How To Pay Taxes In Brazilian Brazilia

|

|

|

- Piers Freeman

- 3 years ago

- Views:

Transcription

1 Walter Thomaz Junior. International Trade Consultant. Phone:

2 TAXATION ON IMPORTS TAX DUTY Social Contribution

3 TAXATION ON IMPORTS "EXTERNAL" "INTERNAL"

4 TAX 1. External : IMPORT DUTY

5 EXTERNAL TAX Import Duty Assessed on the value of the goods imported. Taxable Event: Entrance of foreigner merchandise on Brazilian territory. Basis: on CIF value. Calculation: CIF X Duty % on TEC. Thomaz Consultores Associados

6 INTERNAL TAXES AND DUES. : I.P.I. - EXCISE TAX. I.C.M.S. - VALUE ADDED TAX. PIS/Cofins SOCIAL CONTRIBUTION.

7 INTERNAL TAXES AND DUES. : I.P.I. (Excise Tax) Assessed : on the value of industrial imported goods. Taxable Event : Clearence on Customs. Basis:CIF + I.I. Calculation : (CIF + Import Duty) X % of I.P.I.

8 INTERNAL TAXES AND SOCIAL CONTRIBUTION: ICMS. - Added Tax on Sales and Services. Assessed: on the value of imported goods. Taxable Event: Clearence on Customs. Basis: CIF + Import Duty + Excise Tax + ICMS Calculation: (CIF + Import Duty +IPI) x % ICMS (1 - %ICMS)

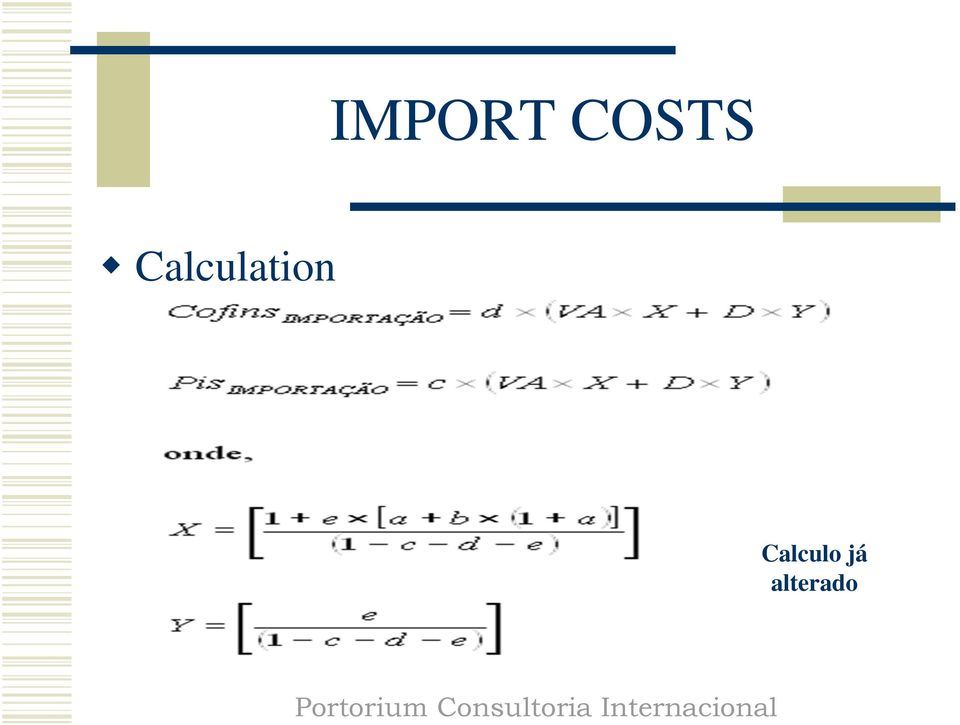

9 INTERNAL TAXES AND DUES. : PIS/Cofins Social Contribution. Assessed: on the value of imported goods. Taxable Event: Entrance of foreigner merchandise on Brazilian territory.

10 Calculation Calculo já alterado

11 VA = CIF a = aliquot of Import Duty b = aliquot of i.p.i. Excise Tax c = aliquot of Pis/Pasep on Importation. d = aliquot of Cofins-Importation. e = aliquot of imposto sobre operações relativas à circulação de mercadorias e sobre prestação de serviços de transporte interestadual e intermunicipal e de comunicação (ICMS) - Added value Tax on Sales and Services. D = others customs expenses (fees, tax, duties etc).

- Added value Tax on")

12 CHARGES: Afrmm Adicional ao Frete para a Renovação da Marinha Mercante: 25% on international sea freight. Siscomex Fee: R$ 40,00 each document. Bill of Landing Fee: average USD Desconsolidation Fee: average USD Bank change fee: USD Customshouse brocker fee: USD

13 EXPENSES: Inland Freight. Customshouse brocker commission: 1% s/cif average. Terminal Handling Charges. Foremanship Fee.

14 Customs goods classification HTUSA The practice demonstrates that is not possible to use HTUSA literally as an NCM code. The correct classification demands the assistance of an expert on brazilian regulamentation.

15 Consequences of a wrong classification: Fine of 1% on CIF wrong classification. Fine of 75% on the diference of the payed duty and the new classification. Fine of 30% on CIF for not having a license on the new classification. Demages on the relationship of the importer and the Customs.

16 For a correct classification: Technical assistence. Official enquiry.

17 SERVICES PROVIDED Establish and open foreign companies in Brazil; Register trademarks and patents; Prepare administrative fiscal procedures to Classify products according to NCM and Brazilian Laws; Prepare custom procedures; Import Product Strategies; Calculate duty and import costs;

18 SERVICES PROVIDED Deals with Special Customs Law; Customs brockerage; Works on Tarrif Reduction; Manage Foreign Trade.

19 Walter Thomaz Junior. International Trade Consultant. Phone:

Brazilian Taxes. Guido Vinci Veirano & Advogados Associados March 2002

Brazilian Taxes Guido Vinci Veirano & Advogados Associados March 2002 Introduction - Legal Standards Federal Constitution of 1988 National Tax Code of 1966 ("CTN") Constitution: establishes the taxing

Brazilian Taxes Guido Vinci Veirano & Advogados Associados March 2002 Introduction - Legal Standards Federal Constitution of 1988 National Tax Code of 1966 ("CTN") Constitution: establishes the taxing

Overview of the Brazilian Tax System

Brazil Upstream Guide Overview of the Brazilian Tax System Upstream taxation and foreign investment 2 I. Overview of the Brazilian Tax System... 3 I.1 Introduction... 3 I.1.A Federal Taxes... 4 I.1.A.1.

Brazil Upstream Guide Overview of the Brazilian Tax System Upstream taxation and foreign investment 2 I. Overview of the Brazilian Tax System... 3 I.1 Introduction... 3 I.1.A Federal Taxes... 4 I.1.A.1.

GLOBAL INDIRECT TAX. Brazil. Country VAT/GST Essentials. kpmg.com TAX

GLOBAL INDIRECT TAX Brazil Country VAT/GST Essentials kpmg.com TAX b Brazil: Country VAT/GST Essentials Brazil: Country VAT/GST Essentials Contents Scope and Rates 2 What supplies are liable to VAT? 2

GLOBAL INDIRECT TAX Brazil Country VAT/GST Essentials kpmg.com TAX b Brazil: Country VAT/GST Essentials Brazil: Country VAT/GST Essentials Contents Scope and Rates 2 What supplies are liable to VAT? 2

NEHRING E ASSOCIADOS ADVOCACIA

CARLOS NEHRING NETTO SUELI AVELLAR FONSECA IVA CHIABRANDO MÁRCIO BELLOCCHI ALESSANDRA MONTEBELO GONSALES CRISTIANO AFONSO NATIVIDADE DANIEL SIBILLE EMERSON SOARES MENDES FRANCISCO NAPOLI JOÃO BURKE PASSOS

CARLOS NEHRING NETTO SUELI AVELLAR FONSECA IVA CHIABRANDO MÁRCIO BELLOCCHI ALESSANDRA MONTEBELO GONSALES CRISTIANO AFONSO NATIVIDADE DANIEL SIBILLE EMERSON SOARES MENDES FRANCISCO NAPOLI JOÃO BURKE PASSOS

TAXATION ON SOFTWARE Dispute Resolution nº 27/2008 of Brazilian Federal Revenue

Brasil 01452-002 SP TAXATION ON SOFTWARE Dispute Resolution nº 27/2008 of Brazilian Federal Revenue In the taxation field, the application given to software still involves some controversy that is related

Brasil 01452-002 SP TAXATION ON SOFTWARE Dispute Resolution nº 27/2008 of Brazilian Federal Revenue In the taxation field, the application given to software still involves some controversy that is related

TAX REDUCTION FOR IMPORTED CAPITAL GOODS IN BRAZIL. The most important thing you need to know!

TAX REDUCTION FOR IMPORTED CAPITAL GOODS IN BRAZIL Tax Exceptions ("Ex"-Tariff) The Tax Exceptions system consists of an instrument through which it is permitted to single out a product or group of products

TAX REDUCTION FOR IMPORTED CAPITAL GOODS IN BRAZIL Tax Exceptions ("Ex"-Tariff) The Tax Exceptions system consists of an instrument through which it is permitted to single out a product or group of products

Merchant Marine Fund (Fundo de Marinha Mercante FMM)

") Merchant Marine Fund (Fundo de Marinha Mercante FMM) 1. What is the Merchant Marine Fund FMM? The Merchant Marine Fund (FMM) was created to provide resources to the development of the Merchant Marine and

Merchant Marine Fund (Fundo de Marinha Mercante FMM) 1. What is the Merchant Marine Fund FMM? The Merchant Marine Fund (FMM) was created to provide resources to the development of the Merchant Marine and

A Basic Primer for a Complex Country Ramon Frias Charles Maniace

More content. More experts. More answers. Indirect Taxation in Brazil A Basic Primer for a Complex Country Ramon Frias Charles Maniace Senior Tax Research Counsel Director - Tax Housekeeping This is one

More content. More experts. More answers. Indirect Taxation in Brazil A Basic Primer for a Complex Country Ramon Frias Charles Maniace Senior Tax Research Counsel Director - Tax Housekeeping This is one

BRAZIL MEANS BUSINESS

BRAZIL MEANS BUSINESS Export Green Trade Mission II: Energy & Environment April 23, 2012 Miguel Hernández Commercial Officer, CS Brazil U.S. Foreign Commercial Service Market Intelligence to help U.S.

BRAZIL MEANS BUSINESS Export Green Trade Mission II: Energy & Environment April 23, 2012 Miguel Hernández Commercial Officer, CS Brazil U.S. Foreign Commercial Service Market Intelligence to help U.S.

NORONHA ADVOGADOS GLOBAL LAWYERS

NORONHA ADVOGADOS GLOBAL LAWYERS São Paulo Rio de Janeiro Brasília Curitiba Recife Belo Horizonte Campo Grande London Lisbon Shanghai Beijing Miami Buenos Aires Johannesburg New Delhi Opportunities and

NORONHA ADVOGADOS GLOBAL LAWYERS São Paulo Rio de Janeiro Brasília Curitiba Recife Belo Horizonte Campo Grande London Lisbon Shanghai Beijing Miami Buenos Aires Johannesburg New Delhi Opportunities and

Session 4: Costing & Pricing How should I price my product?

How should I price my product? Session 5: Approaching the Market Dimitris Kloussiadis & Bob Erwin University of Georgia, SBDC International Trade Center Export-U.com is operated by the US Export Assistance

How should I price my product? Session 5: Approaching the Market Dimitris Kloussiadis & Bob Erwin University of Georgia, SBDC International Trade Center Export-U.com is operated by the US Export Assistance

FISCAL EQUITY: DISTRIBUTIONAL IMPACTS OF TAXATION AND SOCIAL SPENDING IN BRAZIL

FISCAL EQUITY: DISTRIBUTIONAL IMPACTS OF TAXATION AND SOCIAL SPENDING IN BRAZIL Working Paper number 115 October, 2013 Fernando Gaiger Silveira Institute for Applied Economic Research (IPEA) Fernando Rezende

FISCAL EQUITY: DISTRIBUTIONAL IMPACTS OF TAXATION AND SOCIAL SPENDING IN BRAZIL Working Paper number 115 October, 2013 Fernando Gaiger Silveira Institute for Applied Economic Research (IPEA) Fernando Rezende

DHL Customs Services Documentation WayBill Commercial Invoice Packing List. Online Solutions DHL Import Online Express DHL ProView

INDEX Introduction What can be imported by mode required Customs process Taxes and fees Operational flow to Brazil What can be imported by to Brazil mode required Customs process Taxes and fees WayBill

INDEX Introduction What can be imported by mode required Customs process Taxes and fees Operational flow to Brazil What can be imported by to Brazil mode required Customs process Taxes and fees WayBill

Brazil Upstream Guide. Indirect taxation. Upstream taxation and foreign investment

Brazil Upstream Guide Indirect taxation Upstream taxation and foreign investment 2 IV. INDIRECT TAXES... 3 IV.1 Federal Tax on Industrialized Goods IPI... 3 IV.2 State Tax on the Circulation of Merchandise

Brazil Upstream Guide Indirect taxation Upstream taxation and foreign investment 2 IV. INDIRECT TAXES... 3 IV.1 Federal Tax on Industrialized Goods IPI... 3 IV.2 State Tax on the Circulation of Merchandise

Issues Relating To Organizational Forms And Taxation. BRAZIL Demarest e Almeida Advogados

Copyright Lex Mundi Ltd. 2012 Issues Relating To Organizational Forms And Taxation BRAZIL Demarest e Almeida Advogados CONTACT INFORMATION Thiago Giantomassi Demarest e Almeida Advogados Avenida Pedroso

Copyright Lex Mundi Ltd. 2012 Issues Relating To Organizational Forms And Taxation BRAZIL Demarest e Almeida Advogados CONTACT INFORMATION Thiago Giantomassi Demarest e Almeida Advogados Avenida Pedroso

Brazil s customs process can seem complex, but you can avoid major difficulty as long as you know what to expect.

Brazil Overview WELCOME BEM-VINDOS Brazil is the world s sixth largest country both by area and by population, with more than 201 million consumers. In the past two years, it s swapped places with the

Brazil Overview WELCOME BEM-VINDOS Brazil is the world s sixth largest country both by area and by population, with more than 201 million consumers. In the past two years, it s swapped places with the

Doing Business in Brazil

Doing Business in Brazil Law stated as at 01-Jan-2013 Author(s), Demarest Advogados Overview 1. What are the key recent developments affecting doing business in your jurisdiction? In June of 2012 the new

Doing Business in Brazil Law stated as at 01-Jan-2013 Author(s), Demarest Advogados Overview 1. What are the key recent developments affecting doing business in your jurisdiction? In June of 2012 the new

Brazil Round 1. Selected Issues on Brazilian Taxation. Dr. Condorcet Rezende Ulhôa, Canto, Rezende e Guerra - Advogados

Brazil Round 1 Selected Issues on Brazilian Taxation Dr. Condorcet Rezende Ulhôa, Canto, Rezende e Guerra - Advogados Brazilian Tax System - Introduction Basic principles of Brazilian taxation set forth

Brazil Round 1 Selected Issues on Brazilian Taxation Dr. Condorcet Rezende Ulhôa, Canto, Rezende e Guerra - Advogados Brazilian Tax System - Introduction Basic principles of Brazilian taxation set forth

Doing Business in Brazil. Latin America

Doing Business in Brazil Latin America Doing Business in Brazil Doing Business in Brazil - 2009 2009 Baker & McKenzie Materials in this booklet are general comments only, and should not be offered as

Doing Business in Brazil Latin America Doing Business in Brazil Doing Business in Brazil - 2009 2009 Baker & McKenzie Materials in this booklet are general comments only, and should not be offered as

Special report Tax and Brazil

Special report Tax and Brazil The feature, prepared by Deloitte, is the second in the series of reports examining the tax landscape in BRIC countries. The report provides an overview of the tax landscape,

Special report Tax and Brazil The feature, prepared by Deloitte, is the second in the series of reports examining the tax landscape in BRIC countries. The report provides an overview of the tax landscape,

Expanding into Brazil

Expanding into Brazil Support for your Business kpmg.ie Expanding into Brazil 1 Are you looking to expand your business into Brazil? Dynamic Irish businesses are looking to new markets to expand and grow.

Expanding into Brazil Support for your Business kpmg.ie Expanding into Brazil 1 Are you looking to expand your business into Brazil? Dynamic Irish businesses are looking to new markets to expand and grow.

!! !! !! !! MARKET S)INTEREST)IN)INVESTING)IN)COMPANIES MARKET S)INTEREST)IN)INVESTING)IN)COMPANIES EXISTING)INVESTMENT)OPPORTUNITIES)AND)THE)CREATION) AND)DEVELOPMENT)OF)NEW)BUSINESSES MARKET

!! !! !! !! MARKET S)INTEREST)IN)INVESTING)IN)COMPANIES MARKET S)INTEREST)IN)INVESTING)IN)COMPANIES EXISTING)INVESTMENT)OPPORTUNITIES)AND)THE)CREATION) AND)DEVELOPMENT)OF)NEW)BUSINESSES MARKET

THE GEORGE WASHINGTON UNIVERSITY - GWU INSTITUTE OF BRAZILIAN ISSUES - IBI 33 th TAX LOADING IN

THE GEORGE WASHINGTON UNIVERSITY - GWU INSTITUTE OF BRAZILIAN ISSUES - IBI 33 th th MINERVA PROGRAM SPRING, 2013 TAX LOADING IN TELECOMMUNICATIONS IONS SERVICES: A comparative study between the Brazilian

THE GEORGE WASHINGTON UNIVERSITY - GWU INSTITUTE OF BRAZILIAN ISSUES - IBI 33 th th MINERVA PROGRAM SPRING, 2013 TAX LOADING IN TELECOMMUNICATIONS IONS SERVICES: A comparative study between the Brazilian

Porto Alegre 2007 budget: an exercise in fiction

Porto Alegre 2007 budget: an exercise in fiction Paulo Muzell Economist Member of the Coordination Board of Cidade Centro de Assessoria e Estudos Urbanos www.ongcidade.org November 30, 2006 Last October,

Porto Alegre 2007 budget: an exercise in fiction Paulo Muzell Economist Member of the Coordination Board of Cidade Centro de Assessoria e Estudos Urbanos www.ongcidade.org November 30, 2006 Last October,

Cross-Border Buy-and-Sell Transactions

11th Annual Latin American Tax Conference The Biltmore Hotel, Coral Gables, FL March 10-11, 2010 Cross-Border Buy-and-Sell Transactions Argentina Martin J. Barreiro Contents I. Case 1 (Distribution)...1

11th Annual Latin American Tax Conference The Biltmore Hotel, Coral Gables, FL March 10-11, 2010 Cross-Border Buy-and-Sell Transactions Argentina Martin J. Barreiro Contents I. Case 1 (Distribution)...1

Manaus Free Trade Zone. Meeting with Taipei Delegation Brasília, October 25 th, 2013

Manaus Free Trade Zone Meeting with Taipei Delegation Brasília, October 25 th, 2013 MANAUS FREE TRADE ZONE (ZFM) MANAGEMENT MODEL PRESIDENCY OF THE REPUBLIC Ministry of Development, Industry and Foreign

Manaus Free Trade Zone Meeting with Taipei Delegation Brasília, October 25 th, 2013 MANAUS FREE TRADE ZONE (ZFM) MANAGEMENT MODEL PRESIDENCY OF THE REPUBLIC Ministry of Development, Industry and Foreign

Overview of taxation and main tax concerns for Japanese companies in Brazil

Overview of taxation and main tax concerns for Japanese companies in Brazil April 15, 2015 Jorge N. Lopes Jr. 1. Brazilian Main Taxes (1) Direct Taxes on Brazilian Operations Direct Taxes on Brazilian

Overview of taxation and main tax concerns for Japanese companies in Brazil April 15, 2015 Jorge N. Lopes Jr. 1. Brazilian Main Taxes (1) Direct Taxes on Brazilian Operations Direct Taxes on Brazilian

BRAZIL MEANS BUSINESS. In spite of the world financial crisis, Brazil remains an appealing business destination.

BRAZIL MEANS BUSINESS In spite of the world financial crisis, Brazil remains an appealing business destination. GDP compared Latin America (in trillions of US$) REGIONAL DISPARITIES % of total GDP (2008)

BRAZIL MEANS BUSINESS In spite of the world financial crisis, Brazil remains an appealing business destination. GDP compared Latin America (in trillions of US$) REGIONAL DISPARITIES % of total GDP (2008)

The Concise Tax Guide Overview on Taxes in Latin America

The Concise Tax Guide Overview on Taxes in Latin America 2012 Table of Contents Argentina... 1 Brazil... 9 Chile... 19 Colombia... 25 Mexico... 31 Venezuela... 41 Argentina: Overview on Taxes Argentina

The Concise Tax Guide Overview on Taxes in Latin America 2012 Table of Contents Argentina... 1 Brazil... 9 Chile... 19 Colombia... 25 Mexico... 31 Venezuela... 41 Argentina: Overview on Taxes Argentina

FREE TRADE ZONE (ZFM-ZONA FRANCA DE MANAUS), THE WESTERN AMAZON AND THE FREE TRADE AREAS (FTAS).

, THE WESTERN AMAZON AND THE FREE TRADE AREAS (FTAS).") Ministry of 1 INTRODUCTION The purpose of this TAX INCENTIVE GUIDE is to explain the taxation regimes granted to those wishing to apply for tax incentives for producing and trading within the MANAUS FREE

Ministry of 1 INTRODUCTION The purpose of this TAX INCENTIVE GUIDE is to explain the taxation regimes granted to those wishing to apply for tax incentives for producing and trading within the MANAUS FREE

www.pwc.com Brazil macroeconomic and tax overview PwC Tax Brazil

www.pwc.com Brazil macroeconomic and tax overview PwC Tax Brazil December, 2010 Foreword Brazil has matured, both from an economic and political point of view. The economic prospects in 2010 are favorable.

www.pwc.com Brazil macroeconomic and tax overview PwC Tax Brazil December, 2010 Foreword Brazil has matured, both from an economic and political point of view. The economic prospects in 2010 are favorable.

Taxes on Consumption of Goods and Services in Brazil

Taxes on Consumption of Goods and Services in Brazil 1) General Features of Taxation on Consumption 2) Specific Features of Taxes on Consumption 3) Tax Reform of Taxes on Consumption in Brazil Lecturer

Taxes on Consumption of Goods and Services in Brazil 1) General Features of Taxation on Consumption 2) Specific Features of Taxes on Consumption 3) Tax Reform of Taxes on Consumption in Brazil Lecturer

Brazil Import Glossary

Brazil Import Guide Table of Contents. Introduction. DHL Global Forwarding Profile 3. Brazil Import Glossary 4. Brazil Import Regulation Overview 5. Commercial Invoice 6. Air Freight Import Information

Brazil Import Guide Table of Contents. Introduction. DHL Global Forwarding Profile 3. Brazil Import Glossary 4. Brazil Import Regulation Overview 5. Commercial Invoice 6. Air Freight Import Information

Session 4 - The Brazilian Maritime Cluster. Imperatives for an entrepreneurial environment The cabotage: taxes, the legal environment.

Session 4 - The Brazilian Maritime Cluster Imperatives for an entrepreneurial environment The cabotage: taxes, the legal environment. Developed by Eduardo Simeone Breno Gomes RJ, September 13, 2011 WHY

Session 4 - The Brazilian Maritime Cluster Imperatives for an entrepreneurial environment The cabotage: taxes, the legal environment. Developed by Eduardo Simeone Breno Gomes RJ, September 13, 2011 WHY

MANUAL / GUIDELINE AIR SHIPMENTS TO BRAZIL

MANUAL / GUIDELINE AIR SHIPMENTS TO BRAZIL This manual was especially designed to eliminate the problems, which arise when importing cargo through the Brazilian airports, by complying with the main Brazilian

MANUAL / GUIDELINE AIR SHIPMENTS TO BRAZIL This manual was especially designed to eliminate the problems, which arise when importing cargo through the Brazilian airports, by complying with the main Brazilian

Setting up your Business in Brazil Issues to consider

Brazil is the world s fifth largest country. With an estimated population of 194 million in 2012, it is also the world s fifth most populous country after China, India, the United States and Indonesia.

Brazil is the world s fifth largest country. With an estimated population of 194 million in 2012, it is also the world s fifth most populous country after China, India, the United States and Indonesia.

Dealing with tax complexities in Brazil

Dealing with tax complexities in Brazil By: Dudley Juana Anderson Dutra AGENDA Tax complexities in Brazil 1. Overview of main taxes in Brazil IRPJ and CSLL Gross Revenue Taxes: PIS and COFINS Indirect

Dealing with tax complexities in Brazil By: Dudley Juana Anderson Dutra AGENDA Tax complexities in Brazil 1. Overview of main taxes in Brazil IRPJ and CSLL Gross Revenue Taxes: PIS and COFINS Indirect

MM: Display Tax Conditions in Purchase Order for Brazilian Companies

MM: Display Tax Conditions in Purchase Order for Brazilian Companies Applies to: This solution could be applied for release 4.6 and higher. The documents was created using ECC 6.0 For more information,

MM: Display Tax Conditions in Purchase Order for Brazilian Companies Applies to: This solution could be applied for release 4.6 and higher. The documents was created using ECC 6.0 For more information,

FEDERAL REVENUE SECRETARIAT OF BRAZIL GUIDE FOR TRAVELERS CUSTOMS CONTROL AND TAX TREATMENT APPLIED TO BAGGAGE

FEDERAL REVENUE SECRETARIAT OF BRAZIL GUIDE FOR TRAVELERS CUSTOMS CONTROL AND TAX TREATMENT APPLIED TO BAGGAGE IMPORTS AND EXPORTS AND CARRYING OF VALUABLES (August/2013) FOREWORD The purpose of this Guide

FEDERAL REVENUE SECRETARIAT OF BRAZIL GUIDE FOR TRAVELERS CUSTOMS CONTROL AND TAX TREATMENT APPLIED TO BAGGAGE IMPORTS AND EXPORTS AND CARRYING OF VALUABLES (August/2013) FOREWORD The purpose of this Guide

Brazilian Tax System. Brazilian Tax System. March/2013

Brazilian Tax System March/2013 General Features Brazilian Federation Brazil is a federation composed of three highly decentralized government levels, each of them has its political, finance and administrative

Brazilian Tax System March/2013 General Features Brazilian Federation Brazil is a federation composed of three highly decentralized government levels, each of them has its political, finance and administrative

SOLUTIONS. Learning Goal 15

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

Learning Goal 15: Prepare a Classified S1 Learning Goal 15 Multiple Choice 1. b 2. c 3. a 4. b 5. d 6. a 7. c Their importance in paying current liabilities is the main reason current assets are shown

BUYING A PROPERTY IN PORTUGAL

I - FORMALITIES 1. Purchase and Sale of Properties: According to the Portuguese Civil Code, the purchase and sale of any immovable property, urban or rural, must be consigned on a notary deed. Due to the

I - FORMALITIES 1. Purchase and Sale of Properties: According to the Portuguese Civil Code, the purchase and sale of any immovable property, urban or rural, must be consigned on a notary deed. Due to the

Doing Business in Brazil

Doing Business in Brazil www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Businesses Formed by Sole Individuals 6 2.4

Doing Business in Brazil www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Businesses Formed by Sole Individuals 6 2.4

Mexican Tax Law. Value Added Tax (VAT) is assessed on the consummation within the Mexican territory of the following types of transactions:

is assessed on the consummation within the Mexican territory of the following types of transactions:") Mexican Tax Law By: Benjamin C. Rosen brosen@rosenlaw.com.mx Last Update: September 2006 INTRODUCTION Mexican companies (including subsidiaries of foreign companies), as well as permanent establishments

Mexican Tax Law By: Benjamin C. Rosen brosen@rosenlaw.com.mx Last Update: September 2006 INTRODUCTION Mexican companies (including subsidiaries of foreign companies), as well as permanent establishments

Guidebook on Capital Investment Planning for Local Governments

Knowledge PAPERS Guidebook on Capital Investment Planning for Local Governments Design: miki@ultradesigns.com Knowledge PAPERS Guidebook on Capital Investment Planning for Local Governments Olga Kaganova

Knowledge PAPERS Guidebook on Capital Investment Planning for Local Governments Design: miki@ultradesigns.com Knowledge PAPERS Guidebook on Capital Investment Planning for Local Governments Olga Kaganova

Preface to the Third Edition

Preface to the Third Edition Brazil Tax Guide for Foreigners has become the leading reference work in the English language for those interested in foreign investment in Brazil. No other two editions have

Preface to the Third Edition Brazil Tax Guide for Foreigners has become the leading reference work in the English language for those interested in foreign investment in Brazil. No other two editions have

Accounting for Market Distortions in an Integrated Investment Appraisal Framework

Accounting for Market Distortions in an Integrated Investment Appraisal Framework Kemal Bagzibagli 1 Glenn P. Jenkins 2 Octave Semwaga 3 1 Eastern Mediterranean University, North Cyprus 2 Queens University,

Accounting for Market Distortions in an Integrated Investment Appraisal Framework Kemal Bagzibagli 1 Glenn P. Jenkins 2 Octave Semwaga 3 1 Eastern Mediterranean University, North Cyprus 2 Queens University,

Value-Added Tax Across the Latin American Region

Value-Added Tax Across the Latin American Region 11th Annual Latin American Tax Conference The Biltmore Hotel, Coral Gables, FL 10-11 March 2010 Jose Pedro Barnola, Claudio Moretti, Alberto Maturana, Sergio

Value-Added Tax Across the Latin American Region 11th Annual Latin American Tax Conference The Biltmore Hotel, Coral Gables, FL 10-11 March 2010 Jose Pedro Barnola, Claudio Moretti, Alberto Maturana, Sergio

NAPCS Product List for NAICS 4885: Freight Transportation Arrangement

NAPCS List for NAICS 4885: 4885 1 Freight transportation Arranging for the international or domestic transportation of goods, including all necessary customs arrangement services clearances, regulatory

NAPCS List for NAICS 4885: 4885 1 Freight transportation Arranging for the international or domestic transportation of goods, including all necessary customs arrangement services clearances, regulatory

Therefore, The NATIONAL HEAD OF THE ARGENTINE TAX AUTHORITY RESOLVES AS FOLLOWS:

General Resolution 2021/06 AFIP (Argentine Tax Authority) Subject: Postal Service Providers Courier Argentina s María Information System (SIM, as per the acronym in Spanish) Register of Simplified Applications

General Resolution 2021/06 AFIP (Argentine Tax Authority) Subject: Postal Service Providers Courier Argentina s María Information System (SIM, as per the acronym in Spanish) Register of Simplified Applications

New Fee Structure. July/2011

New Fee Structure July/2011 1 BM&FBOVESPA New Fee Structure Bovespa Segment Aligning with the pricing practices in major international markets and showing that BVMF fees are already pretty competitive

New Fee Structure July/2011 1 BM&FBOVESPA New Fee Structure Bovespa Segment Aligning with the pricing practices in major international markets and showing that BVMF fees are already pretty competitive

FORM OF NOTICE OF A MANDATORY PUBLIC TENDER OFFER FOR THE ACQUISITION OF COMMON SHARES ISSUED BY

This is a free translation into English from the Portuguese original of the Edital de Oferta Pública Obrigatória de Aquisição de Ações Ordinárias de Emissão da Souza Cruz S.A. of September 10, 2015, as

This is a free translation into English from the Portuguese original of the Edital de Oferta Pública Obrigatória de Aquisição de Ações Ordinárias de Emissão da Souza Cruz S.A. of September 10, 2015, as

SAP BusinessObjects Electronic Invoicing for Brazil (NF-e)

") SAP BusinessObjects Electronic Invoicing for Brazil (NF-e) Greg Ertel, Director, Solution Marketing SAP Linda McKee, Director, Solution Management, SAP Anil Mahendra, Vice President of Sales, Politec October

SAP BusinessObjects Electronic Invoicing for Brazil (NF-e) Greg Ertel, Director, Solution Marketing SAP Linda McKee, Director, Solution Management, SAP Anil Mahendra, Vice President of Sales, Politec October

HOW TO DO BUSINESS IN THE OIL & GAS AND MARITIME INDUSTRY IN BRAZIL

HOW TO DO BUSINESS IN THE OIL & GAS AND MARITIME INDUSTRY IN BRAZIL All rights reserved. Strict license restrictions apply. Distribution to third parties requiers prior written consent from INTSOK. 2 This

HOW TO DO BUSINESS IN THE OIL & GAS AND MARITIME INDUSTRY IN BRAZIL All rights reserved. Strict license restrictions apply. Distribution to third parties requiers prior written consent from INTSOK. 2 This

THE CHALLENGES OF TAXATION ON E-COMMERCE IN BRAZIL: LESSONS LEARNED FROM THE UNITED STATES

IBI THE INSTITUTE OF BRAZILIAN ISSUES Minerva Program THE CHALLENGES OF TAXATION ON E-COMMERCE IN BRAZIL: LESSONS LEARNED FROM THE UNITED STATES Monique Poggiali de Sousa Advisor: Nickolas Vonortas Washington,

IBI THE INSTITUTE OF BRAZILIAN ISSUES Minerva Program THE CHALLENGES OF TAXATION ON E-COMMERCE IN BRAZIL: LESSONS LEARNED FROM THE UNITED STATES Monique Poggiali de Sousa Advisor: Nickolas Vonortas Washington,

Tax Reform in Brazil and the U.S.

Tax Reform in Brazil and the U.S. Devon M. Bodoh Principal in Charge Latin America Markets, Tax KPMG LLP Carlos Eduardo Toro Director KPMG Brazil Agenda Overview of Global Tax Reform Overview Organization

Tax Reform in Brazil and the U.S. Devon M. Bodoh Principal in Charge Latin America Markets, Tax KPMG LLP Carlos Eduardo Toro Director KPMG Brazil Agenda Overview of Global Tax Reform Overview Organization

INCOTERMS 2015. The current set of Incoterms is Incoterms 2010. A copy of the full terms is available from the International Chamber of Commerce.

INCOTERMS 2015 An overview International Commercial Terms ( Incoterms ) are internationally recognized standard trade terms used in sales contracts. They re used to make sure buyer and seller know: Who

INCOTERMS 2015 An overview International Commercial Terms ( Incoterms ) are internationally recognized standard trade terms used in sales contracts. They re used to make sure buyer and seller know: Who

INCORPORATING A COMPANY IN CAMBODIA

INCORPORATING A COMPANY IN CAMBODIA 1 - LEGAL FRAMEWORK AND REQUIREMENTS Cambodian company framework is covered by a circular issued by the Ministry of Commerce. Different types of company The Cambodian

INCORPORATING A COMPANY IN CAMBODIA 1 - LEGAL FRAMEWORK AND REQUIREMENTS Cambodian company framework is covered by a circular issued by the Ministry of Commerce. Different types of company The Cambodian

INTERNATIONAL EXECUTIVE SERVICES. Brazil. Taxation of International Executives TAX

INTERNATIONAL EXECUTIVE SERVICES Brazil Taxation of International Executives TAX : Taxation of International Executives Overview and Introduction 3 Income Tax 4 Tax Returns and Compliance 4 Tax Rates 6

INTERNATIONAL EXECUTIVE SERVICES Brazil Taxation of International Executives TAX : Taxation of International Executives Overview and Introduction 3 Income Tax 4 Tax Returns and Compliance 4 Tax Rates 6

Doing Business in Brazil: Common Pitfalls & How to Avoid Them

Doing Business in Brazil: Common Pitfalls & How to Avoid Them The Opportunity Why Brazil? 2 Overview Average GDP growth rate of over 5% World s 7 th largest economy Population of 193 million Sophisticated

Doing Business in Brazil: Common Pitfalls & How to Avoid Them The Opportunity Why Brazil? 2 Overview Average GDP growth rate of over 5% World s 7 th largest economy Population of 193 million Sophisticated

Brazil. Country Tax up-date. 2012 Iberoamerica Tax Summit. 16-18 October 2012 Buenos Aires, Argentina

Brazil Country Tax up-date 2012 Iberoamerica Tax Summit 16-18 October 2012 Buenos Aires, Argentina Agenda Murilo Mello, tax partner at KPMG Brazil Agenda Brazil s Economy and perspectives Tax Updates Tax

Brazil Country Tax up-date 2012 Iberoamerica Tax Summit 16-18 October 2012 Buenos Aires, Argentina Agenda Murilo Mello, tax partner at KPMG Brazil Agenda Brazil s Economy and perspectives Tax Updates Tax

ACKNOWLEDGMENTS. Gabriel Rico - CEO, Amcham Brasil

ACKNOWLEDGMENTS The American Chamber of Commerce for Brazil, being the largest Amcham outside the United States is constantly serving its members by building bridges for Brazilian businesses worldwide.

ACKNOWLEDGMENTS The American Chamber of Commerce for Brazil, being the largest Amcham outside the United States is constantly serving its members by building bridges for Brazilian businesses worldwide.

THE CODE. On Taxes and Other Obligatory Payments

THE CODE of the Republic of Kazakhstan On Taxes and Other Obligatory Payments TO THE BUDGET (THE TAX CODE) Effective January 1, 2015 Developed by ITIC in cooperation with the Information Bulletin of the

THE CODE of the Republic of Kazakhstan On Taxes and Other Obligatory Payments TO THE BUDGET (THE TAX CODE) Effective January 1, 2015 Developed by ITIC in cooperation with the Information Bulletin of the

Architecture Services Trade Mission to Brazil. Brazilian Tax Overview October 7, 2013

Architecture Services Trade Mission to Brazil Brazilian Tax Overview October 7, 2013 The tax advice contained herein is not intended or written by EY to be used, and cannot be used, by the recipient for

Architecture Services Trade Mission to Brazil Brazilian Tax Overview October 7, 2013 The tax advice contained herein is not intended or written by EY to be used, and cannot be used, by the recipient for

Emergency Agenda for the Brazilian airline industry

Emergency Agenda for the Brazilian airline industry ABEAR s proposals to stimulate air transportation, economy, connectivity and regional development in Brazil www.abear.com.br Proposals 1. Establishing

Emergency Agenda for the Brazilian airline industry ABEAR s proposals to stimulate air transportation, economy, connectivity and regional development in Brazil www.abear.com.br Proposals 1. Establishing

Tax Impacts to Structure Investments in Brazil Debt or Equity. Andrea Bazzo Lauletta November 2012

Tax Impacts to Structure Investments in Brazil Debt or Equity Andrea Bazzo Lauletta November 2012 Introduction Brazilian Scenario for Non-Resident Investments Brazil has a specific set of rules for non-resident

Tax Impacts to Structure Investments in Brazil Debt or Equity Andrea Bazzo Lauletta November 2012 Introduction Brazilian Scenario for Non-Resident Investments Brazil has a specific set of rules for non-resident

ETHANOL AS PREFERENTIAL FUEL FOR THE FUTURE OF INTERNAL COMBUSTION ENGINE. Ricardo Simões de Abreu Frente Inovar-Auto 2 - Sindipeças Julho de 2015

ETHANOL AS PREFERENTIAL FUEL FOR THE FUTURE OF INTERNAL COMBUSTION ENGINE Ricardo Simões de Abreu Frente Inovar-Auto 2 - Sindipeças Julho de 2015 1 Ethanol is key to complement Brazilian Energetic Matrix

ETHANOL AS PREFERENTIAL FUEL FOR THE FUTURE OF INTERNAL COMBUSTION ENGINE Ricardo Simões de Abreu Frente Inovar-Auto 2 - Sindipeças Julho de 2015 1 Ethanol is key to complement Brazilian Energetic Matrix

Global Tax Dispute Resolution and Controversy Services

Global Tax Dispute Resolution and Controversy Services Tax Dispute Resolution and Controversy Update Litigation overview in Brazil, France and Russia Wednesday 29 July 2015 12:00 pm EST Notice The following

Global Tax Dispute Resolution and Controversy Services Tax Dispute Resolution and Controversy Update Litigation overview in Brazil, France and Russia Wednesday 29 July 2015 12:00 pm EST Notice The following

International Merchandise Trade Statistics

5 International Merchandise Trade Statistics Introduction 5.1 International merchandise trade statistics (IMTS) measure quantities and values of goods that, by moving into or out of an economy, add to

5 International Merchandise Trade Statistics Introduction 5.1 International merchandise trade statistics (IMTS) measure quantities and values of goods that, by moving into or out of an economy, add to

IHO Commission on the Promulgation of Radio Navigational Warning (CPRNW) International Hydrographic Bureau, Monaco

International Hydrographic Bureau, Monaco") IHO Commission on the Promulgation of Radio Navigational Warning (CPRNW) CPRNW9-3.2.1-V International Hydrographic Bureau, Monaco Origin: Brazil MSI Self Assessment - NAVAREA V Submitted by: Brazil 1.

IHO Commission on the Promulgation of Radio Navigational Warning (CPRNW) CPRNW9-3.2.1-V International Hydrographic Bureau, Monaco Origin: Brazil MSI Self Assessment - NAVAREA V Submitted by: Brazil 1.

International Capitals and Foreign Exchange Market in Brazil

International Capitals and Foreign Exchange Market in Brazil Updated October 2015 International Capitals According to Brazilian legislation, the concept of international capital is divided into foreign

International Capitals and Foreign Exchange Market in Brazil Updated October 2015 International Capitals According to Brazilian legislation, the concept of international capital is divided into foreign

EU Webinar Series: Customs Valuation. Jasper Helder, Partner (Amsterdam) Jennifer Revis, Senior Associate (London) Thursday 26 April 2012

Jennifer Revis, Senior Associate (London) Thursday 26 April 2012") EU Webinar Series: Customs Valuation Jasper Helder, Partner (Amsterdam) Jennifer Revis, Senior Associate (London) Thursday 26 April 2012 Agenda The basics Valuation methods First sale Assists/ cost sharing

EU Webinar Series: Customs Valuation Jasper Helder, Partner (Amsterdam) Jennifer Revis, Senior Associate (London) Thursday 26 April 2012 Agenda The basics Valuation methods First sale Assists/ cost sharing

MAURITIUS Business Opportunities to Brazil

MAURITIUS Business Opportunities to Brazil Prepared by: ENTERPRISE MAURITIUS & ABMR Valentim Rebouças & Ivone Andrade São Paulo, Brazil - 15 April 2014 AGENDA 1. Objectives of Survey 2. Research Methodology

MAURITIUS Business Opportunities to Brazil Prepared by: ENTERPRISE MAURITIUS & ABMR Valentim Rebouças & Ivone Andrade São Paulo, Brazil - 15 April 2014 AGENDA 1. Objectives of Survey 2. Research Methodology

CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE

CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION

CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION

Taxes and incentives for renewable energy KPMG INTERNATIONAL. June 2012. kpmg.com

Taxes and incentives for renewable energy KPMG INTERNATIONAL June 2012 kpmg.com 2012 KPMG International Cooperative ( KPMG International ), a Swiss entity. Member firms of the KPMG network of independent

Taxes and incentives for renewable energy KPMG INTERNATIONAL June 2012 kpmg.com 2012 KPMG International Cooperative ( KPMG International ), a Swiss entity. Member firms of the KPMG network of independent

Thinking Beyond Borders

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Tanzania kpmg.com Tanzania Introduction Taxation of individuals under the Income Tax Act 2004 (ITA) is on the basis of both residence and source.

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders Tanzania kpmg.com Tanzania Introduction Taxation of individuals under the Income Tax Act 2004 (ITA) is on the basis of both residence and source.

Corporate and Indirect Tax Rate Survey 2014. kpmg.com/tax

Corporate and Indirect Tax Rate Survey 2014 kpmg.com/tax b Section or Brochure name b Corporate and Indirect Tax Rate Survey 2014 About KPMG s Corporate and Indirect Tax Rate Survey The KPMG International

Corporate and Indirect Tax Rate Survey 2014 kpmg.com/tax b Section or Brochure name b Corporate and Indirect Tax Rate Survey 2014 About KPMG s Corporate and Indirect Tax Rate Survey The KPMG International

U.S.A. Chapter I. Scope of the Convention

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

Receita Federal do Brasil (RFB) www.receita.fazenda.gov.br 1 January to 31 December Last working day of April following end of tax year

www.receita.fazenda.gov.br 1 January to 31 December Last working day of April following end of tax year") Worldwide personal tax guide 2013 2014 Brazil Local Information Tax Authority Receita Federal do Brasil (RFB) Website www.receita.fazenda.gov.br Tax Year 1 January to 31 December Tax Return due date: Last

Worldwide personal tax guide 2013 2014 Brazil Local Information Tax Authority Receita Federal do Brasil (RFB) Website www.receita.fazenda.gov.br Tax Year 1 January to 31 December Tax Return due date: Last

ASPE AT A GLANCE Income Taxes Future Income Taxes Method1

ASPE AT A GLANCE Income Taxes Future Income Taxes Method1 December 2014 SCOPE Income Taxes - Future Income Taxes Method 1 INCOME TAXES Effective Date Fiscal years beginning on or after January 1, 2011

ASPE AT A GLANCE Income Taxes Future Income Taxes Method1 December 2014 SCOPE Income Taxes - Future Income Taxes Method 1 INCOME TAXES Effective Date Fiscal years beginning on or after January 1, 2011

Corporate and Indirect Tax Rate Survey 2014. kpmg.com/tax

Corporate and Indirect Tax Rate Survey 2014 kpmg.com/tax b Section or Brochure name b Corporate and Indirect Tax Rate Survey 2014 About KPMG s Corporate and Indirect Tax Rate Survey The KPMG International

Corporate and Indirect Tax Rate Survey 2014 kpmg.com/tax b Section or Brochure name b Corporate and Indirect Tax Rate Survey 2014 About KPMG s Corporate and Indirect Tax Rate Survey The KPMG International

FRENCH CUSTOMS STRATEGIC PLAN

FRENCH CUSTOMS STRATEGIC PLAN Éditorial by the ministers At the end of 2012, we asked customs to draw up a strategic continuous improvement plan for 2018... French customs main areas of work have been

FRENCH CUSTOMS STRATEGIC PLAN Éditorial by the ministers At the end of 2012, we asked customs to draw up a strategic continuous improvement plan for 2018... French customs main areas of work have been

Simplification Measures in the Foreign Exchange Area

Simplification Measures in the Foreign Exchange Area Updated in October, 2015 Introduction This document intends to describe the recent evolution of the Brazilian exchange market, since when there were

Simplification Measures in the Foreign Exchange Area Updated in October, 2015 Introduction This document intends to describe the recent evolution of the Brazilian exchange market, since when there were

Jurisdictional updates What s new in Brazil? Ana Claudia Akie Utumi autumi@tozzinifreire.com.br May, 2013

Jurisdictional updates What s new in Brazil? Ana Claudia Akie Utumi autumi@tozzinifreire.com.br May, 2013 Ana Claudia Akie Utumi autumi@tozzinifreire.com.br Professional experience: Head of Tax Area at

Jurisdictional updates What s new in Brazil? Ana Claudia Akie Utumi autumi@tozzinifreire.com.br May, 2013 Ana Claudia Akie Utumi autumi@tozzinifreire.com.br Professional experience: Head of Tax Area at

Lawyers of LF «Dmitrieva & Partners» have prepared the list of top news in the field of taxation for the last two weeks

REVIEW OF THE MAIN EVENTS IN THE SPHERE OF TAXATION Lawyers of LF «Dmitrieva & Partners» have prepared the list of top news in the field of taxation for the last two weeks The State Fiscal Service of Ukraine

REVIEW OF THE MAIN EVENTS IN THE SPHERE OF TAXATION Lawyers of LF «Dmitrieva & Partners» have prepared the list of top news in the field of taxation for the last two weeks The State Fiscal Service of Ukraine

Accounting Building Business Skills. Learning Objectives. Learning Objectives. Paul D. Kimmel. Chapter Four: Inventories

Accounting Building Business Skills Paul D. Kimmel Chapter Four: Inventories PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Four: Inventories PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003 John Wiley & Sons Australia,

Real Estate Property Tax in Israel and Tax Incentives for Foreign Direct Investors Investing in Israel By Amit Ben-Yehoshua, Attorney at Law

Real Estate Property Tax in Israel and Tax Incentives for Foreign Direct Investors Investing in Israel By Amit Ben-Yehoshua, Attorney at Law China and Israel Israel and China, greatly differ in size and

Real Estate Property Tax in Israel and Tax Incentives for Foreign Direct Investors Investing in Israel By Amit Ben-Yehoshua, Attorney at Law China and Israel Israel and China, greatly differ in size and

www.boasecohencollins.com 2303-7 Dominion Centre, 43-59 Queen s Road East, Hong Kong Tel: (852) 3416-1711

3416-1711") www.boasecohencollins.com 2303-7 Dominion Centre, 43-59 Queen s Road East, Hong Kong Tel: (852) 3416-1711 1. Why Hong Kong? Hong Kong is one of Asia s most popular cities for doing business because of

www.boasecohencollins.com 2303-7 Dominion Centre, 43-59 Queen s Road East, Hong Kong Tel: (852) 3416-1711 1. Why Hong Kong? Hong Kong is one of Asia s most popular cities for doing business because of

SOFTWARE. CONSULTING. SOLUTIONS. Smart IT Solutions

SOFTWARE. CONSULTING. SOLUTIONS. Smart IT Solutions 2 Content 3 4 6 8 10 11 12 14 dbh Logistics IT AG Key Competences and Overview Customs & Foreign Trade Solutions for Customs Clearance in Europe Compliance

SOFTWARE. CONSULTING. SOLUTIONS. Smart IT Solutions 2 Content 3 4 6 8 10 11 12 14 dbh Logistics IT AG Key Competences and Overview Customs & Foreign Trade Solutions for Customs Clearance in Europe Compliance

Balance of Payments made simple Fedrica Robinson

Balance of Payments made simple by Fedrica Robinson Bank of Jamaica Pamphlet No. 8 2004 Bank of Jamaica Nethersole Place Kingston Jamaica Telephone: 876 922 0750-9 Email: library@boj.org.jm Internet: www.boj.org.jm

Balance of Payments made simple by Fedrica Robinson Bank of Jamaica Pamphlet No. 8 2004 Bank of Jamaica Nethersole Place Kingston Jamaica Telephone: 876 922 0750-9 Email: library@boj.org.jm Internet: www.boj.org.jm

Deutsch Brasilianische Wirtschaftstage - 2009. 01. September 2009

Deutsch Brasilianische Wirtschaftstage - 2009 01. September 2009 Apex-Brasil The Brazilian Trade and Investment Promotion Agency was officially established in 2003 in partnership with national industry

Deutsch Brasilianische Wirtschaftstage - 2009 01. September 2009 Apex-Brasil The Brazilian Trade and Investment Promotion Agency was officially established in 2003 in partnership with national industry

and Incentives for Renewable Energy

ENERGY & SECTORS NATURAL AND RESOURCES THEMES Taxes Title and Incentives here for Renewable Energy Additional information in Univers 45 Light 12pt on 16pt leading Tax kpmg.com Credits and authors in Univers

ENERGY & SECTORS NATURAL AND RESOURCES THEMES Taxes Title and Incentives here for Renewable Energy Additional information in Univers 45 Light 12pt on 16pt leading Tax kpmg.com Credits and authors in Univers

FOREWORD. Cape Verde. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

ASEAN-CHINA AGREEMENT ON TRADE IN SERVICES MYANMAR. Schedule of Specific Commitments. (For the First Package of Commitments)

") ASEAN-CHINA AGREEMENT ON TRADE IN SERVICES ANNEX 1/SC1 MYANMAR Schedule of Specific Commitments (For the First Package of Commitments) 1 MYANMAR - SCHEDULE OF SPECIFIC COMMITMENTS Modes of Supply: 1) Cross-border

ASEAN-CHINA AGREEMENT ON TRADE IN SERVICES ANNEX 1/SC1 MYANMAR Schedule of Specific Commitments (For the First Package of Commitments) 1 MYANMAR - SCHEDULE OF SPECIFIC COMMITMENTS Modes of Supply: 1) Cross-border

Shipping Instructions for General Cargoes only Attention: For Cosmetics, Food, Beverages and Medical Products additional instructions will be given

Shipping Instructions for General Cargoes only Attention: For Cosmetics, Food, Beverages and Medical Products additional instructions will be given 6th LABACE'2009 13-15/8/2009 Vasp Hangar - Congonhas

Shipping Instructions for General Cargoes only Attention: For Cosmetics, Food, Beverages and Medical Products additional instructions will be given 6th LABACE'2009 13-15/8/2009 Vasp Hangar - Congonhas

What are Incoterms? Any mode of transport: Sea and inland waterway transport (only): CIP - Carriage and Insurance Paid

: CIP - Carriage and Insurance Paid") What are Incoterms? International Commerce Terms (Incoterms) are an internationally recognised standard trade terms that set out buyer and seller responsibilities. Incoterms are maintained and developed

What are Incoterms? International Commerce Terms (Incoterms) are an internationally recognised standard trade terms that set out buyer and seller responsibilities. Incoterms are maintained and developed

HAVE AGREED as follows:

CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF ICELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

CONVENTION BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF ICELAND FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME

Chapter 9. Goods and Services Account

Chapter 9. Goods and Services Account A. Introduction to the Current Account 9.1 The current account will be introduced, as in Chapter 2 Overview. B. Introduction to the Goods and Services Account 9.2

Chapter 9. Goods and Services Account A. Introduction to the Current Account 9.1 The current account will be introduced, as in Chapter 2 Overview. B. Introduction to the Goods and Services Account 9.2

DOING BUSINESS IN BRAZIL

DOING BUSINESS IN BRAZIL CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 7 4 Setting up a Business 22 5 Labour 37 6 Taxation 49 7 Accounting & reporting 70 8 UHY Representation

DOING BUSINESS IN BRAZIL CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 7 4 Setting up a Business 22 5 Labour 37 6 Taxation 49 7 Accounting & reporting 70 8 UHY Representation

Soccerex Global Convention 2013 Maracanã Stadium Rio de Janeiro RJ November 30th to December 5th, 2013

Soccerex Global Convention 2013 Maracanã Stadium Rio de Janeiro RJ November 30th to December 5th, 2013 Shipping Guidelines 1 OFFICIAL SHIPPING GUIDELINE TEMPORARY SHIPMENTS Once again, we from Waiver Logistics,

Soccerex Global Convention 2013 Maracanã Stadium Rio de Janeiro RJ November 30th to December 5th, 2013 Shipping Guidelines 1 OFFICIAL SHIPPING GUIDELINE TEMPORARY SHIPMENTS Once again, we from Waiver Logistics,