UNDERSTANDING YOUR FINANCIAL PACKAGE

|

|

|

- Rhoda Williamson

- 9 years ago

- Views:

Transcription

1 UNDERSTANDING YOUR FINANCIAL PACKAGE

2 UNDERSTANDING YOUR FINANCIAL AID Presenter: Lisa Wioskowski Financial Aid Coordinator, TGS Topics Cost of Attendance Federal Loans Fellowships Payments (Stipends) Non-compensatory Compensatory Teaching Asst. Research Asst. Graduate Presenter: Irene Jasper Director of Student Lending Topics Types of Income Taxable vs. Non-Taxable Qualified & Non-qualified Expenses Reporting Documents Resources

3 PH.D. FELLOWSHIPS The Graduate School (TGS) will post tuition, fees, and insurance awards directly to your bursar account around mid-september. TGS will not pay: flex, fines, or parking permits this is the students responsibility. External fellowship awards should be forwarded to TGS Financial Aid Office to verify and determine award for the following examples: Does the fellowship pay a stipend? If so, does Student receive payments? Does the fellowship pay tuition or fees?

4 COST OF ATTENDANCE (COA) BUDGET Fall 2014/Spring 2015 Tuition/Fees/Insurance: Living Portion: $48,878 Room $ 7,767 Board $ 4,563 Transportation $ 1,638 Personal & Misc. $ 3,411 Total $ 17,379 Monthly $1,931 for 9 months

5 FEDERAL LOAN PROGRAMS (FAFSA MUST BE FILED EACH YEAR) Unsubsidized Loan Maximum amount per academic year is $20,500 Interest rate is 6.21% Loan Fee is 1.073% Grace period 6 months after graduation or drop less than part-time (6 units is considered part-time) Grad Plus Loan Maximum amount per academic year is COA (deducting the unsubsidized loan if applicable) Interest rate is 7.21% Loan Fee is 4.292% Grace period is the same as the unsubsidized loan program.

Interest rate is 7.")

6 FELLOWSHIP (STIPEND) PAYMENTS STIPEND PAYMENTS ARE PROCESSED THROUGH PAYROLL NOT THROUGH BURSAR ACCOUNTS Non-compensatory Stipends No service required Paid on the last business day of each month. Compensatory Service required Determined by the department, and the years in which it is required Teaching Assistant Research Assistant Graduate Assistant Paid on the 25 th of each month.

7 SCHOLARSHIPS & FELLOWSHIP INCOME AND THE TAX IMPLICATIONS

8 TYPES OF INCOME Scholarships - Tend to be for the purpose of general education expenses. Fellowships - Generally to aid in the pursuit of study or research. Both considered non-compensatory, and may be taxable depending on expenses paid Research Grants - May be taxable Research Assistant Compensation Generally taxable. Teaching Assistant Compensation Generally taxable, BUT, may be exempt for Social Security tax. Stipends - A form of salary generally taxable

9 STIPEND NON-COMPENSATORY (Unearned) COMPENSATORY (Earned) A Duke student receives financial support to do research solely for his/her thesis that is needed for her degree. The research is not for, nor does it provide a benefit to a faculty member. A student is paid a stipend to participate in a conference directly related to their graduate studies. No work is performed As part of a degree program, a Duke student is paid to participate in summer internship program at an outside organization where he will focus on learning research techniques. He will not be providing a service to the outside organization, but is in a learning role. A faculty member is working on a project and pays a student to assist with the research. The student participation is not a degree requirement. If the student was not assisting with the research, the faculty member would have to hire someone else to do the work or do it himself. A student is paid a stipend to attend a faculty member s conference, arrange seating, mail invitations, and provide chauffeur service to/from hotels. A student is paid as an intern in a Duke department for providing research assistance. There is no program designed to train students as part of their degree requirements. The student is providing a needed service.

10 NON-COMPENSATORY INCOME TAXABLE OR NON-TAXABLE? Depends on the type of expenses paid with the funds and whether you are a degree candidate.

11 NON-DEGREE CANDIDATE Fully taxable

12 DEGREE CANDIDATE Portion used to pay Qualified Expenses is not taxable not included in gross income, and not required to be reported on an income tax return. Portion NOT used to pay Qualified Expenses is taxable included in gross income, and required to be reported on an income tax return.

13 QUALIFIED EXPENSES Tuition and fees required for enrollment Course-related expenses (fees, books, supplies, equipment) must be required of all students in the course

must be required of all")

14 NON-QUALIFED EXPENSES Insurance Medical expenses (including student health fees) Room and board Transportation Recreation fee Parking permit Activity fee

15 REPORTING DOCUMENTS W Misc Courtesy Letter 1098T 1042S Reporting Documents Type of Income Wages ie. Teaching Assistant, Work-Study, compensatory internships Scholarships, fellowships, non-compensatory internships & post-doctoral awards with tax withholding Scholarships, fellowships, non-compensatory internships & post-doctoral awards without tax withholding Duke Administered financial aid posted directly to the Bursar Account (Does not include financial aid administered by third parties) Earnings that fall within the scope of a tax treaty, scholarship, fellowships, non-compensatory internships & post-doctoral awards.

Earnings that fall within the scope of a tax treaty, scholarship, fellowships,")

16 W2

17 W2 Issued by Payroll Service to: Students who have a work requirement in order to receive their scholarship, grant, or fellowship money. All employees of Duke University and Duke University Health System who are US citizens, permanent residents, or residents for tax purposes. To foreign national employees who are not eligible for or do not claim a tax treaty. To foreign national employees whose earnings exceed allowable maximums of a tax treaty.

18 MISC

19 MISC Issued by Accounts Payable to students who are US citizens, permanent residents, or residents for tax purposes, and who receive payments through the non-compensatory payment system. Any scholarship and fellowship payment for which the student elected to have taxes withheld. All postdoctoral scholars and student internship payments. Box 3 Non-compensatory payments are payments Duke University makes to individuals who are receiving payments for scholarships, fellowships, summer internships, or post-doctoral training activities. Individuals receiving these payments are not considered a Duke employee, and are receiving funds through Duke University for educational enrichment opportunities. Box 7 Nonemployee Compensation - It is unlikely that you would receive independent contractor compensation from Duke or another funding agency for your role as a graduate student. Self-employment is indicated by income reported in Box 7 of a 1099-MISC. If you receive Box 7 income from your role as a graduate student, you may want to double-check with the issuing body that they have issued you the correct form.

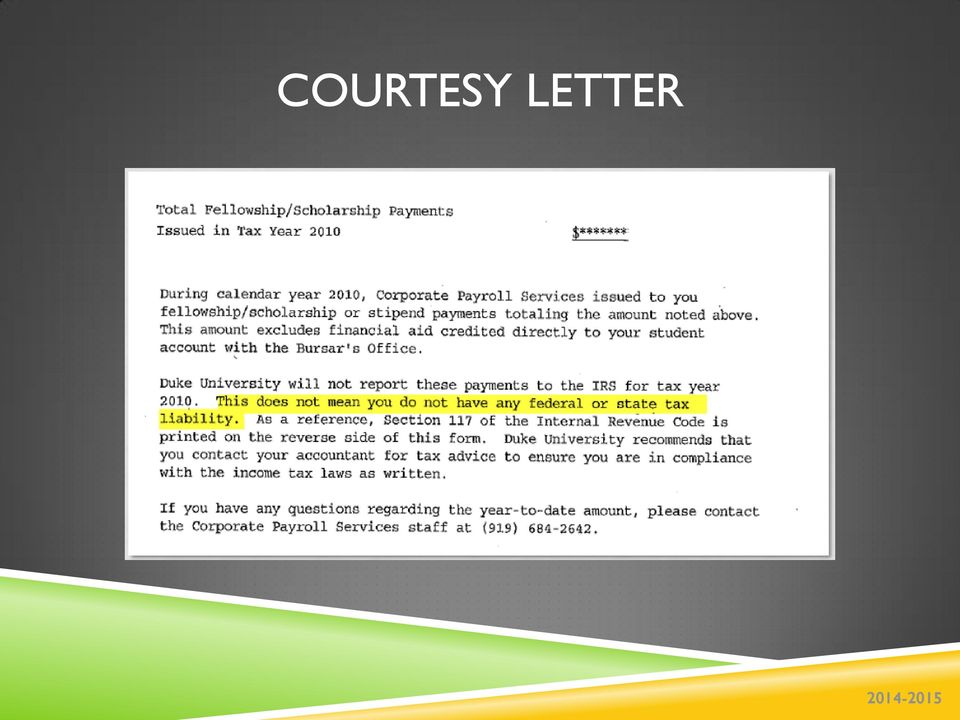

20 COURTESY LETTER

21 COURTESY LETTER The courtesy letter is issued by Payroll Services to students who are US citizens, permanent residents, or residents for tax purposes, who receive scholarships or fellowships through the non-compensatory payment system, and who choose not to have tax withholdings taken from their payments. Duke is not obligated, and doesn t report this amount to the IRS. This does not mean, however, that the payments are not taxable. It is up to the student to determine whether or not this is reportable income. This information is provided as a courtesy.

22 1098 T

23 1098T Box 2 The amount of qualified tuition and related expenses billed through your Bursar account. It is not the amount you paid. Box 5 The amount of scholarship and fellowship payments posted to your Bursar account T is issued by the Bursar s Office to students who are US citizens, permanent residents, or residents for tax purposes, and only to those students who had tuition & qualified fees billed during the calendar year that exceeds grants & scholarships posted during the same period.

24 RESOURCES Tax Seminar for Graduate Students with Sheila Ahler, CPA is full. Once the Tax Seminar recording is available, we will send an with a link provided.

25 RESOURCES

26 RESOURCES

Understanding your Forms W-2 and 1042-S

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

PAYMENTS TO STUDENTS AND THEIR TAXABILITY

The definitions provided in this document supersede all prior definitions. Responsible University Official: Vice President for Student Financial Services Responsible Office: Student Financial Services

The definitions provided in this document supersede all prior definitions. Responsible University Official: Vice President for Student Financial Services Responsible Office: Student Financial Services

Tax Treatment of Scholarships, Fellowships, and Stipends

Tax Treatment of Scholarships, Fellowships, and Stipends Prepared for the PhD students at Oregon Health and Science University March 8, 2011 Martin D. Moll, JD Brian A. Gaskins, CPA, CFP OBJECTIVE: To

Tax Treatment of Scholarships, Fellowships, and Stipends Prepared for the PhD students at Oregon Health and Science University March 8, 2011 Martin D. Moll, JD Brian A. Gaskins, CPA, CFP OBJECTIVE: To

Tax Information for Students and Scholars

Tax Information for Students and Scholars Student Financial Aid with assistance from Internal Revenue Service March 30, 2011 Topics of Discussion Who needs to file a tax return Taxation on Scholarships

Tax Information for Students and Scholars Student Financial Aid with assistance from Internal Revenue Service March 30, 2011 Topics of Discussion Who needs to file a tax return Taxation on Scholarships

TAX GUIDE FOR FOREIGN VISITORS

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1 Candidate for a Degree......

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1 Candidate for a Degree......

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

US Federal Income Tax for F-1 Student Visa Holders

1 US Federal Income Tax for F-1 Student Visa Holders 2 Please do not mistake the following information for tax advice; the following slides are intended for use as a frame of reference for the US Federal

1 US Federal Income Tax for F-1 Student Visa Holders 2 Please do not mistake the following information for tax advice; the following slides are intended for use as a frame of reference for the US Federal

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Marcia Johnson Senior Tax Analyst Benjamin Tsai Senior Tax Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Marcia Johnson Senior Tax Analyst Benjamin Tsai Senior Tax Analyst

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

UNDERSTANDING YOUR FORM W-2 AND 1042-S INFORMATION REGARDING YOUR FORM W-2 WAGE AND TAX STATEMENT The Form W-2 is your wage and tax statement provided by your employer to provide information on your taxable

U.S. Taxation of J-1 Exchange Visitors

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals

University of Utah Tax Services & Payroll Accounting Tax Overview

University of Utah Tax Services & Payroll Accounting Tax Overview Presented by: Kelly Peterson, CPA Tax Manager Tax Services website: www.tax.utah.edu Phone: 581-6699 Email: [email protected]

University of Utah Tax Services & Payroll Accounting Tax Overview Presented by: Kelly Peterson, CPA Tax Manager Tax Services website: www.tax.utah.edu Phone: 581-6699 Email: [email protected]

Federal tax benefits for higher education

Federal tax benefits for higher education Tax year 2010 You know that higher education is an investment in time, energy and money. Thankfully, there are ways to offset your education expenses through tax

Federal tax benefits for higher education Tax year 2010 You know that higher education is an investment in time, energy and money. Thankfully, there are ways to offset your education expenses through tax

United States Taxation for International Students. Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties

United States Taxation for International Students Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties 1 Disclaimer Please keep in mind that University of Arizona employees, while in their

United States Taxation for International Students Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties 1 Disclaimer Please keep in mind that University of Arizona employees, while in their

Scholarships awarded to Nonresident Alien Students

Scholarships awarded to Nonresident Alien Students IRS Compliance Issues Doug Podoll Georgia State University [email protected], 404-413-2070 General Rule Section 1441 of the Internal Revenue Code states

Scholarships awarded to Nonresident Alien Students IRS Compliance Issues Doug Podoll Georgia State University [email protected], 404-413-2070 General Rule Section 1441 of the Internal Revenue Code states

Tax Considerations for Graduate Students

Tax Considerations for Graduate Students Important Information Related to Tuition Assistance Benefit and/or Tuition Remission Disclaimer The information contained herein is accurate to the best of the

Tax Considerations for Graduate Students Important Information Related to Tuition Assistance Benefit and/or Tuition Remission Disclaimer The information contained herein is accurate to the best of the

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services Agenda Important Information for 2012 Returns U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services Agenda Important Information for 2012 Returns U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends

BLOOMFIELD COLLEGE. Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships

BLOOMFIELD COLLEGE Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships Administration & Finance 7/1/2013 Table of Contents INDEPENDENT CONTRACTOR POLICY... 2 Background...

BLOOMFIELD COLLEGE Policy on Independent Contractors; Honorariums; and Prizes, Awards, Gifts & Scholarships Administration & Finance 7/1/2013 Table of Contents INDEPENDENT CONTRACTOR POLICY... 2 Background...

Nonresident Alien Tax Issues and the GLACIER System. A Primer

Nonresident Alien Tax Issues and the System A Primer April 4, 2014 Objectives Review Nonresident Alien tax issues Glacier: Who, What, Where, When & Why? Online Demonstration Pay Period Implications to

Nonresident Alien Tax Issues and the System A Primer April 4, 2014 Objectives Review Nonresident Alien tax issues Glacier: Who, What, Where, When & Why? Online Demonstration Pay Period Implications to

Tax Consequences of Providing IT Consulting Services

Tax Consequences of Providing IT Consulting Services Presented By:, CA, CPA And Offices in Toronto & Chicago 1-888- US TAXES Canadian IT Contractors Can Work: As employees; Pros & Cons of Being an Employee

Tax Consequences of Providing IT Consulting Services Presented By:, CA, CPA And Offices in Toronto & Chicago 1-888- US TAXES Canadian IT Contractors Can Work: As employees; Pros & Cons of Being an Employee

Learning Today, Leading Tomorrow FINANCIAL AID

Learning Today, Leading Tomorrow STUDENT FINANCIAL AID SUCCESSFULLY NAVIGATING THE STUDENT FINANCIAL AID PROCESS The Northern Illinois University Student Financial Aid Office (SFAO) is pleased to assist

Learning Today, Leading Tomorrow STUDENT FINANCIAL AID SUCCESSFULLY NAVIGATING THE STUDENT FINANCIAL AID PROCESS The Northern Illinois University Student Financial Aid Office (SFAO) is pleased to assist

Student loan terms to know

Definition of words related to federal student loans and the Nelnet payment process. Accrue The act of interest accumulating on the borrower s principle balance. Aggregate Loan Limit The maximum total

Definition of words related to federal student loans and the Nelnet payment process. Accrue The act of interest accumulating on the borrower s principle balance. Aggregate Loan Limit The maximum total

MEMORANDUM. Deans, Chairs, Directors and Business Managers. John R. Raymond, M.D. John C. Sutusky, Ph.D. Processing Payments to Fellows and Trainees

OFFICE OF THE Vice President for Finance and Administration ADMINISTRATION BUILDING 171 ASHLEY AVE, SUITE 200B PO BOX 250003 CHARLESTON SC 29425 (843) 792-5050 FAX (843) 792-4975 MEMORANDUM TO: FROM: RE:

OFFICE OF THE Vice President for Finance and Administration ADMINISTRATION BUILDING 171 ASHLEY AVE, SUITE 200B PO BOX 250003 CHARLESTON SC 29425 (843) 792-5050 FAX (843) 792-4975 MEMORANDUM TO: FROM: RE:

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016 MIT International Students Office & Office of the Vice President

Frequently Asked Questions for Non Resident Alien Taxation

Frequently Asked Questions for Non Resident Alien Taxation A. Income 1. Compensation I worked abroad for the summer. Do I have to include this income on my tax return? 2. Scholarships and Fellowships I

Frequently Asked Questions for Non Resident Alien Taxation A. Income 1. Compensation I worked abroad for the summer. Do I have to include this income on my tax return? 2. Scholarships and Fellowships I

Processing of Payments for Non-Employees

Processing of Payments for Non-Employees September 26, 2012 Presented by Steven Truong and Oksana Haehn 1 Today s Topics What is a non-employment payment? What is the department s role? Detailed review

Processing of Payments for Non-Employees September 26, 2012 Presented by Steven Truong and Oksana Haehn 1 Today s Topics What is a non-employment payment? What is the department s role? Detailed review

Welcome to. Payroll Training for UNLV STAFF UNLV. Presented by: Mary Jimenez Green. Controller s Office. University of Nevada Las Vegas

Welcome to Payroll Training for UNLV STAFF Presented by: Mary Jimenez Green Payroll Team Mary Jimenez Green Manager Cynthia Reynolds Supervisor Shyla McLaughlin Processes classified payroll, PERS, and

Welcome to Payroll Training for UNLV STAFF Presented by: Mary Jimenez Green Payroll Team Mary Jimenez Green Manager Cynthia Reynolds Supervisor Shyla McLaughlin Processes classified payroll, PERS, and

The Bursar s Office looks forward to assisting you with your financial needs during your enrollment at Rollins College.

Dear Parents & Students: Important financial information for CPS/A&S students for the 2015-2016 academic year is covered in this document. Information regarding tuition and fees, billing schedules, the

Dear Parents & Students: Important financial information for CPS/A&S students for the 2015-2016 academic year is covered in this document. Information regarding tuition and fees, billing schedules, the

Understanding Your Financial Aid Award

Important information related to your financial aid award from the University of Richmond is contained in this document, including the terms and conditions of your award package. Please review this information

Important information related to your financial aid award from the University of Richmond is contained in this document, including the terms and conditions of your award package. Please review this information

GENERAL INCOME TAX INFORMATION

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

NEW YORK STATE TEACHERS RETIREMENT SYSTEM GENERAL INCOME TAX INFORMATION TABLE OF CONTENTS Taxes on Loans from the Annuity Savings Fund 1 (Tier 1 and 2 Members Only) Taxes on the Withdrawal of the Annuity

Frequently Asked Questions

Frequently Asked Questions Questions and answers are divided into the following topics BEFORE USING GLACIER Tax Prep ENTERING DATA INTO GLACIER Tax Prep RESULTS FROM GLACIER Tax Prep WHAT TO DO WHEN FINISHED

Frequently Asked Questions Questions and answers are divided into the following topics BEFORE USING GLACIER Tax Prep ENTERING DATA INTO GLACIER Tax Prep RESULTS FROM GLACIER Tax Prep WHAT TO DO WHEN FINISHED

OptRight Online: 2013 Year End Customer Guide

November 2013 Wells Fargo Business Payroll Services OptRight Online: 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide

November 2013 Wells Fargo Business Payroll Services OptRight Online: 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide

Nonresident Tax Information Session. Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center

Nonresident Tax Information Session Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center What we will cover. 1. Federal tax issues 2. Forms you receive and fill out 3. Determination

Nonresident Tax Information Session Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center What we will cover. 1. Federal tax issues 2. Forms you receive and fill out 3. Determination

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS Presented by: Lisa Kosiewicz Doran International Student Specialist Office of International Programs Sarah Hintz, CPA Tax and Compliance

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS Presented by: Lisa Kosiewicz Doran International Student Specialist Office of International Programs Sarah Hintz, CPA Tax and Compliance

College Prep Course (BIM) 2015-2016. Empowering our Students for life after high school For Excellence beyond HS

2015-2016. Empowering our Students for life after high school For Excellence beyond HS") College Prep Course (BIM) 2015-2016 Empowering our Students for life after high school For Excellence beyond HS LESSON OBJECTIVE Content Objective The student learn the steps and guidelines in preparing

College Prep Course (BIM) 2015-2016 Empowering our Students for life after high school For Excellence beyond HS LESSON OBJECTIVE Content Objective The student learn the steps and guidelines in preparing

Internal Revenue Service Wage and Investment

Internal Revenue Service Wage and Investment Stakeholder Partnerships, Education and Communication Winter/Spring 2015 Income Tax Workshop for Nonresident Aliens Please Note This workshop is for students

Internal Revenue Service Wage and Investment Stakeholder Partnerships, Education and Communication Winter/Spring 2015 Income Tax Workshop for Nonresident Aliens Please Note This workshop is for students

Graduate School of Arts and Science. Financing Graduate Education

Graduate School of Arts and Science Financing Graduate Education New York University s Graduate School of Arts and Science provides an exciting opportunity to participate in pioneering research, learn

Graduate School of Arts and Science Financing Graduate Education New York University s Graduate School of Arts and Science provides an exciting opportunity to participate in pioneering research, learn

FINANCIAL AID How does it work for you?

FINANCIAL AID How does it work for you? The Office of Admission and Financial Aid, School of Social Work 1798 Asylum Avenue Wet Hartford Connecticut Telephone: 860-570-9125 Fax:860-570 9052 University

FINANCIAL AID How does it work for you? The Office of Admission and Financial Aid, School of Social Work 1798 Asylum Avenue Wet Hartford Connecticut Telephone: 860-570-9125 Fax:860-570 9052 University

FREQUENTLY-ASKED QUESTIONS DARTMOUTH COLLEGE TUITION BENEFITS

FREQUENTLY-ASKED QUESTIONS DARTMOUTH COLLEGE TUITION BENEFITS What are the Dartmouth College Tuition Assistance benefits? The tuition assistance benefits for Dartmouth College employees are available in

FREQUENTLY-ASKED QUESTIONS DARTMOUTH COLLEGE TUITION BENEFITS What are the Dartmouth College Tuition Assistance benefits? The tuition assistance benefits for Dartmouth College employees are available in

Roth 403(b) Contribution Option

Contribution Option") Roth 403(b) Contribution Option Frequently Asked Questions George Mason University offers a Roth 403(b) contribution option under the George Mason University Tax Deferred Savings Plan (the Plan ). The

Roth 403(b) Contribution Option Frequently Asked Questions George Mason University offers a Roth 403(b) contribution option under the George Mason University Tax Deferred Savings Plan (the Plan ). The

Financial Aid @ Austin Grad Overview & Policies

Financial Aid @ Austin Grad Overview & Policies Financial Aid Director Dave Arthur (512) 476-2772 x 105 [email protected] CONTENTS Financing your Austin Grad Education 2 The FAFSA 3 Helpful websites

Financial Aid @ Austin Grad Overview & Policies Financial Aid Director Dave Arthur (512) 476-2772 x 105 [email protected] CONTENTS Financing your Austin Grad Education 2 The FAFSA 3 Helpful websites

The Tuition Assistance Plan

The Tuition Assistance Plan Introduction p. 1 If You Have Questions p. 1 Eligibility p. 2 When You May Begin Receiving Tuition Assistance p. 2 Courses That Qualify for Reimbursement p. 2 Courses That Do

The Tuition Assistance Plan Introduction p. 1 If You Have Questions p. 1 Eligibility p. 2 When You May Begin Receiving Tuition Assistance p. 2 Courses That Qualify for Reimbursement p. 2 Courses That Do

AMERICAN UNIVERSITY OF ANTIGUA COLLEGE OF MEDICINE APPROVED TO PARTICIPATE IN WILLIAM D FORD DIRECT LOAN PROGRAM APPROVAL DATE : 10/15/15

AMERICAN UNIVERSITY OF ANTIGUA COLLEGE OF MEDICINE APPROVED TO PARTICIPATE IN WILLIAM D FORD DIRECT LOAN PROGRAM APPROVAL DATE : 10/15/15 Disclaimer 2 This presentation highlights the basics of Title IV

AMERICAN UNIVERSITY OF ANTIGUA COLLEGE OF MEDICINE APPROVED TO PARTICIPATE IN WILLIAM D FORD DIRECT LOAN PROGRAM APPROVAL DATE : 10/15/15 Disclaimer 2 This presentation highlights the basics of Title IV

Frequently Asked Tax Questions 2014 Tax Filing Season

Frequently Asked Tax Questions 2014 Tax Filing Season Q. How do I determine if I am a resident alien for tax purposes? A. F-1, J-1, M or Q students are considered non-residents for tax purposes for their

Frequently Asked Tax Questions 2014 Tax Filing Season Q. How do I determine if I am a resident alien for tax purposes? A. F-1, J-1, M or Q students are considered non-residents for tax purposes for their

2. Since I already had taxes withheld from my paycheck, do I need to file an income tax return?

GENERAL FILING REQUIREMENTS 1. Who needs to file an income tax return? If you are visiting the U.S. from another country on an F, J, M or Q visa and are classified as a nonresident for U.S. tax purposes,

GENERAL FILING REQUIREMENTS 1. Who needs to file an income tax return? If you are visiting the U.S. from another country on an F, J, M or Q visa and are classified as a nonresident for U.S. tax purposes,

9 - Federal Tax Reporting/ Social Security

Illinois Municipal Retirement Fund Federal Tax Reporting & Social Security / SECTION 9 9 - Federal Tax Reporting/ Social Security APPENDIX - FEDERAL TAX REPORTING/SOCIAL SECURITY... 291 9.00 INTRODUCTION...

Illinois Municipal Retirement Fund Federal Tax Reporting & Social Security / SECTION 9 9 - Federal Tax Reporting/ Social Security APPENDIX - FEDERAL TAX REPORTING/SOCIAL SECURITY... 291 9.00 INTRODUCTION...

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

children s scholarship plan

children s scholarship plan Human Resources Department March 2001 MIT provides two Plans to help you with the cost of continuing education for your children: The Children s Scholarship Plan provides tuition

children s scholarship plan Human Resources Department March 2001 MIT provides two Plans to help you with the cost of continuing education for your children: The Children s Scholarship Plan provides tuition

1. Nonresident Alien or Resident Alien?

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

FAQs about the 1098-T Contents

Contents What is the 1098-T form?... 2 Why did I receive a 1098-T and what am I supposed to do with it?... 2 What other information do I need to claim the tax credit?... 2 Sample 1098-T... 3 Did Saint

Contents What is the 1098-T form?... 2 Why did I receive a 1098-T and what am I supposed to do with it?... 2 What other information do I need to claim the tax credit?... 2 Sample 1098-T... 3 Did Saint

Tax Tips for the. Cosmetology. Barber Industry

Tax Tips for the Cosmetology & Barber Industry Whether a shop owner, an employee, or a booth renter (independent contractor), you need to know your federal tax responsibilities, including how to report

Tax Tips for the Cosmetology & Barber Industry Whether a shop owner, an employee, or a booth renter (independent contractor), you need to know your federal tax responsibilities, including how to report

Financial Aid Application 2008-09

AlfredUniversity Financial Aid Application 2008-09 Student Financial Aid Office Alfred University Saxon Drive Alfred, NY 14802 PHONE: (607) 871-2159 FAX: (607) 871-2252 www.alfred.edu 1. 2. Name Last First

AlfredUniversity Financial Aid Application 2008-09 Student Financial Aid Office Alfred University Saxon Drive Alfred, NY 14802 PHONE: (607) 871-2159 FAX: (607) 871-2252 www.alfred.edu 1. 2. Name Last First

A Guide to Financial Aid 2015-16. The bottom line and how to pay for it.

A Guide to Financial Aid 2015-16 The bottom line and how to pay for it. The Financial Aid Basics We re glad you are interested in attending Anderson University. Perhaps you have already received your acceptance

A Guide to Financial Aid 2015-16 The bottom line and how to pay for it. The Financial Aid Basics We re glad you are interested in attending Anderson University. Perhaps you have already received your acceptance

Independent Special Circumstance Form 2014-2015

Independent Special Circumstance Form 2014-2015 Please print Students Name: Student ID # Last First M.I Address: Phone # City State Zip Please indicate all the circumstances that may apply to your situation.

Independent Special Circumstance Form 2014-2015 Please print Students Name: Student ID # Last First M.I Address: Phone # City State Zip Please indicate all the circumstances that may apply to your situation.

A Guide to Financial Aid 2016-17. The bottom line and how to pay for it.

A Guide to Financial Aid 2016-17 The bottom line and how to pay for it. The Financial Aid Basics We re glad you are interested in attending Anderson University. Perhaps you have already received your acceptance

A Guide to Financial Aid 2016-17 The bottom line and how to pay for it. The Financial Aid Basics We re glad you are interested in attending Anderson University. Perhaps you have already received your acceptance

Instructions for Form 8863

2015 Instructions for Form 8863 Education Credits (American Opportunity and Lifetime Learning Credits) Department of the Treasury Internal Revenue Service General Instructions Section references are to

2015 Instructions for Form 8863 Education Credits (American Opportunity and Lifetime Learning Credits) Department of the Treasury Internal Revenue Service General Instructions Section references are to

GRADUATE APPLICATION INSTRUCTIONS

201/201 GRADUATE APPLICATION INSTRUCTIONS All applicants must submit all of the required materials listed below to complete their applications for review. Do not send materials/credentials to departments.

201/201 GRADUATE APPLICATION INSTRUCTIONS All applicants must submit all of the required materials listed below to complete their applications for review. Do not send materials/credentials to departments.

DISCLAIMER. The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance.

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

TAXES AND GRADUATE STUDENTS. Income reporting requirements and education deduction/ credit possibilities

TAXES AND GRADUATE STUDENTS Income reporting requirements and education deduction/ credit possibilities DISCLOSURE: The materials presented in today s workshop are for informational purposes only and not

TAXES AND GRADUATE STUDENTS Income reporting requirements and education deduction/ credit possibilities DISCLOSURE: The materials presented in today s workshop are for informational purposes only and not

Tax Benefits for Education

Department of the Treasury Internal Revenue Service Contents Future Developments 2 Publication 970 What's New 2 Cat No 25221V Reminders 2 Tax Benefits for Education Introduction 3 For use in preparing

Department of the Treasury Internal Revenue Service Contents Future Developments 2 Publication 970 What's New 2 Cat No 25221V Reminders 2 Tax Benefits for Education Introduction 3 For use in preparing

Financial Aid. Eligibility Requirements for Federal Student Aid. University of California, Irvine 2015-2016 1. On This Page:

University of California, Irvine 2015-2016 1 Financial Aid On This Page: Financial Aid Eligibility Requirements for Federal Student Aid UCI Policies on Satisfactory Academic Progress for Financial Aid

University of California, Irvine 2015-2016 1 Financial Aid On This Page: Financial Aid Eligibility Requirements for Federal Student Aid UCI Policies on Satisfactory Academic Progress for Financial Aid

Payroll Services General Information

Payroll Services General Information Pay Day District employees are paid monthly. Payday is generally the last working day of the month, unless otherwise notified. Direct Deposits As of January 1, 2006,

Payroll Services General Information Pay Day District employees are paid monthly. Payday is generally the last working day of the month, unless otherwise notified. Direct Deposits As of January 1, 2006,

The Small Business Guide To Employment Taxes

The Small Business Guide To Employment Taxes Roanoke Regional Small Business Development Center 210 S. Jefferson Street Roanoke, VA 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

The Small Business Guide To Employment Taxes Roanoke Regional Small Business Development Center 210 S. Jefferson Street Roanoke, VA 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

Revised May 2015 (513) 556-5487

556-5487") Revised May 2015 (513) 556-5487 University of Cincinnati Federal Work-Study Program User s Manual TABLE OF CONTENTS INTRODUCTION... 2 I. PURPOSE OF THE FEDERAL WORK-STUDY PROGRAM... 2 II. THE FEDERAL WORK-STUDY

Revised May 2015 (513) 556-5487 University of Cincinnati Federal Work-Study Program User s Manual TABLE OF CONTENTS INTRODUCTION... 2 I. PURPOSE OF THE FEDERAL WORK-STUDY PROGRAM... 2 II. THE FEDERAL WORK-STUDY

EWU s Academic Value: Financial Aid for Eagles. real numbers, advice that works and a few tips, too

EWU s Academic Value: Financial Aid for Eagles real numbers, advice that works and a few tips, too Is college worth it? Four-year college grads are also more likely to volunteer, vote, read to their children,

EWU s Academic Value: Financial Aid for Eagles real numbers, advice that works and a few tips, too Is college worth it? Four-year college grads are also more likely to volunteer, vote, read to their children,

UNDERSTANDING THE GMS AWARDING PROCESS: A RESOURCE GUIDE FOR GATES MILLENNIUM SCHOLARS

UNDERSTANDING THE GMS AWARDING PROCESS: A RESOURCE GUIDE FOR GATES MILLENNIUM SCHOLARS Table of Contents 1. GMS Greeting............................................ page 1 2. Applying for Federal Financial

UNDERSTANDING THE GMS AWARDING PROCESS: A RESOURCE GUIDE FOR GATES MILLENNIUM SCHOLARS Table of Contents 1. GMS Greeting............................................ page 1 2. Applying for Federal Financial

Departmental Requirements and Procedures for Graduate Degrees in Physiology and Neurobiology

Departmental Requirements and Procedures for Graduate Degrees in Physiology and Neurobiology Effective: September, 2013 to Present TABLE OF CONTENTS A. Research and Rotations 1 B. Curriculum 1 C. Advisory

Departmental Requirements and Procedures for Graduate Degrees in Physiology and Neurobiology Effective: September, 2013 to Present TABLE OF CONTENTS A. Research and Rotations 1 B. Curriculum 1 C. Advisory

The University of Mississippi. Doctoral Degrees

The University of Mississippi Doctoral Degrees GENERAL REQUIREMENTS FOR ALL HIGHER DEGREES Degrees higher than the baccalaureate are granted at The University of Mississippi because of special attainments

The University of Mississippi Doctoral Degrees GENERAL REQUIREMENTS FOR ALL HIGHER DEGREES Degrees higher than the baccalaureate are granted at The University of Mississippi because of special attainments

PAYROLL OFFICE PROCEDURE MANUAL EFFECTIVE JANUARY 1, 1993 REVISED 11-16-09

PAYROLL OFFICE PROCEDURE MANUAL EFFECTIVE JANUARY 1, 1993 REVISED 11-16-09 OBJECTIVE The purpose of the Payroll Office is to process all payments to employees as a direct result of employment at Morehead

PAYROLL OFFICE PROCEDURE MANUAL EFFECTIVE JANUARY 1, 1993 REVISED 11-16-09 OBJECTIVE The purpose of the Payroll Office is to process all payments to employees as a direct result of employment at Morehead

FINANCIAL AID FOR LAW SCHOOL: A PRELIMINARY GUIDE. LSAC.org

LSAC.org FINANCIAL AID FOR LAW SCHOOL: A PRELIMINARY GUIDE INTRODUCTION Legal education is an investment in your future and is a serious financial investment as well. As with any investment, it is important

LSAC.org FINANCIAL AID FOR LAW SCHOOL: A PRELIMINARY GUIDE INTRODUCTION Legal education is an investment in your future and is a serious financial investment as well. As with any investment, it is important

2015 2016 FINANCIAL AID Handbook. alverno.edu

2015 2016 FINANCIAL AID Handbook alverno.edu Dear Student, Welcome to the Alverno College Financial Aid Office! You will find our staff is dedicated to helping you meet the expenses associated with achieving

2015 2016 FINANCIAL AID Handbook alverno.edu Dear Student, Welcome to the Alverno College Financial Aid Office! You will find our staff is dedicated to helping you meet the expenses associated with achieving

Educational Reimbursement Plan. Marathon Petroleum Educational Reimbursement Plan

Marathon Petroleum Educational Reimbursement Plan Effective January 1, 2015 Table of Contents I. Objective... 1 II. Employee Eligibility... 1 III. Educational Reimbursement Benefits... 2 A. Tuition Assistance...

Marathon Petroleum Educational Reimbursement Plan Effective January 1, 2015 Table of Contents I. Objective... 1 II. Employee Eligibility... 1 III. Educational Reimbursement Benefits... 2 A. Tuition Assistance...

LOAN REFLECTION. Directions: Complete the handout below individually and share your answers with your small group.

LOAN REFLECTION Directions: Complete the handout below individually and share your answers with your small group. Have you ever heard the word loan before? In what context? What comes to mind when you

LOAN REFLECTION Directions: Complete the handout below individually and share your answers with your small group. Have you ever heard the word loan before? In what context? What comes to mind when you

The W 2 form is issued and distributed by UCSF Campus Payroll Services. There are two methods of distribution from which you may choose:

Summary The IRS Form W 2 reports taxable earnings paid to employees between January 1 and December 31 of each calendar year. Taxable earnings are gross payments less any tax deferred deductions, such as

Summary The IRS Form W 2 reports taxable earnings paid to employees between January 1 and December 31 of each calendar year. Taxable earnings are gross payments less any tax deferred deductions, such as

INFORMATION ABOUT YOUR FINANCIAL AID AWARD

INFORMATION ABOUT YOUR FINANCIAL AID AWARD 2013-2014 We are pleased to offer financial assistance for your cost of attendance at the University of North Carolina at Chapel Hill. Your award information

INFORMATION ABOUT YOUR FINANCIAL AID AWARD 2013-2014 We are pleased to offer financial assistance for your cost of attendance at the University of North Carolina at Chapel Hill. Your award information

Graduate Student Handbook

Graduate Student Handbook Department of Chemistry and Biochemistry Auburn University Revised Apr. 2008 I. INTRODUCTION General regulations for graduate students at Auburn University are covered in the

Graduate Student Handbook Department of Chemistry and Biochemistry Auburn University Revised Apr. 2008 I. INTRODUCTION General regulations for graduate students at Auburn University are covered in the

Martin A. Darocha, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014

, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014 Following is a brief summary of payroll tax information for 2015. If you

, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014 Following is a brief summary of payroll tax information for 2015. If you