HUD s New RESPA Rules for HUD-1: With Q & A

|

|

|

- Lynne Garrison

- 7 years ago

- Views:

Transcription

1 HUD s New RESPA Rules for HUD-1: With Q & A Presented by: Paul McNutt, Jr. General Counsel Title Resources Guaranty Company The Secretary of HUD announced on Nov. 12, 2008, that effective on January 1, 2010, the loans that are regulated under RESPA will require a new three page HUD-1 to close. The new addition to the HUD-1 will have a comparison the title agent must prepare with the amounts on the lender s new required good faith estimate (GFE) that were given to the consumer. This is compared with the actual closing costs incurred in closing. Also, at the end of the normal buyer/seller sections of the HUD-1 there will be on page 3 of the revised HUD-1 a summary of loan terms that must be filled in by the title agent, with the terms of the loan supplied from the lender. 1

2 The purpose of this new HUD-1 form is to enable a customer to compare from their new lender required GFE, the actual costs incurred at closing. They may want to have this to compare before closing the transaction. So you need to be prepared to request the information from the lender necessary to fill out the comparison with their GFE. The real teeth of the new rules is that the lender will be required to give every borrower of a RESPA loan a GFE, and, certain of the costs stated in the lender GFE must be the same in the actual costs you show on the HUD-1. Some costs may vary no more than 10% from the lender s good faith estimate. And, some costs can vary an unlimited amount. A lender that selects the title company for closing must comply. 2

3 The lender must offer any borrower, whose actual costs in the group that must be no more than 10% over the GFE, a reduction of the costs by the amount necessary to have those costs not over 10% higher than the GFE. This adjustment of costs to the consumer must be done by the lender within 30 days after closing. It will be a lender requirement by HUD. It is not a title requirement for the loan to be insured. Therefore, the title agent must see that the numbers are presented exactly as shown on the lender instructions from their GFE, and show how much the amount each of the costs varies from the actual costs incurred, on the 3rd page comparison chart. The title closing agent will not make changes to the actual costs to bring any good faith estimates into compliance. Both because it is a lender required matter to make the adjustments to the actual amounts, and because any such adjustment by the title agent to induce business could be considered a violation of the federal RESPA anti kick-back rules. The changes to the HUD-1 after closing will be done at the office of the lender, who makes the adjustment with the borrower of their costs to be in compliance with their GFE. 3

4 Details about changes to the HUD- 1 Form for 1/1/2010 Page One The first page of the HUD-1 form is almost unchanged. The only addition is a telephone number for the settlement closing agent is now required. Be sure that is added in your form. 4

5 Page Two The second page of the HUD-1 changes to make it more closely align with the revised GFE form of the lender. This is needed to make the comparisons that will be required on the new Page 3 of the HUD-1. As to Sections 800/900/1000, these may be changed by lender s input to HUD before the new forms are effective, but will not be our concern. We will examine in detail the Sections 1100, 1200 and 1300 series. The principal change is the revision to Section 1100 series, Title Charges. 5

6 6

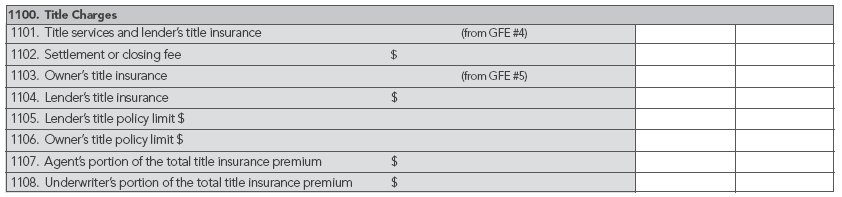

7 1100. Title Charges New Line 1101: Title Services and Lender s Title Insurance Total of all charges formerly itemized in the 1100 series: Lender s Title premium Document Preparation Escrow fees Disbursements to any third parties for title or attorneys regarding closing (Also, will be itemized outside the column later). Here you will include any tax service fees or e filing, down-load fees, etc. The total will be compared with a total from the lender on the GFE on Page 3 of the HUD-1. This will be in the Section for 10% tolerance Title Charges New requirements in HUD s instructions: Certain costs are to be shown in the column,(column meaning the list that will be included in the total shown at line 1400). Others are to be included outside the column (meaning in the lines of text). 7

8 1100. Title Charges Line 1102: Settlement or closing fee Anyone paid fees will be detailed here with text of name and amount, but not in the column Title Charges Line 1103: Owner s Title Policy NEW! This is shown as a borrower cost in column, even if the contract provides that the cost is to be paid by the Seller. The credit to buyer from seller is shown as a page 1 credit to borrower for this cost, if paid by seller. This will be compared with a total from the lender on the GFE on Page 3 of the HUD-1. This will be in the Section for 10% tolerance. 8

9 1100. Title Charges Line 1104: Lender s Title insurance The number is shown here but not in column Title Charges Line 1105: Lender s title policy limit $ This is the liability amount of the policy. The presumption is there is only one Lender s title policy. A second HUD-1 would be required for a split loan. How this is then totaled on the GFE for one lender doing a split loan is not known at this time, but should be answered by HUD before 1/1/

10 1100. Title Charges Line 1106: Owner s title policy limit $ This is the liability amount of the Owner s Title policy. Line 1107: Agent s portion of the total title insurance premium $ This is new and not in column, but a text amount of the part the agent retains Title Charges Line 1108: Underwriter s portion of the total title insurance premium $ This is new and not in column, but a text amount of the underwriters premium amount. Line 1109: Escrow Fee? Not shown, but used in Texas, so probably shown here, not in column as will be totaled with the other 1100 series on line

11 1100. Title Charges Line 1110 Attorney Fees? Not shown, but used in Texas, so probably shown here, not in column, as will be totaled with the other 1100 series on line

12 1200. Government Recording and Transfer Charges Section One Lines 1201, 1202 & 1206 First, the total amount in 1201 of the recording fees. This is in column. This total is also shown in the GFE on the 3rd page and compared in the 10% tolerance column with the amount estimated by the lender Government Recording and Transfer Charges Section One Lines 1201, 1202 & 1206 (cont.) Then, Line 1202 itemizes the total from 1201 by type of document recorded, not in column. The seller portion of these fees must appear in the Seller column and is not totaled in the 1201 total of the borrower but appears as a seller charge for releases. Also, if there are other Seller charges for recording, such as certified copies of probate, heirship affidavits, or divorce decrees, these are itemized on line

13 1200. Government Recording and Transfer Charges Section Two Lines 1203, 1204, & 1205 Second, the amount in 1203 Transfer taxes. This is in column and will be compared with the GFE as a Zero Tolerance item. Lines 1204 and 1205 detail these charges by the City/County and State not in column. As there are no such fees in Texas, this will all be left blank. For all other states, consult your transfer fees. 13

14 1300. Additional Settlement Charges Line 1301 Required services that you can shop for $. This total is all the costs related to such items as survey, pest inspection, radon inspection, or other similar inspections. It is in column. A comparison of the total is made with the GFE on page 3 of the HUD-1, in the unlimited tolerance section. The detailed parties and amounts are then shown on the following lines of 1302, and 1303 not in column if such charges exist Total Settlement Charges This remains the same as in the prior HUD-1. 14

15 Page 3 is new. It begins with the comparisons of each group between the GFE numbers and the HUD-1 actual costs. Then, at the bottom, there is a block for the loan terms. 15

. You place the HUD-1 totals from page 2 in the far column, and the amount given you by the lender from their GFE in the near column.")

16 Comparison of Good Faith Estimate (GFE) and HUD-1 Charges First Section: Charges That Cannot Increase Mostly 800 series lender fees, and the Line 1203 Transfer Taxes (That are not charged in Texas). You place the HUD-1 totals from page 2 in the far column, and the amount given you by the lender from their GFE in the near column. 16

17 Comparison of Good Faith Estimate (GFE) and HUD-1 Charges Second Section: Charges That in Total Cannot Increase More Than 10%. Here are all Title Charges from the 1100 series, and line 1201 Government recording charges of the borrower. You place all the HUD-1 totals of these from page 2 of the HUD-1 in the far column, the GFE totals from the lender in the near column. Then you enter totals of this section HUD-1 and GFE. 17

The final step is to show on the next line the increase (if any) between the GFE and the HUD-1 charges in this section, or the % increase.")

18 Comparison of Good Faith Estimate (GFE) and HUD-1 Charges Second Section: Charges That in Total Cannot Increase More Than 10%. (cont.) The final step is to show on the next line the increase (if any) between the GFE and the HUD-1 charges in this section, or the % increase. If the % is over 10% the lender is under a duty to refund this difference to the borrower within 30 days of funding the loan. 18

19 Comparison of Good Faith Estimate (GFE) and HUD-1 Charges Third Section: Charges That Can Change These include items the borrower controls, such as line 903 homeowner s Insurance, and that depend on the date of the month you close, such as line 90l, the Daily interest charges. They also include the Initial Deposit for your escrow account from line

20 Loan Terms The terms of the loan required to be disclosed on this section are obtained from the lender. The official statement from HUD is: the loan originator shall transmit sufficient information to the closing agent to allow the closing agent to prepare the HUD-1/A, including the new last page. Questions 20

21 Will we use a HUD-1 after 1/1/2010 on any other type of transactions? Definitely not. The new form would be both confusing and unnecessary to any other customer transaction, such as a cash sale, or a commercial transaction. Note also that the new revised HUD-1A form can be used for borrower only transactions. So while you as a title agent are having your computer system reprogrammed to use the new HUD-1 and the new HUD-1A by the beginning of 2010, you will also need a normal closing statement system installed to be used on all other types of transactions that does not have a 3rd page comparison. It is also possible that you may wish to have your system adapt to using a 2 page HUD-1 or HUD-1A for non-hud insured transactions. How can we prepare for this change? You will need to be careful to train on how to review the new HUD-1 with clients, on every loan required to provide the comparison with the new good faith estimate. Be aware that only certain line items will be required to have the comparison of 10% difference, and even that is only as to the total of the section. Not every line item. Where you discover a difference that makes the adjustment by the lender necessary before closing, you should contact the lender and decide how the difference will be handled. It may be changed in the closing, under HUD s guidelines, with a lender credit to borrower possible at closing. Hopefully, this will be rare. 21

22 What if there is a difference between the GFE and the final HUD? Answers from HUD: (T)he rule provides that an inadvertent or technical error in completing the HUD-1/A shall not be deemed a violation of section 4 of RESPA, if a revised HUD-1/A is provided to the borrower and/or seller within 30 calendar days of settlement. This opportunity to cure errors on the HUD-1/A is consistent with HUD s longstanding policy permitting settlement agents to provide revised HUD-1/A settlement statements where errors are discovered after settlement. What if there is a difference between the GFE and the final HUD? Answers from HUD: (cont.) (T)he final rule also provides a loan originator with an opportunity to cure any violation of the tolerance by reimbursing the borrower any amount by which the tolerances were exceeded. This reimbursement bay be made at settlement or within 30 calendar days after settlement. HUD will deem a payment to have been provided in a timely fashion if it is placed in the mail by the loan originator within 30 calendar days after settlement. 22

23 Do we have to re-close if changes are made due to of either errors or reimbursement? HUD states that no signature is required on the HUD-1/A under their regulations, so you may change and resend the lender and parties the corrected HUD-1/A as far as they are regulating the matter. If the lender is required to make a refund you would not be required to handle that money, but could amend the HUD-1/A for all parties when that refund has been made, if requested by the lender. You would need to document the change with a detailed transmittal letter to the parties for your file. How these changes will be handled in your office will be an escrow decision for each agent to adopt before 1/1/2010. Will this new HUD-1/A process be used on all HUD regulated loans? The comparison of costs and requirement of refunds for the 10% tolerance requirements only apply if the lender has directed the business, either by placing the order directly, or having an approved list of title providers. If you are not sure as to whether you are having the lender direct the transaction, or whether you are on their approved provider list, check with the lender before closing beginning January 1,

24 When will changes in the HUD-1/A be required? The implementation is required for all closings that are made January 1, 2010 or later, but many lenders may require use of the new form sooner to be certain they have the process in place if a closing in December were moved to January for any reason. Your computer systems should be enhanced to allow either method before January 1, 2010, so that if you have a closing that holds over into 2010 you also are ready. HUD s Top 21 Questions & Answers on RESPA 2010 Changes as of 11/17/

25 Seller-paid items 1. Q: What if at closing the seller is paying for a settlement service that was listed on the GFE, such as the Owner s title insurance policy? How is that shown on the HUD-1? A: If the seller is paying for a service that was on the GFE, such as Owner s title insurance, the charge remains in the borrower s column on the HUD-1. A credit from the seller to the borrower to offset the charge should be listed on the first page of the HUD-1 in Lines and Lines respectively. HUD Series 2. Q: When the borrower is using a second loan to help finance the purchase of a home, may both loans go on one HUD-1? A: No, each loan must have a separate GFE and a separate HUD-1. The principal amount of the second loan must be listed outside the borrower s column with a brief explanation on Line of the HUD-1 for the primary loan. If the net proceeds of the second loan are less than the principal amount, the net proceeds may be listed on the same line in the borrower s column Second Loan (principal balance $30,000)$29,

26 HUD Series 3. Q: Where do I put the percentage of commission to the real estate agents on the HUD- 1? A: The percentage used to compute the sales commission has been removed from the HUD-1 to better reflect current practices in the real estate industry. The total amount of the commission to each real estate broker or agent must be shown on Lines 701 and 702. The amount of the commissions disbursed at settlement must be shown inside the columns on Line 703. HUD Series 4. Q: May a real estate agent rebate a portion of the agent s commission to the borrower? If so, how should the rebate be listed on the HUD-1? A: Yes, real estate agents may rebate a portion of the agent s commission to the borrower in a real estate transaction. The rebate must be listed as a credit on page 1 of the HUD-1 in Lines , and the name of the party giving the credit must be identified. Real estate agent or broker commission rebates to borrowers do not violate Section 8 of RESPA as long as no part of the commission rebate is tied to a referral of business. 26

27 HUD Series 5. Q: If an attorney prepares loan documents for a lender, where does that charge go on the HUD-1? A: Loan document preparation done on behalf of the loan originator is a processing and administrative service in the origination of a loan and is included in the charge on Line 801 of the HUD-1, and may not be separately itemized. See 24 CFR (b)(1) HUD Series 6. Q: Where is the charge for flood insurance shown on the HUD-1? What if the borrower pays it prior to settlement? A: Flood insurance should be disclosed on Line 904 of the HUD-1 with the charge in the borrower s column. If the borrower pays the insurance prior to closing, the item should be shown on Line 904 of the HUD-1 noted as Paid Outside of Closing or P.O.C. with the charge to the left of the column. 27

28 HUD Series 7. Q: What are title services? A: The term title services includes: 1. Any service involved in the provision of title insurance, including but not limited to: Title examination and evaluation Preparation and issuance of commitment Clearance of underwriting objections Preparation and issuance of policies All processing and administrative services required to perform these functions (e.g. document delivery, preparation and copying, wiring, endorsements, and notary); and 2. The service of conducting a settlement. HUD Series 8. Q: Where should the settlement agent list the commitment fee, wire fee and other miscellaneous title fees on the HUD-1? A: The commitment fee, wire fee, and other miscellaneous fees are included as processing and administrative fees that are part of the definition of title services. All of these types of fees must be included in the charges shown on Line 1101 of the HUD-1, and are not to be itemized separately. 28

29 HUD Series 9. Q: Are document preparation fees included in title services or would they appear as separate line item charges in the borrower s column? A: Document preparation fees are part of administrative or processing fees which are included in the charge in Line 1101 of the HUD-1 and may not be separately itemized. HUD Series 10. Q: Are delivery fees included in title services and therefore included in the Line 1101 of the HUD-1? A: Yes, delivery fees are included in the definition of title services and are included in the charge shown in Line 1101 of the HUD-1. 29

30 HUD Series 11. Q: Are notary fees included in title services and therefore included in Line 1101 of the HUD-1? A: Yes, notary fees are included in the definition of title services and are included in the charge shown in Line 1101 of the HUD-1. HUD Series 12. Q: How is the premium recorded on the HUD- 1if the borrower purchases an enhanced owner s title insurance policy, rather than a basic policy? A: Regardless of whether the borrower chooses to purchase a basic or an enhanced owner s title insurance policy, the premium must be listed in the borrower s column of Line

31 HUD Series 13. Q: If the title agent conducts the settlement, should the charge for conducting the settlement be included in Line 1101 of the HUD-1 with the itemized charge listed outside the column on Line 1102? A: Yes, the charge for conducting the settlement must be included in the total on Line If the charge is paid to a third party, the charge must be itemized outside of the columns on Line HUD Series 14. Q: If the settlement agent hires or pays a third party to facilitate electronic filing, where would that charge be shown on the HUD-1? A: If the settlement agent hires or pays a third party to facilitate electronic filing and the third party is not a governmental entity, the service to facilitate electronic filing is considered an administrative or processing fee included in the charge for title services in Line 1101 on the HUD-1. 31

32 HUD Series 15. Q:If State law requires further itemization of title services or title insurance related fees such as a commitment fee or fees for endorsements to a title policy, how should these fees be listed on the HUD-1? A: If state law requires further itemization of title service or title insurance related fees than required under RESPA, those fees may be itemized on blank lines in the 1100 series on the HUD-1 with the charge listed outside the borrower s column. Endorsements to a title insurance policy may also be listed in Lines 1103 and 1104 as applicable, with the charge listed outside the borrower s column. HUD Series 16. Q: If there are additional governmental recording fees, such as a power of attorney or road maintenance agreement, are they included in Line 1201 of the HUD-1 or can they be charged separately? A: Line 1201 is used to record the total government recording charges. Additional items the lender requires to be recorded, other than those already enumerated in Line 1202, must be itemized on Line The charges for these additional items must be stated outside the column. 32

33 HUD Series 17. Q: If it is required by state or local law for a seller to pay a portion of the total charge for transfer taxes, on what line should the seller s charge be listed on the HUD- 1? A: If it is required by state law for a seller to pay a portion of the total charge for transfer taxes and therefore not on the GFE, the seller s charge should be listed as a charge in the seller s column in Lines 1204 and 1205 on the HUD-1, and the total charges for transfer taxes should be itemized to the left of those columns, as indicated in the following example: 33

34 HUD Series 18. Q: What charges are shown on Line 1301 of the HUD-1? A: Line 1301 is the total of all charges for third party settlement services that the loan originator required but for which the borrower was permitted to select the service provider. The charge on Line 1301 is shown in the borrower s column. All charges included in the total amount on Line 1301 must be separately itemized outside of the columns in Lines 1302 and subsequent lines, identifying the type of service, the name of the provider, and the amount of the charge. HUD Series 19. Q: Where should the charge for the Homeowners Association (HOA) transfer fee be disclosed on the GFE and HUD-1? A: The charge for the HOA transfer fee, unless it is a service required by the loan originator, need not be disclosed on the GFE. The charge for the HOA transfer fee may be shown on a blank line in the 1300 series on the HUD-1. 34

35 20. Q: If a settlement agent revises a HUD-1 to cure a technical error or to reflect a tolerance cure, may the settlement agent mark the HUD-1 as Amended to distinguish from the original HUD-1? A: Yes. If a settlement agent revises a HUD-1 to cure a technical error or to reflect a tolerance cure, the settlement agent may mark the HUD-1 as Amended to distinguish it from the original HUD Q: May a credit for a tolerance cure be listed on page 1 of the HUD-1? A: The cure for a potential tolerance violation may be listed as a credit to the borrower on page 1 of the HUD-1 with a description of the service(s) the credit is applied to. If the tolerance cure is applied to the overall tolerance category Charges That in Total Cannot Increase More Than 10%, the tolerance cure credit may be listed as a lump sum amount on a blank line in Lines with a description of the tolerance category cure. The comparison chart on page 3 of the HUD-1 should reflect the credit given for that service to cure the potential tolerance violation in the appropriate tolerance category. 35

36 This example illustrates a $180 tolerance cure for the 10% tolerance category: 36

Reference for Closing Agents To Provide to Lender Customers. Excerpts from RESPA Rules and FAQ s

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1

& Settlement Statement HUD-1") RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1 2013 Rushmore Loan Management Services LLC. All Rights Reserved. 1 REAL ESTATE SETTLEMENT PROCEDURES ACT RESPA NEW RULE TIMELINE NOVEMBER

RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1 2013 Rushmore Loan Management Services LLC. All Rights Reserved. 1 REAL ESTATE SETTLEMENT PROCEDURES ACT RESPA NEW RULE TIMELINE NOVEMBER

The New RESPA Closing Process

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

EXPLANATION OF THE HUD-1 Settlement Statement

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

Completing the New HUD-1 Settlement Statement

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

Line 700: This line should reflect a calculation of the commission to be paid.

Section L: The Second Page of the HUD-1 Section L appears on and is comprised of the second page of the HUD-1. The two columns reflect the settlement charges to both the Borrower(s) and Seller(s). The

Section L: The Second Page of the HUD-1 Section L appears on and is comprised of the second page of the HUD-1. The two columns reflect the settlement charges to both the Borrower(s) and Seller(s). The

Final RESPA Rule Requirements

Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November 20, 2008. The final rule and

Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November 20, 2008. The final rule and

HUD-1. GFE vs. HUD-1: HUD-1 Introduction:

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

2012 Bulletin 4 Correcting HUD-1 to Cure Tolerance Violations February 10, 2012

2012 Bulletin 4 Correcting HUD-1 to Cure Tolerance Violations February 10, 2012 Recently, a number of questions have been raised arising out of lenders conducting internal audits and discovering tolerance

2012 Bulletin 4 Correcting HUD-1 to Cure Tolerance Violations February 10, 2012 Recently, a number of questions have been raised arising out of lenders conducting internal audits and discovering tolerance

RESPA REFORM. J. Tom Minor Karen W. Ingle

RESPA REFORM J. Tom Minor Karen W. Ingle RESPA Reform Purpose of the RESPA reform Protect consumers from unnecessarily high settlement costs Improve and standardize the Good Faith Estimate Provide an easy

RESPA REFORM J. Tom Minor Karen W. Ingle RESPA Reform Purpose of the RESPA reform Protect consumers from unnecessarily high settlement costs Improve and standardize the Good Faith Estimate Provide an easy

First Mortgage Documents User Guide 139

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge...

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

Notes on the New Settlement Sheets

Notes on the New Settlement Sheets The new GFE and HUD-1 forms are required after January 1, 2010. Settlements after January 1, 2010 with the old GFE are done on the old HUD-1. Settlements before January

Notes on the New Settlement Sheets The new GFE and HUD-1 forms are required after January 1, 2010. Settlements after January 1, 2010 with the old GFE are done on the old HUD-1. Settlements before January

HUD-1 Page 1. All of these fields should be complete.

Final HUD 1 The requirements for accurately completing the HUD-1 Settlement Statement are published based on the rules set forth by HUD, RESPA and Regulation X. The information must be both accurate and

Final HUD 1 The requirements for accurately completing the HUD-1 Settlement Statement are published based on the rules set forth by HUD, RESPA and Regulation X. The information must be both accurate and

Line 1101 is used to record the total for the category of Title services and lender s title insurance. This amount must be listed in the columns.

Lines 1100-1108. This series covers title charges and charges by attorneys and closing or settlement agents. The title charges include a variety of services performed by title companies or others, and

Lines 1100-1108. This series covers title charges and charges by attorneys and closing or settlement agents. The title charges include a variety of services performed by title companies or others, and

Appendix C: HUD-1 Settlement Statement

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

ANNOUNCEMENT #09-34, December 29, 2009

ANNOUNCEMENT #09-34, December 29, 2009 To: All Michigan Mutual Brokers Re: RESPA Changes to the Good Faith Estimate and HUD-1 Table of Contents RESPA Changes to Good Faith Estimate and HUD-1 Important

ANNOUNCEMENT #09-34, December 29, 2009 To: All Michigan Mutual Brokers Re: RESPA Changes to the Good Faith Estimate and HUD-1 Table of Contents RESPA Changes to Good Faith Estimate and HUD-1 Important

G. Property Location H. Settlement Agent: name, address. I. Settlement Date:

A. HUD-1 Settlement Statement U.S. Department Of Housing And Urban Development OMB No 2502-0265Computer form published by Law Disks, www.lawdisks.com B. Type Of Loan: 6. File Number 7. Loan Number 8. Mortgage

A. HUD-1 Settlement Statement U.S. Department Of Housing And Urban Development OMB No 2502-0265Computer form published by Law Disks, www.lawdisks.com B. Type Of Loan: 6. File Number 7. Loan Number 8. Mortgage

40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com. November 12, 2008

Jennifer L. Dozier Telephone: 770-248-2885, ext. 241 Facsimile: 770-248-2883 e-mail: jdozier@franzen-salzano.com 40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com

Jennifer L. Dozier Telephone: 770-248-2885, ext. 241 Facsimile: 770-248-2883 e-mail: jdozier@franzen-salzano.com 40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com

Guide to Completion and Review of DD Form 1705 Reimbursement for Real Estate Sale and/or Purchase Expenses

1. Assemble Your Claim Documents: Submission of one copy of each document is sufficient if the Claim is faxed to DFAS, if a hard copy is mailed, three copies of each document is required. The following

1. Assemble Your Claim Documents: Submission of one copy of each document is sufficient if the Claim is faxed to DFAS, if a hard copy is mailed, three copies of each document is required. The following

RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE

2010-2011 UPDATE COURSE SECTION THREE RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE AND HUD-1 FORMS Outline: Real Estate Settlement Procedures Act RESPA s Purpose Applicability of Law Reforms Implemented

2010-2011 UPDATE COURSE SECTION THREE RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE AND HUD-1 FORMS Outline: Real Estate Settlement Procedures Act RESPA s Purpose Applicability of Law Reforms Implemented

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 11 GFE Expiration... 12 GFE Denial... 12 GFE Written list of providers... 12

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 11 GFE Expiration... 12 GFE Denial... 12 GFE Written list of providers... 12

HUD'S RESPONSE TO HUD SETTLEMENT STATEMENT QUESTIONS RESPA AND HUD-1/1A QUESTIONS

HUD'S RESPONSE TO HUD SETTLEMENT STATEMENT QUESTIONS RESPA AND HUD-1/1A QUESTIONS Question 1: The bank offers several loan programs (rates, term etc.). A GFE is given within three days to match the product

HUD'S RESPONSE TO HUD SETTLEMENT STATEMENT QUESTIONS RESPA AND HUD-1/1A QUESTIONS Question 1: The bank offers several loan programs (rates, term etc.). A GFE is given within three days to match the product

TRID Settlement Service Provider List (SSP List)

") TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) The following FAQs were revised to provide further clarification: GFE General, #33 GFE Important dates, #5 GFE - Block 1, #7 and #8 Sections 4 and 5 Right to

New RESPA Rule FAQs (New items are in bold) The following FAQs were revised to provide further clarification: GFE General, #33 GFE Important dates, #5 GFE - Block 1, #7 and #8 Sections 4 and 5 Right to

ADVISORY MEMORANDUM KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP COMPLIANCE DOCUMENTATION REQUIREMENTS

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Upon completion you will be able to:

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

Agenda This training manual consists of three parts that will provide you with step-bystep instructions about how to complete the Closing Disclosure form required by the Integrated Disclosures Rule Upon

CFPB Consumer Laws and Regulations

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

HERE ARE FIVE THINGS YOU WILL NEED TO KNOW BEFORE THE NEW RULES TAKE EFFECT OCTOBER 3, 2015

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

Information & Instructions: HUD 1 Settlement closing statement PREVIEW

Information & Instructions: HUD 1 Settlement closing statement 1. Section 5 of the Real Estate Settlement Procedures Act of 1974 (Public Law 93-533), effective on June 30, 1976 (RESPA), requires certain

Information & Instructions: HUD 1 Settlement closing statement 1. Section 5 of the Real Estate Settlement Procedures Act of 1974 (Public Law 93-533), effective on June 30, 1976 (RESPA), requires certain

Appendix A to Part 3500 -- Instructions for Completing HUD - 1 and HUD - 1A Settlement Statements

Appendix A to Part 3500 -- Instructions for Completing HUD - 1 and HUD - 1A Settlement Statements The following are instructions for completing Sections A through L of the HUD - 1 settlement statement,

Appendix A to Part 3500 -- Instructions for Completing HUD - 1 and HUD - 1A Settlement Statements The following are instructions for completing Sections A through L of the HUD - 1 settlement statement,

Mortgage- and Lender-Related Settlement Costs. Charges for Establishing and Transferring Ownership. Amounts Paid to State and Local Governments

Mortgage- and Lender-Related Settlement Costs Charges for Establishing and Transferring Ownership Amounts Paid to State and Local Governments "All-in-One" Pricing of Settlement Costs Estimates of Settlement

Mortgage- and Lender-Related Settlement Costs Charges for Establishing and Transferring Ownership Amounts Paid to State and Local Governments "All-in-One" Pricing of Settlement Costs Estimates of Settlement

HUD-1 CHANGES. HUD-1 form. www.rgtc.com

2010 HUD-1 form Highlights New HUD-1 (HUD-1 ver. 2010) is required on all RESPA regulated transactions (residential refinances, residential purchases) beginning 1/1/2010. New HUD-1 adds a new page (page

2010 HUD-1 form Highlights New HUD-1 (HUD-1 ver. 2010) is required on all RESPA regulated transactions (residential refinances, residential purchases) beginning 1/1/2010. New HUD-1 adds a new page (page

The Good Faith Estimate

Module 3 Module 3 The Good Faith Estimate Explanation: This pdf is only a copy of the module slides. To proceed through the course, you must read and click through each slide. The Good Faith Estimates

Module 3 Module 3 The Good Faith Estimate Explanation: This pdf is only a copy of the module slides. To proceed through the course, you must read and click through each slide. The Good Faith Estimates

The Final RESPA Rule

The Final RESPA Rule GFE 2 GFE Triggers borrower s name Social Security number property address monthly income house value or best estimate amount of loan & any other information 3 GFE General provided

The Final RESPA Rule GFE 2 GFE Triggers borrower s name Social Security number property address monthly income house value or best estimate amount of loan & any other information 3 GFE General provided

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

Know Before You Owe. TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation

Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation") Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Settlement. Guide to

Settlement Guide to Mid-States Title of Southwest Virginia is a settlement agency dedicated to being a knowledgeable and practical resource for all parties involved in the real estate closing process.

Settlement Guide to Mid-States Title of Southwest Virginia is a settlement agency dedicated to being a knowledgeable and practical resource for all parties involved in the real estate closing process.

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff

United Wholesale Mortgage 2009 RESPA Webinar New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff November 18, 2009 Phillip L. Schulman, Esq. phil.schulman@klgates.com 202-778-9027 DC-1381985

United Wholesale Mortgage 2009 RESPA Webinar New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff November 18, 2009 Phillip L. Schulman, Esq. phil.schulman@klgates.com 202-778-9027 DC-1381985

TILA-RESPA Integrated Disclosure Rule * January 21, 2015

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

Good Faith Estimate (GFE)

") OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

The Closing Disclosure

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

Common Problems. By identifying these problems we hope to provide guidance to the real estate settlement agent industry and help agents avoid them.

Common Problems Over the years, the Bureau of Insurance has received and reviewed thousands of escrow account analyses and conducted thousands of investigations related to settlements involving Virginia

Common Problems Over the years, the Bureau of Insurance has received and reviewed thousands of escrow account analyses and conducted thousands of investigations related to settlements involving Virginia

General Resources CFPB Resources ALTA Best Practices Closing Insight Notaries Business & Commercial Loans Foreign Consumers

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Understanding Mortgage Lending Closing Costs. by The David Damaré Team

Understanding Mortgage Lending Closing Costs by The David Damaré Team Many lenders are still using their own version of this form. If filled out correctly it is the most accurate accounting of charges

Understanding Mortgage Lending Closing Costs by The David Damaré Team Many lenders are still using their own version of this form. If filled out correctly it is the most accurate accounting of charges

Mortgage Loan Program Loan Transmittal 1 st Mortgage

Mortgage Loan Program Loan Transmittal 1 st Mortgage INSTRUCTIONS: Deliver a copy of this form along with the following documents as specified. Finance Agency 400 Sibley Street, Suite 300 St. Paul, 55101

Mortgage Loan Program Loan Transmittal 1 st Mortgage INSTRUCTIONS: Deliver a copy of this form along with the following documents as specified. Finance Agency 400 Sibley Street, Suite 300 St. Paul, 55101

Administrative Law Division ATCC-SJA-A/4-6122 October 2014 REAL ESTATE CLAIMS DUE TO RELOCATION

1. Civilian Federal employees are entitled to relocation expenses due to certain official duty station transfers. The Fort Knox Office of the Staff Judge Advocate, Administrative Law Division, will process

1. Civilian Federal employees are entitled to relocation expenses due to certain official duty station transfers. The Fort Knox Office of the Staff Judge Advocate, Administrative Law Division, will process

TRID Frequently Asked Questions

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

INTEGRATED MORTGAGE DISCLOSURES CLOSING DISCLOSURE

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

TILA-RESPA Integrated Disclosures

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

DISCLAIMER. Page - 1 - of 17

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

DISCLAIMER The information provided in this presentation and any printed material is for informational purposes only. None of the forms, materials or opinions is offered, or should be construed, as legal

Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents

CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents") page 1 of 6 Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents The Instructions below are provided to assist CHFA s Participating

page 1 of 6 Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents The Instructions below are provided to assist CHFA s Participating

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

RESIDENCE TRANSACTION EXPENSES - HOME PURCHASE

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

UNDERSTANDING THE LOAN ESTIMATE

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

The following breaks down the Loan Estimate by section with examples from Encompass followed by official commentary. Also attached, is a copy of a completed Loan Estimate form provided by the Encompass..

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015. Presenter: Bonnie S. Nachamie

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

TILA-RESPA Integrated Disclosure Rule

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

Disclosures: Providing the consumer information concerning the condition and other aspects of the property or the loan product.

GFE INTRODUCTION: Effective January 1, 2010, HUD restructured the Good Faith Estimate ( GFE ) and HUD-1 forms to facilitate comparison shopping and improve their connection. Because of the new links between

GFE INTRODUCTION: Effective January 1, 2010, HUD restructured the Good Faith Estimate ( GFE ) and HUD-1 forms to facilitate comparison shopping and improve their connection. Because of the new links between

FAQs About RESPA for Industry

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

Real Estate Settlement Procedures Act 1

Real Estate Settlement Procedures Act 1 Examination Objectives To determine if the financial institution has established policies and procedures to ensure compliance with the Real Estate Settlement Procedures

Real Estate Settlement Procedures Act 1 Examination Objectives To determine if the financial institution has established policies and procedures to ensure compliance with the Real Estate Settlement Procedures

1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103

Item #4 / HUD page 2, line 1103") 1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103 In general, the borrower pays for the loan policy. The sales contract or agreement determines

1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103 In general, the borrower pays for the loan policy. The sales contract or agreement determines

OMB NO. 2502-0265 TYPE OF LOAN. 1. FHA () 2. FmHA () CONV.UNIS. (X) 4. VA () 5. CONV. INS. () 6. FILE NUMBER 3911011-UCE2

2. FmHA () CONV.UNIS. (X) 4. VA () 5. CONV. INS. () 6. FILE NUMBER 3911011-UCE2") OMB NO. 2502-0265 B. A. U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT TYPE OF LOAN SETTLEMENT STATEMENT 1. FHA () 2. FmHA () CONV.UNIS. (X) 3. FINAL 4. VA () 5. CONV. INS. () 6. FILE NUMBER 3911011-UCE2

OMB NO. 2502-0265 B. A. U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT TYPE OF LOAN SETTLEMENT STATEMENT 1. FHA () 2. FmHA () CONV.UNIS. (X) 3. FINAL 4. VA () 5. CONV. INS. () 6. FILE NUMBER 3911011-UCE2

The Smart Consumer s Guide to the New Good Faith Estimate

The Smart Consumer s Guide to the New Good Faith Estimate Practical insights on how to use the new GFE and HUD-1 to save money on closing costs for a purchase or refinance. Copyright 2010 ENTITLE DIRECT

The Smart Consumer s Guide to the New Good Faith Estimate Practical insights on how to use the new GFE and HUD-1 to save money on closing costs for a purchase or refinance. Copyright 2010 ENTITLE DIRECT

Chapter 47. The Closing THE REAL ESTATE SETTLEMENT PROCEDURES ACT (RESPA)

") Chapter 47 The Closing THE REAL ESTATE SETTLEMENT PROCEDURES ACT (RESPA) For federally related first mortgages to purchase one-to-four-family dwellings (i.e., almost all residential first mortgage loans

Chapter 47 The Closing THE REAL ESTATE SETTLEMENT PROCEDURES ACT (RESPA) For federally related first mortgages to purchase one-to-four-family dwellings (i.e., almost all residential first mortgage loans

a consumer guide to insurance INSURANCE ADMINISTRATION

a consumer guide to Title insurance INSURANCE ADMINISTRATION a consumer guide to title insurance Table of Contents Introduction... 1 What Is Title Insurance... 1 Who Is Protected By Title Insurance?...

a consumer guide to Title insurance INSURANCE ADMINISTRATION a consumer guide to title insurance Table of Contents Introduction... 1 What Is Title Insurance... 1 Who Is Protected By Title Insurance?...

Provident Bank Mortgage Wholesale Operations FAQ s on TRID

Provident Bank Mortgage Wholesale Operations FAQ s on TRID General 1) Q: Can an email or other communication to the borrower provide a list of standard items that will be needed for the application (income/asset

Provident Bank Mortgage Wholesale Operations FAQ s on TRID General 1) Q: Can an email or other communication to the borrower provide a list of standard items that will be needed for the application (income/asset

F. Name & Address of Lender Seller 1217 Fort Branch Blvd. Austin, TX 78721

File No 2413014409 A. Settlement Statement U.S. Department of Housing and Urban Development OMB No. 2502-0265 B. Type of Loan 1. FHA 2. 6. File Number 7. Loan Number 8. Mortgage Ins Case FmHA 3. Conv Unins

File No 2413014409 A. Settlement Statement U.S. Department of Housing and Urban Development OMB No. 2502-0265 B. Type of Loan 1. FHA 2. 6. File Number 7. Loan Number 8. Mortgage Ins Case FmHA 3. Conv Unins

Answer: ppddocs.com we don t endorse this site or this product, it is just a site we used to input examples for the webinar

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

RESPA QUESTIONS and ANSWERS

What follows are unofficial answers to the questions received by the TLTA-IBAT Panel in connection with the two February Line by Line webinars. Thanks to everyone for sending in such great questions. Hopefully

What follows are unofficial answers to the questions received by the TLTA-IBAT Panel in connection with the two February Line by Line webinars. Thanks to everyone for sending in such great questions. Hopefully

Fidelity National s Florida Underwriting Newsletter

Fidelity National s Florida Underwriting Newsletter HUD ISSUES FINAL RESPA RULE By Karla Staker Gray, State Underwriting Counsel 850 Trafalgar Court, Suite 150 Maitland, FL 32751 (407) 875-9040 (800) 669-7450

Fidelity National s Florida Underwriting Newsletter HUD ISSUES FINAL RESPA RULE By Karla Staker Gray, State Underwriting Counsel 850 Trafalgar Court, Suite 150 Maitland, FL 32751 (407) 875-9040 (800) 669-7450

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Table of Contents Introduction Purchasing Time-line II. Before You Buy

Table of Contents I. Introduction Purchasing Time-line II. Before You Buy Are You Ready to be a Homeowner? III. Determining What You Can Afford IV. Shopping for a House Role of the Real Estate Broker Selecting

Table of Contents I. Introduction Purchasing Time-line II. Before You Buy Are You Ready to be a Homeowner? III. Determining What You Can Afford IV. Shopping for a House Role of the Real Estate Broker Selecting

Table of Contents. I. Introduction. Purchasing Time-line. Before You Buy

Table of Contents I. Introduction II. III. IV. Before You Buy Purchasing Time-line Are You Ready to be a Homeowner? Determining What You Can Afford Shopping for a House Role of the Real Estate Broker Role

Table of Contents I. Introduction II. III. IV. Before You Buy Purchasing Time-line Are You Ready to be a Homeowner? Determining What You Can Afford Shopping for a House Role of the Real Estate Broker Role

Changes to Mortgage Loan Closing Process

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

.") Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate.

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Appendix B: Good Faith Estimate

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,

RESPA Reform and Effective Policy Management

RESPA Reform and Effective Policy Management Topic: This issue of Policy Matters details the best practices for covering normal and customary closing costs in light of the new Real Estate Settlement Procedures

RESPA Reform and Effective Policy Management Topic: This issue of Policy Matters details the best practices for covering normal and customary closing costs in light of the new Real Estate Settlement Procedures

7 business days after loan estimate delivery is the waiting period for consummation (loan closing) after the Loan Estimate Delivery

after the Loan Estimate Delivery") TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

You ve Applied For Your Mortgage. What Happens Next? A Simple Guide To Help You Through The Mortgage Process

You ve Applied For Your Mortgage. What Happens Next? A Simple Guide To Help You Through The Mortgage Process Four Easy Steps You have found the right home at the right price in the right location. Now

You ve Applied For Your Mortgage. What Happens Next? A Simple Guide To Help You Through The Mortgage Process Four Easy Steps You have found the right home at the right price in the right location. Now

HUD Home-Buying Guide

HUD Home-Buying Guide The following home-buying guide comes from the U.S. Department of Housing and Urban Development page 1 INTRODUCTION Congratulations! You have decided to buy a new home. This booklet

HUD Home-Buying Guide The following home-buying guide comes from the U.S. Department of Housing and Urban Development page 1 INTRODUCTION Congratulations! You have decided to buy a new home. This booklet

Income Verification Asset Verification Property Documentation

Independence Title Are you buying or selling a home after October 3, 2015? Nationwide the mortgage lending industry (creditors) will face a big change beginning October 3rd of this year. Here are the 3

Independence Title Are you buying or selling a home after October 3, 2015? Nationwide the mortgage lending industry (creditors) will face a big change beginning October 3rd of this year. Here are the 3

How To Know What Is Needed To Close A Mortgage On A Home Loan

Section A. Settlement Requirements Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on Settlement 5-A-2 Requirements

Section A. Settlement Requirements Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on Settlement 5-A-2 Requirements

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748 Comprehensive Outline Say Goodbye to the HUD1 and GFE on October 1 st, 2015 (or Hello Loan Estimate and Closing Disclosure) Opening

Presented by TREC Instructor: Laura Perry, Attorney TREC course: 7748 Comprehensive Outline Say Goodbye to the HUD1 and GFE on October 1 st, 2015 (or Hello Loan Estimate and Closing Disclosure) Opening

Introduction. The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date.

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

TRID. Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015. 2015 Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

Settlement THE. process

Settlement THE process Settlement Pros is a highly experienced settlement company exclusively dedicated to transactions in the District of Columbia, Maryland and Virginia. Our team is committed to providing

Settlement THE process Settlement Pros is a highly experienced settlement company exclusively dedicated to transactions in the District of Columbia, Maryland and Virginia. Our team is committed to providing

Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents

Table of Contents") HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance

HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

MORTGAGE LOAN DISCLOSURE STATEMENT GOOD FAITH ESTIMATE NONTRADITIONAL MORTGAGE LOAN PRODUCT (ONE TO FOUR RESIDENTIAL UNITS (RE885) INFORMATIONAL SHEET

INFORMATIONAL SHEET") MORTGAGE LOAN DISCLOSURE STATEMENT GOOD FAITH ESTIMATE NONTRADITIONAL MORTGAGE LOAN PRODUCT (ONE TO FOUR RESIDENTIAL UNITS (RE885) INFORMATIONAL SHEET WHEN TO USE THIS FORM NONTRADITIONAL LOAN PRODUCTS

MORTGAGE LOAN DISCLOSURE STATEMENT GOOD FAITH ESTIMATE NONTRADITIONAL MORTGAGE LOAN PRODUCT (ONE TO FOUR RESIDENTIAL UNITS (RE885) INFORMATIONAL SHEET WHEN TO USE THIS FORM NONTRADITIONAL LOAN PRODUCTS

Rules of Department of Insurance, Financial Institutions and Professional Registration Division 500 Property and Casualty Chapter 7 Title

Rules of Department of Insurance, Financial Institutions and Professional Registration Chapter 7 Title Title Page 20 CSR 500-7.020 Scope and Definitions...3 20 CSR 500-7.030 General Instructions...3 20

Rules of Department of Insurance, Financial Institutions and Professional Registration Chapter 7 Title Title Page 20 CSR 500-7.020 Scope and Definitions...3 20 CSR 500-7.030 General Instructions...3 20

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

FRESH. Agenda. Credit Union Integrated Mortgage Disclosures Are you Prepared?

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES...

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES... 2 SUMMARY OF YOUR LOAN... 3 ESCROW ACCOUNT INFORMATION... 4 SUMMARY

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES... 2 SUMMARY OF YOUR LOAN... 3 ESCROW ACCOUNT INFORMATION... 4 SUMMARY