Citizen Charter CONTENTS

|

|

|

- Robyn Fay Blankenship

- 10 years ago

- Views:

Transcription

1 Citizen Charter CONTENTS Sr. No. Subject Page No. 1 Common practices followed by our branches 3 2 Fair banking practices 3 3 Common areas of customer-banker relationship 4 Saving Account 4 Current Account 5 Term Deposit Account 6 Nomination 7 Remittance service 7 Collection service 8 Payment of balance in accounts of deceased customers to survivors / 8 claimants Standing instructions 8 Safe deposit lockers 8 Exchange of soiled/mutilated currency notes 9 Service charges 9 Time-norms for various banking transactions 9 Foreign exchange business 11 Wealth management Insurance products 11 Investment products 11 Advance against financial assets (AAFA) (Overdraft against securities) 11 Credit Card 12 Personal Loan 14 Mortgage Loan 14 4 Alternate delivery channels 15 Internet Banking 15 Phone Banking 15 5 Redressal of complaints 16 Regular access channels 16 Escalations of complaints 16 Further escalations of complaints 16 1 November 2014

2 PREFACE The ability of the banking industry to achieve the socio-economic objectives and in the process bringing more and more customers into its fold will ultimately depend on the satisfaction of the customers. We have a strong belief that a satisfied customer is the foremost factor in developing our business. We, at Citibank, felt that in order to become more customer friendly, the Bank should come out with a charter of its services for the customers. This document highlights Citibank's commitment towards customer satisfaction, thus ensuring accountability and responsibility amongst our officials and staff. This charter for customers not only explains our commitment and responsibilities along with the redressal methods but also specifies the obligations on the part of customers for healthy practices in customer-banker relationships. The charter has been prepared to promote fair banking practices and to give information in respect of various activities relating to customer service. We maintain constant consultations with our customers and seek their feedback to evaluate, improve and widen the range of services provided by us. All our customers are requested to keep us informed of their experiences about the various services rendered by the Bank and feel free to send us your observations. We look forward to sharing with you a mutually beneficial & long term banking relationship. NOTE Information given in this document pertains to Citibank N.A. India (herein referred to as Citibank) and is subject to change/revision. This document should not be considered as a legal document creating rights and obligations. It is for promoting better understanding between Customer and Banker. Only key information on various services/facilities has been provided in this document. Each service has its own detailed Terms and Conditions, which are displayed on our website or can be made available on request. For further details/information, please visit the Citibank website or call your Citibank Phone Banking number or visit your nearest Citibank branch. 2 November 2014

3 1. COMMON PRACTICES FOLLOWED BY OUR BRANCHES 1. Display business hours. 2. Render courteous services. 3. Attend to all customers present in the banking hall at the close of business hours. 4. Provide separate 'Enquiry' or 'May I Help You' counter at branches. 5. Offer nomination facility to all deposit accounts (i.e. account opened in individual capacity) and all safe deposit locker hirers (i.e. individual hirers). 6. Display interest rates for various deposit schemes from time to time. 7. Notify change in interest rates on advances. 8. Provide details of various deposit schemes/services of the Bank. 9. Issue Demand Drafts, Pay Orders, etc. 10. Display Time - Norms for various banking transactions. 11. Pay interest for delayed credit of local and outstation cheques, as per Citibank's policy on collection of cheques/instruments. 12. Accord immediate credit in respect of outstation and local cheques up to a specified limit subject to certain conditions, as per Citibank's policy on collection of cheques/instruments. 13. Provide complaint/suggestion box in the branch premises. 14. Display address of Regional/Zonal and Central Offices as well as Nodal Officer dealing with customer grievances /complaints. 15. Provide monthly statement of accounts/passbook facility for all Savings and Current accounts. 2. FAIR BANKING PRACTICES Customers are requested to 1. Ensure safe custody of cheque book and statement of account/pass book. 2. Preferably use reverse carbon while writing a cheque. 3. Issue crossed/account payee cheques as far as possible. 4. Check the details of the cheque, namely, date, amount in words and figures, crossing, etc. before issuing it. As far as possible, issue cheques after rounding off the amount to the nearest rupee. 5. Not to issue cheque without adequate balance. 6. Maintain minimum net relationship value (NRV) on a monthly basis, as specified by the Bank. The Net Relationship Value(NRV) is the sum total of the daily, end of day balance held across Savings/Current Account, Deposits, Investments, Insurance, Loan against securities, outstanding principal amount on Citibank Home Loan and 25% of demat holdings. 7. Send cheques and other financial instruments by Registered Post or by courier. 8. Use nomination facility. 9. Safe keep account numbers, details of Fixed Deposit, locker numbers, account statements etc. and ensure confidentiality of all Personal Identification Numbers (PINs). 10. Provide accurate information about name, address, telephone number, residential status etc., and also inform change of address, telephone number, residential status, etc., to the Bank. 11. Inform loss of demand draft, cheque leave(s) / book, key of locker, ATM/Debit Card, etc., immediately to the Branch / phone banking. 3 November 2014

4 12. Avail standing instructions facility for repeat transactions. 13. Provide feedback on our services. 14. Pay interest on overdrafts, installments, locker rent and other dues on time. 15. Avail services such as ATM, ECS, NEFT, RTGS, Internet Banking, Mobile Banking, Phone Banking, etc. 16. Not to share phone banking/internet banking passwords and ATM/Debit Card PINs with others and ensure confidentiality. 17. Bring any deficiency in services to the notice of the branch. 18. Not to sign blank cheque/s and also do not record your specimen signature either on pass book and/or on cheque book. 19. Not fall prey to fictitious offers / lottery winnings / remittance of cheap funds in foreign currency from abroad by so-called foreign entities/ individuals or to Indian residents acting as representatives of such entities/individuals. 20. Not undertake online trading in foreign exchange on portals / websites. 21. Keeping the currency notes clean by not writing/scribbling anything on them. 22. Inform the branch immediately, when a Minor turns Major or in the event of the unfortunate demise of any of the account holders. 3. COMMON AREAS OF CUSTOMER-BANKER RELATIONSHIP SAVINGS ACCOUNT 1. These accounts are designed to help the individuals to inculcate a habit of saving money and to meet their future requirement of money. The amounts can be deposited/ withdrawn from these accounts by way of cheques/atms/online transfers. 2. Savings Bank accounts are very popular and can be opened by eligible individual(s) and certain organization(s)/agencies as approved by the Reserve Bank of India (RBI). 3. While opening this account, we will satisfy ourselves about the identity, including verification of address, of a person(s) seeking to open an account, to assist in protecting the prospective customer(s), members of the public and ourselves against fraud and other misuses of the banking system. 4. The Bank requires relevant documents required for identification of the person(s) opening the account. The necessary documents required will be informed at the time of opening the account. 5. The Bank is required to obtain one recent photograph of the person(s) opening the account. 6. As per the provisions of Section 139A of the Income Tax Act, 1961, while opening an account, the Bank is required to obtain Permanent Account Number (PAN) of the person(s) opening the account. In the absence of PAN, the Bank should obtain a declaration in Form No. 60 or 61 as the case may be from the person(s) opening the account. 7. The account holder is required to maintain a certain minimum net relationship value on a monthly basis. The same is communicated in the Schedule of Charges that are included as part of terms and conditions governing operation of such accounts. Failure to maintain a minimum net relationship value in the account will attract levy of monthly fee, as specified in the Schedule of Charges from time to time. 4 November 2014

5 8. Savings Account interest will be calculated on daily balances maintained in your account. The customer will be paid interest on his Savings balance once in six months (March and September). There is no TDS for interest earned on savings account for persons resident in India. 9. Cheques and dividend warrants drawn in the name of account holder(s) will only be collected through this account. Financial Instruments endorsed in favour of the account holder(s) will not be collected through savings bank account. 10. Account holders must use these accounts for personal purposes and not for business transactions. 11. All our Savings bank accounts are provided with free cheque book facility, as specified in the Schedule of Charges. A cheque which is presented after 3 months from the date of issue will be treated as "stale or outdated and shall not be paid. 12. Bank will provide a statement of account to Savings account, on a monthly basis, without any charge. The statement of account will contain all the transactions that have been done on the account during that period. Based on customer s preference, the account statement can be sent as a physical statement or on Accounts which are not operated for over two years are marked as dormant / inoperative, to protect the interest of the depositor. The depositor can request the Bank to activate the account by submitting the documents, as required by the Bank. CURRENT ACCOUNT 1. Current Accounts can be opened by individuals, partnership firms, private and public limited companies, HUFs/specified associates, societies, trusts etc. 2. As required by law, while opening this account we will satisfy ourselves about the identity and verify the address, of a person(s) seeking to open an account, to assist in protecting the prospective customer(s), members of the public and ourselves against fraud and other misuse of the banking system. 3. Formalities/procedures relating to opening of Current Accounts for individuals are same as those mentioned for Savings Bank Accounts. For partnership firms, limited companies, HUFs, trusts, etc. the documentation formalities will be informed to you, at the time of opening the account. 4. The Bank will also require one recent photograph of all the signatories and the Permanent Account Number (PAN) of the person or entity or alternatively obtain declaration in Form No. 60 or 61 as per the Income Tax Act (vide Section 139 A) from the prospective customer. 5. Minimum net relationship value, as stipulated from time to time, will be required to be maintained on a monthly basis. 6. Failure to maintain a minimum net relationship value in the account will attract levy of service charges, as specified by the Bank from time to time. 7. No interest is paid on credit balances kept in a current account. 8. A cheque which is presented after 3 months from the date of issue will be treated as "stale or outdated" and shall not be paid. 9. As per RBI directive, the applicant for Current Account should declare in the account opening form or separately that he/they is/are not enjoying any credit facility with any Bank and if he/they does/do enjoy any credit facility, he/they should declare full particulars thereof indicating the name of the Bank/branch concerned. 5 November 2014

will not be collected through savings bank account. 10.")

6 10. For opening special types of current accounts like for Executors, Administrators, Trustees, Liquidators etc., please contact our nearest branch and the staff will help in opening these types of accounts. TERM DEPOSIT ACCOUNTS 1. Bank offers various deposit schemes to suit the needs and expectations of investing savings and current account customers in every sphere of life. 2. Bank staff shall welcome you to seek more details and shall also be glad to assist in the area of investment in various deposit schemes vis-à-vis your requirements. 3. Term Deposit Accounts can be booked for a minimum period of 7 days. The rates of interest vary depending on the period of deposit. Interest is accrued on a daily basis and paid on maturity of the deposit unless the customer opts for the monthly/quarterly interest option at the time of booking a term deposit. In the case of monthly deposit scheme, the interest shall be calculated for the quarter and paid monthly at discounted value. While a customer is booking a term deposit, an annualized yield is displayed for all tenors greater than 3 months. 4. The manner of calculation of interest is appropriately disclosed to the customer while accepting the deposits. The same is displayed at the bank branches as well. 5. At the time of booking a deposit, explicit maturity instructions are sought from the customer i.e. Credit to linked account or auto renewal on maturity. 6. Premature withdrawal of a Term deposit will result in pre-termination penalty. Pre-term penalty is communicated to all customers upfront in the form of information available at all branches, on the Bank s website and on the deposit booking form (for consumer bank customers)/ fixed deposit advice/ Standing instruction form (for corporate bank customers). 7. The current pre-term penalty is 1% on premature withdrawal of a term deposit. The same is charged on the deposit interest rate for equivalent tenor that was prevalent at the time of booking of the Term deposit or on the rate at which the deposit was booked, whichever is lower. 8. For individual customers, the bank deducts tax at source if the total interest paid/ payable on all term deposits held by a customer exceeds the amount specified in the Income Tax Act. 9. The bank issues a tax deduction certificate (TDS Certificate) for the amount of tax deducted. The customer, if entitled to exemption from TDS can submit declaration in the prescribed format i.e. Form 15G / H. 10. For deposits matured during a particular month, the TDS payment to the government happens as per Rule 30 of the Income Tax Rules, 1962 which prescribes time and mode of payment to Government account of tax deducted at source (TDS) or tax paid under sub-section (1A) of section 192. For deposits outstanding as of the end of the year, TDS on interest accrued for the financial year is paid out as per Rule 30 of the Income Tax Rules, In accordance with Income Tax guidelines, where ever PAN details are not available on our records, the Bank would be deducting TDS at 20% or the TDS rate as applicable per the Income Tax Act, 1961, whichever is higher. 12. In case of premature withdrawals, any tax already deducted on interest will not be refunded by the bank. 6 November 2014

7 NOMINATION 1. Nomination facility is available for all deposit accounts, and safe deposit vaults. 2. Nomination is available for accounts opened in individual capacity (i.e. single/joint accounts as well as accounts of a sole proprietary concern) only, i.e. not for accounts opened in representative capacity. 3. Nomination can be done in favour of one person only. However, nomination in favour of more than one person (i.e. up to 2 persons) is permissible in jointly operated locker accounts with common consent. The rights of nominee arise only after the death of all the depositor(s). 4. Nomination can be made, cancelled or varied by the account holder anytime during his/her lifetime. While making nomination, cancellation or variation, witness is required and the request should be signed by all account holders. 5. Nomination can be made in favour of a minor also and the Nomination form is to be signed by the natural guardian. During the period the minor does not attain majority, the natural guardian will receive the amount on minor s behalf. 6. Customers (new as well as existing) are advised to avail nomination facility, if they have not availed so far. For the existing accounts where nomination is not made, the account holder(s) can do so by filling up the nomination form available with the branches. 7. In case the depositor(s) does not wish to make nomination, the same should be recorded on the account opening form by the depositor(s) with their full signature. REMITTANCE SERVICE 1. Customers may remit funds from one centre to another centre by Demand Draft (DD) or Electronic Funds Transfer (operated through RBI) within applicable limits, based on availability at various locations and by paying specified charges as per the Bank's rules. 2. Demand drafts / Pay Orders for Rs. 50,000 and above will be issued by the banks only by debit to the customer s account or against cheque or other instruments tendered by the purchaser and not against cash payment. 3. Drafts are issued on our branches. They are issued on our Correspondent Bank s branches at centres where we do not have any branch. 4. Banker s cheques and drafts are valid for 3 months from date of issue and can be revalidated by issuing branches on written request of the purchasers. The drafts can be revalidated by the payee(s) if they are identified as the holder in due course. The drafts can be revalidated only once within one year from the date of issue. After one year of the draft, they are to be cancelled at the issuing branch, and a fresh draft obtained after paying the requisite service charges. 5. As directed by the RBI, the bank may issue duplicate demand draft up to Rs. 5,000/- on the basis of adequate indemnity and without obtaining Non-payment advice from the drawee branch. 6. As directed by the RBI, the banks will issue duplicate demand draft to the customer within a fortnight from the receipt of request with necessary indemnities, as applicable. For delay in issuing duplicate draft beyond the above stipulated period, the bank will pay interest at the rate applicable for fixed deposit of corresponding maturity in order to compensate the customer for such delay. 7 November 2014

8 COLLECTION SERVICE Citibank has a Cheque collection policy in line with the directions provided by Reserve Bank of India that provides details as regards the collection services offered by the bank. The Cheque collection policy is available at the Bank's website URL: Amongst other points the policy defines the turnaround time and compensation that will be provided in the event there is a delay in realization of the cheque deposited by an account holder. Customers are requested to deposit their cheque within the stipulated cut-off at the branches to ensure timely clearing. PAYMENT OF BALANCE IN ACCOUNTS OF DECEASED CUSTOMERS TO SURVIVORS / CLAIMANTS As directed by the RBI, the bank has adopted procedures to ensure that settlement of claims in respect of deceased depositors is as simplified as possible. The Deceased Depositors Policy is available at the Bank's website URL: STANDING INSTRUCTIONS Standing instructions can be given to the Bank for transfer/remittance of funds from one account to other account(s) maintained in the same branch, any other branch of the Bank or any other Bank or any other third party. This services / transfers can also be availed through our Online Internet Banking services. For details, please check our online banking site and register for transactions. SAFE DEPOSIT LOCKERS The facility of Safe Deposit Lockers is an additional service offered by the Bank at select branches. The Bank's branches offering this facility will indicate/display this information.. The major aspects governing the services are: Nomination facility is available to individual hirer of Safe Deposit Locker. Loss of key should be immediately informed to the Branch. Lockers are available in different sizes. Lockers are rented out for a minimum period of one year. Rent is payable in advance. In case of overdue rent, the Bank will charge penalty as decided from time to time. With Standing Instruction, the rent may be paid from the deposit account of the hirer. The Bank will allow hiring of locker only if the required documents for identification and other required documents are provided by the hirer(s). Terms and conditions and annual hire charges can be obtained from the branches. The Bank reserves the right to break open the locker if the rent is not paid or in case the locker remains inoperative beyond a stipulated period of time in spite of giving notices as per the Bank rules and recover charges thereof. 8 November 2014

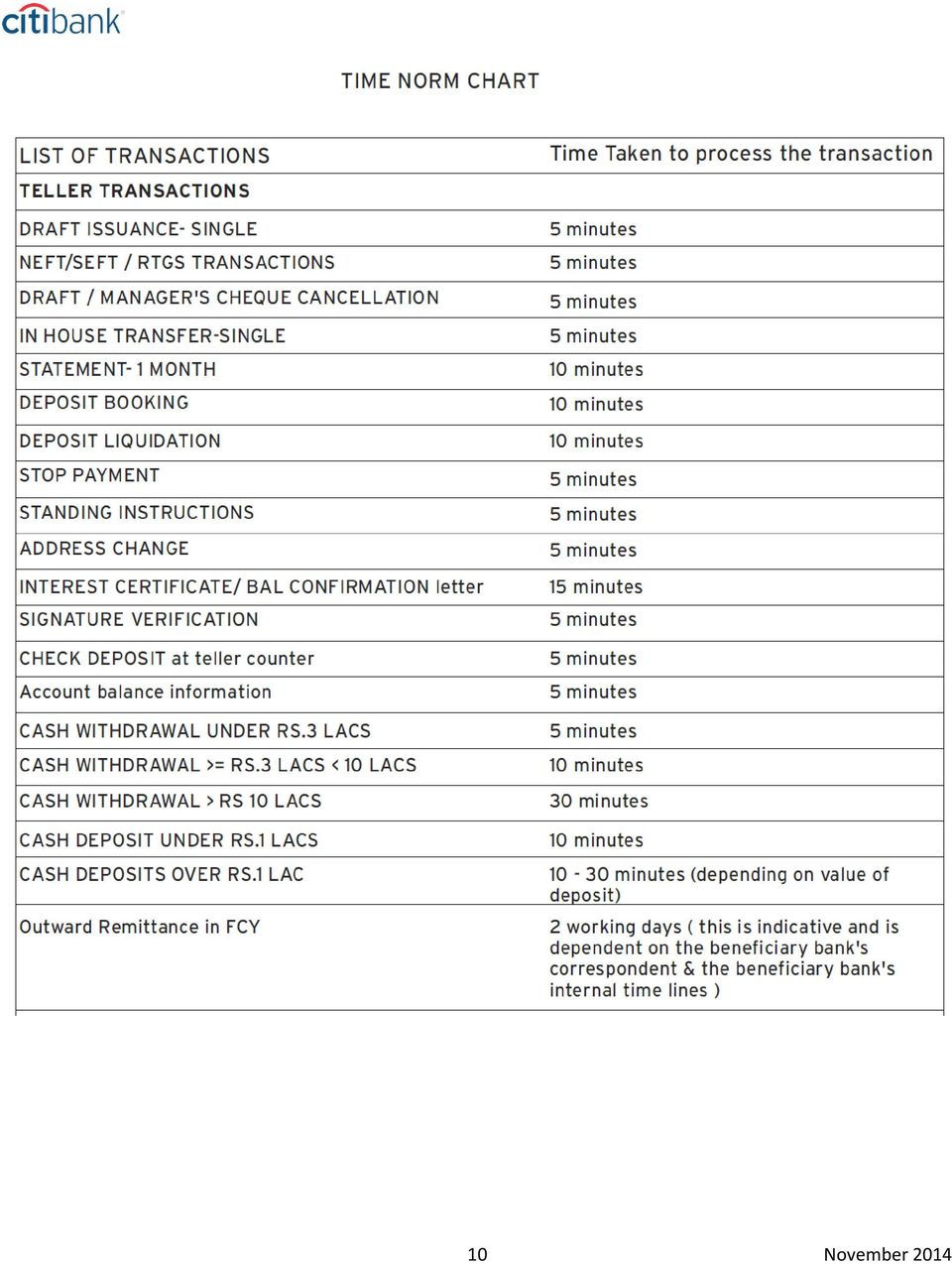

9 EXCHANGE OF SOILED/MUTILATED CURRENCY NOTES All the branches of the Bank will exchange freely, soiled/ mutilated currency notes of all denominations. Currency exchange facility is offered to the Bank's customers and others. The Bank follows RBI guidelines in this respect. SERVICE CHARGES The Bank provides various services to customers for which service charges are levied. Charges are reviewed/revised from time to time. Service charges are levied for collection and remittance of funds, processing of loan proposals, issue of guarantees, issue of duplicate instruments/statements, etc. Charges are communicated to all customers at the time of starting a new banking relationship. Details of service charges are also available on the bank s website and displayed at branches. A copy of the Schedule of charges will also be provided to customers on request. TIME-NORMS FOR VARIOUS BANKING TRANSACTIONS 9 November 2014

10 10 November 2014

11 FOREIGN EXCHANGE BUSINESS The Bank offers a wide range of Foreign Exchange Products and Services to all customers, through its branches. All Foreign Exchange transactions are conducted subject to Rules and Regulations under the Foreign Exchange Management Act, 1999 (FEMA). Details of the exchange rates and charges which will apply to various foreign exchange transactions are available at branches. Cross border payments will be made subject to the provisions of the applicable FEMA Regulations from time to time. WEALTH MANAGEMENT INSURANCE PRODUCTS Citibank is a licensed corporate agent for Life Insurance, General Insurance and Health insurance products. Prior to selecting the insurance companies whose products are proposed to be distributed by the bank to its customers, a detailed due diligence of the insurance company is undertaken by the bank. Citibank does not manufacture any of these products but acts purely as a distributor of the products offered by the insurance company. The offers represented by the insurer may be withdrawn/modified at their sole discretion. INVESTMENT PRODUCTS Citibank India distributes an array of Investment products offered by a range of third party mutual fund product providers. Prior to selecting the Asset Management Company (AMC) whose products are proposed to be distributed by the bank to its customers, a detailed due diligence of the AMC is undertaken by the bank. Citibank does not manufacture any of these products but as mentioned above acts purely as a distributor of the products offered by the AMC. The offers represented by the AMC may be withdrawn/modified at their sole discretion. Citibank adopts a comprehensive methodology of risk profiling of the customer based on their current financial position, their goals and their earning potential. ADVANCE AGAINST FINANCIAL ASSETS (AAFA) (OVERDRAFT AGAINST SECURITIES) 1. This overdraft facility is designed to help individuals avail liquidity against specific securities (equity shares and mutual funds) approved and acceptable to the Bank, without the need to sell or redeem the same. The amount can be withdrawn from the account by way of cheques/atm Card, up to the overdraft limit sanctioned and unutilized in the account. 2. These accounts can be opened only by entities permitted as per the guidelines and internal credit parameters from time to time. Currently, the permitted entities are Individuals and SEBI registered stock brokers. 3. It is the Bank's discretion, based on internal policies, to: 11 November 2014

12 - Grant an overdraft facility to any individual / individual(s) / stock broker - Decide the list of approved securities against which the overdraft limit will be granted - Determine the value of the securities so pledged by the Borrower(s) / Guarantor(s) and - against which the overdraft limit has been granted - Decide the frequency at which the various securities will be valued 4. The overdraft facility will be provided by the Bank only on receipt of confirmation that the lien/pledge have been created, on the securities, in favour of the Bank. 5. Customers to ensure that the overdraft facility provided is used for legitimate business purposes only and not for speculative activities. Similarly, stock brokers can use funds from such overdraft limit only for the purpose of working capital. 6. The Bank will value the pledged securities at regular intervals. The Borrower(s) are required to maintain a minimum margin (as stipulated in the guidelines and/or credit parameters) at all times. If the value of pledged securities falls, the Borrower(s) are required to repay a part of the overdraft limit utilized and/or pledge additional approved securities so as to retain the minimum margin required. The Bank may levy penal interest if the margin amount maintained in the account is less than the prescribed limit. 7. Interest is levied by the Bank at the agreed rate of interest on the amount of the overdraft limit utilized on a monthly basis. The interest amount will be debited to the AAFA account. The Borrower(s) are required to service i.e. pay the interest amount so levied within 15 days of the same being debited. Please visit our website ( to refer to the detailed Terms and conditions for the product. CREDIT CARDS Credit Card is a plastic currency bearing a distinctive identification number with a credit limit that can be used for purchasing goods and services and to obtain cash disbursements on credit. The card member is subsequently billed by the Bank for repayment of the credit extended either in full by the end of a specified period or can be settled in part, with the balance taken as extended credit as per the card issue terms. Interest is charged based on the terms of the card member Terms and Conditions and the Card member may at times be required to pay an annual fee, which will clearly be communicated at the time of the card application. Applicants can choose from a wide variety of Citibank Credit Cards, including but not limited to, Citi-branded cards and co-branded cards in segments like Fuel/ Auto, Shopping & Entertainment, and Special Interest (Affinity cards). Each card comes along with its unique features and rewarding benefits, which are communicated at the time of application, subsequently sent with the Card Plastic in the Welcome Kit. The latest updates are available on the Bank s website. The Bank aims at enhancing the customer experience with best offers and discount deals from time to time. 12 November 2014

13 When a customer applies for a Credit Card the Bank will satisfy itself about the identity and verify address, of a person/s applying for the Credit Card, to assist in protecting the prospective customer/s, members of the public and itself against fraud and other misuses of the banking system The Bank is required to collect one recent passport size photograph and verify the Permanent Account Number (PAN) or alternatively obtain declaration in Form No. 60 or 61 as per the Income Tax Act (vide Section 139A) from the person/s applying for the Credit Card. The Bank will provide to prospective customers details of the documents required for identification of the person/s applying for the Credit Card. The original of all documents will need to be sighted. Documents normally accepted are Valid Passport / Driver's License/Voter s ID Card /Aadhaar Card, Utility Bill not more than 3 months old with name and address (Landline Telephone Bill, Mobile Bill, Electricity Bill, Water or Gas Bill), Bank account statement printed on bank's letterhead, not more than 3 months old, etc. The Bank shall provide the 'Most Important Terms and Conditions' (MITCs) to the prospective customer/customers at all the stages (i.e. during marketing, at the time of application, at the acceptance stage (welcome kit), along with the monthly statement and available on the bank's website). The Bank displays the Schedule of Charges on its website and shall also provide the same to prospective customer/ customers along with the MITC. Method of calculation of annualized percentage rates (APR) and Late Fee on card are explained with examples for better comprehension. The Bank will send the Card member a monthly statement, showing payments and transactions for the month, provided the Card has been active during the said period. Customers should ensure that at least the Minimum Amount Due is paid by the Payment Due Date to keep the card account current and to avoid levy of late charges. If a part payment is made, there would be no interest free period and interest charges would be applicable (including on fresh purchases, if any) via an average daily balance method Payments received against the Card outstanding will be adjusted against all taxes, fees and other charges, interest charges, cash advances and purchases in that order. Customers should contact the Bank immediately at 24-Hour CitiPhone, if a Card is lost, stolen, misplaced, or if someone else knows the PIN or other security information. CitiPhone helpline at the numbers given below: The Bank may tie up with credit bureaus authorised by the RBI and will share credit information including but not limited to current balance, payment history etc., along with demographic details with these credit bureaus, as per the Credit Information Companies (Regulation) Act, November 2014

14 In case of charge disputes, the bank should be informed within 30 days of receipt of the Statement. On receipt of such information, the Bank may reverse the charge on a temporary basis. If, on completion of subsequent investigations, the liability of such charges is ascertained to be to the Account, the charge will be reinstated in a subsequent statement and a fee of Rs. 100 will be charged. The complainant would have a time frame of 60 days for informing the Bank of any other complaints/grievances. If the Card member notifies the Bank of a billing dispute, the Bank will suspend reporting to the bureau till the dispute is resolved. For the comprehensive Terms and Conditions, relevant Credit Card guidelines & local regulations, please visit the Bank's website PERSONAL LOANS Personal Loans is a single applicant product designed to help the salaried individuals to borrow at a competitive interest rate, without a collateral or guarantor. The loan can be availed depending on the requirement and repayment capacity, for personal use. While extending a loan, the bank will satisfy itself about the identity, including verification of address, of an individual seeking to avail a personal loan, as required by law. This is to assist in protecting the prospective customer(s), members of the public and ourselves against fraud and other misuses of the banking system. The Bank requires valid references and relevant documents for identification of the individual applying for the loan. The basic necessary documents are listed in the tear away portion of the application form. The Bank will also require one recent passport size photograph and the Permanent Account Number (PAN) or alternatively obtain declaration in Form No. 60 or 61 as per the Income Tax Act (vide Section 139 A) from the individual applying for the loan. The customer is required to make Equated Monthly Installment (EMI) payments as agreed upon, at the time of applying for the loan. Any default on repayment would attract penal charges as specified in the loan agreement. Interest on these loan accounts is levied monthly at the rate stated in the loan agreement. Customers must use the funds from this personal loan as indicated by them in the end use section of the application form. These funds should not be used for any prohibited purposes as defined from time to time under the regulations. For more details, please refer to the detailed loan agreement and the loan application form or call our Customer Care Unit. MORTGAGE LOANS Citibank through its Mortgage Business extends Housing Loans, Loans against property to the Salaried and Self-employed Customers. Housing Loans are available for purchase of ready/under-construction properties from host of developers or for self-construction. Loans against Properties are extended to customers to utilise 14 November 2014

15 the funds for Business/closing other high cost debts or for Personal Use. Loans are extended to Borrowers at competitive interest rates, basis various credit parameters including assessment of their repayment capacity. Citibank provides Unique Home Credit proposition to save on Interest Costs with the ability to draw down the saves as line of credit or to reduce the principal on permanent basis allowing you to close your loan faster, Best in class service platform with Dedicated CitiPhone banking service platform to service the Home Loan customers. NRI Home Loan Program helps NRIs across the globe to buy the property of their choice in India. Necessary documents are taken from borrowers to ensure that stipulated KYC norms are met with. Disclosures related to documentation requirement, Schedule of Charges etc. are available in our application form. For more details, please refer to for the detailed loan agreement and the loan application form or call our Customer Care Unit. Internet Banking 4. ALTERNATE DELIVERY CHANNELS The Bank offers Internet Banking facility to its customers. This facility is compliant with all the norms and Regulations laid down by the regulator from time to time. Using this facility, customers can enquire on their accounts as well as conduct financial transactions such as funds transfers using NEFT, RTGS and make payment to Credit Card, etc. One can avail of other value added features such as accessing e-statements, making bill payment, communicating with the Bank in a secure mode through a secure mail etc. Phone Banking The Bank offers Phone Banking facility to all customers. Some of the common practices followed by this channel are: 1. Render service 24 hours a day, 7 days a week* 2. Render emergency services (Reporting Lost Card and Stop cheques) 3. Provide details of various financial products and services of the Bank and transact on accounts. 4. Respond to customer queries related to customer account(s) with us, subject to verification of customer identity. 5. Provide a facility for logging complaint/suggestion. 15 November 2014

16 5. REDRESSAL OF COMPLAINTS Citibank is committed to provide products and services of the highest standards. It is our endeavor to provide the best possible assistance to address any concerns that you may have. Kindly find our grievance redressal process below: A. Regular Access Channels You may call our 24X7 CitiPhone helpline at the numbers given below: For other cities, please refer to the Customer Service webpage of If you are a Citibank customer you can also login to using your IPIN (internet password), select your banking relationship and click on Your Queries link to compose your query. A customer complaint register is also available at all Citibank branches to record your concerns. At each of these channels, a complaint reference number will be provided to you. We request you to quote this reference number in all your communications on the same issue. We endeavor to resolve your concern within 5 working days from receipt of the same. B. Escalation of Complaints If you are not satisfied with the response received from the above mentioned access channels, you may: Call our customer care experts at between 10:00 AM and 6:00 PM (Monday to Saturday) except on national holidays (OR) Send an to [email protected] C. For further escalations: Contact our Principal Nodal Officer Ms.Nisha Shriram at [email protected] Call our Grievance Redressal Desk at (local dialing) between 10:00 AM and 6:00 PM (Monday to Saturday) except on national holidays Write to our Principal Nodal Officer at No.2, Club House Road, Chennai November 2014

17 For ease of reference, we request you to mention the complaint reference number and your first contact point in the bank for the concern raised. For contact details of our Nodal Officers and Senior Management Team, please refer to the Customer Service webpage of In the event that you do not receive any response from us within one month from the date you represented your complaint or if you are dissatisfied with the response, you may write to the Banking Ombudsman for an independent review. The details of the Banking Ombudsman scheme are also available on the Customer Service webpage of Citibank is a member of the Banking Codes and Standards Board of India (BCSBI). Please visit our website to view the BCSBI code. Note: Kindly write to us from your registered address. In order to safeguard your interest, we request you not to provide any personal identification details in your communication to the bank. 17 November 2014

Sumitomo Mitsui Banking Corporation Citizen charter. Version: 02

Sumitomo Mitsui Banking Corporation Citizen charter Version: 02 Table of Contents Table of Contents 1. Introduction...1 2. Common practice followed by us...2 3. Fair banking practices...3 4. Common areas

Sumitomo Mitsui Banking Corporation Citizen charter Version: 02 Table of Contents Table of Contents 1. Introduction...1 2. Common practice followed by us...2 3. Fair banking practices...3 4. Common areas

MOST IMPORTANT TERMS AND CONDITIONS

MOST IMPORTANT TERMS AND CONDITIONS The Most Important Terms & Conditions (MITCs) mentioned herein below are to be read and understood in conjunction with the Citibank Cardmember Terms and Conditions (

MOST IMPORTANT TERMS AND CONDITIONS The Most Important Terms & Conditions (MITCs) mentioned herein below are to be read and understood in conjunction with the Citibank Cardmember Terms and Conditions (

ANNEXURE POLICY ON BANK DEPOSITS

ANNEXURE POLICY ON BANK DEPOSITS 1. TYPES OF DEPOSIT ACCOUNTS: While various deposit products offered by the Bank are assigned different names, the deposit products can be categorized broadly into the

ANNEXURE POLICY ON BANK DEPOSITS 1. TYPES OF DEPOSIT ACCOUNTS: While various deposit products offered by the Bank are assigned different names, the deposit products can be categorized broadly into the

STATE BANK OF MYSORE P&SB DEPT::HEAD OFFICE COMMON AREAS OF CUSTOMER BANKER RELATIONSHIP. KNOW YOUR CUSTOMER (KYC NORMS) - General guidelines

- General guidelines") COMMON AREAS OF CUSTOMER BANKER RELATIONSHIP KNOW YOUR CUSTOMER (KYC NORMS) - General guidelines In order to protect the prospective customer/s, members of the public and ourselves against fraud and other

COMMON AREAS OF CUSTOMER BANKER RELATIONSHIP KNOW YOUR CUSTOMER (KYC NORMS) - General guidelines In order to protect the prospective customer/s, members of the public and ourselves against fraud and other

Sumitomo Mitsui Banking Corporation Deposit Policy. Version: 04

Sumitomo Mitsui Banking Corporation Deposit Policy Version: 04 Table of Contents Table of Contents 1. Introduction... 1 2. Types of Deposit Accounts... 2 3. Deposits... 3 4. Account opening and operation

Sumitomo Mitsui Banking Corporation Deposit Policy Version: 04 Table of Contents Table of Contents 1. Introduction... 1 2. Types of Deposit Accounts... 2 3. Deposits... 3 4. Account opening and operation

Deposit Policy. The deposit products can be categorised broadly into the following types. Definitions of major deposits schemes are as under: -

1 Deposit Policy Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking System.

1 Deposit Policy Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking System.

POLICY ON BANK DEPOSITS

POLICY ON BANK DEPOSITS 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

POLICY ON BANK DEPOSITS 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

Mizuho Bank, Ltd. India. Deposit Policy. Revised on May 27, 2015

Mizuho Bank, Ltd. India Deposit Policy Revised on May 27, 2015 DISCLAIMER This Policy has been prepared on the basis of existing regulatory/statutory guidelines, existing risk management policies in the

Mizuho Bank, Ltd. India Deposit Policy Revised on May 27, 2015 DISCLAIMER This Policy has been prepared on the basis of existing regulatory/statutory guidelines, existing risk management policies in the

RBS RETAIL BANK DEPOSIT POLICY

RBS RETAIL BANK DEPOSIT POLICY PREFACE This policy document on deposits outlines the guiding principles in respect of formulation of various deposit products offered by the Bank and terms and conditions

RBS RETAIL BANK DEPOSIT POLICY PREFACE This policy document on deposits outlines the guiding principles in respect of formulation of various deposit products offered by the Bank and terms and conditions

IDBI BANK DEPOSIT POLICY

IDBI BANK DEPOSIT POLICY Page 1. Preamble 1 2. Types of Deposit Account 2 3. Account Opening and Operations of Deposit Accounts 3 3.1 Account Opening 3 3.2 Operations of Deposit Accounts 5 3.3 Mandate

IDBI BANK DEPOSIT POLICY Page 1. Preamble 1 2. Types of Deposit Account 2 3. Account Opening and Operations of Deposit Accounts 3 3.1 Account Opening 3 3.2 Operations of Deposit Accounts 5 3.3 Mandate

POLICY ON BANK DEPOSITS (2014)

") 1 POLICY ON BANK DEPOSITS (2014) PREAMBLE One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of

1 POLICY ON BANK DEPOSITS (2014) PREAMBLE One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of

i) Demand deposits means a deposit received by the BANK which is withdrawable on demand;

Demand deposits means a deposit received by the BANK which is withdrawable on demand;") Policy on Bank Deposits 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

Policy on Bank Deposits 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

DEPOSIT POLICY. Contents

DEPOSIT POLICY Contents 1. Account Opening... 3 1.1 Types of Deposit Accounts... 3 1.2 Operation of Deposit Accounts... 4 2 - Term Deposits for Persons Residents in India... 7 2.1 Term Deposit Products

DEPOSIT POLICY Contents 1. Account Opening... 3 1.1 Types of Deposit Accounts... 3 1.2 Operation of Deposit Accounts... 4 2 - Term Deposits for Persons Residents in India... 7 2.1 Term Deposit Products

RBL Bank Limited. (Formerly: The Ratnakar Bank Limited) Deposit Policy

Deposit Policy") RBL Bank Limited (Formerly: The Ratnakar Bank Limited) Deposit Policy 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors

RBL Bank Limited (Formerly: The Ratnakar Bank Limited) Deposit Policy 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors

Policy on Bank Deposits

Policy on Bank Deposits 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

Policy on Bank Deposits 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

CITIZEN S CHARTER. A Charter for Customer Services

CITIZEN S CHARTER A Charter for Customer Services SEPTEMBER 2014 1 PREFACE The ability of the banking industry to achieve its socio-economic objectives and in the process bring in more customers into its

CITIZEN S CHARTER A Charter for Customer Services SEPTEMBER 2014 1 PREFACE The ability of the banking industry to achieve its socio-economic objectives and in the process bring in more customers into its

POLICY ON BANK DEPOSITS

POLICY ON BANK DEPOSITS PREAMBLE One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

POLICY ON BANK DEPOSITS PREAMBLE One of the important functions of the Bank is to accept deposits from the public for the purpose of lending. In fact, depositors are the major stakeholders of the Banking

POLICY BANK DEPOSITS. Operations & Services Dept. Head Office,Baroda Date: 01.03.2012

POLICY ON BANK DEPOSITS Approved by Board vide agenda item O-2 in its meeting dated 19.03.2012 Operations & Services Dept. Head Office,Baroda Date: 01.03.2012 POLICY ON BANK DEPOSITS 1. PREAMBLE One of

POLICY ON BANK DEPOSITS Approved by Board vide agenda item O-2 in its meeting dated 19.03.2012 Operations & Services Dept. Head Office,Baroda Date: 01.03.2012 POLICY ON BANK DEPOSITS 1. PREAMBLE One of

UNITED BANK OF INDIA

UNITED BANK OF INDIA COMPENSATION POLICY FOR THE YEAR 2014-2015. 1. INTRODUCTION 1.1 Technological progress in payment and settlement systems and the qualitative changes in operational systems and processes

UNITED BANK OF INDIA COMPENSATION POLICY FOR THE YEAR 2014-2015. 1. INTRODUCTION 1.1 Technological progress in payment and settlement systems and the qualitative changes in operational systems and processes

Standard Chartered Bank Outline on settlement of deceased accounts

Standard Chartered Bank Outline on settlement of deceased accounts This policy document on deposits outlines the process followed on deceased deposit accounts. It is expected that this document will impart

Standard Chartered Bank Outline on settlement of deceased accounts This policy document on deposits outlines the process followed on deceased deposit accounts. It is expected that this document will impart

Vishwa Yatra Foreign Travel Card (VYFTC)

") Vishwa Yatra Foreign Travel Card (VYFTC) Eligibility Features The card can be issued to: any bonafide citizen of India who plans to travel abroad except Nepal and Bhutan. Corporates for their employees

Vishwa Yatra Foreign Travel Card (VYFTC) Eligibility Features The card can be issued to: any bonafide citizen of India who plans to travel abroad except Nepal and Bhutan. Corporates for their employees

STATE BANK OF INDIA REG DD TRUTH CHICAGO IN SAVINGS BRANCH DISCLOSURE SAVINGS ACCOUNT

STATE BANK OF INDIA REG DD TRUTH CHICAGO IN SAVINGS BRANCH DISCLOSURE SAVINGS ACCOUNT Interest Rate Information: See Interest rate sheet provided as part of this disclosure. The interest rate and annual

STATE BANK OF INDIA REG DD TRUTH CHICAGO IN SAVINGS BRANCH DISCLOSURE SAVINGS ACCOUNT Interest Rate Information: See Interest rate sheet provided as part of this disclosure. The interest rate and annual

Customer Compensation Policy

Customer Compensation Policy Introduction The Compensation Policy (the Policy) of the Bank is a reflection of the Bank s on-going efforts to provide better service to our customers and set higher standards

Customer Compensation Policy Introduction The Compensation Policy (the Policy) of the Bank is a reflection of the Bank s on-going efforts to provide better service to our customers and set higher standards

I NDUSIND B ANK C REDIT C ARD M OST I MPORTANT T ERMS & C ONDITIONS

I NDUSIND B ANK C REDIT C ARD M OST I MPORTANT T ERMS & C ONDITIONS Back Cover MOST IMPORTANT TERMS & CONDITIONS INDUSIND BANK CREDIT CARDS The Most Important Terms and Conditions (MITC) and all information

I NDUSIND B ANK C REDIT C ARD M OST I MPORTANT T ERMS & C ONDITIONS Back Cover MOST IMPORTANT TERMS & CONDITIONS INDUSIND BANK CREDIT CARDS The Most Important Terms and Conditions (MITC) and all information

POLICY INOPERATIVE AND UNCLAIMED ACCOUNTS

POLICY ON INOPERATIVE AND UNCLAIMED ACCOUNTS Strategy & Business Development Division Table of contents. 1. Introduction 2. Purpose of Classification 3. Definition of Inoperative Accounts 4. Definition

POLICY ON INOPERATIVE AND UNCLAIMED ACCOUNTS Strategy & Business Development Division Table of contents. 1. Introduction 2. Purpose of Classification 3. Definition of Inoperative Accounts 4. Definition

Transactional and Savings Accounts. Combined Product Disclosure Statement and Financial Services Guide

Transactional and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide BOQ Specialist Transaction and Savings Accounts (with Overdraft) Combined Product Disclosure Statement

Transactional and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide BOQ Specialist Transaction and Savings Accounts (with Overdraft) Combined Product Disclosure Statement

SERVICE CHARGES FOR NRI ACCOUNTS

SERVICE CHARGES FOR NRI ACCOUNTS Please Note: These charges are subject to change, without prior notice. Service tax @ 14% will be levied over and above the charge specified. General charges Pass book

SERVICE CHARGES FOR NRI ACCOUNTS Please Note: These charges are subject to change, without prior notice. Service tax @ 14% will be levied over and above the charge specified. General charges Pass book

COUNTRY SCHEDULE NEW ZEALAND

This document constitutes a Country Schedule as referred to in the Conditions and sets out country specific terms on which the Bank provides the Customer with one or more Accounts or Services in New Zealand

This document constitutes a Country Schedule as referred to in the Conditions and sets out country specific terms on which the Bank provides the Customer with one or more Accounts or Services in New Zealand

Service Charges (applicable wef April 1 2015) 1 Minimum monthlyaverage balance requirement and monthly maintenance charges in SB accounts

1 Minimum monthlyaverage balance requirement and monthly maintenance charges in SB accounts") Service Charges (applicable wef April 1 2015) 1 Minimum monthlyaverage balance requirement and monthly maintenance charges in SB accounts 1.1 Where a debit card has been issued (other than CUB-card) to

Service Charges (applicable wef April 1 2015) 1 Minimum monthlyaverage balance requirement and monthly maintenance charges in SB accounts 1.1 Where a debit card has been issued (other than CUB-card) to

Introduction 1. Erroneous debits arising on transactions specified herein below:

Compensation Policy Introduction We (the Bank ) offer high levels of service to our customers. In the event, for some reason beyond our control or inadvertently, we are unable to meet the service levels

Compensation Policy Introduction We (the Bank ) offer high levels of service to our customers. In the event, for some reason beyond our control or inadvertently, we are unable to meet the service levels

Account Type Current Saving Fixed Others (Specify) Constitution: Private Ltd. Co. Public Ltd. Co. NGO Others(Specify)

Constitution: Private Ltd. Co. Public Ltd. Co. NGO Others(Specify)") NEPAL SBI BANK LIMITED...Branch ACCOUNT NUMBER Account Type Current Saving Fixed Others (Specify) Constitution: Private Ltd. Co. Public Ltd. Co. NGO Others(Specify) Currency NPR USD EURO Others ((Specify)

NEPAL SBI BANK LIMITED...Branch ACCOUNT NUMBER Account Type Current Saving Fixed Others (Specify) Constitution: Private Ltd. Co. Public Ltd. Co. NGO Others(Specify) Currency NPR USD EURO Others ((Specify)

Terms & Conditions governing Savings Accounts. To be read in conjunction with Axis Bank Sri Lanka General Terms and Conditions

Terms & Conditions governing Savings Accounts To be read in conjunction with Axis Bank Sri Lanka General Terms and Conditions Contents 1. Scope of this document...1 2. Product details and features...1

Terms & Conditions governing Savings Accounts To be read in conjunction with Axis Bank Sri Lanka General Terms and Conditions Contents 1. Scope of this document...1 2. Product details and features...1

Old Dominion National Bank Consumer ebanking Access Agreement and Electronic Fund Transfer Act Disclosure

Old Dominion National Bank Consumer ebanking Access Agreement and Electronic Fund Transfer Act Disclosure Agreement This Agreement is a contract which establishes the rules governing your electronic access

Old Dominion National Bank Consumer ebanking Access Agreement and Electronic Fund Transfer Act Disclosure Agreement This Agreement is a contract which establishes the rules governing your electronic access

Current/Cheque/Savings Account and Fixed Deposit Terms www.sc.com/gh

Current/Cheque/Savings Account and Fixed Deposit Terms www.sc.com/gh Copyright 2015 Standard Chartered Bank Version 01/2015 Contents 1 Choosing the account that is right for you 1 2 Savings accounts 1

Current/Cheque/Savings Account and Fixed Deposit Terms www.sc.com/gh Copyright 2015 Standard Chartered Bank Version 01/2015 Contents 1 Choosing the account that is right for you 1 2 Savings accounts 1

POLICY ON COLLECTION OF CHEQUES/INSTRUMENTS AND DISHONOUR OF INSTRUMENTS

1. Introduction POLICY ON COLLECTION OF CHEQUES/INSTRUMENTS AND DISHONOUR OF INSTRUMENTS Keeping in view the technological progress in payment and settlement systems and the qualitative changes in operational

1. Introduction POLICY ON COLLECTION OF CHEQUES/INSTRUMENTS AND DISHONOUR OF INSTRUMENTS Keeping in view the technological progress in payment and settlement systems and the qualitative changes in operational

STATE BANK OF PATIALA POLICY ON BANK'S DEPOSITS

STATE BANK OF PATIALA POLICY ON BANK'S DEPOSITS 1 INDEX S.No. Particulars PN 1 Preamble 3 2 Types of Deposit Accounts 3 2(a) Withdrawals 4 2(b) Deposits 4 3. Account Opening and Operation of Deposit accounts

STATE BANK OF PATIALA POLICY ON BANK'S DEPOSITS 1 INDEX S.No. Particulars PN 1 Preamble 3 2 Types of Deposit Accounts 3 2(a) Withdrawals 4 2(b) Deposits 4 3. Account Opening and Operation of Deposit accounts

CorpBank International Credit Card

CorpBank International Credit Card CORPBANK INTERNATIONAL CREDIT CARD MOST IMPORTANT TERMS AND CONDITIONS [MITC] Item INDEX Page No. Definition 1 Fees and Charges 1 Limits 2 Finance Charges 2 Billing and

CorpBank International Credit Card CORPBANK INTERNATIONAL CREDIT CARD MOST IMPORTANT TERMS AND CONDITIONS [MITC] Item INDEX Page No. Definition 1 Fees and Charges 1 Limits 2 Finance Charges 2 Billing and

Bank of Scotland Private Banking Savings Accounts

Bank of Scotland Private Banking Savings Accounts Terms and Conditions Applicable to: Premier Investment Account Premier Reserve Account (for Personal Customers) Premier Reserve Account (for Trusts) 3

Bank of Scotland Private Banking Savings Accounts Terms and Conditions Applicable to: Premier Investment Account Premier Reserve Account (for Personal Customers) Premier Reserve Account (for Trusts) 3

CHEQUE COLLECTION POLICY

CHEQUE COLLECTION POLICY Introduction As a part of normal banking operations, the Bank undertakes collection of cheques deposited by its customers, some of which could also be drawn on non-local bank branches.

CHEQUE COLLECTION POLICY Introduction As a part of normal banking operations, the Bank undertakes collection of cheques deposited by its customers, some of which could also be drawn on non-local bank branches.

ANZ Commercial Card TERMS AND CONDITIONS 11.2015. ANZ Corporate Card ANZ Visa Purchasing Card ANZ Business One

ANZ Commercial Card TERMS AND CONDITIONS 11.2015 ANZ Corporate Card ANZ Visa Purchasing Card ANZ Business One Containing Terms and Conditions for: Facility Terms and Conditions Electronic Banking Conditions

ANZ Commercial Card TERMS AND CONDITIONS 11.2015 ANZ Corporate Card ANZ Visa Purchasing Card ANZ Business One Containing Terms and Conditions for: Facility Terms and Conditions Electronic Banking Conditions

BNZ Advantage Credit Card Terms and Conditions.

BNZ Advantage Credit Card Terms and Conditions. 1 May 2015 This document contains the terms and conditions that apply to BNZ Advantage credit card accounts operated by you, including the terms and conditions

BNZ Advantage Credit Card Terms and Conditions. 1 May 2015 This document contains the terms and conditions that apply to BNZ Advantage credit card accounts operated by you, including the terms and conditions

CUSTOMER COMPENSATION POLICY

CUSTOMER COMPENSATION POLICY 1.1. 1.2. 1.3. 1.4. 1.4.1. 1.4.2. 1.4.3. 1.4.4. This Compensation Policy of the Bank is designed to cover all the incidences where the Bank is liable to make good any financial

CUSTOMER COMPENSATION POLICY 1.1. 1.2. 1.3. 1.4. 1.4.1. 1.4.2. 1.4.3. 1.4.4. This Compensation Policy of the Bank is designed to cover all the incidences where the Bank is liable to make good any financial

I loved reading the terms & conditions! said no one, ever. term deposit terms + conditions

I loved reading the terms & conditions! said no one, ever term deposit terms + conditions index. Part a - general terms and conditions. 2 1 Purpose of this booklet. 2 2 Meaning of words used. 2 3 Opening

I loved reading the terms & conditions! said no one, ever term deposit terms + conditions index. Part a - general terms and conditions. 2 1 Purpose of this booklet. 2 2 Meaning of words used. 2 3 Opening

and Conditions Business Telephone Banking

Terms and Conditions Business Telephone Banking Effective as at 18 April 2015 Contents Introduction 3 Your Bank 3 Our obligation to you 3 Features 4 Description 4 Bank Undertaking Security Deposit Accounts

Terms and Conditions Business Telephone Banking Effective as at 18 April 2015 Contents Introduction 3 Your Bank 3 Our obligation to you 3 Features 4 Description 4 Bank Undertaking Security Deposit Accounts

MAINTENANCE OF DEPOSIT ACCOUNTS BY UCBs

Opening of Accounts Introduction MAINTENANCE OF DEPOSIT ACCOUNTS BY UCBs The practice of obtaining proper introduction should not be treated as a mere formality, but as a measure of safe-guard against

Opening of Accounts Introduction MAINTENANCE OF DEPOSIT ACCOUNTS BY UCBs The practice of obtaining proper introduction should not be treated as a mere formality, but as a measure of safe-guard against

Policy on Collection of Cheques/Instruments

Punjab National Bank Operations, Payment and Settlement Division Customer Care Centre HO: 5, Sansad Marg, New Delhi-110001. Policy on Collection of Cheques/Instruments 1. Introduction Keeping in view the

Punjab National Bank Operations, Payment and Settlement Division Customer Care Centre HO: 5, Sansad Marg, New Delhi-110001. Policy on Collection of Cheques/Instruments 1. Introduction Keeping in view the

Last modified on 16-3-15. IEC Code : c INR Account. c FCY Account* c EEFC Account* Permanent Account Number : Registered Address : Fax : Mobile

The form should be signed after all details are completely filled. All information in the "Entity Details" section is Mandatory. Please complete all sections in BLOCK LETTERS and tick boxes where applicable.

The form should be signed after all details are completely filled. All information in the "Entity Details" section is Mandatory. Please complete all sections in BLOCK LETTERS and tick boxes where applicable.

2. Direct debits/electronic payments (RTGS/NEFT)/other debits to accounts

/other debits to accounts") Compensation Policy Introduction The objective of this policy is to establish a system whereby the bank compensates the customer for any financial loss he/she might incur due to deficiency in service on

Compensation Policy Introduction The objective of this policy is to establish a system whereby the bank compensates the customer for any financial loss he/she might incur due to deficiency in service on

Contents. Choosing the account that is right for you. Savings accounts. Fixed deposits. Current accounts/cheque. Foreign currency.

1 2 3 4 5 6 7 8 9 10 11 12 13 Contents Choosing the account that is right for you Savings accounts Fixed deposits Current accounts/cheque Foreign currency Minimum balances Payments into accounts Payments

1 2 3 4 5 6 7 8 9 10 11 12 13 Contents Choosing the account that is right for you Savings accounts Fixed deposits Current accounts/cheque Foreign currency Minimum balances Payments into accounts Payments

Personal Instalment Loan - Express Loan Application Form

Page 1 of 5 For Bank Use Only Br CA 10EP011 PR ECA001 Applicant Information A/C Off code ears of Residence Home Tel. No. obile Phone & Pager No. are not accepted E I RE To: DBS Bank Hong Kong Limited the

Page 1 of 5 For Bank Use Only Br CA 10EP011 PR ECA001 Applicant Information A/C Off code ears of Residence Home Tel. No. obile Phone & Pager No. are not accepted E I RE To: DBS Bank Hong Kong Limited the

COMPENSATION POLICY. The policy is based on the principles of transparency and fairness in the treatment of customers.

Introduction COMPENSATION POLICY Technological progress in payment and settlement systems and the qualitative changes in operational systems and processes that have been undertaken by various players in

Introduction COMPENSATION POLICY Technological progress in payment and settlement systems and the qualitative changes in operational systems and processes that have been undertaken by various players in

IMPORTANT TERMS AND CONDITIONS To get the complete version, please visit www.hsbc.co.in 1. FEES AND CHARGES a) Annual Membership fees Annual

Annual Membership fees Annual") IMPORTANT TERMS AND CONDITIONS To get the complete version, please visit www.hsbc.co.in 1. FEES AND CHARGES a) Annual Membership fees Annual Membership fees are applicable on the primary and add-on credit

IMPORTANT TERMS AND CONDITIONS To get the complete version, please visit www.hsbc.co.in 1. FEES AND CHARGES a) Annual Membership fees Annual Membership fees are applicable on the primary and add-on credit

SyndicateBank Global Credit Cards EXTRA Power in your purse

SyndicateBank Global Credit Cards EXTRA Power in your purse SyndicateBank Global Credit Card (SBGCC) - a payment product of great value and convenience, is offered to you NOW FREE FOR LIFE (No entrance

SyndicateBank Global Credit Cards EXTRA Power in your purse SyndicateBank Global Credit Card (SBGCC) - a payment product of great value and convenience, is offered to you NOW FREE FOR LIFE (No entrance

HSBC Advance Account Opening Application

HSBC Advance Account Opening Application To The Manager,... Office The Hongkong and Shanghai Banking Corporation Limited Sri Lanka FOR BANK USE ONLY D D M M Y Y Y Y Note : 1. Please complete in Block Letters

HSBC Advance Account Opening Application To The Manager,... Office The Hongkong and Shanghai Banking Corporation Limited Sri Lanka FOR BANK USE ONLY D D M M Y Y Y Y Note : 1. Please complete in Block Letters

CHAPTER 13 COMPLIANCE

CHAPTER 13 COMPLIANCE By a Trading Member / Clearing Member 13.1 Annual Accounts and Audit 13.1.1 Every trading member / clearing member shall prepare annual accounts for each financial year ending on

CHAPTER 13 COMPLIANCE By a Trading Member / Clearing Member 13.1 Annual Accounts and Audit 13.1.1 Every trading member / clearing member shall prepare annual accounts for each financial year ending on

INDUSIND BANK LTD. POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS

INTRODUCTION INDUSIND BANK LTD. POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS This collection policy of the Bank is a reflection of our on-going efforts to provide better service to our Customers and set

INTRODUCTION INDUSIND BANK LTD. POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS This collection policy of the Bank is a reflection of our on-going efforts to provide better service to our Customers and set

TERMS AND CONDITIONS FOR THE ICICI BANK INDIAN RUPEE TRAVEL CARD

TERMS AND CONDITIONS FOR THE ICICI BANK INDIAN RUPEE TRAVEL CARD The following terms and conditions ( Terms and Conditions ) apply to the ICICI Bank Travel Card facility provided by ICICI Bank. For your

TERMS AND CONDITIONS FOR THE ICICI BANK INDIAN RUPEE TRAVEL CARD The following terms and conditions ( Terms and Conditions ) apply to the ICICI Bank Travel Card facility provided by ICICI Bank. For your

David Jones Storecard and David Jones American Express Card Member Agreement, Financial Services Guide and Purchase Protection. Terms and Conditions

David Jones Storecard and David Jones American Express Card Member Agreement, Financial Services Guide and Purchase Protection Terms and Conditions Issued May 2016 DAVID JONES STORECARD AND DAVID JONES

David Jones Storecard and David Jones American Express Card Member Agreement, Financial Services Guide and Purchase Protection Terms and Conditions Issued May 2016 DAVID JONES STORECARD AND DAVID JONES

credit cards Our terms and conditions for Your credit card

credit cards Our terms and conditions for Your credit card Contents PAGE 4 Introduction and Definitions Scope Agreement Read these Terms and Conditions Over-riding laws Guarantees as to service Interpretation

credit cards Our terms and conditions for Your credit card Contents PAGE 4 Introduction and Definitions Scope Agreement Read these Terms and Conditions Over-riding laws Guarantees as to service Interpretation

HiSAVE Fixed Rate Account

UK PLC An FSA regulated UK Bank HiSAVE Fixed Rate Account These terms and conditions apply to the HiSAVE Fixed Rate Account (hereinafter referred to as the "HiSAVE Fixed Rate Account"). They, together

UK PLC An FSA regulated UK Bank HiSAVE Fixed Rate Account These terms and conditions apply to the HiSAVE Fixed Rate Account (hereinafter referred to as the "HiSAVE Fixed Rate Account"). They, together

Deposit Policy. Review and Update: The Deposit Policy will be reviewed at least annually and revised, if necessary.

Deposit Policy Review and Update: The Deposit Policy will be reviewed at least annually and revised, if necessary. Table of Contents 1. Introduction... 3 2. Types of Deposit Accounts... 3 3. Account Opening

Deposit Policy Review and Update: The Deposit Policy will be reviewed at least annually and revised, if necessary. Table of Contents 1. Introduction... 3 2. Types of Deposit Accounts... 3 3. Account Opening

CREDIT CARD. Our terms and conditions for. Your credit card

CREDIT CARD Our terms and conditions for Your credit card 1 Introduction and Definitions 1.1 Scope These Terms and Conditions are a contract between you and BNZ. They apply to the use of your Card, including

CREDIT CARD Our terms and conditions for Your credit card 1 Introduction and Definitions 1.1 Scope These Terms and Conditions are a contract between you and BNZ. They apply to the use of your Card, including

CREDIT CARD MOST IMPORTANT TERMS & CONDITIONS

CREDIT CARD MOST IMPORTANT TERMS & CONDITIONS 2 MOST IMPORTANT TERMS & CONDITIONS a)fees and Charges Description of Charges ING Solaris Credit Card Joining Fee `500 `1,500 Annual Fee Add-on Card Fee Renewal

CREDIT CARD MOST IMPORTANT TERMS & CONDITIONS 2 MOST IMPORTANT TERMS & CONDITIONS a)fees and Charges Description of Charges ING Solaris Credit Card Joining Fee `500 `1,500 Annual Fee Add-on Card Fee Renewal

TRIPARTITE AGREEMENT BETWEEN STOCK BROKER, SUB - BROKER AND CLIENT

TRIPARTITE AGREEMENT BETWEEN STOCK BROKER, SUB - BROKER AND CLIENT This Agreement (hereinafter referred to as Agreement ) is entered into on this day of 20, by and between M/s. First Global Stockbroking

TRIPARTITE AGREEMENT BETWEEN STOCK BROKER, SUB - BROKER AND CLIENT This Agreement (hereinafter referred to as Agreement ) is entered into on this day of 20, by and between M/s. First Global Stockbroking

Investment & Transaction Accounts

Bankwest Investment & Transaction Accounts Terms and Conditions 25 May 2015 making banking easier Terms and Conditions These Terms and Conditions apply to all Investment and Transaction Accounts with us

Bankwest Investment & Transaction Accounts Terms and Conditions 25 May 2015 making banking easier Terms and Conditions These Terms and Conditions apply to all Investment and Transaction Accounts with us

UNION BANK OF INDIA Good People to Bank with

UNION BANK OF INDIA Good People to Bank with For Bank use only BRANCH CODE The Branch Manager Union Bank of India Account No. Account Type ACCOUNT OPENING FORM FOR NON-RESIDENT INDIAN (NRI) I/We request

UNION BANK OF INDIA Good People to Bank with For Bank use only BRANCH CODE The Branch Manager Union Bank of India Account No. Account Type ACCOUNT OPENING FORM FOR NON-RESIDENT INDIAN (NRI) I/We request

ONLINE BANKING APLICATION

ONLINE BANKING APLICATION Taken by: Initials CUSTOMER INFORMATION Extension Name: New User Existing User Modification Address: TIN/SSN: City: State: Zip: Home Phone: Work Phone: Account Name List all the

ONLINE BANKING APLICATION Taken by: Initials CUSTOMER INFORMATION Extension Name: New User Existing User Modification Address: TIN/SSN: City: State: Zip: Home Phone: Work Phone: Account Name List all the

Terms and Conditions of SABB Credit Cards

Terms and Conditions of SABB Credit Cards Important: Before you use The Saudi British Bank MasterCard and/or Visa Card ( the Card ), please carefully read the Cardholder Agreement printed below. By using

Terms and Conditions of SABB Credit Cards Important: Before you use The Saudi British Bank MasterCard and/or Visa Card ( the Card ), please carefully read the Cardholder Agreement printed below. By using

BOC Express Cash Revolving Credit The Most Versatile Balance Transfer Program For Financial Management, Choose the BOC Express Cash Card

BOC Express Cash Revolving Credit The Most Versatile Balance Transfer Program For Financial Management, Choose the BOC Express Cash Card Switch to BOC Express Cash Revolving Credit The Most Versatile Balance

BOC Express Cash Revolving Credit The Most Versatile Balance Transfer Program For Financial Management, Choose the BOC Express Cash Card Switch to BOC Express Cash Revolving Credit The Most Versatile Balance

Online Banking Agreement

Online Banking Agreement Please read the Terms and Conditions below and "sign" below, by checking the box below and click submit. We recommend that you print a copy of this document and maintain a copy

Online Banking Agreement Please read the Terms and Conditions below and "sign" below, by checking the box below and click submit. We recommend that you print a copy of this document and maintain a copy

T +1 (345) 949-0330 / F +1 (345) 945-1448 / E: The Banking Code. Contents

949-0330 / F +1 (345) 945-1448 / E: The Banking Code. Contents") 1107 T +1 (345) 949-0330 / F +1 (345) 945-1448 / E: The Banking Code Contents 1 Introduction 3 2 Our Key Commitments to you 3 3 Helping you to choose Products and Services which meet your Needs 4 4 Interest

1107 T +1 (345) 949-0330 / F +1 (345) 945-1448 / E: The Banking Code Contents 1 Introduction 3 2 Our Key Commitments to you 3 3 Helping you to choose Products and Services which meet your Needs 4 4 Interest

THE NATIONAL TREASURY REPUBLIC OF SOUTH AFRICA RSA GOVERNMENT RETAIL BOND. The smart way to save

THE NATIONAL TREASURY REPUBLIC OF SOUTH AFRICA RSA GOVERNMENT RETAIL BOND The smart way to save Summary of Retail Bond This booklet is a summary of the RSA Retail Bond Owner s manual and should be read

THE NATIONAL TREASURY REPUBLIC OF SOUTH AFRICA RSA GOVERNMENT RETAIL BOND The smart way to save Summary of Retail Bond This booklet is a summary of the RSA Retail Bond Owner s manual and should be read

Most Important Terms & Conditions (Approved by the RMC at its meeting held on 9 th. J une 2015)

") INDIABULLS HOUSING FINANCE LIMITED Most Important Terms & Conditions (Approved by the RMC at its meeting held on 9 th. J une 2015) Indiabulls MITC elaborates the terms and conditions with respect to the

INDIABULLS HOUSING FINANCE LIMITED Most Important Terms & Conditions (Approved by the RMC at its meeting held on 9 th. J une 2015) Indiabulls MITC elaborates the terms and conditions with respect to the

Our standard terms and conditions for Your Advanced Personal Loan.

Our standard terms and conditions for Your Advanced Personal Loan. For loans approved on or after 6 June 2015 6 June 2015 Important Information The information set out below forms part of your disclosure

Our standard terms and conditions for Your Advanced Personal Loan. For loans approved on or after 6 June 2015 6 June 2015 Important Information The information set out below forms part of your disclosure

Credit Card Contract

Credit Card Contract Credit Card Booklet Cardholder enquiries & Lost and stolen cards Telephone : (679) 321 4300 Facsimile : (679) 330 3738 BSP/SecDocTemp006 Page 1 of 21 Template Issue No.3 reviewed 19032012

Credit Card Contract Credit Card Booklet Cardholder enquiries & Lost and stolen cards Telephone : (679) 321 4300 Facsimile : (679) 330 3738 BSP/SecDocTemp006 Page 1 of 21 Template Issue No.3 reviewed 19032012

Credit Card Agreement for Consumer Secured Cards in Capital One Bank (USA), N.A.

, N.A.") Credit Card Agreement for Consumer Secured Cards in Capital One Bank (USA), N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer Agreement.

Credit Card Agreement for Consumer Secured Cards in Capital One Bank (USA), N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer Agreement.

At-Call Savings Accounts

At-Call Savings Accounts Part 1 - At-Call Savings Accounts Product Disclosure Statement (Corporations Act (Cth) 2001) comprises of the following documents Part 1 - Product Disclosure Statement for all

At-Call Savings Accounts Part 1 - At-Call Savings Accounts Product Disclosure Statement (Corporations Act (Cth) 2001) comprises of the following documents Part 1 - Product Disclosure Statement for all

Premium Savings Account (CBS branches only) - High earnings with easy liquidity

- High earnings with easy liquidity") Corporate Office : Gandhinagar : Bangalore 560 009 ------------------------------------------------------------------------------------------------------------ OUR DEPOSIT SCHEMES Savings Deposit Account

Corporate Office : Gandhinagar : Bangalore 560 009 ------------------------------------------------------------------------------------------------------------ OUR DEPOSIT SCHEMES Savings Deposit Account

Transactional and Savings Accounts. Combined Product Disclosure Statement and Financial Services Guide

Transactional and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide Transaction and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide

Transactional and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide Transaction and Savings Accounts Combined Product Disclosure Statement and Financial Services Guide

Deutsche Bank Cheque Collection Policy Updated in November 2013

Deutsche Bank Cheque Collection Policy Updated in November 2013 1. Introduction This collection policy of Deutsche Bank AG, India ( Bank ) is a reflection of our on-going efforts to provide better service

Deutsche Bank Cheque Collection Policy Updated in November 2013 1. Introduction This collection policy of Deutsche Bank AG, India ( Bank ) is a reflection of our on-going efforts to provide better service

POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS

POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS This collection policy of the Bank is a reflection of our on-going efforts to provide better service to our customers and set higher standards for performance.

POLICY ON COLLECTION OF CHEQUES / INSTRUMENTS This collection policy of the Bank is a reflection of our on-going efforts to provide better service to our customers and set higher standards for performance.

Sumitomo Mitsui Banking Corporation Customer Compensation Policy. Version: 02

Sumitomo Mitsui Banking Corporation Customer Compensation Policy Version: 02 Table of Contents Table of Contents 1. Introduction...1 2. Unauthorized/Erroneous Debit...2 3. NACH debits/other debits to Accounts...3

Sumitomo Mitsui Banking Corporation Customer Compensation Policy Version: 02 Table of Contents Table of Contents 1. Introduction...1 2. Unauthorized/Erroneous Debit...2 3. NACH debits/other debits to Accounts...3

DEPOSIT POLICY OF THE BANK.

DEPOSIT POLICY OF THE BANK. For the year 2012-2013. Revised Deposit Policy of the Bank. 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending.

DEPOSIT POLICY OF THE BANK. For the year 2012-2013. Revised Deposit Policy of the Bank. 1. Preamble One of the important functions of the Bank is to accept deposits from the public for the purpose of lending.

CORPORATE ACCOUNT. ...we make the difference

CORPORATE ACCOUNT CORPORATE ACCOUNT GUIDE TO OPENING YOUR ACCOUNT Please complete all the relevant portions of the Application Form and Account Opening mandate and return the package along with the following

CORPORATE ACCOUNT CORPORATE ACCOUNT GUIDE TO OPENING YOUR ACCOUNT Please complete all the relevant portions of the Application Form and Account Opening mandate and return the package along with the following

Policy on Dormant Accounts & Unclaimed Deposits

Policy on Dormant Accounts & Unclaimed Deposits CORPRATE PLANNING DEPARTMENT Table of contents SL No. Contents 1 Preamble 2 Objective 3 Classification of accounts as Dormant Accounts 4 Operational Procedure