The Short-Run Relationship between Stock Market Prices and Macroeconomic Variables in Lithuania: An Application of the Impulse Response Function

|

|

|

- Gilbert Russell

- 8 years ago

- Views:

Transcription

1 ISSN Inzinerine Ekonomika-Engineering Economics(5) ECONOMICS OF ENGINEERING DECISIONS The Short-Run Relationship between Stock Market Prices and Macroeconomic Variables in Lithuania: An Application of the Impulse Response Function Donatas Pilinkus, Vytautas Boguslauskas Kaunas University of Technology Laisves al. 55, LT-44309, Kaunas, Lithuania Scientific literature has been seemingly enriched by various theoretical and empirical studies analysing the relationship between stock market returns and macroeconomic forces during the last few decades. It is often argued that stock prices are determined by some fundamental macroeconomic variables. This implies that macroeconomic variables can influence investors investment decisions and motivates many researchers to investigate the relationships between stock market prices and macroeconomic variables. Different authors select different macroeconomic variables seeking to detect their relationship with stock market prices in various countries. Simultaneously, a number of econometric techniques such as the arbitrage pricing theory, the impulse response function, the error variance decomposition analysis, the vector error correction model, the cointegration analysis, the Granger causality tests and others may be applied for checking the existence of relationship between stock market prices and macroeconomic variables. The current paper attempts to present several classifications of macroeconomic variables, then to select macroeconomic variables for seeking their relationship with stock market prices, and, finally, to define what macroeconomic variables have positive and what macroeconomic variables have negative effects on stock market prices in Lithuania in the short run. Augmented Dickey Fuller test has been employed to check the stationarity of the selected time series since a spurious regression may occur if a time series is not stationary. The Impulse response function has been chosen to test the existence of the short-run relationship between stock market prices and macroeconomic variables. As the results of the Impulse response function are reliable only with a stationary time series the data has been turned into stationary after the second difference. The study embraces six macroeconomic variables (seasonally adjusted gross domestic product at previous year prices, harmonised consumer price index as compared to 2005, the narrow money supply, unemployment rate, short-term interest rates, and exchange rate of the Litas against the US dollar) and the main Lithuanian stock market index the OMX Vilnius index. The data are monthly and extend from the January of 2000 to the June of In general, the results of the paper clearly indicate that macroeconomic variables are significant determinants for stock market prices in Lithuania. Gross domestic product and money supply have a positive effect on stock market prices while most of the time unemployment rate, exchange rate, and short-term interest rates negatively influence stock market prices. The findings of the paper are similar to the results of some other empirical studies. If harmonised consumer price index is considered, then it is the best example of an unstable relationship between a macroeconomic variable and stock market prices in Lithuania. Keywords: macroeconomic variables, stock market prices, short-run relationship, impulse response function, Lithuania. Introduction The relationship between stock market prices and macroeconomic variables has been widely investigated in the scientific literature (Fama, 1981; Ibrahim, 1999; Gunes, 2007, etc.). For this purpose, scientists apply different econometric instruments: the arbitrage pricing theory has been employed by Fama (1981), Schwert (1990), Tursoy, Gunsel, Rjoub (2008); the impulse response function has been applied by Sims (1980), Nishat, Shaheen (2004), Adam, Tweneboah (2008); the error variance decomposition analysis has been incorporated by Lastrapes, Koray (1990), Laopodis (2007); the vector error correction model has been found relevant by Engle, Granger (1987), Kwon, Shin (1999); different types of cointegration analysis have been included by Nasseh, Strauss (2000), Dritsaki, Adamopoulos (2005); the Granger causality tests have been considered by Lee (1992), Hassan (2003), Dritsaki (2005), etc. At the same time, scientists select different macroeconomic variables in their studies. Some authors choose only one or two macroeconomic factors e.g., Comincioli (1995) seeks for the relationship between the stock market index and gross domestic product, Gallegati (2005) also prefers only one macroeconomic factor, though it is an industrial production index, Arabian, Afshar, Anjela (2008) operates with gross domestic product and oil prices; other researchers are apt to analyzing more than ten different macroeconomic variables (Tursoy, Gunsel, Rjoub, 2008). Simultaneously, authors analyze data at different time periods, i.e. daily data (Kurihara, Nezu, 2006), monthly data (Kandir, 2008; Stavarek, 2004), quarterly data (Ahmed, 2008; Comincioli, 1995) or annual data (Hussain, Mahmood, 2001; Naceur, Ghazouani, Omran, 2007).

2 Those scientists who employ the Impulse response function mainly analyze the short-run relationship between macroeconomic variables and stock market prices. This econometric technique has been applied to a number of countries: Pakistan (Nishat, Shaneen, 2004), Malaysia (Ibrahim, 2003), the United States (Fama, Schwert, 1977), India (Darat, Mukherjee, 1987), Japan (Mukherjee, Naka, 1995), Canada (Darrat, 1990), etc. All scientific studies show the relationship between stock market prices and macroeconomic variables. For example, Nishat and Shaneen (2004) have detected a significant opposite relationship between the Karachi stock market index and the consumer price index and a positive relation between the industrial production index and the stock market index; a positive influence of the industrial production index has been proved for a number of European countries as well (Siliverstovs, Duong, 2005; Snieska, 2008) and so no. This technique has not been applied for Lithuania so far. Therefore, the objective of this paper is to define the short-run relationship between Lithuanian stock market prices and macroeconomic variables by employing the Impulse response function. A set of macroeconomic variables will be offered for similar studies in the future. The object of the article is the relationship between macroeconomic variables and stock market prices. Research methods are the logical analysis and synthesis of scientific literature, the comparison and generalization method, the statistical grouping method. Scientific novelty: though scientific literature has been seemingly enriched by theoretical and practical studies analysing the relationship between macroeconomic variables and stock market prices in different countries there is few similar studies in Lithuanian (Norvaišienė, Stankevičienė, Krušinskas, 2008; Ginevičius, Podvezko, 2009; Melnikas, 2008); moreover, no scientists have investigated the short-run relationship between macroeconomic variables and stock market prices in Lithuania applying the Impulse response function. Classification of macroeconomic variables according to the business cycle In the most general sense, macroeconomic variables are treated as statistical indicators that reflect an overall economic situation of the country during some period of time (Rogers, 1998) or as regular data issued by state institutions and indicating the welfare of a country (Mohr, 1998; Darnay, 1998; Ciegis, Ramanauskiene, Startiene, 2009; Kumpikaite, Ciarniene, 2008). The first attempts to calculate macroeconomic variables could be dated as back as the First World War when warring countries wanted to measure the strength of their enemies. Nowadays a large spectrum of macroeconomic variables is regularly published to indicate various tendencies in both private and public life. According to the business cycle, it is possible to distinguish the following groups of macroeconomic variables (Rogers, 1998): Procyclic macroeconomic variables are positively correlated with the overall state of the economy, i.e. they tend to increase when the overall economy is growing. Gross domestic product is considered to be a classical example of procyclic macroeconomic variables. Countercyclic macroeconomic variables, on the contrary, move in the opposite direction of the overall economic cycle: rising when the economy is weakening, and falling when the economy is strengthening. The unemployment rate gets larger when the economy gets worse that s why it is attributed to this group. Acyclic macroeconomic variables have no relation to the health of the economy and are generally of little use. The National Bureau of Economic Research offers another classification according to the timing how macroeconomic variables change relative to the changes of the economy as a whole (Shiskin, Moore, 1968): Leading Lagging Macroeconomic variables GDP plus coincident macroeconomic variables Lagged macroeconomic variables Leading macroeconomic variables Time Figure 1. Leading, lagged and coincident macroeconomic variables

have detected a significant opposite relationship between the Karachi stock market index and the consumer price index and a positive relation between the")

3 Leading macroeconomic variables are indicators which change before the economy changes. Stock market returns are considered as a leading indicator, as they usually begin to decline before the economy declines and they improve before the economy begins to pull out of a recession. Lagged macroeconomic variables are ones that do not change direction until a few quarters after the economy does. The unemployment rate is a lagged economic indicator as unemployment tends to increase for 2 or 3 quarters after the economy starts to improve. Coincident macroeconomic variables are ones that simply move at the same time the economy does and, for example, the gross domestic product is attributed to this group of indicators. Figure 1 depicts how leading, lagged and coincident indicators move compared to gross domestic product throughout time. Leading macroeconomic variables dominate in scientific literature since their fluctuations set signals and help predict what the economy will be like in the future (Chen, 2009; Dua, 2004). It is relevant to state that a separate macroeconomic variable is doomed to subjectivity, thus a set of macroeconomic variables is required for a more precision picture on economic developments. Selection of macroeconomic variables by estimating their relationship with stock market prices Different economic theories such as Classical, Keynesian, Monetary and others allocate unequal power to various macroeconomic variables (Dritsaki, Adamopoulos, 2005). Therefore, it is an uneasy task to select proper macroeconomic variables that could be most valuable in tracing the relationship between macroeconomic variables and stock market prices. The current issue has been investigated for a long time (Miller, Modigliani, 1961). As Chen, Roll and Ross (1986) state, selection of relevant and proper macroeconomic factors requires much efforts and it would be expedient to consider theoretical and empirical literature in this field of study before undertaking such a decision (Humpe, Macmillan, 2007). Dritsaki (2005) notices the most important thing in selecting macroeconomic variables is to preserve that those variables would objectively reflect not only general situation in the country s economy but also financial status of the country. In that respect, many scientists believe that financial resources are closely related to economic output of the country which is measured either by gross domestic product or industrial production volumes (Fama, 1981; Chen, Roll, Ross, 1986; Cheung, Ng, 1998; Binswanger, 2000; Lakstutiene, 2008). Some authors prefer industrial production index to gross domestic product since it is calculated every month (not every quarter) and, thus, more often reflects economic situation (Padhan, 2007). Moreover, industrial production index becomes vital if industrial sector prevails in the country under analysis (Agrawalla, Tuteja, 2007). As DeFina (1991) points out, inflation negatively influences companies due to speedily increasing costs. Seeking for the relationship between stock market and macroeconomic variables inflation is most often measured by consumer price index (Atmadja, 2005; Dritsaki, 2005; Laopodis, 2007), though some scientists also include other inflation reflecting indices, for example, producer price index (Teresienė, Aarma, Dubauskas, 2008). Another popular macroeconomic variable is interest rates in such type of studies. Some authors include only short-term interest rates (Dritsaki, 2005; Atmadja, 2005), others select only long-term interest rates (Siliverstovs, Doung, 2005) while the third group of scientists analyzes both short-term and long-term interest rates (Chen, Roll, Ross, 1986; Mukherjee, Naka, 1995). As a rule, short-term interest rates are influenced by business cycles and monetary policies and long-term interest rates are more related to long-term economic perspectives of the country (Humpe, Macmillan, 2007). Money supply stands for another macroeconomic indicator which many scientists embrace when they seek for the relationship between stock market prices and macroeconomic forces (Urich, Wachtel, 1981; Chaudhuri, Smiles, 2004). Tan and Baharumshah (1999) argue that it is more expedient to analyze the narrow money M1 while others operate with broadly-defined money supply M2 (Tursoy, Gunsel, Rjoub, 2008). There is another group of scientists who avoid this scientific discussion and enrol both concepts of money supply in their empirical investigations. Stock prices can be influenced by exchange rate fluctuations as the currency devaluation may lead to inflationary processes in the country what reduces consumer expenditure and profits earned by local companies. Analysis of the exchange rate fluctuations can be found in a number of empirical studies (Adam, Tweneboah, 2008; Ahmed, 2008; Ibrahim, 2003; Kwon, Shin, 1999). As economists most often speak about gross domestic product, inflation and unemployment analysing various economic phenomena, unemployment should be incorporated into such studies as well (Tursoy, Gunsel, Rjoub, 2008). The aforementioned variables, i.e., gross domestic product, industrial production, inflation, interest rates, money supply, and unemployment rate, reflect domestic economic processes and the exchange rate fluctuations are more related with the international economic context. Data and methodology The macroeconomic variables used in this paper are as follows: seasonally adjusted gross domestic product (GDP) at previous year prices; harmonised consumer price index (HCPI) as compared to 2005, the narrow money supply (M1), i.e. currency in circulation and overnight deposits in Litas and foreign currencies; unemployment rate (UR) reflecting tendencies in the labour market; three months Vilnius interbank offered rate (VILIBOR3M) which is based on the quotes of not less than 5 local commercial banks, designated by the Bank of Lithuania, which are most active in Lithuanian money market; and the exchange rate of Litas against the US dollar (USD_LTL). The data are monthly and extend from the January of 2000 to the June of 2009.

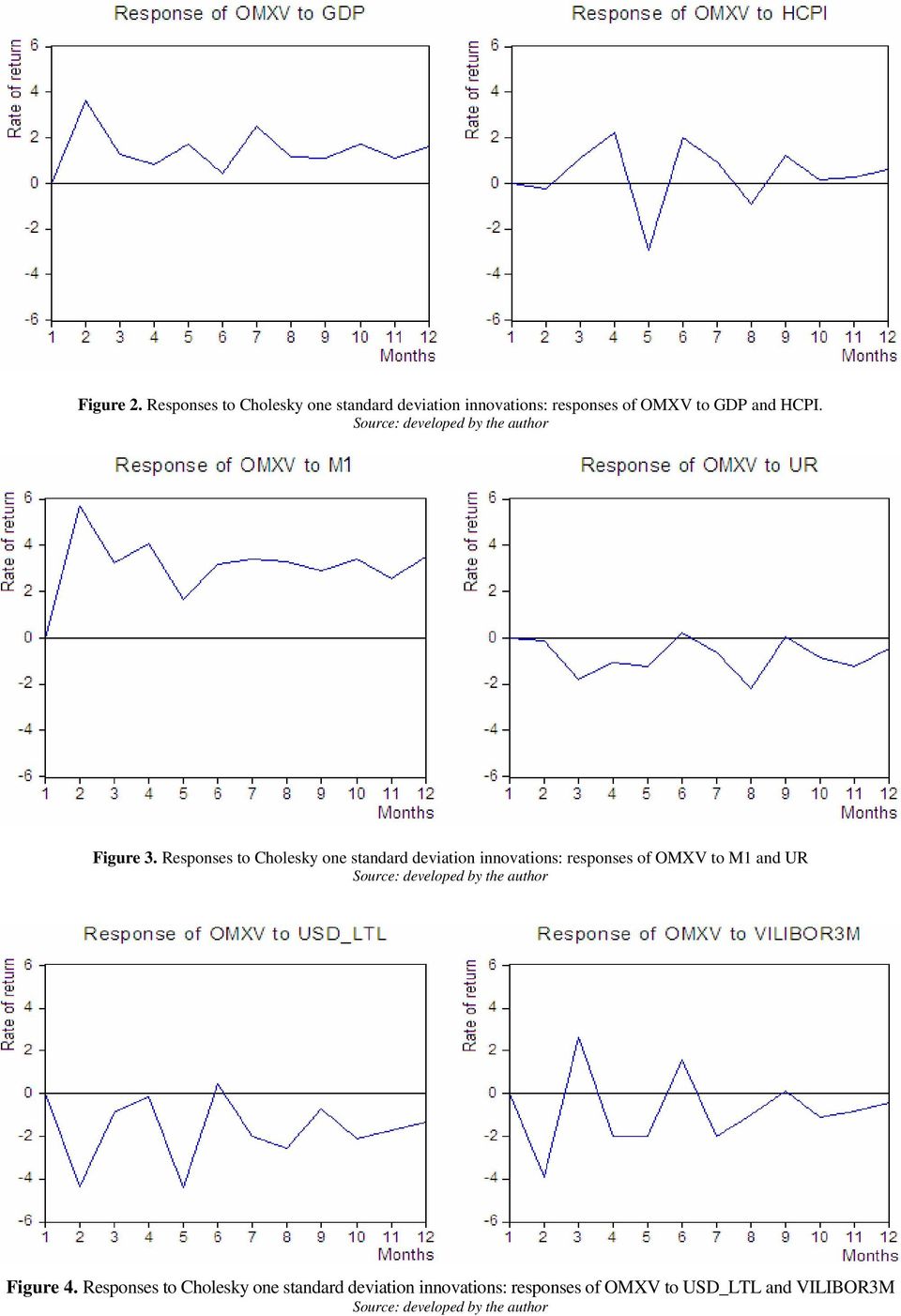

4 The stock price movements are represented by the main Lithuanian stock market index the OMX Vilnius (OMXV) index. A value of the index is acquired on the last business day of the month. The OMXV index indicates stocks which are quoted in the securities exchange of Vilnius. Most Lithuanian companies TEO LT, City Service, Klaipedos Nafta, Ukio bankas and others are included in the index, thus, it may be assumed that dynamics of OMXV index reflects the overall country s economic situation quite reasonably. Time series analysis must be based on stationary data for drawing useful inferences. A data series is said to be stationary if its mean and variance are constant over time and the value of covariance between two time periods depends only on the distance or lag between the two time periods and not on the actual time at which the covariance is computed. The correlation between a series and its lagged values are assumed to depend only on the length of the lag and not when the series started. This property is known as stationarity and any series obeying this is called a stationary time series. The unit root test has been applied to check whether a series is stationary or not. Stationarity condition has been tested using Augmented Dickey Fuller (ADF) test. Compared to Dickey Fuller (DF) test, the ADF approach controls higher-order correlation by adding lagged difference terms of the dependent variable to the regression. The impulse response function, as an econometric technique, has been employed to investigate the short-run (up to one year) impact caused by the vector auto regression model when it received some impulses. The impulse response function describes the response to the error by the endogenous variables. It depicts the current and future responses of endogenous variables to one standard deviation on the disturbing term. Research results on the short-run relationship between stock market prices and macroeconomic variables in Lithuania Table 1 reports the ADF test statistics for the presence of unit root of the level, first and second differences over the sample period. For the level series, the results show the existence of unit root for all variables as it fails to reject the null hypothesis of nonstationarity with an exception of money supply. After the first difference, HCPI, UR, USD_LTL, and OMXV t-statistic results are higher than the critical values, however GDP, M1, and VILIBOR3M are still nonstationary. After second difference, the ADF test of unit root indicates that all variables are stationary and would not cause spurious regression outcomes. Unit root tests on level, first and second differences (critical values at 5% level are in the brackets) Variable ADF statistics Level First differences Second differences GDP -2, (-2,888157) -0, (-2,888157) -7, (-2,888157) HCPI 2, (-2,887425) -7, (-2,887425) -8, (-2,888669) M1-3, (-2,890327) 0, (-2,890327) -7, (-2,890327) UR -1, (-2,887425) -2, (-2,887425) -6, (-2,889753) VILIBOR3M -0, (-2,890327) -2, (-2,890327) -7, (-2,890327) USD_LTL -1, (-2,887190) (-2,887425) -9, (-2,888411) OMXV -0, ( ) -8, (-2,887425) -12,20385 (-2,887909) Table 1 In Figure 2 it is possible to observe that GDP has an immediate positive effect on OMXV index. The effect peaks during the second month and remains positive throughout all twelve months. The result is similar to other studies (Ibrahim, 2003; Somoye, Akintoye, Oseni, 2009). In the meantime, the response of OMXV to HCPI is not as immediate as to GDP and the positive and negative effects interchange each other. The effect continues to be positive only after the ninth months. This support the Rapach s (2002) claim that real stock prices positively respond to a permanent inflation shock in the long-run. Figure 3 outlines the response of OMXV to M1 which is similar to that of GDP even the peak of the effect remains the same, i.e. during the second months. The difference is that the positive effect of M1 is stronger compared to the influence of GDP innovations. The positive influence of money supply has been detected in other studies as well (Dumitrescu, Horobet, 2009). The unemployment rate negatively influences OMXV index most of the time. Therefore, an increase in the unemployment rate causes a decrease of OMXV index and the effect peak is reached during the eighth month. The result is similar to Arestis, Baddeley, and Sawyer (2007) who conducted their analysis in the case of nine euro area countries. Figure 4 discloses that the negative impact of the shock in the exchange rate is similar to the effect of unemployment rate innovations. The difference, however, is that the impact is immediate and it peaks not during the eighth month, as in the case of unemployment, but during the second and fifth months. The result of the negative relationship between the exchange rate and stock prices supports empirical finding of Aydemir and Demirhan (2009) as well as Akin and Basti (2008) for the Turkish market. The influence of VILIBOR3M is more often negative than positive. Similarly, Alam and Uddin (2009) have also proved the existence of a significant negative relationship in fifteen developed and developing countries: Australia, Bangladesh, Canada, Chile, Colombia, Germany, Italy, Jamaica, Japan, Malaysia, Mexico, Philippine, South Africa, Spain, and Venezuela.

5 Figure 2. Responses to Cholesky one standard deviation innovations: responses of OMXV to GDP and HCPI. Figure 3. Responses to Cholesky one standard deviation innovations: responses of OMXV to M1 and UR Figure 4. Responses to Cholesky one standard deviation innovations: responses of OMXV to USD_LTL and VILIBOR3M

6 The above evidence clearly indicates the existence of the short-run relationship between stock market prices and macroeconomic variables in Lithuania. Gross domestic product and money supply are the most influential positive determinants of the OMXV index while unemployment rate, exchange rate, and short-term interest rates mostly have a negative influence on stock prices quoted in the stock market of Lithuania. Conclusions The analysis carried out in this paper reveals that scholars and practitioners offer different classifications of macroeconomic variables. No matter what the classification is, macroeconomic variables are relevant indicators of movements in equity markets. This issue has been widely debated across a variety of markets and time horizons. Many studies undertake different macroeconomic variables when searching for the relationship between macroeconomic factors and stock market prices. A set of six most relevant macroeconomic variables has been selected for the investigation in Lithuania, i.e. gross domestic product, inflation, interest rates, money supply, exchange rate, and unemployment rate. As OMX Vilnius index reflects stock price fluctuations of principal Lithuanian companies and, consequently, indicates the overall country s economic situation it has been chosen as a representative for stock market price fluctuations. The paper reveals the selected variables verify to be proper as significant relationships have been perceived. As a rule, time series are non-stationary, thus Augumented Dickey Fuller test has been employed to test if the data is stationary or not. The selected time series have become stationary only after second difference. The impulse response function has been selected to analyze the short-run relationship between macroeconomic variables and stock market prices as many scientists employ this econometric technique. The applied technique confirms similar results of other studies, i.e. gross domestic product and money supply have a strong positive effect on stock market prices in the short run while unemployment rate, exchange rate, short-term interest rates cause opposite movements for stock prices. This undoubtedly confirms the existence of the short-term relationship between stock market returns and macroeconomic variables in Lithuania. References 1. Adam, A. M., Tweneboah, G. (2008). Macroeconomic factors and stock market movement: evidence from Ghana. Social Science Research Network. Retrieved from 2. Agrawalla, R. K., Tuteja, S.K. (2007). Causality between stock market development and economic growth: a case study of India. Journal of Management Research, 7(3), Ahmed, S. (2008). Aggregate economic variables and stock markets in India. International Research Journal of Finance and Economics, 14, Akin, A., & Basti, E. (2008). An assessment of trading behaviour and performance of foreign investors in Istanbul stock exchange. Transformations in Business & Economics, 7(3), Supplement C, Alam, M., & Uddin, G. S. (2009). Relationship between interest rate and stock price: empirical evidence from developed and developing countries. International Journal of Business and Management, 4(3), Arabian, G., Afshar, T., Ameli, A. (2008). The impact of oil price shocks and stock market on US real GDP growth. IABR&TLC Conference Proceedings. Retrieved from com/programs/puerto_rico_2008/article%20177%20 Arabian,%20Afshar,%20Anjela.pdf 7. Arestis, P., Baddeley, M., Sawyer, M. (2007). The relationship between capital stock, unemployment and wages in nine EMU countries. Bulletin of Economic Research, 59(2), Retrieved from com/abstract= Atmadja, A. S. (2005). The Granger causality tests for the five ASEAN countries stock markets and macroeconomic variables during and post the 1997 Asian financial crisis. Jurnal Manajemen dan Kewirausahaan, 7(1), Aydemir, O., Demirhan, E. (2009). The relationship between stock prices and exchange rates: evidences from Turkey. International Research Journal of Finance and Economics, 23, Binswanger, M. (2000). Stock market booms and real economic activity: is this time different? International Review of Economics & Finance, 2000, 9(4), Chaudhuri, K., Smile, S. (2004). Stock market and aggregate economic activity: evidence from Australia. Applied Financial Economics, 14, Chen, S. S. (2009). Predicting the bear stock market: macroeconomic variables as leading indicators. Journal of Banking & Finance, 33(2), Chen N. F., Roll R., Ross S. A. (1986). Economic forces and the stock market. Journal of Business, 1986, 59(3), Cheung Y.W., Ng, L.K. (1998). International evidence on the stock market and aggregate economic activity. Journal of Empirical Finance, 5, Ciegis, R., Ramanauskiene, J., & Startiene, G. (2009). Theoretical Reasoning of the Use of Indicators and Indices for Sustainable Development Assessment. Inzinerine Ekonomika-Engineering Economics(3), Comincioli, B. (1995). The stock market as a leading indicator: an application of Granger causality. Honors Projects, Paper 54. Retrieved from mons.iwu.edu/econ_honproj/54/ 17. Darrat A. F. (1990). Stock returns, money and fiscal policy. Journal of Financial and Quantitative Analysis, (25)3,

7 18. Darat, A. F., Mukherjee, T. K. (1987). The behavior of the stock market in a developing economy. Economics Letters, 22, Darnay, A.J. (1998). Economic indicators handbook: time series, conversions, documentation. Detroit: Gale. 20. Dritsaki, C., Adamopoulos, A.A. (2005). Causal relationship and macroeconomic activity: empirical results from European Union. American Journal of Applied Science, 2(2), Dritsaki, M. (2005). Linkage between stock market and macroeconomic fundamentals: case study of Athens stock exchange. Journal of Financial Management and Analysis, 18(1), Dua, P. (2004). Business cycles and economic growth: an analysis using leading indicators. Oxford University Press. 23. Dumitrescu, S., Horobet, A. (2009). On the causal relationship between stock prices and exchange rates: evidences from Romania. Social Science Research Network. Retrieved from Engle, R. F., Granger, C. W. J. (1987). Cointegration and error correction: representation, estimation, and testing. Econometrica, 55, Fama, E. (1981). Stock returns, real activity, inflation, and money. American Economic Review, 71, Fama, E. F., Schwert, G. W. (1977). Asset returns and inflation. Journal of Financial Economics, 5, Gallegati, M. (2005). Stock market returns and economic activity: evidence from wavelet analysis. Working Papers , EconWPA. Retrieved from Ginevicius, R., Podvezko, V. (2009). Evaluating the changes in economic and social development of Lithuanian countries by multiple criteria methods. Technological and Economic Development of Economy, 15(3), Gunes, S. (2007). Functional income distribution in Turkey: a cointegration and VECM analysis. Journal of Economic and Social Research, 9(2), Hassan, A. H. (2003). Financial integration of stock markets in the Gulf: a multivariate cointegration analysis. International Journal of Business, 8(3). Retrieved from: Humpe, A., Macmillan, P. (2007). Can macroeconomic variables explain long term stock market movements? A comparison of the US and Japan. CDMA Working Paper No. 07/ Hussain, F., Mahmood, T. (2001). The stock market and the economy of Pakistan. The Pakistan Development Review, 40(2), Ibrahim, M. H. (1999). Macroeconomic variables and stock prices in Malaysia: an empirical analysis. Asian Economic Journal, 13, Ibrahim, M. H., Aziz, H. (2003). Macroeconomic variables and the Malaysian equity market: a view through rolling subsamples. Journal of Economic Studies, 30(1), Kandir, S. Y. (2008). Macroeconomic variables, firm characteristics and stock returns: evidence from Turkey. International Research Journal of Finance and Economics, (16), Kumpikaite, V., & Ciarniene, R. (2008). New training technologies and their use in training and development activities: Survey evidence from Lithuania. Journal of Business Economics and Management, 9(2), Kurihara, Y., Nezu, E. (2006). Recent stock price relationships between Japanese and US stock markets. Studies in Economics and Finance, 23(3), Kwon C. S., Shin T. S. (1999). Cointegration and causality between macroeconomic variables and stock market returns. Global Finance Journal, 10(1), Lakstutiene, A. (2008). Correlation of the indicators of the financial system and gross domestic product in European Union countries. Inzinerine Ekonomika- Engineering Economics(3), Laopodis, N. T. (2007). Fiscal policy, monetary policy, and the stock market. Annual International Conference on Macroeconomic Analysis and International Finance. Retrieved from a.org/barcelona/papers/ StocknFiscalPolicy.pdf 41. Lastrapes, W. D., Koray, F. (1990). International transmission of aggregate shocks under fixed and flexible exchange rate regimes: United Kingdom, France and Germany, 1959 to Journal of International Money and Finance, 9, Lee, B. S. (1992). Causal relations among stock returns, interest rates, real activity and inflation. Journal of Finance, 1992, 47(4), Melnikas, B. (2008). Integral spaces in the European Union: possible trends of the social, economic and technological integration in the Baltic region. Journal of Business Economics and Management, 9(1), Miller, M., Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. Journal of Business, 34(4), Mohr, P. (1998). Economic Indicators. Pretoria: Unisa Press. 46. Mukherjee T. K., & Naka A. (1995). Dynamic relations between macroeconomic variables and the Japanese stock market: an application of a vector error correction model. Journal of Financial Research, 18(2), Naceur, S.B., Ghazouani, S., Omran, M. (2007). The determinants of stock market development in the Middle-Eastern and North African region. Managerial Finance, 33(7), Nasseh, A., Strauss, J. (2000). Stock prices and domestic and international macroeconomic activity: a cointegration approach. Quarterly Review of Economics and Finance, 40(2), Nishat M., Shaheen R. (2004). Macroeconomic factors and Pakistani equity market. The Pakistan Development Review, 43(4), Norvaisiene, R., Stankeviciene, J., Krusinskas, R. (2008). The impact of loan capital on the Baltic listed

, 38-47. 22. Dua, P. (2004).")

8 companies investment and growth. Inzinerine Ekonomika-Engineering Economics(2), Padhan, P.C. (2007). The nexus between stock market and economic activity: an empirical analysis for India. International Journal of Social Economics, 34(10), Rapach, D. E. (2002). The long-run relationship between inflation and real stock prices. Journal of Macroeconomics, 24(3), Rogers, R. M. (1998). Handbook of Key Economic Indicators. New York: McGraw-Hill. 54. Schwert, W. G. (1990). Stock returns and real activity: a century of evidence. Journal of Finance, 45, Shiskin, J., Moore, G. H. (1968). Composite Indexes of Leading, Coincident and Lagging Indicators, Supplement to NBER Report One. Retrieved from Siliverstovs, B., Duong, M. H. (2006). On the role of stock market for real economic activity: evidence for Europe. DIW Berlin Discussion Paper 559, German Institute for Economic Research. Retrieved from dp599.pdf 57. Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48, Snieska, V. (2008). Research into international competitiveness in Inzinerine Ekonomika- Engineering Economics(4), Somoye, R.O.C., Akintoye, I.R., Oseni, J.E. (2009). Determinants of equity prices in the stock markets. International Research Journal of Finance and Economics, (30), Stavarek, D. (2004). Linkages between stock prices and exchange rates in the EU and the United States. Silesian University in Opava. 61. Tan, H. B., Baharumshah, A. Z. (1999). Dynamic causal chain of money, output, interest rate and prices in Malaysia: evidence based on vector-error corection modeling analysis. International Economic Journal, 1999, 13(1), Teresienė, D., Aarma, A., & Dubauskas, G. (2008). Relationship between stock market and macroeconomic volatility. Transformations in Business & Economics, 7(2), Supplement B, Tursoy, T., Gunsel, N., Rjoub, H. (2008). Macroeconomic factors, the APT and the Istanbul stock market. International Research Journal of Finance and Economics, (22), Urich, T., Wachtel, P. (1981). Market response to the weekly money supply announcements in the 1970s. Journal of Finance, 36, Valdés, R. O. (2000). Optimal fiscal strategy for oil exporting countries. International Monetary Fund. Donatas Pilinkus Trumpalaikis sąryšis tarp akcijų kainų ir makroekonominių rodiklių Lietuvoje: reakcijos į impulsą funkcijos pritaikymas Santrauka Mokslinėje literatūroje vis labiau analizuojamas sąryšis tarp makroekonominių rodiklių ir akcijų kainų. Juo ypač susidomėta paskutinius du dešimtmečius. Daugelyje mokslinių šaltinių teigiama, jog egzistuoja sąryšis tarp akcijų kainų ir pagrindinių šalies makroekonominių rodiklių. Taigi galima daryti išvadą, jog makroekonominių rodiklių pokyčiai gali daryti įtaką investuotojų sprendimams. Dėl to dar labiau susidomėta šia tematika. Tyrinėtojai taiko skirtingus ekonometrinius tyrimo metodus, norėdami aptarti sąryšį tarp makroekonominių rodiklių ir akcijų kainų: arbitražinės kainodaros teoriją (Fama, 1981; Schwert, 1990; Tursoy, Gunsel, Rjoub, 2008), reakcijos į impulsą funkciją (Sims, 1980; Nishat, Shaheen, 2004; Adam Tweneboah, 2008), paklaidų variacijos skaidymo analizę (Lastrapes, Koray, 1990; Laopodis, 2007), vektorinių paklaidų korekcijos modelį (Engle, Granger, 1987; Kwon, Shin, 1999); kointegracijos analizę (Nasseh, Strauss, 2000; Dritsaki, Adamopoulos, 2005), Grangerio priežastingumo testus (Lee, 1992; Hassan, 2003; Dritsaki, 2005) ir kt. Tuo pačiu metu skirtingi autoriai renkasi skirtingus makroekonominius rodiklius ir ieško sąryšio tarp jų ir akcijų kainų. Kai kurie autoriai yra linkę taikyti tik vieną ar du makroekonominius rodiklius. Pavyzdžiui, Comincioli (1995) pasirenka tik bendrąjį vidaus produktą, Gallegati (2005) tik pramonės produkcijos indeksą, Arabian, Afshar, Anjela (2008) naudoja bendrąjį vidaus produktą ir naftos kainas, kiti daugiau nei dešimt makroekonominių rodiklių (Tursoy, Gunsel, Rjoub, 2008). Būtina paminėti ir tai, kad skirtingose ekonomikos teorijose, pavyzdžiui, klasikinėje, keinsistinėje, monetarisinėje ir kitose atskiri makroekonominiai rodikliai nevienodai reikšmingi. Dėl šios priežasties yra labai sunku parinkti reikšmingus makroekonominius rodiklius. Ši mokslinė problema yra keliama jau seniai (Miller, Modigliani, 1961). Chen, Roll ir Ross (1986) teigia, kad reikšmingiems makroekonominiams rodikliams parinkti reikalinga daug pastangų, todėl prieš galutinai pasirenkant yra tikslinga išsamiai išanalizuoti tiek teorinę literatūrą, tiek ir empirinius tyrimus (Humpe, Macmillan, 2007). Panašiai skirtingi autoriai renkasi nevienodus laiko periodus, t. y. kasdienius (Kurihara, Nezu, 2006), mėnesinius (Kandir, 2008; Stavarek, 2004), ketvirtinius (Ahmed, 2008; Comincioli, 1995) ar metinius (Hussain, Mahmood, 2001; Naceur, Ghazouani, Omran, 2007) duomenis. Tie mokslininkai, kurie savo tyrimuose taiko reakcijos į impulsą funkciją, analizuoja trumpalaikį sąryšį tarp makroekonominių rodiklių ir akcijų kainų. Ši ekonometrinė tyrimo metodika buvo pritaikyta daugeliui šalių: Pakistanui (Nishat, Shaneen, 2004), Malaizijai (Ibrahim, 2003), Jungtinei Karalystei (Fama, Schwert, 1997), Indijai (Darat, Mukherjee, 1987), Japonijai (Mukherjee, Naka, 1995), Kanadai (Darrat, 1990) ir kt. Visos studijos rodo, kad egzistuoja sąryšis tarp makroekonominių rodiklių ir akcijų kainų. Pavyzdžiui, Nishat ir Shaneen (2004) aptiko reikšmingą atvirkštinį sąryšį tarp Karačio akcijų rinkos indekso ir vartojimo prekių kainų indekso bei tiesioginį sąryšį tarp pramonės produkcijos indekso ir akcijų kainų indekso. Tiesioginis pramonės produkcijos indekso poveikis buvo patvirtintas ir daugelyje Europos valstybių (Siliverstovs, Doung, 2005) ir kt. Kad ir kaip būtų, šis tyrimo metodas dar nebuvo pritaikytas Lietuvai. Būtent ši priežastis ir nulėmė darbo tikslą, t. y. siekį apibrėžti trumpalaikį sąryšį tarp Lietuvos akcijų rinkoje kotiruojamų įmonių kainų ir šalies makroekonominių rodiklių, taikant reakcijos į impulsą funkciją. Šiam tikslui įgyvendinti buvo sudarytas makroekonominių rodiklių rinkinys, kurį galima naudoti ir kituose panašaus pobūdžio studijose. Darbo objektas tai sąryšis tarp makroekonominių rodiklių ir akcijų kainų. Tyrimo metodai yra mokslinės literatūros loginė analizė ir sintezė, lyginamoji analizė ir apibendrinimo metodas, statistinio grupavimo metodas. Temos aktualumas: nors įvairiose šalyse yra gana daug teorinių ir praktinių darbų nagrinėjama tematika, tačiau panašaus pobūdžio studijų Lietuvoje beveik nėra. Be to, nei vienas mokslininkas dar nenagrinėjo trumpalaikio sąryšio tarp makroekonominių rodiklių ir akcijų kainų Lietuvoje, taikant reakcijos į impulsą funkciją. Darbo tikslas yra įgyvendinamas, naudojant Lietuvos akcijų rinkos indeksą OMXV, kuris atspindi daugumos Lietuvos akcijų biržoje kotiruojamų įmonių akcijų kainų svyravimus bei pagrindinius ir dažniausiai panašaus pobūdžio tyrimuose naudojamus makroekonominius rodiklius: bendrąjį vidaus produktą, infliaciją, trumpalaikę palūkanų normą, pinigų pasiūlą M1, valiutos kurso svyravimus, nedarbo lygį. Tai

. Composite Indexes of Leading, Coincident and Lagging Indicators, 1948-67. Supplement to NBER Report One. Retrieved from http://www.nber.org/chapters/c10568 56.")

9 nuo 2000-ųjų metų sausio mėn. iki 2009-ųjų metų birželio mėn. duomenys. Bendrasis vidaus produktas arba pramonės produkcijos apimtis yra svarbūs tokio pobūdžio tyrimams, nes jie atspindi šalies ekonominį augimą (Fama, 1981; Chen, Roll, Ross, 1986; Cheung, Ng, 1998; Binswanger, 2000). DeFina (1991) teigia, kad infliacijos didėjimas daro neigiamą įtaką akcijų kainoms. Infliacija dažniausiai atspindima vartojimo prekių kainų indeksu (Atmadja, 2005; Dritsaki, 2005; Laopodis, 2007), nors kai kurie tyrinėtojai naudoja ir kitus infliaciją atspindinčius indeksus, pavyzdžiui, gamintojų kainų indeksą. Šiame darbe infliaciją atspindi vartojimo prekių kainų indeksas. Dalis mokslininkų renkasi trumpalaikę palūkanų normą (Dritsaki, 2005; Atmadja, 2005), kiti ilgalaikę palūkanų normą (Siliverstovs, Doung, 2005), nors yra ir tokių tyrinėtojų, kurie savo studijose naudoja tiek trumpalaikę, tiek ilgalaikę palūkanų normas kartu (Che, Roll, Ross, 1986; Mukherjee, Naka, 1995). Pinigų pasiūla yra dar vienas svarbus makroekonominis rodiklis (Urich, Wachtel, 1981; Chaudhuri, Smiles, 2004), ieškant sąryšio su akcijų kainomis. Vieni autoriai savo tyrimuose naudoja pinigų pasiūlą siaurąja prasme (Tan, Baharumshah, 1999), kiti platesne prasme M2 (Tursoy, Gunsel, Rjoub, 2008). Akcijų kainų svyravimams gali daryti įtaką ir šalies valiutos kurso svyravimai, todėl daugelis mokslininkų šį rodiklį naudoja empirinėje analizėje (Adam, Tweneboah, 2008; Ahmed, 2008; Ibrahim, 2003; Kwon, Shin, 1999). Kadangi nedarbo lygis yra vienas iš svarbiausių šalies ekonominę padėtį įvertinančių makroekonominių rodiklių, jis taip pat yra naudojamas tiriant sąryšį tarp makroekonominių rodiklių ir akcijų kainų (Tursoy, Gunsel, Rjoub, 2008). Tai dažniausiai mokslinėje literatūroje naudojami makroekonominiai rodikliai, kurie geriausiai atspindi šalies makroekonominius procesus. Tai ir lėmė šių makroekonominių rodiklių pasirinkimą. Kadangi tiriant reakcijos į impulsą funkciją duomenys turi būti stacionarūs, siekiant išvengti netikrų ir iškraipytų sąryšių, todėl buvo pasirinktas vienetinės šaknies testas, kuriuo ir buvo tikrinamas duomenų stacionarumas. Visi duomenys tapo stacionariais diferencijavus antru laipsniu. Atlikti empiriniai tyrimai rodo, kad bendrasis vidaus produktas greitai tiesiogiai veikia OMXV indeksą. Šis poveikis yra stipriausias po dviejų mėnesių, vėliau jis silpnėja, bet išlieka tiesioginis per visą dvylikos mėnesių periodą. Panašius rezultatus yra gavę ir kiti mokslininkai (Ibrahim, 2003; Somoye, Akintoye, Oseni, 2009). Nagrinėjant OMXV indekso ir vartojimo prekių kainų indekso sąryši, galima pastebėti, kad kainų indeksas neturi tokio staigaus poveikio akcijų kainoms kaip bendrasis vidaus produktas ir šis poveikis nėra pastovus. Nuo devinto mėnesio galima įžvelgti tiesioginį sąryšį tarp Lietuvos akcijų kainų indekso ir vartojimo prekių kainų indekso (tai patvirtina Rapach (2002) teiginius), nes tikėtina, jog akcijų kainos turi tiesioginį sąryšį su infliacija ilguoju laikotarpiu. Pinigų pasiūla M1 daro įtaką OMXV indeksui panašiai kaip ir bendrasis vidaus produktas, netgi maksimalus poveikis yra pasiekiamas tuo pačiu metu, t. y. po dviejų mėnesių. Tiesioginė pinigų pasiūlos įtaka yra akcentuojama ir kituose darbuose (Dumitrescu, Horobet, 2009). Nedarbo lygis didžiąją laiko dalį per metus daro neigiamą įtaką OMXV indeksui, t. y. dėl nedarbo lygio augimo mažėja OMXV indeksas, ir šio poveikio didžiausias efektas yra pasiekiamas per aštuntą mėnesį. Panašius rezultatus yra gavę Arestis, Baddeley ir Sawyer (2007), kurie atliko savo tyrimą su devyniomis euro zonos valstybėmis. Valiutos kurso svyravimai, kaip ir nedarbo lygis, daro neigiamą poveikį OMXV indeksui. Tokius pačius rezultatus gavo Aydemir ir Demirhan (2009) Turkijos rinkoje. Trumpalaikės palūkanų normos poveikis akcijų kainoms yra daugiau atvirkštinis nei tiesioginis. Alam ir Uddin (2009) taip pat nustatė, kad reikšmingas atvirkštinis ryšys egzistuoja penkiolikoje išsivysčiusių ir besivystančių pasaulio šalių. Atlikti tyrimo rezultatai rodo, kad Lietuvoje neabejotinai egzistuoja trumpalaikis sąryšis tarp akcijų kainų ir makroekonominių rodiklių. Bendrasis vidaus produktas ir pinigų pasiūla turi didžiausią tiesioginį sąryšį su akcijų kainomis, o nedarbo lygio, valiutos kurso svyravimų ir trumpalaikės palūkanų normos poveikis dažniausiai yra atvirkštinis akcijų kainoms Lietuvos rinkoje. Raktažodžiai: makroekonominiai rodikliai, akcijų kainos, trumpalaikis sąryšis, reakcijos į impulsą funkcija, Lietuva. The article has been reviewed. Received in September, 2009; accepted in December, 2009.

, nors kai kurie tyrinėtojai naudoja ir kitus infliaciją atspindinčius indeksus,")

Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

International Journal of Business and Social Science Vol. 6, No. 4; April 2015 Dynamic Relationship between Interest Rate and Stock Price: Empirical Evidence from Colombo Stock Exchange AAMD Amarasinghe

The relationships between stock market capitalization rate and interest rate: Evidence from Jordan

Peer-reviewed & Open access journal ISSN: 1804-1205 www.pieb.cz BEH - Business and Economic Horizons Volume 2 Issue 2 July 2010 pp. 60-66 The relationships between stock market capitalization rate and

Peer-reviewed & Open access journal ISSN: 1804-1205 www.pieb.cz BEH - Business and Economic Horizons Volume 2 Issue 2 July 2010 pp. 60-66 The relationships between stock market capitalization rate and

The effect of Macroeconomic Determinants on the Performance of the Indian Stock Market

The effect of Macroeconomic Determinants on the Performance of the Indian Stock Market 1 Samveg Patel Abstract The study investigates the effect of macroeconomic determinants on the performance of the

The effect of Macroeconomic Determinants on the Performance of the Indian Stock Market 1 Samveg Patel Abstract The study investigates the effect of macroeconomic determinants on the performance of the

ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate?

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

An Empirical Investigation of the Causal Relationship among Monetary Variables and Equity Market Returns

The Lahore Journal of Economics 14 : 1 (Summer 2009): pp. 115-137 An Empirical Investigation of the Causal Relationship among Monetary Variables and Equity Market Returns Arshad Hasan * and M. Tariq Javed

The Lahore Journal of Economics 14 : 1 (Summer 2009): pp. 115-137 An Empirical Investigation of the Causal Relationship among Monetary Variables and Equity Market Returns Arshad Hasan * and M. Tariq Javed

THE RELATIONSHIP BETWEEN THE STOCK MARKET AND THE ECONOMY: EXPERIENCE FROM INTERNATIONAL FINANCIAL MARKETS

The Bank Relationship of Valletta between Review, the No. Stock 36, Autumn Market and 2007the Economy THE RELATIONSHIP BETWEEN THE STOCK MARKET AND THE ECONOMY: EXPERIENCE FROM INTERNATIONAL FINANCIAL

The Bank Relationship of Valletta between Review, the No. Stock 36, Autumn Market and 2007the Economy THE RELATIONSHIP BETWEEN THE STOCK MARKET AND THE ECONOMY: EXPERIENCE FROM INTERNATIONAL FINANCIAL

Examining the Relationship between ETFS and Their Underlying Assets in Indian Capital Market

2012 2nd International Conference on Computer and Software Modeling (ICCSM 2012) IPCSIT vol. 54 (2012) (2012) IACSIT Press, Singapore DOI: 10.7763/IPCSIT.2012.V54.20 Examining the Relationship between

2012 2nd International Conference on Computer and Software Modeling (ICCSM 2012) IPCSIT vol. 54 (2012) (2012) IACSIT Press, Singapore DOI: 10.7763/IPCSIT.2012.V54.20 Examining the Relationship between

Does Capital Market Development Predict Investment Behaviors in a Developing Country? --- Evidence from Nigeria

Journal of Contemporary Management Submitted on 15/December/2011 Article ID: 1929-0128-2012-01-27-08 Okey O. Ovat Does Capital Market Development Predict Investment Behaviors in a Developing Country? ---

Journal of Contemporary Management Submitted on 15/December/2011 Article ID: 1929-0128-2012-01-27-08 Okey O. Ovat Does Capital Market Development Predict Investment Behaviors in a Developing Country? ---

INTERRELATION OF MONEY AND CAPITAL MARKETS

ISSN 1392-1258. ekonomika 2009 88 INTERRELATION OF MONEY AND CAPITAL MARKETS Meilė Jasienė Professor, Dr. Department of Finance Vilnius University Saulėtekio Av. 9, LT-10222 Vilnius Tel. +370 5 236 61

ISSN 1392-1258. ekonomika 2009 88 INTERRELATION OF MONEY AND CAPITAL MARKETS Meilė Jasienė Professor, Dr. Department of Finance Vilnius University Saulėtekio Av. 9, LT-10222 Vilnius Tel. +370 5 236 61

Co-movements of NAFTA trade, FDI and stock markets

Co-movements of NAFTA trade, FDI and stock markets Paweł Folfas, Ph. D. Warsaw School of Economics Abstract The paper scrutinizes the causal relationship between performance of American, Canadian and Mexican

Co-movements of NAFTA trade, FDI and stock markets Paweł Folfas, Ph. D. Warsaw School of Economics Abstract The paper scrutinizes the causal relationship between performance of American, Canadian and Mexican

Agenda. Business Cycles. What Is a Business Cycle? What Is a Business Cycle? What is a Business Cycle? Business Cycle Facts.

Agenda What is a Business Cycle? Business Cycles.. 11-1 11-2 Business cycles are the short-run fluctuations in aggregate economic activity around its long-run growth path. Y Time 11-3 11-4 1 Components

Agenda What is a Business Cycle? Business Cycles.. 11-1 11-2 Business cycles are the short-run fluctuations in aggregate economic activity around its long-run growth path. Y Time 11-3 11-4 1 Components

INTELLECTUAL CAPITAL AS THE MAIN FACTOR OF COMPANY S VALUE ADDED

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2011, Vol. 5, No. 4(12), p. 560 574 INTELLECTUAL CAPITAL AS THE MAIN FACTOR OF COMPANY S VALUE ADDED Irena Mačerinskienė,

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2011, Vol. 5, No. 4(12), p. 560 574 INTELLECTUAL CAPITAL AS THE MAIN FACTOR OF COMPANY S VALUE ADDED Irena Mačerinskienė,

Relationship between Commodity Prices and Exchange Rate in Light of Global Financial Crisis: Evidence from Australia

Relationship between Commodity Prices and Exchange Rate in Light of Global Financial Crisis: Evidence from Australia Omar K. M. R. Bashar and Sarkar Humayun Kabir Abstract This study seeks to identify

Relationship between Commodity Prices and Exchange Rate in Light of Global Financial Crisis: Evidence from Australia Omar K. M. R. Bashar and Sarkar Humayun Kabir Abstract This study seeks to identify

The Co-integration of European Stock Markets after the Launch of the Euro

PANOECONOMICUS, 2008, 3, str. 309-324 UDC 336.76(4-672 EU:497):339.92 ORIGINAL SCIENTIFIC PAPER The Co-integration of European Stock Markets after the Launch of the Euro José Soares da Fonseca * Summary:

PANOECONOMICUS, 2008, 3, str. 309-324 UDC 336.76(4-672 EU:497):339.92 ORIGINAL SCIENTIFIC PAPER The Co-integration of European Stock Markets after the Launch of the Euro José Soares da Fonseca * Summary:

The Impact of Macroeconomic Fundamentals on Stock Prices Revisited: Evidence from Indian Data

Eurasian Journal of Business and Economics 2012, 5 (10), 25-44. The Impact of Macroeconomic Fundamentals on Stock Prices Revisited: Evidence from Indian Data Pramod Kumar NAIK *, Puja PADHI ** Abstract

Eurasian Journal of Business and Economics 2012, 5 (10), 25-44. The Impact of Macroeconomic Fundamentals on Stock Prices Revisited: Evidence from Indian Data Pramod Kumar NAIK *, Puja PADHI ** Abstract

THE EFFECTS OF BANKING CREDIT ON THE HOUSE PRICE

THE EFFECTS OF BANKING CREDIT ON THE HOUSE PRICE * Adibeh Savari 1, Yaser Borvayeh 2 1 MA Student, Department of Economics, Science and Research Branch, Islamic Azad University, Khuzestan, Iran 2 MA Student,

THE EFFECTS OF BANKING CREDIT ON THE HOUSE PRICE * Adibeh Savari 1, Yaser Borvayeh 2 1 MA Student, Department of Economics, Science and Research Branch, Islamic Azad University, Khuzestan, Iran 2 MA Student,

Relationship between Interest Rate and Stock Price: Empirical Evidence from Developed and Developing Countries

International Journal of Business and Management March, 009 Relationship between Interest Rate and Stock Price: Empirical Evidence from Developed and Developing Countries Md. Mahmudul Alam (Corresponding

International Journal of Business and Management March, 009 Relationship between Interest Rate and Stock Price: Empirical Evidence from Developed and Developing Countries Md. Mahmudul Alam (Corresponding

TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND

I J A B E R, Vol. 13, No. 4, (2015): 1525-1534 TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND Komain Jiranyakul * Abstract: This study

I J A B E R, Vol. 13, No. 4, (2015): 1525-1534 TEMPORAL CAUSAL RELATIONSHIP BETWEEN STOCK MARKET CAPITALIZATION, TRADE OPENNESS AND REAL GDP: EVIDENCE FROM THAILAND Komain Jiranyakul * Abstract: This study

THE STATE S DEBT ACCEPTANCE CRITERIA IDENTIFICATION AND EVALUATION OF THEIR ACCEPTABILITY IN LITHUANIA

ISSN 2029-8234 (online) VERSLO SISTEMOS ir EKONOMIKA BUSINESS SYSTEMS and ECONOMICS THE STATE S DEBT ACCEPTANCE CRITERIA IDENTIFICATION AND EVALUATION OF THEIR ACCEPTABILITY IN LITHUANIA Žaneta KARAZIJIENĖ

ISSN 2029-8234 (online) VERSLO SISTEMOS ir EKONOMIKA BUSINESS SYSTEMS and ECONOMICS THE STATE S DEBT ACCEPTANCE CRITERIA IDENTIFICATION AND EVALUATION OF THEIR ACCEPTABILITY IN LITHUANIA Žaneta KARAZIJIENĖ

EXPORT INSTABILITY, INVESTMENT AND ECONOMIC GROWTH IN ASIAN COUNTRIES: A TIME SERIES ANALYSIS

ECONOMIC GROWTH CENTER YALE UNIVERSITY P.O. Box 208269 27 Hillhouse Avenue New Haven, Connecticut 06520-8269 CENTER DISCUSSION PAPER NO. 799 EXPORT INSTABILITY, INVESTMENT AND ECONOMIC GROWTH IN ASIAN

ECONOMIC GROWTH CENTER YALE UNIVERSITY P.O. Box 208269 27 Hillhouse Avenue New Haven, Connecticut 06520-8269 CENTER DISCUSSION PAPER NO. 799 EXPORT INSTABILITY, INVESTMENT AND ECONOMIC GROWTH IN ASIAN

COINTEGRATION AND CAUSAL RELATIONSHIP AMONG CRUDE PRICE, DOMESTIC GOLD PRICE AND FINANCIAL VARIABLES- AN EVIDENCE OF BSE AND NSE *

Journal of Contemporary Issues in Business Research ISSN 2305-8277 (Online), 2013, Vol. 2, No. 1, 1-10. Copyright of the Academic Journals JCIBR All rights reserved. COINTEGRATION AND CAUSAL RELATIONSHIP

Journal of Contemporary Issues in Business Research ISSN 2305-8277 (Online), 2013, Vol. 2, No. 1, 1-10. Copyright of the Academic Journals JCIBR All rights reserved. COINTEGRATION AND CAUSAL RELATIONSHIP

Empirical Properties of the Indonesian Rupiah: Testing for Structural Breaks, Unit Roots, and White Noise

Volume 24, Number 2, December 1999 Empirical Properties of the Indonesian Rupiah: Testing for Structural Breaks, Unit Roots, and White Noise Reza Yamora Siregar * 1 This paper shows that the real exchange

Volume 24, Number 2, December 1999 Empirical Properties of the Indonesian Rupiah: Testing for Structural Breaks, Unit Roots, and White Noise Reza Yamora Siregar * 1 This paper shows that the real exchange

The price-volume relationship of the Malaysian Stock Index futures market

The price-volume relationship of the Malaysian Stock Index futures market ABSTRACT Carl B. McGowan, Jr. Norfolk State University Junaina Muhammad University Putra Malaysia The objective of this study is

The price-volume relationship of the Malaysian Stock Index futures market ABSTRACT Carl B. McGowan, Jr. Norfolk State University Junaina Muhammad University Putra Malaysia The objective of this study is

An Empirical Study on the Relationship between Stock Index and the National Economy: The Case of China

An Empirical Study on the Relationship between Stock Index and the National Economy: The Case of China Ming Men And Rui Li University of International Business & Economics Beijing, People s Republic of

An Empirical Study on the Relationship between Stock Index and the National Economy: The Case of China Ming Men And Rui Li University of International Business & Economics Beijing, People s Republic of

The Relationship between Current Account and Government Budget Balance: The Case of Kuwait

International Journal of Humanities and Social Science Vol. 2 No. 7; April 2012 The Relationship between Current Account and Government Budget Balance: The Case of Kuwait Abstract Ebrahim Merza Economics

International Journal of Humanities and Social Science Vol. 2 No. 7; April 2012 The Relationship between Current Account and Government Budget Balance: The Case of Kuwait Abstract Ebrahim Merza Economics

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange Farzad Karimi Assistant Professor Department of Management Mobarakeh Branch, Islamic Azad University, Mobarakeh,

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange Farzad Karimi Assistant Professor Department of Management Mobarakeh Branch, Islamic Azad University, Mobarakeh,

MULTIPLE REGRESSIONS ON SOME SELECTED MACROECONOMIC VARIABLES ON STOCK MARKET RETURNS FROM 1986-2010

Advances in Economics and International Finance AEIF Vol. 1(1), pp. 1-11, December 2014 Available online at http://www.academiaresearch.org Copyright 2014 Academia Research Full Length Research Paper MULTIPLE

Advances in Economics and International Finance AEIF Vol. 1(1), pp. 1-11, December 2014 Available online at http://www.academiaresearch.org Copyright 2014 Academia Research Full Length Research Paper MULTIPLE

Asian Economic and Financial Review DETERMINANTS OF THE AUD/USD EXCHANGE RATE AND POLICY IMPLICATIONS

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 DETERMINANTS OF THE AUD/USD EXCHANGE RATE AND POLICY IMPLICATIONS Yu Hsing

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 DETERMINANTS OF THE AUD/USD EXCHANGE RATE AND POLICY IMPLICATIONS Yu Hsing

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES. Mark Rider. Research Discussion Paper 9405. November 1994. Economic Research Department

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES Mark Rider Research Discussion Paper 9405 November 1994 Economic Research Department Reserve Bank of Australia I would like to thank Sally Banguis

EXTERNAL DEBT AND LIABILITIES OF INDUSTRIAL COUNTRIES Mark Rider Research Discussion Paper 9405 November 1994 Economic Research Department Reserve Bank of Australia I would like to thank Sally Banguis

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Danguolė JABLONSKIENĖ. doi:10.13165/ie-13-7-3-08

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2013, Vol. 7, No. 3(17), p. 375 388 INFLUENCE OF PENSION FUNDS AND LIFE INSURANCE ON OLD-AGE PENSION Danguolė

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2013, Vol. 7, No. 3(17), p. 375 388 INFLUENCE OF PENSION FUNDS AND LIFE INSURANCE ON OLD-AGE PENSION Danguolė

Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

A Century of PPP: Supportive Results from non-linear Unit Root Tests

Mohsen Bahmani-Oskooee a, Ali Kutan b and Su Zhou c A Century of PPP: Supportive Results from non-linear Unit Root Tests ABSTRACT Testing for stationarity of the real exchange rates is a common practice

Mohsen Bahmani-Oskooee a, Ali Kutan b and Su Zhou c A Century of PPP: Supportive Results from non-linear Unit Root Tests ABSTRACT Testing for stationarity of the real exchange rates is a common practice

Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

American Journal of Applied Sciences 2 (5): 996-1002, 2005 ISSN 1546-9239 Science Publications, 2005 Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

American Journal of Applied Sciences 2 (5): 996-1002, 2005 ISSN 1546-9239 Science Publications, 2005 Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

Financial Integration of Stock Markets in the Gulf: A Multivariate Cointegration Analysis

INTERNATIONAL JOURNAL OF BUSINESS, 8(3), 2003 ISSN:1083-4346 Financial Integration of Stock Markets in the Gulf: A Multivariate Cointegration Analysis Aqil Mohd. Hadi Hassan Department of Economics, College

INTERNATIONAL JOURNAL OF BUSINESS, 8(3), 2003 ISSN:1083-4346 Financial Integration of Stock Markets in the Gulf: A Multivariate Cointegration Analysis Aqil Mohd. Hadi Hassan Department of Economics, College

Oil Price Fluctuation and Stock Market Performance-The Case of Pakistan

Middle-East Journal of Scientific Research 18 (2): 177-182, 2013 ISSN 1990-9233 IDOSI Publications, 2013 DOI: 10.5829/idosi.mejsr.2013.18.2.12441 Oil Price Fluctuation and Stock Market Performance-The

Middle-East Journal of Scientific Research 18 (2): 177-182, 2013 ISSN 1990-9233 IDOSI Publications, 2013 DOI: 10.5829/idosi.mejsr.2013.18.2.12441 Oil Price Fluctuation and Stock Market Performance-The

Effect of Exchange Rate on Shares Turnover of Karachi Stock Exchange

Effect of Exchange Rate on Shares Turnover of Karachi Stock Exchange Shahid Rasheed Lecturer, Department of Management Sciences, Abasyn University Email: Shahid.rasheed@abasyn.edu.pk Qadar Bakhsh Baloch

Effect of Exchange Rate on Shares Turnover of Karachi Stock Exchange Shahid Rasheed Lecturer, Department of Management Sciences, Abasyn University Email: Shahid.rasheed@abasyn.edu.pk Qadar Bakhsh Baloch

Monetary policy rules and their application in Russia. Economics Education and Research Consortium Working Paper Series ISSN 1561-2422.

Economics Education and Research Consortium Working Paper Series ISSN 1561-2422 No 04/09 Monetary policy rules and their application in Russia Anna Vdovichenko Victoria Voronina This project (02-230) was

Economics Education and Research Consortium Working Paper Series ISSN 1561-2422 No 04/09 Monetary policy rules and their application in Russia Anna Vdovichenko Victoria Voronina This project (02-230) was

CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM)

") 1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

THE EFFECT OF MONETARY GROWTH VARIABILITY ON THE INDONESIAN CAPITAL MARKET

116 THE EFFECT OF MONETARY GROWTH VARIABILITY ON THE INDONESIAN CAPITAL MARKET D. Agus Harjito, Bany Ariffin Amin Nordin, Ahmad Raflis Che Omar Abstract Over the years studies to ascertain the relationship

116 THE EFFECT OF MONETARY GROWTH VARIABILITY ON THE INDONESIAN CAPITAL MARKET D. Agus Harjito, Bany Ariffin Amin Nordin, Ahmad Raflis Che Omar Abstract Over the years studies to ascertain the relationship

FDI and Economic Growth Relationship: An Empirical Study on Malaysia

International Business Research April, 2008 FDI and Economic Growth Relationship: An Empirical Study on Malaysia Har Wai Mun Faculty of Accountancy and Management Universiti Tunku Abdul Rahman Bander Sungai

International Business Research April, 2008 FDI and Economic Growth Relationship: An Empirical Study on Malaysia Har Wai Mun Faculty of Accountancy and Management Universiti Tunku Abdul Rahman Bander Sungai

IMPACT OF FOREIGN EXCHANGE RESERVES ON NIGERIAN STOCK MARKET Olayinka Olufisayo Akinlo, Obafemi Awolowo University, Ile-Ife, Nigeria

International Journal of Business and Finance Research Vol. 9, No. 2, 2015, pp. 69-76 ISSN: 1931-0269 (print) ISSN: 2157-0698 (online) www.theibfr.org IMPACT OF FOREIGN EXCHANGE RESERVES ON NIGERIAN STOCK

International Journal of Business and Finance Research Vol. 9, No. 2, 2015, pp. 69-76 ISSN: 1931-0269 (print) ISSN: 2157-0698 (online) www.theibfr.org IMPACT OF FOREIGN EXCHANGE RESERVES ON NIGERIAN STOCK

Relative Effectiveness of Foreign Debt and Foreign Aid on Economic Growth in Pakistan

Relative Effectiveness of Foreign Debt and Foreign Aid on Economic Growth in Pakistan Abstract Zeshan Arshad Faculty of Management and Sciences, Evening Program, University of Gujrat, Pakistan. Muhammad

Relative Effectiveness of Foreign Debt and Foreign Aid on Economic Growth in Pakistan Abstract Zeshan Arshad Faculty of Management and Sciences, Evening Program, University of Gujrat, Pakistan. Muhammad

COURSES: 1. Short Course in Econometrics for the Practitioner (P000500) 2. Short Course in Econometric Analysis of Cointegration (P000537)

2. Short Course in Econometric Analysis of Cointegration (P000537)") Get the latest knowledge from leading global experts. Financial Science Economics Economics Short Courses Presented by the Department of Economics, University of Pretoria WITH 2015 DATES www.ce.up.ac.za

Get the latest knowledge from leading global experts. Financial Science Economics Economics Short Courses Presented by the Department of Economics, University of Pretoria WITH 2015 DATES www.ce.up.ac.za

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH Grant Keener, Sam Houston State University M.H. Tuttle, Sam Houston State University 21 ABSTRACT Household wealth is shown to have a substantial

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH Grant Keener, Sam Houston State University M.H. Tuttle, Sam Houston State University 21 ABSTRACT Household wealth is shown to have a substantial

How do oil prices affect stock returns in GCC markets? An asymmetric cointegration approach.

How do oil prices affect stock returns in GCC markets? An asymmetric cointegration approach. Mohamed El Hedi AROURI (LEO-Université d Orléans & EDHEC, mohamed.arouri@univ-orleans.fr) Julien FOUQUAU (ESC

How do oil prices affect stock returns in GCC markets? An asymmetric cointegration approach. Mohamed El Hedi AROURI (LEO-Université d Orléans & EDHEC, mohamed.arouri@univ-orleans.fr) Julien FOUQUAU (ESC

Testing for Granger causality between stock prices and economic growth

MPRA Munich Personal RePEc Archive Testing for Granger causality between stock prices and economic growth Pasquale Foresti 2006 Online at http://mpra.ub.uni-muenchen.de/2962/ MPRA Paper No. 2962, posted

MPRA Munich Personal RePEc Archive Testing for Granger causality between stock prices and economic growth Pasquale Foresti 2006 Online at http://mpra.ub.uni-muenchen.de/2962/ MPRA Paper No. 2962, posted

Do Commercial Banks, Stock Market and Insurance Market Promote Economic Growth? An analysis of the Singapore Economy

Do Commercial Banks, Stock Market and Insurance Market Promote Economic Growth? An analysis of the Singapore Economy Tan Khay Boon School of Humanities and Social Studies Nanyang Technological University

Do Commercial Banks, Stock Market and Insurance Market Promote Economic Growth? An analysis of the Singapore Economy Tan Khay Boon School of Humanities and Social Studies Nanyang Technological University

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study Dr.Ahmed-Al-Huseiny* ABSTRACT The Iraqi economy is not isolated from the

Financial Crisis and the fluctuations of the global crude oil prices and their impacts on the Iraqi Public Budget Special Study Dr.Ahmed-Al-Huseiny* ABSTRACT The Iraqi economy is not isolated from the

THE RELEVANCE OF CHICAGO BOARD OPTIONS EXCHANGE VOLATILITY INDEX TO DEVELOPED AND EMERGING STOCK MARKET INDICES. A Thesis. Presented to the Faculty

THE RELEVANCE OF CHICAGO BOARD OPTIONS EXCHANGE VOLATILITY INDEX TO DEVELOPED AND EMERGING STOCK MARKET INDICES A Thesis Presented to the Faculty of Finance programme at ISM University of Management and

THE RELEVANCE OF CHICAGO BOARD OPTIONS EXCHANGE VOLATILITY INDEX TO DEVELOPED AND EMERGING STOCK MARKET INDICES A Thesis Presented to the Faculty of Finance programme at ISM University of Management and

Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data

2012, Vol. 4, No. 2, pp. 103-112 ISSN 2152-1034 Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data Abstract Zukarnain Zakaria Universiti Teknologi

2012, Vol. 4, No. 2, pp. 103-112 ISSN 2152-1034 Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data Abstract Zukarnain Zakaria Universiti Teknologi

THE BENEFIT OF INTERNATIONAL PORTFOLIO DIVERSIFICATION IN ASIAN EMERGING MARKETS TO THE U.S INVESTORS

THE BENEFIT OF INTERNATIONAL PORTFOLIO DIVERSIFICATION IN ASIAN EMERGING MARKETS TO THE U.S INVESTORS Faranak Roshani Zafaranloo Graduate School of Business (UKM-GSB) University Kebangsaaan Malaysia Bangi,

THE BENEFIT OF INTERNATIONAL PORTFOLIO DIVERSIFICATION IN ASIAN EMERGING MARKETS TO THE U.S INVESTORS Faranak Roshani Zafaranloo Graduate School of Business (UKM-GSB) University Kebangsaaan Malaysia Bangi,

Working Papers. Cointegration Based Trading Strategy For Soft Commodities Market. Piotr Arendarski Łukasz Postek. No. 2/2012 (68)

") Working Papers No. 2/2012 (68) Piotr Arendarski Łukasz Postek Cointegration Based Trading Strategy For Soft Commodities Market Warsaw 2012 Cointegration Based Trading Strategy For Soft Commodities Market

Working Papers No. 2/2012 (68) Piotr Arendarski Łukasz Postek Cointegration Based Trading Strategy For Soft Commodities Market Warsaw 2012 Cointegration Based Trading Strategy For Soft Commodities Market

THE UPDATE OF THE EURO EFFECTIVE EXCHANGE RATE INDICES

September 2004 THE UPDATE OF THE EURO EFFECTIVE EXCHANGE RATE INDICES Executive summary In September 2004, the European Central Bank (ECB) has updated the overall trade weights underlying the ECB nominal

September 2004 THE UPDATE OF THE EURO EFFECTIVE EXCHANGE RATE INDICES Executive summary In September 2004, the European Central Bank (ECB) has updated the overall trade weights underlying the ECB nominal

How budget deficit and current account deficit are interrelated in Indian economy

Theoretical and Applied Economics FFet al Volume XXIII (2016), No. 1(606), Spring, pp. 237-246 How budget deficit and current account deficit are interrelated in Indian economy U.J. BANDAY Jamia Millia

Theoretical and Applied Economics FFet al Volume XXIII (2016), No. 1(606), Spring, pp. 237-246 How budget deficit and current account deficit are interrelated in Indian economy U.J. BANDAY Jamia Millia

DAILY VOLATILITY IN THE TURKISH FOREIGN EXCHANGE MARKET. Cem Aysoy. Ercan Balaban. Çigdem Izgi Kogar. Cevriye Ozcan

DAILY VOLATILITY IN THE TURKISH FOREIGN EXCHANGE MARKET Cem Aysoy Ercan Balaban Çigdem Izgi Kogar Cevriye Ozcan THE CENTRAL BANK OF THE REPUBLIC OF TURKEY Research Department Discussion Paper No: 9625

DAILY VOLATILITY IN THE TURKISH FOREIGN EXCHANGE MARKET Cem Aysoy Ercan Balaban Çigdem Izgi Kogar Cevriye Ozcan THE CENTRAL BANK OF THE REPUBLIC OF TURKEY Research Department Discussion Paper No: 9625

Energy consumption and GDP: causality relationship in G-7 countries and emerging markets

Ž. Energy Economics 25 2003 33 37 Energy consumption and GDP: causality relationship in G-7 countries and emerging markets Ugur Soytas a,, Ramazan Sari b a Middle East Technical Uni ersity, Department

Ž. Energy Economics 25 2003 33 37 Energy consumption and GDP: causality relationship in G-7 countries and emerging markets Ugur Soytas a,, Ramazan Sari b a Middle East Technical Uni ersity, Department

Implied volatility transmissions between Thai and selected advanced stock markets

MPRA Munich Personal RePEc Archive Implied volatility transmissions between Thai and selected advanced stock markets Supachok Thakolsri and Yuthana Sethapramote and Komain Jiranyakul Public Enterprise

MPRA Munich Personal RePEc Archive Implied volatility transmissions between Thai and selected advanced stock markets Supachok Thakolsri and Yuthana Sethapramote and Komain Jiranyakul Public Enterprise

THE INDONESIAN STOCK MARKET PERFORMANCE DURING ASIAN ECONOMIC CRISIS AND GLOBAL FINANCIAL CRISIS

THE INDONESIAN STOCK MARKET PERFORMANCE DURING ASIAN ECONOMIC CRISIS AND GLOBAL FINANCIAL CRISIS MARIA PRAPTININGSIH Abstract Volatility in the stock market had strongly affected by the movement of publicly

THE INDONESIAN STOCK MARKET PERFORMANCE DURING ASIAN ECONOMIC CRISIS AND GLOBAL FINANCIAL CRISIS MARIA PRAPTININGSIH Abstract Volatility in the stock market had strongly affected by the movement of publicly

Economic Growth Centre Working Paper Series

Economic Growth Centre Working Paper Series The Impact of Oil Price Fluctuations on Stock Markets in Developed and Emerging Economies by Thai-Ha LE and Youngho CHANG Economic Growth Centre Division of

Economic Growth Centre Working Paper Series The Impact of Oil Price Fluctuations on Stock Markets in Developed and Emerging Economies by Thai-Ha LE and Youngho CHANG Economic Growth Centre Division of

ijcrb.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS AUGUST 2014 VOL 6, NO 4

RELATIONSHIP AND CAUSALITY BETWEEN INTEREST RATE AND INFLATION RATE CASE OF JORDAN Dr. Mahmoud A. Jaradat Saleh A. AI-Hhosban Al al-bayt University, Jordan ABSTRACT This study attempts to examine and study

RELATIONSHIP AND CAUSALITY BETWEEN INTEREST RATE AND INFLATION RATE CASE OF JORDAN Dr. Mahmoud A. Jaradat Saleh A. AI-Hhosban Al al-bayt University, Jordan ABSTRACT This study attempts to examine and study

Centralizuotas mobilių įrenginių valdymas. Andrius Šaveiko andrius.saveiko@atea.lt

Centralizuotas mobilių įrenginių valdymas Andrius Šaveiko andrius.saveiko@atea.lt Turinys Mobilių įrenginių valdymas (MDM) nuo ko pradėti? Situacija MDM rinkoje BYOD koncepcija ar tai įmanoma? MDM sprendimai

Centralizuotas mobilių įrenginių valdymas Andrius Šaveiko andrius.saveiko@atea.lt Turinys Mobilių įrenginių valdymas (MDM) nuo ko pradėti? Situacija MDM rinkoje BYOD koncepcija ar tai įmanoma? MDM sprendimai

Comovements of the Korean, Chinese, Japanese and US Stock Markets.

World Review of Business Research Vol. 3. No. 4. November 2013 Issue. Pp. 146 156 Comovements of the Korean, Chinese, Japanese and US Stock Markets. 1. Introduction Sung-Ky Min * The paper examines Comovements

World Review of Business Research Vol. 3. No. 4. November 2013 Issue. Pp. 146 156 Comovements of the Korean, Chinese, Japanese and US Stock Markets. 1. Introduction Sung-Ky Min * The paper examines Comovements

The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series.

data, like asset returns or growth rates of macroeconomic time series.") Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

The relation between news events and stock price jump: an analysis based on neural network

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 The relation between news events and stock price jump: an analysis based on

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 The relation between news events and stock price jump: an analysis based on

Impact of Macroeconomic Variables on the Stock Market Prices of the Stockholm Stock Exchange (OMXS30)

") J Ö N K Ö P I N G I N T E R N A T I O N A L B U S I N E S S S C H O O L JÖNKÖPING UNIVERSITY Impact of Macroeconomic Variables on the Stock Market Prices of the Stockholm Stock Exchange (OMXS30) Master

J Ö N K Ö P I N G I N T E R N A T I O N A L B U S I N E S S S C H O O L JÖNKÖPING UNIVERSITY Impact of Macroeconomic Variables on the Stock Market Prices of the Stockholm Stock Exchange (OMXS30) Master

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES. Hamid Raza PhD Student, Economics University of Limerick Ireland

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

FINANCIALISATION AND EXCHANGE RATE DYNAMICS IN SMALL OPEN ECONOMIES Hamid Raza PhD Student, Economics University of Limerick Ireland Financialisation Financialisation as a broad concept refers to: a) an

Stock market booms and real economic activity: Is this time different?

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

DEPARTMENT OF ECONOMICS CREDITOR PROTECTION AND BANKING SYSTEM DEVELOPMENT IN INDIA

DEPARTMENT OF ECONOMICS CREDITOR PROTECTION AND BANKING SYSTEM DEVELOPMENT IN INDIA Simon Deakin, University of Cambridge, UK Panicos Demetriades, University of Leicester, UK Gregory James, University

DEPARTMENT OF ECONOMICS CREDITOR PROTECTION AND BANKING SYSTEM DEVELOPMENT IN INDIA Simon Deakin, University of Cambridge, UK Panicos Demetriades, University of Leicester, UK Gregory James, University