Zillow-Trulia Good deal or tragic mistake?

|

|

|

- Christal Shelton

- 7 years ago

- Views:

Transcription

1 Zillow-Trulia Good deal or tragic mistake? Florida Southern College MBA Represented by: Melanie McDaniel James Pelham Michael Scott

2 Abstract Pending FTC approval, the $3.5 billion acquisition of Trulia by rival Zillow will create an online media giant, poised to capture up to 71% of unique web traffic to real estate sites. Reductions in cost due to SG&A overlap, increased R&D capabilities, and pricing power as a result of web traffic volume are the pillars on which this deal was founded. The forecasted market share and growth rates drive sentiment that the Zillow-Trulia deal wields a significant long-term upside for investors. We propose, however, that these assertions do not offset the negative internal and external factors surrounding this deal. The cost saving assumption is marginal compared to combined expense growth. Zillow is still overvalued and the fixed rate stock offer is terrible for Trulia stockholders. Furthermore, the pricing power preposition is heavily reliant on underlying contractual, market, and industry assumptions. Ultimately, this deal requires implementation of extensive and alternative growth strategies for long-term sustainability and success. Analysis of the Deal The acquisition offer presents potential upsides for both companies. Given that it is an all-stock deal, Trulia gets fully integrated as opposed to a cash option where Zillow would be free to purchase only the assets it wants and sell the rest. Additionally, Trulia receives the benefit of Zillow s liquidity. These appear to be the only upsides for Trulia. Zillow, on the other hand, receives much more. Zillow s key feature is its proprietary Zestimate algorithm for homeowners to check their home s value. Consumer sentiment, as a whole, is that the Zestimate feature is inaccurate or outdated in most regions, because it only considers value based on actual sales of comparable homes. The company has also pushed growth at the cost of speed and an easier user interface. Through its acquisition of Trulia, Zillow is getting a more data-driven and easy to use website. The company will benefit significantly from the abundance

3 of data at Trulia s command as well as having already begun to implement a new web design with more streamlined features. Operationally, Zillow is a predominately seller driven business whereas Trulia focuses on buyers and renters. A merging of the two companies specialized functions makes the most sense if the Zillow-Trulia deal hopes to be successful. Web-based real estate search sites, in the short-term, will not have a significant impact on the way people are buying homes. Home buyers still look to real estate agents to do the grunt work for them and that will be the case for a long time. The deal gives Zillow access to the necessary resources to change the future of the real estate industry and compete with brick and mortar realtor companies, some of which intend on developing their own web platform to compete with Zillow and Trulia. Pending closure of the deal, Zillow will walk away with all the upsides at absolutely minimal risk with respect to the acquisition. The terms of the Zillow and Trulia Merger Agreement further advance the position that Zillow is the advantageous party here. Trulia is severely limited in its ability to conduct business until the deal closes or is terminated. Pursuant to Section 5.01 of the Merger Agreement, Trulia cannot do anything but sustain operations without written consent from Zillow. [See Figure 1 for more detail]. This section enumerates 17 different material operations that Trulia cannot do, exposing the company to serious long-term risk should the acquisition fail. As with most contracts, there is language to financially protect both parties in the event the acquisition is not consummated. Each party owes a duty unto the other to pay a fee of $69.8 million in the event the contract is terminated as a result of entering into a Competing

4 Transaction Proposal. Trulia is also owed a duty by Zillow to pay $150 million if the deal does not go through on antitrust issues a fact that some analysts have keyed in on as being a huge detriment to Zillow. The contractual language, however, only obligates Zillow to pay this fee if it does not make reasonable efforts to obtain the necessary antitrust approvals. The requisite effort is reasonable by any M&A standards, limiting Zillow s exposure to the failure. The Merger Agreement also provides Zillow with the power to walk away from the deal if the government attempts to place any restrictions on the acquisition. Traditional merger clauses include an and statement restrictions exist and they adversely affect the company here, Zillow attorneys have included an or statement allowing Zillow the right to walk away regardless of whether or not the materially adverse condition is met. The Agreement was made on an all-stock basis, granting Trulia shareholders.444 shares of the newly combined company for every one stock of Trulia they own. (Pursuant to the Agreement, partial shares are redeemable for cash value). At the announcement of the acquisition, this meant Trulia was valued at over $70 per share, a 25% premium on the trading price that day. Again, however, Trulia is trounced by this deal. Since the announcement, both company s stock prices have decayed. Trulia was trading at $56.35 on July 25 and is now trading at $46.65, a decline in value of 17.2%. Accounting for the fixed exchange rate, if the deal were to close today, one Trulia share would be worth $ That is a decline in value of 32.5% from the premium price of $70.53 at the time the acquisition was announced. The valuation premium has been completely erased and Trulia is now trading at a 2% premium.

5 Analysis of the Future Neither company will survive the failure of this merger. Assuming Zillow fails to comply with the reasonable efforts standard in the Merger Agreement, the company will owe Trulia $150M. With current cash and cash equivalent holdings of $384 million, Zillow s failure to comply would cost them 40% of their current assets. The likelihood of this happening is marginal at best, as Zillow s legal team has a proven ability to beat the system. Should either company elect to enter into a competing acquisition, the associated $69.8 million dollar fee would wipe out 17% of Zillow s current assets or 30% of Trulia s $238 million. Seeing as this is another unlikely event, we now turn to operational analyses. Trulia s outlook pre-merger was bleak. The company s market share of organic search traffic has been in decline since the middle of 2012 [see Figure 2]. Losses attributable to shareholders are also increasing rapidly as the gap between revenue and net income has grown exponentially. Zillow is not safe from this trend either. Between 2012 and 2013, Zillow outspent its revenue growth so drastically, it completely reversed its YOY net income growth trends to below its pre- IPO levels. [Graphic representation of this data can be found in Figures 3 & 4 of the Appendix]. Neither company has included any statement in their 2013 annual reports or 2014 semi-annual reports indicating intentions, processes, or other means of cost cutting to reverse these trends. Rather, management of both Zillow and Trulia have stated that they will continue to scale the companies though expansionary spending. This poses a serious problem for Trulia. Given the language of the Agreement, they cannot make significant operational changes without Zillow s

6 permission. Trulia has thereby signed away its ability to better position itself in the market for long-term sustainability should the merger fail. A competitive analysis reveals Trulia and Zillow also face stiff competition from current and prospective real estate web sites. Move.com was recently acquired by News Corp with a nearly immediate potential to create an online brokerage to compete with brick and mortar realtors. Citron research published a portion of a Q&A between investors and Realogy the largest franchise in real estate agency [see Figure 5 for the excerpt]. In the discussion, CEO Bruce Zipf explicitly states they are building a site to directly compete with Zillow and Trulia to create their own business opportunities. This is possibly the most damning evidence that supports failure for both companies regardless of the merger. Realogy makes up 25% of the U.S. s real estate agency, with the next three competitors totaling only slightly above Realogy s number of agents. Furthermore, the company controls over 20% of the current Zillow/Trulia inventory, mostly in urban areas where revenue for advertising is highest. This is important to note because Realogy s internal site also has a visitor to lead conversion rate of 5.6%, 250% greater than all externally sourced leads [see Figure 6]. The company s advent and implementation of its own consumer facing website will directly and adversely impact the bottom line of Zillow and Trulia, jointly and separately. Should the merger succeed and Zillow-Trulia begins to operate jointly, the combined company has at least bought itself some time to figure out how to monetize a web-based real estate service platform. To recommend a buy in the combined company, however, an assumption would have

7 to be made that the specialized functions of Zillow and Trulia will be merged into one platform focusing on both the buyer and seller. The company would also have to shift its strategy from growth by expense to growth by diversified acquisition and partnership contracts. Eventually, Zillow-Trulia would have to become a one-stop-shop for home buyers. The market presents a unique opportunity where technology-mediated solutions may overtake much of the legacy role of the real estate broker. If handled appropriately, a single platform could manage the entire real estate purchase experience. This would result in higher lead conversions for realtors, making advertising on the Zillow-Trulia website more attractive thereby allowing the combined company to capitalize on the remaining 96% of the $12 billion spent on real estate advertising. Rampant cost cutting would also have to occur. The proposed $100 million savings post-merger will take until 2016 to be fully implemented, and is going to come mostly in the form of streamlining management and eliminating overlapping technology expenses. The biggest cost to both companies is their advertising expense to generate web traffic with the hopes of creating a power play in pricing negotiations. As outlined above, this is a dangerous game considering the shifting trends in the competitive outlook of the online real estate market and cost cutting will work to mitigate the risk associated with failure of the pricing power strategy. Assuming the companies independently release statements outlining a larger cost reduction strategy for longterm growth, we could be swayed to revise to a buy recommendation. Trading around the Zillow-Trulia Deal The foundation of our trading recommendation is based on a neutral sentiment with significant hedging measures. We propose that by using the right call options, an investor could realize over

8 1000% gain on his or her investment with all the downside risk completely hedged away by a merger arbitrage investment strategy. In order to substantially maximize possible returns on the Zillow and Trulia merger, a combined option schedule will be used. As previously described, the Merger Arbitrage strategy will bring a fixed 3.87% return as of October 31, We will use this profit to fund our Total Cost for the option strategy. After investigations, we chose to use a combined Condor and Butterfly spread with March options. This will allow us to capitalize on the pricing of Trulia around the months leading up to the merger. A condor spread [see Figure 7] is a simple option strategy in which the strategists employ a limited-risk, non-directional trade strategy to capture returns based off of low to limited volatility in stocks. In this case, we are going to buy two MAR calls and sell two MAR calls. The two MAR calls we buy will contain an ITM (in-the-money) call and an OTM (out-the-money) call. The two MAR calls we sell will also contain an ITM and OTM call. Of the two calls that are ITM, we will buy the lower strike price. Of the two calls that are OTM, we will buy the higher strike price call. This should create a spread that can be seen in the graph in Appendix X. A condor has limited profit and it can be achieved at maximum when the underlying stock price closes between the middle two strike prices. If the underlying stock price closes outside the maximum or minimum strike prices, this strategy results in the maximum loss of the cost of establishing the position, or net total cost. In addition to establishing a condor, we want to recommend adding a butterfly spread [see Figure 8]. The butterfly spread is a limited-risk, limited-profit strategy. While the condor has four strike prices, the butterfly only has three prices and results in a more pointed graph, as seen in

9 Appendix X. To establish the spread, a trader would purchase an ITM MAR call and an OTM MAR call, and sell two ATM (at-the-money) MAR calls. In this strategy, the maximum profit is realized when the underlying stock price doesn t change from the ATM calls, as only the lower strike call will be ITM. If the price of the underlying stock appreciates past the OTM call or decays past the ITM call, then the trader would realize the maximum loss possible, which is the net cost of establishing this position. To show this strategy with actually numbers, assume the price of contracts on October 31, Trulia (TRLA) closed at $ To establish our combined condor-butterfly spread with a single set of contracts, you would need to purchase the following contracts: 2 MAR 42 with a $16.80 premium and 2 MAR 50 with an $11.40 premium. Then you would need to sell the following contracts: 1 MAR 43 with $16.10 and 3 MAR 47 with a $13.30 premium. This spread results in a net cost of $0.40 to establish. With $41.96 as a minimum and $50.08 maximum, this spread will receive a profit between the two boundaries. Outside these boundaries, an investor will realize a loss up to the maximum of $0.40. The maximum gain for an investor will be just passed $47.00 around $5.25 per set of contracts. The gains and losses on this option strategy are inherently and excruciatingly important for our strategy. Due to the merger arbitrage spread, investors can use the profit from the spread to cover the costs of the option strategy. If you wanted to amplify your returns by a factor of 1000 to $5,250 from the option spread, you would simply purchase and sell the above option strategy by a factor of You would then realize a cost of $400. By going long in TRLA with 250 shares, and going short in Z with 111 shares, you would achieve a $406 profit, due to the fixed

closed at $46.65.")

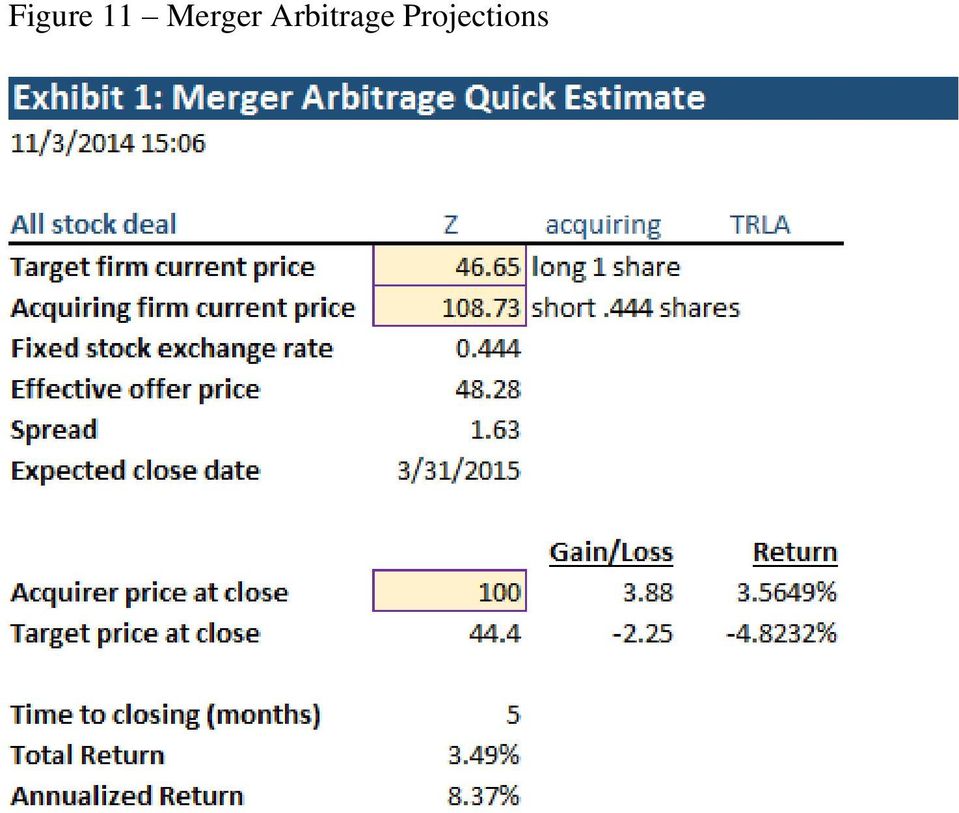

10 conversion spread. In combining this strategy, you eliminate any potential loss and leave yourself to a maximum gain just above of $5.25/contract set or just above $5,250 in this scenario. This is possible and likely due to the decaying trend of Trulia and Zillow stock prices, which correlate by a coefficient of 0.99 since the July 28 th, 2014 and 0.85 since January 3, 2014, but are also buoyed by a gravitation of the price towards $45 for Trulia. Even though the price of Trulia should gravitate towards $45, between October 31, 2014 and March 2015 the price could ebb and flow to $47, resulting in the maximum possible gain. The option strategy s potential downsides can be hedged away completely with a merger arbitrage strategy. A merger arbitrage trade for an all-stock M&A proposal requires going long in the target company and shorting the acquiring company at a rate equal to the fixed exchange rate. Here, an investor would go long 1 share of Trulia and go short.444 shares of Zillow. Closing prices on October 31, 2014 for Zillow and Trulia were $ and $46.65, respectively. The 1 to.444 valuation ratio creates a 349 basis point spread, or 3.49% return (8.37% annualized) via the merger arbitrage investment strategy. To completely offset the loss potential of the options strategy, an investor must purchase 250 shares of Trulia and short 111 shares of Zillow for every 1000 options contract combinations purchased. The investment pays for itself and the long-term return at the time of the closing will completely negate the sunk costs of the options if they expire out of the money. Given that our portfolio is using merger arbitrage as a hedging against losses on the options contract, we do not recommend the use of leverage to generate higher returns.

11

12 Appendix Figure 1 Section 5.01 of the Zillow-Trulia Merger Agreement Figure 2 Trulia s Organic Market Share Decline

13 Figure 3 Trulia s Revenue & Net Income Spread Figure 4 Zillow s Revenue & Net Income Spread

14 Figure 5 Excerpt from Realogy Investor Q&A

15 Figure 6 Realogy Lead Conversion Figures 7 & 8 Condor & Butterfly Spread Illustrations

16 Figures 9 to 11 are snapshots of Excel worksheets used to generate the investment recommendations outlined in the body of this paper. All calculations based on closing prices on 10/31/2014. Figure 9 Zillow-Trulia Stock Price Correlation pre- and post-merger announcement Figure 10 Options Contract P&L Forecast

17 Figure 11 Merger Arbitrage Projections

18 Works Cited Duprey, Rich.(2014). Zillow and Trulia s house might be more straw than brick. Retrieved from Citron.(2014). Zuliagate-the big secret. Retrieved from Giles, Justin.(2014). The Zillow-Trulia merger: looks like it's time to Start selling your shares Glimpses, Edgar. (2014). TRULIA, INC. files (8-K) disclosing entry into a material definitive agreement, other events, financial statements and exhibits. Retrieved from Hoak, Amy.(2014). How the Zillow-Trulia deal affects online home search. Retrieved from and go short. Retrieved from Kasanoff, Bruce.(2014). Are real estate brokers obsolete? Retrieved from

disclosing entry into a material definitive agreement, other events, financial statements and exhibits. Retrieved from http://www.equities.com/index.php?")

19 Solomon, Steven Davidoff.(2014). In real estate listings deal with Zillow, Trulia bears most of the risk. Retrieved from Pinebridge Investments.(2014). Merger arbitrage: beyond deal or no deal. Retrieved from SEC.(2014). Agreement and plan of merger. Retrieved from htm Seeking Alpha.(2014). Trulia shareholders: congratulations, but you should sell right now. Retrieved from

. Trulia shareholders: congratulations, but you should sell right now.")

Muddy Waters Investment Competition. MBA Case Competition 2014 ZILLOW ACQUISITION OVER TRULIA ANALYSIS FULL PAPER

Muddy Waters Investment Competition MBA Case Competition 2014 ZILLOW ACQUISITION OVER TRULIA ANALYSIS FULL PAPER William Vidal Adriana Martins Raquel Clara W.A.R. Consultancy Team 1 Introduction This report

Muddy Waters Investment Competition MBA Case Competition 2014 ZILLOW ACQUISITION OVER TRULIA ANALYSIS FULL PAPER William Vidal Adriana Martins Raquel Clara W.A.R. Consultancy Team 1 Introduction This report

Basics of Spreading: Butterflies and Condors

1 of 31 Basics of Spreading: Butterflies and Condors What is a Spread? Review the links below for detailed information. Terms and Characterizations: Part 1 Download What is a Spread? Download: Butterflies

1 of 31 Basics of Spreading: Butterflies and Condors What is a Spread? Review the links below for detailed information. Terms and Characterizations: Part 1 Download What is a Spread? Download: Butterflies

Running head: ZILLOW AND TRULIA, A REAL ESTATE MERGER 1. Zillow and Trulia: A Real Estate Merger. Wagner College. Giuseppe Badalamenti

Running head: ZILLOW AND TRULIA, A REAL ESTATE MERGER 1 Zillow and Trulia: A Real Estate Merger Wagner College Giuseppe Badalamenti Nicholas De Matteo Kenneth Whitman ZILLOW AND TRULIA, A REAL ESTATE MERGER

Running head: ZILLOW AND TRULIA, A REAL ESTATE MERGER 1 Zillow and Trulia: A Real Estate Merger Wagner College Giuseppe Badalamenti Nicholas De Matteo Kenneth Whitman ZILLOW AND TRULIA, A REAL ESTATE MERGER

How to Trade Options: Strategy Building Blocks

How to Trade Options: Strategy Building Blocks MICHAEL BURKE Important Information and Disclosures This course is provided by TradeStation, a U.S.-based multi-asset brokerage company that seeks to serve

How to Trade Options: Strategy Building Blocks MICHAEL BURKE Important Information and Disclosures This course is provided by TradeStation, a U.S.-based multi-asset brokerage company that seeks to serve

WHAT ARE OPTIONS OPTIONS TRADING

OPTIONS TRADING WHAT ARE OPTIONS Options are openly traded contracts that give the buyer a right to a futures position at a specific price within a specified time period Designed as more of a protective

OPTIONS TRADING WHAT ARE OPTIONS Options are openly traded contracts that give the buyer a right to a futures position at a specific price within a specified time period Designed as more of a protective

VANILLA OPTIONS MANUAL

VANILLA OPTIONS MANUAL BALANCE YOUR RISK WITH OPTIONS Blue Capital Markets Limited 2013. All rights reserved. Content Part A The what and why of options 1 Types of options: Profit and loss scenarios 2

VANILLA OPTIONS MANUAL BALANCE YOUR RISK WITH OPTIONS Blue Capital Markets Limited 2013. All rights reserved. Content Part A The what and why of options 1 Types of options: Profit and loss scenarios 2

Still waiting for disruption

[Type here] MBA Case Competition 2014 Still waiting for disruption Team Solid Ground Brigham Young University Brock Burrows Steve Mineer Jorge Montalva Abstract The real estate market has been moving towards

[Type here] MBA Case Competition 2014 Still waiting for disruption Team Solid Ground Brigham Young University Brock Burrows Steve Mineer Jorge Montalva Abstract The real estate market has been moving towards

WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE

GLOBAL INTRODUCTION WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE Bearish options strategies are options trading strategies that are designed to allow traders to profi t when an exchange rate trends

GLOBAL INTRODUCTION WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE Bearish options strategies are options trading strategies that are designed to allow traders to profi t when an exchange rate trends

Covered Calls. Benefits & Tradeoffs

748627.1.1 1 Covered Calls Enhance ETFs with Options Strategies January 26, 2016 Joe Burgoyne, OIC Benefits & Tradeoffs Joe Burgoyne Director, Options Industry Council www.optionseducation.org 2 The Options

748627.1.1 1 Covered Calls Enhance ETFs with Options Strategies January 26, 2016 Joe Burgoyne, OIC Benefits & Tradeoffs Joe Burgoyne Director, Options Industry Council www.optionseducation.org 2 The Options

Introduction to Options -- The Basics

Introduction to Options -- The Basics Dec. 8 th, 2015 Fidelity Brokerage Services, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917. 2015 FMR LLC. All rights reserved. 744692.1.0 Disclosures Options

Introduction to Options -- The Basics Dec. 8 th, 2015 Fidelity Brokerage Services, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917. 2015 FMR LLC. All rights reserved. 744692.1.0 Disclosures Options

How To Value Trulia And Zillow

MIT Sloan School of Management Zillow s Acquisition of Trulia - The Door to the Online Real Estate Market Muddy Waters Investment Competition The Economist MBA Investment Case Competition 2014 Participants:

MIT Sloan School of Management Zillow s Acquisition of Trulia - The Door to the Online Real Estate Market Muddy Waters Investment Competition The Economist MBA Investment Case Competition 2014 Participants:

Introduction to Options Trading. Patrick Ceresna, MX Instructor

Introduction to Options Trading Patrick Ceresna, MX Instructor 1 Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent

Introduction to Options Trading Patrick Ceresna, MX Instructor 1 Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent

Section 1 - Overview and Option Basics

1 of 10 Section 1 - Overview and Option Basics Download this in PDF format. Welcome to the world of investing and trading with options. The purpose of this course is to show you what options are, how they

1 of 10 Section 1 - Overview and Option Basics Download this in PDF format. Welcome to the world of investing and trading with options. The purpose of this course is to show you what options are, how they

Option Theory Basics

Option Basics What is an Option? Option Theory Basics An option is a traded security that is a derivative product. By derivative product we mean that it is a product whose value is based upon, or derived

Option Basics What is an Option? Option Theory Basics An option is a traded security that is a derivative product. By derivative product we mean that it is a product whose value is based upon, or derived

University of Essex. Term Paper Financial Instruments and Capital Markets 2010/2011. Konstantin Vasilev Financial Economics Bsc

University of Essex Term Paper Financial Instruments and Capital Markets 2010/2011 Konstantin Vasilev Financial Economics Bsc Explain the role of futures contracts and options on futures as instruments

University of Essex Term Paper Financial Instruments and Capital Markets 2010/2011 Konstantin Vasilev Financial Economics Bsc Explain the role of futures contracts and options on futures as instruments

INTRODUCTION TO COTTON OPTIONS Blake K. Bennett Extension Economist/Management Texas Cooperative Extension, The Texas A&M University System

INTRODUCTION TO COTTON OPTIONS Blake K. Bennett Extension Economist/Management Texas Cooperative Extension, The Texas A&M University System INTRODUCTION For well over a century, industry representatives

INTRODUCTION TO COTTON OPTIONS Blake K. Bennett Extension Economist/Management Texas Cooperative Extension, The Texas A&M University System INTRODUCTION For well over a century, industry representatives

Market Microstructure: An Interactive Exercise

Market Microstructure: An Interactive Exercise Jeff Donaldson, University of Tampa Donald Flagg, University of Tampa ABSTRACT Although a lecture on microstructure serves to initiate the inspiration of

Market Microstructure: An Interactive Exercise Jeff Donaldson, University of Tampa Donald Flagg, University of Tampa ABSTRACT Although a lecture on microstructure serves to initiate the inspiration of

How to Win Clients & Protect Portfolios

Ugo Egbunike, Moderator Director of Business Development ETF.com How to Win Clients & Protect Portfolios Howard J. Atkinson, Panelist Managing Director Horizons ETFs Management LLA Michael Khouw, Panelist

Ugo Egbunike, Moderator Director of Business Development ETF.com How to Win Clients & Protect Portfolios Howard J. Atkinson, Panelist Managing Director Horizons ETFs Management LLA Michael Khouw, Panelist

ADVANCED COTTON FUTURES AND OPTIONS STRATEGIES

ADVANCED COTTON FUTURES AND OPTIONS STRATEGIES Blake K. Bennett Extension Economist/Management Texas Cooperative Extension, The Texas A&M University System INTRODUCTION Cotton producers have used futures

ADVANCED COTTON FUTURES AND OPTIONS STRATEGIES Blake K. Bennett Extension Economist/Management Texas Cooperative Extension, The Texas A&M University System INTRODUCTION Cotton producers have used futures

Structured Products. Designing a modern portfolio

ab Structured Products Designing a modern portfolio Achieving your personal goals is the driving motivation for how and why you invest. Whether your goal is to grow and preserve wealth, save for your children

ab Structured Products Designing a modern portfolio Achieving your personal goals is the driving motivation for how and why you invest. Whether your goal is to grow and preserve wealth, save for your children

Understanding Trading Performance in an Order Book Market Structure TraderEx LLC, July 2011

TraderEx Self-Paced Tutorial & Case: Who moved my Alpha? Understanding Trading Performance in an Order Book Market Structure TraderEx LLC, July 2011 How should you handle instructions to buy or sell large

TraderEx Self-Paced Tutorial & Case: Who moved my Alpha? Understanding Trading Performance in an Order Book Market Structure TraderEx LLC, July 2011 How should you handle instructions to buy or sell large

Section 1 - Covered Call Writing: Basic Terms and Definitions

Section 1 - Covered Call Writing: Basic Terms and Definitions Covered call writing is one of the most often-used option strategies, both at the institutional and individual level. Before discussing the

Section 1 - Covered Call Writing: Basic Terms and Definitions Covered call writing is one of the most often-used option strategies, both at the institutional and individual level. Before discussing the

Zillow, Inc. Acquisition of Trulia, Inc. Thomas Bryan Smith, Serena Dang, and Danica Fiew. University of North Texas MBA

ZILLOW, INC. ACQUISITION OF TRULIA, INC. 1 Zillow, Inc. Acquisition of Trulia, Inc. Thomas Bryan Smith, Serena Dang, and Danica Fiew University of North Texas MBA ZILLOW, INC. ACQUISITION OF TRULIA, INC.

ZILLOW, INC. ACQUISITION OF TRULIA, INC. 1 Zillow, Inc. Acquisition of Trulia, Inc. Thomas Bryan Smith, Serena Dang, and Danica Fiew University of North Texas MBA ZILLOW, INC. ACQUISITION OF TRULIA, INC.

Bull Call Spread. BACK TO BASICS: Spread Yourself Around: Example. By David Bickings, Optionetics.com

Bull Call Spread BACK TO BASICS: Spread Yourself Around: Example By David Bickings, Optionetics.com Options are a fantastic investment to make money on the rise and fall of an asset. This is no surprise

Bull Call Spread BACK TO BASICS: Spread Yourself Around: Example By David Bickings, Optionetics.com Options are a fantastic investment to make money on the rise and fall of an asset. This is no surprise

A: SGEAX C: SGECX I: SGEIX

A: SGEAX C: SGECX I: SGEIX NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Salient Global Equity Fund The investment objective of the Salient Global Equity Fund (the Fund ) is to seek long term capital

A: SGEAX C: SGECX I: SGEIX NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Salient Global Equity Fund The investment objective of the Salient Global Equity Fund (the Fund ) is to seek long term capital

Investment valuations in private equity buyouts

By Brian Gallagher, Twin Bridge Capital Partners 11 Introduction Buyout investment math (or mathematics) is the means by which investment sponsors formally analyse the assumptions they make about the past

By Brian Gallagher, Twin Bridge Capital Partners 11 Introduction Buyout investment math (or mathematics) is the means by which investment sponsors formally analyse the assumptions they make about the past

Understanding Options: Calls and Puts

2 Understanding Options: Calls and Puts Important: in their simplest forms, options trades sound like, and are, very high risk investments. If reading about options makes you think they are too risky for

2 Understanding Options: Calls and Puts Important: in their simplest forms, options trades sound like, and are, very high risk investments. If reading about options makes you think they are too risky for

Buying Call or Long Call. Unlimited Profit Potential

Options Basis 1 An Investor can use options to achieve a number of different things depending on the strategy the investor employs. Novice option traders will be allowed to buy calls and puts, to anticipate

Options Basis 1 An Investor can use options to achieve a number of different things depending on the strategy the investor employs. Novice option traders will be allowed to buy calls and puts, to anticipate

Trading Options MICHAEL BURKE

Trading Options MICHAEL BURKE Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading Options... 6 Options Trading Primer... 8 Options

Trading Options MICHAEL BURKE Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading Options... 6 Options Trading Primer... 8 Options

Grooming Your Business for Sale

PRIVATE COMPANIES Grooming Your Business for Sale Plan for the Future but Be Prepared for the Unexpected KPMG ENTERPRISE 2 Grooming Your Business for Sale Grooming Your Business for Sale Plan for the Future

PRIVATE COMPANIES Grooming Your Business for Sale Plan for the Future but Be Prepared for the Unexpected KPMG ENTERPRISE 2 Grooming Your Business for Sale Grooming Your Business for Sale Plan for the Future

Muddy Waters Investment Competition. Analysis on the Zillow Trulia Merger

The Economist MBA Case Competition 2014 Muddy Waters Investment Competition Analysis on the Zillow Trulia Merger Authors Michael Jonas, Juan Guillermo Rintha, Philipp Soechtig Full-Time MBA Class of 2015

The Economist MBA Case Competition 2014 Muddy Waters Investment Competition Analysis on the Zillow Trulia Merger Authors Michael Jonas, Juan Guillermo Rintha, Philipp Soechtig Full-Time MBA Class of 2015

Journal of Financial and Strategic Decisions Volume 13 Number 1 Spring 2000 HISTORICAL RETURN DISTRIBUTIONS FOR CALLS, PUTS, AND COVERED CALLS

Journal of Financial and Strategic Decisions Volume 13 Number 1 Spring 2000 HISTORICAL RETURN DISTRIBUTIONS FOR CALLS, PUTS, AND COVERED CALLS Gary A. Benesh * and William S. Compton ** Abstract Historical

Journal of Financial and Strategic Decisions Volume 13 Number 1 Spring 2000 HISTORICAL RETURN DISTRIBUTIONS FOR CALLS, PUTS, AND COVERED CALLS Gary A. Benesh * and William S. Compton ** Abstract Historical

CHAPTER 18. Initial Public Offerings, Investment Banking, and Financial Restructuring

CHAPTER 18 Initial Public Offerings, Investment Banking, and Financial Restructuring 1 Topics in Chapter Initial Public Offerings Investment Banking and Regulation The Maturity Structure of Debt Refunding

CHAPTER 18 Initial Public Offerings, Investment Banking, and Financial Restructuring 1 Topics in Chapter Initial Public Offerings Investment Banking and Regulation The Maturity Structure of Debt Refunding

MANAGEMENT OPTIONS AND VALUE PER SHARE

1 MANAGEMENT OPTIONS AND VALUE PER SHARE Once you have valued the equity in a firm, it may appear to be a relatively simple exercise to estimate the value per share. All it seems you need to do is divide

1 MANAGEMENT OPTIONS AND VALUE PER SHARE Once you have valued the equity in a firm, it may appear to be a relatively simple exercise to estimate the value per share. All it seems you need to do is divide

Guide to Options Strategies

RECOGNIA S Guide to Options Strategies A breakdown of key options strategies to help you better understand the characteristics and implications of each Recognia s Guide to Options Strategies 1 3 Buying

RECOGNIA S Guide to Options Strategies A breakdown of key options strategies to help you better understand the characteristics and implications of each Recognia s Guide to Options Strategies 1 3 Buying

www.optionseducation.org OIC Options on ETFs

www.optionseducation.org Options on ETFs 1 The Options Industry Council For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations,

www.optionseducation.org Options on ETFs 1 The Options Industry Council For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations,

Purpose of Selling Stocks Short JANUARY 2007 NUMBER 5

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

Understanding Irish Real Estate Investment Trusts. For Financial Advisor Use Only

Understanding Irish Real Estate Investment Trusts For Financial Advisor Use Only What is a Real Estate Investment Trust (REIT)? A REIT is a public listed company which has as its main activity the ownership

Understanding Irish Real Estate Investment Trusts For Financial Advisor Use Only What is a Real Estate Investment Trust (REIT)? A REIT is a public listed company which has as its main activity the ownership

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

RISK MANAGEMENT TOOLS

RISK MANAGEMENT TOOLS Pavilion Advisory Group TM Pavilion Advisory Group is a trademark of Pavilion Financial Corporation used under license by Pavilion Advisory Group Ltd. in Canada and Pavilion Advisory

RISK MANAGEMENT TOOLS Pavilion Advisory Group TM Pavilion Advisory Group is a trademark of Pavilion Financial Corporation used under license by Pavilion Advisory Group Ltd. in Canada and Pavilion Advisory

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

RISK DISCLOSURE STATEMENT FOR SECURITY FUTURES CONTRACTS This disclosure statement discusses the characteristics and risks of standardized security futures contracts traded on regulated U.S. exchanges.

Understanding investment concepts

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157 By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions 201 Edgewater Drive, Suite 255 Wakefield,

A Primer on Valuing Common Stock per IRS 409A and the Impact of FAS 157 By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions 201 Edgewater Drive, Suite 255 Wakefield,

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES The Options Industry Council (OIC) is a non-profit association created to educate the investing public and brokers about the benefits and risks of exchange-traded

LEAPS LONG-TERM EQUITY ANTICIPATION SECURITIES The Options Industry Council (OIC) is a non-profit association created to educate the investing public and brokers about the benefits and risks of exchange-traded

Definitions of Marketing Terms

E-472 RM2-32.0 11-08 Risk Management Definitions of Marketing Terms Dean McCorkle and Kevin Dhuyvetter* Cash Market Cash marketing basis the difference between a cash price and a futures price of a particular

E-472 RM2-32.0 11-08 Risk Management Definitions of Marketing Terms Dean McCorkle and Kevin Dhuyvetter* Cash Market Cash marketing basis the difference between a cash price and a futures price of a particular

Concentrated Stock Overlay INCREMENTAL INCOME FROM CONCENTRATED WEALTH

Concentrated Stock Overlay INCREMENTAL INCOME FROM CONCENTRATED WEALTH INTRODUCING RAMPART CONCENTRATED STOCK OVERLAY STRATEGY When a portfolio includes a concentrated equity position, the risk created

Concentrated Stock Overlay INCREMENTAL INCOME FROM CONCENTRATED WEALTH INTRODUCING RAMPART CONCENTRATED STOCK OVERLAY STRATEGY When a portfolio includes a concentrated equity position, the risk created

Chapter 5 Option Strategies

Chapter 5 Option Strategies Chapter 4 was concerned with the basic terminology and properties of options. This chapter discusses categorizing and analyzing investment positions constructed by meshing puts

Chapter 5 Option Strategies Chapter 4 was concerned with the basic terminology and properties of options. This chapter discusses categorizing and analyzing investment positions constructed by meshing puts

WINNING STOCK & OPTION STRATEGIES

WINNING STOCK & OPTION STRATEGIES DISCLAIMER Although the author of this book is a professional trader, he is not a registered financial adviser or financial planner. The information presented in this

WINNING STOCK & OPTION STRATEGIES DISCLAIMER Although the author of this book is a professional trader, he is not a registered financial adviser or financial planner. The information presented in this

Press Releases. Zillow Announces Acquisition of Trulia for $3.5 Billion in Stock

Press Releases Zillow Announces Acquisition of Trulia for $3.5 Billion in Stock Combination of companies sets stage to offer more real estate tools and services that empower consumers and drive more business

Press Releases Zillow Announces Acquisition of Trulia for $3.5 Billion in Stock Combination of companies sets stage to offer more real estate tools and services that empower consumers and drive more business

The Zillow/Trulia Merger

The Zillow/Trulia Merger TEAM UST LUKE DERY, CHRISTIAN ENGEL, JEFF ANDERSEN Table of Contents Introduction... 2 Real Estate Overview... 2 Online Real Estate Advertising... 3 Near Term Opportunity... 4

The Zillow/Trulia Merger TEAM UST LUKE DERY, CHRISTIAN ENGEL, JEFF ANDERSEN Table of Contents Introduction... 2 Real Estate Overview... 2 Online Real Estate Advertising... 3 Near Term Opportunity... 4

POLICY STATEMENT Q-22

POLICY STATEMENT Q-22 DISCLOSURE DOCUMENT FOR COMMODITY FUTURES CONTRACTS, FOR OPTIONS TRADED ON A RECOGNIZED MARKET AND FOR EXCHANGE-TRADED COMMODITY FUTURES OPTIONS 1. In the case of commodity futures

POLICY STATEMENT Q-22 DISCLOSURE DOCUMENT FOR COMMODITY FUTURES CONTRACTS, FOR OPTIONS TRADED ON A RECOGNIZED MARKET AND FOR EXCHANGE-TRADED COMMODITY FUTURES OPTIONS 1. In the case of commodity futures

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS Direxion Shares Leveraged Exchange-Traded Funds (ETFs) are daily funds that provide 200% or 300% leverage and the ability

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS Direxion Shares Leveraged Exchange-Traded Funds (ETFs) are daily funds that provide 200% or 300% leverage and the ability

Options Markets: Introduction

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

A Unique and Potentially Effective Method of Capital Formation in Today s Financing Environment

Reverse Mergers A Unique and Potentially Effective Method of Capital Formation in Today s Financing Environment Prepared by MDB Capital Group LLC March 2003 Background Reverse mergers have been utilized

Reverse Mergers A Unique and Potentially Effective Method of Capital Formation in Today s Financing Environment Prepared by MDB Capital Group LLC March 2003 Background Reverse mergers have been utilized

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

Invest in your future

Invest in your future Investing, and your Pensions NO BETTER TIME THAN THE PRESENT - Investing, and Your Pension The sooner you start investing, the better off you will be. Taking an early interest in

Invest in your future Investing, and your Pensions NO BETTER TIME THAN THE PRESENT - Investing, and Your Pension The sooner you start investing, the better off you will be. Taking an early interest in

15.433 INVESTMENTS Class 21: Hedge Funds. Spring 2003

15.433 INVESTMENTS Class 21: Hedge Funds Spring 2003 The Beginning of Hedge Funds In 1949, Alfred Jones established the first hedge fund in the U.S. At its beginning, the defining characteristic of a hedge

15.433 INVESTMENTS Class 21: Hedge Funds Spring 2003 The Beginning of Hedge Funds In 1949, Alfred Jones established the first hedge fund in the U.S. At its beginning, the defining characteristic of a hedge

Maximizing Your Equity Allocation

Webcast summary Maximizing Your Equity Allocation 130/30 The story continues May 2010 Please visit jpmorgan.com/institutional for access to all of our Insights publications. Extension strategies: Variations

Webcast summary Maximizing Your Equity Allocation 130/30 The story continues May 2010 Please visit jpmorgan.com/institutional for access to all of our Insights publications. Extension strategies: Variations

Chapter 5. Currency Derivatives. Lecture Outline. Forward Market How MNCs Use Forward Contracts Non-Deliverable Forward Contracts

Chapter 5 Currency Derivatives Lecture Outline Forward Market How MNCs Use Forward Contracts Non-Deliverable Forward Contracts Currency Futures Market Contract Specifications Trading Futures Comparison

Chapter 5 Currency Derivatives Lecture Outline Forward Market How MNCs Use Forward Contracts Non-Deliverable Forward Contracts Currency Futures Market Contract Specifications Trading Futures Comparison

INVESTMENT DICTIONARY

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

CHAPTER 20 Understanding Options

CHAPTER 20 Understanding Options Answers to Practice Questions 1. a. The put places a floor on value of investment, i.e., less risky than buying stock. The risk reduction comes at the cost of the option

CHAPTER 20 Understanding Options Answers to Practice Questions 1. a. The put places a floor on value of investment, i.e., less risky than buying stock. The risk reduction comes at the cost of the option

Zuliagate -- The Big Secret

July 26, 2014 - Zuliagate -- The Big Secret Citron Exposes What the Press Has Ignored The stock market and the real estate industry are all abuzz about the possible merger of Zillow(NASDAQ:Z) and Trulia(NASDAQ:TRLA).

July 26, 2014 - Zuliagate -- The Big Secret Citron Exposes What the Press Has Ignored The stock market and the real estate industry are all abuzz about the possible merger of Zillow(NASDAQ:Z) and Trulia(NASDAQ:TRLA).

Where you hold your investments matters. Mutual funds or ETFs? Why life insurance still plays an important estate planning role

spring 2016 Where you hold your investments matters Mutual funds or ETFs? Why life insurance still plays an important estate planning role Should you undo a Roth IRA conversion? Taxable vs. tax-advantaged

spring 2016 Where you hold your investments matters Mutual funds or ETFs? Why life insurance still plays an important estate planning role Should you undo a Roth IRA conversion? Taxable vs. tax-advantaged

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Arbitrage spreads. Arbitrage spreads refer to standard option strategies like vanilla spreads to

Arbitrage spreads Arbitrage spreads refer to standard option strategies like vanilla spreads to lock up some arbitrage in case of mispricing of options. Although arbitrage used to exist in the early days

Arbitrage spreads Arbitrage spreads refer to standard option strategies like vanilla spreads to lock up some arbitrage in case of mispricing of options. Although arbitrage used to exist in the early days

Nature and Purpose of the Valuation of Business and Financial Assets

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

G. BUSINESS VALUATIONS 1. Nature and Purpose of the Valuation of Business and Financial Assets 2. Models for the Valuation of Shares 3. The Valuation of Debt and Other Financial Assets 4. Efficient Market

Table of Contents. Make Money Trading Options Top-15 Option Trading Strategies. RLCG Management LLC All Rights Reserved Page 2

Table of Contents Introduction: Why Trade Options?... 3 Strategy #1: Buy-Write or Covered Call... 4 Strategy #2: Sell-Write or Covered Put... 5 Strategy #3: Protective Put... 6 Strategy #4: Collar... 7

Table of Contents Introduction: Why Trade Options?... 3 Strategy #1: Buy-Write or Covered Call... 4 Strategy #2: Sell-Write or Covered Put... 5 Strategy #3: Protective Put... 6 Strategy #4: Collar... 7

CONTRACTS FOR DIFFERENCE

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

Single Manager vs. Multi-Manager Alternative Investment Funds

September 2015 Single Manager vs. Multi-Manager Alternative Investment Funds John Dolfin, CFA Chief Investment Officer Steben & Company, Inc. Christopher Maxey, CAIA Senior Portfolio Manager Steben & Company,

September 2015 Single Manager vs. Multi-Manager Alternative Investment Funds John Dolfin, CFA Chief Investment Officer Steben & Company, Inc. Christopher Maxey, CAIA Senior Portfolio Manager Steben & Company,

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.

![Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.](/thumbs/40/20590846.jpg "Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.") Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

CME Options on Futures

CME Education Series CME Options on Futures The Basics Table of Contents SECTION PAGE 1 VOCABULARY 2 2 PRICING FUNDAMENTALS 4 3 ARITHMETIC 6 4 IMPORTANT CONCEPTS 8 5 BASIC STRATEGIES 9 6 REVIEW QUESTIONS

CME Education Series CME Options on Futures The Basics Table of Contents SECTION PAGE 1 VOCABULARY 2 2 PRICING FUNDAMENTALS 4 3 ARITHMETIC 6 4 IMPORTANT CONCEPTS 8 5 BASIC STRATEGIES 9 6 REVIEW QUESTIONS

Options on Beans For People Who Don t Know Beans About Options

Options on Beans For People Who Don t Know Beans About Options Remember when things were simple? When a call was something you got when you were in the bathtub? When premium was what you put in your car?

Options on Beans For People Who Don t Know Beans About Options Remember when things were simple? When a call was something you got when you were in the bathtub? When premium was what you put in your car?

FREQUENTLY ASKED QUESTIONS March 2015

FREQUENTLY ASKED QUESTIONS March 2015 Table of Contents I. Offering a Hedge Fund Strategy in a Mutual Fund Structure... 3 II. Fundamental Research... 4 III. Portfolio Construction... 6 IV. Fund Expenses

FREQUENTLY ASKED QUESTIONS March 2015 Table of Contents I. Offering a Hedge Fund Strategy in a Mutual Fund Structure... 3 II. Fundamental Research... 4 III. Portfolio Construction... 6 IV. Fund Expenses

DFA INVESTMENT DIMENSIONS GROUP INC.

PROSPECTUS February 28, 2014 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. PORTFOLIOS FOR LONG-TERM INVESTORS SEEKING TO INVEST IN:

PROSPECTUS February 28, 2014 Please carefully read the important information it contains before investing. DFA INVESTMENT DIMENSIONS GROUP INC. PORTFOLIOS FOR LONG-TERM INVESTORS SEEKING TO INVEST IN:

Atlas Capital Group, LLC. Form ADV Part 2A Appendix 1: Wrap Fee Program Brochure. W3561 County Road O Appleton, WI 54913. Telephone: 920-659-1202

Atlas Capital Group, LLC Form ADV Part 2A Appendix 1: Wrap Fee Program Brochure W3561 County Road O Appleton, WI 54913 Telephone: 920-659-1202 This wrap fee brochure provides information about the qualifications

Atlas Capital Group, LLC Form ADV Part 2A Appendix 1: Wrap Fee Program Brochure W3561 County Road O Appleton, WI 54913 Telephone: 920-659-1202 This wrap fee brochure provides information about the qualifications

Invesco Unit Trusts Closed-end strategies

Invesco Unit Trusts Closed-end strategies A Closed-end fund primer Closed-end funds have many unique qualities Like traditional mutual funds, closed-end funds are generally professionally managed and their

Invesco Unit Trusts Closed-end strategies A Closed-end fund primer Closed-end funds have many unique qualities Like traditional mutual funds, closed-end funds are generally professionally managed and their

INDEPENDENT. OBJECTIVE. RELIABLE. Options Basics & Essentials: The Beginners Guide to Trading Gold & Silver Options

INDEPENDENT. OBJECTIVE. RELIABLE. 1 About the ebook Creator Drew Rathgeber is a senior broker at Daniels Trading. He has been heavily involved in numerous facets of the silver & gold community for over

INDEPENDENT. OBJECTIVE. RELIABLE. 1 About the ebook Creator Drew Rathgeber is a senior broker at Daniels Trading. He has been heavily involved in numerous facets of the silver & gold community for over

Session X: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics. Department of Economics, City University, London

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

Introduction to Options

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

June 2008 Supplement to Characteristics and Risks of Standardized Options

June 2008 Supplement to Characteristics and Risks of Standardized Options This supplement supersedes and replaces the April 2008 Supplement to the booklet entitled Characteristics and Risks of Standardized

June 2008 Supplement to Characteristics and Risks of Standardized Options This supplement supersedes and replaces the April 2008 Supplement to the booklet entitled Characteristics and Risks of Standardized

Derivative Users Traders of derivatives can be categorized as hedgers, speculators, or arbitrageurs.

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

Example 1. Consider the following two portfolios: 2. Buy one c(s(t), 20, τ, r) and sell one c(s(t), 10, τ, r).

, 20, τ, r) and sell one c(s(t), 10, τ, r).") Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Understanding Stock Options

Understanding Stock Options Introduction...2 Benefits Of Exchange-Traded Options... 4 Options Compared To Common Stocks... 6 What Is An Option... 7 Basic Strategies... 12 Conclusion...20 Glossary...22

Understanding Stock Options Introduction...2 Benefits Of Exchange-Traded Options... 4 Options Compared To Common Stocks... 6 What Is An Option... 7 Basic Strategies... 12 Conclusion...20 Glossary...22

Premier Inc. (NASDAQ:PINC)

") Premier Inc. (NASDAQ:PINC) Recommendation: Long Aneesh Chona, Karthik Bolisetty, & Satya Yerrabolu WITG Healthcare Investing Team April 26, 2015 Thesis Premier s unique business model and growth opportunities

Premier Inc. (NASDAQ:PINC) Recommendation: Long Aneesh Chona, Karthik Bolisetty, & Satya Yerrabolu WITG Healthcare Investing Team April 26, 2015 Thesis Premier s unique business model and growth opportunities

General Risk Disclosure

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

General Risk Disclosure Colmex Pro Ltd (hereinafter called the Company ) is an Investment Firm regulated by the Cyprus Securities and Exchange Commission (license number 123/10). This notice is provided

Terminology and Scripts: what you say will make a difference in your success

Terminology and Scripts: what you say will make a difference in your success Terminology Matters! Here are just three simple terminology suggestions which can help you enhance your ability to make your

Terminology and Scripts: what you say will make a difference in your success Terminology Matters! Here are just three simple terminology suggestions which can help you enhance your ability to make your

SUMMARY PROSPECTUS SDIT Short-Duration Government Fund (TCSGX) Class A

Class A") May 31, 2016 SUMMARY PROSPECTUS SDIT Short-Duration Government Fund (TCSGX) Class A Before you invest, you may want to review the Fund s Prospectus, which contains information about the Fund and its risks.

May 31, 2016 SUMMARY PROSPECTUS SDIT Short-Duration Government Fund (TCSGX) Class A Before you invest, you may want to review the Fund s Prospectus, which contains information about the Fund and its risks.

The 7 Step Guide to Business Exit Planning

The 7 Step Guide to Business Exit Planning It takes a coordinated Team of Professionals experienced in Mergers & Acquisitions, Corporate Law, Taxation and Financial Planning / Wealth Management to successfully

The 7 Step Guide to Business Exit Planning It takes a coordinated Team of Professionals experienced in Mergers & Acquisitions, Corporate Law, Taxation and Financial Planning / Wealth Management to successfully

THE EQUITY OPTIONS STRATEGY GUIDE

THE EQUITY OPTIONS STRATEGY GUIDE APRIL 2003 Table of Contents Introduction 2 Option Terms and Concepts 4 What is an Option? 4 Long 4 Short 4 Open 4 Close 5 Leverage and Risk 5 In-the-money, At-the-money,

THE EQUITY OPTIONS STRATEGY GUIDE APRIL 2003 Table of Contents Introduction 2 Option Terms and Concepts 4 What is an Option? 4 Long 4 Short 4 Open 4 Close 5 Leverage and Risk 5 In-the-money, At-the-money,

PUTS AND CALLS FOR THE CONSERVATIVE INVESTOR Common Sense Strategies

PUTS AND CALLS FOR THE CONSERVATIVE INVESTOR Common Sense Strategies By Edward M. Wolpert Oconee Financial Planning Services www.oconeefps.com Conservative investors can enhance their earnings or reduce

PUTS AND CALLS FOR THE CONSERVATIVE INVESTOR Common Sense Strategies By Edward M. Wolpert Oconee Financial Planning Services www.oconeefps.com Conservative investors can enhance their earnings or reduce

Investment Companies

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

Mutual Funds Mutual Funds Investment companies Financial intermediaries that collect funds form individual investors and invest those funds in a potentially wide rande of securities or other asstes Polling

Valuation of S-Corporations

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

DERIVATIVE INSTRUMENTS RISK STATEMENT FORM (applicable to transactions at Turkish Derivatives Exchange)

") DERIVATIVE INSTRUMENTS RISK STATEMENT FORM (applicable to transactions at Turkish Derivatives Exchange) Important Explanation: While you may generate revenues as a result of the purchase-sale transactions

DERIVATIVE INSTRUMENTS RISK STATEMENT FORM (applicable to transactions at Turkish Derivatives Exchange) Important Explanation: While you may generate revenues as a result of the purchase-sale transactions

Option Values. Option Valuation. Call Option Value before Expiration. Determinants of Call Option Values

Option Values Option Valuation Intrinsic value profit that could be made if the option was immediately exercised Call: stock price exercise price : S T X i i k i X S Put: exercise price stock price : X

Option Values Option Valuation Intrinsic value profit that could be made if the option was immediately exercised Call: stock price exercise price : S T X i i k i X S Put: exercise price stock price : X

Math 194 Introduction to the Mathematics of Finance Winter 2001

Math 194 Introduction to the Mathematics of Finance Winter 2001 Professor R. J. Williams Mathematics Department, University of California, San Diego, La Jolla, CA 92093-0112 USA Email: williams@math.ucsd.edu

Math 194 Introduction to the Mathematics of Finance Winter 2001 Professor R. J. Williams Mathematics Department, University of California, San Diego, La Jolla, CA 92093-0112 USA Email: williams@math.ucsd.edu

SHORT INTRODUCTION OF SHORT SELLING

Financial Assets and Investing SHORT INTRODUCTION OF SHORT SELLING Dagmar Linnertová Faculty of Economics and Administration, Masaryk University, Lipová 41a, 602 00 Brno, e-mail: Dagmar.Linnertova@mail.muni.cz

Financial Assets and Investing SHORT INTRODUCTION OF SHORT SELLING Dagmar Linnertová Faculty of Economics and Administration, Masaryk University, Lipová 41a, 602 00 Brno, e-mail: Dagmar.Linnertova@mail.muni.cz