petty Cash Requisition form (Section 5.7) is used by all budget holders to keep control

1.8 PETTY CASH 72 PETTY CASH To proceed with the issue of petty cash expenditure reimbursements we suggest that the Petty Cash Requisition form (Section 5.7) is used by all budget holders to keep control

Clare College Financial Policies and Procedures Cash & Banking Procedures

Financial Policies and Procedures Cash & Banking Procedures M:\Bursary\Audit Committee\Financial Procedures -.doc- 1 - Contents 1. Banking Procedures 1.1 Receipt of cash and cheques within a department

Financial Policies and Procedures Cash & Banking Procedures M:\Bursary\Audit Committee\Financial Procedures -.doc- 1 - Contents 1. Banking Procedures 1.1 Receipt of cash and cheques within a department

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 5 Summarizing Changes in Financial Position OBJECTIVES The purpose of this lesson is to show how to summarize the transactions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 5 Summarizing Changes in Financial Position OBJECTIVES The purpose of this lesson is to show how to summarize the transactions

Internal Controls over Cash for Small Nonprofits

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

Internal Controls over Cash for Small Nonprofits Internal controls may be a sensitive issue in small nonprofit organizations. These organizations are built on the concepts of honesty, truthfulness, and

FINANCE COMMITTEE PROCEDURES. Audit Process. Cash Handling

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

1 FINANCE COMMITTEE PROCEDURES Audit Process 1. Internal audits are conducted once a year. 2. The bookkeeper will provide the following information: bank statements, prior year vouchers, and access to

Accounting. Chapter 6

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

Chapter 9. Learning Objectives. Define internal control. Objective 1. Internal Control and Cash

PowerPoint to accompany Chapter 9 Internal Control and Cash Learning Objectives 1. Define internal control 2. Describe good internal control procedures 3. Prepare a bank reconciliation and the related

PowerPoint to accompany Chapter 9 Internal Control and Cash Learning Objectives 1. Define internal control 2. Describe good internal control procedures 3. Prepare a bank reconciliation and the related

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS THROUGHOUT THE MONTH Montana Clerks, Treasurers & Finance Officers Institute ~ May 2014 Darla Erickson, Local Government Services

CASH RECONCILIATIONS ~ RELATED INTERNAL CONTROLS & TRACKING DEBITS & CREDITS THROUGHOUT THE MONTH Montana Clerks, Treasurers & Finance Officers Institute ~ May 2014 Darla Erickson, Local Government Services

BOOKKEEPING WITH COMPUTERS

BOOKKEEPING WITH COMPUTERS INTRODUCTION Whether manual or computerised, bookkeeping is essentially the same. Both methods use the same concept of DOUBLE ENTRY, i.e. Debits () and edits (). Double entry

BOOKKEEPING WITH COMPUTERS INTRODUCTION Whether manual or computerised, bookkeeping is essentially the same. Both methods use the same concept of DOUBLE ENTRY, i.e. Debits () and edits (). Double entry

BANKING AND CASH MANAGEMENT APPENDICES TABLE OF CONTENTS

BANKING AND CASH MANAGEMENT APPENDICES TABLE OF CONTENTS APPENDIX CODE APPENDIX A APPENDIX B APPENDIX TITLE Translation Matrix from Provincial Treasury ORCS (Schedule 890168) to Banking and Cash Management

BANKING AND CASH MANAGEMENT APPENDICES TABLE OF CONTENTS APPENDIX CODE APPENDIX A APPENDIX B APPENDIX TITLE Translation Matrix from Provincial Treasury ORCS (Schedule 890168) to Banking and Cash Management

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

Chapter 7 Fraud, Internal Control, and Cash 高立翰

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Chapter 7 Fraud, Internal Control, and Cash 高立翰 Study Objectives 1. Define fraud and internal control. 2. Identify the principles of internal control activities. 3. Explain the applications of internal

Audit of Cash Balances

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

Audit of Cash Balances Chapter 23 2008 Prentice Hall Business Publishing, Auditing 12/e, Arens/Beasley/Elder 23-1 Learning Objective 1 Show the relationship of cash in the bank to the various transaction

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING IF ANY ARE NOT APPLICABLE, INSERT N/A AS YOUR ANSWER. FIRE DISTRICT YEAR UNDER AUDIT

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

How To Reconcile Account Balance In Gpa

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

CHAPTER II GENERAL LEDGER ACCOUNTS

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

Cash Handling Questionnaire

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

for Sage 100 ERP General Ledger Overview Document

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP General Ledger Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Accounting Systems. On a current basis, schools must establish and maintain the following:

Accounting Systems This appendix is a general guide; it is not intended to replace accounting standards established by the American Institute of Certified Public Accountants (AICPA), Financial Accounting

Accounting Systems This appendix is a general guide; it is not intended to replace accounting standards established by the American Institute of Certified Public Accountants (AICPA), Financial Accounting

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT. Test Code: 4100 Version: 01

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

Manual of Accounting Policies and Procedures Bridgewater State College Foundation Bridgewater Alumni Association Table of Contents MANUAL OF 1 ACCOUNTING 1 POLICIES AND PROCEDURES 1 BRIDGEWATER STATE COLLEGE

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL. February 2014

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL February 2014 I. Introduction The purpose of this manual is to describe all accounting policies and procedures currently in use at The

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL February 2014 I. Introduction The purpose of this manual is to describe all accounting policies and procedures currently in use at The

CANI Financial Policy and Procedures

CANI Financial Policy and Procedures Policy CANI Council is conscious of the need to ensure that all funds received by the organisation are used in accordance with the aims and objectives of CANI; that

CANI Financial Policy and Procedures Policy CANI Council is conscious of the need to ensure that all funds received by the organisation are used in accordance with the aims and objectives of CANI; that

Nonprofit Bookkeeping and Accounting Overview

Nonprofit Bookkeeping and Accounting Overview The following activities should occur regularly as part of the yearly accounting cycle. The accounting cycle includes bookkeeping, generating financial statements

Nonprofit Bookkeeping and Accounting Overview The following activities should occur regularly as part of the yearly accounting cycle. The accounting cycle includes bookkeeping, generating financial statements

Procedures & program of auditing assets. Section one Procedures & program of Auditing Fixed Assets

CHAPTER FOUR Procedures & program of auditing assets Section one Procedures & program of Auditing Fixed Assets 1. Record and inspection 1-1 Examining due procedures of the properties of fixed assets. 1-2

CHAPTER FOUR Procedures & program of auditing assets Section one Procedures & program of Auditing Fixed Assets 1. Record and inspection 1-1 Examining due procedures of the properties of fixed assets. 1-2

Important Disclaimer. Copyright Information

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

Job title: Staff Accountant Receivables

Job title: Staff Accountant Receivables Our Firm Capsim Management Simulations Inc designs, builds and delivers the renowned Capstone Business Simulation and a suite of related business simulations to

Job title: Staff Accountant Receivables Our Firm Capsim Management Simulations Inc designs, builds and delivers the renowned Capstone Business Simulation and a suite of related business simulations to

Basic Bookkeeping. Why Keep Records? What Record Keeping System Should I Use? Last Verified: 2005-10-19

Basic Bookkeeping Last Verified: 2005-10-19 Why Keep Records? Good records will keep you informed about the past and present financial position of your business. Good records will keep you in control and

Basic Bookkeeping Last Verified: 2005-10-19 Why Keep Records? Good records will keep you informed about the past and present financial position of your business. Good records will keep you in control and

AAT Level 2 Certificate in Accounting

AAT Level 2 Certificate in Accounting Qualification specification Version date: July 2014 Ofqual qualification number: 60069090 1 Purpose statement Who is this qualification for? The AAT Level 2 Certificate

AAT Level 2 Certificate in Accounting Qualification specification Version date: July 2014 Ofqual qualification number: 60069090 1 Purpose statement Who is this qualification for? The AAT Level 2 Certificate

Government of Pakistan. Accounting Policies and Procedures Manual

Government of Pakistan Accounting Policies and Procedures Manual Table of Contents Table of Contents 1 Introduction 1.1 1.1 Purpose of the Manual 1.3 1.2 Structure of the Manual 1.4 1.3 Reader Guidance

Government of Pakistan Accounting Policies and Procedures Manual Table of Contents Table of Contents 1 Introduction 1.1 1.1 Purpose of the Manual 1.3 1.2 Structure of the Manual 1.4 1.3 Reader Guidance

www.openmiracle.com SRS

www.openmiracle.com SRS Overview of OPENMIRACLE OpenMiracle is an open source accounting software, ie its sourec code is available free of cost for life time. It is an attempt to make software accounting

www.openmiracle.com SRS Overview of OPENMIRACLE OpenMiracle is an open source accounting software, ie its sourec code is available free of cost for life time. It is an attempt to make software accounting

Payment Procedures. Corruption Prevention Department

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

Payment Procedures Corruption Prevention Department best practices 貪 CONTENTS Pages Introduction 1 Procedural Guidelines 1 Payment Methods 2 Autopay 2 Cheques 3 Petty Cash 3 Payment Records 4 Control and

Province of Newfoundland and Labrador. Report on the Program Expenditures and Revenues of the Consolidated Revenue Fund

Province of Newfoundland and Labrador Report on the Program Expenditures and Revenues of the Consolidated Revenue Fund FOR THE YEAR ENDED 31 MARCH 2013 Province of Newfoundland and Labrador Report on the

Province of Newfoundland and Labrador Report on the Program Expenditures and Revenues of the Consolidated Revenue Fund FOR THE YEAR ENDED 31 MARCH 2013 Province of Newfoundland and Labrador Report on the

DIVISION OF ACCOUNTS AND REPORTS POLICY AND PROCEDURE MANUAL Revision Date 04/03/00 Filing Number 4,271 Date Issued 04/76 Page 1 of 5 Revisions #

Date Issued 04/76 Page 1 of 5 SUBJECT Fund Accounting PURPOSE Financial transactions for all state agencies should be recorded in self-balancing groups of accounts established as funds by law or administrative

Date Issued 04/76 Page 1 of 5 SUBJECT Fund Accounting PURPOSE Financial transactions for all state agencies should be recorded in self-balancing groups of accounts established as funds by law or administrative

Providing Business Solutions to Outsource your Finance Department

Providing Business Solutions to Outsource your Finance Department Independent member firm of www.andrews.ca Business Management Services / 1 Contents I. Introduction: Business Management Services II. Outsource

Providing Business Solutions to Outsource your Finance Department Independent member firm of www.andrews.ca Business Management Services / 1 Contents I. Introduction: Business Management Services II. Outsource

Financial Regulations and Rules of the United Nations

9 May 2003 United Nations Financial Regulations and Rules of the United Nations Secretary-General s bulletin 9 May 2003 United Nations Financial Regulations and Rules of the United Nations Secretary-General

9 May 2003 United Nations Financial Regulations and Rules of the United Nations Secretary-General s bulletin 9 May 2003 United Nations Financial Regulations and Rules of the United Nations Secretary-General

TITLE C193 BUSINESS CREDIT CARDS POLICY AND PROCEDURES DEPARTMENT POLICY

TITLE C193 BUSINESS CREDIT CARDS POLICY AND PROCEDURES DEPARTMENT Corporate Services POLICY DIRECTIVE To provide internal control procedures to ensure proper use and authorisation of Credit Card transactions.

TITLE C193 BUSINESS CREDIT CARDS POLICY AND PROCEDURES DEPARTMENT Corporate Services POLICY DIRECTIVE To provide internal control procedures to ensure proper use and authorisation of Credit Card transactions.