Risk Based Capital and Capital Allocation in Insurance. Professor Michael Sherris Australian School of Business

|

|

|

- Bertha Reynolds

- 7 years ago

- Views:

Transcription

1 Risk Based Capital and Capital Allocation in Insurance Professor Michael Sherris Australian School of Business

2 Introduction What Is Capital? Financial capital Funding of productive assets (real capital), expected claims cost in insurance Risk based capital Providing financial solvency and managing volatility in business outcomes Focus on Risk Based Capital Most significant for financial intermediaries Prudential/solvency regulation (Basel II, Solvency II) Economic capital (based on risk) used for pricing and financial management

3 Capital Allocation Capital allocation used for many purposes: Determining actual or expected return on capital by line of business Assessing value of acquiring and divesting businesses/assets Determining line management compensation based on return on capital Pricing allowing for costs of capital Risk quantification using risk based and economic capital

4 Economic capital Current Practice Risk measure used to allocate capital to lines of business VaR in banking, TailVaR in insurance Capital is aggregated (allowing for diversification) to determine enterprise wide risk based capital Diversification, dependence (copula, conditional dependent factor models) Pricing in multiline/multiproduct insurer or bank Capital allocation to risk or line of business Expected return on capital (RAROC).

5 Current Practice Fair rate of return for regulated lines of insurance business Allocation of capital to line of business Fair rate of return on capital - Enterprise wide or varying byline Frictional costs (tax, agency, financial distress) Regulatory solvency requirements Based on risks such as market, credit, insurance, operational and aggregated for enterprise wide solvency Risk models varying for different risks (multivariate normal, frequency and severity, extreme value)

6 Many different risk measures VaR, ruin probability, TailVaR, Current Practice Expected Policyholder Deficit, Insolvency Default Put Option. Which measure makes most economic sense? Many different approaches to allocating capital to line of business proportional to risk measure, proportional to liabilities, marginal allocations, equal expected returns to capital, covariance of losses. How to determine an economically sensible measure?

7 Current Practice Capital allocation generally considers lines of business or risks on an individual basis (which may be assets or liabilities) no direct allowance for dependence between risks or business lines Diversification benefit considered later at the aggregated level Yet, capital is available to support all lines of business. How to allow for this in allocating capital to line of business?

8 Current Practice Surplus Allocation with Different Risk Measures - Normal Assumption 50.00% 40.00% 30.00% Percentage 20.00% beta var tail var sd 10.00% 0.00% Line 1 Line 2 Line 3 Line 4 Line 5 Line 6 Line 7 Line 8 Line 9 Line % Lines of Liabilities

9 Capital Allocation Irrelevance Famous Corporate Finance Theory on Irrelevance of Capital Structure (Modigliani and Miller) Perfect market assumptions, no frictional costs of capital Under these assumptions similar result (almost) holds for capital allocation to line of business/division Different capital allocations are consistent with different expected returns on capital by line and an infinite number of alternatives are possible No value maximising optimum (without market imperfections) Qualification risk based insolvency put must be allocated based on payoffs by line (contribution to insolvency risk has financial impact)

Qualification risk based insolvency put must be allocated based on payoffs by line (contribution to insolvency risk has")

10 Approaches To Capital Allocation Allocate capital to each line based on a risk measure and derive an expected return on capital Choice of risk measure VaR, TailVaR? Expected return on capital same for all lines? adjusted for risk? No agreement. Is there an optimal approach? Use an ERM value maximising (cost minimising) objective and derive implied capital allocations consistent with value maximisation Costs of capital (tax, agency and financial distress) minimisation produces an enterprise VaR target for capital Price elasticity of demand produce value maximising optimum Equity or debtholder perspective? (shareholder or policyholder in insurance)

minimisation produces an enterprise VaR target for capital Price elasticity of demand produce value maximising optimum Equity or debtholder")

11 Capital Allocation and Pricing In Multi-line Businesses Risk based capital should be determined at an enterprise level Minimisation of (expected) tax, agency and financial distress costs Maximisation of shareholder value added (allowing for price elasticity of demand) Pricing of lines of business Cost based on risk-adjusted discounted expected values of cash flows (income minus expenses) No need to allocate capital (except for by-line contribution to insolvency risk) Market price reflects market factors such as price elasticity, profit margins on sales

Market price reflects market factors such as price elasticity, profit")

12 Pricing and Insolvency Framework for fair pricing, capital allocation and insolvency put option value Sherris, M., (2006), Solvency, Capital Allocation and Fair Rate of Return in Insurance, Journal of Risk and Insurance, Vol 73, No 1, (March 2006), (this paper awarded the Casualty Actuarial Society (CAS) 2007 prize for the most valuable contribution to casualty actuarial science published in American Risk and Insurance Association (ARIA) literature in the preceding year) Practical model based on dependent log-normal risks Sherris, M. and John van der Hoek, (2006), Capital Allocation in Insurance: Economic Capital and the Allocation of the Default Option Value, North American Actuarial Journal, April, Volume 10, Number 2,

literature in the preceding year) Practical model based on dependent log-normal risks Sherris, M.")

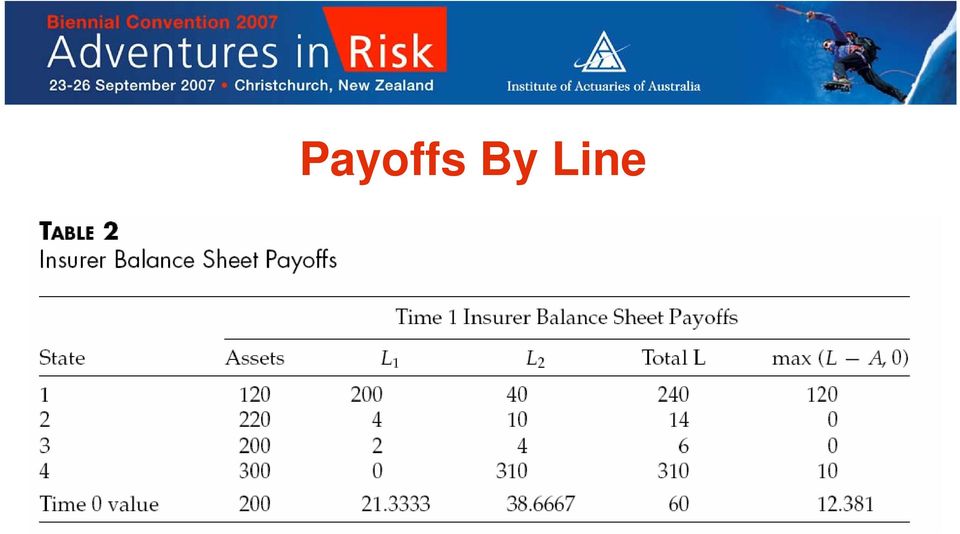

13 Simple Insurance Example Single period example emphasise main concepts Two lines of business - Liability 1 and Liability 2 4 outcomes or states Which liability line is the most risky? VaR or economic capital compared with the insolvency put option value Is capital allocation required for pricing?

14 Simple Insurance Example

15 Payoffs By Line

16 Default Put Risk Measure

17 Equity Payoffs

18 Risk Based Capital Frictional Costs Australian Prudential Regulations and Risk Based Capital using an Internal Model Sutherland-Wong, C. and Sherris, M., (2005), Risk-Based Regulatory Capital for Insurers: A Case Study, Journal of Actuarial Practice, Vol 12, 2005, Minimising frictional costs of insurer capital produces an optimal capital level based on VaR at much lower levels than observed Chandra, V. and M. Sherris (2007), Capital Management and Frictional Costs in Insurance, Australian Actuarial Journal, February 2007, Volume 12, Issue 4.

19 Risk Based Capital VaR Probability for Insurer Liability Probability (L>A+C) % 1.25% 2.00% 2.75% 3.50% Frictional costs of capital (%) 4.25% 5.00% 11% 13.00% 12.00% 15.00% 14.00% Financial distress costs (%)

20 Value Maximisation with Frictional Costs and Demand Elasticity Value maximising approach compared to economic capital and VaR approaches incorporating frictional costs of capital and price elasticity Yow, S. and Sherris, M. (2007), Enterprise Risk Management, Insurer Pricing and Capital Allocation, Geneva Association/IIS Prize winning paper to appear in Geneva Papers on Risk and Insurance Value maximising approach to risk based capital and by-line pricing Yow, S. and Sherris, M. (2007), Enterprise Risk Management, Insurer Value Maximisation, and Market Frictions, Invited Paper 5th Annual Enterprise Risk Management Symposium and 9th Bowles Symposium: The ERM Research Track, Chicago, March 28-30, 2007

21 Maximizing Enterprise Value Added (EVA)

22 Lower optimal capital for higher agency costs 200% 183% 1.0% Economic Capital as a % of Liabilities 150% 100% 50% 26% 22% 19% 17% 15% 0.8% 0.6% 0.4% 0.2% Default Ratio 0% 0% 2% 4% 6% 8% 10% Agency Costs of Capital 0.0% Economic Capital Default Ratio

23 Higher optimal capital for increasing bankruptcy costs 100% 1.0% Economic Capital as a % of Liabilities 80% 60% 40% 20% 26% 28% 29% 31% 31% 32% 0.8% 0.6% 0.4% 0.2% Default Ratio 0% 0% 10% 20% 30% 40% 50% Bankruptcy Costs 0.0% Economic Capital Default Ratio

24 Pricing Strategies Strategy Approach Method of Allocation Assumed Cost of Capital 1 Maximize EVA None None 2 VaR at 99.5% Proportional 15% 3 VaR at 99.5% Proportional 20% 4 VaR at 99.5% Proportional 15% (Commercial) and 25% Personal/Compulsory) 5 Maximize Firm Value None None Table 8: Strategies for insurer pricing and capitalization.

25 Economic Profit Margins 15% 10% Economic Profit Margin 5% Strategy 1 Strategy 2 Strategy 3 Strategy 4 0% Motor Household Fire & ISR Liability CTP -5% Based on assumed price elasticity (not actual market data)

26 Conclusions The science of capital allocation has made significant advances in our understanding of allocation and use of risk based capital, yet limited theoretical guidance on which risk measure is consistent with value maximisation and no well developed economic theory underlying the risk measures different firms use different risk measures no agreement on the appropriate risk measure risk measures are applied inconsistently for different risks, different lines of business, products and divisions for insurer pricing the price of risk should vary with the type of risk under consideration yet most risk based capital approaches implicitly use a common price of risk based on a firm wide expected cost of capital for pricing.

27 Conclusions Recent developments in capital allocation for risk capital for solvency and by-line pricing indicate a new direction is required Importance of risk measure insolvency default option value Allocation by line and fair pricing Frictional costs and market imperfections Value maximising and demand elasticity

Risk-Based Regulatory Capital for Insurers: A Case Study 1

Risk-Based Regulatory Capital for Insurers: A Case Study 1 Christian Sutherland-Wong Bain International Level 35, Chifley Tower 2 Chifley Square Sydney, AUSTRALIA Tel: + 61 2 9229 1615 Fax: +61 2 9223

Risk-Based Regulatory Capital for Insurers: A Case Study 1 Christian Sutherland-Wong Bain International Level 35, Chifley Tower 2 Chifley Square Sydney, AUSTRALIA Tel: + 61 2 9229 1615 Fax: +61 2 9223

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Economic Impact of Capital Level in an Insurance Company

Economic Impact of Capital Level in an Insurance Company Yingjie Zhang CNA Insurance Companies CNA Plaza 30S, Chicago, IL 60685, USA Tel: 312-822-4372 Email: yingjie.zhang@cna.com Abstract Capital level

Economic Impact of Capital Level in an Insurance Company Yingjie Zhang CNA Insurance Companies CNA Plaza 30S, Chicago, IL 60685, USA Tel: 312-822-4372 Email: yingjie.zhang@cna.com Abstract Capital level

ERM-2: Introduction to Economic Capital Modeling

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

Capital Allocation and the Price of Insurance: Evidence from the Merger and Acquisition Activity in the U.S. Property- Liability Insurance Industry

Capital Allocation and the Price of Insurance: Evidence from the Merger and Acquisition Activity in the U.S. Property- Liability Insurance Industry Jeungbo Shim May 2007 ABSTRACT This paper examines empirically

Capital Allocation and the Price of Insurance: Evidence from the Merger and Acquisition Activity in the U.S. Property- Liability Insurance Industry Jeungbo Shim May 2007 ABSTRACT This paper examines empirically

Subject ST9 Enterprise Risk Management Syllabus

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Economic Impact of Capital Level in an Insurance Company

Economic Impact of Capital Level in an Insurance Company by Yingjie Zhang ABSTRACT This paper examines the impact of capital level on policy premium and shareholder return. If an insurance firm has a chance

Economic Impact of Capital Level in an Insurance Company by Yingjie Zhang ABSTRACT This paper examines the impact of capital level on policy premium and shareholder return. If an insurance firm has a chance

optimum capital Is it possible to increase shareholder wealth by changing the capital structure?

78 technical optimum capital RELEVANT TO ACCA QUALIFICATION PAPER F9 Is it possible to increase shareholder wealth by changing the capital structure? The first question to address is what is meant by capital

78 technical optimum capital RELEVANT TO ACCA QUALIFICATION PAPER F9 Is it possible to increase shareholder wealth by changing the capital structure? The first question to address is what is meant by capital

Risk-Based Capital. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Use the table for the questions 18 and 19 below.

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Olav Jones, Head of Insurance Risk

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

Ch. 18: Taxes + Bankruptcy cost

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Chapter 15: Debt Policy

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

THE IMPACT OF INVESTMENT STRATEGY ON THE MARKET VALUE AND PRICING DECISIONS OF A PROPERTY/CASUALTY INSURER. Abstract

THE IMPACT OF INVESTMENT STRATEGY ON THE MARKET VALUE AND PRICING DECISIONS OF A PROPERTY/CASUALTY INSURER TRENT R. VAUGHN Abstract This paper examines the impact of investment strategy on the market value

THE IMPACT OF INVESTMENT STRATEGY ON THE MARKET VALUE AND PRICING DECISIONS OF A PROPERTY/CASUALTY INSURER TRENT R. VAUGHN Abstract This paper examines the impact of investment strategy on the market value

How To Allocate Capital

Allocation of Capital in the Insurance Industry J. David CUMMINS The Wharton School 1. Introduction The purpose of this article is to provide an overview of the various techniques that have been suggested

Allocation of Capital in the Insurance Industry J. David CUMMINS The Wharton School 1. Introduction The purpose of this article is to provide an overview of the various techniques that have been suggested

RBC and its Practical Applications to Non-Life Insurance

RBC and its Practical Applications to Non-Life Insurance 27 April 2006 Authors: John McCrossan Colin Manley Declan Lavelle 1.0 Introduction The title of this paper is RBC and its Practical Applications

RBC and its Practical Applications to Non-Life Insurance 27 April 2006 Authors: John McCrossan Colin Manley Declan Lavelle 1.0 Introduction The title of this paper is RBC and its Practical Applications

Pricing Alternative forms of Commercial insurance cover. Andrew Harford

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

Pricing Alternative forms of Commercial insurance cover Andrew Harford Pricing alternative covers Types of policies Overview of Pricing Approaches Total claim cost distribution Discounting Cash flows Adjusting

ERM Learning Objectives

ERM Learning Objectives INTRODUCTION These Learning Objectives are expressed in terms of the knowledge required of an expert * in enterprise risk management (ERM). The Learning Objectives are organized

ERM Learning Objectives INTRODUCTION These Learning Objectives are expressed in terms of the knowledge required of an expert * in enterprise risk management (ERM). The Learning Objectives are organized

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

A liability driven approach to asset allocation

A liability driven approach to asset allocation Xinliang Chen 1, Jan Dhaene 2, Marc Goovaerts 2, Steven Vanduffel 3 Abstract. We investigate a liability driven methodology for determining optimal asset

A liability driven approach to asset allocation Xinliang Chen 1, Jan Dhaene 2, Marc Goovaerts 2, Steven Vanduffel 3 Abstract. We investigate a liability driven methodology for determining optimal asset

ING Insurance Economic Capital Framework

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

ING Insurance Economic Capital Framework Thomas C. Wilson Chief Insurance Risk Officer Kent University, September 5, 2007 www.ing.com Objectives of this session ING has been using economic capital internally

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium. 21 March 2006

Summary Report for Belgium. 21 March 2006") Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

Quantitative Impact Study 1 (QIS1) Summary Report for Belgium 21 March 2006 1 Quantitative Impact Study 1 (QIS1) Summary Report for Belgium INTRODUCTORY REMARKS...4 1. GENERAL OBSERVATIONS...4 1.1. Market

Embedded Value 2014 Report

Embedded Value 2014 Report Manulife Financial Corporation Page 1 of 13 Background: Consistent with our objective of providing useful information to investors about our Company, and as noted in our 2014

Embedded Value 2014 Report Manulife Financial Corporation Page 1 of 13 Background: Consistent with our objective of providing useful information to investors about our Company, and as noted in our 2014

Chapter 17 Does Debt Policy Matter?

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

The Financial Crises of the 21st Century

The Financial Crises of the 21st Century Workshop of the Austrian Research Association (Österreichische Forschungsgemeinschaft) 18. - 19. 10. 2012 Towards a Unified European Banking Market Univ.Prof. Dr.

The Financial Crises of the 21st Century Workshop of the Austrian Research Association (Österreichische Forschungsgemeinschaft) 18. - 19. 10. 2012 Towards a Unified European Banking Market Univ.Prof. Dr.

Risk-Adjusted Performance Measurement. and Capital Allocation. in Insurance Firms

Risk-Adjusted erformance Measurement and Capital Allocation in Insurance Firms Helmut Gründl Hato Schmeiser Humboldt-Universität zu Berlin, Germany 1 Introduction The Contributions of Merton/erold and

Risk-Adjusted erformance Measurement and Capital Allocation in Insurance Firms Helmut Gründl Hato Schmeiser Humboldt-Universität zu Berlin, Germany 1 Introduction The Contributions of Merton/erold and

QBE INSURANCE GROUP LIMITED. JP Morgan AUSTRALASIAN INVESTMENT CONFERENCE SINGAPORE OCTOBER 2004. Presenter: Neil Drabsch, CFO

QBE INSURANCE GROUP LIMITED JP Morgan AUSTRALASIAN INVESTMENT CONFERENCE SINGAPORE OCTOBER 2004 Presenter: Neil Drabsch, CFO 1 Company overview QBE is an Australian-based general insurance and reinsurance

QBE INSURANCE GROUP LIMITED JP Morgan AUSTRALASIAN INVESTMENT CONFERENCE SINGAPORE OCTOBER 2004 Presenter: Neil Drabsch, CFO 1 Company overview QBE is an Australian-based general insurance and reinsurance

Net revenue 785 25 1,721 05 5,038 54 3,340 65 Tax payable (235 58) (516 32) (1,511 56) (1,002 20)

(516 32) (1,511 56) (1,002 20)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2013 Answers 1 (a) Calculating the net present value of the investment project using a nominal terms approach requires the

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2013 Answers 1 (a) Calculating the net present value of the investment project using a nominal terms approach requires the

The Cost of Financial Frictions for Life Insurers

The Cost of Financial Frictions for Life Insurers Ralph S. J. Koijen Motohiro Yogo University of Chicago and NBER Federal Reserve Bank of Minneapolis 1 1 The views expressed herein are not necessarily

The Cost of Financial Frictions for Life Insurers Ralph S. J. Koijen Motohiro Yogo University of Chicago and NBER Federal Reserve Bank of Minneapolis 1 1 The views expressed herein are not necessarily

Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%

![Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%](/thumbs/40/20831119.jpg "Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

SOA Annual Symposium Shanghai. November 5-6, 2012. Shanghai, China

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 5a: Some Research Results on Insurance Risk Models with Dependent Classes of Business Kam C. Yuen Professor Kam C. Yuen The University

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 5a: Some Research Results on Insurance Risk Models with Dependent Classes of Business Kam C. Yuen Professor Kam C. Yuen The University

Capital Management in a Solvency II World & the Role of Reinsurance

Capital Management in a Solvency II World & the Role of Reinsurance Paolo de Martin CEO SCOR Global Life IAA Colloquium Oslo June 2015 Overview Why I Focus today on Capital Management? Reminder key objectives

Capital Management in a Solvency II World & the Role of Reinsurance Paolo de Martin CEO SCOR Global Life IAA Colloquium Oslo June 2015 Overview Why I Focus today on Capital Management? Reminder key objectives

ARC Centre of Excellence in Population Ageing Research. Working Paper 2012/04

ARC Centre of Excellence in Population Ageing Research Working Paper 2012/04 An Analysis of Reinsurance Optimisation in Life Insurance Elena Veprauskaite 1, Michael Sherris 2 1 School of Management, University

ARC Centre of Excellence in Population Ageing Research Working Paper 2012/04 An Analysis of Reinsurance Optimisation in Life Insurance Elena Veprauskaite 1, Michael Sherris 2 1 School of Management, University

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey Concept The purpose of this paper is to build a bridge between the traditional methods of looking at financial

Property Casualty Insurer Economic Capital using a VAR Model Thomas Conway and Mark McCluskey Concept The purpose of this paper is to build a bridge between the traditional methods of looking at financial

Third Edition. Philippe Jorion GARP. WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Third Edition Philippe Jorion GARP WILEY John Wiley & Sons, Inc.

Economic Capital for Life Insurance Companies Society of Actuaries. Prepared by: Ian Farr Hubert Mueller Mark Scanlon Simon Stronkhorst

Economic Capital for Life Insurance Companies Society of Actuaries Prepared by: Ian Farr Hubert Mueller Mark Scanlon Simon Stronkhorst Towers Perrin February 2008 Table of Contents 1. Introduction...1

Economic Capital for Life Insurance Companies Society of Actuaries Prepared by: Ian Farr Hubert Mueller Mark Scanlon Simon Stronkhorst Towers Perrin February 2008 Table of Contents 1. Introduction...1

Enterprise Financial Risk Management. Kenneth Winston Senior Investment Officer. OppenheimerFunds

OppenheimerFunds Enterprise Financial Risk Management Kenneth Winston Senior Investment Officer 2003 Kenneth J. Winston Kwinston@oppenheimerfunds.com Definition of Enterprise Financial Risk Management

OppenheimerFunds Enterprise Financial Risk Management Kenneth Winston Senior Investment Officer 2003 Kenneth J. Winston Kwinston@oppenheimerfunds.com Definition of Enterprise Financial Risk Management

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment. Craig Turnbull FIA

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment Craig Turnbull FIA Background and Research Objectives 2 Background: DB Pensions and Risk + Aggregate deficits

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment Craig Turnbull FIA Background and Research Objectives 2 Background: DB Pensions and Risk + Aggregate deficits

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

Asymmetric Correlations and Tail Dependence in Financial Asset Returns (Asymmetrische Korrelationen und Tail-Dependence in Finanzmarktrenditen)

") Topic 1: Asymmetric Correlations and Tail Dependence in Financial Asset Returns (Asymmetrische Korrelationen und Tail-Dependence in Finanzmarktrenditen) Besides fat tails and time-dependent volatility,

Topic 1: Asymmetric Correlations and Tail Dependence in Financial Asset Returns (Asymmetrische Korrelationen und Tail-Dependence in Finanzmarktrenditen) Besides fat tails and time-dependent volatility,

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

CEA Working Paper on the risk measures VaR and TailVaR

CEA Working Paper on the risk measures VaR and TailVaR CEA reference: ECO 6294 Date: 7 November 2006 Referring to: Solvency II Related CEA documents: See Appendix Contact person: Patricia Plas, ECOFIN

CEA Working Paper on the risk measures VaR and TailVaR CEA reference: ECO 6294 Date: 7 November 2006 Referring to: Solvency II Related CEA documents: See Appendix Contact person: Patricia Plas, ECOFIN

Risk-Adjusted Performance Measurement for P&C Insurers Richard Goldfarb, FCAS, CFA, FRM Original Draft: December 2006 (Revised: October 2010)

") Risk-Adjusted Performance Measurement for P&C Insurers Richard Goldfarb, FCAS, CFA, FRM Original Draft: December 2006 (Revised: October 2010) Abstract This paper was prepared as an introduction to risk-adjusted

Risk-Adjusted Performance Measurement for P&C Insurers Richard Goldfarb, FCAS, CFA, FRM Original Draft: December 2006 (Revised: October 2010) Abstract This paper was prepared as an introduction to risk-adjusted

Methodology. Discounting. MVM Methods

Methodology In this section, we describe the approaches taken to calculate the fair value of the insurance loss reserves for the companies, lines, and valuation dates in our study. We also describe a variety

Methodology In this section, we describe the approaches taken to calculate the fair value of the insurance loss reserves for the companies, lines, and valuation dates in our study. We also describe a variety

Firm characteristics. The current issue and full text archive of this journal is available at www.emeraldinsight.com/0307-4358.htm

The current issue and full text archive of this journal is available at www.emeraldinsight.com/0307-4358.htm How firm characteristics affect capital structure: an empirical study Nikolaos Eriotis National

The current issue and full text archive of this journal is available at www.emeraldinsight.com/0307-4358.htm How firm characteristics affect capital structure: an empirical study Nikolaos Eriotis National

Stochastic Solvency Testing in Life Insurance. Genevieve Hayes

Stochastic Solvency Testing in Life Insurance Genevieve Hayes Deterministic Solvency Testing Assets > Liabilities In the insurance context, the values of the insurer s assets and liabilities are uncertain.

Stochastic Solvency Testing in Life Insurance Genevieve Hayes Deterministic Solvency Testing Assets > Liabilities In the insurance context, the values of the insurer s assets and liabilities are uncertain.

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869. Words: 3441

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Accounting for (Non-Life) Insurance in Australia

Insurance in Australia") IASB MEETING, APRIL 2005 OBSERVER NOTE (Agenda Item 3a) Accounting for (Non-Life) Insurance in Australia Tony Coleman & Andries Terblanche Presentation to IASB 19 April 2005 Agenda Australian Non-Life

IASB MEETING, APRIL 2005 OBSERVER NOTE (Agenda Item 3a) Accounting for (Non-Life) Insurance in Australia Tony Coleman & Andries Terblanche Presentation to IASB 19 April 2005 Agenda Australian Non-Life

Economic Capital and Financial Risk Management

Economic Capital and Financial Risk Management By Pradip Tapadar, MStat, PhD, FFA, FIAI Contact address School of Mathematics, Statistics and Actuarial Science, University of Kent, Canterbury, CT2 7NZ,

Economic Capital and Financial Risk Management By Pradip Tapadar, MStat, PhD, FFA, FIAI Contact address School of Mathematics, Statistics and Actuarial Science, University of Kent, Canterbury, CT2 7NZ,

CHAPTER 1: INTRODUCTION, BACKGROUND, AND MOTIVATION. Over the last decades, risk analysis and corporate risk management activities have

Chapter 1 INTRODUCTION, BACKGROUND, AND MOTIVATION 1.1 INTRODUCTION Over the last decades, risk analysis and corporate risk management activities have become very important elements for both financial

Chapter 1 INTRODUCTION, BACKGROUND, AND MOTIVATION 1.1 INTRODUCTION Over the last decades, risk analysis and corporate risk management activities have become very important elements for both financial

Discount Rates in General Insurance Pricing

Discount Rates in General Insurance Pricing Peter Mulquiney, Brett Riley, Hugh Miller and Tim Jeffrey Peter Mulquiney, Brett Riley, Hugh Miller and Tim Jeffrey This presentation has been prepared for the

Discount Rates in General Insurance Pricing Peter Mulquiney, Brett Riley, Hugh Miller and Tim Jeffrey Peter Mulquiney, Brett Riley, Hugh Miller and Tim Jeffrey This presentation has been prepared for the

The impact of Solvency II regulation on the ability of insurance companies to provide long term financing: Issues for discussion

The impact of Solvency II regulation on the ability of insurance companies to provide long term financing: Issues for discussion Dario Focarelli Director General ANIA Member of the Advisory Scientific

The impact of Solvency II regulation on the ability of insurance companies to provide long term financing: Issues for discussion Dario Focarelli Director General ANIA Member of the Advisory Scientific

Solvency II Revealed. October 2011

Solvency II Revealed October 2011 Contents 4 An Optimal Insurer in a Post-Solvency II World 10 Changing the Landscape of Insurance Asset Strategy 16 Capital Relief Through Reinsurance 21 Natural Catastrophe

Solvency II Revealed October 2011 Contents 4 An Optimal Insurer in a Post-Solvency II World 10 Changing the Landscape of Insurance Asset Strategy 16 Capital Relief Through Reinsurance 21 Natural Catastrophe

Investment Risk Management Under New Regulatory Framework. Steven Yang Yu Muqiu Liu Redington Ltd

Investment Risk Management Under New Regulatory Framework Steven Yang Yu Muqiu Liu Redington Ltd 06 May 2015 Premiums written in billion RMB Dramatic growth of insurance market 2,500 Direct premium written

Investment Risk Management Under New Regulatory Framework Steven Yang Yu Muqiu Liu Redington Ltd 06 May 2015 Premiums written in billion RMB Dramatic growth of insurance market 2,500 Direct premium written

REVIEW OF QUEENSLAND'S COMPULSORY THIRD PARTY INSURANCE SCHEME'S UNDERWRITING MODEL. Consultation and Process of the Review

REVIEW OF QUEENSLAND'S COMPULSORY THIRD PARTY INSURANCE SCHEME'S UNDERWRITING MODEL Purpose of the Review On 25 March 2010, the Treasurer announced the Motor Accident Insurance Commission (MAIC) would

REVIEW OF QUEENSLAND'S COMPULSORY THIRD PARTY INSURANCE SCHEME'S UNDERWRITING MODEL Purpose of the Review On 25 March 2010, the Treasurer announced the Motor Accident Insurance Commission (MAIC) would

Liability Driven investment by insurers: Topmost priority

Global Journal of Finance and Management. ISSN 0975-6477 Volume 6, Number 5 (2014), pp. 397-402 Research India Publications http://www.ripublication.com Liability Driven investment by insurers: Topmost

Global Journal of Finance and Management. ISSN 0975-6477 Volume 6, Number 5 (2014), pp. 397-402 Research India Publications http://www.ripublication.com Liability Driven investment by insurers: Topmost

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

1 Introduction. 1.1 Three pillar approach

1 Introduction 1.1 Three pillar approach The recent years have shown that (financial) companies need to have a good management, a good business strategy, a good financial strength and a sound risk management

1 Introduction 1.1 Three pillar approach The recent years have shown that (financial) companies need to have a good management, a good business strategy, a good financial strength and a sound risk management

INSURANCE RATING METHODOLOGY

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

The CAPM (Capital Asset Pricing Model) NPV Dependent on Discount Rate Schedule

NPV Dependent on Discount Rate Schedule") The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

Modelling and Management of Tail Risk in Insurance

Modelling and Management of Tail Risk in Insurance IMF conference on operationalising systemic risk monitoring Peter Sohre, Head of Risk Reporting, Swiss Re Washington DC, 27 May 2010 Visit of ntuc ERM

Modelling and Management of Tail Risk in Insurance IMF conference on operationalising systemic risk monitoring Peter Sohre, Head of Risk Reporting, Swiss Re Washington DC, 27 May 2010 Visit of ntuc ERM

Das Risikokapitalmodell der Allianz Lebensversicherungs-AG

Das Risikokapitalmodell der Allianz s-ag Ulm 19. Mai 2003 Dr. Max Happacher Allianz s-ag Table of contents 1. Introduction: Motivation, Group-wide Framework 2. Internal Risk Model: Basics, Life Approach

Das Risikokapitalmodell der Allianz s-ag Ulm 19. Mai 2003 Dr. Max Happacher Allianz s-ag Table of contents 1. Introduction: Motivation, Group-wide Framework 2. Internal Risk Model: Basics, Life Approach

1. CFI Holdings is a conglomerate listed on the Zimbabwe Stock Exchange (ZSE) and has three operating divisions as follows:

and has three operating divisions as follows:") NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

Prudential Supervision of Insurance in Australia. Chris Lewis Immediate Past President

Prudential Supervision of Insurance in Australia Chris Lewis Immediate Past President REGULATORY FRAMEWORK RBA APRA ASIC ACCC Monetary Policy System Stability Payments System Prudential supervision - banks

Prudential Supervision of Insurance in Australia Chris Lewis Immediate Past President REGULATORY FRAMEWORK RBA APRA ASIC ACCC Monetary Policy System Stability Payments System Prudential supervision - banks

Effective Financial Planning for Life Insurance Companies

6 th Global Conference of Actuaries Effective Financial Planning for Life Insurance Companies Presentation by Kim Hoong CHIN Senior Manager and Consultant Asia Financial Services Topics Recent worldwide

6 th Global Conference of Actuaries Effective Financial Planning for Life Insurance Companies Presentation by Kim Hoong CHIN Senior Manager and Consultant Asia Financial Services Topics Recent worldwide

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

A Test Of The M&M Capital Structure Theories Richard H. Fosberg, William Paterson University, USA ABSTRACT Modigliani and Miller (1958, 1963) predict two very specific relationships between firm value

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Weaknesses in Regulatory Capital Models and Their Implications

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

Weaknesses in Regulatory Capital Models and Their Implications Amelia Ho, CA, CIA, CISA, CFE, ICBRR, PMP, MBA 2012 Enterprise Risk Management Symposium April 18-20, 2012 2012 Casualty Actuarial Society,

Financial Economics and Canadian Life Insurance Valuation

Report Financial Economics and Canadian Life Insurance Valuation Task Force on Financial Economics September 2006 Document 206103 Ce document est disponible en français 2006 Canadian Institute of Actuaries

Report Financial Economics and Canadian Life Insurance Valuation Task Force on Financial Economics September 2006 Document 206103 Ce document est disponible en français 2006 Canadian Institute of Actuaries

Capital Structure II

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Some Issues in Risk-Based Capital

The Geneva Papers on Risk and Insurance, 22 (No. 82, January 1997) 76-85 Some Issues in Risk-Based by G. M. Dickinson* Introduction Risk-based capital is employed in two different contexts. Firstly, it

The Geneva Papers on Risk and Insurance, 22 (No. 82, January 1997) 76-85 Some Issues in Risk-Based by G. M. Dickinson* Introduction Risk-based capital is employed in two different contexts. Firstly, it

GUIDELINE NO. 7 PENSION PLAN FUNDING POLICY GUIDELINE

GUIDELINE NO. 7 PENSION PLAN FUNDING POLICY GUIDELINE November 15, 2011 TABLE OF CONTENTS CONTEXT FOR THE GUIDELINE... 3 Pension Plan Funding Principles and Objectives... 3 Purpose of a Funding Policy...

GUIDELINE NO. 7 PENSION PLAN FUNDING POLICY GUIDELINE November 15, 2011 TABLE OF CONTENTS CONTEXT FOR THE GUIDELINE... 3 Pension Plan Funding Principles and Objectives... 3 Purpose of a Funding Policy...

2. Financial data. Financial data. 2.1 Balance sheet

2. Financial data 2.1 Balance sheet At the end of 2009 the aggregate total assets of all insurance and re-insurance entities under ACP supervision stood at EUR 1,822 billion at book value, corresponding

2. Financial data 2.1 Balance sheet At the end of 2009 the aggregate total assets of all insurance and re-insurance entities under ACP supervision stood at EUR 1,822 billion at book value, corresponding

A Shortcut to Calculating Return on Required Equity and It s Link to Cost of Capital

A Shortcut to Calculating Return on Required Equity and It s Link to Cost of Capital Nicholas Jacobi An insurance product s return on required equity demonstrates how successfully its results are covering

A Shortcut to Calculating Return on Required Equity and It s Link to Cost of Capital Nicholas Jacobi An insurance product s return on required equity demonstrates how successfully its results are covering

Counterparty Credit Risk for Insurance and Reinsurance Firms. Perry D. Mehta Enterprise Risk Management Symposium Chicago, March 2011

Counterparty Credit Risk for Insurance and Reinsurance Firms Perry D. Mehta Enterprise Risk Management Symposium Chicago, March 2011 Outline What is counterparty credit risk Relevance of counterparty credit

Counterparty Credit Risk for Insurance and Reinsurance Firms Perry D. Mehta Enterprise Risk Management Symposium Chicago, March 2011 Outline What is counterparty credit risk Relevance of counterparty credit

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

MM1 - The value of the firm is independent of its capital structure (the proportion of debt and equity used to finance the firm s operations).

.") Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Solvency II Standard Formula and NAIC Risk-Based Capital (RBC)

") Solvency II Standard Formula and NAIC Risk-Based Capital (RBC) Report 3 of the CAS Risk-Based Capital (RBC) Research Working Parties Issued by the RBC Dependencies and Calibration Working Party (DCWP)

Solvency II Standard Formula and NAIC Risk-Based Capital (RBC) Report 3 of the CAS Risk-Based Capital (RBC) Research Working Parties Issued by the RBC Dependencies and Calibration Working Party (DCWP)

Presented to the National Association of Insurance Commissioners Life Risk-Based Capital Working Group March 2001 Nashville, TN

Comments from the American Academy of Actuaries Life-Risk Based Capital Committee on a Letter Commenting Upon the Proposed Change to the Treatment of Common Stock in the Life Risk-Based Capital Formula

Comments from the American Academy of Actuaries Life-Risk Based Capital Committee on a Letter Commenting Upon the Proposed Change to the Treatment of Common Stock in the Life Risk-Based Capital Formula

Discounted Cash Flow. Alessandro Macrì. Legal Counsel, GMAC Financial Services

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

COLLECTION & PUBLICATION OF GENERAL INSURANCE STATISTICS AN OVERVIEW OF REGULATORY BEST PRACTICE. Win-Li Toh 20 November 2014

COLLECTION & PUBLICATION OF GENERAL INSURANCE STATISTICS AN OVERVIEW OF REGULATORY BEST PRACTICE Win-Li Toh 20 November 2014 What we ll cover today A potted history of regulation: Australia, NZ, US, Canada

COLLECTION & PUBLICATION OF GENERAL INSURANCE STATISTICS AN OVERVIEW OF REGULATORY BEST PRACTICE Win-Li Toh 20 November 2014 What we ll cover today A potted history of regulation: Australia, NZ, US, Canada

The Discount Rate: A Note on IAS 36

The Discount Rate: A Note on IAS 36 Sven Husmann Martin Schmidt Thorsten Seidel European University Viadrina Frankfurt (Oder) Department of Business Administration and Economics Discussion Paper No. 246

The Discount Rate: A Note on IAS 36 Sven Husmann Martin Schmidt Thorsten Seidel European University Viadrina Frankfurt (Oder) Department of Business Administration and Economics Discussion Paper No. 246

Risk management. Objectives The Group has five objectives for risk and capital management:

Philosophy, principles and objectives Philosophy As a provider of financial services, including insurance, the Group s business is the managed acceptance of risk. Prudential believes that effective risk

Philosophy, principles and objectives Philosophy As a provider of financial services, including insurance, the Group s business is the managed acceptance of risk. Prudential believes that effective risk

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA Abstract This paper summarises the work done in this area by various parties,

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA Abstract This paper summarises the work done in this area by various parties,

3/22/2010. Chapter 11. Eight Categories of Bank Regulation. Economic Analysis of. Regulation Lecture 1. Asymmetric Information and Bank Regulation

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

Chapter 11 Economic Analysis of Banking Regulation Lecture 1 Asymmetric Information and Bank Regulation Adverse Selection and Moral Hazard are the two concepts that underlie government regulation of the

cost of capital, 01 technical this measurement of a company s cost of equity THere are two ways of estimating the cost of equity (the return

01 technical cost of capital, THere are two ways of estimating the cost of equity (the return required by shareholders). Can this measurement of a company s cost of equity be used as the discount rate

01 technical cost of capital, THere are two ways of estimating the cost of equity (the return required by shareholders). Can this measurement of a company s cost of equity be used as the discount rate

SCHEDULE TO INSURANCE GROUP SUPERVISION AMENDMENT RULES 2015 SCHEDULE 3 (Paragraph 30) SCHEDULE OF FINANCIAL CONDITION REPORT OF INSURANCE GROUP [blank] name of Parent The schedule of Financial Condition

SCHEDULE TO INSURANCE GROUP SUPERVISION AMENDMENT RULES 2015 SCHEDULE 3 (Paragraph 30) SCHEDULE OF FINANCIAL CONDITION REPORT OF INSURANCE GROUP [blank] name of Parent The schedule of Financial Condition

Evolution in Government Supervision of the General Insurance Industry

Evolution in Government Supervision of the General Insurance Industry PNG Insurance Director Forum October 2013 Mark Hurst Contents Overview of PNG Industry Evolution of Government Supervision Supervision

Evolution in Government Supervision of the General Insurance Industry PNG Insurance Director Forum October 2013 Mark Hurst Contents Overview of PNG Industry Evolution of Government Supervision Supervision

Modelling operational risk in the insurance industry

April 2011 N 14 Modelling operational risk in the insurance industry Par Julie Gamonet Centre d études actuarielles Winner of the French «Young Actuaries Prize» 2010 Texts appearing in SCOR Papers are

April 2011 N 14 Modelling operational risk in the insurance industry Par Julie Gamonet Centre d études actuarielles Winner of the French «Young Actuaries Prize» 2010 Texts appearing in SCOR Papers are

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

What s wrong with modern capital budgeting?

What s wrong with modern capital budgeting? René M. Stulz Address delivered at the Eastern Finance Association meeting in Miami Beach, April 1999, upon reception of the 1999 Eastern Finance Association

What s wrong with modern capital budgeting? René M. Stulz Address delivered at the Eastern Finance Association meeting in Miami Beach, April 1999, upon reception of the 1999 Eastern Finance Association

The Risk Premium Project (RPP) Update - RPP II Report. Casualty Actuarial Society Committee on Theory of Risk

Update - RPP II Report. Casualty Actuarial Society Committee on Theory of Risk") The Risk Premium Project (RPP) Update - RPP II Report Casualty Actuarial Society Committee on Theory of Risk Authors: Martin Eling, University of Ulm, Germany Hato Schmeiser, University of St. Gallen,

The Risk Premium Project (RPP) Update - RPP II Report Casualty Actuarial Society Committee on Theory of Risk Authors: Martin Eling, University of Ulm, Germany Hato Schmeiser, University of St. Gallen,

On the Applicability of WACC for Investment Decisions

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products

for Sanlam Life Participating Annuity Products") Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products Table of Contents Section 1 - Information 1.1 Background 2 1.2 Purpose

Sanlam Life Insurance Limited Principles and Practices of Financial Management (PPFM) for Sanlam Life Participating Annuity Products Table of Contents Section 1 - Information 1.1 Background 2 1.2 Purpose