The purposes of ACA reporting

|

|

|

- Peregrine Campbell

- 7 years ago

- Views:

Transcription

1

2 Agenda > The purposes of ACA reporting > Affordability and minimum value > Determining applicable large employer status > Determining full-time and full-time equivalent employees > ACA reporting scenarios > ACA reporting requirements: Deadlines and electronic filing > Penalties for noncompliance of ACA reporting requirements > ACA requirements still to come > Employer-provided healthcare coverage options > ACA taxes and fees > Employer mandate: Pay-or-play rules 2

3 The purposes of ACA reporting

4 Minimum essential rule reporting - Internal Revenue Code section 6055 > Requires insurers, unions, and self-insured employers that provide minimum essential coverage (MEC) to submit annual information reports to the IRS each year identifying who is covered. > MEC includes COBRA coverage, major medical coverage provided through a retiree-only plan, and retiree-only health reimbursement arrangements (HRAs). Reporting is not required for HRAs that are integrated with employerprovided health coverage or Medicare supplemental coverage which is offered to retirees. > MEC reports provide information needed to establish that individuals enrolled in MEC do not owe the individual mandate. 4

5 Minimum essential rule reporting - Internal Revenue Code section 6055 > Employer-sponsored coverage Including COBRA and retiree coverage > Individual coverage > Medicare > Medicaid > Children s Health Insurance Program (CHIP) coverage > Some veterans health coverage > TRICARE 5

6 ALE shared responsibility reporting - Internal Revenue Code section 6056 > Requires applicable large employers (ALEs) to report to the IRS each year information on anyone who was a full-time employee (not on dependents or other beneficiaries) for one month or more, whether that person was offered health coverage, and, if so, the lowest amount an employee could pay to get coverage that meets the minimum value requirement. > Employer-shared responsibility reports provide information needed to determine whether the ALE owes tax for failing to offer affordable MEC that provides minimum value and whether fulltime employees appropriately claimed an ACA premium tax credit. > The standard for who is a full-time employee is the same as for the pay or play penalty: a common-law employee working an average of 30 hours per week or 130 hours per month. 6

7 Affordability and minimum value

8 Affordability safe harbors > W-2 safe harbor Measures employee s required contribution for single coverage against employee s W-2 wages Coverage is affordable if cost is 9.5 percent or less of W-2 income > Rate-of-pay safe harbor Affordability based on employee s rate of pay Employee s monthly contribution for single coverage is affordable if 9.5 percent (or lower) monthly wages > Federal poverty level (FPL) safe harbor Determines affordability based on FPL for single individual Coverage is affordable if the employee s contribution for single coverage is 9.5 percent of that FPL (or lower) 8

9 Minimum value coverage > Minimum value measures cost sharing (similar to metal levels for qualified health plans) > To provide minimum value, plan s share of total allowed costs of benefits provided under the plan must be at least 60 percent HRA/health savings account (HSA) amounts to be included > Determining minimum value: Minimum value calculator Design-based safe harbor checklists Appropriate certification by actuary 9

10 Determining applicable large employer status

11 Determining applicable large employer status > The first step in determining the ACA reporting responsibility of an employer is for the employer to determine whether it is an applicable large employer (ALE). 11

12 Applicable large employers > Applicable large employer (ALE): Original definition: Average 50 or more full-time/full-time equivalent (FTE) employees in prior calendar year For 2015: New medium-sized employers (defined in next slide) > Common ownership rules Controlled group rules apply (IRC section 414) All employees taken into account (including union employees) Liability and penalties apply separately to each controlled group member by tax ID number 12

13 Medium-sized employers (subset of ALEs) > Medium-sized employer transition relief was issued February 2014 and is applicable to: Groups that employ fewer than 100 full-time/fte employees on business days during 2014 Groups that meet eligibility conditions > These groups are eligible for another one-year delay of pay-or-play mandate. Groups must: Qualify for delay Request delay from IRS (not automatic) 13

14 Medium-sized employers (subset of ALEs) > Eligibility for transition relief: Employers that change plan years after Feb. 9, 2014, to begin on a later calendar date, are not eligible for the delay. Employers may not reduce workforce size or hours of service from Feb. 9, 2014, to Dec. 31, 2014, in order to qualify based on size. o Changes for bona fide business reasons permissible. Employers may not eliminate or materially reduce coverage offered as of Feb. 9, 2014, during maintenance coverage period. Employers must certify that group meets all eligibility requirements. 14

15 Employer reporting requirements Pay-or-play transition relief: > An ALE with fewer than 100 full-time employees must certify on its 2015 transmittal form that it meets the eligibility requirements. It s not automatic. 15

16 Determining full-time and full-time equivalent employees

17 Full-time (FT) employees > With respect to a calendar month, a full-time employee is: An employee who is employed on average at least 30 hours of service per week or 130 hours per month o 130 hours: 30 x 52 / 12 =

18 Full-time equivalent (FTE) employees > To determine full-time equivalency: Add hours of service in a month for part-time employees (up to 120 hours per person) Divide total hours by 120 Result = number of FTEs for the month 18

19 Counting employees 1. Add full-time employees (including seasonal) for each calendar month in prior calendar year 2. Add FTEs (including seasonal) for each calendar month in prior calendar year 3. Add full-time employees and FTEs together for each month of prior calendar year 4. Add 12 monthly totals and divide by 12 * Special rule for 2015: Employers can use six consecutive months in

20 Special rules > Seasonal employees An employer is not an ALE if: 1) the employer s workforce only exceeds 50 full-time employees for 120 days or less during the calendar year, and 2) the employees in excess of 50 employed during that period were seasonal workers > New companies Calculation based on the average number of full-time employees the employer is reasonably expected to employ on business days in the current calendar year 20

21 ACA reporting scenarios

22 ACA reporting scenarios > General principles of ACA reporting All ALEs will be required to report whether minimum value reportable coverage was offered to any employees who were full-time for at least a month during the year. Except for those employers who are not ALEs and which offer no coverage or only fully insured coverage, all employers are required to complete at least a portion of the ACA reporting, using either the Forms 1094/1095 B or C. Non- ALEs will use the B forms and ALEs will use the C forms, although the ALE can use the B forms for reporting coverage of non-employees. Depending on the funding arrangement of the coverage, it is possible that employees will receive more than one Form 1095 (e.g., one for the employer and one from the insurance carrier). 22

23 ACA reporting scenarios > Fully insured coverage offered by a single ALE > Fully insured coverage offered by a single ALE to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees > Self-funded coverage offered by a single ALE > Self-funded coverage offered by a single ALE to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees > Mix of fully insured and self-funded coverage offered by a single ALE 23

24 ACA reporting scenarios Fully insured vs. self-funded coverage > Fully insured coverage = Insurance carrier directly insures and pays the health claims of covered individuals under a policy Employer submits premiums directly to the insurance company Insurance company pays claims directly to health providers > Self-funded coverage = Employer is responsible for paying health claims of covered individuals from general assets Employer usually retains a third-party administrator to calculate and hold premiums and pay claims to health providers on direction of the employer Employer purchases stop-loss insurance coverage insuring the ability of the employer to pay claims above an individual and aggregate level 24

25 ACA reporting scenarios Fully insured coverage offered by single non-ale > No reporting required by the employer > Insurance carrier is responsible for reporting on any covered individuals using Forms 1094-B and 1095-B > Individuals covered under the fully insured plan will receive a Form 1095-B from the insurance carrier 25

26

27 ACA reporting scenarios Self-funded coverage offered by a single non-ale > Employer reports on any covered individuals using Forms 1094-B and 1095-B > Covered individuals receive a Form 1095-B from the employer 27

28 ACA reporting scenarios Self-funded coverage offered by single non-ale to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees > Employer is responsible for reporting on any nonunion covered individuals using Forms 1094-B and 1095-B > The plan sponsor of the multiemployer union plan reports, is responsible for reporting on any union covered individuals using Forms 1094-B and 1095-B > Nonunion individuals covered under the self-funded coverage receive a Form 1095-B from the employer > Union individuals covered under the multiemployer union plan receive a Form 1095-B from the multiemployer plan sponsor 28

29 ACA reporting scenarios Fully insured coverage offered by single ALE > Employer responsible for reporting whether or not a minimum value, affordable coverage was made to any employees who were full time for at least one month during the year using Form 1094-C and Parts I and II of Form 1095-C > The insurance carrier is responsible for reporting on any covered individuals using Forms 1094-B and 1095-B > Full-time employees receive a Form 1095-C from the employer and individuals covered under the fully insured plan receive a Form 1095-B from the insurance carrier 29

30 ACA reporting scenarios Fully insured coverage offered by single ALE to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees > Employer reports whether a minimum value, affordable offer of coverage was made to any employees (including union employees) who were full time for at least one month during the year (based on the monthly measurement method or look-back measurement method) using Form 1094-C and Parts I and II of Form 1095-C > Insurance carrier reports on any nonunion covered individuals using Forms 1094-B and 1095-B > The plan sponsor of the multiemployer union plan reports on any union plan covered individuals using Forms 1094-B and 1095-B > Full-time employees will receive a Form 1095-C from the employer > Nonunion individuals covered under the fully insured plan receive a Form 1095-B from the insurance carrier, and union-covered individuals will receive a Form 1095-B from the plan sponsor of the union plan 30

31 ACA reporting scenarios Self-funded coverage offered by a single ALE > Employer reports whether or not a minimum value, affordable offer of coverage was made to any employees who were full time for at least one month during the year using Form 1094-C and Parts I and II of Form 1095-C > Employer also reports on any covered individuals using Form 1094-C and Part III of Form 1095-C Forms 1094-B and 1095-B may be used instead of the C forms for non-employees such as COBRA participants and retirees > Full-time employees and individuals covered under the self-funded plan receive a Form 1095-C from the employer; covered non-employees may receive a Form 1095-B from the employer instead 31

32 ACA reporting scenarios Self-funded coverage offered by single ALE to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees > Employer reports whether or not a minimum value, affordable offer of coverage was made to any employees (including union employees) who were full time for at least one month during the year (based on the monthly measurement or look back measurement period) using Form 1094-C and Parts I and II of Form 1095-C > Employer is also responsible for reporting on any nonunion covered individuals on Form 1094-C and Part III of Form 1095-C Forms 1094-B and 1095-B may be used instead of the C forms for nonemployees such as COBRA participants and retirees 32

33 ACA reporting scenarios Self-funded coverage offered by single ALE to nonunion employees and self-funded coverage offered by a multiemployer plan to union employees (cont.) > The plan sponsor of the union coverage is responsible for reporting on any union covered individuals using Forms 1094-B and 1095-B > Full-time employees and nonunion individuals covered under the self-insured plan receive a Form 1095-C from the employer Covered non-employees may receive a Form 1095-B from the employer instead > Union individuals covered under the union plan will receive a Form 1095-B from the plan sponsor of the union plan 33

34 ACA reporting requirements: Deadlines and electronic filing

35 Employer reporting requirements Deadlines: > Returns due Feb. 28 (March 31 if filed electronically*) First return due Monday, March 1, 2016 > Employee statements due Jan. 31 First statements due Monday, Feb. 1, 2016 Electronic filing rules similar to W-2 *Electronic filing is required for all ALEs filing at least 250 returns under section 6056 during the calendar year. Only section 6056 returns are counted in applying the 250 return threshold, and each section 6056 return for a full-time employee is counted as a separate return. 35

36 Penalties for noncompliance of ACA reporting requirements

37 Penalties for noncompliance > Recently increased substantially! The Trade Preferences Extension Act (signed into law June 29, 2015) significantly increased penalties for incorrect information returns, including those required by the ACA The IRS may impose penalties for both failing to file and filing incorrect or incomplete information returns and/or payee statements after the due dates for such forms pursuant to IRC sections 6721 and 6722 > Final ACA regulations provide that penalties will not be imposed on entities that show they made good faith efforts to comply with the reporting requirements for 2015 The IRS has indicated an untimely filed form will not meet the good faith requirement. Should the requirements regarding ACA reporting not be met due to good faith requirements, the penalties may be still be waived if the failure was due to reasonable cause 37

38

39 ACA requirements still to come

40 Section 4980I: ACA Cadillac tax > The Cadillac tax is a 40 percent excise tax on any excess benefit provided to an employee > For 2018, the base dollar threshold is $10,200 for self-only coverage, and $27,500 for coverage other than self-only coverage These base limits will be subject to adjustment based upon a variety of factors. > Notice : Initiated the process of developing regulatory guidance > Notice : Continued the process of developing regulatory guidance 40

41 Upcoming requirements > Nondiscrimination rules Will apply to fully insured non-grandfathered plans Cannot discriminate in favor of highly compensated employees Effective after regulations issued > Automatic enrollment Will apply to large employers (> 200 full-time employees) Must automatically enroll/re-enroll employees in plan, provide notice, and allow them to opt out Effective after regulations issued 41

42 Employer-provided healthcare coverage options

43 Options to employer-provided coverage: Reimbursement of individually obtained coverage > Can an employer drop coverage and reimburse for individualobtained coverage in accordance with Revenue Ruling without incurring ACA mandate penalties? NO! See Notice and Q&As from the IRS and DOL > Notice , Q&A-4 permits an employer to provide additional compensation to employees to make up for lost coverage. But, if an employer increases salary to make up for lost benefits, employer FICA tax obligations will also increase. > Penalties are not tax deductible. > Penalties may be increased if more employers choose to pay them rather than provide coverage. 43

44 Suspending employer-provided coverage: Potential downside to employer > If employees choose to remain uninsured: Increased absenteeism and presenteeism may result o Work time wasted taking care of personal insurance needs Worker compensation costs may go up for what are actually nonwork-related health costs > Competitors may seek labor advantage by continuing to offer coverage 44

45 Options to employer-provided coverage: Utilizing the exchanges > Coverage through the exchange may be more expensive due to the rating requirements > Subsidies phase out rapidly and are significantly less for those at 3 to 4 times the poverty level than for those at 2 times and below > Some employees may not be eligible for subsidies at all and will bear the cost entirely on their own 45

46 ACA taxes and fees

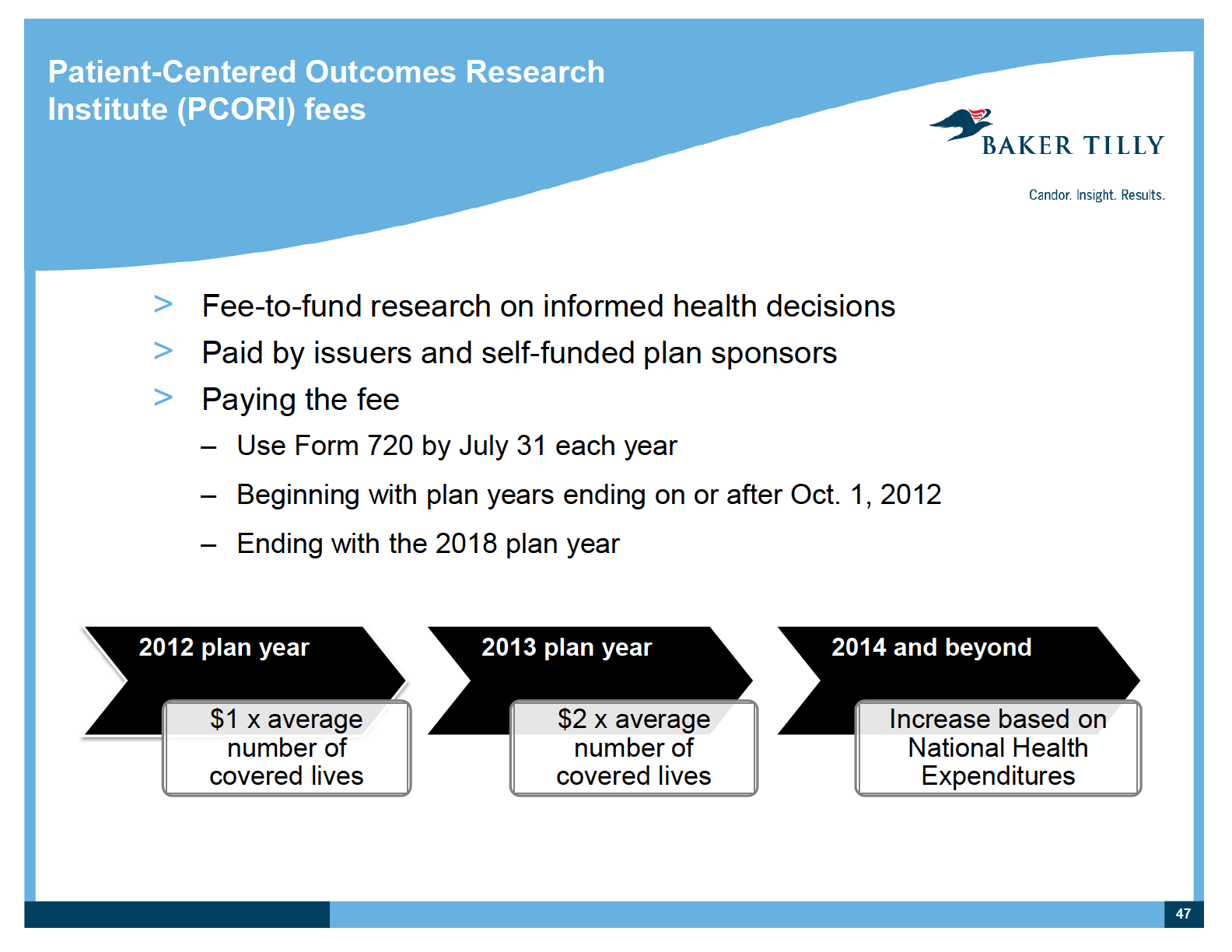

47

48

49

50 The employer mandate: Pay-or-play rules

51 Employer shared responsibility penalties > Large employers subject to pay-or-play rule > Penalties may apply if the employer: Fails to offer minimum essential coverage to 95 percent of full-time employees and dependents (percentage requirement phased in over 2 years) o 2015: must offer coverage to 70 percent of full-time employees o 2016 and beyond: offer coverage to 95 percent of full-time employees Offers coverage that is not affordable or does not provide minimum value > Penalties triggered if any full-time employee gets subsidized coverage through exchange 51

52 Employer penalties > Penalty A: employer failed to offer substantially all full-time employees and dependents opportunity to enroll in employer s plan > Penalty B: employer plan is unaffordable or not minimum value 52

53 Employer penalty amounts > Penalty A: $2,000 per full-time employee, minus the first 30 (for 2015, groups with 100 or more full-time employees can reduce their full-time employee count by 80 when calculating the penalty). > Penalty B: $3,000 for each employee who receives subsidized coverage through an exchange. Amounts shown are annual penalties. Penalties will be calculated on a monthly basis. 53.

54 Non-calendar year plan years > Penalties will not apply right away on Jan. 1, 2015, if: plan is changed to avoid penalties at renewal requirements must be met for this transitional relief > No penalties for months of 2014 plan year that fall in calendar year 2015 > Employees must be offered affordable, minimum value coverage by first day of 2015 plan year Plans will not need to make mid-year or advanced changes 54

55

Employer-Shared Responsibility

Affordable Care Act Planning to Deal with the Pay-or-Play Penalties Effective January 1, 2015 Anne Hydorn Hanson Bridgett LLP Telephone: (415) 995-5893 Email: ahydorn@hansonbridgett.com Judy Boyette Hanson

Affordable Care Act Planning to Deal with the Pay-or-Play Penalties Effective January 1, 2015 Anne Hydorn Hanson Bridgett LLP Telephone: (415) 995-5893 Email: ahydorn@hansonbridgett.com Judy Boyette Hanson

Affordable Care Act Compliance and IRS 1094/95 Filings: Are YOU Ready??

Affordable Care Act Compliance and IRS 1094/95 Filings: Are YOU Ready?? REQUIREMENTS UNDER IRC SECTIONS 6055 AND 6056 Presented by: This Presentation Is Not Legal or tax advice The final word on ACA A

Affordable Care Act Compliance and IRS 1094/95 Filings: Are YOU Ready?? REQUIREMENTS UNDER IRC SECTIONS 6055 AND 6056 Presented by: This Presentation Is Not Legal or tax advice The final word on ACA A

Heffernan Benefit Advisors Presents Health Care Reform: What Non-Profits Need to Know. The session will begin shortly

Heffernan Benefit Advisors Presents Health Care Reform: What Non-Profits Need to Know The session will begin shortly Sound should come through your speakers when the session begins Verify that the volume

Heffernan Benefit Advisors Presents Health Care Reform: What Non-Profits Need to Know The session will begin shortly Sound should come through your speakers when the session begins Verify that the volume

Wells Insurance. 2015 ACA Compliance Update

Wells Insurance 2015 ACA Compliance Update Wells Insurance Today s Agenda Cost-Saving Strategies Deadlines & Implications for you Plan Design Changes Reinsurance Fees Employer Penalty Rules Reporting of

Wells Insurance 2015 ACA Compliance Update Wells Insurance Today s Agenda Cost-Saving Strategies Deadlines & Implications for you Plan Design Changes Reinsurance Fees Employer Penalty Rules Reporting of

IRS Releases 2015 Forms and Instructions for 6055/6056 Reporting

IRS Releases 2015 Forms and Instructions for 6055/6056 Reporting Background Under the Patient Protection and Affordable Care Act (ACA), individuals are required to have health insurance while applicable

IRS Releases 2015 Forms and Instructions for 6055/6056 Reporting Background Under the Patient Protection and Affordable Care Act (ACA), individuals are required to have health insurance while applicable

Health Care Reform - 2016/2017 Strategic Analysis

Health Care Reform - 2016/2017 Strategic Analysis Employers sponsoring health can expect to see no slow-down in Affordable Care Act (ACA) rules, clarifications, and requirements. Understanding these changes,

Health Care Reform - 2016/2017 Strategic Analysis Employers sponsoring health can expect to see no slow-down in Affordable Care Act (ACA) rules, clarifications, and requirements. Understanding these changes,

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by TRUEbenefits LLC On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by TRUEbenefits LLC On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

Patient Protection and Affordable Care Act Compliance Checklist for Employers

October, 2014 Patient Protection and Affordable Care Act Compliance Checklist for Employers Under the Employer Mandate in the Affordable Care Act, effective January 1, 2015, employers with 50 or more full-time

October, 2014 Patient Protection and Affordable Care Act Compliance Checklist for Employers Under the Employer Mandate in the Affordable Care Act, effective January 1, 2015, employers with 50 or more full-time

ACA Employer Reporting Guide. A practical guide to understanding the ACA 6055 and 6056 employer reporting requirements

ACA Employer Reporting Guide A practical guide to understanding the ACA 6055 and 6056 employer reporting requirements Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING... 3 HOW TO USE THIS GUIDE...

ACA Employer Reporting Guide A practical guide to understanding the ACA 6055 and 6056 employer reporting requirements Table of Contents INTRODUCTION TO ACA EMPLOYER REPORTING... 3 HOW TO USE THIS GUIDE...

HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal)

") Group Health Insurance Q & A HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal) 1. Will small employers continue to have 12 month rates as they exist today? a. Yes. Employer groups

Group Health Insurance Q & A HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal) 1. Will small employers continue to have 12 month rates as they exist today? a. Yes. Employer groups

CLICK HERE TO ADD TITLE

CLICK HERE TO ADD TITLE HEALTH CARE REFORM & ITS EFFECTS ON YOUR BUSINESS Presented by Jenny Arthur, SPHR AGENDA Background/History The Past: Previously Implemented HCR Provisions The Present: Current/Pending

CLICK HERE TO ADD TITLE HEALTH CARE REFORM & ITS EFFECTS ON YOUR BUSINESS Presented by Jenny Arthur, SPHR AGENDA Background/History The Past: Previously Implemented HCR Provisions The Present: Current/Pending

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Hickok & Boardman HR Intelligence Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue

Brought to you by Hickok & Boardman HR Intelligence Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue

How To Calculate A Health Care Reform Employer Number

Health Care Reform Key Points Contact Us 855.220.8634 HealthCareReform@eidebailly.com Individual Implications Individual mandate to have health insurance Penalties applies if NO health insurance 2014 -

Health Care Reform Key Points Contact Us 855.220.8634 HealthCareReform@eidebailly.com Individual Implications Individual mandate to have health insurance Penalties applies if NO health insurance 2014 -

How To Report Health Insurance To The Irs

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS were collected at a series of webinars offered by ThinkHR. Introduction The Affordable Care

ACA REPORTING WEBINAR QUESTIONS AND ANSWERS The following questions on ACA reporting requirements to the IRS were collected at a series of webinars offered by ThinkHR. Introduction The Affordable Care

Health Care Reform Where Are We Now? Preparing for 2015

Tuesday, July 1, 2014 2 3 p.m. Central time Health Care Reform Where Are We Now? Preparing for 2015 David Hunt, CHBC Senior Managing Consultant BKD, LLP dhunt@bkd.com Philip Floyd, CFP, CFS Senior Managing

Tuesday, July 1, 2014 2 3 p.m. Central time Health Care Reform Where Are We Now? Preparing for 2015 David Hunt, CHBC Senior Managing Consultant BKD, LLP dhunt@bkd.com Philip Floyd, CFP, CFS Senior Managing

IRS Issues Final Regulations on Employer Shared Responsibility (Play or Pay)

") IRS Issues Final Regulations on Employer Shared Responsibility (Play or Pay) On February 10, 2014, the IRS issued final regulations on the employer-shared responsibility requirements, often known as play

IRS Issues Final Regulations on Employer Shared Responsibility (Play or Pay) On February 10, 2014, the IRS issued final regulations on the employer-shared responsibility requirements, often known as play

PENALTIES Employer Shared Responsibility under the Affordable Care Act (ACA)

") PENALTIES Employer Shared Responsibility under the Affordable Care Act (ACA) What employers need to know to make informed decisions about ACA compliance. Employer Shared Responsibility Under the employer

PENALTIES Employer Shared Responsibility under the Affordable Care Act (ACA) What employers need to know to make informed decisions about ACA compliance. Employer Shared Responsibility Under the employer

Overview of Reporting Requirements. ACA Reporting. Overview. Overview of Reporting Requirements. ACA Reporting Examples

ACA Reporting August 18, 2015 Norbert F. Kugele April A. Goff 2015 Warner Norcross & Judd LLP. All rights reserved. WNJ.com Overview Overview of Reporting Requirements Why have reporting Status of forms

ACA Reporting August 18, 2015 Norbert F. Kugele April A. Goff 2015 Warner Norcross & Judd LLP. All rights reserved. WNJ.com Overview Overview of Reporting Requirements Why have reporting Status of forms

AFFORDABLE CARE ACT REPORTING

AFFORDABLE CARE ACT REPORTING Introduction The Affordable Care Act (ACA) requires the State of Missouri to offer health insurance to full time equivalent employees. The ACA also generally requires individual

AFFORDABLE CARE ACT REPORTING Introduction The Affordable Care Act (ACA) requires the State of Missouri to offer health insurance to full time equivalent employees. The ACA also generally requires individual

IRS Issues final regulations on employer shared responsibility requirements

IRS Issues final regulations on employer shared responsibility requirements Volume 37 Issue 46 April 17, 2014 The employer shared responsibility requirements commonly called the employer mandate are one

IRS Issues final regulations on employer shared responsibility requirements Volume 37 Issue 46 April 17, 2014 The employer shared responsibility requirements commonly called the employer mandate are one

Parker, Smith & Feek - ACA Update: 2014 November 2013

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

Employer s Guide To Health Care Reform

Employer s Guide To Health Care Reform A nonprofit independent licensee of the Blue Cross Blue Shield Association National strength. Local focus. Individual care. SM As part of our commitment to being

Employer s Guide To Health Care Reform A nonprofit independent licensee of the Blue Cross Blue Shield Association National strength. Local focus. Individual care. SM As part of our commitment to being

IRS Final Rule Partially Delays ACA Employer Shared Responsibility Requirement

A Timely Analysis of Legal Developments A S A P February 24, 2014 IRS Final Rule Partially Delays ACA Employer Shared Responsibility Requirement By Ilyse Schuman On February 12, 2014, the Internal Revenue

A Timely Analysis of Legal Developments A S A P February 24, 2014 IRS Final Rule Partially Delays ACA Employer Shared Responsibility Requirement By Ilyse Schuman On February 12, 2014, the Internal Revenue

Year-end Checklist for 2015 Compliance

Brought to you by Fringe Benefit Plans, Inc. / (407) 862-5900 Year-end Checklist for 2015 Compliance The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the

Brought to you by Fringe Benefit Plans, Inc. / (407) 862-5900 Year-end Checklist for 2015 Compliance The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the

Guidance issued on employer shared responsibility requirements

Guidance issued on employer shared responsibility requirements The shared responsibility requirements are one of the most significant provisions that employers need to address under the Affordable Care

Guidance issued on employer shared responsibility requirements The shared responsibility requirements are one of the most significant provisions that employers need to address under the Affordable Care

The Affordable Care Act: Summary of Employer Requirements

The Affordable Care Act: Summary of Employer Requirements July 2012 Discussion Outline Overview of the Affordable Care Act (ACA) Employer coverage requirements Employer reporting requirements Individual

The Affordable Care Act: Summary of Employer Requirements July 2012 Discussion Outline Overview of the Affordable Care Act (ACA) Employer coverage requirements Employer reporting requirements Individual

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA)

") Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

Employee Benefits Compliance

Employee Benefits Compliance Pay or Play Delay, Does it Apply and Strategies to Comply Wells Fargo Insurance 2014 Issues and beyond. U.S. citizens and legal residents are required to have "minimum essential

Employee Benefits Compliance Pay or Play Delay, Does it Apply and Strategies to Comply Wells Fargo Insurance 2014 Issues and beyond. U.S. citizens and legal residents are required to have "minimum essential

American Benefits Council o Benefits Briefing

American Benefits Council o Benefits Briefing PPACA Information Reporting: Forms and Instructions 1095-C and 1094-C Seth T. Perretta Malcolm C. Slee March 12, 2015 Overview Brief refresher on today s main

American Benefits Council o Benefits Briefing PPACA Information Reporting: Forms and Instructions 1095-C and 1094-C Seth T. Perretta Malcolm C. Slee March 12, 2015 Overview Brief refresher on today s main

Helbling Benefits Consulting Your Health Care Reform Partner

Helbling Benefits Consulting Your Health Care Reform Partner Will you be hit with penalties due to health care reform? Once the employer mandate becomes effective, some employers may have to pay a penalty

Helbling Benefits Consulting Your Health Care Reform Partner Will you be hit with penalties due to health care reform? Once the employer mandate becomes effective, some employers may have to pay a penalty

To enforce these penalties and properly administer the premium tax credits, ACA imposes two annual reporting requirements on employers.

Employer Health Coverage Reporting Requirements for 2015 Summary The Affordable Care Act (ACA) includes reporting requirements for health care coverage in 2015. The reports will give information to the

Employer Health Coverage Reporting Requirements for 2015 Summary The Affordable Care Act (ACA) includes reporting requirements for health care coverage in 2015. The reports will give information to the

The Affordable Care Act: Running the ACA Reporting Maze

The Affordable Care Act: Running the ACA Reporting Maze National Association of State Comptrollers March 12, 2015 Prepared by: Russell Chapman Special Counsel Littler Mendelson, P.C. Dallas Office 214.880.8177

The Affordable Care Act: Running the ACA Reporting Maze National Association of State Comptrollers March 12, 2015 Prepared by: Russell Chapman Special Counsel Littler Mendelson, P.C. Dallas Office 214.880.8177

Shared Responsibility: What It Means for Your Business

Shared Responsibility: What It Means for Your Business The provisions of the Affordable Care Act (ACA) apply to nearly all companies in the United States. The ways they apply, however, can be different

Shared Responsibility: What It Means for Your Business The provisions of the Affordable Care Act (ACA) apply to nearly all companies in the United States. The ways they apply, however, can be different

Health in a Handbasket What Employers Need to Know Now

Health in a Handbasket What Employers Need to Know Now Presented by Steven J. Friedman Littler, New York 212-583-2687 Agenda Full Speed Ahead: Again? Pay-or-Play: What is the optimal strategy for you?

Health in a Handbasket What Employers Need to Know Now Presented by Steven J. Friedman Littler, New York 212-583-2687 Agenda Full Speed Ahead: Again? Pay-or-Play: What is the optimal strategy for you?

Health Care Reform. Employer Action Overview

Health Care Reform Page 1 of 6 Health Care Reform Immediatemmediate Employer Action Required Notes Employers must provide a reasonable break time for employees who are nursing mothers to express breast

Health Care Reform Page 1 of 6 Health Care Reform Immediatemmediate Employer Action Required Notes Employers must provide a reasonable break time for employees who are nursing mothers to express breast

NJ CUPA HR The Affordable Care Act & Its Implication for Employers April 4, 2014

NJ CUPA HR The Affordable Care Act & Its Implication for Employers April 4, 2014 About NJBIA Represents 21,000 companies of all sizes and types, which employ over 1 million workers in the State. Advocate

NJ CUPA HR The Affordable Care Act & Its Implication for Employers April 4, 2014 About NJBIA Represents 21,000 companies of all sizes and types, which employ over 1 million workers in the State. Advocate

Two New Reporting Requirements Beginning in 2016 But Are Important Now

Two New Reporting Requirements Beginning in 2016 But Are Important Now Recently, the IRS published final regulations implementing two new information reporting requirements under ACA that are first due

Two New Reporting Requirements Beginning in 2016 But Are Important Now Recently, the IRS published final regulations implementing two new information reporting requirements under ACA that are first due

Treasury and IRS Issue Final Regulations for Reporting Compliance With Affordable Care Act Mandates

Treasury and IRS Issue Final Regulations for Reporting Compliance With Affordable Care Act Mandates April 2014 The Treasury Department and the Internal Revenue Service (IRS) issued final regulations on

Treasury and IRS Issue Final Regulations for Reporting Compliance With Affordable Care Act Mandates April 2014 The Treasury Department and the Internal Revenue Service (IRS) issued final regulations on

IRS Releases Final Forms and Instructions for Affordable Care Act Reporting

IRS Releases Final Forms and Instructions for Affordable Care Act Reporting March 24, 2015 In February 2015, the IRS released final forms and instructions related to information reporting under the Affordable

IRS Releases Final Forms and Instructions for Affordable Care Act Reporting March 24, 2015 In February 2015, the IRS released final forms and instructions related to information reporting under the Affordable

Q&A from Assurex Global Webinar. Employer ACA Reporting Requirements. Q: Where will these forms come from? will the IRS provide them?

Q&A from Assurex Global Webinar Employer ACA Reporting Requirements Questions Q: Where will these forms come from? will the IRS provide them? A: IRS has provided draft Forms 1094 and 1095 along with draft

Q&A from Assurex Global Webinar Employer ACA Reporting Requirements Questions Q: Where will these forms come from? will the IRS provide them? A: IRS has provided draft Forms 1094 and 1095 along with draft

Employer Shared Responsibility (ESR) Questions and Answers.

Questions and Answers.") Employer Shared Responsibility (ESR) Questions and s. Recent ESR Questions asked by members of the accounting community, answered by senior members of Paychex Compliance Department. Question 1. When using

Employer Shared Responsibility (ESR) Questions and s. Recent ESR Questions asked by members of the accounting community, answered by senior members of Paychex Compliance Department. Question 1. When using

Employer-Sponsored Coverage Reporting Requirements

Under ACA rules, all employers that offer self-insured health plans must report new, detailed information on every individual covered under their health plan. There are reporting requirements for self-insured

Under ACA rules, all employers that offer self-insured health plans must report new, detailed information on every individual covered under their health plan. There are reporting requirements for self-insured

Potential Penalties for Employers under the Pay or Play Rules

The Affordable Care Act (ACA) brings many changes to employers and health plans. One such change essentially amounts to a requirement for some employers to offer a certain level health care to their employees

The Affordable Care Act (ACA) brings many changes to employers and health plans. One such change essentially amounts to a requirement for some employers to offer a certain level health care to their employees

Health Care Reform: What to Expect in 2013 2014. Employee Benefits Series. Health Care Reform 2015 COMPLIANCE CHECKLIST

Health Care Reform: What to Expect in 2013 2014 Employee Benefits Series Health Care Reform 2015 COMPLIANCE CHECKLIST This checklist is designed to help employers who sponsor group health plans review

Health Care Reform: What to Expect in 2013 2014 Employee Benefits Series Health Care Reform 2015 COMPLIANCE CHECKLIST This checklist is designed to help employers who sponsor group health plans review

Health Reform. Employer Penalty Delay: What are the Consequences? Impact of the Delay on Employers

Health Reform Employer Penalty Delay: What are the Consequences? Martin Haitz (484) 270-2575 martin.haitz@marcumfs.com Issued date: 07/29/13 The employer penalty provisions and two reporting requirements

Health Reform Employer Penalty Delay: What are the Consequences? Martin Haitz (484) 270-2575 martin.haitz@marcumfs.com Issued date: 07/29/13 The employer penalty provisions and two reporting requirements

Affordable Care Act Update

Affordable Care Act Update Presented by: Jill Brooking, Vice President, Benefits Compliance National Financial Partners Corp. and its subsidiaries do not provide legal or tax advice. Compliance, regulatory

Affordable Care Act Update Presented by: Jill Brooking, Vice President, Benefits Compliance National Financial Partners Corp. and its subsidiaries do not provide legal or tax advice. Compliance, regulatory

March 26, 2015. Q&A from Assurex Global Webinar "Employer ACA Reporting Requirements"

Q&A from Assurex Global Webinar "Employer ACA Reporting Requirements" Question Large employer 500+, have several health insurance coverages some self funded some fully insured so who gets it with both

Q&A from Assurex Global Webinar "Employer ACA Reporting Requirements" Question Large employer 500+, have several health insurance coverages some self funded some fully insured so who gets it with both

Sage HRMS The healthcare reform survival guide. Checklists and explanations to help you meet changing health benefits compliance mandates

Sage HRMS The healthcare reform survival guide Checklists and explanations to help you meet changing health benefits compliance mandates Table of contents Welcome to healthcare reform 3 The big question

Sage HRMS The healthcare reform survival guide Checklists and explanations to help you meet changing health benefits compliance mandates Table of contents Welcome to healthcare reform 3 The big question

The Affordable Care Act: Summary of Employer Requirements

The Affordable Care Act: Summary of Employer Requirements February 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding

The Affordable Care Act: Summary of Employer Requirements February 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding

Health care reform at-a-glance. December 2013

December 2013 Employer mandate Play or pay penalty for failing to offer coverage to at least 95% of all full-time employees (FTE) and children if any FTE gets subsidy in exchange $2,000 (indexed) times

December 2013 Employer mandate Play or pay penalty for failing to offer coverage to at least 95% of all full-time employees (FTE) and children if any FTE gets subsidy in exchange $2,000 (indexed) times

Legislative Brief: 2015 COMPLIANCE CHECKLIST. Laurus Strategies

Laurus Strategies Legislative Brief: 2015 COMPLIANCE CHECKLIST The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago.

Laurus Strategies Legislative Brief: 2015 COMPLIANCE CHECKLIST The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago.

Health Care Reform Guide for Staffing Firms

Oct. 5, 2012 By Edward A. Lenz, Esq. Senior Vice President, Legal and Public Affairs American Staffing Association 703-253-2035 elenz@americanstaffing.net Alden J. Bianchi, Esq. Chairman, Compensation

Oct. 5, 2012 By Edward A. Lenz, Esq. Senior Vice President, Legal and Public Affairs American Staffing Association 703-253-2035 elenz@americanstaffing.net Alden J. Bianchi, Esq. Chairman, Compensation

Employer Tax Penalties Linked to Employees Receiving Tax Credits. Calculation of Non-deductible Excise Taxes Under IRC 4380H

Washington Council Employer Tax Penalties Linked to Employees Receiving Tax Credits Employers will face taxes under IRC 4980H if they do not offer minimum essential coverage or if the coverage they offer

Washington Council Employer Tax Penalties Linked to Employees Receiving Tax Credits Employers will face taxes under IRC 4980H if they do not offer minimum essential coverage or if the coverage they offer

What Employers Need to Know about the Final ACA Reporting Forms

What Employers Need to Know about the Final ACA Reporting Forms We highly recommend that you download the slides prior to the webinar at http://ow.ly/lccoh (case sensitive) Laura Kerekes, SPHR, SHRM-SCP

What Employers Need to Know about the Final ACA Reporting Forms We highly recommend that you download the slides prior to the webinar at http://ow.ly/lccoh (case sensitive) Laura Kerekes, SPHR, SHRM-SCP

Employer s guide to health care reform requirements

Employer s guide to health care reform requirements June 2015 edition As the Affordable Care Act (ACA) continues to be implemented, you ll need to remain aware of the policies and provisions that affect

Employer s guide to health care reform requirements June 2015 edition As the Affordable Care Act (ACA) continues to be implemented, you ll need to remain aware of the policies and provisions that affect

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

The Patient Protection and Affordable Care Act ( ACA ) and Your Facility

and Your Facility") The Patient Protection and Affordable Care Act ( ACA ) and Your Facility By Christine Garrity: Chief Administrative Officer & General Counsel for The Professional Golfers' Association of America President

The Patient Protection and Affordable Care Act ( ACA ) and Your Facility By Christine Garrity: Chief Administrative Officer & General Counsel for The Professional Golfers' Association of America President

Compliance Alert. IRS Notice 2015-87 Clarifies Several ACA Rules for Employers

Compliance Alert IRS Notice 2015-87 Clarifies Several ACA Rules for Employers December 29, 2015 Quick Facts: Notice 2015-87 clarifies a number of ACA rules for employer-provided health coverage. Key topics

Compliance Alert IRS Notice 2015-87 Clarifies Several ACA Rules for Employers December 29, 2015 Quick Facts: Notice 2015-87 clarifies a number of ACA rules for employer-provided health coverage. Key topics

Affordable Care Act (ACA) Violations Penalties and Excise Taxes

Violations Penalties and Excise Taxes") Brought to you by The Insurance Exchange Affordable Care Act (ACA) Violations Penalties and Excise Taxes The Affordable Care Act (ACA) includes numerous reforms for group health plans and creates new compliance

Brought to you by The Insurance Exchange Affordable Care Act (ACA) Violations Penalties and Excise Taxes The Affordable Care Act (ACA) includes numerous reforms for group health plans and creates new compliance

Health Reform in a Nutshell: What Small Businesses Need to Know Now.

Health Reform in a Nutshell: What Small Businesses Need to Know Now. With the passage of the most significant reform of America s modern-day health care system, many small business owners and human resources

Health Reform in a Nutshell: What Small Businesses Need to Know Now. With the passage of the most significant reform of America s modern-day health care system, many small business owners and human resources

Health Reform Employer Impact Analysis. Sample Employer. Prepared for. Date

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Treasury, IRS Release Final Rules on Employer Information Reporting Requirements Under Health Care Law

March 6, 2014 Treasury, IRS Release Final Rules on Employer Information Reporting Requirements Under Health Care Law The Department of the Treasury and the IRS late yesterday (March 6, 2014) released long

March 6, 2014 Treasury, IRS Release Final Rules on Employer Information Reporting Requirements Under Health Care Law The Department of the Treasury and the IRS late yesterday (March 6, 2014) released long

COMMENTARY. Deciding Whether to Play or Pay Under the Affordable Care Act. Q&A 1: What Is the Employer Mandate? JONES DAY

march 2013 JONES DAY COMMENTARY Deciding Whether to Play or Pay Under the Affordable Care Act The Patient Protection and Affordable Care Act (the ACA ) adds a new Section 4980H to the Internal Revenue

march 2013 JONES DAY COMMENTARY Deciding Whether to Play or Pay Under the Affordable Care Act The Patient Protection and Affordable Care Act (the ACA ) adds a new Section 4980H to the Internal Revenue

IRS Health Coverage Reporting Instructions Leave Many Questions Unanswered

September 23, 2014 If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Katie Bjornstad Amin kamin@groom.com (202) 861-2604 Christine L. Keller ckeller@groom.com

September 23, 2014 If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Katie Bjornstad Amin kamin@groom.com (202) 861-2604 Christine L. Keller ckeller@groom.com

ACA Employer Mandate: The Ultimate Guide

ACA Employer Mandate: The Ultimate Guide Table of Contents Are you ready? WHO needs to comply? WHAT forms do you need to file to comply? WHEN do you need to file the forms? WHERE do you get the forms?

ACA Employer Mandate: The Ultimate Guide Table of Contents Are you ready? WHO needs to comply? WHAT forms do you need to file to comply? WHEN do you need to file the forms? WHERE do you get the forms?

Advantage Payroll Services Presents. March 24, 2015 Presenter: Jessica Stelfox, MBA, PHR

(c )A dv an ta ge Pa yr ol l Se rv ic es 20 15 Advantage Payroll Services Presents March 24, 2015 Presenter: Jessica Stelfox, MBA, PHR We encourage you to benefit from resources and information provided

(c )A dv an ta ge Pa yr ol l Se rv ic es 20 15 Advantage Payroll Services Presents March 24, 2015 Presenter: Jessica Stelfox, MBA, PHR We encourage you to benefit from resources and information provided

Health care reform at-a-glance. August 2014

Health care reform at-a-glance August 2014 Employer mandate Shared responsibility payment for failing to offer coverage to at least 95%* of all fulltime employees (FTE) and children if any FTE gets subsidy

Health care reform at-a-glance August 2014 Employer mandate Shared responsibility payment for failing to offer coverage to at least 95%* of all fulltime employees (FTE) and children if any FTE gets subsidy

Health Care Reform: Ready or Not, Here it Comes! Presented by:

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

W-2 Reporting Requirement

Revised January 2012 Notice 2012-9 provides guidance on W-2 reporting requirement IRS Issues New Guidance on Health Care Reform s The Internal Revenue Service (IRS) recently issued IRS Notice 2012-9, which

Revised January 2012 Notice 2012-9 provides guidance on W-2 reporting requirement IRS Issues New Guidance on Health Care Reform s The Internal Revenue Service (IRS) recently issued IRS Notice 2012-9, which

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax The Impact of the Affordable Care Act on International Assignees and Their Health Care Plans Employers and individuals in the United

What s News in Tax Analysis That Matters from Washington National Tax The Impact of the Affordable Care Act on International Assignees and Their Health Care Plans Employers and individuals in the United

ACA imposes a 40 percent excise tax on the cost of coverage exceeding $10,200 for single coverage and $27,500 for family coverage.

Affordable Care Act In Focus: Provisions Impacting Employer-Sponsored Health Coverage Through 2020 While many employers are wondering if self-funding is the right solution for their business, a number

Affordable Care Act In Focus: Provisions Impacting Employer-Sponsored Health Coverage Through 2020 While many employers are wondering if self-funding is the right solution for their business, a number

Employer's guide to health care reform

Employer's guide to health care reform Employer's guide to health care reform: the complete small business resource With the Affordable Care Act (ACA) in full swing, it s important you understand what

Employer's guide to health care reform Employer's guide to health care reform: the complete small business resource With the Affordable Care Act (ACA) in full swing, it s important you understand what

The Insurance Mandates of the Affordable Care Act

1 A. Affordable Care Act Individual Mandate The Insurance Mandates of the Affordable Care Act 1. All citizens of the United States are subject to the individual mandate as are all permanent residents and

1 A. Affordable Care Act Individual Mandate The Insurance Mandates of the Affordable Care Act 1. All citizens of the United States are subject to the individual mandate as are all permanent residents and

Important Effective Dates for Employers and Health Plans

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Affordable Care Act 101: What The Health Care Law Means for Small Employers

Affordable Care Act 101: What The Health Care Law Means for Small Employers These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers should consult

Affordable Care Act 101: What The Health Care Law Means for Small Employers These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers should consult

Since Congress passed the Patient Protection and

A Primer on New Applicable Large Employer Reporting Requirements under the ACA by Kathy A. Lawler and Madeline Sexton Lewis Since Congress passed the Patient Protection and Affordable Care Act (ACA) in

A Primer on New Applicable Large Employer Reporting Requirements under the ACA by Kathy A. Lawler and Madeline Sexton Lewis Since Congress passed the Patient Protection and Affordable Care Act (ACA) in

Fast Forward. 2015 Employer Mandate: Pay or Play?

Fast Forward 2015 Employer Mandate: Pay or Play? Employer Mandate Beginning Jan. 1, 2015, the Affordable Care Act (ACA) will impose an employer mandate that states that grandfathered and non-grandfathered

Fast Forward 2015 Employer Mandate: Pay or Play? Employer Mandate Beginning Jan. 1, 2015, the Affordable Care Act (ACA) will impose an employer mandate that states that grandfathered and non-grandfathered

Your guide to health care reform provisions

Your guide to health care reform provisions February 2014 edition Since the Patient Protection and Affordable Care Act (PPACA) was enacted in March 2010, businesses have been impacted by federal health

Your guide to health care reform provisions February 2014 edition Since the Patient Protection and Affordable Care Act (PPACA) was enacted in March 2010, businesses have been impacted by federal health

Health Care Reform Implications for Employers with Seasonal Employees

Health Care Reform Implications for Employers with Seasonal Employees Many industries (e.g. ski resorts, retail, restaurants, agriculture, fishing and tourism) have a significant number of seasonal employees.

Health Care Reform Implications for Employers with Seasonal Employees Many industries (e.g. ski resorts, retail, restaurants, agriculture, fishing and tourism) have a significant number of seasonal employees.

Christy Tinnes, Brigen Winters and Christine Keller, Groom Law Group, Chartered

Preparing for Health Care Reform A Chronological Guide for Employers This Article provides an overview of the major provisions of health care reform legislation affecting employers and explains the requirements

Preparing for Health Care Reform A Chronological Guide for Employers This Article provides an overview of the major provisions of health care reform legislation affecting employers and explains the requirements

ACA Impact on Health FSAs and HRAs Q&A the following questions were

ACA Impact on Health FSAs and HRAs Q&A the following questions were asked during the two webinar sessions in (January, 2015) Do SBCs need to be provided to retirees who have a Retiree Only HRA? Yes Is

ACA Impact on Health FSAs and HRAs Q&A the following questions were asked during the two webinar sessions in (January, 2015) Do SBCs need to be provided to retirees who have a Retiree Only HRA? Yes Is

The Effect of the Affordable Care Act on Your Small Business. Presented to : Greater Kansas City Chamber Business Class

The Effect of the Affordable Care Act on Your Small Business Presented to : Greater Kansas City Chamber Business Class November 6, 2013 KHN Kaiser Health News Current Headlines October 31- November 4,

The Effect of the Affordable Care Act on Your Small Business Presented to : Greater Kansas City Chamber Business Class November 6, 2013 KHN Kaiser Health News Current Headlines October 31- November 4,

The Affordable Care Act and Its Impact on Multiemployer Plans Selected Coverage Issues

The Affordable Care Act and Its Impact on Multiemployer Plans Selected Coverage Issues 2014 NCCMP Annual Conference September 23, 2014 Hollywood, Florida Carolyn E. Smith Alston & Bird LLP carolyn.smith@alston.com

The Affordable Care Act and Its Impact on Multiemployer Plans Selected Coverage Issues 2014 NCCMP Annual Conference September 23, 2014 Hollywood, Florida Carolyn E. Smith Alston & Bird LLP carolyn.smith@alston.com

Affordable Care Act: Taking Stock and Looking Ahead to 2017

Affordable Care Act: Taking Stock and Looking Ahead to 2017 Presented by: Regina Horton Legal Counsel Keenan Tim Crawford Vice President, Marketing Keenan Today s Agenda IRS Reporting Get Ready for Year

Affordable Care Act: Taking Stock and Looking Ahead to 2017 Presented by: Regina Horton Legal Counsel Keenan Tim Crawford Vice President, Marketing Keenan Today s Agenda IRS Reporting Get Ready for Year

Health Care Reform: Health Plans Overview. Presented by: Brian Lenzo, Preferred Benefits Services

Health Care Reform: Health Plans Overview Presented by: Brian Lenzo, Preferred Benefits Services Agenda What is the legal status of the law? Which plans must comply? Grandfathered plans Reforms currently

Health Care Reform: Health Plans Overview Presented by: Brian Lenzo, Preferred Benefits Services Agenda What is the legal status of the law? Which plans must comply? Grandfathered plans Reforms currently

Important Effective Dates for Employers and Health Plans

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345

Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345") 1 Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345 2 Terms you need to know Required Notices 2014 Plan Requirements The Grandfathered

1 Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345 2 Terms you need to know Required Notices 2014 Plan Requirements The Grandfathered

IRS Reporting for NON-Large Employers

IRS Reporting for NON-Large Employers NMASBO Fall Conference September 24, 2015 Nura Patani, PhD Senior Actuarial Analyst npatani@segalco.com Copyright 2015 by The Segal Group, Inc. All rights reserved.

IRS Reporting for NON-Large Employers NMASBO Fall Conference September 24, 2015 Nura Patani, PhD Senior Actuarial Analyst npatani@segalco.com Copyright 2015 by The Segal Group, Inc. All rights reserved.

IRS Proposes Rules for Federal Subsidy of Health Insurance Purchased in State Exchanges

IRS Proposes Rules for Federal Subsidy of Health Insurance Purchased in State Exchanges August 2011 The Internal Revenue Service (IRS) on August 12, 2011 issued proposed regulations relating to the federal

IRS Proposes Rules for Federal Subsidy of Health Insurance Purchased in State Exchanges August 2011 The Internal Revenue Service (IRS) on August 12, 2011 issued proposed regulations relating to the federal

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years Seyfarth Shaw has generously given permission to Lawyers Alliance for New York to circulate this chart

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years Seyfarth Shaw has generously given permission to Lawyers Alliance for New York to circulate this chart

Health Care Reform Planning for the Financial Impact on Businesses

October 13, 2010 Health Care Reform Planning for the Financial Impact on Businesses Joseph Kra, FSA, MAAA, New York Services provided by Health & Benefits LLC Agenda Future of Employer Sponsored Coverage

October 13, 2010 Health Care Reform Planning for the Financial Impact on Businesses Joseph Kra, FSA, MAAA, New York Services provided by Health & Benefits LLC Agenda Future of Employer Sponsored Coverage

COMMENTARY. The Affordable Care Act: Considerations for Employers with Unionized Workers JONES DAY

March 2014 JONES DAY COMMENTARY The Affordable Care Act: Considerations for Employers with Unionized Workers The Affordable Care Act ( ACA ) infuses new complexities into collective bargaining negotiations

March 2014 JONES DAY COMMENTARY The Affordable Care Act: Considerations for Employers with Unionized Workers The Affordable Care Act ( ACA ) infuses new complexities into collective bargaining negotiations

The Impact on Business

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

Health care reform for large businesses

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

Health Care Law Implementation: What Nonprofits Need to Know WELCOME!

Health Care Law Implementation: What Nonprofits Need to Know WELCOME! Health Care Law Implementation: What Nonprofits Need to Know (PPACA) Health Care Law Implementation: What Nonprofits Need to Know Heather

Health Care Law Implementation: What Nonprofits Need to Know WELCOME! Health Care Law Implementation: What Nonprofits Need to Know (PPACA) Health Care Law Implementation: What Nonprofits Need to Know Heather

2015 Open Enrollment Checklist

Brought to you by Benefit Administration Company, LLC. 2015 Open Enrollment Checklist To prepare for open enrollment, health plan sponsors should become familiar with the legal changes affecting the design

Brought to you by Benefit Administration Company, LLC. 2015 Open Enrollment Checklist To prepare for open enrollment, health plan sponsors should become familiar with the legal changes affecting the design

ACA: Understanding the Defining a Path Forward

ACA: Understanding the Defining a Path Forward by Frances Marbury and Rachael Walker Each organization s unique circumstances will determine how it responds to the Affordable Care Act (ACA). Employers

ACA: Understanding the Defining a Path Forward by Frances Marbury and Rachael Walker Each organization s unique circumstances will determine how it responds to the Affordable Care Act (ACA). Employers

4/8/2013. Health Care Reform and the. NYS Exchange. Dr. Arthur Vercillo, MD Regional President April 8, 2013. Health Care Reform and the NYS Exchange

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health