Ch. 10 Perfect Competition, Monopoly, and Monopolistic Competition

|

|

|

- Benjamin Park

- 7 years ago

- Views:

Transcription

1 Ch. 10 Perfect Competition, Monopoly, and Monopolistic Competition 1

2 2

3 3

4 Four broad categories of market types Perfect competition Monopoly Monopolistic competition Oligopoly 4

5 Table 10.1 Characteristics of Market Types Market structure Examples Number of producers Type of product Power of firm over price Barriers to entry Non-price competition Perfect competition Parts of agriculture are reasonably close Many Standardized None Low None Monopolistic competition Retail trade Many Differentiated Some Low Advertising and product differentiation Oligopoly Computers, oil, steel Few Standardized or differentiated Some High Advertising and product differentiation Monopoly Public utilities One Unique product Considerable Very high Advertising 5

6 1. Perfect competition Many sellers, so many that firms are price takers Homogeneous product Easy entry and exit Perfect information about prices 6

7 Profit maximization in a perfectly competitive market (see book) P = MC Marginal cost curve left of shutdown level (min. variable cost) is supply curve P = MR = MC = AC Firm produces at minimum of average costs! (optimal outcome for industry) In a constant-cost industry increase in demand will lead in the long term to constant prices (i.e. horizontal supply curve) 7

In a constant-cost industry increase in demand will lead in")

8 Frictions in cyberspace Nov 18th 1999 From The Economist print edition Retailing on the Internet, it is said, is almost perfectly competitive. Really? THE explosive growth of the Internet promises a new age of perfectly competitive markets. With perfect information about prices and products at their fingertips, consumers can quickly and easily find the best deals. In this brave new world, retailers profit margins will be competed away, as they are all forced to price at cost. Or so we are led to believe. And yes, studies do show that online retailers tend to be cheaper than conventional rivals, and that they adjust prices more finely and more often. But they also find that price dispersion (the spread between the highest and lowest prices) is often as wide on the Internet as it is in the shopping mall or even wider. Moreover, the retailers with the keenest prices rarely have the biggest sales. Such price dispersion is usually a sign of market inefficiency. In an ideal competitive market, where products are identical, customers are perfectly informed, there is free market entry, a large number of buyers and sellers and no search costs, all sales are made by the retailer with the lowest price. So all prices are driven down to marginal cost. Search costs on the Internet might be expected to be lower and online consumers to be more easily informed about prices. So price dispersion online ought to be narrower than in conventional markets. But it does not seem to be. A recent paper*, by Michael Smith and Erik Brynjolfsson of the Massachusetts Institute of Technology s Sloan School of Management and Joseph Bailey of the University of Maryland, looks at the main research on this topic. One study it cites, by Mr. Bailey, finds that price dispersion for books, CDs and software is no smaller online than it is in conventional markets. Another, by Messrs Brynjolfsson and Smith, finds that prices for identical books and CDs at different online retailers differ by as much as 50%, and on average by 33% for books and 25% for CDs. A third, by Eric Clemons, Il-Horn Hann and Lorin Hitt of the University of Pennsylvania s Wharton School, finds that prices for airline tickets from online travel agents differ by an average of 28%.

9 Monopoly One producer Considerable power over price Unique product Very high barriers to entry 9

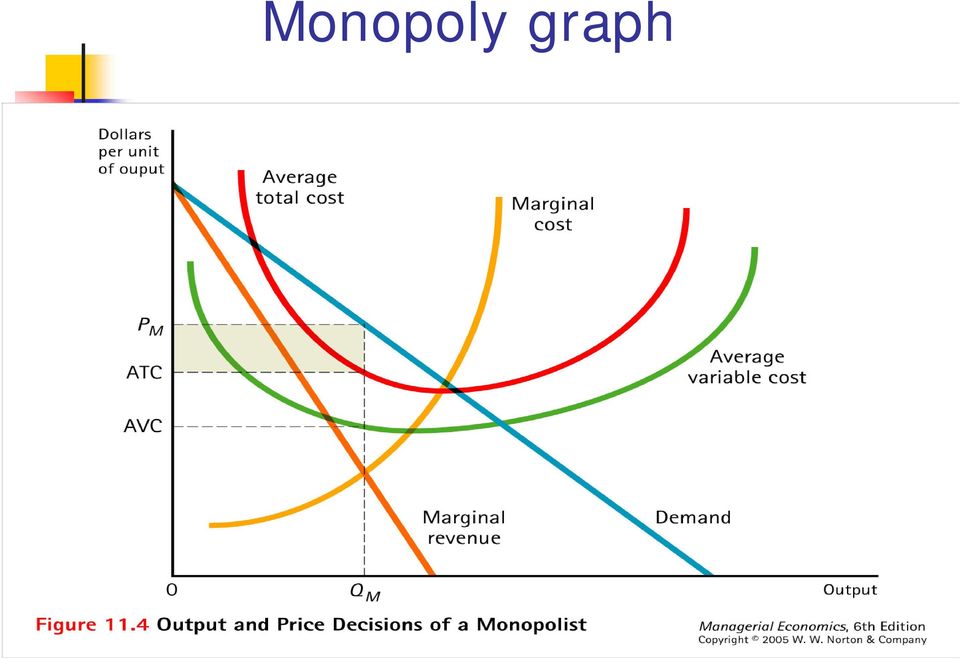

10 Price and Output Decisions for a Monopolist OUTPUT PRICE TR TC MC MR PROFIT

11 Monopoly graph 11

12 Monopolists produce less, price higher than firms in competitive equilibrium MR = P(1 + 1/η) Situation is inefficient, insofar as the sum of consumer and producer surplus is concerned What is producer and consumer surplus? Monopolist has to take demand conditions explicitly into account Why is no other firm entering the market??? 12

13 Other aspects of monopoly Natural monopoly if minimum of average cost occurs only at very high output level (minimum efficient scale) ==> there is only place for one firm in the market! Measure of monopoly power (markup of price over cost): markup = P MC MC 13

: markup =")

14 Sources of monopoly power Natural monopoly (public utilities best example, railway tracks), economies of scale, Capital requirements on production or big sunk costs on entry Patents (17 years), trade secrets (Coke) Exclusive or unique assets (minerals, talent) Locational advantage (popcorn shop in cinema but in general you pay rent for these advantages) Regulation (TV, taxi, telephone in the past) Collusion by competitors 14

Regulation (TV, taxi, telephone in the past) Collusion by")

15 What can a monopolist do? Erect strategic entry barriers Excessive patenting and copyright Limit pricing (set price below monopoly price) Extensive advertising to create brand name to raise cost of entry Create intentionally excess capacity as a warning for a price war 15

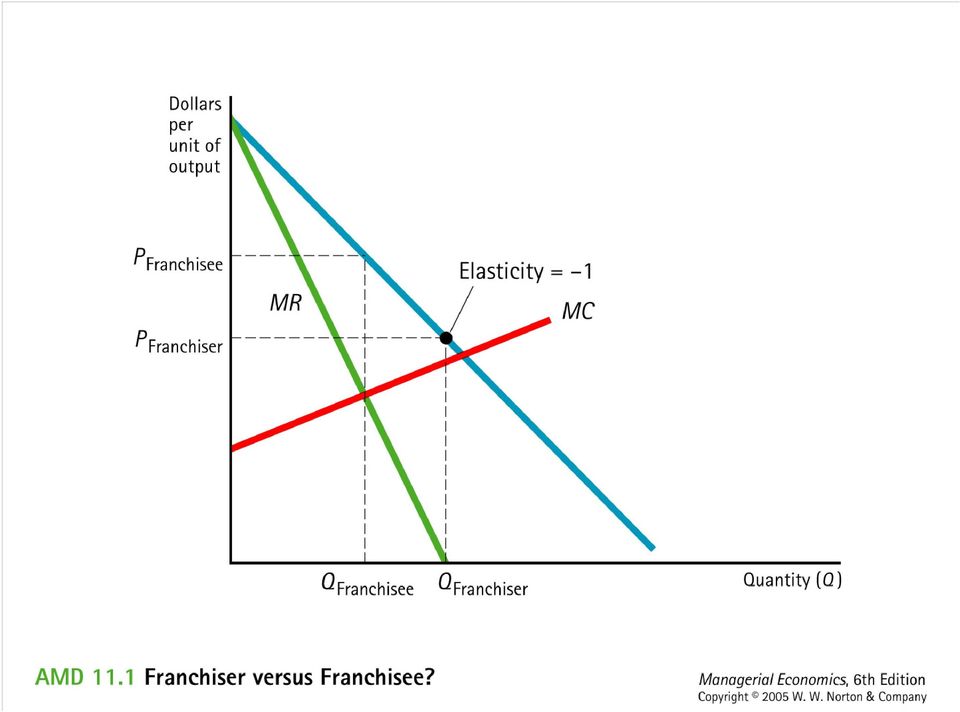

16 Franchising McFood A Franchiser (mother company) gets a fixed percentage of sales, The franchisee is the residual claimant What are the incentives for the two partners? Other problems like number of shops in a region Other examples?? 16

17 17

18 Cost-plus pricing When you ask managers, how they set prices, they always say related to costs, but not demand Two steps: The firm estimates the cost per unit of output of the product usually average cost The firm adds a markup to the estimated average cost Markup = (Price - Cost) / Cost 18

19 Does mark-up pricing maximize profit? TR = QP(Q) TR P 1 MR = = P + Q = P(1 + ) Q Q η M C = M R =... P = M C η ==> markup can be calculated: A markup system will maximize profit if: Price elasticity of demand is known Marginal costs are known (in general only average costs are used) 19

20 Table 13.1: Relationship between Markup and Price Elasticity Price Elasticity of Demand Optimal % Markup of Marginal Cost

21 The Multi-product firm Demand inter-relationships TR = TR X + TR Y MR X = dtr/dq X = dtr X /dq X + dtr Y /dq X MR Y = dtr/dq Y = dtr X /dq Y + dtr Y /dq Y Products can be complements or substitutes for consumers. 21

22 Demand interrelationship What effect does it have on prices? Example: Why do you get peanuts for free in Pubs, but you have to pay for Tub Water? What about water in wine bars or coffee shops? 22

23 Production inter-relationships Products are produced jointly for technical reasons Example: by-products (Abfallprodukte) in plastic production, oil industry... Costs of separate production cannot be separated properly. 2 possibilities: A) products always produced in same proportions B) substitution in production possible 23

24 Optimal pricing for joint products: fixed proportions I 24

25 Optimal pricing for joint products: fixed proportions II 25

26 Joint products: variable proportions Output A can be substituted for output B Iso-revenue curve: combination of output levels A and B with same revenue Iso-cost curve: combination of output levels A and B with same costs Tangency condition 26

27 Optimal pricining for joint products: variable proportions 27

28 3. Monopolistic Competition Many firms Differentiated products (is in general a strategic marketing goal) products are close substitutes to each other; we talk about a product group if similar products Demand curve not completely flat Firms do not react to each other s actions (because there are so many) Easy entry and exit Examples: shirts, candy bars, restaurants, Not tomatoes at Südbahnhof market, or petrol or cars 28

29 Behavior of monopolistically competitive firms Firms in an industry group are similar (symmetric in extreme), i.e. they have the same incentives What happens if firm changes price alone? (dd) Same incentive for other firms to change price (DD) ----> demand is steeper in this case In the extreme: a very small firm changing the price alone has a very flat demand curve! Marketing is important: firms want to make their product unique, in other words: Demand for their product should get more inelastic (steep) Use advertising! 29

30 Demand curve if the firm (dd) or the industry (DD) changes price 30

31 Short-run equilibrium 31

32 Short-run equilibrium Like a monopolist: set price where marginal revenue = marginal cost Profits arise ---> market entry of similar products (firms) Each firm competes for a percentage of total demand, new entry means demand for the individual firm must be lower (shifts left/down) Shift must be so far, that profits disappear I.e. Demand curve must finally be tangential to longrun average cost curve 32

33 Long-run equilibrium Due to market entry demand shifted to the left for the firm Zero profit condition met (Revenue=Costs) Profit-maximization condition met (MC=MR) Problem: production is not cost-efficient Long-run average costs not at minimum cost of product variety 33

34 Perfect Competition (PC) versus Monopolistic Competition (MonC) PC: price equal to long-run marginal cost, in MonC price is always higher as marginal cost: there are people out there who value the good more than the marginal cost to produce it. ==> in principle production should rise PC produces at minimum of long-run average cost, MonC not at the minimum Trade-Off between efficiency (cost) and variety Long-run profit situation is alike, because of entry, but how short is the short-run?? 34

35 Monopolistic Competition: summing up Very common market form No interaction between firms Firm could reduce average cost by producing more Firms try to bind their costumers to the firm: Marketing, advertising plays a role (not in perfect competition) Make the product different from the crowd 35

36 Optimal advertising rule For small variations in output (and/or) if the firm is only small part of the market, we can assume that Price does not change following small changes in advertising To determine optimal advertising, cost of advertising and cost of production must be considered Simple rule: Marginal revenue from an extra dollar of advertising = η (elasticity of demand) 36

37 Optimal advertising expenditure: advertising meant to increase brand consciousness of clients With little advertising, elasticity will be high, because product will be considered as easily substitutable to others, Increase advertising and elasticity will fall 37

38 Advertising Advertising can have two effects: High-price strategy: increase brand concsiousness, don t talk about price: Price elasticity of demand should decrease (demand curve should get steeper) Low-price strategy promotions, i.e. increase sales: Advertise price cuts which should increase price consciousness of customers, i.e price elasticity should increase 38

39 Price elasticity and advertising Price elasticity of demand Brand Chock Full o nuts Maxwell House Folgers Hill Brothers Advertised price change Unadvertised price change 6.5 * *Not significantly different from zero. Source: Katz and Shapiro, Consumer Shopping Behavior in the Retail Coffee Market. 39

40 Problem - Pawnshops During recessions, many people particularly those who have difficulty getting bank loans turn to pawnshops to raise cash. But even during boom years, pawnshops can be very profitable. Because the collateral that customers put up (such as jewelry or guns) is generally worth at least double what is lent, it generally can be sold at a profit. And because the usury laws allow higher interest ceilings for pawnshops than for other lending institutions, pawnshops often charge spectacularly high rates of interest. For example, Florida s pawnshops charge interest rates of 20 % or more per month. According to Steven Kent, an analyst at Goldman, Sachs, pawnshops make 20 % gross profit on defaulted loans and 205 % interest on loans repaid. a) In late 1991, there were about 8,000 pawnshops in the United States, according to American Business Information. This was much higher than in 1986, when the number was about 5,000. Indeed, in late 1991, the number jumped by about 1,000. Why did the number increase? b) In a particular small city, do the pawnshops constitute a perfectly competitive industry? If not, what is the market structure of the industry? c) Are there considerable barriers to enter in the pawnshop industry? (Note: A pawnshop can be opened for less than $125,000, but a number of states have tightened licensing requirements for pawnshops.) 40

41 Solution - Pawnshops a) The pawnshop business appears to be highly profitable on the basis of the question. We should expect that entry into this industry would follow such high profits unless there were barriers to entry. If the current entry in the industry where not enough to eliminate all the supernormal profits being earned, we should expect continued entry until profits were eliminated. b) The market for pawnshop services is likely to be quite local, as local perhaps as neighborhoods. In this case, even though there might be 100 pawnshops in a large city, the market for any individual shop is likely to be oligopolistic or monopolistic. c) Barriers to entry appear low in this industry. Pawnshops do not appear to be any more difficult to start than restaurants or hardware stores. 41

Managerial Economics

Managerial Economics Unit 3: Perfect Competition, Monopoly and Monopolistic Competition Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012 Winter-Ebmer, Managerial Economics: Unit 3 1

Managerial Economics Unit 3: Perfect Competition, Monopoly and Monopolistic Competition Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012 Winter-Ebmer, Managerial Economics: Unit 3 1

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Monopolistic Competition

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Understanding Economics 2nd edition by Mark Lovewell and Khoa Nguyen Chapter 5 Perfect Competition Chapter Objectives! In this chapter you will: " Consider the four market structures, and the main differences

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

Econ 101: Principles of Microeconomics Chapter 16 - Monopolistic Competition and Product Differentiation Fall 2010 Herriges (ISU) Ch. 16 Monopolistic Competition Fall 2010 1 / 18 Outline 1 What is Monopolistic

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition

, 2 nd Edition") CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

CHAPTER 12 MARKETS WITH MARKET POWER Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) One of the requirements for a monopoly is that A) products are high priced. B) there are several close substitutes for the product. C) there is a

Learning Objectives. Chapter 6. Market Structures. Market Structures (cont.) The Two Extremes: Perfect Competition and Pure Monopoly

The Two Extremes: Perfect Competition and Pure Monopoly") Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Pre-Test Chapter 23 ed17

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

b. Cost of Any Action is measure in foregone opportunities c.,marginal costs and benefits in decision making

1 Economics 130-Windward Community College Review Sheet for the Final Exam This final exam is comprehensive in nature and in scope. The test will be divided into two parts: a multiple-choice section and

1 Economics 130-Windward Community College Review Sheet for the Final Exam This final exam is comprehensive in nature and in scope. The test will be divided into two parts: a multiple-choice section and

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!!

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Monopolistic Competition

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Economics Chapter 7 Review

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

Name: Class: Date: ID: A Economics Chapter 7 Review Matching a. perfect competition e. imperfect competition b. efficiency f. price and output c. start-up costs g. technological barrier d. commodity h.

1. Supply and demand are the most important concepts in economics.

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

Page 1 1. Supply and demand are the most important concepts in economics. 2. Markets and Competition a. Market is a group of buyers and sellers of a particular good or service. P. 66. b. These individuals

CHAPTER 6 MARKET STRUCTURE

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

CHAPTER 6 MARKET STRUCTURE CHAPTER SUMMARY This chapter presents an economic analysis of market structure. It starts with perfect competition as a benchmark. Potential barriers to entry, that might limit

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Learning Objectives. After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to:

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Chapter 8. Competitive Firms and Markets

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

MONOPOLIES HOW ARE MONOPOLIES ACHIEVED?

Monopoly 18 The public, policy-makers, and economists are concerned with the power that monopoly industries have. In this chapter I discuss how monopolies behave and the case against monopolies. The case

Monopoly 18 The public, policy-makers, and economists are concerned with the power that monopoly industries have. In this chapter I discuss how monopolies behave and the case against monopolies. The case

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11: Price-Searcher Markets with High Entry Barriers

Chapter 11: Price-Searcher Markets with High Entry Barriers I. Why are entry barriers sometimes high? A. Economies of Scale in some markets average total costs fall over the full range of output. Therefore

Chapter 11: Price-Searcher Markets with High Entry Barriers I. Why are entry barriers sometimes high? A. Economies of Scale in some markets average total costs fall over the full range of output. Therefore

Chapter 7: Market Structures Section 1

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Chapter 7: Market Structures Section 1 Key Terms perfect competition: a market structure in which a large number of firms all produce the same product and no single seller controls supply or prices commodity:

Pricing and Output Decisions: i Perfect. Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Oligopoly and Strategic Pricing

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

R.E.Marks 1998 Oligopoly 1 R.E.Marks 1998 Oligopoly Oligopoly and Strategic Pricing In this section we consider how firms compete when there are few sellers an oligopolistic market (from the Greek). Small

Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry s output.

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.)

") CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

CHAPTER 18 MARKETS WITH MARKET POWER Principles of Economics in Context (Goodwin et al.) Chapter Summary Now that you understand the model of a perfectly competitive market, this chapter complicates the

Figure: Computing Monopoly Profit

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

Monopoly WHY MONOPOLIES ARISE

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

In this chapter, look for the answers to these questions: Why do monopolies arise? Why is MR < P for a monopolist? How do monopolies choose their P and Q? How do monopolies affect society s well-being?

Monopoly. Monopoly Defined

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

12 Monopolistic Competition and Oligopoly

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

CHAPTER 9: PURE COMPETITION

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

CHAPTER 9: PURE COMPETITION Introduction In Chapters 9-11, we reach the heart of microeconomics, the concepts which comprise more than a quarter of the AP microeconomics exam. With a fuller understanding

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits.

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

Equilibrium of a firm under perfect competition in the short-run. A firm is under equilibrium at that point where it maximizes its profits. Profit depends upon two factors Revenue Structure Cost Structure

At the end of Chapter 18, you should be able to answer the following:

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

c. Given your answer in part (b), what do you anticipate will happen in this market in the long-run?

, what do you anticipate will happen in this market in the long-run?") Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Chapter 7: Market Structures Section 3

Chapter 7: Market Structures Section 3 Objectives 1. Describe characteristics and give examples of monopolistic competition. 2. Explain how firms compete without lowering prices. 3. Understand how firms

Chapter 7: Market Structures Section 3 Objectives 1. Describe characteristics and give examples of monopolistic competition. 2. Explain how firms compete without lowering prices. 3. Understand how firms

4. Market Structures. Learning Objectives 4-63. Market Structures

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition.

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

Microeconomics Topic 7: Contrast market outcomes under monopoly and competition. Reference: N. Gregory Mankiw s rinciples of Microeconomics, 2 nd edition, Chapter 14 (p. 291-314) and Chapter 15 (p. 315-347).

Chapter 16 Monopolistic Competition and Oligopoly

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

Econ 101: Principles of Microeconomics

Econ 101: Principles of Microeconomics Chapter 14 - Monopoly Fall 2010 Herriges (ISU) Ch. 14 Monopoly Fall 2010 1 / 35 Outline 1 Monopolies What Monopolies Do 2 Profit Maximization for the Monopolist 3

Econ 101: Principles of Microeconomics Chapter 14 - Monopoly Fall 2010 Herriges (ISU) Ch. 14 Monopoly Fall 2010 1 / 35 Outline 1 Monopolies What Monopolies Do 2 Profit Maximization for the Monopolist 3

UNIVERSITY OF CALICUT MICRO ECONOMICS - II

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION BA ECONOMICS III SEMESTER CORE COURSE (2011 Admission onwards) MICRO ECONOMICS - II QUESTION BANK 1. Which of the following industry is most closely approximates

CHAPTER 11: MONOPOLISTIC COMPETITION AND OLIGOPOLY

CHAPTER 11: MONOPOLISTIC COMPETITION AND OLIGOPOLY Introduction While perfect competition and monopoly represent the extremes of market structures, most American firms are found in the two market structures

CHAPTER 11: MONOPOLISTIC COMPETITION AND OLIGOPOLY Introduction While perfect competition and monopoly represent the extremes of market structures, most American firms are found in the two market structures

AP Microeconomics Review

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

AP Microeconomics Review 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

OLIGOPOLY. Nature of Oligopoly. What Causes Oligopoly?

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

CH 11: OLIGOPOLY 1 OLIGOPOLY When a few big firms dominate the market, the situation is called oligopoly. Any action of one firm will affect the performance of other firms. If one of the firms reduces

This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly.

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

Market Structures This hand-out gives an overview of the main market structures including perfect competition, monopoly, monopolistic competition, and oligopoly. Summary Chart Perfect Competition Monopoly

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The four-firm concentration ratio equals the percentage of the value of accounted for by the four

chapter Perfect Competition and the >> Supply Curve Section 3: The Industry Supply Curve

chapter 9 The industry supply curve shows the relationship between the price of a good and the total output of the industry as a whole. Perfect Competition and the >> Supply Curve Section 3: The Industry

chapter 9 The industry supply curve shows the relationship between the price of a good and the total output of the industry as a whole. Perfect Competition and the >> Supply Curve Section 3: The Industry

SUPPLY AND DEMAND : HOW MARKETS WORK

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

Chapter 9: Perfect Competition

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Pure Competition urely competitive markets are used as the benchmark to evaluate market

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

Profit Maximization. 2. product homogeneity

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

All these models were characterized by constant returns to scale technologies and perfectly competitive markets.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

Economies of scale and international trade In the models discussed so far, differences in prices across countries (the source of gains from trade) were attributed to differences in resources/technology.

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs:

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

EXAM TWO REVIEW: A. Explicit Cost vs. Implicit Cost and Accounting Costs vs. Economic Costs: Economic Cost: the monetary value of all inputs used in a particular activity or enterprise over a given period.

Microeconomics. Lecture Outline. Claudia Vogel. Winter Term 2009/2010. Part III Market Structure and Competitive Strategy

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 25 Lecture Outline Part III Market Structure and Competitive Strategy 12 Monopolistic

Econ 201 Final Exam. Douglas, Fall 2007 Version A Special Codes 00000. PLEDGE: I have neither given nor received unauthorized help on this exam.

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

, Fall 2007 Version A Special Codes 00000 PLEDGE: I have neither given nor received unauthorized help on this exam. SIGNED: PRINT NAME: Econ 201 Final Exam 1. For a profit-maximizing monopolist, a. MR

Monopoly: static and dynamic efficiency M.Motta, Competition Policy: Theory and Practice, Cambridge University Press, 2004; ch. 2

Monopoly: static and dynamic efficiency M.Motta, Competition Policy: Theory and Practice, Cambridge University Press, 2004; ch. 2 Economics of Competition and Regulation 2015 Maria Rosa Battaggion Perfect

Monopoly: static and dynamic efficiency M.Motta, Competition Policy: Theory and Practice, Cambridge University Press, 2004; ch. 2 Economics of Competition and Regulation 2015 Maria Rosa Battaggion Perfect

Economics Chapter 7 Market Structures. Perfect competition is a in which a large number of all produce.

Economics Chapter 7 Market Structures Perfect competition is a in which a large number of all produce. There are Four Conditions for Perfect Competition: 1. 2. 3. 4. Barriers to Entry Factors that make

Economics Chapter 7 Market Structures Perfect competition is a in which a large number of all produce. There are Four Conditions for Perfect Competition: 1. 2. 3. 4. Barriers to Entry Factors that make

Variable Cost. Marginal Cost. Average Variable Cost 0 $50 $50 $0 -- -- -- -- 1 $150 A B C D E F 2 G H I $120 J K L 3 M N O P Q $120 R

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Class: Date: ID: A Principles Fall 2013 Midterm 3 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Trevor s Tire Company produced and sold 500 tires. The

Oligopoly. Unit 4: Imperfect Competition. Unit 4: Imperfect Competition 4-4. Oligopolies FOUR MARKET MODELS

1 Unit 4: Imperfect Competition FOUR MARKET MODELS Perfect Competition Monopolistic Competition Pure Characteristics of Oligopolies: A Few Large Producers (Less than 10) Identical or Differentiated Products

1 Unit 4: Imperfect Competition FOUR MARKET MODELS Perfect Competition Monopolistic Competition Pure Characteristics of Oligopolies: A Few Large Producers (Less than 10) Identical or Differentiated Products

Chapter 14 Monopoly. 14.1 Monopoly and How It Arises

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) A major characteristic of monopoly is A) a single seller of a product. B) multiple sellers of a product. C) two sellers of a product. D) a few sellers

Chapter 14 Monopoly 14.1 Monopoly and How It Arises 1) A major characteristic of monopoly is A) a single seller of a product. B) multiple sellers of a product. C) two sellers of a product. D) a few sellers

Chapter 13 Oligopoly 1

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

Economics 100 Exam 2

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Principle of Microeconomics Econ 202-506 chapter 13

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Principle of Microeconomics Econ 202-506 chapter 13 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The WaveHouse on Mission Beach in San Diego

Market Structure: Duopoly and Oligopoly

WSG10 7/7/03 4:24 PM Page 145 10 Market Structure: Duopoly and Oligopoly OVERVIEW An oligopoly is an industry comprising a few firms. A duopoly, which is a special case of oligopoly, is an industry consisting

WSG10 7/7/03 4:24 PM Page 145 10 Market Structure: Duopoly and Oligopoly OVERVIEW An oligopoly is an industry comprising a few firms. A duopoly, which is a special case of oligopoly, is an industry consisting

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Write down the names of three companies: competition. major competitors.

Write down the names of three companies: 1. Company with very little competition. 2. Company with two to three major competitors. 3. Company with many competitors. Which situation do you think describes

Write down the names of three companies: 1. Company with very little competition. 2. Company with two to three major competitors. 3. Company with many competitors. Which situation do you think describes

Final Exam 15 December 2006

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

Eco 301 Name Final Exam 15 December 2006 120 points. Please write all answers in ink. You may use pencil and a straight edge to draw graphs. Allocate your time efficiently. Part 1 (10 points each) 1. As

An increase in the number of students attending college. shifts to the left. An increase in the wage rate of refinery workers.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

The notion of perfect competition for consumers and producers, and the role of price flexibility in such a context. Ezees Silwady

The notion of perfect competition for consumers and producers, and the role of price flexibility in such a context Ezees Silwady I. Introduction The aim of this paper is to clarify the notion of perfect

The notion of perfect competition for consumers and producers, and the role of price flexibility in such a context Ezees Silwady I. Introduction The aim of this paper is to clarify the notion of perfect

Chapter 7: Market Structure in Government and Nonprofit Industries. Soft Drinks. What is a Market? Do NFPs Compete? Some NFPs Compete Directly

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

Chapter 7: Market Structure in Government and Nonprofit Industries Soft Drinks HTTP:/www.economics.emory.edu/Working_Pa pers/wp/2008wp/frisvold_08_08_paper.pdf What is a Market? A market is a process in

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

D) Marginal revenue is the rate at which total revenue changes with respect to changes in output.

Marginal revenue is the rate at which total revenue changes with respect to changes in output.") Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

Econ 101, section 3, F06 Schroeter Exam #4, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #4, Red Choose the single best answer for each question. 1. Profit is defined as a. net revenue minus depreciation. *. total revenue minus total cost. c. average

Econ 101, section 3, F06 Schroeter Exam #4, Red Choose the single best answer for each question. 1. Profit is defined as a. net revenue minus depreciation. *. total revenue minus total cost. c. average

A2 Micro Business Economics Diagrams

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

A2 Micro Business Economics Diagrams Advice on drawing diagrams in the exam The right size for a diagram is ½ of a side of A4 don t make them too small if needed, move onto a new side of paper rather than

Cooleconomics.com Monopolistic Competition and Oligopoly. Contents:

Cooleconomics.com Monopolistic Competition and Oligopoly Contents: Monopolistic Competition Attributes Short Run performance Long run performance Excess capacity Importance of Advertising Socialist Critique

Cooleconomics.com Monopolistic Competition and Oligopoly Contents: Monopolistic Competition Attributes Short Run performance Long run performance Excess capacity Importance of Advertising Socialist Critique

CEVAPLAR. Solution: a. Given the competitive nature of the industry, Conigan should equate P to MC.

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

Chapter 15: Monopoly WHY MONOPOLIES ARISE HOW MONOPOLIES MAKE PRODUCTION AND PRICING DECISIONS

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Chapter 15: While a competitive firm is a taker, a monopoly firm is a maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Comparisons of Industry Market Structures. Imperfect Competition Market Structure Models (11/10/09)

") Imperfect Market Structure Models (11/10/09) Today: and Monopsony/Oligopsony Thursday: Market Structure, Conduct and erformance Model Exam III 24 th Characteristics Comparisons of Industry Market Structures

Imperfect Market Structure Models (11/10/09) Today: and Monopsony/Oligopsony Thursday: Market Structure, Conduct and erformance Model Exam III 24 th Characteristics Comparisons of Industry Market Structures

Models of Imperfect Competition

Models of Imperfect Competition Monopolistic Competition Oligopoly Models of Imperfect Competition So far, we have discussed two forms of market competition that are difficult to observe in practice Perfect

Models of Imperfect Competition Monopolistic Competition Oligopoly Models of Imperfect Competition So far, we have discussed two forms of market competition that are difficult to observe in practice Perfect

Final Exam (Version 1) Answers

Answers") Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Characteristics of Market Structure PERFECT COMPETITION MONOPOLISITC COMPETITION

Characteristics of Market Structure Place on each wall of the classroom a large sign with one of the following market structures: PERFECT COMPETITION MONOPOLISITC COMPETITION MONOPOLY OLIGOPOLY There are

Characteristics of Market Structure Place on each wall of the classroom a large sign with one of the following market structures: PERFECT COMPETITION MONOPOLISITC COMPETITION MONOPOLY OLIGOPOLY There are

Chapter 9 Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

ECON 600 Lecture 5: Market Structure - Monopoly. Monopoly: a firm that is the only seller of a good or service with no close substitutes.

I. The Definition of Monopoly ECON 600 Lecture 5: Market Structure - Monopoly Monopoly: a firm that is the only seller of a good or service with no close substitutes. This definition is abstract, just

I. The Definition of Monopoly ECON 600 Lecture 5: Market Structure - Monopoly Monopoly: a firm that is the only seller of a good or service with no close substitutes. This definition is abstract, just

Introduction to microeconomics

RELEVANT TO ACCA QUALIFICATION PAPER F1 / FOUNDATIONS IN ACCOUNTANCY PAPER FAB Introduction to microeconomics The new Paper F1/FAB, Accountant in Business carried over many subjects from its Paper F1 predecessor,

RELEVANT TO ACCA QUALIFICATION PAPER F1 / FOUNDATIONS IN ACCOUNTANCY PAPER FAB Introduction to microeconomics The new Paper F1/FAB, Accountant in Business carried over many subjects from its Paper F1 predecessor,