PHAS and SEMAP Indicators for Commissioners August 27, :00 AM to 10:00 AM

|

|

|

- Audra West

- 7 years ago

- Views:

Transcription

1 PHAS and SEMAP Indicators for Commissioners August 27, :00 AM to 10:00 AM Brian L. Nemeroff, CPA - Partner Bringing Solutions and Prosperity to Our Clients Since 1958.

2 Overview Learning Objectives Role of the Auditor (external) Annual Audit Budget to Actual PHAS (Public Housing Assessment) SEMAP (Section 8 Assessment)

SEMAP (Section 8")

3 Overview Monitor Monthly Financial Reports compare Budget to Actual Balance Sheet (statement of net position) Statement of Revenues, Expenses and Changes in Net Position Statement of Cash Flows

4 Acronyms/Terms GAAP - U.S. generally accepted accounting principles. GASB -Gov t Accounting Standards Board GAAP Flyers (& accounting briefs, REAC website) AMP - asset management property COCC - Central Office Cost Center UFRS - uniform reporting financial standards FDS - financial data schedule OMB Circulars A-87 and A Office of Management and Budget A-133 Single Audit Act Yellow Book Gov t Auditing Standards GAGAS Generally Accepted Gov t Auditing Standards GAO Gov t Accountability Office

5 Jokes only and Accountant would find funny What do you call an accountant with an opinion? An auditor. An accountant is someone who solves a problem you didn't know you had in a way you don t understand. What's the difference between an accountant and a lawyer? The accountant knows he's boring. How many accountants does it take to change a light bulb? We didn t budget to change that particular bulb until next year How many did we budget for? Can we just work in the Dark?

6 Auditing Process Items Auditors are Concerned with Financial Report Financial Data Schedule (FDS) Grant Reconciliation Communication with Auditors Understand that the Auditor is External

7 Budgeting Utilize prior year funding formulas & other HUD information for best estimates. Focus should be on latest average rents and occupancy expectations. For asset management PHAs, management fees should be based on expected occupancy and leased vouchers.

8 Budgeting Continued Expenses should be based on the following: Review contract register for inclusion/adjustment. Call local utility companies and utilize web to estimate increases by utility type. Housing assistance payments should be based on latest average unit cost times estimated leased units (revenue & net restricted assets should cover this expense) times the expected pro-ration factor.

9 Budgeting Continued Expenses should be based on the following: Other housing choice voucher expenses should be limited to administrative revenue & net unrestricted assets. Insurance should be based on latest quotes. Employee benefits should be based on historical rates along with health insurance adjustment (generally a significant increase) and latest regulatory percentages along with staffing changes. Salaries should be based on anticipated staffing levels and rates

and latest regulatory percentages along with staffing changes.")

10 Budgeting Continued Historical data for other expenses should be reviewed and projected (sundry, collection costs, maintenance cost, etc.). Revenue should cover debt and depreciation to ensure sustainability Capital expenditures should be budgeted as well along with the source of funds to pay for these expenditures All programs need to individually be sustainable excluding items such as interest income and gain/loss on sale of assets (these vary based on economic factors and other factors - should never be dependent upon)

11 Financial Statements Balance Sheet (Statement of Net Position) The difference between what the PHA owns (assets) and what the PHA owes (liabilities) & cumulative earnings (equity). Statement of Revenues, Expenses and Changes in Net Position This statement presents how the PHA net assets increased or decreased during the current fiscal year. Includes non-cash items such as depreciation, amortization, gain/loss from sale of assets, etc. Ideal is to be positive and to cover non-cash items such as depreciation (shows the ability to maintain your assets through future capital expenditures). Statement of Cash Flows This statement shows how the net change in total cash receipts and cash disbursements of the Authority during the current fiscal year.

.")

12 Audit Consider the Audit in two main sections The Basic FS (the numbers/dollars) Controls and Compliance (Rules and Regs) HUD Government auditing standards A-133 Single Audit Process Review financials to obtain reasonable assurance that the basic financial statements are free of material misstatements An audit includes assessing accounting principles used and significant estimates to evaluate the overall financial statement presentation

13 Audit Items generally tested for controls and compliance: Procurement files, Disbursements AP, Payroll and HAP Employee files, Housing choice voucher Tenant files, Waitlist, SEMAP Due to and from VMS NRP and UNP (Net restricted and unrestricted position) Public housing files Other major Programs

Public housing files Other")

14 Audit Items Auditors are Concerned With: Overstatement of Revenue (and short term assets) Understatement of Expenses (and short term liabilities) Bias in the MDA (Management Discussion and Analysis) Fraud Litigation Subsequent Events Financial Report FDS Information is by Program/Project Unaudited and Audited version Grant Reconciliation

15 Auditors They provide a level of Assurance However, They are external, and not part of the normal internal controls They come in after the fact They test on a sample basis, and There is a chance they may not test the areas that are a concern of the Board

16 2 Key Indicators PHAS General Overview MASS FASS SEMAP SEMAP 101 Indicators Defined and Common Errors

17 TERMS AND DEFINITIONS PHAS Public Housing Assessment System 4 subcomponents MASS Management Assessment Subsystem FASS Financial Assessment Subsystem PASS Physical Assessment Subsystem CFP Capital Fund Program SEMAP Section Eight Management Assessment Program PHA s use a little s it is a Public Housing Authority

18 The Real Estate Assessment Center (REAC) The Unaudited Process- PHA Draft HUD - REAC Review Final Score* Approved Rejected Invalidated *If audit is not required 18

19 The Real Estate Assessment Center (REAC) The Audited process: 19

20 GAAP Flyers

21 Accounting Briefs

22 PHAS Purpose PHAS helps the delivery of services in public housing and enhances trust in public housing system among PHAs, public housing residents, HUD and the general public by providing a management tool for effectively and fairly measuring the performance of a PHA in essential housing operations, including rewards for high performers and consequences for poor performers.

23 PHAS Background PHAs are not owned by the Federal Government United States Housing Act of 1937 Section 6(j) (1) The Secretary shall develop and publish in the Federal Register indicators to assess the management performance of public housing agencies and resident management corporations. The indicators shall be established under section 553 of title 5, United States Code. Such indicators shall enable the Secretary to evaluate the performance of public housing agencies and resident management corporations in all major areas of management operations.

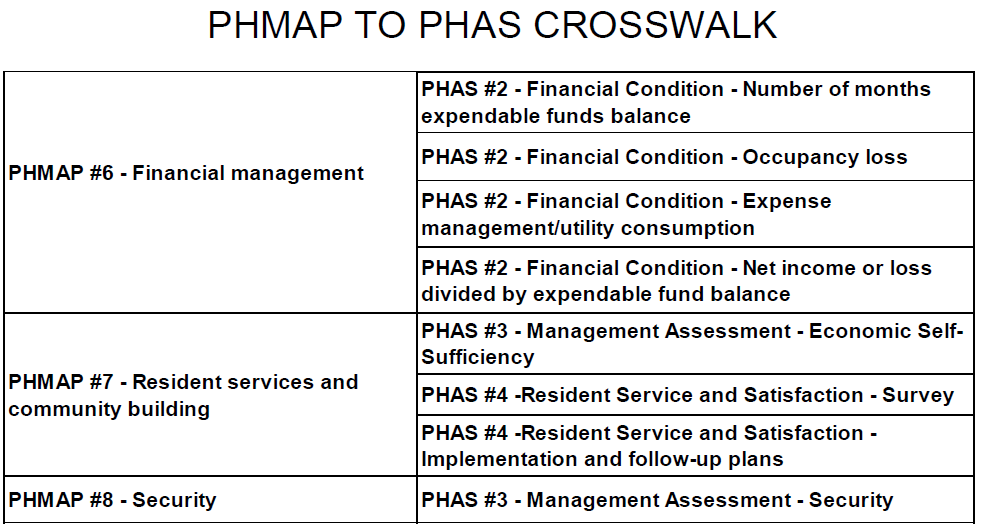

24 PHAS Background Decontrol Indicators Public Housing Management Assessment Program (PHMAP) 24CFR Part Present - Public Housing Assessment System (PHAS) 24CFR Part 902

25 PHAS Background October 1, 1998 PHAS Final Rule February 10, 2000 PHAS Amendments, Final Rule June 6, 2000 Transition Assistance for Certain PHAs Technical Correction, Final Rule July 24, 2003 Deregulation for Small PHAs, Final Rule

26 PHAS Background February 23, 2011 Interim PHAS Rule November 25, 2013 Capital Fund Program, Final Rule

27 PHAS Background

28 PHAS Background

29 Interim PHAS Data Sources

30 Scoring Summary of PHAS

31 PHAS Scoring

32 Improving PHAS Scores Monitor (too late if you wait until after year end) the status and accuracy of submissions frequently in eloccs, PIC, and Secure Systems. Utilize prior year PHAS score results to set annual goals. Plan ahead: be proactive in determining problem areas and fixing them at least 6 months in advance of PHAS due dates.

33 Ratios/formulas FASS

34 FASS 34

35 FDS Sample PHA: FYED: 3/31/14 Line Item No. Account Description Total AMPS Section 8 Housing Choice Voucher Program Cost Center Operating Fund Business Activities - Elimination 111 Cash - Unrestricted 1,823,090 67, ,462 17,476-2,333, Cash - Restricted - Modernization and Development Cash - other restricted 96,655 49, , Cash - Tenant Security Deposits 68, ,402-83, Cash - Restricted for payment of current liability Total Cash 1,988, , ,462 31,878-2,562,927 Total 35

36 Memo Accounts PHA: FYED: 3/31/14 Line Item No Account Description Total AMPS Section 8 Housing Choice Voucher Program Cost Center Operating Fund Business Activities - Elimination Excess (deficiency) of total revenue over (under) total expenses (76,967) (34,625) 150, , , Required annual debt principal payment - 98, , Beginning Equity 8,898, , , ,116-9,867,489 Prior Period Adjustments, Equity transfer and correction of errors Unit Months Available 4,995 3, , Number of Unit Months Leased 4,995 3, , Administrative Fee Equity - 59, , Housing Assistance Payments Equity - 42, , Excess Cash 1,594, ,594, Land Purchases Building Purchases Furniture & Equipment - Dwelling Purchases Furniture & Equipment - Administrative 18, ,231 Total 36

37 FASS 37

38 MENAR 38

39 Debt Service Coverage Ratio 39

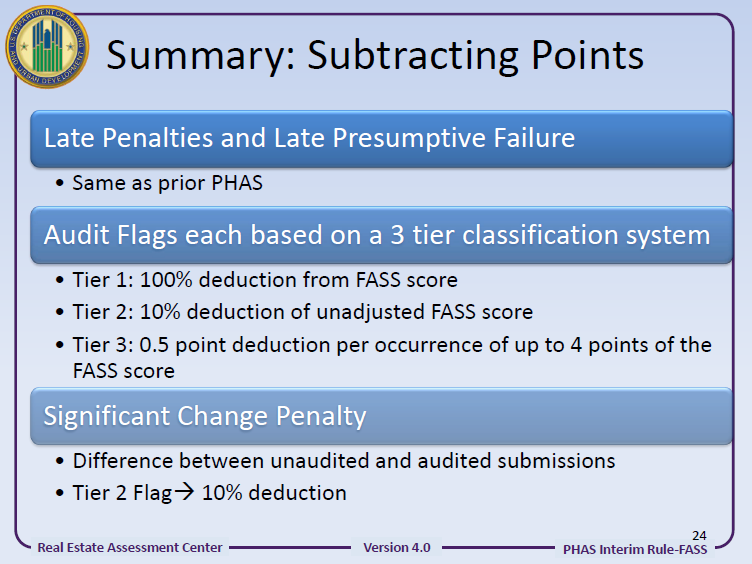

40 FASS - Score Adjustments 40

41 Score Adjustments 41

42 MASS Summary 42

43 MASS

44 MASS - Occupancy

45 MASS - Occupancy

46 MASS TARS

47 MASS TARS

48 MASS Accounts Payable

49 MASS Accounts Payable

50 SEMAP Overview Importance of Section 8 to the Authority What % of the PHA federal funds is Section 8 (more than 60%, almost 80% in some cases) How big is your waitlist and how many vouchers do you have HAP expense is generally the largest expense for most PHAs

51 Overview What are the direct and material compliance areas? Waitlist Inspections Reporting Payment Standards/reasonable rent Utility Allowance Eligibility - Tenant recertifications Timely Accurate

52 SEMAP 101 The Section Eight Management Assessment Program (SEMAP) measures the performance of PHAs that administer the housing choice voucher program in 14 key areas. SEMAP is completed annually by each PHA that administers a Section 8 tenant-based assistance program. The SEMAP certification is required to be submitted within 60 days after the end of the fiscal year. 52

53 SEMAP 101 SEMAP will help HUD target monitoring and assistance efforts to PHA programs that need the most improvement. The 14 indicators of performance show how well PHAs help eligible families afford decent rental units at a reasonable subsidy cost as intended by Federal housing legislation. 53

54 SEMAP - 14 requirements 1. Wait list 2. Reasonable Rent 3. Adjusted income 4. Utility allowance 5. HQS Quality Control 6. HQS Enforcement 7. Expanding housing assistance 8. Payment standards 9. Annual exams 10. Correct Tenant rent 11. Pre-contract HQS inspections 12. Annual HQS Inspections 13. Family Self Sufficiency 14. Bonus Deconcentration Bonus indicator

55 How does SEMAP work? Remotely measures a PHAs performance and administration of the Housing Choice Voucher Program HUD annually assigns a score for each indicator and an overall performance rating: > 90% - high performer 60 89% - standard < 60% - troubled A few instances create an automatic rating of troubled Late submission Auditor unable to issue an opinion on the financial statements or the Schedule of Expenditures of Federal Awards Inadequate performance on any indicator and/or a troubled rating results in the need for remedial action 55

56 What does remedial action entail? HUD will conduct an on-site review of PHAs that are rated as troubled The PHA must implement a corrective action plan that HUD will monitor, to ensure improvement in program management 56

57 So who verifies a PHA s compliance with the 14 self assessed SEMAP indicators? Your Independent Auditor! 57

58 What do Auditors use to test compliance? The Code of Federal Regulations, Title 24- Housing and Urban Development, Chapter 9 Office of Assistance Secretary for Public and Indian Housing OMB Circular A-133 Compliance Supplement 58

59 #1 Requirement for a successful audit DOCUMENTATION! Auditors must have a paper trail to follow Per CFR Per audit standards Most common SEMAP error HINT: all items organized, documented and available for your auditor to review keeps them out of your way! 59

60 HUD FORM 52648

61 HUD FORM

62 Per the CFR

63 Per the CFR

64 Indicator 1: Selection from the Waiting List Definition a) The PHA has written policies in its administrative plan for selecting applicants from the waiting list. b) Applicants reaching the top of the waiting list and applicants admitted were properly selected from the waiting list for admission and met the selection criteria that determined their place on the waiting list and their order of selection. 64

65 Indicator 1: Selection from the Waiting List - Purpose This indicator shows whether the PHA has written policies in its administrative plan for selecting applicants from the waiting list and whether the PHA follows these policies when admitting new tenants. Ensures that all eligible citizens are given a fair and equal chance to receive assistance. 65

66 Indicator 1: Selection from the Waiting List - Score Based on the quality control samples selected, documentation shows that 98% of the families in both samples were properly selected from the waiting list Yes 15 points No 0 Points 66

67 Indicator 1: Selection from the Waiting List - Sample Quality Control (QC) sample is an annual sample of files/records drawn in an unbiased manner and reviewed by the PHA supervisor Per 24 CFR 985.2(b): 67

(3)(i)(B) Note you must draw 2 separate samples to properly test this indicator Applicants reaching the top of the")

68 Indicator 1: Selection from the Waiting List - Sample Per 24 CFR 985.3(a)(3)(i)(B) Note you must draw 2 separate samples to properly test this indicator Applicants reaching the top of the waiting list Applicants admitted to the program 68

69 Indicator 1: Selection from the Waiting List Common Errors and Mistakes Improper samples Inadequate documentation to verify proper procedures Incorrect use of preferences Management override of admission policies Improper scoring If you do not meet the 98% threshold for both samples you must check No in the PHA response (All or nothing) 69

70 Indicator 2: Reasonable Rent Definition The PHA has and implements a reasonable written method to determine and document that the rent to owner is reasonable based on current rents for comparable unassisted units: At the time of initial leasing Before any increase in rent to owner At the HAP contract anniversary if there is a 5% decrease in published FMR in effect 60 days before the anniversary date 70

71 Indicator 2: Reasonable Rent Definition The PHA s method should also take into consideration the location, size, type, quality, and age of the program unit and similar unassisted units, and any amenities, housing services or utilities provided by owners 71

72 Indicator 2: Reasonable Rent Purpose To ensure that landlords are not inflating their rent thresholds due to the fact that the unit is being subsidized by the government To ensure that tenant rent payments are adjusted for any decreases in the FMR if applicable 72

73 Indicator 2: Reasonable Rent Score The PHA follows its written policy for determining rent reasonableness and has documented that rent is reasonable for: 98% of the units sampled 20 points 80 97% of the units sampled 15 points < 80% of the units sampled 0 points 73

74 Indicator 2: Reasonable Rent Sample Per 24 CFR 985.2(b) 74

75 Indicator 2: Reasonable Rent Common Errors and Mistakes Lack of documentation Comparing dissimilar units Using outdated information 75

76 Indicator 3: Determination of Adjusted Income - Definition The PHA s quality control sample of tenant files shows that at the time of admission and reexamination, the PHA properly obtained a third party verification of adjusted income or documented why third party verification was not available. 76

77 Indicator 3: Determination of Adjusted Income - Definition The PHA must also show that they used verified information in determining adjusted income; properly attributed allowances for expenses; and, when the family is responsible for utilities under a lease, the PHA used the appropriate utility allowances for the unit leased in determining the gross rent 77

78 Indicator 3: Determination of Adjusted Income - Purpose To ensure that the tenant rent payment is being calculated based on current and accurate information Remember the other side of the tenant payment is your HAP!! 78

79 Indicator 3: Determination of Adjusted Income - Score The PHA uses independent verification of income, properly attributes allowances and uses the appropriate utility allowances for: 90% or more of the families sampled 20 points 80 89% of the families sampled 15 points < 80% of the families sampled 0 points 79

80 Indicator 3: Determination of Adjusted Income - Sample Per 24 CFR 985.2(b) 80

81 Indicator 3: Determination of Adjusted Income Common Errors and Mistakes Lack of proper documentation Use of outdated information Incorrect annualization of third party information Incorrect calculation of medical expenses (pay attention to detail) Lack of support for a student > 18 years old Use of incorrect utility allowances Zero income tenants 81

82 Indicator 4: Utility Allowance Schedule Definition The PHA maintains an up-to-date utility allowance schedule The PHA reviews utility data once every 12 months and adjusts its utility allowance schedule if there is a change of 10% or more in the rates 82

83 Indicator 4: Utility Allowance Schedule Purpose To ensure that the tenant rent payment is being calculated based on current and accurate information 83

84 Indicator 4: Utility Allowance Schedule Score Documentation shows that the PHA reviewed utility rate data and properly adjusted the utility allowances if necessary Yes 5 points No 0 Points 84

85 Indicator 4: Utility Allowance Schedule Sample No sample for this indicator, you either did it or you didn t 85

86 Indicator 4: Utility Allowance Schedule Common Errors and Mistakes Not obtaining utility rate data every 12 months Not obtaining reliable data Not updating the allowances when required Not updating the information in the system when a change is made 86

87 Indicator 5: HQS Quality Control Inspections - Definition A PHA supervisor (or other qualified person) re-inspected a sample of units during the PHA fiscal year, for quality control of HQS inspections 87

88 Indicator 5: HQS Quality Control Inspections - Purpose To verify that HQS inspections are being performed timely and accurately and are properly tracked by the PHA HQS inspections are performed in order to ensure that the subsidized units are an adequate living environment for the tenants 88

89 Indicator 5: HQS Quality Control Inspections - Score Documentation shows that the PHA reperformed HQS inspections over a cross section of neighborhoods and inspectors Yes 5 points No 0 Points 89

90 Indicator 5: HQS Quality Control Inspections - Sample Per 24 CFR 985.2(b) The PHA s reinspected sample must be drawn from recently completed HQS inspections and represents a cross section of neighborhoods and the work of a cross section of inspectors. 90

91 Indicator 5: HQS Quality Control Inspections Common Errors and Mistakes Annual inspections are not performed Lack of documentation Re - inspections were not performed, or not performed by a supervisor or other qualified individual Sample was not representative of a cross section of neighborhoods and/or inspectors The intent of the reinspection is a QC on the initial inspection. Not an inspection because we need an inspection. ( Quality Control of the Initial Inspection) 91

92 Indicator 6: HQS Enforcement Definition The PHA s quality control sample of case files with failed HQS inspections shows that for all cases sampled: any cited life-threatening deficiencies were corrected within 24 hours from the inspections all other cited HQS deficiencies were corrected within no more than 30 calendar days (or less per admin plan could be 14 days) from the inspection or any PHA approved extensions 92

93 Indicator 6: HQS Enforcement Definition If the HQS deficiencies were not corrected within the required time frame the PHA must: Stop housing assistance payments beginning no later than the first of the month following the specified correction period (abatement) or Take prompt and vigorous action to enforce the family obligations 93

94 Indicator 6: HQS Enforcement Purpose To ensure that HCVP tenants are living in acceptable conditions To ensure that the landlord is properly maintaining the property 94

95 Indicator 6: HQS Enforcement Score Documentation shows that the PHA s QC sample of failed inspections were properly corrected or abated within the appropriate time frame > 98% - 10 points < 98% - 0 points 95

96 Indicator 6: HQS Enforcement Sample Per 24 CFR 985.2(b) 96

97 Indicator 6: HQS Enforcement Common Errors and Mistakes Annual inspections are not performed Incorrect universe used in selecting the sample Follow up of failed inspections not performed timely HAP not abated timely 97

98 SEMAP - 14 requirements 1. Wait list 2. Reasonable Rent 3. Adjusted income 4. Utility allowance 5. HQS Quality Control 6. HQS Enforcement 7. Expanding housing assistance 8. Payment standards 9. Annual exams 10. Correct Tenant rent 11. Pre-contract HQS inspections 12. Annual HQS Inspections 13. Family Self Sufficiency 14. Bonus Deconcentration Bonus indicator

99 Questions or Comments? 99

UNDERSTANDING SECTION EIGHT MANAGEMENT ASSESSMENT PROGRAM (SEMAP)

") UNDERSTANDING SECTION EIGHT MANAGEMENT ASSESSMENT PROGRAM (SEMAP) The Section Eight Management Assessment Program (SEMAP) is HUD s performance measurement tool for the Housing Choice Voucher Program. A

UNDERSTANDING SECTION EIGHT MANAGEMENT ASSESSMENT PROGRAM (SEMAP) The Section Eight Management Assessment Program (SEMAP) is HUD s performance measurement tool for the Housing Choice Voucher Program. A

Office of Public and Indian Housing, Real Estate Assessment Center. Capital Fund Program Reporting ACCOUNTING BRIEF #15

Office of Public and Indian Housing, Real Estate Assessment Center PIH-REAC: PHA-Finance Accounting Briefs Issued Date: August 2011 Capital Fund Program Reporting ACCOUNTING BRIEF #15 GOVERNING REGULATIONS

Office of Public and Indian Housing, Real Estate Assessment Center PIH-REAC: PHA-Finance Accounting Briefs Issued Date: August 2011 Capital Fund Program Reporting ACCOUNTING BRIEF #15 GOVERNING REGULATIONS

State and Area Coordinators

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Public and Indian Housing Special Attention of Notice PIH-2012-21 (HA) Public Housing Agencies administering Housing Choice Voucher Programs Public

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Office of Public and Indian Housing Special Attention of Notice PIH-2012-21 (HA) Public Housing Agencies administering Housing Choice Voucher Programs Public

Clarification of Public Housing Authority Reporting Requirements and OMB Circular A-133 Implications (Accounting Issue # 10)

") Clarification of Public Housing Authority Reporting Requirements and OMB Circular A-133 Implications (Accounting Issue # 10) Background Financial Data Schedule (FDS) submissions are reviewed by HUD s Real

Clarification of Public Housing Authority Reporting Requirements and OMB Circular A-133 Implications (Accounting Issue # 10) Background Financial Data Schedule (FDS) submissions are reviewed by HUD s Real

GUAM HOUSING AND URBAN RENEWAL AUTHORITY. SINGLE AUDIT AND HUD REPORTS And SUPPLEMENTARY INFORMTION

GUAM HOUSING AND URBAN RENEWAL AUTHORITY SINGLE AUDIT AND HUD REPORTS And SUPPLEMENTARY INFORMTION FOR THE YEAR ENDED SEPTEMBER 30, 2014 SAIPAN Family Building, Suite 201 PMB 297 Box 10000 Saipan, MP 96950

GUAM HOUSING AND URBAN RENEWAL AUTHORITY SINGLE AUDIT AND HUD REPORTS And SUPPLEMENTARY INFORMTION FOR THE YEAR ENDED SEPTEMBER 30, 2014 SAIPAN Family Building, Suite 201 PMB 297 Box 10000 Saipan, MP 96950

HUD Property Audits: A Property Manager s Perspective

HUD Property Audits: A Property Manager s Perspective How Best to Prepare / Common Findings in an Audit Objective This session will discuss HUD Property audits from a site manager s perspective covering:

HUD Property Audits: A Property Manager s Perspective How Best to Prepare / Common Findings in an Audit Objective This session will discuss HUD Property audits from a site manager s perspective covering:

Real Estate Assessment Center. Summary of Financial Reporting and Auditing Guidance for HUD Multifamily Program Participants and Independent Auditors

Real Estate Assessment Center Summary of Financial Reporting and Auditing Guidance for HUD Multifamily Program Participants and Independent Auditors Table of Contents Real Estate Assessment Center... 1

Real Estate Assessment Center Summary of Financial Reporting and Auditing Guidance for HUD Multifamily Program Participants and Independent Auditors Table of Contents Real Estate Assessment Center... 1

Request for Proposals Software to Support Management of Federal Housing Programs

INTRODUCTION Request for Proposals Software to Support Management of Federal Housing Programs Through this Request for Proposals ( RFP ), Rhode Island Housing seeks proposals from qualified firms to provide

INTRODUCTION Request for Proposals Software to Support Management of Federal Housing Programs Through this Request for Proposals ( RFP ), Rhode Island Housing seeks proposals from qualified firms to provide

HUD. Ginnie Mae. Fair. Housing. Housing. Inspector General. Public and Indian. Housing. Center for Faith-Based Partnerships

U.S. Department of Housing and Urban Development (HUD) 2 Ginnie Mae Public and Indian Housing Center for Faith-Based Partnerships Community Planning and Development HUD Inspector General Departmental Enforcement

U.S. Department of Housing and Urban Development (HUD) 2 Ginnie Mae Public and Indian Housing Center for Faith-Based Partnerships Community Planning and Development HUD Inspector General Departmental Enforcement

Harlan Stewart, Director, Region X Office of Public Housing, 0APH. Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region X, 0AGA

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Issue Date January 9, 2009 Audit Report Number 2009-SE-1001 TO: Harlan Stewart, Director, Region X Office of Public Housing, 0APH FROM: Joan S. Hobbs, Regional Inspector General for Audit, Seattle, Region

Session 7: Public Housing Capital Fund Program

FASS PH Session 7: Public Housing Capital Fund Program Summer 2014 Overview Financial Data Schedule (FDS) reporting requirements for the CFP Program Reporting of soft and hard costs associated with the

FASS PH Session 7: Public Housing Capital Fund Program Summer 2014 Overview Financial Data Schedule (FDS) reporting requirements for the CFP Program Reporting of soft and hard costs associated with the

William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing, 3FPH

Issue Date October 17, 2005 Audit Report Number 2006-PH-1002 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing,

Issue Date October 17, 2005 Audit Report Number 2006-PH-1002 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH Robert Jennings, Director, Richmond Office of Public Housing,

EHDOC Robert Sharp Towers II Limited Partnership (A Florida Limited Partnership) Financial Report October 31, 2014

Financial Report October 31, 2014") EHDOC Robert Sharp Towers II Limited Partnership Financial Report October 31, 2014 Contents Independent Auditor's Report 1 Financial Statements Balance sheet 2 3 Statement of income 4 Statement of changes

EHDOC Robert Sharp Towers II Limited Partnership Financial Report October 31, 2014 Contents Independent Auditor's Report 1 Financial Statements Balance sheet 2 3 Statement of income 4 Statement of changes

CHAPTER 19 HUD REPORTING REQUIREMENTS, PHA INTERNAL MONITORING REQUIREMENTS

Table of Content CHAPTER 19... 19-1 HUD REPORTING REQUIREMENTS,... 19-1 PHA INTERNAL MONITORING REQUIREMENTS... 19-1 19.1 Chapter Overview... 19-1 19.2 Multifamily Tenant Characteristics System (MTCS)

Table of Content CHAPTER 19... 19-1 HUD REPORTING REQUIREMENTS,... 19-1 PHA INTERNAL MONITORING REQUIREMENTS... 19-1 19.1 Chapter Overview... 19-1 19.2 Multifamily Tenant Characteristics System (MTCS)

Checks and Balances Internal Controls. West Virginia State Auditor s Office Chief Inspector Division

Checks and Balances Internal Controls West Virginia State Auditor s Office Chief Inspector Division POP QUIZ Internal Controls Internal Controls The auditor will test the effectiveness of your internal

Checks and Balances Internal Controls West Virginia State Auditor s Office Chief Inspector Division POP QUIZ Internal Controls Internal Controls The auditor will test the effectiveness of your internal

U.S. Department of Housing and Urban Development Office of Public and Indian Housing

U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention: NOTICE: PIH 2016-08 (HA) Public Housing Agencies; Public Housing Directors Issued: May 6, 2016 Expires:

U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention: NOTICE: PIH 2016-08 (HA) Public Housing Agencies; Public Housing Directors Issued: May 6, 2016 Expires:

Office of Public and Indian Housing, Real Estate Assessment Center

Office of Public and Indian Housing, Real Estate Assessment Center PIH-REAC: PHA-Finance Accounting Briefs Issued Date: June 2013 Revenue Recognition for Housing Assistance Payments and Administrative

Office of Public and Indian Housing, Real Estate Assessment Center PIH-REAC: PHA-Finance Accounting Briefs Issued Date: June 2013 Revenue Recognition for Housing Assistance Payments and Administrative

Pontiac ILF Limited Dividend Housing Association Limited Partnership HUD Project No. 044-35621

Pontiac ILF Limited Dividend Housing Association Financial Report with Supplemental Information December 31, 2013 Certificate of Partners I certify that I have examined the attached financial statements

Pontiac ILF Limited Dividend Housing Association Financial Report with Supplemental Information December 31, 2013 Certificate of Partners I certify that I have examined the attached financial statements

Real Estate Assessment Center PHA- Finance

Real Estate Assessment Center PHA- Finance FINANCIAL INDICATOR METHODOLOGY & ANALYSIS GUIDE (For FYE 9/30/03 through 6/30/06) September 12, 2003 TABLE OF CONTENTS SUMMARY OF CHANGES... 1 I. EFFECTIVE PERIOD...

Real Estate Assessment Center PHA- Finance FINANCIAL INDICATOR METHODOLOGY & ANALYSIS GUIDE (For FYE 9/30/03 through 6/30/06) September 12, 2003 TABLE OF CONTENTS SUMMARY OF CHANGES... 1 I. EFFECTIVE PERIOD...

Contact Information. Oklahoma City Housing Authority 1700 Northeast Fourth Street Oklahoma City, Oklahoma 73117-3800 405-239-7551

Contact Information Oklahoma City Housing Authority 1700 Northeast Fourth Street Oklahoma City, Oklahoma 73117-3800 405-239-7551 Executive Director Director Leasing/Rental Assistance Family Self-Sufficiency

Contact Information Oklahoma City Housing Authority 1700 Northeast Fourth Street Oklahoma City, Oklahoma 73117-3800 405-239-7551 Executive Director Director Leasing/Rental Assistance Family Self-Sufficiency

CHAPTER 7 PAYMENT STANDARDS

Table of Contents CHAPTER 7 PAYMENT STANDARDS 7-1 7.1 Chapter Overview 7-1 7.2 Establishing Payment Standard Amounts 7-2 Payment Standard Amounts within the Basic Range 7-2 Payment Standard Amounts Based

Table of Contents CHAPTER 7 PAYMENT STANDARDS 7-1 7.1 Chapter Overview 7-1 7.2 Establishing Payment Standard Amounts 7-2 Payment Standard Amounts within the Basic Range 7-2 Payment Standard Amounts Based

Understanding SRO. January 2001

Understanding SRO January 2001 The Single Room Occupancy (SRO) program is authorized by Section 441 of the McKinney- Vento Homeless Assistance Act. Under the program, HUD enters into Annual Contributions

Understanding SRO January 2001 The Single Room Occupancy (SRO) program is authorized by Section 441 of the McKinney- Vento Homeless Assistance Act. Under the program, HUD enters into Annual Contributions

Financial Statements and Independent Auditor s Report. DDC Foothills Home (A Colorado Nonprofit Corporation) FHA Project No. 101 HD023 NP PD DD

FHA Project No. 101 HD023 NP PD DD") Financial Statements and Independent Auditor s Report DDC Foothills Home June 30, 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 4 FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION 6 STATEMENT

Financial Statements and Independent Auditor s Report DDC Foothills Home June 30, 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 4 FINANCIAL STATEMENTS STATEMENT OF FINANCIAL POSITION 6 STATEMENT

REQUEST FOR PROPOSAL And STATEMENT OF QUALIFICATIONS FOR INDEPENDENT AUDIT SERVICES

HOUSING AUTHORITY OF THE CITY OF HOMESTEAD REQUEST FOR PROPOSAL And STATEMENT OF QUALIFICATIONS FOR INDEPENDENT AUDIT SERVICES AUGUST 3, 2015 HOMESTEAD HOUSING AUTHORITY 29355 South Federal Highway Homestead,

HOUSING AUTHORITY OF THE CITY OF HOMESTEAD REQUEST FOR PROPOSAL And STATEMENT OF QUALIFICATIONS FOR INDEPENDENT AUDIT SERVICES AUGUST 3, 2015 HOMESTEAD HOUSING AUTHORITY 29355 South Federal Highway Homestead,

MULTIFAMILY FINANCIAL REPORTING REVISIONS TABLE OF CONTENTS

MULTIFAMILY FINANCIAL REPORTING REVISIONS TABLE OF CONTENTS OVERVIEW REAC CHART OF ACCOUNT REVISIONS SUPPLEMENTAL COMPLIANCE DATA REVISIONS FINANCIAL STATEMENT SUBMISSION REVISIONS APPENDIX NO. 1 SIDE-BY-SIDE

MULTIFAMILY FINANCIAL REPORTING REVISIONS TABLE OF CONTENTS OVERVIEW REAC CHART OF ACCOUNT REVISIONS SUPPLEMENTAL COMPLIANCE DATA REVISIONS FINANCIAL STATEMENT SUBMISSION REVISIONS APPENDIX NO. 1 SIDE-BY-SIDE

ILLINOIS HOUSING DEVELOPMENT AUTHORITY FINANCIAL REPORTING GUIDELINES FOR MORTGAGORS OF MULTIFAMILY HOUSING PROJECTS

ILLINOIS HOUSING DEVELOPMENT AUTHORITY FINANCIAL REPORTING GUIDELINES FOR MORTGAGORS OF MULTIFAMILY HOUSING PROJECTS Rev 12/2012 TABLE OF CONTENTS Page I. Introduction 3 II. Accounting and Audit Requirements

ILLINOIS HOUSING DEVELOPMENT AUTHORITY FINANCIAL REPORTING GUIDELINES FOR MORTGAGORS OF MULTIFAMILY HOUSING PROJECTS Rev 12/2012 TABLE OF CONTENTS Page I. Introduction 3 II. Accounting and Audit Requirements

PHA 5-Year and Annual Plan

PHA 5-Year and Annual Plan U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 Expires 4/30/2011 1.0 PHA Information PHA Name: Housing Authority of the

PHA 5-Year and Annual Plan U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 Expires 4/30/2011 1.0 PHA Information PHA Name: Housing Authority of the

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC.

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC. RNO 140000 Report No. AU 16-05 March 2016 www.oig.lsc.gov TABLE OF CONTENTS

LEGAL SERVICES CORPORATION OFFICE OF INSPECTOR GENERAL FINAL REPORT ON SELECTED INTERNAL CONTROLS RHODE ISLAND LEGAL SERVICES, INC. RNO 140000 Report No. AU 16-05 March 2016 www.oig.lsc.gov TABLE OF CONTENTS

GENEVA HOUSE, INC. PROJECT NO. 034-44815NP FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND 2008 FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31,

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2009 AND 2008 FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31,

GENEVA HOUSE, INC. PROJECT NO. 034-11177 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2014 AND

FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2014 AND 2013 CONTENTS INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position

FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2014 AND 2013 CONTENTS INDEPENDENT AUDITOR S REPORT 1-2 FINANCIAL STATEMENTS Statements of Financial Position

CHAPTER 20 FINANCIAL MANAGEMENT

Table of Contents CHAPTER 20... 20-1 Financial Management... 20-1 20.1 Chapter Overview... 20-1 20.2 Financial Management Requirements... 20-1 20.3 Budgeting... 20-2 Estimating Housing Assistance Payments...

Table of Contents CHAPTER 20... 20-1 Financial Management... 20-1 20.1 Chapter Overview... 20-1 20.2 Financial Management Requirements... 20-1 20.3 Budgeting... 20-2 Estimating Housing Assistance Payments...

GENEVA HOUSE, INC. PROJECT NO. 034-11177 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2013 AND

FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2013 AND 2012 CONTENTS INDEPENDENT AUDITOR S REPORT ON THE FINANCIAL STATEMENTS 1-2 FINANCIAL STATEMENTS

FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2013 AND 2012 CONTENTS INDEPENDENT AUDITOR S REPORT ON THE FINANCIAL STATEMENTS 1-2 FINANCIAL STATEMENTS

Monthly Status Update on Berkeley Housing Authority

Office of the Executive Officer INFORMATION CALENDAR May 23, 2006 To: From: Honorable Chairperson and Members of the Housing Authority Phil Kamlarz, Executive Officer Submitted by: Stephen Barton, Housing

Office of the Executive Officer INFORMATION CALENDAR May 23, 2006 To: From: Honorable Chairperson and Members of the Housing Authority Phil Kamlarz, Executive Officer Submitted by: Stephen Barton, Housing

GENEVA HOUSE, INC. PROJECT NO. 034-44815NP FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2011 AND

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2011 AND 2010 CONTENTS INDEPENDENT AUDITOR S REPORT ON THE FINANCIAL STATEMENTS 1-2 FINANCIAL STATEMENTS Statements

FINANCIAL REPORT WITH SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2011 AND 2010 CONTENTS INDEPENDENT AUDITOR S REPORT ON THE FINANCIAL STATEMENTS 1-2 FINANCIAL STATEMENTS Statements

Changes in Financial Management and Reporting for Public Housing Agencies Under the New Operating Fund Rule (24 CFR part 990)

") Changes in Financial Management and Reporting for Public Housing Agencies Under the New Operating Fund Rule (24 CFR part 990) Supplement to HUD Handbook 7475.1 REV., CHG-1, Financial Management Handbook

Changes in Financial Management and Reporting for Public Housing Agencies Under the New Operating Fund Rule (24 CFR part 990) Supplement to HUD Handbook 7475.1 REV., CHG-1, Financial Management Handbook

Financial Data Schedule Line Definition Guide

Office of Public and Indian Housing, Real Estate Assessment Center Financial Assessment Subsystem Public Housing (FASS-PH) Financial Data Schedule Line Definition Guide (FYE 12/31/2013 and forward) Updated

Office of Public and Indian Housing, Real Estate Assessment Center Financial Assessment Subsystem Public Housing (FASS-PH) Financial Data Schedule Line Definition Guide (FYE 12/31/2013 and forward) Updated

William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

CHAPTER 2. OCCUPANCY AUDIT PROCEDURES. Section 1. Scope of the Audit

CHAPTER 2. OCCUPANCY AUDIT PROCEDURES Section 1. Scope of the Audit 2-1. OVERVIEW. The occupancy audit includes a review of PHA admission and occupancy policies, tenant selection, leasing practices, rent

CHAPTER 2. OCCUPANCY AUDIT PROCEDURES Section 1. Scope of the Audit 2-1. OVERVIEW. The occupancy audit includes a review of PHA admission and occupancy policies, tenant selection, leasing practices, rent

Supportive Housing Program (SHP) Self-Monitoring Tools

Self-Monitoring Tools") Supportive Housing Program (SHP) Self-Monitoring Tools U.S. Department of Housing and Urban Development Office of Community Planning and Development Table of Contents INTRODUCTION...1 TOOL 1 MEASURING

Supportive Housing Program (SHP) Self-Monitoring Tools U.S. Department of Housing and Urban Development Office of Community Planning and Development Table of Contents INTRODUCTION...1 TOOL 1 MEASURING

GUIDELINES ON REPORTING AND ATTESTATION REQUIREMENTS OF UNIFORM FINANCIAL REPORTING STANDARDS (UFRS)

") GUIDELINES ON REPORTING AND ATTESTATION REQUIREMENTS OF UNIFORM FINANCIAL REPORTING STANDARDS (UFRS) For Public Housing Authorities Not- for- Profit Multifamily Program Participants For- Profit Multifamily

GUIDELINES ON REPORTING AND ATTESTATION REQUIREMENTS OF UNIFORM FINANCIAL REPORTING STANDARDS (UFRS) For Public Housing Authorities Not- for- Profit Multifamily Program Participants For- Profit Multifamily

Walter Kreher, Director, Multifamily Program Center, 2FHM. Alexander C. Malloy, Regional Inspector General for Audit, 2AGA INTRODUCTION

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE

CHAPTER 5. DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE 5-1 Program Objective. Multifamily projects are an integral part of the U.S. Department of Housing and Urban Development s (HUD) housing programs,

CHAPTER 5. DEVELOPMENT COST CERTIFICATION AUDIT GUIDANCE 5-1 Program Objective. Multifamily projects are an integral part of the U.S. Department of Housing and Urban Development s (HUD) housing programs,

Workers Compensation Commission

Audit Report Workers Compensation Commission March 2012 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

Audit Report Workers Compensation Commission March 2012 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA. U.S. Department of Housing and Urban Development, Washington, DC. Home Equity Conversion Mortgage Program

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA U.S. Department of Housing and Urban Development, Washington, DC Home Equity Conversion Mortgage Program 2014-PH-0001 SEPTEMBER 30, 2014 Issue Date: September

OFFICE OF AUDIT REGION 3 PHILADELPHIA, PA U.S. Department of Housing and Urban Development, Washington, DC Home Equity Conversion Mortgage Program 2014-PH-0001 SEPTEMBER 30, 2014 Issue Date: September

Robert P. Cwieka, Acting Director, Public Housing, 1APH. John A. Dvorak, Regional Inspector General for Audit, Boston Region, 1AGA

Issue Date March 21, 2012 Audit Report Number 2012-BO-1003 TO: Robert P. Cwieka, Acting Director, Public Housing, 1APH FROM: John A. Dvorak, Regional Inspector General for Audit, Boston Region, 1AGA SUBJECT:

Issue Date March 21, 2012 Audit Report Number 2012-BO-1003 TO: Robert P. Cwieka, Acting Director, Public Housing, 1APH FROM: John A. Dvorak, Regional Inspector General for Audit, Boston Region, 1AGA SUBJECT:

Oklahoma Workers Compensation Commission

OPERATIONAL AUDIT Oklahoma Workers Compensation Commission For the period February 1, 2014 through June 30, 2015 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE Audit Report of the Oklahoma

OPERATIONAL AUDIT Oklahoma Workers Compensation Commission For the period February 1, 2014 through June 30, 2015 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE Audit Report of the Oklahoma

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA. Marina Village Apartments Sparks, NV. Section 221(d)(4) Multifamily Insurance Program

(4) Multifamily Insurance Program") OFFICE OF AUDIT REGION 9 LOS ANGELES, CA Marina Village Apartments Sparks, NV Section 221(d)(4) Multifamily Insurance Program 2014-LA-1001 OCTOBER 24, 2013 Issue Date: October 24, 2013 Audit Report Number:

OFFICE OF AUDIT REGION 9 LOS ANGELES, CA Marina Village Apartments Sparks, NV Section 221(d)(4) Multifamily Insurance Program 2014-LA-1001 OCTOBER 24, 2013 Issue Date: October 24, 2013 Audit Report Number:

HPRP Grantee Monitoring Toolkit

HPRP Grantee Monitoring Toolkit About this Toolkit The Homelessness Prevention and Rapid Re-Housing Program (HPRP) provides communities with substantial resources for preventing and ending homelessness.

HPRP Grantee Monitoring Toolkit About this Toolkit The Homelessness Prevention and Rapid Re-Housing Program (HPRP) provides communities with substantial resources for preventing and ending homelessness.

Financial Information Kit

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

STATE OF INDIANA. October 3, 2013. Board of Directors Fremont Housing Authority 3160 Spring Street Fremont, IN 46737

STATE OF INDIANA AN EQUAL OPPORTUNITY EMPLOYER STATE BOARD OF ACCOUNTS 302 WEST WASHINGTON STREET ROOM E418 INDIANAPOLIS, INDIANA 46204-2765 Telephone: (317) 232-2513 Fax: (317) 232-4711 Web Site: www.in.gov/sboa

STATE OF INDIANA AN EQUAL OPPORTUNITY EMPLOYER STATE BOARD OF ACCOUNTS 302 WEST WASHINGTON STREET ROOM E418 INDIANAPOLIS, INDIANA 46204-2765 Telephone: (317) 232-2513 Fax: (317) 232-4711 Web Site: www.in.gov/sboa

General Overview of Financial Management

1 General Overview of Financial Management U.S. Department of Housing and Urban Development Office of Community Planning and Development 2 Compliance Monitoring 3 Compliance Monitoring Types of Compliance

1 General Overview of Financial Management U.S. Department of Housing and Urban Development Office of Community Planning and Development 2 Compliance Monitoring 3 Compliance Monitoring Types of Compliance

BOSTONPOST PROPERTY MANAGER

Bostonpost Affordable Housing Property Manager BOSTONPOST PROPERTY MANAGER mrisoftware.com 2012 MRI Software, LLC. All Rights reserved. 1.800.321.8770 sales@mrisoftware.com 1 BPPM09121 SOLUTION FOR AFFORDABLE

Bostonpost Affordable Housing Property Manager BOSTONPOST PROPERTY MANAGER mrisoftware.com 2012 MRI Software, LLC. All Rights reserved. 1.800.321.8770 sales@mrisoftware.com 1 BPPM09121 SOLUTION FOR AFFORDABLE

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Rent Calculation. Caleb Kopczyk, PHRS US Department of Housing and Urban Development

Rent Calculation Caleb Kopczyk, PHRS US Department of Housing and Urban Development Goals At the end of the day, what will we be able to know and do? Know the elements of annual income Understand the verification

Rent Calculation Caleb Kopczyk, PHRS US Department of Housing and Urban Development Goals At the end of the day, what will we be able to know and do? Know the elements of annual income Understand the verification

Audited Financial Statements Handbook For Multifamily Rental Housing

Audited Financial Statements Handbook For Multifamily Rental Housing California Department of Housing and Community Development California Housing Finance Agency Last Revised: March 2015 Foreword Hcd CalHFA

Audited Financial Statements Handbook For Multifamily Rental Housing California Department of Housing and Community Development California Housing Finance Agency Last Revised: March 2015 Foreword Hcd CalHFA

Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services

Accounting Services") Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services I. Instructions Upland Housing Authority (UHA) is seeking price quotations from qualified individuals or organizations to provide

Request for Quotes Small Purchase (Hourly Rate Pricing) Accounting Services I. Instructions Upland Housing Authority (UHA) is seeking price quotations from qualified individuals or organizations to provide

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

!" #$%&$'$!" #$%&$''

!"#$%&$'$!"#$%&$'' 2 TABLE OF CONTENTS I. RFP - Single Audit Specifications (Pages 3-10) Purpose of Request For Proposal Single Audit Requirements Scope of Examination Proposal Conditions Evaluation of

!"#$%&$'$!"#$%&$'' 2 TABLE OF CONTENTS I. RFP - Single Audit Specifications (Pages 3-10) Purpose of Request For Proposal Single Audit Requirements Scope of Examination Proposal Conditions Evaluation of

FINANCIAL STATEMENT PREPARATION GUIDE

FINANCIAL STATEMENT PREPARATION GUIDE 2013 Table of Contents Page FINANCIAL STATEMENT REQUIREMENTS.. 3 SAMPLE FINANCIAL STATEMENTS... 4 Independent Auditors Report 6 Balance Sheet. 8 Statement of Operations.

FINANCIAL STATEMENT PREPARATION GUIDE 2013 Table of Contents Page FINANCIAL STATEMENT REQUIREMENTS.. 3 SAMPLE FINANCIAL STATEMENTS... 4 Independent Auditors Report 6 Balance Sheet. 8 Statement of Operations.

How To Pay Rent On A Rental Property

Ten Things to Know about RAD When Advising PHAs Gregory A. Byrne RAD Network Partners Workshop August 28, 2013 1. Contract Rents Referred to as current funding Amounts can be found in: RAD Inventory Assessment

Ten Things to Know about RAD When Advising PHAs Gregory A. Byrne RAD Network Partners Workshop August 28, 2013 1. Contract Rents Referred to as current funding Amounts can be found in: RAD Inventory Assessment

U.S. Department of Housing and Urban Development Office of Public and Indian Housing

U.S. Department of Housing and Urban Development Office of Public and Indian Housing PHA Plans Annual Plan for Fiscal Year 2004 NOTE: THIS PHA PLANS TEMPLATE () IS TO BE COMPLETED IN ACCORDANCE WITH INSTRUCTIONS

U.S. Department of Housing and Urban Development Office of Public and Indian Housing PHA Plans Annual Plan for Fiscal Year 2004 NOTE: THIS PHA PLANS TEMPLATE () IS TO BE COMPLETED IN ACCORDANCE WITH INSTRUCTIONS

The University Of California Home Loan Program Corporation (A Component Unit of the University of California)

") Report Of Independent Auditors And Financial Statements The University Of California Home Loan Program Corporation (A Component Unit of the University of California) As of and for the periods ended June

Report Of Independent Auditors And Financial Statements The University Of California Home Loan Program Corporation (A Component Unit of the University of California) As of and for the periods ended June

MEMORANDUM FOR: K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

DCHFA Project Performance Review and Financial Reporting Update Sichao Bai DCHFA Agenda 2010 Project Assessment Review Project Financial Characteristics Financial i Performance Trend Distressed Projects

DCHFA Project Performance Review and Financial Reporting Update Sichao Bai DCHFA Agenda 2010 Project Assessment Review Project Financial Characteristics Financial i Performance Trend Distressed Projects

HCV FREQUENTLY ASKED QUESTIONS

HCV FREQUENTLY ASKED QUESTIONS What is the Housing Choice Voucher program? The Housing Choice Voucher (HCV) program, formerly referred to as Section 8, provides housing assistance payments to help income

HCV FREQUENTLY ASKED QUESTIONS What is the Housing Choice Voucher program? The Housing Choice Voucher (HCV) program, formerly referred to as Section 8, provides housing assistance payments to help income

United States Chemical Safety and Hazard Investigation Board

United States Chemical Safety and Hazard Investigation Board Audit of Financial Statements As of and for the Years Ended September 30, 2005 and 2004 Submitted By Leon Snead & Company, P.C. Certified Public

United States Chemical Safety and Hazard Investigation Board Audit of Financial Statements As of and for the Years Ended September 30, 2005 and 2004 Submitted By Leon Snead & Company, P.C. Certified Public

REQUEST FOR PROPOSALS

REQUEST FOR PROPOSALS The Housing Authority of the city of Pocatello (HACP) is requesting proposals to perform an Annual Audit of the entire operations of the Authority, in compliance with the Single Audit

REQUEST FOR PROPOSALS The Housing Authority of the city of Pocatello (HACP) is requesting proposals to perform an Annual Audit of the entire operations of the Authority, in compliance with the Single Audit

Section 8 Housing Choice Voucher Program

Section 8 Housing Choice Voucher Program Housing Authority of Lackawanna County 145 Railroad Avenue, Peckville, PA 18452 Tel: (570) 489-3972 Fax: (570) 382-8906 Email: HALackawanna@hacl.org Landlord Handbook

Section 8 Housing Choice Voucher Program Housing Authority of Lackawanna County 145 Railroad Avenue, Peckville, PA 18452 Tel: (570) 489-3972 Fax: (570) 382-8906 Email: HALackawanna@hacl.org Landlord Handbook

LIVE-IN AIDES AND THE HOUSING CHOICE VOUCHER PROGRAM

F A C T S H E E T AUGUST 2003 Written by: Lisa Sloane Sloane Associates 160 Orchard St. Lee, MA 01238 Emily Cooper and Ann O Hara The Technical Assistance Collaborative, Inc. 535 Boylston St, Ste. 1301

F A C T S H E E T AUGUST 2003 Written by: Lisa Sloane Sloane Associates 160 Orchard St. Lee, MA 01238 Emily Cooper and Ann O Hara The Technical Assistance Collaborative, Inc. 535 Boylston St, Ste. 1301

CHAPTER 7. RECERTIFICATION, UNIT TRANSFERS, AND GROSS RENT CHANGES

CHAPTER 7. RECERTIFICATION, UNIT TRANSFERS, AND GROSS RENT CHANGES 7-1 Introduction A. As discussed in Chapter 5, a family s eligibility for assistance is based on its income, as determined in accordance

CHAPTER 7. RECERTIFICATION, UNIT TRANSFERS, AND GROSS RENT CHANGES 7-1 Introduction A. As discussed in Chapter 5, a family s eligibility for assistance is based on its income, as determined in accordance

Property Management Services

Property Management Services KMG Prestige is committed to excellence in the delivery of comprehensive and innovative property management services Administration Accounting Maintenance Marketing Risk Management

Property Management Services KMG Prestige is committed to excellence in the delivery of comprehensive and innovative property management services Administration Accounting Maintenance Marketing Risk Management

If a Not-for-profit organization has an organizational audit, it should be submitted with the property audit.

AUDIT REQUIREMENTS All WHEDA-financed & ARRA developments, unless notified previously, are required to submit an annual audited financial statement within 60 days of fiscal year end. If a Not-for-profit

AUDIT REQUIREMENTS All WHEDA-financed & ARRA developments, unless notified previously, are required to submit an annual audited financial statement within 60 days of fiscal year end. If a Not-for-profit

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of All Multifamily Hub Directors Notice H 2011-05

AUDIT GUIDE FOR SECTION 8 MULTI-UNIT HOUSING PROJECTS

AUDIT GUIDE FOR SECTION 8 MULTI-UNIT HOUSING PROJECTS Asset Performance Section 725 Summer Street, NE, Suite B Salem, Oregon 97301-1266 TABLE OF CONTENTS I. INTRODUCTION, PURPOSE AND USE OF AUDIT GUIDE...

AUDIT GUIDE FOR SECTION 8 MULTI-UNIT HOUSING PROJECTS Asset Performance Section 725 Summer Street, NE, Suite B Salem, Oregon 97301-1266 TABLE OF CONTENTS I. INTRODUCTION, PURPOSE AND USE OF AUDIT GUIDE...

Request for Proposals Independent Audit Services

Request for Proposals Independent Audit Services The Greensboro Housing Authority (GHA) herein solicits Request for Proposals (RFP) from qualified, licensed, responsible firms interested in providing GHA

Request for Proposals Independent Audit Services The Greensboro Housing Authority (GHA) herein solicits Request for Proposals (RFP) from qualified, licensed, responsible firms interested in providing GHA

Financial Statements. Young Women's Christian Association of Greater Toronto December 31, 2014

Financial Statements Young Women's Christian Association of Greater Toronto INDEPENDENT AUDITORS' REPORT To the Members of Young Women's Christian Association of Greater Toronto REPORT ON THE FINANCIAL

Financial Statements Young Women's Christian Association of Greater Toronto INDEPENDENT AUDITORS' REPORT To the Members of Young Women's Christian Association of Greater Toronto REPORT ON THE FINANCIAL

VIRGINIA HOUSING DEVELOPMENT AUTHORITY MULTIFAMILY DIVISION MORTGAGOR/GRANTEE S AUDIT GUIDE

VIRGINIA HOUSING DEVELOPMENT AUTHORITY MULTIFAMILY DIVISION MORTGAGOR/GRANTEE S AUDIT GUIDE Control and Management of the Development As an inducement to the Virginia Housing Development Authority (VHDA)

VIRGINIA HOUSING DEVELOPMENT AUTHORITY MULTIFAMILY DIVISION MORTGAGOR/GRANTEE S AUDIT GUIDE Control and Management of the Development As an inducement to the Virginia Housing Development Authority (VHDA)

Financial Statements December 31, 2014 and 2013 Josephine Commons, LLC

Financial Statements Josephine Commons, LLC www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations and Members Equity...

Financial Statements Josephine Commons, LLC www.eidebailly.com Table of Contents Independent Auditor s Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations and Members Equity...

Revolving Loan Fund for Industrial Development Summary *

Owatonna Economic Development Authority (EDA) City of Owatonna Revolving Loan Fund for Industrial Development Summary * Program Purpose: How It Works: Project Eligibility: Minimum Requirements: Use of

Owatonna Economic Development Authority (EDA) City of Owatonna Revolving Loan Fund for Industrial Development Summary * Program Purpose: How It Works: Project Eligibility: Minimum Requirements: Use of

Consolidated Audit Guide for Audits of HUD Programs

Handbook 2000.04 REV-2 CHG-1 U.S. Department of Housing and Urban Development Office of Inspector General Independent Auditors December 2001 Consolidated Audit Guide for Audits of HUD Programs GA: Distribution:

Handbook 2000.04 REV-2 CHG-1 U.S. Department of Housing and Urban Development Office of Inspector General Independent Auditors December 2001 Consolidated Audit Guide for Audits of HUD Programs GA: Distribution:

Streamlined Annual PHA Plan for Fiscal Year: 2007 PHA Name: HOUSING AUTHORITY OF THE COUNTY OF TULARE

PHA Plans Streamlined Annual Version U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 (exp. 08/31/2009) This information collection is authorized by

PHA Plans Streamlined Annual Version U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 (exp. 08/31/2009) This information collection is authorized by

Chapter 8 VOUCHER ISSUANCE AND BRIEFINGS [24 CFR 982.301, 982.302] A. ISSUANCE OF VOUCHERS [24 CFR 982.204(d), 982.54(d)(2)]

![Chapter 8 VOUCHER ISSUANCE AND BRIEFINGS [24 CFR 982.301, 982.302] A. ISSUANCE OF VOUCHERS [24 CFR 982.204(d), 982.54(d)(2)]](/thumbs/40/20959006.jpg "Chapter 8 VOUCHER ISSUANCE AND BRIEFINGS [24 CFR 982.301, 982.302] A. ISSUANCE OF VOUCHERS [24 CFR 982.204(d), 982.54(d)(2)]") Chapter 8 VOUCHER ISSUANCE AND BRIEFINGS [24 CFR 982.301, 982.302] INTRODUCTION The PHA's goals and objectives are designed to assure that families selected to participate are equipped with the tools necessary

Chapter 8 VOUCHER ISSUANCE AND BRIEFINGS [24 CFR 982.301, 982.302] INTRODUCTION The PHA's goals and objectives are designed to assure that families selected to participate are equipped with the tools necessary

COMPARISON BETWEEN HOUSING OPPORTUNITY THROUGH MODERNIZATION ACT (HOTMA) AND CURRENT LAW

AND CURRENT LAW") 820 First Street NE, Suite 510 Washington, DC 20002 Updated February 5, 2016 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org COMPARISON BETWEEN HOUSING OPPORTUNITY THROUGH MODERNIZATION

820 First Street NE, Suite 510 Washington, DC 20002 Updated February 5, 2016 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org COMPARISON BETWEEN HOUSING OPPORTUNITY THROUGH MODERNIZATION

Delaware Health Information Network. Financial Statements and Independent Auditors Report. June 30, 2015 and 2014

Financial Statements and Independent Auditors Report June 30, 2015 and 2014 Issue Date: November 4, 2015 Table of Contents June 30, 2015 and 2014 Page No. Independent Auditors Report 1 Management s Discussion

Financial Statements and Independent Auditors Report June 30, 2015 and 2014 Issue Date: November 4, 2015 Table of Contents June 30, 2015 and 2014 Page No. Independent Auditors Report 1 Management s Discussion

Subpart C Borrower Management and Operations Responsibilities

3560.75 3560.99 another property in the same location; or (2) The MFH has been maintained to such an extent that it can be expected to continue providing affordable, decent, safe and sanitary housing for

3560.75 3560.99 another property in the same location; or (2) The MFH has been maintained to such an extent that it can be expected to continue providing affordable, decent, safe and sanitary housing for

How To Get A Landline Phone Number In A Rural Development

1. NO DOCUMENTATION IN FILE Rural Development (RD) requires that all files contain third party documentation on income, assets and deduction for each resident. This documentation must be obtained at move-in

1. NO DOCUMENTATION IN FILE Rural Development (RD) requires that all files contain third party documentation on income, assets and deduction for each resident. This documentation must be obtained at move-in

SOMERVILLE HOUSING AUTHORITY SECTION 8 ADMINISTRATIVE PLAN ADOPTED: DECEMBER 13, 2006

SOMERVILLE HOUSING AUTHORITY SECTION 8 ADMINISTRATIVE PLAN ADOPTED: DECEMBER 13, 2006 Somerville Housing Authority 1 ADOPTED 12/13/2006 TABLE OF CONTENTS Chapter 1 OBJECTIVES A. APPROACH AND OBJECTIVES......1-8

SOMERVILLE HOUSING AUTHORITY SECTION 8 ADMINISTRATIVE PLAN ADOPTED: DECEMBER 13, 2006 Somerville Housing Authority 1 ADOPTED 12/13/2006 TABLE OF CONTENTS Chapter 1 OBJECTIVES A. APPROACH AND OBJECTIVES......1-8

HOUSING AUTHORITY OF THE CITY OF SAN BUENAVENTURA

HOUSING AUTHORITY OF THE CITY OF SAN BUENAVENTURA PUBLIC HOUSING PROGRAM 2013 Proposed changes to the Admissions and Continued Occupancy Policy *New policy and clarifications are highlighted in yellow

HOUSING AUTHORITY OF THE CITY OF SAN BUENAVENTURA PUBLIC HOUSING PROGRAM 2013 Proposed changes to the Admissions and Continued Occupancy Policy *New policy and clarifications are highlighted in yellow

Attachment B. FCRHA Housing Choice Voucher Section 8 Homeownership Capacity Statement

Attachment B FCRHA Housing Choice Voucher Section 8 Homeownership Capacity Statement The Fairfax County Redevelopment and Housing Authority (FCRHA) has the capacity to administer a Section 8 (Housing Choice

Attachment B FCRHA Housing Choice Voucher Section 8 Homeownership Capacity Statement The Fairfax County Redevelopment and Housing Authority (FCRHA) has the capacity to administer a Section 8 (Housing Choice

Notice PIH 99-14 (HA)

") U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention: State and Area Office Directors of Public Housing; Director, Section 8 Financial Management Center;

U.S. Department of Housing and Urban Development Office of Public and Indian Housing Special Attention: State and Area Office Directors of Public Housing; Director, Section 8 Financial Management Center;

TOWNSHIP OF ROLLAND ISABELLA COUNTY, MICHIGAN AUDITED FINANCIAL STATEMENTS. Fiscal Year Ended March 31, 2010

ISABELLA COUNTY, MICHIGAN AUDITED FINANCIAL STATEMENTS Fiscal Year Ended TABLE OF CONTENTS Independent Auditor s Report.. 1 FINANCIAL STATEMENTS Government Wide Statement of Net Assets. 2 Government Wide

ISABELLA COUNTY, MICHIGAN AUDITED FINANCIAL STATEMENTS Fiscal Year Ended TABLE OF CONTENTS Independent Auditor s Report.. 1 FINANCIAL STATEMENTS Government Wide Statement of Net Assets. 2 Government Wide

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of: All Multifamily Hub Directors Notice H 2012-25

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER Special Attention of: All Multifamily Hub Directors Notice H 2012-25

MHDC Asset Management Reporting System http://amrs.mhdc.com

MHDC Asset Management Reporting System http://amrs.mhdc.com Login Page User Names & Passwords are used to access the AFS, Budget, and Occupancy Modules. Initial Occupancy Module User Name & Passwords are

MHDC Asset Management Reporting System http://amrs.mhdc.com Login Page User Names & Passwords are used to access the AFS, Budget, and Occupancy Modules. Initial Occupancy Module User Name & Passwords are

U.S. Department of Housing and Urban Development Office of Public and Indian Housing

PHA Plans Streamlined Annual Version 1 U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 (exp 08/31/2009) This information collection is authorized

PHA Plans Streamlined Annual Version 1 U.S. Department of Housing and Urban Development Office of Public and Indian Housing OMB No. 2577-0226 (exp 08/31/2009) This information collection is authorized

BANK BRANCH AUDIT PLANNING

BANK BRANCH AUDIT PLANNING Banking Industry in India is developing and expanding day by day. The basic work culture in banks in India is fairly different as compared to banks in other countries. The customers

BANK BRANCH AUDIT PLANNING Banking Industry in India is developing and expanding day by day. The basic work culture in banks in India is fairly different as compared to banks in other countries. The customers

JACKSON-MADISON COUNTY COMMUNITY ECONOMIC DEVELOPMENT COMMISSION (Jackson Convention & Visitors Bureau) FINANCIAL STATEMENTS.

FINANCIAL STATEMENTS.") COMMUNITY ECONOMIC DEVELOPMENT COMMISSION (Jackson Convention & Visitors Bureau) FINANCIAL STATEMENTS June 30, 2015 COMMUNITY ECONOMIC DEVELOPMENT COMMISSION TABLE OF CONTENTS June 30, 2015 Page Roster

COMMUNITY ECONOMIC DEVELOPMENT COMMISSION (Jackson Convention & Visitors Bureau) FINANCIAL STATEMENTS June 30, 2015 COMMUNITY ECONOMIC DEVELOPMENT COMMISSION TABLE OF CONTENTS June 30, 2015 Page Roster

Public Housing Agency (PHA) Plan

Plan") Public Housing Agency (PHA) Plan Desk Guide U.S. Department of Housing and Urban Development Office of Public and Indian Housing Office of Policy, Program and Legislative Initiatives Please Note: This

Public Housing Agency (PHA) Plan Desk Guide U.S. Department of Housing and Urban Development Office of Public and Indian Housing Office of Policy, Program and Legislative Initiatives Please Note: This

MARIETTA HOUSING AUTHORITY 95 Cole Street Marietta, Georgia 30060 (770) 419-3642 fax: (770) 218-0871 REQUEST FOR PROPOSALS

419-3642 fax: (770) 218-0871 REQUEST FOR PROPOSALS") MARIETTA HOUSING AUTHORITY 95 Cole Street Marietta, Georgia 30060 (770) 419-3642 fax: (770) 218-0871 REQUEST FOR PROPOSALS CONSULTANT AND OTHER SERVICES FOR PAPERLESS ADMINISTRATION OF HOUSING CHOICE VOUCHER

MARIETTA HOUSING AUTHORITY 95 Cole Street Marietta, Georgia 30060 (770) 419-3642 fax: (770) 218-0871 REQUEST FOR PROPOSALS CONSULTANT AND OTHER SERVICES FOR PAPERLESS ADMINISTRATION OF HOUSING CHOICE VOUCHER

SHENANDOAH VALLEY SPAY & NEUTER CLINIC, INC. FINANCIAL REPORT

SHENANDOAH VALLEY SPAY & NEUTER CLINIC, INC. FINANCIAL REPORT December 31, 2013 CONTENTS Page INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 3 Statements of

SHENANDOAH VALLEY SPAY & NEUTER CLINIC, INC. FINANCIAL REPORT December 31, 2013 CONTENTS Page INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 3 Statements of

CITY OF ARCADIA, FLORIDA ANNUAL FINANCIAL REPORT. For the Fiscal Year Ended September 30, 2015

ANNUAL FINANCIAL REPORT For the Fiscal Year Ended September 30, 2015 ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015 TABLE OF CONTENTS Page INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S

ANNUAL FINANCIAL REPORT For the Fiscal Year Ended September 30, 2015 ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015 TABLE OF CONTENTS Page INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S