Sustainable Agro-commercial Finance Limited. AgriFin Webinar Date: July 15, 2015

|

|

|

- Eric Evans

- 7 years ago

- Views:

Transcription

1 Sustainable Agro-commercial Finance Limited AgriFin Webinar Date: July 15, 2015

2 Indian Agriculture Scenario Population - 7% of the world ( growing at the rate of 2% per annum) Land - 2.4% (with 43.0 % under cultivation and less than 21.0% under irrigation ) Water Sources Only 4% of the world (monsoon dependent). Precipitation pattern - Uneven and Erratic. 70% of water is used in Irrigation (major water consuming sector) Thus we need technological intervention to intervene into the - water - food - energy security nexus. And Finance 2

3 Why Modern Irrigation Technologies? The productivity of irrigated land is low compared to its potential. The productivity per unit water is very low. Water available for irrigation is becoming scarcer. Micro Irrigation will increase the irrigation cover using the existing available water. Micro-irrigation with fertigation will enhance production per unit input in nutrient poor soils. 3

4 Challenge Declining water resources and acute power shortage and Competitive demand for land Solutions Precision farming with Micro Irrigation that conserves water and power Result Innovative crop cultivation packages ensuring high productivity per unit input. 4

5 Crops Yield (MT/Ha) Conventional Drip Payback period Incremental Qty Incremental income Approx. Cost of Drip Sugarcane ,000 1,00,000 Cotton ,000 1,00,000 Grapes ,500 1,00,000 Potato ,800 1,00,000 Banana ,00,000 87,000 Tomato ,000 1,00,000 Sweet lime ,00,000 55,000 Watermelon ,10,000 87,000 Incremental income is sufficient for the farmer to repay a loan for installing drip irrigation either after 1 st harvest or at most 2 harvests. 5

6 Jain Irrigation Systems Ltd. (JISL) has a multi product industrial profile aimed at the Farmer community spread largely in the rural and semi-urban areas in India. World number one in Drip Irrigation with Pipe Production World number one in Tissue culture Banana Plant Production Engaged extensively in Tissue Culture, Hybrid & Grafted Plants Pioneer of Micro Irrigation Systems in India Globally second and the largest irrigation Company in India. The largest manufacturer of PVC & PC sheets in India and globally among the first 5 Companies Jain Irrigation Systems Ltd 6

7 About SAFL SAFL is a NBFC promoted by Jain Irrigation Systems Limited (JISL). IFC, Washington is the first and anchor investor in the Company with 10% holding. Recently, Mandala Capital Ltd an agri business focused private equity fund has invested in SAFL to the extent of 20% of the total equity holding of Rs.1200 million.(us $ 20 mn) SAFL is exclusively focused on Farm & Farmer SAFL is the first private sector NBFC in India providing only agri- loans with a wide and diverse range of financing options for almost every need of agricultural activity. 7

8 Objectives of SAFL Farmer Empowerment Increased Agricultural Production Rural Prosperity & Inclusive Growth 8

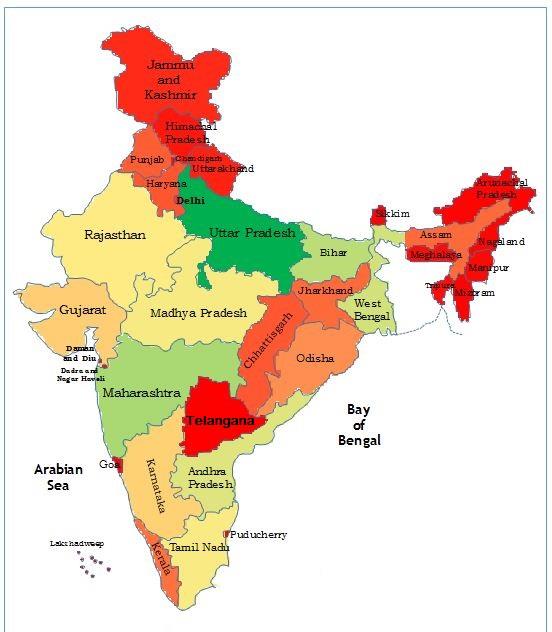

9 Sustainable Agro-commercial Finance Ltd. (SAFL) has been accorded a Certificate of Registration by RBI to function as a Non Banking Finance Company (NBFC) in July SAFL currently has its Head Office in Mumbai, 4 Zonal Offices, 24 Branches & 19 Satellite Offices in Maharashtra state. In addition, SAFL is operating at 6 locations in Karnataka state and 1 location in Telangana state. The distribution network thus comprises 54 offices excluding HO. SAFL is currently offering 10 main products to the agriculture community SAFL s website is An Overview 9

10 INDIA 10

- 47 New Locations other than Maharashtra")

11 Location of Branches in Maharashtra State Satellite Offices -19 Branch /Zonal Offices - 28 Total Offices (Excluding HO) - 47 New Locations other than Maharashtra

12 New Locations in Karnataka & Telangana State New locations other than Maharashtra = 6 Zonal office in Karnataka = 1 12

13 An Overview SAFL has started business operations effectively in April 2013 and has begun its financing activity in the state of Maharashtra, to begin with as Phase I. Phase II will expand operations of SAFL in the states of Karnataka, Andhra Pradesh and Madhya Pradesh. It has started business operations in the state of Karnataka, Andhra Pradesh & Telangana in current FY Phase III will further expand business operations in the states of Gujarat, Tamilnadu, Rajasthan and Haryana. This will occur in FY SAFL will have around 250 offices in India in 5 years time. 13

14 Raising of funds During FY , SAFL has successfully raised funds of Rs 1120 million (approx. US $ mn) by way of equity at premium and debt from an overseas PE Investor by the name of Mandala Capital Ltd.(Mandala). Mandala has invested Rs 240 million (US $ 4 mn) in SAFL s capital with a share premium of Rs 180 million (US $ 3 mn) In addition to the equity subscription mentioned above, Mandala has extended an additional Rs 700 million (US $ mn) to SAFL by way of Non- Convertible Debentures (NCD) without any security. These NCDs are for a period of 75 months to be repaid as a bullet payment after 75 months with half yearly interest payment at rate of 10% p.a. Paid up, Issued and Subscribed Capital: Rs million (US $ 20 mn) 14

Zonal Manager- 1 BDMs- 30 Credit - 2 Legal 1 Recovery - 2 Aurangabad Zone (32) ZM - 1 BDMs- 22 Credit - 4 Legal 3 Recovery-2 Amravati Zone (20) Zonal Manager - 1 BDMs - 16 Credit - 1 Legal - 2")

15 Staff Strength Jalgaon Zone(25) Zonal Manager -1 BDMs 19 Credit 2 Legal 2 Recovery - 1 Mumbai HO (29) MD & CEO -1 Accounts- 4 Admin- 4 Credit- 5 HR-3 IT-1 Legal- 1 Operations-9 Treasury-1 Pune Zone (36) Zonal Manager- 1 BDMs- 30 Credit - 2 Legal 1 Recovery - 2 Aurangabad Zone (32) ZM - 1 BDMs- 22 Credit - 4 Legal 3 Recovery-2 Amravati Zone (20) Zonal Manager - 1 BDMs - 16 Credit - 1 Legal - 2 Total Business Development Managers (BDM) in Maharashtra = ZMs Total (BDM) other than Maharashtra = 5 Total SAFL s staff as on 31 st March 2015:

16 1. Micro Irrigation System Financing 2. Farm equipment financing 3. Contract Farming Finance 4. Agri Projects Financing 5. Agri-business Financing 6. Financing Pipes & or motors / pumps for lift irrigation 7. Dairy Loan Cattle, Equipments & Sheds 8. Solar Module Financing 9. Financing Agro based Industry viz; Ginning mills, Jaggery Unit, food processing unit like fruit juice, Tomato Sauce etc. 10. Short Term Crop Loan Financing offered by SAFL 16

17 Financing offered by SAFL Micro Irrigation System Financing This product is offered to farmers who are in need of financing for purchase / installation of MIS in their farms. The tenor applicable is usually 3 years but can go upto 5 years depending upon crop harvesting period (e.g. pomegranate, mango plantations). Farm Equipment financing This product is offered to farmers who are desirous of buying farm equipment and require financing for the same. These would include tillers, pneumatic ploughs, deweeders, rotavators, harrows, threshers, harvesters etc. The tenure and other product features will vary on the basis of crop; however maximum tenor for this product will be 60 months. 17

18 Financing offered by SAFL Contract Farming Finance This product is offered to farmers who have tie-ups with third party to sell their produce and they are in need of Credit for installation of MIS. The third party will ordinarily guarantee repayment of loan out of agriculture produce supplied by the farmer to the third party. Acceptance of third party s financial credentials will be in conformity with SAFL's pre-determined criteria. Agri Projects Financing Agriculture Project Loans are offered to farmers having strong credit record for a maximum period of 5 years to finance expenses related to farm infra development. Activities that are covered under Agri Project development include land development, farm ponds, Poly Houses / Green Houses, Nursery, Fruit Orchards and such others. 18

19 Financing offered by SAFL Agri-business Financing This product is offered to existing client / farmers / dealers to meet working capital requirements arising out of small and allied businesses. Generally, such type of loan is provided for a maximum period of 3 years and renewed annually on the basis of satisfactory conduct. Financing Pipes & or motors / pumps for lift irrigation This product is offered to farmers who have minimum of 5 acres of land holding and are desirous of installing pipeline for lifting water for their farms and require financing for the same. Components include motors, pumps, pipeline, excavation and installation costs. The tenure is generally 5 years. 19

20 Financing offered by SAFL Dairy Loan Cattle, Equipments & Sheds A medium to long term loan facility to finance expenses related to setting up of dairy project which would include purchase of buffalos / cows / chap cutter / milking machine / shed etc. Solar Module Financing This product is offered to clients for purchase of solar equipment. The objective of this product is to encourage farmers / individuals to invest and utilize renewable sources of energy by providing credit facility in a hassle free manner and at reasonable terms. The usual tenor is 24 to 60 months depending upon the equipment that is financed. Products include solar pumps, solar water heaters, solar lighting appliances. 20

21 Financing offered by SAFL Financing Agro based Industry This product is offered to businesses which require Medium term loan for capital investment or for Short term working capital purpose. Tenure will range between 1 years to 3 years. Businesses include cotton ginning mills, Jaggery units, fruit processing and such others. Short Term Crop Loan is offered as package bundled with other products such as MIS / Lift Irrigation / Agri Project Finance for existing borrowers for meeting immediate needs for working capital of new crops. 21

22 Customer Profile High End Farmers Medium End Farmers Small Farmers Marginal Farmers SAFL Leasehold Land Tillers 22

23 Customer Profile Social Status / Characteristics Leasehold Land Tillers Marginal Farmer Small Farmer Medium End Farmers Higher End Farmers Average Land Holding Annual Family Income 1 acre to 5 acres 1 Acres to 2.5 Acres 2.5 Acres to 5 Acres 5 Acres to 10 Acres > 10 Acres < 1,00,000 < 1,50,000 < 3,00,000 < 6,00,000 > 6,00,000 Repayment Tenure Linked to harvesting cycle Linked to Harvesting Cycle Linked to Harvesting Cycle Linked to Harvesting Cycle Linked to Harvesting Cycle SAFL s customer segment are all individual farmers who are capital starved and need financial assistance for capital investment in their agriculture holding 23

24 Sourcing of business Jain Irrigation has more than 1500 Dealers across Maharashtra state and over 5000 dealers pan India. SAFL also uses the same Dealer network to source clients for its loan products. Thus, most loan proposals originate from Jain Irrigation dealers end. This piggy backing on Jain Irrigation s dealer network facilitates deep penetration minus the distribution cost to SAFL Apart from the above, SAFL s business development officers differentiate potential villages on the basis of various parameters such as crops grown, track record of farmers, availability of irrigation facility, land holding of the farmers and accordingly have been organizing farmer meetings and informing them about various products offered by SAFL. SAFL also organizes camps during a local festival in the villages to impart information and knowledge about the products offered by SAFL. 24

25 Typical Process Flow For Financing Drip Irrigation 1. Jain irrigation s dealer finalises choice of drip irrigation system with farmer including design and components with farmer. He enquires if the farmer needs financing for the same. Most small and marginal farmers need financial assistance. 2. Competitors are banks, co-operative societies & money lenders. The dealer points to SAFL as a good, quick turnaround, hassle free and competitive pricing agency. The dealer offers all assistance to farmer to complete requirements of SAFL. 3. The farmer submits the application form along with land holding documents and KYC documents. The application form provides for information about personal details, land details, family particulars, borrowings, assets, etc. 4. These are handed over by dealer to Business Development Manager (BDM) of SAFL - i.e. the Relationship Manager. 25

26 Typical Process Flow For Financing Drip Irrigation 5. The BDM will carry out a field visit and validate KYC details. He will also verify irrigation source, crop details, standard of living, repayment track record etc. 6. If the loan proposal meets with pre-determined eligibility criteria, only then will the BDM submit above mentioned information and Field Inspection Report (FIR) along with documents to Credit Dept. at Zonal office along with his recommendations. 7. Credit verifies the information contained in the FIR and accompanying documents. Credit also verifies CIBIL (credit information bureau) records to find out loan repayment record. Credit carries out detailed appraisal as per scoring model including rating of the customer, find income levels (pre loan and post loan) to find out capacity towards repayment etc. 26

27 Typical Process Flow For Financing Drip Irrigation 8. Credit either sanctions / rejects the proposal. If sanctioned, Credit issues a sanction letter. The sanction letter is mailed to the BDM who hands it over to the farmer. A copy of the sanction letter also goes to Legal Dept. in zonal office. 9. Legal Dept. prepares the legal documents by filling in all particulars and mails them to BDM to take a print out and execute the same. 10. After execution of legal documents, documents are sent to Legal Dept. for vetting. 11. After vetting legal documents by Legal Dept., and if all documents are in order, Operation department will disburse the loan. 12. In addition to the BDMs, collections and recoveries are carried out by a dedicated Debt Collection team at select locations. 27

28 Process Flow A Summary Dealers provides application forms and information of SAFL s product to the customers Receipt of complete Application form and other documents by dealers / SAFL s Branch staff Verify whether it satisfy minimum criteria Verification by Branch staff with the due diligence / Personal discussion / FIR Execution of Legal documents in line with the sanctions Issuance of Legal documents on the basis of sanctioned terms Appraisal / Sanction by Zonal Credit / appropriate sanctioning authority. Process for disbursement and verification of Legal documents as stipulated in sanction Upon confirmation from Legal, Operations disburses the loan amount and intimate the customer Compliance of Post disbursal documents 28

29 Approach to Credit Decision Borrower Characteristics Crop Characteristics Transactional & Financial Characteristics Credit Score Factor 29

30 Credit Rating Credit rating model is designed on the basis of quantitative as well as qualitative parameters. Some of them are:- Borrower Characteristics Age of the Applicant Annual Family income Year on year growth in income Land holding Farming practice Total loan installment to total income Crop Characteristics Type of Crop with appropriate region Availability of Minimum support price Cropping pattern Potential increase in yield after using MIS Transaction and Financial Characteristics Loan to Valuation of land Tenure of loan Guarantor type CIBIL score 30

31 Performance Indicator Performance indicators of SAFL for the period 1 st April 2014 to 31 st March 2015 Sr. No Category No. of Farmers Amount in Rupees (millions) 1 Sanctions Disbursed Repayments Loan Outstanding NPA (0.70%) Average ticket size per loan:- Rs. 1,20,000 (US $ 2000) Total loan disbursements in last 2 years : over Rs. 2.1 bn (US $ 35 mn) Total farmers assisted in last 27 months : over 20,000 SAFL has broken even in its first full year of business operations 31

32 Cost SAFL operates on cost plus basis. SAFL follows hub & spoke model, where Satellite offices must break even in 1 st year after achieving business of Rs. 30 Mn and are converted into Branch office. Branch offices after achieving business of Rs. 100 Mn are converted into sub-zonal office. 32

33 SWOT Analysis Strengths Easy & Fast appraisal and disbursement based on pre-determined parameters and a credit scoring system. Usage of latest technologies for processing, sanctioning and disbursing loans to farmers. Strong and stable dealer network of Jain Irrigation Systems Ltd. (JISL) which has presence in remote topographies Offer end to end solution to farmers from sale of JISL s product to offering of loans under one roof. Weakness Access to operating capital. 33

34 Opportunity SWOT Analysis Small and marginal farmers who constitute more than 80 per cent of total farmer households in the country face exclusion from the formal financial channels. First entrant in the NBFC channel to provide gamut of agri finance. Threat Downturn in the economy due to low rain fall will have serious impact on the business of SAFL. Competition from existing Banking / Rural banking channels providing loan at lower interest rate. Increase in defaults of agriculture loans in India. 34

35 SAFL's first loan for MIS was sanctioned to Smt. Kamalbai Haribhau Ugale, who is a widow. She belongs to Shevgaon village in Ahmednagar district, Maharashtra state. ACTUAL PICTURES OF BUSINESS SOURCING AND CREATING AWARENESS Smt. Kamalbai Ugale has 1.11 acre land holding which makes her a marginal farmer. Smt. Kamalbai Ugale accepting the sanction letter outside her home from Business Development Manager of SAFL. 35

36 Farmer meetings are arranged regularly across Maharashtra to create awareness about SAFL s products and processes. Jain Irrigation s Dealers acts as First Point of Contact for SAFL s products. Farmers are made aware of pre sanction and post sanction documents that is required to be submitted as well as regarding Rate of interest offered by SAFL for different products. Farmers are also informed about the repercussion of non payment of dues. ACTUAL PICTURES OF BUSINESS SOURCING AND CREATING AWARENESS 36

37 Farmer meetings 37

38 SAFL Officers on field 38

39 SAFL Family 39

40 THE FUTURE VISION TO GROW SAFL INTO A BANK WHICH WOULD BE ONE OF ITS KIND, CATERING TO THE FULL GAMUT OF BANKING SERVICES TO FARMERS ALL OVER INDIA - IN SUM- A UNIQUE INSTITUTION FOCUSSED ON FINANCING AGRICULTURE IN INDIA 40

41

Corporate stewardship Partnering to Improve Agricultural practices. Mumbai Randhir Chauhan

Corporate stewardship Partnering to Improve Agricultural practices Mumbai Randhir Chauhan Flow of Presentation Agriculture in India Overview Present Challenges Why Sustainability? The Way Out Ensuring

Corporate stewardship Partnering to Improve Agricultural practices Mumbai Randhir Chauhan Flow of Presentation Agriculture in India Overview Present Challenges Why Sustainability? The Way Out Ensuring

Muthoot finance ltd. (mfl) IPO note

IPO note") Muthoot finance ltd. (mfl) IPO note Issue Details Issue Date April 18, 2011 April 21, 2011 Issue Size Rs. 8.24-9.01bn Price Band Rs. 160-175 FV Rs.10 Fresh issue 51.5 mn equity shares QIB 50% Non Institutional/HNIs

Muthoot finance ltd. (mfl) IPO note Issue Details Issue Date April 18, 2011 April 21, 2011 Issue Size Rs. 8.24-9.01bn Price Band Rs. 160-175 FV Rs.10 Fresh issue 51.5 mn equity shares QIB 50% Non Institutional/HNIs

Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs)

") Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs) Introduction: The Micro and Small Enterprise (MSE) sector contributes significantly to manufacturing output, employment and exports

Axis Bank Ltd. Policy for lending to Micro and Small Enterprises (MSEs) Introduction: The Micro and Small Enterprise (MSE) sector contributes significantly to manufacturing output, employment and exports

5 Long-term Mechanization Strategy at National Level Issues and Recommendations

5 Long-term Mechanization Strategy at National Level Issues and Recommendations 5.1 PREAMBLE Mechanization has been well received the world over as one of the important elements of modernization of agriculture.

5 Long-term Mechanization Strategy at National Level Issues and Recommendations 5.1 PREAMBLE Mechanization has been well received the world over as one of the important elements of modernization of agriculture.

Agricultural Machinery Custom Hiring Centres (CHC) Model Scheme

Model Scheme") Agricultural Machinery Custom Hiring Centres (CHC) Model Scheme 1. Indian agriculture is undergoing a gradual shift from dependence on human power and animal power to mechanical power because increasing

Agricultural Machinery Custom Hiring Centres (CHC) Model Scheme 1. Indian agriculture is undergoing a gradual shift from dependence on human power and animal power to mechanical power because increasing

1,477 1,688-1,721. Rs.87.7-99.5bn

Larsen and Toubro Finance Holdings (LTFHL) IPO Note: Subscribe 26 th July, 2011 Incorporated in 1994, Larsen and Toubro Finance Holdings is registered with the RBI as an NBFC- Non-Deposit Taking-Systemically

Larsen and Toubro Finance Holdings (LTFHL) IPO Note: Subscribe 26 th July, 2011 Incorporated in 1994, Larsen and Toubro Finance Holdings is registered with the RBI as an NBFC- Non-Deposit Taking-Systemically

FARMER S ACCESS TO AGRICULTURAL CREDIT

FARMER S ACCESS TO AGRICULTURAL CREDIT I. INTRODUCTION Agriculture is a dominant sector of our economy and credit plays an important role in increasing agriculture production. Availability and access to

FARMER S ACCESS TO AGRICULTURAL CREDIT I. INTRODUCTION Agriculture is a dominant sector of our economy and credit plays an important role in increasing agriculture production. Availability and access to

AGRICULTURAL EQUIPMENT SECTOR IN INDIA. September 2009

AGRICULTURAL EQUIPMENT SECTOR IN INDIA September 2009 The share of agriculture in India s GDP has been diminishing The agriculture sector has shown a mild recovery in growth over the past 3 years but the

AGRICULTURAL EQUIPMENT SECTOR IN INDIA September 2009 The share of agriculture in India s GDP has been diminishing The agriculture sector has shown a mild recovery in growth over the past 3 years but the

Housing Development Finance Corporation Limited

Housing Development Finance Corporation Limited March 2014 CONTENTS HDFC Snapshot Mortgage Market in India Operational and Financial Highlights: Mortgages Valuations and Shareholding Key Subsidiaries and

Housing Development Finance Corporation Limited March 2014 CONTENTS HDFC Snapshot Mortgage Market in India Operational and Financial Highlights: Mortgages Valuations and Shareholding Key Subsidiaries and

{' t- A need was felt to formulate a scheme to provide loans to the farming communify for ALL OFFICES

lnstruction Circular No. : 1004 File No. : 30 ALL OFFICES CENTRAL OFFICE, CHANDER MUKHI NARIMAN POINT, MUMBAI-4OOO2 1 PRIORITY SECTOR RURAL DEVELOPMENT DEPARTMENT Date z 07.11.2012 Dept. Running No. :

lnstruction Circular No. : 1004 File No. : 30 ALL OFFICES CENTRAL OFFICE, CHANDER MUKHI NARIMAN POINT, MUMBAI-4OOO2 1 PRIORITY SECTOR RURAL DEVELOPMENT DEPARTMENT Date z 07.11.2012 Dept. Running No. :

Credit Guarantee Fund Trust for Micro and Small Entreprises (CGTMSE) Presentation on Credit Guarantee Scheme

Presentation on Credit Guarantee Scheme") Credit Guarantee Fund Trust for Micro and Small Entreprises (CGTMSE) Presentation on Credit Guarantee Scheme MSE as defined in MSMED Act 2006 Micro and Small Enterprises (MSE) in India MSE is governed

Credit Guarantee Fund Trust for Micro and Small Entreprises (CGTMSE) Presentation on Credit Guarantee Scheme MSE as defined in MSMED Act 2006 Micro and Small Enterprises (MSE) in India MSE is governed

Selfhelpgroups - Default Management and Recoveries: A Study among the Scheduled Caste Women in Andhra Pradesh and Telangana

International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 3 Issue 8 ǁ August. 2014 ǁ PP.58-62 Selfhelpgroups - Default Management and Recoveries:

International Journal of Humanities and Social Science Invention ISSN (Online): 2319 7722, ISSN (Print): 2319 7714 Volume 3 Issue 8 ǁ August. 2014 ǁ PP.58-62 Selfhelpgroups - Default Management and Recoveries:

LOAN ANALYSIS. 1 This is drawn from the FAO-GTZ Aglend Toolkits 1 5 for the training purpose.

LOAN ANALYSIS AGLEND1 is a financial institution that was founded in the early nineties as a microcredit NGO. In the beginning, its target clientele were micro- and small entrepreneurs in the urban area.

LOAN ANALYSIS AGLEND1 is a financial institution that was founded in the early nineties as a microcredit NGO. In the beginning, its target clientele were micro- and small entrepreneurs in the urban area.

IFC and Agri-Finance. Creating Opportunity Where It s Needed Most

IFC and Creating Opportunity Where It s Needed Most Agriculture remains an important activity in emerging markets IMPORTANCE OF AGRICULTURE as major source of livelihood 75% of poor people in developing

IFC and Creating Opportunity Where It s Needed Most Agriculture remains an important activity in emerging markets IMPORTANCE OF AGRICULTURE as major source of livelihood 75% of poor people in developing

Get the facts. What every homeowner who is at least 62 years of age should know about reverse mortgage loans

Get the facts What every homeowner who is at least 62 years of age should know about reverse mortgage loans Dino Guadagnino Reverse Area Sales Manager PHL Federal Reserve Meeting December 1, 2010 1 What

Get the facts What every homeowner who is at least 62 years of age should know about reverse mortgage loans Dino Guadagnino Reverse Area Sales Manager PHL Federal Reserve Meeting December 1, 2010 1 What

An Analytical Study on Production and Export of Fresh and Dry Fruits in Jammu and Kashmir

International Journal of Scientific and Research Publications, Volume 3, Issue 2, February 213 1 An Analytical Study on Production and Export of Fresh and Dry Fruits in Jammu and Kashmir Naseer Ahmad Rather*,

International Journal of Scientific and Research Publications, Volume 3, Issue 2, February 213 1 An Analytical Study on Production and Export of Fresh and Dry Fruits in Jammu and Kashmir Naseer Ahmad Rather*,

SCALING UP AGRICULTURAL FINANCE

SCALING UP AGRICULTURAL FINANCE Can Small Scale farmers be financed on commercial basis by a Financial Institution? The Case of KCB BANK RWANDA LTD Presentation profile 1. Rwanda s Agricultural scene 2.

SCALING UP AGRICULTURAL FINANCE Can Small Scale farmers be financed on commercial basis by a Financial Institution? The Case of KCB BANK RWANDA LTD Presentation profile 1. Rwanda s Agricultural scene 2.

4. EVOLUTION OF CROP INSURANCE SCHEMES IN INDIA

4. EVOLUTION OF CROP INSURANCE SCHEMES IN INDIA 4.1 GENESIS OF CROP INSURANCE SCHEMES IN INDIA What a great achievement for Crop Insurance in India i.e. 250 farmers covered in first ever scheme in 1972

4. EVOLUTION OF CROP INSURANCE SCHEMES IN INDIA 4.1 GENESIS OF CROP INSURANCE SCHEMES IN INDIA What a great achievement for Crop Insurance in India i.e. 250 farmers covered in first ever scheme in 1972

Working Capital Finance to RE SMEs. Gouri Sankar, Managing Director, Maanaveeya Manila, June 16, 2015

Working Capital Finance to RE SMEs Gouri Sankar, Managing Director, Maanaveeya Manila, June 16, 2015 Oikocredit Oikocredit is a Dutch Cooperative working in Development financing in more than 60 countries,

Working Capital Finance to RE SMEs Gouri Sankar, Managing Director, Maanaveeya Manila, June 16, 2015 Oikocredit Oikocredit is a Dutch Cooperative working in Development financing in more than 60 countries,

FOR AFFORDABLE FARM MECHANIZATION NEED, CHALLENGES OPPORTUNITIES

PAY FOR USE FOR AFFORDABLE FARM MECHANIZATION NEED, CHALLENGES OPPORTUNITIES Need For Farm Equipment Rentals and Custom Hiring 2 Small land holdings Underutilized equipment leading to lack of viability

PAY FOR USE FOR AFFORDABLE FARM MECHANIZATION NEED, CHALLENGES OPPORTUNITIES Need For Farm Equipment Rentals and Custom Hiring 2 Small land holdings Underutilized equipment leading to lack of viability

Analysis Of Existing Logistic Setup In Marketing Of Mangoes In Khammam District Of Telangna

IOSR Journal of Engineering (IOSRJEN) ISSN (e): 2250-3021, ISSN (p): 2278-8719 Vol. 05, Issue 12 (December. 2015), V2 PP 42-46 www.iosrjen.org Analysis Of Existing Logistic Setup In Marketing Of Mangoes

IOSR Journal of Engineering (IOSRJEN) ISSN (e): 2250-3021, ISSN (p): 2278-8719 Vol. 05, Issue 12 (December. 2015), V2 PP 42-46 www.iosrjen.org Analysis Of Existing Logistic Setup In Marketing Of Mangoes

A New approach to small

A New approach to small business lending in India contents 01 Addressing a Widespread Credit Shortage 3 02 Lending Products to Suit Your Needs 5 03 Who do we lend to? 7 04 Debt or Equity: Which is right

A New approach to small business lending in India contents 01 Addressing a Widespread Credit Shortage 3 02 Lending Products to Suit Your Needs 5 03 Who do we lend to? 7 04 Debt or Equity: Which is right

FINANCING OF AGRICULTURE BY COMMERCIAL BANKS PROBLEMS FACED BY FARMERS (An Empirical Study)

") FINANCING OF AGRICULTURE BY COMMERCIAL BANKS PROBLEMS FACED BY FARMERS (An Empirical Study) Dr. Kewal Kumar 1 and Atul Gambhir 2 1 Principal, Institute of Management and Technology, Kashipur, Uttarakhand

FINANCING OF AGRICULTURE BY COMMERCIAL BANKS PROBLEMS FACED BY FARMERS (An Empirical Study) Dr. Kewal Kumar 1 and Atul Gambhir 2 1 Principal, Institute of Management and Technology, Kashipur, Uttarakhand

Dairy Farming. 1. Introduction. 2. Scope for Dairy Farming and its National Importance. 3. Financial Assistance Available from Banks for Dairy Farming

Dairy Farming 1. Introduction Dairying is an important source of subsidiary income to small/marginal farmers and agricultural labourers. In addition to milk, the manure from animals provides a good source

Dairy Farming 1. Introduction Dairying is an important source of subsidiary income to small/marginal farmers and agricultural labourers. In addition to milk, the manure from animals provides a good source

Information and Communication Technology for Rural Development

Information and Communication Technology for Rural Development Ankur Mani Tripathi 1, Abhishek Kumar Singh 2, Arvind Kumar 3 * Department of IT, Galgotias College of Engineering and Technology, Gr. Noida

Information and Communication Technology for Rural Development Ankur Mani Tripathi 1, Abhishek Kumar Singh 2, Arvind Kumar 3 * Department of IT, Galgotias College of Engineering and Technology, Gr. Noida

PROJECT PROFILE MODERN COLD STORAGE Prepared by: Kerala State Industrial Development Corporation

PROJECT PROFILE ON MODERN COLD STORAGE Prepared by: Kerala State Industrial Development Corporation PROJECT PROFILE FOR MODERN COLD STORAGE INTRODUCTION Cold Storage is a special kind of room, the temperature

PROJECT PROFILE ON MODERN COLD STORAGE Prepared by: Kerala State Industrial Development Corporation PROJECT PROFILE FOR MODERN COLD STORAGE INTRODUCTION Cold Storage is a special kind of room, the temperature

Comparison of Cost Factor in Formal and Informal Credit Market Fazal Wahid

Comparison of Cost Factor in Formal and Informal Credit Market Abstract The informal credit sources, though their share in the total credit market is declining, can still be reckoned as the main providers

Comparison of Cost Factor in Formal and Informal Credit Market Abstract The informal credit sources, though their share in the total credit market is declining, can still be reckoned as the main providers

INFORMATION BROCHURE. Refinance Scheme for Scheduled Banks for their lending for Housing, 2003

INFORMATION BROCHURE Refinance Scheme for Scheduled Banks for their lending for Housing, 2003 1. Introduction The objective of the scheme is to provide refinance assistance to Scheduled Banks (SBs) in

INFORMATION BROCHURE Refinance Scheme for Scheduled Banks for their lending for Housing, 2003 1. Introduction The objective of the scheme is to provide refinance assistance to Scheduled Banks (SBs) in

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

Poultry Broiler Farming

Poultry Broiler Farming 1. Introduction Poultry meat is an important source of high quality proteins, minerals and vitamins to balance the human diet. Specially developed varieties of chicken (broilers)

Poultry Broiler Farming 1. Introduction Poultry meat is an important source of high quality proteins, minerals and vitamins to balance the human diet. Specially developed varieties of chicken (broilers)

Roles of Public and Private Banks and other Financial Institutions for Effective scaling up of the Insurance Products

Roles of Public and Private Banks and other Financial Institutions for Effective scaling up of the Insurance Products Introduction To achieve the ambitious average GDP growth of 9 per cent per annum target

Roles of Public and Private Banks and other Financial Institutions for Effective scaling up of the Insurance Products Introduction To achieve the ambitious average GDP growth of 9 per cent per annum target

MICRO IRRIGATION A technology to save water

MICRO IRRIGATION A technology to save water 1. Introduction Efficient utilization of available water resources is crucial for a country like, India, which shares 17% of the global population with only

MICRO IRRIGATION A technology to save water 1. Introduction Efficient utilization of available water resources is crucial for a country like, India, which shares 17% of the global population with only

Farmers Cultural Practices. Availability of Planting Material

Identification of Appropriate Postharvest Technologies for Improving Market Access and Incomes for Small Farmers in Sub Saharan Africa and South Asia Commodity Systems Assessment Sunil Saran Amity International

Identification of Appropriate Postharvest Technologies for Improving Market Access and Incomes for Small Farmers in Sub Saharan Africa and South Asia Commodity Systems Assessment Sunil Saran Amity International

Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Unaudited Financial Results Q1 FY 2014-15 July 24, 2014

Unaudited Financial Results Q1 FY 2014-15 July 24, 2014") Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Unaudited Financial Results Q1 FY 2014-15 July 24, 2014 Safe Harbour Statement This document contains certain forward-looking statements

Indiabulls Housing Finance Limited (CIN: L65922DL2005PLC136029) Unaudited Financial Results Q1 FY 2014-15 July 24, 2014 Safe Harbour Statement This document contains certain forward-looking statements

Agricultural Mechanization Strategies in India

050 India Agricultural Mechanization Strategies in India Dr. Champat Raj Mehta Project Coordinator, All India Co-ordinated Research Project (AICRP) on Farm Implements and Machinery (FIM), Central Institute

050 India Agricultural Mechanization Strategies in India Dr. Champat Raj Mehta Project Coordinator, All India Co-ordinated Research Project (AICRP) on Farm Implements and Machinery (FIM), Central Institute

BANK BRANCH AUDIT PLANNING

BANK BRANCH AUDIT PLANNING Banking Industry in India is developing and expanding day by day. The basic work culture in banks in India is fairly different as compared to banks in other countries. The customers

BANK BRANCH AUDIT PLANNING Banking Industry in India is developing and expanding day by day. The basic work culture in banks in India is fairly different as compared to banks in other countries. The customers

SOURCES OF FARM POWER

SOURCES OF FARM POWER A farm power for various agricultural operations can be broadly classified as: (1) Tractive work such as seed bed preparation, cultivation, harvesting and transportation, and (2)

SOURCES OF FARM POWER A farm power for various agricultural operations can be broadly classified as: (1) Tractive work such as seed bed preparation, cultivation, harvesting and transportation, and (2)

MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY

1 MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY Muthoot Vehicle & Asset Finance Ltd. (MVFL) is a Deposit taking Asset Finance Company licensed by the Reserve Bank of India for carrying out non banking

1 MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY Muthoot Vehicle & Asset Finance Ltd. (MVFL) is a Deposit taking Asset Finance Company licensed by the Reserve Bank of India for carrying out non banking

FMB. Financing Agricultural Forum 2012. (March 28 th 30 th 2012) Kampala - Uganda

Kampala - Uganda") FMB Financing Agricultural Forum 2012 (March 28 th 30 th 2012) Kampala - Uganda Contents 1. About FMB 2. Evolution of FMB 3. Product Overview & Characteristics 4. Critical Success Factors 5. Challenges

FMB Financing Agricultural Forum 2012 (March 28 th 30 th 2012) Kampala - Uganda Contents 1. About FMB 2. Evolution of FMB 3. Product Overview & Characteristics 4. Critical Success Factors 5. Challenges

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses by Gary G. Frank 1 Introduction Dairy farms producing milk have numerous sources of income: milk, cull cows, calves,

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses by Gary G. Frank 1 Introduction Dairy farms producing milk have numerous sources of income: milk, cull cows, calves,

NREGA for Water Management

National Rural Employment Guarantee Act NREGA for Water Management 30 th October, 2009 Dr. Rita Sharma Secretary to Government of India Ministry of Rural Development NREGA objective supplement wage-employment

National Rural Employment Guarantee Act NREGA for Water Management 30 th October, 2009 Dr. Rita Sharma Secretary to Government of India Ministry of Rural Development NREGA objective supplement wage-employment

Land Acquisition and Development Finance Part IV

Land Acquisition and Development Finance Part IV In last month s Learn article, we discussed tying up the land and a more in depth formal due diligence process. This article will discuss Development financing.

Land Acquisition and Development Finance Part IV In last month s Learn article, we discussed tying up the land and a more in depth formal due diligence process. This article will discuss Development financing.

Total acres. Land revenue (Rs.) irrigated acres

irrigated acres") Loan Application Format - (CROP LOAN/ KCC) BRANCH Application No. Year The Branch Head IDBI ltd Dear Sir, I/ We hereby apply for a loan of Rs..(Rupees... Only) and furnish below the necessary particulars.

Loan Application Format - (CROP LOAN/ KCC) BRANCH Application No. Year The Branch Head IDBI ltd Dear Sir, I/ We hereby apply for a loan of Rs..(Rupees... Only) and furnish below the necessary particulars.

SREI Infrastructure Ltd.

Report Date 22nd Oct, 2010 Company Name SREI Infrastructure Ltd. Price / Recommendation CMP: - `121 Buy (Medium Risk Medium Return) Company Background SREI Infrastructure Finance Ltd started its operations

Report Date 22nd Oct, 2010 Company Name SREI Infrastructure Ltd. Price / Recommendation CMP: - `121 Buy (Medium Risk Medium Return) Company Background SREI Infrastructure Finance Ltd started its operations

1.0 Marketing KB Drip A Low Cost Drip Solution

1.0 Marketing KB Drip A Low Cost Drip Solution 1.1 Introduction Lack of irrigation is the single most important limiting factor for increasing productivity, cropping intensity and thus, returns to the

1.0 Marketing KB Drip A Low Cost Drip Solution 1.1 Introduction Lack of irrigation is the single most important limiting factor for increasing productivity, cropping intensity and thus, returns to the

Helping New Ag Producers Grow

Helping New Ag Producers Grow Objectives Who is Northwest Farm Credit Services? What services do we provide? How are loan decision made? What are some obstacles our applicants face? Who is Northwest FCS?

Helping New Ag Producers Grow Objectives Who is Northwest Farm Credit Services? What services do we provide? How are loan decision made? What are some obstacles our applicants face? Who is Northwest FCS?

Postal Life Insurance (PLI) IT Modernisation Project

IT Modernisation Project") Postal Life Insurance (PLI) IT Modernisation Project FREQUENTLY ASKED QUESTIONS Part I 1. What is the PLI project? PLI project is a part of the Financial Services System Integration (FSI) solution (IT

Postal Life Insurance (PLI) IT Modernisation Project FREQUENTLY ASKED QUESTIONS Part I 1. What is the PLI project? PLI project is a part of the Financial Services System Integration (FSI) solution (IT

The contribution of Banks & Financial Institutions to the financing of Rural Development

The contribution of Banks & Financial Institutions to the financing of Rural Development Shitangshu Kumar Sur Chowdhury Deputy Governor, Bangladesh Bank - Bangladesh #FinAgri13 140 Overview of Presentation

The contribution of Banks & Financial Institutions to the financing of Rural Development Shitangshu Kumar Sur Chowdhury Deputy Governor, Bangladesh Bank - Bangladesh #FinAgri13 140 Overview of Presentation

Agriculture Insurance Company of India Limited (AIC)

") Q1: What is Insurance? WEATHER BASED CROP INSURANCE SCHEME FREQUENTLY ASKED QUESTIONS (FAQS) Insurance is a tool to protect you against a small probability of a large unexpected loss. It is a technique

Q1: What is Insurance? WEATHER BASED CROP INSURANCE SCHEME FREQUENTLY ASKED QUESTIONS (FAQS) Insurance is a tool to protect you against a small probability of a large unexpected loss. It is a technique

Loan for property (Courtesy: Economic Times, apnaloan & apnapaisa, Accommodation times, i-save & others)

") Loan for property (Courtesy: Economic Times, apnaloan & apnapaisa, Accommodation times, i-save & others) Frequently Asked Questions: Q. What are the steps involve in the process of loan & what fees it

Loan for property (Courtesy: Economic Times, apnaloan & apnapaisa, Accommodation times, i-save & others) Frequently Asked Questions: Q. What are the steps involve in the process of loan & what fees it

Indian Fertilizer Industry in Service of Farmers

Indian Fertilizer Industry in Service of Farmers A. Roy Marketing Director Indian Farmers Fertiliser Cooperative Limited Email: aroy@iffco.in IFA-FAI National Seminar on Sustainable Fertiliser Management

Indian Fertilizer Industry in Service of Farmers A. Roy Marketing Director Indian Farmers Fertiliser Cooperative Limited Email: aroy@iffco.in IFA-FAI National Seminar on Sustainable Fertiliser Management

Indian Mortgage Finance Market Updated for Q1-FY16

ICRA RESEARCH SERVICES Financial ICRA RATING FEATURE Sector Ratings Indian Mortgage Finance Market Updated for Q1-FY16 Performance Review of Housing Finance Companies and Industry Outlook Contacts: Vibha

ICRA RESEARCH SERVICES Financial ICRA RATING FEATURE Sector Ratings Indian Mortgage Finance Market Updated for Q1-FY16 Performance Review of Housing Finance Companies and Industry Outlook Contacts: Vibha

Rating Criteria for Finance Companies

The broad analytical framework used by CRISIL to rate finance companies is the same as that used for banks and financial institutions. In addition, CRISIL also addresses certain issues that are specific

The broad analytical framework used by CRISIL to rate finance companies is the same as that used for banks and financial institutions. In addition, CRISIL also addresses certain issues that are specific

20 th Year of Publication. A monthly publication from South Indian Bank. www.sib.co.in

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 20 th Year of Publication CATEGORIES

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 20 th Year of Publication CATEGORIES

GUIDELINES FOR COMMERCIAL AGRICULTURE CREDIT SCHEME (CACS)

") GUIDELINES FOR COMMERCIAL AGRICULTURE CREDIT SCHEME (CACS) CENTRAL BANK OF NIGERIA (CBN) AND FEDERAL MINISTRY OF AGRICULTURE AND RURAL DEVELOPMENT (FMA&RD) 1.0 Establishment of the Scheme As part of its

GUIDELINES FOR COMMERCIAL AGRICULTURE CREDIT SCHEME (CACS) CENTRAL BANK OF NIGERIA (CBN) AND FEDERAL MINISTRY OF AGRICULTURE AND RURAL DEVELOPMENT (FMA&RD) 1.0 Establishment of the Scheme As part of its

Flexible Repayment at One Acre Fund

Executive Summary To meet client needs cost- effectively, on a large scale, and in difficult operating environments, microfinance institutions (MFIs) have relied on simple and standardized loan products.

Executive Summary To meet client needs cost- effectively, on a large scale, and in difficult operating environments, microfinance institutions (MFIs) have relied on simple and standardized loan products.

Supervision and Follow-up of Advances

Supervision and Follow-up of Advances Jyoti Kumar Pandey Deputy General Manager & Member of Faculty College of Agricultural Banking Reserve Bank of India Pune Credit Life Cycle Theory Credit Opportunity

Supervision and Follow-up of Advances Jyoti Kumar Pandey Deputy General Manager & Member of Faculty College of Agricultural Banking Reserve Bank of India Pune Credit Life Cycle Theory Credit Opportunity

CRISIL Research Impact note

October 2015 Interest rate on home loans to fall 25-30 bps more: CRISIL Research RBI move to cut risk weight will benefit 70% of home loans, 80% of borrowers CRISIL Research expects interest rate on home

October 2015 Interest rate on home loans to fall 25-30 bps more: CRISIL Research RBI move to cut risk weight will benefit 70% of home loans, 80% of borrowers CRISIL Research expects interest rate on home

ESTIMATES OF MORTALITY INDICATORS

CHAPTER 4 ESTIMATES OF MORTALITY INDICATORS Mortality is one of the basic components of population change and related data is essential for demographic studies and public health administration. It is the

CHAPTER 4 ESTIMATES OF MORTALITY INDICATORS Mortality is one of the basic components of population change and related data is essential for demographic studies and public health administration. It is the

19 th Year of Publication. A monthly publication from South Indian Bank. www.sib.co.in

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 19 th Year of Publication SIB STUDENTS

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 19 th Year of Publication SIB STUDENTS

ALLAHABAD BANK SME CREDIT DEPARTMENT HEAD OFFICE: 2, NETHAJI SUBHAS ROAD, KOLKATA-70001

ALLAHABAD BANK SME CREDIT DEPARTMENT HEAD OFFICE: 2, NETHAJI SUBHAS ROAD, KOLKATA-70001 INSTRUCTION CIRCULAR No.13233/ MSME/ 2014-15/04 DATE: 01/08/2014 To: All Offices / Branches Revised General Credit

ALLAHABAD BANK SME CREDIT DEPARTMENT HEAD OFFICE: 2, NETHAJI SUBHAS ROAD, KOLKATA-70001 INSTRUCTION CIRCULAR No.13233/ MSME/ 2014-15/04 DATE: 01/08/2014 To: All Offices / Branches Revised General Credit

LENDING TO PRIORITY SECTOR

LENDING TO PRIORITY SECTOR At a meeting of the National Credit Council held in July 1968, it was emphasised that commercial banks should increase their involvement in the financing of priority sectors,

LENDING TO PRIORITY SECTOR At a meeting of the National Credit Council held in July 1968, it was emphasised that commercial banks should increase their involvement in the financing of priority sectors,

Loan approval procedure and rejection criteria-a conceptual study in PMC bank

Loan approval procedure and rejection criteria-a conceptual study in PMC bank Rekha MFA II year, Jyoti Nivas College Autonomous PG Centre, Bangalore, India B.Percy Bose Associate Professor and Head Department

Loan approval procedure and rejection criteria-a conceptual study in PMC bank Rekha MFA II year, Jyoti Nivas College Autonomous PG Centre, Bangalore, India B.Percy Bose Associate Professor and Head Department

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY

IREDA-NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY SUPPORTED BY THE NATIONAL CLEAN ENERGY FUND IREDA NCEF REFINANCE SCHEME REFINANCE SCHEME FOR PROMOTION OF RENEWABLE ENERGY

Research verification coordinators collaborate with Arkansas Division of Agriculture crop specialists to determine a typical production method for

1 2 3 Research verification coordinators collaborate with Arkansas Division of Agriculture crop specialists to determine a typical production method for application in the crop enterprise budgets. 4 Whole

1 2 3 Research verification coordinators collaborate with Arkansas Division of Agriculture crop specialists to determine a typical production method for application in the crop enterprise budgets. 4 Whole

BASEL DISCLOSURES DOCUMENT AS ON 31 st December 2014 TABLE DF-3 CAPITAL ADEQUACY

BASEL DISCLOSURES DOCUMENT AS ON 31 st December 2014 Qualitative Disclosures (a) A summary discussion of the Bank s approach to assessing the adequacy of its capital to support current and future activities.

BASEL DISCLOSURES DOCUMENT AS ON 31 st December 2014 Qualitative Disclosures (a) A summary discussion of the Bank s approach to assessing the adequacy of its capital to support current and future activities.

Poultry Layer Farming

Poultry Layer Farming 1. Introduction Poultry egg and meat are important sources of high quality proteins, minerals and vitamins to balance the human diet. Commercial layer strains are now available with

Poultry Layer Farming 1. Introduction Poultry egg and meat are important sources of high quality proteins, minerals and vitamins to balance the human diet. Commercial layer strains are now available with

DOCUMENT FOR EXPRESSION OF INTEREST FOR EMPANELMENT OF ADVERTISING AGENCIES

THE ANDHRA PRADESH DAIRY DEVELOPMENT CO-OPERATIVE FEDERATION (APDDCF) LIMITED, LALAPET, HYDERABAD DOCUMENT FOR EXPRESSION OF INTEREST FOR EMPANELMENT OF ADVERTISING AGENCIES ANDHRA PRADESH DAIRY DEVELOPMENT

THE ANDHRA PRADESH DAIRY DEVELOPMENT CO-OPERATIVE FEDERATION (APDDCF) LIMITED, LALAPET, HYDERABAD DOCUMENT FOR EXPRESSION OF INTEREST FOR EMPANELMENT OF ADVERTISING AGENCIES ANDHRA PRADESH DAIRY DEVELOPMENT

AGRICULTURAL PROBLEMS OF JAPAN

AGRICULTURAL PROBLEMS OF JAPAN Takeshi Kimura, Agricultural Counselor Embassy of Japan, Washington, D. C. I would like, first, to sketch the Japanese agricultural situation and, second, to review Japan's

AGRICULTURAL PROBLEMS OF JAPAN Takeshi Kimura, Agricultural Counselor Embassy of Japan, Washington, D. C. I would like, first, to sketch the Japanese agricultural situation and, second, to review Japan's

Reliance Commercial Finance. Loan Against Property. September 2015

Reliance Commercial Finance Loan Against Property September 2015 Disclaimer This presentation does not constitute a prospectus, an offering circular, an advertisement, a private placement offer letter

Reliance Commercial Finance Loan Against Property September 2015 Disclaimer This presentation does not constitute a prospectus, an offering circular, an advertisement, a private placement offer letter

Housing Finance being one of the safest lending avenues has. also contributed to the emergence of new players in the market.not

Introduction: Housing Finance being one of the safest lending avenues has also contributed to the emergence of new players in the market.not only home loans easily available, with intense competition in

Introduction: Housing Finance being one of the safest lending avenues has also contributed to the emergence of new players in the market.not only home loans easily available, with intense competition in

The Consumer and Business Lending Initiative

March 3, 2009 The Consumer and Business Lending Initiative A Note on Efforts to Address Securitization Markets and Increase Lending Overview The Obama administration along with the Federal Reserve, the

March 3, 2009 The Consumer and Business Lending Initiative A Note on Efforts to Address Securitization Markets and Increase Lending Overview The Obama administration along with the Federal Reserve, the

United Bank of India, Head Office: Kolkata Rate of interest Chart on various categories of loans and advances

United Bank of India, Head Office: Kolkata Rate of interest Chart on various categories of loans and advances Sl Category of Advance Rate of Interest (linked with Base rate) Base Rate=9.65% w.e.f 12.10.2015.

United Bank of India, Head Office: Kolkata Rate of interest Chart on various categories of loans and advances Sl Category of Advance Rate of Interest (linked with Base rate) Base Rate=9.65% w.e.f 12.10.2015.

Maharashtra Budget Analysis 2016-17

The Minister of Finance of Maharashtra, Mr. Sudhir Mungantiwar, presented the Budget for Maharashtra for the financial year on March 18, 2016. Budget Highlights The Gross State Domestic Product of Maharashtra

The Minister of Finance of Maharashtra, Mr. Sudhir Mungantiwar, presented the Budget for Maharashtra for the financial year on March 18, 2016. Budget Highlights The Gross State Domestic Product of Maharashtra

National Settlement Services Summit

National Settlement Services Summit Tapping into Reverse Mortgages & the Fastest Growing Mortgage Segment David Gutmann VP & Corporate Counsel Customized Lender s Services Ralph E. Rosynek, Jr. President

National Settlement Services Summit Tapping into Reverse Mortgages & the Fastest Growing Mortgage Segment David Gutmann VP & Corporate Counsel Customized Lender s Services Ralph E. Rosynek, Jr. President

CHAPTER VI ON PRIORITY SECTOR LENDING

CHAPTER VI IMPACT OF PRIORITY SECTOR LENDING 6.1 PRINCIPAL FACTORS THAT HAVE DIRECT IMPACT ON PRIORITY SECTOR LENDING 6.2 ASSOCIATION BETWEEN THE PROFILE VARIABLES AND IMPACT OF PRIORITY SECTOR CREDIT

CHAPTER VI IMPACT OF PRIORITY SECTOR LENDING 6.1 PRINCIPAL FACTORS THAT HAVE DIRECT IMPACT ON PRIORITY SECTOR LENDING 6.2 ASSOCIATION BETWEEN THE PROFILE VARIABLES AND IMPACT OF PRIORITY SECTOR CREDIT

MASTER CIRCULAR ON INTEREST RATES ON ADVANCES

MASTER CIRCULAR ON INTEREST RATES ON ADVANCES A. Purpose To consolidate the directives on interest rates on advances issued by Reserve Bank of India from time to time. B. Classification A statutory directive

MASTER CIRCULAR ON INTEREST RATES ON ADVANCES A. Purpose To consolidate the directives on interest rates on advances issued by Reserve Bank of India from time to time. B. Classification A statutory directive

EVALUATION STUDY OF INTEGRATED RURAL DEVELOPMENT PROGRAMME (IRDP)

") PEO Study No. 134 EVALUATION STUDY OF INTEGRATED RURAL DEVELOPMENT PROGRAMME (IRDP) 1. The Study The integrated Rural Development Programme (IRDP) was launched in 1978-79 in order to deal with the dimensions

PEO Study No. 134 EVALUATION STUDY OF INTEGRATED RURAL DEVELOPMENT PROGRAMME (IRDP) 1. The Study The integrated Rural Development Programme (IRDP) was launched in 1978-79 in order to deal with the dimensions

Arman Financial Services Ltd.

Ahmadabad, India, 8 February, 2016: Arman Financial Services Ltd (Arman), a leading Gujarat based nonbanking financial company (NBFC), with interests in microfinance and two wheelers loans, announced its

Ahmadabad, India, 8 February, 2016: Arman Financial Services Ltd (Arman), a leading Gujarat based nonbanking financial company (NBFC), with interests in microfinance and two wheelers loans, announced its

Trends in Private and Public Investments in Agricultural Marketing Infrastructure in India

Agricultural Economics Research Review Vol. 21 (Conference Number) 2008 pp 371-376 Trends in Private and Public Investments in Agricultural Marketing Infrastructure in India M.S. Jairath* National Institute

Agricultural Economics Research Review Vol. 21 (Conference Number) 2008 pp 371-376 Trends in Private and Public Investments in Agricultural Marketing Infrastructure in India M.S. Jairath* National Institute

How much financing will your farm business

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

IDBI Green Bond Framework

IDBI Green Bond Framework Background IDBI Bank Ltd. is a Universal Bank with its operations driven by a cutting edge core Banking IT platform. The Bank offers personalized banking and financial solutions

IDBI Green Bond Framework Background IDBI Bank Ltd. is a Universal Bank with its operations driven by a cutting edge core Banking IT platform. The Bank offers personalized banking and financial solutions

Low Doc Home Loan Product Specification

Low Doc Home Loan Product Specification For further information www.partners.stgeorge.com.au Mortgage Central 1300 137 532 This product specification is the property of St.George Bank. It is for the use

Low Doc Home Loan Product Specification For further information www.partners.stgeorge.com.au Mortgage Central 1300 137 532 This product specification is the property of St.George Bank. It is for the use

Policy for serving and lending to Micro, small and medium enterprises of India

Policy for serving and lending to Micro, small and medium enterprises of India 1. Background Worldwide, the micro small and medium enterprises (MSMEs) have been accepted as the engine of economic growth

Policy for serving and lending to Micro, small and medium enterprises of India 1. Background Worldwide, the micro small and medium enterprises (MSMEs) have been accepted as the engine of economic growth

The Reverse Mortgage A FINANCIAL SOLUTION TO ELDERS. By Nandhavanam www.icaremylife.com

The Reverse Mortgage A FINANCIAL SOLUTION TO ELDERS By Nandhavanam www.icaremylife.com Concept of Reverse Mortgage During the earning period an individual s major earnings goes towards housing loan repayment.

The Reverse Mortgage A FINANCIAL SOLUTION TO ELDERS By Nandhavanam www.icaremylife.com Concept of Reverse Mortgage During the earning period an individual s major earnings goes towards housing loan repayment.

Schemes for Financing Micro, Small and Medium Enterprises

Schemes for Financing Micro, Small and Medium Enterprises Background The Small Scale Industries Sector, redefined since 2006 as the Micro Small and Medium Enterprises Sector has played a seminal role in

Schemes for Financing Micro, Small and Medium Enterprises Background The Small Scale Industries Sector, redefined since 2006 as the Micro Small and Medium Enterprises Sector has played a seminal role in

Reasons for poor performance of disbursement of Kishan Credit Card and recovery of loan under the scheme in Assam A qualitative study

Volume 2, Issue 1 June 2013 16 RESEARCH ARTICLE ISSN: 2278-5213 Reasons for poor performance of disbursement of Kishan Credit Card and recovery of loan under the scheme in Assam A qualitative study A.

Volume 2, Issue 1 June 2013 16 RESEARCH ARTICLE ISSN: 2278-5213 Reasons for poor performance of disbursement of Kishan Credit Card and recovery of loan under the scheme in Assam A qualitative study A.

CROP INSURANCE TRIBULATIONS AND PROSPECTS OF FARMERS WITH REFERENCE TO NUZVID, KRISHNA DISTRICT

CROP INSURANCE TRIBULATIONS AND PROSPECTS OF FARMERS WITH REFERENCE TO NUZVID, KRISHNA DISTRICT DR.B.RAVI KUMAR ASSISTANT PROFESSOR SREE VIDYANIKETHAN ENGINEERING COLLEGE SREE SAINATH NAGAR A.RANGAMPET,

CROP INSURANCE TRIBULATIONS AND PROSPECTS OF FARMERS WITH REFERENCE TO NUZVID, KRISHNA DISTRICT DR.B.RAVI KUMAR ASSISTANT PROFESSOR SREE VIDYANIKETHAN ENGINEERING COLLEGE SREE SAINATH NAGAR A.RANGAMPET,

DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD)

") DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD) A) Scope of Application : (a) This guidelines applies to Delta Brac Housing Finance Corporation Ltd. (b) (c) DBH has no subsidiary companies. Not

DISCLOSURE ON CAPITAL ADEQUACY & MARKET DISCIPLINE (CAMD) A) Scope of Application : (a) This guidelines applies to Delta Brac Housing Finance Corporation Ltd. (b) (c) DBH has no subsidiary companies. Not

MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY

MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY Muthoot Vehicle & Asset Finance Ltd. (MVFL) is a Deposit taking Asset Finance Company licensed by the Reserve Bank of India for carrying out non banking

MUTHOOT VEHICLE & ASSET FINANCE LTD. LOAN POLICY Muthoot Vehicle & Asset Finance Ltd. (MVFL) is a Deposit taking Asset Finance Company licensed by the Reserve Bank of India for carrying out non banking

CHILLY AND TURMERIC POWDER

CHILLY AND TURMERIC POWDER 1.0 INTRODUCTION Spices are an integral part of the Indian diet since centuries and they are used in vegetarian and non-vegetarian food and snack preparations. They help enhance

CHILLY AND TURMERIC POWDER 1.0 INTRODUCTION Spices are an integral part of the Indian diet since centuries and they are used in vegetarian and non-vegetarian food and snack preparations. They help enhance

The big Small and Medium story - A commentary on SME Financing

The big Small and Medium story - A commentary on SME Financing Mr. Rakesh Singh CEO Limited Key Fundamentals update Developments since Mar 14 Apr Dec 13 Nov 14 New Government Equity Fed tapering / US Recovery

The big Small and Medium story - A commentary on SME Financing Mr. Rakesh Singh CEO Limited Key Fundamentals update Developments since Mar 14 Apr Dec 13 Nov 14 New Government Equity Fed tapering / US Recovery

The Tamilnadu Industrial Investment Corporation Limited, 692, Anna Salai, Nandanam, Chennai 600 0035. FREQUENTLY ASKED QUESTIONS (FAQs)

") The Tamilnadu Industrial Investment Corporation Limited, 692, Anna Salai, Nandanam, Chennai 600 0035. FREQUENTLY ASKED QUESTIONS (FAQs) 1. Does TIIC help in the preparation of project reports for new entrepreneurs?

The Tamilnadu Industrial Investment Corporation Limited, 692, Anna Salai, Nandanam, Chennai 600 0035. FREQUENTLY ASKED QUESTIONS (FAQs) 1. Does TIIC help in the preparation of project reports for new entrepreneurs?

LOW INTEREST LOANS FOR AGRICULTURAL CONSERVATION

LOW INTEREST LOANS FOR AGRICULTURAL CONSERVATION LILAC MANUAL LOW INTEREST LOANS FOR AGRICULTURAL CONSERVATION TABLE OF CONTENTS Introduction... 3 General Eligibility... 4 Specific Eligibility Criteria

LOW INTEREST LOANS FOR AGRICULTURAL CONSERVATION LILAC MANUAL LOW INTEREST LOANS FOR AGRICULTURAL CONSERVATION TABLE OF CONTENTS Introduction... 3 General Eligibility... 4 Specific Eligibility Criteria

Crown Corporation. for the fiscal year 2015 2016. Nova Scotia Farm Loan Board

Crown Corporation B u s i n e s s P l a n s for the fiscal year 2015 2016 Nova Scotia Farm Loan Board Business Plan 2015 2016 Contents Message from the Minister and the Board Chair.... 79 Mission.... 81

Crown Corporation B u s i n e s s P l a n s for the fiscal year 2015 2016 Nova Scotia Farm Loan Board Business Plan 2015 2016 Contents Message from the Minister and the Board Chair.... 79 Mission.... 81

Hippocampus Education Centres Project Report. Background Note on Individual Lending at Swadhaar

Background Note on Individual Lending at Swadhaar Appendix 1 to Streamlining Individual Lending Evaluation Project Report Hippocampus Education Centres Project Report Arun Kumar B Image Image Courtesy

Background Note on Individual Lending at Swadhaar Appendix 1 to Streamlining Individual Lending Evaluation Project Report Hippocampus Education Centres Project Report Arun Kumar B Image Image Courtesy

1. What are the approximate rates for obtaining NHB refinance, NCD, RMBS, Bank loans, Deposits, CPs, ECB, any other instruments?

1. What are the approximate rates for obtaining NHB refinance, NCD, RMBS, Bank loans, Deposits, CPs, ECB, any other instruments? NHB Refinance Under Rural Housing Fund 1 : Interest rate on refinance =

1. What are the approximate rates for obtaining NHB refinance, NCD, RMBS, Bank loans, Deposits, CPs, ECB, any other instruments? NHB Refinance Under Rural Housing Fund 1 : Interest rate on refinance =

CRISIL s Bank Loan Ratings process, scale and default recognition

CRISIL s Bank Loan Ratings process, scale and default recognition Executive Summary A CRISIL bank loan rating (BLR) reflects CRISIL s opinion on the likelihood of the financial obligations (arising out

CRISIL s Bank Loan Ratings process, scale and default recognition Executive Summary A CRISIL bank loan rating (BLR) reflects CRISIL s opinion on the likelihood of the financial obligations (arising out

N200 BILLION INTERVENTION FUND FOR RE-FINANCING AND RESTRUCTURING OF BANKS LOANS TO THE MANUFACTURING SECTOR

N200 BILLION INTERVENTION FUND FOR RE-FINANCING AND RESTRUCTURING OF BANKS LOANS TO THE MANUFACTURING SECTOR 1.0 Introduction CENTRAL BANK OF NIGERIA GUIDELINES The Central Bank of Nigeria in a bid to

N200 BILLION INTERVENTION FUND FOR RE-FINANCING AND RESTRUCTURING OF BANKS LOANS TO THE MANUFACTURING SECTOR 1.0 Introduction CENTRAL BANK OF NIGERIA GUIDELINES The Central Bank of Nigeria in a bid to