Minority Business Loan Mobilization Program Rules

|

|

|

- Anne Gibson

- 9 years ago

- Views:

Transcription

1

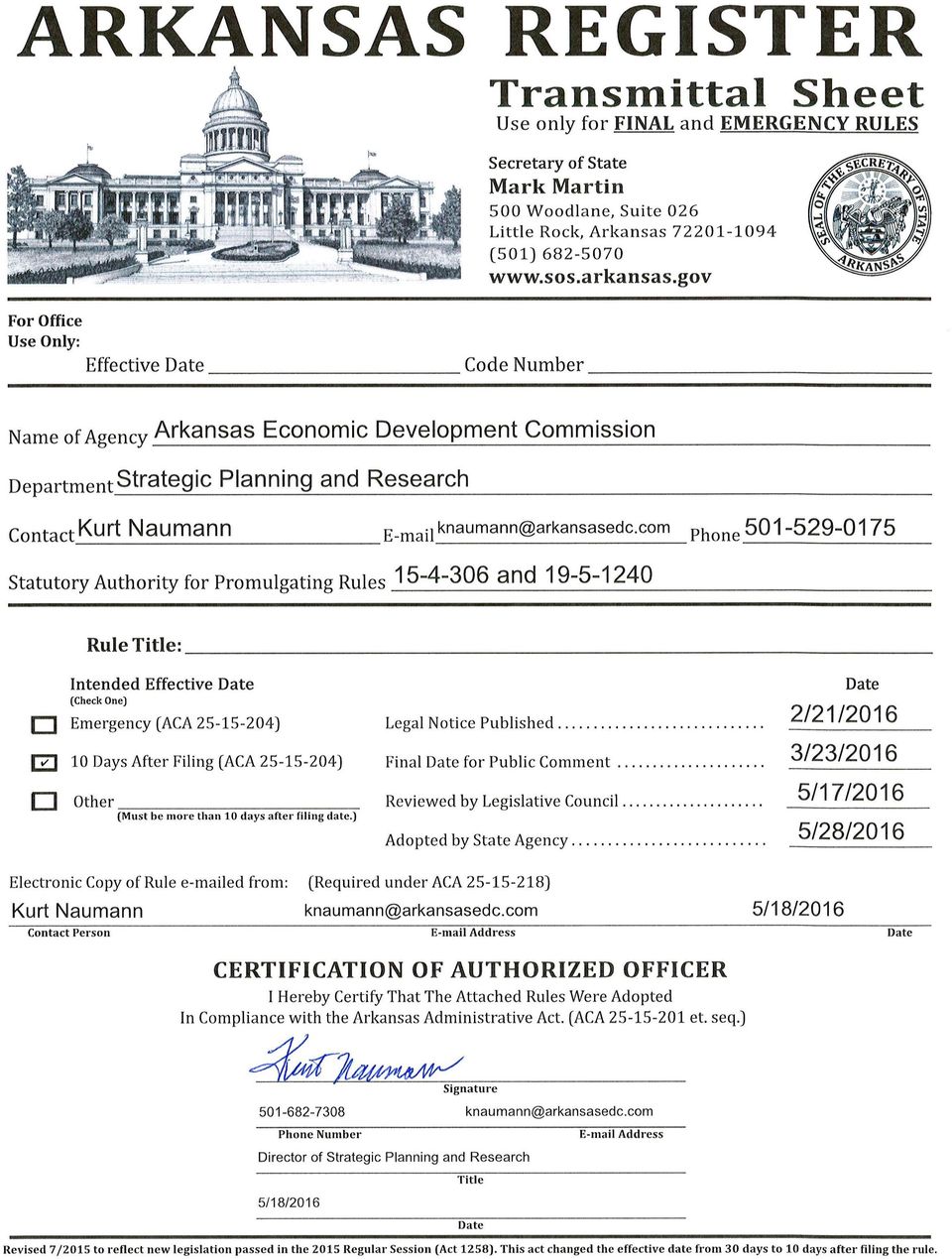

2 Minority Business Loan Mobilization Program Rules I. Introduction Overview Pursuant to authority granted under of the Minority Business Economic Development Act and , which established the Minority Business Loan Mobilization Revolving Fund, the Small and Minority Business Division of the Arkansas Economic Development Commission (AEDC) has established a Minority Business Loan Mobilization Program that may guarantee loans that: 1. Are made by a lender to a borrower who: A. Meets the definitions of minority and minority business enterprise as defined in ; B. Has been certified by the Small and Minority Business Division of the AEDC as a minority business enterprise in accordance with and rules developed pursuant to (a); and C. Has done or is currently doing business with a Federal, state, or local Arkansas governmental entity; 2. Are made for purposes consistent with (d), which identifies three goals of the Minority Business Loan Mobilization Revolving Fund: A. Promote the development of minority business enterprises in the state; B. Increase the ability of minority business enterprises to compete for state contracts; and C. Sustain the economic growth of minority business enterprises in the state; 3. Are made by an approved lender to a borrower for an amount, purpose and term approved in a written loan guaranty authorization (authorization) signed by the AEDC Executive Director and the Director of the Small and Minority Business Division of the AEDC; and, 4. Are made with respect to lender compliance with the terms and conditions of an executed Loan Guaranty Lender Participation Agreement (agreement). II. Definitions 1. Lender means: A. A Federally-chartered bank; B. A State-chartered bank; C. A savings and loan association; Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 1

3 D. A credit union; E. An Arkansas Planning and Development or Economic Development District; or F. Any other form of financial institution regulated by the State of Arkansas or the Federal government; 2. Minority means a lawful permanent resident of this state who is: A. African American; B. Hispanic American; C. American Indian; D. Asian American; E. Pacific Islander American; or F. A service-disabled veteran as designated by the United States Department of Veterans Affairs; 3. Minority business enterprise means a business that is at least fifty-one percent (51%) owned by one (1) or more minority persons as defined in this section; 4. Small and Minority Business Division of the Arkansas Economic Development Commission means the division of the Arkansas Economic Development Commission responsible for administering the Minority Business Loan Mobilization Program. III. Lender Requirements and Responsibilities 1. To be eligible to serve as a lender for a loan that is guaranteed by the Small and Minority Business Division of the AEDC, the lender shall be one of the following financial institutions: A. A Federally-chartered bank; B. A State-chartered bank; C. A savings and loan association; D. A credit union; E. An Arkansas Planning and Development or Economic Development District; or F. Any other form of financial institution regulated by the State of Arkansas or the Federal government. 2. The lender will only approve deals that are consistent with prudent lending practices through review of personal and business financial statements and other documents; the credit standing, repayment capacity, existence of title to and value of collateral pledged to the loan (if any); earnings prospects; and business acumen of the borrower requesting a loan guaranty through the Minority Business Loan Mobilization Program. 3. Upon and after closing the loan and disbursing the loan proceeds, the lender shall cause to be executed, delivered, and, where necessary, filed or recorded Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 2

owned by one (1) or more minority persons as defined in this section; 4.")

4 with the proper authorities, a note, mortgage or trust deed, security agreement, financing statement, continuation statement, and such other instruments, documents and agreements as may be applicable. The lender shall take such other actions as required to assure that the borrower and any guarantor(s) are obligated to repay the loan. 4. The lender shall have valid and enforceable security interest in any collateral and insure that the collateral is adequately maintained and insured and that the interest of the lender and AEDC are fully protected, consistent with prudent lending practices. 5. The lender shall cause all loan documents, including any guaranty agreements, to be properly authorized and executed as required in the authorization. The lender shall take any further action necessary to assure that all guarantor(s) have a binding and enforceable obligation to repay the loan. 6. The lender shall exercise supervision over any collateral and ensure that any collateral is disposed of in a commercially reasonable sale. 7. Services of an escrow agent may be required at the request of AEDC to discuss issues regarding use of proceeds for authorized purposes. 8. Upon request, the lender shall provide to the Small and Minority Business Division of the AEDC all documents executed in connection with the loan, loan disbursements and loan records. 9. The lender will impose no charges on the borrower of a loan guaranteed hereunder that would not normally be imposed had the loan not been guaranteed. 10. The lender will provide the Small and Minority Business Division of the AEDC with such financial information on guaranteed loans as the Small and Minority Business Division of the AEDC may reasonably require. IV. Loan Guaranty Application Process 1. To apply for a loan guaranty under the Minority Business Loan Mobilization Program, a minority business enterprise shall submit an application and any supporting documentation required to the Small and Minority Business Division of the AEDC. 2. The Small and Minority Business Division of the AEDC shall: A. Evaluate each application and any supporting documentation to determine whether the minority business enterprise is eligible for a loan guaranty in accordance with the requirements of et seq. (Minority Business Economic Development Act) and (d) (Minority Business Loan Mobilization Revolving Fund). B. Recommend approval of the minority business enterprise meeting eligibility requirements to the AEDC Executive Director. Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 3

5 C. Notify the minority business enterprise of approval or denial of the application within seven (7) business days of receipt of the application by the Small and Minority Business Division of the AEDC. 3. Upon notification of approval by the Small and Minority Business Division of the AEDC, the approved minority business enterprise will be informed about the next steps including selection of a lender to begin the lender s loan application process. 4. The lender selected by the approved minority business enterprise shall: A. Notify the minority business enterprise of the lender s determination to approve or deny the minority business enterprise s loan application. B. Send written notification of the lender s determination to approve or deny the loan application to the Small and Minority Business Division of the AEDC within seven (7) business days after making the determination. 5. The Small and Minority Business Division of the AEDC will review the approved lender application package and execute a written loan guaranty authorization between the lender and the AEDC. 6. After a loan application has been approved by a lender, the minority business enterprise shall close the loan. 7. The Small and Minority Business Division of the AEDC will retain a copy of the loan package and monitor the project for compliance with program requirements. V. Administration and Servicing of Loans The lender shall maintain the loan instruments, receive all payments, including but not limited to principal and interest, and take other such action as may be required or advisable to administer and service the loan consistent with prudent lending practices. The lender shall not, without prior written consent of the AEDC, engage in any of the following: 1. Make or consent to any transfer or assignment of any note or interest therein or any material alteration in the terms of any loan instrument; 2. Make or consent to any release, conveyance, lease, substitution or exchange of any collateral; 3. Extend or postpone any repayment terms except those authorized in the executed loan guaranty lender participation agreement; and 4. Waive or release any claim against the borrower, surety, guarantor, or other obligor, or any other creditor of trustee in bankruptcy, arising out of any loan instrument. The Small and Minority Business Division of the AEDC will respond to written requests regarding administration and servicing of loans from lenders within fifteen (15) days of receipt or such requests will be deemed not to require the written consent of the Small and Minority Business Division of the AEDC. Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 4

6 VI. Default and Notice of Default The lender agrees to notify the Small and Minority Business Division of the AEDC, in writing, within fifteen (15) business days of notice of actual default. Within fifteen (15) business days after receipt of notice of actual default, the Small and Minority Business Division of the AEDC will notify the lender, in writing, which of the following options the AEDC elects: 1. LIQUIDATION: The Small and Minority Business Division of the AEDC may direct the lender to accelerate the maturity of the loan and proceed to enforce all loan documents to liquidate any security for the loan including proceeding against any guarantor(s), in a commercially reasonable, expeditious manner and in accordance with prudent lending practices. In such an event, the AEDC shall pay the lesser of ninety percent (90%) of the remaining unpaid loan balance, or the guaranty percentage specified in the loan authorization agreement, with a maximum payment not to exceed $100, PAYMENT: The Small and Minority Business Division of the AEDC shall pay the lesser of ninety percent (90%) of the remaining unpaid loan balance, or the guaranty percentage specified in the loan authorization agreement, with a maximum payment not to exceed $100,000, in payments of equal value, but for the acceleration, on the due dates defined in loan documents and may direct the lender to assign all loan documents and rights to the AEDC. The Small and Minority Business Division of the AEDC and lender may take such other action, upon default, as they may agree to in writing. At any time after electing to direct the lender to liquidate, the AEDC may elect the above payment option VI. 2. All proceeds of any collateral or guaranties of any nature (other than guaranties received pursuant to the AEDC guaranty agreement), including, without limitation, right of setoff and counter claim, shall be used to repay and secure the interests of the lender and the AEDC. VII. Requests for Payment of Guaranty In the event that the Small and Minority Business Division of the AEDC has directed the lender to liquidate any collateral, the lender s request for the payment of guaranty shall be accompanied by the lender s written certification: 1. That the lender has liquidated any collateral and all guaranties for the loan and has diligently pursued and exhausted all sources of repayment, unless by mutual consent such pursuit has not been deemed cost-effective; and 2. That the lender has allocated repayments, proceeds of any collateral and any guarantees to the respective interest of the parties, as required by these rules Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 5

7 VIII. Source of Funds or a specific authorization agreed to by both parties, including the remaining unpaid principal and interest. Any guaranties by the Small and Minority Business Division of the AEDC have been entered into under the provisions of Act 1428 of 2009, Sections 10 and 11, and are subject to all terms, restrictions and commitments contained therein. Neither the full faith nor credit of the State of Arkansas or any of its revenues is pledged to meet the obligations of the AEDC under any guaranty agreement. The obligations of the AEDC under Minority Business Loan Mobilization Program guaranty agreements are limited to the funds available in the Minority Business Loan Mobilization Revolving Fund as provided for in Act 1428 of 2009, and any subsequent appropriation for similar purposes. Minority Business Loan Mobilization Program Rules (May 17, 2016) Page 6

8 QUESTIONNAIRE FOR FILING PROPOSED RULES AND REGULATIONS WITH THE ARKANSAS LEGISLATIVE COUNCIL AND JOINT INTERIM COMMITTEE DEPARTMENT/AGENCY Arkansas Economic Development Commission DIVISION DIVISION DIRECTOR CONTACT PERSON Small and Minority Business Division Ms. Pat Nunn-Brown Kurt Naumann ADDRESS 900 West Capitol; Little Rock, AR PHONE NO FAX NO E- MAIL NAME OF PRESENTER AT COMMITTEE MEETING Ms. Pat Nunn Brown, Anthony Armstrong, Kurt Naumann PRESENTER INSTRUCTIONS A. Please make copies of this form for future use. B. Please answer each question completely using layman terms. You may use additional sheets, if necessary. C. If you have a method of indexing your rules, please give the proposed citation after Short Title of this Rule below. D. Submit two (2) copies of this questionnaire and financial impact statement attached to the front of two (2) copies of the proposed rule and required documents. Mail or deliver to: Donna K. Davis Administrative Rules Review Section Arkansas Legislative Council Bureau of Legislative Research One Capitol Mall, 5 th Floor Little Rock, AR ********************************************************************************* 1. What is the short title of this rule? Minority Business Loan Mobilization Program 2. What is the subject of the proposed rule? Administration of the Minority Business Loan Mobilization Program by the Small and Minority Business Division of the Arkansas Economic Development Commission 3. Is this rule required to comply with a federal statute, rule, or regulation? Yes No If yes, please provide the federal rule, regulation, and/or statute citation. 4. Was this rule filed under the emergency provisions of the Administrative Procedure Act? Yes No If yes, what is the effective date of the emergency rule? N/A When does the emergency rule expire? N/A

9 Will this emergency rule be promulgated under the permanent provisions of the Administrative Procedure Act? Yes No 5. Is this a new rule? Yes No If yes, please provide a brief summary explaining the regulation. This new rule defines the administrative process by which the Small and Minority Business Division of the Arkansas Economic Development Commission administers the Minority Business Loan Mobilization Program. Legislation in 2009 created a state miscellaneous fund known as the Minority Business Loan Mobilization Revolving Fund which transferred unexpended fund balances remaining in AEDC s Small Business Loan Fund Account (and other funds as may be authorized) to this new fund. Loan guaranties were authorized beginning in This rule defines the process by which the Small and Minority Business Division of the Arkansas Economic Development Commission reviews and approves minority business enterprise loan guaranty applications and administers the guaranty program. Does this repeal an existing rule? Yes No If yes, a copy of the repealed rule is to be included with your completed questionnaire. If it is being replaced with a new rule, please provide a summary of the rule giving an explanation of what the rule does. Is this an amendment to an existing rule? Yes No If yes, please attach a mark-up showing the changes in the existing rule and a summary of the substantive changes. Note: The summary should explain what the amendment does, and the mark-up copy should be clearly labeled mark-up. 6. Cite the state law that grants the authority for this proposed rule? If codified, please give the Arkansas Code citation (b)(5) and What is the purpose of this proposed rule? Why is it necessary? Conform to Arkansas Administrative Procedures Act regarding the administration of the Minority Business Loan Mobilization Program 8. Please provide the address where this rule is publicly accessible in electronic form via the Internet as required by Arkansas Code (b) Will a public hearing be held on this proposed rule? Yes No If yes, please complete the following: Date: March 23, 2016 Time: 9 am Bessie Moore Conference Room, 2 nd Floor, 900 West Capitol; Little Rock, Place: AR When does the public comment period expire for permanent promulgation? (Must provide a date.) March 21, 2016

10 11. What is the proposed effective date of this proposed rule? (Must provide a date.) June 18, Do you expect this rule to be controversial? Yes No If yes, please explain. The legislature may question the length of time between program initiation and rule promulgation. 13. Please give the names of persons, groups, or organizations that you expect to comment on these rules? Please provide their position (for or against) if known. None anticipated at this time.

11 FINANCIAL IMPACT STATEMENT PLEASE ANSWER ALL QUESTIONS COMPLETELY DEPARTMENT Arkansas Economic Development Commission DIVISION Small and Minority Business Division PERSON COMPLETING THIS STATEMENT Kurt Naumann TELEPHONE NO FAX NO To comply with Ark. Code Ann (e), please complete the following Financial Impact Statement and file two copies with the questionnaire and proposed rules. SHORT TITLE OF THIS RULE Minority Business Loan Mobilization Program 1. Does this proposed, amended, or repealed rule have a financial impact? Yes No 2. Is the rule based on the best reasonably obtainable scientific, technical, economic, or other evidence and information available concerning the need for, consequences of, and alternatives to the rule? Yes No 3. In consideration of the alternatives to this rule, was this rule determined by the agency to be the least costly rule considered? Yes No If an agency is proposing a more costly rule, please state the following: (a) How the additional benefits of the more costly rule justify its additional cost; N/A (b) The reason for adoption of the more costly rule; N/A (c) (d) Whether the more costly rule is based on the interests of public health, safety, or welfare, and if so, please explain; and; N/A Whether the reason is within the scope of the agency s statutory authority; and if so, please explain. N/A 4. If the purpose of this rule is to implement a federal rule or regulation, please state the following: (a) What is the cost to implement the federal rule or regulation? Current Fiscal Year General Revenue Federal Funds Cash Funds Special Revenue Other (Identify) Next Fiscal Year General Revenue Federal Funds Cash Funds Special Revenue Other (Identify)

12 Total Total (b) What is the additional cost of the state rule? Current Fiscal Year General Revenue Federal Funds Cash Funds Special Revenue Other (Identify) Next Fiscal Year General Revenue Federal Funds Cash Funds Special Revenue Other (Identify) Total $0 Total $0 5. What is the total estimated cost by fiscal year to any private individual, entity and business subject to the proposed, amended, or repealed rule? Identify the entity(ies) subject to the proposed rule and explain how they are affected. Current Fiscal Year Next Fiscal Year $ 0 $ 0 6. What is the total estimated cost by fiscal year to state, county, and municipal government to implement this rule? Is this the cost of the program or grant? Please explain how the government is affected. Current Fiscal Year Next Fiscal Year $ 0 $ 0 7. With respect to the agency s answers to Questions #5 and #6 above, is there a new or increased cost or obligation of at least one hundred thousand dollars ($100,000) per year to a private individual, private entity, private business, state government, county government, municipal government, or to two (2) or more of those entities combined? If YES, the agency is required by Ark. Code Ann (e)(4) to file written findings at the time of filing the financial impact statement. The written findings shall be filed simultaneously with the financial impact statement and shall include, without limitation, the following: (1) a statement of the rule s basis and purpose; (2) the problem the agency seeks to address with the proposed rule, including a statement of whether a rule is required by statute; Yes (3) a description of the factual evidence that: (a) justifies the agency s need for the proposed rule; and No

subject to the proposed rule and explain how they are affected. Current Fiscal Year Next Fiscal Year $ 0 $ 0 6.")

13 (b) describes how the benefits of the rule meet the relevant statutory objectives and justify the rule s costs; (4) a list of less costly alternatives to the proposed rule and the reasons why the alternatives do not adequately address the problem to be solved by the proposed rule; (5) a list of alternatives to the proposed rule that were suggested as a result of public comment and the reasons why the alternatives do not adequately address the problem to be solved by the proposed rule; (6) a statement of whether existing rules have created or contributed to the problem the agency seeks to address with the proposed rule and, if existing rules have created or contributed to the problem, an explanation of why amendment or repeal of the rule creating or contributing to the problem is not a sufficient response; and (7) an agency plan for review of the rule no less than every ten (10) years to determine whether, based upon the evidence, there remains a need for the rule including, without limitation, whether: (a) the rule is achieving the statutory objectives; (b) the benefits of the rule continue to justify its costs; and (c) the rule can be amended or repealed to reduce costs while continuing to achieve the statutory objectives.

Minority Business Loan Mobilization Program Lender Participation Agreement

Minority Business Loan Mobilization Program Lender Participation Agreement Section 1 INCLUDED LOANS: Pursuant to authority granted under Act 1428 15-4-306, the Minority Business Division of the Arkansas

Minority Business Loan Mobilization Program Lender Participation Agreement Section 1 INCLUDED LOANS: Pursuant to authority granted under Act 1428 15-4-306, the Minority Business Division of the Arkansas

OREGON BUSINESS DEVELOPMENT DEPARTMENT CREDIT ENHANCEMENT FUND INSURANCE PROGRAM LOAN INSURANCE AGREEMENT

OREGON BUSINESS DEVELOPMENT DEPARTMENT CREDIT ENHANCEMENT FUND INSURANCE PROGRAM LOAN INSURANCE AGREEMENT In consideration of the mutual undertakings set forth in this Agreement, ("Lender") and the State

OREGON BUSINESS DEVELOPMENT DEPARTMENT CREDIT ENHANCEMENT FUND INSURANCE PROGRAM LOAN INSURANCE AGREEMENT In consideration of the mutual undertakings set forth in this Agreement, ("Lender") and the State

CHAPTER 7 - COLLATERALIZATION OF DEPOSITS SECTION.0100 - GENERAL

CHAPTER 7 - COLLATERALIZATION OF DEPOSITS SECTION.0100 - GENERAL 20 NCAC 07.0101 GENERAL INFORMATION (a) This Chapter sets forth the manner in which the official depositories shall provide the collateralization

CHAPTER 7 - COLLATERALIZATION OF DEPOSITS SECTION.0100 - GENERAL 20 NCAC 07.0101 GENERAL INFORMATION (a) This Chapter sets forth the manner in which the official depositories shall provide the collateralization

SUBCHAPTER 03K - REVERSE MORTGAGES SECTION.0100 - ADMINISTRATIVE

SUBCHAPTER 03K - REVERSE MORTGAGES SECTION.0100 - ADMINISTRATIVE 04 NCAC 03K.0101 DEFINITIONS; FILINGS (a) As used in this Subchapter, unless the context clearly requires otherwise: (1) Terms defined in

SUBCHAPTER 03K - REVERSE MORTGAGES SECTION.0100 - ADMINISTRATIVE 04 NCAC 03K.0101 DEFINITIONS; FILINGS (a) As used in this Subchapter, unless the context clearly requires otherwise: (1) Terms defined in

The Florist Credit Union:

The Florist Federal Credit Union BUSINESS LOAN APPLICATION I. GENERAL INFORMATION Applicants Name / Borrower (individual business owner or business name): Tax ID Number: Mailing Address: Contact Person:

The Florist Federal Credit Union BUSINESS LOAN APPLICATION I. GENERAL INFORMATION Applicants Name / Borrower (individual business owner or business name): Tax ID Number: Mailing Address: Contact Person:

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE In this Private Education Line of Credit Agreement and Disclosure ( Agreement ) the terms I, me, my and mine mean each person who

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE In this Private Education Line of Credit Agreement and Disclosure ( Agreement ) the terms I, me, my and mine mean each person who

12.25.2.2 SCOPE: All escrow companies licensed by the state of New Mexico. [12.25.2.2 NMAC - Rp, 12 NMAC 25.2.2, 7/1/15]

![12.25.2.2 SCOPE: All escrow companies licensed by the state of New Mexico. [12.25.2.2 NMAC - Rp, 12 NMAC 25.2.2, 7/1/15]](/thumbs/29/13835639.jpg "12.25.2.2 SCOPE: All escrow companies licensed by the state of New Mexico. [12.25.2.2 NMAC - Rp, 12 NMAC 25.2.2, 7/1/15]") TITLE 12 CHAPTER 25 PART 2 TRADE, COMMERCE AND BANKING ESCROW COMPANIES ESCROW COMPANY ACT 12.25.2.1 ISSUING AGENCY: Financial Institutions Division of the Regulation and Licensing Department, 2550 Cerrillos

TITLE 12 CHAPTER 25 PART 2 TRADE, COMMERCE AND BANKING ESCROW COMPANIES ESCROW COMPANY ACT 12.25.2.1 ISSUING AGENCY: Financial Institutions Division of the Regulation and Licensing Department, 2550 Cerrillos

RHODE ISLAND HOUSING AND MORTGAGE FINANCE CORPORATION REGULATIONS GOVERNING THE REVERSE EQUITY MORTGAGE LOAN PROGRAMS

RHODE ISLAND HOUSING AND MORTGAGE FINANCE CORPORATION REGULATIONS GOVERNING THE REVERSE EQUITY MORTGAGE LOAN PROGRAMS I. DEFINITIONS A. As used in these regulations: 1. "Advance" means a monthly cash advance

RHODE ISLAND HOUSING AND MORTGAGE FINANCE CORPORATION REGULATIONS GOVERNING THE REVERSE EQUITY MORTGAGE LOAN PROGRAMS I. DEFINITIONS A. As used in these regulations: 1. "Advance" means a monthly cash advance

Act on Guaranties and Third-Party Pledges

NB: Unofficial translation Ministry of Justice, Finland Act on Guaranties and Third-Party Pledges (361/1999) Chapter 1 General provisions Section 1 Scope of application and mandatory provisions (1) This

NB: Unofficial translation Ministry of Justice, Finland Act on Guaranties and Third-Party Pledges (361/1999) Chapter 1 General provisions Section 1 Scope of application and mandatory provisions (1) This

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION SECTION A: TYPE OF CREDIT APPLYING FOR Type of Loan Amount Requested Business Line of Credit Primary Purpose of this Loan(s): Equipment Term Loan - Length: Letter of Credit Commercial

BUSINESS LOAN APPLICATION SECTION A: TYPE OF CREDIT APPLYING FOR Type of Loan Amount Requested Business Line of Credit Primary Purpose of this Loan(s): Equipment Term Loan - Length: Letter of Credit Commercial

APPRAISAL MANAGEMENT COMPANY

STATE OF ARKANSAS APPRAISER LICENSING AND CERTIFICATION BOARD APPRAISAL MANAGEMENT COMPANY STATUTES 1 ARKANSAS APPRAISER LICENSING AND CERTIFICATION BOARD APPRAISAL MANAGEMENT COMPANY STATUTES SUBCHAPTER

STATE OF ARKANSAS APPRAISER LICENSING AND CERTIFICATION BOARD APPRAISAL MANAGEMENT COMPANY STATUTES 1 ARKANSAS APPRAISER LICENSING AND CERTIFICATION BOARD APPRAISAL MANAGEMENT COMPANY STATUTES SUBCHAPTER

REPORT OF CONFERENCE COMMITTEE

REPORT OF CONFERENCE COMMITTEE MR. SPEAKER AND MADAM PRESIDENT: We, the undersigned conferees, have had under consideration the amendments to the following entitled BILL: H. B. No. 41: Disaster relief;

REPORT OF CONFERENCE COMMITTEE MR. SPEAKER AND MADAM PRESIDENT: We, the undersigned conferees, have had under consideration the amendments to the following entitled BILL: H. B. No. 41: Disaster relief;

General Conditions for Loans reference No.: General Terms and Conditions for Loans dated 1 March 2016

General Conditions for Loans reference No.: General Terms and Conditions for Loans dated 1 March 2016 These General Conditions for Loans is made between ( Lender )and the Entity who signs the Schedule

General Conditions for Loans reference No.: General Terms and Conditions for Loans dated 1 March 2016 These General Conditions for Loans is made between ( Lender )and the Entity who signs the Schedule

MCE On-Bill Repayment Program Loan Information Request

MCE On-Bill Repayment Program Loan Information Request GENERAL BUSINESS INFORMATION Note: Please print or type all information. Use additional sheets if necessary. Applicant s name (legal business name)

MCE On-Bill Repayment Program Loan Information Request GENERAL BUSINESS INFORMATION Note: Please print or type all information. Use additional sheets if necessary. Applicant s name (legal business name)

2 Be it enacted by the People of the State of Illinois, 4 Section 1. Short title. This Act may be cited as the

SB49 Enrolled LRB9201970MWcd 1 AN ACT concerning home mortgages. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Short title. This Act may be

SB49 Enrolled LRB9201970MWcd 1 AN ACT concerning home mortgages. 2 Be it enacted by the People of the State of Illinois, 3 represented in the General Assembly: 4 Section 1. Short title. This Act may be

MILWAUKEE DOWNTOWN, BUSINESS IMPROVEMENT DISTRICT #21 BUSINESS DEVELOPMENT LOAN POOL (BDPL) GUIDELINES & APPLICATION

GUIDELINES & APPLICATION") MILWAUKEE DOWNTOWN, BUSINESS IMPROVEMENT DISTRICT #21 BUSINESS DEVELOPMENT LOAN POOL (BDPL) GUIDELINES & APPLICATION Created in proud partnership with BUSINESS DEVELOPMENT LOAN POOL (BDLP) Milwaukee Downtown,

MILWAUKEE DOWNTOWN, BUSINESS IMPROVEMENT DISTRICT #21 BUSINESS DEVELOPMENT LOAN POOL (BDPL) GUIDELINES & APPLICATION Created in proud partnership with BUSINESS DEVELOPMENT LOAN POOL (BDLP) Milwaukee Downtown,

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION New Relationship Existing Relationship Branch: Officer: BUSINESS INFORMATION Business Name Tax I.D. Individual Name(s) Social Security # Date of Birth: Proprietorship Partnership

BUSINESS LOAN APPLICATION New Relationship Existing Relationship Branch: Officer: BUSINESS INFORMATION Business Name Tax I.D. Individual Name(s) Social Security # Date of Birth: Proprietorship Partnership

The Trust and Loan Corporations Act, 1997

1 The Trust and Loan Corporations Act, 1997 being Chapter T-22.2* of the Statutes of Saskatchewan, 1997 (effective September 1, 1999, clause 44(a), and section 57 not yet proclaimed) as amended by the

1 The Trust and Loan Corporations Act, 1997 being Chapter T-22.2* of the Statutes of Saskatchewan, 1997 (effective September 1, 1999, clause 44(a), and section 57 not yet proclaimed) as amended by the

WEDCO. Amount Requested Purpose. Repayment Source

WEDCO Wentworth Economic Development Corporation, Inc. 7 Center Street, PO Box 641, Wolfeboro, NH 03894 Phone: 569-4216 Fax: 569-3317 Website: www.wedco NH.org Small Business Loan Application All information

WEDCO Wentworth Economic Development Corporation, Inc. 7 Center Street, PO Box 641, Wolfeboro, NH 03894 Phone: 569-4216 Fax: 569-3317 Website: www.wedco NH.org Small Business Loan Application All information

NC General Statutes - Chapter 54B Article 12 1

Article 12. Mutual Deposit Guaranty Associations. 54B-236. Definitions. The term "institution" as used in this Article shall mean savings and loan associations organized or operated under the provisions

Article 12. Mutual Deposit Guaranty Associations. 54B-236. Definitions. The term "institution" as used in this Article shall mean savings and loan associations organized or operated under the provisions

Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193

45-189 Loan brokers; legislative findings. The Legislature finds that: Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193 (1) Many professional groups are presently licensed or

45-189 Loan brokers; legislative findings. The Legislature finds that: Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193 (1) Many professional groups are presently licensed or

12.19.8.2 SCOPE: All mortgage loan companies licensed by the state of New Mexico. [12.19.8.2 NMAC - Rp, 12 NMAC 19.2.8.2, 12/15/08; A, 08/31/09]

![12.19.8.2 SCOPE: All mortgage loan companies licensed by the state of New Mexico. [12.19.8.2 NMAC - Rp, 12 NMAC 19.2.8.2, 12/15/08; A, 08/31/09]](/thumbs/30/14640466.jpg "12.19.8.2 SCOPE: All mortgage loan companies licensed by the state of New Mexico. [12.19.8.2 NMAC - Rp, 12 NMAC 19.2.8.2, 12/15/08; A, 08/31/09]") TITLE 12 CHAPTER 19 PART 8 TRADE, COMMERCE AND BANKING MORTGAGE LENDING MORTGAGE LOAN COMPANY REQUIREMENTS 12.19.8.1 ISSUING AGENCY: Financial Institutions Division of the Regulation and Licensing Department.

TITLE 12 CHAPTER 19 PART 8 TRADE, COMMERCE AND BANKING MORTGAGE LENDING MORTGAGE LOAN COMPANY REQUIREMENTS 12.19.8.1 ISSUING AGENCY: Financial Institutions Division of the Regulation and Licensing Department.

TABLE OF CONTENTS Insuring of Industrial Mortgages

Connecticut Industrial Building Commission Sec. 32-13 page 1 (9-97) TABLE OF CONTENTS Insuring of Industrial Mortgages Application and fees... 32-13- 1 Commitment or unacceptance... 32-13- 2 Covenant for

Connecticut Industrial Building Commission Sec. 32-13 page 1 (9-97) TABLE OF CONTENTS Insuring of Industrial Mortgages Application and fees... 32-13- 1 Commitment or unacceptance... 32-13- 2 Covenant for

RELIANT COMMUNITY FEDERAL CREDIT UNION BUSINESS CREDIT APPLICATION

Main Office: 10 Benton Pl., PO Box 40, Sodus, NY 14551 800.724.9282 reliantcu.com Brockport Canandaigua Geneva Henrietta Irondequoit Macedon Newark Sodus Webster RELIANT COMMUNITY FEDERAL CREDIT UNION

Main Office: 10 Benton Pl., PO Box 40, Sodus, NY 14551 800.724.9282 reliantcu.com Brockport Canandaigua Geneva Henrietta Irondequoit Macedon Newark Sodus Webster RELIANT COMMUNITY FEDERAL CREDIT UNION

Loan Agreement (Short Form)

") Loan Agreement (Short Form) Document 2050A Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc. nor any of the providers of information that appear

Loan Agreement (Short Form) Document 2050A Access to this document and the LeapLaw web site is provided with the understanding that neither LeapLaw Inc. nor any of the providers of information that appear

NC General Statutes - Chapter 45 Article 9 1

Article 9. Instruments to Secure Equity Lines of Credit. 45-81. Definitions. The following definitions apply in this Article: (1) Authorized person. Any borrower; the legal representative of any borrower;

Article 9. Instruments to Secure Equity Lines of Credit. 45-81. Definitions. The following definitions apply in this Article: (1) Authorized person. Any borrower; the legal representative of any borrower;

Chapter 25 Utah Residential Rehabilitation Act

Chapter 25 Utah Residential Rehabilitation Act 11-25-1 Short title. This act shall be known and may be cited as the "Utah Residential Rehabilitation Act." 11-25-2 Legislative findings -- Liberal construction.

Chapter 25 Utah Residential Rehabilitation Act 11-25-1 Short title. This act shall be known and may be cited as the "Utah Residential Rehabilitation Act." 11-25-2 Legislative findings -- Liberal construction.

CITY OF TULLAHOMA COMMERCIAL REVOLVING LOAN FUND

CITY OF TULLAHOMA COMMERCIAL REVOLVING LOAN FUND Dear Applicant: The Commercial Revolving Loan Program is an economic development tool administered by the City of Tullahoma. The program provides loans

CITY OF TULLAHOMA COMMERCIAL REVOLVING LOAN FUND Dear Applicant: The Commercial Revolving Loan Program is an economic development tool administered by the City of Tullahoma. The program provides loans

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure Please retain for personal records This is your MasterCard Credit Card Agreement and Truth-In-Lending disclosure.

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure Please retain for personal records This is your MasterCard Credit Card Agreement and Truth-In-Lending disclosure.

DKLAHOMA TAX COMMISSION

DKLAHOMA TAX COMMISSION TAx POLICY DIVISION DAWN CASH, DIRECTOR Q* f * \ %/ PHONE ( 405) 521-3133 FACSIMILE ( 405) 522-0063 Re: Our file number Dear This letter ruling is in response to your letter ruling

DKLAHOMA TAX COMMISSION TAx POLICY DIVISION DAWN CASH, DIRECTOR Q* f * \ %/ PHONE ( 405) 521-3133 FACSIMILE ( 405) 522-0063 Re: Our file number Dear This letter ruling is in response to your letter ruling

DEED OF TRUST NOTE SURPLUS CASH WITH CONTINGENT INTEREST. Crownsville, Maryland, 20

Project Name: Project Number: HOME/RHP DEED OF TRUST NOTE SURPLUS CASH WITH CONTINGENT INTEREST $ Crownsville, Maryland, 20 FOR VALUE RECEIVED,, a Maryland (the Borrower ), promises to pay to the order

Project Name: Project Number: HOME/RHP DEED OF TRUST NOTE SURPLUS CASH WITH CONTINGENT INTEREST $ Crownsville, Maryland, 20 FOR VALUE RECEIVED,, a Maryland (the Borrower ), promises to pay to the order

Understanding Regulation U

Understanding Regulation U What every deal lawyer needs to know about the margin regulations November 17, 2011 Craig Unterberg David Aman Federal Margin Regulations Background Authorized under Section

Understanding Regulation U What every deal lawyer needs to know about the margin regulations November 17, 2011 Craig Unterberg David Aman Federal Margin Regulations Background Authorized under Section

Sunrise Loan Fund Application Form

Sunrise Loan Fund Application Form Instructions For Application Form Sections I, II, III. Please provide the information requested. "You" refers to the proprietor, general partner, or corporate officer

Sunrise Loan Fund Application Form Instructions For Application Form Sections I, II, III. Please provide the information requested. "You" refers to the proprietor, general partner, or corporate officer

SECURED DEMAND NOTE COLLATERAL AGREEMENT

SECURED DEMAND NOTE COLLATERAL AGREEMENT This Secured Demand Note Collateral Agreement (the "Agreement") is effective as of the day of, 20 by and between the "Lender") and (the "Borrower"), who mutually

SECURED DEMAND NOTE COLLATERAL AGREEMENT This Secured Demand Note Collateral Agreement (the "Agreement") is effective as of the day of, 20 by and between the "Lender") and (the "Borrower"), who mutually

AGENDA ITEM 4. UNITED STATES DEPARTMENT OF EDUCATION LOAN PURCHASE COMMITMENT PROGRAM AND LOAN PARTICIPATION PURCHASE PROGRAM

AGENDA ITEM 4. UNITED STATES DEPARTMENT OF EDUCATION LOAN PURCHASE COMMITMENT PROGRAM AND LOAN PARTICIPATION PURCHASE PROGRAM Submitted for: Summary: Action On May 7, 2008, President Bush signed into law

AGENDA ITEM 4. UNITED STATES DEPARTMENT OF EDUCATION LOAN PURCHASE COMMITMENT PROGRAM AND LOAN PARTICIPATION PURCHASE PROGRAM Submitted for: Summary: Action On May 7, 2008, President Bush signed into law

STATE OF GEORGIA DEPARTMENT OF BANKING AND FINANCE SPECIAL EDITION IMPORTANT NOTICE PROPOSED RULEMAKING

STATE OF GEORGIA DEPARTMENT OF BANKING AND FINANCE NATHAN DEAL GOVERNOR KEVIN HAGLER COMMISSIONER SPECIAL EDITION IMPORTANT NOTICE PROPOSED RULEMAKING September 24, 2015 NOTICE OF PROPOSED RULEMAKING AND

STATE OF GEORGIA DEPARTMENT OF BANKING AND FINANCE NATHAN DEAL GOVERNOR KEVIN HAGLER COMMISSIONER SPECIAL EDITION IMPORTANT NOTICE PROPOSED RULEMAKING September 24, 2015 NOTICE OF PROPOSED RULEMAKING AND

Issue Paper #16 Loans Group Final Consensus Language: Contextual Format 03/30/2012. Title IV Closed School Loan Discharge

Issue: Statutory Cites: Title IV Closed School Loan Discharge 437(c)(1) and 464(g) Regulatory Cites: 674.33(g), 682.402(d), and 685.214 Summary of Change: Under the current closed school discharge regulations

Issue: Statutory Cites: Title IV Closed School Loan Discharge 437(c)(1) and 464(g) Regulatory Cites: 674.33(g), 682.402(d), and 685.214 Summary of Change: Under the current closed school discharge regulations

747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org

591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org") 747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org February 13, 2015 RESPONSES DUE BY 5:00 PM FRIDAY, MARCH 13, 2015 REQUEST FOR PROPOSALS

747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org February 13, 2015 RESPONSES DUE BY 5:00 PM FRIDAY, MARCH 13, 2015 REQUEST FOR PROPOSALS

MARYLAND ECONOMIC ADJUSTMENT FUND (MEAF) (AN ENTERPRISE FUND OF THE STATE OF MARYLAND) Financial Statements Together with Report of Independent

(AN ENTERPRISE FUND OF THE STATE OF MARYLAND) Financial Statements Together with Report of Independent") (AN ENTERPRISE FUND OF THE STATE OF MARYLAND) Financial Statements Together with Report of Independent Public Accountants For the Years Ended JUNE 30, 2013 AND 2012 CONTENTS REPORT OF INDEPENDENT PUBLIC

(AN ENTERPRISE FUND OF THE STATE OF MARYLAND) Financial Statements Together with Report of Independent Public Accountants For the Years Ended JUNE 30, 2013 AND 2012 CONTENTS REPORT OF INDEPENDENT PUBLIC

If you need assistance completing this application, please email us at [email protected]

LOAN APPLICATION Coös Economic Development Corporation (CEDC) CEDC If you need assistance completing this application, please email us at [email protected] Part A: BUSINESS INFORMATION REGISTERED

LOAN APPLICATION Coös Economic Development Corporation (CEDC) CEDC If you need assistance completing this application, please email us at [email protected] Part A: BUSINESS INFORMATION REGISTERED

Guidelines for completing the Orscheln VISA Credit Card Business Application

Guidelines for completing the Orscheln VISA Credit Card Business Application The guidelines listed below are designed to help you assist the business in submitting a complete business application. Following

Guidelines for completing the Orscheln VISA Credit Card Business Application The guidelines listed below are designed to help you assist the business in submitting a complete business application. Following

PERFORMANCE BOND LABOR AND MATERIAL PAYMENT BOND

Section 00 61 13.13 & 00 61 13.16 Douglas County School District Re.1 Castle Rock, Colorado PERFORMANCE BOND LABOR AND MATERIAL PAYMENT BOND 1. FORMS TO BE USED Two (2) separate bonds are required: Both

Section 00 61 13.13 & 00 61 13.16 Douglas County School District Re.1 Castle Rock, Colorado PERFORMANCE BOND LABOR AND MATERIAL PAYMENT BOND 1. FORMS TO BE USED Two (2) separate bonds are required: Both

DUSTIN McDANIEL ATTORNEY GENERAL OFFICE OF THE ATTORNEY GENERAL 323 CENTER STREET, Suite 200 LITTLE ROCK, AR 72201-2610 (501) 682-2007

682-2007") DUSTIN McDANIEL ATTORNEY GENERAL OFFICE OF THE ATTORNEY GENERAL 323 CENTER STREET, Suite 200 LITTLE ROCK, AR 72201-2610 (501) 682-2007 PAID SOLICITOR APPLICATION FOR REGISTRATION Pursuant to Ark. Code

DUSTIN McDANIEL ATTORNEY GENERAL OFFICE OF THE ATTORNEY GENERAL 323 CENTER STREET, Suite 200 LITTLE ROCK, AR 72201-2610 (501) 682-2007 PAID SOLICITOR APPLICATION FOR REGISTRATION Pursuant to Ark. Code

Drafting Term Sheets and Financing Agreements. Ward Buringrud Partner, Finance and Commercial Law Transactions

Drafting Term Sheets and Financing Agreements Ward Buringrud Partner, Finance and Commercial Law Transactions The business plan What the lender wants What the borrower wants Agenda Term sheet basics and

Drafting Term Sheets and Financing Agreements Ward Buringrud Partner, Finance and Commercial Law Transactions The business plan What the lender wants What the borrower wants Agenda Term sheet basics and

Visa Business Credit Card Visa Business Rewards Credit Card

Visa Business Credit Card Visa Business Rewards Credit Card Card Center, P.O. Box 410436, Kansas City, MO 64141-0436 Branch ID no. Associate ID No. Agent # - BBW 0240 COMPANY INFORMATION Company Name Street

Visa Business Credit Card Visa Business Rewards Credit Card Card Center, P.O. Box 410436, Kansas City, MO 64141-0436 Branch ID no. Associate ID No. Agent # - BBW 0240 COMPANY INFORMATION Company Name Street

Commercial Loan Application. Personal Financial Statement. Certification of Personal Financial Statement

Thank you for your interest in pursuing financing with Valley National Bank. In order to begin the analysis of your credit request, please complete the following: Commercial Loan Application Personal Financial

Thank you for your interest in pursuing financing with Valley National Bank. In order to begin the analysis of your credit request, please complete the following: Commercial Loan Application Personal Financial

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT This Business Credit and Continuing Security Agreement ("Agreement") includes this Agreement and may include a Business Credit Agreement Rider and Business

BUSINESS CREDIT AND CONTINUING SECURITY AGREEMENT This Business Credit and Continuing Security Agreement ("Agreement") includes this Agreement and may include a Business Credit Agreement Rider and Business

(LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION)

") Form RD 3560-41 ` FORM APPROVED (02-05) OMB NO 0575-0189 (LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION) LOAN AND GRANT RESOLUTION OF, 20 RESOLUTION OF THE BOARD OF DIRECTORS OF PROVIDING FOR

Form RD 3560-41 ` FORM APPROVED (02-05) OMB NO 0575-0189 (LABOR HOUSING LOAN AND GRANT TO A NONPROFIT CORPORATION) LOAN AND GRANT RESOLUTION OF, 20 RESOLUTION OF THE BOARD OF DIRECTORS OF PROVIDING FOR

RULES OF TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE INSURANCE DIVISION

RULES OF TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE INSURANCE DIVISION CHAPTER 0780-1-76 SELF-INSURING ASSOCIATIONS AND NON-PROFIT TABLE OF CONTENTS 0780-1-76-.01 Purpose and Scope 0780-1-76-.11 Examinations

RULES OF TENNESSEE DEPARTMENT OF COMMERCE AND INSURANCE INSURANCE DIVISION CHAPTER 0780-1-76 SELF-INSURING ASSOCIATIONS AND NON-PROFIT TABLE OF CONTENTS 0780-1-76-.01 Purpose and Scope 0780-1-76-.11 Examinations

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

COLORADO CONSUMER EQUITY PROTECTION ACT July 1, 2011 Table of Contents COLORADO CONSUMER EQUITY PROTECTION ACT... 1 PART 1 OBLIGOR PROTECTION... 1 5-3.5-101. Definitions.... 1 5-3.5-102. Protection of

Deliverable Obligation Characteristics for North American Corporate Transaction Type

ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: [email protected]

ISDA International Swaps and Derivatives Association, Inc. 360 Madison Avenue, 16th Floor New York, NY 10017 United States of America Telephone: 1 (212) 901-6000 Facsimile: 1 (212) 901-6001 email: [email protected]

06 LC 28 3090S/AP A BILL TO BE ENTITLED AN ACT

0 LC 00S/AP House Bill (AS PASSED HOUSE AND SENATE) By: Representatives Scheid of the nd and Byrd of the 0 th A BILL TO BE ENTITLED AN ACT To create the Woodstock Area Convention and Visitors Bureau Authority

0 LC 00S/AP House Bill (AS PASSED HOUSE AND SENATE) By: Representatives Scheid of the nd and Byrd of the 0 th A BILL TO BE ENTITLED AN ACT To create the Woodstock Area Convention and Visitors Bureau Authority

Home Equity Line of Credit Loan Agreement and Promissory Note

Home Equity Line of Credit Loan Agreement and Promissory Note This agreement sets forth the terms under which Pelican State Credit Union makes a home equity loan to you. By signing this agreement, you

Home Equity Line of Credit Loan Agreement and Promissory Note This agreement sets forth the terms under which Pelican State Credit Union makes a home equity loan to you. By signing this agreement, you

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas Combined Financial Statements and Additional Information for the Year Ended June 30, 2000, and Independent Auditors Report

Arkansas Development Finance Authority, a Component Unit of the State of Arkansas Combined Financial Statements and Additional Information for the Year Ended June 30, 2000, and Independent Auditors Report

AGREEMENT BY AND BETWEEN The Bank of Maine Portland, Maine and The Comptroller of the Currency

AGREEMENT BY AND BETWEEN The Bank of Maine Portland, Maine and The Comptroller of the Currency #2012-167 The Bank of Maine, Portland, Maine ( Bank ) and the Comptroller of the Currency of the United States

AGREEMENT BY AND BETWEEN The Bank of Maine Portland, Maine and The Comptroller of the Currency #2012-167 The Bank of Maine, Portland, Maine ( Bank ) and the Comptroller of the Currency of the United States

Debt Management Policies & Guidelines

Debt Management Policies & Guidelines January, 2004 PREPARED BY: ANDREW E. MEISNER, COUNTY TREASURER PATRICK M. DOHANY, COUNTY TREASURER I. COUNTY'S DEBT POLICY A. Purpose The County recognizes the foundation

Debt Management Policies & Guidelines January, 2004 PREPARED BY: ANDREW E. MEISNER, COUNTY TREASURER PATRICK M. DOHANY, COUNTY TREASURER I. COUNTY'S DEBT POLICY A. Purpose The County recognizes the foundation

ARKANSAS DEPARTMENT OF EDUCATION RULES GOVERNING THE SCHOOL WORKER DEFENSE PROGRAM AND THE SCHOOL WORKER DEFENSE PROGRAM ADVISORY BOARD June 2014

ARKANSAS DEPARTMENT OF EDUCATION RULES GOVERNING THE SCHOOL WORKER DEFENSE PROGRAM AND THE SCHOOL WORKER DEFENSE PROGRAM ADVISORY BOARD June 2014 1.0 PURPOSE 1.01 The purpose of these rules is to establish

ARKANSAS DEPARTMENT OF EDUCATION RULES GOVERNING THE SCHOOL WORKER DEFENSE PROGRAM AND THE SCHOOL WORKER DEFENSE PROGRAM ADVISORY BOARD June 2014 1.0 PURPOSE 1.01 The purpose of these rules is to establish

NORTH DELTA PLANNING AND DEVELOPMENT DISTRICT, INC MISSISSIPPI SMALL BUSINESS ASSISTANCE PROGRAM

NORTH DELTA PLANNING AND DEVELOPMENT DISTRICT, INC MISSISSIPPI SMALL BUSINESS ASSISTANCE PROGRAM APPLICATION PACKAGE For More Information Contact: James Curcio or Jeff Walters Post Office Box 1488 Batesville,

NORTH DELTA PLANNING AND DEVELOPMENT DISTRICT, INC MISSISSIPPI SMALL BUSINESS ASSISTANCE PROGRAM APPLICATION PACKAGE For More Information Contact: James Curcio or Jeff Walters Post Office Box 1488 Batesville,

Selected Text of the Fair Credit Reporting Act (15 U.S.C. 1681 1681v) With a special Focus on the Impact to Mortgage Lenders

With a special Focus on the Impact to Mortgage Lenders") Selected Text of the Fair Credit Reporting Act (15 U.S.C. 1681 1681v) as Amended by the Fair and Accurate Credit Transactions Act of 2003 (Public Law No. 108-159) With a special Focus on the Impact to

Selected Text of the Fair Credit Reporting Act (15 U.S.C. 1681 1681v) as Amended by the Fair and Accurate Credit Transactions Act of 2003 (Public Law No. 108-159) With a special Focus on the Impact to

Real Estate Principles Chapter 12 Quiz

Real Estate Principles Chapter 12 Quiz 1. A prudent lender who is deciding whether or not to make a real estate loan to a prospective borrower will ensure that: A. the market value of the property is greater

Real Estate Principles Chapter 12 Quiz 1. A prudent lender who is deciding whether or not to make a real estate loan to a prospective borrower will ensure that: A. the market value of the property is greater

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

COMMONWEALTH OF VIRGINIA STANDARD PERFORMANCE BOND

(Rev 03/02) Page 1 of 6 COMMONWEALTH OF VIRGINIA STANDARD PERFORMANCE BOND KNOW ALL MEN BY THESE PRESENTS: That, the Contractor ( Principal ) whose principal place of business is located at and ( Surety

(Rev 03/02) Page 1 of 6 COMMONWEALTH OF VIRGINIA STANDARD PERFORMANCE BOND KNOW ALL MEN BY THESE PRESENTS: That, the Contractor ( Principal ) whose principal place of business is located at and ( Surety

Nebraska Debt Management Statutes

Nebraska Debt Management Statutes Neb. Rev. Stat. 69-1201. Terms, defined. As used in sections 69-1201 to 69-1217, unless the context otherwise requires: (1) Debt management shall mean the planning and

Nebraska Debt Management Statutes Neb. Rev. Stat. 69-1201. Terms, defined. As used in sections 69-1201 to 69-1217, unless the context otherwise requires: (1) Debt management shall mean the planning and

VISA BUSINESS CREDIT CARD APPLICATION

UMB i1510018 (R 09/10) VISA BUSINESS CREDIT CARD APPLICATION It s easy to Apply. Incomplete information may cause delays. Please complete in full. [email protected] Fax to 816.843.2485

UMB i1510018 (R 09/10) VISA BUSINESS CREDIT CARD APPLICATION It s easy to Apply. Incomplete information may cause delays. Please complete in full. [email protected] Fax to 816.843.2485

LOAN SERVICING REQUEST GUIDELINES FOR THE COMMERCIAL LOAN SERVICING CENTERS

LOAN SERVICING REQUEST GUIDELINES FOR THE COMMERCIAL LOAN SERVICING CENTERS FRESNO SERVICING CENTER 2719 N. AIR FRESNO DR., STE 107 FRESNO, CA 93727 (559) 487-5650 LITTLE ROCK SERVICING CENTER 2120 RIVERFRONT

LOAN SERVICING REQUEST GUIDELINES FOR THE COMMERCIAL LOAN SERVICING CENTERS FRESNO SERVICING CENTER 2719 N. AIR FRESNO DR., STE 107 FRESNO, CA 93727 (559) 487-5650 LITTLE ROCK SERVICING CENTER 2120 RIVERFRONT

IC 24-4.5-7 Chapter 7. Small Loans

IC 24-4.5-7 Chapter 7. Small Loans IC 24-4.5-7-101 Citation Sec. 101. This chapter shall be known and may be cited as Uniform Consumer Credit Code Small Loans. As added by P.L.38-2002, SEC.1. IC 24-4.5-7-102

IC 24-4.5-7 Chapter 7. Small Loans IC 24-4.5-7-101 Citation Sec. 101. This chapter shall be known and may be cited as Uniform Consumer Credit Code Small Loans. As added by P.L.38-2002, SEC.1. IC 24-4.5-7-102

Please see Section IX. for Additional Information:

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional Staff

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional Staff

Amendment and Consent No. 2 (Morris County Renewable Energy Program, Series 2011)

") Execution Version Amendment and Consent No. 2 (Morris County Renewable Energy Program, Series 2011) by and among MORRIS COUNTY IMPROVEMENT AUTHORITY, COUNTY OF MORRIS, NEW JERSEY, U.S. BANK NATIONAL ASSOCIATION

Execution Version Amendment and Consent No. 2 (Morris County Renewable Energy Program, Series 2011) by and among MORRIS COUNTY IMPROVEMENT AUTHORITY, COUNTY OF MORRIS, NEW JERSEY, U.S. BANK NATIONAL ASSOCIATION

SCHERTZ BANK & TRUST COMMERCIAL LOAN APPLICATION

SCHERTZ BANK & TRUST COMMERCIAL LOAN APPLICATION LOAN REQUEST Business Term loan Commercial Line of Credit Commercial Real Estate Amount Requested $ Proposed Collateral and Value: Term/Month Business Legal

SCHERTZ BANK & TRUST COMMERCIAL LOAN APPLICATION LOAN REQUEST Business Term loan Commercial Line of Credit Commercial Real Estate Amount Requested $ Proposed Collateral and Value: Term/Month Business Legal

CHAPTER 9 Municipality Bankruptcy

U.S. COURTS HTTP://WWW.USCOURTS.GOV/FEDERALCOURTS/BANKRUPTCY/BANKRUPTCY BASICS/CHAPTER9.ASPX CHAPTER 9 Municipality Bankruptcy The chapter of the Bankruptcy Code providing for reorganization of municipalities

U.S. COURTS HTTP://WWW.USCOURTS.GOV/FEDERALCOURTS/BANKRUPTCY/BANKRUPTCY BASICS/CHAPTER9.ASPX CHAPTER 9 Municipality Bankruptcy The chapter of the Bankruptcy Code providing for reorganization of municipalities

Visa Business Card Disclosure Agreement

P.O. Box 8046 Madison, WI 53718-8308 (608) 243-5000 (800) 236-5560 Fax: (608) 243-5029 www.summitcreditunion.com TABULAR DISCLOSURE Annual Percentage Rate 8.00%* (APR for Purchases) Other APR s: Cash Advance

P.O. Box 8046 Madison, WI 53718-8308 (608) 243-5000 (800) 236-5560 Fax: (608) 243-5029 www.summitcreditunion.com TABULAR DISCLOSURE Annual Percentage Rate 8.00%* (APR for Purchases) Other APR s: Cash Advance

SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING AGENDA 1. INFORMATION ON THE SERVICING CENTER

SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING AGENDA 1. INFORMATION ON THE SERVICING CENTER 2. WHAT REQUESTS ARE SUBMITTED TO SERVICING AFTER FINAL

SBA Fresno Commercial Loan Servicing Center Presents GUIDANCE ON SBA 7A LOAN SERVICING & PURCHASING AGENDA 1. INFORMATION ON THE SERVICING CENTER 2. WHAT REQUESTS ARE SUBMITTED TO SERVICING AFTER FINAL

FARM LOAN GUARANTEE PROGRAM

FARM LOAN GUARANTEE PROGRAM LENDER MANUAL Contents ABOUT THIS MANUAL... 4 WHO TO CONTACT... 4 ELIGIBILITY... 5 A. ELIGIBLE LENDERS... 5 Becoming a Participating Lender... 5 B. ELIGIBLE BORROWERS... 5 C.

FARM LOAN GUARANTEE PROGRAM LENDER MANUAL Contents ABOUT THIS MANUAL... 4 WHO TO CONTACT... 4 ELIGIBILITY... 5 A. ELIGIBLE LENDERS... 5 Becoming a Participating Lender... 5 B. ELIGIBLE BORROWERS... 5 C.

ECONOMIC DEVELOPMENT CORPORATION OF THE CITY OF FLINT

ECONOMIC DEVELOPMENT CORPORATION OF THE CITY OF FLINT Dear Applicant: Thank you for your interest in the Economic Development Corporation of the City of Flint loan program. Enclosed are the Commercial

ECONOMIC DEVELOPMENT CORPORATION OF THE CITY OF FLINT Dear Applicant: Thank you for your interest in the Economic Development Corporation of the City of Flint loan program. Enclosed are the Commercial

TOWN OF JAY PROPERTY ASSESSED CLEAN ENERGY (PACE) ORDINANCE

ORDINANCE") TOWN OF JAY PROPERTY ASSESSED CLEAN ENERGY (PACE) ORDINANCE A TRUE COPY ATTEST CERTIFIED BY: Ronda L. Palmer, Town Clerk ENACTED: June 12, 2012 Attest: A true copy of a proposed ordinance entitled: Town

TOWN OF JAY PROPERTY ASSESSED CLEAN ENERGY (PACE) ORDINANCE A TRUE COPY ATTEST CERTIFIED BY: Ronda L. Palmer, Town Clerk ENACTED: June 12, 2012 Attest: A true copy of a proposed ordinance entitled: Town

SBA Policy Notice. TO: All SBA Employees CONTROL NO.: 5000-1382. SUBJECT: Reauthorization of 504 Debt EFFECTIVE: 05/26/2016. Refinancing Program

SBA Policy Notice TO: All SBA Employees CONTROL NO.: 5000-1382 SUBJECT: Reauthorization of 504 Debt Refinancing Program EFFECTIVE: 05/26/2016 The Small Business Jobs Act of 2010 (Jobs Act), P.L. 111-240,

SBA Policy Notice TO: All SBA Employees CONTROL NO.: 5000-1382 SUBJECT: Reauthorization of 504 Debt Refinancing Program EFFECTIVE: 05/26/2016 The Small Business Jobs Act of 2010 (Jobs Act), P.L. 111-240,

State of Illinois Vendor Payment Program. Program Terms December 13, 2012

State of Illinois Vendor Payment Program Program Terms December 13, 2012 Background: As a result of the current cash flow deficit, the State of Illinois (the State ) has been forced to delay payment to

State of Illinois Vendor Payment Program Program Terms December 13, 2012 Background: As a result of the current cash flow deficit, the State of Illinois (the State ) has been forced to delay payment to

COMMERCIAL LOAN APPLICATION

COMMERCIAL LOAN APPLICATION IMPORTANT APPLICANT INFORMATION: Federal law requires financial institutions to obtain sufficient information to verify your identify. You may be asked several questions and

COMMERCIAL LOAN APPLICATION IMPORTANT APPLICANT INFORMATION: Federal law requires financial institutions to obtain sufficient information to verify your identify. You may be asked several questions and

Contract Financing for the Contractor

a Contract Financing for the Contractor SBA s Contract CAPLines Program A Presentation For The Contractor SBA has a Loan Guaranty Program To help Contractors Obtain Financing for Contract Work Its Called

a Contract Financing for the Contractor SBA s Contract CAPLines Program A Presentation For The Contractor SBA has a Loan Guaranty Program To help Contractors Obtain Financing for Contract Work Its Called

FEDERAL RESERVE BANK OF NEW YORK BORROWER-IN-CUSTODY (BIC) OF COLLATERAL CERTIFICATION FORM

OF COLLATERAL CERTIFICATION FORM") FEDERAL RESERVE BANK OF NEW YORK BORROWER-IN-CUSTODY (BIC) OF COLLATERAL CERTIFICATION FORM A. DEPOSITORY INSTITUTION INFORMATION Institution Name: Address: City/State/Zip: ABA: Primary Regulator (Agency

FEDERAL RESERVE BANK OF NEW YORK BORROWER-IN-CUSTODY (BIC) OF COLLATERAL CERTIFICATION FORM A. DEPOSITORY INSTITUTION INFORMATION Institution Name: Address: City/State/Zip: ABA: Primary Regulator (Agency

SENATE BILL No. 358. Introduced by Senator Ducheny. February 25, 2009

SENATE BILL No. Introduced by Senator Ducheny February, 00 An act to amend Section 00 of, and to add Article 0 (commencing with Section 0) to Chapter of Part of Division of Title of, the Corporations Code,

SENATE BILL No. Introduced by Senator Ducheny February, 00 An act to amend Section 00 of, and to add Article 0 (commencing with Section 0) to Chapter of Part of Division of Title of, the Corporations Code,

USDA Forest Service FS-2700-11 (08/06) OMB No. 0596-0082 (Exp. 05/2009) Authorization ID: Contact ID: Use Code:

OMB No. 0596-0082 (Exp. 05/2009) Authorization ID: Contact ID: Use Code:") USDA Forest Service FS-2700-11 (08/06) OMB No. 0596-0082 (Exp. 05/2009) Authorization ID: Contact ID: Use Code: AGREEMENT CONCERNING A SMALL BUSINESS ADMINISTRATION LOAN FOR A HOLDER OF A SPECIAL USE PERMIT

USDA Forest Service FS-2700-11 (08/06) OMB No. 0596-0082 (Exp. 05/2009) Authorization ID: Contact ID: Use Code: AGREEMENT CONCERNING A SMALL BUSINESS ADMINISTRATION LOAN FOR A HOLDER OF A SPECIAL USE PERMIT

Title 33: PROPERTY. Chapter 9: MORTGAGES OF REAL PROPERTY. Table of Contents

Title 33: PROPERTY Chapter 9: MORTGAGES OF REAL PROPERTY Table of Contents Subchapter 1. GENERAL PROVISIONS... 3 Section 501. FORMS... 3 Section 501-A. "POWER OF SALE"... 3 Section 502. ENTRY BY MORTGAGEE...

Title 33: PROPERTY Chapter 9: MORTGAGES OF REAL PROPERTY Table of Contents Subchapter 1. GENERAL PROVISIONS... 3 Section 501. FORMS... 3 Section 501-A. "POWER OF SALE"... 3 Section 502. ENTRY BY MORTGAGEE...

PARTNERSHIP AGREEMENT

PARTNERSHIP AGREEMENT I. INTRODUCTORY The parties to this agreement,, hereinafter referred to as the first party, and, hereinafter referred to as the second party, and both hereinafter referred to as the

PARTNERSHIP AGREEMENT I. INTRODUCTORY The parties to this agreement,, hereinafter referred to as the first party, and, hereinafter referred to as the second party, and both hereinafter referred to as the

Revolving Loan Fund Application Form

Revolving Loan Fund Application Form Instructions For Application Form Sections I, II, III. Please provide the information requested. "You" refers to the proprietor, general partner, or corporate officer

Revolving Loan Fund Application Form Instructions For Application Form Sections I, II, III. Please provide the information requested. "You" refers to the proprietor, general partner, or corporate officer