Improving Target date Offerings: Lessons Proven

|

|

|

- Coleen Miles

- 7 years ago

- Views:

Transcription

1 Improving Target date Offerings: Lessons Proven Provided by FOLIOfn Investments, Inc. Disclosure: The data, information, and content in this white paper are for information, education, and non-commercial purposes only. Historical performance does not represent the performance of any investment advisory firm, and past performance is no guarantee of future results. The information in this white paper does not involve the rendering of personalized investment advice and is limited to the dissemination of opinions on investing. No reader should construe these opinions as an offer of advisory services or as a solicitation to purchase or sell any security by FOLIOfn, Inc. All Rights Reserved. Securities products and services offered through FOLIOfn Investments, Inc. Member FINRA/SIPC.

2 Executive Summary Target date funds are the fastest-growing part of the mutual fund industry 1, and the most important. They are the central to the country s defined contribution (DC) retirement system, underpinning the premise that DC offerings can be both simple and effective. They are an investment for those who default into a retirement selection, and the preferred choice for those who want an all-in-one retirement investment. Consequently it is critical for much of working America that these target date offerings be a superb choice: well-designed and implemented, with reasonable costs, and with beneficial results. Half a dozen years ago, Folio Investing began to examine the universe of target date fund families, with emphasis on the three fund families that dominate the industry (those three fund families today account for three-quarters of all assets in target date offerings). We concluded that the standard methodologies could be substantially improved. Our research suggested that these target date funds were i) not well designed from the outset, ii) not being modified over time to maintain appropriate risk targets, iii) not well described in terms of their goals, and iv) not flexible enough to serve varying investor needs. Given the importance of target date offerings as a primary default retirement vehicle, we introduced our own series of target date portfolios (what we call Folios ) to the public in late 2007, along with supporting research that explained the need for substantial changes in target date offerings. The past five years -- some of the most volatile in the market history -- have validated our research and conclusions. With performance data for the Target date Folios and for target date funds over this period, we have unique insight into what is working with Target date funds, and what is not, and why. Target date strategies can provide investors with the potential for gains provided by equities and other risky asset classes, while mitigating potential losses due to declines in any single asset class. Many target date funds, however, have failed to meet these goals as well as expected. Under-diversification in many funds resulted in their being over-exposed to major equity indexes, and their policy of maintaining static asset allocation at each point in the glide path (as opposed to having target risk levels) resulted in higher sensitivity to market shocks. These flaws have real world implications. High expenses in some funds will consume a substantial fraction of investors lifetime wealth accumulation. Overall, we believe that investors in many of the available target date funds are likely to lose out on as much as half the expected future real returns from the equity and bond markets due to design flaws and high expenses. As an alternative, the Target Date Folios, implemented using low-cost allocations to a diverse set of ETFs, have provided returns substantially higher than those provided by the majority of 1 in-12-months

3 Target date funds. Moreover, these higher returns are achieved with lower sensitivity to market shocks such as we experienced in 2008 and in In sum, the failure of many target date funds to deliver on their promise does not diminish the overall value or importance of target date strategies generally. It simply highlights the need to do it well. With almost five years of operational returns through Q3 of 2012, we have demonstrated that it is possible to implement target date strategies more effectively, with substantial benefits for investors. Introduction * * * Target date funds are the fastest-growing part of the mutual fund industry and are projected to grow to hold almost half of all assets in 401(k) and other defined contribution (DC) retirement plans by This substantial rate of growth is driven by a number of factors, including: The auto-enrollment of employees into retirement plans combined with the designation of Target date strategies as Qualified Default Investment Alternatives (QDIA); The simplification of retirement plan offerings with target date funds providing the easiest way to provide investors a complete investing solution in a single fund; The general lack of confidence among individual investors with respect to how to invest their retirement savings effectively, with target date funds being the default choice; and The data suggesting that target date funds lead to improved performance when compared to the choices that investors would make without such guidance. One study 3 found that 401(k) plan participants who use some kind of help in selecting portfolios (Target date funds, online asset allocation advice, or separately managed accounts) out-performed those who had no help by an average of 2.9% per year, net of fees, from 2006 through Nevertheless, while assets in target date funds are increasing rapidly 4 along with a compelling narrative for future growth, important issues need to be addressed. Target date funds came under considerable criticism in 2008, when many funds designed for investors near retirement suffered dramatic losses. The return for the Help in Defined Contribution Plans: 2006 Through 2010 ( 4

4 funds aimed at investors with a projected retirement date of 2010 (referred to as 2010 funds) averaged -24.6% across the three fund families that hold more than three-quarters of the total assets invested in target date funds. While this loss level was considerably less extreme than the -37% return of the S&P500, 2008 resulted in enormous losses for investors on the cusp of retiring. In the aftermath of 2008, these funds were criticized for being too risky. Then, in , a period of substantially rising equity markets, target date funds generally delivered solid performance. It appeared that their significant failure just a year earlier was soon forgotten, but the positive returns failed to demonstrate whether the risk management issues with target date funds had been resolved. But 2011 provided another test was not terrible for U.S. equities, but international, especially European, equities fared poorly. As our research shows (described more below) many target date funds returns are highly correlated to both major domestic and international equity indexes. Consequently, target date fund performance, again, was generally not good. Many target date funds generated negative returns for the year, even though the S&P500 gained 2.1% (including dividends) and the Barclays Aggregate Bond Index gained 7.8%. The average 2011 return of all target date funds was -1.6% 5. Even funds designed for people near retirement tended to lose money in 2011: the average 2015 fund tracked by Morningstar returned -0.4% in This poor 2011 performance has now prompted a new round of review, and criticism 7. Even worse, target date funds as a group performed poorly in Q3 of 2011 and their aggregate 2011 performance would have been even worse had it not been for a substantial rally in equities in Q4. We calculate 8, for example, that the average of the 2010 funds from the three largest fund families returned -8% in Q3 certainly enough to cause very significant strain on a recent retiree s funds. Morningstar found that the average return across all 2010 funds that they track was a return of -7.1% in Q3 9. These significant swings are precisely what close-in target date funds (offerings for those near retirement) are supposed to mitigate See note 3 above and and_may_stay_that_way.html

5 For investors in or at retirement, losses as large as 7%-8% in a single quarter are excessive. Target date fund offerings continue to exhibit the same flaws as in 2008, notwithstanding the well-founded concerns raised then about the need for change. Target Date Strategies and How Folio Investing Improved Them The poor performance of target date funds in periods of market stress raises a number of questions about fund strategies. Some commentators believed that the magnitude of losses resulted from poor execution of otherwise sound design and strategies. Others concluded that the underlying theory was flawed and that core concepts such as diversification were no longer viable. And others concluded that nothing in fact has gone awry and that levels of loss exhibited in volatile periods are simply inevitable outcomes of extreme market conditions. We have a unique perspective from which to address this question of what s gone wrong target date funds. In 2006, we concluded that the traditional approach was flawed, as described below. To provide investors and plan sponsors with a better solution, we designed and launched an alternative set of target date allocations. These new target date allocations, what we call Target date Folios, 10 were launched and made publicly available by Folio Investing in late Although Folios are not mutual funds or ETFs, they are portfolios of securities (here, ETFs) that an investor can buy or sell in a single transaction. These Folios, like all folios on the Folio Investing platform, can also be customized if an investor wants a more tailored solution. To ensure a true performance record that includes real world effects (such as bid-ask spreads and expense ratios), Folio Investing funded these Folios and traded them on the Folio Investing platform. The Target date Folios match standard target retirement dates in that they are designed for projected retirement dates in five-year increments: 2010, 2015, 2020, etc. through The Folios strategies are very different from industry practice, however. Our view of the limitation of traditional target date fund has now been proved out with the relative performance of the funds versus Folios since the Target Date Folios were launched. The principle fund limitations include: 1) Low levels of effective diversification; and 2) The use of asset allocation glide paths as a surrogate for risk, as opposed to the use of target risk along the glide path. 3) A one size-fits all approach to target date year risk levels; 4) Inadequate descriptions of what an investor should expect; and 10

6 5) Relatively high expenses. Diversification and Risk Our initial research identified the most critical problems with the target date fund design: underdiversification, and a reliance on asset allocation as opposed to risk budgeting for the glide path. These significant flaws persist today. Even though target date funds generally hold multiple underlying funds which themselves each hold hundreds of individual securities, they are not well diversified. Diversification requires more than just owning a large number of holdings. Naïve diversification, 11 as it is referred to, is achieved by combining a large number of individual securities in a portfolio. By contrast, strategic diversification entails the selection of holdings specifically to exploit low correlations between them, with the goal of maximizing expected return vs. risk. Our research suggests that many target date funds are using a naïve diversification strategy. For example, the combination of 60% S&P500 stocks and 40% bonds is often used as a proxy for a diversified portfolio. But this portfolio s returns exhibit a 99% correlation to the S&P500, and have for a long time. Put another way, this portfolio is highly correlated to a single asset class -- large-cap U.S. stocks. When those securities decline significantly, so will the 60/40 portfolio. The bond allocation reduces risk, but the portfolio remains almost perfectly correlated to the S&P500. In recent decades, international equities (as measured by the EAFE index, for example) have become increasingly correlated to U.S. equities, so that even the modest diversification benefits historically provided by combining large cap domestic and international stocks are substantially diminished. The table below shows how very high the actual correlations are of target date fund returns to returns of the major stock indexes. Each composite portfolio for the specified target year is equally weighted among the funds from the three largest target date fund families. These fund families currently hold 75% of all target date fund assets. 11

7 Correlation to: Portfolio equally weighted to three largest 2040 funds Portfolio equally weighted to three largest 2030 funds Portfolio equally weighted to three largest 2020 funds Portfolio equally weighted to three largest 2010 funds S&P500 Stocks 99% 99% 98% 98% EAFE Stocks 95% 95% 95% 95% Emerging Mkt Stocks 92% 92% 92% 92% 10-Year Treasury Yield 39% 37% 34% 30% VIX -69% -68% -67% -66% Correlation of returns between target date fund portfolios and major asset classes and indexes (four years through October 2012) Surprisingly, even the least risky of the target date funds the 2010 funds -- show a very high correlation to the S&P500 and a slightly lower correlation to the EAFE. The significant correlation of these target date funds to the EAFE index, which returned -12.1% in 2011, explains the funds poor performance (relatively speaking) in that year, even with a small gain for the S&P 500. The average return of the three largest 2020 target date funds was -0.7% and the average return of the three largest 2040 funds was -3.6% in 2011, even though the S&P500 gained 2.1% (including dividends) and the Barclays Aggregate Bond Index gained 7.8%. The returns from the target date fund composites have a strong negative correlation to market volatility, as measured by the VIX index. A market with rising VIX will tend to correspond to negative returns from target date funds, and vice versa. Similarly, returns from stock indexes also exhibit a very strong negative correlation to VIX. The conclusion to be drawn here is that volatility shocks in the equity markets, which will correspond to a rise in VIX, will tend to have a substantial negative impact on target date fund performance. But these are precisely the conditions in which investors hope that diversification will protect them. Powerful counter-points to the Target date funds high correlations are the uniformly and significantly lower correlations of the Target date Folios to these same indexes. And although low correlations are not themselves the goal, they do reflect the opportunities that result from strategic diversification. It is the low correlation of a portfolio to major asset classes -- where asset classes move distinctly from one another that demonstrates the risk mitigation in a portfolio:

8 Correlation to: 2040 Moderate Folio 2030 Moderate Folio 2020 Moderate Folio 2010 Moderate Folio S&P500 Stocks 91% 85% 87% 86% EAFE Stocks 91% 89% 87% 85% Emerging Mkt Stocks 90% 88% 84% 83% 10-Year Treasury Yield 14% 6% 5% 5% VIX -60% -56% -56% -54% Correlation of returns between current Target date Folios and major asset classes and indexes (four years of data through October 2012) The performance of the 2010 Moderate 12 Folio versus the composite performance of the three largest 2010 Target date Funds demonstrates why these correlations matter: Target Date Folios / Funds Return Since Inception (12/21/ /28/12) Year 2008 Year 2009 Year 2010 Year Moderate Target Date Folio Average of 3 Largest 2010 Target Date Funds Average Annual Folio Advantage 21.0% -18.1% 18.0% 10.9% 5.2% 16.5% -24.7% 24.3% 12.1% 1.2% 0.8% 6.6% -6.3% -1.2% 4.0% Performance Since Inception (12/21/07 to 9/28/2012) of the 2010 Folios versus the composite performance of the three largest 2010 Target date Funds 13 The 2010 Moderate Folio performed much better in 2011 and in 2008 than the composite of the three largest funds, while under-performing those funds in 2009 and slightly under-performing in Since inception, the 2010 Moderate Folio has provided a cumulative 4.5% in return beyond that of a composite of the three largest 2010 target date funds. As important as the extra return is, the risk mitigation is equally important. The substantially less extreme loss in 2008 and the higher returns in 2011 in the Folio vs. the largest funds are notable. These cumulative performance numbers don t tell the entire story. The higher inverse correlations to VIX in the previous table suggest that the target date funds are more susceptible 12 The Moderate risk folios are designed as alternatives to traditional funds typical risk levels. 13 In this table and in all performance tables in this paper, we have reduced the actual returns of the Folios by 38 bps per year to represent the potential impacts of brokerage expenses.

Year 2008 Year 2009 Year 2010 Year 2011 2010 Moderate Target Date Folio Average of 3 Largest 2010 Target Date Funds Average Annual Folio Advantage 21.0% -18.")

9 to shocks to the broad stock indexes than the Folios. The sensitivity of different funds and folios to a volatility shock is reflected in their performance during the volatile third quarter of 2011: 2010 Moderate Folios vs. Composite Investment in Three Largest 2010 Funds During 2011 (these results include a 38 bps cost for the Folio, accrued daily) The 2010 Moderate Folio and the composite of the three 2010 funds tracked together through mid July, as the market broadly rose and volatility declined. But when the S&P500 suffered a major and rapid decline, and market volatility substantially increased from late July through early October of 2011, the composite of the 2010 Target date funds suffered far more than the 2010 Moderate Folio, as theory and design suggested it would. When the U.S. market rallied late in 2011, the composites of the three largest fund families rose to some extent but they were limited by their substantial correlations to Europe. Abrupt losses are unsettling to investors, but especially for those close to, or in, retirement. The composite of the three largest 2010 target date funds moved from a year-to-date gain of slightly more than 5% in the middle of July 2011 to a 5% loss for the YTD by the start of October. Is the potential for a 10% decline in portfolio value over a two-and-a-half month period acceptable for investors in retirement? There can be no definitive answer, but we are concerned by this level of loss exposure to the major equity indexes. When we look at the 2020, 2030, and 2040 target date results (below), we see the same pattern of behavior but the loss response to a decline in the S&P500 is even more dramatic.

10 2020 Moderate Folio vs. Composite Investment in Three Largest 2020 Funds During 2011

shows that the Folios out-performed substantially in 2008,")

11 2030 Moderate Folio vs. Composite Investment in Three Largest 2030 Funds During Moderate Folio vs. Composite Investment in Three Largest 2040 Funds During 2011 The composite performance statistics for the Target Date Folios (Appendix A) shows that the Folios out-performed substantially in 2008, but one may argue that 2008 was a once-in-alifetime fluke or that the funds have evolved to be less risky. The fund performance in 2011

12 demonstrates the high sensitivity of the largest funds to the major equity indexes, as well as showing how Folios can provide a viable alternative. We now have about five years of operational track record to validate the Target Date Folio methodology. Criticisms directed at target date strategies as a whole are misdirected. Simply put, the concept of a target date offering makes sense. The results produced by the largest target date funds over the past five years suggest problems with the specific implementation of target date strategies rather than of the concept as a whole. Those suggesting the failure of diversified strategic asset allocation -- a major underpinning of both target date funds and Folios -- miss the important conclusion to be drawn from the performance of Target date Folios: well-diversified strategic asset allocations do provide substantial risk mitigation, while also maintaining appropriate allocations to equities and other asset classes with substantial return potential. The problem with many of the existing target date funds is that they are simply not effectively diversified and the final asset allocations are very highly correlated to the major equity indexes. It is not unexpected then that their performance is almost entirely determined by the performance of these indexes and that even the funds for people near retirement will suffer substantial losses if the major indexes fall dramatically. The Target Date Folios demonstrate that improved diversification results in better returns for a given risk level and mitigates the impacts of a large loss in any single asset class. Risk Management One of the central elements of designing and managing a target date strategy is determining appropriate risk levels at each stage in a prospective investor s life and managing portfolios to ensure that the risk levels in a portfolio remain consistent with targets through time. There are different ways to measure and achieve target risk levels. In its simplest form, the target portfolio risk level is expressed by the relative allocation to equities and to fixed income in the portfolio. The greater the percentage allocated to equities, the greater the presumed risk. As retirement approaches, target date strategies typically reduce the allocation to equities along a glide path that is intended to be hold for the life of the fund. This approach is attractive for its simplicity, easy to manage, and easy to describe and monitor. There are some pitfalls in this approach to managing portfolio risk, however. The goal of risk management is matching asset allocations to risk targets. Once a target risk level is determined, the portfolio is managed to maintain that desired level of risk through changes in asset allocation. This distinction in approach is critical. Risk in an asset allocation is primarily determined by two factors: estimates of the expected risk in each asset class and the correlations between asset classes. As correlations among asset classes increase -- as they tend to do in times of market stress the risk of almost every asset allocation tends to increase. This risk increase occurs even if the expected volatility of individual asset classes does not increase. For example, over the past five years, a model

13 portfolio equally allocated to five asset classes -- S&P500, EAFE, emerging market stocks, TIPS and an aggregate bond index -- has risk levels that, according to our estimates, have varied by as much as 29% due to increases in correlation in a single year. Consequently, budgeting for risk has to include consideration of time-varying correlations between asset classes and the variability in market risk a static asset allocation glide path does not do that. During times of market calm, correlations may decrease and risk decreases. Targeting risk allows for adjustments to asset allocations that will help to maintain a fairly constant portfolio risk level. Maintaining a static asset allocation for any given target date (as expressed in the traditional glide path) means that investors may be exposed to wildly varying levels of portfolio risk. Consequently, a glide path that usefully and accurately informs the design of a target date strategy should target risk levels over the course of an investor s life, described in terms of specific risk targets (measured, for example, by volatility), rather than asset allocation glide path 14. This approach to risk budgeting is a key element of the Target Date Folios. Changes in the projected risk level for asset allocations through time can result in substantive changes in the asset allocations. From 2011 to 2012, for example, the Target Date Folios asset allocations were materially modified to decrease their allocations to TIPS while municipal bond ETFs were added. This change was driven by the changes in the correlations between asset classes and their impact on aggregate portfolio risk levels. Matching Investor Risk Tolerance As an additional consideration, our survey of target date funds led us to conclude that the industry s notion that target retirement year by itself was sufficient for all investors retiring in any given period a one-size-fits-all approach to investors in any given retirement cohort -- was not ideal. In other words, we believe retirement year alone is not sufficient to determine an investor s ideal risk-return balance. There are many other factors that can influence an investor s choice and risk tolerance, such as differing views as to the income to be derived from a portfolio, or whether an investor will remain invested through retirement years or are likely to cash out at retirement (often referred to as to or through ). Consequently, while target date funds are an important innovation in terms of providing an offthe-rack investment solution, many investors benefit from the ability to tailor their portfolio risk levels. For that reason, Target Date Folios are offered at Conservative, Moderate, and 14 In addition, it is important to understand the portfolio exposure to specific key drivers. The principal variables we track for this purpose are portfolio correlations to major equity indexes, VIX, and ten-year Treasury yield.

14 Aggressive risk levels. Because they are Folios, each can be further modified or customized if desired. The Folio solutions were designed with two goals: to minimize the risk that an investor would run out of money in retirement (longevity risk) and to minimize the risk of under-performing a risk-free asset from an investor s current age to retirement. The Conservative glide path places more emphasis on protecting current assets and is more appropriate for an investor likely to annuitize all or part of his portfolio. The Moderate glide path is designed for an investor who plans to remain invested and draw income systematically throughout retirement. The Moderate glide path is designed to fault tolerant in the event that an investor decides to annuitize some fraction of the portfolio at retirement. The Aggressive glide path is designed for investors who desire a portfolio with higher return potential and can tolerate the elevated risk levels that accompany such a portfolio. Because of the way that Target Date Folios are constructed, investors, advisors and plan sponsors can easily customize the asset allocations even further if desired. A software company plan sponsor, for example, may wish to under-weight software in the investment portfolios to reduce the total economic impact of a downturn in the software industry. This level of tailoring is a unique feature of implementing a target date strategy via a Folio rather than a fund. Expenses Given that target date vehicles are intended to be held over an entire working career, special attention must be paid to expenses. According to Morningstar, the average expense ratio for target date funds is 0.83%, ranging from a low of 0.18% to a high of 1.3% 15. The average expense ratio for the Target Date Folios is 0.26%. A simple calculation by the Department of Labor suggests that a 1% increase in expenses equates to a reduction of 28% in lifetime accumulated savings 16. More sophisticated and realistic calculations broadly agree with this level of impact 17. Expenses are a major determinant of how much wealth investors in target date vehicles can accumulate over their working careers. Under the assumption of a typical 4% withdrawal rate for people in retirement, a difference of 0.6% per year due to expenses (average fund expense minus average Folio expense) is equivalent to 15% of an investor s annual income in retirement. Costs have a huge impact on investors ability to build wealth over their lifetimes and on the amount of income that they can afford to draw in retirement. Conclusions pdf

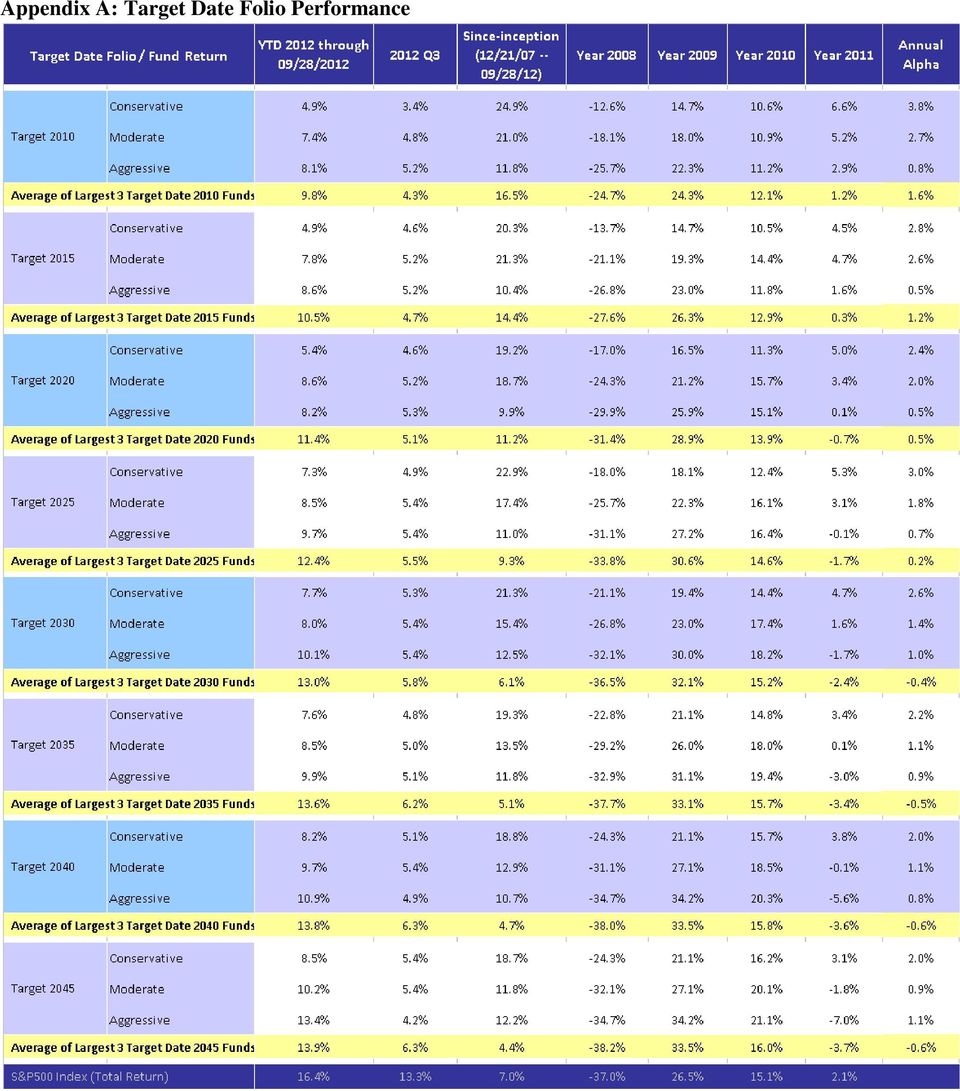

15 The enormous market swings in recent years have wreaked havoc with many investors longterm plans. The anemic returns from equities (1% annualized returns over the five years through October 2012) 18 have put many investors behind their planned savings targets. In addition, the high levels of volatility have been unsettling. These are the kinds of conditions that really make the case for diversified portfolios at an appropriate risk level. Well-diversified portfolios mitigate a portfolio s sensitivity to any single asset class. Furthermore, having access to portfolios that are designed with appropriate risk benchmarks should help investors to closely match their risk exposure to their needs. We have the unique perspective of almost five years of performance history with an alternative approach to creating target date strategies. As we approach five years of performance data, the Target Date Folios have out-performed the target date funds that hold 75%-80% of all target date assets (the three largest fund families in the Target date fund business). The Target Date Folios substantially reduced losses in 2008 vs. the funds and the equity markets as a whole, as well as keeping up with the broad rally in equities in (see Appendix A). In addition, the Target Date Folios out-performed the largest target date fund families in 2011, a volatile year that ended with a modest positive return for the S&P500 but with negative returns for many target date funds. The substantial rally in equities in 2012 has allowed largely undiversified strategies to perform very well. The 2040 Moderate Folio has returned 9.7% through Q3, but that is considerably behind the average of the three largest 2040 funds, which have averaged 13.8% over this period. The S&P500 has gained a total of 16.4% through Q3. When the largest 2010 target date funds lost an average of 24.6% in 2008, investors and market observers were surprised. The fairly large losses suffered by these funds in Q3 of , revived questions with regard to risk management of 2010 funds. We hope that another market shock will not be required to keep attention focused on the need for improved target date designs. When we first analyzed Target date funds, we estimated that under-diversification was costing investors in these funds on the order of 2% per year in return. The Target date Folios were designed, in part, to capture this additional return. Four years later, the Target date Folios have generated slightly more than 1.4% per year in additional return, even after assuming a substantial burden associated with brokerage fees (see Appendix A). The fact that the realized return advantage so closely matches our projections is compelling

16 We have also calculated an annualized alpha for the Target Date Folios. The average alpha 20, since inception, for all of the Target Date Folios up to a projected retirement date of 2045 is 1.7% 21. The average alpha for the composite of the three largest target date fund families for the same range of target dates is 0.2%. The alphas for each Folio are included in Appendix A, along with alphas for fund composites. Because alpha results from the degree to which the returns exceed what can be explained by exposure to an equity index (the S&P500), we expect that any portfolio that includes allocations to other asset classes (bonds, in particular) will allow the portfolio to generate positive alpha. In a target date portfolio, alpha primarily measures the effectiveness of diversification. The alpha that is obtained simply by diversifying a portfolio beyond equities might be called passive alpha. We believe that one of the primary aims of the asset allocations in target date strategies is to provide this passive alpha to investors. Overall, our conclusion is that target date strategies are a very positive development for investors, although the execution of target date strategies as they have been deployed by the most popular funds needs to be substantially improved. Nothing that we are proposing is revolutionary or heretical from the perspective of investing theory. In fact, our approach is broadly consistent with results 22 from a number of well-known asset management practitioners. The potential importance of bringing a more sophisticated portfolio management approach to bear on target date strategies, as we describe here for Target Date Folios, can hardly be over emphasized. It is not unreasonable to estimate that diversified portfolios of equities and bonds may return something on the order of 4% net of inflation 23. If we are correct with regard to the value of more effective diversification (estimated to be on the order of 2% per year), fully half of the potential real returns available to investors could be missed if better asset allocation strategies are not implemented. In addition, more sophisticated risk management procedures, as described here, can be of great importance in keeping portfolio risk levels within bounds that will be acceptable to retail investors. 20 This is CAPM (single factor) alpha 21 The 2050, 2055, and 2060 Target Date Folios were launched in mid 2010 and estimates of alpha for this short a period since inception are very unstable and, consequently, are not included here urns.php

, we expect that any portfolio that includes allocations to other")

17 About Folio Investing Online brokerage Folio Investing is a division of FOLIOfn Investments Inc. The company enables investors and financial advisors to manage stocks, ETFs, and mutual funds as integrated investment portfolios called Folios that deliver control, transparency, and low cost. Investors can create their own Folios, much like creating personalized ETFs or mutual funds, or invest in over 150 Ready-to-Go Folios representing market indices, industry sectors, geographical regions, target dates, and more. The Folio Unlimited pricing plan features unlimited commission-free trading in twice-daily windows for only $29 per month or $290 per year. Ready-to-Go Folios can be managed or unmanaged, are not registered investment companies, and are offered by FOLIOfn Investments Inc., a registered broker-dealer. FOLIOfn Investments Inc., member of FINRA/SIPC, does not provide investment, tax, or legal advice.

18 Appendix A: Target Date Folio Performance

19 1. Inception date for the 2010 to 2045 Folios is 12/21/2007 and the inception date for the 2050 to 2060 Folios is 7/14/ Target Date Folio results have been reduced by 0.38% per year, to reflect an estimate for brokerage expenses. We calculated the average returns for all Target Date mutual funds in the stated categories over the stated period. The 1.46% figure is the average out-performance for 2010, 2015, 2020, 2025, 2030, 2035, 2040, and We obtained data from Yahoo! Finance and mutual fund companies to determine the population of funds and as our source for fund performance information. 3. Comparisons to 2055 and 2060 are generally not shown as most target date fund offerings do not extend to those dates. 4. Alpha is a performance statistic that shows us if a portfolio has generated returns greater than what would be expected based on its risk level, by measuring investment return beyond what can be explained by market risk. Generating higher returns by investing in a riskier portfolio will not result in positive alpha. Similarly, generating above market returns during a market decline by investing in a low-risk portfolio will not result in positive alpha. We provide these statistics to enable you to make informed choices, as different Target Date Folios have different risk levels and Alpha provides insight into the relative performance of the portfolio beyond differences in risk level. 5. These funds were not available during some of the time periods shown here, represented by NA for Not Applicable. As with any investment, investments in Target Date Folios are subject to investment risk including the loss of the principal amount invested. Investors should consider the investment objectives and risks of the Target Date Folios before investing. For more information regarding the Target Date Folios, please visit www. folioinvesting.com. The results through August 2009 are model returns. Past performance is no guarantee of future results. Average performance of the largest 3 target date mutual funds is included to help you assess whether you would have been better off investing in such mutual funds, or with the Target Date Folios by FOLIOfn, Inc. Folio Investing, FOLIOfn, Folio Institutional and Folio Advisor are registered trademarks of FOLIOfn, Inc. All Rights Reserved. Securities products and services are offered through FOLIOfn Investments, Inc., a registered broker-dealer and member FINRA/SIPC. Folios, which are special baskets of securities with specific features offered by Folio Investing can be unmanaged or managed by Folio Investing, by third parties or by you, and are not registered investment companies

A Better Approach to Target Date Strategies

February 2011 A Better Approach to Target Date Strategies Executive Summary In 2007, Folio Investing undertook an analysis of Target Date Funds to determine how these investments might be improved. As

February 2011 A Better Approach to Target Date Strategies Executive Summary In 2007, Folio Investing undertook an analysis of Target Date Funds to determine how these investments might be improved. As

Client Education. Learn About Indexing

Client Education Learn About Indexing 2 What is indexing? 4 The benefits of indexing 8 Putting indexing to work 10 Common indexes Many financial advisors use index funds as the foundation in many of their

Client Education Learn About Indexing 2 What is indexing? 4 The benefits of indexing 8 Putting indexing to work 10 Common indexes Many financial advisors use index funds as the foundation in many of their

DSIP List (Diversified Stock Income Plan)

") Kent A. Newcomb, CFA, Equity Sector Analyst Joseph E. Buffa, Equity Sector Analyst DSIP List (Diversified Stock Income Plan) Commentary from ASG's Equity Sector Analysts January 2014 Concept Review The

Kent A. Newcomb, CFA, Equity Sector Analyst Joseph E. Buffa, Equity Sector Analyst DSIP List (Diversified Stock Income Plan) Commentary from ASG's Equity Sector Analysts January 2014 Concept Review The

Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.) February, 2008

February, 2008") Fixing Target Date Strategies: Target Date Folios Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.) February, 2008 The data, views and information provided in this memorandum

Fixing Target Date Strategies: Target Date Folios Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.) February, 2008 The data, views and information provided in this memorandum

Compounding Effects in Inverse and Leveraged Funds. Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.

Compounding Effects in Inverse and Leveraged Funds Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.) August 2009 1 The data, views and information provided in this memorandum

Compounding Effects in Inverse and Leveraged Funds Prepared Specially for FOLIOfn Investments, Inc. by Quantext (Geoff Considine, Ph.D.) August 2009 1 The data, views and information provided in this memorandum

TARGET DATE COMPASS SM

TARGET DATE COMPASS SM METHODOLOGY As of April 2015 Any and all information set forth herein and pertaining to the Target Date Compass and all related technology, documentation and know-how ( information

TARGET DATE COMPASS SM METHODOLOGY As of April 2015 Any and all information set forth herein and pertaining to the Target Date Compass and all related technology, documentation and know-how ( information

PRINCIPAL ASSET ALLOCATION QUESTIONNAIRES

PRINCIPAL ASSET ALLOCATION QUESTIONNAIRES FOR GROWTH OR INCOME INVESTORS ASSET ALLOCATION PRINCIPAL ASSET ALLOCATION FOR GROWTH OR INCOME INVESTORS Many ingredients go into the making of an effective investment

PRINCIPAL ASSET ALLOCATION QUESTIONNAIRES FOR GROWTH OR INCOME INVESTORS ASSET ALLOCATION PRINCIPAL ASSET ALLOCATION FOR GROWTH OR INCOME INVESTORS Many ingredients go into the making of an effective investment

Managing risk in DC plan lineups The new alpha?

PERSPECTIVES Managing risk in DC plan lineups The new alpha? October 2013 IN BRIEF Defined contribution (DC) plan participants face a broad range of risks when investing for retirement but, historically,

PERSPECTIVES Managing risk in DC plan lineups The new alpha? October 2013 IN BRIEF Defined contribution (DC) plan participants face a broad range of risks when investing for retirement but, historically,

Professionally Managed Portfolios of Exchange-Traded Funds

ETF Portfolio Partners C o n f i d e n t i a l I n v e s t m e n t Q u e s t i o n n a i r e Professionally Managed Portfolios of Exchange-Traded Funds P a r t I : I n v e s t o r P r o f i l e Account

ETF Portfolio Partners C o n f i d e n t i a l I n v e s t m e n t Q u e s t i o n n a i r e Professionally Managed Portfolios of Exchange-Traded Funds P a r t I : I n v e s t o r P r o f i l e Account

Deutsche Alternative Asset Allocation VIP

Alternative Deutsche Alternative Asset Allocation VIP All-in-one exposure to alternative asset classes : a key piece in asset allocation Building a portfolio of stocks, bonds and cash has long been recognized

Alternative Deutsche Alternative Asset Allocation VIP All-in-one exposure to alternative asset classes : a key piece in asset allocation Building a portfolio of stocks, bonds and cash has long been recognized

Mutual Funds Made Simple. Brighten your future with investments

Mutual Funds Made Simple Brighten your future with investments About Invesco Aim When it comes to investing, your sights are set on a financial summit a college diploma, new home or secure retirement.

Mutual Funds Made Simple Brighten your future with investments About Invesco Aim When it comes to investing, your sights are set on a financial summit a college diploma, new home or secure retirement.

Redefining the safety option Target date funds and risk management

PERSPECTIVES Redefining the safety option Target date funds and risk management September 2013 IN BRIEF Defined contribution (DC) plan participants face a broad range of risks when investing for retirement

PERSPECTIVES Redefining the safety option Target date funds and risk management September 2013 IN BRIEF Defined contribution (DC) plan participants face a broad range of risks when investing for retirement

Are you in the wrong target-date fund? Now is a good time to reevaluate

Insights August 2014 Are you in the wrong target-date fund? Now is a good time to reevaluate TDFs may have different investment strategies, glide paths, and investment-related fees. Because these differences

Insights August 2014 Are you in the wrong target-date fund? Now is a good time to reevaluate TDFs may have different investment strategies, glide paths, and investment-related fees. Because these differences

Taking Target Date Fund Evaluation to the Next Level

Taking Target Date Fund Evaluation to the Next Level Lori Lucas Defined Contribution Practice Leader Callan Associates Chicago, Illinois The opinions expressed in this presentation are those of the speaker.

Taking Target Date Fund Evaluation to the Next Level Lori Lucas Defined Contribution Practice Leader Callan Associates Chicago, Illinois The opinions expressed in this presentation are those of the speaker.

SmartRetirement Mutual Fund Commentary

SmartRetirement Mutual Fund Commentary J.P.Morgan Asset Management 3 rd Quarter 2014 Performance Highlights SmartRetirement s Performance Objectives The JPMorgan SmartRetirement Mutual Funds are designed

SmartRetirement Mutual Fund Commentary J.P.Morgan Asset Management 3 rd Quarter 2014 Performance Highlights SmartRetirement s Performance Objectives The JPMorgan SmartRetirement Mutual Funds are designed

RYT Sector Weights. Price Chart

March 11, 2016 GUGGENHEIM SP 500 EQL WEIGHT TECHNOLOGY (RYT) $89.67 Risk: Med Zacks ETF Rank 2 - Buy 2 Fund Type Issuer Technology - broad RYDEXSGI RYT Sector Weights Benchmark Index SP EQUAL WEIGHT INDEX

March 11, 2016 GUGGENHEIM SP 500 EQL WEIGHT TECHNOLOGY (RYT) $89.67 Risk: Med Zacks ETF Rank 2 - Buy 2 Fund Type Issuer Technology - broad RYDEXSGI RYT Sector Weights Benchmark Index SP EQUAL WEIGHT INDEX

CHOOSING YOUR INVESTMENTS

CHOOSING YOUR INVESTMENTS KANSAS BOARD OF REGENTS MANDATORY RETIREMENT PLAN FOR ASSISTANCE GO ONLINE For more information on your retirement plan, investment education, retirement planning tools and more,

CHOOSING YOUR INVESTMENTS KANSAS BOARD OF REGENTS MANDATORY RETIREMENT PLAN FOR ASSISTANCE GO ONLINE For more information on your retirement plan, investment education, retirement planning tools and more,

Considerations for Plan Sponsors: CUSTOM TARGET DATE STRATEGIES

PRICE PERSPECTIVE April 2015 Considerations for Plan Sponsors: CUSTOM TARGET DATE STRATEGIES In-depth analysis and insights to inform your decision making. EXECUTIVE SUMMARY Defined contribution plan sponsors

PRICE PERSPECTIVE April 2015 Considerations for Plan Sponsors: CUSTOM TARGET DATE STRATEGIES In-depth analysis and insights to inform your decision making. EXECUTIVE SUMMARY Defined contribution plan sponsors

The Role of Alternative Investments in a Diversified Investment Portfolio

The Role of Alternative Investments in a Diversified Investment Portfolio By Baird Private Wealth Management Introduction Traditional Investments Domestic Equity International Equity Taxable Fixed Income

The Role of Alternative Investments in a Diversified Investment Portfolio By Baird Private Wealth Management Introduction Traditional Investments Domestic Equity International Equity Taxable Fixed Income

A portfolio that matches your plans.

A portfolio that matches your plans. Amerivest Core Portfolios powered by Morningstar Associates Expert investment management Tailored portfolio recommendations Straightforward, competitive pricing Dedicated

A portfolio that matches your plans. Amerivest Core Portfolios powered by Morningstar Associates Expert investment management Tailored portfolio recommendations Straightforward, competitive pricing Dedicated

Making the Case for Managed Accounts. For financial professional use only

Making the Case for Managed Accounts For financial professional use only Case Study Findings Participants enrolled in our managed account service will see, on average, a 19% increase in projected annual

Making the Case for Managed Accounts For financial professional use only Case Study Findings Participants enrolled in our managed account service will see, on average, a 19% increase in projected annual

One-Stop-Shopping Investment For Retirement Planning

TARGET DATE RETIREMENT FUNDS One-Stop-Shopping Investment For Retirement Planning Investing for retirement can be challenging if you re not an expert. Here s a simple choice for your retirement investing...

TARGET DATE RETIREMENT FUNDS One-Stop-Shopping Investment For Retirement Planning Investing for retirement can be challenging if you re not an expert. Here s a simple choice for your retirement investing...

With interest rates at historically low levels, and the U.S. economy showing continued strength,

Managing Interest Rate Risk in Your Bond Holdings THE RIGHT STRATEGY MAY HELP FIXED INCOME PORTFOLIOS DURING PERIODS OF RISING INTEREST RATES. With interest rates at historically low levels, and the U.S.

Managing Interest Rate Risk in Your Bond Holdings THE RIGHT STRATEGY MAY HELP FIXED INCOME PORTFOLIOS DURING PERIODS OF RISING INTEREST RATES. With interest rates at historically low levels, and the U.S.

REIT QUICK FACTS GUIDE

REIT QUICK FACTS GUIDE FOR FINANCIAL ADVISORS Guidelines for Strategic Portfolio Diversification FINRA-Reviewed Fact Sheets on Stock Exchange-Listed Equity REITs Additional References for Advisors THERE

REIT QUICK FACTS GUIDE FOR FINANCIAL ADVISORS Guidelines for Strategic Portfolio Diversification FINRA-Reviewed Fact Sheets on Stock Exchange-Listed Equity REITs Additional References for Advisors THERE

T. Rowe Price Target Retirement 2030 Fund Advisor Class

T. Rowe Price Target Retirement 2030 Fund Advisor Class Supplement to Summary Prospectus Dated October 1, 2015 Effective February 1, 2016, the T. Rowe Price Mid-Cap Index Fund and the T. Rowe Price Small-Cap

T. Rowe Price Target Retirement 2030 Fund Advisor Class Supplement to Summary Prospectus Dated October 1, 2015 Effective February 1, 2016, the T. Rowe Price Mid-Cap Index Fund and the T. Rowe Price Small-Cap

Exchange Traded Funds

LPL FINANCIAL RESEARCH Exchange Traded Funds February 16, 2012 What They Are, What Sets Them Apart, and What to Consider When Choosing Them Overview 1. What is an ETF? 2. What Sets Them Apart? 3. How Are

LPL FINANCIAL RESEARCH Exchange Traded Funds February 16, 2012 What They Are, What Sets Them Apart, and What to Consider When Choosing Them Overview 1. What is an ETF? 2. What Sets Them Apart? 3. How Are

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

UNDERSTANDING MUTUAL FUNDS. TC83038(0215)3 Cat No 64095(0215)

3 Cat No 64095(0215)") UNDERSTANDING MUTUAL FUNDS 10 % TC83038(0215)3 Cat No 64095(0215) Investing your hard earned money comes with some big decisions. So, before you invest, you need to ask yourself a simple question: What

UNDERSTANDING MUTUAL FUNDS 10 % TC83038(0215)3 Cat No 64095(0215) Investing your hard earned money comes with some big decisions. So, before you invest, you need to ask yourself a simple question: What

Participant Preferences in Target Date Funds: Fresh Insights

Participant Preferences in Target Date Funds: Fresh Insights Findings, Insights and Opportunities White Paper January 216 Research by Voya Investment Management Not FDIC Insured May Lose Value No Bank

Participant Preferences in Target Date Funds: Fresh Insights Findings, Insights and Opportunities White Paper January 216 Research by Voya Investment Management Not FDIC Insured May Lose Value No Bank

ETFs as Investment Options in 401(k) Plans

Plans") T. ROWE PRICE ETFs as Investment Options in 401(k) Plans Considerations for Plan Sponsors By Toby Thompson, CFA, CAIA, T. Rowe Price Defined Contribution Investment Specialist Retirement Insights EXECUTIVE

T. ROWE PRICE ETFs as Investment Options in 401(k) Plans Considerations for Plan Sponsors By Toby Thompson, CFA, CAIA, T. Rowe Price Defined Contribution Investment Specialist Retirement Insights EXECUTIVE

Making Sense of Market Volatility: Retirement Planning Strategies for the Everyday Investor. October, 2008

Making Sense of Market Volatility: Retirement Planning Strategies for the Everyday Investor October, 2008 1 Market Ups and Downs Recent news is full of anxiety-causing developments: Credit crunch Bank

Making Sense of Market Volatility: Retirement Planning Strategies for the Everyday Investor October, 2008 1 Market Ups and Downs Recent news is full of anxiety-causing developments: Credit crunch Bank

Contents. 1 Asset allocation 2 Sub-asset allocation 3 Active/passive combinations 4 Asset location

ETF Strategies Contents Why ETFs? Strategic uses for ETFs 1 Asset allocation 2 Sub-asset allocation 3 Active/passive combinations 4 Asset location Tactical uses for ETFs 1 Portfolio completion 2 Cash

ETF Strategies Contents Why ETFs? Strategic uses for ETFs 1 Asset allocation 2 Sub-asset allocation 3 Active/passive combinations 4 Asset location Tactical uses for ETFs 1 Portfolio completion 2 Cash

Structured Products. Designing a modern portfolio

ab Structured Products Designing a modern portfolio Achieving your personal goals is the driving motivation for how and why you invest. Whether your goal is to grow and preserve wealth, save for your children

ab Structured Products Designing a modern portfolio Achieving your personal goals is the driving motivation for how and why you invest. Whether your goal is to grow and preserve wealth, save for your children

ThoughtCapital. Strategic Diversification for a Lifetime Principal LifeTime Portfolios

Strategic Diversification for a Lifetime Principal LifeTime Portfolios The Principal LifeTime portfolios were launched in response to participants increasing interest in having Do It For Me investment

Strategic Diversification for a Lifetime Principal LifeTime Portfolios The Principal LifeTime portfolios were launched in response to participants increasing interest in having Do It For Me investment

Obligation-based Asset Allocation for Public Pension Plans

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

Mutual Fund Investing Exam Study Guide

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Elimination of the Fidelity Growth & Income Portfolio NUSCO 401k Plan October, 2008

Elimination of the Fidelity Growth & Income Portfolio NUSCO 401k Plan October, 2008 Dear Participant: The Northeast Utilities 401k Advisory Committee, which routinely reviews investments offered under

Elimination of the Fidelity Growth & Income Portfolio NUSCO 401k Plan October, 2008 Dear Participant: The Northeast Utilities 401k Advisory Committee, which routinely reviews investments offered under

Target-Date Funds: It s Time to Take a Closer Look

Target-Date Funds: It s Time to Take a Closer Look Executive summary Over the past few years, retirement plans have seen significant changes in their investment structures, as well as the level of fiduciary

Target-Date Funds: It s Time to Take a Closer Look Executive summary Over the past few years, retirement plans have seen significant changes in their investment structures, as well as the level of fiduciary

Interest Rates and Inflation: How They Might Affect Managed Futures

Faced with the prospect of potential declines in both bonds and equities, an allocation to managed futures may serve as an appealing diversifier to traditional strategies. HIGHLIGHTS Managed Futures have

Faced with the prospect of potential declines in both bonds and equities, an allocation to managed futures may serve as an appealing diversifier to traditional strategies. HIGHLIGHTS Managed Futures have

Diversified Alternatives Index

The Morningstar October 2014 SM Diversified Alternatives Index For Financial Professional Use Only 1 5 Learn More indexes@morningstar.com +1 12 84-75 Contents Executive Summary The Morningstar Diversified

The Morningstar October 2014 SM Diversified Alternatives Index For Financial Professional Use Only 1 5 Learn More indexes@morningstar.com +1 12 84-75 Contents Executive Summary The Morningstar Diversified

Asset allocation A key component of a successful investment strategy

Asset allocation A key component of a successful investment strategy This guide has been produced for educational purposes only and should not be regarded as a substitute for investment advice. Vanguard

Asset allocation A key component of a successful investment strategy This guide has been produced for educational purposes only and should not be regarded as a substitute for investment advice. Vanguard

RISK ASSESSMENT QUESTIONNAIRE

Time Horizon 6/14 Your current situation and future income needs. 1. What is your current age? 2. When do you expect to start drawing income? A Less than 45 A Not for at least 20 years B 45 to 55 B In

Time Horizon 6/14 Your current situation and future income needs. 1. What is your current age? 2. When do you expect to start drawing income? A Less than 45 A Not for at least 20 years B 45 to 55 B In

Evaluating Target Date Funds. 2003 2013 Multnomah Group, Inc. All Rights Reserved.

2003 2013 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In that role, Scott leads Multnomah

2003 2013 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In that role, Scott leads Multnomah

Target Date Fund Selection: More Than Simply Active vs. Passive

Target Date Fund Selection: More Than Simply Active vs. Passive White Paper October 2015 Not FDIC Insured May Lose Value No Bank Guarantee INVESTMENT MANAGEMENT Table of Contents Executive Summary 2 Introduction

Target Date Fund Selection: More Than Simply Active vs. Passive White Paper October 2015 Not FDIC Insured May Lose Value No Bank Guarantee INVESTMENT MANAGEMENT Table of Contents Executive Summary 2 Introduction

white paper Challenges to Target Funds James Breen, President, Horizon Fiduciary Services

Challenges to Target Funds James Breen, President, Horizon Fiduciary Services Since their invention in the early 1990 s Target Date Funds have become a very popular investment vehicle, particularly with

Challenges to Target Funds James Breen, President, Horizon Fiduciary Services Since their invention in the early 1990 s Target Date Funds have become a very popular investment vehicle, particularly with

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS.

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS December 31, 2014 Investment Adviser: MATSON MONEY, INC. 5955 Deerfield

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS December 31, 2014 Investment Adviser: MATSON MONEY, INC. 5955 Deerfield

Six strategies for volatile markets

Six strategies for volatile markets When markets get choppy, it pays to have a plan for your investments, and to stick to it. by Fidelity Viewpoints 06/30/2016 No investor likes to hear that the market

Six strategies for volatile markets When markets get choppy, it pays to have a plan for your investments, and to stick to it. by Fidelity Viewpoints 06/30/2016 No investor likes to hear that the market

CMG Managed High Yield Bond Program. 2015 CMG Capital Management Group, Inc.

CMG Managed High Yield Bond Program About CMG CMG is a Registered Investment Advisor located in King of Prussia, Pennsylvania founded in 1992 by Stephen Blumenthal. Since our inception, CMG has embraced

CMG Managed High Yield Bond Program About CMG CMG is a Registered Investment Advisor located in King of Prussia, Pennsylvania founded in 1992 by Stephen Blumenthal. Since our inception, CMG has embraced

RISK PARITY ABSTRACT OVERVIEW

MEKETA INVESTMENT GROUP RISK PARITY ABSTRACT Several large plans, including the San Diego County Employees Retirement Association and the State of Wisconsin, have recently considered or decided to pursue

MEKETA INVESTMENT GROUP RISK PARITY ABSTRACT Several large plans, including the San Diego County Employees Retirement Association and the State of Wisconsin, have recently considered or decided to pursue

Active vs. Passive Money Management

Active vs. Passive Money Management Exploring the costs and benefits of two alternative investment approaches By Baird s Asset Manager Research Synopsis Proponents of active and passive investment management

Active vs. Passive Money Management Exploring the costs and benefits of two alternative investment approaches By Baird s Asset Manager Research Synopsis Proponents of active and passive investment management

30% 5% of fixed income mutual funds paid capital gains in 2015

FIXED INCOME ETFs: NEW ASSET CLASS, SAME BENEFITS Exchange Traded Funds ( ETFs ) first appealed to equity investors, providing efficient access to the world s stock markets and they have revolutionized

FIXED INCOME ETFs: NEW ASSET CLASS, SAME BENEFITS Exchange Traded Funds ( ETFs ) first appealed to equity investors, providing efficient access to the world s stock markets and they have revolutionized

Are You in the Wrong Target-Date Fund?

Insights August 2014 Are You in the Wrong Target-Date Fund? Now Is a Good Time to Reevaluate TDFs may have different investment strategies, glide paths, and investment-related fees. Because these differences

Insights August 2014 Are You in the Wrong Target-Date Fund? Now Is a Good Time to Reevaluate TDFs may have different investment strategies, glide paths, and investment-related fees. Because these differences

Evaluating Target Date Funds. 2003 2015 Multnomah Group, Inc. All Rights Reserved.

2003 2015 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In this role, Scott leads Multnomah

2003 2015 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In this role, Scott leads Multnomah

Our time-tested approach to investing is very straightforward. And we re ready to make it work for you.

What Works Our time-tested approach to investing is very straightforward. And we re ready to make it work for you. Three important steps. Ten effective principles. Three important steps. Ten effective

What Works Our time-tested approach to investing is very straightforward. And we re ready to make it work for you. Three important steps. Ten effective principles. Three important steps. Ten effective

Guide to mutual fund investing. Start with the basics

Guide to mutual fund investing Start with the basics Pursue your financial goals Why do you invest? For a rainy day? A secure retirement? Funding a college tuition? Having a specific goal in mind will

Guide to mutual fund investing Start with the basics Pursue your financial goals Why do you invest? For a rainy day? A secure retirement? Funding a college tuition? Having a specific goal in mind will

Target-date funds: the to versus through dilemma

November 14 Target-date funds: the to versus through dilemma Leo M. Zerilli, CIMA Head of Investments John Hancock Investments Recent U.S. Department of Labor guidance on target-date funds provides helpful

November 14 Target-date funds: the to versus through dilemma Leo M. Zerilli, CIMA Head of Investments John Hancock Investments Recent U.S. Department of Labor guidance on target-date funds provides helpful

Value? Growth? Or Both?

INDEX INSIGHTS Value? Growth? Or Both? By: David A. Koenig, CFA, FRM, Investment Strategist 1 APRIL 2014 Key points: Growth and value styles offer different perspectives on potential investment opportunities,

INDEX INSIGHTS Value? Growth? Or Both? By: David A. Koenig, CFA, FRM, Investment Strategist 1 APRIL 2014 Key points: Growth and value styles offer different perspectives on potential investment opportunities,

Keeping it Simple: White Paper. Lifestyle Funds: A Streamlined Approach

Keeping it Simple: Lifestyle Funds for Retirement Planning Retirement investors who suspect that things are more complicated than they used to be can take heart from the findings of a new study by American

Keeping it Simple: Lifestyle Funds for Retirement Planning Retirement investors who suspect that things are more complicated than they used to be can take heart from the findings of a new study by American

Target-Date Funds: The Search for Transparency

Target-Date Funds: The Search for Transparency Presented by: Joachim Wettermark, Treasurer Salesforce.com, inc. Linda Ruiz-Zaiko, President Financial, Inc. Qualified Default Investment Alternative (QDIA)

Target-Date Funds: The Search for Transparency Presented by: Joachim Wettermark, Treasurer Salesforce.com, inc. Linda Ruiz-Zaiko, President Financial, Inc. Qualified Default Investment Alternative (QDIA)

RESP Investment Strategies

RESP Investment Strategies Registered Education Savings Plans (RESP): Must Try Harder Graham Westmacott CFA Portfolio Manager PWL CAPITAL INC. Waterloo, Ontario August 2014 This report was written by Graham

RESP Investment Strategies Registered Education Savings Plans (RESP): Must Try Harder Graham Westmacott CFA Portfolio Manager PWL CAPITAL INC. Waterloo, Ontario August 2014 This report was written by Graham

Fixed Income Investing

Fixed Income Investing Why Invest in Fixed Income Fixed income securities (bonds) are a fundamental part of an investing plan for most investors. There are many types of bonds along with varied approaches

Fixed Income Investing Why Invest in Fixed Income Fixed income securities (bonds) are a fundamental part of an investing plan for most investors. There are many types of bonds along with varied approaches

Exchange Traded Funds A Brief Introduction

Exchange Traded Funds A Brief Introduction spdrs.com What You Need to Know about ETFs ETF Basics Potential Benefits of ETFs ETFs versus Mutual Funds The Role of ETFs in Your Portfolio Our Next Steps Frequently

Exchange Traded Funds A Brief Introduction spdrs.com What You Need to Know about ETFs ETF Basics Potential Benefits of ETFs ETFs versus Mutual Funds The Role of ETFs in Your Portfolio Our Next Steps Frequently

BRINKER CAPITAL OVERVIEW. Helping You Invest with Confidence

BRINKER CAPITAL OVERVIEW Helping You Invest with Confidence PARTIALLY INVESTED PERIODIC INVESTMENT FULLY INVESTED Unwavering Focus on Investment Excellence For more than 25 years, Brinker Capital has been

BRINKER CAPITAL OVERVIEW Helping You Invest with Confidence PARTIALLY INVESTED PERIODIC INVESTMENT FULLY INVESTED Unwavering Focus on Investment Excellence For more than 25 years, Brinker Capital has been

Defensive equity. A defensive strategy to Canadian equity investing

Defensive equity A defensive strategy to Canadian equity investing Adam Hornung, MBA, CFA, Institutional Investment Strategist EXECUTIVE SUMMARY: Over the last several years, academic studies have shown

Defensive equity A defensive strategy to Canadian equity investing Adam Hornung, MBA, CFA, Institutional Investment Strategist EXECUTIVE SUMMARY: Over the last several years, academic studies have shown

smart Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan INVEST

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

Rethinking fixed income. By Trevor t. Oliver

12 Rethinking fixed income By Trevor t. Oliver Summer/Fall 2012 The Participant : Issue 02 ssga.com/dc/theparticipant 13 The landscape for this asset class has changed. Our approach should too. Investors

12 Rethinking fixed income By Trevor t. Oliver Summer/Fall 2012 The Participant : Issue 02 ssga.com/dc/theparticipant 13 The landscape for this asset class has changed. Our approach should too. Investors

The unique value of Target-Date Funds

The unique value of Target-Date Funds By Jake Gilliam, Senior Multi-Asset Class Portfolio Strategist supporting Charles Schwab Investment Management September, 2015 Target-Date Funds are excellent low-maintenance

The unique value of Target-Date Funds By Jake Gilliam, Senior Multi-Asset Class Portfolio Strategist supporting Charles Schwab Investment Management September, 2015 Target-Date Funds are excellent low-maintenance

Guide to Understanding Your Northrop Grumman 401(k) Investments

Investments") Guide to Understanding Your Northrop Grumman 401(k) Investments FOR INFORMATIONAL PURPOSES ONLY. THE OPINIONS ARE THOSE OF SAGE CAPITAL AND DO NOT REFLECT THOSE OF NORTHROP GRUMMAN. Understanding Your

Guide to Understanding Your Northrop Grumman 401(k) Investments FOR INFORMATIONAL PURPOSES ONLY. THE OPINIONS ARE THOSE OF SAGE CAPITAL AND DO NOT REFLECT THOSE OF NORTHROP GRUMMAN. Understanding Your

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

RETIREMENT INSIGHTS. Is It Time to Rebalance Your Plan Investments? Mutual Fund Categories: A Primer for New Investors

RETIREMENT INSIGHTS July 2014 Your HFS Team Heffernan Financial Services 188 Spear Street, Suite 550 San Francisco, CA 94105 800-437-0045 rebeccat@heffgroup.com www.heffgroupfs.com CA Insurance Lic# 0I18899

RETIREMENT INSIGHTS July 2014 Your HFS Team Heffernan Financial Services 188 Spear Street, Suite 550 San Francisco, CA 94105 800-437-0045 rebeccat@heffgroup.com www.heffgroupfs.com CA Insurance Lic# 0I18899

5Strategic. decisions for a sound investment policy

5Strategic decisions for a sound investment policy 1 An investment policy sets your course for the long term. Managers of billion-dollar pension and endowment funds know it s nearly impossible to beat

5Strategic decisions for a sound investment policy 1 An investment policy sets your course for the long term. Managers of billion-dollar pension and endowment funds know it s nearly impossible to beat

Wealth Management Solutions

Wealth Management Solutions Invest in the Future Life has significant moments. Making sure you re prepared for them is important. But what can you do when the pace of your life leaves you little time to

Wealth Management Solutions Invest in the Future Life has significant moments. Making sure you re prepared for them is important. But what can you do when the pace of your life leaves you little time to

Building an Investment Strategy

Building an Investment Strategy Building an investment strategy that meets your risk tolerance and investment objectives is critical to successfully preparing for retirement. There are three key steps

Building an Investment Strategy Building an investment strategy that meets your risk tolerance and investment objectives is critical to successfully preparing for retirement. There are three key steps

INVESTMENT OBJECTIVE TTM U.S. CORE ETF DETAILS HIGHLIGHTS

Our uncertain global economy presents a new paradigm for investing. Protecting the wealth you have accumulated is as important as growth. 1/31/2015 Markets move in recognizable trends and countertrends.

Our uncertain global economy presents a new paradigm for investing. Protecting the wealth you have accumulated is as important as growth. 1/31/2015 Markets move in recognizable trends and countertrends.

ishares MINIMUM VOLATILITY SUITE SEEKING TO WEATHER THE MARKET S UP AND DOWNS

ishares MINIMUM VOLATILITY SUITE SEEKING TO WEATHER THE MARKET S UP AND DOWNS Table of Contents 1 Introducing the ishares Minimum Volatility Suite... 02 2 Why Consider the ishares Minimum Volatility Suite?...

ishares MINIMUM VOLATILITY SUITE SEEKING TO WEATHER THE MARKET S UP AND DOWNS Table of Contents 1 Introducing the ishares Minimum Volatility Suite... 02 2 Why Consider the ishares Minimum Volatility Suite?...

NPH Fixed Income Research Update. Bob Downing, CFA. NPH Senior Investment & Due Diligence Analyst

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

Fixed Income Asset Allocation

Fixed Income Asset Allocation j a n n e y fixed income strat e g y While 2015 finished off with big spread widening in high yield, strong performance of our favorite sector, munis, overwhelmed losses in

Fixed Income Asset Allocation j a n n e y fixed income strat e g y While 2015 finished off with big spread widening in high yield, strong performance of our favorite sector, munis, overwhelmed losses in

American Funds Target Date Retirement Series

American Funds Target Date Retirement Series Semi-annual report for the six months ended April 30, 2016 Depending on the proximity to its target date, the fund will seek to achieve the following objectives

American Funds Target Date Retirement Series Semi-annual report for the six months ended April 30, 2016 Depending on the proximity to its target date, the fund will seek to achieve the following objectives

EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX

DECEMBER 2008 Independent advice for the institutional investor EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX EXECUTIVE SUMMARY The CBOE S&P 500 PutWrite Index (ticker symbol

DECEMBER 2008 Independent advice for the institutional investor EVALUATING THE PERFORMANCE CHARACTERISTICS OF THE CBOE S&P 500 PUTWRITE INDEX EXECUTIVE SUMMARY The CBOE S&P 500 PutWrite Index (ticker symbol

Distribution-Focused Strategies A cash flow strategy for retirement

Distribution-Focused Strategies A cash flow strategy for retirement Designed by advisors to meet the need for steady cash flows in retirement with extensive flexibility and control all with low costs.

Distribution-Focused Strategies A cash flow strategy for retirement Designed by advisors to meet the need for steady cash flows in retirement with extensive flexibility and control all with low costs.

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.

![Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.](/thumbs/40/20590846.jpg "Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.") Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Score. Stifel CONQUEST Portfolios. Research-Driven Portfolios PORTFOLIO STRATEGY EXCHANGE TRADED FUNDS. Ease of Diversification

Stifel CONQUEST Portfolios PORTFOLIO STRATEGY The Washington Crossing Advisors Stifel CONQUEST Portfolios seek to add value by actively allocating assets among U.S. equities, bonds, commodities, and foreign

Stifel CONQUEST Portfolios PORTFOLIO STRATEGY The Washington Crossing Advisors Stifel CONQUEST Portfolios seek to add value by actively allocating assets among U.S. equities, bonds, commodities, and foreign

BlackRock Diversa Volatility Control Index *

BlackRock Diversa Volatility Control Index * FOR FIXED INDEX ANNUITIES * Formally known as BlackRock ibld Diversa VC7 ER Index NOT FOR USE IN IOWA FA7363 (2-5) 02545 205 Forethought In order to protect

BlackRock Diversa Volatility Control Index * FOR FIXED INDEX ANNUITIES * Formally known as BlackRock ibld Diversa VC7 ER Index NOT FOR USE IN IOWA FA7363 (2-5) 02545 205 Forethought In order to protect

An Attractive Income Option for a Strategic Allocation

An Attractive Income Option for a Strategic Allocation Voya Senior Loans Suite A strategic allocation provides potential for high and relatively steady income through most credit and rate cycles Improves

An Attractive Income Option for a Strategic Allocation Voya Senior Loans Suite A strategic allocation provides potential for high and relatively steady income through most credit and rate cycles Improves

Evolving beyond plain vanilla ETFs

SCHWAB CENTER FOR FINANCIAL RESEARCH Journal of Investment Research Evolving beyond plain vanilla ETFs Anthony B. Davidow, CIMA Vice President, Alternative Beta and Asset Allocation Strategist, Schwab

SCHWAB CENTER FOR FINANCIAL RESEARCH Journal of Investment Research Evolving beyond plain vanilla ETFs Anthony B. Davidow, CIMA Vice President, Alternative Beta and Asset Allocation Strategist, Schwab

Geoff Considine, Ph.D.