SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

|

|

|

- Alfred Long

- 7 years ago

- Views:

Transcription

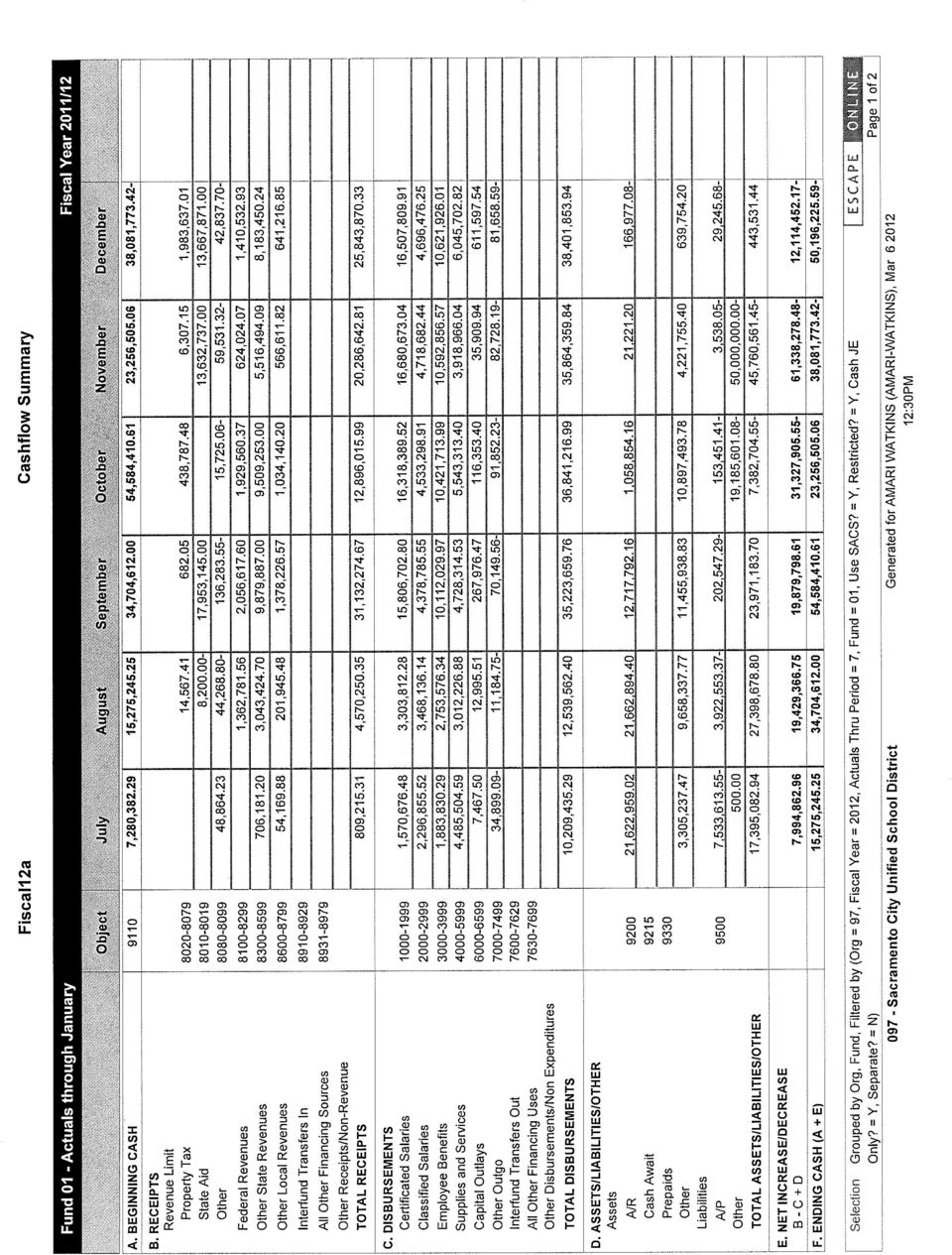

1 SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item#. Meeting Date: March 15, 2012 Subject: Business and Financial Information Information Item Only Approval on Consent Agenda Conference (for discussion only) Conference/First Reading (Action Anticipated: ) Conference/Action Action Public Hearing Division: Administrative Services Recommendation: Receive business and financial information. Background/Rationale: Cash Flow Report for the Period Ending January 31, 2012 Financial Considerations: Reflects standard business information.. Documents Attached: 1a. Executive Summary: Cash Flow Report for the Period Ending January 31, b. Cash Flow Report for the Period Ending January 31, 2012 Estimated Time of Presentation: N/A Submitted by: Patricia A Hagemeyer, Chief Business Officer Approved by: Jonathan P. Raymond, Superintendent

2 Board of Education Executive Summary Administrative Services Approve Cash Flow Report for the Period Ending January 31, 2012 March 15, 2012 I. Overview/History: School districts in California have suffered devastating reductions in funding over the past several years. Cash reserves for most districts are low and Sacramento City Unified School District is no exception. The continued deferral of state revenues has impacted the district to the extent that staff project a negative cash flow in the General Fund by June 30, The review of cash flows have become more important than ever. At the January Board meeting, a request by the Board was made to review system generated cash flow reports. Sample reports were brought to prior Board meetings. This is the first cash flow report brought forward as an information item under the Business and Financial section of the Board agenda. Staff will provide a cash flow report at the second Board meeting of every month. The report is mostly self-explanatory. Receipts indicate cash that the district has received for the revenue limit, federal, state and local funds as well as transfers in from other funds. Disbursements reflect actual payments for salaries and benefits, supplies and services, capital outlay, interfund transfers out and other financing uses. Assets include accounts receivables which are funds owed to the general fund, prepaid expenditures and other types of assets. Liabilities include accounts payable which are funds that the district owes to other entities and other liabilities. An example of other liabilities is the repayment of the Tax Revenue Anticipation Notes (TRAN) in November for $50 million. The most important line to focus on is the ending cash bottom line. That reflects whether the district has sufficient cash to meet its needs or if we need to rely on other sources for cash. It has been normal in previous years to have deficits in November and December as the district awaits property tax revenues. Without the TRAN, the district would not have had sufficient cash in the earlier months of II. Driving Governance: III. Budget: Request by Board of Education to receive monthly cash flow reports. It is important to note that cash information is not the same as budget information. While the district may have a budget set up for a particular program, and funds may be expended, it is possible that the district hasn t yet received the cash from the granting agency. However, the majority of our cash issues are due to the deferral of state funds, which make up the majority of our overall revenues. Administrative Services 1

3 Board of Education Executive Summary Administrative Services Approve Cash Flow Report for the Period Ending January 31, 2012 March 15, 2012 IV. Goals, Objectives and Measures: Provide cash flow information to the Board. In addition, this report provides information related to the need for a borrowing instrument, such as a TRAN as a source of cash. Throughout the discussion of the district s financial plan, staff along with the district s financial advisor from KNN, have closely monitored cash and the Board recently approved the issuance of a TRAN. The Sacramento County Office of Education reviews cash flow information to ensure that the district is able to pay its bills on June 30, V. Major Initiatives: VI. Results: Maintain positive cash flow through June 30, Continuous review of financial options available to the district. Continuous review of cash flow information will inform the Board and public of cash flow issues. VII. Lessons Learned/Next Steps: Cash flow reports will be provided monthly to the Board as an information item. Administrative Services 2

4

5

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: November 7, 2013 Agenda Item# Subject: Approve the Submission of a Credential Waiver Application to the California Commission on

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: November 7, 2013 Agenda Item# Subject: Approve the Submission of a Credential Waiver Application to the California Commission on

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: September 17, 2015 Agenda Item 10.5 Subject: Approve the Declaration of Need for Fully Qualified Educators for the 2015-2016 School

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: September 17, 2015 Agenda Item 10.5 Subject: Approve the Declaration of Need for Fully Qualified Educators for the 2015-2016 School

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: Agenda Item # 10.3 Subject: Information Item Only Approval on Consent Agenda Conference (for discussion only) Conference/First Reading

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Meeting Date: Agenda Item # 10.3 Subject: Information Item Only Approval on Consent Agenda Conference (for discussion only) Conference/First Reading

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# 9.1a Meeting Date: January 22, 2015 Subject: Approval of Grants, Entitlements, and Other Income Agreements Ratification of Other

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# 9.1a Meeting Date: January 22, 2015 Subject: Approval of Grants, Entitlements, and Other Income Agreements Ratification of Other

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# Meeting Date: October 18, 2012 Subject: Grants, Entitlements, and Other Income Agreements Ratification of Other Agreements Approval

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# Meeting Date: October 18, 2012 Subject: Grants, Entitlements, and Other Income Agreements Ratification of Other Agreements Approval

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# Meeting Date: July 18, 2013 Subject: Approve Grants, Entitlements, and Other Income Agreements Ratification of Other Agreements Approval

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# Meeting Date: July 18, 2013 Subject: Approve Grants, Entitlements, and Other Income Agreements Ratification of Other Agreements Approval

A Special Presentation for the Orange County Department of Education

A Special Presentation for the Orange County Department of Education October 19, 2009 Presented By: Ann Hern Director, Management Consulting Services School Services of California, Inc. Debi Deal Fiscal

A Special Presentation for the Orange County Department of Education October 19, 2009 Presented By: Ann Hern Director, Management Consulting Services School Services of California, Inc. Debi Deal Fiscal

Capital Projects Funds. Chapter 7

Capital Projects Funds Chapter 7 Learning Objectives Understand nature of and when to use CPFs Understand typical CPF financing sources, how many CPFs are required, and life cycle of CPF Determine costs

Capital Projects Funds Chapter 7 Learning Objectives Understand nature of and when to use CPFs Understand typical CPF financing sources, how many CPFs are required, and life cycle of CPF Determine costs

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item # 9.1f Meeting Date: November 15, 2012 Subject: Ratification of Superintendent Contract Information Item Only Approval on Consent

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item # 9.1f Meeting Date: November 15, 2012 Subject: Ratification of Superintendent Contract Information Item Only Approval on Consent

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# 12.1

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# 12.1 Meeting Date: June 4, 2015 Subject: Resolution No. 2845: Ethnic Studies Resolution Information Item Only Approval on Consent

SACRAMENTO CITY UNIFIED SCHOOL DISTRICT BOARD OF EDUCATION Agenda Item# 12.1 Meeting Date: June 4, 2015 Subject: Resolution No. 2845: Ethnic Studies Resolution Information Item Only Approval on Consent

A. For completed projects, determine total final costs. Develop or Review Project Budget

Date: June 4, 2012 To: David E. Cash, Superintendent From: David J. Hetyonk, Director of Facilities & Operations Re: Approval of Program Management Agreement with TELACU Construction Management for Program

Date: June 4, 2012 To: David E. Cash, Superintendent From: David J. Hetyonk, Director of Facilities & Operations Re: Approval of Program Management Agreement with TELACU Construction Management for Program

Chapter 3. Adjusting the accounts. Appendix 3A: An alternative method of recording deferrals

1 Chapter 3 Adjusting the accounts Appendix 3A: An alternative method of recording deferrals 2 Learning objectives 1. Prepare adjusting entries for prepaid expenses originally recorded in an expense account

1 Chapter 3 Adjusting the accounts Appendix 3A: An alternative method of recording deferrals 2 Learning objectives 1. Prepare adjusting entries for prepaid expenses originally recorded in an expense account

BUSINESS PLAN. 2012-2013 Florida Virtual School Academy. 14. Facilities If the site is not secured.

III. BUSINESS PLAN 14. Facilities If the site is not secured. F. Explain the school s facility needs, including desired location, size, and layout of space. The financial plan for the proposed school should

III. BUSINESS PLAN 14. Facilities If the site is not secured. F. Explain the school s facility needs, including desired location, size, and layout of space. The financial plan for the proposed school should

HOSPITALS: WORKING CAPITAL ADVANCES. Contents. I. Introduction 1. II. Source of Working Capital Advances 1. III. Maximum Line of Credit 1

ACCOUNTING MANUAL HOSPITALS: WORKING CAPITAL HOSPITALS: WORKING CAPITAL ADVANCES Contents Page I. Introduction 1 II. Source of Working Capital Advances 1 III. Maximum Line of Credit 1 IV. Interest on Working

ACCOUNTING MANUAL HOSPITALS: WORKING CAPITAL HOSPITALS: WORKING CAPITAL ADVANCES Contents Page I. Introduction 1 II. Source of Working Capital Advances 1 III. Maximum Line of Credit 1 IV. Interest on Working

City of Amsterdam. Records and Reports. Report of Examination. Thomas P. DiNapoli. Period Covered: June 1, 2011 March 31, 2013 2013M-266

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY City of Amsterdam Records and Reports Report of Examination Period Covered: June 1, 2011 March 31, 2013 2013M-266

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY City of Amsterdam Records and Reports Report of Examination Period Covered: June 1, 2011 March 31, 2013 2013M-266

The Responsibility of the Board of Education in Managing School District Fiscal Fitness. 2013 New York State School Boards Association, Latham NY

The Responsibility of the Board of Education in Managing School District Fiscal Fitness Develop Fiscal Policies and Procedures Legal Required by law Education General Municipal NYCRR Local Contractual

The Responsibility of the Board of Education in Managing School District Fiscal Fitness Develop Fiscal Policies and Procedures Legal Required by law Education General Municipal NYCRR Local Contractual

BERGER LEWIS ACCOUNTANCY CORPORATION San Jose, California November 8, 2012 - 2 -

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The NeighborWorks America - schedules, City of San Jose - HomeVenture Fund - Lending - schedules, and

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The NeighborWorks America - schedules, City of San Jose - HomeVenture Fund - Lending - schedules, and

SKAGIT COUNTY DEBT POLICY. Page 1 of 12

SKAGIT COUNTY DEBT POLICY Page 1 of 12 SKAGIT COUNTY DEBT POLICY INDEX Page I. Roles and Responsibilities 3 II. Debt and Capital Planning 3-4 III. Credit Objectives 4-5 IV. Purpose, Type and Use of Debt

SKAGIT COUNTY DEBT POLICY Page 1 of 12 SKAGIT COUNTY DEBT POLICY INDEX Page I. Roles and Responsibilities 3 II. Debt and Capital Planning 3-4 III. Credit Objectives 4-5 IV. Purpose, Type and Use of Debt

TRUST AND AGENCY FUNDS

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

T OOL 5. Monitoring and Projecting Cash Flow. Hector Noriega. Monthly Cash Flow Statement

T OOL 5 Monitoring and Projecting Cash Flow Hector Noriega Monthly Cash Flow Statement The cash flow statement reports the cash inflows and cash outflows of an institution during a set period. It indicates

T OOL 5 Monitoring and Projecting Cash Flow Hector Noriega Monthly Cash Flow Statement The cash flow statement reports the cash inflows and cash outflows of an institution during a set period. It indicates

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

Chapter Four. Accounting for Governmental Operating Activities Illustrative Transactions and Financial Statements

Chapter Four Accounting for Governmental Operating Activities Illustrative Transactions and Financial Statements Learning Objectives After studying this chapter, you should be able to: 1. Analyze typical

Chapter Four Accounting for Governmental Operating Activities Illustrative Transactions and Financial Statements Learning Objectives After studying this chapter, you should be able to: 1. Analyze typical

Role of Financial Advisors

Local School Finance Emporium Financial Advisor What You Need to Know May 2012 Keygent LLC 999 N. Sepulveda Blvd., Suite 570 El Segundo, CA 90245 (310) 322 4222 Role of Financial Advisors A financial advisor

Local School Finance Emporium Financial Advisor What You Need to Know May 2012 Keygent LLC 999 N. Sepulveda Blvd., Suite 570 El Segundo, CA 90245 (310) 322 4222 Role of Financial Advisors A financial advisor

Oakland Unified School District. Annual Financial Report

Oakland Unified School District Annual Financial Report June 30, 2015 TABLE OF CONTENTS JUNE 30, 2015 FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial

Oakland Unified School District Annual Financial Report June 30, 2015 TABLE OF CONTENTS JUNE 30, 2015 FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial

The Roles of. for School District Public Financing

The Roles of Finance Team Members for School District Public Financing presented by Adam Bauer, Principal i Fieldman, Rolapp & Associates (949) 660-7303 (949) 295-5735 abauer@fieldman.com FRA127653 Presenter:

The Roles of Finance Team Members for School District Public Financing presented by Adam Bauer, Principal i Fieldman, Rolapp & Associates (949) 660-7303 (949) 295-5735 abauer@fieldman.com FRA127653 Presenter:

CALIFORNIA SCHOOL ACCOUNTING MANUAL

CALIFORNIA SCHOOL ACCOUNTING MANUAL 2013 EDITION APPROVED BY THE CALIFORNIA STATE BOARD OF EDUCATION PUBLISHED BY THE CALIFORNIA DEPARTMENT OF EDUCATION SACRAMENTO, 2013 This page intentionally left blank.

CALIFORNIA SCHOOL ACCOUNTING MANUAL 2013 EDITION APPROVED BY THE CALIFORNIA STATE BOARD OF EDUCATION PUBLISHED BY THE CALIFORNIA DEPARTMENT OF EDUCATION SACRAMENTO, 2013 This page intentionally left blank.

CITY OF DES MOINES, IOWA BALANCE SHEET GOVERNMENTAL FUNDS June 30, 2013

CITY OF DES MOINES, IOWA BALANCE SHEET GOVERNMENTAL FUNDS June 30, 2013 ASSETS DEBT TAX GENERAL SERVICE INCREMENT Cash and investments $ 13,823,153 $ 577,744 $ --- Taxes receivable 57,403,960 30,488,253

CITY OF DES MOINES, IOWA BALANCE SHEET GOVERNMENTAL FUNDS June 30, 2013 ASSETS DEBT TAX GENERAL SERVICE INCREMENT Cash and investments $ 13,823,153 $ 577,744 $ --- Taxes receivable 57,403,960 30,488,253

Board of Supervisors February 10, 2000 Page 2. Summary of Findings

Board of Supervisors February 10, 2000 Page 2 Summary of Findings We have questioned a total of $37,320 in expenditures made by GHS. Of this amount, $24,863 represents disbursements that were undocumented

Board of Supervisors February 10, 2000 Page 2 Summary of Findings We have questioned a total of $37,320 in expenditures made by GHS. Of this amount, $24,863 represents disbursements that were undocumented

FUND BALANCE WHITE PAPER. Illinois Association of School Business Officials (Illinois ASBO)

") FUND BALANCE WHITE PAPER Illinois Association of School Business Officials (Illinois ASBO) This paper outlines the nuances and complexities in the definition of school district fund balances from an audit

FUND BALANCE WHITE PAPER Illinois Association of School Business Officials (Illinois ASBO) This paper outlines the nuances and complexities in the definition of school district fund balances from an audit

Regulations Governing Literary Loan Applications in Virginia

VR270-01-0009 Department of Education (State Board of Education) Regulations Governing Literary Loan Applications in Virginia 1.1. Policy. PART I POLICY It is the policy of the Board of Education to assist

VR270-01-0009 Department of Education (State Board of Education) Regulations Governing Literary Loan Applications in Virginia 1.1. Policy. PART I POLICY It is the policy of the Board of Education to assist

WESTCHESTER PUBLIC LIBRARY BUDGET FINANCE AND PURCHASING POLICIES

WESTCHESTER PUBLIC LIBRARY BUDGET FINANCE AND PURCHASING POLICIES THE BUDGET PROCESS The public library budgeting process is prescribed by law and overseen by the Indiana Department of Local Government

WESTCHESTER PUBLIC LIBRARY BUDGET FINANCE AND PURCHASING POLICIES THE BUDGET PROCESS The public library budgeting process is prescribed by law and overseen by the Indiana Department of Local Government

For personal use only

ASX RELEASE 21 March 2012 Market Update February 2012 The Report on Cash Flows for the month of February 2012, provided in accordance with Listing Rule 4.7B(d), is attached. Debt Facility The Company confirms

ASX RELEASE 21 March 2012 Market Update February 2012 The Report on Cash Flows for the month of February 2012, provided in accordance with Listing Rule 4.7B(d), is attached. Debt Facility The Company confirms

RESOLUTION NO. 14-047 THE EDUCATION PROTECTION ACCOUNT

RESOLUTION NO. 14-047 THE EDUCATION PROTECTION ACCOUNT WHEREAS, the voters approved Proposition 30 on November 6, 2012; WHEREAS, Proposition 30 added Article XIII, Section 36 to the California Constitution

RESOLUTION NO. 14-047 THE EDUCATION PROTECTION ACCOUNT WHEREAS, the voters approved Proposition 30 on November 6, 2012; WHEREAS, Proposition 30 added Article XIII, Section 36 to the California Constitution

Michigan Area Loan Information

FIRST MORTGAGE LOAN APPLICATION Full Corporate Name of Church Street Address City, State, Zip Pastor Church Phone: Date of Application Pastor s Home Phone: Primary Contact Person regarding this application:

FIRST MORTGAGE LOAN APPLICATION Full Corporate Name of Church Street Address City, State, Zip Pastor Church Phone: Date of Application Pastor s Home Phone: Primary Contact Person regarding this application:

REQUEST FOR PROPOSALS. For FINANCIAL ADVISORY SERVICES

REQUEST FOR PROPOSALS For FINANCIAL ADVISORY SERVICES Request for Proposals Issued: July 30, 2012 Deadline for Submittal of Proposals: August 17, 2012 Request for Proposals for Financial Advisory Services

REQUEST FOR PROPOSALS For FINANCIAL ADVISORY SERVICES Request for Proposals Issued: July 30, 2012 Deadline for Submittal of Proposals: August 17, 2012 Request for Proposals for Financial Advisory Services

NEW CONSTRUCTION BP 7214. General Obligation Bonds. I-Facilities

NEW CONSTRUCTION General Obligation Bonds I-Facilities The Governing Board recognizes that school facilities are an essential component of the educational program and that the Board has a responsibility

NEW CONSTRUCTION General Obligation Bonds I-Facilities The Governing Board recognizes that school facilities are an essential component of the educational program and that the Board has a responsibility

STUDENTS LOAN APPLICATION FORM 2016/17

STUDENTS LOAN APPLICATION FORM 2016/17 No payment shall be made to any individual for purposes of securing this student loan. Attach 3 passport photographs * TO BE COMPLETED BY ALL STUDENTS APPLYING FOR

STUDENTS LOAN APPLICATION FORM 2016/17 No payment shall be made to any individual for purposes of securing this student loan. Attach 3 passport photographs * TO BE COMPLETED BY ALL STUDENTS APPLYING FOR

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division DATE: September 15, 2015 TO: FROM: American Express Business Cardholders District Provided V. Luis

INTER-OFFICE CORRESPONDENCE Los Angeles Unified School District Accounting and Disbursements Division DATE: September 15, 2015 TO: FROM: American Express Business Cardholders District Provided V. Luis

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

CHAPTER II GENERAL LEDGER ACCOUNTS

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

CHAPTER II GENERAL LEDGER ACCOUNTS A general ledger is basic to an accounting system. The General Ledger of a fund is a summary record containing the balance of assets, liabilities, deferred revenues,

CONRAD, MONTANA FINANCIAL REPORT. June 30, 2014

FINANCIAL REPORT June 30, 2014 C O N T E N T S PAGE ORGANIZATION - ADVISORY BOARD MEMBER SCHOOLS AND DIRECTOR...1 INDEPENDENT AUDITOR S REPORT... 2 through 4 MANAGEMENT S DISCUSSION AND ANALYSIS... 5 through

FINANCIAL REPORT June 30, 2014 C O N T E N T S PAGE ORGANIZATION - ADVISORY BOARD MEMBER SCHOOLS AND DIRECTOR...1 INDEPENDENT AUDITOR S REPORT... 2 through 4 MANAGEMENT S DISCUSSION AND ANALYSIS... 5 through

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

6. It lengthened its payables period, thereby shortening its cash cycle.

Answers to Concepts Review and Critical Thinking Questions 1. These are firms with relatively long inventory periods and/or relatively long receivables periods. Thus, such firms tend to keep inventory

Answers to Concepts Review and Critical Thinking Questions 1. These are firms with relatively long inventory periods and/or relatively long receivables periods. Thus, such firms tend to keep inventory

Revised January 2005 PUBLISHED BY THE

ACCOUNTING AND FINANCIAL REPORTING FOR LOANS BETWEEN CALIFORNIA CITIES AND RELATED REDEVELOPMENT AGENCIES Revised January 2005 PUBLISHED BY THE CALIFORNIA COMMITTEE ON MUNICIPAL ACCOUNTING (a joint committee

ACCOUNTING AND FINANCIAL REPORTING FOR LOANS BETWEEN CALIFORNIA CITIES AND RELATED REDEVELOPMENT AGENCIES Revised January 2005 PUBLISHED BY THE CALIFORNIA COMMITTEE ON MUNICIPAL ACCOUNTING (a joint committee

Mechanics of a School District Budget

Mechanics of a School District Budget A Guide to Understanding the Illinois School District Budget Process Illinois State Board of Education Revised May 2015 James T. Meeks, Chairman Illinois State Board

Mechanics of a School District Budget A Guide to Understanding the Illinois School District Budget Process Illinois State Board of Education Revised May 2015 James T. Meeks, Chairman Illinois State Board

The University Of California Home Loan Program Corporation (A Component Unit of the University of California)

") Report Of Independent Auditors And Financial Statements The University Of California Home Loan Program Corporation (A Component Unit of the University of California) As of and for the periods ended June

Report Of Independent Auditors And Financial Statements The University Of California Home Loan Program Corporation (A Component Unit of the University of California) As of and for the periods ended June

THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan

Enclosure V.I. THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan AGENDA NUMBER & TITLE: V.I. Approval of Bank Line of Credit Borrowing for 2012-2013 BACKGROUND INFORMATION: The School district

Enclosure V.I. THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan AGENDA NUMBER & TITLE: V.I. Approval of Bank Line of Credit Borrowing for 2012-2013 BACKGROUND INFORMATION: The School district

CALIFORNIA SCHOOL FINANCE AUTHORITY CHARTER SCHOOL REVOLVING LOAN FUND PROGRAM LOAN AGREEMENT NUMBER 14-2014

CALIFORNIA SCHOOL FINANCE AUTHORITY CHARTER SCHOOL REVOLVING LOAN FUND PROGRAM LOAN AGREEMENT NUMBER 14-2014 East Bay Innovation Academy CDS CODE: TBD CHARTER NUMBER 1620 3400 Malcolm Ave, Oakland CA 94605

CALIFORNIA SCHOOL FINANCE AUTHORITY CHARTER SCHOOL REVOLVING LOAN FUND PROGRAM LOAN AGREEMENT NUMBER 14-2014 East Bay Innovation Academy CDS CODE: TBD CHARTER NUMBER 1620 3400 Malcolm Ave, Oakland CA 94605

WASHINGTON UNIVERSITY SCHOOL OF LAW NEW LOAN REPAYMENT ASSISTANCE PROGRAM (LRAP II) (Last updated: January 19, 2015) I INTRODUCTION

(Last updated: January 19, 2015) I INTRODUCTION") WASHINGTON UNIVERSITY SCHOOL OF LAW NEW LOAN REPAYMENT ASSISTANCE PROGRAM (LRAP II) (Last updated: January 19, 2015) I INTRODUCTION To help law students who want to secure employment in low paying public

WASHINGTON UNIVERSITY SCHOOL OF LAW NEW LOAN REPAYMENT ASSISTANCE PROGRAM (LRAP II) (Last updated: January 19, 2015) I INTRODUCTION To help law students who want to secure employment in low paying public

CHAPTER 7 General Journal Entries

CHAPTER 7 Journal Entries Table of Contents Section Page INTRODUCTION 1 1 GENERAL FUND JOURNAL ENTRIES 2 1 Opening Entry... 1 Budget Entries... 2 Budget Entries Modifications... 2 Revenues Property Tax...

CHAPTER 7 Journal Entries Table of Contents Section Page INTRODUCTION 1 1 GENERAL FUND JOURNAL ENTRIES 2 1 Opening Entry... 1 Budget Entries... 2 Budget Entries Modifications... 2 Revenues Property Tax...

FINANCIAL STATEMENTS OF KDD CENTRAL SECURITIES CLEARING CORPORATION (KDD)

") FINANCIAL STATEMENTS OF KDD CENTRAL SECURITIES CLEARING CORPORATION (KDD) for the year ended December 31, 2013 (abbreviated) Ljubljana, February 2014 Boris Tomaž Šnuderl President and CEO Davor Pavić Deputy

FINANCIAL STATEMENTS OF KDD CENTRAL SECURITIES CLEARING CORPORATION (KDD) for the year ended December 31, 2013 (abbreviated) Ljubljana, February 2014 Boris Tomaž Šnuderl President and CEO Davor Pavić Deputy

2012-13 Annual Debt Report. Business Services January 21, 2014. For the Period Ending June 30, 2013. 2012-13 Annual Debt Report.

2012-13 Annual Debt Report For the Period Ending June 30, 2013 Business Services January 21, 2014 2012-13 Annual Debt Report. 2012-13 Annual Debt Report Page intentionally left blank. TABLE OF CONTENTS

2012-13 Annual Debt Report For the Period Ending June 30, 2013 Business Services January 21, 2014 2012-13 Annual Debt Report. 2012-13 Annual Debt Report Page intentionally left blank. TABLE OF CONTENTS

San Leandro Unified School District

San Leandro Unified School District Bond Program Update March 5, 2013 Presented by Ruth Alahydoian KNN Public Finance Ralahydoian@knninc.com Kurt Weidmann Harris & Associates Kweidmann@harris-asoc.com

San Leandro Unified School District Bond Program Update March 5, 2013 Presented by Ruth Alahydoian KNN Public Finance Ralahydoian@knninc.com Kurt Weidmann Harris & Associates Kweidmann@harris-asoc.com

Small Business Development Loan Program (SBDLP)

") Washington County Economic Growth Partnership, Inc. Small Business Development Loan Program (SBDLP) Application 1707 N Shelby Street, Suite 109 Salem, IN 47167 812-883-8803 812-883-8739 FAX E-mail: sabrina.burdine@wcegp.org

Washington County Economic Growth Partnership, Inc. Small Business Development Loan Program (SBDLP) Application 1707 N Shelby Street, Suite 109 Salem, IN 47167 812-883-8803 812-883-8739 FAX E-mail: sabrina.burdine@wcegp.org

SAFEGUARDING ASSOCIATED STUDENT BODY FUNDS CHECKING ON BALANCES

2005-2006 SANTA CLARA COUNTY CIVIL GRAND JURY REPORT SAFEGUARDING ASSOCIATED STUDENT BODY FUNDS CHECKING ON BALANCES Summary The 2005-2006 Santa Clara County Civil Grand Jury (Grand Jury) reviewed the

2005-2006 SANTA CLARA COUNTY CIVIL GRAND JURY REPORT SAFEGUARDING ASSOCIATED STUDENT BODY FUNDS CHECKING ON BALANCES Summary The 2005-2006 Santa Clara County Civil Grand Jury (Grand Jury) reviewed the

5.9 SPECIAL CONSTRUCTION ACCOUNTS STATE TRANSPORTATION BONDS (OPTIONAL ENTRIES) NARRATIVE

NARRATIVE") 5.9 STATE TRANSPORTATION BONDS (OPTIONAL ENTRIES) NARRATIVE When a State Bond Grant has been awarded, the county has the option to set up a State Bond Grant and State Bond Deferred Revenue Accounts. These

5.9 STATE TRANSPORTATION BONDS (OPTIONAL ENTRIES) NARRATIVE When a State Bond Grant has been awarded, the county has the option to set up a State Bond Grant and State Bond Deferred Revenue Accounts. These

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

GENEVA HOUSE, INC. PROJECT NO. 034-44815NP FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND 2008 FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31,

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND 2008 FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31,

PREPARATION for a BUSINESS PLAN

PREPARATION for a BUSINESS PLAN Successful small business expansions and new small business creations lead the way in sustaining existing jobs, forming new jobs, creating new markets and innovations that

PREPARATION for a BUSINESS PLAN Successful small business expansions and new small business creations lead the way in sustaining existing jobs, forming new jobs, creating new markets and innovations that

AD VALOREM TAX ADOPTED BUDGET

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

AD VALOREM TAX ADOPTED BUDGET AGGREGATE TAX RATE AMENDMENT APPROPRIATION ASSESSED VALUE BALANCE FORWARD BALANCE FORWARD - CAPITAL A tax levied on the assessed value of real property (also known as "property

Cash Flow Analysis. 15.511 Corporate Accounting Summer 2004. Professor SP Kothari. Sloan School of Management Massachusetts Institute of Technology

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

Cash Flow Analysis 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 16, 2004 1 Statement of Cash Flows Reports operating

LLC Operating Agreement With Corporate Structure (Delaware)

") LLC Operating Agreement With Corporate Structure (Delaware) Document 1080B www.leaplaw.com Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc.

LLC Operating Agreement With Corporate Structure (Delaware) Document 1080B www.leaplaw.com Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc.

Huron University College. Financial Statements April 30, 2012

Financial Statements April 30, June 27, Independent Auditor s Report To the Executive Board of Huron University College We have audited the accompanying financial statements of Huron University College,

Financial Statements April 30, June 27, Independent Auditor s Report To the Executive Board of Huron University College We have audited the accompanying financial statements of Huron University College,

Hammock Bay Community Development District

Hammock Bay Community Development District FINANCIAL STATEMENTS September 30, 2015 Table of Contents September 30, 2015 REPORT Independent Auditors' Report 1 FINANCIAL STATEMENTS Management s Discussion

Hammock Bay Community Development District FINANCIAL STATEMENTS September 30, 2015 Table of Contents September 30, 2015 REPORT Independent Auditors' Report 1 FINANCIAL STATEMENTS Management s Discussion

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

County of Los Angeles School District General Obligation Bonds White Paper

County of Los Angeles School District General Obligation Bonds White Paper California s Coalition for Adequate School Housing s Fall Conference Tuesday, October 18, 2011 Presented by: Donald Field, Esq.

County of Los Angeles School District General Obligation Bonds White Paper California s Coalition for Adequate School Housing s Fall Conference Tuesday, October 18, 2011 Presented by: Donald Field, Esq.

Computing the Total Assets, Liabilities, and Owner s Equity

21-1 Assets are the total of your cash, the items that you have purchased, and any money that your customers owe you. Liabilities are the total amount of money that you owe to creditors. Owner s equity,

21-1 Assets are the total of your cash, the items that you have purchased, and any money that your customers owe you. Liabilities are the total amount of money that you owe to creditors. Owner s equity,

PROGRAMME COORDINATING BOARD. Financial and Budgetary Matters

3 May 1999 PROGRAMME COORDINATING BOARD Eighth meeting Geneva, 27-28 June 1999 Provisional agenda item 5.2 Financial and Budgetary Matters UNAIDS Operating Reserve Fund 3 May 1999 PROGRAMME COORDINATING

3 May 1999 PROGRAMME COORDINATING BOARD Eighth meeting Geneva, 27-28 June 1999 Provisional agenda item 5.2 Financial and Budgetary Matters UNAIDS Operating Reserve Fund 3 May 1999 PROGRAMME COORDINATING

Financial Statements December 31, 2014 and 2013 Josephine Commons, LLC

Financial Statements Josephine Commons, LLC www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations and Members Equity...

Financial Statements Josephine Commons, LLC www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations and Members Equity...

CHAPTER 7 General Journal Entries

CHAPTER 7 Journal Entries Table of Contents Section - Page INTRODUCTION 1-1 GENERAL FUND JOURNAL ENTRIES 2-1 Opening Entry...2-1 Budget Entries...2-2 Budget Entries Modifications...2-2 Revenues Property

CHAPTER 7 Journal Entries Table of Contents Section - Page INTRODUCTION 1-1 GENERAL FUND JOURNAL ENTRIES 2-1 Opening Entry...2-1 Budget Entries...2-2 Budget Entries Modifications...2-2 Revenues Property

CITY OF MADISON TAX INCREMENTAL DISTRICT NO. 41 Madison, Wisconsin

Madison, Wisconsin FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2013 and From the Date of Creation Through December 31, 2013 TABLE OF CONTENTS As of December 31, 2013

Madison, Wisconsin FINANCIAL STATEMENTS Including Independent Auditors' Report As of December 31, 2013 and From the Date of Creation Through December 31, 2013 TABLE OF CONTENTS As of December 31, 2013

FUND ACCOUNTING VS. EQUITY METHOD OF REPORTING WHICH ONE IS RIGHT FOR YOU?

Financial statements for a homeowners association may be presented using either the Fund Accounting Method of Reporting or the Equity Method of Reporting. Both methods are permitted (when properly formatted)

Financial statements for a homeowners association may be presented using either the Fund Accounting Method of Reporting or the Equity Method of Reporting. Both methods are permitted (when properly formatted)

MINISTRY OF ADVANCED EDUCATION

The mission of the Ministry of Advanced Education and Minister Responsible for Research and Technology is to realize the economic, environmental, cultural and social goals of all British Columbians by

The mission of the Ministry of Advanced Education and Minister Responsible for Research and Technology is to realize the economic, environmental, cultural and social goals of all British Columbians by

State and Local Government Accounting Principles. Chapter 2

State and Local Government Accounting Principles Chapter 2 Learning Objectives Discuss major aspects of government financial reporting model Define fund and examine broad categories Identify MFBA found

State and Local Government Accounting Principles Chapter 2 Learning Objectives Discuss major aspects of government financial reporting model Define fund and examine broad categories Identify MFBA found

Unaudited Actuals Charter Schools Enterprise Fund Expenses by Object

A. REVENUES 1) Revenue Limit Sources 8010-8099 2,430,393.56 3,750,106.00 54.3% 2) Federal Revenue 8100-8299 302,327.54 461,689.25 52.7% 3) Other State Revenue 8300-8599 984,557.86 1,500,453.12 52.4% 4)

A. REVENUES 1) Revenue Limit Sources 8010-8099 2,430,393.56 3,750,106.00 54.3% 2) Federal Revenue 8100-8299 302,327.54 461,689.25 52.7% 3) Other State Revenue 8300-8599 984,557.86 1,500,453.12 52.4% 4)

Homer Township Midland County, Michigan. Financial Statements

Homer Township Midland County, Michigan ================================ Financial Statements TOWNSHIP OFFICIALS OFFICERS Barbara Radosa, Supervisor Ken Schlafley, Clerk Albert Tew, Treasurer TRUSTEES

Homer Township Midland County, Michigan ================================ Financial Statements TOWNSHIP OFFICIALS OFFICERS Barbara Radosa, Supervisor Ken Schlafley, Clerk Albert Tew, Treasurer TRUSTEES

Chapter 21: Chart of Accounts

Chapter 21: Chart of s GAAP ACCOUNTING FOR NON-PROFITS... 100 ing Basis for Churches... 150 TYPICAL FUNDS... 200 CHART OF ACCOUNTS... 400 EXPENDITURES... 500 EXPENSE ACCOUNT CLASSIFICATIONS... 600 CHART

Chapter 21: Chart of s GAAP ACCOUNTING FOR NON-PROFITS... 100 ing Basis for Churches... 150 TYPICAL FUNDS... 200 CHART OF ACCOUNTS... 400 EXPENDITURES... 500 EXPENSE ACCOUNT CLASSIFICATIONS... 600 CHART

ESTATES AT CHERRY LAKE COMMUNITY DEVELOPMENT DISTRICT LAKE COUNTY, FLORIDA FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015

ESTATES AT CHERRY LAKE COMMUNITY DEVELOPMENT DISTRICT LAKE COUNTY, FLORIDA FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015 ESTATES AT CHERRY LAKE COMMUNITY DEVELOPMENT DISTRICT LAKE COUNTY,

ESTATES AT CHERRY LAKE COMMUNITY DEVELOPMENT DISTRICT LAKE COUNTY, FLORIDA FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015 ESTATES AT CHERRY LAKE COMMUNITY DEVELOPMENT DISTRICT LAKE COUNTY,

February 14, 2014. Dear Mr. John Renner and Members of the Board of Fire Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 14, 2014 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 14, 2014 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

A CITIZEN S GUIDE TO THE FEDERAL BUDGET

A CITIZEN S GUIDE TO THE FEDERAL BUDGET BUDGET OF THE UNITED STATES GOVERNMENT Fiscal Year 2001 to a projected 11 percent for 2001 Continuing surplus will reduce these interest

A CITIZEN S GUIDE TO THE FEDERAL BUDGET BUDGET OF THE UNITED STATES GOVERNMENT Fiscal Year 2001 to a projected 11 percent for 2001 Continuing surplus will reduce these interest

Preparing cash budgets

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare

FRASER VALLEY REGIONAL DISTRICT CONSOLIDATED FINANCIAL STATEMENTS

FRASER VALLEY REGIONAL DISTRICT CONSOLIDATED FINANCIAL STATEMENTS December 31, 2014 Consolidated Financial Statements December 31, 2014 Management's Responsibility for the Consolidated Financial Statements

FRASER VALLEY REGIONAL DISTRICT CONSOLIDATED FINANCIAL STATEMENTS December 31, 2014 Consolidated Financial Statements December 31, 2014 Management's Responsibility for the Consolidated Financial Statements

LAKEWOOD RANCH STEWARDSHIP DISTRICT AUDITED FINANCIAL STATEMENTS. FOR THE FISCAL YEAR ENDED September 30, 2013

AUDITED FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED September 30, 2013 FOR THE FISCAL YEAR ENDED September 30, 2013 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 2 MANAGEMENT S DISCUSSION AND

AUDITED FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED September 30, 2013 FOR THE FISCAL YEAR ENDED September 30, 2013 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 2 MANAGEMENT S DISCUSSION AND

Business Plan. In completing the following proposal provide as much detailed information as possible.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

Business Plan A business plan is an integral part of a financing request. It is an introduction to your business, and it provides us with the initial information that we require to start to an application.

May 31 Hilton Indianapolis North June 12 Huntingburg Event Center June 19 Fort Wayne Holiday Inn at IPFW June 20 Munster Centennial Park Clubhouse

2012 Annual Budget Workshop May 31 Hilton Indianapolis North June 12 Huntingburg Event Center June 19 Fort Wayne Holiday Inn at IPFW June 20 Munster Centennial Park Clubhouse Budget Tools 2 Appropriations

2012 Annual Budget Workshop May 31 Hilton Indianapolis North June 12 Huntingburg Event Center June 19 Fort Wayne Holiday Inn at IPFW June 20 Munster Centennial Park Clubhouse Budget Tools 2 Appropriations

State Cashflow Management

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Following is a summary of financial statement position of School Lane Charter School for the period ending May 31, 2016.

TO: Board of Trustees DATE: June 9, 2016 RE: May 31, 2016 Financial Statements Following is a summary of financial statement position of School Lane Charter School for the period ending May 31, 2016. Balance

TO: Board of Trustees DATE: June 9, 2016 RE: May 31, 2016 Financial Statements Following is a summary of financial statement position of School Lane Charter School for the period ending May 31, 2016. Balance

FINANCIAL STATEMENTS REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR KEOTA INDEPENDENT SCHOOL DISTRICT NO. I-43, HASKELL COUNTY, OKLAHOMA

FINANCIAL STATEMENTS REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR KEOTA INDEPENDENT SCHOOL DISTRICT NO. I-43, HASKELL COUNTY, OKLAHOMA JUNE 30, 2015 Audited by SANDERS, BLEDSOE & HEWETT CERTIFIED

FINANCIAL STATEMENTS REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR KEOTA INDEPENDENT SCHOOL DISTRICT NO. I-43, HASKELL COUNTY, OKLAHOMA JUNE 30, 2015 Audited by SANDERS, BLEDSOE & HEWETT CERTIFIED

ANNUAL FINANCIAL REPORT

ANNUAL FINANCIAL REPORT CITY OF PALMDALE, CALIFORNIA HOUSING AUTHORITY For the Fiscal Year Ended June 30, 2011 THIS PAGE LEFT BLANK INTENTIONALLY ANNUAL FINANCIAL REPORT JUNE 30, 2011 TABLE OF CONTENTS

ANNUAL FINANCIAL REPORT CITY OF PALMDALE, CALIFORNIA HOUSING AUTHORITY For the Fiscal Year Ended June 30, 2011 THIS PAGE LEFT BLANK INTENTIONALLY ANNUAL FINANCIAL REPORT JUNE 30, 2011 TABLE OF CONTENTS

Community Unit School District 220 4:40 Page 1 of 5

Page 1 of 5 DEBT MANAGEMENT The policies set forth in this Debt Management Policy (the Policy ) have been developed to provide guidelines relative to the issuance, sale, statutory compliance, and investment

Page 1 of 5 DEBT MANAGEMENT The policies set forth in this Debt Management Policy (the Policy ) have been developed to provide guidelines relative to the issuance, sale, statutory compliance, and investment

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ANNUAL TAX LEVY PACKET

ANNUAL TAX LEVY PACKET OF THE OREGON PARK DISTRICT FOR THE 2013 TAX YEAR We Create Fun for a Lifetime OREGON PARK DISTRICT ANNUAL TAX LEVY PACKET FOR THE 2013 TAX YEAR CONTENTS 2012 Tax Year District Statement

ANNUAL TAX LEVY PACKET OF THE OREGON PARK DISTRICT FOR THE 2013 TAX YEAR We Create Fun for a Lifetime OREGON PARK DISTRICT ANNUAL TAX LEVY PACKET FOR THE 2013 TAX YEAR CONTENTS 2012 Tax Year District Statement

Appendix 4C. Quarterly report for entities admitted on the basis of commitments BIOTRON LIMITED. Quarter ended ( current quarter )

") Appendix 4C Rule 4.7B Introduced 31/03/00 Amended 30/09/01, 24/10/05, 17/12/10 Quarterly report for entities admitted on the basis of commitments Name of entity BIOTRON LIMITED ABN Quarter ended ( current

Appendix 4C Rule 4.7B Introduced 31/03/00 Amended 30/09/01, 24/10/05, 17/12/10 Quarterly report for entities admitted on the basis of commitments Name of entity BIOTRON LIMITED ABN Quarter ended ( current

Control Debt Use Credit Wisely

Lesson 10 Control Debt Use Credit Wisely Lesson Description In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities

Lesson 10 Control Debt Use Credit Wisely Lesson Description In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities

THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan

Enclosure V.F. THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan AGENDA NUMBER & TITLE: V.F. Approval of Bank Line of Credit Borrowing for 2013-14 BACKGROUND INFORMATION: The School district

Enclosure V.F. THE GROSSE POINTE PUBLIC SCHOOL SYSTEM Grosse Pointe, Michigan AGENDA NUMBER & TITLE: V.F. Approval of Bank Line of Credit Borrowing for 2013-14 BACKGROUND INFORMATION: The School district

Richland County Tourism Commission Guidelines for Tourism Event Sponsorship Grants

Richland County Tourism Commission Guidelines for Tourism Event Sponsorship Grants I. Purpose The purpose of this grant program is to support tourism in Richland County. Events that generate paid overnight

Richland County Tourism Commission Guidelines for Tourism Event Sponsorship Grants I. Purpose The purpose of this grant program is to support tourism in Richland County. Events that generate paid overnight

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

APPENDIX 1: A5 Management Discussion and Analysis

APPENDIX 1: A5 Management Discussion and Analysis General overview Objectives The Department of Education and Training (the Department) works in partnership with the community to provide sustainable, high

APPENDIX 1: A5 Management Discussion and Analysis General overview Objectives The Department of Education and Training (the Department) works in partnership with the community to provide sustainable, high

Be it enacted by the People of the State of Illinois,

AN ACT concerning education. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The School Code is amended by changing Section 17-17 and by adding Sections

AN ACT concerning education. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The School Code is amended by changing Section 17-17 and by adding Sections

How To Account For School Money

PART 6 6-1 CLASSIFICATION AND DEFINITION OF CLEARING ACCOUNTS CLASSIFICATION OF CLEARING ACCOUNTS In an accounting system maintained on a cash basis, it becomes necessary to establish certain ledger accounts

PART 6 6-1 CLASSIFICATION AND DEFINITION OF CLEARING ACCOUNTS CLASSIFICATION OF CLEARING ACCOUNTS In an accounting system maintained on a cash basis, it becomes necessary to establish certain ledger accounts