What is a Dedicated Account?

|

|

|

- Wilfrid Hunt

- 10 years ago

- Views:

Transcription

1 What is a Dedicated Account? When the Social Security Administration (SSA) determines that your child is disabled and eligible for Supplemental Security Income benefits (SSI), your child will start getting benefits every month. If time has passed since you first applied, your child will also get back benefits, or retroactive benefits. These can cover the period from the month after you applied until your child was approved. To get this money, you will have to open a separate bank account called a dedicated account. SSA will deposit your child s back benefits into this account. This is your child s money, but there are limits on how you can spend it. You can only use it for items and services that relate to your child s disability and benefit the child. To set up a dedicated account, bring the notice from the SSA showing your child is entitled to back payments to the bank of your choice. Tell them that you would like to set up a dedicated account in your child s name. Remember to bring proper identification. The account must be separate from the account you use for the regular monthly benefit payments and can only be a checking, savings, or money market account. The bank will give you an account number to give to the SSA for direct deposits. The Children s Disability Project created this Saving and Spending Workbook to help you handle your child s back benefits. This handbook will: Explain how you can use the money in your child s dedicated account; Explain how to get permission for a special purchase that will help your child; and Help you keep track of your purchases, receipts, and approval letters. IMPORTANT: The information in this workbook only relates to the money in your child s dedicated account. It does not apply to your child s regular monthly benefits. You can use your child s monthly benefits for daily living expenses, such as food, clothing, and shelter.

2 Do s & Dont s of Dedicated Spending Accounts DO: DO spend money on education, medical needs, and other costs related to your child s disability. DO get permission from the SSA office, in writing, for any purchases that aren t clearly medical or educational. You can appeal the decision if the SSA decides that you can t spend the money the way that you want. DO keep track of how you spend the money. Save your receipts and any letters you get from your child s doctors or teachers explaining why you made the purchase. DON T: DON T spend the money from this account on ordinary living expenses food, rent or mortgage, clothing, or furniture. You can use the money from your child s monthly check for these kinds of expenses. o Exception: if your family is in danger of becoming homeless, or in danger of being evicted, you may be able to spend money in order to rent or buy a home, but you should first check with SSA. DON T mix the money in the dedicated spending account with any other money. DON T throw away your receipts or any letters you get from the SSA office, your child s doctor, or your child s teachers about your request to use the money.

3 Keeping Back Benefits Separate How does the money in my child s dedicated account affect my child s eligibility for benefits? SSI eligibility rules are strict about any income you have and any resources your family has access to. Money in your child s dedicated account does not count as a resource or income. That means your child can get benefits even if the account has more than $2000. Can I put other funds in the dedicated account? The basic answer is NO. In fact, if you mix funds with your child s dedicated account, the SSA might consider the whole account, including the amount that came from the back-payment, a resource. If this brings your child s resources to the $2,000 limit, SSA could stop your child s benefits. It is very important to keep your child s back benefits completely separate from any other money. Are there any special cases when I can add funds to the dedicated account? The rule is that ONLY your child s retroactive awards of SSI can be in the dedicated account. However, in some special cases, you may be able to add funds to an existing dedicated account. You may want to do this when a later SSI payment would put your child over the $2,000 asset limit, and you cannot spend the amount right away. The only types of payments that you may be able to add to an already-established dedicated account are: Later underpayments or back payments from SSA. If you receive another award of back payments or an award due to underpayment, consult the SSA about whether this money can or must be put in your child s dedicated account. Any interest payments created by the money in the dedicated account. You can only add these funds to a dedicated account that has already been created. Once you put this money in the account, it is subject to the same spending rules as the rest of the account. What if I have to add money to the account to open it? You can use a small amount of money (up to about $25) that isn t part of the back-payment to open your child s dedicated spending account. You may have to do this if your bank needs a minimum deposit to open an account. The Social Security Administration calls this a temporary loan. You must withdraw the money that you use to open the account by the end of the month following the month that the SSA deposits the back-payments. The money that you use to open the account will still count as a resource.

4 How to Get Permission for a Special Purchase Money from your child s dedicated account can be used for medical treatment or education and job skills training. It can also be used for other items and services if they are related to your child s disability and benefit the child. If you are not certain that your purchase will be allowed, you should ask for approval first. You don t want to be stuck paying back the cost later! First, put together the following information: What the item is, and about how much it costs (a quote can be helpful); How the item is related to the child s disability; and Letters from the child s doctor or other treatment source that can support the medical use of the item or Letters from the child s teachers or administrators at the school that can support the educational use of the item. Next, contact your local SSA office. Explain to the claims representative that you want to buy something with money from the dedicated account. SSA might make a decision right away over the phone. If SSA does make a decision, ask for something in writing that you can keep in your files. SSA probably won t make a decision on the phone. Instead, SSA may ask you to send them the information that you put together explaining why you need to buy the item. Send SSA a copy of the materials and keep the originals. If the local office says that you cannot make the purchase, you have 30 days to appeal the decision. If it is denied again, you have the right to a hearing before an Administrative Law Judge and can appeal it further to a federal court. If you request approval for a purchase, don t spend the money until you have received approval.

; How the item is related to the child s disability; and Letters from the child s")

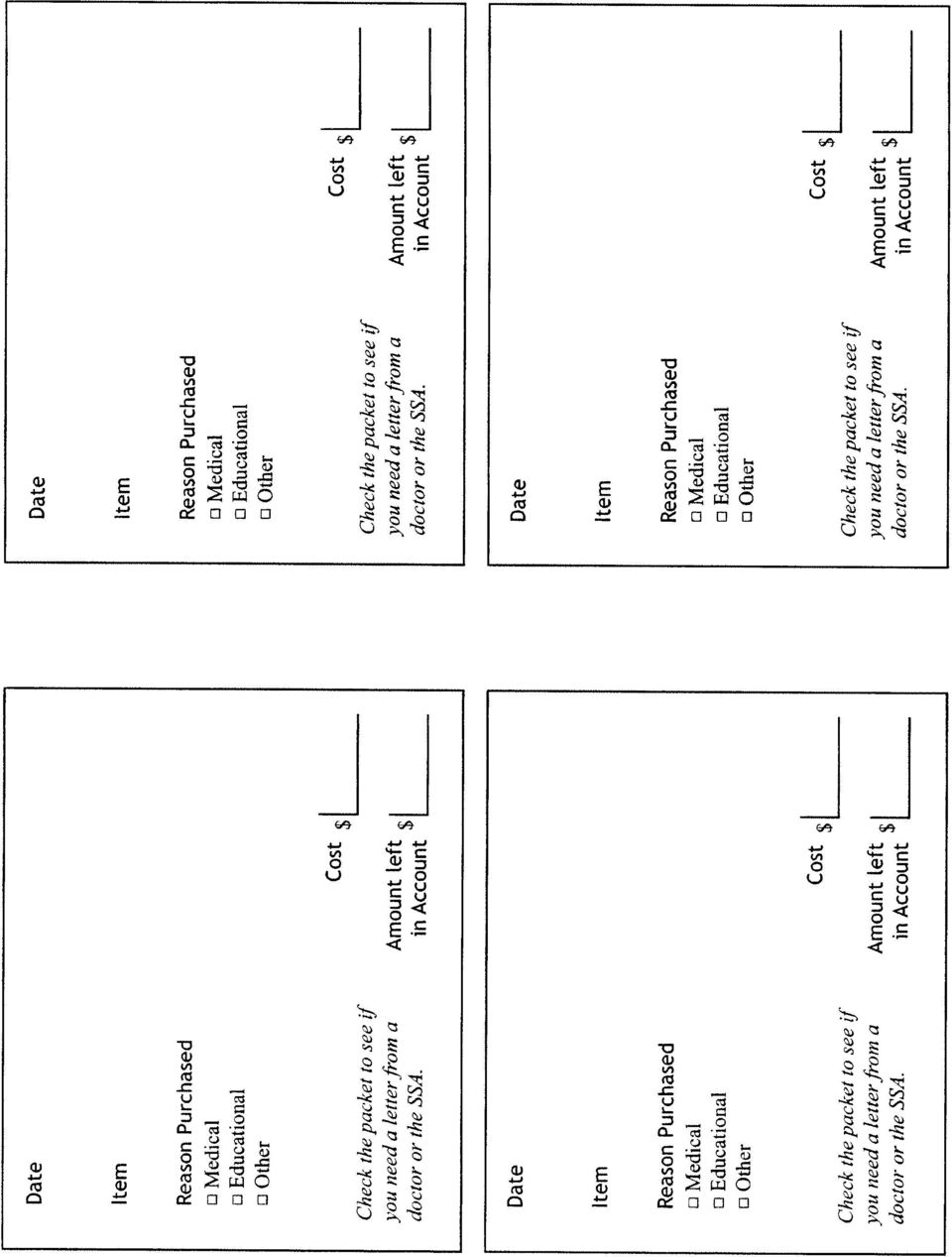

5 How to Keep Track of Your Spending Every year, SSA will ask you to fill out a report on how you used the money from your child s dedicated account. It is very important that you keep track of how you spend the money. Always keep receipts from the purchase and all bank statements. You should also keep any letters from SSA approving a purchase and any letters from doctors or teachers that say why the purchase is necessary. Also keep copies of approval notices. SSA recommends keeping records for at least two years. Use checks or a debit card (sometimes called a check card). If you use checks, the canceled check will be proof of how you spent the money. If you use a debit card, your bank statement will say how much you spent and where you spent it. Track each purchase in an account register or your check register. An account register is a simple way to track your spending. If you record all your purchases at the time you spend the money, it will be easier to explain each purchase later. We provided an account register for you to record each purchase. You may want to make copies before you use it so you don t run out of pages. Balance the accounts each month. Check the account register against your monthly bank statement. If you use a debit card or checks, each transaction will appear on your bank statement.

. If you use checks, the canceled check will be proof of how you spent the money.")

6 Examples of Purchases That May be Allowed Hearing aids and other aids to help the child learn or talk with others Wheelchairs and other items to help the child move around Special class books for deaf or blind students, and other special educational material Special foods, if the child needs them because of the disability Clothing that the child needs because of the disability, such as: o Orthopedic shoes o Special pants for incontinent children Cost of gas and electricity to use special equipment the child needs Special day care or helpful activities like the Special Olympics and summer camps for disabled children Food and veterinary care for a guide dog or another animal that helps the child Repair/replacement bills for walls, carpets or furniture that have been broken by a disabled child Counseling, crisis intervention services, respite care, and therapeutic foster care, if health insurance doesn t cover it Repayment of debt, even repayment of debt to the parent or representative payee for items that you bought to help the child with his or her impairment Attorney fees related to the child's disability claim Special appliances, services, or furniture for the child s disability, such as: o Air conditioning for a child with asthma o A washing machine for an incontinent child o A phone line to make sure you have access to a service you need Household renovations needed for the child's health, such as: o Insulating a home for a child who can t handle very warm or cold temperatures o A separate bedroom needed for a child with emotional disabilities Special toys related to the child s disability Computers, accessories and educational software that can help the child learn or develop other skills Cost to get the child to training classes, therapy sessions, doctors' appointments, etc. o Bus or cab fare o The purchase of a car or van, if needed Remember, you should always keep records of how purchases are related to your child s disability.

7 Examples from Actual Requests The owner of an apartment wanted to evict a family because the autistic child made noisy outbursts. The SSA let the family use money from the dedicated account to rent a house, because the outbursts were part of the child s disability. A child who used a wheelchair needed to get to therapy sessions every week. The SSA approved the cost of a van that could carry the wheelchair because the doctor said the child would need to go to therapy for a long time. The SSA did not let the family buy a special van, because a regular van would work. A disabled child needed new shoes. The SSA denied the request because the shoes weren t related to the child s disability. A family with a disabled child was living in a home with lead based paint and dirty water. The health department said the family had to leave. The SSA let the family use money from the dedicated account for the closing costs and a down payment on a used trailer and a lot. o Even if the family isn t about to be homeless, the SSA might approve the costs for a new home if the current home is in such bad shape that it is bad for the child s health. A child s family had to pay for medications and transportation to hospitals or clinics before the SSA approved the child s claim for SSI. The SSA let the parent use funds from the dedicated account to make up for the past expenses. A parent needed to go out for a short time to shop and take care of personal business. The SSA approved the cost for child care, but not the costs of shopping, a movie, or other expenses that the parent had. A child had tuition costs for a private school. The SSA approved the tuition cost because it is an educational expense. A child s school helped the family pick out a computer and software that would help the child learn. It wasn t the cheapest computer, but the school explained that it was the cheapest one that could run all of the software and last a long time. The SSA approved the purchase because it was an educational expense and the computer they chose was a reasonable price.

8

9

10

11

12

13

14

15

A Guide For Representative Payees

A Guide For Representative Payees Contact Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security Statement,

A Guide For Representative Payees Contact Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security Statement,

A Guide For Representative Payees

A Guide For Representative Payees Contact Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our website

A Guide For Representative Payees Contact Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our website

SOCIAL SECURITY OVERPAYMENTS:

SOCIAL SECURITY OVERPAYMENTS: RESPONDING TO A NOTICE THAT SAYS YOU HAVE BEEN OVERPAID This document contains general information for educational purposes and should not be construed as legal advice. It

SOCIAL SECURITY OVERPAYMENTS: RESPONDING TO A NOTICE THAT SAYS YOU HAVE BEEN OVERPAID This document contains general information for educational purposes and should not be construed as legal advice. It

Dealing with debt Top Tips

Dealing with debt Top Tips Don t ignore the problem it won t go away. The longer you leave it, the worse it will get. Get advice from the Student Advice Centre, Citizens Advice Bureau or other independent

Dealing with debt Top Tips Don t ignore the problem it won t go away. The longer you leave it, the worse it will get. Get advice from the Student Advice Centre, Citizens Advice Bureau or other independent

Making it happen SUPPLEMENTAL SECURITY INCOME (SSI) BENEFITS FOR ADULTS

BENEFITS FOR ADULTS") Making it happen SUPPLEMENTAL SECURITY INCOME (SSI) BENEFITS FOR ADULTS SECTION 1 SECTION 2 Introduction...1 What are Supplemental Security Income (SSI) Benefits?...2 Who is Eligible for SSI Benefits?...2

Making it happen SUPPLEMENTAL SECURITY INCOME (SSI) BENEFITS FOR ADULTS SECTION 1 SECTION 2 Introduction...1 What are Supplemental Security Income (SSI) Benefits?...2 Who is Eligible for SSI Benefits?...2

how much would you spend?

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

Working While Disabled How We Can Help

Working While Disabled How We Can Help 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

Working While Disabled How We Can Help 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

COLLEGE. Going from high school to college. Getting Ready for College CHAPTER 1. Getting organized

CHAPTER 1 COLLEGE Getting Ready for College Going from high school to college means taking more difficult classes, meeting new people, and setting your own hours. But it also means taking charge of your

CHAPTER 1 COLLEGE Getting Ready for College Going from high school to college means taking more difficult classes, meeting new people, and setting your own hours. But it also means taking charge of your

how much would you spend? answer key

scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining a car. Manuel s net monthly

scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining a car. Manuel s net monthly

Contents. Why budget? Do I need to budget? Why budget? 3. Do I need a budget? 3. Some budgeting ideas 4. Talking with a budgeting advisor 5

Managing your money Contents Why budget? Why budget? 3 Do I need a budget? 3 Some budgeting ideas 4 Talking with a budgeting advisor 5 Extra help with costs 6 Budget worksheet to help you get started 7

Managing your money Contents Why budget? Why budget? 3 Do I need a budget? 3 Some budgeting ideas 4 Talking with a budgeting advisor 5 Extra help with costs 6 Budget worksheet to help you get started 7

Supplemental Security Income (SSI) Information for Transitioning Foster Youth

Information for Transitioning Foster Youth") Supplemental Security Income (SSI) Information for Transitioning Foster Youth What Is SSI? Supplemental Security Income (SSI) is a needs-based program that gives cash aid to blind and disabled people (and

Supplemental Security Income (SSI) Information for Transitioning Foster Youth What Is SSI? Supplemental Security Income (SSI) is a needs-based program that gives cash aid to blind and disabled people (and

FACT SHEET. Money matters. Paying bills

12 FACT SHEET Money matters This fact sheet provides advice and information about how best to manage your money to make it easier to manage your household expenses. It also provides details of agencies

12 FACT SHEET Money matters This fact sheet provides advice and information about how best to manage your money to make it easier to manage your household expenses. It also provides details of agencies

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS 1 You should file for bankruptcy only after carefully deciding that bankruptcy is the best way to deal with your financial problems. This pamphlet

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS 1 You should file for bankruptcy only after carefully deciding that bankruptcy is the best way to deal with your financial problems. This pamphlet

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help What is a budget? A budget is a plan for the money you expect to receive and how

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help What is a budget? A budget is a plan for the money you expect to receive and how

Supplemental Security Income (SSI)

") Supplemental Security Income (SSI) Contact Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our

Supplemental Security Income (SSI) Contact Social Security Visit our website Our website, www.socialsecurity.gov, is a valuable resource for information about all of Social Security s programs. At our

SOUTH CAROLINA BAR. Consumer debt and the law

SOUTH CAROLINA BAR Consumer debt and the law D o you owe someone money? Having trouble paying off your debt? This brochure can help you understand your rights as a consumer debtor. WHAT HAPPENS IF YOU

SOUTH CAROLINA BAR Consumer debt and the law D o you owe someone money? Having trouble paying off your debt? This brochure can help you understand your rights as a consumer debtor. WHAT HAPPENS IF YOU

Dimes to Riches Money Management for Teens in Grades 7-12

Dimes to Riches Money Management for Teens in Grades 7-12 s e e r t n o row g t n s e o yd e n o M t a! h k t n a w b o n a k t u n By now yo Your parents are & Life is getting busy and you need cash for

Dimes to Riches Money Management for Teens in Grades 7-12 s e e r t n o row g t n s e o yd e n o M t a! h k t n a w b o n a k t u n By now yo Your parents are & Life is getting busy and you need cash for

SOCIAL SECURITY BENEFITS

SOCIAL SECURITY BENEFITS Social Security is a federal program that pays monthly payments to aged, blind and disabled people. In some cases, dependents and survivors also get benefits. The Social Security

SOCIAL SECURITY BENEFITS Social Security is a federal program that pays monthly payments to aged, blind and disabled people. In some cases, dependents and survivors also get benefits. The Social Security

housing answers for residents of public housing falling behind in the rent Benefits Plus Learning Center Fighting Poverty Strengthening New York

housing answers for residents of public housing falling behind in the rent Benefits Plus Learning Center Fighting Poverty Strengthening New York The Community Service Society of New York (CSS), a non-partisan

housing answers for residents of public housing falling behind in the rent Benefits Plus Learning Center Fighting Poverty Strengthening New York The Community Service Society of New York (CSS), a non-partisan

Benefits For Children With Disabilities

Benefits For Children With Disabilities 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

Benefits For Children With Disabilities 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

Connecticut Birth to Three System. A Family Handbook. Guide 3: Transition to Early Childhood Special Education

Connecticut Birth to Three System A Family Handbook Guide 3: Transition to Early Childhood Special Education July 2013 Connecticut Birth to Three System A Family Handbook This handbook and others are available

Connecticut Birth to Three System A Family Handbook Guide 3: Transition to Early Childhood Special Education July 2013 Connecticut Birth to Three System A Family Handbook This handbook and others are available

government benefits planning: what claimants need to know

government benefits planning: what claimants need to know Government Benefits Hotline: 800-683-4872 [email protected] www.settlement-alliance.com My family relies on Medicaid and Supplemental

government benefits planning: what claimants need to know Government Benefits Hotline: 800-683-4872 [email protected] www.settlement-alliance.com My family relies on Medicaid and Supplemental

SUPPLEMENTAL SECURITY INCOME (SSI)

") SUPPLEMENTAL SECURITY INCOME (SSI) The SSI program makes payments to people with low income, who are age 65 or older, or are blind, or have a disability. The Social Security Administration manages the

SUPPLEMENTAL SECURITY INCOME (SSI) The SSI program makes payments to people with low income, who are age 65 or older, or are blind, or have a disability. The Social Security Administration manages the

Adviceguide Advice that makes a difference

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

YOUR RIGHTS AS A TENANT

YOUR RIGHTS AS A TENANT Under Virginia Law, tenants have certain rights when they move in, while they are renting, and before they can be evicted. The specific rights you have depend on whether or not

YOUR RIGHTS AS A TENANT Under Virginia Law, tenants have certain rights when they move in, while they are renting, and before they can be evicted. The specific rights you have depend on whether or not

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Working While Disabled A Guide to Plans for Achieving Self-Support

Working While Disabled A Guide to Plans for Achieving Self-Support Working While Disabled A Guide to Plans for Achieving Self-Support What is a plan for achieving self-support (PASS)? A plan for achieving

Working While Disabled A Guide to Plans for Achieving Self-Support Working While Disabled A Guide to Plans for Achieving Self-Support What is a plan for achieving self-support (PASS)? A plan for achieving

DEBT DEBT. Dealing with. Self-help guide... abc IN TRAN. www.broadland.gov.uk. communication for all

Self-help guide... DEBT Dealing with DEBT abc www.broadland.gov.uk IN TRAN communication for all Where to get ADVICE on debt problems If you feel that you have money problems that are too difficult to

Self-help guide... DEBT Dealing with DEBT abc www.broadland.gov.uk IN TRAN communication for all Where to get ADVICE on debt problems If you feel that you have money problems that are too difficult to

FAQ: REP PAYEES OPPORTUNITY ACCESS CHOICE. What is a rep payee? What is a beneficiary? Why do I have a payee? Is my payee my legal guardian?

OPPORTUNITY ACCESS CHOICE FAQ: REP PAYEES What is a rep payee? A rep payee (short for representative payee) is a person or an organization picked by Social Security who manages the money you get from Social

OPPORTUNITY ACCESS CHOICE FAQ: REP PAYEES What is a rep payee? A rep payee (short for representative payee) is a person or an organization picked by Social Security who manages the money you get from Social

QUESTIONS CONCERNING BANKRUPTCY

QUESTIONS CONCERNING BANKRUPTCY The Law Office of Paul D. Post, P.A. is a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code. The assistance provided to clients may

QUESTIONS CONCERNING BANKRUPTCY The Law Office of Paul D. Post, P.A. is a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code. The assistance provided to clients may

Employment and Income Assistance for Persons with Disabilities 2015-2016

Employment and Income Assistance for Persons with Disabilities 2015-2016 INTRODUCTION The Employment and Income Assistance Program (EIA) provides financial help to Manitobans who have no other way to support

Employment and Income Assistance for Persons with Disabilities 2015-2016 INTRODUCTION The Employment and Income Assistance Program (EIA) provides financial help to Manitobans who have no other way to support

Home Buyer Self Pre-Qualification Workbook

Home Buyer Self Pre-Qualification Workbook Bethel Community Development Corporation Bethel Community Development Corporation 1525 Michigan Avenue Buffalo, NY 14209 (716) 886-1650, ext 225 Fax: (716) 886-2311

Home Buyer Self Pre-Qualification Workbook Bethel Community Development Corporation Bethel Community Development Corporation 1525 Michigan Avenue Buffalo, NY 14209 (716) 886-1650, ext 225 Fax: (716) 886-2311

Center for Disability Rights, Inc. Community Supplemental Needs Pooled Trust

Center for Disability Rights, Inc. Community Supplemental Needs Pooled Trust What is the Center for Disability Rights Community Supplemental Needs Trust? Individuals who have too much money to qualify

Center for Disability Rights, Inc. Community Supplemental Needs Pooled Trust What is the Center for Disability Rights Community Supplemental Needs Trust? Individuals who have too much money to qualify

A QUICK AND EASY GUIDE TO SSI AND SSDI

A QUICK AND EASY GUIDE TO SSI AND SSDI Independent Living Resource Center San Francisco 649 Mission Street, 3rd Floor San Francisco, CA 94105-4128 (415) 543-6222 (415) 543-6318 Fax (415) 543-6698 TTY only

A QUICK AND EASY GUIDE TO SSI AND SSDI Independent Living Resource Center San Francisco 649 Mission Street, 3rd Floor San Francisco, CA 94105-4128 (415) 543-6222 (415) 543-6318 Fax (415) 543-6698 TTY only

Savings and Bank Accounts

LESSON 2 Savings Savings and Bank Accounts Quick Write Suppose a relative gives you a generous gift of $1,000 for your sixteenth birthday. Your parent or guardian says that you can spend $50 on things

LESSON 2 Savings Savings and Bank Accounts Quick Write Suppose a relative gives you a generous gift of $1,000 for your sixteenth birthday. Your parent or guardian says that you can spend $50 on things

HOMELESS FAMILIES: KNOW YOUR RIGHTS! Do you need help applying for shelter? Call the. HOMELESS RIGHTS PROJECT of the LEGAL AID SOCIETY: 1-800-649-9125

HOMELESS FAMILIES: KNOW YOUR RIGHTS! Do you need help applying for shelter? Call the HOMELESS RIGHTS PROJECT of the LEGAL AID SOCIETY: 1-800-649-9125 If you are calling for the first time, please call

HOMELESS FAMILIES: KNOW YOUR RIGHTS! Do you need help applying for shelter? Call the HOMELESS RIGHTS PROJECT of the LEGAL AID SOCIETY: 1-800-649-9125 If you are calling for the first time, please call

WHAT BANKRUPTCY CAN T DO

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

GUIDE TO DEALING WITH DEBT

GUIDE TO DEALING WITH DEBT CONTENTS Page 4 Where do I start? Page 5 Do I have to pay? What can I afford to pay? Page 7 Who to pay first? Page 10 What can I afford to pay on my Credit Debts? Page 12 What

GUIDE TO DEALING WITH DEBT CONTENTS Page 4 Where do I start? Page 5 Do I have to pay? What can I afford to pay? Page 7 Who to pay first? Page 10 What can I afford to pay on my Credit Debts? Page 12 What

Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY

BUSINESS DEBTLINE Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY FACT SHEET NO. 10 NORTHERN IRELAND What is bankruptcy? Bankruptcy is a way of dealing with debts that you cannot pay.

BUSINESS DEBTLINE Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY FACT SHEET NO. 10 NORTHERN IRELAND What is bankruptcy? Bankruptcy is a way of dealing with debts that you cannot pay.

Banking made clear. Information pack for people with learning disabilities.

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear. Information pack for people with learning disabilities.

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

(02) 9211 5300 1800 226 028

9211 5300 1800 226 028") Centrelink will apply special rules if you have received, or are receiving, compensation for an injury. This self-help guide does not cover all those rules. This guide is for people who: received lump

Centrelink will apply special rules if you have received, or are receiving, compensation for an injury. This self-help guide does not cover all those rules. This guide is for people who: received lump

Dealing with debt - toolkit Information from Southampton City Council. Step 5. Tackle the most important debts first

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Money Advice Pack PB 1

Money Advice Pack 1 Introduction Many people suffer difficulties with money at some time in their lives. Money problems can be caused by a variety of reasons, such as losing your job, illness, decreased

Money Advice Pack 1 Introduction Many people suffer difficulties with money at some time in their lives. Money problems can be caused by a variety of reasons, such as losing your job, illness, decreased

The National Benevolent Charity. Application Form

The National Benevolent Charity Application Form The National Benevolent Charity was founded in 1812 by Peter Hervé to give pensions and allowances to the poor and distressed. Over 200 years later the

The National Benevolent Charity Application Form The National Benevolent Charity was founded in 1812 by Peter Hervé to give pensions and allowances to the poor and distressed. Over 200 years later the

Scottish Welfare Fund. A Guide To Additional Support

Scottish Welfare Fund A Guide To Additional Support Introduction This leaflet provides information about additional support for both Scottish Welfare Fund applicants and Angus residents in general. There

Scottish Welfare Fund A Guide To Additional Support Introduction This leaflet provides information about additional support for both Scottish Welfare Fund applicants and Angus residents in general. There

Planning for a baby. A budget guide for an expecting parent. Three steps to making a budget Tips to make life easier

Planning for a baby. A budget guide for an expecting parent. Three steps to making a budget Tips to make life easier 1 Having a baby has a big effect on your lifestyle. Most new parents have to cope with

Planning for a baby. A budget guide for an expecting parent. Three steps to making a budget Tips to make life easier 1 Having a baby has a big effect on your lifestyle. Most new parents have to cope with

BUDGET PLANNER. Instructions to Complete Budget Planner

BUDGET PLANNER NAME: DATE: Annual income twenty pounds, annual expenditure nineteen nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.

BUDGET PLANNER NAME: DATE: Annual income twenty pounds, annual expenditure nineteen nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.

SETTLEMENT CONSULTING. Special Needs Trust FAQs

SETTLEMENT CONSULTING Special Needs Trust FAQs What Is A Special Needs Trust? The primary purpose of creating a Special Needs Trust is to continue the monthly tax-free SSI disability benefits and secure

SETTLEMENT CONSULTING Special Needs Trust FAQs What Is A Special Needs Trust? The primary purpose of creating a Special Needs Trust is to continue the monthly tax-free SSI disability benefits and secure

Court Costs and Fees (A Guide to Fee Waivers)

") Court Costs and Fees (A Guide to Fee Waivers) Learn what to do if you cannot afford to pay court costs and fees for Family, civil, housing, and small claims cases. If you don't have the money to pay court

Court Costs and Fees (A Guide to Fee Waivers) Learn what to do if you cannot afford to pay court costs and fees for Family, civil, housing, and small claims cases. If you don't have the money to pay court

Disability Benefits For Wounded Warriors

Disability Benefits For Wounded Warriors 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

Disability Benefits For Wounded Warriors 2015 Contacting Social Security Visit our website At our website, www.socialsecurity.gov, you can: Create a my Social Security account to review your Social Security

PART 1. Self Help Debt Pack

PART 1 Self Help Debt Pack CONTENTS Introduction Page 3 How to contact GAIN Page 4 How to use the GAIN Self Help Pack Page 5 STEP 1 List Your Debts Page 7 STEP 2 Your Personal Budget Page 15 STEP 3 Your

PART 1 Self Help Debt Pack CONTENTS Introduction Page 3 How to contact GAIN Page 4 How to use the GAIN Self Help Pack Page 5 STEP 1 List Your Debts Page 7 STEP 2 Your Personal Budget Page 15 STEP 3 Your

212.3 Allowable Deductions for Households with Aged/Disabled Members

212.1 Purpose DEDUCTIONS Section 212 Page 1 This section describes the allowable Food Supplement Program (FSP) deductions. 212.2 General Information Only certain deductions are allowed when determining

212.1 Purpose DEDUCTIONS Section 212 Page 1 This section describes the allowable Food Supplement Program (FSP) deductions. 212.2 General Information Only certain deductions are allowed when determining

Bromsgrove District Council Discretionary Housing Payments

Name: Address Benefit Reference no: Post Code: Depending on certain conditions, we can make extra payments if you are not currently receiving full Housing Benefit or Council Tax Benefit and we feel you

Name: Address Benefit Reference no: Post Code: Depending on certain conditions, we can make extra payments if you are not currently receiving full Housing Benefit or Council Tax Benefit and we feel you

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet What is the Hardship Fund? The Hardship Fund is to help students facing financial hardship. It can provide nonrepayable awards

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet What is the Hardship Fund? The Hardship Fund is to help students facing financial hardship. It can provide nonrepayable awards

Please note: For any return that is prepared while you wait, payment is expected at the time of completion.

Your full name: Please answer the following questions as they relate to the year 2013. While this form is NOT required to be completed, you may be eligible for a 5% discount if this checklist is filled

Your full name: Please answer the following questions as they relate to the year 2013. While this form is NOT required to be completed, you may be eligible for a 5% discount if this checklist is filled

Rights for Landlords and Tenants. In Covington, Newport, Florence, Dayton, Taylor Mill, Ludlow, Bellevue, and Melbourne

Rights for Landlords and Tenants In Covington, Newport, Florence, Dayton, Taylor Mill, Ludlow, Bellevue, and Melbourne Sections Pages Important Words..1 You May Need Advice 2 Who is Covered by URLTA..3

Rights for Landlords and Tenants In Covington, Newport, Florence, Dayton, Taylor Mill, Ludlow, Bellevue, and Melbourne Sections Pages Important Words..1 You May Need Advice 2 Who is Covered by URLTA..3

Bankruptcy may make it possible for you to:

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

Conservatorship. A Booklet for Lanterman Regional Center Families

Conservatorship A Booklet for Lanterman Regional Center Families Table of Contents Introduction...1 How Conservatorship Works...2 Types of Conservatorships Recognized in California...2 Mental Health Conservatorship...2

Conservatorship A Booklet for Lanterman Regional Center Families Table of Contents Introduction...1 How Conservatorship Works...2 Types of Conservatorships Recognized in California...2 Mental Health Conservatorship...2

MAKING YOUR MONEY WORK. Diploma

MAKING YOUR MONEY WORK Diploma MAKING YOUR MONEY WORK YOU CAN MAKE YOUR MONEY WORK A Literacy Partners of Manitoba publication Money is important to everyone. Money has value and is used to get the things

MAKING YOUR MONEY WORK Diploma MAKING YOUR MONEY WORK YOU CAN MAKE YOUR MONEY WORK A Literacy Partners of Manitoba publication Money is important to everyone. Money has value and is used to get the things

lesson thirteen in trouble overheads

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

Don't ignore the problem. Debt won't go away and the longer you leave it the worse it gets.

DEBT ADVICE DEALING WITH YOUR DEBT Don't ignore the problem. Debt won't go away and the longer you leave it the worse it gets. Don't borrow money to pay off your debts. Think carefully, get advice first.

DEBT ADVICE DEALING WITH YOUR DEBT Don't ignore the problem. Debt won't go away and the longer you leave it the worse it gets. Don't borrow money to pay off your debts. Think carefully, get advice first.

How to calculate your taxable profits

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Helpsheet 222 Tax year 6 April 2013 to 5 April 2014 How to calculate your taxable profits A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200 3310 the

Basics of Budgeting. Ten Steps To Create A Budget. Reviewing:

Basics of Budgeting Reviewing: Ten Steps to creating a budget How to find where your money is going Tips to stay on course Budget format included Ten Steps To Create A Budget Basics of Budgeting A budget

Basics of Budgeting Reviewing: Ten Steps to creating a budget How to find where your money is going Tips to stay on course Budget format included Ten Steps To Create A Budget Basics of Budgeting A budget

State Treasury Achieving a Better Life Experience ( STABLE ) Accounts: Frequently Asked Questions

Accounts: Frequently Asked Questions") State Treasury Achieving a Better Life Experience ( STABLE ) Accounts: Frequently Asked Questions BASICS Q: What is a STABLE Account? A: A STABLE Account is an investment account available to eligible

State Treasury Achieving a Better Life Experience ( STABLE ) Accounts: Frequently Asked Questions BASICS Q: What is a STABLE Account? A: A STABLE Account is an investment account available to eligible

What s your Consumer IQ?

What s your Consumer IQ? How savvy a consumer are you? Take this quiz to see how much you know about consumer issues, laws and scams. 1. You receive a credit card offer in the mail. According to the big

What s your Consumer IQ? How savvy a consumer are you? Take this quiz to see how much you know about consumer issues, laws and scams. 1. You receive a credit card offer in the mail. According to the big

Supplemental Security Income (SSI)

") Helping Older Persons With Legal & Long-Term Care Problems Supplemental Security Income (SSI) 1. Who Is Eligible For SSI? You must apply and submit a signed application, be 65 or older, blind or disabled

Helping Older Persons With Legal & Long-Term Care Problems Supplemental Security Income (SSI) 1. Who Is Eligible For SSI? You must apply and submit a signed application, be 65 or older, blind or disabled

Your Right. to Buy. A guide for Scottish Secure Tenants

Your Right to Buy Your Home A guide for Scottish Secure Tenants Your Right to Buy Your Home About this booklet This booklet is for Scottish secure tenants. If you are not a Scottish secure tenant, you

Your Right to Buy Your Home A guide for Scottish Secure Tenants Your Right to Buy Your Home About this booklet This booklet is for Scottish secure tenants. If you are not a Scottish secure tenant, you

Personal Management Merit Badge Worksheet Requirements Were Completely Revised 01/01/98

Personal Management Merit Badge Worksheet Requirements Were Completely Revised 01/01/98 1. Do the following: a) Lead a discussion with your family to identify one family financial goal that must be saved

Personal Management Merit Badge Worksheet Requirements Were Completely Revised 01/01/98 1. Do the following: a) Lead a discussion with your family to identify one family financial goal that must be saved

Topic 2(d) Bank accounts

Bank accounts") Topic 2(d) Bank accounts Storing money in a bank or building society If you have money you don t want to spend immediately, the best thing you can do with it is put it in a bank account. This will keep

Topic 2(d) Bank accounts Storing money in a bank or building society If you have money you don t want to spend immediately, the best thing you can do with it is put it in a bank account. This will keep

BENEFIT, MONEY & DEBT. Advice Services in Dundee

BENEFIT, MONEY & DEBT Advice Services in Dundee i Contents Brooksbank Centre Citizens Advice Bureau Dundee North Law Centre Dundee Carers Centre Discovery Credit Union Dundee Energy Efficiency Advice Project

BENEFIT, MONEY & DEBT Advice Services in Dundee i Contents Brooksbank Centre Citizens Advice Bureau Dundee North Law Centre Dundee Carers Centre Discovery Credit Union Dundee Energy Efficiency Advice Project

ICAEW on Personal Finance

ICAEW on Personal Finance Living away from home for the first time Jack decided he didn t want to go to university after finishing his A-levels. Instead he applied for a Higher Apprenticeship within a

ICAEW on Personal Finance Living away from home for the first time Jack decided he didn t want to go to university after finishing his A-levels. Instead he applied for a Higher Apprenticeship within a

MONEY MANAGEMENT WORKBOOK

MICHIGAN ENERGY ASSISTANCE PROGRAM MONEY MANAGEMENT WORKBOOK Life is a challenge. As the saying goes, just when you're about to make ends meet, someone moves the ends. While it can be a struggle to pay

MICHIGAN ENERGY ASSISTANCE PROGRAM MONEY MANAGEMENT WORKBOOK Life is a challenge. As the saying goes, just when you're about to make ends meet, someone moves the ends. While it can be a struggle to pay

Answers to questions that many parents ask about how the CAH program works. Helpful advice from other parents who have children in the CAH programs

Preface Care at Home: A Handbook for Parents is a guide that is intended to help parents/guardians meet some of the challenges of caring for a physically disabled child at home. It includes information

Preface Care at Home: A Handbook for Parents is a guide that is intended to help parents/guardians meet some of the challenges of caring for a physically disabled child at home. It includes information

Discretionary housing payment and council tax reduction scheme application form

Discretionary housing payment and council tax reduction scheme application form To qualify for a discretionary housing payment to help with your rent you must be getting housing benefit, or housing costs

Discretionary housing payment and council tax reduction scheme application form To qualify for a discretionary housing payment to help with your rent you must be getting housing benefit, or housing costs

When Finances Go Wrong - Debt

When Finances Go Wrong - Debt Very few people now have no debt at all after all a mobile phone contract, or your rent/mortgage are both debts. It becomes an issue for people when they cannot meet the payments

When Finances Go Wrong - Debt Very few people now have no debt at all after all a mobile phone contract, or your rent/mortgage are both debts. It becomes an issue for people when they cannot meet the payments

Disability Insurance Basics

Ameriprise Financial Michael Gluski, CRPC Financial Advisor 12800 University Drive #105 Fort Myers, FL 33907 239-768-8830 [email protected] www.ameripriseadvisors.com/michael.gluski Disability Insurance

Ameriprise Financial Michael Gluski, CRPC Financial Advisor 12800 University Drive #105 Fort Myers, FL 33907 239-768-8830 [email protected] www.ameripriseadvisors.com/michael.gluski Disability Insurance

Your Right. to Buy Your Home. A guide for Scottish Secure Tenants

Your Right to Buy Your Home A guide for Scottish Secure Tenants Your Right to Buy Your Home About this booklet This booklet is for Scottish secure tenants. If you are not a Scottish secure tenant, you

Your Right to Buy Your Home A guide for Scottish Secure Tenants Your Right to Buy Your Home About this booklet This booklet is for Scottish secure tenants. If you are not a Scottish secure tenant, you

Employment and Income Assistance for Single Parents 2015-2016

Employment and Income Assistance for Single Parents 2015-2016 INTRODUCTION The Employment and Income Assistance Program (EIA) provides financial help to Manitobans who have no other way to support themselves

Employment and Income Assistance for Single Parents 2015-2016 INTRODUCTION The Employment and Income Assistance Program (EIA) provides financial help to Manitobans who have no other way to support themselves

A guide to our. Priority Services and ways we can help you manage your energy

A guide to our Priority Services and ways we can help you manage your energy Contents Helping to make life easier Helping you feel safe how to recognise our staff If you re visually-impaired Other services

A guide to our Priority Services and ways we can help you manage your energy Contents Helping to make life easier Helping you feel safe how to recognise our staff If you re visually-impaired Other services

Benefits if you are sick or disabled

Welfare Benefits Council Tax Benefit Housing Benefit Benefits if you are sick or disabled information from the Mind in Enfield Advice Team Social Fund Sickness and/or disability can happen to anyone at

Welfare Benefits Council Tax Benefit Housing Benefit Benefits if you are sick or disabled information from the Mind in Enfield Advice Team Social Fund Sickness and/or disability can happen to anyone at

Getting certain goods VAT free if you have a disability: helpsheet

Getting certain goods VAT free if you have a disability: helpsheet If you re disabled you ll generally have to pay VAT on the things you buy. However, VAT relief s available on a limited range of goods

Getting certain goods VAT free if you have a disability: helpsheet If you re disabled you ll generally have to pay VAT on the things you buy. However, VAT relief s available on a limited range of goods

Medicaid Nursing Home Information

Medicaid Nursing Home Information January 2015 This pamphlet tells you about Medicaid rules for: Utah Nursing Homes. Intermediate Care Facilities for people with Intellectual Disabilities (ICF/ID) This

Medicaid Nursing Home Information January 2015 This pamphlet tells you about Medicaid rules for: Utah Nursing Homes. Intermediate Care Facilities for people with Intellectual Disabilities (ICF/ID) This

Social Security Disability Benefits

Helping Older Persons With Legal & Long-Term Care Problems Social Security Disability Benefits 1. What Disability Programs Are Available From The Social Security Administration (SSA)? SSA offers two major

Helping Older Persons With Legal & Long-Term Care Problems Social Security Disability Benefits 1. What Disability Programs Are Available From The Social Security Administration (SSA)? SSA offers two major

SOME IDEAS THAT MAY HELP WITH. Credit Problems and How to Get Help

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit