November UK Betting Shops: Over-The-Counter Versus Machines

|

|

|

- Andra Cain

- 8 years ago

- Views:

Transcription

1 bsite ve website November 2012 g UK Betting Shops: Over-The-Counter Versus Machines

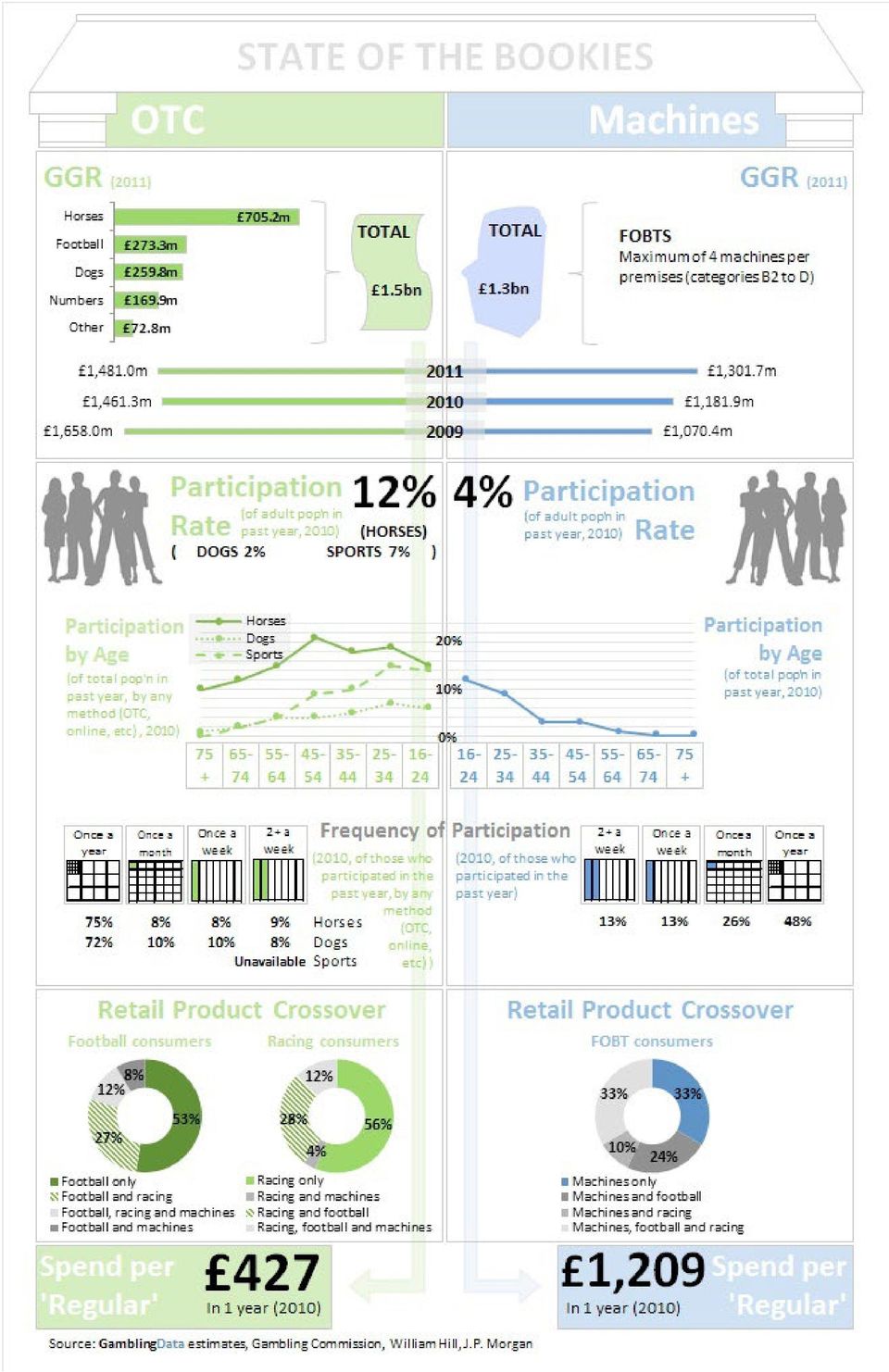

2 Contents Executive Summary The State of the Bookies UK data - Over-the-counter versus machines Key metrics Demographics A closer look Analyst View Logo revisions/options Font: Palatino Roman Blue: From gamblingdata.com Red: from gamblingcompliance.com 91 Waterloo Road, London, SE1 8RT Tel: info@gamblingdata.com This set shows the logos with the co Scott Longley +44(0) scott@gamblingdata.com 2

3 Font: Palatino Roman Blue: From gamblingdata.com Logo revisions/options s Executive Summary Gap narrowing between OTC and machines: Statistics collated by the UK Gambling Commission show that gross gambling yield generated by machines, or fixed odds betting terminals (FOBTs), in UK betting shops is catching up with the total generated by over-the-counter (OTC) betting. From FY2009 to FY2011, gross gambling yield from machines in the UK retail betting industry climbed 21.6 percent from 1.07bn to 1.30bn while the metric for OTC betting fell 10.7 percent over the same period from 1.66bn to 1.48bn. Figures from the two leading high street bookmakers, William Hill and Ladbrokes, back up this trend, with gross win from machines surpassing that from OTC for the first time at both operators in the second half of Red: from gamblingcompliance.com This set shows the logos with the co Reasons for the OTC decline: Decline in OTC has been attributed to factors including competition from fixed odds betting terminals and online gaming, an ageing customer base and the deterioration of the high street. The UK Gambling Commission data suggests that OTC margin deflation has also played a role in recent years, with change in customers attitudes to prices, online competition and structural problems within horseracing contributing to consecutive contractions in industry-wide OTC horseracing margins in FY2010 and FY2011. The consensus outlook on OTC betting among analysts is broadly negative, though there remains a division between those that believe the decline is structural and those that believe it is cyclical and largely recession-related. OTC betting as a complementary product: Product usage data from Kantar Retail relating to the UK retail betting industry as a whole suggests that, while horseracing and football have in recent years typically accounted for around 25 percent and 5-10 percent of UK retail gross gambling yield respectively, the importance of OTC betting to bookmakers lies more in getting people into shops than in directly generating revenue, speaking to its utility as a complementary product. The data indicates that 57 percent of UK retail customers place bets on horseracing and 59 percent on football, versus only 21 percent for machines, and that around 43 percent of the UK retail customers who bet on machines also bet on horseracing, while around 57 percent also bet on football. Measuring the importance of OTC: The product crossover data suggests that any factor impacting positively or negatively on the footfall or dwell time of horseracing punters would have a meaningful knock-on effect on wagering on football and machines. While anecdotal evidence indicates that horseracing remains an important part of the eco-system of betting shops, it is difficult to quantify the extent to which a negative shock to horseracing wagering would impact wagering across all retail products. One pertinent case study was provided when Betfred became the last holdout over the adoption of Turf TV - the firm did not sign up to the broadcaster s live feeds until April 2009, while its major high street rivals had each reached agreements by January The strong growth achieved by the firm in the two year periods bookending a decline in the year ending March 2009 suggests that there was a clear causal link between Betfred s lack of Turf TV pictures during that period and its negative growth in betting turnover. 3

4

5 Font: Palatino Roman Blue: From gamblingdata.com Logo revisions/options s The State of the Bookies Highlighted points OTC revenues have declined over the past three years while the revenues from machines have grown OTC annual revenues have always exceeded machines revenues but in 2011 the difference was only 13.8 percent UBS claim that the economic recession has negatively impacted wagers at the bookies 50 percent of FOBT bettors use the machines more than once a month, compared to just 25 percent for horseracing bettors and 28 percent of greyhound racing punters FOBT bettors tend to be younger players, with a negligible amount of over 65s using the devices, but horseracing bettors are quite evenly distributed across all age groups The age group data shows high correlation between FOBT users and sports bettors and FOBT users and greyhound bettors, but there is a low correlation between FOBT users and horseracing bettors Data from William Hill suggests that 93 percent of its retail customers bet OTC while 21 percent use machines This implies that a machine customer wagers 21.5 times more than an OTC customer over a year If we do the same calculation on William Hill s win, then the average machine gambler lost 3.8 times more than the average OTC customer over the year. JP Morgan reported in an investor note in June this year that spend on FOBTs per participant per year is 642 while it is only 146 for OTC However, using participation frequency data from the UK Gambling Commission s 2010 Prevalence Survey, GamblingData s estimates indicate that the difference in spend is less stark when infrequent customers are removed from the data. Among customers participating once a month or more, GamblingData estimates that the annual spend per regular is 1,209 on FOBTs versus 427 for OTC horseracing betting Approximately 12 percent of the population bet on horseracing OTC, 2 percent of the population bet on greyhounds OTC, while 7 percent use the medium for sports betting Both Ladbrokes and William Hill had 3.86 machines per shop on average in the first half of Gross win per machine week has been growing and Ladbrokes reported a figure of 947 in the period, while at William Hill it was 934 Analysts believe that innovative next generation machines can drive further growth Product mix of OTC betting by wagers reveals that football is steadily becoming more important to the bookmakers and in 2011 it was by far the highest margin product OTC Red: from gamblingcompliance.com This set shows the logos with the co 5

6 This set shows the logos with the co Red: from gamblingcompliance.com live website current gamblingdata.com, From Blue: Roman Palatino Font: Logo revisions/options s UK data: Over-the-counter (OTC) versus machines OTC v machines overview - the crossover evidence It is notable that the bookmakers themselves are keen to promote the existence of an eco-system within their betting outlets, pointing to the cross-fertilisation of customers across all their product types. What is also clear is the degree to which the betting shop audience in absolute terms remains very much an over-the-counter one, despite the rise of machine revenues at the major firms. According to data from William Hill, 94 percent of retail customers bet OTC while a minority 21 percent use only machines. OTC revenues continue to outweigh machine revenues, although the gap between total annual OTC revenues and machine revenues is closing, to around 14 percent in But consistent with the absolute numbers of customer split, the spend per customer for OTC betting is more evenly spread at around the level of 146 per customer per year compared with 642 per customer per year for machines, according to analysis from JP Morgan. But even with the minority cohort of machine gamblers, it might be suggested that the atmosphere of the shop is an important factor in their consumption within a betting shop. A survey conducted by SPA Research of William Hill customers on behalf of the company in 2010 (and reported in an analyst day presentation the next year) showed that 31 percent of customers thought location was the most important aspect of why they bet in shops, while 29 percent said it was a good place to socialise and 28 percent said it was a comfortable environment in which to bet. Tellingly, perhaps, 22 percent said they bet in the shops to watch the results. Another survey for William Hill from Kantar Research also found that 32 percent of shop customers bet solely on racing, while 31 percent bet on football only. The Kantar survey meanwhile suggested that 12 percent of the total UK population bet on horseracing; this corroborates evidence from the Gambling Commission which said back in 2010 that 16 percent of the population had bet on horseracing over the past year. This survey also pointed to how horserace betting was a pastime that appealed across generations with an even distribution of participation across all age groups. Notably, the Kantar survey data indicated that around 43 percent of the UK retail betting customers who bet on machines also bet on horseracing, while around 57 percent also bet on football. Lastly, William Hill s investor presentation back in 2011 made the point that customers who bet on multiple products were the most valuable customers with a relative monthly spend of 268 compared with 120 for racing-only customers and 85 for the football-only cohort. No figures were given for machine-only customers. These figures back up a recent statement from William Hill s major rival Ladbrokes, which said at the time of the company s interim trading statement in August that the OTC business continues to demonstrate its enduring customer appeal, despite challenging conditions on the UK high street. As a note from analysts at Investec back in 2010 put it, the crossover 6

7 potential for retail was still very strong, with good shops likely to be able to see good cross-sell from machines to football to racing because the latter remains an excellent betting medium. Horseracing and machines the analysts view A look at what the analysts say does not spell out good news for the horseracing industry. None are of the opinion that OTC has a particularly bright future, as typified by Credit Suisse s Matthew Gerard who points out that OTC gross win at Ladbrokes and William Hill is declining at around 5 to 8 percent year-on-year, ex any major football tournament. He goes on to state that the prospects for a recovery are now highly unlikely. Slightly more optimism comes from Investec s then gaming analyst Paul Leyland who suggested that primary betting shops would fare well in the future. But these establishments would tend to be those on the high street which are more attuned to football and machines betting, while the tertiary shops in post-industrial locations where horseracing betting was more dominant would be comparatively left behind. A much more positive message on horserace betting and OTC came from a survey conducted by UBS in the summer last year. This report played down the structural decline argument, showing that of 200 sports-betting customers surveyed, only 7 percent said they would shift to online betting in the coming year. The survey also found that environment was important, with shop atmosphere being more important than odds in determining where people might choose to bet. The survey results concur with the comments from another betting professional with years worth of experience at a major firm who pointed out that the feel of a betting shop was a vital factor in attracting and keeping the customers. Racing is still the biggest OTC product, the source said. The shops rely on having racing for the buzz. It s still an important part of the ecosystem. Of course, the betting industry as a whole already has an example of what happens when racing pictures are not available, during the foot and mouth crisis back in That crisis saw the rise of virtual racing and betting, but perhaps a more pertinent example came when Betfred became the last holdout over the adoption of Turf TV. The firm did not sign up to Turf TV s live racing feeds until April 2009, while high street rivals William Hill, Ladbrokes and Coral had each reached agreements with the broadcaster by January Comments made at the time to the Racing Post and other media suggest that Betfred had seen enough evidence on the ground for a fall off in OTC trade to suggest that life in the shops without racing pictures would be less enticing for the public and less profitable for operators. Said one ex-betting shop executive: As Betfred found, it s hard to cut racing if your competitors have it. Figures included in Betfred s annual accounts would appear to back up this observation. In the 12 months to March 30, 2009, a period during which Betfred did not carry Turf TV s pictures while its major competitors did, the group saw betting turnover across all channels fall 3 percent year-onyear, having achieved growth of 16.3 percent in the prior reporting period. Having since undertaken a change in its accounting methods to include 7

8 re-staked winnings as part of its machines turnover, Betfred has generated like-for-like betting turnover growth of 26.3 percent and 17.4 percent in the last two fiscal years. While it is impossible to quantify the impact that the Turf TV deal has had on Betfred s betting turnover, the strong growth achieved by the firm in the two year periods bookending its decline in fiscal 2009 suggests that there was a clear causal link between Betfred s lack of Turf TV pictures during that period and its negative growth in betting turnover. Still, the issue of racing s future in a digital world is not an argument confined to the UK. At a recent Asian Racing Conference held in Istanbul in July, the chief executive of the Hong Kong Jockey Club Winfried Engelbrecht-Bresges pointed out that the digital customer was forging ahead of the racing industry. In response, the HKJC has started using interactive betting tables to enable punters at the track to search for information about any given race, and then bet via cashless transaction. This was aimed at persuading a younger demographic that racing was a game of skill not chance, and it had already notched up some successes in terms of attracting younger punters. As our industry expert suggests, what has happened to the OTC audience is that it has been educated by the evolution taking place in online betting. Not so long ago, 70 percent (of OTC customers) were taking the starting price. Now, over 80 percent of OTC bets are taking the price. Before exchanges, the bookies might price up one or two races in the morning. Now they have prices all day. We ve educated the audience. But this move has come at the detriment of margins. Exchanges have done that. Customers are more knowledgeable. This customer education process means that innovation across all products is being seen as the way to engage the customer base. The introduction of self-service betting terminals, for instance, will bring to the shops something more akin to the wide selection of events available online. Still, as Vaughan Lewis at Morgan Stanley pointed out to GamblingData: In the current climate the machines versus OTC debate is an old argument. Things are starting to normalise in machine revenues. 8

9 Font: Palatino Roman Blue: From gamblingdata.com s Logo revisions/options Key metrics Historical performance The statistics collated by the UK Gambling Commission for the entire retail betting market clearly display the revenue trends of over-the-counter (OTC) decline and machine growth over the past few years. Red: from gamblingcompliance.com Machine revenues grew by 10.4 percent in FY2010 to 1.17bn and 10.1 percent in FY2011 to 1.30bn. OTC betting suffered an 11.9 percent fall in gross gambling yield to 1.46bn in FY2010 but recovered slightly in FY2011 to 1.48bn. In FY2011 OTC betting generated 13.8 percent more in gross gambling yield than machines, the smallest differential to date. Decline in OTC has been attributed to factors including competition from fixed odds betting terminals (FOBTs) and online gaming, an ageing customer base and the deterioration of the high street, while a note released by UBS in June 2011 cited proprietary survey data which showed that the downturn in recent years was largely recession-related, an opinion which supported the view of the bookmakers. Beyond these factors, the UK Gambling Commission data suggests that margin deflation has also played a role in the declines observed in OTC gross gambling yield in recent years. The 11.9 percent decline in OTC gross gambling yield in FY2010 came as a 90 basis point deterioration in industry-wide OTC margins to 15.8 percent exacerbated a more modest 6.5 percent contraction in OTC turnover. With margins on OTC betting on horseracing having fallen from 14.7 percent in FY2009 to 14.1 percent in FY2010 and 13.7 percent in FY2011, analysts at J.P. Morgan wrote in a note to investors in June 2012: Horseracing gross win margin has been eroded over the last decade. In 2001 and 2002, this was driven by competition from online operators, who were able to undercut on-course bookmakers on price. Since 2006, the number of runners per race has also been in decline, partly due to financial problems in the horseracing industry. For bookmakers, this has resulted in pressure on amounts staked (with fewer opportunities for customers to bet) and gross win margin (as fewer runners mean a smaller overround). Retail betting landscape The UK retail bookmaking market is dominated by four main players; William Hill, Ladbrokes, Gala Coral and Betfred/Tote, which collectively account for 82 percent of all betting shops in the UK. This set shows the logos with the co 9

10 In the past three years each of the major operators have increased their estates, most notably Betfred which controlled 1,345 retail premises as at March 31, 2012 versus 840 a year previously thanks to its acquisition of the Tote. This collective move towards expansion indicates that the bookmakers have confidence in the retail market, with Ladbrokes having written in its Summer 2012 interim report that the OTC business continues to demonstrate its enduring customer appeal, despite challenging conditions on the UK high street. Retail outlook The two market leaders in UK retail bookmaking, Ladbrokes and William Hill, are showing indications that machine revenue could come close to exceeding OTC takings in the full-year In the second half of 2011 machines revenue surpassed OTC revenue for the first time at both William Hill and Ladbrokes. In the most recent halfyear results, covering the six months to June 2012, OTC bounced back for both bookmakers, having benefited from an incremental stream of bets during the Euro 2012 football tournament. OTC revenues tend to be cyclical, with first-half results exceeding second-half results while machine revenue has been on a steady upward trend, indicating that it is likely 10

11 machine revenues will repeat last year s feat by surpassing OTC revenues in the second half of this year. In their interim reports for the first half of 2012 both Ladbrokes and William Hill admitted that stakes were swelled by the Euro 2012 tournament but they highlighted that there were 9 percent fewer racing fixtures during the period when compared to the first half of 2011 due to poor weather. Ladbrokes wrote of its first-half performance: We have continued in H1 to demonstrate the strength and growth potential of UK Retail which is benefiting from ongoing efficiency initiatives and further expansion of the estate. In an interim management update for the third quarter of the year, Ladbrokes reported robust 11.5 percent year-on-year growth in machine revenues, down from 20.1 percent in the first six months of 2012, and 0.6 percent growth in OTC revenues, down from 2.4 percent in the first half of the year and weighed down by a post-euro 2012 and Olympics hangover effect through August and September. William Hill management for their part highlighted the impact of the wettest summer on record and a weather-related 4 percent reduction in horseracing fixtures in the quarter as they reported 2 percent growth in machine revenues, down from 4.6 percent in the half-year statement, and 5 percent growth in OTC revenues, in line with the rate achieved in the first half of the year. Coral, the third largest retail operator, has reported similar trends to the two principal bookmakers, with OTC revenues declining in 2011 but the firm s machines segment outperforming prior year results. Shedding some light on the performance in 2012 so far the company related that the new Videobet platform for machines has been largely implemented and performance in the early part of the 2012 financial year is significantly ahead of 2011 levels. The bookmaker also had positive sentiments for OTC, which it said was 9 percent of prior year levels after two quarters of its financial year. 11

12 Font: Palatino Roman Blue: From gamblingdata.com s Logo revisions/options Demographics Participation by frequency In 2010 the Gambling Commission ordered a survey of gambling prevalence in the UK. One of the findings of the survey was that FOBT consumers are much more frequent gamblers than those betting on horseracing or greyhound racing. Red: from gamblingcompliance.com This set shows the logos with the co The data revealed that more than 50 percent of FOBT bettors use the machines more than once a month, compared to just 25 percent for horserace bettors and 28 percent on the dogs. This data might not be as informative as it initially appears, as traditional events such as the Grand National attract a lot of casual bettors who bet very infrequently. Ladbrokes has extended its loyalty card coverage from OTC betting to include machines in The bookmaker highlights the customer insights this strategy reaps: there are currently 100,000 active machine customers using the card and, on the evidence of the data gleaned from the scheme, Ladbrokes plans to increase machine density and focus on utilisation rates during specific times of the day. Participation by age The survey results suggested that 4 percent of the population played FOBTs at some point in 2010, while 16 percent had bet on horseracing, 4 percent on greyhound racing and 9 percent on sports. The survey revealed further details including the age distribution of the bettors, outlined below. The distribution of FOBT bettors is heavily weighted towards younger players with a negligible amount of those 65 or older using the devices. Horseracing bettors however are quite evenly distributed across all age groups with the highest prevalence being in the age bracket, where 21 percent of the population have bet on this type of activity. Greyhound racing and sports bettors are more weighted towards younger age groups but both activities also have a more even distribution than FOBT users. The correlation coefficient between the FOBT age group data and horseracing age group data is only 0.39; with 1 indicating a complete 12

13 positive correlation, -1 a complete negative correlation and 0 a complete lack of correlation. The relatively low correlation reflects the fact that the five over-35 cohorts have a relatively high propensity to gamble on horseracing in shops and a relatively low propensity to use FOBTs, suggesting that the vast majority of product crossover between horseracing bettors and FOBT users occurs in the and age brackets. Product crossover An investor presentation given by William Hill in September 2011 provided more illumination as to the extent of product crossover in UK betting shops. The data - provided by Kantar Retail and relating to the UK retail betting market as a whole - suggests that 31 percent of customers bet on football only and 32 percent on racing only. There are much fewer machine gamblers, at only 21 percent in total, which chimes with the aforementioned Gambling Commission research. Racing and machines have the smallest crossover but there are as many customers who bet on all three main product verticals of football, racing and machines as there are who just play machines. This product usage data is instructive in the context of the aforementioned UK Gambling Commission figures for gross gambling yield across the UK retail betting industry. While horseracing and football have in recent years typically accounted for around 25 percent and 5-10 percent of UK retail GGY respectively, versus just under 50 percent for machines, the data indicates that 57 percent of UK retail customers place bets on horseracing and 59 percent on football, versus only 21 percent for machines. William Hill s accompanying investor presentation emphasised the importance of cross-sell both from online to offline and from OTC to machines, citing Kantar Retail data that showed customers who bet on multiple products in betting shops have an average monthly spend of 268, versus 85 for those who only bet on football and 120 for racing-only punters. Indeed, the product crossover figures suggest that, despite still generating a significant portion of GGY in UK betting shops, horseracing and football s importance to bookmakers lies more in getting people into shops than in directly generating revenue, speaking to their utility as complementary products. 13

14 The Kantar Retail data shows that around 43 percent of the UK retail customers who bet on machines also bet on horseracing (9 percent of the 21 percent machines customer share), while around 57 percent also bet on football. Meanwhile, around 39 percent of the UK retail customers who bet on football also bet on horseracing. Taken as a whole, the data suggests that any factor impacting positively or negatively on the footfall or dwell time of horseracing punters in betting shops would have a meaningful knock-on effect on wagering on football and machines, in addition to wagering on horseracing itself. The same logic would also apply to any factor directly impacting football betting in shops. The data indicates that 93 percent of retail customers bet OTC while 21 percent use machines, meaning that in absolute terms there are 4.4 times more OTC customers than machine customers. In William Hill s 2010 annual report the company stated that 2.5bn was wagered OTC while 12.2bn was wagered on machines. If Kantar s market-wide customer data is considered along with this statistic then it would suggest that an average machine customer wagers 21.5 times more than an OTC customer over a year. This result supports the prevalence survey finding that FOBTs nurture frequent gaming. It should be noted that gross win margin for machines was only 3.2 percent in 2010 while it was 17.9 percent OTC, making FOBTs a much less risky gamble on a bet-by-bet basis. If we do the same calculation on William Hill s win, the data implies that an average machine gambler lost 3.8 times more than an OTC customer over the year. In a semblance of concurrence, JP Morgan reported in an investor note in June this year that spend on FOBTs per participant per year is 642 while it is only 146 OTC. Gambling participation rates recorded in the Gambling Commission s British Gambling Prevalence Survey 2010 formed the basis of these estimates, though a closer look at the participation frequency data included in that report yields a further insight into the differences in average spend per participant between FOBT customers and those who bet on horseracing OTC. While not a like-for-like comparison given that the JP Morgan OTC data point refers to all OTC betting and the equivalent figures cited below refer only to OTC horserace betting, the prevalence survey data indicates that the difference in average spend between FOBT customers and OTC horseracing customers is less stark when the contribution from infrequent participants is removed. Variables FOBTs Horseracing OTC UK adult population (2010) 51,400,000 51,400,000 Participation (%) 4% 12% Participation (#) 2,056,000 6,168,000 Revenue ( ) 1,302,000, ,000,000 Spend per customer ( ) Share of customers participating 48% 75% less than once a month Regular customers (once a month or more) 1,069,120 1,542,000 14

15 Variables FOBTs Horseracing OTC Infrequent customers 986,880 4,626,000 Estimated spend per infrequent customer ( ) Infrequent revenue ( ) 9,868,800 46,260,000 Regular revenue ( ) 1,292,131, ,740,000 Spend per regular ( ) 1, Source: GamblingData estimates, Gambling Commission Reflecting what is sometimes referred to in the industry as the Grand National effect whereby casual punters only visit betting shops once or twice a year to place bets on major races the prevalence study data indicates that 75 percent of OTC horseracing customers have a participation frequency of less than once a month, versus 48 percent for FOBT customers. Taken alongside the Gambling Commission s figures for overall participation and gross gambling yield for the two product verticals, and using the rough assumption of an average annual spend per infrequent customer of 10, the participation frequency data suggests that the spend per regular equals 1,209 for FOBT betting and 427 for OTC betting. While the difference between these two averages is greater in absolute terms than the discrepancy between the overall rates calculated by JP Morgan, it is in fact smaller in relative terms. The JP Morgan figures indicate that FOBT customers spend on average 4.4 times more on the machines than OTC customers do on their chosen product, whereas the GamblingData estimates outlined above suggest that regular FOBT customers spend on average 2.83 times more than their counterparts within the OTC horserace betting cohort. An Investec note from 2010 made the case for product crossover representing a key opportunity for retail operators, noting that quality shops should see good cross-sell from machines and football to horseracing since (racing) remains an excellent betting medium. The investment note went on to point out that the demographics using machines should widen when the cabinets have more diversified content and that machines were bringing in more customers than they were cannibalising. Participation method Most people who bet on horseracing and sports did it OTC however more people bet at the track on greyhounds than by any other method. Betting in person was the way most people bet on these activities but a significant chunk of participation in sports betting was through the online channel. When these numbers are converted to reflect the participation of the population at large, approximately 12 percent of the population bet on horseracing OTC, while 2 percent of bet OTC on greyhounds and 7 percent on sports. 15

16 Font: Palatino Roman Blue: From gamblingdata.com Logo revisions/options s A closer look Machines detail In each of the last nine half year-periods William Hill has increased its average machines per shop, with the metric standing at 3.86, marginally under the maximum of four, as of June Machine gross win margin has grown consistently too and now is at 3.30 percent, up from 2.90 percent in the first half of Gross win per machine week meanwhile grew to 924 in the first half of 2012, up from 901 in 2011 as a whole and 716 in Red: from gamblingcompliance.com This set shows the logos with the co Ladbrokes detailed in its 2012 interim report that it now also averages 3.86 machines per shop, generating average weekly gross win per machine of 947 in the first half of the year, and 970 in the second quarter. Coral is also outpacing William Hill in terms of this metric, having generated an average gross win per machine per week of 938 in the twelve weeks ended June 30, With each bookmaker s shop currently limited to a maximum of four machines the growth in machine density and gross win per machine per week is likely to be curtailed. Legislation allowing more machines could drive growth but analysts also believe that the roll-out of next generation models and content could provide a boost. William Hill conveyed in its interim report this year that it plans to be innovative in every area of its shops, stating: Self-service betting terminals are nearing the end of their trial phase in around 10 percent of the estate and video walls have been installed in 35 shops, giving customers a highend and differentiated viewing experience. OTC detail The product mix of OTC betting reveals that football is steadily becoming more important to the bookies. OTC wagers have fallen over the past three years for all products except football, though horseracing is still by far the most heavily bet on product with a 57.9 percent share of total betting volume via the medium in FY2011. Even though OTC horseracing wagers have fallen in each of the last two years, the product s share of OTC wagers has remained consistent. 16

17 Football generated more revenue per pound bet than all of the other OTC products in 2011 with a stand-out 26.6 percent gross gambling yield margin, aided partially by a favourable run of results but also by the enduring popularity of accumulator betting and the heavy promotion of scorecast combinations. It should be noted however, that football had a margin of only 16.6 percent in 2010, while the other products had margins very similar to their 2011 figures. Wide variations in margins, though often unavoidable in football betting, represent a negative for operators as bookmaking firms prefer steady margins so that they can make accurate forecasts of revenues. Threat from online On the surface neither William Hill s nor Ladbrokes retail business looks to have suffered from the rise of online gambling. William Hill s online business has experienced runaway growth over the last four years while its retail arm has held steady, and even improved in the last half year results. Ladbrokes has endured tougher times online, but in terms of its retail estate it has seen something of a rebound in its recent results because of a re-focusing of its machine content. However when looking at the retail breakdown, it is clear that the OTC revenue stream has declined steadily for the bookmakers with machines making up the difference. It could be the case that some OTC revenue has moved online but machines have still proved popular even though online equivalents are available. In total, 93 percent of retail customers still bet OTC and one of the oftcited attractions of going to the bookies is the television coverage of events and interaction with staff. In a note published in June this year analysts at JP Morgan wrote: The major UK race meetings are shown in every shop, through the SIS and Turf TV services, and the major bookmakers also provide their own commentary and tips. The gap between races provides a natural break in betting and the opportunity to consider future bets. 17

18 Red: from gamblingcompliance.com Font: Palatino Roman Blue: From gamblingdata.com Logo revisions/options s Analyst View Any overview of the recent analyst coverage of the UK retail market must necessarily focus on William Hill and Ladbrokes, given not only the pair s market-leader status, but also the fact that they are publicly listed on the London Stock Exchange and therefore covered by various UK-facing equity research teams. Gala Coral and Betfred/Tote currently comprise just over a third of the British market in terms of betting shops with a combined 3,070 but their status as privately-owned entities means that they tend to go under the radar of analysts covering the sector. As such, the following collection of analyst views on the UK retail space over the last two to three years will be limited entirely to William Hill and Ladbrokes. This set shows the logos with the co 2010 Much of the analyst discussion surrounding Ladbrokes and William Hill in 2010 centred on the debate over whether the pair s retail operations were exhibiting signs of being in a structural or even terminal decline. With prevailing concerns over consumer confidence, an increase in VAT and proposed welfare cuts serving to intensify investor fears over the retail performance of the two bookmaking giants, shares in Ladbrokes and William Hill fell 23 percent and 27 percent respectively from the start of April to the end of November. Credit Suisse, September 30, 2010 Searching For Growth In an investor note which played down the potential for a recovery in the retail OTC segment in 2011 after two years of 6-9 percent underlying (exmajor football tournament) declines in OTC wagers per shop, Matthew Gerard of Credit Suisse wrote: We expect sustained negative pressure on amounts wagered given the profile of retail betting customers, the impact of unemployment, recent government budget measures and uncertainty over racing content. Referencing the ongoing decline of OTC betting, Gerard stated: We estimate that wagers on horseracing, which contribute around 60 percent of OTC wagers and 50 percent of OTC gross win for William Hill and Ladbrokes, are currently declining at around 5 to 8 percent year-on-year, whilst underlying wagers (ex. major tournaments) on football are growing at 5 to 10 percent. With wagering on dog racing, the second largest OTC product for the betting operators, also in decline, growth in football betting is not compensating and like-for-like volumes are in decline. The Credit Suisse note was published following the news that the UK horserace betting levy had fallen for a second straight year, from 91.6m in the year to March 2009 to 75.4m in the year to March 2010; a factor which the analyst believed was acting as both a cause and a consequence of deteriorating OTC wagering activity on racing. Gerard wrote: The prospects for long term growth in slips volume, in our view, are dependent on a recovery in the racing product, which we think is highly unlikely. The UK racing industry is in danger of slipping into a vicious cycle, with declining wagers contributing to a declining levy (calculated as 10 percent of all bookmakers gross win generated from betting on racing in shops, over a certain profit threshold). This in turn leads to reduced prize money for owners and trainers, fewer runners per race, which reduces 18

19 the attractiveness of the product to retail betting customers, and lower wagering volumes. Exane BNP Paribas, October 1, 2010 The Substitution Effect In a bearish note which assessed the extent to which traditional retail betting and gaming businesses are structurally threatened by the online sector, analysts at BNP Paribas stated their opinion that, while OTC revenue generally follows the trends of national GDP, the substitution of activity from offline to online would serve to cause additional pressure to the sector looking forward. Lead analyst Roberta Ciaccia stated: We expect substitution to be driven mainly by demographic trends, given the higher average age of customers in retail versus online (60 percent of clients in the retail business are aged over 45, while the majority of online players are in the age bracket). We believe that the social component of land-based betting in the UK will ensure that the working class, currently accounting for around 70 percent of the OTC customer base, should mostly continue to enjoy the shop betting experience, while the middle class should progressively shift to online. While steering clear of citing a role for gaming machines in the cannibalisation of OTC wagering activity, Ciaccia wrote of the segment s increasing outperformance: Gaming machines wagers, and hence revenue for operators, have grown at a significantly faster pace than pure OTC, thanks to continuous innovation in hardware, contents and array of games. For the future, we believe that this segment should continue to outperform OTC within the retail business, as it appeals in general to a younger audience and can still benefit from strong content innovation. Investec, October 22, 2010 Adding Primary Colour In a wide-reaching note covering the entire UK gambling sector, analysts at Investec struck a slightly more optimistic tone with regard to the future for UK retail betting, telling followers that the emergence of operational improvements should serve to mitigate cyclical economic downside risk and drive long-term growth for the land-based sector. Lead analyst Paul Leyland argued that it is unhelpful to think of all betting shops as suffering from the same challenges and flagged his expectation of a divergence in fortunes for modern or primary shops and old-fashion or tertiary locations. Leyland wrote: We believe the key to understanding betting shops is to segment those that remain traditional horseracing-led haunts in postindustrial locations (between the closed factory and the repossessed pub) and the new high street offer which is effectively able to capitalise on football and machine spend. With William Hill s UK retail estate estimated to comprise 54 percent primary shops at the time of the note s publication versus 40 percent for Ladbrokes, 100 percent for Paddy Power and zero percent for Tote, the analyst continued: We see an increasing discrepancy between high-quality, modern shops in good location and old-fashion shops with poor (tertiary) locations and size leading to difficult demographics and a limited offer. 19

20 We do see tertiary shops in terminal decline, though we believe modern shops should continue to regenerate and grow. We therefore see estate mix as a highly important driver of betting shop growth vs. decline. While labelling football betting as a big differentiator for good quality shops that should continue to grow in revenue terms partly due to latent popularity, and partly because it suits more innovative bets, Leyland noted: We assume horseracing will continue to decline, though we make two important positive qualifications: quality shops should see good cross-sell since it remains an excellent betting medium, and there is always a role for good quality meetings. Significantly, with regard to the impact of FOBTs in betting shops, Leyland asserted that machines are probably bringing in customers more than they are cannibalising and this should accelerate. J.P. Morgan, October 26, 2010 Tough Times Ahead The UK-facing equity research team at JP Morgan initiated coverage on Ladbrokes and William Hill with a negative stance on retail betting, positing that the firms UK shops would be loss-making without the contribution from machines. Speaking of a slow structural decline in retail betting, the analysts stated their belief that OTC margins and volumes would continue to fall due to customers being swayed by the more attractive pricing, the ease to place bets anytime anywhere from increasingly sophisticated mobile phones and the greater product choice of online betting. In addition to outlining the competition from online offerings, the JP Morgan contrasted a stagnating OTC performance with ever more healthy machine figures within retail shops, speculating that retail at both Ladbrokes and William Hill would be loss-making without the operating profit from machines. Analyst Richard Stuber wrote: In 2009 for example, operating profit per shop at Ladbrokes was 64.4k with machines contributing an estimated 102.6k. William Hill was similarly dependent on machines with operating profit per shop of 87k and machines contributing 111.2k. Playing down the perceived benefits of anonymity, cash and community associated with OTC, Stuber expressed pessimism on the long-term attractiveness of the horseracing industry and, given its share of around 60 percent of OTC amounts wagered at Ladbrokes and William Hill, the disproportionate impact it may have on OTC volumes. Stuber explained: We believe that the British horseracing industry is in difficulty, reliant on the bookmakers circa 160m a year contribution through a combination of a horseracing levy (10 percent of gross win), selling content rights (Turf TV) and sponsorship. With its cost base increasing but contributions from the levy falling (in proportion with lower gross win) we struggle to see how the horseracing industry will survive without a major shake-up and potential course closures. The horseracing may need the bookmakers but the bookmakers still need horseracing. 20

THE HOME OF BETTING William Hill PLC corporate presentation September 2015

THE HOME OF BETTING William Hill PLC corporate presentation September 2015 1 Disclaimer This presentation has been prepared by William Hill PLC ( William Hill ). This presentation includes statements that

THE HOME OF BETTING William Hill PLC corporate presentation September 2015 1 Disclaimer This presentation has been prepared by William Hill PLC ( William Hill ). This presentation includes statements that

Agenda. UK Horseracing wagering performance - what are the latest trends? Funding, Levy, Prize Money. Options to improve UK racing revenues

Agenda UK Horseracing wagering performance - what are the latest trends? Funding, Levy, Prize Money Options to improve UK racing revenues 1) The Racing Right 2) Authorised Betting Partner 3) Latest media

Agenda UK Horseracing wagering performance - what are the latest trends? Funding, Levy, Prize Money Options to improve UK racing revenues 1) The Racing Right 2) Authorised Betting Partner 3) Latest media

The evolution of Sports Betting: factors impacting the change on betting focus on British markets

The evolution of Sports Betting: factors impacting the change on betting focus on British markets Dominic Atkinson Commercial Director at Tailorbet Limited Agenda Pre-requisite overview: What is sports

The evolution of Sports Betting: factors impacting the change on betting focus on British markets Dominic Atkinson Commercial Director at Tailorbet Limited Agenda Pre-requisite overview: What is sports

Q3 2015: TRADING IN LINE WITH OUR EXPECTATIONS STRATEGY IMPLEMENTATION UNDERWAY

LADBROKES PLC ( Ladbrokes or the Group ) 22 October 2015 Q3 2015: TRADING IN LINE WITH OUR EXPECTATIONS STRATEGY IMPLEMENTATION UNDERWAY Ladbrokes plc (LSE:LAD) announces its trading update for the three

LADBROKES PLC ( Ladbrokes or the Group ) 22 October 2015 Q3 2015: TRADING IN LINE WITH OUR EXPECTATIONS STRATEGY IMPLEMENTATION UNDERWAY Ladbrokes plc (LSE:LAD) announces its trading update for the three

Racing in the Modern Wagering World. Nigel Roddis December 2007

Racing in the Modern Wagering World Nigel Roddis December 2007 Agenda At The Races New Wagering Opportunities Content Bet Types Technology Summary What Does ATR Do? At The Races is the UK and Ireland s

Racing in the Modern Wagering World Nigel Roddis December 2007 Agenda At The Races New Wagering Opportunities Content Bet Types Technology Summary What Does ATR Do? At The Races is the UK and Ireland s

Strong Online and Multichannel Growth. 567k first time depositors, up 28% on last year, with Coral Connect sign-ups now over 210k

HALF YEAR RESULTS TWENTY EIGHT WEEKS ENDED 11 APRIL 2015 Strong Online and Multichannel Growth HIGHLIGHTS Total Group EBITDA {1/2} 12.2m or 10% ahead of last year After adjusting for regulatory impacts

HALF YEAR RESULTS TWENTY EIGHT WEEKS ENDED 11 APRIL 2015 Strong Online and Multichannel Growth HIGHLIGHTS Total Group EBITDA {1/2} 12.2m or 10% ahead of last year After adjusting for regulatory impacts

LOGO. Racing s Lifeblood The Future Landscape for Wagering

LOGO Racing s Lifeblood The Future Landscape for Wagering LOGO Racing s Lifeblood The Future Landscape for Wagering Speaker: Research Consultant, Aspire Wealth Management Pty Limited The Future Landscape

LOGO Racing s Lifeblood The Future Landscape for Wagering LOGO Racing s Lifeblood The Future Landscape for Wagering Speaker: Research Consultant, Aspire Wealth Management Pty Limited The Future Landscape

The Economic Impact of Fixed Odds Betting Terminals

Landman Economics The Economic Impact of Fixed Odds Betting Terminals A report by Howard Reed (Director, Landman Economics) April 2013 1 Contents Executive Summary... 3 Introduction... 5 1 The shift from

Landman Economics The Economic Impact of Fixed Odds Betting Terminals A report by Howard Reed (Director, Landman Economics) April 2013 1 Contents Executive Summary... 3 Introduction... 5 1 The shift from

The National Business Survey National Report November 2009 Results

The National Business Survey National Report November 2009 Results 1 Executive Summary (1) 2 NBS results from November 2009 demonstrate the continued challenging conditions faced by businesses in England

The National Business Survey National Report November 2009 Results 1 Executive Summary (1) 2 NBS results from November 2009 demonstrate the continued challenging conditions faced by businesses in England

We would be happy to contribute proportionally towards a further prevalence study.

Inspired Gaming Group s response to the DCMS consultation Gambling Act 2005: Triennial Review of Gaming Machine Stake and Prize Limits - Proposals for Changes to Maximum Stake and Prize Limits for Category

Inspired Gaming Group s response to the DCMS consultation Gambling Act 2005: Triennial Review of Gaming Machine Stake and Prize Limits - Proposals for Changes to Maximum Stake and Prize Limits for Category

Fixed Odds Betting Terminals and the Code of Practice. A report for the Association of British Bookmakers Limited SUMMARY ONLY

Fixed Odds Betting Terminals and the Code of Practice A report for the Association of British Bookmakers Limited SUMMARY ONLY Europe Economics Chancery House 53-64 Chancery Lane London WC2A 1QU Tel: (+44)

Fixed Odds Betting Terminals and the Code of Practice A report for the Association of British Bookmakers Limited SUMMARY ONLY Europe Economics Chancery House 53-64 Chancery Lane London WC2A 1QU Tel: (+44)

Indicators of betting as primary gambling activity

Indicators of betting as primary gambling activity Advice note, October 2013 1. Introduction 1.1 The Gambling Commission s (the Commission) interpretation of the framework of the Gambling Act 2005 (the

Indicators of betting as primary gambling activity Advice note, October 2013 1. Introduction 1.1 The Gambling Commission s (the Commission) interpretation of the framework of the Gambling Act 2005 (the

LADBROKES/CORAL MERGER INQUIRY. Summary of hearing with Paddy Power Betfair on 25 February 2016

LADBROKES/CORAL MERGER INQUIRY Summary of hearing with Paddy Power Betfair on 25 February 2016 Background 1. Paddy Power Betfair (PPB) said that it was a multichannel betting and gaming business and that

LADBROKES/CORAL MERGER INQUIRY Summary of hearing with Paddy Power Betfair on 25 February 2016 Background 1. Paddy Power Betfair (PPB) said that it was a multichannel betting and gaming business and that

Gambling Commission. Trends in Gambling Behaviour 2008-2014

Gambling Commission Trends in Gambling Behaviour 2008-2014 Report Name Prepared for Authors Project team Trends in Gambling Behaviour 2008-2014 Gambling Commission Doros Georgiou Karl King Adrian Talbot

Gambling Commission Trends in Gambling Behaviour 2008-2014 Report Name Prepared for Authors Project team Trends in Gambling Behaviour 2008-2014 Gambling Commission Doros Georgiou Karl King Adrian Talbot

How To Understand The History Of Betting In The Uk

BETTING AND THE RACING INDUSTRY ROSS HAMILTON EXTERNAL AFFAIRS OFFICER Overview of British Racing Seminar, Newmarket, 30 September 2015 THE HISTORY OF BRITISH BETTING 1928 Racecourse Betting Act 1961 UK

BETTING AND THE RACING INDUSTRY ROSS HAMILTON EXTERNAL AFFAIRS OFFICER Overview of British Racing Seminar, Newmarket, 30 September 2015 THE HISTORY OF BRITISH BETTING 1928 Racecourse Betting Act 1961 UK

Betting on the Athens Olympic Games

Betting on the Athens Olympic Games An Interim report based on the first 10 days of competition Our research has shown that the amount of betting on the Olympics is now quite staggering and that all events

Betting on the Athens Olympic Games An Interim report based on the first 10 days of competition Our research has shown that the amount of betting on the Olympics is now quite staggering and that all events

Report: February 2015 Released: March 2015

Report: February 2015 Released: March 2015 GB LEISURE IN FEBRUARY 2015 - COMMENT February s spending patterns largely mirrored those seen in January, as Eating Out saw considerable growth, Drinking Out

Report: February 2015 Released: March 2015 GB LEISURE IN FEBRUARY 2015 - COMMENT February s spending patterns largely mirrored those seen in January, as Eating Out saw considerable growth, Drinking Out

Introduction. Financial Performance. Divisional Review. Outlook

1 Introduction Financial Performance Divisional Review Outlook Page 2 Highlights Record operating profit, up 14% to 56.2m 81% of profits from internet and mobile 20% increase in interim dividend Second

1 Introduction Financial Performance Divisional Review Outlook Page 2 Highlights Record operating profit, up 14% to 56.2m 81% of profits from internet and mobile 20% increase in interim dividend Second

Questions raised by deputations

LC Paper No. CB(2)2674/04-05(02) I Questions raised by deputations (1)(a) The Hong Kong Jockey Club (HKJC) has made an assessment of the illegal betting market on the basis of a combination of internal

LC Paper No. CB(2)2674/04-05(02) I Questions raised by deputations (1)(a) The Hong Kong Jockey Club (HKJC) has made an assessment of the illegal betting market on the basis of a combination of internal

First phase of our new poker product, new social sports betting product and new bingo product are all expected to launch as planned

21 May 2013 bwin.party digital entertainment plc Interim Management Statement and Q1 2013 Key Performance Indicators Clean EBITDA in the first quarter was in line with the Board s expectations due to cost

21 May 2013 bwin.party digital entertainment plc Interim Management Statement and Q1 2013 Key Performance Indicators Clean EBITDA in the first quarter was in line with the Board s expectations due to cost

GALA CORAL GROUP RESULTS FOR THE 16 WEEKS ENDED 18 JANUARY 2014

GALA CORAL GROUP RESULTS FOR THE 16 WEEKS ENDED 18 JANUARY 2014 KEY FINANCIALS Quarter 1 FY14 m FY13 m Change) %) Continuing Opco Turnover {1} 356.1 318.3 12%) Continuing Opco Gross Profit {1} 255.1 241.3

GALA CORAL GROUP RESULTS FOR THE 16 WEEKS ENDED 18 JANUARY 2014 KEY FINANCIALS Quarter 1 FY14 m FY13 m Change) %) Continuing Opco Turnover {1} 356.1 318.3 12%) Continuing Opco Gross Profit {1} 255.1 241.3

HOW TO BET ON GREYHOUNDS. Gambling can be addictive. Please play responsibly. http://responsiblegambling.betfair.com

HOW TO BET ON GREYHOUNDS Gambling can be addictive. Please play responsibly. http://responsiblegambling.betfair.com Greyhound racing in the UK takes place every single day (except Christmas Day). The first

HOW TO BET ON GREYHOUNDS Gambling can be addictive. Please play responsibly. http://responsiblegambling.betfair.com Greyhound racing in the UK takes place every single day (except Christmas Day). The first

Strong underlying growth but football results impact margins

Q1 results announcement for the 13 weeks ended 1 April 2014 25 April 2014 Strong underlying growth but football results impact margins Key highlights Continued outstanding growth in Online Sportsbook turnover,

Q1 results announcement for the 13 weeks ended 1 April 2014 25 April 2014 Strong underlying growth but football results impact margins Key highlights Continued outstanding growth in Online Sportsbook turnover,

ARLA Members Survey of the Private Rented Sector

Prepared for The Association of Residential Letting Agents ARLA Members Survey of the Private Rented Sector Fourth Quarter 2013 Prepared by: O M Carey Jones 5 Henshaw Lane Yeadon Leeds LS19 7RW December,

Prepared for The Association of Residential Letting Agents ARLA Members Survey of the Private Rented Sector Fourth Quarter 2013 Prepared by: O M Carey Jones 5 Henshaw Lane Yeadon Leeds LS19 7RW December,

July 2014. UK Commercial & Residential Property Markets Review: July 2014 1

July 2014 UK Commercial & Residential Property Markets Review: July 2014 1 UK Commercial & Residential Property Markets Review: July 2014 2 UK COMMERCIAL & RESIDENTIAL PROPERTY MARKETS REVIEW: JULY 2014

July 2014 UK Commercial & Residential Property Markets Review: July 2014 1 UK Commercial & Residential Property Markets Review: July 2014 2 UK COMMERCIAL & RESIDENTIAL PROPERTY MARKETS REVIEW: JULY 2014

FOR THE SIXTEEN WEEKS ENDED 17 JANUARY 2015. Strong Online and Multichannel Growth

FINANCIAL RESULTS FOR THE SIXTEEN WEEKS ENDED 17 JANUARY 2015 Strong Online and Multichannel Growth HIGHLIGHTS Total Group Opco EBITDA {1/2} 6.8m or 11% ahead of last year Online EBITDA {1} 19% ahead (53%

FINANCIAL RESULTS FOR THE SIXTEEN WEEKS ENDED 17 JANUARY 2015 Strong Online and Multichannel Growth HIGHLIGHTS Total Group Opco EBITDA {1/2} 6.8m or 11% ahead of last year Online EBITDA {1} 19% ahead (53%

Renminbi Depreciation and the Hong Kong Economy

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Renminbi Depreciation and the Hong Kong Economy If the recent weakness of the renminbi persists, it is likely to have a positive direct impact

Thomas Shik Acting Chief Economist thomasshik@hangseng.com Renminbi Depreciation and the Hong Kong Economy If the recent weakness of the renminbi persists, it is likely to have a positive direct impact

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Successful value investing: the long term approach

Successful value investing: the long term approach Neil Walton, Head of Global Strategic Solutions, Schroders Do you have the patience to be a value investor? The long-term outperformance of a value investment

Successful value investing: the long term approach Neil Walton, Head of Global Strategic Solutions, Schroders Do you have the patience to be a value investor? The long-term outperformance of a value investment

RICS Global Commercial Property Monitor Q4 2014

Simon Rubinsohn Chief Economist srubinsohn@rics.org +44 (0)207334 3774 RICS ECONOMICS RICS Global Commercial Property Monitor Q4 2014 * RICS Occupier Sentiment Index (OSI) is constructed by taking an unweighted

Simon Rubinsohn Chief Economist srubinsohn@rics.org +44 (0)207334 3774 RICS ECONOMICS RICS Global Commercial Property Monitor Q4 2014 * RICS Occupier Sentiment Index (OSI) is constructed by taking an unweighted

EXECUTIVE SUMMARY... 3 RETAIL BETTING OVERVIEW... 4 SECTOR EMPLOYMENT... 5 TURNOVER LEVELS... 5 SHOP NUMBERS... 6 TAXATION CONTRIBUTION...

Betting Industry EXECUTIVE SUMMARY... 3 RETAIL BETTING OVERVIEW... 4 SECTOR EMPLOYMENT... 5 TURNOVER LEVELS... 5 SHOP NUMBERS... 6 TAXATION CONTRIBUTION... 6 Average contribution to Exchequer... 7 PAYMENTS

Betting Industry EXECUTIVE SUMMARY... 3 RETAIL BETTING OVERVIEW... 4 SECTOR EMPLOYMENT... 5 TURNOVER LEVELS... 5 SHOP NUMBERS... 6 TAXATION CONTRIBUTION... 6 Average contribution to Exchequer... 7 PAYMENTS

WILLIAM HILL PLC ANALYST AND INVESTOR EVENT THE JOURNEY OF A BET 4 OCTOBER 2013

WILLIAM HILL PLC ANALYST AND INVESTOR EVENT THE JOURNEY OF A BET 4 OCTOBER 2013 1 THE JOURNEY OF A BET Introduction Andrew Lee Managing Director, Online Product and pricing Matthew Warner Director of Sportsbook

WILLIAM HILL PLC ANALYST AND INVESTOR EVENT THE JOURNEY OF A BET 4 OCTOBER 2013 1 THE JOURNEY OF A BET Introduction Andrew Lee Managing Director, Online Product and pricing Matthew Warner Director of Sportsbook

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Carat forecasts growth of 5.0% for 2012 and 5.3% in 2013 with digital advertising overtaking newspapers sooner than expected

23 August 2012 Carat forecasts growth of 5.0% for 2012 and 5.3% in 2013 with digital advertising overtaking newspapers sooner than expected Carat, the world s leading independent media communications agency,

23 August 2012 Carat forecasts growth of 5.0% for 2012 and 5.3% in 2013 with digital advertising overtaking newspapers sooner than expected Carat, the world s leading independent media communications agency,

Insurance market outlook

Munich Re Economic Research 2 May 2013 Global economic recovery provides stimulus to the insurance industry long-term perspective positive as well Once a year, MR Economic Research produces long-term forecasts

Munich Re Economic Research 2 May 2013 Global economic recovery provides stimulus to the insurance industry long-term perspective positive as well Once a year, MR Economic Research produces long-term forecasts

COMMERCIAL LEASE TRENDS FOR 2014

COMMERCIAL LEASE TRENDS FOR 2014 Notes from a Presentation given by N B Maunder Taylor BSc (Hons) MRICS, Partner of Maunder Taylor The following is a written copy of the presentation given by Nicholas

COMMERCIAL LEASE TRENDS FOR 2014 Notes from a Presentation given by N B Maunder Taylor BSc (Hons) MRICS, Partner of Maunder Taylor The following is a written copy of the presentation given by Nicholas

Analyzing the Global Online Gambling Industry

Brochure More information from http://www.researchandmarkets.com/reports/2422644/ Analyzing the Global Online Gambling Industry Description: The global online gambling industry is one of the biggest and

Brochure More information from http://www.researchandmarkets.com/reports/2422644/ Analyzing the Global Online Gambling Industry Description: The global online gambling industry is one of the biggest and

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

The Future of the Scottish Horseracing Sector

The Future of the Scottish Horseracing Sector on Paper September 2014 BiGGAR Economics Midlothian Innovation Centre Pentlandfield, Roslin Midlothian, EH25 9RE Scotland 0131 440 9032 info@biggareconomics.co.uk

The Future of the Scottish Horseracing Sector on Paper September 2014 BiGGAR Economics Midlothian Innovation Centre Pentlandfield, Roslin Midlothian, EH25 9RE Scotland 0131 440 9032 info@biggareconomics.co.uk

The Consumer Holiday Trends Report. ABTA Consumer Survey 2013

The Consumer Holiday Trends Report ABTA Consumer Survey 2013 Number of holidays taken Despite market challenges, British holidaymakers continue to value their holidays with eight in ten 83% taking a holiday

The Consumer Holiday Trends Report ABTA Consumer Survey 2013 Number of holidays taken Despite market challenges, British holidaymakers continue to value their holidays with eight in ten 83% taking a holiday

Transforming Innovating Performing. William Hill analyst and investor day, Leeds Thursday, 22 September 2011

Transforming Innovating Performing William Hill analyst and investor day, Leeds Thursday, 22 September 2011 1 AGENDA 8.40 am Presentations Overview Creating the right product Technology in Retail Innovation

Transforming Innovating Performing William Hill analyst and investor day, Leeds Thursday, 22 September 2011 1 AGENDA 8.40 am Presentations Overview Creating the right product Technology in Retail Innovation

TABLE OF CONTENTS. 1. Lottery and Gambling Industry Overview. 1.1. International Gambling. 1.2. Global Betting, Gambling and Gaming Industry

1 TABLE OF CONTENTS 1. Lottery and Gambling Industry Overview 1.1. International Gambling 1.2. Global Betting, Gambling and Gaming Industry 1.3. Global Online Gaming Market 1.4. Types of Gamblers 2. Europe

1 TABLE OF CONTENTS 1. Lottery and Gambling Industry Overview 1.1. International Gambling 1.2. Global Betting, Gambling and Gaming Industry 1.3. Global Online Gaming Market 1.4. Types of Gamblers 2. Europe

Gambling Market in UK 2015-2019

Brochure More information from http://www.researchandmarkets.com/reports/3330571/ Gambling Market in UK 2015-2019 Description: About Gambling Gambling premises include betting shops for betting on activities

Brochure More information from http://www.researchandmarkets.com/reports/3330571/ Gambling Market in UK 2015-2019 Description: About Gambling Gambling premises include betting shops for betting on activities

Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

August 2014 Gauging Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook for factors that typically impact

TABLE OF CONTENTS. 1. Lottery and Gambling Industry Overview. 1.1. International Gambling. 1.2. Global Betting, Gambling and Gaming Industry

1 TABLE OF CONTENTS 1. Lottery and Gambling Industry Overview 1.1. International Gambling 1.2. Global Betting, Gambling and Gaming Industry 1.3. Global Online Gaming Market 1.4. Types of Gamblers 2. Europe

1 TABLE OF CONTENTS 1. Lottery and Gambling Industry Overview 1.1. International Gambling 1.2. Global Betting, Gambling and Gaming Industry 1.3. Global Online Gaming Market 1.4. Types of Gamblers 2. Europe

Economic Review, April 2012

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

BizBuySell.com Small Business Buyer & Seller Demographic Study

BizBuySell.com Small Business Buyer & Seller Demographic Study Table of Contents Report Executive Summary Younger, More Diverse Buyers Look to Acquire Retiring Baby Boomer Businesses Female Business Buyers

BizBuySell.com Small Business Buyer & Seller Demographic Study Table of Contents Report Executive Summary Younger, More Diverse Buyers Look to Acquire Retiring Baby Boomer Businesses Female Business Buyers

RICS Global Commercial Property Monitor Q3 2014

Simon Rubinsohn Chief Economist srubinsohn@rics.org +44 (0)207334 3774 RICS ECONOMICS RICS Global Commercial Property Monitor Q3 2014 * RICS Occupier Sentiment Index (OSI) is constructed by taking an unweighted

Simon Rubinsohn Chief Economist srubinsohn@rics.org +44 (0)207334 3774 RICS ECONOMICS RICS Global Commercial Property Monitor Q3 2014 * RICS Occupier Sentiment Index (OSI) is constructed by taking an unweighted

/EXPERT INSIGHT INTO THE WORLD OF OFFSHORE COMPANY INCORPORATIONS/

FIRST HALF, 2013 /EXPERT INSIGHT INTO THE WORLD OF OFFSHORE COMPANY INCORPORATIONS/ CONTENTS/ EXECUTIVE SUMMARY [2] THE COMPANY FORMATION ENVIRONMENT [4] GEOGRAPHIC TRENDS [6] 2 EXECUTIVE SUMMARY Welcome

FIRST HALF, 2013 /EXPERT INSIGHT INTO THE WORLD OF OFFSHORE COMPANY INCORPORATIONS/ CONTENTS/ EXECUTIVE SUMMARY [2] THE COMPANY FORMATION ENVIRONMENT [4] GEOGRAPHIC TRENDS [6] 2 EXECUTIVE SUMMARY Welcome

Executive summary. Participation in gambling activities (Chapter 2)

") Executive summary This report presents results from the British Gambling Prevalence Survey (BGPS) 2010. This is the third nationally representative survey of its kind; previous studies were conducted in

Executive summary This report presents results from the British Gambling Prevalence Survey (BGPS) 2010. This is the third nationally representative survey of its kind; previous studies were conducted in

Statement to Parliamentary Committee

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Industry sentiment. Financial Services Survey. www.pwc.co.uk/financialservicessurvey

www.pwc.co.uk/financialservicessurvey CBI/PwC quarterly survey measuring trends and providing insight from the industry Industry sentiment Financial Services Survey Issue number 87 June 2011 The 87th CBI/PwC

www.pwc.co.uk/financialservicessurvey CBI/PwC quarterly survey measuring trends and providing insight from the industry Industry sentiment Financial Services Survey Issue number 87 June 2011 The 87th CBI/PwC

The Search for Yield Continues: A Re-introduction to Bank Loans

INSIGHTS The Search for Yield Continues: A Re-introduction to Bank Loans 203.621.1700 2013, Rocaton Investment Advisors, LLC Executive Summary With the Federal Reserve pledging to stick to its zero interest-rate

INSIGHTS The Search for Yield Continues: A Re-introduction to Bank Loans 203.621.1700 2013, Rocaton Investment Advisors, LLC Executive Summary With the Federal Reserve pledging to stick to its zero interest-rate

Quarterly analysis of the online games market in France

1 31 March 2012 Quarterly analysis of the online games market in France 1 st quarter 2012 2 Summary of activity data The findings below are based on the data that accredited online betting and gaming operators

1 31 March 2012 Quarterly analysis of the online games market in France 1 st quarter 2012 2 Summary of activity data The findings below are based on the data that accredited online betting and gaming operators

INTERIM RESULTS HALF YEAR ENDED 30 JUNE 2013

INTERIM RESULTS HALF YEAR ENDED 30 JUNE 2013 OVERVIEW Results impacted by... Slower machine growth than expected, recent performance volatile MGD and content costs circa 9m in H1 Retail expansion remains

INTERIM RESULTS HALF YEAR ENDED 30 JUNE 2013 OVERVIEW Results impacted by... Slower machine growth than expected, recent performance volatile MGD and content costs circa 9m in H1 Retail expansion remains

Executive Summary. 3 Attracting ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Visa Small Business REPORT AUGUST 0 Spend Insights Visa Small Business Spend Insights monitors the economic confidence of U.S. small business owners by analyzing Visa Business card spend data and responses

Visa Small Business REPORT AUGUST 0 Spend Insights Visa Small Business Spend Insights monitors the economic confidence of U.S. small business owners by analyzing Visa Business card spend data and responses

England Attractions Monitor

England Attractions Monitor Quarter 1 Report January to March 2009 Prepared for by 1. INTRODUCTION In January 2006, VisitBritain commissioned BDRC to launch and manage the England Attractions Monitor,

England Attractions Monitor Quarter 1 Report January to March 2009 Prepared for by 1. INTRODUCTION In January 2006, VisitBritain commissioned BDRC to launch and manage the England Attractions Monitor,

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

Fortuna Entertainment Group NV

Fortuna Entertainment Group NV Investor Presentation October 2012 WILFRED WALSH Fortuna Entertainment Group NV Chairman of the Management Board Wilf Walsh acts as Chairman of the Management Board. In 2009,

Fortuna Entertainment Group NV Investor Presentation October 2012 WILFRED WALSH Fortuna Entertainment Group NV Chairman of the Management Board Wilf Walsh acts as Chairman of the Management Board. In 2009,

50 th Horserace Betting Levy Scheme. Submission of British Horseracing

50 th Horserace Betting Levy Scheme Submission of British Horseracing March 2010 CONTENTS This submission is made by all constituents of British Horseracing ( Racing ) as represented by the Horsemen s

50 th Horserace Betting Levy Scheme Submission of British Horseracing March 2010 CONTENTS This submission is made by all constituents of British Horseracing ( Racing ) as represented by the Horsemen s

TABLE OF CONTENTS. Source of all statistics:

TABLE OF CONTENTS Executive Summary 2 Internet Usage 3 Mobile Internet 6 Advertising Spend 7 Internet Advertising 8 Display Advertising 9 Online Videos 10 Social Media 12 About WSI 14 Source of all statistics:

TABLE OF CONTENTS Executive Summary 2 Internet Usage 3 Mobile Internet 6 Advertising Spend 7 Internet Advertising 8 Display Advertising 9 Online Videos 10 Social Media 12 About WSI 14 Source of all statistics:

Contents Foreword 1 Introduction by Patrick Reeve Executive summary 1. Business confidence and growth ambitions 2. Availability of finance

2014 Contents Foreword 1 Introduction by Patrick Reeve 3 Executive summary 4 1. Business confidence and growth ambitions 4 2. Availability of finance 6 3. Management skills 8 4. Apprenticeships 9 5. Optimists

2014 Contents Foreword 1 Introduction by Patrick Reeve 3 Executive summary 4 1. Business confidence and growth ambitions 4 2. Availability of finance 6 3. Management skills 8 4. Apprenticeships 9 5. Optimists

Why own bonds when yields are low?

Why own bonds when yields are low? Vanguard research November 213 Executive summary. Given the backdrop of low yields in government bond markets across much of the developed world, many investors may be

Why own bonds when yields are low? Vanguard research November 213 Executive summary. Given the backdrop of low yields in government bond markets across much of the developed world, many investors may be

Summary Translation of Question & Answer Session at FY 2012 First Quarter Financial Results Briefing for Analysts

Summary Translation of Question & Answer Session at FY 2012 First Quarter Financial Results Briefing for Analysts Date: July 27, 2012 Location: Fujitsu Headquarters, Tokyo Presenters: Kazuhiko Kato, Corporate

Summary Translation of Question & Answer Session at FY 2012 First Quarter Financial Results Briefing for Analysts Date: July 27, 2012 Location: Fujitsu Headquarters, Tokyo Presenters: Kazuhiko Kato, Corporate

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

Scottish Independence. Charting the implications of demographic change. Ben Franklin. I May 2014 I. www.ilc.org.uk

Scottish Independence Charting the implications of demographic change Ben Franklin I May 2014 I www.ilc.org.uk Summary By 2037 Scotland s working age population is expected to be 3.5% than it was in 2013

Scottish Independence Charting the implications of demographic change Ben Franklin I May 2014 I www.ilc.org.uk Summary By 2037 Scotland s working age population is expected to be 3.5% than it was in 2013

PIVOTAL. U.S. Equity Research Internet / Advertising. Pivotal Research Group

PIVOTAL Pivotal Research Group U.S. Equity Research Internet / Advertising Nielsen Data: TV Dominates Time, Other Media Grows March 5, 2014 BOTTOM LINE: Nielsen published its "Cross-Platform" report for

PIVOTAL Pivotal Research Group U.S. Equity Research Internet / Advertising Nielsen Data: TV Dominates Time, Other Media Grows March 5, 2014 BOTTOM LINE: Nielsen published its "Cross-Platform" report for

The self-employed and pensions

BRIEFING The self-employed and pensions Conor D Arcy May 2015 resolutionfoundation.org info@resolutionfoundation.org +44 (0)203 372 2960 The self-employed and pensions 2 The UK s self-employed populace

BRIEFING The self-employed and pensions Conor D Arcy May 2015 resolutionfoundation.org info@resolutionfoundation.org +44 (0)203 372 2960 The self-employed and pensions 2 The UK s self-employed populace

THE BOSS. The Betting One Stop Shop

THE BOSS The Betting One Stop Shop Strictly Private & Confidential This document has been prepared by Brontide Innovations Ltd (BIL) and is being provided to a limited number of persons solely as a guide

THE BOSS The Betting One Stop Shop Strictly Private & Confidential This document has been prepared by Brontide Innovations Ltd (BIL) and is being provided to a limited number of persons solely as a guide

Press release: UK adspend forecasts lift after strong Q1, improving economy and World Cup

Press release: UK adspend forecasts lift after strong Q1, improving economy and World Cup Embargoed until 00:01am, Tuesday 8 th July 2014 London, 8 th July 2014: Strong performances for TV and Radio in

Press release: UK adspend forecasts lift after strong Q1, improving economy and World Cup Embargoed until 00:01am, Tuesday 8 th July 2014 London, 8 th July 2014: Strong performances for TV and Radio in

The future of charitable donations

The future of charitable donations Contents 3 Introduction 4 Section one: How are donations being made? 5 Who are donations coming from? 6 Assessing the digital preferences of donors 7 Section two: Breaking

The future of charitable donations Contents 3 Introduction 4 Section one: How are donations being made? 5 Who are donations coming from? 6 Assessing the digital preferences of donors 7 Section two: Breaking

Commercial Property Newsletter