An Introduction to Indian Financial System Provisions of Important Acts in Relation to Regulation and Supervision.

|

|

|

- Arline Fitzgerald

- 7 years ago

- Views:

Transcription

1 An Introduction to Indian Financial System Provisions of Important Acts in Relation to Regulation and Supervision October 08, 2012

2 An Introduction to Indian Financial System The financial system plays an important role in promoting economic growth not only by channeling savings into investments but also by improving allocative efficiency of resources. The recent empirical evidence, in fact, suggests that financial system contributes to economic growth more by improving the allocative efficiency of resources than by channeling of resources from savers to investors. An efficient financial system is now regarded as a necessary pre-condition for growth.

3 An Introduction to Indian Financial System. This shift in the emphasis along with opening up of domestic economies to international competition has encouraged emerging market economies (EMEs) to introduce financial sector reforms. In the wake of the financial crises of the 1990s however, the role of the financial system in growth has been subjected to a critical reassessment. Increased financial integration has exposed the countries to the risk of contagion. It is now widely recognised that stability of the financial system is critical for a sustainable growth.

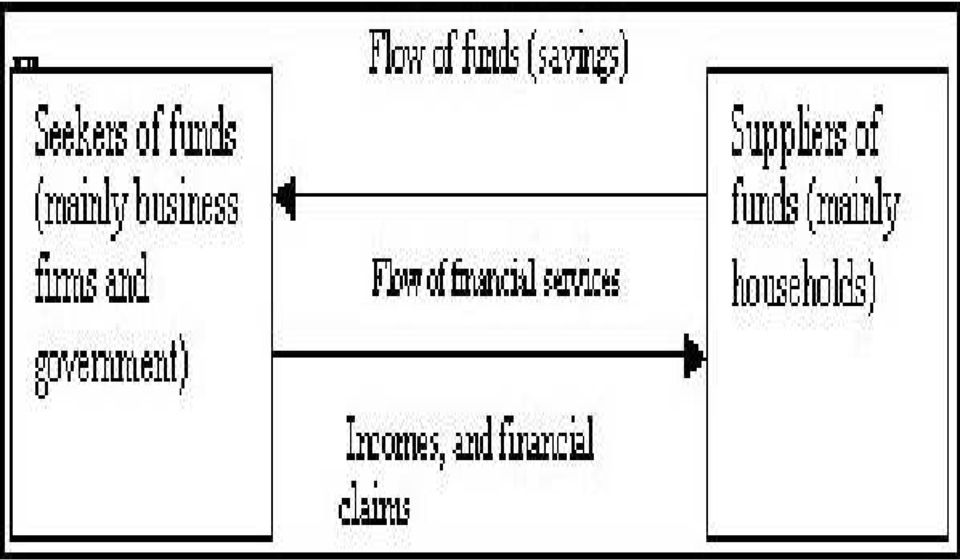

4 Financial System There are areas or people with surplus funds and there are those with a deficit. A financial system or financial sector functions as an intermediary and facilitates the flow of funds fromtheareasofsurplustotheareasofdeficit A Financial System is a composition of various institutions, markets, regulations and laws, practices, money manager, analysts, transactions and claims and liabilities

5

6 Financial System An institutional framework existing in a country to enable financial transactions Three main parts Financial assets (loans, deposits, bonds, equities, etc.) Financial institutions (banks, mutual funds, insurance companies, etc.) Financial markets (money market, capital market, forex market, etc.) Regulation is another aspect of the financial system (RBI, SEBI, IRDA, FMC) Payment and Settlement System Plays a crucial role in it.

Financial markets (money market, capital market, forex market, etc.")

7 Constituents of a Financial System

8 Financial assets/instruments There are instruments for savers such as deposits, equities, mutual fund units, etc. There are instruments for borrowers such as loans, overdrafts, etc. Like businesses, governments too raise funds through issuing of bonds, Treasury bills, etc. Instruments like PPF, KVP, etc. are available to savers who wish to lend money to the government

9 FINANCIAL MARKETS A Financial Market can be defined as the market in which financial assets are created or transferred. As against a real transaction that involves exchange of money for real goods or services, a financial transaction involves creation or transfer of a financial asset. Financial Assets or Financial Instruments represents a claimtothe paymentof a sum of money sometime in the future and /or periodic payment in the form of interest or dividend

10 Money Market Money market refers to the market for short term assets that are close substitutes of money. It is a wholesale debt market for low-risk, highly-liquid, shortterm instrument. Funds are available in this market for periods ranging from a single day up to a year. This market is dominated mostly by government, banks and financial institutions.

11 Organised Money Market Call money market Bill Market Treasury bills Commercial bills Bank loans (short-term) Organised money market comprises RBI, banks (commercial and co-operative)

12 Call Money Market InCallMoneyMarket,daytodayimbalancesinthefunds position of scheduled commercial banks are eased out. The call /notice money market has graduated into a broad and vibrant institution. Call/Notice money is the money borrowed or lent on demand for a very short period. When money is borrowed or lent for a day, it is known as Call (Overnight) Money. Intervening holidays and/or Sunday are excluded for this purpose.

Money.")

13 Call/Notice Money Market If money is borrowed or lent for more than a day and up to 14 days, it is "Notice Money". No collateral security is required to cover these transactions. The entry into this field is restricted by RBI. Commercial Banks, Co-operative Banks and Primary Dealers are allowed to borrow and lend in this market.

14 Money Market Instruments Certificates of Deposit Commercial Paper Inter-bank participation certificates Inter-bank term money Treasury Bills Bill rediscounting Call/notice/term money CBLO Market Repo

15 Treasury Bills Treasury Bills are short term (up to one year) borrowing instruments of the union government. It is an IOU of the Government. It is a promise by the Government to pay a stated sum after expiry of the stated period from the date of issue (14/91/182/364 days i.e. less than one year). They are issued at a discount to the face value, and on maturity the face value is paid to the holder. The rate of discount and the corresponding issue price are determined at each auction.

.")

16 Certificates of Deposit Certificates of Deposit (CDs) are negotiable term deposit certificates issued by a commercial banks/financial Institutions at discount to face value at market rates, with maturity ranging from15daystooneyear. Being securities in the form of promissory notes, transfer of title is easy, by endorsement and delivery. Further, they are governed by the Negotiable Instruments Act. As these certificates are the liabilities of commercial banks/financial institutions, they make sound investments.

17 Commercial Papers CPs enable highly rated corporate borrowers to diversify their sources of short-term borrowings and raise a part of their requirement at competitive rates from the market. Commercial Papers are unsecured debts of corporate. They are issued in the form of promissory notes, redeemable at par to the holder at maturity. Only corporate who get an investment grade rating can issue CPs, as per RBI rules.

18 Forex Market The Forex market deals with the multi-currency requirements, which are met by the exchange of currencies. Depending on the exchange rate that is applicable, the transfer of funds takes place in this market. This is one of the most developed and integrated market across the globe.

19 Credit Market Credit market is a place where banks, FIs and NBFCs purvey short, medium and long-term loans to corporate and individuals.

20 Indian Banking System Central Bank (Reserve Bank of India) Commercial banks Co-operative banks Banks can be classified as: Scheduled (Second Schedule of RBI Act, 1934) Non-Scheduled Scheduled banks can be classified as: Public Sector Banks Private Sector Banks (Old and New) Foreign Banks Regional Rural Banks Co-operative banks

Foreign Banks Regional Rural Banks")

21 Indian Banking System -Overview Indian Banking System Scheduled Banks Non-Scheduled Banks Scheduled Commercial Banks Scheduled Cooperative Banks Non-Scheduled Commercial Banks Non-Scheduled Cooperative Banks Regional Rural Banks Urban Cooperative Banks Local Area Banks (4) Urban Cooperative Banks State Cooperative Banks Rural Cooperative Banks 21

22 Capital Market The capital market is designed to finance the long-term investments. The transactions taking place in this market will be for periods over a year.

23 The Indian Capital Market Development Financial Institutions Industrial Finance Corporation of India (IFCI) State Finance Corporations (SFCs) Industrial Development Finance Corporation (IDFC) Financial Intermediaries Merchant Banks Mutual Funds Leasing Companies Venture Capital Companies

24 Securities Market Refers to the market for shares and debentures of old and new companies New Issues Market-also known as the primary market-refers to raising of new capital in the form of shares and debentures Stock Market-also known as the secondary market. Deals with securities already issued by companies

25 Financial Intermediaries Mutual Funds-Promote savings and mobilise funds which are invested in the stock market and bond market Indirect source of finance to companies Pool funds of savers and invest in the stock market/bond market Their instruments at saver s end are called units Offer many types of schemes: growth fund, income fund, balanced fund Regulated by SEBI

26 Financial Intermediaries. Merchant banking-manage and underwrite new issues, undertake syndication of credit, advise corporate clients on fund raising Subject to regulation by SEBI and RBI SEBI regulates them on issue activity and portfolio management of their business. RBI supervises those merchant banks which are subsidiaries or affiliates of commercial banks Have to adopt stipulated capital adequacy norms and abide by a code of conduct

27 Regulation and Supervision The regulatory framework in India has always been alive to the need for ensuring financial stability on an ongoing basis while fostering growth supporting financial market developments. One of the key factors that helped India to counter the impact of the crisis was the counter-cyclical regulatory environment and micro and macro prudential measures.

28 Developments in India Basel enhancements adopted Liquidity requirements through SLR Countercyclical prudential measures through risk weights and provisioning Guidelines on compensation New regulatory framework for financial conglomerates

29 Umbrella Acts: Legal Frame Work for RBI Reserve Bank of India Act, 1934: governs the Reserve Bank functions Banking Regulation Act, 1949: governs the financial sector Acts governing specific functions : Government Securities Act 2006: Governs government debt market Indian Coinage Act, 1906:Governs currency and coins Foreign Exchange Regulation Act, 1973/Foreign Exchange Management Act, 1999: Governs trade and foreign exchange market "Payment and Settlement Systems Act, 2007: Provides for regulation and supervision of payment systems in India"

30 Section 22 of BR Act- Licensing of banking companies (1) No company shall carry on banking business in India unless it holds a license issued in that behalf by the Reserve Bank (3) Before granting any license under this section, the Reserve Bank may require to be satisfied by an inspection of the books of the company that the following conditions are fulfilled, namely:-

31 Section 22 of BR Act- Licensing of banking companies.. (a) that the company is or will be in a position to pay its present or future depositors in full as their claims accrue; (b) that the affairs of the company are not being, or are not likely to be, conducted in a manner detrimental to the interests of its present or future depositors;

32 Section 22 of BR Act- Licensing of banking companies.. (c) that the general character of the proposed management of the company will not be prejudicial to the public interest of its present or future depositors; (d) that the company has adequate capital structure and earning prospects; (e) that the public interest will be served by the grant of a license to the company to carry on banking business in India;

33 Section 23 of BR Act- Restrictions on opening of new, and transfer of existing, places of business (1) Without obtaining the prior permissions of the Reserve Bank- (a) no banking company shall open a new place of business in India or change otherwise than within the same city, town or village, the location of an existing place of business situated in India; and

34 Section 23 of BR Act- Restrictions on opening of new, and transfer of existing, places of business (b) no banking company incorporated in India shall open a new place of business outside India or change, otherwise than within the same city, town or village in any country or area outside India, the location of an existing place of business situated in that country or area:

35 Section 35 of BR Act Inspection (1) Reserve Bank at any time may, and on being directed so to do by the Central Government shall, cause an inspection to be made by one or more of its officers of any banking company and its books and accounts; and the Reserve Bank shall supply to the banking company a copy of its report on such inspection.

36 35A. Power of the Reserve Bank to give directions (1) Where the Reserve Bank is satisfied that- (a) in the public interest; or (aa) in the interest of banking policy; or (b) to prevent the affairs of any banking company being conducted in a manner detrimental to the interests of the depositor or in a manner prejudicial to the interests of the banking company; or

37 Section 36of BR Act Further powers and functions of Reserve Bank (1) The Reserve Bank may: (a) caution or prohibit banking companies generally or any banking company in particular against entering into any particular transaction or class of transactions, and generally give advice to any banking company; (b) on a request by the companies concerned and subject to the provisions of section 44A, assist, as intermediary or otherwise, in proposals for the amalgamation of such banking companies;

38 Section 45Q of BR Act - Power to inspect (1) The Reserve Bank shall, on being directed so to do by the Central Government or by the High Court, cause an inspection to be made by one or more of its officers of a banking company which is being wound up and its books and accounts. (2) On such inspection, the Reserve Bank shall submit its report to the Central Government and the High Court.

39 Section 45N of RBI Act- Inspection 1[(1) The Bank may, at any time, cause an inspection to be made by one or more of its officers or employees or other persons (hereafter in this section referred to as the inspecting authority)- (i) of any non-banking institution, including a financial institution, for the purpose of verifying the correctness or completeness of any statement, information or particulars furnished to the Bank or for the purpose of obtaining any information or particulars which the non-banking institution has failed to furnish on being called upon to do so; or

40 Acts governing Banking Operations of RBI Companies Act, 1956:Governs banks as companies Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970/1980: Relates to nationalisation of banks Bankers' Books Evidence Act Banking Secrecy Act Negotiable Instruments Act, 1881

41 SARFAESI Act Enables setting up of Asset Management Companies to acquire NPAs of any bank or FI (SASF, ARCIL are examples) NPAs are acquired by issuing debentures, bonds or any other security As a second creditor can serve notice to the defaulting borrower to discharge his/her liabilities in 60 days Failing which the company can take possession of assets, takeover the management of assets and appoint any person to manage the secured assets Borrowers have the right to appeal to the Debts Tribunal after depositing 75% of the amount claimed by the second creditor

42 Acts governing Individual Institutions State Bank of India Act, 1954 regulated by RBI The Industrial Development Bank (Transfer of Undertaking and Repeal) Act, 2003 The Industrial Finance Corporation (Transfer of Undertaking and Repeal) Act, 1993 National Bank for Agriculture and Rural Development Act National Housing Bank Act Deposit Insurance and Credit Guarantee Corporation Act, etc.

43 SEBI Related Acts Securities and Exchange Board of India Act, 1992 Securities Contracts (Regulation) Amendment Act, 2007 The Depositories Act, 1996 The Securities Contract (Regulations) Act 1956

CERTIFICATE COURSE ON FINANCIAL MARKETS AND SECURITIES LAWS. MODULE 1: Introduction to Financial Market & Money Market

CERTIFICATE COURSE ON FINANCIAL MARKETS AND SECURITIES LAWS MODULE 1: Introduction to Financial Market & Money Market Introduction to Financial Market Financial Market Structure o Money Market o Debt Market

CERTIFICATE COURSE ON FINANCIAL MARKETS AND SECURITIES LAWS MODULE 1: Introduction to Financial Market & Money Market Introduction to Financial Market Financial Market Structure o Money Market o Debt Market

International Journal of Recent Scientific Research

ISSN: 0976-3031 International Journal of Recent Scientific Impact factor: 5.114 INDIAN FINANCIAL SYSTEM Shilpa Goyal Volume: 6 Issue: 9 THE PUBLICATION OF INTERNATIONAL JOURNAL OF RECENT SCIENTIFIC RESEARCH

ISSN: 0976-3031 International Journal of Recent Scientific Impact factor: 5.114 INDIAN FINANCIAL SYSTEM Shilpa Goyal Volume: 6 Issue: 9 THE PUBLICATION OF INTERNATIONAL JOURNAL OF RECENT SCIENTIFIC RESEARCH

Introduction to Government Bond, Corporate Bond and Money Markets

Introduction to Government Bond, Corporate Bond and Money Markets Fixed income market in India can be categorized into five segments, Money Market, Government Bond Market, Corporate Bond Market, Interest

Introduction to Government Bond, Corporate Bond and Money Markets Fixed income market in India can be categorized into five segments, Money Market, Government Bond Market, Corporate Bond Market, Interest

Web. Chapter FINANCIAL INSTITUTIONS AND MARKETS

FINANCIAL INSTITUTIONS AND MARKETS T Chapter Summary Chapter Web he Web Chapter provides an overview of the various financial institutions and markets that serve managers of firms and investors who invest

FINANCIAL INSTITUTIONS AND MARKETS T Chapter Summary Chapter Web he Web Chapter provides an overview of the various financial institutions and markets that serve managers of firms and investors who invest

Chapter 1 THE MONEY MARKET

Page 1 The information in this chapter was last updated in 1993. Since the money market evolves very rapidly, recent developments may have superseded some of the content of this chapter. Chapter 1 THE

Page 1 The information in this chapter was last updated in 1993. Since the money market evolves very rapidly, recent developments may have superseded some of the content of this chapter. Chapter 1 THE

BANKING QUESTION AND ANSWERS- PART-1

BANKING QUESTION AND ANSWERS- PART-1 1. Which of the following statements is true? (1) Banks cannot accept demand and time deposits from public (2) Banks can accept only demand deposits from public (3)

BANKING QUESTION AND ANSWERS- PART-1 1. Which of the following statements is true? (1) Banks cannot accept demand and time deposits from public (2) Banks can accept only demand deposits from public (3)

Principles of Banking Module A

Principles of Banking Module A V. Rajendran Venkrajen.in venkrajen@yahoo.com Indian Financial System Financial Market consists of Money market, debt market, forex market, capital market Debt market ->

Principles of Banking Module A V. Rajendran Venkrajen.in venkrajen@yahoo.com Indian Financial System Financial Market consists of Money market, debt market, forex market, capital market Debt market ->

Money Market Operations

CHAPTER 10 Money Market Operations BASIC CONCEPTS 1. Introduction The financial system of any country is a conglomeration of sub-markets, viz money, capital and foreign exchange market. The presence of

CHAPTER 10 Money Market Operations BASIC CONCEPTS 1. Introduction The financial system of any country is a conglomeration of sub-markets, viz money, capital and foreign exchange market. The presence of

Importance of Credit Rating

Importance of Credit Rating A credit rating estimates ability to repay debt. A credit rating is a formal assessment of a corporation, autonomous governments, individuals, conglomerates or even a country.

Importance of Credit Rating A credit rating estimates ability to repay debt. A credit rating is a formal assessment of a corporation, autonomous governments, individuals, conglomerates or even a country.

Merchant Banking & Financial Services MCQ

Merchant Banking & Financial Services MCQ 1. A merchant bank is a financial institution conducting money market activities and: a. Lending b. Underwriting and financial advice c. Investment service 2.

Merchant Banking & Financial Services MCQ 1. A merchant bank is a financial institution conducting money market activities and: a. Lending b. Underwriting and financial advice c. Investment service 2.

Financial Market Instruments

appendix to chapter 2 Financial Market Instruments Here we examine the securities (instruments) traded in financial markets. We first focus on the instruments traded in the money market and then turn to

appendix to chapter 2 Financial Market Instruments Here we examine the securities (instruments) traded in financial markets. We first focus on the instruments traded in the money market and then turn to

Centrale Bank van Curaçao en Sint Maarten. Manual Coordinated Portfolio Investment Survey CPIS. Prepared by: Project group CPIS

Centrale Bank van Curaçao en Sint Maarten Manual Coordinated Portfolio Investment Survey CPIS Prepared by: Project group CPIS Augustus 1, 2015 Contents Introduction 3 General reporting and instruction

Centrale Bank van Curaçao en Sint Maarten Manual Coordinated Portfolio Investment Survey CPIS Prepared by: Project group CPIS Augustus 1, 2015 Contents Introduction 3 General reporting and instruction

Debt securities statistics: the Bank of Thailand s experience 1

Debt securities statistics: the Bank of Thailand s experience 1 Pusadee Ganjarerndee 2 Significant role of debt securities on the Thai economy Prior to the 1997 financial crisis, most capital mobilization

Debt securities statistics: the Bank of Thailand s experience 1 Pusadee Ganjarerndee 2 Significant role of debt securities on the Thai economy Prior to the 1997 financial crisis, most capital mobilization

I. Introduction. II. Financial Markets (Direct Finance) A. How the Financial Market Works. B. The Debt Market (Bond Market)

A. How the Financial Market Works. B. The Debt Market (Bond Market)") University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

Financial Instruments. Chapter 2

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

Financial Instruments Chapter 2 Major Types of Securities debt money market instruments bonds common stock preferred stock derivative securities 1-2 Markets and Instruments Money Market debt instruments

READING 1. The Money Market. Timothy Q. Cook and Robert K. LaRoche

READING 1 The Money Market Timothy Q. Cook and Robert K. LaRoche The major purpose of financial markets is to transfer funds from lenders to borrowers. Financial market participants commonly distinguish

READING 1 The Money Market Timothy Q. Cook and Robert K. LaRoche The major purpose of financial markets is to transfer funds from lenders to borrowers. Financial market participants commonly distinguish

GUIDELINES FOR PRIMARY DEALERSHIP IN MONEY MARKET INSTRUMENTS

MM 0005 (December 2005) CENTRAL BANK OF THE GAMBIA GUIDELINES FOR PRIMARY DEALERSHIP IN MONEY MARKET INSTRUMENTS NOVEMBER 2005 Page 1 of 21 TABLE OF CONTENTS (1.0) Introduction------------------------------------------------------------------------Page

MM 0005 (December 2005) CENTRAL BANK OF THE GAMBIA GUIDELINES FOR PRIMARY DEALERSHIP IN MONEY MARKET INSTRUMENTS NOVEMBER 2005 Page 1 of 21 TABLE OF CONTENTS (1.0) Introduction------------------------------------------------------------------------Page

ADVANCED RELEASE CALENDER

ADVANCED RELEASE CALENDER Data-Series Real Sector Price/ Indices Frequency Due updating on DBIE Wholesale price index (WPI) Monthly On every 14th of the Month, data released with a lag of 14 days. Consumer

ADVANCED RELEASE CALENDER Data-Series Real Sector Price/ Indices Frequency Due updating on DBIE Wholesale price index (WPI) Monthly On every 14th of the Month, data released with a lag of 14 days. Consumer

ROLE OF S.E.B.I. AS A REGULATORY AUTHORITY

ROLE OF S.E.B.I. AS A REGULATORY AUTHORITY Dr. V. Neelaveni Academic consultant, School of Commerce & Management, Dravidian University, Kuppam, Andhra Pradesh, India E-mail: veni2mba@yahoo.co.in ABSTRACT

ROLE OF S.E.B.I. AS A REGULATORY AUTHORITY Dr. V. Neelaveni Academic consultant, School of Commerce & Management, Dravidian University, Kuppam, Andhra Pradesh, India E-mail: veni2mba@yahoo.co.in ABSTRACT

AGREEMENT. between the Ministry of Finance and Central Bank Iceland on Treasury debt management

AGREEMENT between the Ministry of Finance and Central Bank Iceland on Treasury debt management 1. Foundation of the Agreement Pursuant to Article 1 of the Act on the Government Debt Management, no. 43/1990,

AGREEMENT between the Ministry of Finance and Central Bank Iceland on Treasury debt management 1. Foundation of the Agreement Pursuant to Article 1 of the Act on the Government Debt Management, no. 43/1990,

Saving and Investing. Chapter 11 Section Main Menu

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

Saving and Investing How does investing contribute to the free enterprise system? How does the financial system bring together savers and borrowers? How do financial intermediaries link savers and borrowers?

RBI/2007-2008/165 DBOD. No. BP. BC. 38 / 21.04.098/ 2007-08 October 24, 2007. Guidelines on Asset-Liability Management (ALM) System amendments

System amendments") RBI/2007-2008/165 DBOD. No. BP. BC. 38 / 21.04.098/ 2007-08 October 24, 2007 Chairmen / Chief Executive Officers All Commercial Banks (excluding RRBs) Guidelines on Asset-Liability Management (ALM) System

RBI/2007-2008/165 DBOD. No. BP. BC. 38 / 21.04.098/ 2007-08 October 24, 2007 Chairmen / Chief Executive Officers All Commercial Banks (excluding RRBs) Guidelines on Asset-Liability Management (ALM) System

3 SELECTED FINANCIAL ASSETS AND LIABILITIES OF THE NSW PUBLIC SECTOR

34 3 SELECTED FINANCIAL ASSETS AND LIABILITIES OF THE NSW PUBLIC SECTOR 3.1 INTRODUCTION In May 1991, Premiers' Conference endorsed the recommendations contained in the Report on Uniform Presentation of

34 3 SELECTED FINANCIAL ASSETS AND LIABILITIES OF THE NSW PUBLIC SECTOR 3.1 INTRODUCTION In May 1991, Premiers' Conference endorsed the recommendations contained in the Report on Uniform Presentation of

Contents. Chapter 1 Introduction to Financial Services 3

Contents Preface V PART 1: Introduction Chapter 1 Introduction to Financial Services 3 1.1 Finance and Business 3 1.2 Financial Services 4 1.3 Characteristics of Financial Services 4 1.4 Distinctiveness

Contents Preface V PART 1: Introduction Chapter 1 Introduction to Financial Services 3 1.1 Finance and Business 3 1.2 Financial Services 4 1.3 Characteristics of Financial Services 4 1.4 Distinctiveness

Development of Money Markets

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

CITIZENS PROPERTY INSURANCE CORPORATION. INVESTMENT POLICY for. Liquidity Fund (Taxable)

") CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Liquidity Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

CITIZENS PROPERTY INSURANCE CORPORATION INVESTMENT POLICY for Liquidity Fund (Taxable) INTRODUCTION Citizens is a government entity whose purpose is to provide property and casualty insurance for those

Money Market. The money market is the market for low-risk, short-term debt.

Money Market The money market is the market for low-risk, short-term debt. 1 Substitution Different money-market assets are close substitutes. Since an investor in the money market can choose which asset

Money Market The money market is the market for low-risk, short-term debt. 1 Substitution Different money-market assets are close substitutes. Since an investor in the money market can choose which asset

MEMORANDUM OF ASSOCIATION

THE COMPANIES ACTS, 1963 TO 2006 A PUBLIC COMPANY LIMITED BY SHARES AN UMBRELLA TYPE INVESTMENT COMPANY WITH VARIABLE CAPITAL AND HAVING SEGREGATED LIABILITY BETWEEN SUB-FUNDS NATIXIS INTERNATIONAL FUNDS

THE COMPANIES ACTS, 1963 TO 2006 A PUBLIC COMPANY LIMITED BY SHARES AN UMBRELLA TYPE INVESTMENT COMPANY WITH VARIABLE CAPITAL AND HAVING SEGREGATED LIABILITY BETWEEN SUB-FUNDS NATIXIS INTERNATIONAL FUNDS

Q. What is the Debt Market? A. Q. What are securities? A. Q. What are fixed income securities? A.

Q. What is the Debt Market? A. The Debt Market is the market where fixed income securities of various types and features are issued and traded. Debt Markets are therefore, markets for fixed income securities

Q. What is the Debt Market? A. The Debt Market is the market where fixed income securities of various types and features are issued and traded. Debt Markets are therefore, markets for fixed income securities

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS. Peter N. Ireland Department of Economics Boston College. irelandp@bc.edu

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College irelandp@bc.edu http://www2.bc.edu/~irelandp/ec261.html Chapter 2: An Overview of the Financial

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College irelandp@bc.edu http://www2.bc.edu/~irelandp/ec261.html Chapter 2: An Overview of the Financial

Classification and Presentation of Data on Claims and Liabilities

CNB BULLETIN NOTES ON METHODOLOGY 1 Classification and Presentation of Data on Claims and Liabilities The Croatian National Bank has begun to implement the ESA 2010 standard in its statistics, which also

CNB BULLETIN NOTES ON METHODOLOGY 1 Classification and Presentation of Data on Claims and Liabilities The Croatian National Bank has begun to implement the ESA 2010 standard in its statistics, which also

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

FREQUENTLY ASKED QUESTIONS (FAQs) SEBI (INVESTMENT ADVISERS) REGULATIONS, 2013

SEBI (INVESTMENT ADVISERS) REGULATIONS, 2013") FREQUENTLY ASKED QUESTIONS (FAQs) SEBI (INVESTMENT ADVISERS) REGULATIONS, 2013 Disclaimer: These FAQs are prepared with a view to guide market participants on SEBI (Investment Advisers) Regulations, 2013

FREQUENTLY ASKED QUESTIONS (FAQs) SEBI (INVESTMENT ADVISERS) REGULATIONS, 2013 Disclaimer: These FAQs are prepared with a view to guide market participants on SEBI (Investment Advisers) Regulations, 2013

INDIAN FINANCIAL SYSTEM

INDIAN FINANCIAL SYSTEM A. K. Bhatia BLACK PRINTS N E W D E L H I Contents Preface 1. Towards Globalisation of India's Financial Sector Systemic Issues: Opportunities and Risks - Depth of the Indian Financial

INDIAN FINANCIAL SYSTEM A. K. Bhatia BLACK PRINTS N E W D E L H I Contents Preface 1. Towards Globalisation of India's Financial Sector Systemic Issues: Opportunities and Risks - Depth of the Indian Financial

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

International Financial Accounting (IFA) Preparation and presentation of Financial Statements DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

1. Definition of cash components

Opinion n 2015-06 of 3 July 2015 relating to Central Government Accounting Standard 10 Cash Components On 3 July 2015 the Public Sector Accounting Standards Council adopted this Opinion relating to Central

Opinion n 2015-06 of 3 July 2015 relating to Central Government Accounting Standard 10 Cash Components On 3 July 2015 the Public Sector Accounting Standards Council adopted this Opinion relating to Central

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Model Answer. M.Com IV Semester. Financial market and financial services. Paper code- AS 2384

Model Answer M.Com IV Semester Financial market and financial services Paper code- AS 2384 1. (I) Money Market is a market for short term loans or financial assets. As the name implies it does not deal

Model Answer M.Com IV Semester Financial market and financial services Paper code- AS 2384 1. (I) Money Market is a market for short term loans or financial assets. As the name implies it does not deal

CHAPTER 2: THE CANADIAN SECURITIES INDUSTRY

CHAPTER 2: THE CANADIAN SECURITIES INDUSTRY Topic One: Industry Overview 1. Self-regulatory Organizations (SROs). A. The SROs set rules that govern the operations of investment dealers and market activity.

CHAPTER 2: THE CANADIAN SECURITIES INDUSTRY Topic One: Industry Overview 1. Self-regulatory Organizations (SROs). A. The SROs set rules that govern the operations of investment dealers and market activity.

Capital adequacy ratios for banks - simplified explanation and

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

i T-bill (dy) = $10,000 - $9,765 360 = 6.768% $10,000 125

= $10,000 - $9,765 360 = 6.768% $10,000 125") Answers to Chapter 5 Questions 1. First, money market instruments are generally sold in large denominations (often in units of $1 million to $10 million). Most money market participants want or need to

Answers to Chapter 5 Questions 1. First, money market instruments are generally sold in large denominations (often in units of $1 million to $10 million). Most money market participants want or need to

Portfolio investment is covered by general permission subject to following condition/provisions.

PORTFOLIO INVESTMENT SCHEME FOR NRIS Portfolio Investment Scheme for NRIs Schedule 2 and 3 of the Notification No. FEMA 20/2000 RB contains provisions relating to Portfolio investment by NRIs. OCBs are

PORTFOLIO INVESTMENT SCHEME FOR NRIS Portfolio Investment Scheme for NRIs Schedule 2 and 3 of the Notification No. FEMA 20/2000 RB contains provisions relating to Portfolio investment by NRIs. OCBs are

-------------------------------------------------

Unofficial Translation With courtesy of the Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language Please refer to the Thai text for the official

Unofficial Translation With courtesy of the Foreign Banks' Association This translation is for the convenience of those unfamiliar with the Thai language Please refer to the Thai text for the official

Shares Mutual funds Structured bonds Bonds Cash money, deposits

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments Contents 1. Risks connected with the type of financial instrument... 2 Credit

Rigensis Bank AS Information on the Characteristics of Financial Instruments and the Risks Connected with Financial Instruments Contents 1. Risks connected with the type of financial instrument... 2 Credit

1 October 2015. Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet

1 October 2015 Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet Table of Contents 1. Purpose of Policy 2. Objectives of Holding Financial

1 October 2015 Statement of Policy Governing the Acquisition and Management of Financial Assets for the Bank of Canada s Balance Sheet Table of Contents 1. Purpose of Policy 2. Objectives of Holding Financial

Rating Criteria for Finance Companies

The broad analytical framework used by CRISIL to rate finance companies is the same as that used for banks and financial institutions. In addition, CRISIL also addresses certain issues that are specific

The broad analytical framework used by CRISIL to rate finance companies is the same as that used for banks and financial institutions. In addition, CRISIL also addresses certain issues that are specific

Key learning points I

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

Agreement between the Ministry of Finance and Central Bank of Iceland on Treasury debt management

Agreement between the Ministry of Finance and Central Bank of Iceland on Treasury debt management 1. Foundation of the Agreement Under Article 1 of Act No. 43/1990 on the National Debt Management Agency,

Agreement between the Ministry of Finance and Central Bank of Iceland on Treasury debt management 1. Foundation of the Agreement Under Article 1 of Act No. 43/1990 on the National Debt Management Agency,

BOARD NOTICE.. OF 2013 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002

1 BOARD NOTICE.. OF 2013 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002 DETERMINATION OF SECURITIES, CLASSES OF SECURITIES, ASSETS OR CLASSES OF ASSETS THAT MAY BE INCLUDED IN

1 BOARD NOTICE.. OF 2013 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002 DETERMINATION OF SECURITIES, CLASSES OF SECURITIES, ASSETS OR CLASSES OF ASSETS THAT MAY BE INCLUDED IN

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES Official Gazette of Publication: 19.01.2008 26761 Issued By: Prime Ministry

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES Official Gazette of Publication: 19.01.2008 26761 Issued By: Prime Ministry

Introduction: Moreover, regulations and instructions are important sources issued by the CBJ in accordance with the Central Bank of Jordan Law.

Introduction: The Central Bank of Jordan (CBJ), established in the late 1950s, is the monitoring authority of foreign and Jordanian commercial banks and specialized credit institutions. The CBJ is an independent

Introduction: The Central Bank of Jordan (CBJ), established in the late 1950s, is the monitoring authority of foreign and Jordanian commercial banks and specialized credit institutions. The CBJ is an independent

Financial Stability Oversight Council. Staff Guidance. Methodologies Relating to Stage 1 Thresholds. June 8, 2015

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

ACT ON BANKS. The National Council of the Slovak Republic has adopted this Act: SECTION I PART ONE BASIC PROVISIONS. Article 1

ACT ON BANKS The full wording of Act No. 483/2001 Coll. dated 5 October 2001 on banks and on changes and the amendment of certain acts, as amended by Act No. 430/2002 Coll., Act No. 510/2002 Coll., Act

ACT ON BANKS The full wording of Act No. 483/2001 Coll. dated 5 October 2001 on banks and on changes and the amendment of certain acts, as amended by Act No. 430/2002 Coll., Act No. 510/2002 Coll., Act

Capital Market Development in Cambodia

Capital Market Development in Cambodia Hanoi, 1 st March 2007 Dr. Hang Chuon Naron Secretary General Ministry of Economy and Finance Contents Overview of Financial Market Present financial system in Cambodia

Capital Market Development in Cambodia Hanoi, 1 st March 2007 Dr. Hang Chuon Naron Secretary General Ministry of Economy and Finance Contents Overview of Financial Market Present financial system in Cambodia

www.eenadupratibha.net

IBPS PROBATIONARY OFFICERS Banking Knowledge Bank advances and loans Banks collect deposits for low rates of interest and lend for higher rate of interest. The margin between these two rates of interest

IBPS PROBATIONARY OFFICERS Banking Knowledge Bank advances and loans Banks collect deposits for low rates of interest and lend for higher rate of interest. The margin between these two rates of interest

TREASURY AND INVESTMENT MANAGEMENT POLICY

TREASURY AND INVESTMENT MANAGEMENT POLICY 1.0 INTRODUCTION 1.1 This document sets out the policy for the University and its subsidiary companies concerning raising capital finance and investment of surplus

TREASURY AND INVESTMENT MANAGEMENT POLICY 1.0 INTRODUCTION 1.1 This document sets out the policy for the University and its subsidiary companies concerning raising capital finance and investment of surplus

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION Statistics Norway published the first set of annual financial balance sheets in 1957. The accounts recorded the stocks of financial assets and liabilities

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION Statistics Norway published the first set of annual financial balance sheets in 1957. The accounts recorded the stocks of financial assets and liabilities

PROVINCIAL COMPANIES REGULATION

Province of Alberta INSURANCE ACT PROVINCIAL COMPANIES REGULATION Alberta Regulation 124/2001 With amendments up to and including Alberta Regulation 79/2011 Office Consolidation Published by Alberta Queen

Province of Alberta INSURANCE ACT PROVINCIAL COMPANIES REGULATION Alberta Regulation 124/2001 With amendments up to and including Alberta Regulation 79/2011 Office Consolidation Published by Alberta Queen

33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL BROKERAGE FIRMS AND MANAGEMENT COMPANIES I. GENERAL PROVISIONS

APPROVED by Order No. VAS-6 of 12 May 2006 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL

APPROVED by Order No. VAS-6 of 12 May 2006 of the Director of the Public Establishment the Institute of Accounting of the Republic of Lithuania 33 BUSINESS ACCOUNTING STANDARD FINANCIAL STATEMENTS OF FINANCIAL

Act on Investment Firms 26.7.1996/579

Please note: This is an unofficial translation. Amendments up to 135/2007 included, May 2007. Act on Investment Firms 26.7.1996/579 CHAPTER 1 General provisions Section 1 Scope of application This Act

Please note: This is an unofficial translation. Amendments up to 135/2007 included, May 2007. Act on Investment Firms 26.7.1996/579 CHAPTER 1 General provisions Section 1 Scope of application This Act

GUIDE TO THE SURVEY FINANCIAL BALANCE STATISTICS

1(16) GUIDE TO THE SURVEY FINANCIAL BALANCE STATISTICS 1 GENERAL INFORMATION... 3 2 DEFINITION OF DATA... 3 2.1 Positions... 3 2.2... 3 2.3... 4 3 DEFINITION OF VARIABLES... 4 3.1 Financial assets... 4

1(16) GUIDE TO THE SURVEY FINANCIAL BALANCE STATISTICS 1 GENERAL INFORMATION... 3 2 DEFINITION OF DATA... 3 2.1 Positions... 3 2.2... 3 2.3... 4 3 DEFINITION OF VARIABLES... 4 3.1 Financial assets... 4

Central Bank of Iraq. Press Communiqué

Central Bank of Iraq Press Communiqué New Central Bank policy instruments Summary At its August 26 meeting, the Board of the Central Bank of Iraq (CBI) adopted a new Reserve Requirement regulation and

Central Bank of Iraq Press Communiqué New Central Bank policy instruments Summary At its August 26 meeting, the Board of the Central Bank of Iraq (CBI) adopted a new Reserve Requirement regulation and

TERHAD. Training to Labuan Offshore Entities on Compilation of International Investment Position (IIP) Report

Report") TERHAD Training to Labuan Offshore Entities on Compilation of International Investment (IIP) Report September 2012 TERHAD 1. Equity Capital: A/L Definition Form DIa Exposures with Affiliated Enterprises

TERHAD Training to Labuan Offshore Entities on Compilation of International Investment (IIP) Report September 2012 TERHAD 1. Equity Capital: A/L Definition Form DIa Exposures with Affiliated Enterprises

THE BANK'S BALANCE SHEET. Lecture 3 Monetary policy

THE BANK'S BALANCE SHEET Lecture 3 Monetary policy THE BANK'S BALANCE SHEET Like any balance sheet, bank balance sheet lines up the assets on one side and the liabilities on the other side. Two sides equal

THE BANK'S BALANCE SHEET Lecture 3 Monetary policy THE BANK'S BALANCE SHEET Like any balance sheet, bank balance sheet lines up the assets on one side and the liabilities on the other side. Two sides equal

Mutual Funds in Pakistan

Mutual Funds in Pakistan Investors Education Seminar arranged by SECP and ICAP held on 29th January 2015 Presented By First Capital Investments Limited Definition of Mutual Fund A mutual fund is a collective

Mutual Funds in Pakistan Investors Education Seminar arranged by SECP and ICAP held on 29th January 2015 Presented By First Capital Investments Limited Definition of Mutual Fund A mutual fund is a collective

Introduction to Fixed Income (IFI) Course Syllabus

Course Syllabus") Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

Introduction to Fixed Income (IFI) Course Syllabus 1. Fixed income markets 1.1 Understand the function of fixed income markets 1.2 Know the main fixed income market products: Loans Bonds Money market instruments

News Release January 28, 2016. Performance Review: Quarter ended December 31, 2015

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

NOVEMBER 2010 (REVISED)

") CENTRAL BANK OF CYPRUS BANKING SUPERVISION AND REGULATION DIVISION DIRECTIVE TO BANKS ON THE COMPUTATION OF PRUDENTIAL LIQUIDITY IN ALL CURRENCIES NOVEMBER 2010 (REVISED) DIRECTIVE TO BANKS ON THE COMPUTATION

CENTRAL BANK OF CYPRUS BANKING SUPERVISION AND REGULATION DIVISION DIRECTIVE TO BANKS ON THE COMPUTATION OF PRUDENTIAL LIQUIDITY IN ALL CURRENCIES NOVEMBER 2010 (REVISED) DIRECTIVE TO BANKS ON THE COMPUTATION

Statement of Financial Condition

Financial Report for the 14th Business Year 5-1, Marunouchi 1-Chome, Chiyoda-ku, Tokyo Citigroup Global Markets Japan Inc. Rodrigo Zorrilla, Representative Director, President and CEO Statement of Financial

Financial Report for the 14th Business Year 5-1, Marunouchi 1-Chome, Chiyoda-ku, Tokyo Citigroup Global Markets Japan Inc. Rodrigo Zorrilla, Representative Director, President and CEO Statement of Financial

A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT

M. OOZEER A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT 14 May 2015 2 A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT Act No. 5 of 2008 [Amended 14/2009, 10/2010, 36/2011, 38/2011,

M. OOZEER A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT 14 May 2015 2 A CONSOLIDATED VERSION OF THE PUBLIC DEBT MANAGEMENT ACT Act No. 5 of 2008 [Amended 14/2009, 10/2010, 36/2011, 38/2011,

Public Debt and Cash Management

Federation of European Accountants Federation of European Accountants Fédération Fédération des Experts des Experts comptables comptables Européens Européens Public Sector Public Debt and Cash Management

Federation of European Accountants Federation of European Accountants Fédération Fédération des Experts des Experts comptables comptables Européens Européens Public Sector Public Debt and Cash Management

PRUDENTIAL SUPERVISION IN HONG KONG

PRUDENTIAL SUPERVISION IN HONG KONG PREFACE Under the Banking Ordinance ( the Ordinance ), Chapter 155 of the Laws of Hong Kong, the Monetary Authority ( the MA ) is charged with the responsibility for

PRUDENTIAL SUPERVISION IN HONG KONG PREFACE Under the Banking Ordinance ( the Ordinance ), Chapter 155 of the Laws of Hong Kong, the Monetary Authority ( the MA ) is charged with the responsibility for

T he restrictions of Sections 23A and Regulation W

BNA s Banking Report Reproduced with permission from BNA s Banking Report, 100 BBR 109, 1/15/13, 01/15/2013. Copyright 2013 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com REGULATION

BNA s Banking Report Reproduced with permission from BNA s Banking Report, 100 BBR 109, 1/15/13, 01/15/2013. Copyright 2013 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com REGULATION

FAQs on Debenture Trustee

FAQs on Debenture Trustee 1. What is a Debenture? A debenture is an instrument of debt executed by the company acknowledging its obligation to repay the sum at a specified rate and also carrying an interest.

FAQs on Debenture Trustee 1. What is a Debenture? A debenture is an instrument of debt executed by the company acknowledging its obligation to repay the sum at a specified rate and also carrying an interest.

Hong Kong is increasingly seen as a necessary operations

1 TIMOTHY LOH Financial Services & Law Review Setting Up In Hong Kong: A Guide for the Finance Industry Hong Kong is increasingly seen as a necessary operations center for the financial industry. It is

1 TIMOTHY LOH Financial Services & Law Review Setting Up In Hong Kong: A Guide for the Finance Industry Hong Kong is increasingly seen as a necessary operations center for the financial industry. It is

Office of the State Treasurer 200 Piedmont Avenue, Suite 1204, West Tower Atlanta, Georgia 30334-5527 www.ost.ga.gov

Office of the State Treasurer 200 Piedmont Avenue, Suite 1204, West Tower Atlanta, Georgia 30334-5527 www.ost.ga.gov INVESTMENT POLICY FOR THE OFFICE OF THE STATE TREASURER POLICY December 2015 O.C.G.A.

Office of the State Treasurer 200 Piedmont Avenue, Suite 1204, West Tower Atlanta, Georgia 30334-5527 www.ost.ga.gov INVESTMENT POLICY FOR THE OFFICE OF THE STATE TREASURER POLICY December 2015 O.C.G.A.

CHAPTER I INTRODUCTION. This chapter provides the background to the. research proposition and describes the statement of. problem.

CHAPTER I INTRODUCTION This chapter provides the background to the research proposition and describes the statement of problem. 1.1 BACKGROUND The growth and expansion of public sector banks can be categorised

CHAPTER I INTRODUCTION This chapter provides the background to the research proposition and describes the statement of problem. 1.1 BACKGROUND The growth and expansion of public sector banks can be categorised

Chapter 17. Financial Management and Institutions

Chapter 17 Financial Management and Institutions 1 2 3 4 Identify the functions performed by a firm s financial managers. Describe the characteristics and functions of money. Identify the various measures

Chapter 17 Financial Management and Institutions 1 2 3 4 Identify the functions performed by a firm s financial managers. Describe the characteristics and functions of money. Identify the various measures

Chief Executive Officers of All National Banks, Deputy Comptrollers (District) and All Examining Personnel

and All Examining Personnel") O BC - 196 BANKING ISSUANCE Comptroller of the Currency Administrator of National Banks Type: Banking Circular Subject: Securities Lending To: Chief Executive Officers of All National Banks, Deputy Comptrollers

O BC - 196 BANKING ISSUANCE Comptroller of the Currency Administrator of National Banks Type: Banking Circular Subject: Securities Lending To: Chief Executive Officers of All National Banks, Deputy Comptrollers

Trading of Government Securities on the Stock Exchanges

Trading of Government Securities on the Stock Echanges Draft Scheme for comments [Objective With a view to encouraging wider participation of all classes of investors, including retail, across the country

Trading of Government Securities on the Stock Echanges Draft Scheme for comments [Objective With a view to encouraging wider participation of all classes of investors, including retail, across the country

8 Financial Services in India

8 Financial Services in India BASIC CONCEPTS 1. Introduction Financial Services has a broad definition and it can be defined as the products and services offered by institutions like banks of various kinds

8 Financial Services in India BASIC CONCEPTS 1. Introduction Financial Services has a broad definition and it can be defined as the products and services offered by institutions like banks of various kinds

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Investments GUIDE TO FUND RISKS

Investments GUIDE TO FUND RISKS CONTENTS Making sense of risk 3 General risks 5 Fund specific risks 6 Useful definitions 9 2 MAKING SENSE OF RISK Understanding all the risks involved when selecting an

Investments GUIDE TO FUND RISKS CONTENTS Making sense of risk 3 General risks 5 Fund specific risks 6 Useful definitions 9 2 MAKING SENSE OF RISK Understanding all the risks involved when selecting an

Chapter 3. How Securities are Traded

Chapter 3 How Securities are Traded Primary vs. Secondary Security Sales Primary: When firms need to raise capital, they may choose to sell (or float) new securities. These new issues typically are marketed

Chapter 3 How Securities are Traded Primary vs. Secondary Security Sales Primary: When firms need to raise capital, they may choose to sell (or float) new securities. These new issues typically are marketed

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

The Options Clearing Corporation

PROSPECTUS M The Options Clearing Corporation PUT AND CALL OPTIONS This prospectus pertains to put and call security options ( Options ) issued by The Options Clearing Corporation ( OCC ). Certain types

PROSPECTUS M The Options Clearing Corporation PUT AND CALL OPTIONS This prospectus pertains to put and call security options ( Options ) issued by The Options Clearing Corporation ( OCC ). Certain types

CAP. B 3 BANKS AND OTHER FINANCIAL INSTITUTIONS ACT CHAPTER B 3 VOLUME 2

CAP. B 3 BANKS AND OTHER FINANCIAL INSTITUTIONS ACT CHAPTER B 3 VOLUME 2 THE LAWS OF THE FEDERATION OF NIGERIA 2004 ARRANGEMENT OF SECTIONS PART I BANKS ESTABLISHMENT OF BANKS, ETC SECTION 1. Functions,

CAP. B 3 BANKS AND OTHER FINANCIAL INSTITUTIONS ACT CHAPTER B 3 VOLUME 2 THE LAWS OF THE FEDERATION OF NIGERIA 2004 ARRANGEMENT OF SECTIONS PART I BANKS ESTABLISHMENT OF BANKS, ETC SECTION 1. Functions,

How To Decide If A Bank Can Be A Successful Bank

Legal notice All effort has been made to ensure the accuracy of this translation, which is based on the original Slovenian text. All translations of this kind may, nevertheless, be subject to a certain

Legal notice All effort has been made to ensure the accuracy of this translation, which is based on the original Slovenian text. All translations of this kind may, nevertheless, be subject to a certain

During the Fall of 2008, the financial industry as a whole experienced a challenging environment for funding and liquidity as a result of the global economic crisis. Goldman Sachs has, for many years,

During the Fall of 2008, the financial industry as a whole experienced a challenging environment for funding and liquidity as a result of the global economic crisis. Goldman Sachs has, for many years,

BOARD NOTICE 90 OF 2014 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002

STAATSKOERANT, 8 AUGUSTUS 2014 No. 37895 3 BOARD NOTICES BOARD NOTICE 90 OF 2014 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002 DETERMINATION OF SECURITIES, CLASSES OF SECURITIES,

STAATSKOERANT, 8 AUGUSTUS 2014 No. 37895 3 BOARD NOTICES BOARD NOTICE 90 OF 2014 FINANCIAL SERVICES BOARD COLLECTIVE INVESTMENT SCHEMES CONTROL ACT, 2002 DETERMINATION OF SECURITIES, CLASSES OF SECURITIES,

SECURITIES AND FUTURES ACT (CAP. 289)

") Monetary Authority of Singapore SECURITIES AND FUTURES ACT (CAP. 289) NOTICE ON RISK BASED CAPITAL ADEQUACY REQUIREMENTS FOR HOLDERS OF CAPITAL MARKETS SERVICES LICENCES Monetary Authority of Singapore

Monetary Authority of Singapore SECURITIES AND FUTURES ACT (CAP. 289) NOTICE ON RISK BASED CAPITAL ADEQUACY REQUIREMENTS FOR HOLDERS OF CAPITAL MARKETS SERVICES LICENCES Monetary Authority of Singapore

United Kingdom. From: OECD Banking Statistics: Methodological Country Notes 2010

From: OECD Banking Statistics: Methodological Country Notes 2010 Access the complete publication at: http://dx.doi.org/10.1787/9789264089907-en United Kingdom Please cite this chapter as: OECD (2011),

From: OECD Banking Statistics: Methodological Country Notes 2010 Access the complete publication at: http://dx.doi.org/10.1787/9789264089907-en United Kingdom Please cite this chapter as: OECD (2011),

INDONESIA Ali Budiardjo, Nugroho, Reksodiputro

Bank Finance and Regulation Survey INDONESIA Ali Budiardjo, Nugroho, Reksodiputro I. BANKS AND FINANCIAL INSTITUTIONS SUPERVISION 1) Applicable laws and regulation. Provide a list of the main laws and

Bank Finance and Regulation Survey INDONESIA Ali Budiardjo, Nugroho, Reksodiputro I. BANKS AND FINANCIAL INSTITUTIONS SUPERVISION 1) Applicable laws and regulation. Provide a list of the main laws and

CHAPTER 2. Asset Classes. the Money Market. Money market instruments. Capital market instruments. Asset Classes and Financial Instruments

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

2-2 Asset Classes Money market instruments CHAPTER 2 Capital market instruments Asset Classes and Financial Instruments Bonds Equity Securities Derivative Securities The Money Market 2-3 Table 2.1 Major

Roche Capital Market Ltd Financial Statements 2014

Roche Capital Market Ltd Financial Statements 2014 1 Roche Capital Market Ltd - Financial Statements 2014 Roche Capital Market Ltd, Financial Statements Roche Capital Market Ltd, statement of comprehensive

Roche Capital Market Ltd Financial Statements 2014 1 Roche Capital Market Ltd - Financial Statements 2014 Roche Capital Market Ltd, Financial Statements Roche Capital Market Ltd, statement of comprehensive

THE LAW OF THE KYRGYZ REPUBLIC. On securities market

Bishkek July 21, 1998, # 95 THE LAW OF THE KYRGYZ REPUBLIC On securities market Chapter 1. General Provisions Chapter 2. State Regulation of Securities Market Chapter 3. Professional Securities Market

Bishkek July 21, 1998, # 95 THE LAW OF THE KYRGYZ REPUBLIC On securities market Chapter 1. General Provisions Chapter 2. State Regulation of Securities Market Chapter 3. Professional Securities Market