Business Combinations and Noncontrolling Interests

|

|

|

- Suzanna Allison

- 7 years ago

- Views:

Transcription

1 Business Combinations and Noncontrolling Interests Q1 - Q Financial Statement Disclosure Analysis Summary Results and Observations

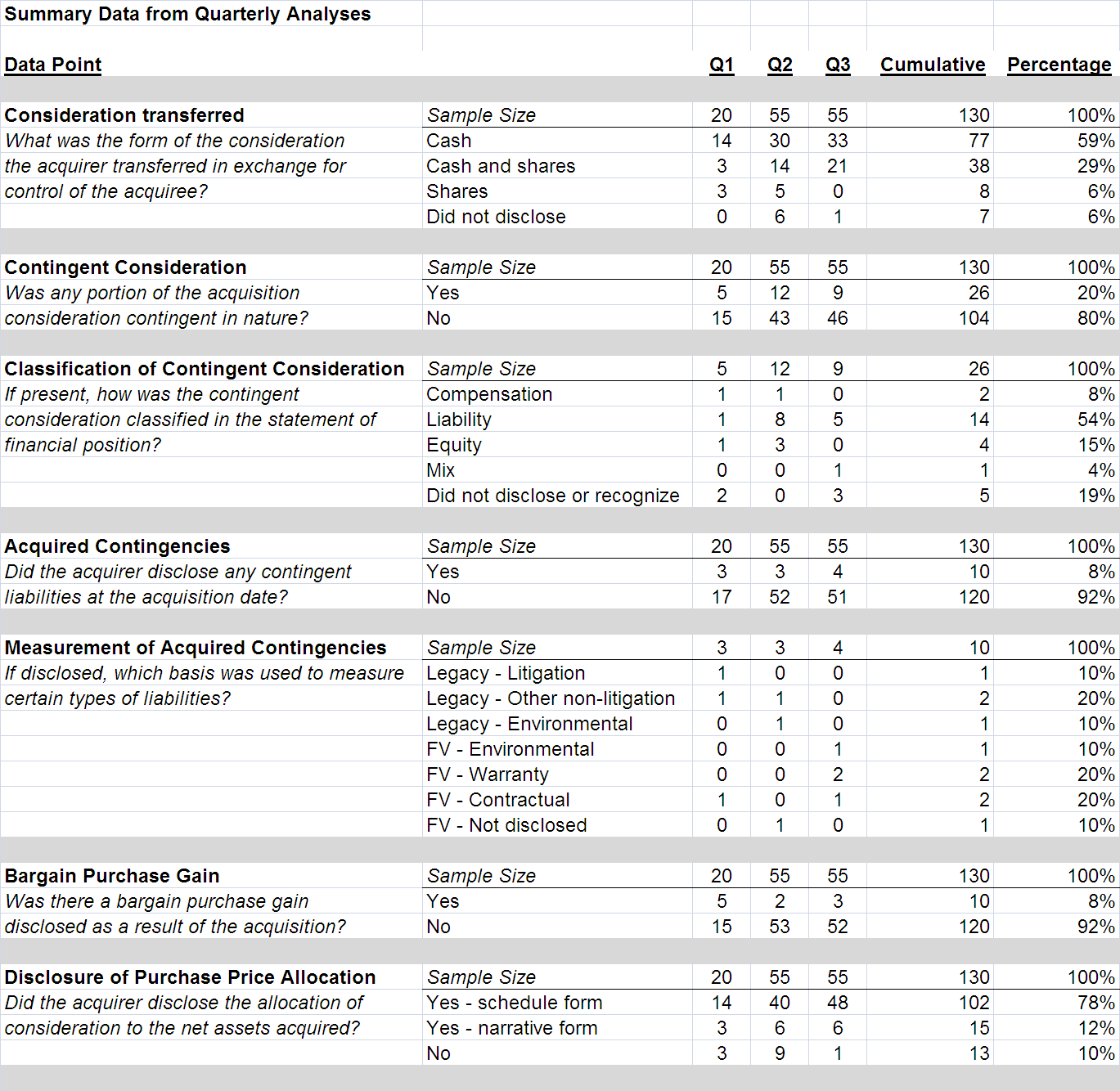

2 Welcome to PricewaterhouseCoopers' (PwC) Business Combinations and Noncontrolling Interests Financial Statement Disclosure Analysis. This document summarizes observations from an analysis of public company transactions that closed during the first three quarters of The primary objective is to provide data, analysis and insights on how certain of the financial statement disclosure requirements related to business combinations and noncontrolling interests have been applied in practice. Overview and Methodology The information presented in this document is summarized from an analysis of 130 public company transactions that closed during the first three quarters of calendar year All disclosures that were analyzed are from companies whose basis of accounting is U.S. Generally Accepted Accounting Principles (U.S. GAAP). 1 The companies that were part of the analysis were selected judgmentally, with the primary criterion for selection being those transactions with the highest values. There was no intentional bias toward any particular industry. Not all of the transactions reviewed were material to a specific acquirer and, accordingly, some disclosures were omitted from the financial statements. Readers should be aware that the results from the reporting periods surveyed may not be indicative of longer-term trends given several prevailing factors, such as the relatively short length of time that the new standards have been in effect, the weaker macro-economic conditions in the U.S. compared to historical norms, and a decrease in acquisition activity in 2009 compared to recent years. For additional data and example disclosures, please refer to the full quarterly disclosure analysis prepared for each of Q1, Q2 and Q from which the data in this summary is derived. Those quarterly analyses are available on PwC's CFOdirect website ( PwC clients who have questions on these publications should contact their engagement partner. Prospective clients and friends should contact the managing partner of the PwC office nearest you, which can be found at The disclosure information presented in this analysis is provided solely to increase your awareness and understanding of the types of disclosures that individual companies have made in particular situations. Because disclosures are specific to the facts and circumstances of the individual company to which they relate, there is no suggestion implied in this information that the disclosures analyzed represent compliance with requirements under U.S. GAAP or are consistent with PwC's views in all circumstances. Accordingly, we make no comments as to the appropriateness, completeness, or accuracy of these disclosures. Further, the findings that are included in this analysis are not intended to represent best practices. 1 The U.S. GAAP accounting standards applicable to business combinations are ASC 805, Business Combinations, and ASC 810, Consolidation (the "new standards"). 1

3 Disclosure Principles The U.S. GAAP disclosure requirements 2 are intended to enable users of financial statements to evaluate the nature and financial effects of: A business combination that occurs either during the current reporting period or after the reporting period, but before the financial statements are issued Adjustments recognized in the current reporting period that relate to business combinations that occurred in current and previous reporting periods The nature of the relationship between the parent and a subsidiary or investee when the parent does not have 100 percent ownership or control All U.S. GAAP disclosures must be reported for each material business combination. All disclosures should be made in the period in which the business combination occurs. Under U.S. GAAP, companies should include the disclosures in subsequent financial statements if an acquisition occurred in a previous reporting period and that period is presented in the financial statements. Companies are also required to disclose information about acquisitions made after the balance sheet date, but before the financial statements are issued. If the initial accounting for the business combination is incomplete, the company should describe which disclosures could not be made and the reasons they could not be made. Companies are also required to disclose gains or losses arising from the deconsolidation of a business when the company loses control of that business. Findings Presented on the following pages is commentary on certain of the more significant findings noted in our analysis. The full set of summarized data is presented afterward. The percentages presented in the findings section should be viewed in connection with the underlying summarized data, as there may be certain limitations in the use of percentages due to the small sample involved in our analysis. 2 The disclosures that are required for all material business combinations that occur during the reporting period can be found in ASC Additionally, ASC (e)-(h), ASC (a)-(e), and ASC (a)-(f) provide disclosure requirements for individually immaterial acquisitions that are collectively material, in the period in which the business combinations occur. The disclosures that are required for noncontrolling interests can be found in ASC

4 Form of Consideration We noted that the form of the acquisition consideration was heavily weighted toward either cash or some mixture of consideration including cash. The new standards require that the value of equity consideration be measured as of the date that control is actually obtained versus the deal announcement date (which was the measurement date for equity consideration under the previous standard). This finding may indicate that equity is a less attractive acquisition currency because of generally lower stock prices compared to prices in recent history and/or companies are seeking to avoid the inherent volatility in pricing that could occur when shares are the form of consideration. Contingent Consideration We noted that contingent consideration was not disclosed in the majority of the acquisition consideration arrangements. This finding may indicate that one of the factors companies considered in structuring their deals was to avoid the use of contingent consideration due to a concern over postacquisition earnings volatility. 3

5 Classification of Contingent Consideration For the transactions that contained contingent consideration, the majority of acquirers classified the contingent consideration arrangement in liabilities on the balance sheet. This classification requires a company to remeasure the liability to fair value at each reporting period and record any adjustment in earnings. While many companies may desire to avoid the resulting income statement volatility, equity classification (which does not require subsequent remeasurement) is generally more difficult to achieve under the new standards. However, the results of the analysis show a greater percentage of equity-classified contingent consideration than perhaps many had expected. Additionally, two of the companies that disclosed the presence of a contingent payment arrangement disclosed that some portion of the arrangement would be accounted for as compensation expense in the post-combination earnings of the acquirer. Disclosure of Purchase Price Allocation One of the requirements of both the previous and new standards is the disclosure of the amounts recognized as of the acquisition date for each major class of assets acquired and liabilities assumed (commonly called the "purchase price allocation"). The overwhelming majority of the transactions included in our sample did disclose this allocation, either in schedule form or narratively. 4

6 Status of Purchase Price Allocation Historically, it was common for companies to disclose as preliminary the purchase price allocation presented in the reporting period in which the acquisition was completed. Previously, adjustments to the initial accounting within the measurement period were prospectively recorded. Now, material adjustments to the initial accounting must be retroactively reflected in the comparative financial statements. Some believed that this change would cause companies to make greater efforts to finalize allocations in the acquisition period to reduce the possibility of a need to recast previous period results. However, the results of our analysis indicate that the majority of companies continue to describe allocations as preliminary. However, we did observe that the few allocations disclosed as being final all related to deals closed in the first month of the quarter. Further, our analysis indicated that the majority of these companies did not specify which particular asset or liability balances are still subject to possible future adjustment. Of the companies that did specify, the most common open items noted were intangible assets, income tax liabilities, accrued liabilities, and pre-acquisition contingent liabilities. Acquired Contingencies The topic of how best to measure contingent liabilities that are acquired in a business combination was the subject of much debate upon the issuance of the related business combinations guidance. Concerns were expressed in the marketplace over measurement complexity, attorney-client privilege and other legal issues and uncertainties involving scope. Our analysis shows that acquired contingent liabilities were disclosed only for a small portion of the transactions in the sample. 5

7 Measurement of Acquired Contingencies Of those acquired contingencies that were disclosed, some were initially measured and recorded at fair value, while others were initially measured and recorded if determined to be probable and reasonably estimable (the "legacy" approach). The new standards allow for such a legacy approach only when fair value cannot be determined during the measurement period. There was an expectation that most companies would use the legacy approach for measuring some of the more common types of contingent liabilities, such as litigation and environmental liabilities, given the many factors and inherent uncertainties in determining fair value for such items. Another expected outcome was that the fair value of warranty liabilities generally would be determinable. Our analysis supports both of these notions. Litigation was measured using a legacy approach, as were environmental liabilities with one exception where the amount involved was de minimis. Additionally, we observed that warranty liabilities and certain other contractual contingencies were measured at fair value. 6

8 Bargain Purchase The new standards now require a company to record a "bargain purchase gain" in earnings at the time of acquisition if the fair value of the net assets acquired exceeds the acquisition consideration. While the new standards indicate that such instances are expected to be infrequent, the results of our analysis show that bargain purchase gains were disclosed with somewhat greater frequency than perhaps expected. This is likely attributable to the economic downturn in the U.S. that continued throughout 2009 and the consolidation of weaker competitors observed in certain industry sectors during that time. These conditions may change as the economy strengthens. Thus, the results of this analysis may not be indicative of longer-term trends that may develop. Acquisition Costs The new standards require companies to expense acquisition costs such as legal, advisory and consulting fees as incurred, which is a change from previous standards under which these costs were capitalized. Companies must also disclose material transaction costs recorded in earnings. This requirement creates some inherent sensitivity for companies who may be incurring material due diligence costs for possible acquisitions which they would rather not disclose until a later period. Our analysis suggests that only approximately half of those in the survey disclosed transactions costs. 7

9 Classification of Acquisition Costs Regarding the classification of acquisition costs in the income statement, the majority of companies (79%) classified these costs as a component of income from operations (Ops). The new standards require disclosure of the line item in the income statement where the costs are recorded. Public Company Disclosures If an acquirer is a public company, there is a requirement to disclose the amount of revenue and earnings of the acquiree since the acquisition date included in the acquirer's consolidated income statement. There is also a requirement to disclose the pro-forma revenue and earnings of the combined entity for two reporting periods as though the acquisition date for the business combination had been as of the beginning date of the immediately-preceding annual reporting period. If these disclosures are deemed impracticable, the acquirer must disclose that fact and explain why it is impracticable. Of the companies that disclosed pro-forma information, the most common items affecting the pro-forma results included: Additional depreciation expense on fixed assets Additional amortization expense on intangible assets Additional interest expense on the financing of the acquisition Additional employee benefits expense Exclusion of acquisition costs Exclusion of integration costs Many companies specifically disclosed that the acquiree results since acquisition and the pro-forma information were not disclosed because the acquisition was not considered material. No companies adjusted the pro-forma results for expected post-acquisition synergies. Several companies specifically disclosed that no adjustments to the pro-forma results had been made for the conforming of acquirer and acquiree accounting policies. 8

10 In-Process Research and Development (IPR&D) Costs The new standards require that IPR&D be initially measured at fair value and classified as an indefinite-lived intangible asset on the date of acquisition. For those companies that disclosed IPR&D and also disclosed the methodology used to initially value the IPR&D, the method used in all cases was a discounted cash flow (DCF) income approach. 9

11 Noncontrolling Interests When noncontrolling interests (NCIs) were disclosed (situations in which the acquirer held less than 100% of the equity interest in the acquiree), the most common valuation technique used to measure the fair value of the noncontrolling interest was the closing market price of the acquired company's shares on the acquisition date. In addition, for those acquisitions with an NCI, the vast majority of acquirers began the consolidated statement of cash flows (SOCF) with the caption "net income," while two variations ("net income attributable to the company" and "net income attributable to common shareholders") were observed. Other Findings In addition to those findings previously presented, we noted the following: None of the companies in the analysis specifically disclosed the presence of "defensive" assets, which are defined as assets that an acquirer does not intend to actively use but does intend to hold (lock up) to prevent others from gaining access to the assets. These assets may present unique accounting and valuation challenges, such as determining an initial fair value from the perspective of a market participant and determining an appropriate period over which to amortize the asset. We observed that 44% of companies in the analysis closed their deals during the first month of the quarter. 18% of companies in the analysis closed deals during the first 10 days of the quarter. These percentages may indicate that companies are timing deals to allow for the most amount of time possible before having to report financial information that includes the initial acquisition accounting. Less than 3% of the companies in the analysis disclosed subsequent measurement period adjustments to the amounts originally recorded when the acquisition was made. This may be the result of the limited length of time that has passed since the acquisition dates in the analysis. This may also be indicative of companies performing more robust due diligence procedures in advance of closing deals and more timely valuations after closing deals. 10

12 None of the companies in the analysis specifically disclosed adjustments to tax account balances that had been recorded in prior years related to old deals. The new standards now require any such adjustments to be recorded in earnings rather than as an adjustment to goodwill on the balance sheet. None of the companies in the analysis specifically disclosed the presence of a reacquired right, which is defined as a right that the acquirer had previously granted to the acquiree to use one or more of the acquirer's recognized or unrecognized assets. Similar to defensive assets, reacquired rights may present unique valuation challenges, such as determining their initial fair value. 11

13 12

14 13

15 Contacts John R. Formica, Jr. Partner Phone: Lawrence N. Dodyk Partner Phone: Kevin McManus Senior Manager Phone: Hadir El Fardy Manager Phone: This publication has been prepared for general information on matters of interest only, and does not constitute professional advice on facts and circumstances specific to any person or entity. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication. The information contained in this material was not intended or written to be used, and cannot be used, for purposes of avoiding penalties or sanctions imposed by any government or other regulatory body. PricewaterhouseCoopers LLP, its members, employees and agents shall not be responsible for any loss sustained by any person or entity who relies on this publication PricewaterhouseCoopers LLP. All rights reserved. "PricewaterhouseCoopers" refers to PricewaterhouseCoopers LLP, a Delaware limited liability partnership, or as the context requires, the PricewaterhouseCoopers global network or other member firms of the network each of which is a separate and independent legal entity. To access additional content on accounting and reporting issues, register for CFOdirect Network ( PricewaterhouseCoopers' online resource for senior financial executives.

This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide.

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Dataline A look at current financial reporting issue

Dataline A look at current financial reporting issue No. 2013-24 November 25, 2013 What s inside: Overview... 1 At a glance... 1 The main details... 1 Contents of the Guide... 2 Concepts and application

Dataline A look at current financial reporting issue No. 2013-24 November 25, 2013 What s inside: Overview... 1 At a glance... 1 The main details... 1 Contents of the Guide... 2 Concepts and application

A guide to. accounting for. Second Edition. Assurance Tax Consulting

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

New Accounting for Business Combinations and Minority Interests

New Accounting for Business Combinations and Minority Interests John Scott Senior Manager, Enterprise Group Travis Wolff January 19, 2010 Agenda Overview and background of the new standards- ASC 805 (FAS

New Accounting for Business Combinations and Minority Interests John Scott Senior Manager, Enterprise Group Travis Wolff January 19, 2010 Agenda Overview and background of the new standards- ASC 805 (FAS

Assets acquired to be used in research and development activities

No. 2014-04 January 30, 2014 What s inside: Overview... 1 Background... 1 Accounting and reporting concepts... 2 Accounting for assets acquired in a business combination that are to be used in R&D activities...

No. 2014-04 January 30, 2014 What s inside: Overview... 1 Background... 1 Accounting and reporting concepts... 2 Accounting for assets acquired in a business combination that are to be used in R&D activities...

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 March 6, 2014 Cross-border acquisitions Due diligence and

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 March 6, 2014 Cross-border acquisitions Due diligence and

Accounting developments

Flash Accounting developments New standards for business combinations and non-controlling interests In January 2009, the Accounting Standards Board (AcSB) of the Canadian Institute of Chartered Accountants

Flash Accounting developments New standards for business combinations and non-controlling interests In January 2009, the Accounting Standards Board (AcSB) of the Canadian Institute of Chartered Accountants

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 December 14, 2011 Did I buy a group of assets or a business?

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 December 14, 2011 Did I buy a group of assets or a business?

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 December 13, 2012 Financial risk management considerations

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 December 13, 2012 Financial risk management considerations

New Accounting for Business Combinations and Non-controlling Interests

IFRS ADVISORY SERVICES New Accounting for Business Combinations and Non-controlling Interests August 2008 KPMG LLP The proposed new accounting standards for business combinations and non-controlling interests

IFRS ADVISORY SERVICES New Accounting for Business Combinations and Non-controlling Interests August 2008 KPMG LLP The proposed new accounting standards for business combinations and non-controlling interests

Getting Merger and Acquisition Accounting Right Presented by: John Donohue, Partner and Fred Frank, Partner Professional Practice Group, Moss Adams

Getting Merger and Acquisition Accounting Right Presented by: John Donohue, Partner and Fred Frank, Partner Professional Practice Group, Moss Adams LLP Agenda 1. Review of basic accounting for business

Getting Merger and Acquisition Accounting Right Presented by: John Donohue, Partner and Fred Frank, Partner Professional Practice Group, Moss Adams LLP Agenda 1. Review of basic accounting for business

Mergers & Acquisitions A snapshot Change the way you think about tomorrow s deals * Stay ahead of the new accounting and reporting standards for M&A

February 2010 Mergers & Acquisitions A snapshot Change the way you think about tomorrow s deals * Stay ahead of the new accounting and reporting standards for M&A Summary Accounting for contingent consideration-

February 2010 Mergers & Acquisitions A snapshot Change the way you think about tomorrow s deals * Stay ahead of the new accounting and reporting standards for M&A Summary Accounting for contingent consideration-

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Financial Accounting Series

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 April 23, 2013 What's inside IPR&D accounting the basics...

Mergers & acquisitions a snapshot Change the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 April 23, 2013 What's inside IPR&D accounting the basics...

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes July 2015 505 9th Street NW Suite 800 Washington DC 20004 202.862.0556 www.seia.org Solar Energy Industries Association

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes July 2015 505 9th Street NW Suite 800 Washington DC 20004 202.862.0556 www.seia.org Solar Energy Industries Association

Getting Merger and Acquisition Accounting Right

Getting Merger and Acquisition Accounting Right Presented by: John Donohue, Partner Professional Practice Group Fred Frank, Partner Professional Practice Group Agenda 1. Review of basic accounting for

Getting Merger and Acquisition Accounting Right Presented by: John Donohue, Partner Professional Practice Group Fred Frank, Partner Professional Practice Group Agenda 1. Review of basic accounting for

New Developments Summary

April 15, 2008 NDS 2008-17 Revised for FASB Codification July 1, 2009 New Developments Summary Business combinations FASB Statement 141 (revised 2007) (ASC 805) Summary On December 4, 2007, the FASB issued

April 15, 2008 NDS 2008-17 Revised for FASB Codification July 1, 2009 New Developments Summary Business combinations FASB Statement 141 (revised 2007) (ASC 805) Summary On December 4, 2007, the FASB issued

IFRS alert... IFRS alert 2008-01. IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements

IFRS alert... IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements Alerts may include Grant Thornton International s analysis of how IFRS should be applied

IFRS alert... IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements Alerts may include Grant Thornton International s analysis of how IFRS should be applied

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

Tax accounting services: Foreign currency tax accounting. October 2012

Tax accounting services: Foreign currency tax accounting October 2012 The globalization of commerce and capital markets has resulted in business, investment and capital formation transactions increasingly

Tax accounting services: Foreign currency tax accounting October 2012 The globalization of commerce and capital markets has resulted in business, investment and capital formation transactions increasingly

INSIGHTS. Final Standard Issued on Accounting for Affordable Housing Tax Credit Investments An In-Depth Look JANUARY 2014

INSIGHTS Final Standard Issued on Accounting for Affordable Housing Tax Credit Investments An In-Depth Look JANUARY 2014 On January 15, 2014, the Financial Accounting Standards Board (FASB) issued ASU

INSIGHTS Final Standard Issued on Accounting for Affordable Housing Tax Credit Investments An In-Depth Look JANUARY 2014 On January 15, 2014, the Financial Accounting Standards Board (FASB) issued ASU

IFRS 3 Business Combinations

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 Describe the steps in applying the acquisition method Explain the recognition and measurement principles of IFRS 3 Determine

IFRS 3 Business Combinations 0 Objectives Define a business combination under IFRS 3 Describe the steps in applying the acquisition method Explain the recognition and measurement principles of IFRS 3 Determine

Financial Reporting for Taxes

Financial Reporting for Taxes TEI May A&A Update Meeting Acquisition accounting May 8, 2012 Orlando, FL Wendi Christensen Deloitte Tax LLP wendichristensen@deloitte.com Agenda Disclosures and supporting

Financial Reporting for Taxes TEI May A&A Update Meeting Acquisition accounting May 8, 2012 Orlando, FL Wendi Christensen Deloitte Tax LLP wendichristensen@deloitte.com Agenda Disclosures and supporting

International Financial Reporting Standard 3 Business Combinations

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

VALUATION observations

March 2009 Vol. 2009-05 230 West Street Suite 700 Columbus, OH 43215 614.221.1120 www.gbqconsulting.com 111 Monument Circle Suite 500 Indianapolis, IN 46204 317.264.2606 www.gbqgoelzer.com VALUATION observations

March 2009 Vol. 2009-05 230 West Street Suite 700 Columbus, OH 43215 614.221.1120 www.gbqconsulting.com 111 Monument Circle Suite 500 Indianapolis, IN 46204 317.264.2606 www.gbqgoelzer.com VALUATION observations

What you need to know about the new accounting standards affecting M&A deals*

What you need to know about the new accounting standards affecting M&A deals* *connectedthinking What you need to know about the new accounting standards affecting M&A deals Executive summary Overview

What you need to know about the new accounting standards affecting M&A deals* *connectedthinking What you need to know about the new accounting standards affecting M&A deals Executive summary Overview

Monster Worldwide Reports Third Quarter 2015 Results

Monster Worldwide Reports Third Quarter 2015 Results Third Quarter Financial Highlights: o Company Exceeds Expectations on All Profitability Metrics For the 5th Consecutive Quarter Adjusted EBITDA Including

Monster Worldwide Reports Third Quarter 2015 Results Third Quarter Financial Highlights: o Company Exceeds Expectations on All Profitability Metrics For the 5th Consecutive Quarter Adjusted EBITDA Including

International Financial Reporting Standards (IFRS)

") FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 November 13, 2014 Companies in distress: Bankruptcy process

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 November 13, 2014 Companies in distress: Bankruptcy process

Interim Consolidated Financial Statements (Unaudited)

") Interim Consolidated Financial Statements (Unaudited) For the Six Months Ended, NTT FINANCE CORPORATION This document has been translated and reclassified from a part of the Japanese

Interim Consolidated Financial Statements (Unaudited) For the Six Months Ended, NTT FINANCE CORPORATION This document has been translated and reclassified from a part of the Japanese

27 Business combinations IFRS 3

27 Business combinations IFRS 3 A Key points When businesses are taken over or merged there are many possible ways of accounting. Mergers are banned it is considered there will always be a dominant acquirer.

27 Business combinations IFRS 3 A Key points When businesses are taken over or merged there are many possible ways of accounting. Mergers are banned it is considered there will always be a dominant acquirer.

How To Calculate Cash Flow From Operating Activities

Lawson Software, Inc. 10 Q Quarterly report pursuant to sections 13 or 15(d) Filed on 10/8/2009 Filed Period 8/31/2009 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10 Q

Lawson Software, Inc. 10 Q Quarterly report pursuant to sections 13 or 15(d) Filed on 10/8/2009 Filed Period 8/31/2009 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10 Q

IFRS news. IFRS 3R and IAS 27R questions and answers. Emerging issues and practical guidance* *connectedthinking PRINT CONTINUED

IFRS news Emerging issues and practical guidance* Supplement July/August 2009 IFRS 3R and IAS 27R questions and answers The revised standards on business combinations and consolidation (IFRS 3 (revised)

IFRS news Emerging issues and practical guidance* Supplement July/August 2009 IFRS 3R and IAS 27R questions and answers The revised standards on business combinations and consolidation (IFRS 3 (revised)

Tax Accounting Services. Goodwill impairment testing: Tax considerations

Tax Accounting Services Goodwill impairment testing: Tax considerations In financial accounting, goodwill is an asset representing the future economic benefits arising from other assets acquired in a business

Tax Accounting Services Goodwill impairment testing: Tax considerations In financial accounting, goodwill is an asset representing the future economic benefits arising from other assets acquired in a business

March 2012. Tax accounting services: Key areas of focus when accounting for income taxes during interim periods

March 2012 Tax accounting services: Key areas of focus when accounting for income taxes during interim periods Tax accounting services About this paper At the close of every quarter, companies recognize

March 2012 Tax accounting services: Key areas of focus when accounting for income taxes during interim periods Tax accounting services About this paper At the close of every quarter, companies recognize

INDEX TO FINANCIAL STATEMENTS. Balance Sheets as of June 30, 2015 and December 31, 2014 (Unaudited) F-2

F-2") INDEX TO FINANCIAL STATEMENTS Page Financial Statements Balance Sheets as of and December 31, 2014 (Unaudited) F-2 Statements of Operations for the three months ended and 2014 (Unaudited) F-3 Statements

INDEX TO FINANCIAL STATEMENTS Page Financial Statements Balance Sheets as of and December 31, 2014 (Unaudited) F-2 Statements of Operations for the three months ended and 2014 (Unaudited) F-3 Statements

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Accounting for Multiple Entities

King Saud University College of Administrative Science Department of Accounting 2 nd Semester, 1426-1427 Accounting for Multiple Entities Chapter 15 Prepared By: Eman Al-Aqeel Professor : Dr: Amal Fouda

King Saud University College of Administrative Science Department of Accounting 2 nd Semester, 1426-1427 Accounting for Multiple Entities Chapter 15 Prepared By: Eman Al-Aqeel Professor : Dr: Amal Fouda

Financial Issue 2010-7 Instruments, Structured

Financial Issue 2010-7 Instruments, Structured October 8, 2010 Products and Real Estate (FSR) Capital Markets Accounting Developments Advisory Issue 2010-8 December 13, 2010 Analysis of ASU 2010-20 Disclosures

Financial Issue 2010-7 Instruments, Structured October 8, 2010 Products and Real Estate (FSR) Capital Markets Accounting Developments Advisory Issue 2010-8 December 13, 2010 Analysis of ASU 2010-20 Disclosures

INTERAGENCY SUPERVISORY GUIDANCE ON BARGAIN PURCHASES AND FDIC- AND NCUA-ASSISTED ACQUISITIONS. June 7, 2010

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of Thrift Supervision INTERAGENCY

Office of the Comptroller of the Currency Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of Thrift Supervision INTERAGENCY

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

Pharmaceutical and Life Sciences Industry Alert. Disposals seller accounting for contingent consideration

www.pwc.com Stay Informed Pharmaceutical and Life Sciences Industry Alert 2014-5 Disposals seller accounting for contingent consideration Background Contingent consideration arrangements in acquisitions

www.pwc.com Stay Informed Pharmaceutical and Life Sciences Industry Alert 2014-5 Disposals seller accounting for contingent consideration Background Contingent consideration arrangements in acquisitions

08FR-003 Business Combinations IFRS 3 revised 11 January 2008. Key points

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

Business Combinations and Consolidated Financial Reporting. Course #6660/QAS6660 Course Material

Business Combinations and Consolidated Financial Reporting Course #6660/QAS6660 Course Material Business Combinations and Consolidated Financial Reporting (Course #6660/QAS6660) Table of Contents Page

Business Combinations and Consolidated Financial Reporting Course #6660/QAS6660 Course Material Business Combinations and Consolidated Financial Reporting (Course #6660/QAS6660) Table of Contents Page

FINANCIAL SUPPLEMENT December 31, 2015

FINANCIAL SUPPLEMENT December 31, 2015 Monster Worldwide, Inc. (together with its consolidated subsidiaries, the Company, Monster, we, our or us ) provides this supplement to assist investors in evaluating

FINANCIAL SUPPLEMENT December 31, 2015 Monster Worldwide, Inc. (together with its consolidated subsidiaries, the Company, Monster, we, our or us ) provides this supplement to assist investors in evaluating

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Business Combinations

Compiled AASB Standard AASB 3 Business Combinations This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013. Early application is permitted.

Compiled AASB Standard AASB 3 Business Combinations This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013. Early application is permitted.

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 June 10, 2015 What's inside Bankruptcy period considerations...

Mergers & acquisitions a snapshot Changing the way you think about tomorrow s deals Stay ahead of the accounting and reporting standards for M&A 1 June 10, 2015 What's inside Bankruptcy period considerations...

Purchase Price Allocations Under ASC 805: A Guide to Allocating Purchase Price for Business Combinations

CERTIFIED PUBLIC ACCOUNTANTS, FORENSIC AND FINANCIAL CONSULTANTS Purchase Price Allocations Under ASC 805: A Guide to Allocating Purchase Price for Business Combinations CERTIFIED PUBLIC ACCOUNTANTS, FORENSIC

CERTIFIED PUBLIC ACCOUNTANTS, FORENSIC AND FINANCIAL CONSULTANTS Purchase Price Allocations Under ASC 805: A Guide to Allocating Purchase Price for Business Combinations CERTIFIED PUBLIC ACCOUNTANTS, FORENSIC

MATRIX IT LTD. AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

Statement of Financial Accounting Standards No. 142

Statement of Financial Accounting Standards No. 142 FAS142 Status Page FAS142 Summary Goodwill and Other Intangible Assets June 2001 Financial Accounting Standards Board of the Financial Accounting Foundation

Statement of Financial Accounting Standards No. 142 FAS142 Status Page FAS142 Summary Goodwill and Other Intangible Assets June 2001 Financial Accounting Standards Board of the Financial Accounting Foundation

US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates

www.pwc.gr US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates 13 January 2014 Training Agenda 1. Accounting for long term debt 2. Capitalization of interest cost

www.pwc.gr US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates 13 January 2014 Training Agenda 1. Accounting for long term debt 2. Capitalization of interest cost

Notes to the Consolidated Financial Statements

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Stock based compensation guidance to increase income statement volatility (see update note below)

") Stock based compensation guidance to increase income statement volatility (see update note below) No. US2016 03 April 19, 2016 (Revised April 25, 2016) What s inside: Background. 1 Key provisions 2 Income

Stock based compensation guidance to increase income statement volatility (see update note below) No. US2016 03 April 19, 2016 (Revised April 25, 2016) What s inside: Background. 1 Key provisions 2 Income

Business Combinations

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

Investments and advances... 313,669

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Investments and advances... 344,499

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

UNITED STATES SECURITIES AND EXCHANGE COMMISSION. Washington, D.C. 20549 FORM 10-Q

È UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

È UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Consolidated financial statements of MTY Food Group Inc. November 30, 2015 and 2014

Consolidated financial statements of MTY Food Group Inc. Independent auditor s report...1 2 Consolidated statements of income... 3 Consolidated statements of comprehensive income... 4 Consolidated statements

Consolidated financial statements of MTY Food Group Inc. Independent auditor s report...1 2 Consolidated statements of income... 3 Consolidated statements of comprehensive income... 4 Consolidated statements

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS. Year ended December 31, 2012

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

Business combinations

Financial reporting developments A comprehensive guide Business combinations October 2015 To our clients and other friends Companies that engage in business combinations face various financial reporting

Financial reporting developments A comprehensive guide Business combinations October 2015 To our clients and other friends Companies that engage in business combinations face various financial reporting

Statement of Financial Accounting Standards No. 25. Statement of Financial Accounting Standards No.25. Business Combinations

Statement of Financial Accounting Standards No. 25 Statement of Financial Accounting Standards No.25 Business Combinations Revised on 30 November 2006 Translated by Ling-Tai Lynette Chou, Professor (National

Statement of Financial Accounting Standards No. 25 Statement of Financial Accounting Standards No.25 Business Combinations Revised on 30 November 2006 Translated by Ling-Tai Lynette Chou, Professor (National

ASPE AT A GLANCE Financial Statement Presentation1

ASPE AT A GLANCE Financial Statement Presentation1 December 2014 Financial Statement Presentation 1 OVERALL CONSIDERATIONS Effective Date Fiscal years beginning on or after January 1, 2011 2 FAIR PRESENTATION

ASPE AT A GLANCE Financial Statement Presentation1 December 2014 Financial Statement Presentation 1 OVERALL CONSIDERATIONS Effective Date Fiscal years beginning on or after January 1, 2011 2 FAIR PRESENTATION

5N PLUS INC. Condensed Interim Consolidated Financial Statements (Unaudited) For the three month periods ended March 31, 2016 and 2015 (in thousands

For the three month periods ended March 31, 2016 and 2015 (in thousands") Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

ADOBE SYSTEMS INCORPORATED (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 (Mark One) FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 (Mark One) FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

Private Company Reporting: Accounting for Goodwill

Private Company Reporting: Accounting for Goodwill Table of Contents EXECUTIVE SUMMARY... 3 SCOPE... 3 DEFINITION OF PUBLIC BUSINESS ENTITY... 3 RECOGNITION & MEASUREMENT... 4 AMORTIZATION OF GOODWILL...

Private Company Reporting: Accounting for Goodwill Table of Contents EXECUTIVE SUMMARY... 3 SCOPE... 3 DEFINITION OF PUBLIC BUSINESS ENTITY... 3 RECOGNITION & MEASUREMENT... 4 AMORTIZATION OF GOODWILL...

Comments on the Request for Information Post-implementation Review: IFRS 3 Business Combinations

The Japanese Institute of Certified Public Accountants 4-4-1, Kudan-Minami, Chiyoda-ku, Tokyo 102-8264 JAPAN Phone: +81-3-3515-1130 Fax: +81-3-5226-3355 e-mail: kigyokaikei@jicpa.or.jp http://www.hp.jicpa.or.jp/english/

The Japanese Institute of Certified Public Accountants 4-4-1, Kudan-Minami, Chiyoda-ku, Tokyo 102-8264 JAPAN Phone: +81-3-3515-1130 Fax: +81-3-5226-3355 e-mail: kigyokaikei@jicpa.or.jp http://www.hp.jicpa.or.jp/english/

Practical guide to IFRS

pwc.com/ifrs Practical guide to IFRS The art and science of contingent consideration in a business combination February 2012 Contents Introduction 1 Practical questions and examples 3 1 Initial classification

pwc.com/ifrs Practical guide to IFRS The art and science of contingent consideration in a business combination February 2012 Contents Introduction 1 Practical questions and examples 3 1 Initial classification

Proposed Statement of Financial Accounting Standards

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

YAHOO INC FORM 10-Q. (Quarterly Report) Filed 08/07/15 for the Period Ending 06/30/15

Filed 08/07/15 for the Period Ending 06/30/15") YAHOO INC FORM 10-Q (Quarterly Report) Filed 08/07/15 for the Period Ending 06/30/15 Address YAHOO! INC. 701 FIRST AVENUE SUNNYVALE, CA 94089 Telephone 4083493300 CIK 0001011006 Symbol YHOO SIC Code 7373

YAHOO INC FORM 10-Q (Quarterly Report) Filed 08/07/15 for the Period Ending 06/30/15 Address YAHOO! INC. 701 FIRST AVENUE SUNNYVALE, CA 94089 Telephone 4083493300 CIK 0001011006 Symbol YHOO SIC Code 7373

Net sales Operating income Ordinary income

Consolidated Financial Statements Summary May 10, 2016 (For the year ended March 31, 2016) English translation from the original Japanese-language document (All financial information has been prepared

Consolidated Financial Statements Summary May 10, 2016 (For the year ended March 31, 2016) English translation from the original Japanese-language document (All financial information has been prepared

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Mar 30, Mar 29, 2014 2015 Net system sales 1,030.0 1,246.5 Net service and field option sales 366.5 403.4 Total net

ASML - Summary IFRS Consolidated Statement of Profit or Loss 1,2 Three months ended, Mar 30, Mar 29, 2014 2015 Net system sales 1,030.0 1,246.5 Net service and field option sales 366.5 403.4 Total net

Mc Graw Hill Education

Fundamentals of Advanced Accounting Sixth Edition Joe B. Hoyle Associate Professor of Accounting Robins School of Business University of Richmond Thomas F. Schaefer KPMG Professor of Accountancy Mendoza

Fundamentals of Advanced Accounting Sixth Edition Joe B. Hoyle Associate Professor of Accounting Robins School of Business University of Richmond Thomas F. Schaefer KPMG Professor of Accountancy Mendoza

Summary Comparison of Part II of the CICA Handbook Accounting

Summary Comparison the CICA Accounting to XFI Version in Part V As December 31, 2009 1. This comparison has been prepared by the staff the Accounting Standards Board (AcSB) and has not been approved by

Summary Comparison the CICA Accounting to XFI Version in Part V As December 31, 2009 1. This comparison has been prepared by the staff the Accounting Standards Board (AcSB) and has not been approved by

Business Combinations and Noncontrolling Interests

Business Combinations and Noncontrolling Interests Q4 2009 Disclosure Analysis An Overview of Results and Observations PwC Business Combinations and Noncontrolling Interests Q4 2009 Disclosure Analysis

Business Combinations and Noncontrolling Interests Q4 2009 Disclosure Analysis An Overview of Results and Observations PwC Business Combinations and Noncontrolling Interests Q4 2009 Disclosure Analysis

136 ST ENGINEERING / ABOVE & BEYOND

136 ST ENGINEERING / ABOVE & BEYOND Independent auditors report Members of the Company Singapore Technologies Engineering Ltd Report on the financial STATEMENTS We have audited the accompanying financial

136 ST ENGINEERING / ABOVE & BEYOND Independent auditors report Members of the Company Singapore Technologies Engineering Ltd Report on the financial STATEMENTS We have audited the accompanying financial

THERATECHNOLOGIES INC.

Interim Consolidated Financial Statements of (In thousands of Canadian dollars) THERATECHNOLOGIES INC. Table of Contents Page Interim Consolidated Financial Positions 1 Interim Consolidated Statements

Interim Consolidated Financial Statements of (In thousands of Canadian dollars) THERATECHNOLOGIES INC. Table of Contents Page Interim Consolidated Financial Positions 1 Interim Consolidated Statements

New approaches regarding business combinations

MPRA Munich Personal RePEc Archive New approaches regarding business combinations Cristina Aurora Bunea-Bontaş and Mihaela Cosmina Petre May 2009 Online at http://mpra.ub.uni-muenchen.de/18133/ MPRA Paper

MPRA Munich Personal RePEc Archive New approaches regarding business combinations Cristina Aurora Bunea-Bontaş and Mihaela Cosmina Petre May 2009 Online at http://mpra.ub.uni-muenchen.de/18133/ MPRA Paper

Business Combinations Harry Klompas, CA Principal, Accounting Standards Board

Business Combinations Harry Klompas, CA Principal, Accounting Standards Board September 2005 Background Focus of Section 1581: eliminate pooling Goodwill and intangible changes were a consequence of this

Business Combinations Harry Klompas, CA Principal, Accounting Standards Board September 2005 Background Focus of Section 1581: eliminate pooling Goodwill and intangible changes were a consequence of this

IASB. Request for Views. Effective Dates and Transition Methods. International Accounting Standards Board

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

IASB International Accounting Standards Board Request for Views on Effective Dates and Transition Methods Respondents are asked to send their comments electronically to the IASB website (www.ifrs.org),

Almost Family Reports First Quarter 2016 Results

Exhibit 99.1 Almost Family, Inc. Steve Guenthner (502) 891-1000 FOR IMMEDIATE RELEASE Almost Family Reports First Quarter 2016 Results Louisville, KY, Almost Family, Inc. (Nasdaq: AFAM), a leading regional

Exhibit 99.1 Almost Family, Inc. Steve Guenthner (502) 891-1000 FOR IMMEDIATE RELEASE Almost Family Reports First Quarter 2016 Results Louisville, KY, Almost Family, Inc. (Nasdaq: AFAM), a leading regional

INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES, INCLUDING FAIR VALUE ACCOUNTING ESTIMATES, AND RELATED DISCLOSURES CONTENTS

INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES, INCLUDING FAIR VALUE ACCOUNTING ESTIMATES, AND RELATED DISCLOSURES (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES, INCLUDING FAIR VALUE ACCOUNTING ESTIMATES, AND RELATED DISCLOSURES (Effective for audits of financial statements for periods beginning

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS. Year ended December 31, 2011

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

Contacts: Media: Margaret Kirch Cohen, +1 312-696-6383 or margaret.cohen@morningstar.com Investors may submit questions to investors@morningstar.com.

Contacts: Media: Margaret Kirch Cohen, +1 312-696-6383 or margaret.cohen@morningstar.com Investors may submit questions to investors@morningstar.com. FOR IMMEDIATE RELEASE Morningstar, Inc. Reports First-Quarter

Contacts: Media: Margaret Kirch Cohen, +1 312-696-6383 or margaret.cohen@morningstar.com Investors may submit questions to investors@morningstar.com. FOR IMMEDIATE RELEASE Morningstar, Inc. Reports First-Quarter

Notes to the Consolidated Financial Statements

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

Similarities and differences. A comparison of full IFRS and IFRS for SMEs

Similarities and differences A comparison of full IFRS and PricewaterhouseCoopers IFRS and corporate governance publications and tools 2009 IFRS technical publications IFRS manual of accounting 2009 PwC

Similarities and differences A comparison of full IFRS and PricewaterhouseCoopers IFRS and corporate governance publications and tools 2009 IFRS technical publications IFRS manual of accounting 2009 PwC

U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009. 5B: Purchase Accounting Under GAAP & IFRS Part I (Advanced)

") U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009 5B: Purchase Accounting Under GAAP & IFRS Part I (Advanced) David L. White Purchase Accounting under GAAP and IFRS

U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009 5B: Purchase Accounting Under GAAP & IFRS Part I (Advanced) David L. White Purchase Accounting under GAAP and IFRS

Quarterly Report W E T H I N K L A S E R. 2nd Quarter Fiscal Year 2008. Jan. 1,2008 - Mar. 31, 2008. ROFIN-SINAR Technologies Inc.

W E T H I N K L A S E R Quarterly Report 2nd Quarter Fiscal Year 2008 Jan. 1,2008 - Mar. 31, 2008 ROFIN-SINAR Technologies Inc. NASDAQ: Prime Standard: RSTI ISIN US7750431022 UNITED STATES SECURITIES AND

W E T H I N K L A S E R Quarterly Report 2nd Quarter Fiscal Year 2008 Jan. 1,2008 - Mar. 31, 2008 ROFIN-SINAR Technologies Inc. NASDAQ: Prime Standard: RSTI ISIN US7750431022 UNITED STATES SECURITIES AND

Report on. 2010 Inspection of PricewaterhouseCoopers LLP (Headquartered in New York, New York) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION KYOCERA CORPORATION

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

eqube Gaming Limited Condensed Interim Consolidated Financial Statements For the Three and Nine Months Ended November 30, 2015 (Unaudited)

") Condensed Interim Consolidated Financial Statements For the Three and Nine Months Ended November 30, 2015 Notice to Reader The following interim consolidated financial statements and notes have not been

Condensed Interim Consolidated Financial Statements For the Three and Nine Months Ended November 30, 2015 Notice to Reader The following interim consolidated financial statements and notes have not been

IFRS compared to US GAAP: An overview

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA TABLE OF CONTENTS

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA TABLE OF CONTENTS Page Consolidated Statements of Income... 67 Consolidated Balance Sheets... 68 Consolidated Statements of Cash Flows... 69 Consolidated

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA TABLE OF CONTENTS Page Consolidated Statements of Income... 67 Consolidated Balance Sheets... 68 Consolidated Statements of Cash Flows... 69 Consolidated

LPL Financial LLC (SEC I.D. No. 8-17668)

") 75 State Street, 24th Floor Boston, MA 02109 2810 Coliseum Centre Drive Charlotte, NC 28217-4645 4707 Executive Drive San Diego, CA 92121-3091 LPL Financial LLC (SEC I.D. No. 8-17668) Statement of Financial

75 State Street, 24th Floor Boston, MA 02109 2810 Coliseum Centre Drive Charlotte, NC 28217-4645 4707 Executive Drive San Diego, CA 92121-3091 LPL Financial LLC (SEC I.D. No. 8-17668) Statement of Financial

Business Combinations

Compiled Accounting Standard AASB 3 Business Combinations This compilation was prepared on 6 March 2006 taking into account amendments made up to and including 22 June 2005. Prepared by the staff of the

Compiled Accounting Standard AASB 3 Business Combinations This compilation was prepared on 6 March 2006 taking into account amendments made up to and including 22 June 2005. Prepared by the staff of the

Verifone Reports Results for the Second Quarter of Fiscal 2016

Verifone Reports Results for the Second Quarter of Fiscal 2016 SAN JOSE, Calif. (BUSINESS WIRE) Verifone (NYSE: PAY), a world leader in payments and commerce solutions, today announced financial results

Verifone Reports Results for the Second Quarter of Fiscal 2016 SAN JOSE, Calif. (BUSINESS WIRE) Verifone (NYSE: PAY), a world leader in payments and commerce solutions, today announced financial results