Lecture 4: Futures and Options Steven Skiena. skiena

|

|

|

- Justina Skinner

- 7 years ago

- Views:

Transcription

1 Lecture 4: Futures and Options Steven Skiena Department of Computer Science State University of New York Stony Brook, NY skiena

2 Foreign Currency Futures Assume that foreign country f has a risk-free interest rate in its own currency of r f. Let S 0 be the spot price in dollars of one unit of f, and F 0 be the future price in dollars of one unit of f. Then F 0 = S 0 e (r r f)t Thus future currency prices are purely a function of the interest rates in the two countries!

3 Pricing Currency Futures If one of these options is better, then I can borrow the initial money and guarantee a risk-free profit.

4 Foreign Currency Arbitrage Note that I can borrow Y units of currency f at rate r f, (costing me Y e r ft in currency f then) convert this to dollars and invest (earning me Y S 0 e rt in dollars then). Thus if F 0 < S 0 e (r r f)t, I can go long on a forward contract to get the Y e r kt in currency f to pay them back at less than I earned on my dollars. Note that I can borrow Y dollars at rate r, (costing me Y e rt in dollars then), convert this to Y/S 0 units of currency f, and invest this at rate r k (earning me (Y/S 0 )e r kt in currency f then) Thus if F 0 > S 0 e (r r f)t I can go short on a forward contract to sell my currency f, earning more than I paid for my dollars.

, convert this to Y/S 0 units of currency f, and invest this at rate r k (earning me (Y/S 0")

5 Futures Contracts Closely related are futures contracts for commodities, traded on exchanges like the Chicago Board of Trade (CBOT). Futures differ from forward contracts in allowing more flexibility on the timing of when the short position must sell. Futures contracts are completely standardized (e.g. 5,000 bushels of number 2 corn for delivery in July) so they can traded on exchanges. Most futures contracts are closed prior to delivery, by buying or selling an offseting contract.

6 Convergence of Future and Spot Prices We expect that the spot price of an asset converges to that of the futures price as the delivery date of the contract approaches otherwise an arbitrage opportunity exists. This convergence means the spot price may go up (down), the futures price may go down (up), or both.

, the futures price may")

7 Arbitrage with Futures If the futures price stays above the spot price, we can buy the asset now and short a futures contract (i.e. agree to sell the asset later at the future price). Then we delivery and clear a profit. If the futures price stays below the spot price, anyone who wants the asset should go long on a futures contract and accept delivery instead of paying the spot price. Such arguments do not factor in the cost of storage, convenience, and the durability of the asset.

8 Expected Future Prices The gap between the spot and futures prices may contain information about the expected future price of the asset. Keynes and Hicks theorized that the expected future price depends upon the behavior of hedgers. Hedgers seek to reduce risk, and are in principle willing to pay for this. Speculators will only be in the game if they can expect profits. Thus if hedgers are going short and speculators are going long, the expected future price should be above the future contract price.

9 Implementing Short Sales Many arbitrage arguments assume the ability to short sell an asset, i.e. sell the asset now without owning it. Unfortunately, such contracts are not available for all assets. However, if the forward price is too low, anyone who owns the asset should sell the asset, invest the proceeds at the riskfree rate, and buy a forward contract to buy it back later at the fixed price. Such arbitrage arguments also work if you can rent/borrow the asset for the desired period from someone who already owns it.

10 Options Options give the right to do something, but not the obligation. Call options permit you to buy an asset for a certain price by a certain date. Owning a call option means you want asset prices to go up. Put options permit you to sell an asset for a certain price by a certain date. Owning a put option means you want asset prices to go down.

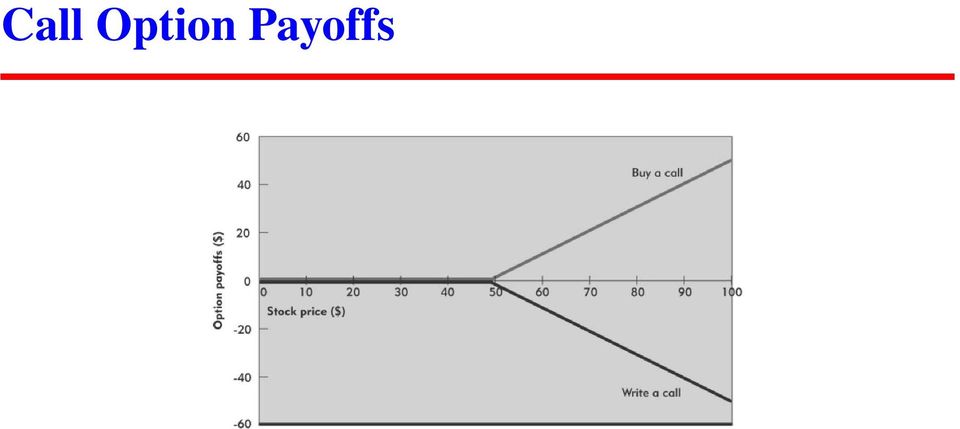

11 Payoff on a Call The payoff of a long position (buying the option) of a call (to buy the asset) at strike price K and current price S t is max(s t K, 0). Why? I win if the current price is greater than what I am allowed to buy it for. My option is worth nothing if the spot price is less than the strike price. The pay for a short position (selling the option) on the call is max(s t K, 0) = min(k S t, 0), by a conservation of money argument.

12 Call Option Payoffs

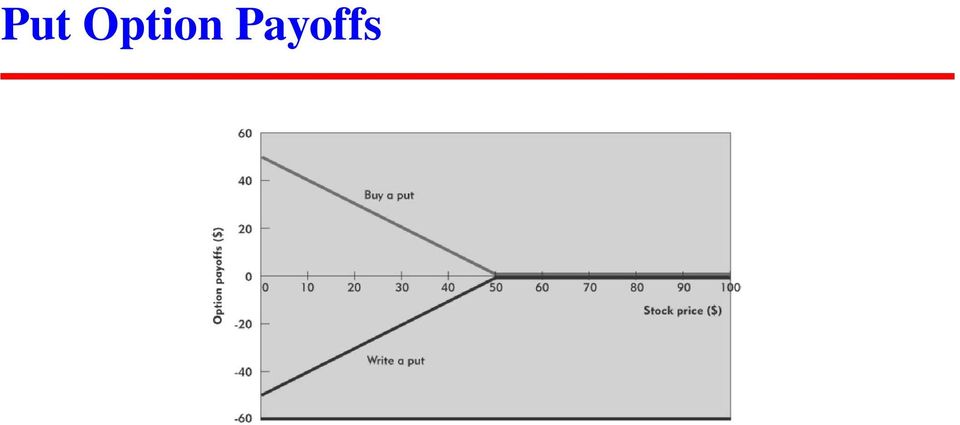

13 Payoff on a Put The payoff of a long position (buying the option) of a put (to sell the asset) at strike price K is max(k S t, 0). The corresponding payoff for the short position (selling the option) is min(s t K, 0). The seller of an option make their gain from what they were originally paid for the option.

.")

14 Put Option Payoffs

Lecture 7: Bounds on Options Prices Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 7: Bounds on Options Prices Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Option Price Quotes Reading the

Lecture 7: Bounds on Options Prices Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Option Price Quotes Reading the

Lecture 3: Forward Contracts Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 3: Forward Contracts Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Derivatives Derivatives are financial

Lecture 3: Forward Contracts Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Derivatives Derivatives are financial

Options Markets: Introduction

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Options Markets: Introduction Chapter 20 Option Contracts call option = contract that gives the holder the right to purchase an asset at a specified price, on or before a certain date put option = contract

Lecture 5: Put - Call Parity

Lecture 5: Put - Call Parity Reading: J.C.Hull, Chapter 9 Reminder: basic assumptions 1. There are no arbitrage opportunities, i.e. no party can get a riskless profit. 2. Borrowing and lending are possible

Lecture 5: Put - Call Parity Reading: J.C.Hull, Chapter 9 Reminder: basic assumptions 1. There are no arbitrage opportunities, i.e. no party can get a riskless profit. 2. Borrowing and lending are possible

Options (1) Class 19 Financial Management, 15.414

Class 19 Financial Management, 15.414") Options (1) Class 19 Financial Management, 15.414 Today Options Risk management: Why, how, and what? Option payoffs Reading Brealey and Myers, Chapter 2, 21 Sally Jameson 2 Types of questions Your company,

Options (1) Class 19 Financial Management, 15.414 Today Options Risk management: Why, how, and what? Option payoffs Reading Brealey and Myers, Chapter 2, 21 Sally Jameson 2 Types of questions Your company,

Factors Affecting Option Prices

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

Lecture 6: Portfolios with Stock Options Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 6: Portfolios with Stock Options Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Portfolios with Options The

Lecture 6: Portfolios with Stock Options Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena Portfolios with Options The

Notes for Lecture 2 (February 7)

") CONTINUOUS COMPOUNDING Invest $1 for one year at interest rate r. Annual compounding: you get $(1+r). Semi-annual compounding: you get $(1 + (r/2)) 2. Continuous compounding: you get $e r. Invest $1 for

CONTINUOUS COMPOUNDING Invest $1 for one year at interest rate r. Annual compounding: you get $(1+r). Semi-annual compounding: you get $(1 + (r/2)) 2. Continuous compounding: you get $e r. Invest $1 for

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 1 - Introduction

Chapter 1 - Introduction Derivative securities Futures contracts Forward contracts Futures and forward markets Comparison of futures and forward contracts Options contracts Options markets Comparison of

Chapter 1 - Introduction Derivative securities Futures contracts Forward contracts Futures and forward markets Comparison of futures and forward contracts Options contracts Options markets Comparison of

Options. + Concepts and Buzzwords. Readings. Put-Call Parity Volatility Effects

+ Options + Concepts and Buzzwords Put-Call Parity Volatility Effects Call, put, European, American, underlying asset, strike price, expiration date Readings Tuckman, Chapter 19 Veronesi, Chapter 6 Options

+ Options + Concepts and Buzzwords Put-Call Parity Volatility Effects Call, put, European, American, underlying asset, strike price, expiration date Readings Tuckman, Chapter 19 Veronesi, Chapter 6 Options

CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS 1. Answer the following questions based on data in Exhibit 7.5. a. How many Swiss francs

INSTRUCTOR S MANUAL: MULTINATIONAL FINANCIAL MANAGEMENT, 9 TH ED. CHAPTER 7 SUGGESTED ANSWERS TO CHAPTER 7 QUESTIONS 1. Answer the following questions based on data in Exhibit 7.5. a. How many Swiss francs

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

2. Exercising the option - buying or selling asset by using option. 3. Strike (or exercise) price - price at which asset may be bought or sold

price - price at which asset may be bought or sold") Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Chapter 21 : Options-1 CHAPTER 21. OPTIONS Contents I. INTRODUCTION BASIC TERMS II. VALUATION OF OPTIONS A. Minimum Values of Options B. Maximum Values of Options C. Determinants of Call Value D. Black-Scholes

Forwards and Futures

Prof. Alex Shapiro Lecture Notes 16 Forwards and Futures I. Readings and Suggested Practice Problems II. Forward Contracts III. Futures Contracts IV. Forward-Spot Parity V. Stock Index Forward-Spot Parity

Prof. Alex Shapiro Lecture Notes 16 Forwards and Futures I. Readings and Suggested Practice Problems II. Forward Contracts III. Futures Contracts IV. Forward-Spot Parity V. Stock Index Forward-Spot Parity

Introduction to Futures Contracts

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

Example 1. Consider the following two portfolios: 2. Buy one c(s(t), 20, τ, r) and sell one c(s(t), 10, τ, r).

, 20, τ, r) and sell one c(s(t), 10, τ, r).") Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Chapter 4 Put-Call Parity 1 Bull and Bear Financial analysts use words such as bull and bear to describe the trend in stock markets. Generally speaking, a bull market is characterized by rising prices.

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Lecture 12. Options Strategies

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

Lecture 12. Options Strategies Introduction to Options Strategies Options, Futures, Derivatives 10/15/07 back to start 1 Solutions Problem 6:23: Assume that a bank can borrow or lend money at the same

Session IX: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics

Session IX: Stock Options: Properties, Mechanics and Valuation Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Stock

Session IX: Stock Options: Properties, Mechanics and Valuation Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Stock

Contingent Claims: A stock option that is a derivative security whose value is contingent on the price of the stock.

Futures and Options Note 1 Basic Definitions: Derivative Security: A security whose value depends on the worth of other basic underlying variables. E.G. Futures, Options, Forward Contracts, Swaps. A derivative

Futures and Options Note 1 Basic Definitions: Derivative Security: A security whose value depends on the worth of other basic underlying variables. E.G. Futures, Options, Forward Contracts, Swaps. A derivative

Expected payoff = 1 2 0 + 1 20 = 10.

Chapter 2 Options 1 European Call Options To consolidate our concept on European call options, let us consider how one can calculate the price of an option under very simple assumptions. Recall that the

Chapter 2 Options 1 European Call Options To consolidate our concept on European call options, let us consider how one can calculate the price of an option under very simple assumptions. Recall that the

Pricing Forwards and Futures

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Pricing Forwards and Futures Peter Ritchken Peter Ritchken Forwards and Futures Prices 1 You will learn Objectives how to price a forward contract how to price a futures contract the relationship between

Lecture 11. Sergei Fedotov. 20912 - Introduction to Financial Mathematics. Sergei Fedotov (University of Manchester) 20912 2010 1 / 7

20912 2010 1 / 7") Lecture 11 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 7 Lecture 11 1 American Put Option Pricing on Binomial Tree 2 Replicating

Lecture 11 Sergei Fedotov 20912 - Introduction to Financial Mathematics Sergei Fedotov (University of Manchester) 20912 2010 1 / 7 Lecture 11 1 American Put Option Pricing on Binomial Tree 2 Replicating

Lecture 4: Properties of stock options

Lecture 4: Properties of stock options Reading: J.C.Hull, Chapter 9 An European call option is an agreement between two parties giving the holder the right to buy a certain asset (e.g. one stock unit)

Lecture 4: Properties of stock options Reading: J.C.Hull, Chapter 9 An European call option is an agreement between two parties giving the holder the right to buy a certain asset (e.g. one stock unit)

Determination of Forward and Futures Prices. Chapter 5

Determination of Forward and Futures Prices Chapter 5 Fundamentals of Futures and Options Markets, 8th Ed, Ch 5, Copyright John C. Hull 2013 1 Consumption vs Investment Assets Investment assets are assets

Determination of Forward and Futures Prices Chapter 5 Fundamentals of Futures and Options Markets, 8th Ed, Ch 5, Copyright John C. Hull 2013 1 Consumption vs Investment Assets Investment assets are assets

CFA Level -2 Derivatives - I

CFA Level -2 Derivatives - I EduPristine www.edupristine.com Agenda Forwards Markets and Contracts Future Markets and Contracts Option Markets and Contracts 1 Forwards Markets and Contracts 2 Pricing and

CFA Level -2 Derivatives - I EduPristine www.edupristine.com Agenda Forwards Markets and Contracts Future Markets and Contracts Option Markets and Contracts 1 Forwards Markets and Contracts 2 Pricing and

Math 194 Introduction to the Mathematics of Finance Winter 2001

Math 194 Introduction to the Mathematics of Finance Winter 2001 Professor R. J. Williams Mathematics Department, University of California, San Diego, La Jolla, CA 92093-0112 USA Email: williams@math.ucsd.edu

Math 194 Introduction to the Mathematics of Finance Winter 2001 Professor R. J. Williams Mathematics Department, University of California, San Diego, La Jolla, CA 92093-0112 USA Email: williams@math.ucsd.edu

Lecture 3: Put Options and Distribution-Free Results

OPTIONS and FUTURES Lecture 3: Put Options and Distribution-Free Results Philip H. Dybvig Washington University in Saint Louis put options binomial valuation what are distribution-free results? option

OPTIONS and FUTURES Lecture 3: Put Options and Distribution-Free Results Philip H. Dybvig Washington University in Saint Louis put options binomial valuation what are distribution-free results? option

Chapter 6. Commodity Forwards and Futures. Question 6.1. Question 6.2

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE

GLOBAL INTRODUCTION WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE Bearish options strategies are options trading strategies that are designed to allow traders to profi t when an exchange rate trends

GLOBAL INTRODUCTION WELCOME TO FXDD S BEARISH OPTIONS STRATEGY GUIDE Bearish options strategies are options trading strategies that are designed to allow traders to profi t when an exchange rate trends

Chapter 15 - Options Markets

Chapter 15 - Options Markets Option contract Option trading Values of options at expiration Options vs. stock investments Option strategies Option-like securities Option contract Options are rights to

Chapter 15 - Options Markets Option contract Option trading Values of options at expiration Options vs. stock investments Option strategies Option-like securities Option contract Options are rights to

Call and Put. Options. American and European Options. Option Terminology. Payoffs of European Options. Different Types of Options

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17)

") OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17) WHAT ARE OPTIONS? Derivative securities whose values are derived from the values of the underlying securities. Stock options quotations from WSJ. A call

OPTIONS MARKETS AND VALUATIONS (CHAPTERS 16 & 17) WHAT ARE OPTIONS? Derivative securities whose values are derived from the values of the underlying securities. Stock options quotations from WSJ. A call

Pricing Forwards and Swaps

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Chapter 7 Pricing Forwards and Swaps 7. Forwards Throughout this chapter, we will repeatedly use the following property of no-arbitrage: P 0 (αx T +βy T ) = αp 0 (x T )+βp 0 (y T ). Here, P 0 (w T ) is

Reading: Chapter 19. 7. Swaps

Reading: Chapter 19 Chap. 19. Commodities and Financial Futures 1. The mechanics of investing in futures 2. Leverage 3. Hedging 4. The selection of commodity futures contracts 5. The pricing of futures

Reading: Chapter 19 Chap. 19. Commodities and Financial Futures 1. The mechanics of investing in futures 2. Leverage 3. Hedging 4. The selection of commodity futures contracts 5. The pricing of futures

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 2. Forwards, Options, and Hedging This lecture covers the basic derivatives contracts: forwards (and futures), and call and put options. These basic contracts are

BUSM 411: Derivatives and Fixed Income 2. Forwards, Options, and Hedging This lecture covers the basic derivatives contracts: forwards (and futures), and call and put options. These basic contracts are

Introduction to Futures Markets

Agricultural Commodity Marketing: Futures, Options, Insurance Introduction to Futures Markets By: Dillon M. Feuz Utah State University Funding and Support Provided by: Fact Sheets Definition of Marketing

Agricultural Commodity Marketing: Futures, Options, Insurance Introduction to Futures Markets By: Dillon M. Feuz Utah State University Funding and Support Provided by: Fact Sheets Definition of Marketing

Derivative: a financial instrument whose value depends (or derives from) the values of other, more basic, underlying values (Hull, p. 1).

the values of other, more basic, underlying values (Hull, p. 1).") Introduction Options, Futures, and Other Derivatives, 7th Edition, Copyright John C. Hull 2008 1 Derivative: a financial instrument whose value depends (or derives from) the values of other, more basic,

Introduction Options, Futures, and Other Derivatives, 7th Edition, Copyright John C. Hull 2008 1 Derivative: a financial instrument whose value depends (or derives from) the values of other, more basic,

9 Basics of options, including trading strategies

ECG590I Asset Pricing. Lecture 9: Basics of options, including trading strategies 1 9 Basics of options, including trading strategies Option: The option of buying (call) or selling (put) an asset. European

ECG590I Asset Pricing. Lecture 9: Basics of options, including trading strategies 1 9 Basics of options, including trading strategies Option: The option of buying (call) or selling (put) an asset. European

Chapter 1 - Introduction

Chapter 1 - Introduction Derivative securities Futures contracts Forward contracts Futures and forward markets Comparison of futures and forward contracts Options contracts Options markets Comparison of

Chapter 1 - Introduction Derivative securities Futures contracts Forward contracts Futures and forward markets Comparison of futures and forward contracts Options contracts Options markets Comparison of

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Option Properties. Liuren Wu. Zicklin School of Business, Baruch College. Options Markets. (Hull chapter: 9)

") Option Properties Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 9) Liuren Wu (Baruch) Option Properties Options Markets 1 / 17 Notation c: European call option price.

Option Properties Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 9) Liuren Wu (Baruch) Option Properties Options Markets 1 / 17 Notation c: European call option price.

MTH6120 Further Topics in Mathematical Finance Lesson 2

MTH6120 Further Topics in Mathematical Finance Lesson 2 Contents 1.2.3 Non-constant interest rates....................... 15 1.3 Arbitrage and Black-Scholes Theory....................... 16 1.3.1 Informal

MTH6120 Further Topics in Mathematical Finance Lesson 2 Contents 1.2.3 Non-constant interest rates....................... 15 1.3 Arbitrage and Black-Scholes Theory....................... 16 1.3.1 Informal

Options on Beans For People Who Don t Know Beans About Options

Options on Beans For People Who Don t Know Beans About Options Remember when things were simple? When a call was something you got when you were in the bathtub? When premium was what you put in your car?

Options on Beans For People Who Don t Know Beans About Options Remember when things were simple? When a call was something you got when you were in the bathtub? When premium was what you put in your car?

Chapter 11 Options. Main Issues. Introduction to Options. Use of Options. Properties of Option Prices. Valuation Models of Options.

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

One Period Binomial Model

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 One Period Binomial Model These notes consider the one period binomial model to exactly price an option. We will consider three different methods of pricing

Lecture 12: The Black-Scholes Model Steven Skiena. http://www.cs.sunysb.edu/ skiena

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Lecture 12: The Black-Scholes Model Steven Skiena Department of Computer Science State University of New York Stony Brook, NY 11794 4400 http://www.cs.sunysb.edu/ skiena The Black-Scholes-Merton Model

Bank of America AAA 10.00% T-Bill +.30% Hypothetical Resources BBB 11.90% T-Bill +.80% Basis point difference 190 50

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

Swap Agreements INTEREST RATE SWAP AGREEMENTS An interest rate swap is an agreement to exchange interest rate payments on a notional principal amount over a specific period of time. Generally a swap exchanges

Assumptions: No transaction cost, same rate for borrowing/lending, no default/counterparty risk

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Estimating Risk free Rates. Aswath Damodaran. Stern School of Business. 44 West Fourth Street. New York, NY 10012. Adamodar@stern.nyu.

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

Math 489/889. Stochastic Processes and. Advanced Mathematical Finance. Homework 1

Math 489/889 Stochastic Processes and Advanced Mathematical Finance Homework 1 Steve Dunbar Due Friday, September 3, 2010 Problem 1 part a Find and write the definition of a ``future'', also called a futures

Math 489/889 Stochastic Processes and Advanced Mathematical Finance Homework 1 Steve Dunbar Due Friday, September 3, 2010 Problem 1 part a Find and write the definition of a ``future'', also called a futures

K 1 < K 2 = P (K 1 ) P (K 2 ) (6) This holds for both American and European Options.

P (K 2 ) (6) This holds for both American and European Options.") Slope and Convexity Restrictions and How to implement Arbitrage Opportunities 1 These notes will show how to implement arbitrage opportunities when either the slope or the convexity restriction is violated.

Slope and Convexity Restrictions and How to implement Arbitrage Opportunities 1 These notes will show how to implement arbitrage opportunities when either the slope or the convexity restriction is violated.

Figure S9.1 Profit from long position in Problem 9.9

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Derivative Users Traders of derivatives can be categorized as hedgers, speculators, or arbitrageurs.

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

Chapter 14 Foreign Exchange Markets and Exchange Rates

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

2 Stock Price. Figure S1.1 Profit from long position in Problem 1.13

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

Treasury Bond Futures

Treasury Bond Futures Concepts and Buzzwords Basic Futures Contract Futures vs. Forward Delivery Options Reading Veronesi, Chapters 6 and 11 Tuckman, Chapter 14 Underlying asset, marking-to-market, convergence

Treasury Bond Futures Concepts and Buzzwords Basic Futures Contract Futures vs. Forward Delivery Options Reading Veronesi, Chapters 6 and 11 Tuckman, Chapter 14 Underlying asset, marking-to-market, convergence

Determination of Forward and Futures Prices

Determination of Forward and Futures Prices Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Short selling A popular trading (arbitrage) strategy is the shortselling or

Determination of Forward and Futures Prices Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Short selling A popular trading (arbitrage) strategy is the shortselling or

Introduction to Options. Commodity & Ingredient Hedging, LLC www.cihedging.com 312-596-7755

Introduction to Options Commodity & Ingredient Hedging, LLC www.cihedging.com 312-596-7755 Options on Futures: Price Protection & Opportunity Copyright 2009 Commodity & Ingredient Hedging, LLC 2 Option

Introduction to Options Commodity & Ingredient Hedging, LLC www.cihedging.com 312-596-7755 Options on Futures: Price Protection & Opportunity Copyright 2009 Commodity & Ingredient Hedging, LLC 2 Option

Hedging Strategies Using

Chapter 4 Hedging Strategies Using Futures and Options 4.1 Basic Strategies Using Futures While the use of short and long hedges can reduce (or eliminate in some cases - as below) both downside and upside

Chapter 4 Hedging Strategies Using Futures and Options 4.1 Basic Strategies Using Futures While the use of short and long hedges can reduce (or eliminate in some cases - as below) both downside and upside

Section 1 - Overview and Option Basics

1 of 10 Section 1 - Overview and Option Basics Download this in PDF format. Welcome to the world of investing and trading with options. The purpose of this course is to show you what options are, how they

1 of 10 Section 1 - Overview and Option Basics Download this in PDF format. Welcome to the world of investing and trading with options. The purpose of this course is to show you what options are, how they

General Information Series

General Information Series 1 Agricultural Futures for the Beginner Describes various applications of futures contracts for those new to futures markets. Different trading examples for hedgers and speculators

General Information Series 1 Agricultural Futures for the Beginner Describes various applications of futures contracts for those new to futures markets. Different trading examples for hedgers and speculators

Options 1 OPTIONS. Introduction

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

1 CASH SETTLED AGRICULTURAL CONTRACT SPECIFICATIONS - FUTURES

1 CASH SETTLED AGRICULTURAL CONTRACT SPECIFICATIONS - FUTURES FUTURES CONTRACT CHICAGO CORN CHICAGO WHEAT KCBT HARD RED Trading system code CORN REDW KANS BEAN MEAL OILS Trading Hours 09h00 12h00 South

1 CASH SETTLED AGRICULTURAL CONTRACT SPECIFICATIONS - FUTURES FUTURES CONTRACT CHICAGO CORN CHICAGO WHEAT KCBT HARD RED Trading system code CORN REDW KANS BEAN MEAL OILS Trading Hours 09h00 12h00 South

Two-State Option Pricing

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

The theory of storage and the convenience yield. 2008 Summer School - UBC 1

The theory of storage and the convenience yield 2008 Summer School - UBC 1 The theory of storage and the normal backwardation theory explain the relationship between the spot and futures prices in commodity

The theory of storage and the convenience yield 2008 Summer School - UBC 1 The theory of storage and the normal backwardation theory explain the relationship between the spot and futures prices in commodity

BEAR: A person who believes that the price of a particular security or the market as a whole will go lower.

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

Trading Terms ARBITRAGE: The simultaneous purchase and sale of identical or equivalent financial instruments in order to benefit from a discrepancy in their price relationship. More generally, it refers

WHAT ARE OPTIONS OPTIONS TRADING

OPTIONS TRADING WHAT ARE OPTIONS Options are openly traded contracts that give the buyer a right to a futures position at a specific price within a specified time period Designed as more of a protective

OPTIONS TRADING WHAT ARE OPTIONS Options are openly traded contracts that give the buyer a right to a futures position at a specific price within a specified time period Designed as more of a protective

Foreign Exchange Market: Chapter 7. Chapter Objectives & Lecture Notes FINA 5500

Foreign Exchange Market: Chapter 7 Chapter Objectives & Lecture Notes FINA 5500 Chapter Objectives: FINA 5500 Chapter 7 / FX Markets 1. To be able to interpret direct and indirect quotes in the spot market

Foreign Exchange Market: Chapter 7 Chapter Objectives & Lecture Notes FINA 5500 Chapter Objectives: FINA 5500 Chapter 7 / FX Markets 1. To be able to interpret direct and indirect quotes in the spot market

Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]

![Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]](/thumbs/40/21465294.jpg "Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] [On Screen]") Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] MODULE 5 Arbitrage and Purchasing Power Parity Conditions [Sheen Liu]: Managers of multinational firms,

Finance 581: Arbitrage and Purchasing Power Parity Conditions Module 5: Lecture 1 [Speaker: Sheen Liu] MODULE 5 Arbitrage and Purchasing Power Parity Conditions [Sheen Liu]: Managers of multinational firms,

EC372 Bond and Derivatives Markets Topic #5: Options Markets I: fundamentals

EC372 Bond and Derivatives Markets Topic #5: Options Markets I: fundamentals R. E. Bailey Department of Economics University of Essex Outline Contents 1 Call options and put options 1 2 Payoffs on options

EC372 Bond and Derivatives Markets Topic #5: Options Markets I: fundamentals R. E. Bailey Department of Economics University of Essex Outline Contents 1 Call options and put options 1 2 Payoffs on options

Futures, Forward and Option Contracts How a Futures Contract works

1 CHAPTER 34 VALUING FUTURES AND FORWARD CONTRACTS A futures contract is a contract between two parties to exchange assets or services at a specified time in the future at a price agreed upon at the time

1 CHAPTER 34 VALUING FUTURES AND FORWARD CONTRACTS A futures contract is a contract between two parties to exchange assets or services at a specified time in the future at a price agreed upon at the time

Chapter 1: Financial Markets and Financial Derivatives

Chapter 1: Financial Markets and Financial Derivatives 1.1 Financial Markets Financial markets are markets for financial instruments, in which buyers and sellers find each other and create or exchange

Chapter 1: Financial Markets and Financial Derivatives 1.1 Financial Markets Financial markets are markets for financial instruments, in which buyers and sellers find each other and create or exchange

IX - Futures FORWARD AND FUTURES CONTRACTS. Soybean Contract: Soybean Contract:

IX - Futures FORWARD AND FUTURES CONTRACTS Forward and Future contracts are legal agreements for the delivery of goods, services, or assets at a specified price, under specified conditions, where the specified

IX - Futures FORWARD AND FUTURES CONTRACTS Forward and Future contracts are legal agreements for the delivery of goods, services, or assets at a specified price, under specified conditions, where the specified

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

This act of setting a price today for a transaction in the future, hedging. hedge currency exposure, short long long hedge short hedge Hedgers

Section 7.3 and Section 4.5 Oct. 7, 2002 William Pugh 7.3 Example of a forward contract: In May, a crude oil producer gets together with a refiner to agree on a price for crude oil. This price is for crude

Section 7.3 and Section 4.5 Oct. 7, 2002 William Pugh 7.3 Example of a forward contract: In May, a crude oil producer gets together with a refiner to agree on a price for crude oil. This price is for crude

Session X: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics. Department of Economics, City University, London

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

I. Derivatives, call and put options, bounds on option prices, combined strategies

I. Derivatives, call and put options, bounds on option prices, combined strategies Beáta Stehlíková Financial derivatives Faculty of Mathematics, Physics and Informatics Comenius University, Bratislava

I. Derivatives, call and put options, bounds on option prices, combined strategies Beáta Stehlíková Financial derivatives Faculty of Mathematics, Physics and Informatics Comenius University, Bratislava

380.760: Corporate Finance. Financial Decision Making

380.760: Corporate Finance Lecture 2: Time Value of Money and Net Present Value Gordon Bodnar, 2009 Professor Gordon Bodnar 2009 Financial Decision Making Finance decision making is about evaluating costs

380.760: Corporate Finance Lecture 2: Time Value of Money and Net Present Value Gordon Bodnar, 2009 Professor Gordon Bodnar 2009 Financial Decision Making Finance decision making is about evaluating costs

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

A future or forward contract is an agreement on price now for delivery of a specific product or service in the future.

LESSON WHAT IS TRADING? Nothing would last for as long as trading has unless there was an absolute need for it. Consumers need things and producers make things. Trading is the introduction of these two

LESSON WHAT IS TRADING? Nothing would last for as long as trading has unless there was an absolute need for it. Consumers need things and producers make things. Trading is the introduction of these two

MODEL TEST PAPER COMMODITIES MARKET MODULE

MODEL TEST PAPER COMMODITIES MARKET MODULE Q:1. Which of the following can be the underlying for a commodity derivative contract? (a) Interest Rate (b) Euro-Indian Rupee (c) Gold (d) NIFTY Q:2. Daily mark

MODEL TEST PAPER COMMODITIES MARKET MODULE Q:1. Which of the following can be the underlying for a commodity derivative contract? (a) Interest Rate (b) Euro-Indian Rupee (c) Gold (d) NIFTY Q:2. Daily mark

Hedging with Futures and Options: Supplementary Material. Global Financial Management

Hedging with Futures and Options: Supplementary Material Global Financial Management Fuqua School of Business Duke University 1 Hedging Stock Market Risk: S&P500 Futures Contract A futures contract on

Hedging with Futures and Options: Supplementary Material Global Financial Management Fuqua School of Business Duke University 1 Hedging Stock Market Risk: S&P500 Futures Contract A futures contract on

Two-State Options. John Norstad. j-norstad@northwestern.edu http://www.norstad.org. January 12, 1999 Updated: November 3, 2011.

Two-State Options John Norstad j-norstad@northwestern.edu http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Two-State Options John Norstad j-norstad@northwestern.edu http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Understanding Options: Calls and Puts

2 Understanding Options: Calls and Puts Important: in their simplest forms, options trades sound like, and are, very high risk investments. If reading about options makes you think they are too risky for

2 Understanding Options: Calls and Puts Important: in their simplest forms, options trades sound like, and are, very high risk investments. If reading about options makes you think they are too risky for

Option Premium = Intrinsic. Speculative Value. Value

Chapters 4/ Part Options: Basic Concepts Options Call Options Put Options Selling Options Reading The Wall Street Journal Combinations of Options Valuing Options An Option-Pricing Formula Investment in

Chapters 4/ Part Options: Basic Concepts Options Call Options Put Options Selling Options Reading The Wall Street Journal Combinations of Options Valuing Options An Option-Pricing Formula Investment in

CME Options on Futures

CME Education Series CME Options on Futures The Basics Table of Contents SECTION PAGE 1 VOCABULARY 2 2 PRICING FUNDAMENTALS 4 3 ARITHMETIC 6 4 IMPORTANT CONCEPTS 8 5 BASIC STRATEGIES 9 6 REVIEW QUESTIONS

CME Education Series CME Options on Futures The Basics Table of Contents SECTION PAGE 1 VOCABULARY 2 2 PRICING FUNDAMENTALS 4 3 ARITHMETIC 6 4 IMPORTANT CONCEPTS 8 5 BASIC STRATEGIES 9 6 REVIEW QUESTIONS

FIXED-INCOME SECURITIES. Chapter 11. Forwards and Futures

FIXED-INCOME SECURITIES Chapter 11 Forwards and Futures Outline Futures and Forwards Types of Contracts Trading Mechanics Trading Strategies Futures Pricing Uses of Futures Futures and Forwards Forward

FIXED-INCOME SECURITIES Chapter 11 Forwards and Futures Outline Futures and Forwards Types of Contracts Trading Mechanics Trading Strategies Futures Pricing Uses of Futures Futures and Forwards Forward

Too good to be true? The Dream of Arbitrage"

Too good to be true? The Dream of Arbitrage" Aswath Damodaran Aswath Damodaran! 1! The Essence of Arbitrage" In pure arbitrage, you invest no money, take no risk and walk away with sure profits. You can

Too good to be true? The Dream of Arbitrage" Aswath Damodaran Aswath Damodaran! 1! The Essence of Arbitrage" In pure arbitrage, you invest no money, take no risk and walk away with sure profits. You can

Chapter 21: Options and Corporate Finance

Chapter 21: Options and Corporate Finance 21.1 a. An option is a contract which gives its owner the right to buy or sell an underlying asset at a fixed price on or before a given date. b. Exercise is the

Chapter 21: Options and Corporate Finance 21.1 a. An option is a contract which gives its owner the right to buy or sell an underlying asset at a fixed price on or before a given date. b. Exercise is the

Forward exchange rates

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

a. What is the portfolio of the stock and the bond that replicates the option?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

University of Essex. Term Paper Financial Instruments and Capital Markets 2010/2011. Konstantin Vasilev Financial Economics Bsc

University of Essex Term Paper Financial Instruments and Capital Markets 2010/2011 Konstantin Vasilev Financial Economics Bsc Explain the role of futures contracts and options on futures as instruments

University of Essex Term Paper Financial Instruments and Capital Markets 2010/2011 Konstantin Vasilev Financial Economics Bsc Explain the role of futures contracts and options on futures as instruments

Lecture 4: Derivatives

Lecture 4: Derivatives School of Mathematics Introduction to Financial Mathematics, 2015 Lecture 4 1 Financial Derivatives 2 uropean Call and Put Options 3 Payoff Diagrams, Short Selling and Profit Derivatives

Lecture 4: Derivatives School of Mathematics Introduction to Financial Mathematics, 2015 Lecture 4 1 Financial Derivatives 2 uropean Call and Put Options 3 Payoff Diagrams, Short Selling and Profit Derivatives

Bailouts and Stimulus Plans. Eugene F. Fama

Bailouts and Stimulus Plans Eugene F. Fama Robert R. McCormick Distinguished Service Professor of Finance Booth School of Business University of Chicago There is an identity in macroeconomics. It says

Bailouts and Stimulus Plans Eugene F. Fama Robert R. McCormick Distinguished Service Professor of Finance Booth School of Business University of Chicago There is an identity in macroeconomics. It says

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

International Finance and Hedging Currency Risk. John Board

International Finance and Hedging Currency Risk John Board Country Risk Country Risk The risk that the business environment in the host country changes unexpectedly Increases the risk to multinational

International Finance and Hedging Currency Risk John Board Country Risk Country Risk The risk that the business environment in the host country changes unexpectedly Increases the risk to multinational

TREATMENT OF PREPAID DERIVATIVE CONTRACTS. Background

Traditional forward contracts TREATMENT OF PREPAID DERIVATIVE CONTRACTS Background A forward contract is an agreement to deliver a specified quantity of a defined item or class of property, such as corn,

Traditional forward contracts TREATMENT OF PREPAID DERIVATIVE CONTRACTS Background A forward contract is an agreement to deliver a specified quantity of a defined item or class of property, such as corn,