The IIA Standards: The IPPF Framework

|

|

|

- Magdalene Underwood

- 9 years ago

- Views:

Transcription

1 The IIA Standards: The IPPF Framework S P E A K E R : D O T T. R O B E R TO R O S ATO C O U R S E O F B U S I N E S S A U D I T I N G U N I V E R S I T Y O F R O M E T O R V E R G A T A D E C E M B E R 2015

2 IPPF: Authoritative Guidance for Internal Auditing Practitioners The International Professional Practices Framework (IPPF) is the conceptual framework that organizes authoritative guidance promulgated by The Institute of Internal Auditors The IIA Established in 1941, The IIA is an international professional association with more than 180,000 member worldwide. It s universally acknowledged as the trustworthy, global, guidance-setting body, providing internal audit professionals worldwide with knowledge and methodologies The scope of the IPPF is only authoritative guidance developed by an IIA international technical committee (International Internal Auditing Standards Board, Professional Issues Committee, Global Ethics Committee, and Public Sector Committee) following appropriate due process 2

3 IA Standards and Guidance: A Vision for the Future Story The Framework has been developed to organise the full range of internal audit guidance from IIA Global in an accessible way. Standards - first issued 1978 Professional Practices Framework International Professional Practices Framework January 2009 Code of Ethics Vision for the Future is a task force focused on reviewing the scope of the framework and increasing the transparency and flexibility of IIA guidance development, review, and issuance processes. The aim is assessing whether gaps existed between the evolving internal audit practices and the Standards, enhancing the guidance structure and development processes. 3

4 The Framework for Internal Audit Effectiveness: The New IPPF In July 2015, The IIA released a new IPPF to better support internal audit practitioners in fulfilling the profession s evolving role with an insightful, proactive, and future-focused perspective. The Framework includes two types of guidance: 1. Mandatory guidance: For IIA members compliance is required and is essential for the professional practice of internal auditing 2. Recommended guidance: It describes practices for the effective implementation of mandatory guidance. Therefore, compliance is strongly recommended 4

5 Path to Internal Audit Effectiveness 5

6 What internal audit aspires to accomplish within an organization? MISSION What do IAs try to achieve through their activity? To enhance and protect organizational value by providing stakeholders with risk-based, objective and reliable assurance, advice and insight. The Mission of Internal Audit describes internal audit s primary purpose and overarching goal. Achievement of the mission is supported by the entire IPPF, including the mandatory elements of the Definition, Core Principles for the Professional Practice of Internal Auditing, the Code of Ethics, and Standards, as well as all recommended guidance. Assurance An objective examination of evidence for the purpose of providing an independent assessment on governance, risk management, and control processes for the organization. Advice Advisory, the nature and scope of which are agreed with the client, are intended to improve an organization's governance, risk management, and control processes without assuming management responsibility 6 Insight To be truly effective, IA should focus proactively on key risks and issues facing organizations with catalyst, analysis, assessments

7 MISSION: A changing role Assurance Provider Strategic Business Advisor Compliance Inspector 7

8 What internal audit is? DEFINITION Which are IA nature of work and objects of evaluation? Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. The Definition of Internal Auditing states the fundamental purpose, nature, and scope of internal auditing 8

9 Which are the focal point for IA in order to be present and operating effectively? Core Principles Which are the criteria in order to evaluate IA effectiveness? An Internal auditor is effective if 1. Demonstrates uncompromised integrity 2. Demonstrates competence and due professional care 3. Is objective and free from undue influence (independent) Principles relate to the individual internal auditor and collectively to the internal audit activity Input 8. Provides risk-based assurance 9. Is insightful, proactive, and future-focused 10. Promotes organizational improvement Principles relate to the outcomes or results of an internal audit activity Output Process 4. Aligns with the strategies, objectives, and risks of the organization 5. Is appropriately positioned and adequately resourced 6. Demonstrates quality and continuous improvement 7. Communicates effectively Principles relate to the internal audit activity and its processes Failure to achieve any of the Principles would imply that an internal audit activity was not as effective as it could be in achieving internal audit s mission 9

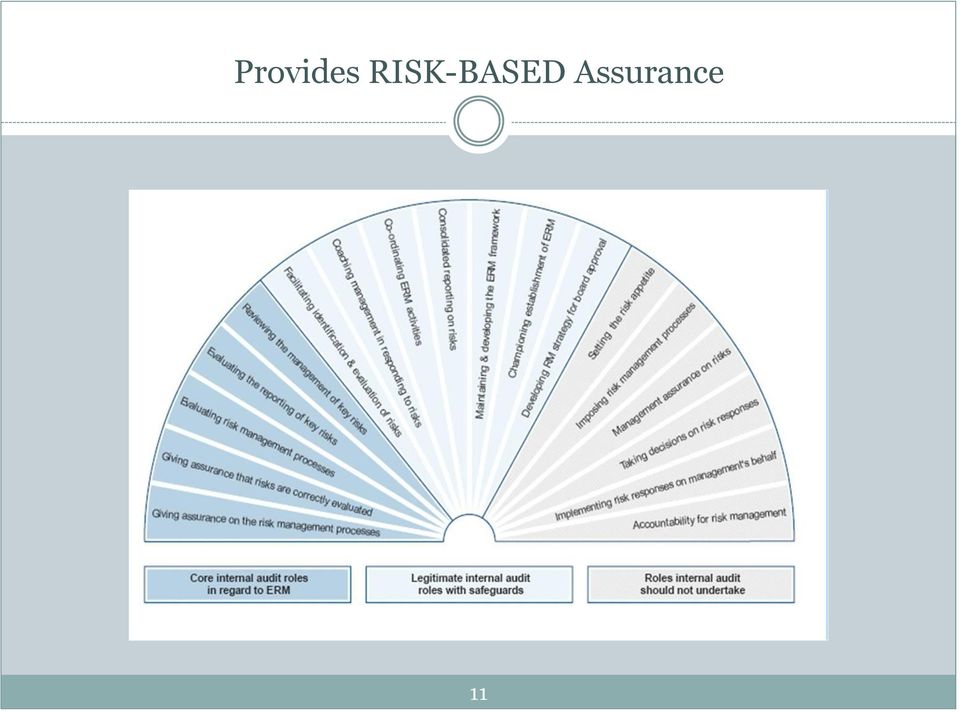

10 Provides RISK-BASED Assurance There isn t a definition of risk based internal auditing (RBIA) provided by the IPPF WHY?? RBIA is a methodology that links internal auditing to an organization's overall risk management framework. RBIA allows internal audit to provide assurance to the board that risk management processes are managing risks effectively, in relation to the risk appetite (Position Statement IIA UK and Ireland) Assessing risk maturity Periodic audit planning Individual audit assignments 10

Assessing risk maturity Periodic audit planning")

11 Provides RISK-BASED Assurance 11

12 Which are the minimum requirements for conduct? Code of Ethics Which are behavioral expectations rather than specific activities? 4 PRINCIPLES 12 RULES Integrity The integrity of internal auditors establishes trust and thus provides the basis for reliance on their judgment Honesty, Diligence, Responsibility Compliance No illegal acts Respect of company ethical value Objectivity Internal auditors exhibit the highest level of professional objectivity in gathering, evaluating, and communicating information about the activity or process being examined. Internal auditors make a balanced assessment of all the relevant circumstances and are not unduly influenced by their own interests or by others in forming judgments. No operational responsibilities Avoid any pressures Conflicts of Interest Disclosure Confidentiality Internal auditors respect the value and ownership of information they receive and do not disclose information without appropriate authority unless there is a legal or professional obligation to do so. Prudency Correct use of info Competency Internal auditors apply the knowledge, skills, and experience needed in the performance of internal auditing services. Knowledge, skills, and experience Compliance with IPPF QAIP 12

13 Which are the Attributes of organizations and individuals performing internal audit services? International Standards Which are the criteria against which the performance of IA services can be measured? International Standards for the Professional Practice of Internal Auditing (Standards) provide a framework of principle-focused criteria for performing and promoting internal auditing. Mandatory requirements consisting of: Statements of basic requirements for professional practice of internal auditing Interpretations which clarify terms or concepts within the Statements. Glossary Attribute Standards address the characteristics of organizations and parties performing internal audit activities Performance Standards describe the nature of internal audit activities and provide criteria for performance evaluation 13

14 How to implement the Mandatory Guidance? Recommended Guidance How to conduct the activity in compliance with the Standards? Recommended guidance is endorsed by The IIA through a formal approval process. It describes practices for effective implementation of The IIA's Core Principles, Definition of Internal Auditing, Code of Ethics, and Standards The recommended elements of the IPPF are: Practice Advisories / Implementation Guidance Address approach, methodology and considerations, but NOT detailed processes and procedures. Concise and timely guidance to assist internal auditors in applying Code of Ethics and Standards and promoting good practices. Includes practices relating to: international, country, or industry specific issues; specific types of engagements; and legal or regulatory issues Implementation Guidance/Practice Advisories - Recommended Guidance (Dic 2015) Ref # Implementation Guide/Practice Advisory Date IG1000 NEW! IG1000: Purpose, Authority, and Responsibility July 2015 (Supersedes: PA Internal Audit Charter) Organizational Independence January Board Interaction January Individual Objectivity January Impairment to Independence or Objectivity January A1-1 Assessing Operations for Which Internal Auditors Were Previously Responsible January 2009 Supplemental Guidance (Practice Guides) Detailed guidance for conducting internal audit activities. Includes detailed processes and procedures, such as tools and techniques, programs, and step-by-step approaches, including examples of deliverables. 17 Global Technology Audit Guides (GTAG) related to information technology (IT) management, control, and security. 3 Guide on the assessment of IT Risk (GAIT) address a specific aspect of IT risk and control assessment 23 Additional Practice Guides Provides detailed guidance for conducting internal audit activities, including processes and procedures, tools and techniques, programs, step-by-step approaches, and examples of deliverables 14

15 Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent with the Definition of Internal Auditing, the Code of Ethics, and the Standards. The chief audit executive must periodically review the internal audit charter and present it to senior management and the board for approval. Approved by Board Internal Audit Authority Audit Charter Mutual agreement upon 15 IA objectives and responsibilities. The expectations Functional and administrative reporting lines Level of authority (including access to records, physical property and personnel)

16 Attribute Standards 1100 Independence and Objectivity The internal audit activity must be independent, and internal auditors must be objective in performing their work. Organizational Independence to carry out internal audit responsibilities in an unbiased manner Individual Objectivity Impartial e unbiased mental attitude that avoids any conflict of interest. FOCUS ON: Dual-Reporting Relationships Functional reporting to the Board Direct Interaction with the Board FOCUS ON Disclosure of Impairment Presumptions Previous Responsibilities Gifts policy 16

17 Attribute Standards 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Knowledge, skills, and other competencies SYSTEMATIC DISCIPLINED APPROACH Care and skill expected of a reasonably prudent and competent internal auditor internal audit standards, procedures, and techniques / accounting principles and techniques / indicators of fraud. key information technology risks and controls an understanding of management principles / an appreciation of accounting, economics, commercial law, taxation, finance, quantitative methods, information technology, risk management, and fraud. skills in dealing with people / in oral and written communications OR competent advice and assistance Extent of work needed to achieve the engagement's objectives Relative complexity, materiality, or significance of matters Adequacy and effectiveness of governance, risk management, and control processes; Probability of significant errors, fraud, or noncompliance; and Cost of assurance in relation to potential benefits Continuing Professional Development 17

18 Attribute Standards 1300 Proficiency and Due Professional Care The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects of the internal audit activity. Ongoing monitoring Periodic selfassessments External Assessments Full external assessment External validation Statement of conformity with the International Standards for the Professional Practice of Internal Auditing Internal Assessments CERTICATION 18

19 Performance Standards 2000 Managing the Internal Audit Activity The chief audit executive must effectively manage the internal audit activity to ensure it adds value to the organization. Planning Communi cation and Reporting Resource Management Coordination Policies and Procedures 19

20 Impact Planning Institutional Risks (as identified through ARMSC processes) Audit Universe Academic Faculty Renewal Leadership & Admin Structure Academic Reputation Risk/ Audit Universe Risk Assessment Prioritisation Selection and Sizing Audit Plan Approval Enrolment Growth and Complexit y Base Fundin g Relations hip with Key Supporte rs Research Growth, Complexi ty and Stewards hip Academic & Administrativ e Units, Centres Institutes Risk Parameters Coverage Parameters Required Audits HR Processes IT Infrastructu re Safety and Security Core Processes (e.g. Risk Management, Strategic Planning, Financial Reporting) Major IT Systems Sword Audit risk assessment Universe Internal Audit Universe Risk Framework Risks H M Inherent Risk Exposure Departm ents Operatio nal process es Multiple risk sources Audit universe Risk mapping to multiple sources Total Assurance sources Intervention type audit plan Projects Project 1 Project 2 Project 3 Project 4 Description Scope and Objective Scope and Objective Scope and Objective Scope and Objective Risk-Based Internal Audit Plan Type Audit - Assurance Audit - Assurance Audit - Consulting Audit - Assurance Priority L Timi ng L Quarter / Year Quarter / Year Quarter / Year Quarter / Year M Probabi lity Level of Effort Hours Hours Hours Hours H 20

21 Planning 21

22 Performance Standards 2100 Nature of Work The internal audit activity must evaluate and contribute to the improvement of governance, risk management, and control processes using a systematic and disciplined approach Governance Risk Management Control Combination of processes and structures implemented by the board to inform, direct, manage, and monitor the activities of the organization toward the achievement of its objectives Process, effected by board, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives. Process, effected by an board, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives relating to operations, reporting, and compliance Ethical principles and values? Efficient organization and accountability? Information & communication on risks and controls? Coordination and information flows between Key Governance Actors? Identification of objectives in line with mission? Evaluation of significant risks?? Selection of risk response in line with risk appetite? Risk reporting? 22 Controls proportionated to risks? Controls in line with risk tolerance and acceptance? Reasonable assurance of achieving the objectives (strategic; reliability and integrity of information; effectiveness and efficiency of operations; Safeguard the assets; Compliance)?

23 Performance Standards 2200 Engagement Planning Internal auditors must develop and document a plan for each engagement, including the engagement's objectives, scope, timing, and resource allocations Objectives of the activity Significant risks Adequacy of ERM& SCI Opportunity of improvememnts Planning Considerations Engagement Objectives Risk to be audited Criteria to be used Errors tollerance What we are going to audit? Where we should focus? Engagement Resource Allocation Engagement Scope Evaluation of nature and complexity of each engagement, time constraints, and available resources. How to deal with budget constrains and assurance needs? How to achieve engagement aims? Relevant systems, records, personnel, and physical properties 23

24 Performance Standards 2240 Engagement Work Program Internal auditors must develop and document work programs that achieve the engagement objectives. Scope Testing strategies Supervision Audit Program Objectives Evidences collecting Performance Resources allocation Working papers Quality Direction Execution Supervision 24

25 Performance Standards 2300 Performing the Engagement Internal auditors must identify, analyze, evaluate, and document sufficient information to achieve the engagement's objectives. Identifying Information Sufficient Analysis and Evaluation Reliable Relevant Useful Data Analytics & Continuous Auditing Detailed testin and Walthrough Analytical procedures Root cause analysis Documenting Information Relevant information to support the conclusions and engagement results 25

26 Performance Standards 2400 Communicating Results Internal auditors must communicate the results of engagements. Observations and recommendations are based on the following attributes: Criteria: The standards, measures, or expectations used in making an evaluation and/or verification TO BE Condition: The factual evidence that the internal auditor found in the course of the examination AS IS Cause: The reason for the difference between expected and actual conditions. Effect: The risk or exposure the organization and/or others encounter because of the gaps (the impact of the difference) Recommendations: based on the cause Accurate Involved Management Complete Timely Quality of Communications Objective Clear Board Corporate Governance Bodies Disseminating Results Parties who can ensure that the results are given due consideration Top Management CEO / CFO Constructive Concise Assurance Providers 26

27 Performance Standards 2500 Monitoring Progress The chief audit executive must establish and maintain a system to monitor the disposition of results communicated to management. The implementation status of recommendations is the barometer of reputation of Internal Audit Added value, Effectiveness and Reputation should be measured not statically, on the amount of audits, but dynamically considering the improvements accomplished Main value from IA activity does not derive neither from deficiencies reported nor recommendations made; but from respective resolution and implementation Main failure of the IA lies on indifference and inaction of management with respect to corrective action and persistence of detected risks Effective Recommendation Management Involvement and Committment Monitoring Tools 27

28 Performance Standards Communicating the Acceptance of Risks When the chief audit executive concludes that management has accepted a level of risk that may be unacceptable to the organization, the chief audit executive must discuss the matter with senior management. If the chief audit executive determines that the matter has not been resolved, the chief audit executive must communicate the matter to the board. IT IS NOT THE RESPONSIBILITY OF THE CHIEF AUDIT EXECUTIVE TO RESOLVE THE RISK 28

29 Audit Charter and Internal Audit Manual: Case Study S P E A K E R : D O T T. R O B E R TO R O S ATO C O U R S E O F B U S I N E S S A U D I T I N G U N I V E R S I T Y O F R O M E T O R V E R G A T A D E C E M B E R 2015

30 Audit Charter Purpose Audit Charter Must Define the position of IA into the organization Indicate the extent of Internal Auditing activities Allow unconditional access to the data, people, information and assets, whenever this is needed for Internal Audit activity 30

31 Audit Charter: main of Independence and Objectivity INTERNAL AUDITING MUST BE INDIPENDENT INTERNAL AUDITOR ARE INDEPENDENT WHEN MAY CARRY OUT THEIR RESPONSABILITIES WITHOUT TIES INDEPENDENCE IS ASSURED WHEN INTERNAL AUDIT REFERS FUNCTIONALLY TO THE BOARD Independence allows Internal Auditor to formulate an unbiased and objective opinion Adequate organizational position and objectivity of Internal Auditor resulting from proficiency and due professional care are prerequisite of independence. The Board approves the audit charter Independence Objectivity Charter 31

32 Audit Charter: Minimum Content INTERNAL AUDIT VISION Elements of Audit Charter MISSION DEFINITION SCOPE POSITION AND ROLE 32

33 Audit Charter: Vision and Mission Vision Long Term Objectives Raise awareness of the risks and controls throughout the organization and promote company's values. Mission Ultimate Reason of Internal Audit Activity Review the adequacy of the internal control and risk management system, its functioning and effectiveness, providing a reasonable assurance to Corporate and Control Bodies and to Top Management 33

34 Audit Charter: Definition and Scope Definition Nature of work Internal Auditing is an independent and objective assurance and consulting activity that is guided by a philosophy of adding value to improve the operations of the organization. It assists the organization in accomplishing its objectives by bringing a systematic and disciplined approach to evaluate and improve the effectiveness of the organization's governance, risk management, internal control Scope Responsabilità and Authority The scope of internal auditing encompasses, but is not limited to, the examination and evaluation of the adequacy and effectiveness of the organization's governance, risk management, and internal controls as well as the quality of performance in carrying out assigned responsibilities to achieve the organization s stated goals and objectives. The internal audit activity, with strict accountability for confidentiality and safeguarding records and information, is authorized full, free, and unrestricted access to any and all of organization records, physical properties, and personnel pertinent to carrying out any engagement. All employees are requested to assist the internal audit activity in fulfilling its roles and responsibilities. The internal audit activity will also have free and unrestricted access to the Board 34

35 Audit Charter: Position Board Audit Committee Position CEO Statutory Auditors Board Internal Audit Activity Functional reporting line Hierarchic reporting line Administrative reporting line 35

36 Internal Audit Manual 2040 Policies and Procedures «The chief audit executive must establish policies and procedures to guide the internal audit activity» The form and content of policies and procedures are dependent upon the size and structure of the internal audit activity and the complexity of its work: A small internal audit activity may be managed informally. Its audit staff may be directed and controlled through daily, close supervision and memoranda that state policies and procedures to be followed. In a large internal audit activity, more formal and comprehensive policies and procedures are essential to guide the internal audit staff in the execution of the internal audit plan. 36

37 IA Manual Objectives Establishing uniform criteria for internal control and risk management evaluation Standardizing operating activities and practices regarding Internal Control System NEEDS Supporting a continuous improvement of methodologies and practices Optimizing efficiency and productivity of Internal Audit Activity 37

38 IA Manual Content 1. Risk Management and Internal Control Frameworks 4. Audit Process 2. Internal audit organization, position and role 5. Communication and reporting 3. Audit Planning 6. Quality Assurance and Improvement Program 7. Human Resource Management 38

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Introduction to the International Standards Internal auditing is conducted in diverse legal and cultural environments;

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Introduction to the International Standards Internal auditing is conducted in diverse legal and cultural environments;

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Revised: October 2012 i Table of contents Attribute Standards... 3 1000 Purpose, Authority, and Responsibility...

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Revised: October 2012 i Table of contents Attribute Standards... 3 1000 Purpose, Authority, and Responsibility...

Internal Audit Standards

Internal Audit Standards Department of Public Expenditure & Reform November 2012 Copyright in material supplied by third parties remains with the authors. This includes: - the Definition of Internal Auditing

Internal Audit Standards Department of Public Expenditure & Reform November 2012 Copyright in material supplied by third parties remains with the authors. This includes: - the Definition of Internal Auditing

Standards for the Professional Practice of Internal Auditing

Standards for the Professional Practice of Internal Auditing THE INSTITUTE OF INTERNAL AUDITORS 247 Maitland Avenue Altamonte Springs, Florida 32701-4201 Copyright c 2001 by The Institute of Internal Auditors,

Standards for the Professional Practice of Internal Auditing THE INSTITUTE OF INTERNAL AUDITORS 247 Maitland Avenue Altamonte Springs, Florida 32701-4201 Copyright c 2001 by The Institute of Internal Auditors,

BOARD OF EDUCATION OF BALTIMORE COUNTY OFFICE OF INTERNAL AUDIT - OPERATIONS MANUAL INTERNAL AUDIT OPERATIONS MANUAL

BOARD OF EDUCATION OF BALTIMORE COUNTY INTERNAL AUDIT OPERATIONS MANUAL BACKGROUND The Office of Internal Audit Operations Manual was developed to be used as a guide and resource for the Office of Internal

BOARD OF EDUCATION OF BALTIMORE COUNTY INTERNAL AUDIT OPERATIONS MANUAL BACKGROUND The Office of Internal Audit Operations Manual was developed to be used as a guide and resource for the Office of Internal

INTERNAL AUDIT CHARTER AND TERMS OF REFERENCE

INTERNAL AUDIT CHARTER AND TERMS OF REFERENCE CHARTERED INSTITUTE OF INTERNAL AUDIT DEFINITION OF INTERNAL AUDIT Internal auditing is an independent, objective assurance and consulting activity designed

INTERNAL AUDIT CHARTER AND TERMS OF REFERENCE CHARTERED INSTITUTE OF INTERNAL AUDIT DEFINITION OF INTERNAL AUDIT Internal auditing is an independent, objective assurance and consulting activity designed

Effective Internal Audit in the Financial Services Sector

Effective Internal Audit in the Financial Services Sector Recommendations from the Committee on Internal Audit Guidance for Financial Services: How They Relate to the Global Institute of Internal Auditors

Effective Internal Audit in the Financial Services Sector Recommendations from the Committee on Internal Audit Guidance for Financial Services: How They Relate to the Global Institute of Internal Auditors

Public Sector Internal Audit Standards

Public Sector Internal Audit Standards Table of Contents Section 1 Introduction 3 Section 2 Applicability 6 Section 3 Definition of Internal Auditing 8 Section 4 Code of Ethics 9 Section 5 Standards 12

Public Sector Internal Audit Standards Table of Contents Section 1 Introduction 3 Section 2 Applicability 6 Section 3 Definition of Internal Auditing 8 Section 4 Code of Ethics 9 Section 5 Standards 12

Public Sector Internal Audit Standards. Applying the IIA International Standards to the UK Public Sector

Public Sector Internal Audit Standards Applying the IIA International Standards to the UK Public Sector Issued by the Relevant Internal Audit Standard Setters: In collaboration with: Public Sector Internal

Public Sector Internal Audit Standards Applying the IIA International Standards to the UK Public Sector Issued by the Relevant Internal Audit Standard Setters: In collaboration with: Public Sector Internal

The Framework for Quality Assurance

Chapter 1 The Framework for Quality Assurance O v e rv i e w One of internal audit s major assets is its credibility with stakeholders. To provide credible assistance and constructive challenge to management,

Chapter 1 The Framework for Quality Assurance O v e rv i e w One of internal audit s major assets is its credibility with stakeholders. To provide credible assistance and constructive challenge to management,

Public Sector Internal Audit Standards. Applying the IIA International Standards to the UK Public Sector

Public Sector Internal Audit Standards Applying the IIA International Standards to the UK Public Sector Issued by the Relevant Internal Audit Standard Setters: In collaboration with: Public Sector Internal

Public Sector Internal Audit Standards Applying the IIA International Standards to the UK Public Sector Issued by the Relevant Internal Audit Standard Setters: In collaboration with: Public Sector Internal

MISSION STATEMENT OBJECTIVES IN ACCOMPLISHING OUR MISSION

MISSION STATEMENT Internal Audit exists to support administration and the Board of Directors in the effective discharge of their responsibilities. Using our knowledge and professional judgment, we will

MISSION STATEMENT Internal Audit exists to support administration and the Board of Directors in the effective discharge of their responsibilities. Using our knowledge and professional judgment, we will

INTERNAL AUDIT MANUAL

དང ལ ར ས ལ ན ཁག Internal Audit Manual INTERNAL AUDIT MANUAL Royal Government of Bhutan 2014 i i ii ii Internal Audit Manual དང ལ ར ས ལ ན ཁག ROYAL GOVERNMNET OF BHUTAN MINISTRY OF FINANCE TASHICHHO DZONG

དང ལ ར ས ལ ན ཁག Internal Audit Manual INTERNAL AUDIT MANUAL Royal Government of Bhutan 2014 i i ii ii Internal Audit Manual དང ལ ར ས ལ ན ཁག ROYAL GOVERNMNET OF BHUTAN MINISTRY OF FINANCE TASHICHHO DZONG

Internal Auditing Guidelines

Internal Auditing Guidelines Recommendations on Internal Auditing for Lottery Operators Issued by the WLA Security and Risk Management Committee V1.0, March 2007 The WLA Internal Auditing Guidelines may

Internal Auditing Guidelines Recommendations on Internal Auditing for Lottery Operators Issued by the WLA Security and Risk Management Committee V1.0, March 2007 The WLA Internal Auditing Guidelines may

EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW)

") EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW) Phil Tarling PRESIDENT Carolyn Dittmeier VICE PRESIDENT Head Office: c/o IIA Belgium Koningstraat 109-111, bus 5 - B-1000 Brussels (Belgium)

EUROPEAN CONFEDERATION OF INSTITUTES OF INTERNAL AUDITING (IVZW) Phil Tarling PRESIDENT Carolyn Dittmeier VICE PRESIDENT Head Office: c/o IIA Belgium Koningstraat 109-111, bus 5 - B-1000 Brussels (Belgium)

SECTION B DEFINITION, PURPOSE, INDEPENDENCE AND NATURE OF WORK OF INTERNAL AUDIT

SECTION B DEFINITION, PURPOSE, INDEPENDENCE AND NATURE OF WORK OF INTERNAL AUDIT Through CGIAR Financial Guideline No 3 Auditing Guidelines Manual the CGIAR has adopted the IIA Definition of internal auditing

SECTION B DEFINITION, PURPOSE, INDEPENDENCE AND NATURE OF WORK OF INTERNAL AUDIT Through CGIAR Financial Guideline No 3 Auditing Guidelines Manual the CGIAR has adopted the IIA Definition of internal auditing

1. This bulletin, which contains the Charter of the Office of Internal Oversight Services (IOS) of

of") UNIDO/DGB/(M).92/Rev.3 28 January 2015 Distribution: All staff members at headquarters, established offices and permanent missions 1. This bulletin, which contains the Charter of the Office of Internal

UNIDO/DGB/(M).92/Rev.3 28 January 2015 Distribution: All staff members at headquarters, established offices and permanent missions 1. This bulletin, which contains the Charter of the Office of Internal

IIA Position Paper: THE THREE LINES OF DEFENSE IN EFFECTIVE RISK MANAGEMENT AND CONTROL

IIA Position Paper: THE THREE LINES OF DEFENSE IN EFFECTIVE RISK MANAGEMENT AND CONTROL JANUARY 2013 TABLE OF CONTENTS Introduction... 1 Before the Three Lines: Risk Management Oversight and Strategy-Setting...

IIA Position Paper: THE THREE LINES OF DEFENSE IN EFFECTIVE RISK MANAGEMENT AND CONTROL JANUARY 2013 TABLE OF CONTENTS Introduction... 1 Before the Three Lines: Risk Management Oversight and Strategy-Setting...

The Institute of Internal Auditors 247 Maitland Avenue Altamonte Springs, FL 32701-4201 USA

INTERNATIONAL Professional Practices Framework (IPPF) Disclosure Copyright 2009 by The Institute of Internal Auditors Research Foundation (IIARF), 247 Maitland Avenue, Altamonte Springs, Florida 32701-4201.

INTERNATIONAL Professional Practices Framework (IPPF) Disclosure Copyright 2009 by The Institute of Internal Auditors Research Foundation (IIARF), 247 Maitland Avenue, Altamonte Springs, Florida 32701-4201.

Positioning the internal audit function within the Solvency II framework Key challenges. Ludovic Bardon Senior Manager Audit Deloitte Luxembourg

Positioning the internal audit function within the Solvency II framework Key challenges Jérôme Sosnowski Director Governance, Risk & Compliance Deloitte Luxembourg Ludovic Bardon Senior Manager Audit Deloitte

Positioning the internal audit function within the Solvency II framework Key challenges Jérôme Sosnowski Director Governance, Risk & Compliance Deloitte Luxembourg Ludovic Bardon Senior Manager Audit Deloitte

Internal Audit Quality Assessment. Presented To: World Intellectual Property Organization

Internal Audit Quality Assessment Presented To: World Intellectual Property Organization April 2014 Table of Contents List of Acronyms 3 Page Executive Summary Opinion as to Conformance to the Standards,

Internal Audit Quality Assessment Presented To: World Intellectual Property Organization April 2014 Table of Contents List of Acronyms 3 Page Executive Summary Opinion as to Conformance to the Standards,

What Every Director. How to get the most from your internal audit. Endorsed by

What Every Director Should Know How to get the most from your internal audit Endorsed by Foreword This is the second edition of our flagship governance guide What every director should know. Since we published

What Every Director Should Know How to get the most from your internal audit Endorsed by Foreword This is the second edition of our flagship governance guide What every director should know. Since we published

Administrative Guidelines on the Internal Control Framework and Internal Audit Standards

Administrative Guidelines on the Internal Control Framework and Internal Audit Standards GCF/B.09/18 18 February 2015 Meeting of the Board 24 26 March 2015 Songdo, Republic of Korea Agenda item 24 Page

Administrative Guidelines on the Internal Control Framework and Internal Audit Standards GCF/B.09/18 18 February 2015 Meeting of the Board 24 26 March 2015 Songdo, Republic of Korea Agenda item 24 Page

Internal Oversight Division Internal Audit Manual

Internal Oversight Division Internal Audit Manual Updated Version November 2014 March 2015 1 1. PURPOSE... 2 2. INTERNAL AUDIT FUNCTION... 3 3. ORGANIZATIONAL STRUCTURE AND RESPONSIBILITIES... 4 3.1 THE

Internal Oversight Division Internal Audit Manual Updated Version November 2014 March 2015 1 1. PURPOSE... 2 2. INTERNAL AUDIT FUNCTION... 3 3. ORGANIZATIONAL STRUCTURE AND RESPONSIBILITIES... 4 3.1 THE

How To Comply With The Law Of The Firm

A Firm s System of Quality Control 2523 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8. Effective date: Applicable to a CPA firm s system of quality control

A Firm s System of Quality Control 2523 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8. Effective date: Applicable to a CPA firm s system of quality control

Practice Guide COORDINATING RISK MANAGEMENT AND ASSURANCE

Practice Guide COORDINATING RISK MANAGEMENT AND ASSURANCE March 2012 Table of Contents Executive Summary... 1 Introduction... 1 Risk Management and Assurance (Assurance Services)... 1 Assurance Framework...

Practice Guide COORDINATING RISK MANAGEMENT AND ASSURANCE March 2012 Table of Contents Executive Summary... 1 Introduction... 1 Risk Management and Assurance (Assurance Services)... 1 Assurance Framework...

Internal Audit Charter. Version 1 (7 November 2013)

") Version 1 (7 November 2013) CONTENTS Details Page EXECUTIVE SUMMARY... 2 1. BACKGROUND... 3 10. PSIAS REQUIREMENTS... 3 12. DEFINITION OF THE CHIEF AUDIT EXECUTIVE (CAE)... 4 14. DEFINITION OF THE BOARD...

Version 1 (7 November 2013) CONTENTS Details Page EXECUTIVE SUMMARY... 2 1. BACKGROUND... 3 10. PSIAS REQUIREMENTS... 3 12. DEFINITION OF THE CHIEF AUDIT EXECUTIVE (CAE)... 4 14. DEFINITION OF THE BOARD...

INTERNAL AUDITING POLICIES AND PROCEDURES MANUAL

INTERNAL AUDITING POLICIES AND PROCEDURES MANUAL 2 TABLE OF CONTENTS Contents A. INTERNAL AUDIT OVERVIEW... 5 A.1 RATIONALE... 5 A-2 CHARTER... 5 A-3 MISSION STATEMENT, OBJECTIVES AND VALUES... 9 A-3.1

INTERNAL AUDITING POLICIES AND PROCEDURES MANUAL 2 TABLE OF CONTENTS Contents A. INTERNAL AUDIT OVERVIEW... 5 A.1 RATIONALE... 5 A-2 CHARTER... 5 A-3 MISSION STATEMENT, OBJECTIVES AND VALUES... 9 A-3.1

RISK BASED AUDITING: A VALUE ADD PROPOSITION. Participant Guide

RISK BASED AUDITING: A VALUE ADD PROPOSITION Participant Guide About This Course About This Course Adding Value for Risk-based Auditing Seminar Description In this seminar, we will focus on: The foundation

RISK BASED AUDITING: A VALUE ADD PROPOSITION Participant Guide About This Course About This Course Adding Value for Risk-based Auditing Seminar Description In this seminar, we will focus on: The foundation

MISSION VALUES. The guide has been printed by:

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

Internal Auditing: Assurance, Insight, and Objectivity

Internal Auditing: Assurance, Insight, and Objectivity WHAT IS INTERNAL AUDITING? INTERNAL AUDITING business people all around the world are familiar with the term. But do they understand the value it

Internal Auditing: Assurance, Insight, and Objectivity WHAT IS INTERNAL AUDITING? INTERNAL AUDITING business people all around the world are familiar with the term. But do they understand the value it

Practice guide. quality assurance and IMProVeMeNt PrograM

Practice guide quality assurance and IMProVeMeNt PrograM MarCh 2012 Table of Contents Executive Summary... 1 Introduction... 2 What is Quality?... 2 Quality in Internal Audit... 2 Conformance or Compliance?...

Practice guide quality assurance and IMProVeMeNt PrograM MarCh 2012 Table of Contents Executive Summary... 1 Introduction... 2 What is Quality?... 2 Quality in Internal Audit... 2 Conformance or Compliance?...

PRACTICE ADVISORIES FOR INTERNAL AUDIT

Société Française de Réalisation, d'etudes et de Conseil Economics and Public Management Department PRACTICE ADVISORIES FOR INTERNAL AUDIT Tehnical Assistance to the Ministry of Finance for Development

Société Française de Réalisation, d'etudes et de Conseil Economics and Public Management Department PRACTICE ADVISORIES FOR INTERNAL AUDIT Tehnical Assistance to the Ministry of Finance for Development

Guidance Note: Corporate Governance - Board of Directors. March 2015. Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

Guidance Note: Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

October 20, 2015. Sincerely. Anthony Chavez, CIA, CGAP, CRMA Director, Internal Audit Division

Internal Audit Annual Report Fiscal Year 2015 October 20, 2015 Honorable Greg Abbott, Governor Members of the Legislative Budget Board Members of the Sunset Advisory Commission Mr. John Keel, CPA, State

Internal Audit Annual Report Fiscal Year 2015 October 20, 2015 Honorable Greg Abbott, Governor Members of the Legislative Budget Board Members of the Sunset Advisory Commission Mr. John Keel, CPA, State

INTERNAL AUDITING S ROLE IN SECTIONS 302 AND 404

INTERNAL AUDITING S ROLE IN SECTIONS 302 AND 404 OF THE U.S. SARBANES-OXLEY ACT OF 2002 May 26, 2004 Copyright 2004 by, 247 Maitland Avenue, Altamonte Springs, Florida, 32701-4201, USA Internal Auditing

INTERNAL AUDITING S ROLE IN SECTIONS 302 AND 404 OF THE U.S. SARBANES-OXLEY ACT OF 2002 May 26, 2004 Copyright 2004 by, 247 Maitland Avenue, Altamonte Springs, Florida, 32701-4201, USA Internal Auditing

Internal Audit Manual

Internal Audit Manual Version 1.0 AUDIT AND EVALUATION SECTOR AUDIT AND ASSURANCE SERVICES BRANCH INDIAN AND NORTHERN AFFAIRS CANADA April 25, 2008 #933907 Acknowledgements The Institute of Internal Auditors

Internal Audit Manual Version 1.0 AUDIT AND EVALUATION SECTOR AUDIT AND ASSURANCE SERVICES BRANCH INDIAN AND NORTHERN AFFAIRS CANADA April 25, 2008 #933907 Acknowledgements The Institute of Internal Auditors

SAI GLOBAL LIMITED Risk Management Policy

SAI GLOBAL LIMITED Risk Management Policy SAI Global Ltd ABN 67050611642 Last Updated: February 2012 Contents 1. Risk Management... 3 2. Policy... 3 3. Risk Management Philosophy... 3 4. Risk Appetite...

SAI GLOBAL LIMITED Risk Management Policy SAI Global Ltd ABN 67050611642 Last Updated: February 2012 Contents 1. Risk Management... 3 2. Policy... 3 3. Risk Management Philosophy... 3 4. Risk Appetite...

Internal Audit Charter

February 2015 Contacts For general enquiries, please contact: Daryn Wedd General Manager Internal Audit T 9227 0978 E [email protected] Media enquiries, please contact: Ms Kristen Kaus Media and Communications

February 2015 Contacts For general enquiries, please contact: Daryn Wedd General Manager Internal Audit T 9227 0978 E [email protected] Media enquiries, please contact: Ms Kristen Kaus Media and Communications

GAO. Government Auditing Standards. 2011 Revision. By the Comptroller General of the United States. United States Government Accountability Office

GAO United States Government Accountability Office By the Comptroller General of the United States December 2011 Government Auditing Standards 2011 Revision GAO-12-331G GAO United States Government Accountability

GAO United States Government Accountability Office By the Comptroller General of the United States December 2011 Government Auditing Standards 2011 Revision GAO-12-331G GAO United States Government Accountability

Internal Audit Charters

Internal Audit Charters Part of a series of notes to help Centers review their own internal management processes from the point of view of managing risks and promoting good governance and value for money,

Internal Audit Charters Part of a series of notes to help Centers review their own internal management processes from the point of view of managing risks and promoting good governance and value for money,

How quality assurance reviews can strengthen the strategic value of internal auditing*

How quality assurance reviews can strengthen the strategic value of internal auditing* PwC Advisory Internal Audit Table of Contents Situation Pg. 02 In response to an increased focus on effective governance,

How quality assurance reviews can strengthen the strategic value of internal auditing* PwC Advisory Internal Audit Table of Contents Situation Pg. 02 In response to an increased focus on effective governance,

The IIA Global Internal Audit Competency Framework

About The IIA Global Internal Audit Competency Framework The IIA Global Internal Audit Competency Framework (the Framework) is a tool that defines the competencies needed to meet the requirements of the

About The IIA Global Internal Audit Competency Framework The IIA Global Internal Audit Competency Framework (the Framework) is a tool that defines the competencies needed to meet the requirements of the

B o a r d of Governors of the Federal Reserve System. Supplemental Policy Statement on the. Internal Audit Function and Its Outsourcing

B o a r d of Governors of the Federal Reserve System Supplemental Policy Statement on the Internal Audit Function and Its Outsourcing January 23, 2013 P U R P O S E This policy statement is being issued

B o a r d of Governors of the Federal Reserve System Supplemental Policy Statement on the Internal Audit Function and Its Outsourcing January 23, 2013 P U R P O S E This policy statement is being issued

Data Analysis: The Cornerstone of Effective Internal Auditing. A CaseWare Analytics Research Report

Data Analysis: The Cornerstone of Effective Internal Auditing A CaseWare Analytics Research Report Contents Why Data Analysis Step 1: Foundation - Fix Any Cracks First Step 2: Risk - Where to Look Step

Data Analysis: The Cornerstone of Effective Internal Auditing A CaseWare Analytics Research Report Contents Why Data Analysis Step 1: Foundation - Fix Any Cracks First Step 2: Risk - Where to Look Step

Quality Assurance Checklist

Internal Audit Foundations Standards 1000, 1010, 1100, 1110, 1111, 1120, 1130, 1300, 1310, 1320, 1321, 1322, 2000, 2040 There is an Internal Audit Charter in place Internal Audit Charter is in place The

Internal Audit Foundations Standards 1000, 1010, 1100, 1110, 1111, 1120, 1130, 1300, 1310, 1320, 1321, 1322, 2000, 2040 There is an Internal Audit Charter in place Internal Audit Charter is in place The

INTERNAL AUDIT FRAMEWORK

INTERNAL AUDIT FRAMEWORK April 2007 Contents 1. Introduction... 3 2. Internal Audit Definition... 4 3. Structure... 5 3.1. Roles, Responsibilities and Accountabilities... 5 3.2. Authority... 11 3.3. Composition...

INTERNAL AUDIT FRAMEWORK April 2007 Contents 1. Introduction... 3 2. Internal Audit Definition... 4 3. Structure... 5 3.1. Roles, Responsibilities and Accountabilities... 5 3.2. Authority... 11 3.3. Composition...

GAO. Government Auditing Standards: Implementation Tool

United States Government Accountability Office GAO By the Comptroller General of the United States December 2007 Government Auditing Standards: Implementation Tool Professional Requirements Tool for Use

United States Government Accountability Office GAO By the Comptroller General of the United States December 2007 Government Auditing Standards: Implementation Tool Professional Requirements Tool for Use

Annual Assessment of the External Auditor

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

PRACTICE GUIDE. Formulating and Expressing Internal Audit Opinions

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

PRACTICE GUIDE Formulating and Expressing Internal Audit Opinions 2 of 23 Table of Contents 1. Executive Summary... 1 2. Introduction... 2 3. Planning the Expression of an Opinion... 3 3.1 Expressing an

Internal Audit Terms of Reference

Internal Audit Terms of Reference Introduction 1. The Internal Audit Terms of Reference (ToR) describes the framework within which the Internal Audit Service is delivered. It is intended to act as a guide

Internal Audit Terms of Reference Introduction 1. The Internal Audit Terms of Reference (ToR) describes the framework within which the Internal Audit Service is delivered. It is intended to act as a guide

DNV GL Assessment Checklist ISO 9001:2015

DNV GL Assessment Checklist ISO 9001:2015 Rev 0 - December 2015 4 Context of the Organization No. Question Proc. Ref. Comments 4.1 Understanding the Organization and its context 1 Has the organization

DNV GL Assessment Checklist ISO 9001:2015 Rev 0 - December 2015 4 Context of the Organization No. Question Proc. Ref. Comments 4.1 Understanding the Organization and its context 1 Has the organization

ENTERPRISE RISK MANAGEMENT POLICY

ENTERPRISE RISK MANAGEMENT POLICY TITLE OF POLICY POLICY OWNER POLICY CHAMPION DOCUMENT HISTORY: Policy Title Status Enterprise Risk Management Policy (current, revised, no change, redundant) Approving

ENTERPRISE RISK MANAGEMENT POLICY TITLE OF POLICY POLICY OWNER POLICY CHAMPION DOCUMENT HISTORY: Policy Title Status Enterprise Risk Management Policy (current, revised, no change, redundant) Approving

How to gather and evaluate information

09 May 2016 How to gather and evaluate information Chartered Institute of Internal Auditors Information is central to the role of an internal auditor. Gathering and evaluating information is the basic

09 May 2016 How to gather and evaluate information Chartered Institute of Internal Auditors Information is central to the role of an internal auditor. Gathering and evaluating information is the basic

the role of the head of internal audit in public service organisations 2010

the role of the head of internal audit in public service organisations 2010 CIPFA Statement on the role of the Head of Internal Audit in public service organisations The Head of Internal Audit in a public

the role of the head of internal audit in public service organisations 2010 CIPFA Statement on the role of the Head of Internal Audit in public service organisations The Head of Internal Audit in a public

Department of Audit and Compliance. Quality Self-Assessment

Department of Audit and Compliance Quality Self-Assessment November 2014 CONTENTS EXECUTIVE SUMMARY... 2 PURPOSE OF SELF-ASSESSMENT... 4 SELF-ASSESSMENT SCOPE OF WORK... 4 RESULTS OF SELF-ASSESSMENT WORK...

Department of Audit and Compliance Quality Self-Assessment November 2014 CONTENTS EXECUTIVE SUMMARY... 2 PURPOSE OF SELF-ASSESSMENT... 4 SELF-ASSESSMENT SCOPE OF WORK... 4 RESULTS OF SELF-ASSESSMENT WORK...

The New IPPF: What to Expect

The New IPPF: What to Expect Agenda Reminder the previous IPPF Why a new IPPF? What is not changing What s new (and why) What to expect going forward Reminder the Previous IPPF Why a new IPPF? Questions

The New IPPF: What to Expect Agenda Reminder the previous IPPF Why a new IPPF? What is not changing What s new (and why) What to expect going forward Reminder the Previous IPPF Why a new IPPF? Questions

Internal Audit Division

Internal Audit Division at the Financial Conduct Authority Information Pack April 2013 Contents of Information Pack A. Introduction B. Internal Audit Terms of Reference C. Organisation D. Skills and Competencies

Internal Audit Division at the Financial Conduct Authority Information Pack April 2013 Contents of Information Pack A. Introduction B. Internal Audit Terms of Reference C. Organisation D. Skills and Competencies

Effective Internal Audit in the Financial. Services Sector. Non Executive Directors (NEDs) and the Management of Risk

and the Management of Risk") Consultation document Effective Internal Audit in the Financial A survey of heads of internal audit Services Sector Non Executive Directors (NEDs) and the Management of Risk Draft recommendations to the

Consultation document Effective Internal Audit in the Financial A survey of heads of internal audit Services Sector Non Executive Directors (NEDs) and the Management of Risk Draft recommendations to the

INTERNATIONAL STANDARD ON AUDITING 610 USING THE WORK OF INTERNAL AUDITORS CONTENTS

INTERNATIONAL STANDARD ON 610 USING THE WORK OF INTERNAL AUDITORS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

INTERNATIONAL STANDARD ON 610 USING THE WORK OF INTERNAL AUDITORS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

IS Audit and Assurance Guideline 2202 Risk Assessment in Planning

IS Audit and Assurance Guideline 2202 Risk Assessment in Planning The specialised nature of information systems (IS) audit and assurance and the skills necessary to perform such engagements require standards

IS Audit and Assurance Guideline 2202 Risk Assessment in Planning The specialised nature of information systems (IS) audit and assurance and the skills necessary to perform such engagements require standards

Audit and Risk Committee Charter. 1. Membership of the Committee. 2. Administrative matters

Audit and Risk Committee Charter The Audit and Risk Committee (the Committee ) is a Committee of the Board established with the specific powers delegated to it under Clause 8.15 of the Company s Constitution

Audit and Risk Committee Charter The Audit and Risk Committee (the Committee ) is a Committee of the Board established with the specific powers delegated to it under Clause 8.15 of the Company s Constitution

A Guide to Corporate Governance for QFC Authorised Firms

A Guide to Corporate Governance for QFC Authorised Firms January 2012 Disclaimer The goal of the Qatar Financial Centre Regulatory Authority ( Regulatory Authority ) in producing this document is to provide

A Guide to Corporate Governance for QFC Authorised Firms January 2012 Disclaimer The goal of the Qatar Financial Centre Regulatory Authority ( Regulatory Authority ) in producing this document is to provide

Establishing a Quality Assurance and Improvement Program

Chapter 2 Establishing a Quality Assurance and Improvement Program O v e rv i e w IIA Practice Guide, Quality Assurance and Improvement Program, states that Quality should be built in to, and not on to,

Chapter 2 Establishing a Quality Assurance and Improvement Program O v e rv i e w IIA Practice Guide, Quality Assurance and Improvement Program, states that Quality should be built in to, and not on to,

Guidance for audit committees. The internal audit function

Guidance for audit committees The internal audit function March 2004 The Combined Code on Corporate Governance July 2003 C.3 Audit Committee and Auditors Main Principle: The board should establish formal

Guidance for audit committees The internal audit function March 2004 The Combined Code on Corporate Governance July 2003 C.3 Audit Committee and Auditors Main Principle: The board should establish formal

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

How To Understand The Role Of An Internal Audit

Top Ten Issues facing Internal Auditing in the Future The IIA Dallas Chapter April 6, 2006 Presented by: David A. Richards, CIA, CPA President The Institute of Internal Auditors [email protected] 1

Top Ten Issues facing Internal Auditing in the Future The IIA Dallas Chapter April 6, 2006 Presented by: David A. Richards, CIA, CPA President The Institute of Internal Auditors [email protected] 1

SunTrust Banks, Inc. Audit Committee of the Board of Directors Charter

SunTrust Banks, Inc. Audit Committee of the Board of Directors Charter PURPOSE The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of SunTrust Banks, Inc. (the Company

SunTrust Banks, Inc. Audit Committee of the Board of Directors Charter PURPOSE The Audit Committee (the Committee ) is appointed by the Board of Directors (the Board ) of SunTrust Banks, Inc. (the Company

Audit, Risk and Compliance Committee Charter

1. Background Audit, Risk and Compliance Committee Charter The Audit, Risk and Compliance Committee is a Committee of the Board of Directors ( Board ) of Syrah Resources Limited (ACN 125 242 284) ( Syrah

1. Background Audit, Risk and Compliance Committee Charter The Audit, Risk and Compliance Committee is a Committee of the Board of Directors ( Board ) of Syrah Resources Limited (ACN 125 242 284) ( Syrah

Audit of the Test of Design of Entity-Level Controls

Audit of the Test of Design of Entity-Level Controls Canadian Grain Commission Audit & Evaluation Services Final Report March 2012 Canadian Grain Commission 0 Entity Level Controls 2011 Table of Contents

Audit of the Test of Design of Entity-Level Controls Canadian Grain Commission Audit & Evaluation Services Final Report March 2012 Canadian Grain Commission 0 Entity Level Controls 2011 Table of Contents

DATA ANALYSIS: THE CORNERSTONE OF EFFECTIVE INTERNAL AUDITING. A CaseWare IDEA Research Report

DATA ANALYSIS: THE CORNERSTONE OF EFFECTIVE INTERNAL AUDITING A CaseWare IDEA Research Report CaseWare IDEA Inc. is a privately held software development and marketing company, with offices in Toronto

DATA ANALYSIS: THE CORNERSTONE OF EFFECTIVE INTERNAL AUDITING A CaseWare IDEA Research Report CaseWare IDEA Inc. is a privately held software development and marketing company, with offices in Toronto

Application of King III Corporate Governance Principles

APPLICATION of KING III CORPORATE GOVERNANCE PRINCIPLES 2013 Application of Corporate Governance Principles This table is a useful reference to each of the principles and how, in broad terms, they have

APPLICATION of KING III CORPORATE GOVERNANCE PRINCIPLES 2013 Application of Corporate Governance Principles This table is a useful reference to each of the principles and how, in broad terms, they have

Performance Measures for Internal Auditing

Performance Measures for Internal Auditing A simple question someone may ask is Why measure performance? An even simpler response would be that what gets measured gets done. McMaster University s discussion

Performance Measures for Internal Auditing A simple question someone may ask is Why measure performance? An even simpler response would be that what gets measured gets done. McMaster University s discussion

PUBLIC ACCOUNTANTS COUNCIL HANDBOOK

PUBLIC ACCOUNTANTS COUNCIL HANDBOOK Adopted by the Public Accountants Council for the Province of Ontario: April 17, 2006 PART I: PROFESSIONAL COMPETENCY REQUIREMENTS FOR PUBLIC ACCOUNTING PART II: PRACTICAL

PUBLIC ACCOUNTANTS COUNCIL HANDBOOK Adopted by the Public Accountants Council for the Province of Ontario: April 17, 2006 PART I: PROFESSIONAL COMPETENCY REQUIREMENTS FOR PUBLIC ACCOUNTING PART II: PRACTICAL

Application of King III Corporate Governance Principles

Application of Corporate Governance Principles Application of Corporate Governance Principles This table is a useful reference to each of the principles and how, in broad terms, they have been applied

Application of Corporate Governance Principles Application of Corporate Governance Principles This table is a useful reference to each of the principles and how, in broad terms, they have been applied

APPLICATION OF KING III CORPORATE GOVERNANCE PRINCIPLES 2014

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

WOOLWORTHS HOLDINGS LIMITED CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 CORPORATE GOVERNANCE PRINCIPLES 2014 This table is a useful reference to each of the King III principles

A&CS Assurance Review. Accounting Policy Division Rule Making Participation in Standard Setting. Report

A&CS Assurance Review Accounting Policy Division Rule Making Participation in Standard Setting Report April 2010 Table of Contents Background... 1 Engagement Objectives, Scope and Approach... 1 Overall

A&CS Assurance Review Accounting Policy Division Rule Making Participation in Standard Setting Report April 2010 Table of Contents Background... 1 Engagement Objectives, Scope and Approach... 1 Overall

Instructional Designer Standards: Competencies & Performance Statements

Standards Set 2012 ibstpi Instructional Designer Standards: Competencies & Performance Statements The 2012 ibstpi Instructional Designer Competencies and Performance statements are copyrighted by the International

Standards Set 2012 ibstpi Instructional Designer Standards: Competencies & Performance Statements The 2012 ibstpi Instructional Designer Competencies and Performance statements are copyrighted by the International

Utah Educational Leadership Standards, Performance Expectations and Indicators

Utah Educational Leadership Standards, Performance Expectations and Indicators Standard 1: Visionary Leadership An educational leader promotes the success of every student by facilitating the development,

Utah Educational Leadership Standards, Performance Expectations and Indicators Standard 1: Visionary Leadership An educational leader promotes the success of every student by facilitating the development,

Board of Directors and Senior Management 2. Audit Management 4. Internal IT Audit Staff 5. Operating Management 5. External Auditors 5.

Table of Contents Introduction 1 IT Audit Roles and Responsibilities 2 Board of Directors and Senior Management 2 Audit Management 4 Internal IT Audit Staff 5 Operating Management 5 External Auditors 5

Table of Contents Introduction 1 IT Audit Roles and Responsibilities 2 Board of Directors and Senior Management 2 Audit Management 4 Internal IT Audit Staff 5 Operating Management 5 External Auditors 5

COMPLIANCE CHARTER 1

COMPLIANCE CHARTER 1 Contents 1. Compliance Policy Statement... 2 2. Purpose... 2 3. Mission and objective of the Directorate: Compliance... 2 3.1 Mission... 2 3.2 Objective... 3 4. Compliance risk management...

COMPLIANCE CHARTER 1 Contents 1. Compliance Policy Statement... 2 2. Purpose... 2 3. Mission and objective of the Directorate: Compliance... 2 3.1 Mission... 2 3.2 Objective... 3 4. Compliance risk management...

Internal Audit Manual

COMPTROLLER OF ACCOUNTS Ministry of Finance Government of the Republic of Trinidad Tobago Internal Audit Manual Prepared by the Financial Management Branch, Treasury Division, Ministry of Finance TABLE

COMPTROLLER OF ACCOUNTS Ministry of Finance Government of the Republic of Trinidad Tobago Internal Audit Manual Prepared by the Financial Management Branch, Treasury Division, Ministry of Finance TABLE

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR OCTOBER 2014 Table of Contents Executive Summary... 1 Introduction... 1 Public Sector Characteristics... 4 Public Sector Structure...

Practice Guide ASSESSING ORGANIZATIONAL GOVERNANCE IN THE PUBLIC SECTOR OCTOBER 2014 Table of Contents Executive Summary... 1 Introduction... 1 Public Sector Characteristics... 4 Public Sector Structure...

Initial Professional Development Technical Competence (Revised)

") IFAC Board Exposure Draft July 2012 Comments due: November 1, 2012 Proposed International Education Standard (IES) 2 Initial Professional Development Technical Competence (Revised) COPYRIGHT, TRADEMARK,

IFAC Board Exposure Draft July 2012 Comments due: November 1, 2012 Proposed International Education Standard (IES) 2 Initial Professional Development Technical Competence (Revised) COPYRIGHT, TRADEMARK,

National Occupational Standards. Compliance

National Occupational Standards Compliance NOTES ABOUT NATIONAL OCCUPATIONAL STANDARDS What are National Occupational Standards, and why should you use them? National Occupational Standards (NOS) are statements

National Occupational Standards Compliance NOTES ABOUT NATIONAL OCCUPATIONAL STANDARDS What are National Occupational Standards, and why should you use them? National Occupational Standards (NOS) are statements

Human Services Quality Framework. User Guide

Human Services Quality Framework User Guide Purpose The purpose of the user guide is to assist in interpreting and applying the Human Services Quality Standards and associated indicators across all service

Human Services Quality Framework User Guide Purpose The purpose of the user guide is to assist in interpreting and applying the Human Services Quality Standards and associated indicators across all service

INSTITUTE OF FINANCIAL ADVISERS INC. P2 - PRACTICE STANDARDS

INSTITUTE OF FINANCIAL ADVISERS INC. P2 - PRACTICE STANDARDS EFFECTIVE 1 JANUARY 2012 TABLE OF CONTENTS INTRODUCTION... 2 Professional Financial Advice... 2 The Six-Step Process... 2 The Core Components...

INSTITUTE OF FINANCIAL ADVISERS INC. P2 - PRACTICE STANDARDS EFFECTIVE 1 JANUARY 2012 TABLE OF CONTENTS INTRODUCTION... 2 Professional Financial Advice... 2 The Six-Step Process... 2 The Core Components...

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER Purpose The Audit Committee ( Committee ) shall assist the Board of Directors (the Board ) in the oversight of (1) the integrity of the financial statements of the Company, (2)

AUDIT COMMITTEE CHARTER Purpose The Audit Committee ( Committee ) shall assist the Board of Directors (the Board ) in the oversight of (1) the integrity of the financial statements of the Company, (2)

Qualification details

Qualification details Title New Zealand Diploma in Organisational Risk and Compliance (Level 6) Version 1 Qualification type Diploma Level 6 Credits 120 NZSCED 080317 Quality Management DAS classification

Qualification details Title New Zealand Diploma in Organisational Risk and Compliance (Level 6) Version 1 Qualification type Diploma Level 6 Credits 120 NZSCED 080317 Quality Management DAS classification

Professional Development for Engagement Partners Responsible for Audits of Financial Statements (Revised)

") IFAC Board Exposure Draft August 2012 Comments due: December 11, 2012 Proposed International Education Standard (IES) 8 Professional Development for Engagement Partners Responsible for Audits of Financial

IFAC Board Exposure Draft August 2012 Comments due: December 11, 2012 Proposed International Education Standard (IES) 8 Professional Development for Engagement Partners Responsible for Audits of Financial

COSO Internal Control Integrated Framework (2013)

") COSO Internal Control Integrated Framework (2013) The Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its updated Internal Control Integrated Framework (2013 Framework)

COSO Internal Control Integrated Framework (2013) The Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its updated Internal Control Integrated Framework (2013 Framework)

august09 tpp 09-05 Internal Audit and Risk Management Policy for the NSW Public Sector OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper

august09 09-05 Internal Audit and Risk Management Policy for the NSW Public Sector OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Preface Corporate governance - which refers broadly to the processes

august09 09-05 Internal Audit and Risk Management Policy for the NSW Public Sector OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Preface Corporate governance - which refers broadly to the processes

Risk committee performance evaluation

Risk committee performance evaluation While there is currently not a legal or regulatory requirement for board risk committees to complete a performance evaluation, King III recommends regular performance

Risk committee performance evaluation While there is currently not a legal or regulatory requirement for board risk committees to complete a performance evaluation, King III recommends regular performance

A Risk-Based Audit Strategy November 2006 Internal Audit Department

Mental Health Mental Retardation Authority of Harris County ENTERPRISE RISK MANAGEMENT A Framework For Assessing, Evaluating And Measuring Our Agency s Risk A Risk-Based Audit Strategy November 2006 Internal

Mental Health Mental Retardation Authority of Harris County ENTERPRISE RISK MANAGEMENT A Framework For Assessing, Evaluating And Measuring Our Agency s Risk A Risk-Based Audit Strategy November 2006 Internal

11/12/2013. Role of the Board. Risk Appetite. Strategy, Planning and Performance. Risk Governance Framework. Assembling an effective team

Role of the Board Risk Appetite Strategy, Planning and Performance Risk Governance Framework Assembling an effective team Role of the CEO Accountability and Disclosure 1 Board members should act on a fully

Role of the Board Risk Appetite Strategy, Planning and Performance Risk Governance Framework Assembling an effective team Role of the CEO Accountability and Disclosure 1 Board members should act on a fully

Following up recommendations/management actions

09 May 2016 Following up recommendations/management actions Chartered Institute of Internal Auditors At the conclusion of an audit, findings and proposed recommendations are discussed with management and

09 May 2016 Following up recommendations/management actions Chartered Institute of Internal Auditors At the conclusion of an audit, findings and proposed recommendations are discussed with management and