STATE OF NEVADA DEPARTMENT OF TAXATION CONSTRUCTION

|

|

|

- Adelia Jennings

- 7 years ago

- Views:

Transcription

1 STATE OF NEVADA DEPARTMENT OF TAXATION CONSTRUCTION

2 Includes any person who acts solely in a professional capacity to improve real property by NAC

3 The following are included in this group: NAC

4 The term does NOT include: An employee A licensed architect A licensed professional engineer A manufacturer of Modular homes Sectionalized housing Prefabricated homes NAC (1)

5 Construction Contract A construction contract for improvement to real property is a contract for erecting constructing affixing a structure to real property affixing other improvement on or to real property remodeling Altering NAC (2) Adding or repairing an improvement to real property

6 Construction Contract»May be formal or informal»advertised contracts»negotiated contracts Fixed price contracts Cost reimbursable contracts Lump-sum contracts Time and material contracts NAC (2)

7 Application of Tax A construction contractor is considered a consumer of all tangible personal property purchased for use in improving real property. A construction contractor is required to pay the tax on all material purchases that will be used in the construction job. NAC

8 Government Contracts»Tangible personal property purchased by a contractor for use in a government job is subject to the tax. NAC (1)

9 Government Contracts A contractor may not enter into a contract for a public work claiming to be a constituent part of the governmental entity which sponsors or finances the public work. A contract for a public work may be entered into provided that the contract requires the payment of any state/local taxes that would normally be due had the contract not been with a tax-exempt entity. (AB 332, 2015 Legislation Session, effective 7/1/2015)

10 Government Contracts If the public body is going to perform the public work itself, it is not required to pay any local or state taxes for the purchase and use of construction materials or goods. (AB 332, 2015 Legislation Session, effective 7/1/2015

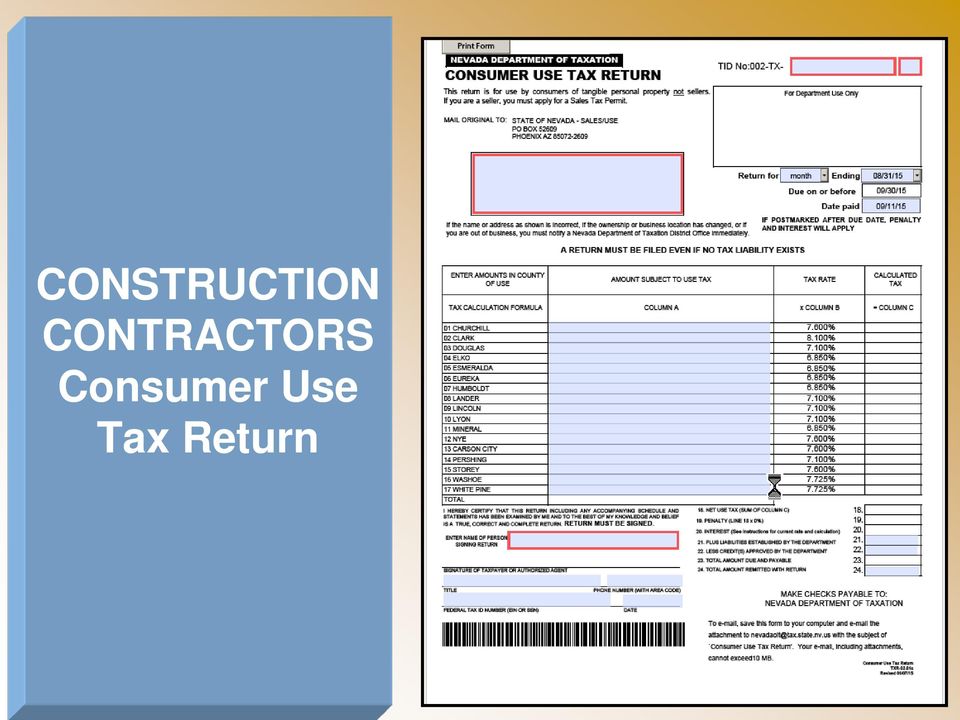

11 CONSTRUCTION CONTRACTORS Consumer Use Tax Return

12 Change in Sales Tax Rate Construction contractors bid future jobs which include the current sales tax rate When the sales tax rate changes. the construction contractor can apply for an exemption from the increased tax rate. Contractors must complete a Contract Summary Form and submit to the Department. Once approved, the contractor will be required to self-report the use tax at the former tax rate. Complete instructions and the form are available on the Department of Taxation s website under Common Forms. NRS 377B.110(6)

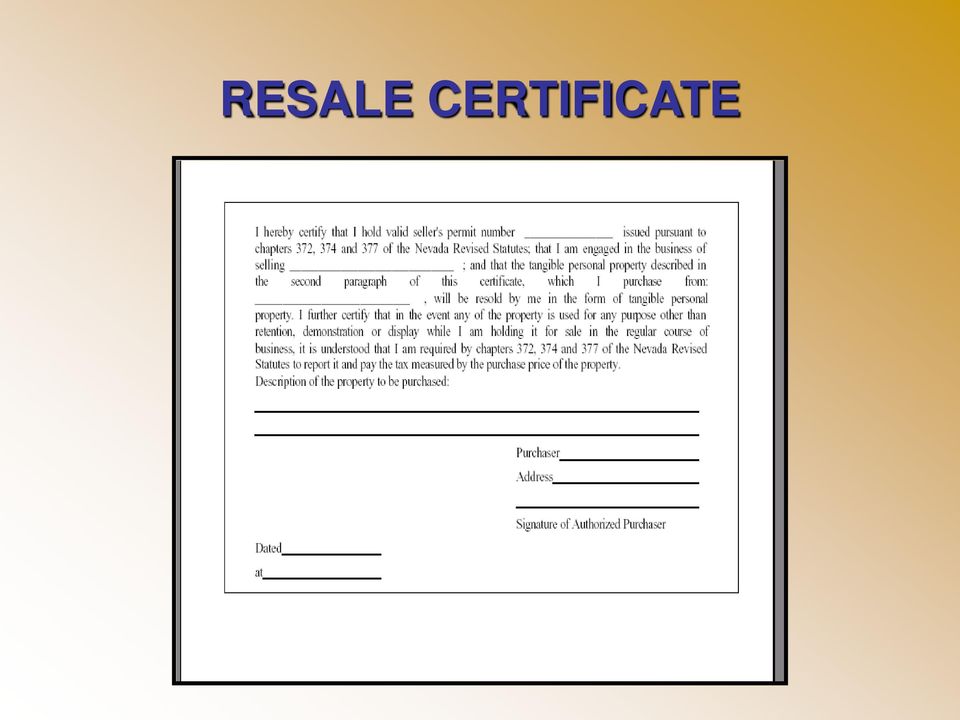

13 Resale Certificates A construction contractor may be registered as a retailer As a retailer, the contractor may use a resale certificate for purchases, and report the tax when the materials are used in a job or sold at retail. A retailer construction contractor may NOT use a resale certificate for purchases of tools or supplies which are used in the trade.

14 RESALE CERTIFICATE

15 Fabrication Labor Fabrication labor is labor which results in the creation of tangible personal property. Fabrication labor is taxable in a retail sale where no installation to real property is involved. A contract for improvement to real property which includes fabrication and installation is not considered a retail transaction; the contractor is liable for tax on the materials only in such a transaction. NAC

16 Purchases out of State Materials purchased out of state and delivered to Nevada for a Nevada job are subject to Nevada tax. Tax legitimately paid to other state is honored by Nevada; however, if the other state tax rate is lower than the Nevada rate, the difference is due to Nevada NRS , NAC

17 RECORDS TO BE KEPT Purchase invoices Sales journals General ledgers Job files Other records»must keep records for four (4) years NRS

18 Written Response Most tax issues can be addressed by the Department of Taxation. Please be advised that any responses to inquires made to the Department are only binding if put in writing, such as Nevada Revised Statutes, Administrative Code, Nevada Tax Notes, or in written correspondence.

19 DEPARTMENT OF TAXATION Contact Information Our offices are open Monday-Friday 8:00 AM 5:00 PM Contact our Call Center at Southern Nevada: Grant Sawyer Office Building 555 E. Washington Avenue Suite 1300 Las Vegas, NV OR 2550 Paseo Verde Parkway Suite 180 Henderson, NV Carson City: 1550 College Parkway Suite 115 Carson City, NV Reno: 4600 Kietzke Lane Building L, Suite 235 Reno, NV 89502

LAWS GOVERNING AUTO INDUSTRY

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

Automobile LAWS GOVERNING AUTO INDUSTRY Two of the main chapters of the Nevada Revised Statutes and Nevada Administrative Code discussed today are: Chapter 372: Sales and Use Taxes Chapter 482: Motor Vehicles

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

Department of Taxation

Department of Taxation Commerce Tax Presentation Deonne E. Contine, Executive Director Sumiko Maser, Chief Deputy Executive Director Paulina Oliver, Deputy Executive Director What do I need to do to determine

Department of Taxation Commerce Tax Presentation Deonne E. Contine, Executive Director Sumiko Maser, Chief Deputy Executive Director Paulina Oliver, Deputy Executive Director What do I need to do to determine

NEVADA TAX NOTES Official Newsletter of the Department of Taxation

N E V A D A D E P A R T M E N T O F T A X A T I O N NEVADA TAX NOTES Official Newsletter of the Department of Taxation OCTOBER 2012 h t t p : / /www.t a x. s t a t e. n v. u s ISSUE NO. 180 Register, File

N E V A D A D E P A R T M E N T O F T A X A T I O N NEVADA TAX NOTES Official Newsletter of the Department of Taxation OCTOBER 2012 h t t p : / /www.t a x. s t a t e. n v. u s ISSUE NO. 180 Register, File

STEP ONE: Create a Corporation, Limited Liability Company, Partnership or Sole Proprietorship Legal Organization

LICENSING & PERMITS VIRGINIA CITY AND STOREY COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings necessary for business operations in Lyon

LICENSING & PERMITS VIRGINIA CITY AND STOREY COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings necessary for business operations in Lyon

LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY

www.nsbdc.org (800) 240-7094 LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description

www.nsbdc.org (800) 240-7094 LICENSING & PERMITS IN LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description

NEVADA TAX NOTES NEVADA DEPARTMENT OF TAXATION * * * Official Newsletter of the Department of Taxation DEPARTMENT OF TAXATION OFFICES

NEVADA DEPARTMENT OF TAXATION NEVADA TAX NOTES Official Newsletter of the Department of Taxation JULY 2010 h t t p : / / t a x. s t a t e. n v. u s ISSUE NO. 171 DEPARTMENT OF TAXATION OFFICES CALL CENTER

NEVADA DEPARTMENT OF TAXATION NEVADA TAX NOTES Official Newsletter of the Department of Taxation JULY 2010 h t t p : / / t a x. s t a t e. n v. u s ISSUE NO. 171 DEPARTMENT OF TAXATION OFFICES CALL CENTER

City of Elko Business License Application 1751 College Ave. Elko, NV 89801 Phone (775)777-7138 Fax (775)777-7129 Email: buslic@ci.elko.nv.

777-7138 Fax (775)777-7129 Email: buslic@ci.elko.nv.") City of Elko Business License Application 1751 College Ave. Elko, NV 89801 Phone (775)777-7138 Fax (775)777-7129 Email: buslic@ci.elko.nv.us Welcome to your new business venture in the City of Elko! This

City of Elko Business License Application 1751 College Ave. Elko, NV 89801 Phone (775)777-7138 Fax (775)777-7129 Email: buslic@ci.elko.nv.us Welcome to your new business venture in the City of Elko! This

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 12-19 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 12-19 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 12-19 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

STATE OF NEVADA FIRST AMENDED NOTICE OF INTENT TO ACT UPON A PROPOSED PERMANENT REGULATION R013-15

BRIAN SANDOVAL Governor KATERI CARRAHER Interim Executive Officer STATE OF NEVADA PUBLIC EMPLOYEES BENEFITS PROGRAM 901 S. Stewart Street, Suite 1001 Carson City, Nevada 89701 Telephone (775) 684-7000

BRIAN SANDOVAL Governor KATERI CARRAHER Interim Executive Officer STATE OF NEVADA PUBLIC EMPLOYEES BENEFITS PROGRAM 901 S. Stewart Street, Suite 1001 Carson City, Nevada 89701 Telephone (775) 684-7000

SALES AND USE TAX TECHNICAL BULLETINS SECTION 17

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

SECTION 17 - NONPROFIT ENTITIES - HOSPITALS, EDUCATIONAL INSTITUTIONS, CHURCHES, ORPHANAGES AND OTHER CHARITABLE OR RELIGIOUS INSTITUTIONS AND ORGANIZATIONS AND QUALIFIED RETIREMENT FACILITIES WHOSE PROPERTY

Sales and Use Tax on Building Contractors

Sales and Use Tax on Building Contractors GT-800007 R. 03/15 Definitions Fabrication Cost The cost to a real property contractor to fabricate an item. This cost includes direct materials, labor, and other

Sales and Use Tax on Building Contractors GT-800007 R. 03/15 Definitions Fabrication Cost The cost to a real property contractor to fabricate an item. This cost includes direct materials, labor, and other

This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.

ST 08-0176-GIL 12/10/2008 SERVICE OCCUPATION TAX This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.) December 10, 2008

ST 08-0176-GIL 12/10/2008 SERVICE OCCUPATION TAX This letter concerns tangible personal property transferred incident to sales of service. See 86 Ill. Adm. Code 140.01. (This is a GIL.) December 10, 2008

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 04-20 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

Sales and Use Tax on Construction, Improvements, Installations and Repairs

Sales and Use Tax on Construction, Improvements, Installations and Repairs GT-800067 R.09/14 In Florida, the taxing of property improvements, installation, and repairs varies according to the exact nature

Sales and Use Tax on Construction, Improvements, Installations and Repairs GT-800067 R.09/14 In Florida, the taxing of property improvements, installation, and repairs varies according to the exact nature

S&U-8 Alarm Systems. Rev. 8/99

S&U-8 Alarm Systems Introduction Sales and installations of alarm and security systems such as burglar and fire alarms are generally taxable in New Jersey. However, the sales tax requirements differ based

S&U-8 Alarm Systems Introduction Sales and installations of alarm and security systems such as burglar and fire alarms are generally taxable in New Jersey. However, the sales tax requirements differ based

Sales and Use Tax Treatment of Construction Contractors Throughout the States

Sales and Use Tax Treatment of Construction Contractors Throughout the States by Dan Davis, MBA (Tax), CPA, CFE Construction: General Rule Although the wording may differ from state to state, a construction

Sales and Use Tax Treatment of Construction Contractors Throughout the States by Dan Davis, MBA (Tax), CPA, CFE Construction: General Rule Although the wording may differ from state to state, a construction

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

STATE OF NEVADA OFFICE OF THE ATTORNEY GENERAL PRIVATE INVESTIGATORS LICENSING BOARD

CATHERINE CORTEZ MASTO Attorney General STATE OF NEVADA OFFICE OF THE ATTORNEY GENERAL PRIVATE INVESTIGATORS LICENSING BOARD 3476 Executive Pointe Way, Suite 14 Carson City, Nevada 89706 MECHELE RAY Executive

CATHERINE CORTEZ MASTO Attorney General STATE OF NEVADA OFFICE OF THE ATTORNEY GENERAL PRIVATE INVESTIGATORS LICENSING BOARD 3476 Executive Pointe Way, Suite 14 Carson City, Nevada 89706 MECHELE RAY Executive

Office of Tax Policy Analysis Technical Services Division June 24, 2005

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S031121A

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S031121A

PROPOSED REGULATION OF THE TAXICAB AUTHORITY OF THE DEPARTMENT OF BUSINESS AND INDUSTRY. LCB File No. R003-16

PROPOSED REGULATION OF THE TAXICAB AUTHORITY OF THE DEPARTMENT OF BUSINESS AND INDUSTRY LCB File No. R003-16 NOTICE OF THE AGENDA FOR WORKSHOP TO SOLICIT COMMENTS ON PROPOSED REGULATIONS - LEASING TAXICABS

PROPOSED REGULATION OF THE TAXICAB AUTHORITY OF THE DEPARTMENT OF BUSINESS AND INDUSTRY LCB File No. R003-16 NOTICE OF THE AGENDA FOR WORKSHOP TO SOLICIT COMMENTS ON PROPOSED REGULATIONS - LEASING TAXICABS

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S890817A On August

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S890817A On August

ST 10-0035-GIL 04/19/2010 CONSTRUCTION CONTRACTORS

ST 10-0035-GIL 04/19/2010 CONSTRUCTION CONTRACTORS When a construction contractor permanently affixes tangible personal property to real property, the contractor is deemed the end user of that tangible

ST 10-0035-GIL 04/19/2010 CONSTRUCTION CONTRACTORS When a construction contractor permanently affixes tangible personal property to real property, the contractor is deemed the end user of that tangible

SALT Whitepapers. Definition of Contractor

Business Strategists Certified Public Accountants Echelbarger, Himebaugh, Tamm & Co., P.C. SALT Whitepapers The application of the Michigan Sales Tax and the Michigan Use Tax to construction contractors

Business Strategists Certified Public Accountants Echelbarger, Himebaugh, Tamm & Co., P.C. SALT Whitepapers The application of the Michigan Sales Tax and the Michigan Use Tax to construction contractors

ST 13-0021-GIL 04/30/2013 SERVICE OCCUPATION TAX

04/30/2013 SERVICE OCCUPATION TAX The Service Occupation Tax is a tax imposed upon servicemen engaged in the business of making sales of service in this State, based on the tangible personal property transferred

04/30/2013 SERVICE OCCUPATION TAX The Service Occupation Tax is a tax imposed upon servicemen engaged in the business of making sales of service in this State, based on the tangible personal property transferred

Real Estate. Office Help and Other Services. Commissions. South Dakota Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501

South Dakota Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 Real Estate July 2013 This Tax Facts is designed to explain how sales and use tax applies to Real Estate Brokers' commissions

South Dakota Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 Real Estate July 2013 This Tax Facts is designed to explain how sales and use tax applies to Real Estate Brokers' commissions

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

Businesses Qualifying for Chapter 100 Financing

Businesses Qualifying for Chapter 100 Financing MUNICIPALITIES AND BUSINESSES aa Pursuant to Section 536.010(6)(c)RSMo, this document is an intergovernmental memorandum developed to provide guidance to

Businesses Qualifying for Chapter 100 Financing MUNICIPALITIES AND BUSINESSES aa Pursuant to Section 536.010(6)(c)RSMo, this document is an intergovernmental memorandum developed to provide guidance to

Georgia Sales and Use Tax Issues For Nonprofits Organizations. April 14, 2009

Georgia Sales and Use Tax Issues For Nonprofits Organizations April 14, 2009 Overview Application of Sales/Use Taxes to Nonprofits Scope of Sales/Use Taxes in General Potential Exemptions/Exclusions From

Georgia Sales and Use Tax Issues For Nonprofits Organizations April 14, 2009 Overview Application of Sales/Use Taxes to Nonprofits Scope of Sales/Use Taxes in General Potential Exemptions/Exclusions From

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT In support of business and economic development, the State of Nevada and its units of local government endeavor to maintain fair competition, promote growth,

BUSINESS ENTITIES AND ECONOMIC DEVELOPMENT In support of business and economic development, the State of Nevada and its units of local government endeavor to maintain fair competition, promote growth,

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

INFORMATION BULLETIN #10 SALES TAX APRIL 2012. (Replaces Bulletin #10 dated June 2008)

") INFORMATION BULLETIN #10 SALES TAX APRIL 2012 (Replaces Bulletin #10 dated June 2008) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the general public.

INFORMATION BULLETIN #10 SALES TAX APRIL 2012 (Replaces Bulletin #10 dated June 2008) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the general public.

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 S 1 SENATE BILL 870. Short Title: Refine Sales & Use Tax on RMI. (Public)

") GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S 1 SENATE BILL 0 Short Title: Refine Sales & Use Tax on RMI. (Public) Sponsors: Referred to: Senators Rucho, Rabon, Tillman (Primary Sponsors); and Ford. Finance

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION S 1 SENATE BILL 0 Short Title: Refine Sales & Use Tax on RMI. (Public) Sponsors: Referred to: Senators Rucho, Rabon, Tillman (Primary Sponsors); and Ford. Finance

Revenue Ruling No. 10-003 November 10, 2010 Sales Tax Oil and Gas Well Fracturing Services Purpose The purpose of this Revenue Ruling is to provide

Revenue Ruling No. 10-003 Sales Tax Oil and Gas Well Fracturing Services Purpose The purpose of this Revenue Ruling is to provide guidance to Department of Revenue employees and taxpayers to clarify the

Revenue Ruling No. 10-003 Sales Tax Oil and Gas Well Fracturing Services Purpose The purpose of this Revenue Ruling is to provide guidance to Department of Revenue employees and taxpayers to clarify the

SALES AND USE TAX TECHNICAL BULLETINS SECTION 18

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

SECTION 18 - CERTAIN GOVERNMENTAL ENTITIES - THE STATE, COUNTIES, CITIES AND OTHER POLITICAL SUBDIVISIONS 18-1 PURCHASES AND SALES BY AND DONATIONS TO GOVERNMENTAL ENTITIES A. Purchases By Governmental

PROPOSED REGULATION OF THE STATE BOARD OF COSMETOLOGY. LCB File No. R064-15

PROPOSED REGULATION OF THE STATE BOARD OF COSMETOLOGY LCB File No. R064-15 Main Office: Branch Office: 1785 E. Sahara Avenue, Suite 255 4600 Kietzke Lane, Building O, Suite 262 Las Vegas, NV 89104 Reno,

PROPOSED REGULATION OF THE STATE BOARD OF COSMETOLOGY LCB File No. R064-15 Main Office: Branch Office: 1785 E. Sahara Avenue, Suite 255 4600 Kietzke Lane, Building O, Suite 262 Las Vegas, NV 89104 Reno,

North Carolina Department of Revenue

DIRECTIVE Subject: Real Property Contracts Tax: Sales and Use Tax Law: N.C. Gen. Stat. 105-164.4(a)(13) & 105-164.4H Issued By: Sales and Use Tax Division Date: March 17, 2015 Number: SD-15-1 This directive

DIRECTIVE Subject: Real Property Contracts Tax: Sales and Use Tax Law: N.C. Gen. Stat. 105-164.4(a)(13) & 105-164.4H Issued By: Sales and Use Tax Division Date: March 17, 2015 Number: SD-15-1 This directive

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-29 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

A Consumer s Guide To Hiring

NEVADA STATE BOARD OF ARCHITECTURE, INTERIOR DESIGN AND RESIDENTIAL DESIGN A Consumer s Guide To Hiring Architects Residential Designers Registered Interior Designers TABLE OF CONTENTS INTRODUCTION...

NEVADA STATE BOARD OF ARCHITECTURE, INTERIOR DESIGN AND RESIDENTIAL DESIGN A Consumer s Guide To Hiring Architects Residential Designers Registered Interior Designers TABLE OF CONTENTS INTRODUCTION...

Florida Department of Revenue. Repair of Tangible Personal Property Standard Industry Guide

Florida Department of Revenue Repair of Tangible Personal Property Standard Industry Guide PURPOSE This guide provides an auditor with information on the subject industry. This information will assist

Florida Department of Revenue Repair of Tangible Personal Property Standard Industry Guide PURPOSE This guide provides an auditor with information on the subject industry. This information will assist

Taxpayer Services Division Technical Services Bureau

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau Exemption for Certain Precious Metal Bullion Effective September 1, 1989, precious metal bullion sold

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau Exemption for Certain Precious Metal Bullion Effective September 1, 1989, precious metal bullion sold

STATE OF NEVADA. Department of Employment, Training and Rehabilitation EMPLOYMENT SECURITY DIVISION 500 E. Third Street Carson City, Nevada 89713-0001

STATE OF NEVADA Brian Sandoval Governor Don Soderberg Director Renee Olson Administrator Department of Employment, Training and Rehabilitation EMPLOYMENT SECURITY DIVISION 500 E. Third Street Carson City,

STATE OF NEVADA Brian Sandoval Governor Don Soderberg Director Renee Olson Administrator Department of Employment, Training and Rehabilitation EMPLOYMENT SECURITY DIVISION 500 E. Third Street Carson City,

A Short Summary on What You Can Do to Improve Your Home Business

NOTICE OF INTENT TO ACT UPON A REGULATION Notice of Public Hearing for the Adoption of Proposed New Regulations The Nevada Governor s Office of Economic Development will hold a public hearing at 1:30 PM

NOTICE OF INTENT TO ACT UPON A REGULATION Notice of Public Hearing for the Adoption of Proposed New Regulations The Nevada Governor s Office of Economic Development will hold a public hearing at 1:30 PM

NOTICE OF INTENT TO ACT UPON REGULATION

JIM GIBBONS Governor DIANNE CORNWALL Director STATE OF NEVADA FINANCIAL INSTITUTIONS DIVISION DEPARTMENT OF BUSINESS AND INDUSTRY GEORGE E. BURNS Commissioner STEVEN W. KONDRUP Deputy Commissioner NOTICE

JIM GIBBONS Governor DIANNE CORNWALL Director STATE OF NEVADA FINANCIAL INSTITUTIONS DIVISION DEPARTMENT OF BUSINESS AND INDUSTRY GEORGE E. BURNS Commissioner STEVEN W. KONDRUP Deputy Commissioner NOTICE

162 Washington Avenue, Albany, NY 12231

Local Law Filing New York State Department of State 162 Washington Avenue, Albany, NY 12231 County of Tioga Local Law No. 5 of the Year 1997. A Local Law increasing the rate of taxes on sales and uses

Local Law Filing New York State Department of State 162 Washington Avenue, Albany, NY 12231 County of Tioga Local Law No. 5 of the Year 1997. A Local Law increasing the rate of taxes on sales and uses

Construction Contractors

16 Construction Contractors Chapter 16 Construction Contractors A. General Information A construction contractor is the user or consumer of everything he buys. A construction contractor is a person or

16 Construction Contractors Chapter 16 Construction Contractors A. General Information A construction contractor is the user or consumer of everything he buys. A construction contractor is a person or

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.S971114A On November

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.S971114A On November

Contracts. Definitions. Guidelines for contractors and subcontractors

0. Contractors www.revenue.state.mn.us 128 Sales Tax Fact Sheet What s New in 2014 The sales and use tax on repair and maintenance of certain business equipment has been repealed effective April 1, 2014.

0. Contractors www.revenue.state.mn.us 128 Sales Tax Fact Sheet What s New in 2014 The sales and use tax on repair and maintenance of certain business equipment has been repealed effective April 1, 2014.

ADOPTED REGULATION OF THE BOARD OF OCCUPATIONAL THERAPY. LCB File No. R017-14. Effective October 24, 2014

ADOPTED REGULATION OF THE BOARD OF OCCUPATIONAL THERAPY LCB File No. R017-14 Effective October 24, 2014 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted.

ADOPTED REGULATION OF THE BOARD OF OCCUPATIONAL THERAPY LCB File No. R017-14 Effective October 24, 2014 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted.

How To Tax On Art

Audit Manual Chapter 11 Advertising Agencies, Graphic Artists, Printers, and Related Enterprises Sales and Use Tax Department California State Board of Equalization This is an advisory publication providing

Audit Manual Chapter 11 Advertising Agencies, Graphic Artists, Printers, and Related Enterprises Sales and Use Tax Department California State Board of Equalization This is an advisory publication providing

Sales Tax Guidelines: How Kansas Motor Vehicle Dealers and Leasing Companies Should Charge Sales Tax on Leases

JOAN WAGNON, SECRETARY DEPARTMENT OF REVENUE POLICY AND RESEARCH MARK PARKINSON, GOVERNOR DEPARTMENT OF REVENUE POLICY AND RESEARCH Sales Tax Guidelines: How Kansas Motor Vehicle Dealers and Leasing Companies

JOAN WAGNON, SECRETARY DEPARTMENT OF REVENUE POLICY AND RESEARCH MARK PARKINSON, GOVERNOR DEPARTMENT OF REVENUE POLICY AND RESEARCH Sales Tax Guidelines: How Kansas Motor Vehicle Dealers and Leasing Companies

Business tax tip #6 Retail Sales Involving Exemption Certificates

Business tax tip #6 Retail Sales Involving Exemption Certificates What is an exemption certificate? It is a wallet-sized card, bearing the holder's eight-digit exemption number. Certificates issued to

Business tax tip #6 Retail Sales Involving Exemption Certificates What is an exemption certificate? It is a wallet-sized card, bearing the holder's eight-digit exemption number. Certificates issued to

Procedures for Independent Contractor Agreement

Procedures for Independent Contractor Agreement Reviewed: December 22, 2011 All requests to procure independent contractor services are required to utilize the UNR Independent Contractor Agreement (ICA)

Procedures for Independent Contractor Agreement Reviewed: December 22, 2011 All requests to procure independent contractor services are required to utilize the UNR Independent Contractor Agreement (ICA)

INFORMATION BULLETIN #4 SALES TAX SEPTEMBER 2011. (Replaces Bulletin #4 dated August 2011)

") INFORMATION BULLETIN #4 SALES TAX SEPTEMBER 2011 (Replaces Bulletin #4 dated August 2011) DISCLAIMER: SUBJECT: Information bulletins are intended to provide nontechnical assistance to the general public.

INFORMATION BULLETIN #4 SALES TAX SEPTEMBER 2011 (Replaces Bulletin #4 dated August 2011) DISCLAIMER: SUBJECT: Information bulletins are intended to provide nontechnical assistance to the general public.

April 4, 2014. Dear Xxxxx:

ST 14-0017-GIL 04/04/2014 COMPUTER SOFTWARE This letter discusses the taxability of computer software licenses and maintenance agreements. See 86 Ill. Adm. Code 130.1935 and 86 Ill. Adm. Code 140.301.

ST 14-0017-GIL 04/04/2014 COMPUTER SOFTWARE This letter discusses the taxability of computer software licenses and maintenance agreements. See 86 Ill. Adm. Code 130.1935 and 86 Ill. Adm. Code 140.301.

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

NEVADA BUSINESS REGISTRATION FORM INSTRUCTIONS Completion of this form will provide the common information needed and/or required by participating state and local government agencies. Important details

BULK SALES - BUYING AND SELLING BUSINESS ASSETS

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

QUESTION: 1- Are the premiums paid by customers to providers for home service contracts only subject to the 2% premium tax and not to sales tax?

Executive Director Marshall Stranburg QUESTION: 1- Are the premiums paid by customers to providers for home service contracts only subject to the 2% premium tax and not to sales tax? 2- Are the amounts

Executive Director Marshall Stranburg QUESTION: 1- Are the premiums paid by customers to providers for home service contracts only subject to the 2% premium tax and not to sales tax? 2- Are the amounts

1999 Sales & Use Tax Study: Manufacturers & Contractors: Sales and Use Tax Implications of Construction Contracts COST Washington, DC

1999 Sales & Use Tax Study: Manufacturers & Contractors: Sales and Use Tax Implications of Construction Contracts COST Washington, DC ARIZONA Name of Preparer: Name of Reviewer: Betty Conn C. Stephen Rosander

1999 Sales & Use Tax Study: Manufacturers & Contractors: Sales and Use Tax Implications of Construction Contracts COST Washington, DC ARIZONA Name of Preparer: Name of Reviewer: Betty Conn C. Stephen Rosander

Business tax tip #4 If You Make Purchases for Resale

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

SALES AND USE TAX TECHNICAL BULLETINS SECTION 37 37-1 SALES BY AND SALES TO THE UNITED STATES GOVERNMENT OR ANY AGENCIES OR INSTRUMENTALITIES THEREOF

SECTION 37 - THE UNITED STATES GOVERNMENT OR AGENCIES THEREOF 37-1 SALES BY AND SALES TO THE UNITED STATES GOVERNMENT OR ANY AGENCIES OR INSTRUMENTALITIES THEREOF A. Exemptions Sales by and sales directly

SECTION 37 - THE UNITED STATES GOVERNMENT OR AGENCIES THEREOF 37-1 SALES BY AND SALES TO THE UNITED STATES GOVERNMENT OR ANY AGENCIES OR INSTRUMENTALITIES THEREOF A. Exemptions Sales by and sales directly

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 4

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 4 CONTRACTORS AND SUBCONTRACTORS This bulletin is intended solely as advice to assist persons in determining, exercising

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 4 CONTRACTORS AND SUBCONTRACTORS This bulletin is intended solely as advice to assist persons in determining, exercising

NEVADA STATE BOARD OF COSMETOLOGY

NEVADA STATE BOARD OF COSMETOLOGY Main Office: Branch Office: 1785 E. Sahara Avenue, Suite 255 4600 Kietzke Lane, Building O, Suite 262 Las Vegas, NV 89104 Reno, NV 89502 Phone: (702) 486-6542 Phone: (775)

NEVADA STATE BOARD OF COSMETOLOGY Main Office: Branch Office: 1785 E. Sahara Avenue, Suite 255 4600 Kietzke Lane, Building O, Suite 262 Las Vegas, NV 89104 Reno, NV 89502 Phone: (702) 486-6542 Phone: (775)

Information for Construction Contractors. Terry O Neill Taxpayer Service Specialist

Information for Construction Contractors Terry O Neill Taxpayer Service Specialist Today s Webinar Definitions and details 4 types of contractors Sales tax for each type of contractor Materials, Equipment,

Information for Construction Contractors Terry O Neill Taxpayer Service Specialist Today s Webinar Definitions and details 4 types of contractors Sales tax for each type of contractor Materials, Equipment,

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE. The issues raised by Petitioner, Ronald Webb Builder & Contractor, Inc.

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S011029A

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S011029A

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING #11-57 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING #11-57 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation of

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING #11-57 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation of

IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/

1 IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/ WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government

1 IRS GUIDELINES FOR FORM 1099 FOR STATE AND LOCAL GOVERNMENTS IRS Webinar: http://www.tax.gov/1099webinar/ WHO MUST FILE Any entity conducting a trade or business is required to file Form 1099. Government

INFORMATION BULLETIN #2 SALES TAX MARCH 2013 (Replaces Bulletin #2 dated January 2013) Effective Date: 1 March 2013

Effective Date: 1 March 2013") INFORMATION BULLETIN #2 SALES TAX MARCH 2013 (Replaces Bulletin #2 dated January 2013) Effective Date: 1 March 2013 SUBJECT: Original Manufacturer Warranties, Optional Maintenance Contracts, and Optional

INFORMATION BULLETIN #2 SALES TAX MARCH 2013 (Replaces Bulletin #2 dated January 2013) Effective Date: 1 March 2013 SUBJECT: Original Manufacturer Warranties, Optional Maintenance Contracts, and Optional

Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA

Page 1 of 9 Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA The objective of this section is to introduce and review some of the foundational components of Georgia

Page 1 of 9 Section 1: Georgia Sales and Use Tax Principles Presented by Ned A. Lenhart, CMI, CPA The objective of this section is to introduce and review some of the foundational components of Georgia

STATE OF NEVADA NOTICE OF MEETING/HEARING. DATE: Saturday, September 26, 2015 TIME: 10:00 a.m.

BRIAN SANDOVAL Governor BENJAMIN LURIE, DC President LAWRENCE DAVIS, DC Vice President DAVID G. ROVETTI, DC Secretary-Treasurer STATE OF NEVADA JACK NOLLE, DC Member MAGGIE COLUCCI, DC Member TRACY DiFILLIPPO,

BRIAN SANDOVAL Governor BENJAMIN LURIE, DC President LAWRENCE DAVIS, DC Vice President DAVID G. ROVETTI, DC Secretary-Treasurer STATE OF NEVADA JACK NOLLE, DC Member MAGGIE COLUCCI, DC Member TRACY DiFILLIPPO,

START-UP NY certificates

New York State Department of Taxation and Finance START-UP NY Business Fact Sheet The following sections provide information about the two different START-UP NY certificates you will receive and the tax

New York State Department of Taxation and Finance START-UP NY Business Fact Sheet The following sections provide information about the two different START-UP NY certificates you will receive and the tax

SUMMARY. Jan 30, 2001. Re: Technical Assistance Advisement 01A-009 Sales and Use Tax -- Security Systems Sections 212.05, 212.06, F.S.

SUMMARY QUESTION: Are contracts who install security and alarm systems contracts for real property improvements or sales of tangible personal property? ANSWER - Based on Facts Below: Contracts who furnish

SUMMARY QUESTION: Are contracts who install security and alarm systems contracts for real property improvements or sales of tangible personal property? ANSWER - Based on Facts Below: Contracts who furnish

REVISED ADOPTED REGULATION OF THE DEPARTMENT OF EDUCATION. LCB File No. R061-08. Effective September 18, 2008

REVISED ADOPTED REGULATION OF THE DEPARTMENT OF EDUCATION LCB File No. R061-08 Effective September 18, 2008 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be

REVISED ADOPTED REGULATION OF THE DEPARTMENT OF EDUCATION LCB File No. R061-08 Effective September 18, 2008 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be

PST-57 Issued: March 2000 Revised: March 2016 INFORMATION FOR BUSINESSES PROVIDING REPAIR AND INSTALLATION SERVICES

Information Bulletin PST-57 Issued: March 2000 Revised: March 2016 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT Click here to complete our short READER SURVEY INFORMATION FOR BUSINESSES PROVIDING

Information Bulletin PST-57 Issued: March 2000 Revised: March 2016 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT Click here to complete our short READER SURVEY INFORMATION FOR BUSINESSES PROVIDING

(Draft No. 2.1 H.577) Page 1 of 20 5/3/2016 - MCR 7:40 PM. The Committee on Finance to which was referred House Bill No. 577

Page 1 of 20 5/3/2016 - MCR 7:40 PM. The Committee on Finance to which was referred House Bill No. 577") (Draft No.. H.) Page of // - MCR :0 PM TO THE HONORABLE SENATE: The Committee on Finance to which was referred House Bill No. entitled An act relating to voter approval of electricity purchases by municipalities

(Draft No.. H.) Page of // - MCR :0 PM TO THE HONORABLE SENATE: The Committee on Finance to which was referred House Bill No. entitled An act relating to voter approval of electricity purchases by municipalities

Pe r f e c t i n g a. Ne va d a. Caryn S. Tijsseling. Prepared and Presented by. Lewis and Roca LLP 775-321-3426 CTijsseling@LRLaw.

Pe r f e c t i n g a Mechanic s Lien in Ne va d a Prepared and Presented by Caryn S. Tijsseling Lewis and Roca LLP 775-321-3426 CTijsseling@LRLaw.com Overview of Construction Liens The Nevada Revised Statutes

Pe r f e c t i n g a Mechanic s Lien in Ne va d a Prepared and Presented by Caryn S. Tijsseling Lewis and Roca LLP 775-321-3426 CTijsseling@LRLaw.com Overview of Construction Liens The Nevada Revised Statutes

REVENUE ADMINISTRATIVE BULLETIN 2002-15. Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND REQUIREMENTS

JOHN ENGLER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING DOUGLAS B. ROBERTS STATE TREASURER REVENUE ADMINISTRATIVE BULLETIN 2002-15 Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND

JOHN ENGLER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING DOUGLAS B. ROBERTS STATE TREASURER REVENUE ADMINISTRATIVE BULLETIN 2002-15 Approved: June 10, 2002 SALES AND USE TAX EXEMPTIONS AND

State Tax Chart Results

Tax Chart Results Tax Type: Sales/Use Advertising Services This chart shows whether or not the state taxes advertising services. Advertising MD Taxable Certain advertising services are nontaxable. Armored

Tax Chart Results Tax Type: Sales/Use Advertising Services This chart shows whether or not the state taxes advertising services. Advertising MD Taxable Certain advertising services are nontaxable. Armored

Gross Receipts. Gross Receipts. Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501. July 2013

South Gross Dakota Receipts Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 This fact sheet is designed to provide general guidelines and examples of what is included in a retailer

South Gross Dakota Receipts Department of Revenue 445 East Capitol Avenue Pierre, South Dakota 57501 This fact sheet is designed to provide general guidelines and examples of what is included in a retailer

SALES AND USE TAX TECHNICAL BULLETINS SECTION 31 31-1 CONTRACTORS, SUBCONTRACTORS AND RETAILER-CONTRACTORS

SECTION 31 - CONTRACTORS AND BUILDING MATERIALS 31-1 CONTRACTORS, SUBCONTRACTORS AND RETAILER-CONTRACTORS A. Contractors are deemed to be consumers of tangible personal property which they use in fulfilling

SECTION 31 - CONTRACTORS AND BUILDING MATERIALS 31-1 CONTRACTORS, SUBCONTRACTORS AND RETAILER-CONTRACTORS A. Contractors are deemed to be consumers of tangible personal property which they use in fulfilling

2015 NEVADA TAX REFORMS. Commerce Tax, Modified Business Tax, Business License Fee

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax jhicks@bhfs.com 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax jhicks@bhfs.com 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.Z950802D On August

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO.Z950802D On August

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 cslewis@stoel.com Kevin T. Pearson 900 SW Fifth Avenue, Suite

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 cslewis@stoel.com Kevin T. Pearson 900 SW Fifth Avenue, Suite

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE. Petitioner submits the following facts as the basis for this Advisory Opinion.

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S941017B On October

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S941017B On October

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S040818B

New York State Department of Taxation and Finance Office of Tax Policy Analysis Technical Services Division STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S040818B

CITY OF CHICAGO DEPARTMENT OF REVENUECHICAGO USE TAX FOR NONTITLED PERSONAL PROPERTY REGULATIONS

CITY OF CHICAGO DEPARTMENT OF REVENUECHICAGO USE TAX FOR NONTITLED PERSONAL PROPERTY REGULATIONS Effective date: June 1, 2004 Original effective date: March 3, 1992 1. Description of Tax The Chicago Use

CITY OF CHICAGO DEPARTMENT OF REVENUECHICAGO USE TAX FOR NONTITLED PERSONAL PROPERTY REGULATIONS Effective date: June 1, 2004 Original effective date: March 3, 1992 1. Description of Tax The Chicago Use

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 10-24 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

New Electronic Stamping Regulations

NEVADA STATE BOARD OF ARCHITECTURE, INTERIOR DESIGN & RESIDENTIAL DESIGN 2080 E. Flamingo Rd., Suite 120 Las Vegas, NV 89119 (702) 486-7300 phone (702) 486-7304 fax nsbaidrd@nsbaidrd.nv.gov Nevada State

NEVADA STATE BOARD OF ARCHITECTURE, INTERIOR DESIGN & RESIDENTIAL DESIGN 2080 E. Flamingo Rd., Suite 120 Las Vegas, NV 89119 (702) 486-7300 phone (702) 486-7304 fax nsbaidrd@nsbaidrd.nv.gov Nevada State

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S960209A On February

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S960209A On February

Referred to Committee on Taxation. SUMMARY Revises provisions relating to tobacco. (BDR 32-175)

") ASSEMBLY BILL NO. COMMITTEE ON TAXATION (ON BEHALF OF THE ATTORNEY GENERAL) PREFILED DECEMBER 0, 0 Referred to Committee on Taxation A.B. SUMMARY Revises provisions relating to tobacco. (BDR -) FISCAL

ASSEMBLY BILL NO. COMMITTEE ON TAXATION (ON BEHALF OF THE ATTORNEY GENERAL) PREFILED DECEMBER 0, 0 Referred to Committee on Taxation A.B. SUMMARY Revises provisions relating to tobacco. (BDR -) FISCAL

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 07-05 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

Department of Legislative Services

Department of Legislative Services Maryland General Assembly 2008 Session HB 1169 FISCAL AND POLICY NOTE House Bill 1169 Ways and Means (Delegate Barve) Sales and Use Tax - Computer Services Exemption

Department of Legislative Services Maryland General Assembly 2008 Session HB 1169 FISCAL AND POLICY NOTE House Bill 1169 Ways and Means (Delegate Barve) Sales and Use Tax - Computer Services Exemption

This letter discusses sales of software. See 86 Ill. Adm. Code 130.1935. (This is a GIL.)

") ST 07-0125-GIL 08/16/2007 COMPUTER SOFTWARE This letter discusses sales of software. See 86 Ill. Adm. Code 130.1935. (This is a GIL.) August 16, 2007 Dear Xxxxx: This letter is in response to your letter

ST 07-0125-GIL 08/16/2007 COMPUTER SOFTWARE This letter discusses sales of software. See 86 Ill. Adm. Code 130.1935. (This is a GIL.) August 16, 2007 Dear Xxxxx: This letter is in response to your letter

Exempt Organizations: Sales and Purchases

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts DECEMBER 2010 Organizations that have applied for and received a letter of exemption from sales tax don t have

City and County of Denver, Colorado TAX GUIDE Topic No. 18 Data Processing

City and County of Denver, Colorado TAX GUIDE Topic No. 18 Data Processing The Denver Revised Municipal Code ( DRMC ) imposes sales or use tax on the purchase price or charge for data processing equipment

City and County of Denver, Colorado TAX GUIDE Topic No. 18 Data Processing The Denver Revised Municipal Code ( DRMC ) imposes sales or use tax on the purchase price or charge for data processing equipment

Manufactured & Modular Homes

South Dakota Manufactured & Modular Homes Department of Revenue & Regulation 445 East Capitol Avenue Pierre, South Dakota 57501-3185 Manufactured & Modular Homes D e c e m b e r 2 0 1 1 This Tax Facts

South Dakota Manufactured & Modular Homes Department of Revenue & Regulation 445 East Capitol Avenue Pierre, South Dakota 57501-3185 Manufactured & Modular Homes D e c e m b e r 2 0 1 1 This Tax Facts

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE. Petitioner submitted the following facts as the basis for this Advisory Opinion.

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S990316A On March

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S990316A On March

Service Tax Liability in Illinois - A Guide For Search and Information Technology

11/29/2012 SERVICE OCCUPATION TAX If tangible personal property is transferred incident to sales of service, this will result in either Service Occupation Tax liability or Use Tax liability for the serviceman

11/29/2012 SERVICE OCCUPATION TAX If tangible personal property is transferred incident to sales of service, this will result in either Service Occupation Tax liability or Use Tax liability for the serviceman

Draft Regulation Prewritten Software Accessed Remotely

Draft Regulation Prewritten Software Accessed Remotely The Vermont Department of Taxes is soliciting comments on draft regulatory language related to the collection of sales tax on prewritten software

Draft Regulation Prewritten Software Accessed Remotely The Vermont Department of Taxes is soliciting comments on draft regulatory language related to the collection of sales tax on prewritten software

CITY OF NORTH LAS VEGAS PERFORMANCE BOND

CITY OF NORTH LAS VEGAS PERFORMANCE BOND BOND NUMBER DATE EXECUTED IMPORTANT: SURETY COMPANIES EXECUTING BONDS MUST BE LICENSED TO ISSUE SURETY BY THE STATE OF NEVADA INSURANCE DIVISION PURSUANT TO NRS

CITY OF NORTH LAS VEGAS PERFORMANCE BOND BOND NUMBER DATE EXECUTED IMPORTANT: SURETY COMPANIES EXECUTING BONDS MUST BE LICENSED TO ISSUE SURETY BY THE STATE OF NEVADA INSURANCE DIVISION PURSUANT TO NRS