Pathways to Financial Empowerment

|

|

|

- David Lucas

- 9 years ago

- Views:

Transcription

1 Pathways to Financial Empowerment May 14, 2015 Ann Solomon, Federation Strategic Initiatives Manager Sarah Sable, Neighborhood Trust, Chief Program Officer 1

2 Agenda Overview Background & Financial Counseling Survey Results Pathways Approach to Financial Counseling Pathways to Financial Empowerment Initiative Structure Questions?

3 Household Financial Challenges Source: Pew Charitable Trusts. The Precarious State of Family Balance Sheets, January 2015.

4

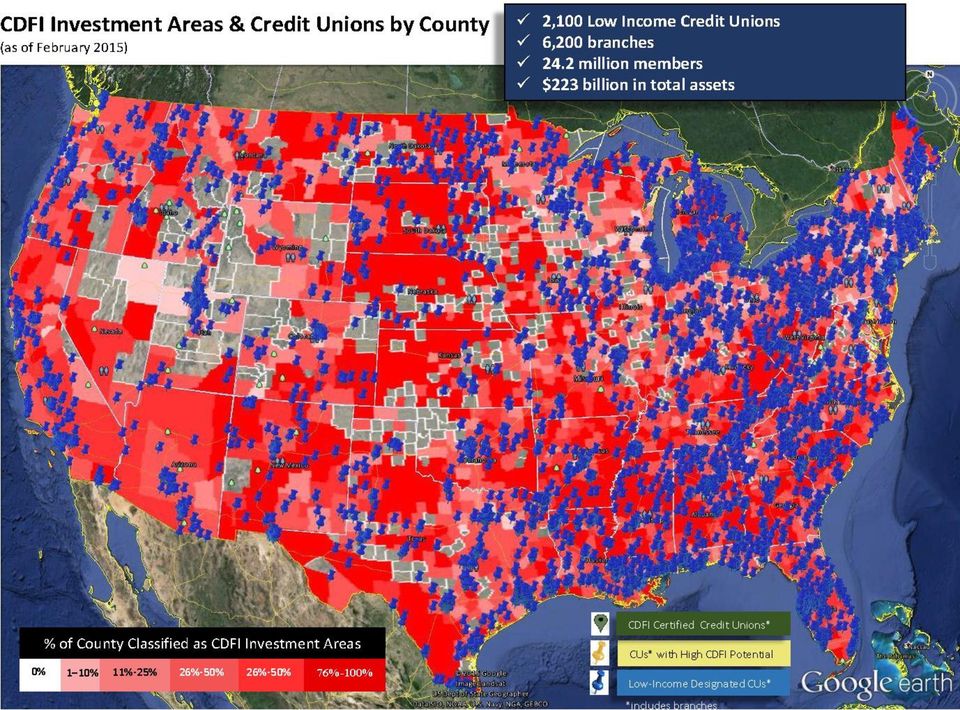

5 CU Financial Counseling Percentage of Credit Unions Offering Financial Counseling 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Mainstream Credit Unions Low Income Designated Credit Unions Sources: National Federation of Community Development Credit Unions and Credit Union National Association, CDFI Certification: A Building Block for Credit Union Growth, May CDFI Certified Credit Unions

6 Survey Results on Credit Union Financial Counseling Annual Volume of Counseling Clients FTE Delivering Counseling > 50 11% 8% % 29% 8% 10% 26% Less than % 16% 24% 24% More than 5

7 Most CUs Not Tracking Outcomes Does the credit union track results from financial counseling? Yes 38% No 62%

8 Value of Impact Measurement More so than ever before, the community development field is under the gun to prove that it is making a difference in its targeted markets. - Sean Zielenbach, Federal Reserve Bank of Boston In this environment, impacts-aware products and services offer a renaissance moment for credit unions to rethink and rebuild relevance in attracting members "Choosing Relevance, Filene Research Institute Financial Health Is The New Marketing Ron Shevlin, The Financial Brand Measurement Enables Credit Unions to: Evaluate effectiveness Gain insights into financial health and product usage Quantify credit union s impact in the community

9 Pathways to Financial Empowerment Initiative Goals: Develop a sustainable model for the integration of financial counseling into CU operations. Combine counseling with high-impact financial products to achieve better outcomes for clients. Track and demonstrate impact of counseling through standard data collection platform.

10 A Sustainable Model for Credit Union Financial Counseling Our approach to financial counseling helps both members and credit unions achieve their financial goals. Our program outlines a clear pathway to financial empowerment for credit union members. Each stage on the pathway is linked to specific credit union products that not only improve the financial health of members, but also provide a sustainable revenue stream to the credit union. Ensuring members effectively utilize the range of credit union products and services will create a sustainable revenue stream for the financial counseling program

11 A Pathway to financial empowerment that connects clients at different stages to credit union products Financial Rut Catching Up Getting Ahead Major Debt Crisis Under banked High-interest debt issues No established credit No savings Working on shortterm goals Working on longterm goals Sample Financial Products Debt payment plan Checking account Savings account Direct deposit Debt consolidation loan Balance transfer credit card Secured/ credit builder loan Savings / money market Club Account Certificate of Deposit Auto loan Personal loan Mortgage Retirement account Credit card

12 Financial Counseling Model Overview Outreach Counsel Support Measure 1 Market program to targeted member segment Use credit union services to identify members needing counseling and conduct outreach 2 Assess member financial situation 3 Develop Financial Action Plan 4 Leverage technology to help members follow their Financial Action Plans Create supportive environment with CU staff 5 Measure client outcomes Measure credit union impact

13 Metrics: Gain a better understanding of how counseling impacts your clients and your CU Client Tracking Total members served through workshops or individual counseling Referrals from Credit Union staff Clients who applied for CU accounts, loans, and other products Financial Products Balances in savings products: measure the increase in member savings as a result of counseling Credit Report Credit score: Are members more creditworthy as a result of counseling? Change in total debt: measure the decrease in costly, high-interest debts like credit cards, collections Debt to Credit Union: track uptake of recommended loan products and the status of the loan Take Action Today Do clients follow recommendations of counselors and take action to achieving their goals? Are clients empowered and feel more in control of their financial future?

14 Timeline Pathways to Financial Empowerment Structure June 12, 2015: Applications Due June 15 June 26, 2015: Application follow-up. July 2015: Pilot Credit Unions Announced July September 2015: Initial Remote Orientation and Training for Pilot Credit Unions; Execution of Grant Contracts October 14-16, 2015: Training in New York City October 2015 September 2016: Credit unions provide financial counseling for 12-month implementation period. October 2016 December 2016: Reporting, Evaluation, and Initiative Wrap Up

15 Benefits for Pilot CUs Training on the model in New York City in October 2015 (travel stipend provided); Grant of $20,000 to support program costs; Ongoing technical assistance through monthly Learning Network calls; One-year license for outcome tracking system Analysis of financial counseling impact For exceptional performers, possible additional grant of $5,000-$8,000 for pilot credit unions to expand

16 Overview of database features General Salesforce features: Cloud-based, making all your clients information easily accessible. Can be used with any web browser, even on your phone. Easy search Ability to text, , and manage communication with clients directly from the database Dashboards & Reporting Evaluate client progress over time.

17 Overview of TA Assessment of CUs in order to customize training to their needs October in-person training in NYC. Interactive, dialogue-based approach Topics overview: Diagnosing client financial health, Motivating clients to Take Action Behavioral economics Salesforce tips and tricks Ongoing support Webinars to share challenges and best practices Individual support as needed Site visits

18 Commitments of Pilot CUs Deliver counseling to at least 250 individuals Dedicate an initiative contact person Utilize the data tracking platform to capture financial information for all counseling clients Participate in monthly technical assistance and learning calls Extract data from core processor on product usage of counseling clients, including account balances and loan performance

19 What we re looking for Credit unions that: Serve a predominantly low-income and/or underserved community Provide in-house, one-on-one financial counseling Are excited about opportunity to learn and improve Have the capacity to meet Initiative commitments Are current Federation members or plan to become members

20 Questions?

Welcome! AFI Program Overview & Grant Application Process. AFI Resource Center 1-866-778-6037 [email protected]

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 [email protected] Assets for Independence Special federally funded 5-year grants to organizations that enable

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 [email protected] Assets for Independence Special federally funded 5-year grants to organizations that enable

FES: Keep It An Overview of Financial Service Strategies and Tools

FES: Keep It An Overview of Financial Service Strategies and Tools Cathie Mahon Community Development Consultant Keep it: Tools and Strategies Getting People Banked - Linking people to products and services

FES: Keep It An Overview of Financial Service Strategies and Tools Cathie Mahon Community Development Consultant Keep it: Tools and Strategies Getting People Banked - Linking people to products and services

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO www.sfofe.org Dear Partners, Supporters, Colleagues and Friends, We launched our groundbreaking Kindergarten to College program with the campaign

DREAM HUGE BUILDING A FINANCIALLY EMPOWERED SAN FRANCISCO www.sfofe.org Dear Partners, Supporters, Colleagues and Friends, We launched our groundbreaking Kindergarten to College program with the campaign

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum. Moving Ahead Through Financial Management. Module Three: Mastering Credit Basics

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Building responsible financial institutions. Capacity building for MFIs, banks, networks and associations

Building responsible financial institutions Capacity building for MFIs, banks, networks and associations MFC Services Presentation 2015 What We Do We support microfinance institutions, credit unions and

Building responsible financial institutions Capacity building for MFIs, banks, networks and associations MFC Services Presentation 2015 What We Do We support microfinance institutions, credit unions and

Comparison of Historical Rates: Credit Unions, Savings Banks, and Other Banks Data compiled by Datatrac, Inc. Contact: Ken Wanek at 1-800-257-7101.

36 month Used Auto Loan, 2 Year-Old Auto Credit Unions 4.94 4.95 5.62 Savings Banks 7.05 6.96 7.49 Other Banks 7.78 7.09 7.78 48 month Used Auto Loan, 2 Year-Old Auto (Comparison of average credit union,

36 month Used Auto Loan, 2 Year-Old Auto Credit Unions 4.94 4.95 5.62 Savings Banks 7.05 6.96 7.49 Other Banks 7.78 7.09 7.78 48 month Used Auto Loan, 2 Year-Old Auto (Comparison of average credit union,

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services [email protected].

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services [email protected] 302-255-9245 http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org

Mary Dupont, Director of Financial Empowerment State of Delaware, DE Dept. of Health and Social Services [email protected] 302-255-9245 http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org

Game-Changing Program For Financial Advisors & Insurance Agents. (An Introduction to TicoonSales)

") Game-Changing Program For Financial Advisors & Insurance Agents (An Introduction to TicoonSales) Who We Are In business since 1996 About Ticoon 100% focused on the Canadian financial services and life

Game-Changing Program For Financial Advisors & Insurance Agents (An Introduction to TicoonSales) Who We Are In business since 1996 About Ticoon 100% focused on the Canadian financial services and life

To dial-in: (866) 740-1260 Access Code: 7309390#

740-1260 Access Code: 7309390#") To dial-in: (866) 740-1260 Access Code: 7309390# If you are having technical difficulties, please email: [email protected] www.creditbuildersalliance.org 2012 Credit Builders Alliance, Inc.

To dial-in: (866) 740-1260 Access Code: 7309390# If you are having technical difficulties, please email: [email protected] www.creditbuildersalliance.org 2012 Credit Builders Alliance, Inc.

Program Overview. 595 Market Street, 16th Floor San Francisco, CA 94105 800.808.4327 www.balancepro.org

Program Overview 595 Market Street, 16th Floor San Francisco, CA 94105 800.808.4327 www.balancepro.org Our Financial Fitness Program In a tenuous economy where borrowers continue to struggle and the risks

Program Overview 595 Market Street, 16th Floor San Francisco, CA 94105 800.808.4327 www.balancepro.org Our Financial Fitness Program In a tenuous economy where borrowers continue to struggle and the risks

FIRST ACCOUNTS: A US Treasury Department Program Expanding Access to Financial Institutions

FIRST ACCOUNTS: A US Treasury Department Program Expanding Access to Financial Institutions Program Study by the Center for Impact Research, the University of Chicago Graduate School of Business, the Center

FIRST ACCOUNTS: A US Treasury Department Program Expanding Access to Financial Institutions Program Study by the Center for Impact Research, the University of Chicago Graduate School of Business, the Center

Six Strategies of Communication to Increase Tuition Payment and Student Retention

Six Strategies of Communication to Increase Tuition Payment and Student Retention Introductions Joseph Shroyer Associate Director, USFSCO Andrea Pellegrini Assistant Director, USFSCO 2 Session Overview

Six Strategies of Communication to Increase Tuition Payment and Student Retention Introductions Joseph Shroyer Associate Director, USFSCO Andrea Pellegrini Assistant Director, USFSCO 2 Session Overview

SAMPLE EVALUATION INSTRUMENTS

1 SAMPLE EVALUATION INSTRUMENTS This section contains samples of evaluation instruments that can be generated for each evaluation option. Note that the type of the instrument generated depends on the evaluation

1 SAMPLE EVALUATION INSTRUMENTS This section contains samples of evaluation instruments that can be generated for each evaluation option. Note that the type of the instrument generated depends on the evaluation

A joint project of the Delaware Office of Financial Empowerment and United Way of Delaware

A joint project of the Delaware Office of Financial Empowerment and United Way of Delaware http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org Asset Development: Home ownership, Education, Retirement,

A joint project of the Delaware Office of Financial Empowerment and United Way of Delaware http://www.youtube.com/watch?v=jrktcvurow8 www.standbymede.org Asset Development: Home ownership, Education, Retirement,

CreditAbility: Build a Strong Credit History. Brought to you by Duke University FCU

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

: Build a Strong Credit History Brought to you by Duke University FCU Seminar Objectives Learn: Who needs to build good credit, and why Significance of credit report and score How to establish credit if

In Preparation for Our First Meeting. In our first visit with you there are two objectives. Overview Questionnaire

In our first visit with you there are two objectives 1. You need to learn about us so you can decide if we are the right financial advisor for you. We want to make sure that you understand what we do,

In our first visit with you there are two objectives 1. You need to learn about us so you can decide if we are the right financial advisor for you. We want to make sure that you understand what we do,

SLDS Workshop Summary: Data Use

SLDS Workshop Summary: Data Use Developing a Data Use Strategy This publication aims to help states detail the current status of their State Longitudinal Data System (SLDS) data use strategy and identify

SLDS Workshop Summary: Data Use Developing a Data Use Strategy This publication aims to help states detail the current status of their State Longitudinal Data System (SLDS) data use strategy and identify

BANKING 101. Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

BANKING 101 Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn about issues dealing

Powerful ways to have an impact on employee engagement

Powerful ways to have an impact on employee engagement Powerful ways to have an impact on employee engagement An engaged workforce is a critical component to your company s success. When employees are

Powerful ways to have an impact on employee engagement Powerful ways to have an impact on employee engagement An engaged workforce is a critical component to your company s success. When employees are

Understanding Credit

Understanding Credit Topics covered: Establishing Credit Credit Scores Repairing Credit Why is credit necessary? Applying for a loan Applying for a credit card Applying for a mortgage Renting an apartment/house

Understanding Credit Topics covered: Establishing Credit Credit Scores Repairing Credit Why is credit necessary? Applying for a loan Applying for a credit card Applying for a mortgage Renting an apartment/house

Consumer protections and energy affordability

1 Consumer protections and energy affordability SACOSS Hardship & Affordability Conference 29 th April 2015 Lauren Solomon Manager of Retail & Social Policy Agenda for today 2 1. Energy affordability in

1 Consumer protections and energy affordability SACOSS Hardship & Affordability Conference 29 th April 2015 Lauren Solomon Manager of Retail & Social Policy Agenda for today 2 1. Energy affordability in

Credit Union Alternatives to High Cost Payday Loans

Credit Union Alternatives to High Cost Payday Loans Sarah Marshall, North Side Community Federal Credit Union October 17, 2013 North Side Community Federal Credit Union Celebrating 40 years of community

Credit Union Alternatives to High Cost Payday Loans Sarah Marshall, North Side Community Federal Credit Union October 17, 2013 North Side Community Federal Credit Union Celebrating 40 years of community

College Financing Survey

CONSUMER REPORTS NATIONAL RESEARCH CENTER College Financing Survey 2016 Nationally Representative Online Survey May 10, 2016 Introduction In March-April, 2016 the Consumer Reports National Research Center

CONSUMER REPORTS NATIONAL RESEARCH CENTER College Financing Survey 2016 Nationally Representative Online Survey May 10, 2016 Introduction In March-April, 2016 the Consumer Reports National Research Center

City of Los Angeles, 2003-2008 Consolidated Plan

, 2003-2008 Consolidated Plan D. Other Special Needs Supportive and Housing Services The Mayor has identified residents with special needs as a top priority for the Consolidated Plan and Annual Action

, 2003-2008 Consolidated Plan D. Other Special Needs Supportive and Housing Services The Mayor has identified residents with special needs as a top priority for the Consolidated Plan and Annual Action

The High Cost of Being Poor

The High Cost of Being Poor Throughout the United States, low-income people face high costs for many necessary services and items, from basic financial services to housing to food to insurance to transportation.

The High Cost of Being Poor Throughout the United States, low-income people face high costs for many necessary services and items, from basic financial services to housing to food to insurance to transportation.

IMPROVING YOUR CREDIT AND DEBT

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

IMPROVING YOUR CREDIT AND DEBT The Credit & Debt Problem Americans are loaded with credit-card debt. The average American household with at least one credit card has nearly $15,950 in credit-card debt

Virtual VITA: Expanding Free Tax Preparation. Program Insights

Virtual VITA: Expanding Free Tax Preparation Program Insights Virtual VITA: Expanding Free Tax Preparation Program Insights New York City Department of Consumer Affairs Office of Financial Empowerment

Virtual VITA: Expanding Free Tax Preparation Program Insights Virtual VITA: Expanding Free Tax Preparation Program Insights New York City Department of Consumer Affairs Office of Financial Empowerment

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

Latino Community Credit Union (LCCU , North Carolina

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

Affordable Housing Partnership Housing Counseling Program

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

Affordable Housing Partnership Housing Counseling Program ORGANIZATION AND STAFF INFORMATION Name of Organization: Affordable Housing Partnership of the Capital Region Inc. 255 Orange Street Albany, New

SMALL BUSINESS BANKING

SMALL BUSINESS BANKING for your business GET MORE FROM YOUR BANKING RELATIONSHIP We understand that there are no two businesses alike. In fact, in today s competitive environment, business owners have

SMALL BUSINESS BANKING for your business GET MORE FROM YOUR BANKING RELATIONSHIP We understand that there are no two businesses alike. In fact, in today s competitive environment, business owners have

Evaluation Plan: Process Evaluation for Hypothetical AmeriCorps Program

Evaluation Plan: Process Evaluation for Hypothetical AmeriCorps Program Introduction: This evaluation plan describes a process evaluation for Financial Empowerment Corps (FEC), an AmeriCorps State and

Evaluation Plan: Process Evaluation for Hypothetical AmeriCorps Program Introduction: This evaluation plan describes a process evaluation for Financial Empowerment Corps (FEC), an AmeriCorps State and

Welcome. Sincerely, Tim & Nichole Gardner Financial Planning

Welcome Welcome to Gardner Financial Planning. Our goal is to help each client to achieve their life's goals through a unique combination of proactive, integrated financial planning and asset management.

Welcome Welcome to Gardner Financial Planning. Our goal is to help each client to achieve their life's goals through a unique combination of proactive, integrated financial planning and asset management.

SECOND MIDTERM EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS FEBRUARY 25, 2004

SECOND MIDTERM EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS FEBRUARY 25, 2004 This exam has 25 questions on five pages. Before you begin, please check to make sure that your copy has all 25 questions

SECOND MIDTERM EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS FEBRUARY 25, 2004 This exam has 25 questions on five pages. Before you begin, please check to make sure that your copy has all 25 questions

Follow us on Twitter: @FairfaxEDA. Tweet about this session: #fceda. www.hodgespart.com

Follow us on Twitter: @FairfaxEDA Tweet about this session: Marketing Communications Strategies and Tactics Content Marketing 101 Agenda What is content marketing? Who uses content marketing and why? How

Follow us on Twitter: @FairfaxEDA Tweet about this session: Marketing Communications Strategies and Tactics Content Marketing 101 Agenda What is content marketing? Who uses content marketing and why? How

EVALUATION OF BANK/CDFI PARTNERSHIP OPPORTUNITIES

IV. EVALUATION OF BANK/CDFI PARTNERSHIP OPPORTUNITIES Banks should carefully review prospective relationships with CDFIs. In particular, they should evaluate the CDFI s service area relative to the bank

IV. EVALUATION OF BANK/CDFI PARTNERSHIP OPPORTUNITIES Banks should carefully review prospective relationships with CDFIs. In particular, they should evaluate the CDFI s service area relative to the bank

LinkedIn Sales Strategies for Suppliers and Subcontractors to the Construction Industry. LinkedSelling.com

LinkedIn Sales Strategies for Suppliers and Subcontractors to the Construction Industry LinkedSelling.com Why LinkedIn Matters? Over 135 145 150 Million Users Worldwide 77% of Users are Age 25 and Above

LinkedIn Sales Strategies for Suppliers and Subcontractors to the Construction Industry LinkedSelling.com Why LinkedIn Matters? Over 135 145 150 Million Users Worldwide 77% of Users are Age 25 and Above

Table of Contents. Foreword 3. Introduction 5. What s the strategy? 7. The vision 7. The strategy 7. The goals 7. The priorities 8

Table of Contents Message from Minister Sorenson 2 Foreword 3 National Strategy for Financial Literacy Count me in, Canada 5 Introduction 5 What s the strategy? 7 The vision 7 The strategy 7 The goals

Table of Contents Message from Minister Sorenson 2 Foreword 3 National Strategy for Financial Literacy Count me in, Canada 5 Introduction 5 What s the strategy? 7 The vision 7 The strategy 7 The goals

Community Development Financial Institutions

Community Development Financial Institutions A P U B L I C A T I O N O F T H E C D F I D A T A P R O J E C T What are community development financial institutions? Community development financial institutions

Community Development Financial Institutions A P U B L I C A T I O N O F T H E C D F I D A T A P R O J E C T What are community development financial institutions? Community development financial institutions

Tuition Rx College Planning Marketing System. The Ultimate Marketing Tool!

Tuition Rx College Planning Marketing System The Ultimate Marketing Tool! College funding is absolutely the best, untapped lead generation opportunity in financial services today! Why? The Urgency Factor

Tuition Rx College Planning Marketing System The Ultimate Marketing Tool! College funding is absolutely the best, untapped lead generation opportunity in financial services today! Why? The Urgency Factor

How To Understand Credit Rating And Credit Rating

Keeping Score: Why Credit Matters LESSON 1 Keeping Score: Why Credit Matters LESSON 1: TEACHERS GUIDE In the middle of a football grandfinal, keeping score is the norm. But when it comes to life, many

Keeping Score: Why Credit Matters LESSON 1 Keeping Score: Why Credit Matters LESSON 1: TEACHERS GUIDE In the middle of a football grandfinal, keeping score is the norm. But when it comes to life, many

5/30/2012 PERFORMANCE MANAGEMENT GOING AGILE. Nicolle Strauss Director, People Services

PERFORMANCE MANAGEMENT GOING AGILE Nicolle Strauss Director, People Services 1 OVERVIEW In the increasing shift to a mobile and global workforce the need for performance management and more broadly talent

PERFORMANCE MANAGEMENT GOING AGILE Nicolle Strauss Director, People Services 1 OVERVIEW In the increasing shift to a mobile and global workforce the need for performance management and more broadly talent

CONCEPT PAPER: NEW YORK CITY ANNUAL TAX SEASON INITIATIVE

CONCEPT PAPER: NEW YORK CITY ANNUAL TAX SEASON INITIATIVE Release Date: September, 2015 Bill de Blasio, Mayor Julie Menin, Commissioner 1 I. BACKGROUND The Department of Consumer Affairs (DCA) empowers

CONCEPT PAPER: NEW YORK CITY ANNUAL TAX SEASON INITIATIVE Release Date: September, 2015 Bill de Blasio, Mayor Julie Menin, Commissioner 1 I. BACKGROUND The Department of Consumer Affairs (DCA) empowers

Drive Interactivity and Engagement in Your Webinars

FROM PRESENTATION TO CONVERSATION Drive Interactivity and Engagement in Your Webinars 1 AUDIENCE ENGAGEMENT IS ESSENTIAL Webinars have become a top-tier marketing tool, with an ever-growing number of companies

FROM PRESENTATION TO CONVERSATION Drive Interactivity and Engagement in Your Webinars 1 AUDIENCE ENGAGEMENT IS ESSENTIAL Webinars have become a top-tier marketing tool, with an ever-growing number of companies

The Customer Experience

The Customer Experience Anne Lockie EVP, Sales & Marketing Segment Overview Key Markets Growth Markets Prime Markets Commercial Markets Youth Nexus Small Business Borrowers & Builders Business Agriculture

The Customer Experience Anne Lockie EVP, Sales & Marketing Segment Overview Key Markets Growth Markets Prime Markets Commercial Markets Youth Nexus Small Business Borrowers & Builders Business Agriculture

Startup Toolbox: Budgeting

Startup Toolbox: Budgeting Issued by Alyssa Gregory Many small business owners struggle with finding sufficient funds at some point in the lifecycle of their business. This toolbox will help you learn

Startup Toolbox: Budgeting Issued by Alyssa Gregory Many small business owners struggle with finding sufficient funds at some point in the lifecycle of their business. This toolbox will help you learn

First, some background

Selecting a Financial Wellness Service Provider Presented by: Douglas G. Prince, CPA, AIF, PRP Chief Executive Officer ProCourse Fiduciary Advisors, LLC 866.824.8040 [email protected] www.procourseadv.com

Selecting a Financial Wellness Service Provider Presented by: Douglas G. Prince, CPA, AIF, PRP Chief Executive Officer ProCourse Fiduciary Advisors, LLC 866.824.8040 [email protected] www.procourseadv.com

Promoting the Health and Well-Being of Families During Difficult Times. Family Financial Management Planning for the Future

Promoting the Health and Well-Being of Families During Difficult Times Family Financial Management Planning for the Future DenYelle Baete Kenyon, Doctoral Student, Lynne M. Borden, Extension Specialist

Promoting the Health and Well-Being of Families During Difficult Times Family Financial Management Planning for the Future DenYelle Baete Kenyon, Doctoral Student, Lynne M. Borden, Extension Specialist

NCUA LETTER TO CREDIT UNIONS

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA DATE: July 2001 LETTER NO.: 01-CU-07 TO: SUBJ: Federally Insured Credit Unions Office of Credit Union

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA DATE: July 2001 LETTER NO.: 01-CU-07 TO: SUBJ: Federally Insured Credit Unions Office of Credit Union