FUTURE OF ENERGY & INVESTMENTS IN GAS NETWORKS PHASE 2 - CONSUMER WILLINGNESS TO PAY FOR ALTERNATIVE HEATING SOURCES

|

|

|

- Mitchell Pierce

- 7 years ago

- Views:

Transcription

1 FUTURE OF ENERGY & INVESTMENTS IN GAS NETWORKS PHASE 2 - CONSUMER WILLINGNESS TO PAY FOR ALTERNATIVE HEATING SOURCES 1 Final Report - August 2015

2 Contents 1. EXECUTIVE SUMMARY Introduction & Background Purpose, Major Finding & Conclusion Phase Purpose Major Finding & Conclusion FINDINGS Understanding when the consumer s decision is made and why? Changing Heating Sources - Consumer Cyclical Change Pattern Understanding how the decision to change systems may be made now and into the future? Current Consumer(s) Decisions in Year Future Consumer(s) Decisions by Year Understanding what support consumers need? Understanding what influences the consumer s decision to change to a replacement system? Current - What Influences the consumers decision? Future What factors may influence the consumer s decision going forward? Understanding the consumer s ability to be able to pay for changes to heating systems Understanding which efficient heating systems/energy sources homeowners find most (and least) attractive? Understanding why changes by consumers can be driven by external influences Legislation Technological Changes Financial Incentives to motivate change to more environmentally friendly solutions Willingness to change Heating Systems/Energy Sources - Understanding actual changes made by UK Consumers (May 2015) Sample Theory on Willingness to change to Alternative Heating Systems/Energy Sources Actual Statistical Changes to Alternative Heating Systems/Energy Sources Domestic Consumers Changing to Solar Panels Wadebridge Conclusion, Recommendations & Next Steps References APPENDICES Sample Population Mapping of the different categorisation of different consumer type(s)

3 Figure 1 Categorisation of Cohorts of Consumer Types... 7 Figure 2 Bridgend (East) Mapping of Cohorts of Consumer Types... 7 Figure 3 Cyclical Change Pattern Heating Systems 1 in 20 years... 9 Figure 4 Typical Successful Gas Infill Sites - Consumers Changing Heating System Patterns (Over 20 years) Figure 5 Decision Tree Analysis -Energy Source Changeover -Willingness to Pay Figure 6 Gas Infill Projects - Local Authority Influence - 10 Year Period ( ) Figure 7 Gas In fill Projects - Local Authority Influence - 2 year period ( ) Figure 8 Gross Disposable Household Incomes (GDHI) - Bridgend Comparison with other locations Figure 9 Chew Valley Infill Project Map Figure 10 Actual Numbers of Domestic Consumers with Accredited Alternative Systems Up to May Report By: Chris Clarke, Director of Asset Management and H, S & E, Wales & West Utilities. Steve Harding, Asset Manager, Wales & West Utilities Roy Leach, Director, Business Navigators Ltd. John Wych, Director, Business Navigators Ltd. 3

- Bridgend Comparison with other locations... 19 Figure 9 Chew Valley Infill Project Map.")

4 1. EXECUTIVE SUMMARY 1.1 Introduction & Background Research has been undertaken into the future need for gas networks in Bridgend, South Wales, in Phase 1 - FUTURE OF ENERGY & INVESTMENTS IN GAS NETWORKS - A REVIEW OF 4 AREAS IN BRIDGEND, SOUTH WALES (May 2015). The Phase 1 report confirmed the need for investment in future gas networks; and also highlighted the need for further research to be undertaken into consumer willingness to pay for investment in changing heating energy sources e.g. Heat Networks (HNs), Air Source Heat Pumps (ASHP). This is now the focus of this Phase 2 research. 1.2 Purpose, Major Finding & Conclusion Phase Purpose The primary purpose of this Phase 2 review, is to understand consumer willingness to change and to pay, in Bridgend, which is a typical town (and other locations), in relation to changing energy sources. This includes assessing likely consumer responses to various payment levels and over what payback periods, and what criteria e.g. incentives which might be needed to influence consumers, to pay for alternative heating systems e.g. heating networks, Air Source Heat Pumps (ASHP). Previous research has assumed consumers will change, but not identified if they would and under what circumstances i.e. top down assumptions. This will be undertaken by reviewing previous research and by undertaking additional research, including reviewing a number of real energy source switching projects ( Gas Infill Projects ), which have previously offered domestic consumers alternative heating and cooking i.e. by providing gas supplies to new areas in Wales and the South West of England. These Gas Infill Projects were offered to consumers to change their previous energy heating sources i.e. switching from other energy sources e.g. coal, bottle gas, electricity and oil; to mains gas, supplied from constructing a new gas network in their specific area. Historically, the Gas Infill Projects reviewed in this research cover the 25 year period, and offer a unique insight into consumer attitudes and potential barriers to change which can then be used going forward. Whilst the focus of this research is on Bridgend, South Wales, and the South West of England, historically Gas Infill Projects have been undertaken across the UK and this learning can be applied in other areas Major Finding & Conclusion The major finding(s) from this research into previous Gas Infill Projects and other research, is that the economic/financial constraint (the cost(s) to the domestic gas consumer) aligned with the consumers desire (behaviour) and/or ability to invest and pay; are the major barrier to changes for all domestic consumers. e.g. in the case of Gas Infill Projects, the contribution to the capital cost of the construction of the gas network and the costs of a new gas central heating system. This research has categorised clusters of consumers into certain cohorts using a bottom up approach and identified that there is no one size fits all solution. For example different financial solutions are required between domestic and non-domestic consumers. Equally, different financial solutions are needed for different cohorts within these two main categories of energy users. For example, comparing consumers living in social housing compared with consumers who own their property. For non-domestic consumers e.g. businesses, restaurants, schools, hospitals, etc. there would need to be a robust commercial business case to influence them to change and invest. This also varies depending upon any funding which may be available 4

5 A key finding is that the majority of domestic consumers (87%) will not change their existing heating provision unless significant financial benefits will be accrued, and only then if they have funding available, i.e. readily available cash to replace a heating system or low cost loans, and only if the system is coming close to the end of its cost effective life cycle and/or actually fails. Without these potential failure signs, then consumers would simply opt to do nothing. If their current system was operating well and providing heat for their homes they would not change their heating systems and spend money unnecessarily. One way of influencing consumers is by providing financial incentives to motivate them to change to alternative heating systems. Different types of consumers are highly likely to have different motivators to change. For example, domestic consumers need the heating system for the fundamental need for warmth and comfort, for reliability and for lower energy costs; whereas non-domestic consumers may be motivated to change based more on a commercially viable business decision. Different types of domestic and non-domestic consumer have been examined and the hypothesis of installing an alternative heating system e.g. a communal heating network and internal heating system has been considered. We have assumed that the likely investment in such a system would be significant for consumers and would be invested upfront (Year 0). A reasonable assessment was then made of how each type of consumer may make a decision based on the different payback periods for the consumer to break even on their investment. The hypothesis assumes the consumer would need two key economic benefits. 1) Financial incentives to change 2) Savings from reduced energy usage and costs from a communal heating network. In conclusion of this research summary, there is one Primary Critical Success Factors (CSF) and several secondary CSF s which are, and will be needed, in order to influence a cross section of domestic and non-domestic consumers to change heating systems to move to more environmentally energy saving solutions e.g. communal heating networks, Air Source Heat Pumps (ASHP). Going forward, this economic/financial constraint is one of the major challenges to overcome for domestic consumers (householders) and non-domestic consumers (private landlords; social housing associations, business consumers etc.) when considering changing to lower carbon heating systems. Primary CSF - Economic/Financial From this research there is no doubt, that there needs to be a very strong financial case of savings in both a) significant financial incentives which provide payback in reasonable time periods b) future energy bills and additionally i.e. it is highly likely that incentives will be needed to achieve break even within 0-5 years for the significant majority of domestic and non-domestic consumers. For successful Gas Infill Projects, for over 30 years, a Critical Success Factor has been that the initial investment in constructing the new gas networks in these areas, and the financial risk associated with that initial investment, is being made, underwritten and supported by the Gas Network undertaking the construction of the new gas network. Currently WWU, in South Wales and the South West of England. For example, 1.7 million for a recent (2014) Gas Infill Project in Rhewl Mostyn, Flintshire, Wales for 425 plus properties. Clearly, if other alternative heating networks s e.g. Communal Heating Networks were to be constructed, then the investment and the inherent risks associated with that investment would need to be funded, underwritten and supported somehow? Another Critical Success Factor on recent successful Gas Infill Projects has been that additional and separate funding has been provided for Fuel Poor Areas. The current Renewable Heating Incentive (RHI) is not motivating large numbers of domestic consumers to change to green heating systems/energy sources; significantly less than 1% of UK Dwellings/Consumers have taken up the opportunity with accredited installations in their homes. DECC Non Domestic RHI and Domestic RHI Monthly Deployment Numbers 9th April, May, 2015 (May 2015) Secondary CSF - Reliability & Sustainability Consumers will need to be convinced that replacement systems e.g. communal heating networks are reliable, readily available when heat is needed, provide minimum hassle to install and operate, and are long term sustainable solutions. Secondary CSF - Expertise & Support - Many homeowners (over 80%) rely very heavily on outside expertise, advice and support to change their heating systems. This support is needed to enable them to make the decision and to influence them to change. In the case of Gas Infill Projects and Social Housing, the most successful change 5

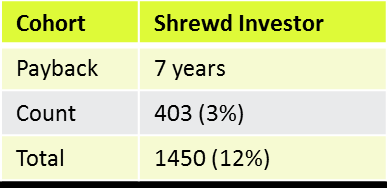

6 programmes occur when they have significant funding, but also of critical importance is when they are driven and supported by Local Authorities (LA s) and Social Housing Associations/Landlords. When there is then a commitment from a critical mass of social housing dwellings, private homeowners within the same area can and do benefit from being within the same cost effective Gas Infill Project. Secondary CSF Environmentally Friendly Drivers - Interestingly, from previous consumer research less than 25% of consumers, would be encouraged to change simply by more environmentally friendly heating systems. (DECC, Ipsos Mori, EST). However, this and other research into practical and real examples of recent (2015) opportunities to change, for example, consumers changing to green electricity tariffs, the actual numbers who have changed in reality is significantly lower at only 0.36% of people who have switched tariffs have actually gone green. (http.blog.moneysavingexpert.com/2014/11/04/green-energy-is-surprisingly-unpopular/) In summary, this research has uniquely categorised clusters of domestic and consumers into different cohorts respectively. A sample of domestic (11071) and non domestic (1090) consumers from Bridgend (East), South Wales were considered and assumptions made. These are analysed in Figure 1 below Categorisation of Cohorts of Consumer Types and mapped to Bridgend (East) in Figure 2 below Bridgend (East) Mapping of Cohorts of Consumer Types. End User Consumers with minimal resources and who cannot borrow money - Will not change because they have no financial means to change. Consumer/Investors who will need significantly high incentives to encourage them to change 3 Year Breakeven. Business Consumer e.g. retail outlet 5 Year Breakeven. Comparator - With the current Renewable Heating Incentive (RHI) Period Shrewd Investor with cash; Stable business 7 Year Break even Consumers with minimal if any resources, including consumers who do not own dwellings and rent from private landlords. Also, consumers who would have very poor credit ratings and would not be able to borrow money at reasonable interest rates. This includes, but is not limited to, consumers designated as fuel poor under current UK Policy (2015), who are living in private rented accommodation. It would be highly unlikely that this group of consumers would ever be able to change. If you have no money to invest then payback periods become irrelevant. An estimated one third (33%) 3986 consumers from the total sample population of domestic and non domestic consumers of in Bridgend (East), South Wales are assumed to be in this category. If an extremely high incentive of energy saved was offered, which provides for a break even in 3 years, the normal consumer, with the finances available, would be highly likely to invest to obtain a very quick commercial return on that investment and also to enhance the capital value of their property. An estimated one third (48%) 5805 of domestic and non domestic consumers from the total sample population of in Bridgend (East) South Wales, are assumed to be in this category. If a high incentive was offered, providing a break even in 5 years, the business consumer e.g. retail outlet; would be likely to invest to obtain a commercial return on investment in a reasonable commercial period. The investment would be made on a commercial basis and would need to provide a better return than other investment e.g. other business investments which would provide cost reductions or investments to expand sales or production. An estimated (8%) 921 of domestic and non domestic consumers from the total sample population of in Bridgend (East) South Wales, are assumed to be in this category. The current (June 2015) highest RHI incentive offered is (p/kwh) of energy saved (electricity p/kwh). This is for Solar Thermal at a comparative investment of not greater than 10,000 (2015 prices). An incentive would need to be offered which is comparable with, or better than, the current RHI Incentive which is currently (in 2015) provided for 7 years. An estimated (3%) 403 of domestic and non-domestic consumers from the total sample population of in Bridgend (East) South Wales, are assumed to be in this category. 6

7 Social Housing/Housing Association Landlord(s) 10 year break even. Long Term Investors Public Sector Buildings e.g. library, doctor's surgery for public consumers year break even. Social Housing Landlords maintaining the ongoing capital value of their housing stock, within a year cycle for heating systems, e.g. typically 12 years in Bridgend; they may be influenced to invest with a payback of 10 years. If additional Fuel Poor funding was also available for eligible consumers within this Social Housing population, this would then become even more financially attractive to Social Housing Landlords. This would enable householders/dwellings to be removed from Fuel Poverty as soon as the investment is made in year 1. An estimated (8%) 937 of domestic and non domestic consumers from the total sample population of in Bridgend (East) South Wales, are assumed to be in this category. The longer term investor maintaining the longer term value of say, a public building within a year property cycle, may be influenced to invest with a payback of 15 years. An estimated (1%) 110 of domestic and non domestic consumers from the total sample population of in Bridgend (East) South Wales, are assumed to be in this category. Figure 1 Categorisation of Cohorts of Consumer Types In summary of Figure 1, significant incentives would need to be offered to provide different categories of consumers with a return on their investment within reasonable periods for each cohort of consumers, ranging from 3 15 year break even scenarios, see below. Given the assumptions made, the sample of domestic (11071) and non domestic (1090) consumers, are mapped below within Bridgend (East), South Wales. For the detailed maps, please see Appendix 5.1. Figure 2 Bridgend (East) Mapping of Cohorts of Consumer Types 7

8 In reviewing the above figures 1 & 2, you will note: The majority (81%) are domestic consumers from two major categories i.e. Consumers with minimal resources and who cannot borrow money, who will not change because they have no financial means to change (33%); plus Consumer/Investors who will need significantly high incentives to encourage them to change with a rapid 3 Year payback period to break even on their investment. There are small clusters of Social Housing/Housing Association Landlord(s). These landlords would need to be encouraged to invest to maintain the ongoing capital value of their housing stock. This cluster represents an estimated (8%) 937 of the total sample population. The remaining consumers (9%) are non domestic i.e. commercial businesses and public sector libraries, offices etc. Further research is needed into the total Costs & Benefits for the different clusters of consumers from the sample of domestic (11071) and non domestic (1090) consumers, which are mapped above within Bridgend (East), South Wales. 2. FINDINGS 2.1 Understanding when the consumer s decision is made and why? Previous research has identified that the majority of consumers (67% plus) primarily replace their existing heating systems through necessity e.g. if it is becoming uneconomic to repair. Significantly, without breakdowns and/or increasing costs of repairs to their existing systems, the majority of consumers would simply opt to do nothing. However, once this expert advice was accepted i.e. that their individual central heating systems might fail and they could be without heat; then the majority 68% of consumers had replaced their existing heating systems within 12 months. (DECC, Ipsos Mori, EST) This is supported by the experience gained from our current research into previous Gas Infill Projects, even when the economic and financial benefits of switching to a new mains gas supply are made very obvious to consumers; the vast majority (over 70%) opt to do nothing initially; do not consider investing in a new gas system to be a priority for their limited resources; and are very reluctant to change unless their existing heating provision is coming close to the end of its cost effective life cycle and/or actually fails. For existing dwellings on the gas network, when existing systems need changing 80% of gas consumers prefer gas condensing boilers as their preferred form of heating (DECC, Ipsos Mori, EST). This aligns with current independent expert advice, e.g. modern gas condensing boilers are around 93% efficient, and gas is the cheapest non-renewable way to heat your home. ( Guide to Heating Systems) However, this consumer preference for choosing gas condensing boilers over gas non-condensing boilers has not been driven by financial pay back and savings in gas bills; it has in point of fact been driven by legislative changes in UK Building Regulations, supported by expert advice and guidance. Minimum provision for new systems in new and existing dwellings - the boiler efficiency should be not less than 86% (SEDBUK) value, and in existing dwellings and only in exceptional circumstance should be not less than 78% if natural gas fired. (The Building Regulations 2000 (as amended 2006) Domestic Heating Compliance Guide Table 1 (Part L of Schedule 1 to the Building Regulations is concerned with the conservation of fuel and power in buildings). Modern gas condensing boilers operating at around 93% efficiency comply with this key Regulation Changing Heating Sources - Consumer Cyclical Change Pattern This cyclical change pattern has a significant impact on when home owning domestic gas consumers are most likely to change their existing heating systems. Without any form of incentive or taxation or policy or legislative change, then typically, it would be on average 1 system change in an individual dwelling (on average) every 20 years. If we assume (based on this research), that 8

.")

9 Total Poulation Changing - (Cumulative %) consumers change their heating systems when they are becoming uneconomic to repair and/or costly to run and/or fail. On this basis, if we take any population of 100 dwellings in Bridgend (or any town) and consider the probability of change, then on average 5 dwellings would change their heating system each year over a typical 20 year life cycle. This aligns with current independent financial expert advice ( - How old should your boiler be before you replace it?). The figure 2 below highlights the cyclical pattern of the cumulative nature of the average change over a 20 year period. For example, in any given average population of 100 dwellings, following this typical cycle, Only 5% are likely to change their heating systems in year 1 (as a result of failure/unreliability). A total of one fifth (20%) are likely to have changed their heating systems by the end of year 4. A total of one third (33%) are likely to have changed their heating systems by the end of year 6. One half (50%) are likely to have changed their heating systems during year 10. About 25% of consumers are unlikely change their heating systems for over 15 years into the future. Based on the assumptions in this research, 100% of consumers are likely to change their systems by the end of year 20 (1 in 20 years). This is based on existing current technology and gas in urban areas Cyclical Change Pattern - Consumers Changing Heating Systems (Average 1 in 20 years) - Population Any 100 Dwellings e.g. in Bridgend - Numbers Changing Systems (Cumulative) - Over 20 year period Years boilers Figure 3 Cyclical Change Pattern Heating Systems 1 in 20 years Once the need arises i.e. the consumer s existing system is uneconomic to repair or is about to fail; then two in five (39%) had actually replaced their individual domestic heating systems in less than 1 year (actually within 3 months of the need arising) emphasising the fundamental need for people to have heat for comfort. (DECC, Ipsos Mori, EST) This cyclical change pattern is supported by our research into unsuccessful Gas Infill Projects, when typically less than 5% of consumers make definite commitments to want to change to mains gas within the first 0-3 months, even when there are compelling financial benefits e.g. reduced energy costs. 9

10 Population Changing (Cumulative %) With regard to successful Gas Infill Projects, figure 3 below highlights the typical pattern once the initial minimum viable number of 30% of dwellings accept the financial contribution, less than 2000 (2015 prices) which the domestic consumers pays towards the cost on the gas mains infrastructure. For example, for a Successful Gas Infill Project, the pattern is follows Initially, under the current protocols, there is a requirement for 30% of dwellings to change before the project is considered to be financially viable and construction commences (if this minimum of 30% is not met then the project is unsuccessful and construction of the gas mains infrastructure does not commence) After this initial 30% plus switching, then typically low numbers (less than 5%) change to mains gas each year as their heating systems start to fail and become uneconomic to repair and a replacement gas heating system may become attractive as a financially viable option. After 5 years, typically less than 40% of the total population of domestic dwellings have changed This research of Gas Infill Projects over 20 years old sees the numbers changing plateauing at 70% e.g. Chew Valley (Case Study 3 in Section below) i.e. 30% have not converted/connected to gas Typical Successful Gas Infill Sites - Consumers Changing Heating System Patterns (Over 20 years) Dwellings Population (Extract) Years Figure 4 Typical Successful Gas Infill Sites - Consumers Changing Heating System Patterns (Over 20 years) Why are the above critically important going forward in understanding a consumer s willingness to change and invest in other heating sources? The complimentary change patterns highlighted at figures 2 & 3 above respectively; are very significant going forward because they impacts on various existing and future critical aspects of any planned change programme: Costs to Consumers & Timing of Replacement (Demand Side) For example, the costs which may be charged for providing such new heating systems e.g. communal district heating networks. Clearly, when the costs of the new heating systems e.g. communal district heating networks; would need to be at the same as, or necessarily have lower full life cost than the current costs of existing individual gas central heating 10

After this")

11 systems, otherwise why would the consumer change? Other factors will include the consumer s ability and resources to pay for such new systems and the timing of such payments. Influencing Consumers to Change before their current cyclical change This is highly unlikely to happen. For example, when you assess a potential new Gas Infill Area, there is a high probability that one quarter (25%) of consumers are likely to have invested in their existing system e.g. oil fired boilers; within the previous 5 years. Having made that relatively recent investment in their homes, it is highly unlikely that they will change for another years, otherwise they would have simply wasted their previous/current investment. When you can incentivise domestic consumers to change you need a critical mass of, say, a minimum of 30% before the alternative energy source becomes viable. Commercial Market Drivers - Cost Benefit Analysis (CBA) - Business Investment (Supply Side) There is a scarcity now in 2015, of organisations in the market place looking to construct communal heating systems. The financial case from any entrepreneurial businesses who may want to enter into this market to invest in providing alternative replacement heating systems is critically important to success. This pattern impacts directly on the viability of any businesses wanting to achieve a commercial return on their investment. Such new entrants would expect a result over a reasonable payback period. Typically, within 5 years. If you look at the pattern at Figure 3 above, by year 5, typically on Gas Infill Projects less than 40% of domestic consumers have changed. Even after 20 years only 70% have changed. These numbers are critical to commercial investment decisions. Policy Changes, Incentives, Taxes and the Timing These would need to be significant; and would need to be provided at the right time and in the right way to overcome the potential inertia and resistance to change. They would need to be successful in changing consumer behaviours. 2.2 Understanding how the decision to change systems may be made now and into the future? The decision tree analysis in figure 3 below aims to outline how a typical consumer(s) may decide whether to change over to an alternative heating source. This is based on the evidence from Gas Infill Projects. The Key Assumptions made in this decision tree analysis are: That an alternative heating system e.g. a heating network is available from year 2 up to year 25. Estimated total costs to change to an alternative heating system in the range 8,000-10,000 (2015 prices) Assumes no compelling incentive subsidy is offered to consumers (Current 2015 Policy) 11

Decisions in Year 2 This is based on the evidence in the Gas Infill Projects in Wales and the South West over the 25 year period 1990-2015 and this has then been applied to")

12 Figure 5 Decision Tree Analysis -Energy Source Changeover -Willingness to Pay Current Consumer(s) Decisions in Year 2 This is based on the evidence in the Gas Infill Projects in Wales and the South West over the 25 year period and this has then been applied to potential alternative heating sources to replace gas. Decision Point Contribution by the Consumer to the construction of the Infrastructure If the contribution from the domestic consumer towards the infrastructure costs is greater than 2,000 (2015 prices) per dwelling, then the domestic gas consumer is highly unlikely to change. The process would end then and the domestic consumer would then remain on their existing heating system i.e. individual gas central heating system. The gas network would be needed to support the chosen energy source for those domestic gas consumers beyond year 2. Decision Point Reasonable Payback Periods If the contribution from the domestic consumer towards the infrastructure costs for the heating network is from zero to less than 2000 (2015 prices) per dwelling, then the existing domestic gas consumer is likely to need to make the decision on how much they need to contribute per annum and over what reasonable payback periods. If the payback period is greater than 5 years, it is reasonable to assume that a majority of consumers are unlikely to commit to change. The process would end and those domestic gas consumers would then remain with their existing 12

13 heating i.e. individual gas central heating system(s). The gas network would still be needed to support the chosen energy source for those domestic gas consumers. There is a 15% probability that consumers will switch to the new heating source, will also no longer require gas for cooking and therefore at the end of Year 2 an estimated 15% of the current population of gas consumers in Bridgend (or any town) will no longer require the Gas Infrastructure. Therefore, given the reasonable assumptions in this research, there is a probability that 85% will still require a gas network beyond year 2, for at least another 20 years, (based on the average change cycle for heating systems) Future Consumer(s) Decisions by Year 25 Decision Point Contribution by the Consumer to the construction of the Infrastructure As with year 2 above, if the contribution from the domestic consumer towards the infrastructure costs is greater than 2000 (2015 prices) per dwelling, then the domestic gas consumer is highly unlikely to change to an alternative heating system. The process would end at that point and those domestic gas consumers would then remain with their existing heating i.e. individual gas central heating system. The gas network would be needed to support the chosen energy source for that domestic gas consumer beyond year 25, for at least another 20 years, based on the average change cycle for heating systems. This is based on the evidence from our primary research into Gas Infill Projects Decision Point Reasonable Payback Periods As with year 2 above, if the contribution from the domestic consumer towards the infrastructure costs for the heating network is from zero to less than 2000 (2015 prices) per dwelling, then the existing domestic gas consumer is then likely to need to make the decision on how much they need to contribute per annum and over what reasonable payback periods. If the payback period is greater than 5 years, it is reasonable to assume that a majority of consumers by year 25 are unlikely to change. The process would end then and those domestic gas consumers would then remain with their existing heating i.e. individual gas central heating system(s). The gas network would be needed to support the chosen energy source for that domestic gas consumer. This flow chart is based on the research undertaken into Gas Infill Projects in Wales & South West over the period early 1990 s to For example, please see section G.D.H.I. Comparative Indicator South West, below and specifically, Case Study#3 Successful Gas Infill Project - Longer Term Take Up - Chew Valley (1992). By the end of year 25, it is estimated that there is a 35% probability that consumers will have switched to the new heating source, will no longer require gas for cooking and therefore by Year 25 an estimated 35% of the current population of gas consumers in Bridgend (or any town) will no longer require the Gas Infrastructure. Therefore, given the reasonable assumptions made in this research there is a probability that 65% will still require a gas network beyond year 25, for at least another 20 years, (based on the average change cycle for heating systems) totalling 45 years (from to 2015 to 2055 or beyond). In summary, based on the evidence from Gas Infill Projects, consumers will make long term decisions (20 years and beyond) on whether to change heating systems based on the costs i.e. if over 2,000 (2015 prices) for the costs of the infrastructure only, they are highly unlikely to change. Also, a majority may not have monies available to invest and therefore reasonable payback periods i.e. less than 5 years are also important. Given that under current UK Policy, that there no compelling financial incentives to change (and/or or punitive carbon taxes have not been introduced) that there is a probability that approximately 0-15% domestic consumers may change within 2 years; and 0-35% may have changed within 25 years. This is supported by the research into longer term Gas Infill Projects in Wales and the South West of England which commenced in the early 1990s, when by 2015, only one third of consumers have changed. For example, please see section G.D.H.I. Comparative 13

14 Indicator South West, below and specifically, Case Study#3 Successful Gas Infill Project - Longer Term Take Up - Chew Valley (1992). 2.3 Understanding what support consumers need? Consumers Need Expert Advice & Support - Consumers need expert support and advice, previous research has identified that a total of 80% of gas consumers need expert advice to reach their decision to change e.g. that their existing system is becoming uneconomic to run and/or actually fails to work. This expert advice is sourced from various places e.g. boiler servicemen (42%); energy supplier or builder (14%); friend with expertise in plumbing or heating (24%). (DECC, Ipsos Mori, EST). Why is this support critically important? This support is needed and should not be underestimated as is it is critical to the success in understanding one of the critical elements of what consumers will need to influence them to change heating systems. Across the UK, gaining the support of the national and local networks of Local Authorities; Social Housing Associations; larger organisations e.g. British Gas; Small and Medium Sized Enterprises (SME s) e.g. boiler servicemen, suppliers, builders, gas installers, plumbers etc.; it will all be critical to achieve their support and commitment so that, in turn, they will then be able to use their expertise to influence and support consumers to change to. Also, it is highly likely that this will require boiler service men, gas installers, and plumbers etc. to be educated and convinced that other heating systems options e.g. heating networks, Air Source Heat Pumps (ASHP) are viable and sustainable alternatives; and also additional training may be required to provide the skills to install the new alternative systems. Otherwise it is likely that they would remain motivated to recommend consumers to continue to install gas boilers in individual dwellings, rather than communal heating networks. This need for support is also evident in the research from Gas Infill Projects, a few examples below. When the change was enabled by, driven by, and support and funded provided by, the relevant Local Authorities/Government Departments/Social Housing Associations then this was a key enabler to ensure the Gas Infill Projects were successful. Case Study #1 - Gas Infill Project Supported by Anglesey Council - Llanerchaymedd Anglesey (2013) There was a contribution of 1488 respectively per dwelling, required from each consumer. The upfront investment which was funded by WWU was 745,000 for this project. A Critical Success Factor (CSF) for this scheme was the work, support and funding enabled and provided by Wales & West Utilities working closely with Anglesey Council. There were 122 social homes in the village so this underpinned the investment. In addition to the social homes, Anglesey Council also supported the promotion of the scheme to private homes which has now seen a total of 179 connections in the first 2 years up to (WWU Infill - Consumer Willingness to Pay) Case Study#2 - Gas Infill Project - Aston Hall (2014) and Rhewl Mostyn (2014), Flintshire - There was a mains contribution of 2363 (Aston Hall) & 3026 (Rhewl Mostyn) respectively per dwelling, required from each consumer; to justify the construction of the new gas network. The upfront investment which was funded by WWU was 195,000 for Aston Hall and 1,175,000 for Rhewl Mostyn respectively. A Critical Success Factor (CSF) for these two schemes was the enabling, drive, and support provided by Flintshire Council working closely with Wales & West Utilities. In addition to the social housing, the Local Authority offered low costs loans to private customers alongside the fuel poor scheme funding which will boost the uptake to 55 properties on Aston hall and 259 at Rhewl Mostyn by the end of (WWU Infill - Consumer Willingness to Pay). 14

. Why is this support critically important?")

15 Co-ordinated & Proactive Support from Local Authorities in Wales, underpinned by Welsh Government Support There were minimal Gas Infill Schemes being driven forward into construction by Local Authorities in Wales during the period i.e. 2 (4%) from 46 constructed Gas Infill Projects over that 10 year period. Compared with private homeowners driving forward the majority of projects forward 44 (96%) from 46 constructed projects over that same 10 year period. Gas Infill Projects - Taken to Construction (Period ) - 2 (<1% p.a.) from 46 constructed projects over 10 year period - Driven by LA's. [CELLRANGE], [VALUE] [CELLRANGE], [VALUE] Driven by Local Authority (LA) Driven by Private Homeowners Figure 6 Gas Infill Projects - Local Authority Influence - 10 Year Period ( ) This has changed significantly since 2012, a significant number of successful schemes have been driven forward into construction by Local Authorities in Wales, working closely with Wales & West Utilities during the period i.e. 4 (average of 44% per annum) from 9 constructed projects. Private homeowners still drive forward around 4/5 Gas Infill Projects average per annum, but the mix has changed significantly. Local Authorities have in the last 2 3 years also driven forward Gas Infill Projects as well, see Figure 3 below. When combined with schemes driven forward by private homeowners, the local authorities in Wales have effectively doubled the number of projects being taken forward to constructing in recent years ( ). Gas Infill Projects - Taken to Construction (Period ) - 4 (44%) from 9 constructed projects during the most recent 2 years - Driven by procative LA's [CELLRANGE], [VALUE] [CELLRANGE], [VALUE] Driven by Local Authority Driven by Private Homeowners Figure 7 Gas In fill Projects - Local Authority Influence - 2 year period ( ) 15

- 2 (<1% p.a.) from 46 constructed projects over 10 year period - Driven by LA's.")

16 The Case Studies #1 & #2 above are two examples of a significant increase in the proportionate number of larger infills progressing as a result of proactive Local Authorities in Wales, working closely with Wales and West Utilities, supporting and driving forward Gas Infill Schemes. These have used funding for eligible existing domestic properties under the Fuel Poor Network Extension scheme. Various other Gas Infill Projects have also been supported by funding from national schemes such as CERT, CESP and ECO as well as the regional schemes including Warm Front in England and NEST. For the case studies #1 & #2 above, ARBED (the Strategic Energy Performance Investment Programme in Wales which supports the Welsh Government commitment to reduce climate change, help eradicate fuel poverty and boost economic development and regeneration in Wales) has provided additional funding. Social landlords are likely to invest up to a total of 4,000 per dwelling to improve their housing stock if the other options of oil systems or heat pumps will cost them more in terms of the full life costs. (WWU Infill - Consumer Willingness to Pay) (WWU Infill - Consumer Willingness to Pay) Success This Fuel Poor Funding was one Critical Success Factor in ensuring that the Gas Infill Projects within these Social Housing Areas, have progressed to construction and are successful. This includes privately owned dwellings being able to change their heating source and benefitting from the same Gas Infill Project in their area. For example, in Case Study#2 above (Rhewl Mostyn, Holywell, Flintshire) the total cost of both the mains and service construction was approx per dwelling. However, for householders/dwellings who were in fuel poverty within the Fuel Poor Scheme, they were eligible to approx per dwelling in Fuel Poor Allowances (within the previous Scheme approved by Ofgem). Effectively, this reduced the contribution needed for those eligible householders/dwellings in that project to approx per dwelling. Additional ARBED funding was also provided to eligible homeowners in Fuel Poverty. Another Critical Success Factor in ensuring that these WWU Gas Infill Projects are successful is the fact that the initial investment in constructing the new gas networks in these areas, and the financial risk associated with that initial investment, is being made, underwritten and supported by WWU, for example, 1.7 million in Rhewl Mostyn, Flintshire, Wales for 425 plus properties. Clearly, if other alternative heating networks s e.g. Communal Heating Networks were to be constructed the investment and the inherent risks associated with that investment would need to be funded, underwritten and supported somehow? In this specific Gas Infill Project 214 properties, including the majority of Social Housing dwellings and fuel poor householders, are now (June 2015) connected to gas and benefitting from lower energy costs. In the last 2 years, an additional 49 privately owned dwellings will have been connected, (including low interest loans being offered to consumers in privately owned dwellings); totalling 259 dwellings (social housing plus privately owned housing connected). Using the cyclical change pattern at Figure 2 above (15 year cycle of change), in a population of 399 private dwellings you would expect on average approx. 26 properties (7%) per year to need to change heating systems i.e. because their current system is becoming uneconomic to repair; so far over 2 years this is aligned closely with what has happened in Rhewl Mostyn, Holywell, Flintshire. Monitoring beyond There remains an opportunity for a further 350 dwellings, mostly privately owned, to connect to gas when their current systems are uneconomic to repair and/or fail, but, at a total cost of 4000 total mains and services contribution per dwelling, it will be interesting to monitor over the next 13 years, when approximately 26 properties per annum are likely to need to change their heating systems, whether they connect to the now available gas network or whether they consider the 4,000 contribution to the mains and services costs to be prohibitive, and therefore they stay with their existing source of heating. This unique piece of research into Bridgend, South Wales includes social housing and it is highly likely that significant financial incentives will be required and also co-ordination and support will be needed e.g. by Bridgend Council. 16

17 2.4 Understanding what influences the consumer s decision to change to a replacement system? Current - What Influences the consumers decision? For domestic consumers e.g. homeowners, social housing tenants; private landlords renting domestic property, the primary factor which influence the decision to change to a replacement system is financial. Financial Decision Domestic Consumers The most important factor is cost e.g. for domestic consumers, low energy bills, the system being cheap and easy to run (DECC, Ipsos Mori, EST). This economic influence is critical to the consumer s decision and is supported by the research into Gas Infill Schemes. For example, whenever the mains contribution is in excess of 3,300 (2015 prices), there has been minimal take up and the schemes have never progressed over the period (WWU Infill - Consumer Willingness to Pay). Financial/Commercial Decision Landlords - Having a heating system which must be compliant with legislation, maintains the value of the property and is cheap and easy to run. (WWU Infill - Consumer Willingness to Pay). Social landlords will invest up to 4,000 in gas systems to improve their housing stock, if they have available funds and the alternative options of oil systems or heat pumps will cost more than gas heating systems on a full asset life cost comparison basis. (WWU Infill - Consumer Willingness to Pay) Secondary factors for consumers are Reliability, Sustainability & Ease of Use - The heating system must provide instant heat to survive and for comfort, immediately when required in cold weather, and for cooking for ease of use and for the source to be responsive and controllable. (Famous TV Advert Slogan: Cook ability that s the beauty of gas ) How the decision to change to another system is made? Consumer Bias to what they know - The consumer bias is still towards what they know and use now i.e. Currently, existing individual gas c/h systems for 54% of consumers, because this type of heating system is well known and so are the upfront and running costs - Within this the two most important determinants a) The size and fit with their property. b) Intuitively the credibility of this type of heating system for the UK climate. (DECC, Ipsos Mori, EST). This is supported from this research into Gas Infill Projects e.g. Case Study#3 Successful Gas Infill Project - Longer Term Take Up - Chew Valley (1992) below when after 20 years 30% of consumers have still not changed from their existing heating systems which they know and use e.g. oil fired central heating systems. (WWU Infill - Consumer Willingness to Pay) Future What factors may influence the consumer s decision going forward? Basically, the same factors i.e. reliability of the system; the Economic/Financial factors; and Expertise & Support are critically important and are most likely to influence the consumer s willingness to change their heating systems going forward. 17

, there has been minimal take up and the schemes have never progressed over the period 1990-2015.")

18 Reliability Consumers would want systems they know and feel comfortable with. (DECC, Ipsos Mori, EST) Economic/Financial Factors Lower Running Costs Important to consumers are running costs e.g. 37% would replace heating systems if energy costs rise considerably; Only 13% would be influenced positively by a 'one off upfront grant' and Less than 9% would be influenced positively by an annual tariff incentive. (DECC, Ipsos Mori, EST). Most consumers (67%) expected to reduce their energy bills by installing energy efficiency measures and agree it is sensible to improve insulation in their homes - 70% said they would be willing to invest in better insulation in order to receive financial assistance towards a more efficient heating system. Investment in Alternative Heating Sources None of the Gas Infill Scheme projects have ever progressed if the contribution to the mains element of the network is in excess of 3300 (2015 Prices). Positive responses, with average mains contribution circa Sufficient numbers of private owned households will not pay more than 2,000. (WWU Infill - Consumer Willingness to Pay). Environmental Benefits - Interestingly, previous research has suggested less than 25% of consumers, would be encouraged to change simply by more environmentally friendly heating systems. (DECC, Ipsos Mori, EST) However, this research has looked into practical and real examples of recent (2015) opportunities to change, for example, consumers changing to green electricity tariffs, the actual numbers who have changed in reality is significantly lower at only 0.36% of people who have switched to green tariffs and have actually gone green. (http.blog.moneysavingexpert.com/2014/11/04/green-energy-is-surprisingly-unpopular/) In summary, for any new heating systems to be successful and to influence consumers to get them to change willingly, they would need to provide the consumers with a financially cost effective solution e.g. lower running costs; and there is a limit of to the amount consumers are prepared to invest in the heating network mains external to the property of circa 3,000 and also be reliable. (WWU Infill - Consumer Willingness to Pay) Understanding the consumer s ability to be able to pay for changes to heating systems. Using the Gross Disposable Household Income (GDHI) figures (Office for National Statistics Prices), this research has looked at the Bridgend consumer s actual ability to be able to pay for changes to heating systems, and compared this with the GDHI Averages Nationally and with GDHI Averages in other UK locations e.g. South of England and London. 18

19 Locations Comparison of Bridgend with National and sample other locations Gross Disposable Household Income (GDHI) - Average 's per head per annum Mid Wales - Corris, Gwynedd Bridgend & Neath Port Talbot Wales Isle of Anglesey 13,511 14,122 14,623 15,022 Scotland England South West of England 16,267 17,066 17,523 London 21, ,000 10,000 15,000 20,000 25,000 GDHI per head (2012 Prices) Figure 8 Gross Disposable Household Incomes (GDHI) - Bridgend Comparison with other locations GDHI is defined as the average money that individuals (households) have for spending or saving. That is money left after expenditure associated with income e.g. taxes and social security contributions. It is calculated gross of any deductions for capital consumption. (Office for National Statistics) GDHI may be a useful comparative indicator of the monies which household(s) may have able and be a gauge of the consumer s actual ability to be able pay for alternative heating systems in different locations in the UK GDHI A Comparative Indicator - South West Of England South West of England At 17,523 GDHI per head, the South West of England has a slightly higher (2.7%) GDHI when compared with the England national average of GDHI per head, from our Research into Gas Infill Projects, there is some evidence that some areas of higher GDHI, e.g. more affluent parts of the South West of England; are more likely to be in a stronger financial position to pay for changes to heating systems when compared with other parts of the UK, as follows Case Study#3 Successful Gas Infill Project - Longer Term Take Up - Chew Valley (1992) The Chew Valley, when compared with other parts of England, is a relatively affluent area close to Bristol, in the South West of England. The Chew Valley Infill was proposed and commissioned over 22 years ago providing gas supplies to in excess of 5200 properties in this Chew Valley Area. Please see Figure 9 Chew Valley Infill Project Map. This was a very successful Infill scheme in a relatively affluent area of England, so in this case there is some positive correlation between GDHI, the financial contribution expected from consumers, and the success of Gas Infill Projects. However, even here, in 2015, the overall connection rate has reached a plateau at 70% saturation rate of consumers who have switched to mains gas, even after over 20 years. Within the 30% of domestic consumers who have still not changed, the majority use oil as their primary energy source for heating, even though this has been consistently more expensive than mains gas. This real example highlights the challenges in motivating consumers to change to alternative heating/energy sources. 19

20 Figure 9 Chew Valley Infill Project Map Case Study#4 Successful Infill Project Very low volumes/high cost Wells, Somerset (2014) There are less than 1% of Gas Infill Projects in Wales and the South West, which proceed when the mains contribution for the provision of the gas network is in excess of 2,000 i.e. the cost to private homeowners who finance this contribution themselves. One exception to this was a project to supply gas to 6 large detached dwellings in Wells, Somerset, when the mains contribution was relatively high at 4570 per dwelling. This scheme did go ahead and the mains were constructed, primarily because the owners were relatively affluent and were prepared to invest to enhance the long term value of their valuable properties GDHI A Comparative Indicator Wales Isle of Anglesey, Wales - At 15,022 GDHI per head, the Isle of Anglesey has a slightly higher (2.7%) GDHI when compared with the Welsh national average of 14,623 GDHI per head. However, when compared with say the South West of England s 17,523 GDHI per head. Anglesey s 15,022 GDHI per head is actually 14% lower than the GDHI in the South West. Case Study#5 Failed Gas Infill Project - Gaerwen on Anglesey (2013) - This infill scheme was proposed in 2013 and was supported by Wales & the West Utilities, who canvassed the area to encourage take up by providing supporting information on likely cost savings and tangible energy cost savings benefits to gas consumers. A total of 600 properties and businesses were canvassed and contacted in 2013, even though the mains contribution costs to get the gas network into the area were relatively low i.e. around 1,500 per dwelling (approximately 10% of the annual GDHI per head in Anglesey). Only 40 expressions of interest from private homes and businesses plus 20 from council properties have been received to date (June 2015), this falls short of the critical mass of 180 (30%) supporting gas consumers/dwellings which are needed to consider progressing this Gas Infill scheme to construction. This is typical of some of the responses to engagement within some communities, who remain reluctant to change to other forms 20

21 of heating systems, because of their inability to pay for such changes, even when there are obvious future financial benefits to the domestic and business gas consumers. Bridgend, South Wales You will note from figure 6 above, that for our area of research in Bridgend, South Wales that at 14,122 GDHI per head per annum this is 3.4% lower than the Welsh national average of 14,623 GDHI per head per annum; and is 15.7% lower than Anglesey s 15,022 GDHI per head per annum. Based on GDHI, Bridgend households are in the lowest 10% of disposable incomes in the UK, this is highly likely to a have a significant adverse impact on their ability to be able to afford to pay for alternative heating systems. Case Study#6 Failed Gas Infill Project Corris, Gwynedd (2014) GDHI - The Impact of Costs on the Consumer s Decision Making Process to change to an alternative heating system, this includes when substantial Fuel Poverty Funding is available - This was a scheme proposed in 2012, around 150 dwellings in Corris. Initially, there was a very positive response from local domestic and business consumers, and this was expected to be a successful project. The cost of provision of the network including the mains and the services to the individual properties was approximately 2,450 per dwelling. Significant funding of 2,700 funding was available within the WWU, Ofgem supported, and Warm Home Assistance Programme for Fuel Poor, but, this contribution was only for those eligible dwellings/homes in Corris. It was also limited to the contribution to the mains and services costs for those eligible homes. There would have been additional costs to home owners of for the installation of internal individual gas central heating systems. Firm quotes were issued to homeowners, but, only 5 were prepared to commit. The scheme support faded and the project was closed without proceeding to construction. You will note from figure 2 above, for Corris that at 13,511 GDHI per head per annum, this is 8% lower than the Welsh national average of 14,623 GDHI per head per annum, which makes Corris one of the lowest GDHI areas in the UK. Even with significant funding available and positive efforts being made, in such a Fuel Poor area desperate for reduced energy costs, the scheme failed to go ahead. If people need their very low GDHI to pay for daily essentials and to survive today, it is highly unlikely that they will be able to afford to pay for replacement heating systems without substantial funding to support them. In some areas of South Wales, in Gas Infill Area communities and ex mining areas; there are small numbers of exemployees of the National Coal Board (NCB) and/or British Coal Corporation (BCC), who live in dwellings in these potential Gas Infill Areas, who are still eligible for concessionary coal under the National Concessionary Fuel Scheme ( With concessionary energy, these exemployees living in these dwellings are highly unlikely to change to mains gas. There are only small numbers of such people/dwellings that receive this concession, but that could be the difference between an Infill Scheme progressing or not Average UK Debt The average household debt in the UK (including mortgages) was 54,197 (Nov 2013 Prices). The average household debt in the UK (excluding mortgages) was 6,016 (Nov 2013 Prices). The Money Charity Debt Statistics (January 2014). If you assume that the cost of installing a replacement heating system e.g. Gas Infill Project or a local Heating Network or an Air Source Heat Pump (ASHP); is in the range of ,000. If this was added to mortgages then it is reasonable to assume this may increase average household debt in the UK (including mortgages) by, in the range of 9% - 18%. If this is not added to the mortgage, e.g. personal loans, this may increase average household debt in the UK (excluding mortgages) by, in the range of 50% - 166%. In summary, based on GDHI, i.e. the money that some households/individuals have to save or spend ; it may not actually be the domestic gas consumer s willingness to pay, but, simply their ability to afford to pay which is the 21

22 critical limiting factor on whether consumers decide to change to other heating systems or not. This applies even if there are obvious future benefits of changing e.g. reduced heating bills, less hassle, reliability, lower future running costs; more environmentally friendly systems etc. and additionally other funding available for eligible domestic gas consumers in some Fuel Poor Areas. If consumers simply cannot afford to invest now in new alternative heating systems (with no disposable income to spare; and also given the current UK average debt figures if people simply cannot afford to borrow the money and/or pay back loans) then change to alternative heating sources is very highly unlikely to happen, even though consumers may be very willing to change. 2.5 Understanding which efficient heating systems/energy sources homeowners find most (and least) attractive? Consumer s Preference - Previous research has identified that the majority (80%) of domestic gas consumers who are already within the existing gas networks prefer individual gas central heating systems. (DECC, Ipsos Mori, EST).This reaffirms the position that consumers actually prefer cost effective, clean and reliable gas heating systems i.e. what they know and understand. With regard to alternative heating and power sources, Micro CHP was a preferred alternative, with 46% of consumers who would consider this favourably as an alternative heating and power source. Heating Networks would be considered favourably as an alternative by 34% of gas consumers both at an emotional and practical level, as they felt it increased the efficiency of generation and would therefore collectively reduce costs. Whilst, for domestic gas consumers who are not currently within the existing gas networks, 53% would consider Ground Source Heat Pumps (GSHP s) as a favourable alternative. (DECC, Ipsos Mori, EST). Consumer s Priority Previous research has identified that 71% of consumers specifically prefer an individual gas combination boiler and this is most attractive to them because of their awareness of this technology being more effective and efficient than previous gas central heating boiler technology and gas being reliable and suitable for the UK Climate. (DECC, Ipsos Mori, EST). Consumer Education - Clearly, to influence consumers and to motivate them to be willing to change, any proposed replacement heating systems e.g. heating networks; would need to be more effective and efficient than existing combination boilers and provide additional benefits e.g. reduced running costs and/or lower energy costs. Additionally, consumers will need to be educated and convinced to change. Consumer Awareness of Unfavourable Solutions Previous research has identified that a majority of consumers (72%) would find Air Source Heat Pumps (ASHP s) less attractive. Once again reliability is a factor. The ASHP lacked credibility as a reliable technology among some homeowners (particularly those living in colder parts of Great Britain) as they did not believe it would work at low temperatures. The Least Attractive option being Micro Biomass which is considered to be visually unattractive; 'too much hassle' i.e. with dealing with the fuel source for biomass. (DECC, Ipsos Mori, EST) 2.6 Understanding why changes by consumers can be driven by external influences Legislation European and UK National legislation are key external factors which influence change e.g. directly by changes to UK Building Regulations, requiring newly constructed properties to have significant energy conservation improvements e.g. higher standards of insulation; embedded into the construction of the property to improve energy efficiency during the build of the property Technological Changes The gas combination boiler which is now the most preferred solution for the majority of consumers, (influenced by advice from experts), was developed to improve the efficiency of heat energy being produced; and effectively 22

23 reducing the amount of gas being used to produce that same level of heat energy thereby reducing the carbon being produced. Proactive and progressive legislative changes may be required to influence consumers to change to improved alternative heating systems such as heating networks and to accelerate the rate of change to achieve carbon reduction targets by 2030 and 2050 respectively Financial Incentives to motivate change to more environmentally friendly solutions Financial Incentives have been offered to motivate change to more environmentally friendly solutions For example, solar photovoltaics, the current (June 2015) highest RHI incentive offered is (p/kwh) of energy saved (electricity p/kwh). This has been successful in motivating business investors to construct larger scale solar sites and installations and also consumer s to install solar panels on domestic dwellings as follows: 'Overall solar PV capacity at the end of 2015 Q1 stood at 6,521 MW, an increase of 25 per cent (1,285 MW) on that at the end of 2014 Q4 (due to unaccredited large-scale sites deploying ahead of the end of the RO year). This represented 687,642 installations in 2015 Q1, an increase of 5.7 per cent on that at the end of 2014 Q4. DECC Solar Photovoltaics Deployment Statistics (May 2015) 'Capacity commissioned and accredited under the Renewables Obligation stood at 2,327 MW, which is a rise of 15 per cent (308 MW) from 2014 Q4. Capacity accredited under the Renewables Obligation represents 36 per cent of total solar deployment. DECC Solar Photovoltaics Deployment Statistics (May 2015) 'Capacity commissioned and accredited under the GB Feed in Tariff stood at 2,993 MW, an increase of 5.0 per cent (143 MW) on that at the end of 2014 Q4. Capacity confirmed on GB Feed in Tariffs represents 46 per cent of total solar deployment. DECC Solar Photovoltaics Deployment Statistics (May 2015) Clearly, by the end of March 2015 solar PV MW capacity has increased by 25% to 6,521 MW when compared with the end of December Over the same period the number of installations has increased by 5.7% to 687, Willingness to change Heating Systems/Energy Sources - Understanding actual changes made by UK Consumers (May 2015) This research has compared previous sample research with actual changes made by UK Consumers. For example, sample research by the Department of Energy & Climate Change (DECC) Homeowners Willingness to Take up More Efficient Heating Systems (March 2013) report by Ipsos MORI and the Energy Saving Trust, compared with actual changes/statistics made by UK Consumers, for example, DECC Non Domestic RHI and Domestic RHI Monthly Deployment Numbers 9th April, May, 2015 (May 2015) Sample Theory on Willingness to change to Alternative Heating Systems/Energy Sources Department of Energy & Climate Change (DECC) Homeowners Willingness to Take up More Efficient Heating Systems (March 2013) report by Ipsos MORI and the Energy Saving Trust - With regard to alternative heating and power sources, Micro CHP was a preferred alternative, with 46% of consumers who would consider this favourably as an alternative heating and power source. Heating Networks would be considered favourably as an alternative by 34% of gas consumers both at an emotional and practical level, as they felt it increased the efficiency of generation and would therefore collectively reduce costs. Whilst, for domestic gas consumers who are not currently within the existing gas networks, 53% would consider Ground Source Heat Pumps (GSHP s) as a favourable alternative. (DECC, Ipsos Mori, EST). If we apply this sample research from 2013, and if we then extrapolate this sample theory to the UK population estimated at 19 million domestic dwelling this would suggest, in theory at least, that many millions of UK domestic consumers would consider changing to alternative heating, but how many have actually changed? 23

24 When you compare and contrast this with the actual numbers deployed/changes to Alternative Heating Systems, both prior to, and since the introduction on 9th April of the current Renewable Heating Incentive (RHI) up to 31 May, 2015; then only a relatively small number i.e. totalling approx. (see Figure 8 below) and certainly not millions of domestic consumers have taken advantage of previous incentives and the current RHI and actually changed to alternative heating systems/energy sources Actual Statistical Changes to Alternative Heating Systems/Energy Sources Department of Energy & Climate Change (DECC) Non Domestic RHI and Domestic RHI Monthly Deployment Numbers 9th April, May, 2015 (May 2015) Domestic consumers who have actually changed in Great Britain. 1. Numbers of legacy system changes and numbers of accredited domestic installations completed prior to 9 th April, Numbers of accredited domestic installations completed, since the introduction of the RHI during the 14 month period 9 th April, st May, 2015; 3. Total of 1. & 2 above i.e. total of all accredited domestic installations completed. 1. Accredited Installations Legacy Systems Prior to Accredited Installations - Since the Introduction of the current RHI ( ) Total of All Accredited Installations Air Source Heat Pump 11,616 3,405 15,021 (ASHP) Ground Source Heat Pump 4, ,684 (GSHP) Biomass Systems 3,162 5,385 8,547 Solar Thermal 5,003 1,369 6,372 Totals 23,808 10,816 34,624 Figure 10 Actual Numbers of Domestic Consumers with Accredited Alternative Systems Up to May 2015 In summary, the current RHI is not stimulating interest and is not motivating large numbers of domestic consumers to change to alternative heating systems/energy sources Domestic Consumers Changing to Solar Panels Wadebridge Using a bottom up approach, from the domestic consumer s viewpoint, this research has uniquely aimed to review and identify any real examples of groups of consumers actually changing their energy sources. For example, in May 2015, the BBC reported on solar energy and domestic consumers actually installing solar panels on domestic dwellings in Wadebridge, Cornwall. Around 500 houses in Wadebridge on the Camel estuary already have panels on their roofs - nearly 10% of homes in the area of around 5000 dwellings - making the town a contender for the solar power 'capital' of the UK. Cornwall, with 1,541 sunshine hours every year, is particularly rich in this resource. But people living anywhere in the UK can also benefit. Providing you are prepared to invest at least 5,000 - and wait for a decade to get your money back - the eventual savings could be considerable. "It is fairly likely from the information we've been able to gather that Wadebridge has the highest concentration of panels in the country," says 24

25 Jerry Clark, of the Wadebridge Renewable Energy Network (WREN). The town where one in ten have opted for solar power ( This once again confirms that even with financial incentives being available to motivate consumers to change and a proactive local network (WREN); minimal (10%) of consumers have actually changed to solar energy as an alternative energy source. Interestingly, this was reported by a BBC Personal Finance Reporter within BBC Business, indicating Personal Finances are a key driver in influencing consumer s ability and willingness to pay. 3 Conclusion, Recommendations & Next Steps The primary finding of this research has been that financial (domestic consumers) and commercial/finance (non domestic consumers) is the primary driver(s) which will determine whether or not domestic and non-domestic consumers will change their energy sources and heating systems. The current RHI is not motivating large numbers of domestic consumers to change to green heating systems/energy sources. Using a bottom up approach, this research has uniquely identified different cohorts of consumers, and within these cohorts, significant variations in their ability and willingness to pay for changes to their energy sources and heating systems over different periods of time to receive a payback on the investment domestic and non-domestic consumers make. Now need to understand what home energy policy would be required that would satisfy the consumer willingness to pay criteria. For example, in order to encourage consumers to switch to lower carbon energy sources, one option is to set significantly higher financial incentives (consumer pull measures) and/or penalties (consumer push) related to energy use and the installation of lower carbon heating systems. What level of incentives/penalties would realistically influence consumers to switch? 25

26 4 References Department of Energy & Climate Change (DECC) Homeowners Willingness to Take up More Efficient Heating Systems (March 2013) report by Ipsos MORI and the Energy Saving Trust. Wales & West Utilities (WWU Infill) - An analysis of fuel switching and consumer willingness to pay for a new energy source impact on heat network utilisation (May 2015) Wales & West Utilities Mapping of different types of customer classifications (July 2015) The Potential & Costs of District Heating Networks A Report to the Department of Energy & Climate Change (April 2009) Poyry, Faber Maunsell/ AECOM (April 2009) Gross Disposable Household Income (GDHI) figures (Office for National Statistics Prices) How old should your boiler be before you replace it? - Guide to Heating Systems The Building Regulations 2000 (as amended 2006) Domestic Heating Compliance Guide Table 1 (Part L of Schedule 1 to the Building Regulations is concerned with the conservation of fuel and power in buildings) DECC Solar Photovoltaics Deployment Statistics (May 2015) DECC Non Domestic RHI and Domestic RHI Monthly Deployment Numbers 9 th April, May, 2015 (May 2015) The town where one in ten have opted for solar power Gross Disposable Household Income (GDHI) figures - (Office for National Statistics) The Money Charity Debt Statistics (January 2014) 26

27 5. APPENDICES 5.1 Sample Population Mapping of the different categorisation of different consumer type(s) This appendix includes mapping of different categories of different consumer types as referenced in Section Figure 1, above. 27

28 28

GREEN DEAL Saving money by understanding the Energy Agenda. Dave Princep BSc LLB MCIEH

GREEN DEAL Saving money by understanding the Energy Agenda Dave Princep BSc LLB MCIEH Energy Efficiency Energy Efficiency What a difference a years makes! Energy Efficiency 2010 Energy Efficiency 2011

GREEN DEAL Saving money by understanding the Energy Agenda Dave Princep BSc LLB MCIEH Energy Efficiency Energy Efficiency What a difference a years makes! Energy Efficiency 2010 Energy Efficiency 2011

Extra help where it is needed: a new Energy Company Obligation

Extra help where it is needed: a new Energy Company Obligation May 2011 The content of this paper is subject to the consultation outcome Contents 1 Our objectives for the ECO 1.1 Householder support: Lower

Extra help where it is needed: a new Energy Company Obligation May 2011 The content of this paper is subject to the consultation outcome Contents 1 Our objectives for the ECO 1.1 Householder support: Lower

Domestic energy consumption in Barnet has reduced but remains higher than the British average:

HOME ENERGY EFFICIENCY ACT (HECA) RETURN LB BARNET 31ST MARCH 2013 The following report sets out the energy conservation actions being or proposed to be taken by London Borough of Barnet that it considers

HOME ENERGY EFFICIENCY ACT (HECA) RETURN LB BARNET 31ST MARCH 2013 The following report sets out the energy conservation actions being or proposed to be taken by London Borough of Barnet that it considers

(92 plus) (81-91) (69-80) (55-68) (39-54) (21-38) (1-20)

(81-91) (69-80) (55-68) (39-54) (21-38) (1-20)") Energy Performance Certificate Georgia House Stud Bradley Road Burrough Green NEWMARKET CB8 9NH Dwelling type: Detached house Date of assessment: 17 August 2011 Date of certificate: 17 August 2011 Reference

Energy Performance Certificate Georgia House Stud Bradley Road Burrough Green NEWMARKET CB8 9NH Dwelling type: Detached house Date of assessment: 17 August 2011 Date of certificate: 17 August 2011 Reference

Your guide to the Energy Company Obligation (ECO) How we can make it work for you. A5_ECOguide_AW.indd 2 24/10/2012 16:04

How we can make it work for you. A5_ECOguide_AW.indd 2 24/10/2012 16:04") Your guide to the Energy Company Obligation (ECO) How we can make it work for you A5_ECOguide_AW.indd 2 24/10/2012 16:04 Energy Company Obligation guide 2 Your ECO Partner The current Carbon Emissions

Your guide to the Energy Company Obligation (ECO) How we can make it work for you A5_ECOguide_AW.indd 2 24/10/2012 16:04 Energy Company Obligation guide 2 Your ECO Partner The current Carbon Emissions

tap into opportunities to develop your business

Find out more about the Green Deal, ECO and renewable energy markets and how your business can benefit tap into opportunities to develop your business Background and overview Over recent years, the UK

Find out more about the Green Deal, ECO and renewable energy markets and how your business can benefit tap into opportunities to develop your business Background and overview Over recent years, the UK

Energy Performance Certificate

Energy Performance Certificate 0 Raleigh Drive CULLOMPTON EX15 1FZ Dwelling type: Date of assessment: Date of certificate: Reference number: Type of assessment: Total floor area: Semi detached house 09

Energy Performance Certificate 0 Raleigh Drive CULLOMPTON EX15 1FZ Dwelling type: Date of assessment: Date of certificate: Reference number: Type of assessment: Total floor area: Semi detached house 09

Grants for Renewable Energy and Sustainable Projects in Schools March 2010 Update

Grants for Renewable Energy and Sustainable Projects in Schools March 2010 Update If your school is considering introducing micro regeneration technologies the following contacts may be of use to fund

Grants for Renewable Energy and Sustainable Projects in Schools March 2010 Update If your school is considering introducing micro regeneration technologies the following contacts may be of use to fund

Biomass Funding Solutions. Have Your Investment Pay its Way. The renewable energy experts throughout East Anglia

Biomass Funding Solutions Have Your Investment Pay its Way Biomass The renewable energy experts throughout East Anglia Installing Biomass since 2011. Abel Energy s finance solutions allow you to invest

Biomass Funding Solutions Have Your Investment Pay its Way Biomass The renewable energy experts throughout East Anglia Installing Biomass since 2011. Abel Energy s finance solutions allow you to invest

Housing Association Regulatory Assessment

Welsh Government Housing Directorate - Regulation Housing Association Regulatory Assessment Melin Homes Limited Registration number: L110 Date of publication: 20 December 2013 Welsh Government Housing

Welsh Government Housing Directorate - Regulation Housing Association Regulatory Assessment Melin Homes Limited Registration number: L110 Date of publication: 20 December 2013 Welsh Government Housing

Response to the Green Deal and Energy Company Obligation consultation

End Fuel Poverty Coalition c/o 65 Thornbury Road London SW2 4DB info@endfuelpoverty.org.uk www.endfuelpoverty.org.uk Green Deal Legislation Team Department of Energy & Climate Change 1st Floor Area D,

End Fuel Poverty Coalition c/o 65 Thornbury Road London SW2 4DB info@endfuelpoverty.org.uk www.endfuelpoverty.org.uk Green Deal Legislation Team Department of Energy & Climate Change 1st Floor Area D,

Views and Experiences of Electricity and Gas Customers in Northern Ireland

Views and Experiences of Electricity and Gas Customers in Northern Ireland www.socialmarketresearch.co.uk 1 EXECUTIVE SUMMARY In December 2010, the Utility Regulator (UR) commissioned Social Market Research

Views and Experiences of Electricity and Gas Customers in Northern Ireland www.socialmarketresearch.co.uk 1 EXECUTIVE SUMMARY In December 2010, the Utility Regulator (UR) commissioned Social Market Research

Energy Performance Certificate