Hedge Fund Investment Thesis Payment Networks and MasterCard. What I Learnt on Wall Street June 2016

|

|

|

- Erin Simmons

- 7 years ago

- Views:

Transcription

1 Hedge Fund Investment Thesis Payment Networks and MasterCard What I Learnt on Wall Street June 2016

. MasterCard operates a duopoly in the electronic payments market.")

2 What is it? 2 MasterCard is a payment technology and network company, operating the world s second largest payment network connecting banks, consumers, and merchants in over 210 countries. MasterCard was collectively owned by the banks until it became public in 2006 (Visa went public in 2008). MasterCard operates a duopoly in the electronic payments market. 85% of all retail transactions globally are still in cash. MasterCard will benefit from : a) the transition to electronic payments b) increase in personal consumption spending (PCE) c) rising middle class in Emerging Markets.

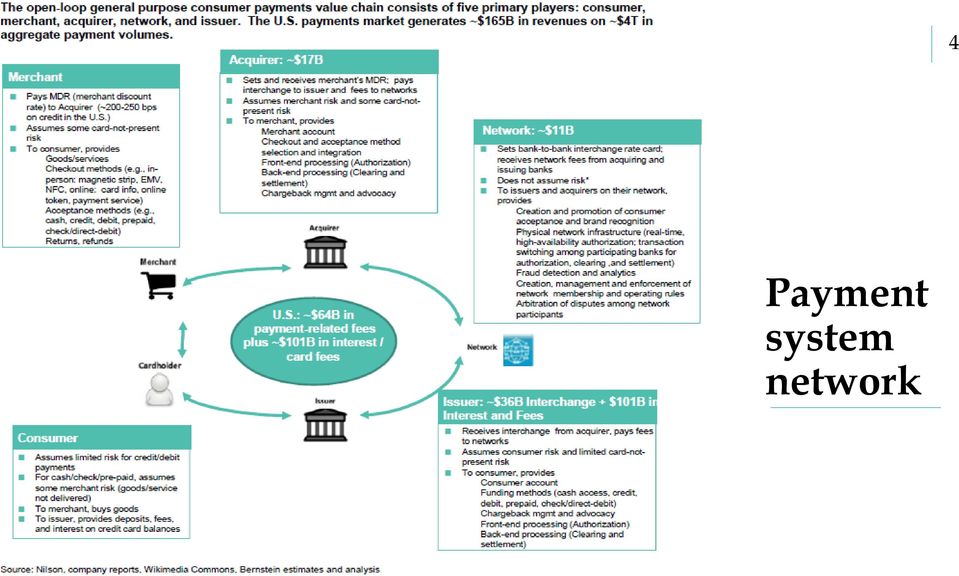

3 How does the credit card ecosystem work? 3 At the highest level, the electronic payment ecosystem is funded indirectly through the Merchant Discount Rate (MDR), a fee embedded in the sales price of products purchased at a retailer. The MDR encompasses all the transaction related fees associated with processing, settling, and clearing a transaction through all participants in the network and is subtracted from the total amount paid by the consumer when payment is remitted to the merchant. The MDR is negotiated between a merchant acquirer and a merchant, and caries significantly based on the merchant s purchase volume: the higher the merchant s purchase volume, the lower the MDR.

4 Payment system network 4

5 What is the MDR 5 The MDR is composed of the following fees: Interchange Interchange typically comprises the largest portion of the MDR in a transaction, and is intended to cover the cost of cardholder charge offs and most credit card fraud. At the low end, interchange ranges between a flat fee of $0.23 (for a debit transaction), and 2.95% at the high end (when a premium high-end credit card is used). Interchange rates for various transaction and card types are set by the card networks, although issuing banks receive the entire interchange fee, Visa and MasterCard do not receive any portion of the interchange fee. Interchange received the greatest scrutiny of any aspect of the electronic payment ecosystem over the past five years. As part of the Dodd-Frank financial reform legislation in the United States, Congress sought to regulate the fees charged by banks for consumer credit card transactions (see our discussion of regulation elsewhere in this report).

6 MDR continued 6 Network and data processing fee The network fee is charged by the card network for routing the transaction, and is typically in the range of 4 25 bps of the purchase price. Merchant acquiring/processing fees The processing fee is charged by the merchant s credit card processor for transaction handling and clearing on the merchant side, and is typically assessed as a fixed fee (for example $ $0.10 per transaction, depending on volume). The acquiring fee is changed by the merchant s acquiring bank for handling and settling the transaction, and is intended to cover costs related to settling transaction balances with merchants, as well as the cost of merchant fraud.

.")

7 Business Overview 7 MasterCard is a technology company in the global payments industry that connects consumers, financial institutions, merchants, governments and businesses worldwide, enabling them to use electronic forms of payment instead of cash and checks. A typical transaction on their network involves four participants, in addition to MasterCard: card holder, merchant, issuer (card holder s financial institution) and the acquirer (the merchant s financial institution).

8 Business Overview (Contd.) 8

8")

9 Business Drivers 9 Consumption growth Card Penetration into Cash economy Growth in online / electronic payment

10 Consumption Growth 10 Payment volumes rise and fall with personal consumption expenditure PCE Certain countries have higher growth in PCE, while others lag. In addition you have to understand what types of PCE spending could a card be used. Simplistically one can assume that 60% of global GDP is PCE and a then a smaller 80% of PCE is Purchase PCE. PCE that isn t purchased : Housing expenses, healthcare (ex-out of pocket), Financial Services, Social Security If GDP grows 3% globally, then consumption grows ~5-6%per annum.

, Financial Services, Social Security If GDP grows 3%")

11 Card Penetration 11 In terms of growth attribution, Visa and MasterCard estimate that : 50% comes from cash/check penetration 25% from PCE growth globally & 25% from pricing. Management guided to for : 11-14% CAGR revenue growth, minimum of 50% operating margins and at least 20% CAGR of EPS. Card penetration is estimated to be about ~40% currently, and is expected to grow 2-4% per annum.

12 Cash to Electronic Transition: 12 Both Visa & MasterCard are focused on the singular growth opportunity surrounding cash transaction volume. According to Visa s estimate, of the ~$13 trillion PCE in Developed Markets, 41% is still in Cash / Check. This represent a ~$5 trillion opportunity, growing at 4% per annum. This implies that PCE is growing at ~$500 billion per annum. While in Emerging Markets, the PCE is ~$10 trillion, with 62% in Cash / Check. This represents a ~$6 trillion opportunity growing at 10% per annum. This means that only is there a ~$6 trillion opportunity there today, but that PCE as a whole is growing at ~$1 trillion per annum.

13 EM Penetration Levels: 13 Penetration levels of at least 60-70% are attainable, as some countries are there already while many lag far behind.

14 Revenue Drivers: 14 Domestic assessments: fees charged to issuers and acquirers based primarily on the dollar volume of activity on cards and other devices. The revenue here is a function of: a) assessment fee b) GDV and c) rebates as a % of revenues. These fees have historically been 9-10 bps. GDV is expected to grow as a function of a) number of cards issued and b) growth in mobile payments. Broadly about a transition from cash to electronic payments. Cross-border volume fees: cross border volume fees are charged to issuers and acquirers based on the GDV of activity where the merchant country and issue country are different. MA charges a cross-border fee equal to 0.8% of the transaction amount on all international purchases. In some circumstances when the transaction is in a foreign currency, a currency conversion fee is also charged. Cross-border volumes are a function of the travel market, as more people go abroad, higher likelihood of cross border fees.

15 Revenue Drivers (continued) 15 Transaction processing fees: fees charged for both domestic and cross-border transactions, based on the number of transactions. The revenues here are a function of: a) MA connectivity fee b) total transactions processed c) authorization / settlement and switch fee per transaction and d) rebates as a % of revenues. Authorization fees have historically been 7 cents per transaction. Connectivity fee of 0.5 cents per transaction. Service fees: fees charged for consulting, research, compliance and penalties.

rebates as a % of revenues. Authorization fees have historically been 7 cents per transaction.")

16 Business Economics 16 Of the 1-4% fee charged at purchase, MasterCard gets about 20 bps. About 150 bps goes to the buyers / customers bank. Another bps to the hardware partner, the MSP (merchant service provider), merchant s bank. Effectively by using the MasterCard network, the merchant and buyer is signing up to pay them an incremental 20 bps. Not a high number, and not one likely to change / impact purchase decisions. MasterCard has significant operating leverage in the business, between 2009 and 2013, revenues grew by 60-65%, but net income grew by over 100%, and earnings per share grew by over 130% (due to buy backs).

17 MasterCard's goals: Increase their core businesses globally, both for products such as credit, debit, prepaid and commercial and increasing the number of payment transactions 2. Seek new areas of growth in New markets Encourage current consumers / businesses to use MasterCard for new payment areas Bring in SMEs which have not historically used MasterCard products Financial inclusion for the unbanked and under banked Building new areas of business by: Taking advantage of the opportunities from the convergence of physical and digital worlds; Using data analytics, loyalty solutions and fraud protection services to add value

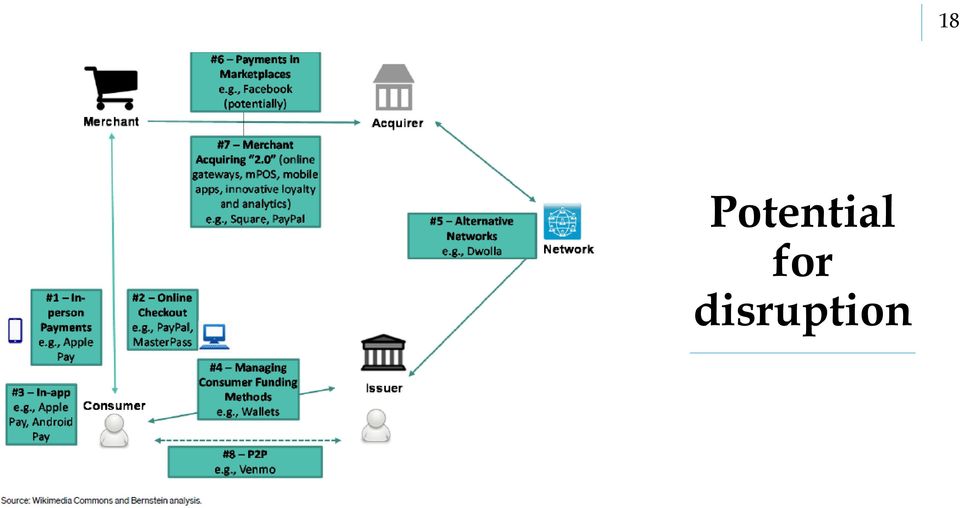

18 Potential for disruption 18

19 Understanding the duopoly & its impact 19 Both Visa and MasterCard make about bps in net yield per transaction. This amount is relatively stable, and slightly higher for Visa. Net Yield = Net revenue (revenue after the impact of client incentives) per $100 purchase volumes.

20 What impacts yield 20 Yields are a dynamic equilibrium and are driven by the following forces: Negative for yields: Increased client incentives Increasing debit mix Lower mix of cross border volumes Positive for yields: Growth in online retail Online has higher credit vs debit usage Increase in international processing

21 Long term risks to yield 21 The biggest risk to the industry is a loss of duopoly pricing power This can come from a loss of price discipline or new technology

22 Can margins grow? 22 These are high tech payment networks, so there should be a lot of room for margin growth with growing volume and scale. But what is the evidence? Visa which is 2x the size of MA, has a higher margins than MA MA: ~50% JPM: ~60%

23 Why the difference in margin 23

24 Simple Model 24 Volume Growth: 8-10% Revenue Growth: 8-10% Net Income Growth: 13-16% (from operating leverage / margin expansion) EPS Growth: 16-20% (from buy backs) While PCE only grows at 5-6%, with growing penetration you can get 3-4% of additional volume growth, especially a lot of the growth comes from EM countries where both PCE and penetration are growing faster.

25 Simple Model (Contd.) 25 Income Statement Year Domestic Assessments 3,387 3,688 3,967 4,108 4,590 5,090 Cross Border Volume Fees 2,268 2,715 3,054 3,213 3,590 3,990 Transaction Processing Fees 3,199 3,554 4,035 4,358 4,800 5,300 Other Revenues 1,154 1,331 1,688 2,014 2,180 2,300 Rebates and Incentives -2,617-2,976-3,303-3,936-4,300-4,800 Total Revenue 7,391 8,312 9,441 9,757 10,860 11,880 Revenue Growth 12% 14% 3% 11% 9% General & Administrative (COGS) 2,429 2,615 3,152 3,185 3,365 3,500 Gross Margin 67% 69% 67% 67% 69% 71% Advertising & Development EBITDA 4,187 4,856 5,427 5,713 6,606 7,450 EBITDA Margins 57% 58% 57% 59% 61% 63% Depreciation Operating Income / EBIT 3,957 4,598 5,106 5,370 6,259 7,090 EBIT Margin 54% 55% 54% 55% 58% 60% Interest / Investment Income Pre-tax Income 3,952 4,595 5,079 5,330 6,227 7,060 Tax 1,181 1,414 1,462 1,467 1,744 1,977 Tax Rate % 29.9% 30.8% 28.8% 27.5% 28.0% 28.0% Net Income 2,771 3,181 3,617 3,863 4,483 5,083 Shares Outstanding 1,255 1,216 1,168 1,136 1, EPS EPS Growth 18.5% 18.4% 9.8% 20.1% 17.4% Cash flow Model Cashflow from Operations 3,001 3,439 3,938 4,206 4,830 5,443 Capex Free Cash flow 2,783 3,139 3,604 3,926 4,500 5,143 FCF Yield 3.65% 4.18% 4.78% FCF Growth 14.6% 14.3%

26 Global Payment Processors Comp Sheet 26 MasterCard Visa American Express Market Cap ($, bn) Revenues ($, bn) Operating Margin % 55% 64% 26% Free Cashflow Yield % 3.5% 3.6% P/E Multiple (2015) ROE 50% 20% 29% Operating Exp /Transaction Personnel Costs/Transaction (cents) Advertising as % of Opex 20% 20% Personnel as % of Opex 47% 41% Global Credit Card Market Share 30% 41% US Credit Card Market Share 22% 47% Europe Credit Card Market Share 30% 1% Payment Volume Growth 13% 10% Revenue Growth % 13% 11% Net Income Growth % 16% 13% Europe % of Volume 28% 1% US % of Volume 35% 52% EM % of Volume 33% 42%

27 MasterCard vs Visa? 27 Both are driven by the same big themes: Card penetration PCE growth Stable yields Buy backs MasterCard also gives you potential for margin improvement / cost cutting and ex-us (EM) share gain

28 Impact of EURUSD 28 About 30% of MasterCard s revenue is non-usd, primarily earned in Europe. This adds an Additional layer of volatility and noise when EURUSD have large moves. In 2015, when EURUSD depreciated significantly, top line & income growth was impacted.

29 Valuation 29 MasterCard isn t cheap if you can assume that valuation multiples can stay around 23-25x, then you can buy this with a 2-3 year view as a multiyear compounder.

30 When to buy this stock 30 On weakness!

31 When to buy this stock (cont d) 31 In late 2014, the market was unsure about their business, and the stock had gone nowhere for over a year. This seemed out of place to us given their growing top line. We began buying in the high 70 s. In late 2015, around $95-100, we sold 25-30% of the position, since the multiple has re-rated without a growth in earnings. Even the best businesses and stocks have 10-20% moves in a year. Do your work and then be ready.

32 Appendix 32 History of MasterCard: 1966: Founded as the Interbank Card Association (ICA) 1969: "Master Charge purchased by the California Bank Association 1979: Renamed MasterCard to reflect a commitment to international growth 1985: Acquired an interest in EuroCard (predecessor to Europay International) 1988: Acquired the Cirrus ATM Network 1991: Launched Maestro, the world s first online point-of-sale debit network 1997: Launched Priceless advertising campaign 2001: Launched MasterCard Advisors, the largest global consultancy focused on the payments industry 2002: Merged with Europay International

33 Appendix (Contd.) : Converted from a membership association to a private share corporation 2006: Transitioned to a public company with a new corporate governance and ownership structure MasterCard begins trading on the New York Stock Exchange under ticker symbol MA. The MasterCard Foundation was formed 2010: Ajay Banga named CEO 2010: Launched MasterCard Labs to promote greater innovation in electronic payments 2010: Acquired DataCash Group plc, to expand e-commerce payment solutions 2011: Completes acquisition of the prepaid card program management operations of Travelex (now referred to as Access Prepaid Worldwide) and announced a joint venture with Telefónica to offer mobile financial solutions in Latin America 2012: Acquired Truaxis, Inc., a California-based provider of credit and debit card-linked offers made to consumers through merchants and financial institutions : Introduced MasterPass, established HomeSend joint venture with eservglobal and Bics, and acquired Provus and C-SA

We believe First Data is well positioned to take advantage of all of these trends given the breadth of our solutions and our global operating

Given recent payment data breaches, clients are increasingly demanding robust security and fraud solutions; and Financial institutions continue to outsource and leverage technology providers given their

Given recent payment data breaches, clients are increasingly demanding robust security and fraud solutions; and Financial institutions continue to outsource and leverage technology providers given their

TSYS Analyst Day May 20, 2015. 2015 Total System Services, Inc. All rights reserved worldwide.

TSYS Analyst Day May 20, 2015 > FORWARD-LOOKING STATEMENTS This presentation and comments made by management contain forward-looking statements including, among others, statements regarding the expected

TSYS Analyst Day May 20, 2015 > FORWARD-LOOKING STATEMENTS This presentation and comments made by management contain forward-looking statements including, among others, statements regarding the expected

eservglobal Investor Roadshow January, 2014

eservglobal Investor Roadshow January, 2014 eservglobal is an internationally recognised, leading provider of solutions that bridge the telco and financial worlds eservglobal: at a glance Comprehensive

eservglobal Investor Roadshow January, 2014 eservglobal is an internationally recognised, leading provider of solutions that bridge the telco and financial worlds eservglobal: at a glance Comprehensive

[ What the Changes Mean, and How to Get Your Share of the Savings ]

![[ What the Changes Mean, and How to Get Your Share of the Savings ]](/thumbs/27/11052426.jpg "[ What the Changes Mean, and How to Get Your Share of the Savings ]") Dancing With Debit After the Durbin Amendment [ What the Changes Mean, and How to Get Your Share of the Savings ] By Dan Toughey, President, TouchNet Information Systems, Inc. For the college business

Dancing With Debit After the Durbin Amendment [ What the Changes Mean, and How to Get Your Share of the Savings ] By Dan Toughey, President, TouchNet Information Systems, Inc. For the college business

Canadian Tire: Value Under the Hood

Canadian Tire: Value Under the Hood May 2006 Pershing Square Capital Management, L.P. Disclaimer Pershing Square Capital Management's ("Pershing") analysis and conclusions regarding Canadian Tire Corporation

Canadian Tire: Value Under the Hood May 2006 Pershing Square Capital Management, L.P. Disclaimer Pershing Square Capital Management's ("Pershing") analysis and conclusions regarding Canadian Tire Corporation

Heartland Payment Systems Inc. April 11, 2014

Heartland Payment Systems Inc. April 11, 2014 General Overview Heartland Payment Systems (HPY) provides electronic payment processing for merchants. They install point-of-sale terminals for their Small

Heartland Payment Systems Inc. April 11, 2014 General Overview Heartland Payment Systems (HPY) provides electronic payment processing for merchants. They install point-of-sale terminals for their Small

2015 annual results. 16 th March 2016

2015 annual results 16 th March 2016 Legal disclaimer Certain statements in this document are forward-looking statements. These forward-looking statements speak only as at the date of this document. These

2015 annual results 16 th March 2016 Legal disclaimer Certain statements in this document are forward-looking statements. These forward-looking statements speak only as at the date of this document. These

2013 Full Year Results. 28 March 2014

2013 Full Year Results 28 March 2014 Agenda 1. Full year highlights 2. Business performance 3. Corporate strategy 4. Summary Full year highlights 3 Full year highlights Exceptional full year results -

2013 Full Year Results 28 March 2014 Agenda 1. Full year highlights 2. Business performance 3. Corporate strategy 4. Summary Full year highlights 3 Full year highlights Exceptional full year results -

Equity Analysis and Capital Structure. A New Venture s Perspective

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

A S H A R E D J O U R N E Y MasterCard Annual Report 2014

A SHARED JOURNEY MasterCard Annual Report 2014 SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA For the Years Ended December 31 (in millions, except per share and operating data) 2014 2013 2012 Statement

A SHARED JOURNEY MasterCard Annual Report 2014 SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA For the Years Ended December 31 (in millions, except per share and operating data) 2014 2013 2012 Statement

Banking Fees in Australia

Banking Fees in Australia The Reserve Bank has conducted a survey on bank fees each year since 1997. The results of the latest survey show that banks aggregate fee income was unchanged in 2. Fee income

Banking Fees in Australia The Reserve Bank has conducted a survey on bank fees each year since 1997. The results of the latest survey show that banks aggregate fee income was unchanged in 2. Fee income

by DualCurrency Systems

Introducing Universal Reward Solutions SM and In-Network Advantage SM by DualCurrency Systems Affinity and Loyalty Marketing Beyond Discounts DualCurrency: Stretching Cash with Rewards With traditional

Introducing Universal Reward Solutions SM and In-Network Advantage SM by DualCurrency Systems Affinity and Loyalty Marketing Beyond Discounts DualCurrency: Stretching Cash with Rewards With traditional

J.P. MORGAN CHASE & CO.: THE CREDIT CARD SEGMENT OF

SENEM ACET COSKUN BUS 9200 - FALL 2008 - MIDTERM J.P. MORGAN CHASE & CO.: THE CREDIT CARD SEGMENT OF THE FINANCIAL SERVICES INDUSTRY I-Executive Summary Consumers are increasingly using plastic cards and

SENEM ACET COSKUN BUS 9200 - FALL 2008 - MIDTERM J.P. MORGAN CHASE & CO.: THE CREDIT CARD SEGMENT OF THE FINANCIAL SERVICES INDUSTRY I-Executive Summary Consumers are increasingly using plastic cards and

European Payment Card Systems for the 21 st Century. A paper from MasterCard Europe

U European Payment Card Systems for the 21 st Century A paper from MasterCard Europe For four decades, MasterCard Europe 1 has been working successfully with European banks to deliver secure, efficient

U European Payment Card Systems for the 21 st Century A paper from MasterCard Europe For four decades, MasterCard Europe 1 has been working successfully with European banks to deliver secure, efficient

How to Talk to Vendors about Accepting Card Payments

How to Talk to Vendors about Accepting Card Payments Presented by: David Nakagawa Maureen Sudbay Kristen Bolden Visa Overview 14,600 Financial institution clients 1 2.2 billion Visa cards (as of June 30,

How to Talk to Vendors about Accepting Card Payments Presented by: David Nakagawa Maureen Sudbay Kristen Bolden Visa Overview 14,600 Financial institution clients 1 2.2 billion Visa cards (as of June 30,

MASTERCARD INC FORM 10-K. (Annual Report) Filed 02/13/15 for the Period Ending 12/31/14

Filed 02/13/15 for the Period Ending 12/31/14") MASTERCARD INC FORM 10-K (Annual Report) Filed 02/13/15 for the Period Ending 12/31/14 Address 2000 PURCHASE STREET PURCHASE, NY 10577 Telephone 9142492000 CIK 0001141391 Symbol MA SIC Code 7389 - Business

MASTERCARD INC FORM 10-K (Annual Report) Filed 02/13/15 for the Period Ending 12/31/14 Address 2000 PURCHASE STREET PURCHASE, NY 10577 Telephone 9142492000 CIK 0001141391 Symbol MA SIC Code 7389 - Business

ACHIEVING OUR VISION A WORLD BEYOND CASH

ACHIEVING OUR VISION A WORLD BEYOND CASH MasterCard Annual Report 2013 SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA For the Years Ended December 31 (in millions, except per share and operating data) 2013

ACHIEVING OUR VISION A WORLD BEYOND CASH MasterCard Annual Report 2013 SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA For the Years Ended December 31 (in millions, except per share and operating data) 2013

Understanding Your Merchant Fees Presented by:

Understanding Your Merchant Fees Presented by: Melinda Speer Terry Endres VP Strategic Sales Executive SVP Treasury Management Officer Health, Institutions, & Government Government Treasury Services Chicago,

Understanding Your Merchant Fees Presented by: Melinda Speer Terry Endres VP Strategic Sales Executive SVP Treasury Management Officer Health, Institutions, & Government Government Treasury Services Chicago,

E LE CTRO NI C PAYME NT SYSTE M S 101 ELECTRONIC PAYMENT SYSTEMS 101. Amitabh Saxena, Managing Director, Digital Disruptions

E LE CTRO NI C PAYE NT SYSTE S 101 ELECTRONIC PAYENT SYSTES 101 Amitabh Saxena, anaging Director, Digital Disruptions Definitions and History In its simplest form, a payment is any exchange of value between

E LE CTRO NI C PAYE NT SYSTE S 101 ELECTRONIC PAYENT SYSTES 101 Amitabh Saxena, anaging Director, Digital Disruptions Definitions and History In its simplest form, a payment is any exchange of value between

Reed Elsevier Results 2013 Erik Engstrom, CEO Duncan Palmer, CFO

Reed Elsevier Results Erik Engstrom, CEO Duncan Palmer, CFO FORWARD-LOOKING STATEMENTS This presentation contains forward-looking statements within the meaning of Section 27A of the US Securities Act of

Reed Elsevier Results Erik Engstrom, CEO Duncan Palmer, CFO FORWARD-LOOKING STATEMENTS This presentation contains forward-looking statements within the meaning of Section 27A of the US Securities Act of

Powering Global Commerce. Company Overview May 2015

Powering Global Commerce Company Overview May 2015 Disclaimer Forward-looking Statements. Use of Non-GAAP financial measures 2 This presentation and comments made by management contain forward-looking

Powering Global Commerce Company Overview May 2015 Disclaimer Forward-looking Statements. Use of Non-GAAP financial measures 2 This presentation and comments made by management contain forward-looking

FURTHER PROFIT GROWTH IN FIRST-HALF 2015

FURTHER PROFIT GROWTH IN FIRST-HALF 2015 Net sales of 37.7bn, up +5.2% (+2.9% on an organic basis) Growth in Recurring Operating Income: 726m, +2.6% at constant rates Strong growth in adjusted net income,

FURTHER PROFIT GROWTH IN FIRST-HALF 2015 Net sales of 37.7bn, up +5.2% (+2.9% on an organic basis) Growth in Recurring Operating Income: 726m, +2.6% at constant rates Strong growth in adjusted net income,

Position Paper. issuers. how to leverage EC s regulation proposal. on interchange fees for card-based payment transactions

Position Paper issuers how to leverage EC s regulation proposal on interchange fees for card-based payment transactions The issuing landscape has dramatically changed over the last few years increased

Position Paper issuers how to leverage EC s regulation proposal on interchange fees for card-based payment transactions The issuing landscape has dramatically changed over the last few years increased

2015 Fourth Quarter and Full Year Results Acquisition of TransFirst

Acquisition of TransFirst January 26, 2016 2016 Total System Services, Inc. All rights reserved worldwide. > CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS This presentation contains statements that

Acquisition of TransFirst January 26, 2016 2016 Total System Services, Inc. All rights reserved worldwide. > CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS This presentation contains statements that

STEADY DOMESTIC CASHFLOW EXPLOSIVE INTERNATIONAL GROWTH

STEADY DOMESTIC CASHFLOW EXPLOSIVE INTERNATIONAL GROWTH 1 REQUIRED STATEMENT ABOUT FORECASTS Calpian s models and projections are based on certain key assumptions, including but not limited to the following:

STEADY DOMESTIC CASHFLOW EXPLOSIVE INTERNATIONAL GROWTH 1 REQUIRED STATEMENT ABOUT FORECASTS Calpian s models and projections are based on certain key assumptions, including but not limited to the following:

American Express Global Business to Business Group. Ed Gilligan Vice Chairman and Group CEO

American Express Global Business to Business Group Ed Gilligan Vice Chairman and Group CEO August 6, 2008 Agenda B2B Business Model Tale of Two Segments Future Outlook 2 B2B Overview Global Commercial

American Express Global Business to Business Group Ed Gilligan Vice Chairman and Group CEO August 6, 2008 Agenda B2B Business Model Tale of Two Segments Future Outlook 2 B2B Overview Global Commercial

Equifax Reports Fourth Quarter and Full Year 2008 Results; Provides First Quarter 2009 Guidance

1550 Peachtree Street, N.W. Atlanta, Georgia 30309 NEWS RELEASE Contact: Jeff Dodge Tim Klein Investor Relations Media Relations (404) 885-8804 (404) 885-8555 jeff.dodge@equifax.com tim.klein@equifax.com

1550 Peachtree Street, N.W. Atlanta, Georgia 30309 NEWS RELEASE Contact: Jeff Dodge Tim Klein Investor Relations Media Relations (404) 885-8804 (404) 885-8555 jeff.dodge@equifax.com tim.klein@equifax.com

GAAP quarterly net income of $1.9 billion or $0.80 per share including non-cash, non-operating

Visa Inc. Reports Fiscal First Quarter 2016 Results GAAP quarterly net income of $1.9 billion or $0.80 per share including non-cash, non-operating income related to the revaluation of the Visa Europe put

Visa Inc. Reports Fiscal First Quarter 2016 Results GAAP quarterly net income of $1.9 billion or $0.80 per share including non-cash, non-operating income related to the revaluation of the Visa Europe put

World-wide trends in innovation on the acquiring side

World-wide trends in innovation on the acquiring side CPSS-World Bank retail payments forum Perugia, March 19 th 2013 Edgar, Dunn & Company, 2013 Yogesh Oka Yogesh.Oka@edgardunn.com David Poe David.Poe@edgardunn.com

World-wide trends in innovation on the acquiring side CPSS-World Bank retail payments forum Perugia, March 19 th 2013 Edgar, Dunn & Company, 2013 Yogesh Oka Yogesh.Oka@edgardunn.com David Poe David.Poe@edgardunn.com

Payment Card Reform Framework. Concept Paper

Payment Concept Paper Issued on: 10 October 2014 Card Reform Framework TABLE OF CONTENTS PREFACE 1 PART A OVERVIEW... 2 1. Introduction 2 2. Objective... 8 3. Scope. 8 4. Applicability... 9 5. Legal provisions..

Payment Concept Paper Issued on: 10 October 2014 Card Reform Framework TABLE OF CONTENTS PREFACE 1 PART A OVERVIEW... 2 1. Introduction 2 2. Objective... 8 3. Scope. 8 4. Applicability... 9 5. Legal provisions..

ACQUIRER PASS THROUGH FEES

ACQUIRER PASS THROUGH FEES BASED ON VOLUME BASED ON NUMBER OF TRANSACTIONS ASSESSMENTS (V/MC/DISC) VISA SETTLEMENT NETWORK ACCESS FEE VISA INTERNATIONAL ASSESSMENT FEE VISA INTERNATIONAL ACQUIRER FEE MASTERCARD

ACQUIRER PASS THROUGH FEES BASED ON VOLUME BASED ON NUMBER OF TRANSACTIONS ASSESSMENTS (V/MC/DISC) VISA SETTLEMENT NETWORK ACCESS FEE VISA INTERNATIONAL ASSESSMENT FEE VISA INTERNATIONAL ACQUIRER FEE MASTERCARD

A world beyond cash: priceless. MasterCard Annual Report 2011

A world beyond cash: priceless MasterCard Annual Report 2011 Summary Consolidated Financial and Other Data All figures throughout this report in U.S. dollars For the Years Ended December 31 (in millions

A world beyond cash: priceless MasterCard Annual Report 2011 Summary Consolidated Financial and Other Data All figures throughout this report in U.S. dollars For the Years Ended December 31 (in millions

THOUGHT LEADERSHIP THE GOLDEN AGE OF CARD PAYMENTS

THOUGHT LEADERSHIP THE GOLDEN AGE OF CARD PAYMENTS 1 TABLE OF CONTENTS EXECUTIVE SUMMARY... 3 HISTORICALLY, COSTS HAVE STYMIED GROWTH OF CARD PAYMENTS... 3 GOLDEN AGE OF CARD PAYMENTS... 5 MORE VOLATILITY

THOUGHT LEADERSHIP THE GOLDEN AGE OF CARD PAYMENTS 1 TABLE OF CONTENTS EXECUTIVE SUMMARY... 3 HISTORICALLY, COSTS HAVE STYMIED GROWTH OF CARD PAYMENTS... 3 GOLDEN AGE OF CARD PAYMENTS... 5 MORE VOLATILITY

Western Union (WU) Raimondas Lencevicius

Raimondas Lencevicius") Western Union (WU) Raimondas Lencevicius Disclaimers I am not a registered investment advisor and I do not offer any investment advise No parts of this talk are suggestions to invest, not invest, buy or

Western Union (WU) Raimondas Lencevicius Disclaimers I am not a registered investment advisor and I do not offer any investment advise No parts of this talk are suggestions to invest, not invest, buy or

UK Card Payments 2014

UK Card Payments 2014 THE UK CARDS ASSOCIATION Payment cards are the most popular non-cash payment method in the UK by volume. They allow cardholders to pay for goods and services easily and conveniently,

UK Card Payments 2014 THE UK CARDS ASSOCIATION Payment cards are the most popular non-cash payment method in the UK by volume. They allow cardholders to pay for goods and services easily and conveniently,

Introduction to Bankcard Basics

Introduction to Bankcard Basics Global Vision Group August 2006 Page -1- Contents Topic Background The Players Transaction Authorization and Settlement Types of Card Products & Competition Credit Decision

Introduction to Bankcard Basics Global Vision Group August 2006 Page -1- Contents Topic Background The Players Transaction Authorization and Settlement Types of Card Products & Competition Credit Decision

Credit vs. Debit: The Network Perspective

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

International Processing for the Financial Industry

Payment Services International for the Financial Industry State-of-the-art transaction processing and an unparalleled bandwidth of operational services to support banks and payment service providers worldwide.

Payment Services International for the Financial Industry State-of-the-art transaction processing and an unparalleled bandwidth of operational services to support banks and payment service providers worldwide.

Payments Package: Questions and Answers

Payments Package: Questions and Answers Date: November 2013 Contact: Ruth Milligan, T: +32 2 737 05 95, milligan@eurocommerce.be A. Introduction The Commission published its Payments Package on 24 July

Payments Package: Questions and Answers Date: November 2013 Contact: Ruth Milligan, T: +32 2 737 05 95, milligan@eurocommerce.be A. Introduction The Commission published its Payments Package on 24 July

OptimizeRx OPRX. Buy. Platform Potential Continues to Grow $0.87 $4.00. Refer to the last two pages of this report for Disclosures

Nov 14, 2014 Healthcare OptimizeRx Platform Potential Continues to Grow Other OTC OPRX Buy Rating Unchanged Current Price $0.87 Target Price $4.00 Market Capitalization 20.32M Shares Outstanding 23.36M

Nov 14, 2014 Healthcare OptimizeRx Platform Potential Continues to Grow Other OTC OPRX Buy Rating Unchanged Current Price $0.87 Target Price $4.00 Market Capitalization 20.32M Shares Outstanding 23.36M

Decision on the CMA s review of the Credit Cards (Merchant Acquisition) Order 1990

Order 1990") Decision on the CMA s review of the Credit Cards (Merchant Acquisition) Order 1990 Contents Page Summary... 1 Introduction... 2 Background... 4 Monitoring activity... 7 Market developments... 7 Stakeholder

Decision on the CMA s review of the Credit Cards (Merchant Acquisition) Order 1990 Contents Page Summary... 1 Introduction... 2 Background... 4 Monitoring activity... 7 Market developments... 7 Stakeholder

Belden. Leading the Way to an Interconnected World. December 2015. 2015 Belden Inc. belden.com @BeldenInc

Belden Leading the Way to an Interconnected World December 2015 2015 Belden Inc. belden.com @BeldenInc Leading The Way to an Interconnected World Delivering highly-engineered signal transmission solutions

Belden Leading the Way to an Interconnected World December 2015 2015 Belden Inc. belden.com @BeldenInc Leading The Way to an Interconnected World Delivering highly-engineered signal transmission solutions

An Insightful Analysis Report on APPLE,INC

An Insightful Analysis Report on APPLE,INC Analysis Conducted by: Yiyan Wang & Xuequan Ma UConn SMF: 2014-2015 Prepared on: April 7 th, 2015 Executive Summary Apple Stock Price VS SP500 in 5 Years Business

An Insightful Analysis Report on APPLE,INC Analysis Conducted by: Yiyan Wang & Xuequan Ma UConn SMF: 2014-2015 Prepared on: April 7 th, 2015 Executive Summary Apple Stock Price VS SP500 in 5 Years Business

Optimal Payments Plc

Optimal Payments Plc Cash is dead: the future of payments Collins Stewart Hawkpoint Technology Group Seminar London, 5 October 2011 1 Agenda 1 Introduction to Optimal Payments 2 The changing face of payments

Optimal Payments Plc Cash is dead: the future of payments Collins Stewart Hawkpoint Technology Group Seminar London, 5 October 2011 1 Agenda 1 Introduction to Optimal Payments 2 The changing face of payments

Q3 2014 Financial Highlights. October 15, 2014

October 15, 2014 This presentation contains non-gaap measures relating to the company's performance. You can find the reconciliation of these measures to the nearest comparable GAAP measures in the appendix

October 15, 2014 This presentation contains non-gaap measures relating to the company's performance. You can find the reconciliation of these measures to the nearest comparable GAAP measures in the appendix

BALANCE SHEET AND INCOME STATEMENT

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

BANCOLOMBIA S.A. (NYSE: CIB; BVC: BCOLOMBIA, PFBCOLOM) REPORTS CONSOLIDATED NET INCOME OF COP 1,879 BILLION FOR 2014, AN INCREASE OF 24% COMPARED TO 2013. Operating income increased 23.8% during 2014 and

MasterCard response to the Department of Finance public consultation Regulation (EU) 2015/751 on Interchange Fees for Card-based payment transactions

2015/751 on Interchange Fees for Card-based payment transactions") MasterCard response to the Department of Finance public consultation Regulation (EU) 2015/751 on Interchange Fees for Card-based payment transactions MasterCard MasterCard Worldwide (MasterCard) is a public-listed,

MasterCard response to the Department of Finance public consultation Regulation (EU) 2015/751 on Interchange Fees for Card-based payment transactions MasterCard MasterCard Worldwide (MasterCard) is a public-listed,

Payment Acceptance Strategies in a Global Ecommerce Environment

A division of Pivotal Payments Payment Acceptance Strategies in a Global Ecommerce Environment Presented by: Patrick Huynh, Senior Vice President, Client Solutions Introduction About GlobalOne GlobalOne

A division of Pivotal Payments Payment Acceptance Strategies in a Global Ecommerce Environment Presented by: Patrick Huynh, Senior Vice President, Client Solutions Introduction About GlobalOne GlobalOne

Financial Translation. Pierre Courduroux Senior Vice President and Chief Financial Officer

Financial Translation Pierre Courduroux Senior Vice President and Chief Financial Officer Forward-Looking Statements Certain statements contained in this presentation are forward-looking statements, such

Financial Translation Pierre Courduroux Senior Vice President and Chief Financial Officer Forward-Looking Statements Certain statements contained in this presentation are forward-looking statements, such

Q3 2013 Financial Highlights. October 16, 2013

October 16, 2013 This presentation contains non-gaap measures relating to the company's performance. You can find the reconciliation of these measures to the nearest comparable GAAP measures in the appendix

October 16, 2013 This presentation contains non-gaap measures relating to the company's performance. You can find the reconciliation of these measures to the nearest comparable GAAP measures in the appendix

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization...

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

2015 UK Payment Statistics. Key statistics on the UK payment clearings, cash, card payments and payment markets

2015 UK Payment Statistics Key statistics on the UK payment clearings, cash, card payments and payment markets The following companies contributed to the data within this publication. More details of referenced

2015 UK Payment Statistics Key statistics on the UK payment clearings, cash, card payments and payment markets The following companies contributed to the data within this publication. More details of referenced

Who Are The Parties Involved In Credit Card Processing?

Who Are The Parties Involved In Credit Card Processing? Often one of the hardest and most frustrating things that a business owner must encounter when starting and running a business is choosing the right

Who Are The Parties Involved In Credit Card Processing? Often one of the hardest and most frustrating things that a business owner must encounter when starting and running a business is choosing the right

Visa Canada Interchange Reimbursement Fees

Visa Canada The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed in Canada. 1 Visa uses interchange reimbursement fees as transfer fees between

Visa Canada The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed in Canada. 1 Visa uses interchange reimbursement fees as transfer fees between

Barclaycard presentation. Valerie Soranno Keating, CEO Barclaycard November 2014

Barclaycard presentation Valerie Soranno Keating, CEO Barclaycard November 2014 Barclaycard makes a material contribution to Barclays Group profits Barclays Adjusted PBT (Inc. CTA) 9 months to Q3, total

Barclaycard presentation Valerie Soranno Keating, CEO Barclaycard November 2014 Barclaycard makes a material contribution to Barclays Group profits Barclays Adjusted PBT (Inc. CTA) 9 months to Q3, total

Competition policy brief

Issue 2015-3 June 2015 ISBN 978-92-79-38783-8, ISSN: 2315-3113 Competition policy brief Occasional discussion papers by the Competition Directorate General of the European Commission The Interchange Fees

Issue 2015-3 June 2015 ISBN 978-92-79-38783-8, ISSN: 2315-3113 Competition policy brief Occasional discussion papers by the Competition Directorate General of the European Commission The Interchange Fees

Wirecard AG Investor Presentation. Results 1st. quarter of fiscal 2011

Wirecard AG Investor Presentation Results 1st. quarter of fiscal 2011 Agenda 1 Results, Company and Stock 2 Growth Drivers, Trends and Outlook 2011 3 Financial Data 2011 Wirecard AG 2 Key Figures 1 st

Wirecard AG Investor Presentation Results 1st. quarter of fiscal 2011 Agenda 1 Results, Company and Stock 2 Growth Drivers, Trends and Outlook 2011 3 Financial Data 2011 Wirecard AG 2 Key Figures 1 st

H1 2014 RESULTS AND BUSINESS UPDATE

H1 2014 RESULTS AND BUSINESS UPDATE Strong top line growth of 104% in GMV and margin improvement for Proven Winners Rocket Internet s performance on track and in line with expectations foodpanda grew into

H1 2014 RESULTS AND BUSINESS UPDATE Strong top line growth of 104% in GMV and margin improvement for Proven Winners Rocket Internet s performance on track and in line with expectations foodpanda grew into

Private Label ACH Debit Programs

Private Label ACH Debit Programs What Doesn t Meet The Eye Can Be A Real Eye-Opener Merchants are increasingly focusing on managing payment transactional costs. As a result, some merchants are considering

Private Label ACH Debit Programs What Doesn t Meet The Eye Can Be A Real Eye-Opener Merchants are increasingly focusing on managing payment transactional costs. As a result, some merchants are considering

An Education in Merchant Processing

An Education in Merchant Processing Presented by: Michael Mintz COO - AMG Payment Solutions Today s Agenda Introduction and Background Important Industry Terms The Electronic Payment Process Interchange

An Education in Merchant Processing Presented by: Michael Mintz COO - AMG Payment Solutions Today s Agenda Introduction and Background Important Industry Terms The Electronic Payment Process Interchange

Discover Financial Services. Discover Overview. December 2006

Discover Overview December 2006 Legal Notice The information herein contains forward-looking statements, including without limitation statements about the expected effects, timing and completion of the

Discover Overview December 2006 Legal Notice The information herein contains forward-looking statements, including without limitation statements about the expected effects, timing and completion of the

Comments of Travis B. Plunkett, Legislative Director

Comments of Travis B. Plunkett, Legislative Director To The Federal Reserve Board of Governors On 12 CFR Part 235 Docket No. R 1404 Debit Card Interchange Fees and Routing; Proposed Rule February 22, 2011

Comments of Travis B. Plunkett, Legislative Director To The Federal Reserve Board of Governors On 12 CFR Part 235 Docket No. R 1404 Debit Card Interchange Fees and Routing; Proposed Rule February 22, 2011

Global Network Services

Global Network Services David House, Group President, Global Network and Establishment Services and Travelers Cheques and Prepaid Services Group February 4, 2004 1 Global Network Services Benefits of Partnership!

Global Network Services David House, Group President, Global Network and Establishment Services and Travelers Cheques and Prepaid Services Group February 4, 2004 1 Global Network Services Benefits of Partnership!

Management Commentary. Second Quarter 2015 Results

Management Commentary Second Quarter 2015 Results The RetailMeNot, Inc. ( RetailMeNot ) earnings call will begin on August 5, 2015 at 7:00am central time (8:00am eastern time) and will include prepared

Management Commentary Second Quarter 2015 Results The RetailMeNot, Inc. ( RetailMeNot ) earnings call will begin on August 5, 2015 at 7:00am central time (8:00am eastern time) and will include prepared

4Q15 Earnings February 2016

4Q15 Earnings February 2016 Forward-Looking Statements The statements contained in this presentation that refer to plans and expectations for the next quarter, the full year or the future are forward-looking

4Q15 Earnings February 2016 Forward-Looking Statements The statements contained in this presentation that refer to plans and expectations for the next quarter, the full year or the future are forward-looking

Mobile financial services to emerging markets. Annual General Meeting March 2015

Mobile financial services to emerging markets Annual General Meeting March 2015 Agenda Our Market Core Mobile Money business The HomeSend Joint Venture eservglobal s ambitions 2 "Other generations have

Mobile financial services to emerging markets Annual General Meeting March 2015 Agenda Our Market Core Mobile Money business The HomeSend Joint Venture eservglobal s ambitions 2 "Other generations have

Interchange Optimization: Are you getting the best rate?

2012 Interchange Optimization: Are you getting the best rate? Northpark Town Center 1200 Abernathy Road, Suite 1700 Atlanta, Georgia 30328 (800) 846-1305 www.optimizedpmts.com There are many costs associated

2012 Interchange Optimization: Are you getting the best rate? Northpark Town Center 1200 Abernathy Road, Suite 1700 Atlanta, Georgia 30328 (800) 846-1305 www.optimizedpmts.com There are many costs associated

Transformation of payment systems: channels, technologies and business models

Transformation of payment systems: channels, technologies and business models Payments Asia Summit, March 2009 Island Shangri La, Hong Kong Dr John Ure Director, TPRC Pte Ltd (Singapore) Associate Professor

Transformation of payment systems: channels, technologies and business models Payments Asia Summit, March 2009 Island Shangri La, Hong Kong Dr John Ure Director, TPRC Pte Ltd (Singapore) Associate Professor

Renminbi banking business in Hong Kong

Renminbi banking business in Hong Kong by the External Department Hong Kong s renminbi banking business was launched in early 24 to facilitate crossborder tourist spending and to further strengthen economic

Renminbi banking business in Hong Kong by the External Department Hong Kong s renminbi banking business was launched in early 24 to facilitate crossborder tourist spending and to further strengthen economic

Introduction. Now, I ll turn the call over to Mark Loughridge.

Introduction Thank you. This is Patricia Murphy, Vice President of Investor Relations for IBM. I m here with Mark Loughridge, IBM s Senior Vice President and CFO, Finance and Enterprise Transformation.

Introduction Thank you. This is Patricia Murphy, Vice President of Investor Relations for IBM. I m here with Mark Loughridge, IBM s Senior Vice President and CFO, Finance and Enterprise Transformation.

The Role of Interchange Fees on Debit and Credit Card Transactions in the Payments System

Economic Brief May 2011, EB11-05 The Role of Interchange Fees on Debit and Credit Card Transactions in the Payments System By Tim Mead, Renee Courtois Haltom, and Margaretta Blackwell When consumers use

Economic Brief May 2011, EB11-05 The Role of Interchange Fees on Debit and Credit Card Transactions in the Payments System By Tim Mead, Renee Courtois Haltom, and Margaretta Blackwell When consumers use

Visa U.S.A. Interchange Reimbursement Fees

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3

: Record Revenues in Q3") Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

FINANCIAL RESULTS Q4/2015 & 2015 ESA TIHILÄ, CEO NICLAS ROSENLEW, CFO FEBRUARY 2, 2016

FINANCIAL RESULTS Q4/2015 & 2015 ESA TIHILÄ, CEO NICLAS ROSENLEW, CFO FEBRUARY 2, 2016 IMPORTANT NOTICE The following information contains, or may be deemed to contain, forward-looking statements. These

FINANCIAL RESULTS Q4/2015 & 2015 ESA TIHILÄ, CEO NICLAS ROSENLEW, CFO FEBRUARY 2, 2016 IMPORTANT NOTICE The following information contains, or may be deemed to contain, forward-looking statements. These

W.W. Grainger, Inc. First Quarter 2015 Results Page 1 of 9

W.W. Grainger, Inc. First Quarter 2015 Results Page 1 of 9 News Release GRAINGER REPORTS RESULTS FOR THE 2015 FIRST QUARTER Revises 2015 Guidance Quarterly Summary Sales of $2.4 billion, up 2 percent Operating

W.W. Grainger, Inc. First Quarter 2015 Results Page 1 of 9 News Release GRAINGER REPORTS RESULTS FOR THE 2015 FIRST QUARTER Revises 2015 Guidance Quarterly Summary Sales of $2.4 billion, up 2 percent Operating

Payment Card Reform Framework

Issued on: 23 December 2014 BNM/RH/STD 029-7 Payment Systems PART A OVERVIEW 1. Introduction... 1 2. Scope... 2 3. Applicability... 2 4. Legal provisions... 3 5. Effective date... 3 6. Interpretation...

Issued on: 23 December 2014 BNM/RH/STD 029-7 Payment Systems PART A OVERVIEW 1. Introduction... 1 2. Scope... 2 3. Applicability... 2 4. Legal provisions... 3 5. Effective date... 3 6. Interpretation...

BUY. KELLTON TECH SOLUTIONS LTD Result Update (CONSOLIDATED): Q1 FY16. CMP 226.50 Target Price 260.00. JANUARY 9 th 2015 SYNOPSIS ISIN: INE164B01022

: Q1 FY16. CMP 226.50 Target Price 260.00. JANUARY 9 th 2015 SYNOPSIS ISIN: INE164B01022") BUY CMP 226.50 Target Price 260.00 KELLTON TECH SOLUTIONS LTD Result Update (CONSOLIDATED): Q1 FY16 JANUARY 9 th 2015 ISIN: INE164B01022 Index Details Stock Data Sector IT Software Products BSE Code 519602

BUY CMP 226.50 Target Price 260.00 KELLTON TECH SOLUTIONS LTD Result Update (CONSOLIDATED): Q1 FY16 JANUARY 9 th 2015 ISIN: INE164B01022 Index Details Stock Data Sector IT Software Products BSE Code 519602

Leveraging Regional Debit Networks to Reduce Online Card Acceptance Costs in a Post-Durbin World

Leveraging Regional Debit Networks to Reduce Online Card Acceptance Costs in a Post-Durbin World September 2015 By: Zac Ebrams 1 Leveraging Debit Networks to Reduce Online Card Acceptance Costs in a Post-Durbin

Leveraging Regional Debit Networks to Reduce Online Card Acceptance Costs in a Post-Durbin World September 2015 By: Zac Ebrams 1 Leveraging Debit Networks to Reduce Online Card Acceptance Costs in a Post-Durbin

Credit card: permits consumers to purchase items while deferring payment

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

Finance Master. Winter 2015/16. Jprof. Narly Dwarkasing University of Bonn, IFS

Finance Master Winter 2015/16 Jprof. Narly Dwarkasing University of Bonn, IFS Chapter 2 Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet 2.3 The Income Statement 2.4 The Statement

Finance Master Winter 2015/16 Jprof. Narly Dwarkasing University of Bonn, IFS Chapter 2 Outline 2.1 Firms Disclosure of Financial Information 2.2 The Balance Sheet 2.3 The Income Statement 2.4 The Statement

Earnings attributed to equity shareholders after tax were K9.1 billion (2005: K6.1 billion), a rise of 49% and Return on Shareholders funds of 39%.

, a rise of 49% and Return on Shareholders funds of 39%.") MANAGING DIRECTOR S REVIEW OVERVIEW Zambia enjoyed a robust economic growth of 5.8% in 2006 (2005: 5.2%) mainly driven by positive growth in mining, construction and transport sectors. Other positive developments

MANAGING DIRECTOR S REVIEW OVERVIEW Zambia enjoyed a robust economic growth of 5.8% in 2006 (2005: 5.2%) mainly driven by positive growth in mining, construction and transport sectors. Other positive developments

TripAdvisor Reports Fourth Quarter and Full Year 2013 Financial Results

TripAdvisor Reports Fourth Quarter and Full Year 2013 Financial Results NEWTON, MA, February 11, 2014 -- TripAdvisor, Inc. (NASDAQ: TRIP), the world s largest travel website*, today announced financial

TripAdvisor Reports Fourth Quarter and Full Year 2013 Financial Results NEWTON, MA, February 11, 2014 -- TripAdvisor, Inc. (NASDAQ: TRIP), the world s largest travel website*, today announced financial

Europe: Growth of +7.8% in Recurring Operating Income France: New half of improved profitability

2014 FIRST HALF RESULTS: CONTINUED GROWTH Organic sales growth of 4.3% Increase in Recurring Operating Income of +13.8% Strong increase in adjusted net income, Group share of +16.7% Strong profit growth

2014 FIRST HALF RESULTS: CONTINUED GROWTH Organic sales growth of 4.3% Increase in Recurring Operating Income of +13.8% Strong increase in adjusted net income, Group share of +16.7% Strong profit growth

Financial Analysis Project. Apple Inc.

MBA 606, Managerial Finance Spring 2008 Pfeiffer/Triangle Financial Analysis Project Apple Inc. Prepared by: Radoslav Petrov Course Instructor: Dr. Rosemary E. Minyard Submission Date: 5 May 2008 Petrov,

MBA 606, Managerial Finance Spring 2008 Pfeiffer/Triangle Financial Analysis Project Apple Inc. Prepared by: Radoslav Petrov Course Instructor: Dr. Rosemary E. Minyard Submission Date: 5 May 2008 Petrov,

Third Quarter 2015 Financial Highlights:

DISCOVERY COMMUNICATIONS REPORTS THIRD QUARTER 2015 RESULTS, INCREASES BUYBACK AUTHORIZATION BY $2 BILLION AND ANNOUNCES RESUMPTION OF SHARE REPURCHASES BEGINNING IN FOURTH QUARTER 2015 Third Quarter 2015

DISCOVERY COMMUNICATIONS REPORTS THIRD QUARTER 2015 RESULTS, INCREASES BUYBACK AUTHORIZATION BY $2 BILLION AND ANNOUNCES RESUMPTION OF SHARE REPURCHASES BEGINNING IN FOURTH QUARTER 2015 Third Quarter 2015

H1 2014 Earning Results JULY 30 TH, 2014

H1 2014 Earning Results JULY 30 TH, 2014 Disclaimer This document includes forward looking statements relating to Ingenico Group s future prospects, development and business strategies. By their nature,

H1 2014 Earning Results JULY 30 TH, 2014 Disclaimer This document includes forward looking statements relating to Ingenico Group s future prospects, development and business strategies. By their nature,

FOURTH QUARTER NET INCOME INCREASES 12% TO A RECORD $5.32 BILLION FOURTH QUARTER EPS OF $1.02, UP 12% REVENUES INCREASE 9% TO $21.

FOURTH QUARTER NET INCOME INCREASES 12% TO A RECORD $5.32 BILLION FOURTH QUARTER EPS OF $1.02, UP 12% REVENUES INCREASE 9% TO $21.9 BILLION CITIGROUP 2004 NET INCOME OF $17.0 BILLION, EPS OF $3.26 REVENUES

FOURTH QUARTER NET INCOME INCREASES 12% TO A RECORD $5.32 BILLION FOURTH QUARTER EPS OF $1.02, UP 12% REVENUES INCREASE 9% TO $21.9 BILLION CITIGROUP 2004 NET INCOME OF $17.0 BILLION, EPS OF $3.26 REVENUES

Secure Financial Transactions Any Time, Any Place

Secure Financial Transactions Any Time, Any Place Euronet Software Solutions Gold-Net Global Payment Solution Become a Processor Providing Authorization, Clearing, Settlement, Value Added Services and

Secure Financial Transactions Any Time, Any Place Euronet Software Solutions Gold-Net Global Payment Solution Become a Processor Providing Authorization, Clearing, Settlement, Value Added Services and

UK Card Payments 2015

UK Card Payments 2015 THE UK CARDS ASSOCIATION Cards are the most popular payment method in the UK by value. They allow cardholders to pay for goods and services easily, conveniently and securely. Card

UK Card Payments 2015 THE UK CARDS ASSOCIATION Cards are the most popular payment method in the UK by value. They allow cardholders to pay for goods and services easily, conveniently and securely. Card

Management Presentation Q2/2012 Results. 8 August 2012

Management Presentation Q2/2012 Results 8 August 2012 Cautionary statement This presentation contains forward-looking statements which involve risks and uncertainties. The actual performance, results and

Management Presentation Q2/2012 Results 8 August 2012 Cautionary statement This presentation contains forward-looking statements which involve risks and uncertainties. The actual performance, results and

Pharmacy Benefits Managers

One Corporate Center Rye, NY 10580-1422 Tel (914) 921-5072 Fax (914) 921-5098 www.gabelli.com August 18, 2004 Gabelli & Company, Inc. Pharmacy Benefits Managers Second Quarter Update Claims in millions

One Corporate Center Rye, NY 10580-1422 Tel (914) 921-5072 Fax (914) 921-5098 www.gabelli.com August 18, 2004 Gabelli & Company, Inc. Pharmacy Benefits Managers Second Quarter Update Claims in millions

What is SEPA? Fact Sheet. Streamlining Payments in Europe

Fact Sheet Streamlining Payments in Europe The Single Euro Payments Area (SEPA) is the area where citizens, companies and other economic players will be able to make and receive payments in euros (whether

Fact Sheet Streamlining Payments in Europe The Single Euro Payments Area (SEPA) is the area where citizens, companies and other economic players will be able to make and receive payments in euros (whether

Spectra Energy Reports Second Quarter 2008 Results, Net Income Up 51 Percent from Prior Year

Media: Analysts: Molly Boyd (713) 627-5923 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: August 6, 2008 Spectra Energy Reports Second Quarter 2008 Results, Net Income Up 51 Percent

Media: Analysts: Molly Boyd (713) 627-5923 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: August 6, 2008 Spectra Energy Reports Second Quarter 2008 Results, Net Income Up 51 Percent

First-Quarter 2014 Financial Results

First-Quarter 2014 Financial Results www.unisys.com/investor Ed Coleman Chairman & CEO Janet Haugen SVP & CFO April 22, 2014 Disclaimer Statements made by Unisys during today's presentation that are not

First-Quarter 2014 Financial Results www.unisys.com/investor Ed Coleman Chairman & CEO Janet Haugen SVP & CFO April 22, 2014 Disclaimer Statements made by Unisys during today's presentation that are not

THE INNOVATION JOURNEY:

THE INNOVATION JOURNEY: The last four years and into the future Presentation to the Australian Payments Forum Monday 15 April 2013 Where were we? DCITA Report 2006 APCA Innovation Report 2008/9 What s

THE INNOVATION JOURNEY: The last four years and into the future Presentation to the Australian Payments Forum Monday 15 April 2013 Where were we? DCITA Report 2006 APCA Innovation Report 2008/9 What s

Capital Markets Day Athens, 16 January 2006 ALPHA. Retail Banking. G. Aronis Senior Manager, Retail Banking

Capital Markets Day Athens, 16 January 2006 ALPHA BANΚ Retail Banking G. Aronis Senior Manager, Retail Banking Contents: page Retail Banking at a Glance 3 Strategic Emphasis on Retail Banking 4 Household

Capital Markets Day Athens, 16 January 2006 ALPHA BANΚ Retail Banking G. Aronis Senior Manager, Retail Banking Contents: page Retail Banking at a Glance 3 Strategic Emphasis on Retail Banking 4 Household

RFP Administration In this section, provide contact details, such as who to contact for the RFP, phone number, e-mail, address, etc:

RFP GUIDE THE REQUEST FOR PROPOSAL PROCESS When your organization decides to move forward with the adoption of a new card program or modification of an existing program the Request for Proposal ("RFP")

RFP GUIDE THE REQUEST FOR PROPOSAL PROCESS When your organization decides to move forward with the adoption of a new card program or modification of an existing program the Request for Proposal ("RFP")

Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

A RE T HE U.S. CHIP RULES ENOUGH?

August 2015 A RE T HE U.S. CHIP RULES ENOUGH? A longer term view of security and the payments landscape is needed. Abstract: The United States is finally modernizing its card payment systems and confronting

August 2015 A RE T HE U.S. CHIP RULES ENOUGH? A longer term view of security and the payments landscape is needed. Abstract: The United States is finally modernizing its card payment systems and confronting