A s a retailer, you know the importance of obtaining a seller s permit when

|

|

|

- Julian Fox

- 7 years ago

- Views:

Transcription

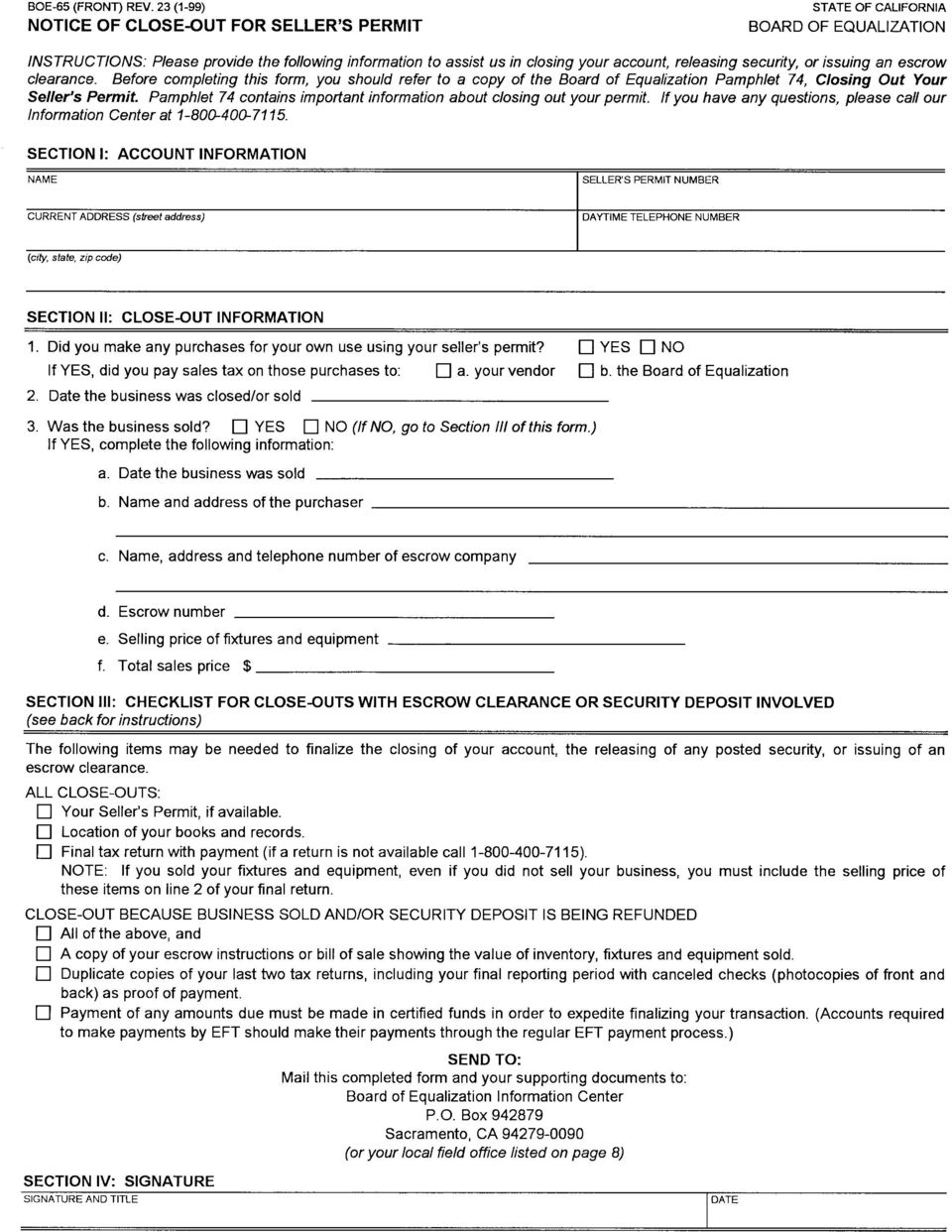

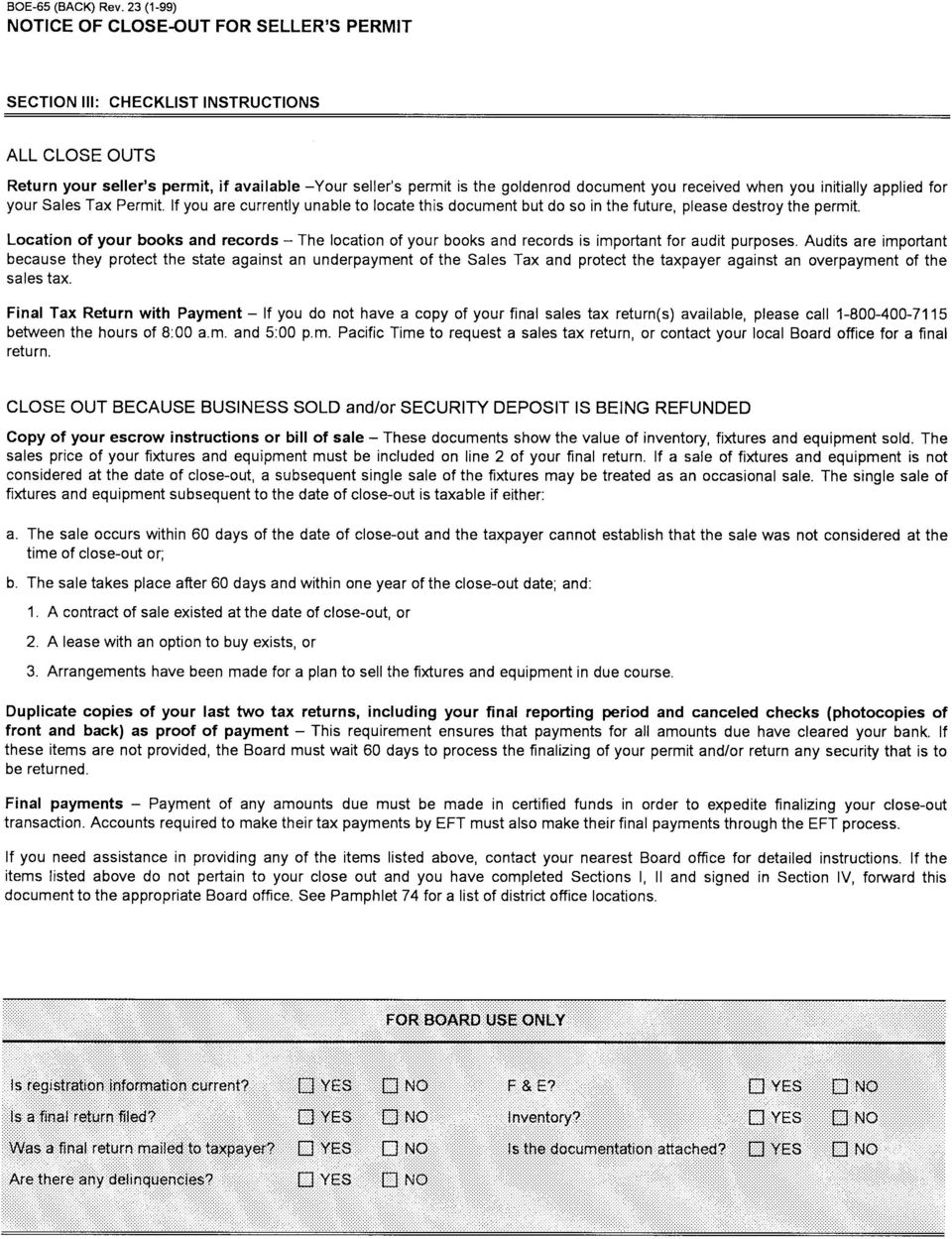

1 STATE BOARD OF EQUALIZATION SALES AND USE TAX PROCEDURES CLOSING OUT YOUR SELLER S PERMIT A s a retailer, you know the importance of obtaining a seller s permit when you start a business. It is equally important to know that you must tell the Board to close out your permit when you are no longer actively engaged in business or when you change the ownership of a continuing business. If you fail to notify the Board of these changes, you may be liable for tax, interest and penalties which are incurred after you no longer own or operate the business. Failure to close out your permit can result in a tax liability even though you no longer own or operate the business. This pamphlet covers the following topics related to closing out your permit: Notifying the Board Filing your final tax return Taxable sales after closing out your permit Successor s liability and tax clearances Changes in ownership (See page 3 for examples of such changes) If you want more information about any of these topics, please contact the Board s Information Center at Staff will be happy to answer your questions. Notifying the Board If you sell or close out your business, you must let us know in writing. The following information may be needed before we can close out your account: January 1999 Publication 74 The date you stopped being actively engaged in business. Your reason for not being actively engaged in business. The means you used to dispose of your resale inventory, fixtures, leasehold improvements, and equipment. If you sold any of these items, you will need to disclose the selling price. If you sold your entire business or resale inventory, you need to give both the selling price and the name of the buyer. The purchase price of retained inventory. Your current address and daytime telephone number Your copy of the seller s permit, if available You can use the enclosed form, Notice of Close-Out for Seller s Permit, to notify us (see page 5). The form will be reviewed by staff, who will contact you if additional information is required. If no additional information is needed, staff will close out your account and cancel your seller s permit. You also need to file your final sales and use tax return and any prior returns (including prepayments) which you have not yet filed. To expedite your closeout, you should file these returns with the local office and pay any tax, penalty and interest with certified funds. If you pay by a personal check and BOARD MEMBERS E. L. SORENSEN, JR. Executive Director JOHAN KLEHS First District, Hayward DEAN F. ANDAL Second District, Stockton CLAUDE PARRISH Third Dist rict, Torrance JOHN CHIANG Fourth District, Los Angeles KATHLEEN CONNELL State Controller, Sacramento

2 Closing Out Your Seller s Permit January 1999 cannot provide a copy of the cancelled check, it could take eight or more weeks to close your account. After you have paid your entire liability (including liabilities resulting from an audit), staff will return any security you have on deposit. It is important to remember that, even after providing all information and having your permit closed out, you must still keep your business records for four years. Filing Your Final Tax Return Even though you have closed out your permit, you must still report your sales up to the closeout date. This includes any sales of fixtures, leasehold improvements, or equipment that occurred as part of the close or sale of your business. You must also report any inventory you intend to retain for your own use if that inventory was purchased without payment of sales tax. To help expedite the closeout you should separately report and identify the sale of fixtures and equipment and retained inventory on line 2 of your final sales and use tax return. Sales of inventory to another seller or the purchaser of your business are not taxable, but should be reported as Sales for Resale on line 4 of your return. A resale certificate should be obtained from the buyer and saved with your records. Normally, you may file your final return on its regular monthly or quarterly due date. However, taxpayers who report annually must file the final return by the due date of the quarter in which they close out their permit. Closing out your permit and filing your final return does not relieve you of a liability for unpaid tax whether reported or unreported. You are required to pay all tax incurred while actively engaged in business. If the business is a corporation which has added or included tax as part of the price of the property it has sold, corporate officers or other persons may be held personally liable for unpaid tax if they willfully failed to pay or caused not to be paid the tax that was due and were: Responsible for filing returns or paying tax, or Under a duty to act for the corporation in complying with the Sales and Use Tax Law If you think you may have difficulty paying tax that is due, you should contact the local office handling your permit. Taxable Sales After Closing Out Your Permit Before requesting the close-out of your permit, you should be sure that you will make no more sales. You qualify as a seller if you make three or more sales of tangible personal property (including retained inventory, fixtures, leasehold improvements, or equipment) in any 12-month period. As a seller, you are required to register with the Board and to report and pay any sales tax due. In certain cases, a single sale of fixtures and equipment which occurs after the closeout can also be taxable. A sale which occurs within 60 days is normally considered taxable unless you can prove that the sale was not planned at the close-out date. A sale that occurs after 60 days, but within one year, is taxable if: There was a contract of sale at the close out date, or A lease with an option to buy existed at the closeout date, or There is evidence that a plan existed to sell the fixtures and equipment in due course You are liable for use tax if you make personal or business use of property Page 2

3 Closing Out Your Seller s Permit January 1999 purchased without tax, for example, resale inventory. You are required to report and pay use tax on the cost of such property. Successor s Liability and Tax Clearance If you are selling your business, you need to be aware of successor s liability. Under the law, the buyer of a business or stock of goods must withhold from the purchase price an amount sufficient to cover the seller s liability for tax, interest, and penalties. If a sufficient amount is not withheld, the buyer becomes personally liable for the amount that should have been withheld. This is called "successor's liability" and is limited to an amount equal to the purchase price. To be released from this liability, the buyer may request a certificate of tax clearance from the Board. If a tax clearance is needed to complete the sale of your business, you need to remember that it can take up to 60 days or more to obtain a clearance, especially if an audit is required and your books and records are not available for review. You can help the clearance process by ensuring that the escrow company or buyer promptly files a written request for a clearance with the local office. You should also remember that: The liability of a successor does not replace your primary liability for unpaid tax, interest, or penalties. The Board will generally only try to collect from a successor if unable to do so from the seller of the business. The amount of money you actually receive on the sale of your business may be reduced by the amount you owe for sales and use tax. If you owe tax, the Board generally will not issue a tax clearance until it receives full payment of your liability or until an amount equal to your liability is put into escrow. Changes in Ownership If you continue to operate your business but change its form of ownership, you are required to obtain a new seller's permit. A permit is valid only for the business entity (such as an individual, partnership, corporation, or joint venture) in whose name it was issued and certain changes in ownership will invalidate it. For example a new permit is required when: A proprietorship or partnership incorporates. A corporation dissolves to become a partnership or proprietorship. A partnership adds or drops a partner. This can include changes in marital status for a husband-wife co-ownership. Any change in the general partners of a general partnership. A corporate reorganization results in a new corporation. A sole proprietor adds a partner. If you are planning or have already made such changes, you should contact the Board s Information Center (see page 4). Failure to notify the Board of a change in ownership can make you liable for the taxes owed by the new owner. Since some changes in ownership might also include taxable transfers of tangible personal property, it is always better to contact the Board before making the change. The staff can review the planned change and tell you if it would be subject to tax and if you will need a new permit. NOTE The statements in this pamphlet are general and are current as of the date on the cover. The Sales and Use Tax Law (Revenue and Taxation Code, Section 6001 and following) is complex and subject to change. If there is a conflict between the law and this pamphlet, any decisions will be based on the law and not this pamphlet. Page 3

4 Closing Out Your Seller s Permit January 1999 For More Information Information Center Please call the Center if you have general questions or need to learn more about closing our your permit To speak to a representative, call between 8:00 a.m and 5:00 p.m., Monday through Friday, excluding State holidays. Automated services, including a fax-back service, are available 24 hours a day. Persons with hearing disabilities can contact the Center at the following numbers: TDD phones, ; voice phones, Your Taxpayers Rights Advocate The State Board of Equalization wants to make dealing with us as easy as possible. As a result, we have appointed a Taxpayers Rights Advocate to help you with problems you cannot resolve at other levels. You can write to them at: Taxpayers Rights Advocate ; State Board of Equalization; 450 N Street, MIC:70; PO Box ; Sacramento, CA Or call: (toll free) ) (fax) Regulations These following Sales and Use Tax Regulations apply to close-outs: Regulation Occasional Sales Regulation Buildings and Other Property Affixed to Realty Regulation Permits Regulation Successor's Liability Please call the Information Center to order copies of these regulations. Copies can also be downloaded or viewed from our website. Page 4

5

6

7 Page 7 intentionally left blank.

8 Closing Out Your Seller s Permit January 1999 FIELD OFFICE LOCATIONS AND ADDRESSES AREA TELEPHONE CALIFORNIA CITIES OFFICE ADDRESS CODE NUMBER Bakersfield th Street, Suite 380, PO Box 1728, City of Industry Crossroads Parkway, PO Box 90818, Culver City 5901 Green Valley Circle, PO Box 3652, El Centro 1550 W. Main Street, Eureka 134 D Street, Suite 301, PO Box 4884, (hours 10 a.m.-2 p.m. M-F) Fresno 5070 N. Sixth Street, Suite 110, PO Box 28580, Laguna Hills Moulton Parkway, Suite 100, PO Box 30890, Norwalk E. Imperial Highway, PO Box 409, Oakland 1515 Clay Street, Suite 303, Rancho Mirage Bob Hope Drive, Suite 301, Redding 391 Hemstead Drive, PO Box , Riverside 3737 Main Street, Suite 1000, Sacramento 3321 Power Inn Road, Suite 210, Salinas 111 East Navajo Drive, Suite 100, San Diego 1350 Front Street, Rm 5047, San Francisco 455 Golden Gate Avenue, Suite 7500, San Jose 250 South Second Street, San Marcos 334 Via Vera Cruz, Suite 107, Santa Ana 28 Civic Center Plaza, Rm 239, PO Box 12040, Santa Rosa 50 D Street, Rm 230, PO Box 730, Stockton 31 East Channel Street, Rm 264, PO Box 1890, Suisun City 333 Sunset Avenue, Suite 330, Torrance 680 W. Knox Street, Suite 200, PO Box T, Van Nuys Sherman Way, Suite 250, (PO Box 7735, Van Nuys, ) Ventura 4820 McGrath Street, Suite 260, Ventura, FIELD OFFICE FOR OUT-OF-STATE ACCOUNTS Sacramento 3321 Power Inn Road, Suite 130, PO Box , HEADQUARTERS Sacramento PO Box , Addresses and telephone numbers are current as of , but are subject to change. We recommend you call the office before visiting. Page 8

Closing Out Your Account

Closing Out Your Account PUBLICATION 74 DECEMBER 2015 BOARD MEMBERS (Names updated 2016) SEN. GEORGE RUNNER (Ret.) First District Lancaster FIONA MA, CPA Second District San Francisco JEROME E. HORTON

Closing Out Your Account PUBLICATION 74 DECEMBER 2015 BOARD MEMBERS (Names updated 2016) SEN. GEORGE RUNNER (Ret.) First District Lancaster FIONA MA, CPA Second District San Francisco JEROME E. HORTON

Tax Collection Procedures

Introduction What s Inside... Pay the full amount due or tell us 1 why you can t 1 We will honor your rights 1 Items to note 2 Payment options 2-3 Collection & Enforcement Actions 4-6 Liens Levies Additional

Introduction What s Inside... Pay the full amount due or tell us 1 why you can t 1 We will honor your rights 1 Items to note 2 Payment options 2-3 Collection & Enforcement Actions 4-6 Liens Levies Additional

California Seller s Permit Application for Individuals/Partnerships/Corporations/Organizations (Regular or Temporary)

") BOE-400-SPA Rev. 1 (7-05) California Seller s Permit Application for Individuals/Partnerships/Corporations/Organizations (Regular or Temporary) State Board of Equalization Seller S Permit APPlicAtion Seller

BOE-400-SPA Rev. 1 (7-05) California Seller s Permit Application for Individuals/Partnerships/Corporations/Organizations (Regular or Temporary) State Board of Equalization Seller S Permit APPlicAtion Seller

FRANCHISE AND PERSONAL INCOME TAX APPEALS

STATE BOARD OF EQUALIZATION FRANCHISE AND PERSONAL INCOME TAX APPEALS If you disagree with a Franchise Tax Board decision about your liability for franchise or personal income taxes, or about your eligibility

STATE BOARD OF EQUALIZATION FRANCHISE AND PERSONAL INCOME TAX APPEALS If you disagree with a Franchise Tax Board decision about your liability for franchise or personal income taxes, or about your eligibility

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

A Guide to CalPERS. When You Change Retirement Systems

A Guide to CalPERS When You Change Retirement Systems This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS Introduction...2 When You Change Retirement Systems....2

A Guide to CalPERS When You Change Retirement Systems This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS Introduction...2 When You Change Retirement Systems....2

Division of Workers Compensation headquarters DIVISION WORKERS' COMPENSATION DISTRICT OFFICES

Administrative director - Carrie Nevans Court administrator - Keven Star Chief legal counsel Destie Overpeck Executive medical director Vacant Chief, programmatic services - Angela Michael Chief, legislation

Administrative director - Carrie Nevans Court administrator - Keven Star Chief legal counsel Destie Overpeck Executive medical director Vacant Chief, programmatic services - Angela Michael Chief, legislation

State Disability Insurance Provisions

State Disability Insurance Provisions This pamphlet is for general information only, and does not have the force and effect of law, rule or regulation. DE 2515 Rev. 54 (8-06 ) (INTERNET) Cover + 5 Pages

State Disability Insurance Provisions This pamphlet is for general information only, and does not have the force and effect of law, rule or regulation. DE 2515 Rev. 54 (8-06 ) (INTERNET) Cover + 5 Pages

DIVISION OF WORKERS' COMPENSATION HEADQUARTERS

Acting administrative director Destie Overpeck Chief judge Richard Newman Special advisor Susan Hamilton Chief, legal counsel Destie Overpeck Executive medical director Rupali Das MD. Chief, programmatic

Acting administrative director Destie Overpeck Chief judge Richard Newman Special advisor Susan Hamilton Chief, legal counsel Destie Overpeck Executive medical director Rupali Das MD. Chief, programmatic

When You Change Retirement Systems

When You Change Retirement Systems California Public Employees Retirement System Changing Retirement Systems When You Change Retirement Systems This booklet provides information on the rights and benefi

When You Change Retirement Systems California Public Employees Retirement System Changing Retirement Systems When You Change Retirement Systems This booklet provides information on the rights and benefi

CACalifornia Taxpayers Bill of Rights

CACalifornia Taxpayers Bill of Rights Inside 01 Taxpayers Bill of Rights legislation enacted 1988 02 Taxpayers Bill of Rights legislation enacted 1997 Information for Taxpayers» 03 California Taxpayers

CACalifornia Taxpayers Bill of Rights Inside 01 Taxpayers Bill of Rights legislation enacted 1988 02 Taxpayers Bill of Rights legislation enacted 1997 Information for Taxpayers» 03 California Taxpayers

Online Banking, Bill Pay, and E-Statements

Online Banking, Bill Pay, and E-Statements ERROR RESOLUTION NOTICE In case of errors or questions about your electronic transfers, call or write us at the telephone number or address listed in this brochure,

Online Banking, Bill Pay, and E-Statements ERROR RESOLUTION NOTICE In case of errors or questions about your electronic transfers, call or write us at the telephone number or address listed in this brochure,

DIVISION OF WORKERS' COMPENSATION HEADQUARTERS

Administrative director Destie Overpeck Chief judge Richard Newman Acting chief, legal counsel George Parisotto Executive medical director Rupali Das MD Chief, programmatic services Denise Vargas Electronic

Administrative director Destie Overpeck Chief judge Richard Newman Acting chief, legal counsel George Parisotto Executive medical director Rupali Das MD Chief, programmatic services Denise Vargas Electronic

Recover Your. Unpaid Wages. Commissioner s Office

Recover Your Unpaid Wages With the California Labor Commissioner s Office The Labor Commissioner s Office, also called the Division of Labor Standards Enforcement (DLSE), is a part of the California Department

Recover Your Unpaid Wages With the California Labor Commissioner s Office The Labor Commissioner s Office, also called the Division of Labor Standards Enforcement (DLSE), is a part of the California Department

Manufactured Housing Retailer s Special Inventory

Glenn Hegar Texas Comptroller of Public Accounts Manufactured Housing Retailer s Special Inventory Instructions for Filing Forms and Paying Property Taxes April 2015 By publishing this manual, the Texas

Glenn Hegar Texas Comptroller of Public Accounts Manufactured Housing Retailer s Special Inventory Instructions for Filing Forms and Paying Property Taxes April 2015 By publishing this manual, the Texas

COLORADO DEPARTMENT OF REVENUE GUIDE TO THE MANAGED AUDIT PROGRAM FOR SALES AND USE TAXES

GUIDE TO THE FOR SALES AND USE TAXES AS OF June 29, 2007 Contents Preface Introduction to the Managed Audit Program............... 3 Reviewing your sales.................................... 5 Reviewing

GUIDE TO THE FOR SALES AND USE TAXES AS OF June 29, 2007 Contents Preface Introduction to the Managed Audit Program............... 3 Reviewing your sales.................................... 5 Reviewing

DISABILITY INSURANCE PROVISIONS

DISABILITY INSURANCE PROVISIONS DE 2515 Rev. 56 (11-08) (INTERNET) Cover + 5 Pages CU/GA 892 B Disability is any illness or injury, either physical or mental, that prevents you from doing your regular

DISABILITY INSURANCE PROVISIONS DE 2515 Rev. 56 (11-08) (INTERNET) Cover + 5 Pages CU/GA 892 B Disability is any illness or injury, either physical or mental, that prevents you from doing your regular

Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two

Michael Thomas-Region one Leilani Pfeifer-Region two") Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two Agenda Overview of the Client Assistance Program 1 2 3 4 Rehabilitation Act of 1973 Vocational Rehabilitation Process

Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two Agenda Overview of the Client Assistance Program 1 2 3 4 Rehabilitation Act of 1973 Vocational Rehabilitation Process

Alameda County Mental Health Plan 2025 Fairmont San Leandro, CA 94578 Local: (510) 346-1010 ACCESS Toll-free: (800) 491-9099

346-1010 ACCESS Toll-free: (800) 491-9099") Access Units for All California Counties Providers who verify that clients have Medi-Cal from counties other than San Bernardino should contact the county corresponding to the client s Medi-Cal status

Access Units for All California Counties Providers who verify that clients have Medi-Cal from counties other than San Bernardino should contact the county corresponding to the client s Medi-Cal status

Taxpayer Services Division Technical Services Bureau

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau GUIDELINES FOR BULK SALES TRANSACTIONS This memorandum highlights and summarizes the rights, obligations,

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau GUIDELINES FOR BULK SALES TRANSACTIONS This memorandum highlights and summarizes the rights, obligations,

California Foreclosure and Eviction Process. CACTTC Annual Conference June 11, 2008

California Foreclosure and Eviction Process CACTTC Annual Conference June 11, 2008 California s 58 Counties California Foreclosure Timeline California Foreclosure Process STAGE 1 3 MONTH PERIOD Day 1-90

California Foreclosure and Eviction Process CACTTC Annual Conference June 11, 2008 California s 58 Counties California Foreclosure Timeline California Foreclosure Process STAGE 1 3 MONTH PERIOD Day 1-90

Your Workers Compensation Benefits

Your Workers Compensation Benefits CALIFORNIA This form should be given to all newly hired employees in the State of California. Its content applies to industrial injuries on or after January 1, 2013.

Your Workers Compensation Benefits CALIFORNIA This form should be given to all newly hired employees in the State of California. Its content applies to industrial injuries on or after January 1, 2013.

Avoiding Common Sales and Use Tax Problems

State Board Of Equalization Avoiding Common Sales and Use Tax Problems This presentation is designed to help you avoid some of the most common sales and use tax mistakes. The Board of Equalization maintains

State Board Of Equalization Avoiding Common Sales and Use Tax Problems This presentation is designed to help you avoid some of the most common sales and use tax mistakes. The Board of Equalization maintains

If you have kept your shares at the default service provider, Morgan Stanley, please refer to this document for service feature details.

Morgan Stanley Services Information provided in the summary is solely being provided as a means of educating employees about Morgan Stanley s default service provider role in administering the stock plan

Morgan Stanley Services Information provided in the summary is solely being provided as a means of educating employees about Morgan Stanley s default service provider role in administering the stock plan

Lowndes County Licensing and Tax Guide

Lowndes County Licensing and Tax Guide Contents: Business Licenses 1 Zoning 1 Building Construction/Occupancy 2 Health Permits 2 Tradename Registration 2 Federal Licenses 3 State Licenses 4 Sales and Use

Lowndes County Licensing and Tax Guide Contents: Business Licenses 1 Zoning 1 Building Construction/Occupancy 2 Health Permits 2 Tradename Registration 2 Federal Licenses 3 State Licenses 4 Sales and Use

Personal Physician Predesignation and March 2006 Change of Physician Rules Approved

Briefing Personal Physician Predesignation and March 2006 Change of Physician Rules Approved On March 14, 2006, The California Office of Administrative Law Department approved new rules and regulations

Briefing Personal Physician Predesignation and March 2006 Change of Physician Rules Approved On March 14, 2006, The California Office of Administrative Law Department approved new rules and regulations

Date. Name Street City, State Zip. Dear Member:

C Benefit Services Division P.O. Box 942711 Sacramento, CA 94229-2711 888 CalPERS (or 888-225-7377) Reply To: Section 445 TDD - (916) 795-3240; FAX (916) 795-3988 Date Name Street City, State Zip Dear

C Benefit Services Division P.O. Box 942711 Sacramento, CA 94229-2711 888 CalPERS (or 888-225-7377) Reply To: Section 445 TDD - (916) 795-3240; FAX (916) 795-3988 Date Name Street City, State Zip Dear

COMPANY NAME CITY ST PHONE ABC Supply Co Inc Fort Mohave AZ 520 768-8383 RSG Gilbert AZ 480 557-6309 ABC Supply Co Inc Glendale AZ 602 934-7320

COMPANY NAME CITY ST PHONE ABC Supply Co Inc Fort Mohave AZ 520 768-8383 RSG Gilbert AZ 480 557-6309 ABC Supply Co Inc Glendale AZ 602 934-7320 Bradco Supply Glendale AZ 623 931-7950 Pacific Supply Glendale

COMPANY NAME CITY ST PHONE ABC Supply Co Inc Fort Mohave AZ 520 768-8383 RSG Gilbert AZ 480 557-6309 ABC Supply Co Inc Glendale AZ 602 934-7320 Bradco Supply Glendale AZ 623 931-7950 Pacific Supply Glendale

DISABILITY INSURANCE PROVISIONS

DISABILITY INSURANCE PROVISIONS DE 2515 Rev. 57 (11-09) (INTERNET) Cover + 5 Pages CU/GA 892 B Disability is any illness or injury, either physical or mental, that prevents you from doing your regular

DISABILITY INSURANCE PROVISIONS DE 2515 Rev. 57 (11-09) (INTERNET) Cover + 5 Pages CU/GA 892 B Disability is any illness or injury, either physical or mental, that prevents you from doing your regular

COMPANY NAME : SHY CREATION, INC. Distributor of Fine Jewelry 650 S. Hill St. Ste. 428 Los Angeles, CA 90014 TEL: (213)623-8900; FAX: (213)623-0860

623-8900; FAX: (213)623-0860") COMPANY NAME : SHY CREATION, INC. Distributor of Fine Jewelry 650 S. Hill St. Ste. 428 Los Angeles, CA 90014 TEL: (213)623-8900; FAX: (213)623-0860 Thank you for your interest in Shy Creation. Please provide

COMPANY NAME : SHY CREATION, INC. Distributor of Fine Jewelry 650 S. Hill St. Ste. 428 Los Angeles, CA 90014 TEL: (213)623-8900; FAX: (213)623-0860 Thank you for your interest in Shy Creation. Please provide

Bank of Brodhead PO Box 108 806 E Exchange St Brodhead WI 53520-0108

Bank of Brodhead PO Box 108 806 E Exchange St Brodhead WI 53520-0108 Consumer Internet Banking Agreement and Disclosures 1. Coverage. This Agreement applies to your use of our Online Banking Service ("Internet

Bank of Brodhead PO Box 108 806 E Exchange St Brodhead WI 53520-0108 Consumer Internet Banking Agreement and Disclosures 1. Coverage. This Agreement applies to your use of our Online Banking Service ("Internet

How To Get A Workers Compensation Insurance In California

Almost every employed Californian is protected by workers compensation for job related injuries or illness. Therefore it s important that both employer and employees understand workers compensation insurance.

Almost every employed Californian is protected by workers compensation for job related injuries or illness. Therefore it s important that both employer and employees understand workers compensation insurance.

Connecticut Tax Issues An Overview for Property Developers and Managers

Connecticut Tax Issues An Overview for Property Developers and Managers Felicia S. Hoeniger, Esq. Robinson & Cole Michael J. O Sullivan, Assistant Director, Appellate Division Connecticut Department of

Connecticut Tax Issues An Overview for Property Developers and Managers Felicia S. Hoeniger, Esq. Robinson & Cole Michael J. O Sullivan, Assistant Director, Appellate Division Connecticut Department of

PST-5 Issued: June 1984 Revised: August 2015 GENERAL INFORMATION

Information Bulletin PST-5 Issued: June 1984 Revised: August 2015 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT GENERAL INFORMATION Click here to complete our short READER SURVEY This bulletin

Information Bulletin PST-5 Issued: June 1984 Revised: August 2015 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT GENERAL INFORMATION Click here to complete our short READER SURVEY This bulletin

Homeowner Handbook. 88 King Street Burlington, Vermont 05401 802-862-6244

Homeowner Handbook 88 King Street Burlington, Vermont 05401 802-862-6244 January 2012 Table of Contents Review of the Ground Lease Page 2 Review of the Housing Subsidy Covenant Page 3 Lease and Membership

Homeowner Handbook 88 King Street Burlington, Vermont 05401 802-862-6244 January 2012 Table of Contents Review of the Ground Lease Page 2 Review of the Housing Subsidy Covenant Page 3 Lease and Membership

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware. By R. Scott Jones, Esq.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

State of California Franchise Tax Board. Real Estate Withholding Guidelines. FTB Pub. 1016 (REV 12-2003)

") State of California Franchise Tax Board Real Estate Withholding Guidelines FTB Pub. 1016 (REV 12-2003) For additional information, contact the Withholding Services and Compliance Section Telephone: (888)

State of California Franchise Tax Board Real Estate Withholding Guidelines FTB Pub. 1016 (REV 12-2003) For additional information, contact the Withholding Services and Compliance Section Telephone: (888)

FIRST DISTRICT DEAN F. ANDAL, STOCKTON SECOND DISTRICT CLAUDE PARRISH, TORRANCE THIRD DISTRICT JOHN CHIANG, LOS ANGELES

SPECIAL TOPIC SURVEY ASSESSMENT COORDINATION BETWEEN REAL PROPERTY AND BUSINESS PROPERTY DIVISIONS ON TENANT IMPROVEMENTS DECEMBER 1999 CALIFORNIA STATE BOARD OF EQUALIZATION JOHAN KLEHS, HAYWARD FIRST

SPECIAL TOPIC SURVEY ASSESSMENT COORDINATION BETWEEN REAL PROPERTY AND BUSINESS PROPERTY DIVISIONS ON TENANT IMPROVEMENTS DECEMBER 1999 CALIFORNIA STATE BOARD OF EQUALIZATION JOHAN KLEHS, HAYWARD FIRST

Payroll Tax Requirements

Payroll Tax Requirements 2016 Federal Payroll Tax Rates New federal income tax withholding tables will be issued for 2016. This information will be included in IRS Publication 15 (Circular E). FICA and

Payroll Tax Requirements 2016 Federal Payroll Tax Rates New federal income tax withholding tables will be issued for 2016. This information will be included in IRS Publication 15 (Circular E). FICA and

Appellate Lawyer s Directory

Appellate Lawyer s Directory Part 1: Projects, Appellate Courts & Attorney Listings A Publication of Central California Appellate Program 2011 Table of Contents -- Part 1 Appointed Counsel Projects.. 1

Appellate Lawyer s Directory Part 1: Projects, Appellate Courts & Attorney Listings A Publication of Central California Appellate Program 2011 Table of Contents -- Part 1 Appointed Counsel Projects.. 1

Sparkle Power Inc. 48502 Kato Road, Fremont, CA 94538

SPI Sales Rep: Lead Code in SAP CREDIT APPLICATION AND AGREEMENT (Revised 06/2009) INSTRUCTIONS: Please print or type. Form must be completed in all parts to be processed. If a corporation, the signature

SPI Sales Rep: Lead Code in SAP CREDIT APPLICATION AND AGREEMENT (Revised 06/2009) INSTRUCTIONS: Please print or type. Form must be completed in all parts to be processed. If a corporation, the signature

Step 1 of 3: Calculating Tax Due Box 1 Enter total gross sales and services on Nation Land (to nearest dollar; see in instructions)

") Federal Employer Identification Number (EIN) Legal name (print legal name as it appears on your Certificate of Authority) D/B/A (doing business as) name Street Address City, state, ZIP code Oneida Indian

Federal Employer Identification Number (EIN) Legal name (print legal name as it appears on your Certificate of Authority) D/B/A (doing business as) name Street Address City, state, ZIP code Oneida Indian

BULK SALES - BUYING AND SELLING BUSINESS ASSETS

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

BULLETIN NO. TAMTA 002 Issued October 2010 THE TAX ADMINISTRATION AND MISCELLANEOUS TAXES ACT BULK SALES - BUYING AND SELLING BUSINESS ASSETS This bulletin explains the seller s and buyer s requirements

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

A Guide to LLCs. Forming a Limited Liability Company

A Guide to LLCs Forming a Limited Liability Company Advantages of Forming an LLC Real Estate Investments and LLCs Operating and Maintaining an LLC Comparing LLCs to Other Business Structures Table of Contents

A Guide to LLCs Forming a Limited Liability Company Advantages of Forming an LLC Real Estate Investments and LLCs Operating and Maintaining an LLC Comparing LLCs to Other Business Structures Table of Contents

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY STATE OF HAWAII DEPARTMENT OF TAXATION Benjamin J. Cayetano Governor Ray K. Kamikawa Director of Taxation Revised June, 1998 A MESSAGE FROM THE DIRECTOR

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY STATE OF HAWAII DEPARTMENT OF TAXATION Benjamin J. Cayetano Governor Ray K. Kamikawa Director of Taxation Revised June, 1998 A MESSAGE FROM THE DIRECTOR

Lloyd Hara. Assessor BUSINESS PERSONAL PROPERTY LISTING INSTRUCTIONS FOR 2015

Department of Assessments Personal Property Section - Listing 500 Fourth Avenue, Room 736 Seattle, WA 98104-2384 personal.property@kingcounty.gov Lloyd Hara Assessor (PLAN) BUSINESS PERSONAL PROPERTY LISTING

Department of Assessments Personal Property Section - Listing 500 Fourth Avenue, Room 736 Seattle, WA 98104-2384 personal.property@kingcounty.gov Lloyd Hara Assessor (PLAN) BUSINESS PERSONAL PROPERTY LISTING

California PLACE ADDRESS LABEL HERE FRANCHISE TAX BOARD STATE OF CALIFORNIA. Forms & Instructions

PLACE ADDRESS LABEL HERE California Forms & Instructions 568 2007 Limited Liability Company Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Betty T. Yee, Member Michael C. Genest, Member

PLACE ADDRESS LABEL HERE California Forms & Instructions 568 2007 Limited Liability Company Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Betty T. Yee, Member Michael C. Genest, Member

Hotel Room Tax. Annual Growth

Hotel Room Tax Description The Hotel Room Tax (or transient occupancy tax ) is a 14 percent tax levied on hotel room charges. The tax is collected by hotel operators from guests and remitted to the Treasurer/Tax

Hotel Room Tax Description The Hotel Room Tax (or transient occupancy tax ) is a 14 percent tax levied on hotel room charges. The tax is collected by hotel operators from guests and remitted to the Treasurer/Tax

INVESTMENT ADVISORY AGREEMENT

The undersigned client ( I ) agrees to engage WealthStrategies Financial Advisors, LLC ( you ) as advisor for the Account(s) custodied with FOLIOfn Investments, Inc. ( Account(s) ) upon the following terms

The undersigned client ( I ) agrees to engage WealthStrategies Financial Advisors, LLC ( you ) as advisor for the Account(s) custodied with FOLIOfn Investments, Inc. ( Account(s) ) upon the following terms

California State Department of Fair Employment and Housing 611 West Sixth Street, 15th Floor Los Angeles, CA 90017 800-233-3212

California Housing Resources Provided by Consumer Action (www.consumer-action.org) Note: If any of the contact information here has changed, please email info@consumeraction.org B Bay Area Legal Aid 2

California Housing Resources Provided by Consumer Action (www.consumer-action.org) Note: If any of the contact information here has changed, please email info@consumeraction.org B Bay Area Legal Aid 2

If you had a loan serviced by Ocwen Loan Servicing, LLC, your rights may be affected by a class action settlement, including your right to money.

UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF CALIFORNIA If you had a loan serviced by Ocwen Loan Servicing, LLC, your rights may be affected by a class action settlement, including your right

UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF CALIFORNIA If you had a loan serviced by Ocwen Loan Servicing, LLC, your rights may be affected by a class action settlement, including your right

Annual Notice of Changes for 2014 (This 2014 Annual Notice of Changes is effective October 1, 2013 December 31, 2014.)

") Blue Shield 65 Plus (HMO) offered by Blue Shield of California Annual Notice of Changes for 2014 (This 2014 Annual Notice of Changes is effective October 1, 2013 December 31, 2014.) You are currently enrolled

Blue Shield 65 Plus (HMO) offered by Blue Shield of California Annual Notice of Changes for 2014 (This 2014 Annual Notice of Changes is effective October 1, 2013 December 31, 2014.) You are currently enrolled

2012 PAYROLL RATES AND LIMITS. Employee Withholding Rate Wage Base Dollar Amount

2012 PAYROLL RATES AND LIMITS Gross Maximum Employee Withholding Rate Wage Base Dollar Amount FICA/Social Security 4.20% * $110,100 $4,624.20 FICA/Medicare Portion 1.45% No Limit No Limit Total FICA 7.65%

2012 PAYROLL RATES AND LIMITS Gross Maximum Employee Withholding Rate Wage Base Dollar Amount FICA/Social Security 4.20% * $110,100 $4,624.20 FICA/Medicare Portion 1.45% No Limit No Limit Total FICA 7.65%

Shareowner Service Plus Plan SM Investment Brochure

Shareowner Service Plus Plan SM Investment Brochure CUSIP# 585055 10 6 Sponsored and Administered by Wells Fargo Shareowner Services Dear Shareholders and Interested Investors: Wells Fargo Shareowner Services

Shareowner Service Plus Plan SM Investment Brochure CUSIP# 585055 10 6 Sponsored and Administered by Wells Fargo Shareowner Services Dear Shareholders and Interested Investors: Wells Fargo Shareowner Services

PAUL, WEISS, RIFKIND, WHARTON & GARRISON LLP BASIC TAX ISSUES FOR A NEW BUSINESS IN NEW YORK CITY

PAUL, WEISS, RIFKIND, WHARTON & GARRISON LLP BASIC TAX ISSUES FOR A NEW BUSINESS IN NEW YORK CITY To ensure compliance with Internal Revenue Service Circular 230, you are hereby notified that: (a) any

PAUL, WEISS, RIFKIND, WHARTON & GARRISON LLP BASIC TAX ISSUES FOR A NEW BUSINESS IN NEW YORK CITY To ensure compliance with Internal Revenue Service Circular 230, you are hereby notified that: (a) any

Instructions West Virginia Sales & Use Tax Return (WV/CST-200CU)

") Instructions West Virginia Sales & Use Tax Return (WV/CST-200CU) General Instructions WV/CST-200CU is used to report or amend state and municipal sales and use taxes in West Virginia on tangible personal

Instructions West Virginia Sales & Use Tax Return (WV/CST-200CU) General Instructions WV/CST-200CU is used to report or amend state and municipal sales and use taxes in West Virginia on tangible personal

Key Features of the Elevate General Investment Account and the Elevate Stocks & Shares Individual Savings Account

Elevate Key Features of the Elevate General Investment Account and the Elevate Stocks & Shares Individual Savings Account Important Information The Financial Conduct Authority (FCA) is a financial services

Elevate Key Features of the Elevate General Investment Account and the Elevate Stocks & Shares Individual Savings Account Important Information The Financial Conduct Authority (FCA) is a financial services

A Guide to Your CalPERS. Temporary Annuity

A Guide to Your CalPERS Temporary Annuity This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS Introduction...2 How Does It Work?....2 Am I Eligible?....2 How Much

A Guide to Your CalPERS Temporary Annuity This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS Introduction...2 How Does It Work?....2 Am I Eligible?....2 How Much

PC Connect Agreement & Disclosure Receipt of Disclosures Equipment Requirements Definition of Business Day

PC Connect Agreement & Disclosure This agreement provides information about the Sutter Community Bank PC Connect Online banking service and contains the disclosures required by the Electronic Funds Transfer

PC Connect Agreement & Disclosure This agreement provides information about the Sutter Community Bank PC Connect Online banking service and contains the disclosures required by the Electronic Funds Transfer

(c) The statutory provisions for taxation of personal income are contained within Revenue and Taxation Code sections 17001 to 18181 inclusive.

The statutory provisions for taxation of personal income are contained within Revenue and Taxation Code sections 17001 to 18181 inclusive.") SECTION 1. STATEMENT OF FINDINGS (a) Our state Revenue and Taxation Code provides for the taxation of personal income, corporate income and gross receipts or sales price of tangible personal property sold

SECTION 1. STATEMENT OF FINDINGS (a) Our state Revenue and Taxation Code provides for the taxation of personal income, corporate income and gross receipts or sales price of tangible personal property sold

Real Estate Withholding Guidelines

State of California Franchise Tax Board FTB Publication 1016 Real Estate Withholding Guidelines Contents Purpose... 2 Legal Authority... 2 General Information... 2 Definitions... 2 Real Estate Withholding

State of California Franchise Tax Board FTB Publication 1016 Real Estate Withholding Guidelines Contents Purpose... 2 Legal Authority... 2 General Information... 2 Definitions... 2 Real Estate Withholding

Important information. Key Features of the Prudential International Investment Portfolio (Capital Redemption Option)

") Important information Key Features of the Prudential International Investment Portfolio (Capital Redemption Option) > Contents About this booklet 4 About the Prudential International Investment Portfolio

Important information Key Features of the Prudential International Investment Portfolio (Capital Redemption Option) > Contents About this booklet 4 About the Prudential International Investment Portfolio

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD This agreement and disclosure applies to payment orders and funds transfers governed by the Electronic Fund Transfer Act.

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE PERSONAL CHECK and/or ATM CARD This agreement and disclosure applies to payment orders and funds transfers governed by the Electronic Fund Transfer Act.

Limited Liability Company Filing Information. General LLC Information. Annual Fee. Annual Tax

STATE OF CALIFORNIA SACRAMENTO CA 94257-0540 General LLC Information Limited liability companies (LLCs) combine traditional corporate and partnership characteristics. The Beverly-Killea Limited Liability

STATE OF CALIFORNIA SACRAMENTO CA 94257-0540 General LLC Information Limited liability companies (LLCs) combine traditional corporate and partnership characteristics. The Beverly-Killea Limited Liability

Sales & Use Tax Questions for the Business Person. Publication 53B May 2012

10 Sales & Use Tax Questions for the Business Person Publication 53B May 2012 1 Q. My business purchases supplies from an out-of-state vendor who then ships the property to my California business. Are

10 Sales & Use Tax Questions for the Business Person Publication 53B May 2012 1 Q. My business purchases supplies from an out-of-state vendor who then ships the property to my California business. Are

Disability Rights California

Disability Rights California California s protection and advocacy system BAY AREA REGIONAL OFFICE 1330 Broadway, Suite 500 Oakland, CA 94612 Tel: (510) 267-1200 TTY: (800) 719-5798 Toll Free: (800) 776-5746

Disability Rights California California s protection and advocacy system BAY AREA REGIONAL OFFICE 1330 Broadway, Suite 500 Oakland, CA 94612 Tel: (510) 267-1200 TTY: (800) 719-5798 Toll Free: (800) 776-5746

Limited Liability Company Filing Information. LLCs are not subject to the annual tax and fee if. both of the following are true:

STATE OF CALIFORNIA SACRAMENTO CA 95827-0540 General LLC Information Limited liability companies (LLCs) combine traditional corporate and partnership characteristics. The California Revised Uniform Limited

STATE OF CALIFORNIA SACRAMENTO CA 95827-0540 General LLC Information Limited liability companies (LLCs) combine traditional corporate and partnership characteristics. The California Revised Uniform Limited

Checking Account Overdraft Agreement

Checking Account Overdraft Agreement Account Name Account Number Share # This Overdraft Agreement ("Agreement") describes the circumstances when we (the Credit Union) will pay overdrafts in your checking

Checking Account Overdraft Agreement Account Name Account Number Share # This Overdraft Agreement ("Agreement") describes the circumstances when we (the Credit Union) will pay overdrafts in your checking

Copyright Prop 65 News. All Rights Reserved.

A TTOR NEYS June 16, 2014 The Kroger Co. do CSC Lawyers Incorporating Service 2710 Gateway Oaks Dr., Ste 150N Sacramento, CA 95833 Re: NOTICE OF VIOLATION AGAINST THE KROGER CO., OF CALIFORNIA HEALTH &

A TTOR NEYS June 16, 2014 The Kroger Co. do CSC Lawyers Incorporating Service 2710 Gateway Oaks Dr., Ste 150N Sacramento, CA 95833 Re: NOTICE OF VIOLATION AGAINST THE KROGER CO., OF CALIFORNIA HEALTH &

Starting a Small Business in SC

Starting a Small Business in SC Search DOR A General Tax Guide for Starting a Small Business in SC Alcohol Beverage Licensing Bingo Business Registration Forms Corporate Estate Tax Fiduciary Individual

Starting a Small Business in SC Search DOR A General Tax Guide for Starting a Small Business in SC Alcohol Beverage Licensing Bingo Business Registration Forms Corporate Estate Tax Fiduciary Individual

GENERAL REGISTRATION APPLICATION - BUSINESS INFORMATION

GENERAL REGISTRATION APPLICATION - BUSINESS INFORMATION ENCLOSURES REQUIRED WITH THIS FORM a) Evidence of business status (i.e., Articles of Incorporation, Certificate of Limited Partnership, Articles

GENERAL REGISTRATION APPLICATION - BUSINESS INFORMATION ENCLOSURES REQUIRED WITH THIS FORM a) Evidence of business status (i.e., Articles of Incorporation, Certificate of Limited Partnership, Articles

Appendix D: Register of Federal & State Government Unit Addresses [FRBP 5003(e)]

![Appendix D: Register of Federal & State Government Unit Addresses [FRBP 5003(e)]](/thumbs/24/3881250.jpg "Appendix D: Register of Federal & State Government Unit Addresses [FRBP 5003(e)]") : Register of Federal & State Government Unit Addresses [FRBP 5003(e)] Court Manual D-1 January 2015 This Page Intentionally Left Blank Court Manual D-2 January 2015 1.0 Federal Rules of Bankruptcy Procedure

: Register of Federal & State Government Unit Addresses [FRBP 5003(e)] Court Manual D-1 January 2015 This Page Intentionally Left Blank Court Manual D-2 January 2015 1.0 Federal Rules of Bankruptcy Procedure

REIMBURSEMENT MEMORANDUM OF AGREEMENT (STATE AND LOCAL GOVERNMENT ENTITY)

") REIMBURSEMENT MEMORANDUM OF AGREEMENT (STATE AND LOCAL GOVERNMENT ENTITY) I. Parties This Memorandum of Agreement (MOA) and the attached USCIS SAVE Non-Federal Submission Form constitute the complete MOA

REIMBURSEMENT MEMORANDUM OF AGREEMENT (STATE AND LOCAL GOVERNMENT ENTITY) I. Parties This Memorandum of Agreement (MOA) and the attached USCIS SAVE Non-Federal Submission Form constitute the complete MOA

Business tax tip #4 If You Make Purchases for Resale

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Business tax tip #4 If You Make Purchases for Resale If you're a buyer... Does my sales and use tax license entitle me to make purchases without paying sales and use tax? No. Contrary to what many people

Member information Date Name Street City, State Zip. Dear Member:

C Benefit Services Division P.O. Box 942711 Sacramento, CA 94229-2711 888 CalPERS (or 888-225-7377) Reply To: Section 445 TDD - (916) 795-3240; FAX (916) 795-3988 Member information Date Name Street City,

C Benefit Services Division P.O. Box 942711 Sacramento, CA 94229-2711 888 CalPERS (or 888-225-7377) Reply To: Section 445 TDD - (916) 795-3240; FAX (916) 795-3988 Member information Date Name Street City,

A Guide to CalPERS. Employment After Retirement

A Guide to CalPERS Employment After Retirement This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS What Retirees Should Know Before Working After Retirement...2 All

A Guide to CalPERS Employment After Retirement This page intentionally left blank to facilitate double-sided printing. TABLE OF CONTENTS What Retirees Should Know Before Working After Retirement...2 All

Computershare Investment Plan

Genuine Parts Company Common Stock Computershare Investment Plan A Dividend Reinvestment Plan for registered shareholders This plan is sponsored and administered by Computershare Trust Company, N.A. Not

Genuine Parts Company Common Stock Computershare Investment Plan A Dividend Reinvestment Plan for registered shareholders This plan is sponsored and administered by Computershare Trust Company, N.A. Not

Senior Workers Compensation Payroll Auditor

Department(s): Senior Workers Compensation Payroll Auditor (DEPARTMENTAL PROMOTIONAL) 9399-00109324-30346KP State Compensation Insurance Fund-HDQTRS Opening Date: 09/21/2012 8:00:00 AM Closing Date: 10/12/2012

Department(s): Senior Workers Compensation Payroll Auditor (DEPARTMENTAL PROMOTIONAL) 9399-00109324-30346KP State Compensation Insurance Fund-HDQTRS Opening Date: 09/21/2012 8:00:00 AM Closing Date: 10/12/2012

NOTICE OF PUBLIC HEARING SUBJECT: ROUTES FOR THE THROUGH TRANSPORTATION OF HIGHWAY ROUTE CONTROLLED QUANTITY SHIPMENTS OF RADIOACTIVE MATERIALS

NOTICE OF PUBLIC HEARING SUBJECT: ROUTES FOR THE THROUGH TRANSPORTATION OF HIGHWAY ROUTE CONTROLLED QUANTITY SHIPMENTS OF RADIOACTIVE MATERIALS The California Highway Patrol (CHP) proposes to adopt regulations

NOTICE OF PUBLIC HEARING SUBJECT: ROUTES FOR THE THROUGH TRANSPORTATION OF HIGHWAY ROUTE CONTROLLED QUANTITY SHIPMENTS OF RADIOACTIVE MATERIALS The California Highway Patrol (CHP) proposes to adopt regulations

Estados Unidos CALIFORNIA. Lesiones de trabajo. Salario mínimo, pago de salarios, trabajo de menores. Ayuda especial a trabajadores agrícolas

CALIFORNIA Salario mínimo, pago de salarios, trabajo de menores Oficina estatal Oficina principal 455 Golden Gate Avenue, 8th Floor, San Francisco, CA 94102 Tel.: (415) 703-5300 Los Angeles 320 W 4th Street,

CALIFORNIA Salario mínimo, pago de salarios, trabajo de menores Oficina estatal Oficina principal 455 Golden Gate Avenue, 8th Floor, San Francisco, CA 94102 Tel.: (415) 703-5300 Los Angeles 320 W 4th Street,

NUC-1 Illinois Business Registration

Illinois Department of Revenue NUC-1 Illinois Business Registration Read this information first You must read the instructions before completing this form. Be sure to complete all of the information that

Illinois Department of Revenue NUC-1 Illinois Business Registration Read this information first You must read the instructions before completing this form. Be sure to complete all of the information that

Admin 101 Participant Directory 2014

Counselor, Outreach, Degree and Transfer Pasadena City College Associate Director Rancho Santiago CCD Coordinator of Outreach & Recruitment LA City College Business Services Supervisor San Jose City College

Counselor, Outreach, Degree and Transfer Pasadena City College Associate Director Rancho Santiago CCD Coordinator of Outreach & Recruitment LA City College Business Services Supervisor San Jose City College

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO FILE AN APPLICATION FOR CHANGED ASSESSMENT An Informational Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

ASSESSMENT APPEALS BOARD COUNTY OF SANTA BARBARA HOW TO FILE AN APPLICATION FOR CHANGED ASSESSMENT An Informational Guide For Santa Barbara County Property Owners and Authorized Agents Assessment Appeals

CALIFORNIA STATE BOARD OF EQUALIZATION APPEALS DIVISION FINAL ACTION SUMMARY ) ) ) ) ) ) ) )

) ) ) ) ) ) )") CALIFORNIA STATE BOARD OF EQUALIZATION APPEALS DIVISION FINAL ACTION SUMMARY In the Matter of the Petition for Redetermination Under the Sales and Use Tax Law of: GURMAIL SINGH Petitioner Account Number:

CALIFORNIA STATE BOARD OF EQUALIZATION APPEALS DIVISION FINAL ACTION SUMMARY In the Matter of the Petition for Redetermination Under the Sales and Use Tax Law of: GURMAIL SINGH Petitioner Account Number:

Appendix B Sample Contract for Deed. This Agreement, made this day of, between, called Seller,

Appendix B Sample Contract for Deed This Agreement, made this day of, between, called Seller, whose address is [NUMBER AND STREET] [CITY] [STATE] [ZIP], and, called Buyer, whose address is [NUMBER AND

Appendix B Sample Contract for Deed This Agreement, made this day of, between, called Seller, whose address is [NUMBER AND STREET] [CITY] [STATE] [ZIP], and, called Buyer, whose address is [NUMBER AND

Trust Estate Settlement Process

Trust Estate Settlement Process Settlement of a trust estate involves the process necessary to transfer asset ownership from the deceased person s trust to the parties entitled to receive the assets, according

Trust Estate Settlement Process Settlement of a trust estate involves the process necessary to transfer asset ownership from the deceased person s trust to the parties entitled to receive the assets, according

Regional Customer Service Center FasTrak License Agreement and Customer Terms and Conditions Revised July 1, 2015

Application and License Agreement Please read this Application and License Agreement carefully. By opening a FasTrak account and using the FasTrak Toll Tag or FasTrak Flex Toll Tag, you agree to the following

Application and License Agreement Please read this Application and License Agreement carefully. By opening a FasTrak account and using the FasTrak Toll Tag or FasTrak Flex Toll Tag, you agree to the following

(7) For taxable years beginning after December 31, 2012, every. nonresident estate having for the taxable year any gross income

For taxable years beginning after December 31, 2012, every. nonresident estate having for the taxable year any gross income") IC 6-3-4 Chapter 4. Returns and Remittances IC 6-3-4-1 Who must make returns Sec. 1. Returns with respect to taxes imposed by this act shall be made by the following: (1) Every resident individual having

IC 6-3-4 Chapter 4. Returns and Remittances IC 6-3-4-1 Who must make returns Sec. 1. Returns with respect to taxes imposed by this act shall be made by the following: (1) Every resident individual having

Required Reports Regarding Healthcare-Related Services (AA-2015-08)

") Academic and Student Affairs 401 Golden Shore, 6th Floor Long Beach, CA 90802-4210 www.calstate.edu Loren J. Blanchard Executive Vice Chancellor Tel: 562-951-4710 Email lblanchard@calstate.edu Code: M

Academic and Student Affairs 401 Golden Shore, 6th Floor Long Beach, CA 90802-4210 www.calstate.edu Loren J. Blanchard Executive Vice Chancellor Tel: 562-951-4710 Email lblanchard@calstate.edu Code: M

California Department of Corrections and Rehabilitation Bid No. 110004 Treatment Service Areas Exhibit A-2

Region I North: 335 Parolees Alpine, Amador, Butte, Calaveras, Colusa, El Dorado, Glenn, Lassen, Modoc, Nevada, Placer, Plumas, Sacramento, San Joaquin, Shasta, Sierra, Siskiyou, Sutter, Tehama, Trinity,

Region I North: 335 Parolees Alpine, Amador, Butte, Calaveras, Colusa, El Dorado, Glenn, Lassen, Modoc, Nevada, Placer, Plumas, Sacramento, San Joaquin, Shasta, Sierra, Siskiyou, Sutter, Tehama, Trinity,

National Margin Lending. Make your investment portfolio work for you

National Margin Lending Make your investment portfolio work for you Contents What is Margin Lending? 3 Why choose National Margin lending? 5 Why gear? 6 How much can you borrow with National Margin Lending?

National Margin Lending Make your investment portfolio work for you Contents What is Margin Lending? 3 Why choose National Margin lending? 5 Why gear? 6 How much can you borrow with National Margin Lending?

This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters.

Letter This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters. Subject: Demand for payment and intent to levy wages This letter is to notify you of a debt referred

Letter This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters. Subject: Demand for payment and intent to levy wages This letter is to notify you of a debt referred

Sales Associate Course. Brokerage Activities and Procedures

Sales Associate Course Chapter Five Brokerage Activities and Procedures 1 Brokerage Offices All active brokers must maintain an office Requirements Registered with the Department of Business and Professional

Sales Associate Course Chapter Five Brokerage Activities and Procedures 1 Brokerage Offices All active brokers must maintain an office Requirements Registered with the Department of Business and Professional

Notice of Requirements for Chapter 11 Debtors in Possession ( Notice of Requirements )

") U.S. Department of Justice United States Trustee Central District of California 411 W. Fourth St. 725 S. Figueroa St. 3801 University Ave. 21051 Warner Center Lane Suite 9041 Suite 2600 Suite 720 Suite

U.S. Department of Justice United States Trustee Central District of California 411 W. Fourth St. 725 S. Figueroa St. 3801 University Ave. 21051 Warner Center Lane Suite 9041 Suite 2600 Suite 720 Suite

Cities of: Costa Mesa (safety only) Fresno Pasadena San Diego San Jose. Page 1 of 4. my CalPERS 0802

Fresno Pasadena San Diego San Jose. Page 1 of 4. my CalPERS 0802") If you are in the process or have already separated from all CalPERS-covered employment, you will need to consider whether you want to keep your retirement contributions on deposit with CalPERS or receive

If you are in the process or have already separated from all CalPERS-covered employment, you will need to consider whether you want to keep your retirement contributions on deposit with CalPERS or receive

State of California Franchise Tax Board. Audit / Protest / Appeals (The process)

") State of California Franchise Tax Board Audit / Protest / Appeals (The process) Table of Contents Introduction / 3 Before the Audit / 4 Audit Procedures / 5 After the Audit / 10 Notice of Proposed Assessment

State of California Franchise Tax Board Audit / Protest / Appeals (The process) Table of Contents Introduction / 3 Before the Audit / 4 Audit Procedures / 5 After the Audit / 10 Notice of Proposed Assessment

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

LICENSING & PERMITS LAS VEGAS, NORTH LAS VEGAS, HENDERSON, BOULDER CITY, MESQUITE AND CLARK COUNTY These are the suggested steps along with a listing and a brief description of each of the forms and filings

Vanguard SEP-IRA Installment Distribution Request

Vanguard SEP-IRA Installment Distribution Request SIIDR Effective July 2014 Print clearly, preferably in capital letters and black ink. Complete this form to authorize Vanguard to initiate a series of

Vanguard SEP-IRA Installment Distribution Request SIIDR Effective July 2014 Print clearly, preferably in capital letters and black ink. Complete this form to authorize Vanguard to initiate a series of

All You Need to Know About Obtaining and Maintaining your California Contractor s License

All You Need to Know About Obtaining and Maintaining your California Contractor s License California law requires that all contractors operating in the State be properly licensed by the Contractors State

All You Need to Know About Obtaining and Maintaining your California Contractor s License California law requires that all contractors operating in the State be properly licensed by the Contractors State