President s Report. December 9, 2015

|

|

|

- Ronald Quinn

- 9 years ago

- Views:

Transcription

1 President s Report December 9, 2015

2 Budget to Actual Direct Written Premium (DWP) 2

3 Budget to Actual Depopulation Net Earned Premium (NEP) 3

4 Budget to Actual Policies-In-Force (PIF) 4

5 Assumption Comparison 2014 to ,600,000 1,400,000 1,359,138 1,200,000 1,000,000 1,109,634 1,064, , , , , , , , , , OIR Approved Requested by Insurers Assumption Offers Made Assumed 5 Note: November and December 2015 Assumed values are estimated.

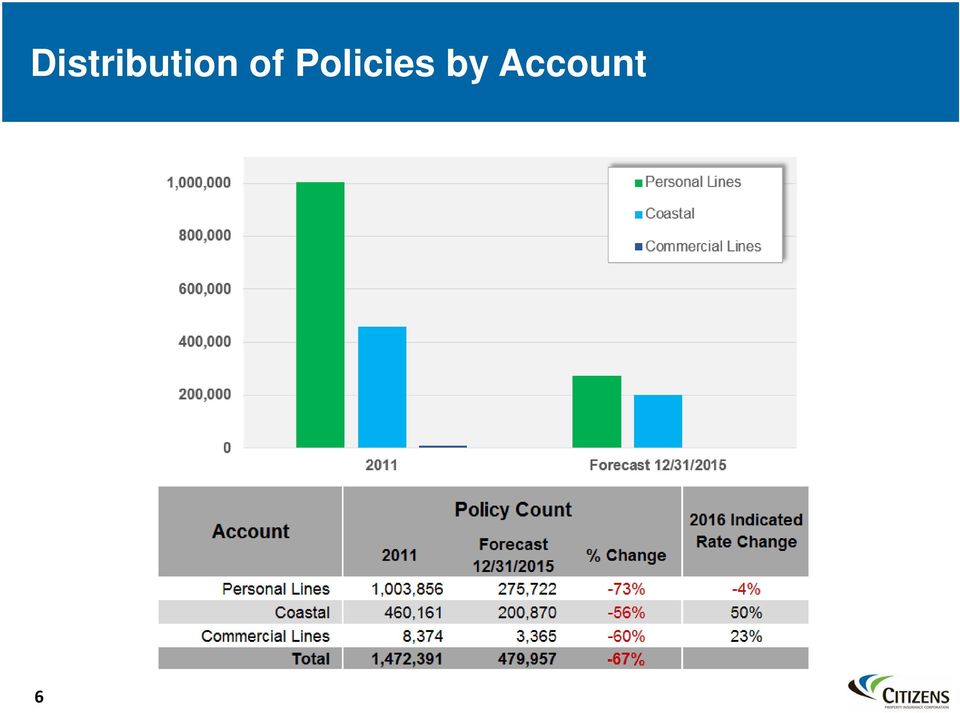

6 Distribution of Policies by Account 6

7 Forecasted Financial Statements ( ) *Private reinsurance placements for 2016 and 2017 include $204M and $115M of ceded premium, respectively. The 2016 ceded premium includes a committed $164M on multi year contracts not expiring in 2015 as well as $40M of risk transfer. 7

8 PML Reduction: 2015 Risk Transfer Timeline Went to Market for 2015 Placement Placement of 2015 Coverage Modeled Losses as of Date 1 in 100 Year Single Occurrence PML ($ in billions) Coastal Account PLA/CLA Total 12/31/2014 $ $ $ /30/2015 $ $ $ Pro Forma 2016 Placement 06/30/2016 $ $ $ Coastal Account storm risk decreased over 8% or $680 million from initial 2015 pricing (year end 2014) to the beginning of hurricane season (June 2015) With the success of the depopulation program, Citizens could see an additional 25% decrease in storm risk before the start of the 2016 hurricane season (from June 2015 to June 2016) 8 Notes: 1) PLA and CLA are combined to be consistent with Florida Hurricane Catastrophe Fund (FHCF) account allocation. PLA/CLA combined PMLs are added to the Coastal PMLs to be consistent for surplus distribution. 2) PMLs include a provision for loss adjustment expense.

8 Notes: 1) PLA and CLA are combined to be consistent")

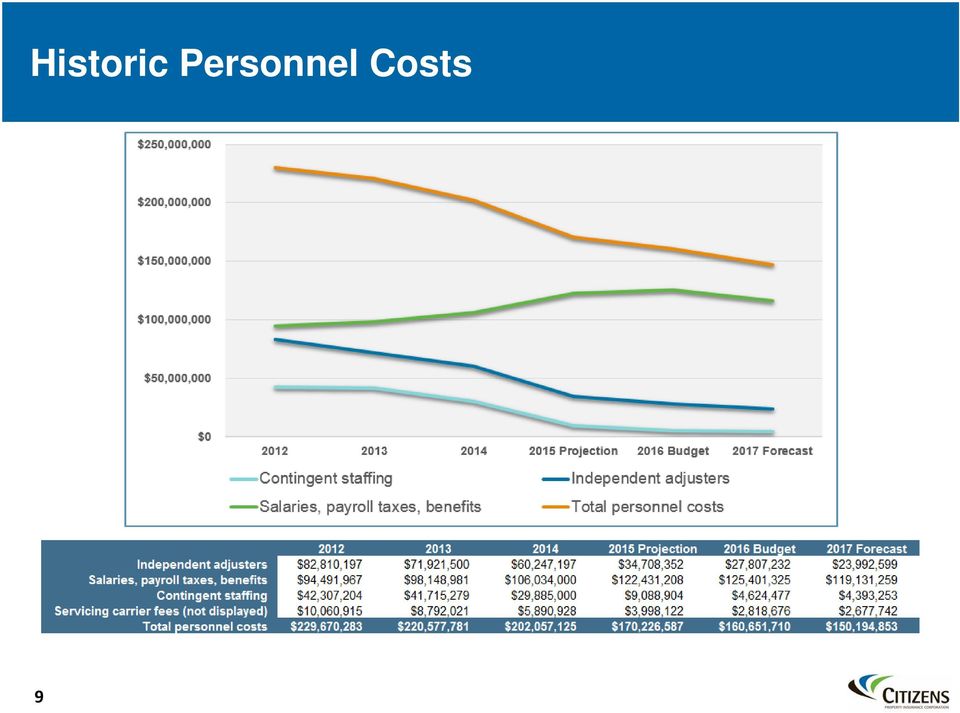

9 Historic Personnel Costs 9

10 Historic Resources 10 Notes: 1) "Year End" is as of 12/31 each calendar year; The 2015 YTD is as of 11/6/2015 2) "Service Carriers" are McNeill/CCC and MGI/Personal Lines only

11 Resource Demands YTD 2013 YTD 2014 YTD 2015 Litigated Claims Reopened 6,303 7,307 8,214-2,000 4,000 6,000 8,000 10,000 Litigated claims have been averaging 800 new cases per month, and that trend is expected to continue into 2016 Cycle time for litigated cases from FNOL is averaging 740 days and is expected to continue into 2016 Monthly transaction activity: Average of 11,000 new business policies/month stable Average of 95,000 Customer Care Center calls/month stable to increasing Average of 6,400 Personal Lines Customer Service calls/month stable Average of 230 Commercial Lines Customer Service calls/month stable Average of 1,500 IT service requests/month stable to increasing Depopulation transactions (tags and untags) have increased 25-30% year-over-year since

have increased 25-30%")

12 Depopulated Policies Serviced by CPIC Following depopulation, Citizens continues to service policies removed through renewal on the paper of the takeout carrier. The Policies Serviced metric provides the number of policies in that status as of each year end in the exhibit presented here. Services on the policy include the following: Endorsement billing/processing Policy change requests Collection and application of premium installments Customer Care/Call Center services In addition, for reference in the table below, policies serviced counts are shown as a percentage of year-end PIF. Therefore, as in the case of projected 2015 values, for every 100 policies in force, there are approximately 44 that Citizens will continue to service until such time as the policy renews. Account PLA 33.03% 53.07% 48.67% 21.05% 9.52% CLA 0.00% 45.57% 33.46% 27.78% 12.18% Coastal 10.21% 28.31% 38.88% 26.32% 11.63% Combined 24.15% 42.43% 44.47% 23.02% 10.21% 12

13 Expense Ratio Comparison The expense ratio; (Administrative and Underwriting Expenses / DWP) has been utilized as a measure of how efficiently Citizens operates in comparison to private market carriers within the state Provided below is a listing of expense ratios for a select group of Florida domiciled carriers Underwriting expenses as displayed have been adjusted to remove the effects of ceding commission on ceded and assumed reinsurance. Citizens estimates our rate inadequacy s impact on the expense ratio to be approximately 1-3% taking into consideration statutory and glide path requirements. Citizens combined expense ratio has increased as a result of the increasing rate at which policies have been depopulated since On the following exhibits, the Administrative and Underwriting Expenses are plotted year over year from actuals with preliminary forecasts for 2016 and

14 Administrative Expense Components CITIZENS SPECIFIC PROGRAMS AFFECTING EXPENSES Glide path Depopulation Program, Market Services Clearinghouse Litigated Claims Strategy Insource Strategy (KPMG) Field Underwriting, Field Agency Management Vendor Management Scalability (expand & contract based upon market conditions, catastrophe readiness for all policy count scenarios) Core Program STANDARD ADMINISTRATIVE EXPENSE Salaries and related employee costs Contingent staffing Professional services Office and equipment rental costs Software maintenance and licensing Telecommunications Depreciation Other operating expenses 16.3% Expense Ratio 27% VARIABLE UNDERWRITING EXPENSE Varies with direct written premium Producer commissions Taxes and assessments Servicing carrier fees Other underwriting expenses Other processing fees 10.7% 13

15 Underwriting Expense Results Underwriting expenses include: Producer commissions Taxes and assessments Servicing carrier fees Other underwriting expenses Other processing fees Underwriting Expense Results Underwriting Expenses $ 281,161,338 $ 210,377,381 $ 132,842,848 $ 97,489,360 $ 86,890,878 Direct Written Premium $ 2,761,637,564 $ 2,083,869,844 $ 1,285,273,193 $ 909,235,682 $ 838,353,727 Underwriting Ratio 10.18% 10.10% 10.34% 10.72% 10.36% Underwriting expenses respond to the overall level of direct written premium and policy transactions processed by third parties (ie. MacNeill). As a result, this expense category s overall contribution to the expense ratio is anticipated to remain at approximately 10%, despite the significant overall dollar value decrease in the category. 15

.")

16 Administrative Expense Results Administrative Expenses include: Salaries and related employee costs Contingent staffing Professional services Office and equipment rental costs Software maintenance and licensing Telecommunications Depreciation Other operating expenses Administrative expenses for 2016 were budgeted to achieve an overall 5% decrease from the targeted administrative expense for the year ended 12/31/2015. Therefore, 2017 administrative expenses were forecasted and are displayed with a 7.5% decrease as compared to 2016 budget. 16

17 Historical Expense and Premium Comparison 04/ 05 Storm Season Poe Assumption Premium Rates held at 2006 rate level through 2009 Wind Mitigation Credits introduced; Discounts doubled in second year High volume of depopulation Wind Mitigation Inspection Outreach Insolvency of 3 domestic insurers Premium Rate Glide Path Core Policy System Implementation High volume of depopulation 17

18 Underwriting and Acquisition Costs Incurred on Depopulation ANNUAL CEDED WRITTEN PREMIUM DEPOPULATION P 2016 B 2017 F PLA $ (289,278,084) $ (261,513,840) $ (105,584,893) $ (47,012,807) $ (21,363,134) CLA (41,103,961) (10,721,420) (8,129,629) (3,055,483) CST (98,289,021) (153,228,561) (80,510,684) (77,095,754) (32,226,025) COMB $ (387,567,105) $ (455,846,362) $ (196,816,996) $ (132,238,189) $ (56,644,642) CEDING COMMISSIONS FOREGONE ON DEPOPULATED 10.5% P 2016 B 2017 F PLA $ (30,374,199) $ (27,458,953) $ (11,086,414) $ (4,936,345) $ (2,243,129) CLA (4,315,916) (1,125,749) (853,611) (320,826) CST (10,320,347) (16,088,999) (8,453,622) (8,095,054) (3,383,733) COMB $ (40,694,546) $ (47,863,868) $ (20,665,785) $ (13,885,010) $ (5,947,687) DWP $ 2,761,637,564 $ 2,083,869,844 $ 1,285,273,193 $ 909,235,682 $ 838,353,727 18

$ (27,458,953) $ (11,086,414) $ (4,936,345) $ (2,243,129) CLA (4,315,916) (1,125,749) (853,611) (320,826) CST (10,320,347) (16,088,999)")

19 Coastal Account: 2015 Layer Chart (not to scale) Projection ($'s in millions) Combined PLA CLA Coastal Beginning Surplus $ 7,384.0 $ 2,487.6 $ 1,559.4 $ 3,337.0 Net income / (loss) $ 70.9 $ 77.8 $ 50.7 $ (57.6) Ending Surplus $ 7,454.9 $ 2,565.4 $ 1,610.1 $ 3, Surplus Exposed (%) 26% 16% 6% 43% 1 50 Surplus Exposed (%) 28% 18% 7% 46% Surplus Exposed (%) 47% 51% 19% 57%

26% 16% 6% 43% 1 50 Surplus Exposed (%) 28% 18% 7% 46% 1 100 Surplus")

20 PLA/CLA: 2015 Layer Chart (not to scale) 20

")

21 Coastal Account: Projected 2016 Layer Chart No New Reinsurance Purchase (not to scale) The following surplus exposed, net income and ending surplus detail by account includes a committed $164M on multi-year contracts not expiring in The effect of the budgeted private risk transfer spend in the Coastal Account of $40M in a lower layer (not included in the layer chart above) is shown in the final column. The percentage of surplus exposed varies depending on the composition of the risk transfer program placed ($'s in millions) No New Risk Transfer Private Risk Transfer Combined PLA CLA Coastal Spend of $40M Coastal Beginning Surplus $ 7,454.9 $ 2,565.4 $ 1,610.1 $ 3,279.4 $ 3,279.4 Net income / (loss) $ 53.4 $ 55.1 $ 26.0 $ (27.7) $ (67.7) Ending Surplus $ 7,508.3 $ 2,620.5 $ 1,636.1 $ 3,251.7 $ 3, Surplus Exposed (%) 23% 13% 5% 40% 29% 33% 1 50 Surplus Exposed (%) 29% 14% 5% 53% 38% 43% Surplus Exposed (%) 48% 43% 16% 68% 53% 57%

22 PLA/CLA: Projected 2016 Layer Chart (not to scale) 22

23 Coastal Account: Forecast 2017 Layer Chart (not to scale) Forecast includes $115 million for the purchase of new private risk transfer in the Coastal Account. The percentage of surplus exposed may vary depending on the composition of the risk transfer program placed Forecast ($'s in millions) Combined PLA CLA Coastal Beginning Surplus $ 7,468.3 $ 2,620.5 $ 1,636.1 $ 3,211.7 Net income / (loss) $ $ 38.3 $ 27.6 $ 60.3 Ending Surplus $ 7,594.5 $ 2,658.8 $ 1,663.7 $ 3, Surplus Exposed (%) 14% 13% 3% 20% 1 50 Surplus Exposed (%) 17% 14% 4% 26% Surplus Exposed (%) 41% 43% 11% 55%

24 PLA/CLA: Projected 2017 Layer Chart (not to scale) 24

25 Reconciliation of Storm Risk and Surplus 25 Notes: 1) Storm Risk is as measured by 100 year probable maximum loss (PML) plus estimated loss adjustment expenses using the Florida Hurricane Catastrophe Fund (FHCF) account allocation where PLA and CLA are combined. PLA/CLA combined PMLs are added to the Coastal PMLs to be consistent for surplus distribution. 2) Surplus, Florida Hurricane Catastrophe Fund (FHCF) & Assessments are as projected at beginning of storm season. Not all PLA/CLA surplus is needed to fund storm risk in 2014; a deficit in the Coastal Account results in the assessment. 3) In , a portion of private risk transfer covers a larger storm risk than shown above. 4) 2015 FHCF projections are preliminary and actual amounts may differ significantly from these projections. 5) PMLs from use a weighted average of 1/3rd Standard Sea Surface Temperature (SSST) and 2/3rd Warm Sea Surface Temperature (WSST) PMLs reflect only SSST and are based on 06/30/2015 exposures.

26 Appendix: Layer Chart Assumptions ASSUMPTIONS 2015 Citizens 2015 Budgeted DWP $1.67 Billion (Coastal $0.84 Billion; PLA/CLA $0.83 Billion) Citizens Policyholder Surcharge Maximum % Per Account 15% 2015 Regular Assessment Base (projected) $37.63 Billion Regular Assessment Maximum % Per Account 2% for Coastal; 0% for PLA/CLA 2014 Emergency Assessment Base $39.30 Billion PMLs are based on modeled losses as of June 30, 2015 per AIR Touchstone, Version 1.5 reflecting the Standard Sea Surface Temperature (SSST) Event Catalog including Demand Surge, excluding Storm Surge, and include 10% of loss to account for loss adjustment expense (LAE). Interim Return Periods are derived by Linear Interpolation 2015 Projected Surplus = audited 2014 surplus projected net income assuming no hurricanes. Citizens 2015 FHCF coverage is based on preliminary retention estimates and payment multiples. Actual Citizens FHCF attachment and limits of coverage could differ significantly from estimates. NOTES These charts are imperfect! They attempt to show projected claims paying resources, but they are approximations only. Four significant complicating factors are described below: 1) Coastal PML vs. PLA/CLA PML: An actual 100 year PML event in Coastal Account may not be a 100 year PML event for PLA/CLA. The relative magnitude of actual losses for Coastal and PLA/CLA will depend on the storm size and path 2) Combining PLA and CLA: The PLA and CLA are separate accounts for deficit calculation and assessment purposes, but are combined for FHCF and credit purposes. It is impossible to accurately show the PML resources situation of these accounts on either separate or combined charts since simplifications must be made in either case that could prove materially inaccurate. Although we show the combined accounts, there is no guarantee that they will have deficits at the same time or of similar magnitude 3) Non residential exposure: Commercial non residential (CNR) exposures in the CLA and Coastal Account are not reinsured by FHCF. Actual deficits and assessments may be significantly different than an aggregated PML would otherwise indicate. The charts include a provisional estimate for CNR losses of 14.5% in the Coastal Account for all return times for 2015, 15% for projected 2016 and CNR is a negligible portion of the PLA/CLA Accounts and so is not considered in those charts 4) Liquidity: These charts do not show the liquidity needs of the accounts. An account with ample PML resources may still require liquidity as many of the PML resources are not available immediately following a major hurricane. The timing and magnitude of receivables such as FHCF recoveries and assessments are unknown. 26

Citizens Property Insurance Corporation Presentation to the Financial Services Commission

Citizens Property Insurance Corporation Presentation to the Financial Services Commission Barry Gilway, President/CEO and Executive Director June 26, 2012 Policy Counts An Historical Look at Citizens Growth

Citizens Property Insurance Corporation Presentation to the Financial Services Commission Barry Gilway, President/CEO and Executive Director June 26, 2012 Policy Counts An Historical Look at Citizens Growth

Citizens Property Insurance Corporation

Citizens Property Insurance Corporation Barry Gilway, President/CEO and Executive Director Sharon Binnun, CFO December 4, 2012 Citizens Basics What is Citizens? A State-created, not-for-profit, tax-exempt

Citizens Property Insurance Corporation Barry Gilway, President/CEO and Executive Director Sharon Binnun, CFO December 4, 2012 Citizens Basics What is Citizens? A State-created, not-for-profit, tax-exempt

Florida Residential Property Exposure

Florida Office of Insurance Regulation Presentation for the: Florida Chamber of Commerce Annual Insurance Summit Orlando, Florida January 2010 The materials presented here were compiled by the OIR and

Florida Office of Insurance Regulation Presentation for the: Florida Chamber of Commerce Annual Insurance Summit Orlando, Florida January 2010 The materials presented here were compiled by the OIR and

As of July 31, 2011, Citizens reported it had a total of 1,408,584 policies in-force throughout the state.

Committee on Banking and Insurance Statement of the Issue The Florida Senate Issue Brief 2012-226 September 2011 CITIZENS PROPERTY INSURANCE Citizens Property Insurance Corporation (Citizens or the Corporation)

Committee on Banking and Insurance Statement of the Issue The Florida Senate Issue Brief 2012-226 September 2011 CITIZENS PROPERTY INSURANCE Citizens Property Insurance Corporation (Citizens or the Corporation)

Study of Recent Legislative Changes to Florida Property Insurance Mechanisms

Study of Recent Legislative Changes to Florida Property Insurance Mechanisms Prepared for Associated Industries of Florida March 19, 2007 2007 Towers Perrin Summary of key findings Recent Florida legislation,

Study of Recent Legislative Changes to Florida Property Insurance Mechanisms Prepared for Associated Industries of Florida March 19, 2007 2007 Towers Perrin Summary of key findings Recent Florida legislation,

Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. November 2014.

Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting November 2014 Document 214114 Ce document est disponible en français 2014 Canadian Institute of Actuaries

Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting November 2014 Document 214114 Ce document est disponible en français 2014 Canadian Institute of Actuaries

Understanding Citizens Assessments. A review of assessments based on Florida Law

Understanding Citizens Assessments A review of assessments based on Florida Law Effective July 1, 2008 Course objective Understand the assessment mechanism as it relates to Citizens accounts. 2 Three Separate

Understanding Citizens Assessments A review of assessments based on Florida Law Effective July 1, 2008 Course objective Understand the assessment mechanism as it relates to Citizens accounts. 2 Three Separate

Citizens Property Insurance Corporation (An enterprise fund of the State of Florida) Financial Statements and Supplementary Information

Financial Statements and Supplementary Information") Citizens Property Insurance Corporation (An enterprise fund of the State of Florida) Financial Statements and Supplementary Information Years Ended December 31, 2015 and 2014 Table of Contents Independent

Citizens Property Insurance Corporation (An enterprise fund of the State of Florida) Financial Statements and Supplementary Information Years Ended December 31, 2015 and 2014 Table of Contents Independent

Florida Hurricane Catastrophe Fund. Annual Report of Aggregate Net Probable Maximum Losses, Financing Options, and Potential Assessments

Florida Hurricane Catastrophe Fund Annual Report of Aggregate Net Probable Maximum Losses, Financing Options, and Potential Assessments Table of Contents Purpose and Scope 3 Introduction 3 Aggregate Net

Florida Hurricane Catastrophe Fund Annual Report of Aggregate Net Probable Maximum Losses, Financing Options, and Potential Assessments Table of Contents Purpose and Scope 3 Introduction 3 Aggregate Net

Current Status of the Florida Property Insurance Market

2010 Property Insurance Summit Current Status of the Florida Property Insurance Market January 28, 2010 Orlando, Florida John Forney, CFA Managing Director, Public Finance Raymond James & Associates, Inc.

2010 Property Insurance Summit Current Status of the Florida Property Insurance Market January 28, 2010 Orlando, Florida John Forney, CFA Managing Director, Public Finance Raymond James & Associates, Inc.

11/15/06 12:20pm PROPERTY & CASUALTY INSURANCE REFORM COMMITTEE FINAL RECOMMENDATIONS (11/15/06)

") PROPERTY & CASUALTY INSURANCE REFORM COMMITTEE FINAL RECOMMENDATIONS (11/15/06) Residential Insurance Market/Consumer Issues 1. Transparency for consumers (residential and commercial). Require the premium

PROPERTY & CASUALTY INSURANCE REFORM COMMITTEE FINAL RECOMMENDATIONS (11/15/06) Residential Insurance Market/Consumer Issues 1. Transparency for consumers (residential and commercial). Require the premium

F INANCIAL S TATEMENTS S TATUTORY B ASIS. Citizens Property Insurance Corporation Years Ended December 31, 2004 and 2003 AND S UPPLEMENTAL S CHEDULES

F INANCIAL S TATEMENTS S TATUTORY B ASIS AND S UPPLEMENTAL S CHEDULES Citizens Property Insurance Corporation Years Ended December 31, 2004 and 2003 Financial Statements Statutory Basis and Supplemental

F INANCIAL S TATEMENTS S TATUTORY B ASIS AND S UPPLEMENTAL S CHEDULES Citizens Property Insurance Corporation Years Ended December 31, 2004 and 2003 Financial Statements Statutory Basis and Supplemental

Biennial Report to the 84th Legislature December 30, 2014

Biennial Report to the 84 th Legislature December 30, 2014 Table of Contents Purpose... 2 Executive Summary... 3 TWIA Operations Overview... 4 History and Regulatory Changes... 4 Post-HB 3 Improvements...

Biennial Report to the 84 th Legislature December 30, 2014 Table of Contents Purpose... 2 Executive Summary... 3 TWIA Operations Overview... 4 History and Regulatory Changes... 4 Post-HB 3 Improvements...

Basic Reinsurance Accounting Selected Topics

Basic Reinsurance Accounting Selected Topics By Ralph S. Blanchard, III, FCAS, MAAA and Jim Klann, FCAS, MAAA CAS Study Note The purpose of this study note is to educate actuaries on certain basic reinsurance

Basic Reinsurance Accounting Selected Topics By Ralph S. Blanchard, III, FCAS, MAAA and Jim Klann, FCAS, MAAA CAS Study Note The purpose of this study note is to educate actuaries on certain basic reinsurance

CALIFORNIA EARTHQUAKE AUTHORITY. Financial Statements. December 31, 2001 and 2000. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Three Embarcadero Center San Francisco, CA 94111 Independent Auditors Report The Board of Directors California Earthquake Authority: We have

Financial Statements (With Independent Auditors Report Thereon) Three Embarcadero Center San Francisco, CA 94111 Independent Auditors Report The Board of Directors California Earthquake Authority: We have

Insurance Company Solvency Regulation

Insurance Company Solvency Regulation An Overview for the Financial Services Commission Presented by Insurance Commissioner Kevin M. McCarty January 13, 2009 1 Overview Evolution of the Florida property

Insurance Company Solvency Regulation An Overview for the Financial Services Commission Presented by Insurance Commissioner Kevin M. McCarty January 13, 2009 1 Overview Evolution of the Florida property

) ) ) ) ) ) PREPARED DIRECT TESTIMONY OF SAN DIEGO GAS AND ELECTRIC COMPANY (U 902 E)

) ) ) ) ) PREPARED DIRECT TESTIMONY OF SAN DIEGO GAS AND ELECTRIC COMPANY (U 902 E)") Application No: A.0-0-xxx Exhibit No.: Witness: Maury De Bont In the Matter of the Application of San Diego Gas & Electric Company (U 0 E) for Authorization to Recover Unforeseen Liability Insurance Premium

Application No: A.0-0-xxx Exhibit No.: Witness: Maury De Bont In the Matter of the Application of San Diego Gas & Electric Company (U 0 E) for Authorization to Recover Unforeseen Liability Insurance Premium

North Carolina Insurance Underwriting Association

North Carolina Insurance Underwriting Association Statutory Financial Statements and Supplemental Schedules (With Independent Auditor s Report Thereon) December 31, 2014 and 2013 Contents Independent Auditor

North Carolina Insurance Underwriting Association Statutory Financial Statements and Supplemental Schedules (With Independent Auditor s Report Thereon) December 31, 2014 and 2013 Contents Independent Auditor

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE EDUCATION INSURANCE COMPANY COMBINING FINANCIAL STATEMENTS JUNE 30, 2013

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE COMBINING FINANCIAL STATEMENTS UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE TABLE OF CONTENTS Page(s) Independent Auditors Report

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE COMBINING FINANCIAL STATEMENTS UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE TABLE OF CONTENTS Page(s) Independent Auditors Report

Citizens Property Insurance Corporation

FINANCIAL STATEMENTS STATUTORY BASIS AND SUPPLEMENTAL SCHEDULES Citizens Property Insurance Corporation December 31, 2013 and 2012 Financial Statements Statutory Basis and Supplemental Schedules Table

FINANCIAL STATEMENTS STATUTORY BASIS AND SUPPLEMENTAL SCHEDULES Citizens Property Insurance Corporation December 31, 2013 and 2012 Financial Statements Statutory Basis and Supplemental Schedules Table

James Walmsley, Senior Manager, Lloyd s International Market Access (extension 5131)

") market bulletin Ref: Y3982 Title Florida: new legislation HB 1A Purpose Type From The law referred to as HB 1A contains provisions affecting many aspects of the insurance industry in Florida. This bulletin

market bulletin Ref: Y3982 Title Florida: new legislation HB 1A Purpose Type From The law referred to as HB 1A contains provisions affecting many aspects of the insurance industry in Florida. This bulletin

August 20, 2012. Docket number: 2012-15685. Dear Director McRaith,

Director, Federal Insurance Office Department of the Treasury Federal Insurance Office 1500 Pennsylvania Avenue NW Washington, D.C. 20220 Re: Input to FIO s study on the breadth and scope of the global

Director, Federal Insurance Office Department of the Treasury Federal Insurance Office 1500 Pennsylvania Avenue NW Washington, D.C. 20220 Re: Input to FIO s study on the breadth and scope of the global

MINNESOTA AGGREGATE FINANCIAL DATA REPORTING GUIDEBOOK. Annual Calls for Experience Valued as of December 31, 2015

MINNESOTA AGGREGATE FINANCIAL DATA REPORTING GUIDEBOOK Annual Calls for Experience Valued as of December 31, 2015 11/5/2015 ANNUAL CALLS FOR EXPERIENCE As the licensed Data Service Organization in Minnesota,

MINNESOTA AGGREGATE FINANCIAL DATA REPORTING GUIDEBOOK Annual Calls for Experience Valued as of December 31, 2015 11/5/2015 ANNUAL CALLS FOR EXPERIENCE As the licensed Data Service Organization in Minnesota,

Citizens Property Insurance Corporation

Citizens Property Insurance Corporation Barry Gilway, President/CEO and Executive Director October 8, 2013 Commercial Non-Residential Business Overview Commercial Non-Residential Citizens writes both commercial

Citizens Property Insurance Corporation Barry Gilway, President/CEO and Executive Director October 8, 2013 Commercial Non-Residential Business Overview Commercial Non-Residential Citizens writes both commercial

Massachusetts General Law Chapter 152, 25O and 53A. Classification of risks and premiums: distribution of premiums among employers.

1 A. General Massachusetts General Law Chapter 152, 25O and 53A. Classification of risks and premiums: distribution of premiums among employers. 1. Who May Insure Workers Compensation Risks Any insurance

1 A. General Massachusetts General Law Chapter 152, 25O and 53A. Classification of risks and premiums: distribution of premiums among employers. 1. Who May Insure Workers Compensation Risks Any insurance

The New Florida Insurance Bill SB 130

BILL: SB 130 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional

BILL: SB 130 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional

Florida Property Insurance Market Analysis and Recommendations

Florida Property Insurance Market Analysis and Recommendations Presentation to The Florida Senate Banking and Insurance Committee February 6, 2013 Locke Burt, Chairman and President Security First Insurance

Florida Property Insurance Market Analysis and Recommendations Presentation to The Florida Senate Banking and Insurance Committee February 6, 2013 Locke Burt, Chairman and President Security First Insurance

The Florida Property Insurance Debate: Governor Rick Scott and Charlie Crist Campaign Review

The Florida Property Insurance Debate: Governor Rick Scott and Charlie Crist Campaign Review KEY PLAYERS Jeb Bush Florida Governor 1999-2006 Charlie Crist Florida Governor 2007-2010 Rick Scott Florida

The Florida Property Insurance Debate: Governor Rick Scott and Charlie Crist Campaign Review KEY PLAYERS Jeb Bush Florida Governor 1999-2006 Charlie Crist Florida Governor 2007-2010 Rick Scott Florida

financial supplement 31 december 2009 Contact: Jonathan Creagh-Coen Telephone: +44 (0) 207 264 4066 Email: [email protected]

207 264 4066 Email: jcc@lancashiregroup.com") financial supplement 31 december 2009 Contact: Jonathan Creagh-Coen Telephone: +44 (0) 207 264 4066 Email: [email protected] NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE

financial supplement 31 december 2009 Contact: Jonathan Creagh-Coen Telephone: +44 (0) 207 264 4066 Email: [email protected] NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE

Minnesota Workers' Compensation Assigned Risk Plan. Financial Statements Together with Independent Auditors' Report

Minnesota Workers' Compensation Assigned Risk Plan Financial Statements Together with Independent Auditors' Report December 31, 2012 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS: Balance

Minnesota Workers' Compensation Assigned Risk Plan Financial Statements Together with Independent Auditors' Report December 31, 2012 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS: Balance

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look. Moderator: W. Scott Lennox, FSA, FCAS, FCIA

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

Session 25 L, Introduction to General Insurance Ratemaking & Reserving: An Integrated Look Moderator: W. Scott Lennox, FSA, FCAS, FCIA Presenter: Houston Cheng, FCAS, FCIA Society of Actuaries 2013 Annual

Residual Markets. Residual Markets in which insurers participate to make coverage available to those unable to obtain coverage in Standard Market

Residual Markets David C. Marlett, PhD, CPCU Chair, Department of Finance, Banking and Insurance Appalachian State University [email protected] 828.262.2849 http://insurance.appstate.edu/ Residual

Residual Markets David C. Marlett, PhD, CPCU Chair, Department of Finance, Banking and Insurance Appalachian State University [email protected] 828.262.2849 http://insurance.appstate.edu/ Residual

United Fire & Casualty Company Reports Record Quarterly Earnings

FOR IMMEDIATE RELEASE For: United Fire & Casualty Company 118 Second Avenue SE, PO Box 73909 Cedar Rapids, Iowa 52407-3909 Contact: John A. Rife, President/CEO, 319-399-5700 United Fire & Casualty Company

FOR IMMEDIATE RELEASE For: United Fire & Casualty Company 118 Second Avenue SE, PO Box 73909 Cedar Rapids, Iowa 52407-3909 Contact: John A. Rife, President/CEO, 319-399-5700 United Fire & Casualty Company

THE EMPIRE LIFE INSURANCE COMPANY

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2013 Unaudited Issue Date: August 9, 2013 These condensed interim consolidated financial

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2013 Unaudited Issue Date: August 9, 2013 These condensed interim consolidated financial

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY. FIRST QUARTER 2000 Consolidated Financial Statements (Non audited)

") INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

Florida Senate - 2016 SB 1274

By Senator Latvala 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 A bill to be entitled An act relating to sinkhole insurance; amending s. 624.407, F.S.; specifying

By Senator Latvala 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 A bill to be entitled An act relating to sinkhole insurance; amending s. 624.407, F.S.; specifying

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU EXPLORING THE COST OF A WORKERS COMPENSATION INSURANCE POLICY

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU EXPLORING THE COST OF A WORKERS COMPENSATION INSURANCE POLICY 2007 INTRODUCTION This booklet provides a basic explanation of how the cost of a New Jersey

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU EXPLORING THE COST OF A WORKERS COMPENSATION INSURANCE POLICY 2007 INTRODUCTION This booklet provides a basic explanation of how the cost of a New Jersey

FINANCIAL REVIEW. 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

ACTUARIAL CONSIDERATIONS IN THE DEVELOPMENT OF AGENT CONTINGENT COMPENSATION PROGRAMS

ACTUARIAL CONSIDERATIONS IN THE DEVELOPMENT OF AGENT CONTINGENT COMPENSATION PROGRAMS Contingent compensation plans are developed by insurers as a tool to provide incentives to agents to obtain certain

ACTUARIAL CONSIDERATIONS IN THE DEVELOPMENT OF AGENT CONTINGENT COMPENSATION PROGRAMS Contingent compensation plans are developed by insurers as a tool to provide incentives to agents to obtain certain

Reflecting Reinsurance Costs in Rate Indications for Homeowners Insurance by Mark J. Homan, FCAS

Reflecting Reinsurance Costs in Rate Indications for Homeowners Insurance by Mark J. Homan, FCAS 223 Reflecting Reinsurance Costs in Rate Indications for Homeowners Insurance by Mark J. Homan Biograuhv

Reflecting Reinsurance Costs in Rate Indications for Homeowners Insurance by Mark J. Homan, FCAS 223 Reflecting Reinsurance Costs in Rate Indications for Homeowners Insurance by Mark J. Homan Biograuhv

Homeowners Insurance in the States

Testimony to the Senate Business and Commerce Committee Senator John J. Carona, Chair Texas Legislature Tuesday, July 10, 2012 Heather Morton National Conference of State Legislatures Denver, Colorado

Testimony to the Senate Business and Commerce Committee Senator John J. Carona, Chair Texas Legislature Tuesday, July 10, 2012 Heather Morton National Conference of State Legislatures Denver, Colorado

WORKERS COMPENSATION AND EMPLOYERS LIABILITY INSURANCE POLICY RETROSPECTIVE PREMIUM ENDORSEMENT THREE YEAR PLAN MULTIPLE LINES

WORKERS COMPENSATION AND EMPLOYERS LIABILITY INSURANCE POLICY RETROSPECTIVE PREMIUM ENDORSEMENT THREE YEAR PLAN MULTIPLE LINES This endorsement is issued because you chose to have the cost of the insurance

WORKERS COMPENSATION AND EMPLOYERS LIABILITY INSURANCE POLICY RETROSPECTIVE PREMIUM ENDORSEMENT THREE YEAR PLAN MULTIPLE LINES This endorsement is issued because you chose to have the cost of the insurance

Statutory Financial Statements and Report of Independent Certified Public Accountants. Massachusetts Catholic Self-Insurance Group, Inc.

Statutory Financial Statements and Report of Independent Certified Public Accountants Massachusetts Catholic Self-Insurance Group, Inc. Contents Page Report of Independent Certified Public Accountants

Statutory Financial Statements and Report of Independent Certified Public Accountants Massachusetts Catholic Self-Insurance Group, Inc. Contents Page Report of Independent Certified Public Accountants

PNB Life Insurance Inc. Risk Management Framework

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

Group Captive Insurance Programs for Property and Casualty Coverages

Group Captive Insurance Programs for Property and Casualty Coverages Duke Niedringhaus, ARM Vice President J.W. Terrill, Inc. April 2013 Group captive insurance programs can be an attractive alternative

Group Captive Insurance Programs for Property and Casualty Coverages Duke Niedringhaus, ARM Vice President J.W. Terrill, Inc. April 2013 Group captive insurance programs can be an attractive alternative

GLOSSARY OF ACTUARIAL AND RATEMAKING TERMINOLOGY

GLOSSARY OF ACTUARIAL AND RATEMAKING TERMINOLOGY Term Accident Accident Date Accident Period Accident Year Case- Incurred Losses Accident Year Experience Acquisition Cost Actuary Adverse Selection (Anti-Selection,

GLOSSARY OF ACTUARIAL AND RATEMAKING TERMINOLOGY Term Accident Accident Date Accident Period Accident Year Case- Incurred Losses Accident Year Experience Acquisition Cost Actuary Adverse Selection (Anti-Selection,

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

Regulatory Process for Reviewing Hurricane Models and use in Florida Rate Filings Robert Lee, FCAS Florida Office of Insurance Regulation CAS IN FOCUS TAMING CATS OCTOBER 2012 1 Antitrust Notice The Casualty

U.S. Homeowners Market

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

U.S. Homeowners Market Casualty Actuarial Society Spring Meeting Kelleen Arquette, FCAS, MAAA May 2013 2013 Towers Watson. All rights reserved. AGENDA Agenda Market Overview Market Definition Direct Written

GLOSSARY. A contract that provides for periodic payments to an annuitant for a specified period of time, often until the annuitant s death.

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with the Group and its business. The terms and their meanings may not correspond to standard industry

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with the Group and its business. The terms and their meanings may not correspond to standard industry

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated