LIST OF CONTENTS AND TABLES

|

|

|

- Hester Jacobs

- 7 years ago

- Views:

Transcription

1

2 LIST OF CONTENTS AND TABLES Fruit/vegetable Juice in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Off-trade Sales of Fruit/Vegetable Juice by Category: Volume Table 2 Off-trade Sales of Fruit/Vegetable Juice by Category: Value Table 3 Off-trade Sales of Fruit/Vegetable Juice by Category: % Volume Growth Table 4 Off-trade Sales of Fruit/Vegetable Juice by Category: % Value Growth Table 5 Leading Flavours for 100% Juice: % Volume Breakdown Table 6 Leading Flavours for Nectars (25-99% Juice): % Volume Breakdown Table 7 Leading Flavours for Juice Drinks (up to 24% Juice): % Volume Breakdown Table 8 % Share of Smoothies in 100% Juice and Nectars (25-99% Juice): Off-trade Value Table 9 Chilled Vs Ambient Reconstituted 100% Juice: % Analysis Table 10 Company Shares of Fruit/Vegetable Juice by Off-trade Volume Table 11 Brand Shares of Fruit/Vegetable Juice by Off-trade Volume Table 12 Company Shares of Fruit/Vegetable Juice by Off-trade Value Table 13 Brand Shares of Fruit/Vegetable Juice by Off-trade Value Table 14 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: Volume Table 15 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: Value Table 16 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: % Volume Growth Table 17 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: % Value Growth Fruit/vegetable Juice in South Korea - Company Profiles Haitai Beverage Co Ltd in Soft Drinks (south Korea) Strategic Direction Key Facts Summary 1 Haitai Beverage Co Ltd: Key Facts Summary 2 Haitai Beverage Co Ltd: Operational Indicators Company Background Production Summary 3 Haitai Beverage Co Ltd: Production Statistics

: % Volume Breakdown 2005-2010.")

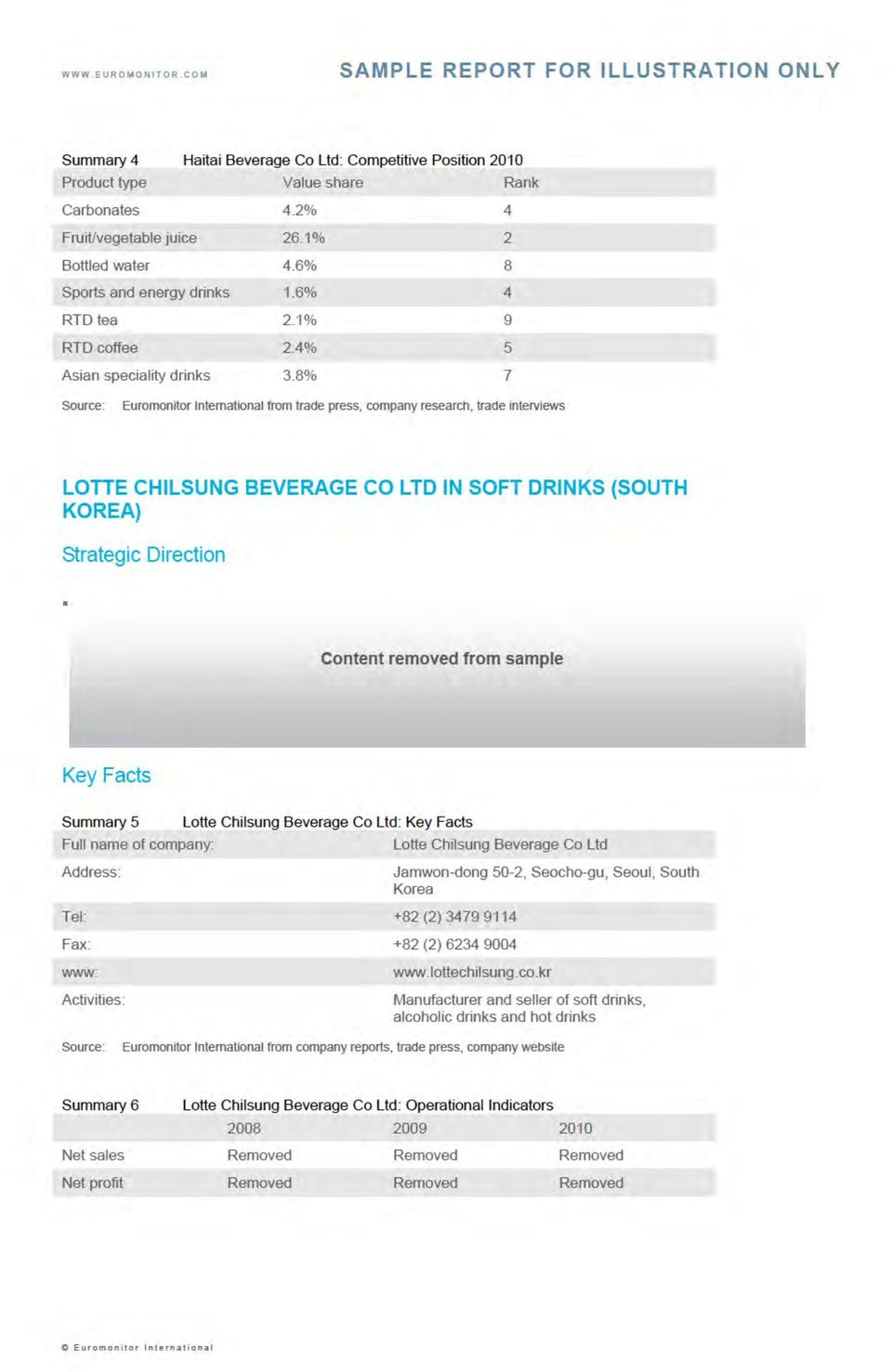

3 Competitive Positioning Summary 4 Haitai Beverage Co Ltd: Competitive Position Lotte Chilsung Beverage Co Ltd in Soft Drinks (south Korea) Strategic Direction Key Facts Summary 5 Lotte Chilsung Beverage Co Ltd: Key Facts Summary 6 Lotte Chilsung Beverage Co Ltd: Operational Indicators Company Background Production Summary 7 Lotte Chilsung Beverage Co Ltd: Production Statistics Competitive Positioning Summary 8 Lotte Chilsung Beverage Co Ltd: Competitive Position Woongjin Food Co Ltd in Soft Drinks (south Korea) Strategic Direction Key Facts Summary 9 Woongjin Food Co Ltd: Key Facts Summary 10 Woongjin Food Co Ltd: Operational Indicators Company Background Production Summary 11 Woongjin Food Co Ltd: Production Statistics Competitive Positioning Summary 12 Woongjin Food Co Ltd: Competitive Position Soft Drinks in South Korea - Industry Overview Executive Summary Premiumisation Leads Healthy Growth Health and Wellness Continues To Attract Consumers Two Leading Companies Maintain Positions sparkling Becomes Popular Soft Drinks Will See Rapid Growth But Rapid Change Key Trends and Developments Premiumisation Continues To Drive Growth sparkling Well Received by South Korean Consumers Leading Players Remain in Strong Positions Specialist Coffee Shops the Entry Channel for Premium Soft Drinks Marketing Strategies Through Smartphones Become Active Market Data Table 18 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: Volume Table 19 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: % Volume Growth Table 20 Off-trade vs On-trade Sales of Soft Drinks by Channel: Value Table 21 Off-trade vs On-trade Sales of Soft Drinks by Channel: % Value Growth Table 22 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Category: Volume

... 14 Strategic Direction... 14 Key Facts... 15 Summary 9 Woongjin Food Co Ltd: Key Facts.")

4 Table 23 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Category: % Volume Table 24 Off-trade vs On-trade Sales of Soft Drinks by Category: Value Table 25 Off-trade vs On-trade Sales of Soft Drinks by Category: % Value Table 26 Off-trade Sales of Soft Drinks (as sold) by Category: Volume Table 27 Off-trade Sales of Soft Drinks (as sold) by Category: % Volume Growth Table 28 Off-trade Sales of Soft Drinks by Category: Value Table 29 Off-trade Sales of Soft Drinks by Category: % Value Growth Table 30 Company Shares of Off-trade Soft Drinks (as sold) by Volume Table 31 Brand Shares of Off-trade Soft Drinks (as sold) by Volume Table 32 Company Shares of Off-trade Soft Drinks (RTD) by Volume Table 33 Brand Shares of Off-trade Soft Drinks (RTD) by Volume Table 34 Company Shares of Off-trade Soft Drinks by Value Table 35 Brand Shares of Off-trade Soft Drinks by Value Table 36 Off-trade Sales of Soft Drinks by Category and Distribution Format: % Analysis Table 37 Forecast Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: Volume Table 38 Forecast Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: % Volume Growth Table 39 Forecast Off-trade vs On-trade Sales of Soft Drinks by Channel: Value Table 40 Forecast Off-trade vs On-trade Sales of Soft Drinks by Channel: % Value Growth Table 41 Forecast Off-trade Sales of Soft Drinks (as sold) by Category: Volume Table 42 Forecast Off-trade Sales of Soft Drinks (as sold) by Category: % Volume Growth Table 43 Forecast Off-trade Sales of Soft Drinks by Category: Value Table 44 Forecast Off-trade Sales of Soft Drinks by Category: % Value Growth Appendix Fountain Sales in South Korea Data Table 45 Off-trade vs On-trade Fountain Sales of Soft Drinks: Volume Table 46 Off-trade vs On-trade Fountain Sales of Soft Drinks: % Volume Growth Table 47 Off-trade vs On-trade Fountain Sales of Carbonates: Volume Table 48 Off-trade vs On-trade Fountain Sales of Carbonates: % Volume Growth Table 49 Forecast Off-trade vs On-trade Fountain Sales of Soft Drinks: Volume

by Volume 2006-2010.")

5 Table 50 Forecast Off-trade vs On-trade Fountain Sales of Soft Drinks: % Volume Growth Table 51 Forecast Off-trade vs On-trade Fountain Sales of Carbonates: Volume Table 52 Forecast Off-trade vs On-trade Fountain Sales of Carbonates: % Volume Growth Definitions Summary 13 Research Sources... 38

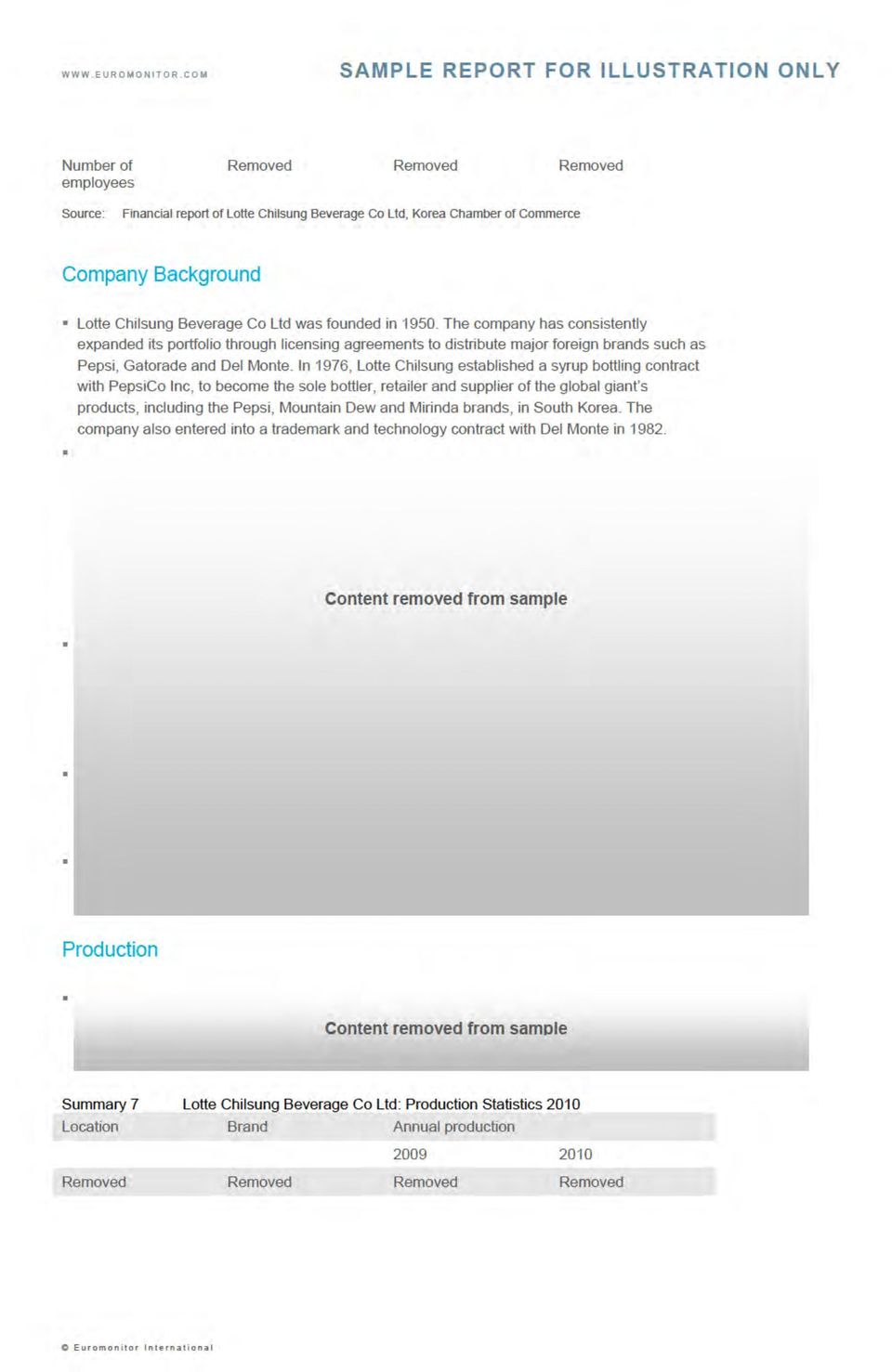

6 FRUIT/VEGETABLE JUICE IN SOUTH KOREA - CATEGORY ANALYSIS HEADLINES In 2010, sales increase by 1% in total current value terms and decrease by 2% in total volume terms Growth of chilled premium fruit/vegetable juice puts a brake on the overall decline in total fruit/vegetable juice sales Juice drinks excluding Asian posts the strongest performance, with sales rising by 5% in total value terms Average unit prices increase by 3% in 2010 in total value terms Lotte Chilsung Beverage Co Ltd maintains leading position with off-trade value share of 39% in 2010 Fruit/vegetable juice sales are expected to decline at a CAGR of 1% in total value and total volume terms over the forecast period TRENDS The premiumisation of fruit/vegetable juice accelerated in 2010 though fruit/vegetable juice market continued declining in Since 2004, the category has seen sales decline; however more fruit/vegetable juice manufacturers introduced chilled juices under reconstituted 100% juice in Chilled juices have been taking the place of existing fruit/vegetable juice, to account for an 11% share in terms of off-trade volume sales in Given the health and wellness trend, consumers preferred more natural fruit/vegetable juice and manufacturers also introduced various flavours of chilled fruit/vegetable juice to meet consumer demand. While general consumers preference for lighter and lower calorie drinks will bring continued market declining in fruit/vegetable juice in South Korea, chilled 100% fruit/vegetable juice will continue appealing to more health conscious South Korean consumers. With the popularity of chilled 100% juice in South Korea, the leading soft drinks manufacturer, Lotte Chilsung Beverage Co Ltd, renewed its Del Monte Cold brand, adding the flavour of Cheju Tangerine, which used to be sold as unfrozen nectar containing only 50% juice. The renewed Del Monte Cold is available through most grocery retailers, however the larger 950ml and 1.89-litre packs are mainly distributed through supermarkets/hypermarkets, while smaller 235ml packs tend to be distr buted through convenience stores. Every year since 2005, Asian juice drinks has seen a double-digit decline. The most popular flavours in Asian juice drinks in South Korea are plum juice and aloe juice. As more consumers become aware that these products contain high levels of sugar, diet-conscious consumers have shifted away from these products. With these trends, there have been no significant new product developments and the Asian juice drinks category is expected to continue its negative direction during the forecast period. Average unit prices increased by 3% in 2010 in total value terms, mainly due to a process of premiumisation. While most 100% juice is from reconstituted 100% juice, more South Korean

7 consumers look for better tasting juice and manufacturers have actively expanded chilled reconstituted 100% juice products during COMPETITIVE LANDSCAPE Lotte Chilsung Beverage Co Ltd maintained its leading position in fruit/vegetable juice in 2010 with a 39% off-trade value share. Reflecting the overall decline in the fruit/vegetable juice category, the company saw its volume and value sales decline in In addition, as competition in the chilled juice segment became intense, the company s value and volume share in fruit/vegetable juice was reduced by new manufacturers. In particular, the company showed a weak performance in juice drinks (up to 24% juice), with the continuing decline of Asian juice drinks in Due to the weak performance of Asian juice drinks, the company gradually discontinued their brands since PROSPECTS Although there is increasing demand for premium fruit/vegetable juice in South Korea, the category overall is not likely to recover to show positive growth during forecast period, with an annual 1% decline in off-trade value and volume sales expected. While fruit/vegetable juice is considered to be a healthy drink, because of its sometimes high sugar content, diet-conscious South Korean consumers still try to avoid it. Unless there are new products in development which appeal to young female consumers in their 20s and 30s, the negative performance is expected to continue.

8 CATEGORY DATA Table 1 Off-trade Sales of Fruit/Vegetable Juice by Category: Volume million litres 100% Juice - Frozen 100% Juice - Not from Concentrate 100% Juice - Reconstituted 100% Juice Juice Drinks (up to 24% Juice) - Asian Juice Drinks - Frozen Juice Drinks - Juice Drinks Excluding Asian Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) - Frozen Nectars - Unfrozen Nectars Fruit/Vegetable Juice Table 2 Off-trade Sales of Fruit/Vegetable Juice by Category: Value Won billion 100% Juice - Frozen 100% Juice - Not from Concentrate 100% Juice - Reconstituted 100% Juice Juice Drinks (up to 24% Juice) - Asian Juice Drinks - Frozen Juice Drinks - Juice Drinks Excluding Asian Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice)

- Asian Juice Drinks - Frozen Juice Drinks - Juice Drinks Excluding Asian Fruit-Flavoured Drinks (No Juice Content)")

9 - Frozen Nectars - Unfrozen Nectars Fruit/Vegetable Juice, Table 3 Off-trade Sales of Fruit/Vegetable Juice by Category: % Volume Growth % volume growth 100% Juice - Frozen 100% Juice - Not from Concentrate 100% Juice - Reconstituted 100% Juice Juice Drinks (up to 24% Juice) - Asian Juice Drinks - Frozen Juice Drinks - Juice Drinks Excluding Asian Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) - Frozen Nectars - Unfrozen Nectars Fruit/Vegetable Juice 2009/ CAGR 2005/10 TOTAL Table 4 Off-trade Sales of Fruit/Vegetable Juice by Category: % Value Growth % current value growth 100% Juice - Frozen 100% Juice - Not from Concentrate 100% Juice - Reconstituted 100% Juice Juice Drinks (up to 24% Juice) - Asian Juice Drinks - Frozen Juice Drinks - Juice Drinks Excluding Asian Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) - Frozen Nectars - Unfrozen Nectars Fruit/Vegetable Juice 2009/ CAGR 2005/10 TOTAL Table 5 Leading Flavours for 100% Juice: % Volume Breakdown % retail volume

Nectars (25-99% Juice) - Frozen Nectars - Unfrozen Nectars Fruit/Vegetable Juice 2009/10 2005-10 CAGR 2005/10")

10 Apple Carrot Grape Orange Tomato Vegetable Other flavours Total Table 6 Leading Flavours for Nectars (25-99% Juice): % Volume Breakdown % retail volume Grape Mango Orange Tangerine Tomato Other flavours Total Table 7 % retail volume Leading Flavours for Juice Drinks (up to 24% Juice): % Volume Breakdown Grape Guava Lemon Orange Plum Pomegranate Other flavours Total Table 8 % value analysis % Share of Smoothies in 100% Juice and Nectars (25-99% Juice): Off-trade Value 2010 Smoothies Others Total 100% Juice Nectars (25-99% Juice)

: % Volume Breakdown 2005-2010 2005 2006 2007 2008 2009 2010 Grape Guava Lemon Orange Plum Pomegranate")

11 Table 9 Chilled Vs Ambient Reconstituted 100% Juice: % Analysis % retail volume Chilled Juices Ambient Juices Total Table 10 Company Shares of Fruit/Vegetable Juice by Off-trade Volume % off-trade volume Company Total Table 11 Brand Shares of Fruit/Vegetable Juice by Off-trade Volume % off-trade volume Brand Company

12 Total Table 12 Company Shares of Fruit/Vegetable Juice by Off-trade Value % off-trade value rsp Company Total Table 13 Brand Shares of Fruit/Vegetable Juice by Off-trade Value % off-trade value rsp Brand Company

13 Total Table 14 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: Volume million litres 100% Juice Juice Drinks (up to 24% Juice) Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) Fruit/Vegetable Juice

14 Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 15 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: Value Won billion 100% Juice Juice Drinks (up to 24% Juice) Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) Fruit/Vegetable Juice Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 16 % volume growth Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: % Volume Growth / CAGR 2010/15 TOTAL 100% Juice Juice Drinks (up to 24% Juice) Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) Fruit/Vegetable Juice Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 17 Forecast Off-trade Sales of Fruit/Vegetable Juice by Category: % Value Growth % constant value growth 100% Juice Juice Drinks (up to 24% Juice) Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) Fruit/Vegetable Juice CAGR 2010/15 TOTAL Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources

Fruit-Flavoured Drinks (No Juice Content) Nectars (25-99% Juice) Fruit/Vegetable Juice Euromonitor")

15

16

17

18

19

20

21

22 SOFT DRINKS IN SOUTH KOREA - INDUSTRY OVERVIEW EXECUTIVE SUMMARY Premiumisation Leads Healthy Growth In 2010, soft drinks experienced healthy growth, registering a 6% increase in off-trade value sales and a 5% increase in off-trade volume sales, thanks to a premiumisation trend, especially within bottled water, fruit/vegetable juice, carbonates and RTD coffee. Imported and premium brands of bottled water, carbonated bottled water and fruit/vegetable juice recorded healthy growth rates. In the case of fruit/vegetable juice, the category continued to see declining volume sales but imported premium juice expanded its presence in South Korea. New flavours of carbonates and renewed brands without sugar and preservatives were also popular launches. However, RTD tea and Asian speciality drinks showed volume declines as they fell out of fashion. Health and Wellness Continues To Attract Consumers With the growing health and wellness trend, healthy concepts remained popular among South Korean consumers. In particular, various vitamins have been used to target different consumer groups and manufacturers have highlighted the varied functions of different vitamins in their products, targeting sophisticated South Korean consumers. Vitamin B has been marketed for its anti-ageing properties. Vitamin C and collagen remained among the favourite ingredients for skin health. At the same time, manufacturers tried to strengthen healthy brands through advertising, the shape of packaging and using brand names to appeal to a sophisticated South Korean consumer base. Two Leading Companies Maintain Positions Lotte Chilsung Beverage Co Ltd and Coca-Cola Korea Co maintained the two leading positions in 2010, accounting for a 48% combined share in off-trade value terms. Lotte Chilsung remained in the leading position with 33% of off-trade value sales in The company strengthened its product portfolio, launching premium fruit/vegetable juice and sports drinks and renewing its well-known carbonates and flavoured bottled water lines, recording a positive growth rate although a decline in share. Coca-Cola Korea also introduced a smaller version of its Coca-Cola brand, Mini Coke, which proved popular among younger consumers. sparkling Becomes Popular In 2010, sparkling was a popular concept within soft drinks. South Koreans generally perceive sparkling drinks to be less healthy, a traditional perception associated with carbonates. However, carbonates have seen continued positive growth since 2008, despite the health and wellness trend. Growing numbers of South Korean consumers looking for refreshing carbonated options in soft drinks have become apparent. New product developments, presented as sparkling versions of fruit/vegetable juice and RTD tea, were introduced during Carbonated bottled water experienced strong growth in Furthermore, manufacturers offered health-positioned drinks in a carbonated format to attract consumers who are sensitive to their health needs.

23 Soft Drinks Will See Rapid Growth But Rapid Change KEY TRENDS AND DEVELOPMENTS Premiumisation Continues To Drive Growth Current Impact Outlook

24 Future Impact sparkling Well Received by South Korean Consumers Current Impact Outlook

25 Future Impact Leading Players Remain in Strong Positions Current Impact Outlook

26 Future Impact Specialist Coffee Shops the Entry Channel for Premium Soft Drinks Current Impact Outlook

27 Future Impact Marketing Strategies Through Smartphones Become Active Current Impact Outlook Future Impact

28 MARKET DATA Table 1 million litres OFF-trade ON-trade Total Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: Volume Note: Excludes powder concentrates Table 2 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: % Volume Growth % volume growth OFF-trade ON-trade Total 2009/ CAGR 2005/10 TOTAL Note: Excludes powder concentrates Table 3 Off-trade vs On-trade Sales of Soft Drinks by Channel: Value Won billion OFF-trade ON-trade Total Table 4 Off-trade vs On-trade Sales of Soft Drinks by Channel: % Value Growth % current value growth OFF-trade ON-trade Total 2009/ CAGR 2005/10 TOTAL

29 Table 5 million litres Off-trade vs On-trade Sales of Soft Drinks (as sold) by Category: Volume 2010 Off-trade On-trade TOTAL Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Note: Excludes powder concentrates Table 6 Off-trade vs On-trade Sales of Soft Drinks (as sold) by Category: % Volume 2010 % volume analysis Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Off-trade On-trade Total Note: Excludes powder concentrates Table 7 Off-trade vs On-trade Sales of Soft Drinks by Category: Value 2010 Won billion Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Off-trade On-trade TOTAL

30 Table 8 Off-trade vs On-trade Sales of Soft Drinks by Category: % Value 2010 % value analysis Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Off-trade On-trade Total Table 9 Off-trade Sales of Soft Drinks (as sold) by Category: Volume million litres Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Note: Excludes powder concentrates Table 10 Off-trade Sales of Soft Drinks (as sold) by Category: % Volume Growth % volume growth Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks 2009/ CAGR 2005/10 TOTAL Note: Excludes powder concentrates Table 11 Off-trade Sales of Soft Drinks by Category: Value

31 Won billion Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Table 12 Off-trade Sales of Soft Drinks by Category: % Value Growth % current value growth Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks 2009/ CAGR 2005/10 TOTAL Table 13 Company Shares of Off-trade Soft Drinks (as sold) by Volume % off-trade volume Company

32 Total Note: Excludes powder concentrates Table 14 Brand Shares of Off-trade Soft Drinks (as sold) by Volume % off-trade volume Brand Company

33 Total Note: Excludes powder concentrates Table 15 Company Shares of Off-trade Soft Drinks (RTD) by Volume % off-trade volume Company Others Total

34 Table 16 Brand Shares of Off-trade Soft Drinks (RTD) by Volume % off-trade volume Brand Company

35 Total Table 17 Company Shares of Off-trade Soft Drinks by Value % off-trade value rsp Company Total Table 18 Brand Shares of Off-trade Soft Drinks by Value % off-trade value rsp Brand Company

36 Others Total Table 19 Off-trade Sales of Soft Drinks by Category and Distribution Format: % Analysis 2010

37 % off-trade BW C Con F/VJ RTD C RTD T Store-Based Retailing Grocery Retailers Supermarkets/Hypermarkets Discounters Small Grocery Retailers Convenience Stores Independent Small Grocers Forecourt Retailers Other Grocery Retailers Non-Grocery Retailers Non-Store Retailing Vending Homeshopping Internet Retailing Direct Selling Total SED ASD Store-Based Retailing Grocery Retailers Supermarkets/Hypermarkets Discounters Small Grocery Retailers Convenience Stores Independent Small Grocers Forecourt Retailers Other Grocery Retailers Non-Grocery Retailers Non-Store Retailing Vending Homeshopping Internet Retailing Direct Selling Total Key: Note: BW = bottled water; C = carbonates; Con = concentrates; F/VJ = fruit/vegetable juice; RTD C = RTD coffee; RTD T = RTD tea; SED = sports and energy drinks; ASD = Asian speciality drinks Excludes powder concentrates Table 20 Forecast Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: Volume million litres OFF-trade ON-trade Total Note: Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Excludes powder concentrates

38 Table 21 Forecast Off-trade vs On-trade Sales of Soft Drinks (as sold) by Channel: % Volume Growth % volume growth OFF-trade ON-trade Total 2014/ CAGR 2010/15 TOTAL Note: Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Excludes powder concentrates Table 22 Forecast Off-trade vs On-trade Sales of Soft Drinks by Channel: Value Won billion OFF-trade ON-trade Total Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 23 Forecast Off-trade vs On-trade Sales of Soft Drinks by Channel: % Value Growth % current value growth OFF-trade ON-trade Total 2014/ CAGR 2010/15 TOTAL Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 24 Forecast Off-trade Sales of Soft Drinks (as sold) by Category: Volume million litres Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Note: Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Excludes powder concentrates

39 Table 25 % volume growth Forecast Off-trade Sales of Soft Drinks (as sold) by Category: % Volume Growth / CAGR 2010/15 TOTAL Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Note: Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Excludes powder concentrates Table 26 Forecast Off-trade Sales of Soft Drinks by Category: Value Won billion Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources Table 27 Forecast Off-trade Sales of Soft Drinks by Category: % Value Growth % constant value growth Bottled Water Carbonates Concentrates Fruit/Vegetable Juice RTD Coffee RTD Tea Sports and Energy Drinks Asian Speciality Drinks Soft Drinks CAGR 2010/15 TOTAL Euromonitor International from trade associations, trade press, company research, trade interviews, trade sources

40 APPENDIX Fountain Sales in South Korea Trends Fountain sales continued positive growth in on-trade volume terms while fountain on-trade volume sales through convenience stores declined during In South Korea, most fountain sales occurred in the foodservice channel, which accounted for a 97% share of total fountain volume sales in Fountain sales through convenience stores tend to be subject to seasonality, with demand being higher in summer. As such, few convenience stores offer fountain sales for soft drinks in South Korea. In addition, most convenience stores are limited in their selling space, making it increasingly difficult to site the fountains on the premises. Only a small number around school zones tend to offer fountain sales. DATA Table 28 Off-trade vs On-trade Fountain Sales of Soft Drinks: Volume million litres OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total

41 Note: Total fountain on-trade volume data included in on-trade Table 29 Off-trade vs On-trade Fountain Sales of Soft Drinks: % Volume Growth % fountain volume growth OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total 2009/ CAGR 2005/10 TOTAL Note: Total fountain on-trade volume data included in on-trade Table 30 Off-trade vs On-trade Fountain Sales of Carbonates: Volume million litres OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total Note: Total fountain on-trade volume data included in on-trade Table 31 Off-trade vs On-trade Fountain Sales of Carbonates: % Volume Growth % fountain volume growth OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total 2009/ CAGR 2005/10 TOTAL Note: Total fountain on-trade volume data included in on-trade

42 Table 32 Forecast Off-trade vs On-trade Fountain Sales of Soft Drinks: Volume million litres OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total,,,,,, Note: Total fountain on-trade volume data included in on-trade Table 33 Forecast Off-trade vs On-trade Fountain Sales of Soft Drinks: % Volume Growth % fountain volume growth OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total 2014/ CAGR 2010/15 TOTAL Note: Total fountain on-trade volume data included in on-trade Table 34 Forecast Off-trade vs On-trade Fountain Sales of Carbonates: Volume million litres OFF-trade ON-trade Fountain ON-trade volume through c-store Fountain ON-trade volume through food store Total fountain ON-trade volume Total 2, , , , , ,612.6 Note: Total fountain on-trade volume data included in on-trade

43

44

45

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Rtd Coffee in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Off-trade Sales of : Volume

LIST OF CONTENTS AND TABLES Rtd Coffee in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Off-trade Sales of : Volume

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Sports and Energy Drinks in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Still vs Carbonated

LIST OF CONTENTS AND TABLES Sports and Energy Drinks in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Still vs Carbonated

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Bottled Water in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Institutional Bottled Water Sales...

LIST OF CONTENTS AND TABLES Bottled Water in South Korea - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Institutional Bottled Water Sales...

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Soft Drinks in South Korea - Industry Overview... 1 Executive Summary... 1 Premiumisation Leads Healthy Growth... 1 Health and Wellness Continues To Attract Consumers... 1 Two

LIST OF CONTENTS AND TABLES Soft Drinks in South Korea - Industry Overview... 1 Executive Summary... 1 Premiumisation Leads Healthy Growth... 1 Health and Wellness Continues To Attract Consumers... 1 Two

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES in Morocco - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Machine Sales: 2005-2010... 4 Table 2 Retail

LIST OF CONTENTS AND TABLES in Morocco - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Machine Sales: 2005-2010... 4 Table 2 Retail

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Dog Food in Taiwan - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Indicators... 4 Table 1 Dog Owning Households: % Analysis

LIST OF CONTENTS AND TABLES Dog Food in Taiwan - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Indicators... 4 Table 1 Dog Owning Households: % Analysis

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Away-from-home Tissue and Hygiene in Thailand - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Away-From-Home

LIST OF CONTENTS AND TABLES Away-from-home Tissue and Hygiene in Thailand - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Away-From-Home

List of Contents and Tables

List of Contents and Tables HERBAL/TRADITIONAL PRODUCTS IN SWEDEN - CATEGORY ANALYSIS... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Products:

List of Contents and Tables HERBAL/TRADITIONAL PRODUCTS IN SWEDEN - CATEGORY ANALYSIS... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Products:

Bottled Water - Market Overview

Bottled Water - Market Overview July 2012 Disclaimer The following information is offered in good faith and represents an unqualified interpretation of a range of industry commentary and market data. It

Bottled Water - Market Overview July 2012 Disclaimer The following information is offered in good faith and represents an unqualified interpretation of a range of industry commentary and market data. It

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Mobile Phones in the Netherlands - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Sales of Mobile Phones:

LIST OF CONTENTS AND TABLES Mobile Phones in the Netherlands - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Sales of Mobile Phones:

Functional Drinks in Brazil

Brochure More information from http://www.researchandmarkets.com/reports/64306/ Functional Drinks in Brazil Description: In 2008, Coca-Cola launched i9 Hidrotônico in lemon flavour. Targeted at young consumers,

Brochure More information from http://www.researchandmarkets.com/reports/64306/ Functional Drinks in Brazil Description: In 2008, Coca-Cola launched i9 Hidrotônico in lemon flavour. Targeted at young consumers,

25.02.2013. Russian juice market analysis

25.02.2013 Russian juice market analysis Russian concentrate market Concentrates increases in off-trade RTD volume by 3% and in off-trade value by 14% in 2011 Powder concentrates increases by 1% in off-trade

25.02.2013 Russian juice market analysis Russian concentrate market Concentrates increases in off-trade RTD volume by 3% and in off-trade value by 14% in 2011 Powder concentrates increases by 1% in off-trade

List of Contents and Tables

List of Contents and Tables PERSONAL GOODS IN SWEDEN... 1 Executive Summary... 1 Sales of Personal Goods Unaffected by Global Crisis... 1 Sales in More Sectors Driven by Well-known Brands... 1 Swedish

List of Contents and Tables PERSONAL GOODS IN SWEDEN... 1 Executive Summary... 1 Sales of Personal Goods Unaffected by Global Crisis... 1 Sales in More Sectors Driven by Well-known Brands... 1 Swedish

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Direct Selling in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 1 Prospects... 2 Channel Data... 2 Table 1 Direct Selling by Category: Value

LIST OF CONTENTS AND TABLES Direct Selling in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 1 Prospects... 2 Channel Data... 2 Table 1 Direct Selling by Category: Value

List of Contents and Tables

List of Contents and Tables ANALGESICS IN SWEDEN - CATEGORY ANALYSIS... 1 Headlines... 1 Trends... 1 Switches... 2 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Analgesics

List of Contents and Tables ANALGESICS IN SWEDEN - CATEGORY ANALYSIS... 1 Headlines... 1 Trends... 1 Switches... 2 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Analgesics

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Biscuits in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Biscuits by Category:

LIST OF CONTENTS AND TABLES Biscuits in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Biscuits by Category:

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Baby Care in the United Arab Emirates - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Baby

LIST OF CONTENTS AND TABLES Baby Care in the United Arab Emirates - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Baby

Changing Tastes The UK Soft Drinks Annual Report 2015

Changing Tastes The UK Soft Drinks Annual Report 2015 Changing tastes The number of consumers switching to low, no and mid calorie drinks in 2014 speaks volumes for industry s efforts to meet changing

Changing Tastes The UK Soft Drinks Annual Report 2015 Changing tastes The number of consumers switching to low, no and mid calorie drinks in 2014 speaks volumes for industry s efforts to meet changing

MSU Product Center Strategic Marketing Institute. The Market for Orange Juice Challenges and Opportunities. Getachew Abate

MSU Product Center Strategic Marketing Institute Working Paper 2-102605 The Market for Orange Juice Challenges and Opportunities Getachew Abate MSU Product Center For Agriculture and Natural Resources

MSU Product Center Strategic Marketing Institute Working Paper 2-102605 The Market for Orange Juice Challenges and Opportunities Getachew Abate MSU Product Center For Agriculture and Natural Resources

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Breakfast Cereals in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Breakfast Cereals

LIST OF CONTENTS AND TABLES Breakfast Cereals in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Category Data... 3 Table 1 Sales of Breakfast Cereals

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Pet Care in Taiwan - Industry Overview... 1 Executive Summary... 1 Market Size Booms Due To Higher Volume Growth and Increasing Unit Prices... 1 Pet Demographic Shift Leads

LIST OF CONTENTS AND TABLES Pet Care in Taiwan - Industry Overview... 1 Executive Summary... 1 Market Size Booms Due To Higher Volume Growth and Increasing Unit Prices... 1 Pet Demographic Shift Leads

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Oral Care in the United Arab Emirates - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 1 Prospects... 2 Category Data... 2 Table 1 Sales of Oral

LIST OF CONTENTS AND TABLES Oral Care in the United Arab Emirates - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 1 Prospects... 2 Category Data... 2 Table 1 Sales of Oral

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Internet in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Channel Data... 3 Table 1 Internet by Category: Value 2006-2011...

LIST OF CONTENTS AND TABLES Internet in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 2 Channel Data... 3 Table 1 Internet by Category: Value 2006-2011...

Marketing Business Case

Running head: Coca-Cola Company NEW MEXICO HIGHLANDS UNIVERSITY Marketing Business Case Coca-Cola Company Molina, Ines The Coca-Cola Company has an intensive distribution and bottlers systems that its

Running head: Coca-Cola Company NEW MEXICO HIGHLANDS UNIVERSITY Marketing Business Case Coca-Cola Company Molina, Ines The Coca-Cola Company has an intensive distribution and bottlers systems that its

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Health and Beauty Specialist Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Channel Data... 4 Table 1 Health

LIST OF CONTENTS AND TABLES Health and Beauty Specialist Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Channel Data... 4 Table 1 Health

Overview of the Korean alcoholic drink market - focusing on Spirits

Overview of the Korean alcoholic drink market - focusing on Spirits January, 2011 Agricultural office, Seoul 1. Market background 1) Legal drinking age In South Korea the legal drinking age is 19-years-old,

Overview of the Korean alcoholic drink market - focusing on Spirits January, 2011 Agricultural office, Seoul 1. Market background 1) Legal drinking age In South Korea the legal drinking age is 19-years-old,

Direct Selling in the US

Brochure More information from http://www.researchandmarkets.com/reports/1542416/ Direct Selling in the US Description: Value sales through direct selling increased by just 1% in 2014 amid struggles from

Brochure More information from http://www.researchandmarkets.com/reports/1542416/ Direct Selling in the US Description: Value sales through direct selling increased by just 1% in 2014 amid struggles from

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Chocolate Confectionery in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Chocolate

LIST OF CONTENTS AND TABLES Chocolate Confectionery in Argentina - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 3 Table 1 Sales of Chocolate

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Apparel Specialist Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Channel Formats... 3 Chart 1 Apparel Specialist Retailers: Stefanel in Padova... 3

LIST OF CONTENTS AND TABLES Apparel Specialist Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Channel Formats... 3 Chart 1 Apparel Specialist Retailers: Stefanel in Padova... 3

Grocery Retailers in Turkey

Brochure More information from http://www.researchandmarkets.com/reports/1668358/ Grocery Retailers in Turkey Description: Grocery retailers registers a slightly higher growth than 2013 in current value

Brochure More information from http://www.researchandmarkets.com/reports/1668358/ Grocery Retailers in Turkey Description: Grocery retailers registers a slightly higher growth than 2013 in current value

Successes, Challenges and Opportunities

Successes, Challenges and Opportunities Marge Leahy, PhD Director, Health and Wellness American Heart Association Added Sugars Conference May 5, 2010 The Coca-Cola Company and the Beverage Industry The

Successes, Challenges and Opportunities Marge Leahy, PhD Director, Health and Wellness American Heart Association Added Sugars Conference May 5, 2010 The Coca-Cola Company and the Beverage Industry The

PASTA IN EUROPE: OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS

PASTA IN EUROPE: OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS UNAFPA/SEMOULIERS AND IPO BOARD MEETING 23 MAY 2014 - LYON ILDIKO SZALAI SENIOR ANALYST EUROMONITOR INTERNATIONAL About Euromonitor International

PASTA IN EUROPE: OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS UNAFPA/SEMOULIERS AND IPO BOARD MEETING 23 MAY 2014 - LYON ILDIKO SZALAI SENIOR ANALYST EUROMONITOR INTERNATIONAL About Euromonitor International

Grocery Retailers in Hungary

Brochure More information from http://www.researchandmarkets.com/reports/1830115/ Grocery Retailers in Hungary Description: 2014 was the first full financial year in which the tobacco retailing system

Brochure More information from http://www.researchandmarkets.com/reports/1830115/ Grocery Retailers in Hungary Description: 2014 was the first full financial year in which the tobacco retailing system

IRI Pulse Report Drinks

IRI Pulse Report Drinks Welcome to the Pulse H1 2015 edition for drinks. We hope you find it useful. Please do not hesitate to contact us if you have any questions or comments at EU.Marketing@IRIworldwide.com.

IRI Pulse Report Drinks Welcome to the Pulse H1 2015 edition for drinks. We hope you find it useful. Please do not hesitate to contact us if you have any questions or comments at EU.Marketing@IRIworldwide.com.

Goldman Sachs JBWere Private Wealth Management Forum 2006 Terry Davis Managing Director, CCA

Goldman Sachs JBWere Private Wealth Management Forum 2006 Terry Davis Managing Director, CCA 11 April 2006 1 Consistent delivery continues in margins, EPS and dividends Sales & EBIT % 1 Earnings per share

Goldman Sachs JBWere Private Wealth Management Forum 2006 Terry Davis Managing Director, CCA 11 April 2006 1 Consistent delivery continues in margins, EPS and dividends Sales & EBIT % 1 Earnings per share

Coca Cola Research Paper and SWOT Analysis

Coca Cola Research Paper and SWOT Analysis 1. Background and History Coca-Cola s history dates back to the late 1800s when Atlanta pharmacist John Pemberton mixed caramel-colored syrup with carbonated

Coca Cola Research Paper and SWOT Analysis 1. Background and History Coca-Cola s history dates back to the late 1800s when Atlanta pharmacist John Pemberton mixed caramel-colored syrup with carbonated

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Apparel in Ukraine - Industry Overview... 1 Executive Summary... 1 Recovery of Apparel Market Begins... 1 Slow Shift Towards Modern Retail... 1 State Focuses on Unofficial Imports...

LIST OF CONTENTS AND TABLES Apparel in Ukraine - Industry Overview... 1 Executive Summary... 1 Recovery of Apparel Market Begins... 1 Slow Shift Towards Modern Retail... 1 State Focuses on Unofficial Imports...

Swire Beverages - A Strategic Perspective

Beverages Division Delivering Refreshing Soft Drinks Swire Beverages manufactures, markets and distributes refreshing soft drinks to consumers in Hong Kong, Taiwan, Mainland China, and the. 56 OVERVIEW

Beverages Division Delivering Refreshing Soft Drinks Swire Beverages manufactures, markets and distributes refreshing soft drinks to consumers in Hong Kong, Taiwan, Mainland China, and the. 56 OVERVIEW

Suntory Beverage & Food Limited 2015 Strategies for Core Brands in Japan

SBF0226(2015.1.22) Suntory Beverage & Food Limited 2015 Strategies for Core Brands in Japan [Review of 2014] In the overall Japanese soft drink industry in 2014, demand was estimated slightly lower than

SBF0226(2015.1.22) Suntory Beverage & Food Limited 2015 Strategies for Core Brands in Japan [Review of 2014] In the overall Japanese soft drink industry in 2014, demand was estimated slightly lower than

TELLING THE GOOD STORY OF COFFEE SERVICE AND VENDING

TELLING THE GOOD STORY OF COFFEE SERVICE AND VENDING KEY DEFINITIONS What is a Vending Machine? A Vending Machine is an operational machine located at either a client site or in a public location designed

TELLING THE GOOD STORY OF COFFEE SERVICE AND VENDING KEY DEFINITIONS What is a Vending Machine? A Vending Machine is an operational machine located at either a client site or in a public location designed

Healthy tradition since 1934. Quality and sustainability. Modern technologies flexible employees. Competence and experience

Healthy tradition since 1934 Founded in 1934 the company started as a fruit processing factory, located outside the small city Ellefeld in Saxony/ Germany and has today become part of an international

Healthy tradition since 1934 Founded in 1934 the company started as a fruit processing factory, located outside the small city Ellefeld in Saxony/ Germany and has today become part of an international

Product coverage: Dark Beer, Lager, Lager by Origin, Low/Non- Alcohol Beer, Stout.

Brochure More information from http://www.researchandmarkets.com/reports/1541415/ Beer - Azerbaijan Description: Beer producers in Azerbaijan benefit from a wide supply of raw materials for beer production,

Brochure More information from http://www.researchandmarkets.com/reports/1541415/ Beer - Azerbaijan Description: Beer producers in Azerbaijan benefit from a wide supply of raw materials for beer production,

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Grocery Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Traditional Vs Modern... 3 Channel Formats... 3 Chart 1 Modern Grocery Retailing: Billa in Padova...

LIST OF CONTENTS AND TABLES Grocery Retailers in Italy - Category analysis... 1 Headlines... 1 Trends... 1 Traditional Vs Modern... 3 Channel Formats... 3 Chart 1 Modern Grocery Retailing: Billa in Padova...

B.C. Agrifoods Trade Overview

B.C. Agrifoods Trade Overview Water Focus on Japan and China Prepared by: Corporate Statistics and Research Unit, Ministry of Agriculture Britney.Elder@gov.bc.ca Source: Global Trade Atlas (May 2014),

B.C. Agrifoods Trade Overview Water Focus on Japan and China Prepared by: Corporate Statistics and Research Unit, Ministry of Agriculture Britney.Elder@gov.bc.ca Source: Global Trade Atlas (May 2014),

Gasteiner Mineralwasser GmbH

Gasteiner Mineralwasser GmbH Vienna, in May 2010 Gasteiner mineral water: The crystalclear water from the Hohe Tauern National Park Gasteiner mineral water is one of the bestknown and most popular Austrian

Gasteiner Mineralwasser GmbH Vienna, in May 2010 Gasteiner mineral water: The crystalclear water from the Hohe Tauern National Park Gasteiner mineral water is one of the bestknown and most popular Austrian

THAILAND B2C E-COMMERCE MARKET 2015

PUBLICATION DATE: AUGUST 2015 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-5 TABLE OF CONTENTS I PAGE 6 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 7 METHODOLOGY I PAGE 8 RELATED REPORTS I PAGE 9

PUBLICATION DATE: AUGUST 2015 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-5 TABLE OF CONTENTS I PAGE 6 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 7 METHODOLOGY I PAGE 8 RELATED REPORTS I PAGE 9

Soft Drink Tax Regulation 1993-8 Amended 04/2008

Soft Drink Tax Regulation 1993-8 Amended 04/2008 Agency 006.05 These rules and regulations are promulgated for the enforcement and administration of Act 7 of 1992 (2nd Ex. Sess.). A. DEFINITIONS 1. "Bottle"

Soft Drink Tax Regulation 1993-8 Amended 04/2008 Agency 006.05 These rules and regulations are promulgated for the enforcement and administration of Act 7 of 1992 (2nd Ex. Sess.). A. DEFINITIONS 1. "Bottle"

Coca-Cola Case Analyses. <Student Name> <Name and Section # of course> <Instructor Name> <Date>

Running Head: COCA-COLA CASE Coca-Cola Case Analyses Coca-Cola Case 2 Coca-Cola Case Analyses This paper is about the company Coca-Cola

Running Head: COCA-COLA CASE Coca-Cola Case Analyses Coca-Cola Case 2 Coca-Cola Case Analyses This paper is about the company Coca-Cola

Retailing in the Philippines

Brochure More information from http://www.researchandmarkets.com/reports/354797/ Retailing in the Philippines Description: The significant growth in the private sector, which includes many businesses operating

Brochure More information from http://www.researchandmarkets.com/reports/354797/ Retailing in the Philippines Description: The significant growth in the private sector, which includes many businesses operating

Acquisition of Lucozade and Ribena Business from GlaxoSmithKline plc

Acquisition of Lucozade and Ribena Business from GlaxoSmithKline plc September 9, 2013 Suntory Beverage & Food Ltd. 1 Transaction Overview Transaction Structure Acquisition of Lucozade and Ribena brands

Acquisition of Lucozade and Ribena Business from GlaxoSmithKline plc September 9, 2013 Suntory Beverage & Food Ltd. 1 Transaction Overview Transaction Structure Acquisition of Lucozade and Ribena brands

BEVERAGE DIGEST THE BEVERAGE INDUSTRY S LEADING INFORMATION RESOURCE FOR BREAKING NEWS, ANALYSIS & DATA

THE NEWSLETTER THE FACT BOOK COKE/PEPSI SYSTEM BOOKS BOTTLER TERRITORY MAPS CONFERENCES BEVERAGE DIGEST THE BEVERAGE INDUSTRY S LEADING INFORMATION RESOURCE FOR BREAKING NEWS, ANALYSIS & DATA MARCH 26,

THE NEWSLETTER THE FACT BOOK COKE/PEPSI SYSTEM BOOKS BOTTLER TERRITORY MAPS CONFERENCES BEVERAGE DIGEST THE BEVERAGE INDUSTRY S LEADING INFORMATION RESOURCE FOR BREAKING NEWS, ANALYSIS & DATA MARCH 26,

GLOBAL CONVENIENCE SYMPOSIUM growing demand, changing structures

GLOBAL CONVENIENCE SYMPOSIUM growing demand, changing structures Individual presentation from session 1: EVOLUTION OF FORECOURT CONVENIENCE STORES IN SOUTH AFRICA EVOLUTION OF FORECOURT CONVENIENCE STORES

GLOBAL CONVENIENCE SYMPOSIUM growing demand, changing structures Individual presentation from session 1: EVOLUTION OF FORECOURT CONVENIENCE STORES IN SOUTH AFRICA EVOLUTION OF FORECOURT CONVENIENCE STORES

Retailing - Hungary. Phone: +44 20 8123 2220 Fax: +44 207 900 3970 office@marketpublishers.com https://marketpublishers.com

Retailing - Hungary Phone: +44 20 8123 2220 Fax: +44 207 900 3970 office@marketpublishers.com Retailing - Hungary Date: May 1, 2010 Pages: 168 Price: US$ 2,100.00 ID: RC49AA0BB11EN Since the beginning

Retailing - Hungary Phone: +44 20 8123 2220 Fax: +44 207 900 3970 office@marketpublishers.com Retailing - Hungary Date: May 1, 2010 Pages: 168 Price: US$ 2,100.00 ID: RC49AA0BB11EN Since the beginning

Suntory Beverage & Food Limited 2016 Strategies for Core Brands in Japan

SBF0384(2016.1.20) Suntory Beverage & Food Limited 2016 Strategies for Core Brands in Japan [Review of 2015] In the overall Japanese soft drink industry in 2015, while the first half of the year remained

SBF0384(2016.1.20) Suntory Beverage & Food Limited 2016 Strategies for Core Brands in Japan [Review of 2015] In the overall Japanese soft drink industry in 2015, while the first half of the year remained

Strengthening the business foundation through concentration on core brands and generation of synergies

Review of Operations Soft Drinks Strengthening the business foundation through concentration on core brands and generation of synergies Katsutoshi Takahashi Director and Corporate Officer in charge of

Review of Operations Soft Drinks Strengthening the business foundation through concentration on core brands and generation of synergies Katsutoshi Takahashi Director and Corporate Officer in charge of

Department of Health and Human Services Centers for Disease Control and Prevention

Rethink your drink. Department of Health and Human Services Centers for Disease Control and Prevention When it comes to weight loss, there s no lack of diets promising fast results. There are low-carb

Rethink your drink. Department of Health and Human Services Centers for Disease Control and Prevention When it comes to weight loss, there s no lack of diets promising fast results. There are low-carb

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES Retailing in Italy - Industry Overview... 1 Executive Summary... 1 Retail Sales Recover Slightly in 2010 and 2011... 1 M-commerce Increasing in Importance in Italy... 1 Italians

LIST OF CONTENTS AND TABLES Retailing in Italy - Industry Overview... 1 Executive Summary... 1 Retail Sales Recover Slightly in 2010 and 2011... 1 M-commerce Increasing in Importance in Italy... 1 Italians

Q1 / 2015: INTERIM REPORT WITHIN THE FIRST HALF-YEAR OF 2015. Berentzen-Gruppe Aktiengesellschaft Haselünne / Germany

Q1 / 2015: INTERIM REPORT WITHIN THE FIRST HALF-YEAR OF 2015 Berentzen-Gruppe Aktiengesellschaft Haselünne / Germany Securities Identification Number 520 163 International Securities Identification Numbers

Q1 / 2015: INTERIM REPORT WITHIN THE FIRST HALF-YEAR OF 2015 Berentzen-Gruppe Aktiengesellschaft Haselünne / Germany Securities Identification Number 520 163 International Securities Identification Numbers

Reinventing Dairy in Convenience Stores Based on Retail and Shopper Insights

Reinventing Dairy in Convenience Stores Based on Retail and Shopper Insights 1 Convenience Store Types Source: Finding the Way : A Practical Roadmap for Capturing Emerging Opportunities in Convenience

Reinventing Dairy in Convenience Stores Based on Retail and Shopper Insights 1 Convenience Store Types Source: Finding the Way : A Practical Roadmap for Capturing Emerging Opportunities in Convenience

The Ultimate Smoothie Guide 1

The Ultimate Smoothie Guide 1 HEALTHY & DELICIOUS SMOOTHIE RECIPES smoothie recipes with health benefits Nourishing Smoothie Recipe Detox Smoothie Recipe Weight Loss Smoothie Recipe Anti-Aging Smoothie

The Ultimate Smoothie Guide 1 HEALTHY & DELICIOUS SMOOTHIE RECIPES smoothie recipes with health benefits Nourishing Smoothie Recipe Detox Smoothie Recipe Weight Loss Smoothie Recipe Anti-Aging Smoothie

Vermont Retail and Grocers Association Webinar

Vermont Retail and Grocers Association Webinar 2015 Legislative Changes C a n d a c e M o r g a n, D i r e c t o r P o l i c y, O u t r e a c h, a n d L e g i s l a t i v e A f f a i r s D e v o n J. G

Vermont Retail and Grocers Association Webinar 2015 Legislative Changes C a n d a c e M o r g a n, D i r e c t o r P o l i c y, O u t r e a c h, a n d L e g i s l a t i v e A f f a i r s D e v o n J. G

Mobile Phones - US. Euromonitor International : Country Sector Briefing

- Euromonitor International : Country Sector Briefing July 2010 List of Contents and Tables Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Sales of Mobile

- Euromonitor International : Country Sector Briefing July 2010 List of Contents and Tables Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 3 Category Data... 4 Table 1 Sales of Mobile

A STUDY ON INFLUENCE OF ADVERTISEMENT IN CONSUMER BRAND PREFERENCE (Special Reference to Soft Drinks Market in Hosur Town)

") A STUDY ON INFLUENCE OF ADVERTISEMENT IN CONSUMER BRAND PREFERENCE (Special Reference to Soft Drinks Market in Hosur Town) Dr.A. VinayagaMoorthy Professor, Department of Commerce, Periyar University,Salem-11.

A STUDY ON INFLUENCE OF ADVERTISEMENT IN CONSUMER BRAND PREFERENCE (Special Reference to Soft Drinks Market in Hosur Town) Dr.A. VinayagaMoorthy Professor, Department of Commerce, Periyar University,Salem-11.

UK Wine Market Overview 2013

UK Wine Market Overview 2013 The UK market continues to follow the trend of recent years whereby wine volume sales continue to fall (down 2% annually) while value continues to rise year on year, up 1%

UK Wine Market Overview 2013 The UK market continues to follow the trend of recent years whereby wine volume sales continue to fall (down 2% annually) while value continues to rise year on year, up 1%

LIST OF CONTENTS AND TABLES

LIST OF CONTENTS AND TABLES in Australia - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 4 Category Data... 5 Table 1 by Category: Units/Outlets 2005-2010...

LIST OF CONTENTS AND TABLES in Australia - Category analysis... 1 Headlines... 1 Trends... 1 Competitive Landscape... 2 Prospects... 4 Category Data... 5 Table 1 by Category: Units/Outlets 2005-2010...

Frozen fruit smoothies

Frozen fruit smoothies www.nudgedrinks.co.uk enquiries@nudgedrinks.co.uk tel: 01206 580484 facebook.com/nudgedrinks @nudgedrinks Contents About us page 1 Our smoothies page 2 Our flavours page 3 How to

Frozen fruit smoothies www.nudgedrinks.co.uk enquiries@nudgedrinks.co.uk tel: 01206 580484 facebook.com/nudgedrinks @nudgedrinks Contents About us page 1 Our smoothies page 2 Our flavours page 3 How to

DIRECT QUESTIONS: MD STORE OPERATIONS HELP DESK

NON-ALCOHOLIC BEVERAGE POG STRATEGY DIRECT QUESTIONS: MD STORE OPERATIONS HELP DESK STRATEGY Category Segments Water Hydration (Isotonics) Juice Coffee Tea Energy Carbonated Soft Drinks (CSD) Non Alcoholic

NON-ALCOHOLIC BEVERAGE POG STRATEGY DIRECT QUESTIONS: MD STORE OPERATIONS HELP DESK STRATEGY Category Segments Water Hydration (Isotonics) Juice Coffee Tea Energy Carbonated Soft Drinks (CSD) Non Alcoholic

Thank you for joining the Vermont Retail and Grocers Association Webinar presented by the Vermont Department of Taxes. The webinar will begin

Thank you for joining the Vermont Retail and Grocers Association Webinar presented by the Vermont Department of Taxes. The webinar will begin shortly. Vermont Retail and Grocers Association Webinar 2015

Thank you for joining the Vermont Retail and Grocers Association Webinar presented by the Vermont Department of Taxes. The webinar will begin shortly. Vermont Retail and Grocers Association Webinar 2015

VIDEO WORKSHEET. Review: #300007. Name: Hour:

#300007 Name: Hour: Review: VIDEO WORKSHEET After watching each segment of Obesity in a Bottle II: How to Pick Healthy Beverages, answer the following questions. How to Choose Healthy Beverages 1. What

#300007 Name: Hour: Review: VIDEO WORKSHEET After watching each segment of Obesity in a Bottle II: How to Pick Healthy Beverages, answer the following questions. How to Choose Healthy Beverages 1. What

USING THE FOOD LABEL TO FIND ITEMS THAT MEET THE EAT SMART IN PARKS GUIDELINES

USING THE FOOD LABEL TO FIND ITEMS THAT MEET THE EAT SMART IN PARKS GUIDELINES FOOD LABELS Food Nacho chips label Although one serving of chips (1 ounce) meets the calorie guideline, 3 ounces of chips

USING THE FOOD LABEL TO FIND ITEMS THAT MEET THE EAT SMART IN PARKS GUIDELINES FOOD LABELS Food Nacho chips label Although one serving of chips (1 ounce) meets the calorie guideline, 3 ounces of chips

Office Coffee Service (OCS) Market in the US 2014-2018

Market in the US 2014-2018") Brochure More information from http://www.researchandmarkets.com/reports/2970670/ Office Coffee Service (OCS) Market in the US 2014-2018 Description: About Office Coffee Service There is nothing as refreshing

Brochure More information from http://www.researchandmarkets.com/reports/2970670/ Office Coffee Service (OCS) Market in the US 2014-2018 Description: About Office Coffee Service There is nothing as refreshing

Market Survey Report

Market Survey Report ItalianWine Market in South Korea Seoul, December 2013 Prepared by Ran Woo, ITCCK Contents: 1. Objectives 2. Introduction 3. Market Position of Italian wine in Korea A. General market

Market Survey Report ItalianWine Market in South Korea Seoul, December 2013 Prepared by Ran Woo, ITCCK Contents: 1. Objectives 2. Introduction 3. Market Position of Italian wine in Korea A. General market

World Tea News Market Report - October 2013. Increasing Value for the World s Most Consumed Beverage

World Tea News Market Reports are concise snapshots of information and experienced analysis on diverse factors impacting the global tea industry. From distribution channels and packaging formats to demographics

World Tea News Market Reports are concise snapshots of information and experienced analysis on diverse factors impacting the global tea industry. From distribution channels and packaging formats to demographics

FUNCTIONAL BEVERAGES FROM ENERGY TO RELAXATION WHITE PAPER // TREND RESOURCES. Lisa Demme, Beverage

page 1 FUNCTIONAL BEVERAGES FROM ENERGY TO RELAXATION Lisa Demme, Beverage In 2011 the energy drinks and energy shots market sales were estimated at $8.1 billion, which represented a dollar sales growth

page 1 FUNCTIONAL BEVERAGES FROM ENERGY TO RELAXATION Lisa Demme, Beverage In 2011 the energy drinks and energy shots market sales were estimated at $8.1 billion, which represented a dollar sales growth

An initiative of the BC Pediatric Society & the Heart and Stroke Foundation. Extensions

An initiative of the BC Pediatric Society & the Heart and Stroke Foundation Extensions Extensions Classroom Extension Activities Mathematics: Graph the Results (Lessons 2-4)...124 Snack Check (Lesson 2)..................

An initiative of the BC Pediatric Society & the Heart and Stroke Foundation Extensions Extensions Classroom Extension Activities Mathematics: Graph the Results (Lessons 2-4)...124 Snack Check (Lesson 2)..................

Cold Facts About Frozen Foods

Cold Facts About Frozen Foods HOT TOPIC REPORT October 2012 Update ver since Clarence Birdseye first developed a process to freeze and preserve food nutrients and flavor in 1944, the frozen food industry

Cold Facts About Frozen Foods HOT TOPIC REPORT October 2012 Update ver since Clarence Birdseye first developed a process to freeze and preserve food nutrients and flavor in 1944, the frozen food industry

United States of America Food & Beverage Market Study. June 2013

United States of America Food & Beverage Market Study June 2013 1. Introduction This research was carried out by Global Strategy, Inc. (www.consultgsi.com), a U.S. business development and market research

United States of America Food & Beverage Market Study June 2013 1. Introduction This research was carried out by Global Strategy, Inc. (www.consultgsi.com), a U.S. business development and market research

WHAT WILL WE MAKE OF THIS MOMENT? HENKEL SHOWER PROJECT: MARKETING CAMPAIGN FOCUSED ON SUSTAINABILITY

WHAT WILL WE MAKE OF THIS MOMENT? HENKEL SHOWER PROJECT: MARKETING CAMPAIGN FOCUSED ON SUSTAINABILITY Exploring Sustainability as a Strategic Opportunity (08.05.2015) Anastasia Lavrentyeva, Davide Bramati,

WHAT WILL WE MAKE OF THIS MOMENT? HENKEL SHOWER PROJECT: MARKETING CAMPAIGN FOCUSED ON SUSTAINABILITY Exploring Sustainability as a Strategic Opportunity (08.05.2015) Anastasia Lavrentyeva, Davide Bramati,

Market Audit Sports and Energy Drinks UK Market Focussing on the Microenvironment of Red Bull

Market Audit Sports and Energy Drinks UK Market Focussing on the Microenvironment of Red Bull William Hanrahan Student Number: 060953199 Stage 2 Marketing: ACE2002 1 Contents 1.0 Executive Summary...3

Market Audit Sports and Energy Drinks UK Market Focussing on the Microenvironment of Red Bull William Hanrahan Student Number: 060953199 Stage 2 Marketing: ACE2002 1 Contents 1.0 Executive Summary...3

New Jersey School Nutrition Policy Questions and Answers

New Jersey School Nutrition Policy Questions and Answers FOR ALL GRADE LEVELS: Items that are prohibited to be served, sold or given out as free promotion anywhere on school property at anytime before

New Jersey School Nutrition Policy Questions and Answers FOR ALL GRADE LEVELS: Items that are prohibited to be served, sold or given out as free promotion anywhere on school property at anytime before

Super Duper Smoothies

Super Duper Smoothies A Report On What Makes a Good Smoothie and 7 Great Smoothie Recipes Written by: Olivia Parker The History of the Smoothie The smoothie first made its debut in health food stores in

Super Duper Smoothies A Report On What Makes a Good Smoothie and 7 Great Smoothie Recipes Written by: Olivia Parker The History of the Smoothie The smoothie first made its debut in health food stores in

The Coca Cola Company: Marketing Strategy

The Coca Cola Company: Marketing Strategy Contents Introduction and Summary of the Company... 3 Environmental Analysis... 3 Political... 4 Economic... 4 Social... 4 Technological... 5 Customer analysis

The Coca Cola Company: Marketing Strategy Contents Introduction and Summary of the Company... 3 Environmental Analysis... 3 Political... 4 Economic... 4 Social... 4 Technological... 5 Customer analysis

Table 9 Page 12 Q13. Which of the following produce items have you purchased FRESH (NOT frozen, canned or dried) in the past 12 months?

in the past 12 months?") Banner 1 Table 1 Page 1 Q5. What is your household income? Table 2 Page 2 Q6. What is your marital status? Table 3 Page 3 Q7. How many dependent children do you have? Table 4 Page 4 Q8. In which state

Banner 1 Table 1 Page 1 Q5. What is your household income? Table 2 Page 2 Q6. What is your marital status? Table 3 Page 3 Q7. How many dependent children do you have? Table 4 Page 4 Q8. In which state

Vitality Healthy Schools list of approved and banned drinks

Vitality Healthy Schools list of approved and banned drinks Any drink with more than ½ teaspoon (2.5g) per 100ml (2.5%) may not be sold in the tuck shop. Drinks that may be sold in the tuck shop Water

Vitality Healthy Schools list of approved and banned drinks Any drink with more than ½ teaspoon (2.5g) per 100ml (2.5%) may not be sold in the tuck shop. Drinks that may be sold in the tuck shop Water

The Modern Shopper MAY 2015

The Modern Shopper MAY 21 The Modern Shopper Fluent s inaugural The Modern Shopper survey provides insights into the latest consumer trends of interest to shopper marketing, grocery retail, and consumer

The Modern Shopper MAY 21 The Modern Shopper Fluent s inaugural The Modern Shopper survey provides insights into the latest consumer trends of interest to shopper marketing, grocery retail, and consumer

Tim Salt. Managing Director, Diageo Australia

Tim Salt Managing Director, Diageo Australia Tim Salt Managing Director, Diageo Australia Tim Salt Managing Director, Diageo Australia & New Zealand Nationality: Australian (UK born) Role description:

Tim Salt Managing Director, Diageo Australia Tim Salt Managing Director, Diageo Australia Tim Salt Managing Director, Diageo Australia & New Zealand Nationality: Australian (UK born) Role description:

Nutri Lean Lifestyle 30

Nutri Lean Lifestyle 30 Day 1-2 ( phase 1 - detoxification) Morning 1 Probiotic 1-1.5 scoops Forever Lite Shake /300 ml natural, juice without sugar or soya milk ( might be repeated for dinner ) 2 Forever

Nutri Lean Lifestyle 30 Day 1-2 ( phase 1 - detoxification) Morning 1 Probiotic 1-1.5 scoops Forever Lite Shake /300 ml natural, juice without sugar or soya milk ( might be repeated for dinner ) 2 Forever

Confronting Challenges

Confronting Challenges U.S. and International Developments and Statistics for 2008 By John G. Rodwan, Jr. 12 Despite an uncharacteristically staid performance in 2008, bottled water remains a beverage

Confronting Challenges U.S. and International Developments and Statistics for 2008 By John G. Rodwan, Jr. 12 Despite an uncharacteristically staid performance in 2008, bottled water remains a beverage

PRESS RELEASE Drinktec 2013 11092013

Döhler at Innovative natural food & beverage ingredients Many new products and product applications Integrated solutions for the food & beverage industry "WE BRING IDEAS TO LIFE." is the central theme

Döhler at Innovative natural food & beverage ingredients Many new products and product applications Integrated solutions for the food & beverage industry "WE BRING IDEAS TO LIFE." is the central theme

Snack Foods and Beverages In South Carolina Schools A comparison of state policy with USDA s nutrition standards

A data table from The Pew Charitable Trusts and the Robert Wood Johnson Foundation Jan 2015 Snack Foods and Beverages In South Carolina Schools A comparison of state policy with USDA s nutrition standards

A data table from The Pew Charitable Trusts and the Robert Wood Johnson Foundation Jan 2015 Snack Foods and Beverages In South Carolina Schools A comparison of state policy with USDA s nutrition standards

State of Mobile Commerce Growing like a weed

State of Mobile Commerce Growing like a weed Q1 2015 Executive Summary Mobile commerce is growing like a weed. Mobile is 29% of ecommerce transactions in the US and 34% globally. By the end of 2015, mobile

State of Mobile Commerce Growing like a weed Q1 2015 Executive Summary Mobile commerce is growing like a weed. Mobile is 29% of ecommerce transactions in the US and 34% globally. By the end of 2015, mobile

Advertising. Task 1 Advertisement What are the following pictures advertising?

Advertising Task 1 Advertisement What are the following pictures advertising? Look at the three advertisements below and think about which product or service each image can be used for? Try to be as creative

Advertising Task 1 Advertisement What are the following pictures advertising? Look at the three advertisements below and think about which product or service each image can be used for? Try to be as creative

Cosmetics Market in Asia: Favorable Demographics Fuel Sales

Brochure More information from http://www.researchandmarkets.com/reports/575260/ Cosmetics Market in Asia: Favorable Demographics Fuel Sales Description: The Japanese cosmetics market is in a stable condition

Brochure More information from http://www.researchandmarkets.com/reports/575260/ Cosmetics Market in Asia: Favorable Demographics Fuel Sales Description: The Japanese cosmetics market is in a stable condition

2. Definitions Alcohol Alcohol Management Plan Alcohol-related harm - Amenity and good order of the locality Authorised customer Authorised visitor

MACKENZIE, TIMARU AND WAIMATE DISTRICT COUNCILS JOINT LOCAL ALCOHOL POLICY 1. Background This Local Alcohol Policy (LAP) has been developed jointly by the Mackenzie, Timaru and Waimate District Councils.

MACKENZIE, TIMARU AND WAIMATE DISTRICT COUNCILS JOINT LOCAL ALCOHOL POLICY 1. Background This Local Alcohol Policy (LAP) has been developed jointly by the Mackenzie, Timaru and Waimate District Councils.

Guide from ShopperVista Channel Focus Online Channel. www.shoppervista.igd.com shopper@igd.com +44 (0) 1923 851 956 @igdshoppernews

1923 851 956 @igdshoppernews") Guide from ShopperVista Channel Focus Online Channel www.shoppervista.igd.com shopper@igd.com +44 (0) 1923 851 956 @igdshoppernews Hello and welcome This guide is from IGD s ShopperVista Channel Focus

Guide from ShopperVista Channel Focus Online Channel www.shoppervista.igd.com shopper@igd.com +44 (0) 1923 851 956 @igdshoppernews Hello and welcome This guide is from IGD s ShopperVista Channel Focus

Making relentless efforts to become the leading integrated alcohol beverages company, one that continues to evolve

Review of Operations Alcohol Beverages Making relentless efforts to become the leading integrated alcohol beverages company, one that continues to evolve Akiyoshi Koji Director in charge of Alcohol Beverages

Review of Operations Alcohol Beverages Making relentless efforts to become the leading integrated alcohol beverages company, one that continues to evolve Akiyoshi Koji Director in charge of Alcohol Beverages

Karlovarské minerální vody, a.s. Company catalogue

Karlovarské minerální vody, a.s. Company catalogue HISTORY There has been a spa in the pristine natural surroundings of Karlovy Vary (Carlsbad) since 1867, when Heinrich Mattoni founded Karlovarske mineralni

Karlovarské minerální vody, a.s. Company catalogue HISTORY There has been a spa in the pristine natural surroundings of Karlovy Vary (Carlsbad) since 1867, when Heinrich Mattoni founded Karlovarske mineralni

Buying Healthy Food on a Budget: Cooking Matters at the Store NATIONAL SPONSOR

Buying Healthy Food on a Budget: Cooking Matters at the Store NATIONAL SPONSOR It All Starts with the Cart Survey Says What do low-income families say is their biggest barrier to making healthy meals?

Buying Healthy Food on a Budget: Cooking Matters at the Store NATIONAL SPONSOR It All Starts with the Cart Survey Says What do low-income families say is their biggest barrier to making healthy meals?

Analysis of through-chain pricing of food products (Summary version) Freshlogic 24 August 2012

Freshlogic 24 August 2012") Analysis of through-chain pricing of food products (Summary version) Freshlogic August 0 Introduction Objective This document has been prepared by Freshlogic as an internal briefing paper for Coles on

Analysis of through-chain pricing of food products (Summary version) Freshlogic August 0 Introduction Objective This document has been prepared by Freshlogic as an internal briefing paper for Coles on

Competitive Advantage Through Multi Distribution. Mike Bishop PCA LIFE Korea November 2004

Competitive Advantage Through Multi Distribution Mike Bishop PCA LIFE Korea November 2004 39 Market overview Significant life insurance market 2 nd largest in Asia (after Japan) 7 th largest in the world

Competitive Advantage Through Multi Distribution Mike Bishop PCA LIFE Korea November 2004 39 Market overview Significant life insurance market 2 nd largest in Asia (after Japan) 7 th largest in the world