Massachusetts State Treasurer s Office (STO) Guidelines for Current and Advance Refundings

|

|

|

- Derrick Jordan

- 7 years ago

- Views:

Transcription

1 Massachusetts State Treasurer s Office (STO) Guidelines for Current and Advance Refundings The STO intends to evaluate refunding opportunities for Massachusetts bonds based on a refunding efficiency approach. 1 In the past, refunding decisions by the STO were based solely on a present value (PV) cashflow savings threshold test. In the future, in addition to PV savings, the STO will also consider in its decision the forfeited option value of the refunded bonds. In case the refunding bonds are also callable, their option value should also be incorporated. The STO will base its decision on whether the projected PV savings are sufficient in comparison to the net loss of option value. The STO will consider refunding proposals only if the efficiency of the transaction exceeds 85%. Please screen and analyze refunding opportunities based on the following assumptions: Calculation of savings Determine PV savings by discounting each cashflow using the spot rate derived from the non-call par curve for Commonwealth bonds For advance refundings, provide the projected escrow yield Option valuation Use a standard lognormal interest rate model (like Black-Karasinski or Black-Derman Toy) Assume 15% short-term volatility and 0% mean reversion factor In case of advance refunding, provide the estimated value of the advance refunding option (incremental to the value of the call/current refunding option). If the value of the advance refunding option is ignored, please disclose this fact. If the proposal calls for callable refunding bonds, include the option value of the refunding bonds Incorporate projected future transaction costs in the calculation of option value(s) Presentation Please use the spreadsheet being sent along with these guidelines as a template for presenting results of the refunding analysis back to the STO 1 Refunding efficiency: a generalized approach, Andrew J. Kalotay, Deane Yang, and Frank J. Fabozzi, Applied Financial Economics Letters, Vol. 3, Issue 3, May 2007, pages

2 A N D R E W K A L O T A Y A S S O C I A T E S, I N C. Interest Rate Volatility Input for Refunding Analysis April 23, 2013 Issuers of municipal bonds have traditionally used rules of thumb based on present value savings in order to make decisions on when to refund. For example, many will act when a threshold of 3% savings is reached. This is in marked contrast to the corporate and agency world, where issuers usually ensure that they capture a high percentage of the option value being given up. The ratio of savings to forfeited option value is referred to as refunding efficiency. 1 The State Treasurer s Office of the Commonwealth of Massachusetts wants to bring more rigorous analysis to bear on its refunding decisions, and has decided to use refunding efficiency rather than present value savings targets. In order to calculate the option value that is part of the efficiency calculation, it is necessary to specify an appropriate interest rate volatility. 2 The STO, in consultation with its advisors, Andrew Kalotay Associates, currently recommends 15%. Most sophisticated issuers in the taxable market use security-specific volatilities derived from the swaption volatility matrix according to the bond s maturity and remaining time to call. In the municipal market, where information is imperfect, we recommend a simpler approach. A single volatility has the advantage of allowing the STO to view all submitted refunding proposals on an apples-to-apples basis. If each proposing bank was allowed to specify its own volatility, this would not be possible. A question that may arise is whether the recommended volatility of 15% is too low or too high. Option value, which increases with volatility, forms the denominator in the refunding efficiency ratio. Thus, too high a volatility understates the efficiency, which in turn triggers fewer refundings. Conversely, too low a volatility overstates the efficiency, which results in refunding too early. A good starting point is to estimate the implied volatility of new callable issues. Unfortunately, in the municipal market the information available for this purpose is limited. In this vacuum, the MMD yield curves are relied on as a consensus benchmark. 1 As discussed in the guidelines provided by the STO. 2 This refers to the volatility of the short-term rate that would be an input, with zero mean reversion, into a Black-Karasinski or a Black-Derman-Toy interest rate process. The implied volatilities of longer rates would be lower than that of the of the short-term rate. Page 1 Andrew Kalotay Associates, inc., 61 Broadway, New York, NY

3 Figure 1: Implied Volatility in MMD 5% NC10 Curve (4/19/2013) Yield (%) Par NCL Stripped from MMD 5% NC10 at 25% vol MMD Par NCL Implied by MMD 5% NCL MMD 5% NCL Maturity (Years) MMD provides both a 5% callable (NC10) curve and a 5% optionless curve. We estimated the interest rate volatility implied by the relationship between these two curves. The results are shown on the Figure 1 above. It turns out that a volatility of 25% comes close to explaining the difference between MMD s 5% callable and optionless curves. We then applied a couple of sanity checks. In general, the better the credit, the more the market charges (in terms of implied volatility) for embedded call options. For example, the GSE s are charged a high percentage of swaption volatility levels for their callable issues. At the other extreme, the implied volatility of high yield callable bonds is negligible because investors are not averse to receiving their principal back early, in light of the credit risk. For reference, Table 1 below indicates that the volatility for swaptions, exercisable 10 years from now, ranges from 23.0% to 26.7% an upper bound, but obviously too high for municipalities. Table 1: Volatilities of At-The-Money Swaptions Excercisable in 10 Years (4/22/13) Underlying Swap Term (yrs) Volatility (%) Source: Bloomberg The second sanity check is to determine the implied coupon premium for par callable bonds relative to par non-callable bonds. Using 30NC10 as a reference point, our discussion with muni professionals suggests that most consider a basis point Page 2 Andrew Kalotay Associates, inc., 61 Broadway, New York, NY

4 coupon premium to be reasonable. Table 2 below shows that a volatility of 15% applied to the Massachusetts par NCL curve in the Refunding Example provided by the STO would result in a par callable coupon premium (relative to par NCL) of about 25 basis points. Table 2: Is a Volatility of 15% Reasonable? 30NC10 Par Coupon Premium Interest Rate Volatility (%) Over Par 30NCL (bps) (Recommended by STO) (Implied MMD volatility) 47 In conclusion, under current market conditions, using a single volatility of 15% is not unreasonable. The STO may revise this number if there is a sustained and significant change in the interest rate environment. Page 3 Andrew Kalotay Associates, inc., 61 Broadway, New York, NY

Over Par 30NCL (bps) 8 9 15 (Recommended by STO) 25 25 (Implied MMD volatility) 47 In conclusion, under current market conditions,")

5 Illustrative Refunding Analysis According to Massachusetts State Treasury Guidelines Prepared on behalf of: April 19, 2013

6 Market Inputs New issue scale (YTC or YTM) for the Commonwealth of Massachusetts Show coupon by maturity; indicate call provision E.g. 5% for all maturities, NC-10 at par Treasury, SLGS, or Agency rates used in advance refundings Throughout this document: indicates mandatory inclusion with refunding proposals 2

7 Convert Market Scale Into Format for Standard Bond Analytics* Use 15% interest rate volatility to calculate: Optionless (non-call life) par yield curve Spot (pure discount) rates Note: Mass. may change vol. specification from time to time, depending on market conditions *Such as would be used on the Bloomberg OAS1 page, for example 3

8 Scale Conversion Example 15% vol Conversion methodology described in: What Makes the Muni Yield Curve Rise? Journal of Fixed Income (Winter 2009) 4

9 Treasury, SLGS, or Agency NCL Rates Provide at least up to the longest relevant call date 5

10 Current underwriting fee Transaction Costs Affects savings in the contemplated transaction Schedule of fees by maturity Needed to capture costs in future refundings Reduces option value 6

11 Underwriting Fees Example Current fee reduces savings (Show for each bond) Applicable to future refunding opportunities; reduces option value of refunding candidate and of callable replacement bond 7

12 Analytical Results Outstanding bond PV of cash flows (to nominal maturity) Option value (call, advance refunding, total) Replacement bond PV of cash flows (to nominal maturity) Option value (if relevant) 8

Option value (if")

13 Refunding Efficiency Use Generalized Refunding Efficiency Formula = Present only those candidates with efficiency of at least 50% Refunding Efficiency: A Generalized Approach Applied Financial Economic Letters, 2007 Efficiency when the refunding bond is also callable 9

14 Refunding Candidate 10

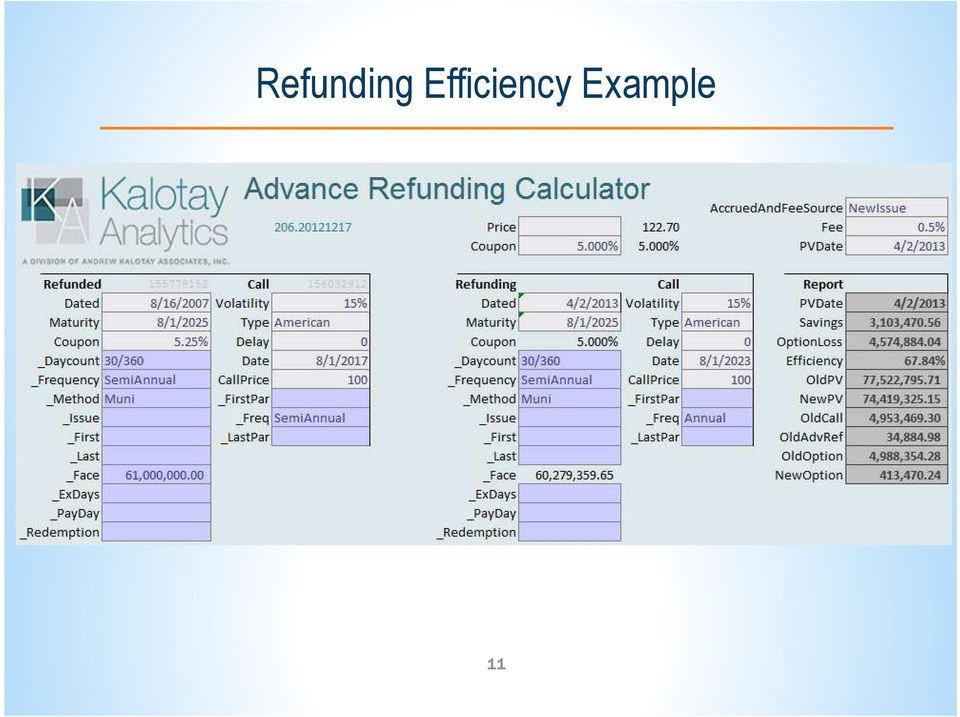

15 Refunding Efficiency Example 11

16 Cash Flow Savings Example Spot rates derived from input scale 12

17 Note That At a 15% interest rate volatility, the implied 30-year NCL rate is 3.696% (Scale Conversion Example) The spot rate for discounting a 2/1/2025 cash flow is 3.074% (Cash Flow Savings Example) According to the Refunding Efficiency Example, PV savings=$3.103mm Option value of the outstanding 5.25% bonds=$4.988mm, ($4.953MM call, $0.035MM advance refunding) Option value of the refunding bond=$0.413mm Net loss of option value=$4.575mm Refunding efficiency=67.85% 13

18 Comments on Analytics Results calculated using Kalotay s iterate and Advance Refunding Calculator However, proposals may utilize any suitable software Discounting and call option valuation should follow standard textbook methodology See Valuation of Municipal Bonds with Embedded Options Handbook of Municipal Securities, 2008, ed. F. Fabozzi Value of the advance refunding option was calculated using Kalotay s proprietary algorithm Reasonable alternatives are acceptable See The Timing of Advance Refunding of Tax-Exempt Municipal Bonds Kalotay and May Municipal Finance Journal (Fall 1998) 14

482 0900 15")

19 Contact Information Andrew Kalotay (212)

20 The Commonwealth of Massachusetts General Obligation Bonds Refunding Analysis Rates as of [add date] Delivery Date 5/1/2013 Costs of Issuance $5.00 Bonds Ranked by: Refunding efficiency, high to low Refunding Efficiency Volatility Assumption 15% Interest Rate Model Black-Karasinski Existing Bond New Bond Negative Arbitrage CUSIP Series Coupon Maturity Par Call Date Call Price Yrs. to Call Yrs. to Maturity Call to Maturity Spread Coupon Current Market Yield Price Maturity Escrow Yield $ Negative Arb % of Par N7G4 Consolidated Loan of 2006, Series D 5.000% 8/1/ ,990,000 8/1/ % 1.260% 0.400% (474,362) -2.97% N7H2 Consolidated Loan of 2006, Series D 4.250% 8/1/2020 6,620,000 8/1/ % 1.520% 0.400% (251,252) -3.80% N7K5 Consolidated Loan of 2006, Series D 4.300% 8/1/2021 2,910,000 8/1/ % 1.760% 0.400% (133,648) -4.59% PFH8 Consolidated Loan of 2007, Series C 5.000% 8/1/ ,000,000 8/1/ % 1.260% 0.620% (903,571) -2.91% PKK1 Consolidated Loan of 2007, Series C 5.250% 8/1/ ,000,000 8/1/ % 1.760% 0.620% (1,754,794) -5.16% PFM7 Consolidated Loan of 2007, Series C 5.250% 8/1/ ,000,000 8/1/ % 1.960% 0.620% (3,200,822) -6.04% PFJ4 Consolidated Loan of 2007, Series C 5.000% 8/1/ ,000,000 8/1/ % 1.520% 0.620% (1,303,942) -4.07% PFN5 Consolidated Loan of 2007, Series C 5.250% 8/1/ ,000,000 8/1/ % 2.150% 0.620% (3,982,602) -6.87%

21 Cumulative Results PV Savings Break-Even Analysis Option Value (% old par) PV Savings Escrow Efficiency $ Savings % of Par Break-Even Rate Increase to Eliminate Savings PV01 Old Bond New Bond Net Loss Refunding Efficiency Refunded Par $ Savings % of Par 70.2% 1,117, % 0.25% 99% 15,990,000 1,117, % 60.0% 376, % 0.26% 98% 22,610,000 1,493, % 57.7% 182, % 0.24% 97% 25,520,000 1,675, % 54.3% 1,074, % 0.22% 96% 56,520,000 2,750, % 56.5% 2,275, % 95% 90,520,000 5,025, % 56.1% 4,086, % 94% 143,520,000 9,111, % 54.4% 1,554, % 93% 175,520,000 10,665, % 55.0% 4,861, % 92% 233,520,000 15,527, %

22 The Commonwealth of Massachusetts General Obligation Bonds Refunding Analysis Mass. G.O. Scale for Refunding Bonds Mass. G.O. Spot Rate Curve Maturity Rate Maturity Rate % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % % %

23 The Commonwealth of Massachusetts General Obligation Bonds Refunding Analysis Summary of Refunding Results Principal Amortization Annual Budgetary Savings (current market rates) (current market rates) Scenario Analysis Current Market Rates 25 bps Decrease 25 bps Increase Maturity Par Fiscal Year Gross Savings Par Amount Refunded $ - $ - $ - 8/1/2013 $ $ - Refunding Par Amount $ - $ - $ - 8/1/ ,000, ,000,000 Average Life 8/1/ ,000, ,500,000 Arbitrage Yield 8/1/ ,000, ,000,000 All-In TIC 8/1/ ,000, ,000,000 Escrow Yield 8/1/ ,000, ,000,000 Gross Savings ($) $ 18,000,000 $ - $ - 8/1/ ,000, ,500,000 PV Savings ($) $ - $ - $ - 8/1/ ,000, ,000 PV Savings (%) 8/1/ ,000, ,750,000 Weighted Average Efficiency 95% 96% 94% 8/1/ ,000, ,000,000 Negative Arbitrage $ - $ - $ - Total $ 134,000,000 Total $ 18,000,000

Cutting-Edge Analytics For Municipal Bonds

Cutting-Edge Analytics For Municipal Bonds Andrew Kalotay, Ph.D. Boston, June 2, 2014 Andrew Kalotay Associates, Inc. Overview of Firm Debt management advisor since 1990 Municipal clients include Massachusetts

Cutting-Edge Analytics For Municipal Bonds Andrew Kalotay, Ph.D. Boston, June 2, 2014 Andrew Kalotay Associates, Inc. Overview of Firm Debt management advisor since 1990 Municipal clients include Massachusetts

Mismanagement of Municipal Debt Puts a Hole in Everybody s Pocket

Mismanagement of Municipal Debt Puts a Hole in Everybody s Pocket August 8, 2012 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com Bird s Eye View of Municipal Finance Significant segment of

Mismanagement of Municipal Debt Puts a Hole in Everybody s Pocket August 8, 2012 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com Bird s Eye View of Municipal Finance Significant segment of

Optimal Tax Management of Municipal Bonds

Optimal Tax Management of Municipal Bonds Andrew Kalotay President, Andrew Kalotay Associates, Inc. 61 Broadway Ste 1400 New York NY 10006 (212) 482 0900 andy@kalotay.com Page 1 Optimal Tax Management

Optimal Tax Management of Municipal Bonds Andrew Kalotay President, Andrew Kalotay Associates, Inc. 61 Broadway Ste 1400 New York NY 10006 (212) 482 0900 andy@kalotay.com Page 1 Optimal Tax Management

Playing the Mortgage Game Like a Professional www.kalotay.com/calculators

Playing the Mortgage Game Like a Professional www.kalotay.com/calculators January 24, 2007 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com The Size of the Mortgage Market Home mortgages $10

Playing the Mortgage Game Like a Professional www.kalotay.com/calculators January 24, 2007 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com The Size of the Mortgage Market Home mortgages $10

2. Determine the appropriate discount rate based on the risk of the security

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

NEW YORK STATE DIVISION OF THE BUDGET DEBT MANAGEMENT POLICIES STATE-SUPPORTED DEBT

NEW YORK STATE DIVISION OF THE BUDGET DEBT MANAGEMENT POLICIES STATE-SUPPORTED DEBT LAST REVISED: October 2012 Introduction: The following provides a summary of the State s Debt Management Policies and

NEW YORK STATE DIVISION OF THE BUDGET DEBT MANAGEMENT POLICIES STATE-SUPPORTED DEBT LAST REVISED: October 2012 Introduction: The following provides a summary of the State s Debt Management Policies and

OR/MS Today - June 2007. Financial O.R. A Pointer on Points

OR/MS Today - June 2007 Financial O.R. A Pointer on Points Given the array of residential mortgage products, should a homebuyer pay upfront points in order to lower the annual percentage rate? Introducing

OR/MS Today - June 2007 Financial O.R. A Pointer on Points Given the array of residential mortgage products, should a homebuyer pay upfront points in order to lower the annual percentage rate? Introducing

Chapter 8. Step 2: Find prices of the bonds today: n i PV FV PMT Result Coupon = 4% 29.5 5? 100 4 84.74 Zero coupon 29.5 5? 100 0 23.

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

The US Municipal Bond Risk Model. Oren Cheyette

The US Municipal Bond Risk Model Oren Cheyette THE US MUNICIPAL BOND RISK MODEL Overview Barra s integrated risk model includes coverage of municipal bonds accounting for marketwide and issuer-specific

The US Municipal Bond Risk Model Oren Cheyette THE US MUNICIPAL BOND RISK MODEL Overview Barra s integrated risk model includes coverage of municipal bonds accounting for marketwide and issuer-specific

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

Tax rules for bond investors

Tax rules for bond investors Understand the treatment of different bonds Paying taxes is an inevitable part of investing for most bondholders, and understanding the tax rules, and procedures can be difficult

Tax rules for bond investors Understand the treatment of different bonds Paying taxes is an inevitable part of investing for most bondholders, and understanding the tax rules, and procedures can be difficult

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

Floating-Rate Securities

Floating-Rate Securities A floating-rate security, or floater, is a debt security whose coupon rate is reset at designated dates and is based on the value of a designated reference rate. - Handbook of

Floating-Rate Securities A floating-rate security, or floater, is a debt security whose coupon rate is reset at designated dates and is based on the value of a designated reference rate. - Handbook of

CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS PROBLEM SETS 1. While it is true that short-term rates are more volatile than long-term rates, the longer duration of the longer-term bonds makes their prices and their

CHAPTER 16: MANAGING BOND PORTFOLIOS PROBLEM SETS 1. While it is true that short-term rates are more volatile than long-term rates, the longer duration of the longer-term bonds makes their prices and their

How To Sell A Callable Bond

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

1.1 Callable bonds A callable bond is a fixed rate bond where the issuer has the right but not the obligation to repay the face value of the security at a pre-agreed value prior to the final original maturity

Modeling and Valuing Mortgage Assets

Modeling and Valuing Mortgage Assets Interest rates have increased since hitting cyclical (and generational) lows over a year ago in June 2003. As interest rates increase, most banks experience a decrease

Modeling and Valuing Mortgage Assets Interest rates have increased since hitting cyclical (and generational) lows over a year ago in June 2003. As interest rates increase, most banks experience a decrease

Virginia State University Policies Manual. Title: Debt Management Guidelines and Procedures Policy: 1500

Purpose a. To provide guidance to Virginia State University in undertaking long-term debt obligations benefiting the University. b. To provide a structured framework for the issuance of long-term debt

Purpose a. To provide guidance to Virginia State University in undertaking long-term debt obligations benefiting the University. b. To provide a structured framework for the issuance of long-term debt

American Options and Callable Bonds

American Options and Callable Bonds American Options Valuing an American Call on a Coupon Bond Valuing a Callable Bond Concepts and Buzzwords Interest Rate Sensitivity of a Callable Bond exercise policy

American Options and Callable Bonds American Options Valuing an American Call on a Coupon Bond Valuing a Callable Bond Concepts and Buzzwords Interest Rate Sensitivity of a Callable Bond exercise policy

Alliance Consulting BOND YIELDS & DURATION ANALYSIS. Bond Yields & Duration Analysis Page 1

BOND YIELDS & DURATION ANALYSIS Bond Yields & Duration Analysis Page 1 COMPUTING BOND YIELDS Sources of returns on bond investments The returns from investment in bonds come from the following: 1. Periodic

BOND YIELDS & DURATION ANALYSIS Bond Yields & Duration Analysis Page 1 COMPUTING BOND YIELDS Sources of returns on bond investments The returns from investment in bonds come from the following: 1. Periodic

LOS 56.a: Explain steps in the bond valuation process.

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

Municipal bonds are widely thought of as

Volume 72 Number 1 216 CFA Institute Tax-Efficient Trading of Municipal Bonds Andrew Kalotay The author proposes a dynamic strategy to optimize the after-tax performance of a municipal bond portfolio.

Volume 72 Number 1 216 CFA Institute Tax-Efficient Trading of Municipal Bonds Andrew Kalotay The author proposes a dynamic strategy to optimize the after-tax performance of a municipal bond portfolio.

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

ANALYSIS OF FIXED INCOME SECURITIES

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

Optimal mortgage refinancing: application of bond valuation tools to household risk management

Applied Financial Economics Letters, 28, 4, 141 149 Optimal mortgage refinancing: application of bond valuation tools to household risk management Andrew J. Kalotay a, Deane Yang b and Frank J. Fabozzi

Applied Financial Economics Letters, 28, 4, 141 149 Optimal mortgage refinancing: application of bond valuation tools to household risk management Andrew J. Kalotay a, Deane Yang b and Frank J. Fabozzi

Introduction to Bond Math Presentation to CDIAC

October 2, 2008 Peter Taylor, Managing Director, Public Finance Department Matthew Koch, Vice President, Public Finance Department Introduction to Bond Math Presentation to CDIAC Agenda Agenda I. What

October 2, 2008 Peter Taylor, Managing Director, Public Finance Department Matthew Koch, Vice President, Public Finance Department Introduction to Bond Math Presentation to CDIAC Agenda Agenda I. What

Asset Valuation Debt Investments: Analysis and Valuation

Asset Valuation Debt Investments: Analysis and Valuation Joel M. Shulman, Ph.D, CFA Study Session # 15 Level I CFA CANDIDATE READINGS: Fixed Income Analysis for the Chartered Financial Analyst Program:

Asset Valuation Debt Investments: Analysis and Valuation Joel M. Shulman, Ph.D, CFA Study Session # 15 Level I CFA CANDIDATE READINGS: Fixed Income Analysis for the Chartered Financial Analyst Program:

Topics in Chapter. Key features of bonds Bond valuation Measuring yield Assessing risk

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

Chapter Review and Self-Test Problems. Answers to Chapter Review and Self-Test Problems

236 PART THREE Valuation of Future Cash Flows Chapter Review and Self-Test Problems 7.1 Bond Values A Microgates Industries bond has a 10 percent coupon rate and a $1,000 face value. Interest is paid semiannually,

236 PART THREE Valuation of Future Cash Flows Chapter Review and Self-Test Problems 7.1 Bond Values A Microgates Industries bond has a 10 percent coupon rate and a $1,000 face value. Interest is paid semiannually,

Debt Management Policy

Debt Management Policy Introduction One of the keys to sound financial management is the development of a debt policy. This need is recognized by bond rating agencies, and development of a debt policy

Debt Management Policy Introduction One of the keys to sound financial management is the development of a debt policy. This need is recognized by bond rating agencies, and development of a debt policy

Understanding duration and convexity of fixed income securities. Vinod Kothari

Understanding duration and convexity of fixed income securities Vinod Kothari Notation y : yield p: price of the bond T: total maturity of the bond t: any given time during T C t : D m : Cashflow from

Understanding duration and convexity of fixed income securities Vinod Kothari Notation y : yield p: price of the bond T: total maturity of the bond t: any given time during T C t : D m : Cashflow from

DEBT MANAGEMENT POLICY

Page 1 of 5 DEBT LIMITS Credit Ratings The school district seeks to maintain the highest possible credit ratings for all categories of short- and long-term debt that can be achieved without compromising

Page 1 of 5 DEBT LIMITS Credit Ratings The school district seeks to maintain the highest possible credit ratings for all categories of short- and long-term debt that can be achieved without compromising

State of Maryland Debt Management and Interest Rate Exchange Agreement Policies

State of Maryland Debt Management and Interest Rate Exchange Agreement Policies 1.0 Objective This Debt Management and Interest Rate Exchange Agreement Policy (Policy), prepared by the Maryland State Treasurer

State of Maryland Debt Management and Interest Rate Exchange Agreement Policies 1.0 Objective This Debt Management and Interest Rate Exchange Agreement Policy (Policy), prepared by the Maryland State Treasurer

Perspectives September

Perspectives September 2013 Quantitative Research Option Modeling for Leveraged Finance Part I Bjorn Flesaker Managing Director and Head of Quantitative Research Prudential Fixed Income Juan Suris Vice

Perspectives September 2013 Quantitative Research Option Modeling for Leveraged Finance Part I Bjorn Flesaker Managing Director and Head of Quantitative Research Prudential Fixed Income Juan Suris Vice

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

University of Kentucky

University of Kentucky Debt Policy Purpose To fulfill its mission, the University of Kentucky must make ongoing strategic capital investments in academic, student life, healthcare, and other plant facilities

University of Kentucky Debt Policy Purpose To fulfill its mission, the University of Kentucky must make ongoing strategic capital investments in academic, student life, healthcare, and other plant facilities

Credit Default Swaps (CDS)

") Introduction to Credit Default Swaps (CDS) CDS Market CDS provide investors with the ability to easily and efficiently short credit Shorting allows positions to be taken in forward credit risk ik CDS allow

Introduction to Credit Default Swaps (CDS) CDS Market CDS provide investors with the ability to easily and efficiently short credit Shorting allows positions to be taken in forward credit risk ik CDS allow

Trading the Yield Curve. Copyright 1999-2006 Investment Analytics

Trading the Yield Curve Copyright 1999-2006 Investment Analytics 1 Trading the Yield Curve Repos Riding the Curve Yield Spread Trades Coupon Rolls Yield Curve Steepeners & Flatteners Butterfly Trading

Trading the Yield Curve Copyright 1999-2006 Investment Analytics 1 Trading the Yield Curve Repos Riding the Curve Yield Spread Trades Coupon Rolls Yield Curve Steepeners & Flatteners Butterfly Trading

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

Combining Tax Exempt, Short-Term Bonds with Taxable GNMA Sale and 4% LIHTCs for Affordable Apartment Financings

SWAC Southwest LIHTC Workshop Dallas, TX September 22, 2015 Combining Tax Exempt, Short-Term Bonds with Taxable GNMA Sale and 4% LIHTCs for Affordable Apartment Financings Kent Neumann, Esq. Partner Eichner

SWAC Southwest LIHTC Workshop Dallas, TX September 22, 2015 Combining Tax Exempt, Short-Term Bonds with Taxable GNMA Sale and 4% LIHTCs for Affordable Apartment Financings Kent Neumann, Esq. Partner Eichner

Administrative Regulations POLICY STATUS: POLICY NUMBER: POLICY ADDRESS:

CATEGORY: POLICY STATUS: Administrative Regulations POLICY TITLE: POLICY NUMBER: POLICY ADDRESS: POLICY PURPOSE: APPLIES TO: SUB-SECTIONS: POLICY STATEMENT Debt Policy In support of its mission, the University

CATEGORY: POLICY STATUS: Administrative Regulations POLICY TITLE: POLICY NUMBER: POLICY ADDRESS: POLICY PURPOSE: APPLIES TO: SUB-SECTIONS: POLICY STATEMENT Debt Policy In support of its mission, the University

Call provision/put provision

Call provision/put provision Call put provision refers to the embedded options offered in some bonds. (see embedded options). They can provide the bond issuer lots of flexibility. As such, the structuring

Call provision/put provision Call put provision refers to the embedded options offered in some bonds. (see embedded options). They can provide the bond issuer lots of flexibility. As such, the structuring

Rising Interest Rates and Municipal Bond Performance

Rising Interest Rates and Municipal Performance September 2013 INTRODUCTION Adam Mackey Managing Director Municipal Fixed Income Fixed income investors are justifiably anxious about recent increases in

Rising Interest Rates and Municipal Performance September 2013 INTRODUCTION Adam Mackey Managing Director Municipal Fixed Income Fixed income investors are justifiably anxious about recent increases in

C(t) (1 + y) 4. t=1. For the 4 year bond considered above, assume that the price today is 900$. The yield to maturity will then be the y that solves

(1 + y) 4. t=1. For the 4 year bond considered above, assume that the price today is 900$. The yield to maturity will then be the y that solves") Economics 7344, Spring 2013 Bent E. Sørensen INTEREST RATE THEORY We will cover fixed income securities. The major categories of long-term fixed income securities are federal government bonds, corporate

Economics 7344, Spring 2013 Bent E. Sørensen INTEREST RATE THEORY We will cover fixed income securities. The major categories of long-term fixed income securities are federal government bonds, corporate

Municipal Swaps: Realities and Misconceptions

Municipal Swaps: Realities and Misconceptions Washington, D.C. December 11, 2012 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com Bird s Eye View of Municipal Finance Significant segment of

Municipal Swaps: Realities and Misconceptions Washington, D.C. December 11, 2012 61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com Bird s Eye View of Municipal Finance Significant segment of

Bond Valuation. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Bond Valuation: An Overview

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Marquette University College of Business Administration Department of Finance

Marquette University College of Business Administration Department of Finance FINA 189 Fixed Income Securities Syllabus Fall 2007 M W 2:25 p.m. 3:40 p.m. 388 Straz Hall Instructor: David S. Krause, PhD

Marquette University College of Business Administration Department of Finance FINA 189 Fixed Income Securities Syllabus Fall 2007 M W 2:25 p.m. 3:40 p.m. 388 Straz Hall Instructor: David S. Krause, PhD

CHAPTER 14: BOND PRICES AND YIELDS

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

CHAPTER 23: FUTURES, SWAPS, AND RISK MANAGEMENT PROBLEM SETS 1. In formulating a hedge position, a stock s beta and a bond s duration are used similarly to determine the expected percentage gain or loss

Relative value analysis: calculating bond spreads Moorad Choudhry January 2006

Relative value analysis: calculating bond spreads Moorad Choudhry January 2006 Relative value analysis: bond spreads Moorad Choudhry Investors measure the perceived market value, or relative value, of

Relative value analysis: calculating bond spreads Moorad Choudhry January 2006 Relative value analysis: bond spreads Moorad Choudhry Investors measure the perceived market value, or relative value, of

FNCE 301, Financial Management H Guy Williams, 2006

REVIEW We ve used the DCF method to find present value. We also know shortcut methods to solve these problems such as perpetuity present value = C/r. These tools allow us to value any cash flow including

REVIEW We ve used the DCF method to find present value. We also know shortcut methods to solve these problems such as perpetuity present value = C/r. These tools allow us to value any cash flow including

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

1.2 Structured notes

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

1.2 Structured notes Structured notes are financial products that appear to be fixed income instruments, but contain embedded options and do not necessarily reflect the risk of the issuing credit. Used

Fixed Income: Practice Problems with Solutions

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION

FLOATING RATE NOTE PRICING SPECIFICATION") MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION This document outlines the use of the margin discounting methodology to price vanilla money market floating rate notes as endorsed

MONEY MARKET SUBCOMMITEE(MMS) FLOATING RATE NOTE PRICING SPECIFICATION This document outlines the use of the margin discounting methodology to price vanilla money market floating rate notes as endorsed

Pricing Methodology Key for ASC 820 Reporting

Institutional Retirement and Trust Methodology Key for ASC 820 Reporting How to use the Methodology Key This Key is sorted by ascending Asset number. Asset /Category information on this Key is minor asset

Institutional Retirement and Trust Methodology Key for ASC 820 Reporting How to use the Methodology Key This Key is sorted by ascending Asset number. Asset /Category information on this Key is minor asset

How To Value Bonds

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Presented by Erin Gore Executive VP, Wells Fargo Bank, N.A. Doug Brown Director, Wells Fargo Securities

Primer on Debt Financing and Treasury Management Presented by Erin Gore Executive VP, Wells Fargo Bank, N.A. Doug Brown Director, Wells Fargo Securities Disclosure This communication is for informational

Primer on Debt Financing and Treasury Management Presented by Erin Gore Executive VP, Wells Fargo Bank, N.A. Doug Brown Director, Wells Fargo Securities Disclosure This communication is for informational

The Term Structure of Interest Rates CHAPTER 13

The Term Structure of Interest Rates CHAPTER 13 Chapter Summary Objective: To explore the pattern of interest rates for different-term assets. The term structure under certainty Forward rates Theories

The Term Structure of Interest Rates CHAPTER 13 Chapter Summary Objective: To explore the pattern of interest rates for different-term assets. The term structure under certainty Forward rates Theories

City of Philadelphia Debt Management Policy December 2009

City of Philadelphia Debt Management Policy December 2009 I. INTRODUCTION While the issuance of debt is often an appropriate method of financing capital projects and major equipment acquisition, it needs

City of Philadelphia Debt Management Policy December 2009 I. INTRODUCTION While the issuance of debt is often an appropriate method of financing capital projects and major equipment acquisition, it needs

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

Convertible Bonds on Bloomberg

Convertible Bonds on Bloomberg News NI DRV Scroll through all the derivatives news. NI BONWATCH Read the latest bond alert news items. TNI EQL Bloomberg's specific news category for equity linked news

Convertible Bonds on Bloomberg News NI DRV Scroll through all the derivatives news. NI BONWATCH Read the latest bond alert news items. TNI EQL Bloomberg's specific news category for equity linked news

Understanding Premium Bonds

Understanding Premium Bonds Many individual investors prefer to purchase individual bonds at prices around par value (100), or even at a discount to par. With interest rates hovering near historic lows,

Understanding Premium Bonds Many individual investors prefer to purchase individual bonds at prices around par value (100), or even at a discount to par. With interest rates hovering near historic lows,

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

LOCKING IN TREASURY RATES WITH TREASURY LOCKS

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

LOCKING IN TREASURY RATES WITH TREASURY LOCKS Interest-rate sensitive financial decisions often involve a waiting period before they can be implemen-ted. This delay exposes institutions to the risk that

Learning Curve September 2005. Understanding the Z-Spread Moorad Choudhry*

Learning Curve September 2005 Understanding the Z-Spread Moorad Choudhry* A key measure of relative value of a corporate bond is its swap spread. This is the basis point spread over the interest-rate swap

Learning Curve September 2005 Understanding the Z-Spread Moorad Choudhry* A key measure of relative value of a corporate bond is its swap spread. This is the basis point spread over the interest-rate swap

Chapter 4 Valuing Bonds

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

Interest Rates and Bond Valuation

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Bond valuation and bond yields

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

Bonds and Yield to Maturity

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Massachusetts Bay Transportation Authority Fiscal and Management Control Board

Massachusetts Bay Transportation Authority 99 Summer Street Suite 1020 Boston, MA 02110 May 2, 2016 Overview of the Engagement PFM has been engaged to undertake four tasks: 1. Analyze Current Outstanding

Massachusetts Bay Transportation Authority 99 Summer Street Suite 1020 Boston, MA 02110 May 2, 2016 Overview of the Engagement PFM has been engaged to undertake four tasks: 1. Analyze Current Outstanding

Chapter 5: Valuing Bonds

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

Weekly Relative Value

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

Tenor Adjustments for a Basis Swap

Tenor Adjustments for a Basis Swap by Chandrakant Maheshwari Praveen Maheshwari Table of Contents 1. Introduction 3 2. Tenor Adjustment Methodology for a Basis Swap 3 3. Why this Tenor Spread so important

Tenor Adjustments for a Basis Swap by Chandrakant Maheshwari Praveen Maheshwari Table of Contents 1. Introduction 3 2. Tenor Adjustment Methodology for a Basis Swap 3 3. Why this Tenor Spread so important

Chapter 11. Bond Pricing - 1. Bond Valuation: Part I. Several Assumptions: To simplify the analysis, we make the following assumptions.

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

Palm Beach County School District

Palm Beach County School District Synthetic Refunding Opportunities July 6, 2005 presented by Public Financial Management 300 South Orange Avenue Suite 1170 Orlando, FL 32801 407 648-2208 Table of Contents

Palm Beach County School District Synthetic Refunding Opportunities July 6, 2005 presented by Public Financial Management 300 South Orange Avenue Suite 1170 Orlando, FL 32801 407 648-2208 Table of Contents

City of Philadelphia Debt Management Policy August 2015

City of Philadelphia Debt Management Policy August 2015 I. INTRODUCTION While the issuance of debt is often an appropriate method of financing capital projects and major equipment acquisition, it needs

City of Philadelphia Debt Management Policy August 2015 I. INTRODUCTION While the issuance of debt is often an appropriate method of financing capital projects and major equipment acquisition, it needs

WEST BASIN MUNICIPAL WATER DISTRICT Debt Management Policy Administrative Code Exhibit G January 2015

1.0 Purpose The purpose of this Debt Management Policy ( Policy ) is to establish parameters and provide guidance as to the issuance, management, continuing evaluation of and reporting on all debt obligations.

1.0 Purpose The purpose of this Debt Management Policy ( Policy ) is to establish parameters and provide guidance as to the issuance, management, continuing evaluation of and reporting on all debt obligations.

Analytical Research Series

EUROPEAN FIXED INCOME RESEARCH Analytical Research Series INTRODUCTION TO ASSET SWAPS Dominic O Kane January 2000 Lehman Brothers International (Europe) Pub Code 403 Summary An asset swap is a synthetic

EUROPEAN FIXED INCOME RESEARCH Analytical Research Series INTRODUCTION TO ASSET SWAPS Dominic O Kane January 2000 Lehman Brothers International (Europe) Pub Code 403 Summary An asset swap is a synthetic

VALUATION OF FIXED INCOME SECURITIES. Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting

VALUATION OF FIXED INCOME SECURITIES Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting OUTLINE Introduction Valuation Principles Day Count Conventions Duration Covexity Exercises

VALUATION OF FIXED INCOME SECURITIES Presented By Sade Odunaiya Partner, Risk Management Alliance Consulting OUTLINE Introduction Valuation Principles Day Count Conventions Duration Covexity Exercises

FIXED INCOME SECURITY VALUATION FINANCE 6545. Warrington College of Business University of Florida

FIXED INCOME SECURITY VALUATION FINANCE 6545 Warrington College of Business University of Florida David T. Brown William R. Hough Professor of Finance 392-2820 david.brown@warrington.ufl.edu Class: Monday

FIXED INCOME SECURITY VALUATION FINANCE 6545 Warrington College of Business University of Florida David T. Brown William R. Hough Professor of Finance 392-2820 david.brown@warrington.ufl.edu Class: Monday

Section I. Introduction

Section I. Introduction Purpose and Overview In its publication entitled Best Practice Debt Management Policy, the Government Finance Officers Association (GFOA) states that Debt management policies are

Section I. Introduction Purpose and Overview In its publication entitled Best Practice Debt Management Policy, the Government Finance Officers Association (GFOA) states that Debt management policies are

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

Goals. Bonds: Fixed Income Securities. Two Parts. Bond Returns

Goals Bonds: Fixed Income Securities History Features and structure Bond ratings Economics 71a: Spring 2007 Mayo chapter 12 Lecture notes 4.3 Bond Returns Two Parts Interest and capital gains Stock comparison:

Goals Bonds: Fixed Income Securities History Features and structure Bond ratings Economics 71a: Spring 2007 Mayo chapter 12 Lecture notes 4.3 Bond Returns Two Parts Interest and capital gains Stock comparison:

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

Learning Curve An introduction to the use of the Bloomberg system in swaps analysis Received: 1st July, 2002 Aaron Nematnejad works in the fixed income analytics team at Bloomberg L.P. in London. He graduated

Calling the Calls on Municipal Bonds And How To Use Calls To Seek Higher Yields

Calling the Calls on Municipal Bonds And How To Use Calls To Seek Higher Yields Investors can get hurt by bond calls, particularly when they buy premium bonds without knowing all the calls in advance.

Calling the Calls on Municipal Bonds And How To Use Calls To Seek Higher Yields Investors can get hurt by bond calls, particularly when they buy premium bonds without knowing all the calls in advance.

Bond Valuation. What is a bond?

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond

Fixed Income Quantitative Credit Research February 27, 2006 Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond Claus M. Pedersen Explaining the Lehman Brothers Option Adjusted Spread

Fixed Income Quantitative Credit Research February 27, 2006 Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond Claus M. Pedersen Explaining the Lehman Brothers Option Adjusted Spread

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

LIFE INSURANCE AND WEALTH MANAGEMENT PRACTICE COMMITTEE AND GENERAL INSURANCE PRACTICE COMMITTEE Information Note: Discount Rates for APRA Capital Standards Contents 1. Status of Information Note 3 2.

Debt Policy Certification Program

Washington Municipal Treasurers Association Debt Policy Certification Program Sample Debt Policy [ISSUER NAME] [EMBLEM OF ISSUER] DEBT POLICY (SAMPLE) ADOPTED [DATE] (DRAFT 7/28/2003) TABLE OF CONTENTS

Washington Municipal Treasurers Association Debt Policy Certification Program Sample Debt Policy [ISSUER NAME] [EMBLEM OF ISSUER] DEBT POLICY (SAMPLE) ADOPTED [DATE] (DRAFT 7/28/2003) TABLE OF CONTENTS

Debt Management Policies & Guidelines

Debt Management Policies & Guidelines January, 2004 PREPARED BY: ANDREW E. MEISNER, COUNTY TREASURER PATRICK M. DOHANY, COUNTY TREASURER I. COUNTY'S DEBT POLICY A. Purpose The County recognizes the foundation

Debt Management Policies & Guidelines January, 2004 PREPARED BY: ANDREW E. MEISNER, COUNTY TREASURER PATRICK M. DOHANY, COUNTY TREASURER I. COUNTY'S DEBT POLICY A. Purpose The County recognizes the foundation

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

US TREASURY SECURITIES - Issued by the U.S. Treasury Department and guaranteed by the full faith and credit of the United States Government.

Member NASD/SIPC Bond Basics TYPES OF ISSUERS There are essentially five entities that issue bonds: US TREASURY SECURITIES - Issued by the U.S. Treasury Department and guaranteed by the full faith and

Member NASD/SIPC Bond Basics TYPES OF ISSUERS There are essentially five entities that issue bonds: US TREASURY SECURITIES - Issued by the U.S. Treasury Department and guaranteed by the full faith and

issue brief Duration Basics January 2007 Duration is a term used by fixed-income investors, California Debt and Investment Advisory Commission

issue brief California Debt and Investment Advisory Commission # 06-10 January 2007 Duration Basics Introduction Duration is a term used by fixed-income investors, financial advisors, and investment advisors.

issue brief California Debt and Investment Advisory Commission # 06-10 January 2007 Duration Basics Introduction Duration is a term used by fixed-income investors, financial advisors, and investment advisors.

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates Cash Flow Financial transactions and investment opportunities are described by cash flows they generate. Cash flow: payment

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates Cash Flow Financial transactions and investment opportunities are described by cash flows they generate. Cash flow: payment

Impact of rising interest rates on preferred securities

Impact of rising interest rates on preferred securities This report looks at the risks preferred investors may face in a rising-interest-rate environment. We are currently in a period of historically low

Impact of rising interest rates on preferred securities This report looks at the risks preferred investors may face in a rising-interest-rate environment. We are currently in a period of historically low

Finance Homework Julian Vu May 28, 2008

Finance Homework Julian Vu May 28, 2008 Assignment: p. 28-29 Problems 1-1 and 1-2 p. 145-147 Questions 4-2, 4-3, and 4-4, and Problems 4-1, 4-2, 4-3, and 4-13 P1-1 A Treasury Bond that matures in 10 years

Finance Homework Julian Vu May 28, 2008 Assignment: p. 28-29 Problems 1-1 and 1-2 p. 145-147 Questions 4-2, 4-3, and 4-4, and Problems 4-1, 4-2, 4-3, and 4-13 P1-1 A Treasury Bond that matures in 10 years

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What