Financial Literacy in Guidance and Career Education Career Studies (GLC2O) Connections to Financial Literacy

|

|

|

- Edwin Parker

- 8 years ago

- Views:

Transcription

1 LESSON PLAN Financial Literacy in Guidance and Career Education Career Studies (GLC2O) Connections to Financial Literacy In small groups, students work on a saving and spending plan and develop balanced budgets to creatively respond to the challenges of making ends meet in life after secondary school. Students use critical thinking skills and problem-solving strategies to plan responses to different financial challenges that might occur in their lives after secondary school. Curriculum Expectations Learning Goals Exploration of Opportunities identify a broad range of options for present and future learning, work, and community involvement Identifying Personal Options - identify and describe a variety of learning opportunities for secondary school students, including secondary school courses, community-based learning and co-curricular activities - compare a variety of postsecondary learning options and identify those most suited to them based on their personal interests, competencies, and aspirations The following expectations from the Discovering the Workplace course (GLD2O) could also be addressed in this lesson. Essential Skills for Working and Learning identify and describe the workplace essential skills necessary for success in life, school, and work Understanding Workplace Essential Skills - describe how the essential skills are transferable from home to school, school to work, occupation to occupation, and sector to sector Essential Skills for Working and Learning identify the literacy and numeracy strategies that support the application of workplace essential skills, and use them to complete specific tasks in school, in the community, or in real or simulated workplace settings Using Literacy and Numeracy Strategies - identify the numeracy strategies required for calculation and estimation, and use them effectively to manage money to work with schedules and budgets, to analyse data and to measure and make numerical calculations using real workplace materials in school, in the community, or in real or simulated workplace settings - identify strategies for reading and interpreting text and use them effectively for specific tasks in school, in the community, or in real or simulated workplace settings, using real workplace materials Essential Skills for Working and Learning describe learning and thinking strategies, and use them effectively in school or in the community Using Learning and Thinking Strategies - describe a process for decision making and use it effectively in situations in school and in the community By the end of this lesson, students will be able to: identify opportunities for increasing income and/or decreasing expenses when living on a student budget. Sample Success Criterion I used creative options to develop a balanced saving and spending plan and budget (i.e., one in which my income is larger than my expenses). PAGE 1 OF 4

2 Financial Literacy in Guidance and Career Education Career Studies (GLC2O) Instructional Components and Context Readiness Students have previously worked on written reports of managing an income on minimum wage. They ve reflected on personal experiences geared towards managing money and have formed opinions based on viewing a short film. They have practised using critical thinking skills to respond to challenging situations such as mock job interviews. Students have had some initial prior discussions about accessing loans and the use of credit. Terminology Budget Debt Expenses Grant Income Loan Materials and Resources Statements, facts and recent statistics printed on large paper to post around the room Think about this template Thinking about Loans and Credit Cards cut into strips chart paper and markers Colour-coded Budget Scenario Cards placed on board ahead of time in a grid format Each of the rows represents different categories as follows: Income (Bright Green) Tuition and associated costs (Orange) Housing (Dark Blue) Utilities (Light Blue) Transportation (Yellow) Cell Phone (Dark Green) Cable, Phone, Internet (Purple) Print the various scenario cards on the corresponding coloured paper or use coloured markers to show the different categories. Prepare simulated unexpected expenses red cards to distribute to students later. PAGE 2 OF 4

3 Financial Literacy in Guidance and Career Education Career Studies (GLC2O) Minds On Small Groups Four Corners Find 4-5 recent facts and statistics from Canadian/Ontario websites which provide objective information about finances. Print out the facts on large pieces of paper and post around the classroom. Sample websites for recent financial information include: The Financial Consumer Agency of Canada The Investor Education Fund Sample facts/statistics: 1. Ontario Student Loan default rates have been steadily declining and are now at the lowest levels since rates began being tracked in From a high of 23.5 per cent in 1997, Ontario s student loan default rate fell to 7.6 per cent in According to a 2008 Environics survey, six out of ten young Canadians aged are in debt of some kind, with credit card debt being the most common, followed by student loans. 3. With respect to payday loans (also called internet or storefront loans), for every $100 borrowed, one could pay $20 in service fees and interest. Students choose the fact that surprises them the most and go to stand beside that fact. Students at each station work together to complete the Think About This handout. Action! Small Groups Build a Scenario Students form groups of 4-5. One representative from each group comes to the board and selects one card from each category of the grid. Categories include: income, tuition and associated fees, housing, utilities, vehicle, cell phone and cable/phone/internet. The cards together form the groups specific scenarios with which they will be working. Provide some clarifying information about the information on the cards. For example, income can include employment income, student grants and loans, gifts from family. Tuition costs include some associated costs such as fees and text books. Working in their groups, students calculate their income and their expenses, and develop a plan for saving and spending. Co-construct success criteria that will be used to assess their plan. Some groups may come to realize that they do not have enough income to cover all of their expenses. Encourage the students to brainstorm different strategies and solutions to resolve this issue. After several minutes, randomly distribute the red unexpected expenses cards to each group (e.g., $300 cell phone bill, $500 trip to the mall, $150 laptop repair). Encourage students to think creatively and critically to determine how they will increase their income or reduce their expenses in order to have a balanced budget, when they also consider the red unexpected expenses cards. Connections Assessment for Learning Circulate around the groups, reviewing their answers on the Think About This sheet to get a sense of what students already know about budgeting, student loans, credit card debt, etc. Connections Assessment for Learning Assess whether students include suggestions and strategies related to increasing income and also decreasing expenses. Assessment as Learning Self Assessment: Students review their group s spending and saving plan and budget. Are they balanced (i.e., income meets or exceeds expenses)? Differentiated Instruction Ask students to discuss in their groups, their own oops moments, (i.e., create their own red cards ). If they wish to switch their red card for one of their own oops moments, groups can choose to switch. Differentiated Instruction Make calculators available for students who need them. Strategically group students so they can support each other with calculations. PAGE 3 OF 4

4 Financial Literacy in Guidance and Career Education Career Studies (GLC2O) Consolidation Small Groups Presentations Students work in their groups to present their saving and spending plan and budgets for their scenarios to the class. Audience members are invited to provide additional creative solutions to the solutions presented. Small Groups Some Thoughts About Loans and Credit Cards Post the Thinking about Loans and Credit Cards questions for students to consider as they work in groups to develop advice statements about financial planning and money management, based on their experience with the Action activity and in prior discussions. The students write out their statements on paper slips. Distribute a slip with one statement on it to each student. Students take turns reading the statements. Students reflect on the statements and talk in small groups, then share their thoughts in response to the statements with the whole class. Possible guiding questions for discussion: Do you agree/disagree with the statement? Why? Do you have any experience related to this experience? What other statements could you add to offer advice to your peers? Connections Assessment of Learning Circulate around the groups, reviewing their answers on the Think About This sheet to get a sense of what students already know about budgeting, student loans, credit card debt, etc. Extension Students can develop and hand in personal plans and budgets, either using their own income (generated from part time jobs/allowance etc) and expenses or using a scenario developed for this purpose. Be sensitive to the fact that some students may appreciate the practical application of this activity using their own income and expenses while other students who do not have a source of income may not be comfortable working with information about their expenses on a classroom activity. Have a variety of options available for students. PAGE 4 OF 4

5 Think About This How does this fact fit with what you already know? In what ways does this fact surprise you? What are some of the implications of this fact? Why should we care?

6 Thinking About Loans and Credit Cards Use your experience in today s activity and the questions below to consider what financial planning advice you can offer to your peers. 1. Think in advance about the kinds of purchases for which you may want to use a credit card. Will you use it for everyday purchases like food and clothing? For you, is this a good idea? Why or why not? 2. Making only the minimum payment each month increases the amount of time it will take to pay off debts. Also, making minimum payments will result in increases in the amount of interest paid. If you are trying to pay your debts off more quickly what should you consider when it comes to making minimum payments on a credit card? 3. If you can t afford a purchase today, what would need to be different so that you would be able to afford it tomorrow, or even next month? 4. How can you learn about your credit score? What is your credit history? (See the following site for information How can cancelling a credit card impact your credit score? 5. Stores tend to keep their target group in mind when setting up displays. Eye catching colour and design strategies can make you believe that you need the item and can encourage impulse purchases. Considering this, what advice can you offer your peers? 6. How can tracking your spending habits help you? 7. Payday loans (also called Internet or Storefront loans) offer quick payment for an upcoming pay cheque. The fees and interest charged by payday loan companies can be very high. What advice can you offer regarding these loans? 8. In addition to student grants and scholarships what other options could be considered in order to pay for postsecondary education? 9. When negotiating student loans repayment schedules with the lender, what would be the advantages and disadvantages of reducing the length of repayment time?

7 Income Full-time Employment $65,000/year Savings $18,000

8 Income Part-Time Employment $20,000 per year Full-Time Employment $110,000 per year

9 Income OSAP $10,000 per year

10 Tuition and associated costs University Tuition + Textbooks $8500 per year University Tuition $6000 per year

11 Tuition and associated costs US or Abroad Tuition $18,000 per year Travel for a Year First $5000

12 Tuition and associated costs College Tuition and Used Books $3000

13 Housing Rent $700 per month Rent with a Roommate $400 per month

14 Housing Rent $1200 per month Mortgage $800 per month

15 Housing Live at Home $0 per month

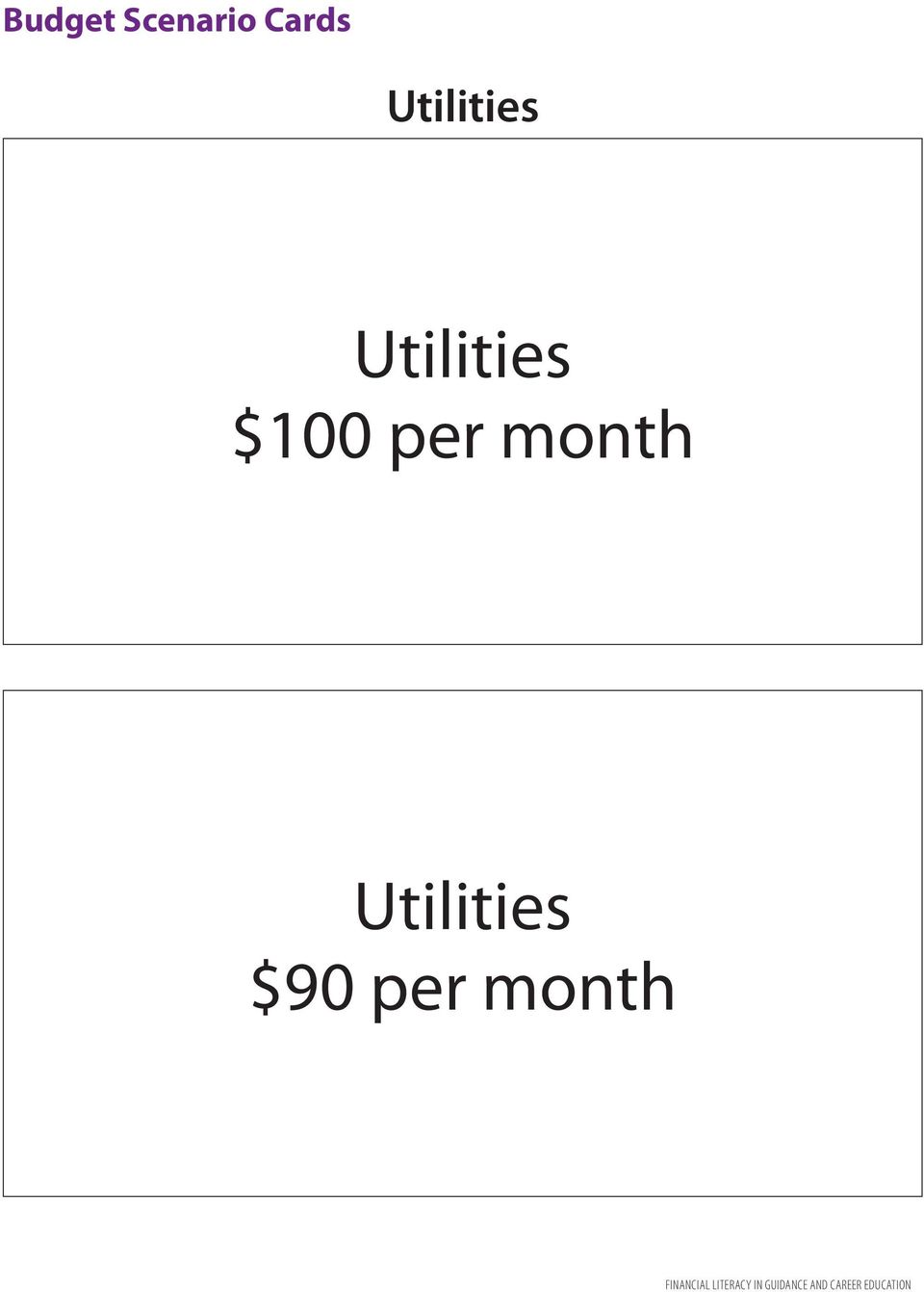

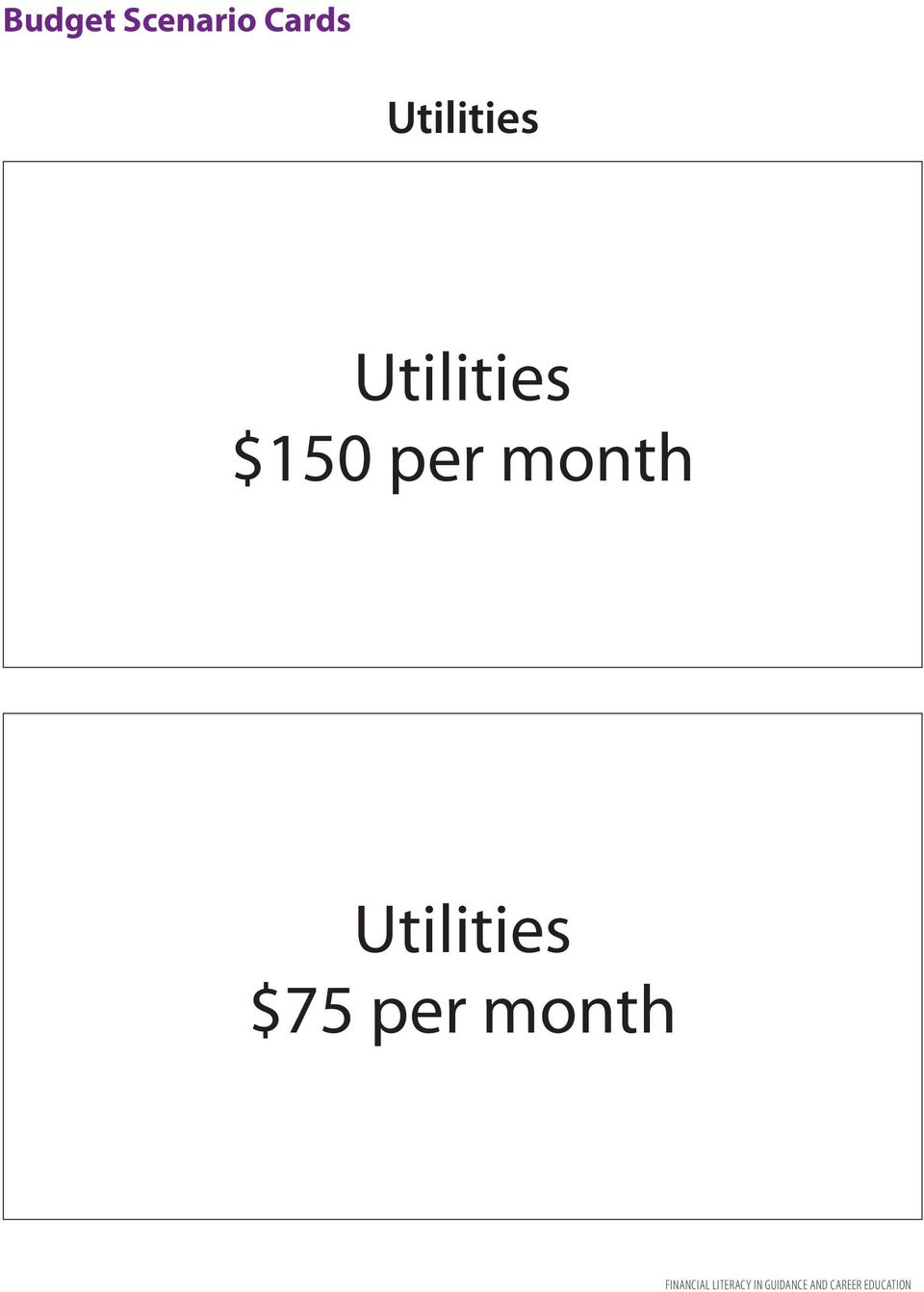

16 Utilities Utilities $100 per month Utilities $90 per month

17 Utilities Utilities $150 per month Utilities $75 per month

18 Utilities Utilities $120 per month

19 Transportation Used Car $3000 one-time-payment Car Payments $454 Bi-Weekly (for four years)

20 Transportation Car Payments $219 month (5 year lease) Transit Pass $109 per month

21 Transportation Car Payments $150 bi-weekly (5 year loan)

22 Cell Phone Cell Phone $400 per month Cell Phone Pay as you go - $20 per month

23 Cell Phone Cell Phone $200 per month Cell Phone $100 per month

24 Cell Phone No Cell Phone $0

25 Cable, Phone, Internet Cable, Phone, Internet $150 per month Cable, Phone, Internet $115 per month

26 Cable, Phone, Internet Internet only (no cable or phone) $45 per month Phone only $20 per month

27 Cable, Phone, Internet No cable, phone or Internet $0 per month

28 Unexpected Expenses Credit Card Bill $350 Shopping at the Mall $500

29 Unexpected Expenses Laptop Repair $150 Cell Phone Bill $300

30 Unexpected Expenses Car Repair $400

Business Studies, Grades 9/10, Information and Communication Technology in Business, BTT1O/BTT2O

FINANCIAL LITERACY Overview Students develop an understanding of concepts and skills related to financial literacy as they learn to use productivity software to record and communicate spending decisions

FINANCIAL LITERACY Overview Students develop an understanding of concepts and skills related to financial literacy as they learn to use productivity software to record and communicate spending decisions

Personal Loans 101: UNDERSTANDING APR

Personal Loans 101: UNDERSTANDING APR In today s world, almost everyone needs access to credit. Whether it is to make a small purchase, pay for an unexpected emergency, repair the car or obtain a mortgage

Personal Loans 101: UNDERSTANDING APR In today s world, almost everyone needs access to credit. Whether it is to make a small purchase, pay for an unexpected emergency, repair the car or obtain a mortgage

The Danger of Debt: Avoiding Financial Pitfalls LESSON 3

The Danger of Debt: Avoiding Financial Pitfalls LESSON 3 The Danger of Debt: Avoiding Financial Pitfalls LESSON 3: TEACHERS GUIDE When teens borrow money from a friend or relative to buy the latest gadget,

The Danger of Debt: Avoiding Financial Pitfalls LESSON 3 The Danger of Debt: Avoiding Financial Pitfalls LESSON 3: TEACHERS GUIDE When teens borrow money from a friend or relative to buy the latest gadget,

Ohio State Benchmarks Social Studies Economics: Personal Finance Family & Consumer Science - Personal Financial Literacy

Ohio State Benchmarks Social Studies Economics: Personal Finance Family & Consumer Science - Personal Financial Literacy Correlation to Virtual Business - Personal Finance Course Concepts Virtual Business

Ohio State Benchmarks Social Studies Economics: Personal Finance Family & Consumer Science - Personal Financial Literacy Correlation to Virtual Business - Personal Finance Course Concepts Virtual Business

Your Money Matters! Financial Literacy Teacher Guide. Thanks to TD for helping us bring this resource to schools for free.

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

The Danger of Debt: Avoiding Financial Pitfalls

The Danger of Debt: Avoiding Financial Pitfalls LESSON 15: TEACHERS GUIDE When teens borrow money from a friend or relative to buy the latest gadget, the thought of returning the payment often comes second

The Danger of Debt: Avoiding Financial Pitfalls LESSON 15: TEACHERS GUIDE When teens borrow money from a friend or relative to buy the latest gadget, the thought of returning the payment often comes second

What You Need To Know. Trent s Student Guide to Financial Literacy 2012-13

What You Need To Know Trent s Student Guide to Financial Literacy 2012-13 Welcome to Trent University. In addition to the academic challenges students encounter in university, there are financial challenges

What You Need To Know Trent s Student Guide to Financial Literacy 2012-13 Welcome to Trent University. In addition to the academic challenges students encounter in university, there are financial challenges

LESSON 7 -- CREDIT REPORTS AND CREDIT SCORES

LESSON 7 -- CREDIT REPORTS AND CREDIT SCORES LESSON DESCRIPTION AND BACKGROUND Using the Better Money Habits video What s the Difference Between a Credit Report and a Credit Score? (www.bettermoneyhabits.com),

LESSON 7 -- CREDIT REPORTS AND CREDIT SCORES LESSON DESCRIPTION AND BACKGROUND Using the Better Money Habits video What s the Difference Between a Credit Report and a Credit Score? (www.bettermoneyhabits.com),

Transportation Technology Vehicle Ownership

2011-12 Financial Literacy within Technological Education 1 Transportation Technology Vehicle Ownership Since making financial decisions has become an increasingly complex task in the modern world, people

2011-12 Financial Literacy within Technological Education 1 Transportation Technology Vehicle Ownership Since making financial decisions has become an increasingly complex task in the modern world, people

Keeping Score: Why Credit Matters

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Teacher Resource Guide

Teacher Resource Guide EverFi - Financial Literacy EverFi - Financial Literacy teaches, assesses and certifies students in critical financial concepts through the latest online, interactive curriculum

Teacher Resource Guide EverFi - Financial Literacy EverFi - Financial Literacy teaches, assesses and certifies students in critical financial concepts through the latest online, interactive curriculum

MEETING THE OREGON STATE STANDARDS FINANCIAL AVENUE CORE CONCEPT EARNING SPENDING SAVING BORROWING PROTECT

MEETING THE OREGON STATE STANDARDS Financial Avenue provides online courses to help students gain important knowledge about the basics of personal money management. The Financial Avenue online financial

MEETING THE OREGON STATE STANDARDS Financial Avenue provides online courses to help students gain important knowledge about the basics of personal money management. The Financial Avenue online financial

OBJECTIVES. The BIG Idea MONEY MATTERS. How much will it cost to buy, operate, and insure a car? Paying for a Car

Paying for a Car 4 MONEY MATTERS The BIG Idea How much will it cost to buy, operate, and insure a car? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II. What Can You Spend? (15 minutes) III. Getting

Paying for a Car 4 MONEY MATTERS The BIG Idea How much will it cost to buy, operate, and insure a car? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II. What Can You Spend? (15 minutes) III. Getting

The RBF also licenses some credit institutions that provide personal loans (for education, travel etc), business loans, mortgages and vehicle loans.

, business loans, mortgages and vehicle loans.") Welcome again to the Public Awareness column provided by the Reserve Bank of Fiji (RBF). This month s article focuses on borrowing money and managing that credit. We also provide some issues you should

Welcome again to the Public Awareness column provided by the Reserve Bank of Fiji (RBF). This month s article focuses on borrowing money and managing that credit. We also provide some issues you should

Personal Loans 101: Understanding

Personal Loans 101: Understanding APR Everyone needs access to affordable credit, whether it is to make a small purchase, pay for an unexpected emergency, repair their car or obtain a mortgage on their

Personal Loans 101: Understanding APR Everyone needs access to affordable credit, whether it is to make a small purchase, pay for an unexpected emergency, repair their car or obtain a mortgage on their

Using Credit Wisely LESSON 14: TEACHERS GUIDE

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

Grade 11 Essential Mathematics. Unit 2: Managing Your Money

Name: Grade 11 Essential Mathematics Unit 2: Page 1 of 16 Types of Accounts Banks offer several types of accounts for their customers. The following are the three most popular accounts used for everyday

Name: Grade 11 Essential Mathematics Unit 2: Page 1 of 16 Types of Accounts Banks offer several types of accounts for their customers. The following are the three most popular accounts used for everyday

Students will devise a savings plan for college.

Lesson Description Students will analyze data to determine the relationship between level of educational attainment and weekly earnings and the relationship between level of educational attainment and

Lesson Description Students will analyze data to determine the relationship between level of educational attainment and weekly earnings and the relationship between level of educational attainment and

Overview. Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand your credit Prevent identity theft

Lisa Croat and Andrea Clark Lunch provided by the Higher One Financial Literacy Counts Grant Overview Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand

Lisa Croat and Andrea Clark Lunch provided by the Higher One Financial Literacy Counts Grant Overview Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand

Gr. 6-12 English Language arts Standards, Literacy in History/Social Studies and Technical Studies

Credit Lesson Description Concepts In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities on an individual s net

Credit Lesson Description Concepts In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities on an individual s net

Repayment Resource Guide. Planning for Student Success

Repayment Resource Guide Planning for Student Success 2013 Table of Contents Table of Contents... 1 Introduction... 3 Purpose of Document... 3 Role of Post Secondary Institutions... 3 Consequences of Student

Repayment Resource Guide Planning for Student Success 2013 Table of Contents Table of Contents... 1 Introduction... 3 Purpose of Document... 3 Role of Post Secondary Institutions... 3 Consequences of Student

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Literacy. Credit basics

Literacy Credit basics 2 Contents HANDOUT 6-1 Types of credit Type of credit Lender Uses Conditions Revolving credit Credit Cards (secured and unsecured NOT prepaid) To make purchases, pay bills, make

Literacy Credit basics 2 Contents HANDOUT 6-1 Types of credit Type of credit Lender Uses Conditions Revolving credit Credit Cards (secured and unsecured NOT prepaid) To make purchases, pay bills, make

How To Understand Credit Rating And Credit Rating

Keeping Score: Why Credit Matters LESSON 1 Keeping Score: Why Credit Matters LESSON 1: TEACHERS GUIDE In the middle of a football grandfinal, keeping score is the norm. But when it comes to life, many

Keeping Score: Why Credit Matters LESSON 1 Keeping Score: Why Credit Matters LESSON 1: TEACHERS GUIDE In the middle of a football grandfinal, keeping score is the norm. But when it comes to life, many

Grade 9 Financial Literacy & Visual Arts

Grade 9 Financial Literacy & Visual Arts Intermediate Course Outline: Career Pathways in Art: Planning For Your Future Editor: Christina Yarmol, Writer: Peter Bates Resource to Support the 2011 Financial

Grade 9 Financial Literacy & Visual Arts Intermediate Course Outline: Career Pathways in Art: Planning For Your Future Editor: Christina Yarmol, Writer: Peter Bates Resource to Support the 2011 Financial

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description This lesson builds on Grade 7, Lesson 1. Students will calculate net income and categorize expenses to create a budget. Percentages for each category will be calculated and analyzed.

Lesson Description This lesson builds on Grade 7, Lesson 1. Students will calculate net income and categorize expenses to create a budget. Percentages for each category will be calculated and analyzed.

Borrowing Money and Dealing with Debt

making ends meet... and more! Borrowing Money and Dealing with Debt Before You Begin As we know from previous modules relationships are a key factor in determining where women choose to borrow money, as

making ends meet... and more! Borrowing Money and Dealing with Debt Before You Begin As we know from previous modules relationships are a key factor in determining where women choose to borrow money, as

MANAGING MADE EASY: WHY IT IS IMPORTANT TO START YOUNG WHAT YOU NEED TO KNOW

MANAGING YOUR BUDGETING MONEY: WHY IT IS IMPORTANT MADE EASY: TO START YOUNG WHAT YOU NEED TO KNOW A free publication provided by This complimentary publication is provided by Consolidated Credit Consolidated

MANAGING YOUR BUDGETING MONEY: WHY IT IS IMPORTANT MADE EASY: TO START YOUNG WHAT YOU NEED TO KNOW A free publication provided by This complimentary publication is provided by Consolidated Credit Consolidated

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description The students are presented with real life situations in which young people have to make important decisions about their future. Students use an online tool to examine how the cost of

Lesson Description The students are presented with real life situations in which young people have to make important decisions about their future. Students use an online tool to examine how the cost of

Banking made clear. Information pack for people with learning disabilities.

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear. Information pack for people with learning disabilities.

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Banking made clear Information pack for people with learning disabilities. This handy guide provides information about how you can: open and manage your own bank account keep safe when you are using your

Money Borrowing money

Money Borrowing money Aims: To enable young people to explore ways of borrowing money and the advantages and possible consequences of doing so. Learning Outcomes: By the end of the session the participants

Money Borrowing money Aims: To enable young people to explore ways of borrowing money and the advantages and possible consequences of doing so. Learning Outcomes: By the end of the session the participants

Financial Literacy in Grade 11 Mathematics Understanding Annuities

Grade 11 Mathematics Functions (MCR3U) Connections to Financial Literacy Students are building their understanding of financial literacy by solving problems related to annuities. Students set up a hypothetical

Grade 11 Mathematics Functions (MCR3U) Connections to Financial Literacy Students are building their understanding of financial literacy by solving problems related to annuities. Students set up a hypothetical

C.A.L.M. 20 Unscheduled. Unit 5

C.A.L.M. 20 Unscheduled Unit 5 Independent Living Name: Unit 5 Independent Living Complete all parts of this unit on the assignment sheets provided. Assignment 1 Values and guiding principles for independent

C.A.L.M. 20 Unscheduled Unit 5 Independent Living Name: Unit 5 Independent Living Complete all parts of this unit on the assignment sheets provided. Assignment 1 Values and guiding principles for independent

Understanding Credit

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Make a Smart Start Toward Financial Success SUNY ORANGE STUDENTS

Make a Smart Start Toward Financial Success SUNY ORANGE STUDENTS A College Education is a Smart Investment High School Graduate $25,000 Some College $30,000 Associate s Degree $32,000 Bachelor s Degree

Make a Smart Start Toward Financial Success SUNY ORANGE STUDENTS A College Education is a Smart Investment High School Graduate $25,000 Some College $30,000 Associate s Degree $32,000 Bachelor s Degree

The stock market: How it works

GRADE 9 11 This lesson introduces students to the stock market. Students will understand the difference between primary and secondary markets and explain the relationship between bids and asks in determining

GRADE 9 11 This lesson introduces students to the stock market. Students will understand the difference between primary and secondary markets and explain the relationship between bids and asks in determining

GFL Comparison SB 40, New Standards, Old Standards

SB 40 Requirement New Standards GFL Comparison SB 40, New Standards, Old Standards STANDARD 1: Students will understand how values, culture, and economic forces affect personal financial priorities and

SB 40 Requirement New Standards GFL Comparison SB 40, New Standards, Old Standards STANDARD 1: Students will understand how values, culture, and economic forces affect personal financial priorities and

MONEY MATTERS. Paying for College

MONEY MATTERS Paying for College INSIDE 02 Frequently Asked Questions 05 Fanshawe Financial Resources: Filling the Gap Financial Aid & Student Awards bursaries awards scholarships Back Cover Web Links

MONEY MATTERS Paying for College INSIDE 02 Frequently Asked Questions 05 Fanshawe Financial Resources: Filling the Gap Financial Aid & Student Awards bursaries awards scholarships Back Cover Web Links

FNSFLT203A Develop understanding of debt and consumer credit

FNSFLT203A Develop understanding of debt and consumer credit Revision Number: 1 FNSFLT203A Develop understanding of debt and consumer credit Modification History Not applicable. Unit Descriptor Unit descriptor

FNSFLT203A Develop understanding of debt and consumer credit Revision Number: 1 FNSFLT203A Develop understanding of debt and consumer credit Modification History Not applicable. Unit Descriptor Unit descriptor

Time Tested Tips for Long-Term Wealth

Time Tested Tips for Long-Term Wealth Everyday Wealth Guide.com 2013, all rights reserved The Importance of Cash Flow The first step to achieving long-term wealth is cash flow management. One of the best

Time Tested Tips for Long-Term Wealth Everyday Wealth Guide.com 2013, all rights reserved The Importance of Cash Flow The first step to achieving long-term wealth is cash flow management. One of the best

Budget Busters: Who s Breaking the Bank?

Time Required: 15 minutes Budget Busters: Where does all your money go? No matter how much money you earn, a careful budget lets you know exactly what happens to your cash. Below are three different cash

Time Required: 15 minutes Budget Busters: Where does all your money go? No matter how much money you earn, a careful budget lets you know exactly what happens to your cash. Below are three different cash

Midwestern University Tomorrow s Healthcare Team

Midwestern University Tomorrow s Healthcare Team Midwestern University students face important and challenging personal and financial decisions throughout their enrollment and after graduation. Sensible

Midwestern University Tomorrow s Healthcare Team Midwestern University students face important and challenging personal and financial decisions throughout their enrollment and after graduation. Sensible

Handbook: The Cost of Borrowing. Learn what you need to know quickly.

Handbook: The Cost of Borrowing Learn what you need to know quickly. Money Matters Handbook: The Cost of Borrowing Groceries cost. Clothes cost. Furniture costs. And it costs to borrow money. The amount

Handbook: The Cost of Borrowing Learn what you need to know quickly. Money Matters Handbook: The Cost of Borrowing Groceries cost. Clothes cost. Furniture costs. And it costs to borrow money. The amount

DEBT CHECK-UP: ARE YOU AT RISK IF INTEREST RATES RISE?

BUDGETING AND MONEY MANAGEMENT DEBT CHECK-UP: ARE YOU AT RISK IF INTEREST RATES RISE? Interest rates are at all-time lows in Canada, but they are likely to rise at some point. When they do, you can expect

BUDGETING AND MONEY MANAGEMENT DEBT CHECK-UP: ARE YOU AT RISK IF INTEREST RATES RISE? Interest rates are at all-time lows in Canada, but they are likely to rise at some point. When they do, you can expect

SM4-1: Credit Card Application (version 1)

") SM4-1: Credit Card Application (version 1) SM4-1: Credit Card Application (version 1) pg. 1 of 2 SM4-1: Credit Card Application (version 1) continued SM4-1: Credit Card Application (version 1) pg. 2 of

SM4-1: Credit Card Application (version 1) SM4-1: Credit Card Application (version 1) pg. 1 of 2 SM4-1: Credit Card Application (version 1) continued SM4-1: Credit Card Application (version 1) pg. 2 of

Unit Two Support for Starting a Business - You Are Not Alone

Unit Two Support for Starting a Business - You Are Not Alone Contents Unit Overview 3 Learning and Teaching Activities within this Unit 5 Theme 1 What s the Idea? 6 Theme 2 The Entrepreneur s Experience

Unit Two Support for Starting a Business - You Are Not Alone Contents Unit Overview 3 Learning and Teaching Activities within this Unit 5 Theme 1 What s the Idea? 6 Theme 2 The Entrepreneur s Experience

Cooperative Education Financial Literacy Lesson Plan 3 Credit

Connections to Financial Literacy Cooperative Education Financial Literacy Lesson Plan 3 Credit The financial literacy knowledge and skills which will be addressed in this lesson as they relate to the

Connections to Financial Literacy Cooperative Education Financial Literacy Lesson Plan 3 Credit The financial literacy knowledge and skills which will be addressed in this lesson as they relate to the

Meeting the West Virginia State Standards

Meeting the West Virginia State Standards Financial Avenue provides online courses and mini-modules to help students gain important knowledge about the basics of personal money management. The Financial

Meeting the West Virginia State Standards Financial Avenue provides online courses and mini-modules to help students gain important knowledge about the basics of personal money management. The Financial

Credit: Pros and Cons

Credit: Pros and Cons Unit: 05 Lesson: 02 Suggested Duration: 4 Days Lesson Synopsis: All economic operations depend on the flow of money and credit through the economy. The focus of this lesson is to

Credit: Pros and Cons Unit: 05 Lesson: 02 Suggested Duration: 4 Days Lesson Synopsis: All economic operations depend on the flow of money and credit through the economy. The focus of this lesson is to

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

What Is Direct Loan Entrance Counseling?

What Is Direct Loan Entrance Counseling? Federal regulations require that you, as a first-time student loan borrower, complete an Entrance Counseling session. You can complete the entire session online

What Is Direct Loan Entrance Counseling? Federal regulations require that you, as a first-time student loan borrower, complete an Entrance Counseling session. You can complete the entire session online

Lesson Description. Texas Essential Knowledge and Skills (Target standards) National Standards (Supporting standards) PFL Terms Interest rate

National Standards (Supporting standards) PFL Terms Interest rate") Lesson Description This lesson focuses on the various sources people use for borrowing money or using credit. Some people, especially those who do not know all their options, borrow money from lenders

Lesson Description This lesson focuses on the various sources people use for borrowing money or using credit. Some people, especially those who do not know all their options, borrow money from lenders

My Credit Report Card

Lesson 1: My Credit Report Card Lesson Overview: This lesson will provide students with an overview of elements that are included in their credit report. Students will examine how various behaviors affect

Lesson 1: My Credit Report Card Lesson Overview: This lesson will provide students with an overview of elements that are included in their credit report. Students will examine how various behaviors affect

how much would you spend?

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

Living Debt Free. By Douglas Hoyes. BA, CA, CIRP, CBV, Trustee Co-Founder of

Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP, CBV, Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP, CBV, Trustee Co-Founder,

Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP, CBV, Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP, CBV, Trustee Co-Founder,

Teacher's Guide. Lesson Eight. Cars and Loans 01/11

Teacher's Guide $ Lesson Eight Cars and Loans 01/11 cars and loans websites websites for cars and loans The internet is probably the most extensive and dynamic source of information in our society. The

Teacher's Guide $ Lesson Eight Cars and Loans 01/11 cars and loans websites websites for cars and loans The internet is probably the most extensive and dynamic source of information in our society. The

516-294 Portage Ave Winnipeg, MB R3C 0B9 Phone #: (204) 989-1900 Fax #: (204) 989-1908 Toll Free #: 1-888-573-2383 E-mail: info@cfcs.mb.

989-1900 Fax #: (204) 989-1908 Toll Free #: 1-888-573-2383 E-mail: info@cfcs.mb.") 516-294 Portage Ave Winnipeg, MB R3C 0B9 Phone #: (204) 989-1900 Fax #: (204) 989-1908 Toll Free #: 1-888-573-2383 E-mail: info@cfcs.mb.ca debthelpmanitoba.com Todays Session Overview of Services Banking

516-294 Portage Ave Winnipeg, MB R3C 0B9 Phone #: (204) 989-1900 Fax #: (204) 989-1908 Toll Free #: 1-888-573-2383 E-mail: info@cfcs.mb.ca debthelpmanitoba.com Todays Session Overview of Services Banking

HOW MUCH HOUSE CAN YOU AFFORD?: STUDENT HANDOUT

INDIVIDUAL BORROWING LESSON: HOW MUCH HOUSE CAN YOU AFFORD?: STUDENT HANDOUT Congratulations! You were able to save and invest more than 10 percent of your budget over a few years, and you now have $10,000

INDIVIDUAL BORROWING LESSON: HOW MUCH HOUSE CAN YOU AFFORD?: STUDENT HANDOUT Congratulations! You were able to save and invest more than 10 percent of your budget over a few years, and you now have $10,000

Hofstra North Shore-LIJ School of Medicine. Office of Financial Aid

Hofstra North Shore-LIJ School of Medicine Office of Financial Aid Consumer Credit and Your Credit Report Joseph M. Nicolini, MHA Director of Financial Aid What We Will Cover Consumer credit and credit

Hofstra North Shore-LIJ School of Medicine Office of Financial Aid Consumer Credit and Your Credit Report Joseph M. Nicolini, MHA Director of Financial Aid What We Will Cover Consumer credit and credit

Personal Financial Literacy

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

General Financial Literacy

General Financial Literacy Levels: Grades 11-12 Units of Credit: 0.50 Core Code: 01-00-00-00-100 Prerequisite: None COURSE DESRIPTION The General Financial Literacy course for juniors and seniors encompasses

General Financial Literacy Levels: Grades 11-12 Units of Credit: 0.50 Core Code: 01-00-00-00-100 Prerequisite: None COURSE DESRIPTION The General Financial Literacy course for juniors and seniors encompasses

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description Students will learn various methods to pay for college, including savings, grants, scholarships, student loans, and work-study. They will create an interactive notebook in which they

Lesson Description Students will learn various methods to pay for college, including savings, grants, scholarships, student loans, and work-study. They will create an interactive notebook in which they

Theme Introduction: Credit. Missouri Competencies: Credit

THEME 6 Theme Introduction: COURSE TITLE: Personal Finance Missouri Competencies: SC.3: Compare the advantages and disadvantages of different payment methods. SC.4: Analyze the benefits and costs of consumer

THEME 6 Theme Introduction: COURSE TITLE: Personal Finance Missouri Competencies: SC.3: Compare the advantages and disadvantages of different payment methods. SC.4: Analyze the benefits and costs of consumer

Financial Empowerment Curriculum. Moving Ahead Through Financial Management. Module Three: Mastering Credit Basics

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

JA ECONOMICS FOR SUCCESS (2012 Version)

") JA ECONOMICS FOR SUCCESS (2012 Version) Important Notes: Reference Working with Students page before teaching. Session 1 When giving directions to students, please provide oral and written explanation

JA ECONOMICS FOR SUCCESS (2012 Version) Important Notes: Reference Working with Students page before teaching. Session 1 When giving directions to students, please provide oral and written explanation

Four Steps to Reduce Your Debt

Four Steps to Reduce Your Debt Overview Simple steps you can take to reduce your debt. Admit that you have a problem and commit yourself to fixing it. Stop debt spending. Make a spending plan. Pay down

Four Steps to Reduce Your Debt Overview Simple steps you can take to reduce your debt. Admit that you have a problem and commit yourself to fixing it. Stop debt spending. Make a spending plan. Pay down

Paying with Plastic: An Introduction to Credit Cards

financial literacy Paying with Plastic: An Introduction to Credit Cards Aim To foster awareness of the link between responsible credit card use and the ability to achieve financial goals. Objectives At

financial literacy Paying with Plastic: An Introduction to Credit Cards Aim To foster awareness of the link between responsible credit card use and the ability to achieve financial goals. Objectives At

Improving Access to Postsecondary Education

Ministry of Finance JOBS FOR TODAY AND TOMORROW 2016 ONTARIO BUDGET Improving Access to Postsecondary Education The government is transforming student financial assistance to make postsecondary education

Ministry of Finance JOBS FOR TODAY AND TOMORROW 2016 ONTARIO BUDGET Improving Access to Postsecondary Education The government is transforming student financial assistance to make postsecondary education

lesson thirteen in trouble overheads

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

Essential Skills. for Entrepreneurs. Instructor s Overview

Essential Skills for Entrepreneurs Workplace Education Manitoba, 2009 All rights reserved; no part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any

Essential Skills for Entrepreneurs Workplace Education Manitoba, 2009 All rights reserved; no part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any

Youth Education Agenda Age 13-17: Real Life

Youth Education Agenda Age 13-17: Real Life Orientation Each child will receive a worksheet with an assigned credit score, occupation, and annual income. Real Life Session 1. Set Savings Goal 2. Life Stages

Youth Education Agenda Age 13-17: Real Life Orientation Each child will receive a worksheet with an assigned credit score, occupation, and annual income. Real Life Session 1. Set Savings Goal 2. Life Stages

MODULE EIGHT. Credit Reports MODULE EIGHT

making ends meet... and more! Before You Begin Once again, a need for trusting relationships is likely to affect whether women will go to a Credit Bureau. Through conversations with Stella s Circle participants

making ends meet... and more! Before You Begin Once again, a need for trusting relationships is likely to affect whether women will go to a Credit Bureau. Through conversations with Stella s Circle participants

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING

ABCs OF MORTGAGES SERIES BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING Smart mortgage decisions start here About Financial Consumer Agency of Canada (FCAC) With educational materials

ABCs OF MORTGAGES SERIES BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING Smart mortgage decisions start here About Financial Consumer Agency of Canada (FCAC) With educational materials

What are the risks of choosing and using credit cards?

Credit Cards 2 Money Matters The BIG Idea What are the risks of choosing and using credit cards? AGENDA Approx. 45 minutes I. Warm Up: A Credit Card You Can t Pass Up? (10 minutes) II. Credit Card Advantages

Credit Cards 2 Money Matters The BIG Idea What are the risks of choosing and using credit cards? AGENDA Approx. 45 minutes I. Warm Up: A Credit Card You Can t Pass Up? (10 minutes) II. Credit Card Advantages

A simulation of budgeting for grades 9-12 (3-5 players) Reach as many savings goals as possible without going over budget.

Reach as many savings goals as possible without going over budget.") A simulation of budgeting for grades 9-12 (3-5 players) 2011-14 - Scott Dixon Life Goal Reach as many savings goals as possible without going over budget. Getting Ready Draw a career card Prepare Expense

A simulation of budgeting for grades 9-12 (3-5 players) 2011-14 - Scott Dixon Life Goal Reach as many savings goals as possible without going over budget. Getting Ready Draw a career card Prepare Expense

How To Get EXACTLY What You Need Financially To Go To College. Student/Parent Workbook

How To Get EXACTLY What You Need Financially To Go To College Student/Parent Workbook How To Get EXACTLY What You Need Financially To Go To College Too many students graduate with more debt than they can

How To Get EXACTLY What You Need Financially To Go To College Student/Parent Workbook How To Get EXACTLY What You Need Financially To Go To College Too many students graduate with more debt than they can

Shopping Savvy. 2 days. What should shoppers know before they spend their hard earned money? Materials. Overview

B L A C K F R I D A Y L E S S O N Shopping Savvy L E S S O N 2 days What should shoppers know before they spend their hard earned money? Overview Students work in small groups to prepare for a news conference

B L A C K F R I D A Y L E S S O N Shopping Savvy L E S S O N 2 days What should shoppers know before they spend their hard earned money? Overview Students work in small groups to prepare for a news conference

Income, Expenses and Budget module

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

Credit and Debt Management module

Credit and Debt Management module Trainer s introduction Credit and debt probably cause more serious consumer problems than any other topic. It s relatively easy to take on debt, but harder to manage it

Credit and Debt Management module Trainer s introduction Credit and debt probably cause more serious consumer problems than any other topic. It s relatively easy to take on debt, but harder to manage it

How Credit Affects Your Life Episode # 205

How Credit Affects Your Life Episode # 205 LESSON LEVEL Grades 9-12 Key topics Credit Debit Debt Time Needed Preview & Screening: 45 minutes Activity #1: 45-60 minutes Activity #2: 60-90 minutes Episode

How Credit Affects Your Life Episode # 205 LESSON LEVEL Grades 9-12 Key topics Credit Debit Debt Time Needed Preview & Screening: 45 minutes Activity #1: 45-60 minutes Activity #2: 60-90 minutes Episode

Part 4: Borrowing Money and Using Credit

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

LESSON: Understanding credit and your credit report

LESSON: Understanding credit and your credit report 70 minutes Financial Literacy Outcome At the end of this lesson, students will: describe the impact of credit history and credit reports on their future

LESSON: Understanding credit and your credit report 70 minutes Financial Literacy Outcome At the end of this lesson, students will: describe the impact of credit history and credit reports on their future

SAMPLE. Quick Facts CONGRATULATIONS. Mr. John Doe, YOUR MORTGAGE PLAN ON YOUR HOME PURCHASE! about your mortgage. $450,000.00

1 SAMPLE Mr. John Doe, CONGRATULATIONS ON YOUR HOME PURCHASE! Quick Facts about your mortgage. AMOUNT $450,000.00 TERM INTEREST RATE 3.00% FIXED TERM, 5 YEARS PAYMENT $2,129.60 / MONTH TERM 5 Years ENDS

1 SAMPLE Mr. John Doe, CONGRATULATIONS ON YOUR HOME PURCHASE! Quick Facts about your mortgage. AMOUNT $450,000.00 TERM INTEREST RATE 3.00% FIXED TERM, 5 YEARS PAYMENT $2,129.60 / MONTH TERM 5 Years ENDS

Lesson 9 Take Control of Debt: Using Credit Wisely

Lesson 9 Take Control of Debt: Use Credit Wisely Lesson Description In this lesson, students review the balance sheet (Lesson 1) and the budget worksheet (Lesson 2) and consider ways to use these two documents

Lesson 9 Take Control of Debt: Use Credit Wisely Lesson Description In this lesson, students review the balance sheet (Lesson 1) and the budget worksheet (Lesson 2) and consider ways to use these two documents

Take Charge of Your Finances Semester Course designed for 10 th -12 th grade students Class Period Length 45 minutes

Take Charge of Your Finances Semester Course designed for 10 th -12 th grade students Class Period Length 45 minutes SCANS Skills: Basic Skills: reading, writing, mathematics, listening, speaking Thinking

Take Charge of Your Finances Semester Course designed for 10 th -12 th grade students Class Period Length 45 minutes SCANS Skills: Basic Skills: reading, writing, mathematics, listening, speaking Thinking

Site Tour Main Page Paying for College Money Management Student Loan Repayment Paying For College Money Management Student Loan Repayment

Site Tour Main Page GradReady is organized by three core topics: Paying for College, Money Management, and Student Loan Repayment. This concept enables the student to access financial literacy topics that

Site Tour Main Page GradReady is organized by three core topics: Paying for College, Money Management, and Student Loan Repayment. This concept enables the student to access financial literacy topics that

Teacher's Guide. Lesson Nine. In Trouble 04/09

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

The Good Credit Game Alignment with Financial Education National Standards

The Good Credit Game Alignment with Financial Education National Standards There are a number of national standards for teaching personal finance and financial literacy. Many of the learning objectives

The Good Credit Game Alignment with Financial Education National Standards There are a number of national standards for teaching personal finance and financial literacy. Many of the learning objectives

Don t Become a Victim

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

Don t Become a Victim Life Smarts: 1. Determine the federal laws that assist consumers from becoming victims of predatory lending. What is predatory lending? Predatory lending is the unfair, deceptive,

WealthStyles. Cornerstone of a solid financial plan Wise debt management

WealthStyles Cornerstone of a solid financial plan Wise debt management Two years ago, David moved to a new city and put quite a few purchases on his credit card as he furnished a new home. Then, unexpectedly,

WealthStyles Cornerstone of a solid financial plan Wise debt management Two years ago, David moved to a new city and put quite a few purchases on his credit card as he furnished a new home. Then, unexpectedly,

What are local sources of part-time work for teens and how can I find out more about them?

Jobs for Teens 2 FINDING A JOB The BIG Idea What are local sources of part-time work for teens and how can I find out more about them? AGENDA Approx. 45 minutes I. Warm Up (10 minutes) II. How to Make

Jobs for Teens 2 FINDING A JOB The BIG Idea What are local sources of part-time work for teens and how can I find out more about them? AGENDA Approx. 45 minutes I. Warm Up (10 minutes) II. How to Make

Money Math for Teens. Credit Score

Money Math for Teens This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation, Channel One

Money Math for Teens This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation, Channel One

hours to qualify for the secondary school diploma.

The Ontario Secondary School Program is designed to equip students with the knowledge and skills they will need to lead satisfying and productive lives. The program will prepare students for further education

The Ontario Secondary School Program is designed to equip students with the knowledge and skills they will need to lead satisfying and productive lives. The program will prepare students for further education

College Loan Debt: Is It Worth It?

College Loan Debt: Is It Worth It? Lesson Overview In this lesson, students compare the benefits of a college education (which is primarily increased earning capacity) with the costs of borrowing to pay

College Loan Debt: Is It Worth It? Lesson Overview In this lesson, students compare the benefits of a college education (which is primarily increased earning capacity) with the costs of borrowing to pay

Home Sweet Home: Purchasing a Place

Home Sweet Home: Purchasing a Place LESSON 16: TEACHERS GUIDE Ask teens to describe their dream homes, and many will rattle off the features of the latest celebrity mansion they ve seen on TV: 10 bedrooms,

Home Sweet Home: Purchasing a Place LESSON 16: TEACHERS GUIDE Ask teens to describe their dream homes, and many will rattle off the features of the latest celebrity mansion they ve seen on TV: 10 bedrooms,

Faculty Innovator Grant 2011 Center for Learning Technologies. Final Report Form

Faculty Innovator Grant 2011 Final Report Form Primary Faculty Name: Hongwei Zhu Department: Information Technology and Decision Sciences Email Address: hzhu@odu.edu Office Phone Number: 683-5175 Project

Faculty Innovator Grant 2011 Final Report Form Primary Faculty Name: Hongwei Zhu Department: Information Technology and Decision Sciences Email Address: hzhu@odu.edu Office Phone Number: 683-5175 Project

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Experiencing. Personal Finance. An Illustrated Introduction to Personal Finance. Margaret Williams Mathew Georghiou

Sample Pages Experiencing Personal Finance An Illustrated Introduction to Personal Finance Margaret Williams Mathew Georghiou Table of Contents 3 Contents 1. Welcome... 7 2. GoVenture Personal Finance...

Sample Pages Experiencing Personal Finance An Illustrated Introduction to Personal Finance Margaret Williams Mathew Georghiou Table of Contents 3 Contents 1. Welcome... 7 2. GoVenture Personal Finance...