A&A UPDATE. February 6, 2016 Danielle Supkis Cheek & Sarah Elliott

|

|

|

- Marvin Hubbard

- 7 years ago

- Views:

Transcription

1 A&A UPDATE February 6, 2016 Danielle Supkis Cheek & Sarah Elliott

2 FASB Financial Accounting Standards Board

3 Revenue Recognition Five Steps 1. Identify the contract(s) with the customer Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services 2. Identify performance obligations 3. Determine the transaction price 4. Allocate the transaction price 5. Recognize revenue when performance obligation is satisfied

4 Why do I care now? Delayed effective date: Public companies (+ some non-profits + some benefit plans) Periods beginning after 12/15/17 (so 2018 calendar years) Other entities: +1 year (so 2019 calendar years) Public companies report 3 years of earnings, and if opt retrospective application (NOW!) (see full standard for full transition guidance)

Public companies report 3 years of earnings, and if opt retrospective")

5 ID the contract Determine price Recognize revenue ID the performance obligation Allocate price Contract must meet the following criteria: - Approved by both parties - Each party s rights are identifiable - Payment terms are identifiable - Contract has commercial substance - Collection is probable Two or more contracts should be combined when they are entered into near the same time with the same customer if one or more of the following criteria are met: - Contracts are negotiated as a package - Consideration in one contract depends on price or performance in the other - Goods or services in the contracts are a single performance obligation

6 ID the contract Determine price Recognize revenue ID the performance obligation Allocate price Promise to transfer a distinct good or service criteria Customer can benefit from good or service: On its own OR Together with other readily available goods or services (including goods or services previously acquired from entity) Promise is separately identifiable: Integration Modification or customization Highly dependent or interrelated

Promise is separately identifiable: Integration Modification or customization Highly dependent")

7 ID the contract Determine price Recognize revenue ID the performance obligation Allocate price Variable Consideration Significant Financing Non-Cash Consideration Consideration Payable to Customer Estimate using expected value, most likely amount, constraint Adjust consideration if timing provides customer or entity with significant benefit of financing Measure at fair value unless it cannot be reasonably estimated Reduction of the transaction price unless in exchange for a distinct good or service

8 ID the contract Determine price Recognize revenue ID the performance obligation Allocate price Allocate the amount to which the entity expects to be entitled to each performance obligation Relative standalone selling price basis Estimate selling prices if not observable Residual estimation techniques may be appropriate in certain situations Discounts and contingent amounts Allocate entirely to specific performance obligation if specified criteria met

9 ID the contract Determine price Recognize revenue ID the performance obligation Allocate price Recognize revenue as/when satisfy performance obligation by transferring good/service Over Time: A performance obligation is satisfied over time if one of the following criteria is met: The customer simultaneously receives and consumes the benefits as the entity performs The entity s performance creates or enhances an asset that the customer controls The asset does not have an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date Point in Time: All others Recognized at point in which customer obtains control. Indicators are: Present right to payment Legal title Physical possession Risk and reward of ownership Customer acceptance

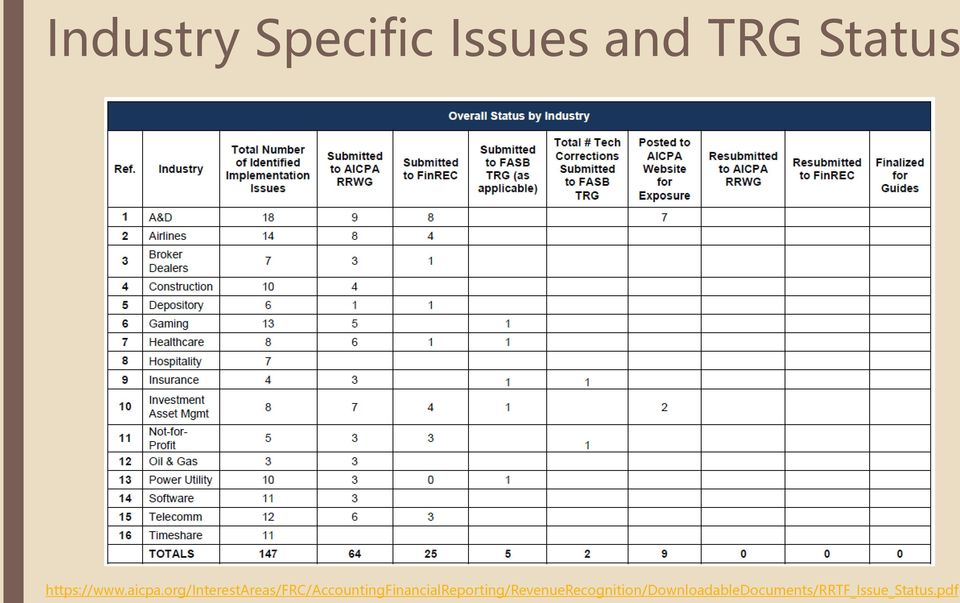

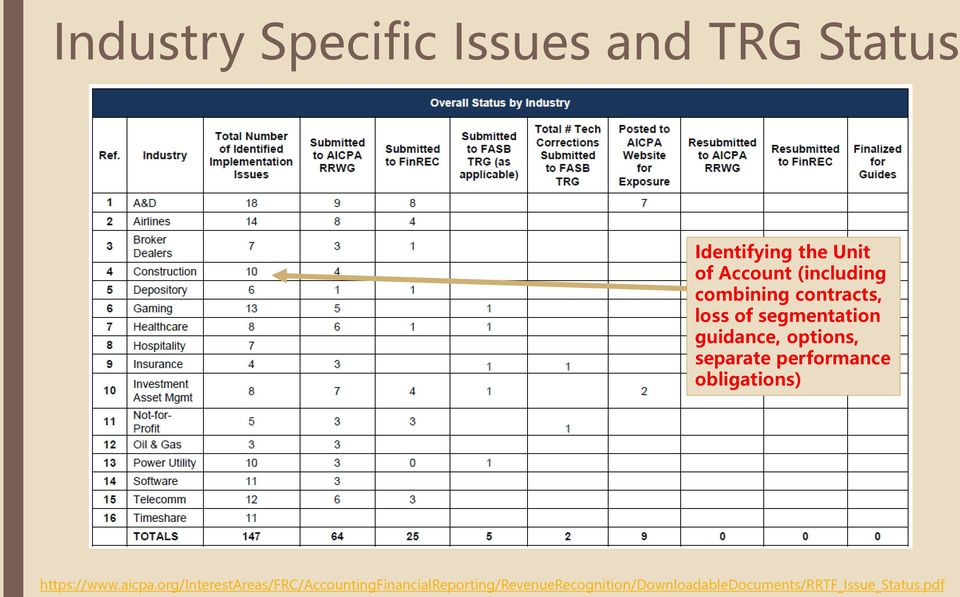

10 Industry Specific Issues and TRG Status

11 Industry Specific Issues and TRG Status Identifying the Unit of Account (including combining contracts, loss of segmentation guidance, options, separate performance obligations)

12 Narrow Scope Improvements & Practical Expedients Exposure Draft Comment Period Just Closed Collectability concerns in step 1 (makes it easier to meet collectability criteria to ability and intention to pay) Presentation of sales taxes collected (permit an accounting election to exclude amounts collected from sales taxes for all sales from transaction price) Non-cash consideration (fair value at contract inception) Contracts already completed or modified before transaction dates (various practical expedients) Transition disclosure technical correction (don t have to disclose the impact to the current period of adoption, only prior periods)

Transition disclosure technical correction (don t have to disclose the impact to the current period of adoption,")

13 Principal vs. Agent (gross vs. net) Reporting Exposure Draft Comment period closed An entity determines whether it is a principal or an agent for each specified good or service promised to the customer. An entity determines the nature of each specified good or service (e.g., whether it is a good, a service, or a right to a good or service). When another party is involved in providing goods or services to a customer, an entity that is a principal obtains control of: (a) a good or another asset from the other party that it then transfers to the customer; (b) a right to a service that will be performed by another party, which gives the entity the ability to direct that party to provide the service to the customer on the entity s behalf; or (c) a good or service from the other party that it combines with other goods or services to provide the specified good or service to the customer.

a good or another asset from the other party that it then transfers")

14 Center For Plain English Accounting Fortune Favors the Prepared Series on Revenue Recognition Industry specific articles Non profits Real estate More coming

15 Leases As of Nov 2015, Expecting Final Standard in Q and looking at effective dates of: A lease is a contract, or part of a contract, that conveys the right to control the use an identified asset (the underlying asset) for a period of time in exchange for consideration - Public companies years beginning after 12/15/18 (so 2019 calendar year) - Other entities: +1 year

- Other entities: +1")

16 Key Areas More changes in November 2015 made from the 2 nd ED Dual approach for lessee accounting (differs from IFRS) Type A Lease (today s capital lease) Record right to use asset and separate lease liability With amortization and interest expense separate New: Exception for leases that commence at or near end of underlying asset s economic life (last 25%) Type B Lease (today s operating lease) Record right to use asset and separate lease liability But get single lease expense on income statement (straight line) Exception for short term (<12 month leases) Can apply to leases at portfolio level Non-public entities can use risk free rate rather than incremental borrowing rate as the discount rate (only relief for non-publics)

http://www.fasb.")

17 Why do I care now? Lease agreement contract modification maybe required Debt covenants and other key ratios

18 PCC Preferability Removes effective date for all PCC Accounting Standards Updates (ASUs)! Therefore, not required to assess preferability to switch to a PCC alternative after the effective date for a 1 st time adoption (& transition guidance for goodwill and swaps extended) PCC Alternatives Goodwill amortization (ASU ) Interest rate swap simplifications (ASU ) Common control leasing arrangements (ASU ) Don t have to consider as VIEs Identifiable intangibles (ASU ) Do not have to separately recognize non-competes & customer related intangibles (unless than can be independently sold) Would still require preferability to switch back and forth

Do not have to separately recognize non-competes & customer related intangibles (unless than can")

19 Other Simplifications All allow for early adoption! Extraordinary Items gone! (ASU ) Inventory Measurement LCM (but market was replacement cost; net realizable value; NRC less normal profit margin) (ASU ) Now lower of cost or NRV Deferred taxes all DTAs & DTLs are non-current (ASU ) Debt issuance cost direct deduction to liability (ASU )

Debt issuance cost direct deduction to")

20 Going Concern Substantial doubt on ability to continue as going concern = probable that entity will be unable to meet its obligations as they come due. Management responsibility to assess ability to continue as a going concern from 1 year from date financial statements issued or available to be issued (NOT from the balance sheet date) based on information known or knowable at that time. Auditing issues But evaluate ability to continue as going concern of a reasonable period of time NOT to exceed one year beyond balance sheet date & other definition differences See ASB interpretations: ards/auditattest/pages/recentaainter pretations.aspx No more holding financials for a year Don t forget emphasis of matter paragraphs as needed

21 Debt Classification Simplicaition Exposure Draft Expected Q Got a debt covenant waiver exception but only on 4-3 vote. No wavier for after yearend debt refinances or certain acceleration clauses. The Board decided that an entity should classify a debt as noncurrent if one or both of the following criteria are met as of the balance sheet date: The liability is contractually due to be settled more than 12 months (or operating cycle, if longer) after the balance sheet date The entity has a contractual right to defer settlement of the liability for at least 12 months (or operating cycle, if longer) after the balance sheet date. The Board decided that decisions about the classification of debt should be made based on facts and circumstances that exist as of the reporting date (that is, as of the balance sheet date).

22 Non-Profit Presentation - 2 net assets classes (with and with out donor restrictions) - Operating vs. non-operating activities based on mission with transfers - Direct method cash flow REQUIRED (with changes to groupings) - Placed into service for release from restriction (rather than option for upon expenditure) - Disclosure changes (including require statement of functional expenses & liquidity disclosures) - Investment income net of expenses But excepting that it will be probably re- Source: KPMG Issues In Depth, May 2015, FASB s Proposed Changes to Not For Profits Financials

23 2x Materiality EDs #1: Conceptual Framework: Modify definition of materiality to a legal concept. As defined by US Supreme Court: - a substantial likelihood that the... fact would have been viewed by the reasonable investor as having significantly altered the "total mix" of information made available - delicate assessments of the inferences a 'reasonable shareholder' would draw from a given set of facts and the significance of those inferences to him... TSC Industries v. Northway, Inc., 426 U.S. 438, 449 (1976) & Basic, Inc. v. Levinson, 485 U.S. 224 (1988) #2: Notes to the Financial Statements materiality is applied to quantitative and qualitative disclosures individually and in the aggregate in the context of the financial statements taken as a whole; therefore, some, all, or none of the requirements in the disclosure section may be material refers to materiality as a legal concept state specifically that an omission of immaterial information is not an accounting error. Auditing Issues? Aggregate omissions Immaterial uncorrected misstatement Misstatement vs. error Management communications Peer review Issues? Remember uncertain tax provision

24 Other Exposure Drafts & Standards Recognition & Measurement of Financial Assets & Liabilities (final standard just released) Definition of a Business (comment period just closed) Cash Flows (ED just release last week, comment period until 3/29) Common Controlled Entities (ED expected Q1 2016) Share-Based Payments (final standard expected Q1 2016) Equity Method of Accounting (final standard expected Q1 2016) Hedging Simplifications (ED expected Q2 2016) Impairment of Financial Instruments (final standard expected Q2 2016) And More

25 FASB Technical Agenda As of February 3, 2016: Financial performance reporting Pensions & other post retirement employee benefit plans Intangible assets Distinguishing liabilities from equity Consolidations Inventory & costs of sales

26 GAAS & OTHER Generally Accepted Auditing Standards

27 GAAS & Other Uncertain tax provision disclosure changes (removed TPA ) Thank you CPEA! 5/Pages/elimination-of-the-disclosure.aspx Peer Review Board Exposure Draft (comment deadline ended 1/31) ents/improve_transparency_effectiveness_pr_ed.pdf Auditor s Report Dual reporting with IASB or PCAOB DOL reporting Direct Engagements Debate (Task force forming) Attest services without an assertion from management

28 General Overview of SSARS No. 21 Private Companies Practice Section 28

29 SSARS 21 Supersedes all existing AR sections except for AR Section 120, Compilation of Pro Forma Financial Information Prospective financial information is currently codified in Attest Standards The clarified SSARS on compilation of pro forma financial information was exposed for public comment in early December 2015 along with a proposed standard on compilation of prospective financial information. - The comment period ends on May 6, Final standards are expected to be issued in Q Effective for financial statement periods ending on or after December 15, 2015 Private Companies Practice Section 29

30 General Overview of SSARS 21 SSARS No. 21 is formatted into four separate sections: Section 60, General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services Section 70, Preparation of Financial Statements Section 80, Compilation Engagements Section 90, Review of Financial Statements These sections have been codified with the prefix AR- C to denote them from the pre-ssars No. 21 AR sections. Private Companies Practice Section 30

31 Section 70 Financial Statement Preparation Private Companies Practice Section 31

32 Section 70 Overview Non-attest financial statement preparation service Bright line between accounting services (preparation) and reporting services (compilation or review) Financial statements may be provided to third parties Private Companies Practice Section 32

33 Section 70 Overview Applies when engaged to prepare financial statements but not engaged to perform an audit, review, or compilation on those financial statements. Does not apply when engaged to merely assist in preparing financial statements the financial statements are prepared as a by-product of another engagement The understanding with the client as to what the engagement entails is important. Private Companies Practice Section 33

34 Section 70 Overview Examples of when AR-C 70 may apply Preparation of financial statements prior to audit or review by another accountant Preparation of financial statements to be presented alongside the tax return Preparation of personal financial statements for presentation alongside a financial plan Preparation of a single financial statement Using the information in a general ledger to prepare financial statements outside of an accounting software system Private Companies Practice Section 34

35 Section 70 Overview Examples of when AR-C 70 does not apply Preparation of financial statements when the accountant is engaged to perform an audit, review, or compilation of such financial statements Preparation of financial statements with a tax return solely for submission to taxing authorities Personal financial statements that are prepared for inclusion in written personal financial plans prepared by the accountant Financial statements prepared in conjunction with litigation services that involve pending or potential legal or regulatory proceedings Private Companies Practice Section 35

36 Section 70 Planning An engagement letter signed by both the accountant and management or those charged with governance is required No determination about independence is required Identify clients who may be interested in engaging us to perform preparation engagements. SSARS 8 engagements Accounting assistance Private Companies Practice Section 36

37 Section 70 Financial Statements Financial statements can be prepared with or without disclosures Disclose that substantially all disclosures are omitted If using a special purpose framework include a description Financial statements can be prepared with a known departure but must be disclosed Private Companies Practice Section 37

38 Section 70 Legend/Disclaimer No report is required, even if the financial statements are expected to be used by a third party A legend is required on each page of the financial statements indicating, at a minimum, no assurance is provided. Examples: No assurance is provided on these financial statements. These financial statements have not been subjected to an audit, review, or compilation engagement, and no assurance is provided on them. Other statements that convey that no assurance is provided on the financial statements are acceptable. The legend can be shown as headers or footers. Private Companies Practice Section 38

39 Section 80 Compilation Engagements Private Companies Practice Section 39

40 Section 80 Overview of Changes Applies when the accountant is engaged to perform a compilation engagement Some changes to the engagement letter and report A report is always required Engagements in which the accountant prepares financial statements but no report is required are covered by section 70 Accountant is no longer required to be concerned about distribution as they were with management use only financial statements (SSARS 8 engagements) Private Companies Practice Section 40

41 Section 90 Review Engagements Private Companies Practice Section 41

42 Section 90 Overview of Changes Some changes to the engagement letter Some changes to the management representation letter Some changes to fieldwork requirements Review report has been updated Expanded communications with management or those charged with governance Private Companies Practice Section 42

43 Reminders Obtain signed SSARS No. 21 engagement letters on year end 2015 engagements Ensure you re using the SSARS No. 21 reports for compilations and reviews on year end 2015 financial statements Ensure you re using the SSARS No. 21 management letters for reviews Talk to SSARS 8 engagements clients now to determine level of engagement Private Companies Practice Section 43

44 Questions? Private Companies Practice Section 44

45 DANIELLE SUPKIS CHEEK, CPA*, CFE, CVA D. SUPKIS CHEEK, PLLC Danielle Supkis Cheek is the founder D. Supkis Cheek, PLLC, a CPA firm specializing in the accounting, audit, and forensics needs for small and medium sized businesses. Danielle earned her Bachelors from Rice University in Houston, TX, and her Master of Science in Accountancy from the University of Virginia in Charlottesville, VA. She is a Certified Public Account (CPA) in the State of Texas, a Certified Fraud Examiner (CFE), and a Certified Valuation Analyst (CVA). Danielle is a Member of the PCPS Technical Issues Committee with the American Institute for CPAs, runs the National Office for the American Woman s Society of CPAs, was a recipient of the Woman of Excellence Award by the Federation of Houston Professional, was a 2014 Texas Society of CPA s Rising Star, is a 2015 and under 40 by the CPA Practice Advisor and a under 40 by the NACVA. Danielle is also passionate about teaching financial literacy and is VP of Finance for the Woman s Resource Center of Greater Houston (a financial literacy non-profit). In addition, she is an Adjunct Professor at Rice University s Jones School of Business teaching accounting for entrepreneurs. Danielle can be contacted at Danielle@SupkisCheek.com or * Licensed only in Texas

46 SARAH ELLIOTT, CPA ELLIVATE ADVISORS, LLC In her former role as a client service partner and member of leadership of a high-growth, regional accounting firm, Sarah discovered her true passion is building relationships and understanding and developing people. She also gained significant practical experience implementing and maintaining high quality professional development programming. In 2014, Sarah decided to combine her passion for the people side of her business and practical expertise to launch Ellivate Advisors. Ellivate Advisors is dedicated to elevating emerging leaders in the CPA profession to best in class through simple, high impact professional development programming. Ellivate Advisors parters with individuals and firms using two primary service offerings: professional coaching for emerging women leaders and strategic consulting focused on customizing professional development programming within firms. Prior to founding Ellivate Advisors, Sarah practiced public accounting for 14 years, including ten years at PricewaterhouseCoopers, LLP ( PwC ) where she performed a two year rotation in their National Office. While at PwC, Sarah served as a subject matter expert on PCAOB and AICPA standards and firm audit policy and methodology.

Revenue Recognition (Topic 605)

") Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

www.pwc.com Current Accounting and Reporting Developments Webcast Series Third Quarter 2015

www.pwc.com Current Accounting and Reporting Developments Webcast Series Third Quarter 2015 Welcome Beth Paul Accounting Services Group Team Leader Paula Loop Center for Board Governance and Investor Resource

www.pwc.com Current Accounting and Reporting Developments Webcast Series Third Quarter 2015 Welcome Beth Paul Accounting Services Group Team Leader Paula Loop Center for Board Governance and Investor Resource

No. 2014-09 May 2014. Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification

An Amendment of the FASB Accounting Standards Codification") No. 2014-09 May 2014 Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative

No. 2014-09 May 2014 Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative

Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80

Compilation of Financial Statements 2035 AR Section 9080 Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80 1. Reporting When There Are Significant Departures

Compilation of Financial Statements 2035 AR Section 9080 Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80 1. Reporting When There Are Significant Departures

IFRS 15: an overview of the new principles of revenue recognition

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

SPECIAL REPORT: Comprehensive Coverage of the New U.S. GAAP Revenue Recognition Requirements

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Accounting and Auditing Update 2014-18 (June 2014): SPECIAL REPORT: Comprehensive

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Accounting and Auditing Update 2014-18 (June 2014): SPECIAL REPORT: Comprehensive

New Accounting Standard Brings Big Changes to Lease Reporting on Financial Statements

New Accounting Standard Brings Big Changes to Lease Reporting on Financial Statements The Financial Accounting Standards Board (FASB) has issued its long-awaited update revising the proper treatment of

New Accounting Standard Brings Big Changes to Lease Reporting on Financial Statements The Financial Accounting Standards Board (FASB) has issued its long-awaited update revising the proper treatment of

Welcome. PrimeGlobal. Template for PowerPoint Slides Stacey Painter, CPA President, Loscalzo Associates. January 5, 2015

Welcome PrimeGlobal January 5, 2015 Loscalzo s FASB Updates 2012 Template for PowerPoint Slides Stacey Painter, CPA President, Loscalzo Associates A SmartPros Ltd. Company www.loscalzo.com (732) 741-1600

Welcome PrimeGlobal January 5, 2015 Loscalzo s FASB Updates 2012 Template for PowerPoint Slides Stacey Painter, CPA President, Loscalzo Associates A SmartPros Ltd. Company www.loscalzo.com (732) 741-1600

12/17/2015. FASB Update: Recent Developments in Financial Reporting INTRODUCTION INTRODUCTION. Presented by. Dave Koeppen & Troy Hyatt

FASB Update: Recent Developments in Financial Reporting Presented by Dave Koeppen & Troy Hyatt 2015 Boise State University 1 INTRODUCTION Simplification Projects ASU 2015-01: Simplifying Income Statement

FASB Update: Recent Developments in Financial Reporting Presented by Dave Koeppen & Troy Hyatt 2015 Boise State University 1 INTRODUCTION Simplification Projects ASU 2015-01: Simplifying Income Statement

What s On the FASB s Technical Agenda for 2016?

What s On the FASB s Technical Agenda for 2016? As you plan for the year ahead, you may wonder how changes to the accounting standards might affect the information you report on your company s financial

What s On the FASB s Technical Agenda for 2016? As you plan for the year ahead, you may wonder how changes to the accounting standards might affect the information you report on your company s financial

Understanding the New Revenue Recognition Model. Marion Adams, CPA Swenson Advisors, LLP

Understanding the New Revenue Recognition Model Marion Adams, CPA, LLP ASU No. 2014-09 Revenue from Contracts with Customers Overview May 28, 2014 - FASB and IASB issued converged guidance Will replace

Understanding the New Revenue Recognition Model Marion Adams, CPA, LLP ASU No. 2014-09 Revenue from Contracts with Customers Overview May 28, 2014 - FASB and IASB issued converged guidance Will replace

This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide.

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Proposed Statement of Financial Accounting Standards

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

Going concern. FASB defines management s going concern assessment and disclosure responsibilities. At a glance. Background

No. US2014-07 September 23, 2014 What s inside: Background... 1 Key provisions... 2 Disclosure threshold: Substantial doubt... 2 Consideration of management s plans... 4 Required disclosures... 6 What

No. US2014-07 September 23, 2014 What s inside: Background... 1 Key provisions... 2 Disclosure threshold: Substantial doubt... 2 Consideration of management s plans... 4 Required disclosures... 6 What

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

The Depository Trust Company

The Depository Trust Company Unaudited Condensed Consolidated Financial Statements as of March 31, 2016 and December 31, 2015 and for the three months ended March 31, 2016 and 2015 THE DEPOSITORY TRUST

The Depository Trust Company Unaudited Condensed Consolidated Financial Statements as of March 31, 2016 and December 31, 2015 and for the three months ended March 31, 2016 and 2015 THE DEPOSITORY TRUST

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

Stock based compensation guidance to increase income statement volatility (see update note below)

") Stock based compensation guidance to increase income statement volatility (see update note below) No. US2016 03 April 19, 2016 (Revised April 25, 2016) What s inside: Background. 1 Key provisions 2 Income

Stock based compensation guidance to increase income statement volatility (see update note below) No. US2016 03 April 19, 2016 (Revised April 25, 2016) What s inside: Background. 1 Key provisions 2 Income

ACCOUNTING ISSUES. Presenters:

ACCOUNTING ISSUES Presenters: Stephen Sommerville, Partner, PricewaterhouseCoopers LLP Donald Heisler, Partner, Deloitte & Touche LLP Diane M. Irvine, Director, INRIX, Inc., Rightside, XO Group, Inc.,

ACCOUNTING ISSUES Presenters: Stephen Sommerville, Partner, PricewaterhouseCoopers LLP Donald Heisler, Partner, Deloitte & Touche LLP Diane M. Irvine, Director, INRIX, Inc., Rightside, XO Group, Inc.,

Short term leases, defined as a lease term of one year or less, are to be accounted for under the same operating lease method that currently exists.

Lease Accounting Updated January 2014 Page 1 Lease Accounting The pending changes in lease accounting have been a hot topic item since 2009, when the Financial Accounting Standards Board (FASB) and International

Lease Accounting Updated January 2014 Page 1 Lease Accounting The pending changes in lease accounting have been a hot topic item since 2009, when the Financial Accounting Standards Board (FASB) and International

RELIANCE INDUSTRIES (MIDDLE EAST) DMCC 1. Reliance Industries (Middle East) DMCC Reports and Financial Statements for the year ended 31 December 2014

DMCC 1. Reliance Industries (Middle East) DMCC Reports and Financial Statements for the year ended 31 December 2014") RELIANCE INDUSTRIES (MIDDLE EAST) DMCC 1 Reliance Industries (Middle East) DMCC Reports and Financial Statements for the year ended 31 December 2014 2 RELIANCE INDUSTRIES (MIDDLE EAST) DMCC Independent

RELIANCE INDUSTRIES (MIDDLE EAST) DMCC 1 Reliance Industries (Middle East) DMCC Reports and Financial Statements for the year ended 31 December 2014 2 RELIANCE INDUSTRIES (MIDDLE EAST) DMCC Independent

Financial Accounting Series

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

AICPA Technical Hotline's Top A&A Issues Facing CPAs

AICPA Technical Hotline's Top A&A Issues Facing CPAs Kristy L. Illuzzi, CPA Frances S. McClintock, CPA Kristy L. Illuzzi, CPA Kristy Illuzzi moved to North Carolina and joined the AICPA in May 2007 as

AICPA Technical Hotline's Top A&A Issues Facing CPAs Kristy L. Illuzzi, CPA Frances S. McClintock, CPA Kristy L. Illuzzi, CPA Kristy Illuzzi moved to North Carolina and joined the AICPA in May 2007 as

SSARS 21 Review, Compilation, and Preparation of Financial Statements

SSARS 21 Review, Compilation, and Preparation of Financial Statements Course Objectives Provide background information that resulted in SSARS 21 Introduce new Preparation Standard Compare the Compilation

SSARS 21 Review, Compilation, and Preparation of Financial Statements Course Objectives Provide background information that resulted in SSARS 21 Introduce new Preparation Standard Compare the Compilation

Financial Instruments Where are we? Recognition and Measurement Impairment Derivatives

Financial Instruments Where are we? Recognition and Measurement Impairment Derivatives Susan Cosper Kirk Silva Mark LaMonte Robert Uhl Financial Instruments Needs Fixing? FASB issued a new standard on

Financial Instruments Where are we? Recognition and Measurement Impairment Derivatives Susan Cosper Kirk Silva Mark LaMonte Robert Uhl Financial Instruments Needs Fixing? FASB issued a new standard on

A Guide to for Financial Instruments in the Public Sector

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

LEASES DIVERGENT PATHS IFRS NEWSLETTER

IFRS NEWSLETTER LEASES Issue 14, March 2014 After eight years of working jointly, it now appears likely that a key outcome of the Boards leases project will be to make it harder to compare the financial

IFRS NEWSLETTER LEASES Issue 14, March 2014 After eight years of working jointly, it now appears likely that a key outcome of the Boards leases project will be to make it harder to compare the financial

Lease accounting update

Financial Executives International 22 March 2012 Agenda Where are we now? Timing? What are the proposed changes to lease accounting? Overview of implications and considerations What are companies doing

Financial Executives International 22 March 2012 Agenda Where are we now? Timing? What are the proposed changes to lease accounting? Overview of implications and considerations What are companies doing

New Developments Summary

April 2, 2014 NDS 2014-04 New Developments Summary Lessee consolidation of lessor entities under common control FASB provides long-requested relief to private companies Summary The FASB recently issued

April 2, 2014 NDS 2014-04 New Developments Summary Lessee consolidation of lessor entities under common control FASB provides long-requested relief to private companies Summary The FASB recently issued

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Private company variable interest entity relief

No. US2014-03 July 17, 2014 What s inside: Background... 1 Key provisions... 2 Common control... 3 Lease arrangement... 4 Leasing activities... 4 Sufficient collateral... 5 Examples... 6 Transition from

No. US2014-03 July 17, 2014 What s inside: Background... 1 Key provisions... 2 Common control... 3 Lease arrangement... 4 Leasing activities... 4 Sufficient collateral... 5 Examples... 6 Transition from

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Summary of Certain Differences between SFRS and US GAAP

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Defining Issues. FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting. March 2014, No. 14-17. Key Facts

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Defining Issues March 2014, No. 14-17 FASB and IASB Take Divergent Paths on Key Aspects of Lease Accounting At their March 18-19 meeting to redeliberate the proposals in their 2013 exposure drafts (EDs)

Revenue from contracts with customers

No. US2014-01 June 11, 2014 What s inside: Background... 1 Key provisions...2 Scope... 2 The five-step approach... 3 Step 1: Identify the contract(s)... 3 Step 2: Identify performance obligations... 5

No. US2014-01 June 11, 2014 What s inside: Background... 1 Key provisions...2 Scope... 2 The five-step approach... 3 Step 1: Identify the contract(s)... 3 Step 2: Identify performance obligations... 5

A guide to. accounting for. Second Edition. Assurance Tax Consulting

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

A guide to accounting for Business Combinations Second Edition Assurance Tax Consulting A guide to accounting for Business Combinations Second Edition January 2012 This publication is provided as an information

(unaudited expressed in Canadian Dollars)

") Condensed Consolidated Interim Financial Statements of CARGOJET INC. For the three month periods ended (unaudited expressed in Canadian Dollars) This page intentionally left blank Condensed Consolidated

Condensed Consolidated Interim Financial Statements of CARGOJET INC. For the three month periods ended (unaudited expressed in Canadian Dollars) This page intentionally left blank Condensed Consolidated

08FR-003 Business Combinations IFRS 3 revised 11 January 2008. Key points

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

NEED TO KNOW. Leases The 2013 Exposure Draft

NEED TO KNOW Leases The 2013 Exposure Draft 2 LEASES - THE 2013 EXPOSURE DRAFT TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main

NEED TO KNOW Leases The 2013 Exposure Draft 2 LEASES - THE 2013 EXPOSURE DRAFT TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main

NEED TO KNOW. Leases A Project Update

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

NEED TO KNOW Leases A Project Update 2 LEASES - A PROJECT UPDATE TABLE OF CONTENTS Introduction 3 Existing guidance and the rationale for change 4 The IASB/FASB project to date 5 The main proposals 6 Definition

Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement)

") FASB STAFF POSITION No. APB 14-1 Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) Date Posted: May 9, 2008 Introduction

FASB STAFF POSITION No. APB 14-1 Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) Date Posted: May 9, 2008 Introduction

Leases (Topic 840) Proposed Accounting Standards Update. Issued: August 17, 2010 Comments Due: December 15, 2010

Proposed Accounting Standards Update. Issued: August 17, 2010 Comments Due: December 15, 2010") Proposed Accounting Standards Update Issued: August 17, 2010 Comments Due: December 15, 2010 Leases (Topic 840) This Exposure Draft of a proposed Accounting Standards Update of Topic 840 is issued by the

Proposed Accounting Standards Update Issued: August 17, 2010 Comments Due: December 15, 2010 Leases (Topic 840) This Exposure Draft of a proposed Accounting Standards Update of Topic 840 is issued by the

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

LEASES PERMISSION TO BALLOT IFRS NEWSLETTER

IFRS NEWSLETTER LEASES Issue 17, March 2015 After almost ten years of joint work the IASB and the FASB have decided to ballot different lease accounting proposals. Kimber Bascom, KPMG s global IFRS leasing

IFRS NEWSLETTER LEASES Issue 17, March 2015 After almost ten years of joint work the IASB and the FASB have decided to ballot different lease accounting proposals. Kimber Bascom, KPMG s global IFRS leasing

INDEX TO FINANCIAL STATEMENTS. Balance Sheets as of June 30, 2015 and December 31, 2014 (Unaudited) F-2

F-2") INDEX TO FINANCIAL STATEMENTS Page Financial Statements Balance Sheets as of and December 31, 2014 (Unaudited) F-2 Statements of Operations for the three months ended and 2014 (Unaudited) F-3 Statements

INDEX TO FINANCIAL STATEMENTS Page Financial Statements Balance Sheets as of and December 31, 2014 (Unaudited) F-2 Statements of Operations for the three months ended and 2014 (Unaudited) F-3 Statements

Advanced Accounting Update on Business Combinations (Chapters 1-8) July 20, 2004

July 20, 2004") Advanced Accounting Update on Business Combinations (Chapters 1-8) July 20, 2004 Potential changes are listed by the chapter that they first impact. Bolded items are from sources other than the contemplated

Advanced Accounting Update on Business Combinations (Chapters 1-8) July 20, 2004 Potential changes are listed by the chapter that they first impact. Bolded items are from sources other than the contemplated

INTERNATIONAL STANDARD ON REVIEW ENGAGEMENTS 2410 REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY CONTENTS

INTERNATIONAL STANDARD ON ENGAGEMENTS 2410 OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY (Effective for reviews of interim financial information for periods beginning

INTERNATIONAL STANDARD ON ENGAGEMENTS 2410 OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY (Effective for reviews of interim financial information for periods beginning

Oil & Gas Spotlight Fueling Discussion About the FASB s New Revenue Recognition Standard

October 2014 Oil & Gas Spotlight Fueling Discussion About the FASB s New Revenue Recognition Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

October 2014 Oil & Gas Spotlight Fueling Discussion About the FASB s New Revenue Recognition Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

www.pwc.com/us/insurance New Revenue Recognition Rules How will they affect loyalty programs?

www.pwc.com/us/insurance New Revenue Recognition Rules How will they affect loyalty programs? In May 2014, the U.S. Financial Accounting Standards Board (FASB) and the International Accounting Standards

www.pwc.com/us/insurance New Revenue Recognition Rules How will they affect loyalty programs? In May 2014, the U.S. Financial Accounting Standards Board (FASB) and the International Accounting Standards

Lifting the fog* Accounting for uncertainty in income taxes

Lifting the fog* Accounting for uncertainty in income taxes Contents Introduction 01 Identifying uncertain tax positions 02 Recognizing uncertain tax positions 03 Measuring the tax benefit 04 Disclosures

Lifting the fog* Accounting for uncertainty in income taxes Contents Introduction 01 Identifying uncertain tax positions 02 Recognizing uncertain tax positions 03 Measuring the tax benefit 04 Disclosures

Danielle Supkis Cheek, CPA, CFE, CVA

EDUCATION Danielle Supkis Cheek, CPA, CFE, CVA www.supkischeek.com Danielle@SupkisCheek.com 701 N. Post Oak Rd. Suite 635 Houston, TX 77024 713-893-5625 University of Virginia, M.S. of Accountancy, Charlottesville,

EDUCATION Danielle Supkis Cheek, CPA, CFE, CVA www.supkischeek.com Danielle@SupkisCheek.com 701 N. Post Oak Rd. Suite 635 Houston, TX 77024 713-893-5625 University of Virginia, M.S. of Accountancy, Charlottesville,

3 4 5 6 FINANCIAL SECTION Five-Year Summary (Consolidated) TSUKISHIMA KIKAI CO., LTD. and its consolidated subsidiaries Years ended March 31 (Note 1) 2005 2004 2003 2002 2001 2005 For the year: Net sales...

3 4 5 6 FINANCIAL SECTION Five-Year Summary (Consolidated) TSUKISHIMA KIKAI CO., LTD. and its consolidated subsidiaries Years ended March 31 (Note 1) 2005 2004 2003 2002 2001 2005 For the year: Net sales...

Example Directors' Report, Auditor's Report and Illustrative Financial Statements for Private Entities prepared in accordance with the HKFRS for

Example Directors' Report, Auditor's Report and Illustrative Financial Statements for Private Entities prepared in accordance with the HKFRS for Private Entities (with Hong Kong Companies Ordinance disclosures)

Example Directors' Report, Auditor's Report and Illustrative Financial Statements for Private Entities prepared in accordance with the HKFRS for Private Entities (with Hong Kong Companies Ordinance disclosures)

Technology Spotlight The Future of Revenue Recognition

Technology Spotlight The Future of Revenue Recognition For Private Circulation Only January 2015 Contents Executive summary 3 Background 4 Key Accounting Issues 5 Other Accounting Issues 13 Considerations

Technology Spotlight The Future of Revenue Recognition For Private Circulation Only January 2015 Contents Executive summary 3 Background 4 Key Accounting Issues 5 Other Accounting Issues 13 Considerations

PBL: Accounting for Professionals. Competency: Accounts Concepts, Principles, Terminology

Competency: Accounts Concepts, Principles, Terminology 1. Identify and apply Generally Accepted Accounting Principles (GAAP). 2. Apply the steps in the Accounting cycle. 3. Post and analyze transactions

Competency: Accounts Concepts, Principles, Terminology 1. Identify and apply Generally Accepted Accounting Principles (GAAP). 2. Apply the steps in the Accounting cycle. 3. Post and analyze transactions

Statement of Financial Accounting Standards No. 25. Statement of Financial Accounting Standards No.25. Business Combinations

Statement of Financial Accounting Standards No. 25 Statement of Financial Accounting Standards No.25 Business Combinations Revised on 30 November 2006 Translated by Ling-Tai Lynette Chou, Professor (National

Statement of Financial Accounting Standards No. 25 Statement of Financial Accounting Standards No.25 Business Combinations Revised on 30 November 2006 Translated by Ling-Tai Lynette Chou, Professor (National

Paper P2 (INT) Corporate Reporting (International) Tuesday 10 December 2013. Professional Level Essentials Module

Corporate Reporting (International) Tuesday 10 December 2013. Professional Level Essentials Module") Professional Level Essentials Module Corporate Reporting (International) Tuesday 10 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections:

Professional Level Essentials Module Corporate Reporting (International) Tuesday 10 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections:

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

The leasing standard. A comprehensive look at the new model and its impact. At a glance. Background. Key provisions. Definition and scope

No. US2016-02 March 02, 2016 What s inside: Background... 1 Key provisions... 1 Definition and scope... 1 Contract consideration and allocation... 4 Lessee accounting model... 5 Lessor accounting model...

No. US2016-02 March 02, 2016 What s inside: Background... 1 Key provisions... 1 Definition and scope... 1 Contract consideration and allocation... 4 Lessee accounting model... 5 Lessor accounting model...

Business Combinations

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) July 7, 2015 What s inside: Overview... 1 Distinct performance obligations...

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) July 7, 2015 What s inside: Overview... 1 Distinct performance obligations...

Financial Issue 2010-7 Instruments, Structured

Financial Issue 2010-7 Instruments, Structured October 8, 2010 Products and Real Estate (FSR) Capital Markets Accounting Developments Advisory Issue 2010-8 December 13, 2010 Analysis of ASU 2010-20 Disclosures

Financial Issue 2010-7 Instruments, Structured October 8, 2010 Products and Real Estate (FSR) Capital Markets Accounting Developments Advisory Issue 2010-8 December 13, 2010 Analysis of ASU 2010-20 Disclosures

Goodwill PCC Alternative Assurance Tax Advisory dhgllp.com

Assurance Tax Advisory dhgllp.com Overview...3 Appendix A - Frequently Asked Questions...4 1.704.367.7020 dhgllp.com 2016 by Dixon Hughes Goodman LLP. All rights reserved. Permission is granted to view,

Assurance Tax Advisory dhgllp.com Overview...3 Appendix A - Frequently Asked Questions...4 1.704.367.7020 dhgllp.com 2016 by Dixon Hughes Goodman LLP. All rights reserved. Permission is granted to view,

Jollibee Foods Corporation and Subsidiaries

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

Jollibee Foods Corporation and Subsidiaries Consolidated Financial Statements December 31, 2013 and 2012 and Years Ended December 31, 2013, 2012 and 2011 and Independent Auditors Report SyCip Gorres Velayo

Statement of Financial Accounting Standards No. 144

Statement of Financial Accounting Standards No. 144 FAS144 Status Page FAS144 Summary Accounting for the Impairment or Disposal of Long-Lived Assets August 2001 Financial Accounting Standards Board of

Statement of Financial Accounting Standards No. 144 FAS144 Status Page FAS144 Summary Accounting for the Impairment or Disposal of Long-Lived Assets August 2001 Financial Accounting Standards Board of

IFRS Project Insights Insurance Contracts

IFRS Project Insights Insurance Contracts December 2015 The International Accounting Standards Board ( IASB / the Board ) is undertaking a comprehensive project on the accounting for insurance contracts,

IFRS Project Insights Insurance Contracts December 2015 The International Accounting Standards Board ( IASB / the Board ) is undertaking a comprehensive project on the accounting for insurance contracts,

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Interim Condensed Consolidated Financial Statements NOBLE IRON INC. For the three months ended March 31, 2015 and 2014 (Unaudited)

") Interim Condensed Consolidated Financial Statements NOBLE IRON INC. MANAGEMENT S COMMENTS ON UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS NOTICE OF NO AUDITOR REVIEW OF INTERIM FINANCIAL

Interim Condensed Consolidated Financial Statements NOBLE IRON INC. MANAGEMENT S COMMENTS ON UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS NOTICE OF NO AUDITOR REVIEW OF INTERIM FINANCIAL

IFRS alert... IFRS alert 2008-01. IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements

IFRS alert... IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements Alerts may include Grant Thornton International s analysis of how IFRS should be applied

IFRS alert... IASB publishes new Standards on Business Combinations and Consolidated and Separate Financial Statements Alerts may include Grant Thornton International s analysis of how IFRS should be applied

STOCKCROSS FINANCIAL SERVICES, INC. REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION DECEMBER 31, 2012

REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED

REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED

International Financial Reporting Standards (IFRS)

") FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

Report on. 2010 Inspection of PricewaterhouseCoopers LLP (Headquartered in New York, New York) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

IFRS news. IFRS 3R and IAS 27R questions and answers. Emerging issues and practical guidance* *connectedthinking PRINT CONTINUED

IFRS news Emerging issues and practical guidance* Supplement July/August 2009 IFRS 3R and IAS 27R questions and answers The revised standards on business combinations and consolidation (IFRS 3 (revised)

IFRS news Emerging issues and practical guidance* Supplement July/August 2009 IFRS 3R and IAS 27R questions and answers The revised standards on business combinations and consolidation (IFRS 3 (revised)

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED FASB Interpretation No. 48 Accounting for Uncertainty in Income Taxes an interpretation of FASB Statement No. 109 Copyright 2010

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED FASB Interpretation No. 48 Accounting for Uncertainty in Income Taxes an interpretation of FASB Statement No. 109 Copyright 2010

The Auditor s Consideration of an Entity s Ability to Continue as a Going Concern *

An Entity s Ability to Continue as a Going Concern 2047 AU Section 341 The Auditor s Consideration of an Entity s Ability to Continue as a Going Concern * Source: SAS No. 59. See section 9341 for interpretations

An Entity s Ability to Continue as a Going Concern 2047 AU Section 341 The Auditor s Consideration of an Entity s Ability to Continue as a Going Concern * Source: SAS No. 59. See section 9341 for interpretations

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

Consolidation (Topic 810)

") No. 2014-07 March 2014 Consolidation (Topic 810) Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements a consensus of the Private Company Council An Amendment of the FASB

No. 2014-07 March 2014 Consolidation (Topic 810) Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements a consensus of the Private Company Council An Amendment of the FASB

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

Stay Informed Pharmaceutical and Life Sciences Industry Alert 2015-3. FASB Income tax projects update A PLS perspective Background

Stay Informed Pharmaceutical and Life Sciences Industry Alert 2015-3 FASB Income tax projects update A PLS perspective Background The FASB has accelerated the pace of rulemaking in recent months, largely

Stay Informed Pharmaceutical and Life Sciences Industry Alert 2015-3 FASB Income tax projects update A PLS perspective Background The FASB has accelerated the pace of rulemaking in recent months, largely

Broker-dealers: Prepare for the new revenue recognition standard

Broker-dealers: Prepare for the new revenue recognition standard Last May, the FASB and IASB issued a converged standard on revenue recognition (Accounting Standards Codification [ASC] Topics 606 and 610;

Broker-dealers: Prepare for the new revenue recognition standard Last May, the FASB and IASB issued a converged standard on revenue recognition (Accounting Standards Codification [ASC] Topics 606 and 610;

IAS - 17. Leases. By: http://www.worldgaapinfo.com

IAS - 17 Leases International Accounting Standard No 17 (IAS 17) Leases This revised standard replaces IAS 17 (revised 1997) Leases, and will apply for annual periods beginning on or after January 1, 2005.

IAS - 17 Leases International Accounting Standard No 17 (IAS 17) Leases This revised standard replaces IAS 17 (revised 1997) Leases, and will apply for annual periods beginning on or after January 1, 2005.

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Similarities and differences

www.pwc.ch Similarities and differences IFRS for SMEs IFRS SWISS GAAP FER 2010/11 Edition Some practical examples IFRS for SMEs IFRS SWISS GAAP FER Similarities and differences 2010/11 Edition This PwC

www.pwc.ch Similarities and differences IFRS for SMEs IFRS SWISS GAAP FER 2010/11 Edition Some practical examples IFRS for SMEs IFRS SWISS GAAP FER Similarities and differences 2010/11 Edition This PwC

IFRS for SMEs IFRS Swiss GAAP FER

IFRS for SMEs IFRS Swiss GAAP FER Similarities and differences 2009 Edition IFRS for SMEs IFRS Swiss GAAP FER Similarities and differences 2009 Edition This PricewaterhouseCoopers publication is for those

IFRS for SMEs IFRS Swiss GAAP FER Similarities and differences 2009 Edition IFRS for SMEs IFRS Swiss GAAP FER Similarities and differences 2009 Edition This PricewaterhouseCoopers publication is for those

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Notes to the Consolidated Financial Statements

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

Deutsche Bank 2 Consolidated Financial Statements 289 Notes to the Consolidated Financial Statements 1 Significant Accounting Policies and Critical Accounting Estimates Notes to the Consolidated Financial

International Accounting Standard 39 Financial Instruments: Recognition and Measurement

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

CHICAGO PARKING METERS, LLC (A Delaware Limited Liability Company) Financial Statements. December 31, 2013 and 2012

Financial Statements. December 31, 2013 and 2012") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Financial Statements: Balance Sheets as of 2 Statements of Income for the years ended 3 Statements

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Financial Statements: Balance Sheets as of 2 Statements of Income for the years ended 3 Statements

International Financial Reporting Standard 3 Business Combinations

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

Brewers Retail Inc. Financial Statements December 31, 2015 (in thousands of Canadian dollars)

") Financial Statements March 10, 2016 Independent Auditor s Report To the Shareholders of Brewers Retail Inc. We have audited the accompanying financial statements of Brewers Retail Inc., which comprise

Financial Statements March 10, 2016 Independent Auditor s Report To the Shareholders of Brewers Retail Inc. We have audited the accompanying financial statements of Brewers Retail Inc., which comprise

Financial Reporting for Taxes

Financial Reporting for Taxes TEI May A&A Update Meeting Acquisition accounting May 8, 2012 Orlando, FL Wendi Christensen Deloitte Tax LLP wendichristensen@deloitte.com Agenda Disclosures and supporting

Financial Reporting for Taxes TEI May A&A Update Meeting Acquisition accounting May 8, 2012 Orlando, FL Wendi Christensen Deloitte Tax LLP wendichristensen@deloitte.com Agenda Disclosures and supporting

Financial Services Investment Companies (Topic 946)

") Proposed Accounting Standards Update Issued: October 21, 2011 Comments Due: January 5, 2012 Financial Services Investment Companies (Topic 946) Amendments to the Scope, Measurement, and Disclosure Requirements

Proposed Accounting Standards Update Issued: October 21, 2011 Comments Due: January 5, 2012 Financial Services Investment Companies (Topic 946) Amendments to the Scope, Measurement, and Disclosure Requirements

Audit, Review, Compilation, and Preparation of Financial Statements

Audit, Review, Compilation, and Preparation of Financial Statements DISCLAIMER: This publication has not been approved, disapproved or otherwise acted upon by any senior technical committees of, and does

Audit, Review, Compilation, and Preparation of Financial Statements DISCLAIMER: This publication has not been approved, disapproved or otherwise acted upon by any senior technical committees of, and does

IFRS: An update for boards and audit committees. Updated October 2010

IFRS: An update for boards and audit committees Updated October 2010 2 Contents 5 Foreword 6 Issues guide 6 Inventory 7 Consolidation policy 8 Financial statement presentation 9 Revenue 10 Business combinations

IFRS: An update for boards and audit committees Updated October 2010 2 Contents 5 Foreword 6 Issues guide 6 Inventory 7 Consolidation policy 8 Financial statement presentation 9 Revenue 10 Business combinations