Cegedim Half-year results 2009 September 2009

|

|

|

- Justina Poole

- 7 years ago

- Views:

Transcription

1 Cegedim Half-year results 2009 September

2 Cegedim : Healthcare - its primary market Cegedim Founded in 1969 by Jean-Claude Labrune Jean-Claude Labrune family hold 67 % of Cegedim through FCB 849 millions of revenue in ,200 employees Market leader World leader in the CRM for the pharmaceutical industry Leading provider of strategic data for the pharmaceutical industry European leader of software for healthcare professionals French leader in management of health flows Customers : All players in the healthcare world All major pharmaceutical companies Doctors, pharmacists and paramedics in Europe Insurers and healthcare mutuals in France 2

3 First half-year 2009 Full compliance with banks covenants 6 months in advance 3

4 Healthcare: A steady long-term growth Healthcare continues spending growth Ageing population Global demographics growth Incremental growth of the pharmaceuticals market between $ billions USA China Higher sales of drugs continues India France Japan U.K. Canada Brazil Germany Reducing of hospitalization costs through the use of drugs Expanding the use of drugs from cure to prevention Source Mc Kinsey& Company : 35 to 40 new drugs introduced per year. Source : McKinsey Big pharma companies should launch more products per year between 2006 and 2012 than during the previous 4 years. Source: Datamonitor Need for a high level of marketing spending 4

5 Emerging countries Growth factors Increase of incomes and emergence of middle-class households Improvement of medical infrastructure Rising of chronic diseases (cardiovascular, obesity, diabetes, cancer, asthma) Setting health insurance Adoption of product patents Cegedim Only specialized player on the market Global presence Largest R&D budget on its niche 5

6 Global presence Split of H revenues 6

7 Main Group hosting and R&D centers Largest Hosting facilities and R&D team in the CRM Pharma industry 800 employees 37 % in France, 38 % in India, 13 % in the US and 10 % in Asia 8 % of revenues devoted to R&D Able to respond to global and local clients needs 7

8 Cegedim provides solutions at every stage of drug lifecycle 8

9 Cegedim serves all the healthcare value chain 9

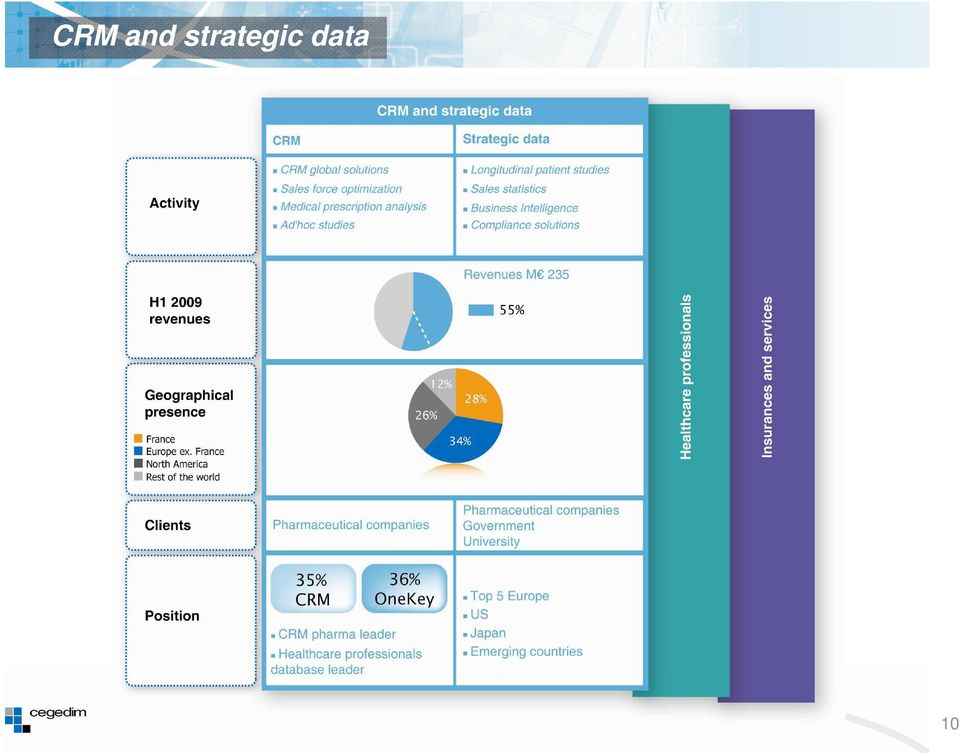

10 CRM and strategic data 10

11 Cegedim s solutions dedicated to pharmaceutical companies 11

12 Cegedim : Positioning at the center of drug world Delivery and sales Pharmaceutical Companies Promotion Wholesalers Data Data Medical Reps Pharmacies Data Data Doctors Products Patients Prescription 12

13 A market share in continuous progression 40% 35% 30% 25% 20% 15% More than 200,000 user in the pharmaceutical industry (Presence in more 80 countries) 10% 5% 0% Evolution of world CRM market share World CRM market share US CRM market share World OneKey market share 13

14 Market trends are opportunities for Cegedim New drugs concern specialties and requires the use of promotional tools ever more sophisticated Product pipeline by 2015 Others 29% Oncology 27% Outsourcing of IT, compliance and databases Increase of regulatory requirements Cardiovascular 7% Gastrointestinal 10% Anti-infective 10% Neuropsychiarty 17% Need of CRM solutions to increase sale force effectiveness KAM, KOL, Analyses, market research, 70% concentrated in 5 therapeutic areas. Source: McKinsey & Company Data are a cornerstone Need for best data in order to optimize the knowledge of 75% prescribers and patients behavior. Without update, data quality decays rapidly 100% 50% 25% 0% Bad Good # of months 14

15 Key customer wins/renewals in 2009 Leading Biotech company EU / Mobile Intelligence SaaS in 32 countries Bristol Myers Squibb US / Support services extension Mobile Intelligence in Neuroscience Sanofi aventis Global / Agreement for Mobile Intelligence as worldwide platform Mid-size pharma companies US / Mobile Intelligence SaaS for KOL and KAM 2 Top 10 pharma company & 1 leading biopharma US / Compliance solutions Auxilium US / Mobile Intelligence SaaS Global food company Europe / Hosting Numerous contracts in OTC Europe / One of the most dynamic segments of the pharmacy market 15

16 Growth factors Sign global contracts Extend our services to all countries (Compliance, Data, Market research ) Extend to other healthcare market our expertise Animal health, consumer health, medical device, health nutrition, Continue to expand our solution of outsourcing of IT infrastructures Release of MI version 5.0 in early September Simplified customization and configuration seamless integration with OneKey) Extend OneKey services with new products Authentication, web access 16

Extend OneKey services")

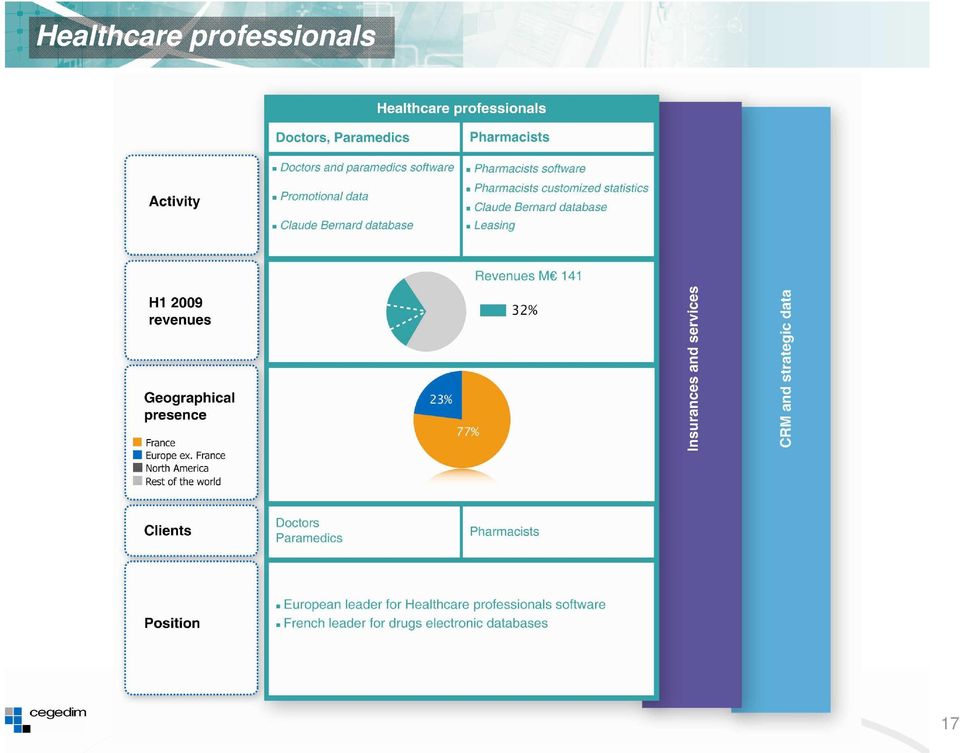

17 Healthcare professionals 17

18 Healthcare professionals Growth factors Interoperability between software Dematerialization of patient data Need for exchange of information between healthcare professionals Qualitative improvement of medical practice Medical control of healthcare spending 18

19 Healthcare professionals 19

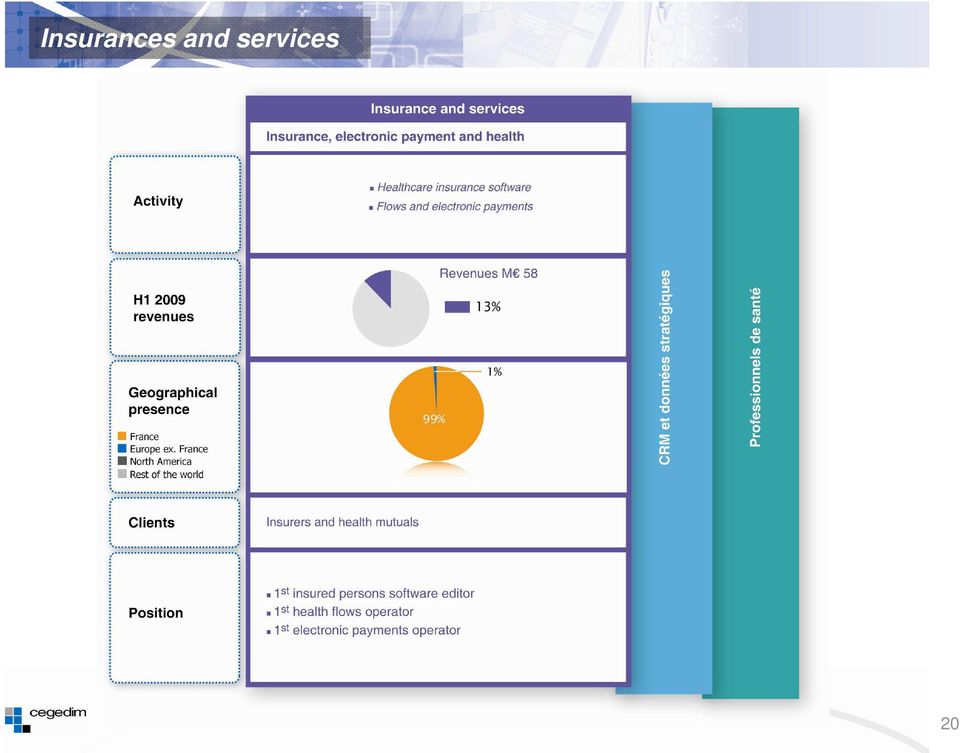

20 Insurances and services 20

21 Insurances and services Software publishing and flows management Publishing sector specific software packages Outsourcing of software solutions for health insurance Management of healthcare flows (250 millions EDI flow per year) Management of healthcare billing and payment flows Services related to front office Growth factors Breakeven of the data flow management platform Willingness of governments to improve the efficiency of healthcare system Merger / concentration Dematerialization Development in Morocco 21

22 Growth strategy Pharmaceutical companies Extend European SaaS model to the US Develop OneKey business in the US Develop business in emerging countries Adapt of outsourcing offer Adapt our products to new needs of sale forces Extend to other healthcare and not healthcare market our expertise External growth Healthcare professionals Expand in US Take advantage of Obama s plan External growth Insurances Development in Morocco Improve product offering Increase the value chain Integration: Become THE platform of flows in France 22

23 Financial Information 23

24 Financial information Good revenue mix By regions By activities By customers Good revenue visibility Strong recurring revenue model Multi-year contracts High switching costs Financial situation under control Net cash of 69M as of June 30 th Full compliance with bank covenants Integration and restructuring plans Positive impact on margins from 1H 2009 R&D optimization 24

25 Growth factors Revenue drivers Market growth Commercial success Successful integration of Dendrite Worldwide player Cegelease Health reforms Margin drivers Integration and restructuring plans R&D optimization Standardization of the CRM product Set up of CHS Strong performance form Insurances and services 25

26 Customer mix Only one customer represents more than 3% of the Group s revenue Sanofi aventis: 6 % of 2008 Group s revenue Top 5 customers 16 % of 2008 Group s revenue Top 10 customers 23 % of 2008 Group s revenue Strong customer loyalty High switching cost High levels of customer satisfaction Long term contracts 26

27 First half-year 2009 revenues: 5% increase L-f-L * (*) at constant scope and exchange rates. 27

28 H margin 28

29 H Operating margin by sectors (*) Operating profit restated with exceptional charges (IFRS) and restructuring and integration costs 29

30 H income statement 30

31 H income statement 31

32 H Balance sheet 32

33 Covenants overview In millions of euros H Total bank borrowings Total cash Net bank loans Net bank debt / Contractual* EBITDA Contractual* EBITDA / Financial expenses (senior debts) * As defined in the covenants of the financial contratc for the acquisition of Dendrite 33

34 H Cash flow 34

35 2009 Outlook Cegedim remains right on tract, is meeting its repayment deadlines and developing new products suited to market needs. As a result, we confirm our 2009 revenue growth target of approximately 6%. Furthermore, all of the cost-cutting measures adopted in 2008 are expected to continue to boost margins, all other things being equal. 35

36 Cegedim market price 105,00 Financial press release 95,00 Q2 07 TO H1 07 Roadshow in Europe Roadshow in the USA 85,00 Q3 07 TO 75,00 65,00 55,00 Q4 07 TO Q1 08 TO Q2 08 TO H1 08 H1 09 Q2 09 TO 45, Results Q3 08 TO 2008 Results RS USA Q1 09 TO 35,00 25,00 Q4 08 TO 31/07/ /12/ /04/ /08/ /12/ /04/ /08/

37 Cegedim share Shareholders Stock information Quotation: NYSE Euronext Paris - compartiment B Quotation date: April 1995 ISIN code: FR Reuters code: CGDM.PA Bloomberg code: CGM Closing date: December, 31 Share value at first listing: 9.52 euros Number of shares at 08/31/2009: 9,331,449 Analysts coverage CA Cheuvreux : Michaël Beucher CM-CIC Securities : Jean-Pascal Brivady Gilbert Dupont : Nicolas Montel / Guillaume Cuvillier Market capitalization at 09/24/2009 : 606 million euros Natixis Securities : Richard Beaudoux Oddo & Cie : Xavier-Emmanuel Pingault Société Générale : Patrick Jousseaume 37

38 Appendix 38

39 Cegedim s history 39

40 No direct competitors on the entire value chain Leasing Mutual software Flows Compliance Pharmacists software Doctors software Market research Strategic data Data base Integration Services CRM SaaS CRM Licence Local actor 40

Cegedim 2008 results and 2009 outlook April 23 th, 2009

Cegedim 2008 results and 2009 outlook April 23 th, 2009 Cegedim profil Founded in 1969 by Jean-Claude Labrune 40 years of experience in healthcare, improving sales and marketing effectiveness for Pharmaceutical

Cegedim 2008 results and 2009 outlook April 23 th, 2009 Cegedim profil Founded in 1969 by Jean-Claude Labrune 40 years of experience in healthcare, improving sales and marketing effectiveness for Pharmaceutical

This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private

Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation Reform Act of 1995). By their nature, forward-looking

Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation Reform Act of 1995). By their nature, forward-looking

Cegedim 2 nd Annual Investor Summit January 12, 2012

Cegedim 2 nd Annual Investor Summit January 12, 2012 Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities

Cegedim 2 nd Annual Investor Summit January 12, 2012 Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities

Cegedim continues to develop

Public company with share capital of 13,336,506.43 euros Trade and Commercial Register: Nanterre B 350 422 622 www.cegedim.com PRESS RELEASE Page 1 Full-Year Financial Information as of December 31, 2010

Public company with share capital of 13,336,506.43 euros Trade and Commercial Register: Nanterre B 350 422 622 www.cegedim.com PRESS RELEASE Page 1 Full-Year Financial Information as of December 31, 2010

DEVOTEAM reports 2011 financials: 7% increase in revenues and 6% growth of diluted earnings per share

DEVOTEAM reports 2011 financials: 7% increase in revenues and 6% growth of diluted earnings per share Paris, February 29 th, 2012 In millions of euros (1) 31.12.2011 31.12.2010 change Revenues 528.1 495.0

DEVOTEAM reports 2011 financials: 7% increase in revenues and 6% growth of diluted earnings per share Paris, February 29 th, 2012 In millions of euros (1) 31.12.2011 31.12.2010 change Revenues 528.1 495.0

HALF-YEARLY NEWS. Letter 13 2007. Touax is listed in Paris on NYSE Euronext Paris Compartment B (ISIN code FR0000033003). Message from the Managers

. Message from the Managers") Letter 13 2007 HALF-YEARLY NEWS Message from the Managers With its position as the leading lessor of shipping containers and river barges in Europe, and as a strong challenger in modular buildings and

Letter 13 2007 HALF-YEARLY NEWS Message from the Managers With its position as the leading lessor of shipping containers and river barges in Europe, and as a strong challenger in modular buildings and

Safe Harbor Statement

1 Safe Harbor Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation Reform Act of 1995). By their nature, forwardlooking

1 Safe Harbor Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation Reform Act of 1995). By their nature, forwardlooking

UDG Healthcare plc An International Healthcare Services Organisation

UDG Healthcare plc An International Healthcare Services Organisation Jefferies 2014 Global Healthcare Conference 2014 Liam FitzGerald, CEO 20 November 2014 1 FORWARD LOOKING STATEMENTS Some statements

UDG Healthcare plc An International Healthcare Services Organisation Jefferies 2014 Global Healthcare Conference 2014 Liam FitzGerald, CEO 20 November 2014 1 FORWARD LOOKING STATEMENTS Some statements

INSIDE Secure First half of 2015 results

INSIDE Secure First half of results Q2 revenue of $18.6 million is up 14% compared with low point reached in Q1 leading to a total of $35.0 million in H1 Adjusted gross margin 1 of $16.4 million (47.0%

INSIDE Secure First half of results Q2 revenue of $18.6 million is up 14% compared with low point reached in Q1 leading to a total of $35.0 million in H1 Adjusted gross margin 1 of $16.4 million (47.0%

Neopost. FY 2002 results

Neopost FY 2002 results April 2003 2002: an eventful year External growth - Finalisation of the acquisition and integration of Ascom Hasler - Acquisition of Stielow Our own achievements - New products

Neopost FY 2002 results April 2003 2002: an eventful year External growth - Finalisation of the acquisition and integration of Ascom Hasler - Acquisition of Stielow Our own achievements - New products

Credit Suisse - Global Health Care Conference. March 1, 2012

Credit Suisse - Global Health Care Conference March 1, 2012 Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties. Future results

Credit Suisse - Global Health Care Conference March 1, 2012 Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties. Future results

From Brand Management to Global Business Management in Market-Driven Companies *

From Brand Management to Global Business Management in Market-Driven Companies * Emilio Zito ** Abstract Over the past several years, the most competitive mass-market companies (automobile, high-tech,

From Brand Management to Global Business Management in Market-Driven Companies * Emilio Zito ** Abstract Over the past several years, the most competitive mass-market companies (automobile, high-tech,

STATS WINDOW. INDUSTRY REVIEW AT A GLANCE Global Pharmaceutical Industry

Volume 6, Issue 6, December 2013 STATS WINDOW The Pacific Business Review International has taken an initiative to start a section which will provide a snapshot of major Global & Indian economic indicators

Volume 6, Issue 6, December 2013 STATS WINDOW The Pacific Business Review International has taken an initiative to start a section which will provide a snapshot of major Global & Indian economic indicators

Ipsen Jefferies Healthcare Conference

Ipsen Jefferies Healthcare Conference November 2015 IPSEN pour nom de la société - 07/04/2011 / page 1 Disclaimer This presentation includes only summary information and does not purport to be comprehensive.

Ipsen Jefferies Healthcare Conference November 2015 IPSEN pour nom de la société - 07/04/2011 / page 1 Disclaimer This presentation includes only summary information and does not purport to be comprehensive.

First quarter 2012 results. Good performance of the 100 % online offering

First quarter 2012 results Good performance of the 100 % online offering Continued momentum in online banking in France 17,000 new current accounts 13,400 new bank savings account Strong growth in balance

First quarter 2012 results Good performance of the 100 % online offering Continued momentum in online banking in France 17,000 new current accounts 13,400 new bank savings account Strong growth in balance

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

P R E S S R E L E A S E

Paris, 5 May 2015 Coface begins 2015 with robust results: increased turnover and profitability in Q1 Growth in turnover : +5.3% at current scope and exchange rates (+2.3% at constant scope and exchange

Paris, 5 May 2015 Coface begins 2015 with robust results: increased turnover and profitability in Q1 Growth in turnover : +5.3% at current scope and exchange rates (+2.3% at constant scope and exchange

EVT Execute & EVT Innovate Leading drug discovery

EVT Execute & EVT Innovate Leading drug discovery Evotec AG, Nine-month 2015 Interim Report, 10 November 2015 Forward-looking statements Information set forth in this presentation contains forward-looking

EVT Execute & EVT Innovate Leading drug discovery Evotec AG, Nine-month 2015 Interim Report, 10 November 2015 Forward-looking statements Information set forth in this presentation contains forward-looking

Most countries will experience an increase in pharmaceutical spending per capita by 2018

6 Most countries will experience an increase in pharmaceutical spending per capita by 218 Pharmaceutical spending per capita, 213 versus 218 1,6 1,4 Pharmaceutical Spend per Capita 1,2 1, 8 6 4 2 US Japan

6 Most countries will experience an increase in pharmaceutical spending per capita by 218 Pharmaceutical spending per capita, 213 versus 218 1,6 1,4 Pharmaceutical Spend per Capita 1,2 1, 8 6 4 2 US Japan

A LEADING GLOBAL HEALTHCARE COMPANY

A LEADING GLOBAL HEALTHCARE COMPANY Roadshow Boston March 2, 2016 Frankfurt stock exchange (DAX30): FRE US ADR program (OTC): FSNUY www.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains

A LEADING GLOBAL HEALTHCARE COMPANY Roadshow Boston March 2, 2016 Frankfurt stock exchange (DAX30): FRE US ADR program (OTC): FSNUY www.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains

Contacts Investor Relations Press Relations

Contacts Investor Relations: Patrick Gouffran +33 (0)1 40 67 29 26 pgouffran@axway.com Press Relations: Sylvie Podetti +33 (0)1 47 17 22 40 spodetti@axway.com Press release Axway: total revenue growth

Contacts Investor Relations: Patrick Gouffran +33 (0)1 40 67 29 26 pgouffran@axway.com Press Relations: Sylvie Podetti +33 (0)1 47 17 22 40 spodetti@axway.com Press release Axway: total revenue growth

The Healthcare market in Brazil

www.pwc.com.br The Healthcare market in Brazil Brazilian Healthcare market: one of the most promising and attractive in the world Context Fifth largest country in area and population, with 8.51 million

www.pwc.com.br The Healthcare market in Brazil Brazilian Healthcare market: one of the most promising and attractive in the world Context Fifth largest country in area and population, with 8.51 million

2014 HALF YEAR RESULTS 4 September 2014

862m H1 2014 Revenues 2014 HALF YEAR RESULTS 4 September 2014 57% of Revenues for International in H1 2014 21,657 Employees In H1 2014 Disclaimer This presentation contains forward-looking statements (as

862m H1 2014 Revenues 2014 HALF YEAR RESULTS 4 September 2014 57% of Revenues for International in H1 2014 21,657 Employees In H1 2014 Disclaimer This presentation contains forward-looking statements (as

33% increase in ADSL Free Cash Flow to 436 million. Successful integration of Alice with a positive contribution of 83 million to the Group s EBITDA

2010 ANNUAL RESULTS Paris, 9 March 2011 Record revenues of 2 billion Group EBITDA in excess of 39% of revenues 78% growth in net profit to 313 million 2G and 3G roaming deal signed with Orange 33% increase

2010 ANNUAL RESULTS Paris, 9 March 2011 Record revenues of 2 billion Group EBITDA in excess of 39% of revenues 78% growth in net profit to 313 million 2G and 3G roaming deal signed with Orange 33% increase

PRESS RELEASE AXA RECORDS VERY STRONG FY07 TOP LINE GROWTH SUSTAINED ORGANIC GROWTH SUCCESSFUL INTEGRATION OF WINTERTHUR

PRESS RELEASE January 31, 2008 AXA RECORDS VERY STRONG FY07 TOP LINE GROWTH SUSTAINED ORGANIC GROWTH SUCCESSFUL INTEGRATION OF WINTERTHUR LIFE & SAVINGS NEW BUSINESS VOLUME 1 UP 24% (UP 8% ON A COMPARABLE

PRESS RELEASE January 31, 2008 AXA RECORDS VERY STRONG FY07 TOP LINE GROWTH SUSTAINED ORGANIC GROWTH SUCCESSFUL INTEGRATION OF WINTERTHUR LIFE & SAVINGS NEW BUSINESS VOLUME 1 UP 24% (UP 8% ON A COMPARABLE

Optimum Solutions Supplied Globally by Hitachi s Consulting Service

Optimum Solutions Supplied Globally by Hitachi s Consulting Service 40 Optimum Solutions Supplied Globally by Hitachi s Consulting Service Sachiko Tsutsui Takashi Hayashi Yasushi Miura Motoki Tsumita OVERVIEW:

Optimum Solutions Supplied Globally by Hitachi s Consulting Service 40 Optimum Solutions Supplied Globally by Hitachi s Consulting Service Sachiko Tsutsui Takashi Hayashi Yasushi Miura Motoki Tsumita OVERVIEW:

Global Privatization Trends in Healthcare and Health Insurance. Hank Kearney Global Health Access, LLC a PHM International company

Global Privatization Trends in Healthcare and Health Insurance Invest 2001 Dubai 3 April, 2001 Hank Kearney Global Health Access, LLC a PHM International company 2001 INVEST 2001 DUBAI HEALTH CARE & INSURANCE

Global Privatization Trends in Healthcare and Health Insurance Invest 2001 Dubai 3 April, 2001 Hank Kearney Global Health Access, LLC a PHM International company 2001 INVEST 2001 DUBAI HEALTH CARE & INSURANCE

DISCUSSION SUMMARY. Q3 & 9M FY16 Results Highlights. Consolidated Financials. About Us. Business Strategy & Outlook

DISHMAN PHARMACEUTICALS & CHEMICALS LIMITED Q3 & 9M FY16 RESULTS UPDATE FEBRUARY 2016 DISCUSSION SUMMARY Q3 & 9M FY16 Results Highlights Consolidated Financials About Us Business Strategy & Outlook 2 SAFE

DISHMAN PHARMACEUTICALS & CHEMICALS LIMITED Q3 & 9M FY16 RESULTS UPDATE FEBRUARY 2016 DISCUSSION SUMMARY Q3 & 9M FY16 Results Highlights Consolidated Financials About Us Business Strategy & Outlook 2 SAFE

2013 FIRST HALF RESULTS

08/29/2013 2013 FIRST HALF RESULTS ANALYSTS AND INVESTORS MEETING Patrick Bensabat Chairman and Chief Executive Officer Christophe Dumoulin Deputy Chief Executive Officer Content 1. The Group 2. Highlights

08/29/2013 2013 FIRST HALF RESULTS ANALYSTS AND INVESTORS MEETING Patrick Bensabat Chairman and Chief Executive Officer Christophe Dumoulin Deputy Chief Executive Officer Content 1. The Group 2. Highlights

A LEADING GLOBAL HEALTH CARE GROUP. Frankfurt Stock Exchange (DAX30): FRE US ADR program (OTC): FSNUY wwww.fresenius.com/investors

: FRE US ADR program (OTC): FSNUY wwww.fresenius.com/investors") A LEADING GLOBAL HEALTH CARE GROUP Frankfurt Stock Exchange (DAX30): FRE US ADR program (OTC): FSNUY wwww.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains forward-looking statements

A LEADING GLOBAL HEALTH CARE GROUP Frankfurt Stock Exchange (DAX30): FRE US ADR program (OTC): FSNUY wwww.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains forward-looking statements

Tieto Corporation. Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014

Tieto Corporation Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014 Financial facts Customer sales in 2013* ) : EUR 1607 million EBIT margin excl. one-off items **) : 8.8%

Tieto Corporation Lasse Heinonen CFO Tanja Lounevirta Head of Investor Relations 27 October 2014 Financial facts Customer sales in 2013* ) : EUR 1607 million EBIT margin excl. one-off items **) : 8.8%

CONTENTS. Executive and supervisory bodies; statutory auditors 3. Financial highlights 4. Interim management report 7

CONTENTS Executive and supervisory bodies; statutory auditors 3 Financial highlights 4 Interim management report 7 Condensed consolidated financial statements 19 Statement by the company officer responsible

CONTENTS Executive and supervisory bodies; statutory auditors 3 Financial highlights 4 Interim management report 7 Condensed consolidated financial statements 19 Statement by the company officer responsible

Ludwigshafen, February 25, 2014

Ludwigshafen, February 25, 2014 Analyst Conference FY2013 Cautionary note regarding forward-looking statements This presentation may contain forward-looking statements that are subject to risks and uncertainties,

Ludwigshafen, February 25, 2014 Analyst Conference FY2013 Cautionary note regarding forward-looking statements This presentation may contain forward-looking statements that are subject to risks and uncertainties,

Annual General Shareholder Meeting. April 28th, 2011

Annual General Shareholder Meeting 1 April 28th, 211 SAF-HOLLAND - Business Units at a Glance Business Unit Trailer Systems Sales 21: EUR 323mn (51% of group sales) Axle Systems Landing Gears Kingpins

Annual General Shareholder Meeting 1 April 28th, 211 SAF-HOLLAND - Business Units at a Glance Business Unit Trailer Systems Sales 21: EUR 323mn (51% of group sales) Axle Systems Landing Gears Kingpins

Financial information - 3 rd quarter and 9 months 2015/2016

Press Release Paris, 11 February 2016 Financial information - 3 rd quarter and 9 months 2015/2016 Strong improvement in third quarter revenue, up 26% on 2014/2015 9 months revenue showed good growth at

Press Release Paris, 11 February 2016 Financial information - 3 rd quarter and 9 months 2015/2016 Strong improvement in third quarter revenue, up 26% on 2014/2015 9 months revenue showed good growth at

Health Care Worldwide. Citi - European Credit Conference September 24, 2015 - London

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Innovations in Pharma Sales Operations

Innovations in Pharma Sales Operations Sales Ops Importance in Pharma Pharmaceutical organizations are going through fundamental restructuring. They are facing changing regulations, intense cost pressure,

Innovations in Pharma Sales Operations Sales Ops Importance in Pharma Pharmaceutical organizations are going through fundamental restructuring. They are facing changing regulations, intense cost pressure,

REFERENCE CODE GDHC269DFR PUBLICATION DATE JULY 2013 PREMARIN (POSTMENOPAUSAL VAGINAL ATROPHY) - FORECAST AND MARKET ANALYSIS TO 2022

- FORECAST AND MARKET ANALYSIS TO 2022") REFERENCE CODE GDHC269DFR PUBLICATION DATE JULY 2013 PREMARIN Executive Summary Premarin (conjugated estrogen cream): Key Metrics in the Seven Major Pharmaceutical Markets 2012 Market Sales US 5EU Japan

REFERENCE CODE GDHC269DFR PUBLICATION DATE JULY 2013 PREMARIN Executive Summary Premarin (conjugated estrogen cream): Key Metrics in the Seven Major Pharmaceutical Markets 2012 Market Sales US 5EU Japan

Global Insurance CONTENTS. Report Synopsis. Industry Surveys. March 2006. 1. Executive Summary 10. 2. Highlights 12

Industry Surveys Global Insurance www.reportsure.com March 2006 Report Synopsis In 2004 insurance premiums accounted for nearly 8% of global GDP, with a value of USD 3,244 billion. The industry grew by

Industry Surveys Global Insurance www.reportsure.com March 2006 Report Synopsis In 2004 insurance premiums accounted for nearly 8% of global GDP, with a value of USD 3,244 billion. The industry grew by

CONFERENCE CALL Q1/2016 RESULTS. Frankfurt stock exchange (DAX30): FRE US ADR program (OTC): FSNUY www.fresenius.com/investors

: FRE US ADR program (OTC): FSNUY www.fresenius.com/investors") CONFERENCE CALL Q1/2016 RESULTS Frankfurt stock exchange (DAX30): FRE US ADR program (OTC): FSNUY www.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains forward-looking statements

CONFERENCE CALL Q1/2016 RESULTS Frankfurt stock exchange (DAX30): FRE US ADR program (OTC): FSNUY www.fresenius.com/investors SAFE HARBOR STATEMENT This presentation contains forward-looking statements

EU Supply Plc ( EU Supply, the Company or the Group ) Interim results for the six months ended 30 June 2015

Interim results for the six months ended 30 June 2015") 9 September EU Supply Plc ( EU Supply, the Company or the Group ) Interim results for the six months ended EU Supply, the e-procurement SaaS provider, is pleased to announce its unaudited interim results

9 September EU Supply Plc ( EU Supply, the Company or the Group ) Interim results for the six months ended EU Supply, the e-procurement SaaS provider, is pleased to announce its unaudited interim results

Press release Regulated information

IBA TRADING UPDATE - THIRD QUARTER 2014 Louvain-La-Neuve, Belgium, 13 November 2014 - IBA (Ion Beam Applications S.A., EURONEXT), the world s leading provider of proton therapy solutions for the treatment

IBA TRADING UPDATE - THIRD QUARTER 2014 Louvain-La-Neuve, Belgium, 13 November 2014 - IBA (Ion Beam Applications S.A., EURONEXT), the world s leading provider of proton therapy solutions for the treatment

Global Pharmaceuticals Marketing Channel Reference EDITION

Global Pharmaceuticals Marketing Channel Reference EDITION 2015 ABOUT IMS HEALTH IMS Health is a leading global information and technology services company providing clients in the healthcare industry

Global Pharmaceuticals Marketing Channel Reference EDITION 2015 ABOUT IMS HEALTH IMS Health is a leading global information and technology services company providing clients in the healthcare industry

shutterstock.com Interim Management and Strategic Transactions for International Life Science Companies TCG: experienced, connected, proven success

shutterstock.com Interim Management and Strategic Transactions for International Life Science Companies TCG: experienced, connected, proven success Proven success and contacts. Not just talk. TCG is a

shutterstock.com Interim Management and Strategic Transactions for International Life Science Companies TCG: experienced, connected, proven success Proven success and contacts. Not just talk. TCG is a

Net attributable income totaled 64.7million in first-half 2015 compared with 69.0 million in firsthalf

HALF-YEAR RESULTS 2015 H1 2015: FURTHER STRONG GROWTH FOR COMMUNICATION AND SHIPPING SOLUTIONS Sales up 10.4%, or -1.1% organically 1 CSS activities: organic growth of 16.0% Current operating margin 2

HALF-YEAR RESULTS 2015 H1 2015: FURTHER STRONG GROWTH FOR COMMUNICATION AND SHIPPING SOLUTIONS Sales up 10.4%, or -1.1% organically 1 CSS activities: organic growth of 16.0% Current operating margin 2

A Leading Global Health Care Group

A Leading Global Health Care Group HSBC Healthcare Day, November 12, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

A Leading Global Health Care Group HSBC Healthcare Day, November 12, 2014 For detailed financial information please see our annual/quarterly reports and/or conference call materials on www.fresenius.com/ir.

Full year results. March 2012

2 0 1 1 Full year results March 2012 1 DISCLAIMER Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation

2 0 1 1 Full year results March 2012 1 DISCLAIMER Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation

Annual Results 2008/2009

Annual Results 2008/2009 Contents Financial statements Financial statements The market Strategy The market Faiveley Transport Outlook Strategy Outlook Outlook 2 Financial statements Financial statements

Annual Results 2008/2009 Contents Financial statements Financial statements The market Strategy The market Faiveley Transport Outlook Strategy Outlook Outlook 2 Financial statements Financial statements

Capital Markets Day, November 28, 2012 TOM TAILOR GROUP - STRATEGY UPDATE DIETER HOLZER CHIEF EXECUTIVE OFFICER

Capital Markets Day, November 28, 2012 TOM TAILOR GROUP - STRATEGY UPDATE DIETER HOLZER CHIEF EXECUTIVE OFFICER TOM TAILOR GROUP AT A GLANCE Retail Wholesale TOM TAILOR BONITA TOM TAILOR Retail stores

Capital Markets Day, November 28, 2012 TOM TAILOR GROUP - STRATEGY UPDATE DIETER HOLZER CHIEF EXECUTIVE OFFICER TOM TAILOR GROUP AT A GLANCE Retail Wholesale TOM TAILOR BONITA TOM TAILOR Retail stores

Dr. Reddy s Q3 and 9M FY16 Financial Results

Press Release DR. REDDY'S LABORATORIES LTD. 8-2-337, Road No. 3, Banjara Hills, Hyderabad - 500034. Telangana, India. INVESTOR RELATIONS KEDAR UPADHYE kedaru@drreddys.com (Ph: +91-40-66834297) CONTACT

Press Release DR. REDDY'S LABORATORIES LTD. 8-2-337, Road No. 3, Banjara Hills, Hyderabad - 500034. Telangana, India. INVESTOR RELATIONS KEDAR UPADHYE kedaru@drreddys.com (Ph: +91-40-66834297) CONTACT

Patient Services Pharma s Best Kept Secret

Accenture Life Sciences Rethink Reshape Restructure...for better patient outcomes Patient Services Pharma s Best Kept Secret Accenture Research Note: Key findings from a survey of 10,000 patients around

Accenture Life Sciences Rethink Reshape Restructure...for better patient outcomes Patient Services Pharma s Best Kept Secret Accenture Research Note: Key findings from a survey of 10,000 patients around

Cloud Computing Market India

Cloud Computing Market India October 2014 Executive Summary Market Overview In, overall value of cloud computing services in India was INR x1, being largely driven by factors such as scalability, flexibility

Cloud Computing Market India October 2014 Executive Summary Market Overview In, overall value of cloud computing services in India was INR x1, being largely driven by factors such as scalability, flexibility

Quarterly Financial Report of Fresenius Group

Quarterly Financial Report of Fresenius Group applying United States Generally Accepted Accounting Principles (US GAAP) 1 st Half and 2 nd Quarter 2009 2 CONTENTS E 3 FRESENIUS GROUP FIGURES AT A GLANCE

Quarterly Financial Report of Fresenius Group applying United States Generally Accepted Accounting Principles (US GAAP) 1 st Half and 2 nd Quarter 2009 2 CONTENTS E 3 FRESENIUS GROUP FIGURES AT A GLANCE

Pascal Quiry July 2010

Please send any questions on this case study to the author via the mail box on the web site www.vernimmen.net Pascal Quiry July 2010 This document may not be used, reproduced or sold without the authorisation

Please send any questions on this case study to the author via the mail box on the web site www.vernimmen.net Pascal Quiry July 2010 This document may not be used, reproduced or sold without the authorisation

Airbus Group Reports Improved Nine-Month (9m) Results 2014

Results 2014") Airbus Group Reports Improved Nine-Month () Results Financial performance reflects operational progress, guidance confirmed Revenues increase four percent to 40.5 billion EBIT* before one-off rises 12

Airbus Group Reports Improved Nine-Month () Results Financial performance reflects operational progress, guidance confirmed Revenues increase four percent to 40.5 billion EBIT* before one-off rises 12

2014 Results. Information meeting 30 March 2015

2014 Results Information meeting 30 March 2015 1 Table of contents 1. Compliance, a public health challenge Dominique Pautrat 2. Financial results on 31 Dec 2014 Jean-Yves Samson 3. 2014 activity and outlooks

2014 Results Information meeting 30 March 2015 1 Table of contents 1. Compliance, a public health challenge Dominique Pautrat 2. Financial results on 31 Dec 2014 Jean-Yves Samson 3. 2014 activity and outlooks

Normand Laberge Vice-President Regulatory & Scientific Affairs Rx&D. Globalization of Clinical Research: Trends & Implications for Canada

Normand Laberge Vice-President Regulatory & Scientific Affairs Rx&D Globalization of Clinical Research: Trends & Implications for Success Rates by Phase and Therapeutic Area Source: Nature Reviews Drug

Normand Laberge Vice-President Regulatory & Scientific Affairs Rx&D Globalization of Clinical Research: Trends & Implications for Success Rates by Phase and Therapeutic Area Source: Nature Reviews Drug

Q3 2015 Financial Results and Corporate Update. November 4, 2015

Q3 2015 Financial Results and Corporate Update November 4, 2015 Introductions and Forward- Looking Statements Silvia Taylor, SVP Investor Relations and Corporate Affairs Agenda Introductions and Forward-Looking

Q3 2015 Financial Results and Corporate Update November 4, 2015 Introductions and Forward- Looking Statements Silvia Taylor, SVP Investor Relations and Corporate Affairs Agenda Introductions and Forward-Looking

Press release Boulogne-Billancourt, 29 July 2015

Press release Boulogne-Billancourt, 29 July 2015 In the appendices included in the press release dated this morning, the consolidated financial data (statement of financial position, income statement and

Press release Boulogne-Billancourt, 29 July 2015 In the appendices included in the press release dated this morning, the consolidated financial data (statement of financial position, income statement and

Improving Asthma Diagnosis and Treatment

Improving Asthma Diagnosis and Treatment January 2015 Contents/Agenda Introduction to Aerocrine Preliminary Q4/YTD 2014 Highlights Aerocrine Evolution NOT FOR DISTRIBUTION IN OR TO THE U.S. (OR TO U.S.

Improving Asthma Diagnosis and Treatment January 2015 Contents/Agenda Introduction to Aerocrine Preliminary Q4/YTD 2014 Highlights Aerocrine Evolution NOT FOR DISTRIBUTION IN OR TO THE U.S. (OR TO U.S.

In millions of euros H1 2015 H1 2014 Change. In millions of euros At June 30, 2015 At Dec 31, 2014 Change

Paris, July 28, 2015 2015 half-year results - NRJ Group Solid growth in Television revenue (+9.7%) Revenue 1 : 185.1 million (+2.0%) Current operating profit 1 : 14.3 million vs. 15.0 million Net profit

Paris, July 28, 2015 2015 half-year results - NRJ Group Solid growth in Television revenue (+9.7%) Revenue 1 : 185.1 million (+2.0%) Current operating profit 1 : 14.3 million vs. 15.0 million Net profit

Health Care Worldwide

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

2014 Wells Fargo Healthcare Conference June 17, 2014 NYSE: Q

2014 Wells Fargo Healthcare Conference June 17, 2014 NYSE: Q Copyright 2013 Quintiles Forward Looking Statements and Use of Non-GAAP Financial Measures This presentation contains forward-looking statements

2014 Wells Fargo Healthcare Conference June 17, 2014 NYSE: Q Copyright 2013 Quintiles Forward Looking Statements and Use of Non-GAAP Financial Measures This presentation contains forward-looking statements

Income Statement Format and Disclosures 2007 Conference call for Financial Analysts, November 2007 Ian Bishop

Income Statement Format and Disclosures 2007 Conference call for Financial Analysts, November 2007 Ian Bishop This presentation contains certain forward-looking statements. These forward-looking statements

Income Statement Format and Disclosures 2007 Conference call for Financial Analysts, November 2007 Ian Bishop This presentation contains certain forward-looking statements. These forward-looking statements

A Leading Global Health Care Group

A Leading Global Health Care Group Credit Suisse Global Health Care Conference, March 4, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials

A Leading Global Health Care Group Credit Suisse Global Health Care Conference, March 4, 2015 For detailed financial information please see our annual/quarterly reports and/or conference call materials

The Shifting World of Debt Collection Eurofinas Session Introduction by BenchMark Consulting International

The Shifting World of Debt Collection Eurofinas Session Introduction by BenchMark Consulting International October 2014 Consulting for Financial Services with Industry Experts Projects in 40 countries

The Shifting World of Debt Collection Eurofinas Session Introduction by BenchMark Consulting International October 2014 Consulting for Financial Services with Industry Experts Projects in 40 countries

Financial results Q1 2015 Numericable-SFR returns to growth, EBITDA up by 21%

Press release Saint-Denis, May 12 th 2015 Financial results Q1 2015 Numericable-SFR returns to growth, EBITDA up by 21% Clear market leader in Fiber with investment plan to accelerate the Fiber and 4G

Press release Saint-Denis, May 12 th 2015 Financial results Q1 2015 Numericable-SFR returns to growth, EBITDA up by 21% Clear market leader in Fiber with investment plan to accelerate the Fiber and 4G

Phone: +44 20 8123 2220 Fax: +44 207 900 3970 office@marketpublishers.com https://marketpublishers.com

North American Home Healthcare Market, By Product [Blood Glucose Meter, ECG, IV Equipment, Nutrition, Wheelchair, Fitness, Heart Rate Monitor, Pregnancy Test Kit], Services [Respiratory Therapy, Rehabilitation

North American Home Healthcare Market, By Product [Blood Glucose Meter, ECG, IV Equipment, Nutrition, Wheelchair, Fitness, Heart Rate Monitor, Pregnancy Test Kit], Services [Respiratory Therapy, Rehabilitation

Great Expectations: Why Pharma Companies Can t Ignore Patient Services

Accenture Life Sciences Rethink Reshape Restructure... for better patient outcomes Great Expectations: Why Pharma Companies Can t Ignore Patient Services Accenture Research Note: Key findings from a survey

Accenture Life Sciences Rethink Reshape Restructure... for better patient outcomes Great Expectations: Why Pharma Companies Can t Ignore Patient Services Accenture Research Note: Key findings from a survey

Medical Equipment Monthly Deals Analysis: January 2015- M&A and Investment Trends

Medical Equipment Monthly Deals Analysis: January 2015- M&A and Investment Trends Reference Code: GDME0470MD Publication Date: March 2015 Independent Medical Equipment Research M&A Trends and Analysis

Medical Equipment Monthly Deals Analysis: January 2015- M&A and Investment Trends Reference Code: GDME0470MD Publication Date: March 2015 Independent Medical Equipment Research M&A Trends and Analysis

S&T - Company Presentation. April 2015

S&T - Company Presentation April 2015 About S&T AG S&T engineers Appliances for vertical markets Appliances comprise of dedicated hardware + combined software solutions Vertical niche solutions for Automation

S&T - Company Presentation April 2015 About S&T AG S&T engineers Appliances for vertical markets Appliances comprise of dedicated hardware + combined software solutions Vertical niche solutions for Automation

Abbott Nutrition. Attractive Profile and Compelling Growth Opportunities

Attractive Profile and Compelling Growth Opportunities Forward-Looking Statement Some statements in this presentation may be forward-looking statements for purposes of the Private Securities Litigation

Attractive Profile and Compelling Growth Opportunities Forward-Looking Statement Some statements in this presentation may be forward-looking statements for purposes of the Private Securities Litigation

FIS Mergent Online. Walsh College Library. Select one or more of the databases to search

Walsh College Library FIS Mergent Online U.S. Company Data Financial information on over 25,000 U.S. public companies (active & inactive) International Company Data Financial information for over 20,000

Walsh College Library FIS Mergent Online U.S. Company Data Financial information on over 25,000 U.S. public companies (active & inactive) International Company Data Financial information for over 20,000

The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results. Profits double as strategy delivers continued improved performance

Unaudited Interim Results. Profits double as strategy delivers continued improved performance") The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results Profits double as strategy delivers continued improved performance The Group (AIM: RTG), one of the UK s leading recruitment

The ReThink Group plc ( ReThink Group or the Group ) Unaudited Interim Results Profits double as strategy delivers continued improved performance The Group (AIM: RTG), one of the UK s leading recruitment

At the heart of activities

Cegedim At the heart of activities Meetings and Demonstration January 11, 2011 Contents Cegedim Group : 2010 Highlights and 2011 Outlook Zoom Cliquez on CRM pour & Strategic modifier Data le style du titre

Cegedim At the heart of activities Meetings and Demonstration January 11, 2011 Contents Cegedim Group : 2010 Highlights and 2011 Outlook Zoom Cliquez on CRM pour & Strategic modifier Data le style du titre

Health Care Worldwide

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

Press Release. Vallourec reports Q4 and Full Year 2012 results

Press Release Vallourec reports Q4 and Full Year 2012 results Boulogne-Billancourt, 20 February 2013 - Vallourec, world leader in premium tubular solutions, today announced its results for the fourth quarter

Press Release Vallourec reports Q4 and Full Year 2012 results Boulogne-Billancourt, 20 February 2013 - Vallourec, world leader in premium tubular solutions, today announced its results for the fourth quarter

GCC Pharmaceutical Industry

GCC Pharmaceutical Industry First coordination meeting for the pharmaceutical industry in the GCC and Yemen Dr. Aasim Qureshi 11 April 2011 Global Pharmaceuticals Industry The pharmaceutical industry is

GCC Pharmaceutical Industry First coordination meeting for the pharmaceutical industry in the GCC and Yemen Dr. Aasim Qureshi 11 April 2011 Global Pharmaceuticals Industry The pharmaceutical industry is

MSD Information Technology Global Innovation Center. Digitization and Health Information Transparency

MSD Information Technology Global Innovation Center Digitization and Health Information Transparency 10 February 2014 1 We are seeking energetic, forward thinking graduates to join our Information Technology

MSD Information Technology Global Innovation Center Digitization and Health Information Transparency 10 February 2014 1 We are seeking energetic, forward thinking graduates to join our Information Technology

EURO DISNEY S.C.A. Reports Fiscal Year 2015 Results

EURO DISNEY S.C.A. Reports 2015 Results Resort revenues increased 9% due to higher volumes and guest spending in both theme parks and hotels, reflecting the success of the Group's long term strategy Real

EURO DISNEY S.C.A. Reports 2015 Results Resort revenues increased 9% due to higher volumes and guest spending in both theme parks and hotels, reflecting the success of the Group's long term strategy Real

A Leading Global Health Care Group

A Leading Global Health Care Group Commerzbank German Investment Seminar January 11/12, 2016 For detailed financial information please see our annual/quarterly reports and/or conference call materials

A Leading Global Health Care Group Commerzbank German Investment Seminar January 11/12, 2016 For detailed financial information please see our annual/quarterly reports and/or conference call materials

Third quarter results as of December 31, 2014. Investor presentation

Third quarter results as of December 31, 2014 Investor presentation February, 26 th 2015 Disclaimer Certain statements included or incorporated by reference within this presentation may constitute forwardlooking

Third quarter results as of December 31, 2014 Investor presentation February, 26 th 2015 Disclaimer Certain statements included or incorporated by reference within this presentation may constitute forwardlooking

Life Sciences & Healthcare

Life Sciences & Healthcare 03 Taylor Wessing is a leading European law firm advising life sciences and healthcare businesses, those who fund them and those who work for them Taylor Wessing has been voted:

Life Sciences & Healthcare 03 Taylor Wessing is a leading European law firm advising life sciences and healthcare businesses, those who fund them and those who work for them Taylor Wessing has been voted:

Trends in the pharmaceutical industry. Presentation to I3H ULB Jan.16

Presentation to I3H ULB Jan.16 1 Hystorical evolution of value added Economic / market Pharma companies had several periods and adapted the value creation model The great success of blockbuster model delayed

Presentation to I3H ULB Jan.16 1 Hystorical evolution of value added Economic / market Pharma companies had several periods and adapted the value creation model The great success of blockbuster model delayed

Global outlook: Healthcare

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

2014 HALF-YEARLY RESULTS

2014 HALF-YEARLY RESULTS Continued revenue growth Run rate for bank card collections in excess of 560 million Strategic investment initiative is maintained Brussels, 30 July 2014, 7:30 AM Regulated information

2014 HALF-YEARLY RESULTS Continued revenue growth Run rate for bank card collections in excess of 560 million Strategic investment initiative is maintained Brussels, 30 July 2014, 7:30 AM Regulated information

Brochure More information from http://www.researchandmarkets.com/reports/3292678/

Brochure More information from http://www.researchandmarkets.com/reports/3292678/ Asia Pacific (India, China, Australia, South Korea & Others) Insulin Market (Rapid Acting, Short Acting, Pre-Mixed, Long

Brochure More information from http://www.researchandmarkets.com/reports/3292678/ Asia Pacific (India, China, Australia, South Korea & Others) Insulin Market (Rapid Acting, Short Acting, Pre-Mixed, Long

Multiple Sclerosis. Current and Future Players. GDHC1009FPR/ Published March 2013

Multiple Sclerosis Current and Future Players GDHC1009FPR/ Published March 2013 Executive Summary Moderate Growth in the Multiple Sclerosis Market is Expected from 2012 2022 GlobalData estimates the 2012

Multiple Sclerosis Current and Future Players GDHC1009FPR/ Published March 2013 Executive Summary Moderate Growth in the Multiple Sclerosis Market is Expected from 2012 2022 GlobalData estimates the 2012

Commercial Insight: Cancer Targeted Therapies and Immunotherapies -Top monoclonal antibody brands will resist competitive pressures through to 2019

Brochure More information from http://www.researchandmarkets.com/reports/1314569/ Commercial Insight: Cancer Targeted Therapies and Immunotherapies -Top monoclonal antibody brands will resist competitive

Brochure More information from http://www.researchandmarkets.com/reports/1314569/ Commercial Insight: Cancer Targeted Therapies and Immunotherapies -Top monoclonal antibody brands will resist competitive

REGISTRATION DOCUMENT 2010 ANNUAL FINANCIAL REPORT INCLUDED

This is a free translation into English of the Document de Référence 2010 issued in French and is provided solely for the convenience of English speaking readers. This document should be read in conjunction

This is a free translation into English of the Document de Référence 2010 issued in French and is provided solely for the convenience of English speaking readers. This document should be read in conjunction

Global Medical Practice Management Software Market Outlook: 2014-2020

Brochure More information from http://www.researchandmarkets.com/reports/3159021/ Global Medical Practice Management Software Market Outlook: 2014-2020 Description: Medical practice management software

Brochure More information from http://www.researchandmarkets.com/reports/3159021/ Global Medical Practice Management Software Market Outlook: 2014-2020 Description: Medical practice management software

Clinical Trial Trends Outline Complexity for Supply Chain. Scott Ohanesian, VP Commercial Operations APAC Email: Scott.Ohanesian@marken.

Clinical Trial Trends Outline Complexity for Supply Chain Scott Ohanesian, VP Commercial Operations APAC Email: Scott.Ohanesian@marken.com 29 May 2013 Biotechnology Sales on the Rise Source: EvaluatePharma

Clinical Trial Trends Outline Complexity for Supply Chain Scott Ohanesian, VP Commercial Operations APAC Email: Scott.Ohanesian@marken.com 29 May 2013 Biotechnology Sales on the Rise Source: EvaluatePharma

The Future of Consumer Health Care

The Future of Consumer Health Care Coming Together To Lead The Consumer Health Care Industry 2 Creating a New Business Model in Consumer Health Care 3 Serve More Consumers In More Parts of the World, More

The Future of Consumer Health Care Coming Together To Lead The Consumer Health Care Industry 2 Creating a New Business Model in Consumer Health Care 3 Serve More Consumers In More Parts of the World, More

Pharmaceutical Sector and

Introduction to the Pharmaceutical Sector and Rebate Contracts in Germany Dr. Frank Verheyen, Director WINEG Tim Steimle, Head of Pharmacy Department Hamburg, May 2010 General Facts about the pharmaceutical

Introduction to the Pharmaceutical Sector and Rebate Contracts in Germany Dr. Frank Verheyen, Director WINEG Tim Steimle, Head of Pharmacy Department Hamburg, May 2010 General Facts about the pharmaceutical

Enhancing Value With Financial & Operational Excellence

Enhancing Value With Financial & Operational Excellence Robert Hombach CFO & COO Enhancing Value With Financial & Operational Excellence Growing Sales & Earnings Generating value in attractive markets

Enhancing Value With Financial & Operational Excellence Robert Hombach CFO & COO Enhancing Value With Financial & Operational Excellence Growing Sales & Earnings Generating value in attractive markets

Credit Suisse Global Health Care Conference. March 5, 2013

Credit Suisse Global Health Care Conference March 5, 2013 Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties. Future results

Credit Suisse Global Health Care Conference March 5, 2013 Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties. Future results

H1 2015 Audio webcast RESULTS PRESENTATION. July 30, 2015

H1 2015 Audio webcast RESULTS PRESENTATION July 30, 2015 DISCLOSURE This presentation contains no confidential material and may include publicly available market information which has not been independently

H1 2015 Audio webcast RESULTS PRESENTATION July 30, 2015 DISCLOSURE This presentation contains no confidential material and may include publicly available market information which has not been independently

EQUINIX, INC. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS - GAAP PRESENTATION (in thousands, except per share data) (unaudited)

(unaudited)") CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS - GAAP PRESENTATION (in thousands, except per share data) Recurring revenues $ 314,727 $ 282,117 $ 216,517 $ 834,080 $ 610,384 Non-recurring revenues 15,620

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS - GAAP PRESENTATION (in thousands, except per share data) Recurring revenues $ 314,727 $ 282,117 $ 216,517 $ 834,080 $ 610,384 Non-recurring revenues 15,620

Delcin Consulting Group

Delcin Consulting Group 1375 Locust Street, Suite 200, Walnut Creek, CA 94596 Phone: 925-276-2095 Fax: 925-276-2096 Email: info@delcinconsulting.com Website: www.delcinconsulting.com All Rights Reserved,

Delcin Consulting Group 1375 Locust Street, Suite 200, Walnut Creek, CA 94596 Phone: 925-276-2095 Fax: 925-276-2096 Email: info@delcinconsulting.com Website: www.delcinconsulting.com All Rights Reserved,

McKesson and the Future of Healthcare

McKesson Corporation One Post Street San Francisco, CA 94104 John H. Hammergren Chairman and Chief Executive Officer To Our Stockholders: Each year at this time, I share with you my perspective on how

McKesson Corporation One Post Street San Francisco, CA 94104 John H. Hammergren Chairman and Chief Executive Officer To Our Stockholders: Each year at this time, I share with you my perspective on how