Tax Basics: What Every Bankruptcy Attorney Should Know

|

|

|

- Imogene Preston

- 7 years ago

- Views:

Transcription

1 Tax Basics: What Every Bankruptcy Attorney Should Know 1

2 Areas of Focus 1. Secured tax claims and tax claims entitled to priority 2. Nondischargeable tax claims 3. The short tax year election 4. Cancellation of indebtedness income in bankruptcy 2

3 Preliminary Matters: Always Obtain a Transcript and Previous Returns Previous Returns. Provided by the Internal Revenue Service (IRS) for a small fee. Tax Transcript. The tax transcript is a document which lists each transaction between the taxpayer and the IRS. It displays matters of both substantive importance and those that are of only administrative significance. The transcript is free to request from the IRS. Transaction Codes Pocket Guide. A reference to aid in understanding the transcript. Tax Transcript is Frequently Dispositive. The transcript may be introduced into evidence, and courts may rely on it to resolve factual disagreements among the parties. See Roberts v. C.I.R., 87 T.C.M. (CCH) 1228 (T.C. 2004), Schroeder v. C.I.R., 84 T.C.M. (CCH) 141 (T.C. 2002). 3

4 Secured Tax Claims and Tax Claims Entitled to Priority 4

5 Secured Tax Claims Attachment. A lien attaches under IRC 6321 when the tax is assessed and the amount remains unpaid after payment is demanded. The lien attaches to all of the debtor s pre-petition property. See U.S. v. Rogers, 103 S. Ct (1983). It is generally unenforceable after 10 years. 26 U.S.C Perfection. Occurs when a Notice of Federal Tax Lien is filed with the appropriate state entity. 26 U.S.C Absent pre-petition perfection, the IRS will be treated as an unsecured creditor. United States v. TM Bldg. Products, Ltd., 231 B.R. 364, 370 (S.D. Fla. 1998) Competing Liens. First in time, first in right governs, and federal tax liens generally do not prime existing liens. See I.R.S. v. McDermott, 507 U.S. 447, 449 (1993). Some liens may also have priority over a previously perfected federal tax lien. See 26 U.S.C. 6323(b)(1)-(10). Secured Tax Claims and Tax Claims Entitled to Priority 5

Competing Liens. First in time, first in right governs, and federal tax liens generally do not prime existing liens. See I.R.S. v.")

6 Pre-Petition Income Tax Claims Entitled to Priority Under 11 U.S.C. 507(a)(8)(A) 3 Year Rule. Taxes associated with a return that was filed within 3 years of the bankruptcy Filing. 240 Day Rule. Taxes assessed within 240 days before the bankruptcy filing. Extended to include 30 days plus the time period in which an offer in compromise was pending. Assessible but not Assessed. Taxes assessible after the bankruptcy is filed, but not yet assessed. Secured Tax Claims and Tax Claims Entitled to Priority 6

7 7

8 Pre-Petition Non-Income Tax Claims Entitled to Priority Under 11 U.S.C. 507(a)(8)(B)-(G) Property Taxes. Pre-petition property taxes last payable within one year of the bankruptcy filing. Trust Fund Taxes. Taxes which must be collected and paid over to the IRS. Employment Taxes. Taxes associated with wages, salaries, or commissions for which a return is last due after three years before the bankruptcy filing. Pecuniary Penalties. Includes only non-punitive penalties that are related to priority tax claims and which serve as compensation for actual pecuniary loss. (Punitive penalties are paid after general unsecured creditors pursuant to 11 U.S.C. 726(a)(4)). Excise Taxes. Customs Duties. Secured Tax Claims and Tax Claims Entitled to Priority 8

9 Post-Petition Tax Claims Entitled to Priority: Administrative Expense Tax Claims Under 11 U.S.C. 507(a)(2) and 503(b)(1)(B)-(C) Administrative Expense Tax Claims. The actual, necessary costs and expenses of preserving the estate including Any secured or unsecured tax incurred by the estate except a tax of the kind specified in 507(a)(8) [pre-petition tax claims] (including property taxes and taxes attributable to an excessive allowance of a tentative carryback adjustment), together with any associated fine, penalty, or reduction in credit. Administrative Expense Treatment Only Available When Estate is Separate Taxable Entity. A tax incurred by the estate is a tax for which the estate itself is liable. Hall v. United States, 132 S. Ct. 1882, 1883 (2012). Where the estate is not a separate taxable entity, the tax is the liability of the debtor alone. Id. at Secured Tax Claims and Tax Claims Entitled to Priority 9

![claims] (including property taxes and taxes attributable to an excessive allowance of a tentative carryback adjustment), together with any associated fine, penalty, or reduction in credit.](/docs-images/48/19380306/images/page_9.jpg "Administrative Expense Treatment Only Available When Estate is Separate Taxable Entity. A tax incurred by the estate is a tax for which the estate itself is liable. Hall v. United States, 132 S. Ct.")

10 Post-Petition Tax Claims Entitled to Priority: Tax Claims on Certain Wages, Salaries, and Commissions Under 11 U.S.C. 507(a)(4) Priority for Certain Wages, Salaries, or Commissions Earned Within 180 Days Before the Bankruptcy Includes Associated Taxes. Any corresponding income taxes or social security taxes withheld from employees wages are included. Only Applies to Post-Petition Tax Withholdings. Payroll tax withholdings do not occur until the wage, salary, or commission is actually paid as part of the claims distribution process. Therefore, all tax withholdings effectively occur post-petition. See Otte v. United States, 419 U.S. 43, (1974). Nondischargeable Tax Claims 10

. Nondischargeable Tax Claims 10")

11 Plan Confirmation Requires Payment of Priority Tax Claims in Full Chapter 13 Plan Confirmation. A plan must provide for payment in full, in deferred cash payments, of all priority tax claims in order to be confirmed. 11 U.S.C. 1322(a)(2). Chapter 11 Plan Confirmation. In order for a Chapter 11 plan to be confirmed, it must provide for full payment in cash on the effective date of the plan of all administrative tax claims under 11 U.S.C. 507(a)(2). 11 U.S.C. 1129(a)(9). It must also provide deferred cash payments totaling the full amount of any priority tax claim under 11 U.S.C. 507(a)(4) whose holder has accepted the plan, and full payment in cash on the effective date of the plan for any priority tax claim under 11 U.S.C. 507(a)(4) whose holder has not accepted the plan. Id. Finally, the plan must provide cash installments totaling the full amount of any priority tax claim under 11 U.S.C. 507(a)(8). Id. Secured Tax Claims and Tax Claims Entitled to Priority 11

12 Nondischargeable Tax Claims 12

13 Nondischargeable Tax Claims Under 11 U.S.C. 523(a)(1) and 523(a)(7) in Chapter 7 and Chapter 11 Individual Debtor Cases Prepetition Priority Taxes. All taxes entitled to priority under 11 U.S.C. 507(a)(8). Unfiled or Delinquent Return. Includes any tax for which a return was required and was not filed or was filed late and within two years from the bankruptcy filing. Fraudulent Return or Tax Evasion. Evasion is defined as a willful attempt to evade or defeat a tax. Punitive Tax Penalties. Unless the non-pecuniary penalty relates to a transaction or event that is more than 3 years old. Nondischargeable Tax Claims 13

14 Nondischargeable Tax Claims in Chapter 13 Under 11 U.S.C. 1328(a)(2) Unfiled or Delinquent Return. Includes any tax for which a return was required and was not filed or was filed late and within two years from the bankruptcy filing. The associated post-petition interest is also not dischargeable. Fraudulent Return or Tax Evasion. Evasion is defined as a willful attempt to evade or defeat a tax. The associated post-petition interest is also not dischargeable. Assessible but not Assessed. Taxes assessible after the bankruptcy filing, but not yet assessed. Trust Fund Taxes. Taxes which must be collected and paid over to the IRS. The associated postpetition interest is also not dischargeable. Nondischargeable Tax Claims 14

15 Post-Petition and Post-Confirmation Interest Secured Tax Claims. Post-petition and post-confirmation interest accrues on oversecured claims. Administrative Tax Claims. Interest accrues and is likely also an administrative priority. See, e.g., In re Weinstein, 272 F.3d 39, 47 (1st Cir. 2001) and In re Colortex Indus., Inc., 19F.3d1371(11th Cir. 1994). Other Priority Tax Claims in Chapter 11 and Chapter 13. Post-petition interest accrues where the debtor is solvent under 11 U.S.C. 726(a)(5), and with respect to the time between the filing of the petition and plan confirmation. Post-confirmation interest accrues on priority tax claims in Chapter 11, but not in Chapter 13 cases. Nondischargeable Tax Claims 15

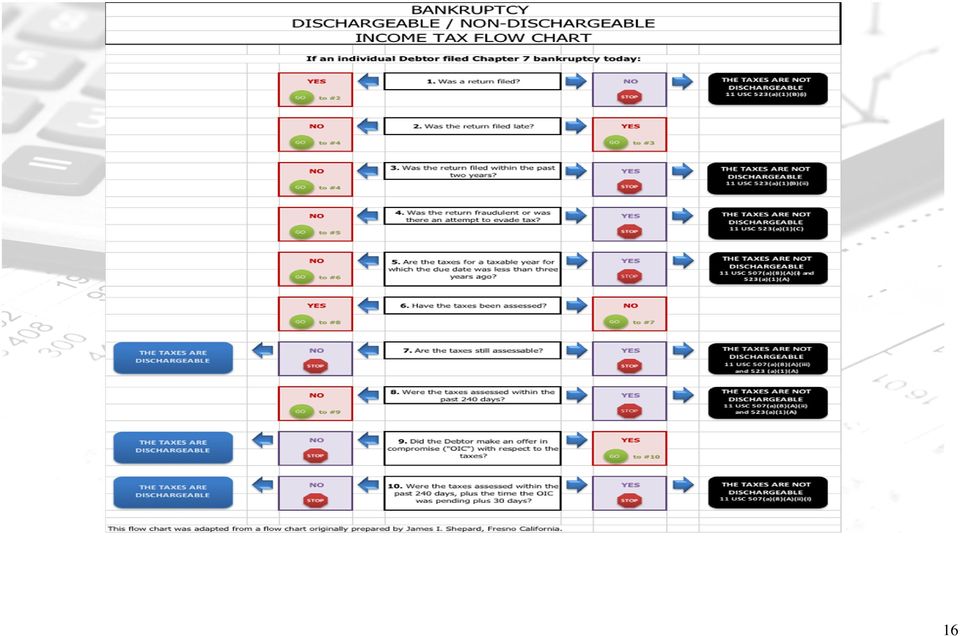

16 16

17 The Short Tax Year Election 17

18 Bankruptcy May Create a Separate Taxable Entity Individual Debtor Chapter 7 and 11 Cases. The bankruptcy filing makes the estate a separate taxable entity from the debtor. Chapter 13 Cases and Commercial Cases. The bankruptcy filing does not create a separate taxable entity. The Short Tax Year Election 18

19 Succession of Tax Attributes Estate s Tax Attributes. The estate receives the same tax attributes to which the debtor had been entitled before bankruptcy. 26 U.S.C. 1398(g). When Succession Occurs. The succession occurs upon the filing of the bankruptcy petition. The estate succeeds to the attributes of the debtor as they existed on the first day of the debtor s taxable year in which the case commences. These attributes include, for instance, deductions, NOLS, carrybacks, carryforwards, and the same basis, holding period, and character of any transferred asset as that asset held in the debtor s prepetition hands. The Short Tax Year Election 19

20 Determining the Estate s Taxable Income Generally. The estate calculates its taxable income like any other taxpayer. 26 U.S.C. 1398(c)(1) No Double Counting. Income is reported by the debtor or the estate, but not both. Amounts Included and Excluded from Gross Income. Estate s gross income includes that which is, or is derived from, property of the estate. See 11 U.S.C. 541(a)(1), (7). The estate s gross income excludes amounts received or accrued by the debtor pre-petition. 26 U.S.C. 1398(e)(1). Tax Free Disposition of Assets from Debtor to Estate. No gain, loss, recapture, or acceleration of income or deductions occurs upon the transfer of assets from the debtor to the estate, or from the estate to the debtor upon termination of the estate. The Short Tax Year Election 20

(1). Tax Free Disposition of Assets from Debtor to Estate.")

21 The Short-Year Election Under 26 U.S.C. 1398(d) Generally. The election allows a debtor with non-exempt assets to split his or her tax year into two, shorter taxable years. Absent the election, the bankruptcy filing does not affect the debtor s tax year. First Tax Year. Ends on the day before the day the bankruptcy petition is filed. Second Tax Year. Begins on the day the petition is filed, and ends on the same day that the debtor s tax year would have ended absent the election. The Short Tax Year Election 21

22 Making the Short-Year Election - Treas. Reg T How and When. The election is made when the taxpayer files its return for the first short taxable year on or before the 15th day of the fourth full month following the end of the first short taxable year. The taxpayer should write Section 1398 Election at the top of the return. Making the Election While Requesting an Extension of Time to File a Return. The election may also be made by attaching a statement of election to an application for extension of time for filing a return that satisfies the extension of time requirements for filing a return under 26 U.S.C for the first short taxable year. The Short Tax Year Election 22

23 Benefits of Making the Short-Year Election Tax Liability for First Short Year. The tax liability for the first short year becomes a prepetition, albeit nondischargeable, priority claim under 11 U.S.C. 507(a)(8). Utilization of Valuable Tax Attributes. The election permits the debtor to utilize valuable tax attributes before they would otherwise pass to the estate. The Short Tax Year Election 23

24 Cancellation of Indebtedness Income in Bankruptcy 24

25 Cancellation of Indebtedness Included in Gross Income. Gross income includes income from the discharge of indebtedness unless an exception or an exclusion under 108 applies. See 26 U.S.C. 61(a)(12). Defined. (1) whether at the inception of the loan transaction, the borrowed funds were excluded from the taxpayer s income upon receipt because of the offsetting obligation to repay; and (2) if so, whether the taxpayer s obligation to repay has been cancelled, forgiven, or reduced. American Bar Association Section of Taxation, Report of the Section 108 Real Estate and Partnership Task Force, Part 1, 46 TAX LAW. 209, 224 (1992). Cancellation of Indebtedness Income in Bankruptcy 25

26 Exceptions to the Realization of Cancellation of Indebtedness Income Gift. The cancellation of the debt was intended as a gift. Disputed Debt. The amount of the debt, not the collectibility, is disputed. Lost Deduction. Where the payment of the discharged liability would have otherwise permitted a deduction. Purchase Price Adjustment. Discharge may be treated as a reduction of the purchase price of an asset (and corresponding decrease in basis) where the debt arises out of the asset s purchase. 26 U.S.C. 108(e)(5). Cancellation of Indebtedness Income in Bankruptcy 26

27 Exceptions to the Recognition of Income Realized from the Cancellation of Indebtedness Under 26 U.S.C. 108 Bankruptcy. Discharge Occurs in a Title 11 Case. 26 U.S.C. 108(a)(1)(A). The taxpayer must be under the court s jurisdiction, and the discharge must be either granted by the court or effectuated pursuant to a court-approved plan. 26 U.S.C. 108(d)(2). Insolvency. The debtor is insolvent immediately preceding the discharge. 26 U.S.C. 108(a)(1)(B). The amount of cancellation of indebtedness income excluded from gross income may not exceed the amount by the which the taxpayer is insolvent immediately preceding the discharge. 26 U.S.C. 108(a)(3). A taxpayer is insolvent to the extent that its liabilities exceed the fair market value of its assets immediately preceding the discharge. 26 U.S.C. 108(d)(3). Cancellation of Indebtedness Income in Bankruptcy 27

28 Attribute and Basis Reduction Rule for Cancellation of Indebtedness Income Excluded Under 26 U.S.C. 108(a) Generally. A taxpayer must reduce certain tax attributes, or first elect to reduce his or her basis in depreciable property, by the amount of excluded cancellation of indebtedness income. 26 U.S.C. 108(b). Any remaining amount is excluded forever. Treas. Reg (a)(2). Cancellation of Indebtedness Income in Bankruptcy 28

29 Reduction in Tax Attributes Absent Election to Reduce Basis in Depreciable Property Reduction in Tax Attributes. Absent a basis reduction election, 108(b)(2) requires tax attributes to be reduced in the following order: 1. NOLs 2. General business credits 3. Minimum tax credits 4. Capital loss carryovers 5. Basis in the taxpayer s property. See 26 U.S.C and Treas. Reg Passive activity loss and credit carryovers 7. Foreign tax credit carryovers Cancellation of Indebtedness Income in Bankruptcy 29

30 Reduction in Tax Attributes with Election to First Reduce Basis in Depreciable Property When Basis Reduction Takes Effect. Reduction occurs at the beginning of the tax year after the tax year in which the discharge occurs. Mechanics. If the election is made, tax attributes are reduced under 26 U.S.C. 108 in the following manner: 1. Basis in Depreciable Property (but not below zero) 2. Carryovers and credits except foreign tax credits 3. Basis in nondepreciable property 4. Foreign tax credit carryovers Cancellation of Indebtedness Income in Bankruptcy 30

31 Questions 31

no--asset 7 s asset 7 s

Bankruptcy Questions Answered! Attorney to Non- Attorney Robert McKenzie, EA, Esq. Types of Bankruptcies This is not an easy subject, but our goal is to distill it to key issues you need to know as a return

Bankruptcy Questions Answered! Attorney to Non- Attorney Robert McKenzie, EA, Esq. Types of Bankruptcies This is not an easy subject, but our goal is to distill it to key issues you need to know as a return

Discussion Questions for Tax Basics: What Every Bankruptcy Attorney Should Know

Discussion Questions for Tax Basics: What Every Bankruptcy Attorney Should Know 1. Individual Debtor s Liability for Corporate Tax Debt Are officers and directors responsible person[s] within the meaning

Discussion Questions for Tax Basics: What Every Bankruptcy Attorney Should Know 1. Individual Debtor s Liability for Corporate Tax Debt Are officers and directors responsible person[s] within the meaning

This Chief Counsel Advice responds to your request for assistance. This advice may not be used or cited as precedent.

Office of Chief Counsel Internal Revenue Service memorandum Number: 201005029 Release Date: 2/5/2010 CC:PA:Br5 POSTN-137568-09 UILC: 09.00.00-00 date: October 21, 2009 to: from: Michael Skeen, Associate

Office of Chief Counsel Internal Revenue Service memorandum Number: 201005029 Release Date: 2/5/2010 CC:PA:Br5 POSTN-137568-09 UILC: 09.00.00-00 date: October 21, 2009 to: from: Michael Skeen, Associate

Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy

Income Tax Valuation Insights Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy Robert F. Reilly, CPA, and Ashley L. Reilly Many professional practitioners and small business

Income Tax Valuation Insights Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy Robert F. Reilly, CPA, and Ashley L. Reilly Many professional practitioners and small business

Discharging Taxes in Bankruptcy

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

Bankruptcy Tax Guide. Contents. Publication 908. Future Developments. Get forms and other Information faster and easier by: Internet IRS.

Department of the Treasury Internal Revenue Service Publication 908 (Rev. October 2012) Cat. No. 15309S Bankruptcy Tax Guide Contents Future Developments... 1 What's New... 2 Reminders... 2 Introduction...

Department of the Treasury Internal Revenue Service Publication 908 (Rev. October 2012) Cat. No. 15309S Bankruptcy Tax Guide Contents Future Developments... 1 What's New... 2 Reminders... 2 Introduction...

Bankruptcy Filing and Federal Employment Taxes. Bad investments, too great an assumption of risk, circumstances beyond their control.

I. What causes someone to file for bankruptcy? Bad investments, too great an assumption of risk, circumstances beyond their control. II. The options A. Individuals Chapter 7, Chapter 11, i Chapter 13 B.

I. What causes someone to file for bankruptcy? Bad investments, too great an assumption of risk, circumstances beyond their control. II. The options A. Individuals Chapter 7, Chapter 11, i Chapter 13 B.

Intersection of Tax Law and Bankruptcy Law

Intersection of Tax Law and Bankruptcy Law Tracy A. Marion Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 (office) 256-945-0944 (cell) TAM@LanierFord.com

Intersection of Tax Law and Bankruptcy Law Tracy A. Marion Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 (office) 256-945-0944 (cell) TAM@LanierFord.com

BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE. Dennis Brager, Esq.*

Adapted from an article that originally appeared in the California Tax Lawyer, Winter 1997 BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE Dennis Brager, Esq.* Many individuals, including accountants and

Adapted from an article that originally appeared in the California Tax Lawyer, Winter 1997 BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE Dennis Brager, Esq.* Many individuals, including accountants and

Tax Issues for Bankruptcy & Insolvency

Tax Issues for Bankruptcy & Insolvency By David S. De Jong, Esquire, CPA Stein, Sperling, Bennett, De Jong, Driscoll & Greenfeig, PC 25 West Middle Lane Rockville, Maryland 20850 301-838-3204 ddejong@steinsperling.com

Tax Issues for Bankruptcy & Insolvency By David S. De Jong, Esquire, CPA Stein, Sperling, Bennett, De Jong, Driscoll & Greenfeig, PC 25 West Middle Lane Rockville, Maryland 20850 301-838-3204 ddejong@steinsperling.com

DEBT FORGIVENESS AND MODIFICATION: A Primer for the Non-tax Attorney. Wayne R. Johnson, Esq. 1

DEBT FORGIVENESS AND MODIFICATION: A Primer for the Non-tax Attorney by Wayne R. Johnson, Esq. 1 The last two years have been trying to say the least. The dot-com implosion and the events of September

DEBT FORGIVENESS AND MODIFICATION: A Primer for the Non-tax Attorney by Wayne R. Johnson, Esq. 1 The last two years have been trying to say the least. The dot-com implosion and the events of September

a) State and Local Taxes Bankruptcy Code 346, 728 and 1146.

State and Local Taxes Bankruptcy Code 346, 728 and 1146.") a) State and Local Taxes Bankruptcy Code 346, 728 and 1146. Because the United States Constitution provides that all tax legislation must originate in the House of Representatives, the Bankruptcy Code,

a) State and Local Taxes Bankruptcy Code 346, 728 and 1146. Because the United States Constitution provides that all tax legislation must originate in the House of Representatives, the Bankruptcy Code,

WORKING OUT AND RESTRUCTURING DISTRESSED DEBT TAX TRAPS AND TECHNIQUES TO ACHIEVE FAVORABLE OUTCOMES

WORKING OUT AND RESTRUCTURING DISTRESSED DEBT TAX TRAPS AND TECHNIQUES TO ACHIEVE FAVORABLE OUTCOMES State Bar of Wisconsin Annual Convention May 6, 2009 Richard A. Latta Michael Best & Friedrich LLP One

WORKING OUT AND RESTRUCTURING DISTRESSED DEBT TAX TRAPS AND TECHNIQUES TO ACHIEVE FAVORABLE OUTCOMES State Bar of Wisconsin Annual Convention May 6, 2009 Richard A. Latta Michael Best & Friedrich LLP One

Tax Refund Interception on Account of Discharged Debt

Tip of the Month January 2012 Tax Refund Interception on Account of Discharged Debt Submitted by Christopher Wilcox AmeriCorps VISTA Attorney at Volunteer Lawyers Network Often, debtors that file for bankruptcy

Tip of the Month January 2012 Tax Refund Interception on Account of Discharged Debt Submitted by Christopher Wilcox AmeriCorps VISTA Attorney at Volunteer Lawyers Network Often, debtors that file for bankruptcy

1 of 5 11/21/2006 2:25 PM

1 of 5 11/21/2006 2:25 PM Internal Revenue Bulletin: 2006-40 October 2, 2006 Notice 2006-83 Individual Chapter 11 Debtors Table of Contents Section 1. PURPOSE Section 2. BACKGROUND AND GENERAL LEGAL PRINCIPLES

1 of 5 11/21/2006 2:25 PM Internal Revenue Bulletin: 2006-40 October 2, 2006 Notice 2006-83 Individual Chapter 11 Debtors Table of Contents Section 1. PURPOSE Section 2. BACKGROUND AND GENERAL LEGAL PRINCIPLES

Federal Income Taxes. Chapter 11

Chapter 11 Federal Income Taxes I. Introduction...1 II. Find Expert Advice...1 III. Losses Due to Disaster...2 A. Deducting Casualty Losses...2 B. Quick Tax Refunds From Casualty Losses...2 C. Complications

Chapter 11 Federal Income Taxes I. Introduction...1 II. Find Expert Advice...1 III. Losses Due to Disaster...2 A. Deducting Casualty Losses...2 B. Quick Tax Refunds From Casualty Losses...2 C. Complications

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ Richard Charles Grosenick Office of Chief Counsel IRS Special Assistant United States Attorney 211 W. Wisconsin Ave. Suite 807

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ Richard Charles Grosenick Office of Chief Counsel IRS Special Assistant United States Attorney 211 W. Wisconsin Ave. Suite 807

Transcript for Canceled Debt (Tax Consequences)

") Transcript for Canceled Debt (Tax Consequences) Hello. I m Jean Wetzler, with a reenactment of a March 2009 IRS National Phone Forum on the Tax Consequences of Canceled Debt. The presenter for the phone

Transcript for Canceled Debt (Tax Consequences) Hello. I m Jean Wetzler, with a reenactment of a March 2009 IRS National Phone Forum on the Tax Consequences of Canceled Debt. The presenter for the phone

Cancellation of Debt

Cancellation of Debt ROBERT E. MCKENZIE Arnstein & Lehr LLP Arnstein & Lehr LLP 1 Debt Cancellation If a debt is canceled or forgiven, other than as a gift or bequest, the debtor generally must include

Cancellation of Debt ROBERT E. MCKENZIE Arnstein & Lehr LLP Arnstein & Lehr LLP 1 Debt Cancellation If a debt is canceled or forgiven, other than as a gift or bequest, the debtor generally must include

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO ) ) ) ) ) ) ) ) ) PROCEDURAL BACKGROUND

) ) ) ) ) ) ) ) PROCEDURAL BACKGROUND") BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioners. DOCKET NO. 20644 DECISION PROCEDURAL BACKGROUND On August 3, 2007, the Income Tax Audit Division of the Idaho

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioners. DOCKET NO. 20644 DECISION PROCEDURAL BACKGROUND On August 3, 2007, the Income Tax Audit Division of the Idaho

UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

Treatment of COD Income by Partnerships

Treatment of COD Income by Partnerships Stafford Presentation January 28, 2015 Polsinelli PC. In California, Polsinelli LLP Allocation of COD Income COD income is allocated to those partners who are partners

Treatment of COD Income by Partnerships Stafford Presentation January 28, 2015 Polsinelli PC. In California, Polsinelli LLP Allocation of COD Income COD income is allocated to those partners who are partners

Bankruptcy and Tax Debts

Bankruptcy and Tax Debts Rules for Discharging Tax Debts in Bankruptcy Gary W Lundgren, EA - Mar 11, 2011 Income tax debts may be eligible for discharge under Chapter 7 or Chapter 13 of the Bankruptcy

Bankruptcy and Tax Debts Rules for Discharging Tax Debts in Bankruptcy Gary W Lundgren, EA - Mar 11, 2011 Income tax debts may be eligible for discharge under Chapter 7 or Chapter 13 of the Bankruptcy

Tax Talk For Tough Times: A Primer On Cancellation Of Debt And Related Partnership Matters

Tax Talk For Tough Times: A Primer On Cancellation Of Debt And Related Partnership Matters Walter R. Rogers, Jr. Tough times often result in canceled debt and unexpected income. Walter R. Rogers, Jr.,

Tax Talk For Tough Times: A Primer On Cancellation Of Debt And Related Partnership Matters Walter R. Rogers, Jr. Tough times often result in canceled debt and unexpected income. Walter R. Rogers, Jr.,

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA ABSTRACT With the recent decline in the real estate market, many taxpayers,

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA ABSTRACT With the recent decline in the real estate market, many taxpayers,

Leveraging New IRS Rules Eliminating 36-Month Testing Period for Cancellation of Debt Income

Leveraging New IRS Rules Eliminating 36-Month Testing Period for Cancellation of Debt Income MONDAY, DECEMBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

Leveraging New IRS Rules Eliminating 36-Month Testing Period for Cancellation of Debt Income MONDAY, DECEMBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

1/5/2016. S Corporations. Objectives. Define an S Corp

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

RESTRUCTURING DEBT ON DISTRESSED REAL ESTATE

RESTRUCTURING DEBT ON DISTRESSED REAL ESTATE A. Alteration of Mortgage Debt 1. Cancellation or Reduction of Principal Amount of Mortgage Debt - Impact on Mortgagor a. General rule b. No Foreclosure c.

RESTRUCTURING DEBT ON DISTRESSED REAL ESTATE A. Alteration of Mortgage Debt 1. Cancellation or Reduction of Principal Amount of Mortgage Debt - Impact on Mortgagor a. General rule b. No Foreclosure c.

FARM LEGAL SERIES June 2015 Tax Considerations in Liquidations and Reorganizations

Agricultural Business Management FARM LEGAL SERIES June 2015 Tax Considerations in Liquidations and Reorganizations Phillip L. Kunkel, Jeffrey A. Peterson, S. Scott Wick Attorneys, Gray Plant Mooty INTRODUCTION

Agricultural Business Management FARM LEGAL SERIES June 2015 Tax Considerations in Liquidations and Reorganizations Phillip L. Kunkel, Jeffrey A. Peterson, S. Scott Wick Attorneys, Gray Plant Mooty INTRODUCTION

Business Reorganization Committee ABI Committee News

Business Reorganization Committee ABI Committee News In This Issue: Volume 10, Number 1 / February 2011 Taxing Problems for Debtors - Treatment of Property Taxes Digging the Nail Out of the Coffin: LLC

Business Reorganization Committee ABI Committee News In This Issue: Volume 10, Number 1 / February 2011 Taxing Problems for Debtors - Treatment of Property Taxes Digging the Nail Out of the Coffin: LLC

Common Foreclosure and Cancellation of Debt Issues for Real Property (edited transcript)

") Common Foreclosure and Cancellation of Debt Issues for Real Property (edited transcript) Yvonne McDuffie-Williams: Thank you. As he said, my name is Yvonne McDuffie-Williams. I am a senior program analyst

Common Foreclosure and Cancellation of Debt Issues for Real Property (edited transcript) Yvonne McDuffie-Williams: Thank you. As he said, my name is Yvonne McDuffie-Williams. I am a senior program analyst

Reduction of Tax Attributes Due to Discharge of Indebtedness (and Section 1082 Basis Adjustment)

") Form 982 (Rev. July 2013) Department of the Treasury Internal Revenue Service Name shown on return Reduction of Tax Attributes Due to Discharge of Indebtedness (and Section 1082 Basis Adjustment) OMB No.

Form 982 (Rev. July 2013) Department of the Treasury Internal Revenue Service Name shown on return Reduction of Tax Attributes Due to Discharge of Indebtedness (and Section 1082 Basis Adjustment) OMB No.

Tax Relief for Businesses in Distress American Bar Association Section of Taxation

Tax Relief for Businesses in Distress American Bar Association Section of Taxation 5-Year Carryback of 2008 and 2009 Net Operating Losses (NOLs) for Eligible Small Businesses (ESBs) For 2008 and 2009,

Tax Relief for Businesses in Distress American Bar Association Section of Taxation 5-Year Carryback of 2008 and 2009 Net Operating Losses (NOLs) for Eligible Small Businesses (ESBs) For 2008 and 2009,

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY by Roy F. Kiplinger Kiplinger Law Firm, P.C. August 5, 2010 We pride ourselves in providing quality legal services

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY by Roy F. Kiplinger Kiplinger Law Firm, P.C. August 5, 2010 We pride ourselves in providing quality legal services

TAX CONSEQUENCES OF MORTGAGE MODIFICATIONS

TAX CONSEQUENCES OF MORTGAGE MODIFICATIONS 1 Presenters: Jeff Gentes, Connecticut Fair Housing Center Elizabeth Maresca, Fordham Law School Diane E. Thompson, NCLC CANCELLATION OF DEBT - GENERAL RULES

TAX CONSEQUENCES OF MORTGAGE MODIFICATIONS 1 Presenters: Jeff Gentes, Connecticut Fair Housing Center Elizabeth Maresca, Fordham Law School Diane E. Thompson, NCLC CANCELLATION OF DEBT - GENERAL RULES

How To Discharge A Tax Debt

How to Bankrupt Income Taxes 507 & 523 Attorney Nick C Thompson Louisville KY 40223 800 Stone Creek Parkway Suite 6 Louisville KY 40223 502-429-0057 Bankruptcy@Bankruptcy-Divorce.com www.bankruptcy-divorce.com

How to Bankrupt Income Taxes 507 & 523 Attorney Nick C Thompson Louisville KY 40223 800 Stone Creek Parkway Suite 6 Louisville KY 40223 502-429-0057 Bankruptcy@Bankruptcy-Divorce.com www.bankruptcy-divorce.com

Cancellation of Debt A Special Focus on Home Foreclosures

Cancellation of Debt A Special Focus on Home Foreclosures Mary M. Gillum, Coordinator and Attorney Tennessee Taxpayer Project Legal Aid Society of Middle Tennessee and the Cumberlands (Graphics from Microsoft

Cancellation of Debt A Special Focus on Home Foreclosures Mary M. Gillum, Coordinator and Attorney Tennessee Taxpayer Project Legal Aid Society of Middle Tennessee and the Cumberlands (Graphics from Microsoft

SOLUTIONS FOR THE MOST COMMONLY RECURRING TAX PROBLEMS OF FINANCIALLY DISTRESSED CLIENTS

SOLUTIONS FOR THE MOST COMMONLY RECURRING TAX PROBLEMS OF FINANCIALLY DISTRESSED CLIENTS By Condé Cox, Of Counsel, Greene & Markley PC, Portland Oregon (Copyright, Condé Cox, 2010) Foreclosures and financial

SOLUTIONS FOR THE MOST COMMONLY RECURRING TAX PROBLEMS OF FINANCIALLY DISTRESSED CLIENTS By Condé Cox, Of Counsel, Greene & Markley PC, Portland Oregon (Copyright, Condé Cox, 2010) Foreclosures and financial

Garnishments BEYOND Child Support

Garnishments BEYOND Child Support Agenda Involuntary nta Deductions Federal Tax Levy State Tax Levy Student Loan Creditor Garnishment Bankruptcy 1 Involuntary Deductions Involuntary deductions Neither

Garnishments BEYOND Child Support Agenda Involuntary nta Deductions Federal Tax Levy State Tax Levy Student Loan Creditor Garnishment Bankruptcy 1 Involuntary Deductions Involuntary deductions Neither

PENNSYLVANIA PERSONAL INCOME TAX GUIDE CANCELLATION OF DEBT FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES

CHAPTER 24: CANCELLATION OF DEBT FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES TABLE OF CONTENTS I. OVERVIEW OF CANCELLATION OF DEBT FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES... 7 A. In General...

CHAPTER 24: CANCELLATION OF DEBT FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES TABLE OF CONTENTS I. OVERVIEW OF CANCELLATION OF DEBT FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES... 7 A. In General...

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-44 WARNING

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-44 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

TENNESSEE DEPARTMENT OF REVENUE LETTER RULING # 11-44 WARNING Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This presentation

UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF NEVADA (SOUTHERN DIVISION OF NEVADA)

") UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF NEVADA (SOUTHERN DIVISION OF NEVADA) CHAPTER 13 GUIDELINES (LAS VEGAS) (FOURTH EDITION: August 2000) This form may periodically be revised. The Office

UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF NEVADA (SOUTHERN DIVISION OF NEVADA) CHAPTER 13 GUIDELINES (LAS VEGAS) (FOURTH EDITION: August 2000) This form may periodically be revised. The Office

Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not?

income is taxable or not?") Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not? For tax purposes, the general rule is that all debt

Is Cancellation of Debt Income Taxable? One question that I am asked often these days is whether cancellation of debt (COD) income is taxable or not? For tax purposes, the general rule is that all debt

The IRS Can Offset Post-petition Tax Overpayments Against Pre-petition Tax Liabilities. Kyle J. TumSuden, J.D. Candidate 2016

The IRS Can Offset Post-petition Tax Overpayments Against Pre-petition Tax Liabilities 2015 Volume VII No. 27 The IRS Can Offset Post-petition Tax Overpayments Against Pre-petition Tax Liabilities Kyle

The IRS Can Offset Post-petition Tax Overpayments Against Pre-petition Tax Liabilities 2015 Volume VII No. 27 The IRS Can Offset Post-petition Tax Overpayments Against Pre-petition Tax Liabilities Kyle

Tax Implications of Farm Liquidation, Debt Forgiveness, and Bankruptcy

Tax Implications of Farm Liquidation, Debt Forgiveness, and Bankruptcy Prepared by C. Robert Holcomb, EA, Extension Educator, University of Minnesota Extension Revised December 9, 2009 Introduction: A

Tax Implications of Farm Liquidation, Debt Forgiveness, and Bankruptcy Prepared by C. Robert Holcomb, EA, Extension Educator, University of Minnesota Extension Revised December 9, 2009 Introduction: A

MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 (eff. 12/20/07). ABA Tax Section, Pro Bono Committee, Saturday, May 8, 2008, 9:00a.m.

. ABA Tax Section, Pro Bono Committee, Saturday, May 8, 2008, 9:00a.m.") MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 (eff. 12/20/07). ABA Tax Section, Pro Bono Committee, Saturday, May 8, 2008, 9:00a.m. By Frances D. Sheehy, Esq. Law Office of Frances D. Sheehy 1367 Lyons

MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 (eff. 12/20/07). ABA Tax Section, Pro Bono Committee, Saturday, May 8, 2008, 9:00a.m. By Frances D. Sheehy, Esq. Law Office of Frances D. Sheehy 1367 Lyons

Outline: 108 Cancellation of Debt Income

Outline: 108 Cancellation of Debt Income Contents Page I. GROSS INCOME INCLUDES... 2 A. Definition... 2 B. Policies... 3 II. 108 GENERALLY... 4 A. Definitions... 4 B. 108(a) Exclusions from Income... 5

Outline: 108 Cancellation of Debt Income Contents Page I. GROSS INCOME INCLUDES... 2 A. Definition... 2 B. Policies... 3 II. 108 GENERALLY... 4 A. Definitions... 4 B. 108(a) Exclusions from Income... 5

business owner issues and depreciation deductions

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

Income Tax Planning for Commercial Real Estate Debt Restructuring

Bankruptcy Planning Insights Income Tax Planning for Commercial Real Estate Debt Restructuring Robert F. Reilly, CPA Many industry observers forecast a continued downturn in the commercial real estate

Bankruptcy Planning Insights Income Tax Planning for Commercial Real Estate Debt Restructuring Robert F. Reilly, CPA Many industry observers forecast a continued downturn in the commercial real estate

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION FINDINGS OF FACT AND CONCLUSIONS OF LAW

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION In re: JOSEPH R. O LONE, Case No.: 3:00-bk-5003-JAF Debtor. Chapter 7 / FINDINGS OF FACT AND CONCLUSIONS OF LAW This case

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION In re: JOSEPH R. O LONE, Case No.: 3:00-bk-5003-JAF Debtor. Chapter 7 / FINDINGS OF FACT AND CONCLUSIONS OF LAW This case

Enforcing Liens On Exempt And Excluded Property

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200634012 Release Date: 8/25/2006 CC:PA:CBS:02:DADonnelly POSTN-116657-06 UILC: 09.26.05-00 date: June 23, 2006 to: Edwin A. Herrera

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200634012 Release Date: 8/25/2006 CC:PA:CBS:02:DADonnelly POSTN-116657-06 UILC: 09.26.05-00 date: June 23, 2006 to: Edwin A. Herrera

Presented by: David L. Rice, Esq. For CalCPA Pasadena Discussion Group. (c) David L. Rice

David L. Rice") Presented by: David L. Rice, Esq. For CalCPA Pasadena Discussion Group 1 Mortgage defaults and foreclosures are of a national concern. In 2011, nearly 5,000,000 borrowers are behind on their mortgage.

Presented by: David L. Rice, Esq. For CalCPA Pasadena Discussion Group 1 Mortgage defaults and foreclosures are of a national concern. In 2011, nearly 5,000,000 borrowers are behind on their mortgage.

Insolvency Procedures under Section 108

Income Tax Insolvency Insights Insolvency Procedures under Section 108 Irina Borushko and Urmi Sampat In the current prolonged recession, many industrial and commercial entities have had to restructure

Income Tax Insolvency Insights Insolvency Procedures under Section 108 Irina Borushko and Urmi Sampat In the current prolonged recession, many industrial and commercial entities have had to restructure

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION. In re. Case No. 8:04-bk-10201-KRM BACKGROUND KATHY L.

In re UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION KATHY L. COLE, Case No. 8:04-bk-10201-KRM Debtor. ) KATHY L. COLE, vs. Plaintiff, Adversary No. 04-00361 UNITED STATES OF

In re UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION KATHY L. COLE, Case No. 8:04-bk-10201-KRM Debtor. ) KATHY L. COLE, vs. Plaintiff, Adversary No. 04-00361 UNITED STATES OF

Chapter 12 is a reorganization for family farmers and fishing families, which is similar to Chapter 13.

GENERAL INFORMATION ABOUT THE BANKRUPTCY SYSTEM INCLUDING THE RIGHTS AND DUTIES OF CHAPTER 13 DEBTORS (and other information necessary to assist a debtor in completion of the chapter 13 plan) WHAT IS BANKRUPTCY?

GENERAL INFORMATION ABOUT THE BANKRUPTCY SYSTEM INCLUDING THE RIGHTS AND DUTIES OF CHAPTER 13 DEBTORS (and other information necessary to assist a debtor in completion of the chapter 13 plan) WHAT IS BANKRUPTCY?

NY County Lawyers Association Consumer Bankruptcy Committee Winter 1999 Dealing with the Taxing Authorities in Bankruptcy Matters

Page 1 of 16 NY County Lawyers Association Consumer Bankruptcy Committee Winter 1999 Dealing with the Taxing Authorities in Bankruptcy Matters I. Tax Collection Fundamentals: Non-Bankruptcy Alternatives

Page 1 of 16 NY County Lawyers Association Consumer Bankruptcy Committee Winter 1999 Dealing with the Taxing Authorities in Bankruptcy Matters I. Tax Collection Fundamentals: Non-Bankruptcy Alternatives

FORECLOSURE TAXATION

FORECLOSURE TAXATION Phil Rosenkranz Attorney At Law Legal Aid Society of Milwaukee 521 North 8th Street Milwaukee, Wisconsin 53233 (414) 727-5300 (414) 291-5488 (fax) prosenkranz@lasmilwaukee.com Sean

FORECLOSURE TAXATION Phil Rosenkranz Attorney At Law Legal Aid Society of Milwaukee 521 North 8th Street Milwaukee, Wisconsin 53233 (414) 727-5300 (414) 291-5488 (fax) prosenkranz@lasmilwaukee.com Sean

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE NOTE: This document is not an official pronouncement of the law or the position of the Service and cannot be used, cited,

REAL ESTATE PROPERTY FORECLOSURE and CANCELLATION OF DEBT AUDIT TECHNIQUE GUIDE NOTE: This document is not an official pronouncement of the law or the position of the Service and cannot be used, cited,

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA DIVISION www.flmb.uscourts.gov ORDER CONFIRMING PLAN

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA DIVISION www.flmb.uscourts.gov In re: Case No. Chapter 13 Debtor. 1 / ORDER CONFIRMING PLAN THIS CASE came on for a hearing on *, 201* following

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA DIVISION www.flmb.uscourts.gov In re: Case No. Chapter 13 Debtor. 1 / ORDER CONFIRMING PLAN THIS CASE came on for a hearing on *, 201* following

Non-Performing Loans

Non-Performing Loans Non-Performing Loans Accounting Treatment Legal Factors Tax Treatment Audit Process NPL Accounting Types of Loans Subject to Nonaccrual Accounting Commercial Loans Consumer Real Estate

Non-Performing Loans Non-Performing Loans Accounting Treatment Legal Factors Tax Treatment Audit Process NPL Accounting Types of Loans Subject to Nonaccrual Accounting Commercial Loans Consumer Real Estate

USING BANKRUPTCY TO PROVIDE RELIEF FROM TAX DEBT

USING BANKRUPTCY TO PROVIDE RELIEF FROM TAX DEBT EXPLORE ALL OPTIONS - Collection Statute End Date--IRC 6502 - Offer in Compromise--IRC 7122 - Installment Agreement--IRC 6159 - Currently uncollectible

USING BANKRUPTCY TO PROVIDE RELIEF FROM TAX DEBT EXPLORE ALL OPTIONS - Collection Statute End Date--IRC 6502 - Offer in Compromise--IRC 7122 - Installment Agreement--IRC 6159 - Currently uncollectible

General Rules 1. All income is taxable.

Chapter 17 Pages 239-252 General Rules 1. All income is taxable. p. 239 2. Cancelled debt is income. 3. Cancelled debt is taxable: a. To a solvent taxpayer. b. To the extent solvency is restored. Warning!

Chapter 17 Pages 239-252 General Rules 1. All income is taxable. p. 239 2. Cancelled debt is income. 3. Cancelled debt is taxable: a. To a solvent taxpayer. b. To the extent solvency is restored. Warning!

United States Bankruptcy Court - Northern District of Alabama BUSINESS DEBTOR S AFFIRMATIONS

CHAPTER 11 OPERATING ORDER FORM 04/00 BUSINESS BA-01 Operating reports are to be filed monthly, in duplicate, with the Bankruptcy Clerk s Office by the 15 th of each month BUSINESS DEBTOR S AFFIRMATIONS

CHAPTER 11 OPERATING ORDER FORM 04/00 BUSINESS BA-01 Operating reports are to be filed monthly, in duplicate, with the Bankruptcy Clerk s Office by the 15 th of each month BUSINESS DEBTOR S AFFIRMATIONS

DISCHARGE OF INDEBTEDNESS INCOME PLANNING OPPORTUNITIES

DISCHARGE OF INDEBTEDNESS INCOME PLANNING OPPORTUNITIES Thomas Mammarella Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, DE 19806 Tel: (302) 652-2900 Fax: (302) 652-1142 tmammarella@gfmlaw.com

DISCHARGE OF INDEBTEDNESS INCOME PLANNING OPPORTUNITIES Thomas Mammarella Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, DE 19806 Tel: (302) 652-2900 Fax: (302) 652-1142 tmammarella@gfmlaw.com

Tax Effects of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005

Tax Effects of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 By Matthew P. Crouch Common Definitions: This outline uses terms, which, while common to bankruptcy practitioners, may

Tax Effects of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 By Matthew P. Crouch Common Definitions: This outline uses terms, which, while common to bankruptcy practitioners, may

Internal Revenue Service. Department of the Treasury Washington, DC 20224. Number: 200442011 Release Date: 10/15/2004

Internal Revenue Service Number: 200442011 Release Date: 10/15/2004 Department of the Treasury Washington, DC 20224 Index Number: 382.12-08, 468B.02-00 ---------------------------------------------- -------------------------------------------

Internal Revenue Service Number: 200442011 Release Date: 10/15/2004 Department of the Treasury Washington, DC 20224 Index Number: 382.12-08, 468B.02-00 ---------------------------------------------- -------------------------------------------

Selected Debt Restructuring Issues. Friday, January 22, 2010 Tax Law Section

Selected Debt Restructuring Issues Friday, January 22, 2010 Tax Law Section Robert E. August, Esq. Merline & Meacham, PA P.O. Box 10796 Greenville, SC 29603 p. (864) 242-4080 f. (864) 242-5758 baugust@merlineandmeacham.com

Selected Debt Restructuring Issues Friday, January 22, 2010 Tax Law Section Robert E. August, Esq. Merline & Meacham, PA P.O. Box 10796 Greenville, SC 29603 p. (864) 242-4080 f. (864) 242-5758 baugust@merlineandmeacham.com

INTRODUCTION TO BANKRUPTCY CODE REMEDIES. 101 Overview... 1. 115 Glossary... 2. 125 Advantages and Disadvantages of Tax Remedies...

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview......................... 1 115 Glossary......................... 2 125 Advantages and Disadvantages of Tax Remedies....... 6.01 Tax Code remedy: statute

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview......................... 1 115 Glossary......................... 2 125 Advantages and Disadvantages of Tax Remedies....... 6.01 Tax Code remedy: statute

INTRODUCTION TO BANKRUPTCY CODE REMEDIES. 101 Overview...1. 115 Glossary...2. 125 Advantages and Disadvantages of Tax Remedies...6

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview...1 115 Glossary...2 125 Advantages and Disadvantages of Tax Remedies...6.01 Tax Code remedy: statute of limitation on collection.6.02 Tax Code remedy:

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview...1 115 Glossary...2 125 Advantages and Disadvantages of Tax Remedies...6.01 Tax Code remedy: statute of limitation on collection.6.02 Tax Code remedy:

The 1099- C, Insolvency, and the Cancellation of Debt: What you Need to Know

Moving Your Practice in the Right Direction TM The 1099- C, Insolvency, and the Cancellation of Debt: What you Need to Know A Practice Essentials Presentation 2010 OnePath Practice Management Advisors,

Moving Your Practice in the Right Direction TM The 1099- C, Insolvency, and the Cancellation of Debt: What you Need to Know A Practice Essentials Presentation 2010 OnePath Practice Management Advisors,

Consumer Tax Toolbox: What Wrenches, Hammers and Nails Do You Need to Deal with Consumer Tax Issues?

Consumer Tax Toolbox: What Wrenches, Hammers and Nails Do You Need to Deal with Consumer Tax Issues? CONSUMER TRACK Christine L. Myatt, Moderator Nexsen Pruet; Greensboro, N.C. Leon S. Jones Jones & Walden,

Consumer Tax Toolbox: What Wrenches, Hammers and Nails Do You Need to Deal with Consumer Tax Issues? CONSUMER TRACK Christine L. Myatt, Moderator Nexsen Pruet; Greensboro, N.C. Leon S. Jones Jones & Walden,

Sect. 108 and Cancellation of Debt Income: Navigating IRS Rules

Sect. 108 and Cancellation of Debt Income: Navigating IRS Rules Wayne R. Strasbaugh Ballard Spahr LLP 1735 Market Street, 51st Floor Philadelphia, Pennsylvania 19103 strasbaugh@ballardspahr.com October

Sect. 108 and Cancellation of Debt Income: Navigating IRS Rules Wayne R. Strasbaugh Ballard Spahr LLP 1735 Market Street, 51st Floor Philadelphia, Pennsylvania 19103 strasbaugh@ballardspahr.com October

PROPERTY TAX BULLETIN

PROPERTY TAX BULLETIN Number 139 August 2006 Shea Riggsbee Denning, Editor COLLECTING PROPERTY TAXES IN BANKRUPTCY Shea Riggsbee Denning and Robert E. Price Jr. News that a taxpayer is filing for bankruptcy

PROPERTY TAX BULLETIN Number 139 August 2006 Shea Riggsbee Denning, Editor COLLECTING PROPERTY TAXES IN BANKRUPTCY Shea Riggsbee Denning and Robert E. Price Jr. News that a taxpayer is filing for bankruptcy

Order of creditor and shareholder ranking on a company s insolvency

Order of creditor and shareholder ranking on a company insolvency This table is part of the PLC multi-jurisdictional guide to restructuring and insolvency law. For a full list of jurisdictional Q&As visit

Order of creditor and shareholder ranking on a company insolvency This table is part of the PLC multi-jurisdictional guide to restructuring and insolvency law. For a full list of jurisdictional Q&As visit

Objectives. Discuss S corp fringe benefits.

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

Glossary. is the process of increasing account value, usually associated with interest or other time-dependent increments of account value.

ACCELERATION ACCOUNT SERVICING ACCRUE ACTIVE COLLECTION ADMINISTRATIVE COSTS/ LATE CHARGES ADMINISTRATIVE OFFSET ADMINISTRATIVE WAGE GARNISHMENT (AWG) is declaring the full amount of a debt due and payable

ACCELERATION ACCOUNT SERVICING ACCRUE ACTIVE COLLECTION ADMINISTRATIVE COSTS/ LATE CHARGES ADMINISTRATIVE OFFSET ADMINISTRATIVE WAGE GARNISHMENT (AWG) is declaring the full amount of a debt due and payable

TAXATION AND THE BANKRUPTCY CODE

Chapter 4: Other Recommendations and Issues TAXATION AND THE BANKRUPTCY CODE COMMENTS PREPARED BY PROFESSOR JACK WILLIAMS RECOMMENDATIONS 4.2.1 Clarify provisions of the Bankruptcy Code on providing reasonable

Chapter 4: Other Recommendations and Issues TAXATION AND THE BANKRUPTCY CODE COMMENTS PREPARED BY PROFESSOR JACK WILLIAMS RECOMMENDATIONS 4.2.1 Clarify provisions of the Bankruptcy Code on providing reasonable

DEBT CANCELLATION AND FORECLOSURE ISSUES Code Sec 108 Income for Discharge of Indebtedness and Code Sec 1017 Discharge of Indebtedness

Debt Cancellation & Foreclosure DEBT CANCELLATION AND FORECLOSURE ISSUES Code Sec 108 Income for Discharge of Indebtedness and Code Sec 1017 Discharge of Indebtedness NOTE - Bankruptcy This material only

Debt Cancellation & Foreclosure DEBT CANCELLATION AND FORECLOSURE ISSUES Code Sec 108 Income for Discharge of Indebtedness and Code Sec 1017 Discharge of Indebtedness NOTE - Bankruptcy This material only

Collecting Back Taxes: The IRS Statute of Limitations Explained

Collecting Back Taxes: The IRS Statute of Limitations Explained A Practice Essentials CLE Program Presenter: Benjamin A. Stolz, Esq. 1 Copyright 2011 OnePath Practice Management Advisors, LLC Disclaimer

Collecting Back Taxes: The IRS Statute of Limitations Explained A Practice Essentials CLE Program Presenter: Benjamin A. Stolz, Esq. 1 Copyright 2011 OnePath Practice Management Advisors, LLC Disclaimer

Taxpayers. What You Should Know. I Found My Voice At The IRS

Cancellation Advocating of Debt for Taxpayers What You Should Know I Found My Voice At The IRS National Taxpayer Advocate Podcast Current Law IRS Office of Chief Counsel Cancellation of Debt Section 61(a)(12)

Cancellation Advocating of Debt for Taxpayers What You Should Know I Found My Voice At The IRS National Taxpayer Advocate Podcast Current Law IRS Office of Chief Counsel Cancellation of Debt Section 61(a)(12)

ROSE KRAIZA : SUPERIOR COURT. v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009

NO. CV 04 4002676 ROSE KRAIZA : SUPERIOR COURT : TAX SESSION v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009 MEMORANDUM OF DECISION ON MOTION

NO. CV 04 4002676 ROSE KRAIZA : SUPERIOR COURT : TAX SESSION v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009 MEMORANDUM OF DECISION ON MOTION

TAX CONSIDERATIONS IN REAL ESTATE TRANSACTIONS. Investment by Foreign Persons in U.S. Real Estate

TAX CONSIDERATIONS IN REAL ESTATE TRANSACTIONS Investment by Foreign Persons in U.S. Real Estate Keith R. Gercken Pillsbury Winthrop LLP San Francisco, California Overview U.S. taxation of foreign persons

TAX CONSIDERATIONS IN REAL ESTATE TRANSACTIONS Investment by Foreign Persons in U.S. Real Estate Keith R. Gercken Pillsbury Winthrop LLP San Francisco, California Overview U.S. taxation of foreign persons

Internal Revenue Service

Internal Revenue Service Number: 200741003 Release Date: 10/12/2007 Index Number: 468B.07-00, 162.00-00, 461.00-00, 461.01-00, 172.01-00, 172.01-05, 172.06-00, 108.01-00, 108.01-01, 108.02-00 -----------------------

Internal Revenue Service Number: 200741003 Release Date: 10/12/2007 Index Number: 468B.07-00, 162.00-00, 461.00-00, 461.01-00, 172.01-00, 172.01-05, 172.06-00, 108.01-00, 108.01-01, 108.02-00 -----------------------

Recognizing Loss Across Borders: More than Meets the Eye

Recognizing Loss Across Borders: More than Meets the Eye Daniel C. White Philip B. Wright April 23, 2015 (updated) St. Louis International Tax Group, Inc. 1 Overview I. Overview II. III. IV. Loss Recognition

Recognizing Loss Across Borders: More than Meets the Eye Daniel C. White Philip B. Wright April 23, 2015 (updated) St. Louis International Tax Group, Inc. 1 Overview I. Overview II. III. IV. Loss Recognition

UNITED STATES TRUSTEE REGION 8 GUIDELINES FOR DEBTORS-IN-POSSESSION

UNITED STATES TRUSTEE REGION 8 GUIDELINES FOR DEBTORS-IN-POSSESSION 1. GENERAL REQUIREMENTS A. Compliance with Laws & Rules - The debtor is required to comply in all respects with the Bankruptcy Code,

UNITED STATES TRUSTEE REGION 8 GUIDELINES FOR DEBTORS-IN-POSSESSION 1. GENERAL REQUIREMENTS A. Compliance with Laws & Rules - The debtor is required to comply in all respects with the Bankruptcy Code,

This publication is distributed with the understanding that the authors and publisher are not engaged in rendering legal, accounting or other

This publication is distributed with the understanding that the authors and publisher are not engaged in rendering legal, accounting or other professional advice and assume no liability in connection with

This publication is distributed with the understanding that the authors and publisher are not engaged in rendering legal, accounting or other professional advice and assume no liability in connection with

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE RECOMMENDATION LANGUAGE The principal amount to be paid to [creditor] is to be reduced to the amount stated in the creditor s proof of

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE RECOMMENDATION LANGUAGE The principal amount to be paid to [creditor] is to be reduced to the amount stated in the creditor s proof of

Wage Garnishments, Levies, And Child Support Withholding

Page 1 Wage Garnishments, Levies, And Child Support Withholding All Wage Garnishments, Levies, and Child Support Withholding Orders are processed by University Payroll Services. Do not accept any Withholding

Page 1 Wage Garnishments, Levies, And Child Support Withholding All Wage Garnishments, Levies, and Child Support Withholding Orders are processed by University Payroll Services. Do not accept any Withholding

INERNATIONAL INSOLVENCY INSTITUTE COMMITTEE ON PRIORITY OF TAX CLAIMS IN INSOLVENCY PROCEEDINGS 1 NATIONAL LAW QUESTIONNAIRE

INERNATIONAL INSOLVENCY INSTITUTE COMMITTEE ON PRIORITY OF TAX CLAIMS IN INSOLVENCY PROCEEDINGS 1 NATIONAL LAW QUESTIONNAIRE NAME OF COUNTRY: NAME, ADDRESS, TELEPHONE, AND EMAIL OF ATTORNEY COMPLETING

INERNATIONAL INSOLVENCY INSTITUTE COMMITTEE ON PRIORITY OF TAX CLAIMS IN INSOLVENCY PROCEEDINGS 1 NATIONAL LAW QUESTIONNAIRE NAME OF COUNTRY: NAME, ADDRESS, TELEPHONE, AND EMAIL OF ATTORNEY COMPLETING

CHAPTER 13 PAYROLL TAX. 13.03 Definitions. As used in this Chapter, unless the context requires otherwise:

CHAPTER 13 PAYROLL TAX 13.03 Definitions. As used in this Chapter, unless the context requires otherwise: A. Department means the Department of Revenue, State of Oregon. B. District means the Tri-County

CHAPTER 13 PAYROLL TAX 13.03 Definitions. As used in this Chapter, unless the context requires otherwise: A. Department means the Department of Revenue, State of Oregon. B. District means the Tri-County

What does it mean for real property to be secured by or encumbered by debt?

What does it mean for real property to be secured by or encumbered by debt? Todd Golub Beverly Katz David A. Miller Baker & McKenzie LLP Internal Revenue Service Ernst & Young LLP Chicago, Illinois Washington,

What does it mean for real property to be secured by or encumbered by debt? Todd Golub Beverly Katz David A. Miller Baker & McKenzie LLP Internal Revenue Service Ernst & Young LLP Chicago, Illinois Washington,

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 11-59 WARNING

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 11-59 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING # 11-59 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

The tax consequences of cancellation of indebtedness

March April 2008 Financially Distressed S Corporations and their Shareholders: Finding Glitz in a Post-Gitlitz World By Steven W. Swibel After the Gitlitz case was decided by the U.S. Supreme Court in

March April 2008 Financially Distressed S Corporations and their Shareholders: Finding Glitz in a Post-Gitlitz World By Steven W. Swibel After the Gitlitz case was decided by the U.S. Supreme Court in

Presentation for. CSEA IRS/Practitioner Fall Seminars. S Corporation. Darrell Early, IRS. Date September 27, 2012

Presentation for CSEA IRS/Practitioner Fall Seminars S Corporation Darrell Early, IRS Date September 27, 2012 Agenda What is an S Corporation? Why would a Corporation make the S election? How does a Corporation

Presentation for CSEA IRS/Practitioner Fall Seminars S Corporation Darrell Early, IRS Date September 27, 2012 Agenda What is an S Corporation? Why would a Corporation make the S election? How does a Corporation

HOMEOWNERS ASSOCIATIONS AND BANKRUPTCY - STRATEGIES

HOMEOWNERS ASSOCIATIONS AND BANKRUPTCY - STRATEGIES DENNIS J. LeVINE, ESQ. Fla. Bar No. 375993 Dennis LeVine & Associates, P.A. P.O. Box 707 Tampa, Florida 33601 (813) 253-0777 (813) 253-0975 (fax) dennis@bcylaw.com

HOMEOWNERS ASSOCIATIONS AND BANKRUPTCY - STRATEGIES DENNIS J. LeVINE, ESQ. Fla. Bar No. 375993 Dennis LeVine & Associates, P.A. P.O. Box 707 Tampa, Florida 33601 (813) 253-0777 (813) 253-0975 (fax) dennis@bcylaw.com

IN THE COMMONWEALTH COURT OF PENNSYLVANIA. City of Philadelphia : : v. : No. 85 C.D. 2006 : Argued: November 14, 2006 James Carpino, : Appellant :

IN THE COMMONWEALTH COURT OF PENNSYLVANIA City of Philadelphia : : v. : No. 85 C.D. 2006 : Argued: November 14, 2006 James Carpino, : Appellant : BEFORE: HONORABLE ROBERT SIMPSON, Judge HONORABLE MARY

IN THE COMMONWEALTH COURT OF PENNSYLVANIA City of Philadelphia : : v. : No. 85 C.D. 2006 : Argued: November 14, 2006 James Carpino, : Appellant : BEFORE: HONORABLE ROBERT SIMPSON, Judge HONORABLE MARY

REAL ESTATE DEBT OUTS ) AND FORECLOSURES: SELECTED TAX CONSEQUENCES

AND FORECLOSURES: SELECTED TAX CONSEQUENCES") REAL ESTATE DEBT RESTRUCTURING ( WORK- OUTS ) AND FORECLOSURES: SELECTED TAX CONSEQUENCES Presented by Robert Falb Robert Honigman Arent Fox LLP Washington, DC New York, NY Los Angeles, CA October 15 and

REAL ESTATE DEBT RESTRUCTURING ( WORK- OUTS ) AND FORECLOSURES: SELECTED TAX CONSEQUENCES Presented by Robert Falb Robert Honigman Arent Fox LLP Washington, DC New York, NY Los Angeles, CA October 15 and

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO In re: ALAN GREENWAY, Bankruptcy Case No. 04-04100 dba Greenway Seed Co., Debtor. MEMORANDUM OF DECISION Appearances: D. Blair Clark, RINGERT,

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO In re: ALAN GREENWAY, Bankruptcy Case No. 04-04100 dba Greenway Seed Co., Debtor. MEMORANDUM OF DECISION Appearances: D. Blair Clark, RINGERT,

Presented by Walter Copeland, CPA Heather Kovalsky, CPA Brimmer, Burek & Keelan LLP

Presented by Walter Copeland, CPA Heather Kovalsky, CPA Brimmer, Burek & Keelan LLP 1. Cost Segregation Study What is a cost segregation study and how is it done? What is the IRS position on cost segregation?

Presented by Walter Copeland, CPA Heather Kovalsky, CPA Brimmer, Burek & Keelan LLP 1. Cost Segregation Study What is a cost segregation study and how is it done? What is the IRS position on cost segregation?

Continuing Professional Education

Continuing Professional Education Course Number CPE20908 Revision Date: 11/15/2008 Debt Relief Income & Insolvent Taxpayer Exclusion Learning Objectives After completing this course, the student will be

Continuing Professional Education Course Number CPE20908 Revision Date: 11/15/2008 Debt Relief Income & Insolvent Taxpayer Exclusion Learning Objectives After completing this course, the student will be