Measuring Risk in Internationally Diversified Bond Portfolios. Summary

|

|

|

- Rodney Golden

- 7 years ago

- Views:

Transcription

1 Measuring Risk in Internationally Diversified Bond Portfolios Stan Beckers BARRA International, 65 London Wall, London EC2M 5TU, United Kingdom Summary In this paper we argue that the traditional measures of risk in bond portfolio management (duration and convexity) are irrelevant in an international context. Starting from a discussion of the drawbacks of duration within a domestic setting, we develop a multifactor model as a prime alternative. This multifactor model allows for non-parallel shifts in the term structure and accommodates the risk inherent in changing yield spreads. This multifactor model can be easily generalized to apply in a multicurrency environment. In an international context, currency risk, which tends to be totally ignored by the traditional duration measure, plays a crucial role. The multiple factor framework can be extended to specifically incorporate this currency risk in addition to the cross market term structure effects. In this respect the multi-factor risk model could become the natural framework for the measurement of international fixed income risk. Résumé Mesurer le Risque dans des Portefeuilles d Obligations Diversifiées Internationalement Dans cet article, nous démontrons que les mesures traditionnelles de risque dans la gestion de portefeuilles d obligations (durée et convexité) sont inappropriées dans un contexte international. En partant d une discussion sur les inconvénients de la durée dans un cadre national, nous développons un modèle multifacteur en tant que principale alternative. Ce modèle multifacteur autorise les déplacements non-parallèles dans la structure de durée et adapte le risque inhérent en changeant les distributions de rendement. Ce modèle multifacteur peut être facilement généralisé pour être applicable dans un environnement multi-devise. Dans un contexte international, le risque de devise, qui a tendance à être entièrement ignoré par la mesure de durée traditionnelle, joue un rôle crucial. Le cadre de facteur multiple peut être étendu pour inclure spécifiquement ce risque de devise en plus des effets de structure de durée inter-marchés. De ce point de vue, le modèle de risque multi-facteurs pourrait devenir le cadre naturel du calcul du risque de revenu fixe international. 139

2 1. INTRODUCTION The benefits of international diversification are well documented : most pension funds and insurance companies have typically increased their international exposure during the last decade. It is interesting to note though that this growing internationalization of investment management has mostly been attributable to the equity portion of these funds. Indeed, with a few exceptions, there has been little theoretical analysis of the investment implications of international fixed income investment ( see Cholerton, Pieraerts and Solnik [1986], Jorion [1987 and 1989]). Without doubt this is partly due to the comparative lack of data covering the major international bond markets. There is however also a general feeling that the arguments for international bond investment are weaker because the large impact of currency on the risk - return profile of multicurrency bond portfolios. Our aim in this article is to discuss and quantify the various dimensions of risk in international fixed income markets. 2. DATA For this study we have restricted our attention to the government bond markets of the major international countries. It should obviously be recognized that the government bond sector is in a number of cases only a small part of a country's fixed income market. This is especially the case in the U.S. and Japan. Moreover the Euromarkets are omitted completely due to the extremely poor quality of the available data for these markets. It should also be noted that the government bond sector will have different characteristics from other fixed income sectors in the same market (such as the junk bonds in the U.S., the index-linked sector in the U.K. or the mortgage backed bonds in Denmark). The government sector - although representative of the basic default free term structure of interest rates - may therefore only partially capture the universe of all bonds and will therefore not completely reflect the 'true' global bond market. A final caveat concerns the liquidity of the individual issues. Many of the government bonds - perhaps up to 60% of the issues in some countries - are not sufficiently liquid for their pricing to be reliable. Further, in some markets only a few issues may trade in sufficient size to accommodate large institutional funds. The following Table summarizes the liquidity of the different Government Bond Markets as assessed by JP Morgan Securities 140

![Indeed, with a few exceptions, there has been little theoretical analysis of the investment implications of international fixed income investment ( see Cholerton, Pieraerts and Solnik [1986], Jorion](/docs-images/46/21737342/images/page_2.jpg "[1987 and 1989]). Without doubt this is partly due to the comparative lack of data covering the major international bond markets.")

3 Table 1 : Relative liquidity of different government bond markets Market Number Traded Actively traded Benchmark U.S. Japan Germany U.K. France THE PROBLEM WITH DURATION (AND CONVEXITY) When assessing the risk characteristics of internationally diversified bond portfolios, the traditional measures of risk in the context of a single market - (option adjusted) duration and convexity - break down. Before suggesting an alternative approach we will first briefly discuss the relevance of these concepts within a domestic setting. The duration of a bond approximately captures the price change associated with a given yield change (see figure 1). The duration measure implicitly assumes that the price-yield relation is linear (as measured by the tangent to the price- yield curve). The error implied by the duration measure will therefore be a function of its curvature ( or convexity). A portfolio manager who would only quantify the interest rate risk of his portfolio through its duration may be using an inadequate measure of price sensitivity except for very small changes in yield. In addition duration implicitly assumes identical shifts in yield for instruments with different maturities i.e. duration will only be correct for very small and parallel shifts in the yield curve. It will therefore be obvious that duration will not completely describe the inherent interest rate risk in a fixed income portfolio and that the degree of approximation is a function of the nature of the term structure shift. As a rule of thumb one could say that for the major bond markets across the world duration typically explains about 70% of the cross sectional differences in returns between different bonds, although the measure is much less accurate for Japan ( see Table 2). 141

.")

4 Table 2 : Average adjusted R - Squared Weekly data January - December 1989 Model U.S. Japan U.K. Germany Duration Duration + Convexity France Convexity partly remedies some of the shortcomings of duration. Technically convexity is related to the second derivative of the price - yield curve and reflects the speed with which the price changes when the yields change. Although the combined use of duration and convexity gives us a more complete picture of the price sensitivity of a fixed income portfolio, they will only be fully descriptive of the price yield dynamics if the relationship between the two is exactly quadratic. The combined use of duration and convexity on average (for the major international bond markets) accounts for about 75 % of the cross sectional differences in bond returns. In short, the usage of duration and convexity crucially depends on the assumption of parallel shifts in the yield curve. In this respect they rely upon a fairly simplistic description of the term structure dynamics which can be reduced to one factor : a uniform up - or downward shift. To the extent that other interest rate factors are at play in the market, they will be ignored by this approach. In other words when interest rates only move up or down uniformly, we would be able to completely explain the differences in return between various bonds through their differences in duration or convexity (i.e their different sensitivities to this market factor). The objections against duration and convexity therefore break down in two parts : - there is probably more than one factor needed to describe the dynamics of the term structure : it may change in shape as well as shift up or down. In addition there may be other factors of value such as a price for liquidity, quality, tax advantages (some UK gilts being free of tax to residents abroad for instance) etc... - there are probably other characteristics beyond the duration and convexity of the bond needed in order to capture the exposure of the instrument to these additional sources of value 142

5 4. MULTIPLE SOURCES OF RISK As outlined in the previous paragraph, the framework within which duration and convexity are used is fairly limiting. Even within a domestic setting it would be more satisfying if additional factors of value and price sensitive bond characteristics could be taken into account. As far as the term structure dynamics are concerned, one could learn from the historical yield curve behaviour which particular changes have taken place in the past. One way of assessing these dymnamics is to describe the returns to pure zero coupon bonds of differing maturities ( the yield curve dynamics will then be expressed in terms of the changes to zero coupon bonds or discount factors applying at a certain point along the maturity spectrum). Using this approach, the yield curve can be described in terms of the price of pure discount bonds of different maturities, each of which can move independently. Other sources of value can be captured in terms of yield spreads associated with liquidity, quality, current yield, tax treatment etc... The changes in these spreads through time will again give an indication of the inherent riskiness of each of these characteristics. Formally let us describe the following valuation specification : where P = bond market price CF(t i ) = expected cash flow at time. t i d(t i ) = discount factor applicable at date t i ( or equivalently the current price of a zero coupon bond maturing at time t i ) x. j = bond exposure to factor j a j = market price (or equivalent yield spread) associated with factor j e = bond pricing error Note that the above equation assumes that cash flows only occur on dates t (typically these grid dates are judiciously chosen along the maturity spectrum such as 1, 143

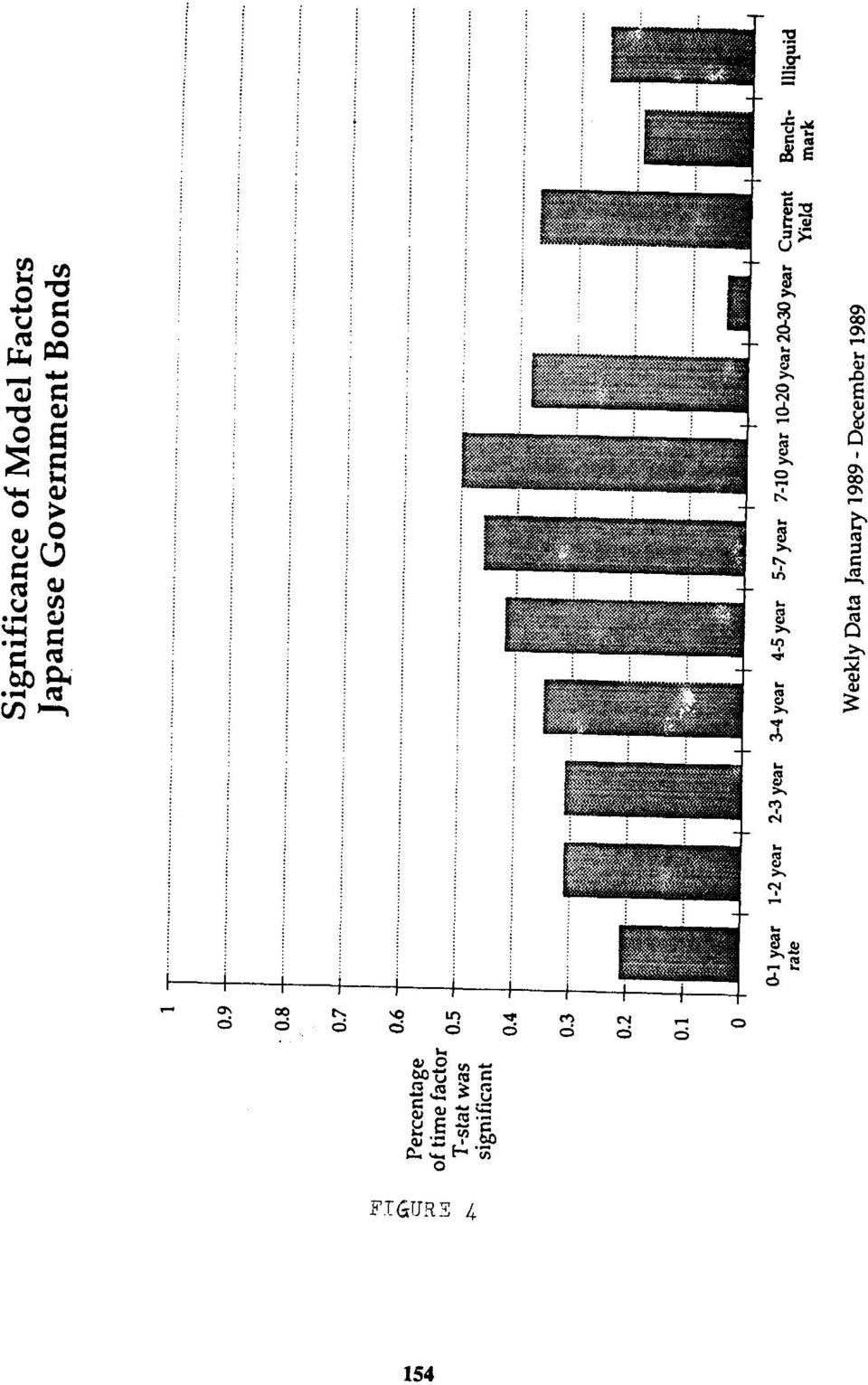

6 2, 3, 4, 5, 7, 10, 20 and 30 years into the future), Cash flows occurring between these dates are proportionately allocated to the previous and following grid date under preservation of present value and duration. The price of each bond is therefore given by the present value of its future ( re- allocated) cash flow stream. This present value is adjusted in function of any bond specific characteristics which may affect this particular instrument. Hence the value of any instrument will be influenced by the default- free term structure as it applies to all issues in a given market as well as by the distinguishing bond characteristics which will have a price in the market. Note that these distinguishing bond characteristics may be market specific ( the UK has the Free of Tax to residents Abroad feature, the US has flower bonds, Japan has very strong liquidity effects etc...). The relevant parameters of the valuation function (dt i and a j ), can then be estimated for a cross-section of representative bonds on a given date. This estimation can be done subject to all sorts of constraints which for instance impose smoothness on the functional form of the term structure. (for a detailed discussion see for instance Sevilla and Beckers 1990). Our research has shown that the above specification is very robust across markets and through time. In most of the major markets the term structure can be defined using a limited number of zero coupon rates ( typically 1, 2, 3, 4, 5, 7, 10, 20 and 30 years to maturity). On average there are another 2 to 3 factors (possibly different from market to market) which contribute to the explanation of differential asset prices. The following Table summarizes the relevant yield spreads for the major markets Table 3 : Relevant yield spreads for the major markets Spread Benchmark status Liquidity Current Yield Free of tax to Residents abroad Callable Perpetuals Markets where applicable ALL ALL ALL U.K. U.S., U.K. U.K. Figures 2 through 6 summarize the relevance of the different factors of value in each market (using the standard T-statistic as the criterion for significance). It can be inferred that current yield is a very important 144

7 source of value in Japan (over and above the term structure factors). Also, Liquidity spreads have a significant impact on bond prices in Japan and Germany. Another insight into the accuracy of the full-factor model can be gained by evaluating the increase in explanatory power obtained by the inclusion of the different factors of value : As can be inferred from Table 4, on average the model achieves an increase in R-Squared of about 8%. Table 4 : Average Adjusted R-Squared Weekly Data January December 1989 Model U.S. Japan U.K. Germany France Duration + Convexity Full Factor Model The improvement is smallest for the French government bond market, possibly because for the period under consideration (1989) parallel shifts in the term structure were most prevalent. The above relationship can be estimated at regular intervals (daily, weekly, monthly), herewith capturing the markets sources of value [a i and d(t i 11. From the time series behaviour of these parameters we can also estimate their risk (volatility) and correlations. In particular we can estimate the volatility of the 1 year zero coupon rate, its correlation with changes in the 7 year zero coupon rate, the volatility of the liquidity yield spread and its correlation with the 5 year zero coupon rate. The core of a bond risk model is therefore an estimate of the variances and covariances of the term structure and yield spread factors. Beyond the market-wide sources of risk, there remains a - typically small- component of bond specific risk. This risk may be due to unique, idiosyncratic characteristics associated with an individual issue. In the above model specification this specific risk is captured by the standard deviation of the pricing error e. Especially for government bonds the specific risk is mostly negligibly small (or equivalently the above model will capture the majority of the pricing relationship ). Specific risk is by definition non-hedgeable but will on the other hand diversify very quickly since it is unrelated across different instruments. 145

8 It will now be obvious that we have extended the single factor duration/convexity concept into a multidimensional framework : The price risk of a 5 year bond for instance will be a function of its sensitivity to the 1, 2, 3,4 and 5 year zero coupon rates since the price risk of its coupon and principal payments will be a function of the volatility of these rates (as well as of the size of the cash flows which will be paid out). If the 1 year rate is more volatile than the 3 year rate (i.e. if the term structure typically moves more at the short end than at the longer end), this will be reflected in a relatively higher risk (volatility) being assigned to the 1 year coupon than to the 3 year coupon. 5. RISK MEASUREMENT FOR MULTICURRENCY PORTFOLIOS The multifactor approach outlined above can be generalized quite easily to a multicurrency context. In fact this is the only viable approach since the notions of duration and convexity - although useful within a given base currency - loose all their meaning in internationally diversified portfolios. Indeed, although duration and convexity have the portfolio property (i.e. the duration and convexity of a portfolio are the capitalization weighted averages of the individual bonds ) and it would therefore be technically feasible to compute the duration and convexity of a multicurrency portfolio, these measures would be meaningless. The computation of duration and convexity within a multicurrency portfolio would only be relevant to the extent that there would only be a single interest rate process (i.e. that interest rate movements across the different markets are perfectly correlated and move in a parallel fashion) and that there is no currency risk. For example a portfolio which contains a US Treasury with a duration of 5 years and a German government bond with a duration of 3 years (with an equal weight in each) could be said to have a duration of 4 years. Note that this measure would be identical irrespective of the base currency of the investor (i.e. the duration based measure would imply that the risk of this portfolio is the same irrespective of whether one is US dollar, DM or Yen based). In other words the duration calculation totally ignores the currency dimension. In addition the duration would refer to a sensitivity to changes in a 'global' term structure which would somehow be a combination of the US and German term structures ( which in turn would be assumed to be perfectly correlated). While duration and convexity have lost all meaning, the 146

. If the")

9 extension of the multiple factor approach to international portfolios is very straightforward : A risk model can be estimated for each important international market ( in excess local currency terms). We can then extend the model by not only considering the within country variances and correlations but also taking into account the crosscurrency correlations : we could calculate the correlation between changes in the 3 year zero coupon rate in US dollars and the 3 year rate in Sterling, similarly for the correlation between the 5 year zero coupon rate in DM and the 3 year rate in Yen or the correlation between changes in the French Franc current yield spread and the Japanese liquidity spread. 6. CURRENCY RISK IN INTERNATIONAL BOND PORTFOLIOS Note that so far we have completely ignored the currency dimension. In this paragraph we will argue that currency risk - properly defined - can be separated from the local market risk. Currency is a complicating issue in international asset pricing. It is well known that deviations from Purchasing Power Parity at any given point in time are significant and persist for long periods, fluctuating in a random way. Investors with different base currencies would therefore face different expected real returns when looking at the same asset, resulting in a base-currency specific portfolio construction. To be more specific, let us introduce the following notation. We will distinguish between the base or numeraire currency of the investor and between local returns that apply to a 'local' investor. Let rx rc rfl be the random rate of return due to changes in exchange rates e.g. the rate of depreciation of Sterling versus DM be the random rate of return due to changes in exchange rates plus any interest received as a result of an investment in the foreign risk-free rate be the short term risk free interest rate a local investor would receive Formally : 147

10 Further let rl rn be the total rate of return on a bond as experienced by a local investor be the total rate of return on a foreign bond expressed in the investor's numeraire currency Hence or The last term captures the cross product between exchange rate movements and each bond's excess return over the local short term risk free rate. This term will typically be small, especially over periods such as a month or shorter. In appendix 1 we illustrate the magnitude of this cross-product term for aggregate bond market returns from a US dollar base currency. The effect doesn't exceed more than a few basis points per month on average for aggregate market returns. Therefore : In other words, the foreign bond rate of return in the numeraire currency is approximately equal to the currency rate of return plus the excess rate of return of the foreign bond in the local market. Further, the excess rate of return of the bond in the numeraire currency is where rfn is the risk free rate of return in the domestic ( or numeraire ) currency. In other words the excess rate of return in the numeraire currency is (approximately) equal to the excess rate of return on the currency plus the excess rate of return of the foreign bond in its local market. [ As an aside, an investor who would hedge his exchange rate risk through a (fairly priced ) forward sale of his initial investment would incur a cost of rfn - rc. The currency hedged foreign bond rate of return in the numeraire currency is then 148

11 i.e. the currency hedged rate of return on the foreign asset expressed in the numeraire currency is approximately equal to the numeraire risk free rate plus the excess rate of return of the foreign asset (over its risk free rate). [For the arguments around currency hedging see Kaplanis and Schaefer (1990) and Thomas (1988) and (1989) ]. It will therefore be natural for most international investors to look at the currency policy separately from the local market decision. In particular the risk an investor is exposed to can now be subdivided into a market risk component (which is independent of his base currency), a currency risk component and the cross product term between the two (i.e. the correlation between currency and local market movement). The currency risk can be measured straightforwardly as the volatility of currency movements (measured from a given numeraire currency) and their correlations through time. 7. AN INTERNATIONAL FIXED INCOME MULTIFACTOR RISK MODEL From a risk measurement point of view,the currency risk block completes the international risk model. In particular the model will consist of the following building blocks : - the within country block capturing the volatility of the term structure and yield spreads within a given market (expressed in local currency terms) - the cross - country block reflecting the correlations between term structure and yield spread movements across different markets (each expressed in local currency terms) - the currency block which measures the volatilities and correlations between exchange rate movements (measured from the investor's base currency perspective) - the currency - local market block which contains the correlations between exchange rate movements (measured from the investor's base currency) and interest rate or yield spread movements in different markets (expressed in local market terms). The risk model captures the essential (fundamental) sources of risk in the international fixed income market. Given this model the risk of any individual asset or portfolio can be determined in function of its 149

, a currency risk component and the cross product term")

12 senstitivity to these-risk factors. These exposures can be Identified straightforwardly since they are a function of -the exposure of the bond (portfolio) to different parts of the term structure in each market (i.e. which cash flow will be received at each grid date) - the exposure to yield spread risk in each market (which will be a function of the bond's coupon, liquidity, benchmark status etc...) - the exposure to currency risk as a function of the fraction of the present value of each bond (portfolio) denominated in different base currencies than the numeraire currency The combination of exposures and their riskiness allows one then to quantify the expected return volatility (i.e. the uncertainty around the expected return). This will be expressed in standard deviation terms, reflecting by how much the realized return could deviate from the expected return. The accuracy of the risk measure crucially depends on the stability of the historic risk measures. Imbedded in the risk model are the historic term structure (and currency) movements. To the extent that structural changes take place within each of these market ( Sterling joining the EMS, Belgium tying its term structure to that of Germany... ), the historically observed patterns may no longer be valid into the future. Experience has shown though that the use of historic risk measures is a valuable and accurate predictor of future return volatility in most cases. 8. SUMMARY In this paper we argue that the traditional measures of risk in bond portfolio management (duration and convexity) are irrelevant in an international context. Starting from a discussion of the drawbacks of duration within a domestic setting, we develop a multifactor model as a prime alternative. This multifactor model allows for nonparallel shifts in the term structure and accommodates the risk inherent in changing yield spreads. This multifactor model can be easily generalized to apply in a multicurrency environment. In an international context, currency risk plays a crucial role which tends to be totally ignored by the traditional duration measure. The multiple factor framework can be extended to specifically incorporate this currency risk in addition to the cross market term structure effects. 150

.")

13 THE PRICE -YIELD RELATIONSHIP. FIGURE 1 151

14 FIGURE 2 152

15 FIGURE 3 153

16 FIGURE 4 154

17 FIGURE 5 155

18 FIGURE 6 156

19 BIBLIOGRAPHY Chollerton, K., Pieraerts P. and B. Solnik 'Why invest in foreign currency bonds.', Journal of Portfolio Management, Summer 1986 Jorion P. ' Why buy international Management Review, Sept/oct 1987 bonds?'. Investment Jorion P.,' Asset Allocation with hedged and unhedged foreign stocks and bonds', The journal of Portfolio Management, Summer 1989 Kaplanis E. and S. Schaefer, ' Exchange Risk and International Diversification in bond and equity portfolios ', London Business School Working Paper IFA , January 1990 Sevilla A. and S. Beckers 'An algorithm for the valuation of fixed income instruments ', in Advances in Mathematical Programming and Financial Planning, Volume 2, JAI Press, 1990 Thomas L. ' International Bonds : Stripping away Currency Risk', Investment Management Review, March/April 1988 Thomas L. 'The performance of currency-hedged foreign bonds', Financial Aanalysts Journal, May/june

20 APPENDIX 1: MAGNITUDE OF CROSS PRODUCT OF EXCHANGE RATE MOVEMENTS AND LOCAL MARKET EXCESS RETURNS (monthly data) Base Currency : U.S. Dollar Observation period : January February 1989 Data Series : Salomon Government Bond Series Country Cross Product Annual Standard Deviation Mean Std with cross without cross prod. terms prod. terms Australia Canada France Germany Japan Netherlands Switzerland UK :

Risk and Return in the Canadian Bond Market

Risk and Return in the Canadian Bond Market Beyond yield and duration. Ronald N. Kahn and Deepak Gulrajani (Reprinted with permission from The Journal of Portfolio Management ) RONALD N. KAHN is Director

Risk and Return in the Canadian Bond Market Beyond yield and duration. Ronald N. Kahn and Deepak Gulrajani (Reprinted with permission from The Journal of Portfolio Management ) RONALD N. KAHN is Director

Valuation and Risk Analysis of International Bonds

Valuation and Risk Analysis of International Bonds Brian P. Murphy and David Won *Reprinted with permission from The Handbook of Fixed Income Securities. Brian P. Murphy, Product Manager, BARRA, Inc. David

Valuation and Risk Analysis of International Bonds Brian P. Murphy and David Won *Reprinted with permission from The Handbook of Fixed Income Securities. Brian P. Murphy, Product Manager, BARRA, Inc. David

VANDERBILT AVENUE ASSET MANAGEMENT

SUMMARY CURRENCY-HEDGED INTERNATIONAL FIXED INCOME INVESTMENT In recent years, the management of risk in internationally diversified bond portfolios held by U.S. investors has been guided by the following

SUMMARY CURRENCY-HEDGED INTERNATIONAL FIXED INCOME INVESTMENT In recent years, the management of risk in internationally diversified bond portfolios held by U.S. investors has been guided by the following

International Diversification and Exchange Rates Risk. Summary

International Diversification and Exchange Rates Risk Y. K. Ip School of Accounting and Finance, University College of Southern Queensland, Toowoomba, Queensland 4350, Australia Summary The benefits arisen

International Diversification and Exchange Rates Risk Y. K. Ip School of Accounting and Finance, University College of Southern Queensland, Toowoomba, Queensland 4350, Australia Summary The benefits arisen

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate?

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

Is the Forward Exchange Rate a Useful Indicator of the Future Exchange Rate? Emily Polito, Trinity College In the past two decades, there have been many empirical studies both in support of and opposing

How Hedging Can Substantially Reduce Foreign Stock Currency Risk

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

Risk Management Series

AAA AAA AAA AAA AAA AAA AAA AAA AAA AAA January 1996 Managing Market Exposure Robert Litterman Kurt Winkelmann Acknowledgements The authors are grateful to Mike Asay, Alex Bergier, Jean- Paul Calamaro,

AAA AAA AAA AAA AAA AAA AAA AAA AAA AAA January 1996 Managing Market Exposure Robert Litterman Kurt Winkelmann Acknowledgements The authors are grateful to Mike Asay, Alex Bergier, Jean- Paul Calamaro,

Estimating Risk free Rates. Aswath Damodaran. Stern School of Business. 44 West Fourth Street. New York, NY 10012. Adamodar@stern.nyu.

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

Estimating Risk free Rates Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 Adamodar@stern.nyu.edu Estimating Risk free Rates Models of risk and return in finance start

Staying alive: Bond strategies for a normalising world

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

Staying alive: Bond strategies for a normalising world Dr Peter Westaway Chief Economist, Europe Vanguard Asset Management November 2013 This document is directed at investment professionals and should

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Vanguard research July 2014

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

Sources of return for hedged global bond funds

Research commentary Sources of return for hedged global bond funds August 2012 Author Roger McIntosh Executive summary. The recent results in key bond market indices demonstrate the importance of a strategic,

Research commentary Sources of return for hedged global bond funds August 2012 Author Roger McIntosh Executive summary. The recent results in key bond market indices demonstrate the importance of a strategic,

PROTECTING YOUR PORTFOLIO WITH BONDS

Your Global Investment Authority PROTECTING YOUR PORTFOLIO WITH BONDS Bond strategies for an evolving market Market uncertainty has left many investors wondering how to protect their portfolios during

Your Global Investment Authority PROTECTING YOUR PORTFOLIO WITH BONDS Bond strategies for an evolving market Market uncertainty has left many investors wondering how to protect their portfolios during

Active Fixed Income: A Primer

Active Fixed Income: A Primer www.madisonadv.com Active Fixed Income: A Primer Most investors have a basic understanding of equity securities and may even spend a good deal of leisure time reading about

Active Fixed Income: A Primer www.madisonadv.com Active Fixed Income: A Primer Most investors have a basic understanding of equity securities and may even spend a good deal of leisure time reading about

CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS PROBLEM SETS 1. While it is true that short-term rates are more volatile than long-term rates, the longer duration of the longer-term bonds makes their prices and their

CHAPTER 16: MANAGING BOND PORTFOLIOS PROBLEM SETS 1. While it is true that short-term rates are more volatile than long-term rates, the longer duration of the longer-term bonds makes their prices and their

Model for. Eleven factors to consider when evaluating bond holdings. Passage of time

PERFORMANCEAttribution A Model for FIXED-INCOME PORTFOLIOS Eleven factors to consider when evaluating bond holdings. BY NABIL KHOURY, MARC VEILLEUX & ROBERT VIAU Performance attribution analysis partitions

PERFORMANCEAttribution A Model for FIXED-INCOME PORTFOLIOS Eleven factors to consider when evaluating bond holdings. BY NABIL KHOURY, MARC VEILLEUX & ROBERT VIAU Performance attribution analysis partitions

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Why own bonds when yields are low?

Why own bonds when yields are low? Vanguard research November 213 Executive summary. Given the backdrop of low yields in government bond markets across much of the developed world, many investors may be

Why own bonds when yields are low? Vanguard research November 213 Executive summary. Given the backdrop of low yields in government bond markets across much of the developed world, many investors may be

Managing Risk/Reward in Fixed Income

INSIGHTS Managing Risk/Reward in Fixed Income Using Global Currency-Hedged Indices as Benchmarks In the pursuit of alpha, is it better to use a global hedged or unhedged index as a benchmark for measuring

INSIGHTS Managing Risk/Reward in Fixed Income Using Global Currency-Hedged Indices as Benchmarks In the pursuit of alpha, is it better to use a global hedged or unhedged index as a benchmark for measuring

UNITED KINGDOM DEBT MANAGEMENT OFFICE. The DMO's Yield Curve Model

United Kingdom Debt Management Office Cheapside House 138 Cheapside London EC2V 6BB UNITED KINGDOM DEBT MANAGEMENT OFFICE The DMO's Yield Curve Model July 2000 The DMO s yield curve model Introduction

United Kingdom Debt Management Office Cheapside House 138 Cheapside London EC2V 6BB UNITED KINGDOM DEBT MANAGEMENT OFFICE The DMO's Yield Curve Model July 2000 The DMO s yield curve model Introduction

Aide-Mémoire. Impact of Currency Exchange Fluctuations on UNHCR s Operations

Aide-Mémoire Impact of Currency Exchange Fluctuations on UNHCR s Operations 1. Following a request at the thirty-second meeting of the Standing Committee in March 2005, under the agenda item Update on

Aide-Mémoire Impact of Currency Exchange Fluctuations on UNHCR s Operations 1. Following a request at the thirty-second meeting of the Standing Committee in March 2005, under the agenda item Update on

Traditionally, venturing outside the United States has involved two investments:

WisdomTree ETFs INTERNATIONAL HEDGED EQUITY FUND HDWM Approximately 50% of the world s equity opportunity set is outside of the United States, 1 and the majority of that is in developed international stocks,

WisdomTree ETFs INTERNATIONAL HEDGED EQUITY FUND HDWM Approximately 50% of the world s equity opportunity set is outside of the United States, 1 and the majority of that is in developed international stocks,

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

CHAPTER 15 INTERNATIONAL PORTFOLIO INVESTMENT SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. What factors are responsible for the recent surge in international portfolio

An Attractive Income Option for a Strategic Allocation

An Attractive Income Option for a Strategic Allocation Voya Senior Loans Suite A strategic allocation provides potential for high and relatively steady income through most credit and rate cycles Improves

An Attractive Income Option for a Strategic Allocation Voya Senior Loans Suite A strategic allocation provides potential for high and relatively steady income through most credit and rate cycles Improves

3Q14. Are Unconstrained Bond Funds a Substitute for Core Bonds? August 2014. Executive Summary. Introduction

3Q14 TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? August 2014 Executive Summary PETER WILAMOSKI, PH.D. Director of Economic Research Proponents of unconstrained bond funds

3Q14 TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? August 2014 Executive Summary PETER WILAMOSKI, PH.D. Director of Economic Research Proponents of unconstrained bond funds

The relationship between exchange rates, interest rates. In this lecture we will learn how exchange rates accommodate equilibrium in

The relationship between exchange rates, interest rates In this lecture we will learn how exchange rates accommodate equilibrium in financial markets. For this purpose we examine the relationship between

The relationship between exchange rates, interest rates In this lecture we will learn how exchange rates accommodate equilibrium in financial markets. For this purpose we examine the relationship between

IASB/FASB Meeting Week beginning 11 April 2011. Top down approaches to discount rates

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler mzeitler@iasb.org +44 (0)20 7246 6453 Shayne Kuhaneck skuhaneck@fasb.org

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler mzeitler@iasb.org +44 (0)20 7246 6453 Shayne Kuhaneck skuhaneck@fasb.org

Using Derivatives in the Fixed Income Markets

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

Using Derivatives in the Fixed Income Markets A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction While derivatives may have a

Hedging Foreign Exchange Risk?

Investing in Emerging Stock Hedging Foreign Exchange Risk? Hedging currency risk is beneficial in developed, but not in emerging stock markets. Shmuel Hauser, Matityahu Marcus, and Uzi Yaari SHMUEL HAUSER

Investing in Emerging Stock Hedging Foreign Exchange Risk? Hedging currency risk is beneficial in developed, but not in emerging stock markets. Shmuel Hauser, Matityahu Marcus, and Uzi Yaari SHMUEL HAUSER

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

A Short Introduction to Credit Default Swaps

A Short Introduction to Credit Default Swaps by Dr. Michail Anthropelos Spring 2010 1. Introduction The credit default swap (CDS) is the most common and widely used member of a large family of securities

A Short Introduction to Credit Default Swaps by Dr. Michail Anthropelos Spring 2010 1. Introduction The credit default swap (CDS) is the most common and widely used member of a large family of securities

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

Quantitative Portfolio Strategy

Quantitative Portfolio Strategy Lev Dynkin 201-524-2839 ldynkin@lehman.com Tony Gould, CFA 212-526-2821 agould@lehman.com CURRENCY HEDGING IN FIXED INCOME PORTFOLIOS Introduction Portfolio managers typically

Quantitative Portfolio Strategy Lev Dynkin 201-524-2839 ldynkin@lehman.com Tony Gould, CFA 212-526-2821 agould@lehman.com CURRENCY HEDGING IN FIXED INCOME PORTFOLIOS Introduction Portfolio managers typically

Distinguishing duration from convexity

Distinguishing duration from convexity Vanguard research May 010 Executive summary. For equity investors, the perception of risk is generally straightforward: Market risk the possibility that prices may

Distinguishing duration from convexity Vanguard research May 010 Executive summary. For equity investors, the perception of risk is generally straightforward: Market risk the possibility that prices may

Are Unconstrained Bond Funds a Substitute for Core Bonds?

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

Rethinking Fixed Income

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

How To Get A Better Return From International Bonds

International fixed income: The investment case Why international fixed income? International bonds currently make up the largest segment of the securities market Ever-increasing globalization and access

International fixed income: The investment case Why international fixed income? International bonds currently make up the largest segment of the securities market Ever-increasing globalization and access

Corporate Risk Management Advisory Services FX and interest rate solutions for clients

Corporate Risk Management Advisory Services FX and interest rate solutions for clients Risk Management: The UBS Warburg approach UBS Warburg has built an outstanding reputation in the management of foreign

Corporate Risk Management Advisory Services FX and interest rate solutions for clients Risk Management: The UBS Warburg approach UBS Warburg has built an outstanding reputation in the management of foreign

Duration and convexity

Duration and convexity Prepared by Pamela Peterson Drake, Ph.D., CFA Contents 1. Overview... 1 A. Calculating the yield on a bond... 4 B. The yield curve... 6 C. Option-like features... 8 D. Bond ratings...

Duration and convexity Prepared by Pamela Peterson Drake, Ph.D., CFA Contents 1. Overview... 1 A. Calculating the yield on a bond... 4 B. The yield curve... 6 C. Option-like features... 8 D. Bond ratings...

A Flexible Benchmark Relative Method of Attributing Returns for Fixed Income Portfolios

White Paper A Flexible Benchmark Relative Method of Attributing s for Fixed Income Portfolios By Stanley J. Kwasniewski, CFA Copyright 2013 FactSet Research Systems Inc. All rights reserved. A Flexible

White Paper A Flexible Benchmark Relative Method of Attributing s for Fixed Income Portfolios By Stanley J. Kwasniewski, CFA Copyright 2013 FactSet Research Systems Inc. All rights reserved. A Flexible

Forward guidance: Estimating the path of fixed income returns

FOR INSTITUTIONAL AND PROFESSIONAL INVESTORS ONLY NOT FOR RETAIL USE OR PUBLIC DISTRIBUTION Forward guidance: Estimating the path of fixed income returns IN BRIEF Over the past year, investors have become

FOR INSTITUTIONAL AND PROFESSIONAL INVESTORS ONLY NOT FOR RETAIL USE OR PUBLIC DISTRIBUTION Forward guidance: Estimating the path of fixed income returns IN BRIEF Over the past year, investors have become

SAMPLE MID-TERM QUESTIONS

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

Life Cycle Asset Allocation A Suitable Approach for Defined Contribution Pension Plans Challenges for defined contribution plans While Eastern Europe is a prominent example of the importance of defined

Investment Assumptions Used in the Valuation of Life and Health Insurance Contract Liabilities

Educational Note Investment Assumptions Used in the Valuation of Life and Health Insurance Contract Liabilities Committee on Life Insurance Financial Reporting September 2014 Document 214099 Ce document

Educational Note Investment Assumptions Used in the Valuation of Life and Health Insurance Contract Liabilities Committee on Life Insurance Financial Reporting September 2014 Document 214099 Ce document

Guidance on the management of interest rate risk arising from nontrading

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

IAA PAPER VALUATION OF RISK ADJUSTED CASH FLOWS AND THE SETTING OF DISCOUNT RATES THEORY AND PRACTICE

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Swaps: complex structures

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

Swaps: complex structures Complex swap structures refer to non-standard swaps whose coupons, notional, accrual and calendar used for coupon determination and payments are tailored made to serve client

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

White Paper Whitepaper Options on 10-Year U.S. Treasury Note & Euro Bund Futures in Fixed Income Portfolio Analysis Copyright 2015 FactSet Research Systems Inc. All rights reserved. Options on 10-Year

Alliance Consulting BOND YIELDS & DURATION ANALYSIS. Bond Yields & Duration Analysis Page 1

BOND YIELDS & DURATION ANALYSIS Bond Yields & Duration Analysis Page 1 COMPUTING BOND YIELDS Sources of returns on bond investments The returns from investment in bonds come from the following: 1. Periodic

BOND YIELDS & DURATION ANALYSIS Bond Yields & Duration Analysis Page 1 COMPUTING BOND YIELDS Sources of returns on bond investments The returns from investment in bonds come from the following: 1. Periodic

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

FIXED INCOME MANAGEMENT

P R O D U C T S FIXED INCOME MANAGEMENT MEMBER OF THE SBA AND REGISTERED SECURITIES DEALER Dynagest is a specialist in international bond management, offering a wide selection of fixed rate investment

P R O D U C T S FIXED INCOME MANAGEMENT MEMBER OF THE SBA AND REGISTERED SECURITIES DEALER Dynagest is a specialist in international bond management, offering a wide selection of fixed rate investment

Chapter 11. International Economics II: International Finance

Chapter 11 International Economics II: International Finance The other major branch of international economics is international monetary economics, also known as international finance. Issues in international

Chapter 11 International Economics II: International Finance The other major branch of international economics is international monetary economics, also known as international finance. Issues in international

Chapter 9. Forecasting Exchange Rates. Lecture Outline. Why Firms Forecast Exchange Rates

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Forecasting

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Forecasting

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

Why Strategic Bond funds are failing investors

Why Strategic Bond funds are failing investors March 2016 For Professional Investors only The rise of Strategic Bonds The IA Sterling Strategic Bond sector was launched to much fanfare in 2008. The birth

Why Strategic Bond funds are failing investors March 2016 For Professional Investors only The rise of Strategic Bonds The IA Sterling Strategic Bond sector was launched to much fanfare in 2008. The birth

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

Fund guide. Prudence Bond Prudence Managed Investment Bond

Fund guide Prudence Bond Prudence Managed Investment Bond Introduction to this guide We know that choosing which fund may be best for you isn t easy there are many options and everyone is different so

Fund guide Prudence Bond Prudence Managed Investment Bond Introduction to this guide We know that choosing which fund may be best for you isn t easy there are many options and everyone is different so

Vanguard research July 2014

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

The Understanding buck stops here: the hedge return : Vanguard The impact money of currency market hedging funds in foreign bonds Vanguard research July 214 Charles Thomas, CFA; Paul M. Bosse, CFA Hedging

Equity Market Risk Premium Research Summary. 12 April 2016

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

Debt Instruments Set 10

Debt Instruments Set 10 Backus/December 1, 1998 Credit Risk on Corporate Debt 0. Overview Global Debt Markets Yield Spreads Default and Recovery Rates Valuation Bond Ratings Registration Basics Credit

Debt Instruments Set 10 Backus/December 1, 1998 Credit Risk on Corporate Debt 0. Overview Global Debt Markets Yield Spreads Default and Recovery Rates Valuation Bond Ratings Registration Basics Credit

Solution: The optimal position for an investor with a coefficient of risk aversion A = 5 in the risky asset is y*:

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Bonds and Yield to Maturity

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Disclosure of European Embedded Value (summary) as of March 31, 2012

as of March 31, 2012") May 25, 2012 SUMITOMO LIFE INSURANCE COMPANY Disclosure of European Embedded Value (summary) as of 2012 This is the summarized translation of the European Embedded Value ( EEV ) of Sumitomo Life Insurance

May 25, 2012 SUMITOMO LIFE INSURANCE COMPANY Disclosure of European Embedded Value (summary) as of 2012 This is the summarized translation of the European Embedded Value ( EEV ) of Sumitomo Life Insurance

Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist?

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments ANNA SUPERA-KUC CFA Director Investing in foreign assets comes with the additional

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments ANNA SUPERA-KUC CFA Director Investing in foreign assets comes with the additional

Credit Risk Stress Testing

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

1 Credit Risk Stress Testing Stress Testing Features of Risk Evaluator 1. 1. Introduction Risk Evaluator is a financial tool intended for evaluating market and credit risk of single positions or of large

Diversify portfolios with U.S. and international bonds

Diversify portfolios with U.S. and international bonds Investing broadly across asset classes such as stocks, bonds and cash can help reduce volatility and risk within a portfolio. Canadian investors have

Diversify portfolios with U.S. and international bonds Investing broadly across asset classes such as stocks, bonds and cash can help reduce volatility and risk within a portfolio. Canadian investors have

Chapter 14 Foreign Exchange Markets and Exchange Rates

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

Chapter 14 Foreign Exchange Markets and Exchange Rates International transactions have one common element that distinguishes them from domestic transactions: one of the participants must deal in a foreign

An introduction to Value-at-Risk Learning Curve September 2003

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

Measurement of Banks Exposure to Interest Rate Risk and Principles for the Management of Interest Rate Risk respectively.

INTEREST RATE RISK IN THE BANKING BOOK Over the past decade the Basel Committee on Banking Supervision (the Basel Committee) has released a number of consultative documents discussing the management and

INTEREST RATE RISK IN THE BANKING BOOK Over the past decade the Basel Committee on Banking Supervision (the Basel Committee) has released a number of consultative documents discussing the management and

Chapter 5. Conditional CAPM. 5.1 Conditional CAPM: Theory. 5.1.1 Risk According to the CAPM. The CAPM is not a perfect model of expected returns.

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

Chapter 5 Conditional CAPM 5.1 Conditional CAPM: Theory 5.1.1 Risk According to the CAPM The CAPM is not a perfect model of expected returns. In the 40+ years of its history, many systematic deviations

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND For professional investors only A NEW OPPORTUNITY Absolute return funds offer an attractive, alternative source of alpha outright or as part of a balanced

ROYAL LONDON ABSOLUTE RETURN GOVERNMENT BOND FUND For professional investors only A NEW OPPORTUNITY Absolute return funds offer an attractive, alternative source of alpha outright or as part of a balanced

Obligation-based Asset Allocation for Public Pension Plans

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

Obligation-based Asset Allocation for Public Pension Plans Market Commentary July 2015 PUBLIC PENSION PLANS HAVE a single objective to provide income for a secure retirement for their members. Once the

MERCER PORTFOLIO SERVICE MONTHLY REPORT

MERCER PORTFOLIO SERVICE MONTHLY REPORT MAY 206 Mercer Superannuation (Australia) Limited ABN 79 004 77 533 Australian Financial Services Licence # 235906 is the trustee of the Mercer Portfolio Service

MERCER PORTFOLIO SERVICE MONTHLY REPORT MAY 206 Mercer Superannuation (Australia) Limited ABN 79 004 77 533 Australian Financial Services Licence # 235906 is the trustee of the Mercer Portfolio Service

Weekly Relative Value

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

Debt Instruments Set 3

Debt Instruments Set 3 Backus/February 9, 1998 Quantifying Interest Rate Risk 0. Overview Examples Price and Yield Duration Risk Management Convexity Value-at-Risk Active Investment Strategies Debt Instruments

Debt Instruments Set 3 Backus/February 9, 1998 Quantifying Interest Rate Risk 0. Overview Examples Price and Yield Duration Risk Management Convexity Value-at-Risk Active Investment Strategies Debt Instruments

Reg. no 2014/1392 30 September 2014. Central government debt management

Reg. no 2014/1392 30 September 2014 Central government debt management Proposed guidelines 2015 2018 1 Summary 1 Proposed guidelines 2015 2018 2 The objective for the management of central government debt

Reg. no 2014/1392 30 September 2014 Central government debt management Proposed guidelines 2015 2018 1 Summary 1 Proposed guidelines 2015 2018 2 The objective for the management of central government debt

Evolution of Performance Attribution Methodologies. Carl Bacon Round-Table Performance Attribution Zurich, 23 rd June 2004

Evolution of Performance Attribution Methodologies Carl Bacon Round-Table Performance Attribution Zurich, 23 rd June 2004 What is Performance Measurement? What Calculation of Portfolio Return, Benchmark

Evolution of Performance Attribution Methodologies Carl Bacon Round-Table Performance Attribution Zurich, 23 rd June 2004 What is Performance Measurement? What Calculation of Portfolio Return, Benchmark

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management Naoki Matsuyama Investment Administration Department, The Neiji Mutual Life Insurance Company, 1-1 Marunouchi, 2-chome, Chiyoda-ku,

Unrealized Gains in Stocks from the Viewpoint of Investment Risk Management Naoki Matsuyama Investment Administration Department, The Neiji Mutual Life Insurance Company, 1-1 Marunouchi, 2-chome, Chiyoda-ku,

With interest rates at historically low levels, and the U.S. economy showing continued strength,

Managing Interest Rate Risk in Your Bond Holdings THE RIGHT STRATEGY MAY HELP FIXED INCOME PORTFOLIOS DURING PERIODS OF RISING INTEREST RATES. With interest rates at historically low levels, and the U.S.

Managing Interest Rate Risk in Your Bond Holdings THE RIGHT STRATEGY MAY HELP FIXED INCOME PORTFOLIOS DURING PERIODS OF RISING INTEREST RATES. With interest rates at historically low levels, and the U.S.

Good for business: get your forex transactions on track

Companies Foreign currencies Good for business: get your forex transactions on track Do you want to hedge foreign currency risks or invest in forex? A bank that takes your needs into account and provides

Companies Foreign currencies Good for business: get your forex transactions on track Do you want to hedge foreign currency risks or invest in forex? A bank that takes your needs into account and provides

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

LDI Fundamentals: Is Our Strategy Working? A survey of pension risk management metrics Pension plan sponsors have increasingly been considering liability-driven investment (LDI) strategies as an approach

Principles and Trade-Offs when Making Issuance Choices in the UK

Please cite this paper as: OECD (2011), Principles and Trade-Offs when Making Issuance Choices in the UK, OECD Working Papers on Sovereign Borrowing and Public Debt Management, No. 2, OECD Publishing.

Please cite this paper as: OECD (2011), Principles and Trade-Offs when Making Issuance Choices in the UK, OECD Working Papers on Sovereign Borrowing and Public Debt Management, No. 2, OECD Publishing.

MBA Finance Part-Time Present Value

MBA Finance Part-Time Present Value Professor Hugues Pirotte Spéder Solvay Business School Université Libre de Bruxelles Fall 2002 1 1 Present Value Objectives for this session : 1. Introduce present value

MBA Finance Part-Time Present Value Professor Hugues Pirotte Spéder Solvay Business School Université Libre de Bruxelles Fall 2002 1 1 Present Value Objectives for this session : 1. Introduce present value

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

Risk and Return Models: Equity and Debt. Aswath Damodaran 1

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

2 Stock Price. Figure S1.1 Profit from long position in Problem 1.13

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

Problem 1.11. A cattle farmer expects to have 12, pounds of live cattle to sell in three months. The livecattle futures contract on the Chicago Mercantile Exchange is for the delivery of 4, pounds of cattle.

Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator

University of Stavanger (UiS) Stavanger Masters Program Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator The number in brackets is the weight for each problem. The weights

University of Stavanger (UiS) Stavanger Masters Program Final Exam MØA 155 Financial Economics Fall 2009 Permitted Material: Calculator The number in brackets is the weight for each problem. The weights

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Navigating through flexible bond funds

For professional investors Navigating through flexible bond funds WHITE PAPER February 2015 Kommer van Trigt Winfried G. Hallerbach ROBECO GLOBAL TOTAL RETURN BOND FUND Contents Introduction 3 Flexible

For professional investors Navigating through flexible bond funds WHITE PAPER February 2015 Kommer van Trigt Winfried G. Hallerbach ROBECO GLOBAL TOTAL RETURN BOND FUND Contents Introduction 3 Flexible

NPH Fixed Income Research Update. Bob Downing, CFA. NPH Senior Investment & Due Diligence Analyst

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

Chapter 12. Page 1. Bonds: Analysis and Strategy. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

Funds in Court Information Guide INVESTMENT RISKS

Funds in Court Information Guide INVESTMENT RISKS NOTE: The information in this document is for information purposes only. The information is not intended to be and does not constitute financial advice

Funds in Court Information Guide INVESTMENT RISKS NOTE: The information in this document is for information purposes only. The information is not intended to be and does not constitute financial advice