FIN Investments: Portfolio Performance Evaluation

|

|

|

- Bryce Bradley

- 7 years ago

- Views:

Transcription

1 FIN Investments: Portfolio Performance Evaluation Types of Abnormal Performance: (1) Stock Selectivity (2) Market Timing Portfolio Performance Evaluation Estimate market model in risk premium form: [R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + ε(pt) where R(pt) is the mutual fund return, including dividends, subtracting fees & expenses, R(mt) is the CRSP value-weighted portfolio return (or the S&P 500 index with dividends), and R(ft) is the default-free interest rate over the time interval t (e.g., 1 month Tbill yield) Prof. Schwert 1-2 Spring 1997

, and R(ft) is the default-free interest rate over the time interval t (e.g., 1 month Tbill yield) Prof.")

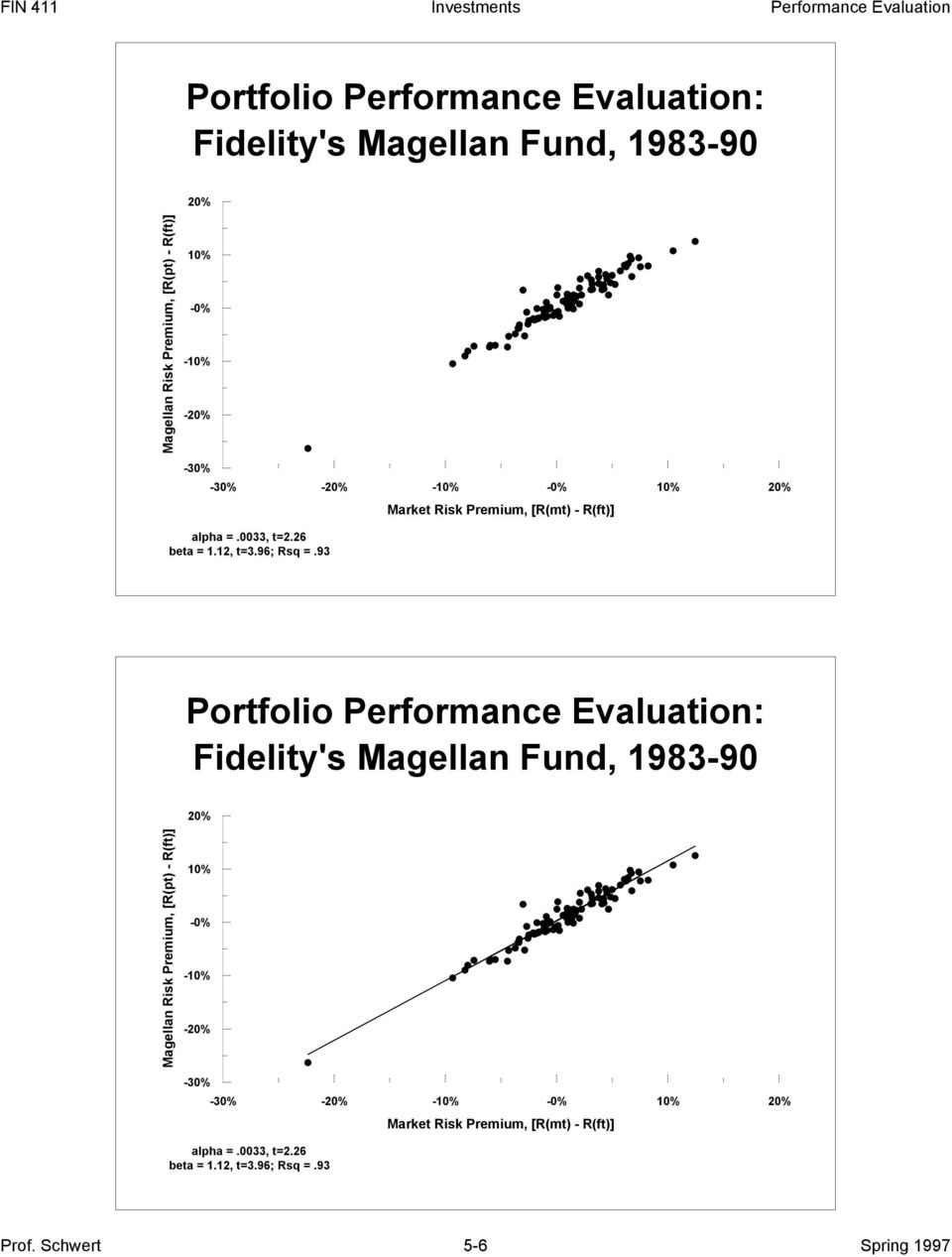

2 Risk Premium Market Model [R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + ε(pt) If the Sharpe-Lintner CAPM is true, then E[R(pt) -R(ft)] = β(p) E[R(mt) - R(ft)], so α(p) should equal 0. If the estimate of α(p) is significantly greater (less) than 0, then the mutual fund has out- (under-) performed the risk-adjusted benchmark This is sometimes called Jensen's alpha Fidelity's Magellan Fund Fidelity's Magellan Fund has been advertised for many years as having had outstanding performance by testing this fund we are probably biased in favor of finding abnormal performance else why would Fidelity spend so much on advertising? using monthly data from , and ignoring the 3% up-front load fee (i.e., you get $.97 of investments when you send them $1), β(p) is 1.12 (t = 3.96 for β=1), α(p) is.0033 (t = 2.26), and Rsquared is.93 Prof. Schwert 3-4 Spring 1997

, β(p) is 1.")

3 20% -0% -20% -30% -30% -20% -0% 20% alpha =.0033, t=2.26 beta = 1.12, t=3.96; Rsq =.93 20% -0% -20% -30% -30% -20% -0% 20% alpha =.0033, t=2.26 beta = 1.12, t=3.96; Rsq =.93 Prof. Schwert 5-6 Spring 1997

4 Testing for Market Timing Ability If you thought you had market timing ability (i.e., you could tell when stock returns would be higher than Tbill returns), you should be more heavily invested in stocks in those periods This would imply that the beta of your portfolio would be higher when market risk premiums were positive (and lower when they were negative): [R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + + β up (p) D(t) [R(mt) - R(ft)] + ε(pt) where D(t) = 1 if [R(mt) - R(ft)] > 0, and 0 otherwise Fidelity's Magellan Fund: Market Timing? [R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + + β up(p) D(t) [R(mt) - R(ft)] + ε(pt) where D(t) = 1 if [R(mt) - R(ft)] > 0 For , α(p) =.0060, t=4.18 β(p) = 1.19, t=3.79 for β =1 β up(p) = -.16, t=-1.75 for β up = 0 so it looks like Magellan has negative market timing ability, but stronger positive selectivity ability using this method Prof. Schwert 7-8 Spring 1997

![[R(mt) - R(ft)] + + β up (p) D(t) [R(mt) - R(ft)] + ε(pt) where D(t) = 1 if [R(mt) - R(ft)] > 0, and 0 otherwise Fidelity's Magellan Fund: Market Timing?](/docs-images/47/23772132/images/page_4.jpg "[R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + + β up(p) D(t) [R(mt) - R(ft)] + ε(pt) where D(t) = 1 if [R(mt) - R(ft)] > 0 For 1983-90, α(p) =.0060, t=4.18 β(p) = 1.19, t=3.79 for β =1 β up(p) = -.")

5 20% MAG Rmv Abs(Rmv) -0% -20% -30% -30% -20% -0% 20% alpha =.0060, t=4.18 beta = 1.19, t=3.79; beta(up) = -.16, t=-1.75 Market Timing Fund A (hypothetical) Market Timing Fund makes investments in either long-term Corporate bonds, or in the stock market (S&P index fund) depending on whether the fund managers feel "Bullish" or "Bearish" about the stock market using monthly data from , β(p) is.52 (t = for β=1), α(p) is.0195 (t = 8.77), and Rsquared is.57 it looks like this fund has strong "selectivity" ability (about 2% per month)!! Prof. Schwert 9-10 Spring 1997

, α(p) is.0195 (t = 8.77), and Rsquared is.")

6 15% 5% 0% -5% -30% -20% -0% 20% 15% 5% -0% -5% -15% -30% -20% -0% 20% alpha =.0195, t=8.77 beta =.52, t= Prof. Schwert Spring 1997

7 Market Timing Fund: Market Timing? [R(pt) -R(ft)] = α(p) + β(p) [R(mt) - R(ft)] + + β up (p) D(t) [R(mt) - R(ft)] + ε(pt) where D(t) = 1 if [R(mt) - R(ft)] > 0 For , α(p) =.0048, t=2.74 β(p) =.14, t= for β =1 β up(p) =.84, t= 7.72 for β up = 0 so it looks like the Market Timing Fund still has small positive selectivity ability (.5% per month), but strong positive market timing ability β is.84 higher in months when [R(mt) - R(ft)] > 0 15% 5% -0% -5% -15% -30% -20% -0% 20% alpha =.0048, t=2.74 beta =.14, t=-13.83; beta(up) =.84, t=7.72 Prof. Schwert Spring 1997

8 Style Analysis Recently, many people have become interested in determining the "style" used by investment managers "growth" - stocks that have high earnings growth rates presumably high capital gains, lower dividend yields, higher risk "value" - stocks that have assets that are undervalued by the market high book/market ratios Graham & Dodd; Buffett? Style Analysis Some managers specialize by: industry (sector funds) country equity capitalization large cap; small cap; etc. asset class stocks; bonds; high-risk bonds age of company recent IPOs Prof. Schwert Spring 1997

country equity capitalization large cap; small cap; etc.")

9 Style Analysis Two approaches to analyzing style: compare with other funds similarly identified (self-determination) Lipper use correlations with passive portfolios of different types to determine similarities in return patterns Bill Sharpe's web page use Fama-French three factor risk model [market, size, B/M] Style Analysis The general point for performance evaluation is to compare an actively managed fund with a passive fund that holds similar types of stocks compare international stock fund with Morgan-Stanley World Index compare a small-cap fund with the DFA small cap index fund compare growth or value funds with the Vanguard growth or value index funds Prof. Schwert Spring 1997

10 Performance Evaluation: Summary (1) Straightforward to measure abnormal performance on a risk-adjusted basis (2) Most studies of mutual funds find that the average α across funds is not different from 0 it is debatable whether, net of fees and load charges, mutual fund managers can beat a passive, no-load well-diversified fund (e.g., S&P 500 index fund) (3) Typical large mutual fund is well-diversified (R-squared between.85 and.95) Performance Evaluation: Questions (1) Suppose you tested for selectivity and timing for a mutual fund of Eastern European stocks. Do you think that the results are as reliable as for the Magellan Fund (for example)? Why, or why not? (2) If you wanted to analyze the performance of mutual funds that specialized in small cap stocks, do you think your estimate of selectivity (α) would be significantly different from 0? Why, or why not? Prof. Schwert Spring 1997

? Why, or why not?")

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

The number of mutual funds has grown dramatically in recent

Risk-Adjusted Performance of Mutual Funds Katerina Simons Economist, Federal Reserve Bank of Boston. The author is grateful to Richard Kopcke and Peter Fortune for helpful comments and to Jay Seideman

Risk-Adjusted Performance of Mutual Funds Katerina Simons Economist, Federal Reserve Bank of Boston. The author is grateful to Richard Kopcke and Peter Fortune for helpful comments and to Jay Seideman

How To Understand The Value Of A Mutual Fund

FCS5510 Sample Homework Problems and Answer Key Unit03 CHAPTER 6. INVESTMENT COMPANIES: MUTUAL FUNDS PROBLEMS 1. What is the net asset value of an investment company with $10,000,000 in assets, $500,000

FCS5510 Sample Homework Problems and Answer Key Unit03 CHAPTER 6. INVESTMENT COMPANIES: MUTUAL FUNDS PROBLEMS 1. What is the net asset value of an investment company with $10,000,000 in assets, $500,000

Mutual Funds and Other Investment Companies. Chapter 4

Mutual Funds and Other Investment Companies Chapter 4 Investment Companies financial intermediaries that collect funds from individual investors and invest in a portfolio of assets shares = claims to portfolio

Mutual Funds and Other Investment Companies Chapter 4 Investment Companies financial intermediaries that collect funds from individual investors and invest in a portfolio of assets shares = claims to portfolio

The Case For Passive Investing!

The Case For Passive Investing! Aswath Damodaran Aswath Damodaran! 1! The Mechanics of Indexing! Fully indexed fund: An index fund attempts to replicate a market index. It is relatively simple to create,

The Case For Passive Investing! Aswath Damodaran Aswath Damodaran! 1! The Mechanics of Indexing! Fully indexed fund: An index fund attempts to replicate a market index. It is relatively simple to create,

Portfolio Performance Measures

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

Mutual Fund Performance

Mutual Fund Performance When measured before expenses passive investors who simply hold the market portfolio must earn zero abnormal returns. This means that active investors as a group must also earn

Mutual Fund Performance When measured before expenses passive investors who simply hold the market portfolio must earn zero abnormal returns. This means that active investors as a group must also earn

Market Efficiency and Behavioral Finance. Chapter 12

Market Efficiency and Behavioral Finance Chapter 12 Market Efficiency if stock prices reflect firm performance, should we be able to predict them? if prices were to be predictable, that would create the

Market Efficiency and Behavioral Finance Chapter 12 Market Efficiency if stock prices reflect firm performance, should we be able to predict them? if prices were to be predictable, that would create the

Investments 11 - Final Investment Plan Questions & Answers

Personal Finance: Another Perspective Investments 11 - Final Investment Plan Questions & Answers Updated 2013-11-04 11 Questions 1. How do I set up an investment account? 2. What is the difference between

Personal Finance: Another Perspective Investments 11 - Final Investment Plan Questions & Answers Updated 2013-11-04 11 Questions 1. How do I set up an investment account? 2. What is the difference between

Chapter 7 Risk, Return, and the Capital Asset Pricing Model

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

Investing on hope? Small Cap and Growth Investing!

Investing on hope? Small Cap and Growth Investing! Aswath Damodaran Aswath Damodaran! 1! Who is a growth investor?! The Conventional definition: An investor who buys high price earnings ratio stocks or

Investing on hope? Small Cap and Growth Investing! Aswath Damodaran Aswath Damodaran! 1! Who is a growth investor?! The Conventional definition: An investor who buys high price earnings ratio stocks or

Low Volatility Investing: A Consultant s Perspective

Daniel R. Dynan, CFA, CAIA ddynan@meketagroup.com M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 fax 781 471 3411 www.meketagroup.com M:\MARKETING\Conferences

Daniel R. Dynan, CFA, CAIA ddynan@meketagroup.com M E K E T A I N V E S T M E N T G R O U P 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 fax 781 471 3411 www.meketagroup.com M:\MARKETING\Conferences

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NDPERS 457 Companion Plan Quarterly Report 1 st Quarter 1/1/2014 3/31/2014

NDPERS 457 Companion Plan Quarterly Report 1 st Quarter 1/1/2014 3/31/2014 North Dakota Public Employees Retirement System 400 E Bdwy, Suite 505 Box 1657 Bismarck, ND 58502 NDPERS 401(a) Defined Contribution

NDPERS 457 Companion Plan Quarterly Report 1 st Quarter 1/1/2014 3/31/2014 North Dakota Public Employees Retirement System 400 E Bdwy, Suite 505 Box 1657 Bismarck, ND 58502 NDPERS 401(a) Defined Contribution

Review for Exam 2. Instructions: Please read carefully

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

Practice Set #4 and Solutions.

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

FIN-469 Investments Analysis Professor Michel A. Robe Practice Set #4 and Solutions. What to do with this practice set? To help students prepare for the assignment and the exams, practice sets with solutions

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA II MODULO ASSET MANAGEMENT LECTURE 3

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA II MODULO ASSET MANAGEMENT LECTURE 3 1 MANAGEMENT APPROACH OVERVIEW Portfolios need maintenance and periodic revision: Because the needs of the beneficiary

ECONOMIA DEGLI INTERMEDIARI FINANZIARI AVANZATA II MODULO ASSET MANAGEMENT LECTURE 3 1 MANAGEMENT APPROACH OVERVIEW Portfolios need maintenance and periodic revision: Because the needs of the beneficiary

Financial Markets And Financial Instruments - Part I

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

Financial Markets And Financial Instruments - Part I Financial Assets Real assets are things such as land, buildings, machinery, and knowledge that are used to produce goods and services. Financial assets

AlphaSolutions Reduced Volatility Bull-Bear

AlphaSolutions Reduced Volatility Bull-Bear An investment model based on trending strategies coupled with market analytics for downside risk control Portfolio Goals Primary: Seeks long term growth of capital

AlphaSolutions Reduced Volatility Bull-Bear An investment model based on trending strategies coupled with market analytics for downside risk control Portfolio Goals Primary: Seeks long term growth of capital

Bonds, Preferred Stock, and Common Stock

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An

Bonds, Preferred Stock, and Common Stock I. Bonds 1. An investor has a required rate of return of 4% on a 1-year discount bond with a $100 face value. What is the most the investor would pay for 2. An

Quantitative Asset Manager Analysis

Quantitative Asset Manager Analysis Performance Measurement Forum Dr. Stephan Skaanes, CFA, CAIA, FRM PPCmetrics AG Financial Consulting, Controlling & Research, Zurich, Switzerland www.ppcmetrics.ch Copenhagen,

Quantitative Asset Manager Analysis Performance Measurement Forum Dr. Stephan Skaanes, CFA, CAIA, FRM PPCmetrics AG Financial Consulting, Controlling & Research, Zurich, Switzerland www.ppcmetrics.ch Copenhagen,

Building and Interpreting Custom Investment Benchmarks

Building and Interpreting Custom Investment Benchmarks A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all fi gures are based in USD. 1 Introduction From simple beginnings,

Building and Interpreting Custom Investment Benchmarks A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all fi gures are based in USD. 1 Introduction From simple beginnings,

Risk and Return: Estimating Cost of Capital

Lecture: IX 1 Risk and Return: Estimating Cost o Capital The process: Estimate parameters or the risk-return model. Estimate cost o equity. Estimate cost o capital using capital structure (leverage) inormation.

Lecture: IX 1 Risk and Return: Estimating Cost o Capital The process: Estimate parameters or the risk-return model. Estimate cost o equity. Estimate cost o capital using capital structure (leverage) inormation.

A Case for Index Fund Portfolios A study of strategy, probability and payout

A Case for Index Fund Portfolios A study of strategy, probability and payout Richard A. Ferri, CFA, Portfolio Solutions Alex C. Benke, CFP, Betterment The Shift to Indexing ICI 2014 Factbook Scope of the

A Case for Index Fund Portfolios A study of strategy, probability and payout Richard A. Ferri, CFA, Portfolio Solutions Alex C. Benke, CFP, Betterment The Shift to Indexing ICI 2014 Factbook Scope of the

Learn about active and passive investing. Investor education

Learn about active and passive investing Investor education Active, passive or both: Which is right for you? Portfolios can be built using actively managed and index mutual funds either individually or

Learn about active and passive investing Investor education Active, passive or both: Which is right for you? Portfolios can be built using actively managed and index mutual funds either individually or

Personal Investment Strategies. Personal Investment Strategies

Personal Investment Strategies Bill Schwert June 12, 1999 http://schwert.ssb.rochester.edu Why Do You Save (Invest)? Answers depend on: age dependents income assets liabilities Why Do You Save (Invest)?

Personal Investment Strategies Bill Schwert June 12, 1999 http://schwert.ssb.rochester.edu Why Do You Save (Invest)? Answers depend on: age dependents income assets liabilities Why Do You Save (Invest)?

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

Investment Portfolio Management and Effective Asset Allocation for Institutional and Private Banking Clients www.mce-ama.com/2396 Senior Managers Days 4 www.mce-ama.com 1 WHY attend this programme? This

Mutual Fund Performance and Expense Ratios. A study of U.S. domestic diversified equity mutual funds. Master Thesis

Mutual Fund Performance and Expense Ratios A study of U.S. domestic diversified equity mutual funds Tilburg School of Economics and Management Department of Finance Master Thesis Student name: Aitenov

Mutual Fund Performance and Expense Ratios A study of U.S. domestic diversified equity mutual funds Tilburg School of Economics and Management Department of Finance Master Thesis Student name: Aitenov

RISKS IN MUTUAL FUND INVESTMENTS

RISKS IN MUTUAL FUND INVESTMENTS Classification of Investors Investors can be classified based on their Risk Tolerance Levels : Low Risk Tolerance Moderate Risk Tolerance High Risk Tolerance Fund Classification

RISKS IN MUTUAL FUND INVESTMENTS Classification of Investors Investors can be classified based on their Risk Tolerance Levels : Low Risk Tolerance Moderate Risk Tolerance High Risk Tolerance Fund Classification

Application of a Linear Regression Model to the Proactive Investment Strategy of a Pension Fund

Application of a Linear Regression Model to the Proactive Investment Strategy of a Pension Fund Kenneth G. Buffin PhD, FSA, FIA, FCA, FSS The consulting actuary is typically concerned with pension plan

Application of a Linear Regression Model to the Proactive Investment Strategy of a Pension Fund Kenneth G. Buffin PhD, FSA, FIA, FCA, FSS The consulting actuary is typically concerned with pension plan

3. You have been given this probability distribution for the holding period return for XYZ stock:

Fin 85 Sample Final Solution Name: Date: Part I ultiple Choice 1. Which of the following is true of the Dow Jones Industrial Average? A) It is a value-weighted average of 30 large industrial stocks. )

Fin 85 Sample Final Solution Name: Date: Part I ultiple Choice 1. Which of the following is true of the Dow Jones Industrial Average? A) It is a value-weighted average of 30 large industrial stocks. )

APPENDIX 7.4. An updated estimate of the required return on equity

APPENDIX 7.4 An updated estimate of the required return on equity Energex revised regulatory proposal July 2015 An updated estimate of the required return on equity REPORT PREPARED FOR ENERGEX June 2015

APPENDIX 7.4 An updated estimate of the required return on equity Energex revised regulatory proposal July 2015 An updated estimate of the required return on equity REPORT PREPARED FOR ENERGEX June 2015

FIN 3710. Final (Practice) Exam 05/23/06

Exam 05/23/06") FIN 3710 Investment Analysis Spring 2006 Zicklin School of Business Baruch College Professor Rui Yao FIN 3710 Final (Practice) Exam 05/23/06 NAME: (Please print your name here) PLEDGE: (Sign your name

FIN 3710 Investment Analysis Spring 2006 Zicklin School of Business Baruch College Professor Rui Yao FIN 3710 Final (Practice) Exam 05/23/06 NAME: (Please print your name here) PLEDGE: (Sign your name

VALUE ADDED INDEXING SM PERSPECTIVES. Top Ten List: Why Passive Investing Wins SUMMARY:

VALUE ADDED INDEXING SM PERSPECTIVES Top Ten List: Why Passive Investing Wins SUMMARY: Too often the active vs. passive investing debate focuses only on performance. While research shows passive strategies

VALUE ADDED INDEXING SM PERSPECTIVES Top Ten List: Why Passive Investing Wins SUMMARY: Too often the active vs. passive investing debate focuses only on performance. While research shows passive strategies

BASKET A collection of securities. The underlying securities within an ETF are often collectively referred to as a basket

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,

Cash Holdings and Mutual Fund Performance. Online Appendix

Cash Holdings and Mutual Fund Performance Online Appendix Mikhail Simutin Abstract This online appendix shows robustness to alternative definitions of abnormal cash holdings, studies the relation between

Cash Holdings and Mutual Fund Performance Online Appendix Mikhail Simutin Abstract This online appendix shows robustness to alternative definitions of abnormal cash holdings, studies the relation between

Econ 422 Summer 2006 Final Exam Solutions

Econ 422 Summer 2006 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Econ 422 Summer 2006 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

ECON 422A: FINANCE AND INVESTMENTS

ECON 422A: FINANCE AND INVESTMENTS LECTURE 10: EXPECTATIONS AND THE INFORMATIONAL CONTENT OF SECURITY PRICES Mu-Jeung Yang Winter 2016 c 2016 Mu-Jeung Yang OUTLINE FOR TODAY I) Informational Efficiency:

ECON 422A: FINANCE AND INVESTMENTS LECTURE 10: EXPECTATIONS AND THE INFORMATIONAL CONTENT OF SECURITY PRICES Mu-Jeung Yang Winter 2016 c 2016 Mu-Jeung Yang OUTLINE FOR TODAY I) Informational Efficiency:

Benchmarking Low-Volatility Strategies

Benchmarking Low-Volatility Strategies David Blitz* Head Quantitative Equity Research Robeco Asset Management Pim van Vliet, PhD** Portfolio Manager Quantitative Equity Robeco Asset Management forthcoming

Benchmarking Low-Volatility Strategies David Blitz* Head Quantitative Equity Research Robeco Asset Management Pim van Vliet, PhD** Portfolio Manager Quantitative Equity Robeco Asset Management forthcoming

1 2 3 4 5 6 Say that you need to generate $4,000 per month in retirement and $1,000 will come from social security and you have no other pension. This leaves $3,000 per month, or $36,000 per year, that

1 2 3 4 5 6 Say that you need to generate $4,000 per month in retirement and $1,000 will come from social security and you have no other pension. This leaves $3,000 per month, or $36,000 per year, that

11.3% -1.5% Year-to-Date 1-Year 3-Year 5-Year Since WT Index Inception

WisdomTree ETFs WISDOMTREE HIGH DIVIDEND FUND DHS Nearly 10 years ago, WisdomTree launched its first dividend-focused strategies based on our extensive research regarding the importance of focusing on

WisdomTree ETFs WISDOMTREE HIGH DIVIDEND FUND DHS Nearly 10 years ago, WisdomTree launched its first dividend-focused strategies based on our extensive research regarding the importance of focusing on

About Hedge Funds. What is a Hedge Fund?

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

Assignments must be submitted by midnight on their due date. Assignments that need to be redone should be submitted by one week from the due date.

List of Assignments Assignment 1. Finding information about a stock. 2. Finding information about interest rates 3. Examine an actively managed stock fund 4. Examine a bond fund 5. Investing goals and

List of Assignments Assignment 1. Finding information about a stock. 2. Finding information about interest rates 3. Examine an actively managed stock fund 4. Examine a bond fund 5. Investing goals and

The Best Mutual Funds: DFA or Vanguard?

The Best Mutual Funds: DFA or Vanguard? The most important favor that long-term investors can do for themselves is to invest in the right kinds of assets, or asset classes. Examples of asset classes are

The Best Mutual Funds: DFA or Vanguard? The most important favor that long-term investors can do for themselves is to invest in the right kinds of assets, or asset classes. Examples of asset classes are

What is your Investment IQ?

What is your Investment IQ? Jason Smith, CFA Nationwide Investment Management Group NRM-9322AO 1 DISCLOSURES This material is NOT, and should not be construed as INVESTMENT ADVICE. Principal Risks Investing

What is your Investment IQ? Jason Smith, CFA Nationwide Investment Management Group NRM-9322AO 1 DISCLOSURES This material is NOT, and should not be construed as INVESTMENT ADVICE. Principal Risks Investing

amleague PROFESSIONAL PERFORMANCE DATA

amleague PROFESSIONAL PERFORMANCE DATA APPENDIX 2 amleague Performance Ratios Definition Contents This document aims at describing the performance ratios calculated by amleague: 1. Standard Deviation 2.

amleague PROFESSIONAL PERFORMANCE DATA APPENDIX 2 amleague Performance Ratios Definition Contents This document aims at describing the performance ratios calculated by amleague: 1. Standard Deviation 2.

Glossary of Investment Terms

online report consulting group Glossary of Investment Terms glossary of terms actively managed investment Relies on the expertise of a portfolio manager to choose the investment s holdings in an attempt

online report consulting group Glossary of Investment Terms glossary of terms actively managed investment Relies on the expertise of a portfolio manager to choose the investment s holdings in an attempt

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS PROBLEM SETS 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS PROBLEM SETS 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period

T. Rowe Price Blue Chip Growth Portfolio

Equity 6-3-216 This fact sheet is provided because the Investment Division is available within a variable universal life policy issued by New York Life Insurance and Annuity Corporation. Variable Universal

Equity 6-3-216 This fact sheet is provided because the Investment Division is available within a variable universal life policy issued by New York Life Insurance and Annuity Corporation. Variable Universal

Practice Questions for Midterm II

Finance 333 Investments Practice Questions for Midterm II Winter 2004 Professor Yan 1. The market portfolio has a beta of a. 0. *b. 1. c. -1. d. 0.5. By definition, the beta of the market portfolio is

Finance 333 Investments Practice Questions for Midterm II Winter 2004 Professor Yan 1. The market portfolio has a beta of a. 0. *b. 1. c. -1. d. 0.5. By definition, the beta of the market portfolio is

CFA Examination PORTFOLIO MANAGEMENT Page 1 of 6

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

BUSINESS FINANCE (FIN 312) Spring 2008

Spring 2008") BUSINESS FINANCE (FIN 312) Spring 2008 Assignment 3 Instructions: please read carefully You can either do the assignment by yourself or work in a group of no more than two. You should show your work how

BUSINESS FINANCE (FIN 312) Spring 2008 Assignment 3 Instructions: please read carefully You can either do the assignment by yourself or work in a group of no more than two. You should show your work how

Hedge Funds: A Preamble. Michael F. Percia

Hedge Funds: A Preamble Michael F. Percia 1 Hedge Funds: A Preamble Presentation Overview Hedge Funds 101 Discussion/Questions Definition Strategies Industry Size Relative Risk/Return 2 Hedge Funds: A

Hedge Funds: A Preamble Michael F. Percia 1 Hedge Funds: A Preamble Presentation Overview Hedge Funds 101 Discussion/Questions Definition Strategies Industry Size Relative Risk/Return 2 Hedge Funds: A

Why are Some Diversified U.S. Equity Funds Less Diversified Than Others? A Study on the Industry Concentration of Mutual Funds

Why are Some Diversified U.S. Equity unds Less Diversified Than Others? A Study on the Industry Concentration of Mutual unds Binying Liu Advisor: Matthew C. Harding Department of Economics Stanford University

Why are Some Diversified U.S. Equity unds Less Diversified Than Others? A Study on the Industry Concentration of Mutual unds Binying Liu Advisor: Matthew C. Harding Department of Economics Stanford University

Chapter 5. Conditional CAPM. 5.1 Conditional CAPM: Theory. 5.1.1 Risk According to the CAPM. The CAPM is not a perfect model of expected returns.

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Q1 March 31, 2016 MFS TECHNOLOGY FUND

Q1 March 31, 2016 MFS TECHNOLOGY FUND Asset class Equity Objective Seeks capital appreciation. Portfolio management Matthew D. Sabel 6 years with MFS 19 years in industry A diversified technology strategy

Q1 March 31, 2016 MFS TECHNOLOGY FUND Asset class Equity Objective Seeks capital appreciation. Portfolio management Matthew D. Sabel 6 years with MFS 19 years in industry A diversified technology strategy

Madison Investment Advisors LLC

Madison Investment Advisors LLC Intermediate Fixed Income SELECT ROSTER Firm Information: Location: Year Founded: Total Employees: Assets ($mil): Accounts: Key Personnel: Matt Hayner, CFA Vice President

Madison Investment Advisors LLC Intermediate Fixed Income SELECT ROSTER Firm Information: Location: Year Founded: Total Employees: Assets ($mil): Accounts: Key Personnel: Matt Hayner, CFA Vice President

Evolving beyond plain vanilla ETFs

SCHWAB CENTER FOR FINANCIAL RESEARCH Journal of Investment Research Evolving beyond plain vanilla ETFs Anthony B. Davidow, CIMA Vice President, Alternative Beta and Asset Allocation Strategist, Schwab

SCHWAB CENTER FOR FINANCIAL RESEARCH Journal of Investment Research Evolving beyond plain vanilla ETFs Anthony B. Davidow, CIMA Vice President, Alternative Beta and Asset Allocation Strategist, Schwab

Are Mutual Fund Shareholders Compensated for Active Management Bets?

Are Mutual Fund Shareholders Compensated for Active Management Bets? Russ Wermers Department of Finance Robert H. Smith School of Business University of Maryland at College Park College Park, MD 2742-1815

Are Mutual Fund Shareholders Compensated for Active Management Bets? Russ Wermers Department of Finance Robert H. Smith School of Business University of Maryland at College Park College Park, MD 2742-1815

Benchmarking Real Estate Performance Considerations and Implications

Benchmarking Real Estate Performance Considerations and Implications By Frank L. Blaschka Principal, The Townsend Group The real estate asset class has difficulties in developing and applying benchmarks

Benchmarking Real Estate Performance Considerations and Implications By Frank L. Blaschka Principal, The Townsend Group The real estate asset class has difficulties in developing and applying benchmarks

Analysis of the Impact of Redemption Fees on Mutual Fund Performance: A Study on US Small Value Funds

Analysis of the Impact of Redemption Fees on Mutual Fund Performance: A Study on US Small Value Funds By Junxuan Zhu A research project submitted in partial fulfillment of requirement for the degree of

Analysis of the Impact of Redemption Fees on Mutual Fund Performance: A Study on US Small Value Funds By Junxuan Zhu A research project submitted in partial fulfillment of requirement for the degree of

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1 The unit investment trusts named above (the Portfolios

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1 The unit investment trusts named above (the Portfolios

The Effect of Closing Mutual Funds to New Investors on Performance and Size

The Effect of Closing Mutual Funds to New Investors on Performance and Size Master Thesis Author: Tim van der Molen Kuipers Supervisor: dr. P.C. de Goeij Study Program: Master Finance Tilburg School of

The Effect of Closing Mutual Funds to New Investors on Performance and Size Master Thesis Author: Tim van der Molen Kuipers Supervisor: dr. P.C. de Goeij Study Program: Master Finance Tilburg School of

Market timing at home and abroad

Market timing at home and abroad by Kenneth L. Fisher Chairman, CEO & Founder Fisher Investments, Inc. 13100 Skyline Boulevard Woodside, CA 94062-4547 650.851.3334 and Meir Statman Glenn Klimek Professor

Market timing at home and abroad by Kenneth L. Fisher Chairman, CEO & Founder Fisher Investments, Inc. 13100 Skyline Boulevard Woodside, CA 94062-4547 650.851.3334 and Meir Statman Glenn Klimek Professor

FIN 423/523 Repurchase Tender Offers

FIN 423/523 Repurchase Tender Offers 1. Cash flow out of the firm to shareholders alternative to dividend payments before recent changes in the tax laws, capital gains were taxed at lower rates (so this

FIN 423/523 Repurchase Tender Offers 1. Cash flow out of the firm to shareholders alternative to dividend payments before recent changes in the tax laws, capital gains were taxed at lower rates (so this

Behavioral Portfolio Management CFA Society of San Antonio Mamacita s San Antonio January 16, 2014

Behavioral Portfolio Management CFA Society of San Antonio Mamacita s San Antonio January 16, 2014 C. Thomas Howard, PhD Emeritus Professor of Finance Daniels College of Business CEO and Director of Research

Behavioral Portfolio Management CFA Society of San Antonio Mamacita s San Antonio January 16, 2014 C. Thomas Howard, PhD Emeritus Professor of Finance Daniels College of Business CEO and Director of Research

Market Efficiency: Definitions and Tests. Aswath Damodaran

Market Efficiency: Definitions and Tests 1 Why market efficiency matters.. Question of whether markets are efficient, and if not, where the inefficiencies lie, is central to investment valuation. If markets

Market Efficiency: Definitions and Tests 1 Why market efficiency matters.. Question of whether markets are efficient, and if not, where the inefficiencies lie, is central to investment valuation. If markets

Return in Investing in Equity Mutual Funds from 1990 to 2009

Return in Investing in Equity Mutual Funds from 1990 to 2009 Lam H. Nguyen, McNair Scholar The Pennsylvania State University McNair Faculty Research Adviser: James Miles, Ph.D. Professor of Finance, Joseph

Return in Investing in Equity Mutual Funds from 1990 to 2009 Lam H. Nguyen, McNair Scholar The Pennsylvania State University McNair Faculty Research Adviser: James Miles, Ph.D. Professor of Finance, Joseph

I.e., the return per dollar from investing in the shares from time 0 to time 1,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

Navigator International Equity/ADR

CCM-16-06-637 As of 6/30/2016 Navigator International Navigate Global Equities with a Disciplined, Research-Backed Approach to Security Selection With heightened volatility and increased correlations across

CCM-16-06-637 As of 6/30/2016 Navigator International Navigate Global Equities with a Disciplined, Research-Backed Approach to Security Selection With heightened volatility and increased correlations across

Review for Exam 2. Instructions: Please read carefully

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES Characteristics. Short-term IOUs. Highly Liquid (Like Cash). Nearly free of default-risk. Denomination. Issuers Types Treasury Bills Negotiable

2: ASSET CLASSES AND FINANCIAL INSTRUMENTS MONEY MARKET SECURITIES Characteristics. Short-term IOUs. Highly Liquid (Like Cash). Nearly free of default-risk. Denomination. Issuers Types Treasury Bills Negotiable

Morgan Stanley Universal Institutional Funds US Real Estate Portfolio Class I

Equity 3-31-216 This fact sheet is provided because the Investment Division is available within a variable universal life policy issued by New York Life Insurance and Annuity Corporation. Variable Universal

Equity 3-31-216 This fact sheet is provided because the Investment Division is available within a variable universal life policy issued by New York Life Insurance and Annuity Corporation. Variable Universal

RISK ASSESSMENT QUESTIONNAIRE

Time Horizon 6/14 Your current situation and future income needs. 1. What is your current age? 2. When do you expect to start drawing income? A Less than 45 A Not for at least 20 years B 45 to 55 B In

Time Horizon 6/14 Your current situation and future income needs. 1. What is your current age? 2. When do you expect to start drawing income? A Less than 45 A Not for at least 20 years B 45 to 55 B In

Capital Idea: Take a more dynamic approach to managing volatility in target date funds.

Capital Idea: Take a more dynamic approach to managing volatility in target date funds. We believe that target date series should feature not only a gradual reduction in equities over time, but also a

Capital Idea: Take a more dynamic approach to managing volatility in target date funds. We believe that target date series should feature not only a gradual reduction in equities over time, but also a

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS PROBLEM SETS 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period

CHAPTER 11: THE EFFICIENT MARKET HYPOTHESIS PROBLEM SETS 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period

The Equity Risk Premium, the Liquidity Premium, and Other Market Premiums. What is the Equity Risk Premium?

The Equity Risk, the, and Other Market s Roger G. Ibbotson Professor, Yale School of Management Canadian Investment Review Investment Innovation Conference Bermuda November 2011 1 What is the Equity Risk?

The Equity Risk, the, and Other Market s Roger G. Ibbotson Professor, Yale School of Management Canadian Investment Review Investment Innovation Conference Bermuda November 2011 1 What is the Equity Risk?

Finding outperforming managers. Randolph B. Cohen Harvard Business School

Finding outperforming managers Randolph B. Cohen Harvard Business School 1 Conventional wisdom holds that: Managers can t pick stocks and therefore don t beat the market It s impossible to pick winning

Finding outperforming managers Randolph B. Cohen Harvard Business School 1 Conventional wisdom holds that: Managers can t pick stocks and therefore don t beat the market It s impossible to pick winning

Stock Return Momentum and Investor Fund Choice

Stock Return Momentum and Investor Fund Choice TRAVIS SAPP and ASHISH TIWARI* Journal of Investment Management, forthcoming Keywords: Mutual fund selection; stock return momentum; investor behavior; determinants

Stock Return Momentum and Investor Fund Choice TRAVIS SAPP and ASHISH TIWARI* Journal of Investment Management, forthcoming Keywords: Mutual fund selection; stock return momentum; investor behavior; determinants

Value of Equity and Per Share Value when there are options and warrants outstanding. Aswath Damodaran

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Value of Equity and Per Share Value when there are options and warrants outstanding Aswath Damodaran 1 Equity Value and Per Share Value: A Test Assume that you have done an equity valuation of Microsoft.

Chapter 9. The Valuation of Common Stock. 1.The Expected Return (Copied from Unit02, slide 39)

") Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Readings Chapters 9 and 10 Chapter 9. The Valuation of Common Stock 1. The investor s expected return 2. Valuation as the Present Value (PV) of dividends and the growth of dividends 3. The investor s required

Sector Fund Performance: Analysis of Cash Flow Volatility and Returns

Sector Fund Performance: Analysis of Cash Flow Volatility and Returns Ashish TIWARI * and Anand M. VIJH ** ABSTRACT Sector funds are an important and growing segment of the mutual fund industry. This paper

Sector Fund Performance: Analysis of Cash Flow Volatility and Returns Ashish TIWARI * and Anand M. VIJH ** ABSTRACT Sector funds are an important and growing segment of the mutual fund industry. This paper

The Morningstar Category TM Classifications for 529 Investment Options

The Morningstar Category TM Classifications for 529 Investment Options (for 529 portfolios available for sale in the United States) Morningstar Methodology Paper October 31, 2013 2013 Morningstar, Inc.

The Morningstar Category TM Classifications for 529 Investment Options (for 529 portfolios available for sale in the United States) Morningstar Methodology Paper October 31, 2013 2013 Morningstar, Inc.

2 11,455. Century Small Cap Select Instl SMALL-CAP as of 09/30/2015. Investment Objective. Fund Overview. Performance Overview

SMALL-CAP as of 09/30/2015 Investment Objective Century Small Cap Select Fund (CSCS) seeks long-term capital growth. Performance Overview Cumulative % Annualized % Quarter Year Since to Date to Date 1

SMALL-CAP as of 09/30/2015 Investment Objective Century Small Cap Select Fund (CSCS) seeks long-term capital growth. Performance Overview Cumulative % Annualized % Quarter Year Since to Date to Date 1

Chapter 12. Investing in the Stock Market. The Indexing Alternative. The Performance of Active and Passive Funds

Chapter 12 Investing in the Stock Market Most investors, both institutional and individual, will find the best way to own common stocks is through an index fund that charges minimal fees. Warren Buffet

Chapter 12 Investing in the Stock Market Most investors, both institutional and individual, will find the best way to own common stocks is through an index fund that charges minimal fees. Warren Buffet

The performance of mutual funds during the financial crisis

The performance of mutual funds during the financial crisis Abstract The performance of mutual funds has been an interesting topic of research in the last few decades. The most common measurements for

The performance of mutual funds during the financial crisis Abstract The performance of mutual funds has been an interesting topic of research in the last few decades. The most common measurements for

Mid-Term Spring 2003

Mid-Term Spring 2003 1. (1 point) You want to purchase XYZ stock at $60 from your broker using as little of your own money as possible. If initial margin is 50% and you have $3000 to invest, how many shares

Mid-Term Spring 2003 1. (1 point) You want to purchase XYZ stock at $60 from your broker using as little of your own money as possible. If initial margin is 50% and you have $3000 to invest, how many shares

Navigator Global Equity ETF

Portfolio Allocation Portfolio Overview Clark Capital Management Group is an employee-owned, independent Investment Advisory firm providing institutional-quality investment solutions to individuals, corporations,

Portfolio Allocation Portfolio Overview Clark Capital Management Group is an employee-owned, independent Investment Advisory firm providing institutional-quality investment solutions to individuals, corporations,

Non-FDIC Insured May Lose Value No Bank Guarantee. Time-Tested Investment Strategies for the Long Term

Non-FDIC Insured May Lose Value No Bank Guarantee Time-Tested Investment Strategies for the Long Term Rely on These Four Time-Tested Strategies to Keep You on Course. Buy Right and Sit Tight Keep Your

Non-FDIC Insured May Lose Value No Bank Guarantee Time-Tested Investment Strategies for the Long Term Rely on These Four Time-Tested Strategies to Keep You on Course. Buy Right and Sit Tight Keep Your

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

Risk and Return Models: Equity and Debt. Aswath Damodaran 1

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Financial Market Efficiency and Its Implications

Financial Market Efficiency: The Efficient Market Hypothesis (EMH) Financial Market Efficiency and Its Implications Financial markets are efficient if current asset prices fully reflect all currently available

Financial Market Efficiency: The Efficient Market Hypothesis (EMH) Financial Market Efficiency and Its Implications Financial markets are efficient if current asset prices fully reflect all currently available

Stonegate Wealth Management. Registered Investment Advisor 17-17 Route 208 Fair Lawn, N.J. 07410 (201) 791-0085 www.stonegatewealth.

791-0085 www.stonegatewealth.") Stonegate Wealth Management Registered Investment Advisor 17-17 Route 208 Fair Lawn, N.J. 07410 (201) 791-0085 www.stonegatewealth.com Stonegate Wealth Management $200 Million in assets under management.

Stonegate Wealth Management Registered Investment Advisor 17-17 Route 208 Fair Lawn, N.J. 07410 (201) 791-0085 www.stonegatewealth.com Stonegate Wealth Management $200 Million in assets under management.

Alpha - the most abused term in Finance. Jason MacQueen Alpha Strategies & R-Squared Ltd

Alpha - the most abused term in Finance Jason MacQueen Alpha Strategies & R-Squared Ltd Delusional Active Management Almost all active managers claim to add Alpha with their investment process This Alpha

Alpha - the most abused term in Finance Jason MacQueen Alpha Strategies & R-Squared Ltd Delusional Active Management Almost all active managers claim to add Alpha with their investment process This Alpha

Chapter 13 Composition of the Market Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z,

Chapter 13 Composition of the arket Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z, and a riskless government security. Evaluated at current prices in

Chapter 13 Composition of the arket Portfolio 1. Capital markets in Flatland exhibit trade in four securities, the stocks X, Y and Z, and a riskless government security. Evaluated at current prices in

Covered Call Investing and its Benefits in Today s Market Environment

ZIEGLER CAPITAL MANAGEMENT: MARKET INSIGHT & RESEARCH Covered Call Investing and its Benefits in Today s Market Environment Covered Call investing has attracted a great deal of attention from investors

ZIEGLER CAPITAL MANAGEMENT: MARKET INSIGHT & RESEARCH Covered Call Investing and its Benefits in Today s Market Environment Covered Call investing has attracted a great deal of attention from investors

Wealth Management Education Series. Explore the Field of Mutual Funds

Wealth Management Education Series Explore the Field of Mutual Funds Wealth Management Education Series Explore the Field of Mutual Funds Managing your wealth well is like tending a beautiful formal garden

Wealth Management Education Series Explore the Field of Mutual Funds Wealth Management Education Series Explore the Field of Mutual Funds Managing your wealth well is like tending a beautiful formal garden

2012 Campion Asset Management, LLC Page 1

Introduction. As your investment committee evaluates how to best manage your organization s long-term reserve, you will be presented with two alternatives for implementing your strategic asset allocation:

Introduction. As your investment committee evaluates how to best manage your organization s long-term reserve, you will be presented with two alternatives for implementing your strategic asset allocation: