LEGISLATIVE COUNCIL BRIEF

|

|

|

- Edwina Heath

- 7 years ago

- Views:

Transcription

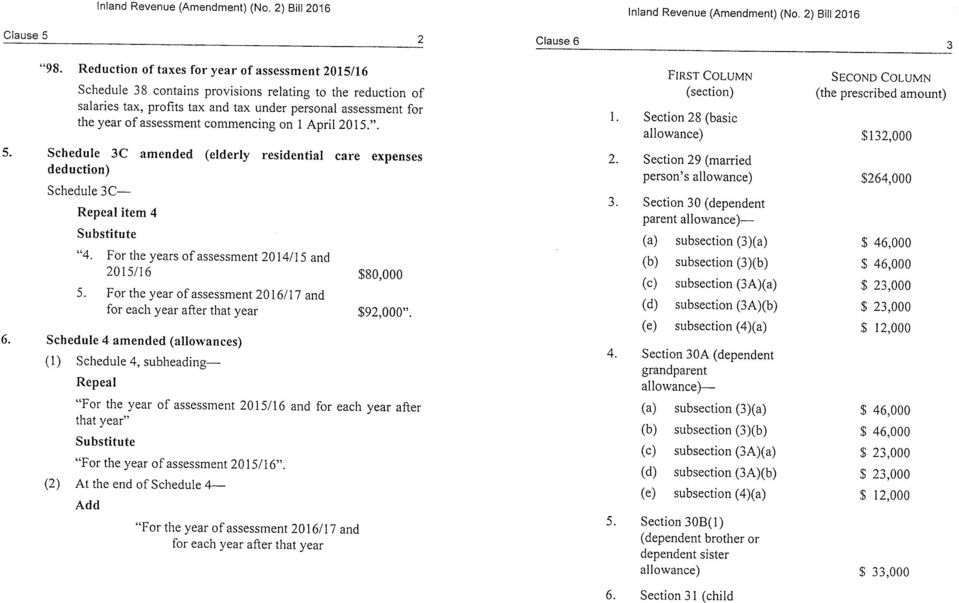

1 File Ref.: TsyB R 183/535-1/5/0 (16-17) (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (AMENDMENT) (NO. 2) BILL 2016 INTRODUCTION A At the meeting of the Executive Council on 24 February 2016, the Council ADVISED and the Chief Executive ORDERED that the Inland Revenue (Amendment) (No. 2) Bill 2016 (the Bill), at Annex A, should be introduced into the Legislative Council (LegCo) to implement the following concessionary revenue measures proposed in the Budget (a) for salaries tax and tax under personal assessment with effect from the year of assessment 2016/17 (i) to increase the basic allowance and the single parent allowance both from $120,000 to $132,000 and the married person s allowance from $240,000 to $264,000; (ii) to increase the dependent parent/grandparent allowance and the additional dependent parent/grandparent allowance for each eligible parent/grandparent both from $40,000 to $46,000 (for aged 60 or above) and from $20,000 to $23,000 (for aged 55 or above but below 60); and (iii) to raise the deduction ceiling for elderly residential care expenses for each eligible parent/grandparent from $80,000 to $92,000; and (b) to reduce salaries tax, tax under personal assessment and profits tax for the year of assessment 2015/16 by 75%, subject to a ceiling of $20,000 per case.

to increase the basic allowance and the single parent allowance both from $120,000 to $132,000 and")

2 JUSTIFICATIONS Proposed Increases in Allowances and Deduction Ceiling 2. To relieve the tax burden of salaries tax payers, and to alleviate their burden in maintaining dependent parents or grandparents, the Budget proposes to adjust two categories of allowances for salaries tax and tax under personal assessment as follows (a) (b) increasing the basic allowance and the single parent allowance both by 10% from the current $120,000 to $132,000, and the married person s allowance also by 10% from the current $240,000 to $264,000; increasing the allowances/ deduction related to parents and grandparents by 15% (i) from $40,000 to $46,000 for maintaining a dependent parent or grandparent aged 60 or above 1, and from $20,000 to $23,000 for those aged between 55 and 59. The same increase applies to the additional allowance granted to taxpayers residing with these parents or grandparents continuously throughout the year; and (ii) from the current $80,000 to $92,000 as the deduction ceiling a taxpayer may claim for the elderly residential care expenses for each parent or grandparent admitted to residential care homes According to the existing provisions of the Inland Revenue Ordinance ( IRO ), should the deduction for elderly residential care expenses be allowed to a person or his/her spouse (paragraph 2(b)(ii) above), no person is entitled to claim dependent parent/grandparent allowance (paragraph 2(b)(i) above) for the same parent/grandparent for the same year of assessment. 1 2 That allowance may also be claimed in respect of a dependent parent or grandparent who is under the age of 60 and is eligible to claim an allowance under the Government s Disability Allowance Scheme, as provided for under sections 30(1) and 30A(1) of the Inland Revenue Ordinance. The deduction is claimed in respect of elderly residential care expenses for a parent or grandparent who is either aged 60 or above, or who is under the age of 60 and is eligible to claim an allowance under the Government s Disability Allowance Scheme, as provided for under section 26D(1) of the Inland Revenue Ordinance

from $40,000 to $46,000 for maintaining a")

3 4. The measures in paragraph 2 above will take effect for the year of assessment 2016/17 onwards. The proposed measures as set out in paragraph 2(a) above will benefit 1.93 million taxpayers of salaries tax and tax under personal assessment. The revenue forgone is estimated to be $2.9 billion a year. The proposed measures as set out in paragraph 2(b) above will benefit taxpayers. The revenue forgone is estimated to be $860 million a year. Proposed One-off Tax Reduction for the Year of Assessment 2015/16 5. Government has proposed a number of one-off relief measures in the Budget. These include a one-off reduction of salaries tax, tax under personal assessment and profits tax for the year of assessment 2015/16 by 75%, subject to a ceiling of $20,000 per case. The reduction will be reflected in the taxpayers final tax payable for the year of assessment 2015/16. The proposed one-off reduction of salaries tax and tax under personal assessment will benefit 1.96 million taxpayers, whereas the proposed one-off reduction of profits tax will benefit tax-paying corporations and unincorporated businesses. The revenue forgone for is $18.9 billion. OTHER OPTIONS 6. We must amend the IRO to give effect to the relevant proposals. There is no other option. THE BILL 7. The major provisions of the Bill are as follows (a) (b) Clause 3 amends section 89 of the IRO to provide that the transitional provisions set out in the new Schedule 37 (added by clause 7) have effect in relation to a person liable to pay provisional salaries tax in respect of the year of assessment 2016/17. Clause 4 adds a new section 98 to the IRO. The new section and the new Schedule 38 (added by clause 7) provide for the reduction of salaries tax, profits tax and tax under personal assessment payable for the year of assessment 2015/16 by 75%, subject to a maximum of $20,000 in each case

4 (c) Clause 5 amends Schedule 3C to the IRO to increase the maximum amount of elderly residential care expenses deductible from assessable income from $80,000 to $92,000 for the year of assessment 2016/17 and subsequent years of assessment. (d) Clause 6 amends Schedule 4 to the IRO to increase (i) the amount of basic allowance granted under section 28 of the IRO from $120,000 to $132,000; (ii) the amount of married person s allowance granted under section 29 of the IRO from $240,000 to $264,000; (iii) the amounts of dependent parent allowance and additional dependent parent allowance granted in respect of a parent (aged 60 or above, or who is under the age of 60 and is eligible to claim an allowance under the Government s Disability Allowance Scheme (GDAS)) under section 30(1) of the IRO, both from $40,000 to $46,000; (iv) the amounts of dependent parent allowance and additional dependent parent allowance granted in respect of a parent (aged 55 or above but below 60) under section 30(1A) of the IRO, both from $20,000 to $23,000; (v) the amounts of dependent grandparent allowance and additional dependent grandparent allowance granted in respect of a grandparent (aged 60 or above, or who is under the age of 60 and is eligible to claim an allowance under GDAS) under section 30A(1) of the IRO, both from $40,000 to $46,000; (vi) the amounts of dependent grandparent allowance and additional dependent grandparent allowance granted in respect of a grandparent (aged 55 or above but below 60) under section 30A(1A) of the IRO, both from $20,000 to $23,000; and (vii) the amount of single parent allowance granted under section 32 of the IRO from $120,000 to $132,

the amounts of dependent parent allowance and additional dependent parent allowance granted in respect of a parent (aged 60 or")

5 The increases take effect for the year of assessment 2016/17 and subsequent years of assessment. (e) Clause 7 adds new Schedules 37 and 38 to the IRO. The new Schedule 37 provides for the transitional arrangements relating to the assessment of, and holding over of payment of, provisional salaries tax for the year of assessment 2016/17. LEGISLATIVE TIMETABLE 8. The legislative timetable will be as follows Publication in the Gazette 4 March 2016 First Reading and commencement of Second Reading debate Resumption of Second Reading debate, committee stage and Third Reading 16 March 2016 To be notified IMPLICATIONS OF THE PROPOSAL B 9. The proposal is in conformity with the Basic Law, including the provisions concerning human rights. The proposal will not affect the binding effect of the existing provisions of the IRO and its subsidiary legislation. The financial, economic, sustainability and family implications of the proposal are at Annex B. The proposal has no productivity, environmental, gender or civil service implications. PUBLIC CONSULTATION 10. Owing to the confidentiality of the Budget, no formal consultation was conducted specifically in respect of the proposals in the Bill. The Financial Secretary has conducted consultations with LegCo Members, various business and professional bodies as well as the general public when formulating the Budget. Their views have been taken into account in drawing up those proposals

6 PUBLICITY 11. We will issue a press release on the Bill on 4 March A spokesperson will be available to answer media and public enquiries. ENQUIRIES 12. Enquiries on this Brief can be addressed to Mr Gary Poon, Principal Assistant Secretary for Financial Services and the Treasury (Treasury) at Financial Services and the Treasury Bureau 2 March

at 2810 2370.")

7 LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (AMENDMENT) (NO. 2) BILL 2016 ANNEXES Annex A Inland Revenue (Amendment) (No. 2) Bill 2016 Annex B Financial, Economic, Sustainability and Family Implications of the Proposal

Bill 2016 Annex B Financial, Economic, Sustainability and")

8 Annex A

9

10

11

12

13

14 Annex B Financial, Economic, Sustainability and Family Implications of the Proposal Financial Implications It is estimated that the proposed increases in basic allowance, single parent allowance, married person s allowance, dependent parent/grandparent allowance and deduction ceiling for elderly residential care expenses will involve a total of $3.8 billion a year as revenue forgone. As for the proposed one-off reduction of salaries tax, tax under personal assessment and profits tax for the year of assessment 2015/16, the estimated one-off revenue forgone is $18.9 billion. Economic Implications 2. The proposed concessionary tax measures will help relieve the financial burden of taxpayers, and possibly generate some mild stimulus to consumer spending. The proposed one-off reduction of profits tax will allow enterprises, especially small and medium ones, to have more disposable funds. Sustainability Implications 3. The proposed concessionary tax measures are expected to generate economic benefits to households through increasing their disposable incomes and to promote social harmony through alleviating taxpayers burden in maintaining dependent parents or grandparents. The proposed one-off reduction of profits tax will encourage enterprises to make more reinvestment with a view to enhancing their competitiveness. Family Implications 4. The proposed increases in the dependent parent/grandparent allowances and deduction ceiling for elderly residential care expenses will help strengthen taxpayers capability to provide support for and foster care of elderly family members. Besides, the proposed increase in the basic allowance, single parent allowance and married person s allowance will also help relieve the financial burden of related families.

LEGISLATIVE COUNCIL BRIEF. Inland Revenue Ordinance (Chapter 112)

") File Ref: TsyB R 183/800-1-1/38/0 (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (DOUBLE TAXATION RELIEF AND PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME)

File Ref: TsyB R 183/800-1-1/38/0 (C) LEGISLATIVE COUNCIL BRIEF Inland Revenue Ordinance (Chapter 112) INLAND REVENUE (DOUBLE TAXATION RELIEF AND PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME)

LEGISLATIVE COUNCIL BRIEF. Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE

PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE") File Ref: HAB/CR 19/1/2 LEGISLATIVE COUNCIL BRIEF Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE INTRODUCTION Annex Pursuant to section 7(b) of the Legal Aid Ordinance

File Ref: HAB/CR 19/1/2 LEGISLATIVE COUNCIL BRIEF Legal Aid Ordinance (Chapter 91) PROPOSED RESOLUTION UNDER THE LEGAL AID ORDINANCE INTRODUCTION Annex Pursuant to section 7(b) of the Legal Aid Ordinance

A guide to Salaries Tax (2) which income is assessable and which deductions are allowable

which income is assessable and which deductions are allowable") A guide to Salaries Tax (2) which income is assessable and which deductions are allowable Foreword This guide helps you understand what income is assessable and what deductions are allowable under Salaries

A guide to Salaries Tax (2) which income is assessable and which deductions are allowable Foreword This guide helps you understand what income is assessable and what deductions are allowable under Salaries

立 法 會. Legislative Council. Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013. Background brief

(No.3) Bill 2013. Background brief") 立 法 會 Legislative Council LC Paper No. CB(1)790/13-14(02) Ref : CB1/BC/3/13 Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013 Background brief Purpose 1. This paper provides background information

立 法 會 Legislative Council LC Paper No. CB(1)790/13-14(02) Ref : CB1/BC/3/13 Bills Committee on Inland Revenue (Amendment) (No.3) Bill 2013 Background brief Purpose 1. This paper provides background information

立 法 會 Legislative Council

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

立 法 會 Legislative Council Paper for the House Committee Meeting on 16 October 2015 Legal Service Division Report on Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 LC Paper No.

LEGISLATIVE COUNCIL BRIEF. Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615)

Ordinance (Chapter 615)") File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

File Ref: G13/21C LEGISLATIVE COUNCIL BRIEF Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Chapter 615) Anti-Money Laundering and Counter-Terrorist Financing

LEGISLATIVE COUNCIL BRIEF ELECTRONIC TRANSACTIONS (EXCLUSION) (AMENDMENT) ORDER 2015

(AMENDMENT) ORDER 2015") File Ref: GCIO 107/4/3 XXVI LEGISLATIVE COUNCIL BRIEF ELECTRONIC TRANSACTIONS (EXCLUSION) (AMENDMENT) ORDER 2015 INTRODUCTION On 29 September 2015, the Permanent Secretary for Commerce and Economic Development

File Ref: GCIO 107/4/3 XXVI LEGISLATIVE COUNCIL BRIEF ELECTRONIC TRANSACTIONS (EXCLUSION) (AMENDMENT) ORDER 2015 INTRODUCTION On 29 September 2015, the Permanent Secretary for Commerce and Economic Development

Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong

in Hong Kong") CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

CB(1)931/14-15(03) Proposal to Attract Enterprises to Establish Corporate Treasury Centres ( CTCs ) in Hong Kong LegCo Panel on Financial Affairs Meeting on 1 June 2015 2015 16 Budget To attract multinational

Declaration of Change of Titles (Communications and Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015

Notice 2015") Declaration of Change of Titles Technology Branch and Section 1 B4949 Declaration of Change of Titles Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015 (Made by the

Declaration of Change of Titles Technology Branch and Section 1 B4949 Declaration of Change of Titles Technology Branch and Secretaries of Communications and Technology Branch) Notice 2015 (Made by the

LEGISLATIVE COUNCIL BRIEF. Rehabilitation Centres Ordinance (Cap. 567) Rehabilitation Centres (Appointment) (Amendment) Order 2014

Rehabilitation Centres (Appointment) (Amendment) Order 2014") Ref. : SEC 2/1/21 LEGISLATIVE COUNCIL BRIEF Rehabilitation Centres Ordinance (Cap. 567) Rehabilitation Centres (Appointment) (Amendment) Order 2014 Training Centres Ordinance (Cap. 280) Training Centre

Ref. : SEC 2/1/21 LEGISLATIVE COUNCIL BRIEF Rehabilitation Centres Ordinance (Cap. 567) Rehabilitation Centres (Appointment) (Amendment) Order 2014 Training Centres Ordinance (Cap. 280) Training Centre

LEGISLATIVE COUNCIL BRIEF. Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015

INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015") File Ref.: INS/2/3C(2015) LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015 INTRODUCTION The Secretary for Financial

File Ref.: INS/2/3C(2015) LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) ORDINANCE 2015 (COMMENCEMENT) NOTICE 2015 INTRODUCTION The Secretary for Financial

A Brief Guide to Personal Assessment. Whether Tax may be Reduced through Election for Personal Assessment

A Brief Guide to Personal Assessment Whether Tax may be Reduced through Election for Personal Assessment Foreword This leaflet explains 1. what Personal Assessment is, 2. how Personal Assessment may reduce

A Brief Guide to Personal Assessment Whether Tax may be Reduced through Election for Personal Assessment Foreword This leaflet explains 1. what Personal Assessment is, 2. how Personal Assessment may reduce

Income tax personal allowance for those born after 5 April 1938 for 2015-16

Income tax personal allowance for those born after 5 April 1938 for 2015-16 Who is likely to be affected? Income tax payers, employers and pension providers. General description of the measure For 2015-16,

Income tax personal allowance for those born after 5 April 1938 for 2015-16 Who is likely to be affected? Income tax payers, employers and pension providers. General description of the measure For 2015-16,

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST

CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST These notes are issued for the information

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 35 (REVISED) CONCESSIONARY DEDUCTIONS: SECTIONS 26E AND 26F HOME LOAN INTEREST These notes are issued for the information

LEGISLATIVE COUNCIL BRIEF

File Ref.: IB&W/2/1/5/4C LEGISLATIVE COUNCIL BRIEF Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32) Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 INTRODUCTION

File Ref.: IB&W/2/1/5/4C LEGISLATIVE COUNCIL BRIEF Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32) Companies (Winding Up and Miscellaneous Provisions) (Amendment) Bill 2015 INTRODUCTION

A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions

The need-to-know for new businesses and commonly asked questions") A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions Foreword This guide will help answer some of the questions that owners of small

A guide to Profits Tax for unincorporated businesses (1) The need-to-know for new businesses and commonly asked questions Foreword This guide will help answer some of the questions that owners of small

LEGISLATIVE COUNCIL BRIEF

File reference: FH CR 1/1/3781/10 LEGISLATIVE COUNCIL BRIEF ELECTRONIC HEALTH RECORD SHARING SYSTEM BILL A INTRODUCTION At the meeting of the Executive Council on 8 April 2014, the Council ADVISED and

File reference: FH CR 1/1/3781/10 LEGISLATIVE COUNCIL BRIEF ELECTRONIC HEALTH RECORD SHARING SYSTEM BILL A INTRODUCTION At the meeting of the Executive Council on 8 April 2014, the Council ADVISED and

Corporation tax: research and development tax credits: consumables

Corporation tax: research and development tax credits: consumables Who is likely to be affected? Companies carrying out research and development (R&D) activities. General description of the measure The

Corporation tax: research and development tax credits: consumables Who is likely to be affected? Companies carrying out research and development (R&D) activities. General description of the measure The

Employee shareholder status: capital gains tax exemption

Employee shareholder status: capital gains tax exemption Who is likely to be affected? Individuals who have taken up the 'employee shareholder employment status and have capital gains. General description

Employee shareholder status: capital gains tax exemption Who is likely to be affected? Individuals who have taken up the 'employee shareholder employment status and have capital gains. General description

ITEM FOR FINANCE COMMITTEE

For discussion on 7 December 2012 FCR(2012-13)59 ITEM FOR FINANCE COMMITTEE HEAD 94 LEGAL AID DEPARTMENT Subhead 700 General non-recurrent New Item Injection into the Supplementary Legal Aid Fund Members

For discussion on 7 December 2012 FCR(2012-13)59 ITEM FOR FINANCE COMMITTEE HEAD 94 LEGAL AID DEPARTMENT Subhead 700 General non-recurrent New Item Injection into the Supplementary Legal Aid Fund Members

Legislative Council Secretariat FACT SHEET. Major sources of Government revenue

FACT SHEET Major sources of Government 1. Sources of Government 1.1 Government is the aggregate of operating 1 and capital 2. In the Financial Year ("FY") 2012-2013, the Government amounted to HK$442.2

FACT SHEET Major sources of Government 1. Sources of Government 1.1 Government is the aggregate of operating 1 and capital 2. In the Financial Year ("FY") 2012-2013, the Government amounted to HK$442.2

How To Regulate Genetically Modified Organisms

File Ref : EPD CR 9/15/26 Pt. 5 LEGISLATIVE COUNCIL BRIEF Genetically Modified Organisms (Control of Release) Ordinance GENETICALLY MODIFIED ORGANISMS (DOCUMENTATION FOR IMPORT AND EXPORT) REGULATION INTRODUCTION

File Ref : EPD CR 9/15/26 Pt. 5 LEGISLATIVE COUNCIL BRIEF Genetically Modified Organisms (Control of Release) Ordinance GENETICALLY MODIFIED ORGANISMS (DOCUMENTATION FOR IMPORT AND EXPORT) REGULATION INTRODUCTION

The phasing out of standard income tax on employees (SITE)

") The phasing out of standard income tax on employees (SITE) 1. Introduction 1 March 2011 saw the start of the phasing out of Standard Income Tax on Employees (SITE). SITE taxpayers who received more than

The phasing out of standard income tax on employees (SITE) 1. Introduction 1 March 2011 saw the start of the phasing out of Standard Income Tax on Employees (SITE). SITE taxpayers who received more than

LEGISLATIVE COUNCIL BRIEF

File Ref.: ENB CR 4/2061/08 LEGISLATIVE COUNCIL BRIEF District Cooling Services Bill INTRODUCTION A At the meeting of the Executive Council on 26 August 2014, the Council ADVISED and the Chief Executive

File Ref.: ENB CR 4/2061/08 LEGISLATIVE COUNCIL BRIEF District Cooling Services Bill INTRODUCTION A At the meeting of the Executive Council on 26 August 2014, the Council ADVISED and the Chief Executive

LEGISLATIVE COUNCIL BRIEF. Clearing and Settlement Systems (Amendment) Bill 2015

Bill 2015") File Ref: B&M/2/1/20C LEGISLATIVE COUNCIL BRIEF Clearing and Settlement Systems Ordinance (Chapter 584) Clearing and Settlement Systems (Amendment) Bill 2015 INTRODUCTION At the meeting of the Executive

File Ref: B&M/2/1/20C LEGISLATIVE COUNCIL BRIEF Clearing and Settlement Systems Ordinance (Chapter 584) Clearing and Settlement Systems (Amendment) Bill 2015 INTRODUCTION At the meeting of the Executive

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES. Suggested Answers

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : June 2007 The suggested answers are published for the purpose of assisting students

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : June 2007 The suggested answers are published for the purpose of assisting students

Bank levy amendments. Detailed proposal. Who is likely to be affected? General description of the measure. Policy objective. Background to the measure

Bank levy amendments Who is likely to be affected? UK banks, banking groups and building societies; foreign banking groups operating in the UK through permanent establishments or subsidiaries; and UK banks

Bank levy amendments Who is likely to be affected? UK banks, banking groups and building societies; foreign banking groups operating in the UK through permanent establishments or subsidiaries; and UK banks

Capital gains tax private residence relief final period exemption

Capital gains tax private residence relief final period exemption Who is likely to be affected? Individuals who own one or more properties that they have lived in as their main residence at any time. General

Capital gains tax private residence relief final period exemption Who is likely to be affected? Individuals who own one or more properties that they have lived in as their main residence at any time. General

Survivor and death benefits

Survivor and death benefits January 2011 The Teachers Pension Scheme (TPS) provides important benefits which may be paid to your beneficiaries after your death. within 2 years of TP becoming aware of the

Survivor and death benefits January 2011 The Teachers Pension Scheme (TPS) provides important benefits which may be paid to your beneficiaries after your death. within 2 years of TP becoming aware of the

A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2014-2015

INFORMATION PAMPHLET A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2014-2015 INLAND REVENUE DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION A BRIEF GUIDE

INFORMATION PAMPHLET A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2014-2015 INLAND REVENUE DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION A BRIEF GUIDE

Southern State Superannuation (Insurance) Variation Regulations 2008

Variation Regulations 2008") No 310 of 2008 published in Gazette 18.12.2008 p 5671 South Australia Southern State Superannuation (Insurance) Variation Regulations 2008 under the Southern State Superannuation Act 1994 Contents Part

No 310 of 2008 published in Gazette 18.12.2008 p 5671 South Australia Southern State Superannuation (Insurance) Variation Regulations 2008 under the Southern State Superannuation Act 1994 Contents Part

Legislative Council Panel on Financial Affairs. Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

CB(1)870/14-15(04) For discussion on 1 June 2015 Legislative Council Panel on Financial Affairs Proposal to Attract Enterprises to Establish Corporate Treasury Centres in Hong Kong PURPOSE In his 2015-16

立 法 會. Legislative Council. Paper for the House Committee Meeting on 11 March 2016

立 法 會 Legislative Council Paper for the House Committee Meeting on 11 March 2016 Legal Service Division Report on Medical Registration (Amendment) Bill 2016 LC Paper No. LS44/15-16 I. SUMMARY 1. The Bill

立 法 會 Legislative Council Paper for the House Committee Meeting on 11 March 2016 Legal Service Division Report on Medical Registration (Amendment) Bill 2016 LC Paper No. LS44/15-16 I. SUMMARY 1. The Bill

Financial Advisers (Amendment) Bill

Bill") Financial Advisers (Amendment) Bill Bill No. 15/2015. Read the first time on 11 May 2015. A BILL intituled An Act to amend the Financial Advisers Act (Chapter 110 of the 2007 Revised Edition). Be it enacted

Financial Advisers (Amendment) Bill Bill No. 15/2015. Read the first time on 11 May 2015. A BILL intituled An Act to amend the Financial Advisers Act (Chapter 110 of the 2007 Revised Edition). Be it enacted

Property Management Services Bill. Contents

C2717 Property Management Services Bill Contents Clause Page Part 1 Preliminary 1. Short title and commencement... C2727 2. Interpretation... C2727 3. Property management services... C2733 4. Disciplinary

C2717 Property Management Services Bill Contents Clause Page Part 1 Preliminary 1. Short title and commencement... C2727 2. Interpretation... C2727 3. Property management services... C2733 4. Disciplinary

Children s Television Programmes - Tax Relief For the producers

Children s television tax relief Who is likely to be affected? Companies within the charge to corporation tax that are directly involved in the production of children s television programmes. General description

Children s television tax relief Who is likely to be affected? Companies within the charge to corporation tax that are directly involved in the production of children s television programmes. General description

Venture capital trusts

Venture capital trusts Who is likely to be affected? This measure will affect individuals who invest in venture capital trusts (VCTs) and the VCTs in which they invest. General description of the measure

Venture capital trusts Who is likely to be affected? This measure will affect individuals who invest in venture capital trusts (VCTs) and the VCTs in which they invest. General description of the measure

PERSONAL DENTAL SERVICES STATEMENT OF FINANCIAL ENTITLEMENTS 2013

PERSONAL DENTAL SERVICES STATEMENT OF FINANCIAL ENTITLEMENTS 2013 1. Introduction TABLE OF CONTENTS PART 1 ANNUAL AGREEMENT VALUES 2. Negotiated Annual Agreement Values Nomination of first Negotiated Annual

PERSONAL DENTAL SERVICES STATEMENT OF FINANCIAL ENTITLEMENTS 2013 1. Introduction TABLE OF CONTENTS PART 1 ANNUAL AGREEMENT VALUES 2. Negotiated Annual Agreement Values Nomination of first Negotiated Annual

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998

EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998 These notes are issued for the information and

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 34 (REVISED) EXEMPTION FROM PROFITS TAX (INTEREST INCOME) ORDER 1998 These notes are issued for the information and

Trust Deed for National Provident Lump Sum Cash Accumulation Scheme

Trust Deed for National Provident Lump Sum Cash Accumulation Scheme as amended by Deeds of Amendment dated: 30 September 1991 29 May 1992 30 March 1993 21 July 1993 18 November 1993 21 December 1995 29

Trust Deed for National Provident Lump Sum Cash Accumulation Scheme as amended by Deeds of Amendment dated: 30 September 1991 29 May 1992 30 March 1993 21 July 1993 18 November 1993 21 December 1995 29

ON THE SOCIAL ASSISTANCE SCHEME IN KOSOVO

1 UNITED NATIONS United Nations Interim Administration Mission in Kosovo UNMIK NATIONS UNIES Mission d Administration Intérimaire des Nations Unies au Kosovo PROVISIONAL INSTITUTIONS OF SELF GOVERNMENT

1 UNITED NATIONS United Nations Interim Administration Mission in Kosovo UNMIK NATIONS UNIES Mission d Administration Intérimaire des Nations Unies au Kosovo PROVISIONAL INSTITUTIONS OF SELF GOVERNMENT

Employees Retirement Fund Plan Amendments

Employees Retirement Fund Plan Amendments An ordinance amending Chapter 40A of the Dallas City Code to revise certain provisions of the City of Dallas employees retirement fund plan to comply with federal

Employees Retirement Fund Plan Amendments An ordinance amending Chapter 40A of the Dallas City Code to revise certain provisions of the City of Dallas employees retirement fund plan to comply with federal

Double taxation relief: revenue protection

Double taxation relief: revenue protection Who is likely to be affected? Companies which make claims for double taxation relief (DTR) may be affected by this measure. General description of the measure

Double taxation relief: revenue protection Who is likely to be affected? Companies which make claims for double taxation relief (DTR) may be affected by this measure. General description of the measure

TAXATION OF INCOME FROM SALARY TAX YEAR 2015 (July 01, 14 TO June 30, 15)

") CIRCULAR NO. 18 OF (INCOME TAX) TAXATION OF INCOME FROM SALARY TAX YEAR 2015 (July 01, 14 TO June 30, 15) The Circular on taxation of Income Salary is being updated as under:- The Computation of Tax of

CIRCULAR NO. 18 OF (INCOME TAX) TAXATION OF INCOME FROM SALARY TAX YEAR 2015 (July 01, 14 TO June 30, 15) The Circular on taxation of Income Salary is being updated as under:- The Computation of Tax of

Improving the operation of the Construction Industry Scheme

Improving the operation of the Construction Industry Scheme Who is likely to be affected? Businesses and individuals who are subcontractors or contractors participating in the scheme. Also commercial third

Improving the operation of the Construction Industry Scheme Who is likely to be affected? Businesses and individuals who are subcontractors or contractors participating in the scheme. Also commercial third

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議. ACCA Hong Kong Budget Submission 2016/17

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議 ACCA Hong Kong Budget Submission 2016/17 EXECUTIVE SUMMARY... 1 PROPOSALS... 4 1 Business Enabling Environment... 4 1.1 One-Belt-One-Road Initiative... 4 1.1.1 Implementation

ACCA 香 港 分 會 2016/17 年 度 財 政 預 算 案 建 議 ACCA Hong Kong Budget Submission 2016/17 EXECUTIVE SUMMARY... 1 PROPOSALS... 4 1 Business Enabling Environment... 4 1.1 One-Belt-One-Road Initiative... 4 1.1.1 Implementation

Dated 29 February 2016. Flood Re Limited. Payments Dispute Process. Version 1.0

Dated 29 February 2016 Flood Re Limited Payments Dispute Process Version 1.0 1. General 1.1 The following provisions will apply to all disputes referred to and conducted under this Payments Dispute Resolution

Dated 29 February 2016 Flood Re Limited Payments Dispute Process Version 1.0 1. General 1.1 The following provisions will apply to all disputes referred to and conducted under this Payments Dispute Resolution

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 9 (REVISED) MAJOR DEDUCTIBLE ITEMS UNDER SALARIES TAX

MAJOR DEDUCTIBLE ITEMS UNDER SALARIES TAX") Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 9 (REVISED) MAJOR DEDUCTIBLE ITEMS UNDER SALARIES TAX These notes are issued for the information of taxpayers and

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 9 (REVISED) MAJOR DEDUCTIBLE ITEMS UNDER SALARIES TAX These notes are issued for the information of taxpayers and

Student Loan Scheme (Repayment Bonus) Amendment Act 2009

Amendment Act 2009") Student Loan Scheme (Repayment Bonus) Amendment Act 2009 Public Act 2009 No 33 Date of assent 22 September 2009 Commencement see section 2 Contents Page 1 Title 2 2 Commencement 2 3 Principal Act amended

Student Loan Scheme (Repayment Bonus) Amendment Act 2009 Public Act 2009 No 33 Date of assent 22 September 2009 Commencement see section 2 Contents Page 1 Title 2 2 Commencement 2 3 Principal Act amended

PLEASE NOTE. For more information concerning the history of these regulations, please see the Table of Regulations.

PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to November 7, 2009. It is intended for information and reference purposes

PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to November 7, 2009. It is intended for information and reference purposes

LC Paper No. CB(1)1313/04-05(01) (English version only)

1313/04-05(01) (English version only)") LC Paper No. CB(1)1313/04-05(01) (English version only) Bankruptcy:: The Maiin Processiing Stages Creditor s Petition A company or a person who is owed a sum of $10,000 or more by an individual or a firm

LC Paper No. CB(1)1313/04-05(01) (English version only) Bankruptcy:: The Maiin Processiing Stages Creditor s Petition A company or a person who is owed a sum of $10,000 or more by an individual or a firm

Briefing for Bills Committee

CB(1)504/12-13(01) Briefing for Bills Committee Inland Revenue and Stamp Duty Legislation (Alternative Bond Schemes) (Amendment) Bill 2012 1 Why developing Islamic finance? Among the fastest growing segments

CB(1)504/12-13(01) Briefing for Bills Committee Inland Revenue and Stamp Duty Legislation (Alternative Bond Schemes) (Amendment) Bill 2012 1 Why developing Islamic finance? Among the fastest growing segments

Additional Contribution Form. IWeb Share Dealing Self Invested Personal Pension

Additional Contribution Form IWeb Share Dealing Self Invested Personal Pension Additional Contribution Form This is an application form to pay an additional one-off contribution or establish a regular

Additional Contribution Form IWeb Share Dealing Self Invested Personal Pension Additional Contribution Form This is an application form to pay an additional one-off contribution or establish a regular

Title: Code for Dealing in Securities

GSK Policy Title: Code for Dealing in Securities Official Short Title: Code for Dealing in Securities Key Points No employee may deal in GlaxoSmithKline plc securities ( GSK securities ) if he or she is

GSK Policy Title: Code for Dealing in Securities Official Short Title: Code for Dealing in Securities Key Points No employee may deal in GlaxoSmithKline plc securities ( GSK securities ) if he or she is

香 港 特 別 行 政 區 政 府. The Government of the Hong Kong Special Administrative Region. Development Bureau Technical Circular (Works) No.

No.") 政 府 總 部 發 展 局 工 務 科 香 港 特 別 行 政 區 政 府 The Government of the Hong Kong Special Administrative Region Works Branch Development Bureau Government Secretariat 香 港 添 馬 添 美 道 2 號 政 府 總 部 西 翼 1 8 樓 18/F, West

政 府 總 部 發 展 局 工 務 科 香 港 特 別 行 政 區 政 府 The Government of the Hong Kong Special Administrative Region Works Branch Development Bureau Government Secretariat 香 港 添 馬 添 美 道 2 號 政 府 總 部 西 翼 1 8 樓 18/F, West

How To Get A Small Business License In Australia

1 L.R.O. 2007 Small Business Development CAP. 318C CHAPTER 318C SMALL BUSINESS DEVELOPMENT ARRANGEMENT OF SECTIONS SECTION 1. Short title. 2. Interpretation. 3. Small business. 4. Approved small business

1 L.R.O. 2007 Small Business Development CAP. 318C CHAPTER 318C SMALL BUSINESS DEVELOPMENT ARRANGEMENT OF SECTIONS SECTION 1. Short title. 2. Interpretation. 3. Small business. 4. Approved small business

Clarifications on Tax Compliance for Undisclosed Foreign Income and Assets

Circular No. 13 of 2015 F. No. 142/18/2015-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes (TPL Division) *** Dated 6 th of July, 2015 Clarifications on

Circular No. 13 of 2015 F. No. 142/18/2015-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes (TPL Division) *** Dated 6 th of July, 2015 Clarifications on

LEGAL PRACTITIONERS (AMENDMENT) ORDINANCE 2012 CONTENTS

ORDINANCE 2012 CONTENTS") LEGAL PRACTITIONERS (AMENDMENT) 2012 A2751 CONTENTS Section Page 1. Short title A2755 2. Commencement A2755 3. Section 2 amended (Interpretation) A2755 4. Section 6 amended (Practising certificates solicitors)

LEGAL PRACTITIONERS (AMENDMENT) 2012 A2751 CONTENTS Section Page 1. Short title A2755 2. Commencement A2755 3. Section 2 amended (Interpretation) A2755 4. Section 6 amended (Practising certificates solicitors)

Limits to tax relief and tax-free benefits

TAX LIMITS FINAL SALARY AND CAREER REVALUED BENEFITS SECTIONS Limits to tax relief and tax-free benefits Introduction Pension benefits earned by individuals in the UK, which qualify to receive tax relief,

TAX LIMITS FINAL SALARY AND CAREER REVALUED BENEFITS SECTIONS Limits to tax relief and tax-free benefits Introduction Pension benefits earned by individuals in the UK, which qualify to receive tax relief,

SSAS application form

SSAS application form By completing this form together with the Trust Deed you agree to appoint Bespoke Pension Management as Scheme Practitioner to your SSAS Scheme. You understand that we will assume

SSAS application form By completing this form together with the Trust Deed you agree to appoint Bespoke Pension Management as Scheme Practitioner to your SSAS Scheme. You understand that we will assume

Retirement and Death Benefit Scheme Rules

Retirement and Death Benefit Scheme Rules (2012 Rules) AEGON took advice from a firm of specialist pensions lawyers to produce these Rules. It is, however, the Trustees responsibility to ensure that these

Retirement and Death Benefit Scheme Rules (2012 Rules) AEGON took advice from a firm of specialist pensions lawyers to produce these Rules. It is, however, the Trustees responsibility to ensure that these

BEGA CHEESE LIMITED (ACN 008 358 503) SECURITY TRADING POLICY

SECURITY TRADING POLICY") 1.0 OBJECTIVES 1.1. The ordinary shares of Bega Cheese Limited (Bega Cheese) are listed on the ASX. 1.2. Definitions to assist in the interpretation of this policy are set out in clause 10.1 of this policy.

1.0 OBJECTIVES 1.1. The ordinary shares of Bega Cheese Limited (Bega Cheese) are listed on the ASX. 1.2. Definitions to assist in the interpretation of this policy are set out in clause 10.1 of this policy.

24 December 2010. Mr Wade Baggott Company Announcements Australian Securities Exchange Exchange Plaza Perth WA 6000. Dear Wade,

ABN 71 124 374 321 123B Colin Street, West Perth WA 6005 PO Box 708, West Perth WA 6872 Phone +61 8 9215 7600 Fax +61 8 9485 1283 24 December 2010 Mr Wade Baggott Company Announcements Australian Securities

ABN 71 124 374 321 123B Colin Street, West Perth WA 6005 PO Box 708, West Perth WA 6872 Phone +61 8 9215 7600 Fax +61 8 9485 1283 24 December 2010 Mr Wade Baggott Company Announcements Australian Securities

STAMP DUTY LAND TAX BILL

STAMP DUTY LAND TAX BILL DRAFT EXPLANATORY NOTES INTRODUCTION 1. These explanatory notes relate to the Stamp Duty Land Tax Bill as introduced into the House of Commons on 4 December 2014. They have been

STAMP DUTY LAND TAX BILL DRAFT EXPLANATORY NOTES INTRODUCTION 1. These explanatory notes relate to the Stamp Duty Land Tax Bill as introduced into the House of Commons on 4 December 2014. They have been

Guide to Profit Sharing Schemes

Guide to Profit Sharing Schemes PROFIT SHARING SCHEMES This booklet describes the provisions of Chapter 1 of Part 17, Taxes Consolidation Act, 1997 and Schedule 11 of that Act, incorporating all amendments

Guide to Profit Sharing Schemes PROFIT SHARING SCHEMES This booklet describes the provisions of Chapter 1 of Part 17, Taxes Consolidation Act, 1997 and Schedule 11 of that Act, incorporating all amendments

Deductibility of contributions for. employees and. self-employed persons

Deductibility of contributions for employees and self-employed persons Mandatory Provident Fund Scheme or Recognized Occupational Retirement Scheme Mandatory Provident Fund Scheme (MPFS) Employees (full-time

Deductibility of contributions for employees and self-employed persons Mandatory Provident Fund Scheme or Recognized Occupational Retirement Scheme Mandatory Provident Fund Scheme (MPFS) Employees (full-time

EXCEPTED UNREGISTERED TRUST DEED

DATED 2014 EXCEPTED UNREGISTERED TRUST DEED relating to NAME OF SCHEME: One Crown Court 66 Cheapside London EC2V 6LR www.pitmans.com Contents Clause Heading 1. General Interpretation and Definitions 2.

DATED 2014 EXCEPTED UNREGISTERED TRUST DEED relating to NAME OF SCHEME: One Crown Court 66 Cheapside London EC2V 6LR www.pitmans.com Contents Clause Heading 1. General Interpretation and Definitions 2.

DELHI ELECTRICITY REGULATORY COMMISSION VINIYAMAK BHAWAN, C-BLOCK, SHIVALIK, MALVIYA NAGAR, NEW DELHI-110017

DELHI ELECTRICITY REGULATORY COMMISSION VINIYAMAK BHAWAN, C-BLOCK, SHIVALIK, MALVIYA NAGAR, NEW DELHI-110017 Delhi Electricity Regulatory Commission invites applications from eligible candidates for filling

DELHI ELECTRICITY REGULATORY COMMISSION VINIYAMAK BHAWAN, C-BLOCK, SHIVALIK, MALVIYA NAGAR, NEW DELHI-110017 Delhi Electricity Regulatory Commission invites applications from eligible candidates for filling

Education Services for Overseas Students Act 2000

Education Services for Overseas Students Act 2000 Act No. 164 of 2000 as amended This compilation was prepared on 17 December 2008 taking into account amendments up to Act No. 144 of 2008 The text of any

Education Services for Overseas Students Act 2000 Act No. 164 of 2000 as amended This compilation was prepared on 17 December 2008 taking into account amendments up to Act No. 144 of 2008 The text of any

LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY. Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg.

Regulations (Cap. 60 sub. leg.") CB(1)278/06-07(06) For information On 21 November 2006 LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg. E) Introduction

CB(1)278/06-07(06) For information On 21 November 2006 LEGISLATIVE COUNCIL PANEL ON COMMERCE AND INDUSTRY Proposed amendments to the Import and Export (Registration) Regulations (Cap. 60 sub. leg. E) Introduction

CHAPTER 21 RETIREMENT ANNUITY CONTRACTS. Revised July, 2013

CHAPTER 21 RETIREMENT ANNUITY CONTRACTS Revised July, 2013 Introduction 21.1 The legislation governing retirement annuity contracts (RACs), often referred to as personal pensions, is contained in Sections

CHAPTER 21 RETIREMENT ANNUITY CONTRACTS Revised July, 2013 Introduction 21.1 The legislation governing retirement annuity contracts (RACs), often referred to as personal pensions, is contained in Sections

LEGISLATIVE COUNCIL BRIEF. Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

LEGISLATIVE COUNCIL BRIEF Resolution of the Legislative Council under Section 48A of the Employees Compensation Ordinance, Cap 282 Resolution of the Legislative Council under Section 40 of the Pneumoconiosis

2015 No. 1810 INCOME TAX. The Scottish Rate of Income Tax (Consequential Amendments) Order 2015

Order 2015") S T A T U T O R Y I N S T R U M E N T S 2015 No. 1810 INCOME TAX The Scottish Rate of Income Tax (Consequential Amendments) Order 2015 Made - - - - 20th October 2015 Coming into force in accordance with

S T A T U T O R Y I N S T R U M E N T S 2015 No. 1810 INCOME TAX The Scottish Rate of Income Tax (Consequential Amendments) Order 2015 Made - - - - 20th October 2015 Coming into force in accordance with

PERSONAL PENSION (TOP UP PLAN) APPLICATION TO INCREASE CONTRIBUTIONS FOR OFFICE USE ONLY. Agency Number

APPLICATION TO INCREASE CONTRIBUTIONS FOR OFFICE USE ONLY. Agency Number") PERSONAL PENSION (TOP UP PLAN) APPLICATION TO INCREASE CONTRIBUTIONS Agency Number FOR OFFICE USE ONLY Arranged by: Application to increase contributions Did your adviser give you advice in respect of

PERSONAL PENSION (TOP UP PLAN) APPLICATION TO INCREASE CONTRIBUTIONS Agency Number FOR OFFICE USE ONLY Arranged by: Application to increase contributions Did your adviser give you advice in respect of

LEGISLATIVE COUNCIL PANEL ON PLANNING, LANDS AND WORKS. Interest Rates for Provisional Payment, Redemption Money

For discussion on 21 November 2000 LEGISLATIVE COUNCIL PANEL ON PLANNING, LANDS AND WORKS Interest Rates for Provisional Payment, Redemption Money and Compensation Payable under Various s INTRODUCTION

For discussion on 21 November 2000 LEGISLATIVE COUNCIL PANEL ON PLANNING, LANDS AND WORKS Interest Rates for Provisional Payment, Redemption Money and Compensation Payable under Various s INTRODUCTION

Securities trading policy

Securities trading policy Corporate Travel Management Limited ACN 131 207 611 Level 11 Central Plaza Two 66 Eagle Street Brisbane QLD 4000 GPO Box 1855 Brisbane QLD 4001 Australia ABN 42 721 345 951 Telephone

Securities trading policy Corporate Travel Management Limited ACN 131 207 611 Level 11 Central Plaza Two 66 Eagle Street Brisbane QLD 4000 GPO Box 1855 Brisbane QLD 4001 Australia ABN 42 721 345 951 Telephone

PAPER IIC HONG KONG OPTION

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2008 PAPER IIC HONG KONG OPTION ADVANCED INTERNATIONAL TAXATION TIME ALLOWED 3¼ HOURS You should answer FOUR out of seven questions. Each question carries

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2008 PAPER IIC HONG KONG OPTION ADVANCED INTERNATIONAL TAXATION TIME ALLOWED 3¼ HOURS You should answer FOUR out of seven questions. Each question carries

LEGISLATIVE COUNCIL BRIEF. Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) BILL 2014

INSURANCE COMPANIES (AMENDMENT) BILL 2014") File Ref: C2/2/50C LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) BILL 2014 A INTRODUCTION At the meeting of the Executive Council on 8 April 2014,

File Ref: C2/2/50C LEGISLATIVE COUNCIL BRIEF Insurance Companies Ordinance (Chapter 41) INSURANCE COMPANIES (AMENDMENT) BILL 2014 A INTRODUCTION At the meeting of the Executive Council on 8 April 2014,

PUBLIC SERVICE ACT 2005. An Act to make provision in respect of the public service of Lesotho and for related matters. PART I - PRELIMINARY

PUBLIC SERVICE ACT 2005 An Act to make provision in respect of the public service of Lesotho and for related matters. Enacted by the Parliament of Lesotho Short title and commencement PART I - PRELIMINARY

PUBLIC SERVICE ACT 2005 An Act to make provision in respect of the public service of Lesotho and for related matters. Enacted by the Parliament of Lesotho Short title and commencement PART I - PRELIMINARY

ARTICLE I Tax Relief for the Elderly

Proposed Amendment to Ordinance on Tax Relief: Chapter 57, Article I of the New Canaan Code is hereby amended as follows. Deletions are marked by strikeouts, and new language is marked by underlined italics.

Proposed Amendment to Ordinance on Tax Relief: Chapter 57, Article I of the New Canaan Code is hereby amended as follows. Deletions are marked by strikeouts, and new language is marked by underlined italics.

Hawaii Individual Income Tax Statistics

Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii November 2014 Prepared

Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii Hawaii Individual Income Tax Statistics Tax Year 2012 Department of Taxation State of Hawaii November 2014 Prepared

Manchester City Council. Revised Local Council Tax Support Scheme 2014. effective as uprated from 1 April 2015

Manchester City Council Revised Local Council Tax Support Scheme 2014 effective as uprated from 1 April 2015 1 Introduction The Welfare Reform Act 2012 abolished Council Tax Benefit and the Local Government

Manchester City Council Revised Local Council Tax Support Scheme 2014 effective as uprated from 1 April 2015 1 Introduction The Welfare Reform Act 2012 abolished Council Tax Benefit and the Local Government

Companies (Amendment) Bill

Bill") Bill No. 25/2014. Companies (Amendment) Bill Read the first time on 8 September 2014. A BILL intituled An Act to amend the Companies Act (Chapter 50 of the 2006 Revised Edition), and to make consequential

Bill No. 25/2014. Companies (Amendment) Bill Read the first time on 8 September 2014. A BILL intituled An Act to amend the Companies Act (Chapter 50 of the 2006 Revised Edition), and to make consequential

AS TABLED IN THE HOUSE OF ASSEMBLY

AS TABLED IN THE HOUSE OF ASSEMBLY A BILL entitled INSURANCE AMENDMENT ACT 2014 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 Citation Inserts section 15A Amends section 17A Amends section 30JA Amends

AS TABLED IN THE HOUSE OF ASSEMBLY A BILL entitled INSURANCE AMENDMENT ACT 2014 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 Citation Inserts section 15A Amends section 17A Amends section 30JA Amends

Limits to tax relief and tax-free benefits

TAX LIMITS FINAL SALARY AND CAREER REVALUED BENEFITS SECTIONS Limits to tax relief and tax-free benefits Introduction Pension benefits earned by individuals in the UK which qualify to receive tax relief

TAX LIMITS FINAL SALARY AND CAREER REVALUED BENEFITS SECTIONS Limits to tax relief and tax-free benefits Introduction Pension benefits earned by individuals in the UK which qualify to receive tax relief

In this policy: AASB124 means the Australian Accounting Standards Board 124 December 2012 including its subsequent replacements.

1 Definitions In this policy: AASB124 means the Australian Accounting Standards Board 124 December 2012 including its subsequent replacements. ASX Board Chair Company Secretary Corporations Act Director

1 Definitions In this policy: AASB124 means the Australian Accounting Standards Board 124 December 2012 including its subsequent replacements. ASX Board Chair Company Secretary Corporations Act Director

Partnerships review: limited liability partnerships: treatment of salaried members

Partnerships review: limited liability partnerships: treatment of salaried members Who is likely to be affected? Individual members of a limited liability partnership (LLP) who work for the LLP on terms

Partnerships review: limited liability partnerships: treatment of salaried members Who is likely to be affected? Individual members of a limited liability partnership (LLP) who work for the LLP on terms

UCC Supplementary Life Assurance Scheme Member s Booklet

UCC Supplementary Life Assurance Scheme Member s Booklet Sub-Title taking care of you... Introduction University College Cork (UCC) has established the UCC Supplementary Life Assurance Scheme (the Scheme)

UCC Supplementary Life Assurance Scheme Member s Booklet Sub-Title taking care of you... Introduction University College Cork (UCC) has established the UCC Supplementary Life Assurance Scheme (the Scheme)

GDC 1970 Pension and Life Assurance Plan

Item 12 Council 5 December 2013 GDC 1970 Pension and Life Assurance Plan Purpose of paper Action Public/Private Corporate Strategy 2013-15 Business Plan 2013 Decision Trail Recommendations Authorship of

Item 12 Council 5 December 2013 GDC 1970 Pension and Life Assurance Plan Purpose of paper Action Public/Private Corporate Strategy 2013-15 Business Plan 2013 Decision Trail Recommendations Authorship of

Human Resources. Employee Payroll FAQ

Human Resources RESOURCE DOCUMENT - V1. 2014 PAGE 1 OF 10 FAQ Index 1. What should I do if I am commencing employment in Ireland for the first time? 2. What should I do if I am moving employment? 3. What

Human Resources RESOURCE DOCUMENT - V1. 2014 PAGE 1 OF 10 FAQ Index 1. What should I do if I am commencing employment in Ireland for the first time? 2. What should I do if I am moving employment? 3. What

Case 1:08-cv-00361-WMS-HKS Document 234 Filed 05/01/13 Page 1 of 17

Case 1:08-cv-00361-WMS-HKS Document 234 Filed 05/01/13 Page 1 of 17 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF NEW YORK SECURITIES AND EXCHANGE COMMISSION, Plaintiff, 08 CV 361S v. WATERMARK FINANCIAL

Case 1:08-cv-00361-WMS-HKS Document 234 Filed 05/01/13 Page 1 of 17 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF NEW YORK SECURITIES AND EXCHANGE COMMISSION, Plaintiff, 08 CV 361S v. WATERMARK FINANCIAL

Legislative Council Panel on Financial Affairs

For information Legislative Council Panel on Financial Affairs Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Amendment of Schedule 2) Notice 2015 PURPOSE This

For information Legislative Council Panel on Financial Affairs Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Amendment of Schedule 2) Notice 2015 PURPOSE This

European Central Bank

This version of the ECB Pension Scheme rules has been produced for members of staff who take up employment with the ECB on or after 1 June 2009. European Central Bank Conditions of Employment for Staff

This version of the ECB Pension Scheme rules has been produced for members of staff who take up employment with the ECB on or after 1 June 2009. European Central Bank Conditions of Employment for Staff

The Financial Secretary, Mr. John Tsang, delivered the 2014-15 Budget Speech at the Legislative Council on 26 February 2014.

February 2014 THE 2014-15 BUDGET The Financial Secretary, Mr. John Tsang, delivered the 2014-15 Budget Speech at the Legislative Council on 26 February 2014. In this Tax Flash, we set out a summary of

February 2014 THE 2014-15 BUDGET The Financial Secretary, Mr. John Tsang, delivered the 2014-15 Budget Speech at the Legislative Council on 26 February 2014. In this Tax Flash, we set out a summary of

Payroll Tax Rebate Scheme (Jobs Action Plan) Amendment (Fresh Start Support) Act 2014 No 78

Amendment (Fresh Start Support) Act 2014 No 78") New South Wales Payroll Tax Rebate Scheme (Jobs Action Plan) Amendment (Fresh Start Support) Act 2014 No 78 Contents 1 Name of Act 2 2 Commencement 2 Schedule 1 Amendment of Payroll Tax Rebate Scheme (Jobs

New South Wales Payroll Tax Rebate Scheme (Jobs Action Plan) Amendment (Fresh Start Support) Act 2014 No 78 Contents 1 Name of Act 2 2 Commencement 2 Schedule 1 Amendment of Payroll Tax Rebate Scheme (Jobs

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

STAKEHOLDER PENSION SCHEME (UK, N+ & Global staff) A Guide to the Stakeholder Pension Scheme

A Guide to the Stakeholder Pension Scheme") STAKEHOLDER PENSION SCHEME (UK, N+ & Global staff) A Guide to the Stakeholder Pension Scheme The Stakeholder scheme is a money purchase scheme - this means it does not offer guaranteed benefits related

STAKEHOLDER PENSION SCHEME (UK, N+ & Global staff) A Guide to the Stakeholder Pension Scheme The Stakeholder scheme is a money purchase scheme - this means it does not offer guaranteed benefits related

Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap)

") Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap) Who is likely to be affected? Large groups of companies that are subject to the debt cap. General description of the measure This

Amendments to the Tax Treatment of Financing Costs and Income (Debt Cap) Who is likely to be affected? Large groups of companies that are subject to the debt cap. General description of the measure This

[8.3.8] Relief for interest paid on certain home loans. Section 244, 244A and 245 TCA 1997

![[8.3.8] Relief for interest paid on certain home loans. Section 244, 244A and 245 TCA 1997](/thumbs/26/7500772.jpg "[8.3.8] Relief for interest paid on certain home loans. Section 244, 244A and 245 TCA 1997") Last updated February 2015 [8.3.8] Relief for interest paid on certain home loans Section 244, 244A and 245 TCA 1997 The purpose of this instruction is to set out the rules, guidelines and procedures regarding

Last updated February 2015 [8.3.8] Relief for interest paid on certain home loans Section 244, 244A and 245 TCA 1997 The purpose of this instruction is to set out the rules, guidelines and procedures regarding

Legislative Council Panel on Administration of Justice and Legal Services. Further Expansion of the Supplementary Legal Aid Scheme

LC Paper No. CB(2)600/11-12(01) For discussion on 20 December 2011 Legislative Council Panel on Administration of Justice and Legal Services Further Expansion of the Supplementary Legal Aid Scheme PURPOSE

LC Paper No. CB(2)600/11-12(01) For discussion on 20 December 2011 Legislative Council Panel on Administration of Justice and Legal Services Further Expansion of the Supplementary Legal Aid Scheme PURPOSE