Credit Card Payment Services: Regulations for Annual Fees, Merchant Discounts and Interchange Fees

|

|

|

- Jerome Sullivan

- 7 years ago

- Views:

Transcription

1 Credit Card Payment Services: Regulations for Annual Fees, Merchant Discounts and Interchange Fees G. Gülsün Akın, Ahmet Faruk Aysan, Gültekin Göllü, Levent Yıldıran

2 Turkish Credit Card Market 2 nd biggest in Europe after the UK: Cards: 15m in 2002, 47m in 2010 Transaction volume: 24b TL in 2002, 234b in 2010 Till 2006, no annual fees, but very high interest rates 130% APR, while inflation was 10% 25 issuers, six controlled 80% of the market, 15-25% of profits High incidence of delinquency, default, foreclosures Very strong anti-credit-card public sentiment Market failures: Ausubel (1991), Calem et al.(2006), Akın et al. (2011) Credit Cards Law in March 2006: Interest rates, minimum amount payable, interest fee calculation method, limits, contracts, solicitations, etc.

, Akın et al.")

3 Banks started to collect annual fees from cardholders in 2006 A strong reaction by consumers and consumer unions Claim: After fall in their interest income, banks reprised their services and exercised excessive market power in payment services market. Hence, annual fees should be banned. Lawsuits, counter lawsuits, Supreme Court of Appeal BDDK, Ministry of Industry and Commerce, Consumer Protection Law Objective: Do annual fees and merchant discounts collected by banks suggest excessive market power? Are further price regulations needed? Data: CBRT, BDDK, BAT, all nonparticipation banks (20), , 383 observations Panzar-Rosse (1987) method

4 Revenues from credit cards Total revenue Interest revenue Noninterest revenue Average prices of credit and payment services 0,1 0,08 0,06 0,04 0,02 0 Mean of normalized IR Mean of normalized NIR

5 Background Credit Instrument: Anytime, no application, uncollateralized, within limits Contractual rate if payment >= minimum amount Overdue rate if payment < minimum amount Payment Instrument: Convenience, safety, record keeping facility Merchants: Boosted sales Cardholders: Interest-free grace period, benefits(bonus points, travel miles/insurance, rewards, discounts), reservations, internet shopping, installments, etc. 70% of cardholders only use payment services Cardholder Good or service Merchant Price + Annual fee Merchant discount Issuer Interchange fee Price Price Acquirer

6 The cost of providing payment services to be borne by cardholders and merchants Investments in technological infrastructure Funding cost during grace period Personnel expenses Other operating expenses Two-sided markets: Platform services for both cardholders and merchants To remain on board Benefits for merchants>= merchant discounts Benefits for cardholders>= annual fees Other complaints about payment service fees Interchange Fees: anticompetitive, collusively determined, must be regulated IF regulation in 2005 by TCA Merchant Discounts: Much higher than annual fees, asymmetric prices, they must be regulated as well. Optimal merchant discounts, annual fees? Very difficult, beyond the scope. Do annual fees and merchant discounts collected by banks suggest excessive power? Should annual fees and merchant discounts be regulated as well? Bolt et al. (2011) Annual fees depend on benefits from both credit and payment services Two-part pricing on the cardholders side: annual fees, interest rates Costs must be born by cardholders and merchants If interest rates are restricted, banks shift the burden to merchant discounts and/or annual fees

7 Panzar-Rosse method From profit maximizing equilibrium conditions Ln (R it ) = α 0 + Σ f α f Ln (P f, it ) +Σ k β k X k, it +ε it From profit maximizing equilibrium conditions R it : revenue of firm i at time t P f : price of factor input f X k : control variable k ε it : error term The PR H-statistic: H = Σ f α f sum of the factor price elasticities of revenue H = 1 competitive market H 0 monopoly/collusive oligopoly 0 < H < 1 monopolistic/oligopolistic competition??? Long-run competitive equilibrium test (Shaffer 1982) Ln (ROA it ) = α 0 + Σ f α f Ln (P f, it ) +Σ k β k X k, it +ε it H ROA = Σ f α f H ROA = 0 long-run competitive equilibrium

Ln (ROA it ) = α 0 + Σ f α f Ln (P f, it ) +Σ k β k X k, it +ε it H ROA = Σ f α f H ROA = 0 long-run")

8 Criticisms for PR Bikker et al. (2012) Scaling leads to misspecification Average cost curves Long-run equilibrium Shaffer and Spierdijk (2015) For oligopolistic markets H<0 and H>0 are possible Results for competitive case H=1 are robust

9 Variables Dependent variable: NIR (Noninterest revenue) CF (cost of funds): ratio of interest expenses on funding resources to all funding resources (resources: deposits, borrowings and money market takings) PK (price of physical capital): depreciation of fixed assets / fixed assets W (average wage): total personnel expenses / number of employees Other explanatory variables: Age, Advertisement expense, Tr (Trend) and TrS (Trend squared)

and TrS")

10 Summary Statistics

11 Model NIR i,t = c i + α 1 CF i,t +α 2 W i,t +α 3 PK i,t + β 1 Tr t + β 2 TrS t +γ 1 IF reg +γ 2 (IF reg*cf) i,t +γ 3 (IF reg*w) i,t +γ 4 (IF reg *PK) i,t +δ 1 IR reg +δ 2 (IR reg*cf) i,t +δ 3 (IR reg*w) i,t +δ 4 (IR reg*pk) i,t + ξ i,t H = α 1 +α 2 +α 3 H IF = α 1 + α 2 +α 3 +γ 2 + γ 3 + γ 4 H IR = α 1 + α 2 +α 3 +γ 2 + γ 3 + γ 4 + δ 2 + δ 3 + δ 4

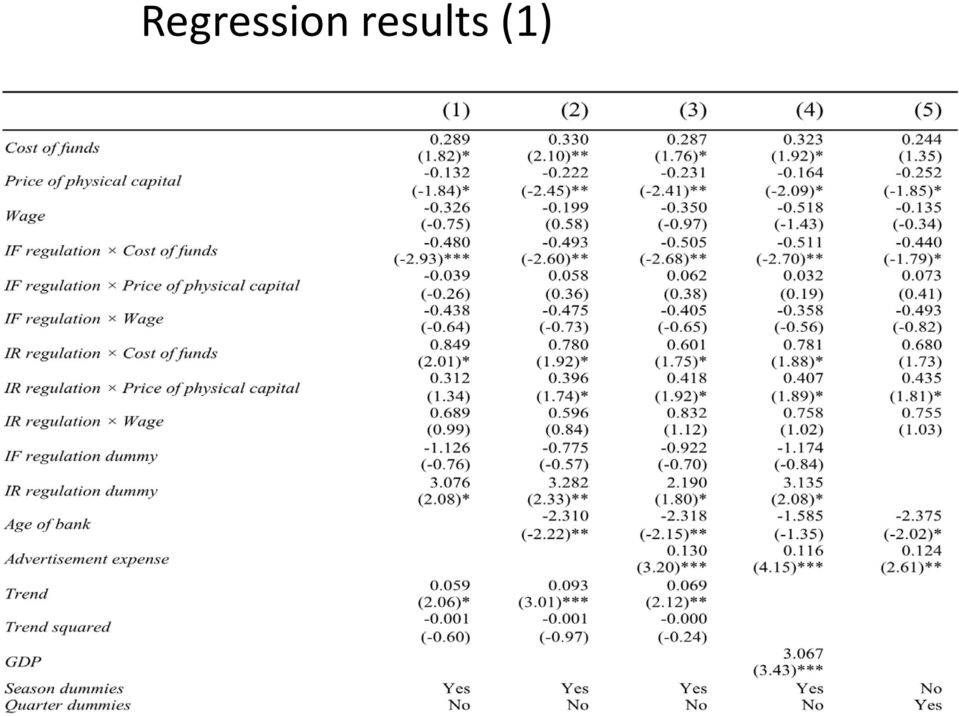

12 Regression results (1)

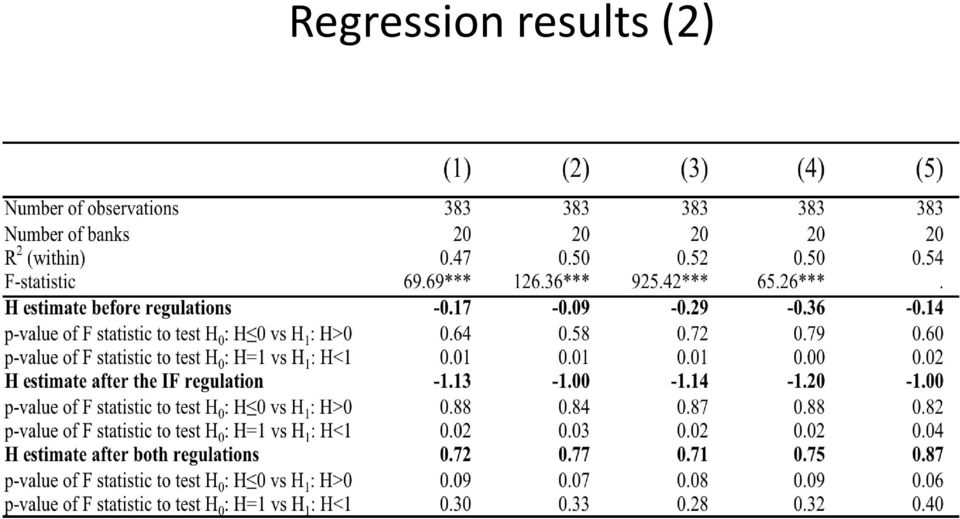

13 Regression results (2)

14 Regression results (3)

15

16 Results Banks prices and revenues rose after the IR regulation But no evidence for excessive market power Revenues increased and H approached 1 after the IR regulation factor input prices must have risen in this period

17 April-June 2006-financial turmoil Interest rates in developed countries Capital outflows from emerging countries Polarization prior to 2007 elections Governor and MP committee appointed in April Reduction in policy rate 25bp Inflation exceeded the target rate by 3% 15% depreciation Increase in policy rate by 400bp and lending rate by 600bp These rates could not be lowered till the end of 2007

18 Conclusion Regulation should always be based on sound economic analysis After IR regulation banks prices and revenues rose, but no evidence for excessive market power We attribute the rise in banks prices to a rise in costs coinciding with IR regulation IR regulation restrained prices in credit services banks had to pass along increase in costs to prices in payment services Our results do not justify further price regulations in the payment services market Banning annual fees across the board Transfer from noncardholders or light users to heavy users A menu of services and fees consumers self-select

The Role of Simultaneous Regulations of Credit Services and Payment Services on Competition

The Role of Simultaneous Regulations of Credit Services and Payment Services on Competition Abstract. In credit card markets, banks earn revenue from both credit services and payment services of credit

The Role of Simultaneous Regulations of Credit Services and Payment Services on Competition Abstract. In credit card markets, banks earn revenue from both credit services and payment services of credit

Non-Price Competition in Credit Card Markets through Bank Level Benefits. Gulsun Akin, Ahmet Faruk Aysan, Gazi Ishak Kara and Levent Yildiran

Non-Price Competition in Credit Card Markets through Bank Level Benefits Gulsun Akin, Ahmet Faruk Aysan, Gazi Ishak Kara and Levent Yildiran Non-price competition in credit card markets through bank level

Non-Price Competition in Credit Card Markets through Bank Level Benefits Gulsun Akin, Ahmet Faruk Aysan, Gazi Ishak Kara and Levent Yildiran Non-price competition in credit card markets through bank level

Credit Card Solicitations. Can I reduce the number of credit card solicitations I receive?

Credit Card Solicitations Before applying for a credit card it is wise to shop around for the card that best suits your needs. Interest rates, annual fees and grace periods are some of the features that

Credit Card Solicitations Before applying for a credit card it is wise to shop around for the card that best suits your needs. Interest rates, annual fees and grace periods are some of the features that

VI. Real Business Cycles Models

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

α α λ α = = λ λ α ψ = = α α α λ λ ψ α = + β = > θ θ β > β β θ θ θ β θ β γ θ β = γ θ > β > γ θ β γ = θ β = θ β = θ β = β θ = β β θ = = = β β θ = + α α α α α = = λ λ λ λ λ λ λ = λ λ α α α α λ ψ + α =

α α λ α = = λ λ α ψ = = α α α λ λ ψ α = + β = > θ θ β > β β θ θ θ β θ β γ θ β = γ θ > β > γ θ β γ = θ β = θ β = θ β = β θ = β β θ = = = β β θ = + α α α α α = = λ λ λ λ λ λ λ = λ λ α α α α λ ψ + α =

COMPETITION POLICY IN TWO-SIDED MARKETS

COMPETITION POLICY IN TWO-SIDED MARKETS Jean-Charles Rochet (IDEI, Toulouse University) and Jean Tirole (IDEI and MIT) Prepared for the conference Advances in the Economics of Competition Law, Rome, June

COMPETITION POLICY IN TWO-SIDED MARKETS Jean-Charles Rochet (IDEI, Toulouse University) and Jean Tirole (IDEI and MIT) Prepared for the conference Advances in the Economics of Competition Law, Rome, June

Lecture 3: The Theory of the Banking Firm and Banking Competition

Lecture 3: The Theory of the Banking Firm and Banking Competition This lecture focuses on the industrial organisation approach to the economics of banking, which considers how banks as firms react optimally

Lecture 3: The Theory of the Banking Firm and Banking Competition This lecture focuses on the industrial organisation approach to the economics of banking, which considers how banks as firms react optimally

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

ANSWERS TO END-OF-CHAPTER QUESTIONS 23-1 Briefly indicate the basic characteristics of pure competition, pure monopoly, monopolistic competition, and oligopoly. Under which of these market classifications

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Regulations and Competition in Credit Card Market in Turkey

Regulations and Competition in Credit Card Market in Turkey Gazi I. Kara Ahmet Faruk Aysan Levent Yıldıran Ahmet Nusret Müslim Umut Dur Abstract Turkish credit card market experienced a strong growth with

Regulations and Competition in Credit Card Market in Turkey Gazi I. Kara Ahmet Faruk Aysan Levent Yıldıran Ahmet Nusret Müslim Umut Dur Abstract Turkish credit card market experienced a strong growth with

Competition In Iran s Banking Sector: Panzar-Rosse Approach

Iran. Econ. Rev. Vol.19, No.1, 2015. p. 29-39 Abstract T Competition In Iran s Banking Sector: Panzar-Rosse Approach 1 2 *, Farhad khodad Kashi, Jamal Zarein beynabadi Yeghaneh Mosavi 3 Received: 2015/02/21

Iran. Econ. Rev. Vol.19, No.1, 2015. p. 29-39 Abstract T Competition In Iran s Banking Sector: Panzar-Rosse Approach 1 2 *, Farhad khodad Kashi, Jamal Zarein beynabadi Yeghaneh Mosavi 3 Received: 2015/02/21

Chapter 16 Monopolistic Competition and Oligopoly

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

Chapter 16 Monopolistic Competition and Oligopoly Market Structure Market structure refers to the physical characteristics of the market within which firms interact It is determined by the number of firms

The Failure of Competition in the Credit Card Market in Turkey: The New. Empirical Evidence

The Failure of Competition in the Credit Card Market in Turkey: The New Empirical Evidence Abstract The high credit card interest rates in Turkey attracted considerable attention in recent years to regulate

The Failure of Competition in the Credit Card Market in Turkey: The New Empirical Evidence Abstract The high credit card interest rates in Turkey attracted considerable attention in recent years to regulate

SHORT-RUN PRODUCTION

TRUE OR FALSE STATEMENTS SHORT-RUN PRODUCTION 1. According to the law of diminishing returns, additional units of the labour input increase the total output at a constantly slower rate. 2. In the short-run

TRUE OR FALSE STATEMENTS SHORT-RUN PRODUCTION 1. According to the law of diminishing returns, additional units of the labour input increase the total output at a constantly slower rate. 2. In the short-run

Market Structure and Credit Card Pricing: What Drives the Interchange?

Market Structure and Credit Card Pricing: What Drives the Interchange? Zhu Wang December 10, 2007 Abstract This paper presents a model for the credit card industry, where oligopolistic card networks price

Market Structure and Credit Card Pricing: What Drives the Interchange? Zhu Wang December 10, 2007 Abstract This paper presents a model for the credit card industry, where oligopolistic card networks price

CREDIT UNION TRENDS REPORT

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 216 (March 216 Data) Highlights During March, credit unions picked-up 577, in new memberships, loan and savings balances grew at a % and 7.6%

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 216 (March 216 Data) Highlights During March, credit unions picked-up 577, in new memberships, loan and savings balances grew at a % and 7.6%

The Real Business Cycle Model

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

DEPOSIT INSURANCE AND MONEY MARKET FREEZES. Max Bruche & Javier Suarez CEMFI. 10th Annual Bank of Finland/CEPR Conference Helsinki, 15-16 October 2009

DEPOSIT INSURANCE AND MONEY MARKET FREEZES Max Bruche & Javier Suarez CEMFI 10th Annual Bank of Finland/CEPR Conference Helsinki, 15-16 October 2009 1 Introduction We examine the causes & consequences

DEPOSIT INSURANCE AND MONEY MARKET FREEZES Max Bruche & Javier Suarez CEMFI 10th Annual Bank of Finland/CEPR Conference Helsinki, 15-16 October 2009 1 Introduction We examine the causes & consequences

Modelling Monetary Policy of the Bank of Russia

Modelling Monetary Policy of the Bank of Russia Yulia Vymyatnina Department of Economics European University at St.Peterbsurg Monetary Policy in central and Eastern Europe Tutzing, 8-10 July 2009 Outline

Modelling Monetary Policy of the Bank of Russia Yulia Vymyatnina Department of Economics European University at St.Peterbsurg Monetary Policy in central and Eastern Europe Tutzing, 8-10 July 2009 Outline

The Profitability of Credit Card Operations of Depository Institutions

The Profitability of Credit Card Operations of Depository Institutions An Annual Report by the Board of Governors of the Federal Reserve System, submitted to the Congress pursuant to Section 8 of the Fair

The Profitability of Credit Card Operations of Depository Institutions An Annual Report by the Board of Governors of the Federal Reserve System, submitted to the Congress pursuant to Section 8 of the Fair

DECISION ON DETERMINING THE INTERCHANGE FEE IN VISA AND MASTERCARD SYSTEMS

DECISION ON DETERMINING THE INTERCHANGE FEE IN VISA AND MASTERCARD SYSTEMS The proceedings initiated upon a complaint of the Polish Organisation of Commerce and Distribution, were conducted under Polish

DECISION ON DETERMINING THE INTERCHANGE FEE IN VISA AND MASTERCARD SYSTEMS The proceedings initiated upon a complaint of the Polish Organisation of Commerce and Distribution, were conducted under Polish

FinQuiz Notes 2 0 1 5

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

REVIEW OF THE STUDY OF THE COSTS OF PAYMENT SERVICES

REVIEW OF THE STUDY OF THE COSTS OF PAYMENT SERVICES Abbreviations GDP ECB ESCB MIF Gross Domestic Product European Central Bank European System of Central Banks Multilateral Interchange Fee Totals / percentages

REVIEW OF THE STUDY OF THE COSTS OF PAYMENT SERVICES Abbreviations GDP ECB ESCB MIF Gross Domestic Product European Central Bank European System of Central Banks Multilateral Interchange Fee Totals / percentages

HYPOTHESIS TESTING: POWER OF THE TEST

HYPOTHESIS TESTING: POWER OF THE TEST The first 6 steps of the 9-step test of hypothesis are called "the test". These steps are not dependent on the observed data values. When planning a research project,

HYPOTHESIS TESTING: POWER OF THE TEST The first 6 steps of the 9-step test of hypothesis are called "the test". These steps are not dependent on the observed data values. When planning a research project,

Regulating Consumer Financial Products: Evidence from Credit Cards

Regulating Consumer Financial Products: Evidence from Credit Cards Sumit Agarwal, NUS Souphala Chomsisengphet, OCC Neale Mahoney, Chicago Booth and NBER Johannes Stroebel, NYU Stern Economics of Payments

Regulating Consumer Financial Products: Evidence from Credit Cards Sumit Agarwal, NUS Souphala Chomsisengphet, OCC Neale Mahoney, Chicago Booth and NBER Johannes Stroebel, NYU Stern Economics of Payments

Chapter 3 Quantitative Demand Analysis

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

Banking Fees in Australia

Banking Fees in Australia The Reserve Bank has conducted a survey on bank fees each year since 1997. The results of the latest survey show that banks aggregate fee income was unchanged in 2. Fee income

Banking Fees in Australia The Reserve Bank has conducted a survey on bank fees each year since 1997. The results of the latest survey show that banks aggregate fee income was unchanged in 2. Fee income

Working Papers in Responsible Banking & Finance

Working Papers in Responsible Banking & Finance Risk Based Pricing in the Credit Card Industry: Evidence from US Survey Data By José Liñares-Zegarra and John O. S. Wilson Abstract: This paper explores

Working Papers in Responsible Banking & Finance Risk Based Pricing in the Credit Card Industry: Evidence from US Survey Data By José Liñares-Zegarra and John O. S. Wilson Abstract: This paper explores

Competition and Concentration in the EU Banking Industry 1

Competition and Concentration in the EU Banking Industry 1 J.A. Bikker and J.M. Groeneveld 2 Research Series Supervision no. 8 De Nederlandsche Bank June 1998 Abstract This paper presents empirical evidence

Competition and Concentration in the EU Banking Industry 1 J.A. Bikker and J.M. Groeneveld 2 Research Series Supervision no. 8 De Nederlandsche Bank June 1998 Abstract This paper presents empirical evidence

2. Illustration of the Nikkei 225 option data

1. Introduction 2. Illustration of the Nikkei 225 option data 2.1 A brief outline of the Nikkei 225 options market τ 2.2 Estimation of the theoretical price τ = + ε ε = = + ε + = + + + = + ε + ε + ε =

1. Introduction 2. Illustration of the Nikkei 225 option data 2.1 A brief outline of the Nikkei 225 options market τ 2.2 Estimation of the theoretical price τ = + ε ε = = + ε + = + + + = + ε + ε + ε =

Pre-Test Chapter 23 ed17

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Pre-Test Chapter 23 ed17 Multiple Choice Questions 1. The kinked-demand curve model of oligopoly: A. assumes a firm's rivals will ignore a price cut but match a price increase. B. embodies the possibility

Recent evidence on concentration and competition in Turkish banking sector

Theoretical and Applied Economics Volume XIX (2012), No. 8(573), pp. 19-28 Recent evidence on concentration and competion in Turkish banking sector Fatih MACIT Suleyman Sah Universy, Istambul, Turkey fmac@ssu.edu.tr

Theoretical and Applied Economics Volume XIX (2012), No. 8(573), pp. 19-28 Recent evidence on concentration and competion in Turkish banking sector Fatih MACIT Suleyman Sah Universy, Istambul, Turkey fmac@ssu.edu.tr

UK Card Payments 2014

UK Card Payments 2014 THE UK CARDS ASSOCIATION Payment cards are the most popular non-cash payment method in the UK by volume. They allow cardholders to pay for goods and services easily and conveniently,

UK Card Payments 2014 THE UK CARDS ASSOCIATION Payment cards are the most popular non-cash payment method in the UK by volume. They allow cardholders to pay for goods and services easily and conveniently,

The Federal Reserve System. The Structure of the Fed. The Fed s Goals and Targets. Economics 202 Principles Of Macroeconomics

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad The Federal Reserve System The Federal Reserve System, or the Fed, is the central bank of the United States. Supplemental Notes to Monetary

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad The Federal Reserve System The Federal Reserve System, or the Fed, is the central bank of the United States. Supplemental Notes to Monetary

Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM Report to the Congress on the Profitability of Credit Card Operations of Depository Institutions Submitted to the Congress pursuant to section 8 of the

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

CHAPTER 22: FUTURES MARKETS PROBLEM SETS 1. There is little hedging or speculative demand for cement futures, since cement prices are fairly stable and predictable. The trading activity necessary to support

Are Cartel Laws Bad for Business? Evidence from the UK

Are Cartel Laws Bad for Business? Evidence from the UK George Symeonidis University of Essex Abstract. This paper examines the impact of cartel policy on firms' profits using a panel data set of UK manufacturing

Are Cartel Laws Bad for Business? Evidence from the UK George Symeonidis University of Essex Abstract. This paper examines the impact of cartel policy on firms' profits using a panel data set of UK manufacturing

Pricing in a Competitive Market with a Common Network Resource

Pricing in a Competitive Market with a Common Network Resource Daniel McFadden Department of Economics, University of California, Berkeley April 8, 2002 I. This note is concerned with the economics of

Pricing in a Competitive Market with a Common Network Resource Daniel McFadden Department of Economics, University of California, Berkeley April 8, 2002 I. This note is concerned with the economics of

The Welfare Implication of Lifting the No Surcharge Rule in. Credit Card Markets

The Welfare Implication of Lifting the No Surcharge Rule in Credit Card Markets Hongru Tan November 5, 015 Abstract This paper investigates the welfare implications of banning the no surcharge rule (NSR)

The Welfare Implication of Lifting the No Surcharge Rule in Credit Card Markets Hongru Tan November 5, 015 Abstract This paper investigates the welfare implications of banning the no surcharge rule (NSR)

UK Card Payments 2015

UK Card Payments 2015 THE UK CARDS ASSOCIATION Cards are the most popular payment method in the UK by value. They allow cardholders to pay for goods and services easily, conveniently and securely. Card

UK Card Payments 2015 THE UK CARDS ASSOCIATION Cards are the most popular payment method in the UK by value. They allow cardholders to pay for goods and services easily, conveniently and securely. Card

Economics 101 Multiple Choice Questions for Final Examination Miller

Economics 101 Multiple Choice Questions for Final Examination Miller PLEASE DO NOT WRITE ON THIS EXAMINATION FORM. 1. Which of the following statements is correct? a. Real GDP is the total market value

Economics 101 Multiple Choice Questions for Final Examination Miller PLEASE DO NOT WRITE ON THIS EXAMINATION FORM. 1. Which of the following statements is correct? a. Real GDP is the total market value

PRIME + 6.74% - PRIME + 14.74% based on your creditworthiness

Southwest 66 Credit Union 4041 E 52 nd Street, Odessa, TX 79762 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT FOR YOUR MASTERCARD/VISA ACCOUNT Interest Rates and Interest Charges Annual Percentage Rate

Southwest 66 Credit Union 4041 E 52 nd Street, Odessa, TX 79762 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT FOR YOUR MASTERCARD/VISA ACCOUNT Interest Rates and Interest Charges Annual Percentage Rate

Competition policy brief

Issue 2015-3 June 2015 ISBN 978-92-79-38783-8, ISSN: 2315-3113 Competition policy brief Occasional discussion papers by the Competition Directorate General of the European Commission The Interchange Fees

Issue 2015-3 June 2015 ISBN 978-92-79-38783-8, ISSN: 2315-3113 Competition policy brief Occasional discussion papers by the Competition Directorate General of the European Commission The Interchange Fees

U = x 1 2. 1 x 1 4. 2 x 1 4. What are the equilibrium relative prices of the three goods? traders has members who are best off?

Chapter 7 General Equilibrium Exercise 7. Suppose there are 00 traders in a market all of whom behave as price takers. Suppose there are three goods and the traders own initially the following quantities:

Chapter 7 General Equilibrium Exercise 7. Suppose there are 00 traders in a market all of whom behave as price takers. Suppose there are three goods and the traders own initially the following quantities:

TURKEY S CREDIT CARD INDUSTRY: SWIPE WISELY

TURKEY S CREDIT CARD INDUSTRY: SWIPE WISELY Christopher Schoell Introduction In recent years credit cards have penetrated the Turkish market, with circulation growing to 44.4 million cards as of December

TURKEY S CREDIT CARD INDUSTRY: SWIPE WISELY Christopher Schoell Introduction In recent years credit cards have penetrated the Turkish market, with circulation growing to 44.4 million cards as of December

1 Multiple Choice - 50 Points

Econ 201 Final Winter 2008 SOLUTIONS 1 Multiple Choice - 50 Points (In this section each question is worth 1 point) 1. Suppose a waiter deposits his cash tips into his savings account. As a result of only

Econ 201 Final Winter 2008 SOLUTIONS 1 Multiple Choice - 50 Points (In this section each question is worth 1 point) 1. Suppose a waiter deposits his cash tips into his savings account. As a result of only

CREDIT UNION TRENDS REPORT

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 215 (March 215 data) Highlights During March, credit unions picked up 496, new memberships, credit union loan balances grew at an annualized pace,

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics May 215 (March 215 data) Highlights During March, credit unions picked up 496, new memberships, credit union loan balances grew at an annualized pace,

FTC Facts. For Consumers Federal Trade Commission. Choosing A Credit Card: The Deal is in the Disclosures

FTC Facts For Consumers Federal Trade Commission For The Consumer June 2008 www.ftc.gov 1-877-ftc-help Choosing A Credit Card: The Deal is in the Disclosures A credit card lets you buy things and pay for

FTC Facts For Consumers Federal Trade Commission For The Consumer June 2008 www.ftc.gov 1-877-ftc-help Choosing A Credit Card: The Deal is in the Disclosures A credit card lets you buy things and pay for

Elasticity. Definition of the Price Elasticity of Demand: Formula for Elasticity: Types of Elasticity:

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule. Jean-Charles Rochet and Jean Tirole

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule Jean-Charles Rochet and Jean Tirole April 4, 2003 Preliminary version. Please do not circulate. 1 Abstract The paper analyzes the costs

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule Jean-Charles Rochet and Jean Tirole April 4, 2003 Preliminary version. Please do not circulate. 1 Abstract The paper analyzes the costs

Chapter Objectives. Chapter 6. Short Term Credit Management. Major Topics. Reasons for Using Credit. How to Get Credit. Disadvantages of Using Credit

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule. Jean-Charles Rochet and Jean Tirole

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule Jean-Charles Rochet and Jean Tirole September 19, 2003 1 Abstract Payment card associations Visa and MasterCard offer both debit and

Tying in Two-Sided Markets and The Impact of the Honor All Cards Rule Jean-Charles Rochet and Jean Tirole September 19, 2003 1 Abstract Payment card associations Visa and MasterCard offer both debit and

Chapter 13 Money and Banking

Chapter 13 Money and Banking Multiple Choice Questions Choose the one alternative that best completes the statement or answers the question. 1. The most important function of money is (a) as a store of

Chapter 13 Money and Banking Multiple Choice Questions Choose the one alternative that best completes the statement or answers the question. 1. The most important function of money is (a) as a store of

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model.

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

Is a Cash Back Mortgage right for you?

Is a Cash Back Mortgage right for you? Conditions and Disclosure Details ERCU CASH BACK MORTGAGE OVERVIEW Eagle River Credit Union offers cash back ranging from 1% to 5% of the total mortgage loan amount

Is a Cash Back Mortgage right for you? Conditions and Disclosure Details ERCU CASH BACK MORTGAGE OVERVIEW Eagle River Credit Union offers cash back ranging from 1% to 5% of the total mortgage loan amount

CONSULTATION PAPER Ministry of Law: LAW 06/011/016 MAS: P009-2006 August 2006. Unsecured Credit Rules

CONSULTATION PAPER : LAW 06/011/016 MAS: P009-2006 August 2006 Unsecured Credit Rules TABLE OF CONTENTS 1. Introduction 4 2. Proposed amendments to unsecured credit rules for financial institutions 2.1

CONSULTATION PAPER : LAW 06/011/016 MAS: P009-2006 August 2006 Unsecured Credit Rules TABLE OF CONTENTS 1. Introduction 4 2. Proposed amendments to unsecured credit rules for financial institutions 2.1

Chapter 6. Commodity Forwards and Futures. Question 6.1. Question 6.2

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

Chapter 6 Commodity Forwards and Futures Question 6.1 The spot price of a widget is $70.00. With a continuously compounded annual risk-free rate of 5%, we can calculate the annualized lease rates according

Does the interest rate for business loans respond asymmetrically to changes in the cash rate?

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2013 Does the interest rate for business loans respond asymmetrically to changes in the cash rate? Abbas

University of Wollongong Research Online Faculty of Commerce - Papers (Archive) Faculty of Business 2013 Does the interest rate for business loans respond asymmetrically to changes in the cash rate? Abbas

Why payment card fees are biased against merchants

Why payment card fees are biased against merchants Julian Wright November 2010 Abstract I formalize the popular argument that payment card networks such as MasterCard and Visa charge merchants too much

Why payment card fees are biased against merchants Julian Wright November 2010 Abstract I formalize the popular argument that payment card networks such as MasterCard and Visa charge merchants too much

VISA. Classic. Credit Card. Agreement and Disclosure Statement. Classic. Federally insured by NCUA

Classic The Partnership FCU MAILING ADDRESS For ALL correspondence, deposits & loan payments PO Box 18539 Washington DC 20036-8539 VISA Classic Credit Card Member Services & Loans Audio Response ADVANTAGE

Classic The Partnership FCU MAILING ADDRESS For ALL correspondence, deposits & loan payments PO Box 18539 Washington DC 20036-8539 VISA Classic Credit Card Member Services & Loans Audio Response ADVANTAGE

Macroeconomics, 8e (Parkin) Testbank 1

Testbank 1") Macroeconomics, 8e (Parkin) Testbank 1 Chapter 9 Money, the Price Level, and Inflation 9.1 What is Money? 1) The functions of money are A) medium of exchange and the ability to buy goods and services.

Macroeconomics, 8e (Parkin) Testbank 1 Chapter 9 Money, the Price Level, and Inflation 9.1 What is Money? 1) The functions of money are A) medium of exchange and the ability to buy goods and services.

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE Introduction The working capital cycle is the period of time which elapses between the points at which cash is used in the supply/production process, to

THE WORKING CAPITAL CYCLE IN INTERNATIONAL TRADE Introduction The working capital cycle is the period of time which elapses between the points at which cash is used in the supply/production process, to

Life can be complex. Your Life Insurance shouldn t be.

Future Generali Saral Bima Life can be complex. Your Life Insurance shouldn t be. This is a Non-Linked, Non-Participating, Regular Premium, Endowment Insurance Plan. Future Generali Saral Bima is an insurance

Future Generali Saral Bima Life can be complex. Your Life Insurance shouldn t be. This is a Non-Linked, Non-Participating, Regular Premium, Endowment Insurance Plan. Future Generali Saral Bima is an insurance

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

A Sarsa based Autonomous Stock Trading Agent

A Sarsa based Autonomous Stock Trading Agent Achal Augustine The University of Texas at Austin Department of Computer Science Austin, TX 78712 USA achal@cs.utexas.edu Abstract This paper describes an autonomous

A Sarsa based Autonomous Stock Trading Agent Achal Augustine The University of Texas at Austin Department of Computer Science Austin, TX 78712 USA achal@cs.utexas.edu Abstract This paper describes an autonomous

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement This is your Cardholder Agreement with Provident Credit Union which outlines the terms to

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement This is your Cardholder Agreement with Provident Credit Union which outlines the terms to

Do Commodity Price Spikes Cause Long-Term Inflation?

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

No. 11-1 Do Commodity Price Spikes Cause Long-Term Inflation? Geoffrey M.B. Tootell Abstract: This public policy brief examines the relationship between trend inflation and commodity price increases and

Visa Account Rates, Fees and Terms

Visa Account Rates, Fees and Terms INTEREST RATES AND INTEREST CHARGES Annual Percentage Rate (APR) for Purchases, Cash Advances, and Balance Transfers Visa Classic 8.9% to 17..9% Visa Platinum 8.4% to

Visa Account Rates, Fees and Terms INTEREST RATES AND INTEREST CHARGES Annual Percentage Rate (APR) for Purchases, Cash Advances, and Balance Transfers Visa Classic 8.9% to 17..9% Visa Platinum 8.4% to

a GAO-06-929 GAO CREDIT CARDS Increased Complexity in Rates and Fees Heightens Need for More Effective Disclosures to Consumers

GAO September 2006 United States Government Accountability Office Report to the Ranking Minority Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs,

GAO September 2006 United States Government Accountability Office Report to the Ranking Minority Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs,

University of Maryland Fraternity & Sorority Life Spring 2015 Academic Report

University of Maryland Fraternity & Sorority Life Academic Report Academic and Population Statistics Population: # of Students: # of New Members: Avg. Size: Avg. GPA: % of the Undergraduate Population

University of Maryland Fraternity & Sorority Life Academic Report Academic and Population Statistics Population: # of Students: # of New Members: Avg. Size: Avg. GPA: % of the Undergraduate Population

AP Microeconomics Chapter 12 Outline

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

Consumption, Saving, and Investment, Part 1

Agenda Consumption, Saving, and, Part 1 Determinants of National Saving 5-1 5-2 Consumption and saving decisions : Desired consumption is the consumption amount desired by households Desired national saving

Agenda Consumption, Saving, and, Part 1 Determinants of National Saving 5-1 5-2 Consumption and saving decisions : Desired consumption is the consumption amount desired by households Desired national saving

+ Auto Loans & Services + Connecting ALL Your Auto Needs.

+ Auto Loans & Services + Connecting ALL Your Auto Needs. Find it Finance it Insure it Love it Love your car and how you get it. Whether you re looking to buy, fi nance, refi nance or insure, we ve got

+ Auto Loans & Services + Connecting ALL Your Auto Needs. Find it Finance it Insure it Love it Love your car and how you get it. Whether you re looking to buy, fi nance, refi nance or insure, we ve got

Volker Nienhaus Profitability of Islamic Banks Competing with Interest Banks, JRIE, Vol. 1, No, 1, Summer 1403/1983

J. Res. Islamic Econ., Vol. 1, No. 2, pp. 69-73 (1404/1984) Volker Nienhaus Profitability of Islamic Banks Competing with Interest Banks, JRIE, Vol. 1, No, 1, Summer 1403/1983 Comments: M. Fahim Khan It

J. Res. Islamic Econ., Vol. 1, No. 2, pp. 69-73 (1404/1984) Volker Nienhaus Profitability of Islamic Banks Competing with Interest Banks, JRIE, Vol. 1, No, 1, Summer 1403/1983 Comments: M. Fahim Khan It

Unit 31 A Hypothesis Test about Correlation and Slope in a Simple Linear Regression

Unit 31 A Hypothesis Test about Correlation and Slope in a Simple Linear Regression Objectives: To perform a hypothesis test concerning the slope of a least squares line To recognize that testing for a

Unit 31 A Hypothesis Test about Correlation and Slope in a Simple Linear Regression Objectives: To perform a hypothesis test concerning the slope of a least squares line To recognize that testing for a

Money Math for Teens. Before You Choose a Credit Card

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Money Math for Teens Before You Choose a Credit Card This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Volatility in the Overnight Money-Market Rate

5 Volatility in the Overnight Money-Market Rate Allan Bødskov Andersen, Economics INTRODUCTION AND SUMMARY This article analyses the day-to-day fluctuations in the Danish overnight money-market rate during

5 Volatility in the Overnight Money-Market Rate Allan Bødskov Andersen, Economics INTRODUCTION AND SUMMARY This article analyses the day-to-day fluctuations in the Danish overnight money-market rate during

1. Which of the following statements is an implication of the semi-strong form of the. Prices slowly adjust over time to incorporate past information.

COURSE 2 MAY 2001 1. Which of the following statements is an implication of the semi-strong form of the Efficient Market Hypothesis? (A) (B) (C) (D) (E) Market price reflects all information. Prices slowly

COURSE 2 MAY 2001 1. Which of the following statements is an implication of the semi-strong form of the Efficient Market Hypothesis? (A) (B) (C) (D) (E) Market price reflects all information. Prices slowly

Macquarie Card Services

Macquarie Card Services Understanding Interest Macquarie Card Services is a division of Macquarie Bank Limited ABN 46 008 583 542 Australian Credit Licence 237502 which provides and administers credit.

Macquarie Card Services Understanding Interest Macquarie Card Services is a division of Macquarie Bank Limited ABN 46 008 583 542 Australian Credit Licence 237502 which provides and administers credit.

A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

12th International Congress on Insurance: Mathematics and Economics July 16-18, 2008 A Uniform Asymptotic Estimate for Discounted Aggregate Claims with Subexponential Tails XUEMIAO HAO (Based on a joint

Conditional guidance as a response to supply uncertainty

1 Conditional guidance as a response to supply uncertainty Appendix to the speech given by Ben Broadbent, External Member of the Monetary Policy Committee, Bank of England At the London Business School,

1 Conditional guidance as a response to supply uncertainty Appendix to the speech given by Ben Broadbent, External Member of the Monetary Policy Committee, Bank of England At the London Business School,

14.74 Lecture 9: Child Labor

14.74 Lecture 9: Child Labor Prof. Esther Duflo March 9, 2004 1 The Facts In 2002, 210 million did child labor, half of them full time. 10% of the world s children work full time. In central Africa, 33%

14.74 Lecture 9: Child Labor Prof. Esther Duflo March 9, 2004 1 The Facts In 2002, 210 million did child labor, half of them full time. 10% of the world s children work full time. In central Africa, 33%

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

Survey of Macroeconomics, MBA 641 Fall 2006, Quiz 4 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The central bank for the United States

Modelling the Liquidity Premium on Corporate Bonds

1 Modelling the Liquidity Premium on Corporate Bonds Paul van Loon (*), Andrew J.G. Cairns, Alex McNeil Heriot-Watt University & The Actuarial Research Centre (ARC) (**) Alex Veys Partnership Acknowledgements:

1 Modelling the Liquidity Premium on Corporate Bonds Paul van Loon (*), Andrew J.G. Cairns, Alex McNeil Heriot-Watt University & The Actuarial Research Centre (ARC) (**) Alex Veys Partnership Acknowledgements:

SAMPLE PAPER II ECONOMICS Class - XII BLUE PRINT

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

SAMPLE PAPER II ECONOMICS Class - XII Maximum Marks 100 Time : 3 hrs. BLUE PRINT Sl. No. Form of Very Short Short Answer Long Answer Total Questions (1 Mark) (3, 4 Marks) (6 Marks) Content Unit 1 Unit

HOUSEHOLD CREDIT DELINQUENCY: DOES THE BORROWERS INDEBTEDNESS PROFILE PLAY A ROLE?*

HOUSEHOLD CREDIT DELINQUENCY: DOES THE BORROWERS INDEBTEDNESS PROFILE PLAY A ROLE?* Luísa Farinha** Ana Lacerda** 1. INTRODUCTION The recent economic crisis, in a context of high households indebtedness

HOUSEHOLD CREDIT DELINQUENCY: DOES THE BORROWERS INDEBTEDNESS PROFILE PLAY A ROLE?* Luísa Farinha** Ana Lacerda** 1. INTRODUCTION The recent economic crisis, in a context of high households indebtedness

Agenda. Productivity, Output, and Employment, Part 1. The Production Function. The Production Function. The Production Function. The Demand for Labor

Agenda Productivity, Output, and Employment, Part 1 3-1 3-2 A production function shows how businesses transform factors of production into output of goods and services through the applications of technology.

Agenda Productivity, Output, and Employment, Part 1 3-1 3-2 A production function shows how businesses transform factors of production into output of goods and services through the applications of technology.

GAO CREDIT CARDS. Rising Interchange Fees Have Increased Costs for Merchants, but Options for Reducing Fees Pose Challenges

GAO United States Government Accountability Office Report to Congressional Addressees November 2009 CREDIT CARDS Rising Interchange Fees Have Increased Costs for Merchants, but Options for Reducing Fees

GAO United States Government Accountability Office Report to Congressional Addressees November 2009 CREDIT CARDS Rising Interchange Fees Have Increased Costs for Merchants, but Options for Reducing Fees

Chapter 1. Why Study Money, Banking, and Financial Markets?

Chapter 1 Why Study Money, Banking, and Financial Markets? Why Study Money, Banking, and Financial Markets To examine how financial markets such as bond, stock and foreign exchange markets work To examine

Chapter 1 Why Study Money, Banking, and Financial Markets? Why Study Money, Banking, and Financial Markets To examine how financial markets such as bond, stock and foreign exchange markets work To examine

OLS Examples. OLS Regression

OLS Examples Page 1 Problem OLS Regression The Kelley Blue Book provides information on wholesale and retail prices of cars. Following are age and price data for 10 randomly selected Corvettes between

OLS Examples Page 1 Problem OLS Regression The Kelley Blue Book provides information on wholesale and retail prices of cars. Following are age and price data for 10 randomly selected Corvettes between

3. a. If all money is held as currency, then the money supply is equal to the monetary base. The money supply will be $1,000.

Macroeconomics ECON 2204 Prof. Murphy Problem Set 2 Answers Chapter 4 #2, 3, 4, 5, 6, 7, and 9 (on pages 102-103) 2. a. When the Fed buys bonds, the dollars that it pays to the public for the bonds increase

Macroeconomics ECON 2204 Prof. Murphy Problem Set 2 Answers Chapter 4 #2, 3, 4, 5, 6, 7, and 9 (on pages 102-103) 2. a. When the Fed buys bonds, the dollars that it pays to the public for the bonds increase

Corporate Taxes and Securitization

Corporate Taxes and Securitization The Journal of Finance by JoongHo Han KDI School of Public Policy and Management Kwangwoo Park Korea Advanced Institute of Science and Technology (KAIST) George Pennacchi

Corporate Taxes and Securitization The Journal of Finance by JoongHo Han KDI School of Public Policy and Management Kwangwoo Park Korea Advanced Institute of Science and Technology (KAIST) George Pennacchi

Q = ak L + bk L. 2. The properties of a short-run cubic production function ( Q = AL + BL )

") Learning Objectives After reading Chapter 10 and working the problems for Chapter 10 in the textbook and in this Student Workbook, you should be able to: Specify and estimate a short-run production function

Learning Objectives After reading Chapter 10 and working the problems for Chapter 10 in the textbook and in this Student Workbook, you should be able to: Specify and estimate a short-run production function

2.If actual investment is greater than planned investment, inventories increase more than planned. TRUE.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Production Functions and Cost of Production

1 Returns to Scale 1 14.01 Principles of Microeconomics, Fall 2007 Chia-Hui Chen October, 2007 Lecture 12 Production Functions and Cost of Production Outline 1. Chap 6: Returns to Scale 2. Chap 6: Production

1 Returns to Scale 1 14.01 Principles of Microeconomics, Fall 2007 Chia-Hui Chen October, 2007 Lecture 12 Production Functions and Cost of Production Outline 1. Chap 6: Returns to Scale 2. Chap 6: Production

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis. Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT Trade credit is a non-bank financing offered by a supplier to finance

Bank Loans, Trade Credits, and Borrower Characteristics: Theory and Empirical Analysis Byung-Uk Chong*, Ha-Chin Yi** March, 2010 ABSTRACT Trade credit is a non-bank financing offered by a supplier to finance

Why Do Merchants Accept Credit Cards?

Why Do Merchants Accept Credit Cards? Sujit Chakravorti Ted To September 1999 Abstract In this article, we investigate why merchants accept credit cards for payment despite the relatively high cost of

Why Do Merchants Accept Credit Cards? Sujit Chakravorti Ted To September 1999 Abstract In this article, we investigate why merchants accept credit cards for payment despite the relatively high cost of

A Just fee or Just a Fee? An Examination of Credit Card Late Fees

A Just fee or Just a Fee? An Examination of Credit Card Late Fees CRL Research Report: Credit Cards June 8, 2010 Joshua M. Frank, senior researcher EXECUTIVE SUMMARY The Federal Credit CARD Act of 2009

A Just fee or Just a Fee? An Examination of Credit Card Late Fees CRL Research Report: Credit Cards June 8, 2010 Joshua M. Frank, senior researcher EXECUTIVE SUMMARY The Federal Credit CARD Act of 2009

Box 1: Four party credit card schemes

The relevant sections of the Payment Systems (Regulation) Act 1998 are provided in Attachment 1. The Reserve Bank did not designate the three party card schemes, the American Express card system and the

The relevant sections of the Payment Systems (Regulation) Act 1998 are provided in Attachment 1. The Reserve Bank did not designate the three party card schemes, the American Express card system and the

Important Disclosure Information Travis Credit Union Credit Cards MasterCard or VISA Credit Card R. Interest Rates and Interest Chargestext

Annual Percentage Rate (APR) for purchases* Platinum Rewards VISA 8.99% to 15.99% Important Disclosure Information Travis Credit Union Credit Cards R MasterCard or VISA Credit Card R MasterCard Gold 10.99%

Annual Percentage Rate (APR) for purchases* Platinum Rewards VISA 8.99% to 15.99% Important Disclosure Information Travis Credit Union Credit Cards R MasterCard or VISA Credit Card R MasterCard Gold 10.99%