Public Accounts for the fiscal year ended 31 March Volume 1. Printed by Authority of the Legislature Fredericton, N.B. Financial Statements

|

|

|

- Drusilla Long

- 8 years ago

- Views:

Transcription

1 Public Accounts for the fiscal year ended Volume 1 Printed by Authority of the Legislature Fredericton, N.B. Financial Statements

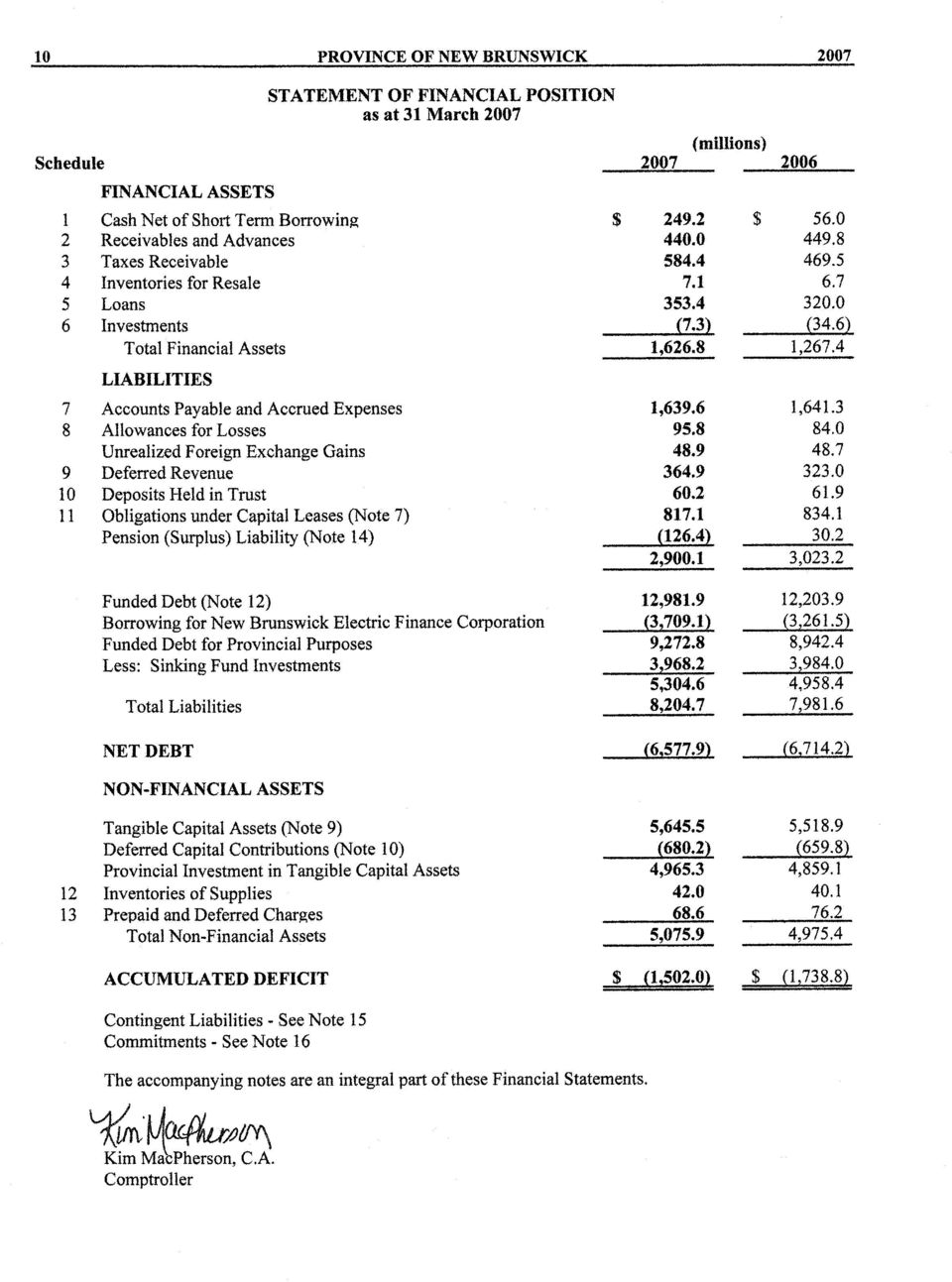

2

3 Public Accounts for the fiscal year ended Volume 1 Financial Statements ISSN

4

5 2007 PROVINCE OF NEW BRUNSWICK iii TABLE OF CONTENTS Audited Financial Statements Introduction to Volume I 1 Statement of Responsibility 2 Results for the Year 3 Major Variance Analysis 5 Auditor's Report 9 Statement of Financial Position 10 Statement of Operations 11 Statement of Cash Flow 12 Statement of Change in Net Debt 13 Notes to the Financial Statements 14 Schedules to the Financial Statements 41

6

7 2007 PROVINCE OF NEW BRUNSWICK 1 INTRODUCTION VOLUME I The Public Accounts of the Province of New Brunswick are presented in five volumes. This volume contains the audited financial statements of the Provincial Reporting Entity as described in note 1 to the financial statements. They include a Statement of Financial Position, a Statement of Operations, a Statement of Cash Flow and a Statement of Change in Net Debt. This volume also contains the Auditor s Report, Statement of Responsibility, management s comments on the results of the year and a variance analysis. Volume II contains unaudited supplementary information to the Financial Statements presented in Volume I. It presents summary statements for revenue and expenditure as well as five-year comparative statements. This volume also contains detailed information on Supplementary Appropriations, Funded Debt, statements of the General Sinking Fund, Securities Held, and revenue and expenditure by government department (this includes salary, travel, supplier, grant and contribution, and loan disbursement listings). Volume III contains the financial statements of those corporations, boards and commissions which are accountable for the administration of their financial affairs and resources to the Government or the Legislature of the Province. The Government or Legislature also has the power to control these organizations either through ownership or through legislative provisions. Volume IV contains the financial statements of various trust funds which the Province administers as Trustee. Volume V contains salary listings of certain government organizations, including Regional Health Authorities, New Brunswick Power Corporation, and New Brunswick Liquor Corporation. The salary listings are for employees who received earnings during the year ended 31 December 2006 in excess of $40,000.

8

9 2007 PROVINCE OF NEW BRUNSWICK 3 General Comments RESULTS FOR THE YEAR The Province had a surplus for the fiscal year ended of $236.8 million. This represents a significant increase over the budgeted surplus of $22.2 million. There are two primary reasons for the larger surplus. The first is adjustments to prior years Personal and Corporate income taxes which contributed to a $109.6 million increase on those taxes. The second is due to an increase in metallic minerals tax revenue of $112.2 million over the budgeted amount. This resulted primarily from significantly higher than anticipated world zinc prices. There were several other variances which are discussed in more detail in the major variance section below. Summary Financial Information Statement of Financial Position Financial Assets $ 1,626.8 $ 1,267.4 Liabilities (8,204.7) (7,981.6) Net Debt (6,577.9) (6,714.2) Tangible Capital Assets 5, ,518.9 Deferred Capital Contributions (680.2) (659.8) Other Non Financial Assets Total Non Financial Assets 5, ,975.4 Accumulated Deficit $ (1,502.0) $ (1,738.8) Statement of Operations Revenue Provincial Own Sources $ 4,184.7 $ 3,952.6 Revenue Federal Sources 2, ,370.5 Total Revenue 6, ,323.1 Expenses 6, ,088.1 Surplus / (Deficit) $ $ Statement of Change in Net Debt Opening Net Debt $ (6,714.2) $ (6,828.2) Decrease in Net Debt Ending Net Debt $ (6,577.9) $ (6,714.2)

10 4 PROVINCE OF NEW BRUNSWICK 2007 Fiscal Management Measures The Government uses multiple measures to guide its fiscal management, a number of which are described below. Surplus The surplus for the year ended was $ million which is slightly more than the $235.0 million surplus generated in the previous year and significantly greater than the budgeted surplus of $22.2 million. Net Debt In Volume I of the 31 March 2006 Public Accounts, the following table disclosed the net debt at the end of each year since Year Net Debt $7,048.9 $6,898.9 $6,734.5 $6,832.4 $6,923.6 $6,778.3 $6,655.7 In 2007, the government had an actuarial valuation completed of the retirement allowance liability and included the employees of the Regional Health Authorities for the first time since their results were consolidated in This required a restatement of Net Debt as follows: Year Net Debt $7,056.3 $6,914.8 $6,758.8 $6,865.3 $6,965.0 $6,828.2 $6,714.2 Net debt was reduced by a further $136.3 million during the year ended to reach a balance of $6,577.9 million. The following table reports the net debt position at the end of each of the past seven years. Year Net Debt $7,056.3 $6,914.8 $6,758.8 $6,865.3 $6,965.0 $6,828.2 $6,714.2 $6,577.9 The reduction in net debt over the seven year period therefore has been $478.4 million. Net Debt as a Percentage of Gross Domestic Product At 31 December 1999, the Province s Gross Domestic Product was $19,041.0 million. Therefore, the restated net debt as at 31 March 2000 was 37.1% of GDP at the time. The Province s GDP at 31 December 2006 was $25,221.0 million, so the net debt to GDP ratio stands at 26.1% for the year ended 31 March 2007.

11 2007 PROVINCE OF NEW BRUNSWICK 5 Year GDP $19,041.0 $20,085.0 $20,684.0 $21,169.0 $22,346.0 $23,487.0 $24,162.0 $25,221.0 Net Debt $ 7,056.3 $ 6,914.8 $ 6,758.8 $ 6,865.3 $ 6,965.0 $ 6,828.2 $ 6,714.2 $ 6,577.9 Ratio 37.1% 34.4% 32.7% 32.4% 31.2% 29.1% 27.8% 26.1% This table reports that there has been a steady seven year improvement in the net debt to GDP ratio (a reduction of 11.0 percentage points from the starting point of 37.1%). For purposes of the Fiscal Responsibility and Balanced Budget Act, an improvement in the net debt to GDP ratio over successive fiscal periods is targeted. This means that the net debt to GDP ratio for the year ended must be lower than the year ended 31 March The ratio of net debt to GDP has improved by 5.1 percentage points from 2004 to Debt Charges The Province s debt charges for the year ended, calculated as the amount spent on servicing the public debt less sinking fund earnings, totaled $327.6 million, $79.4 million less than what the Province spent in Favourable interest rates and a strong Canadian dollar in are largely responsible for this difference. Results According to the Fiscal Responsibility and Balanced Budget Act The Province adopted the Fiscal Responsibility and Balanced Budget Act (FRBBA) and repealed the Balanced Budget Act in This Act requires that total expenses not exceed total revenues for the fiscal period commencing 1 April 2004 and ending. During the year, the Government generated a $115.4 million surplus for Balanced Budget purposes. This combined with the surplus to date according to the FRBBA resulted in a cumulative surplus of $597.8 million as is shown in the following table. Surplus According to Fiscal Responsibility and Balanced Budget Act Cumulative Surplus - FRBBA $ $ $115.4 $ MAJOR VARIANCE ANALYSIS Explanations of major variances are presented below, first for revenue, followed by expenses. In this analysis, comparisons are made between the actual results for and either the budget or actual results for REVENUE Provincial Sources Taxes Taxes are up $241.1 million from the Budget. Metallic minerals tax is up $112.2 million primarily due to significant increases in world zinc prices, and prior-year adjustments. Personal income tax

12 6 PROVINCE OF NEW BRUNSWICK 2007 is up $70.4 million and corporate income tax is up $39.2 million both due to positive prior-year adjustments related to the 2005 taxation year. Harmonized sales tax is up $57.8 million due to increased federal payments and the elimination of the home energy HST rebate. The increases have been partially offset by decreases in some other taxes. Gasoline and motive fuels tax is $21.1 million lower than budget largely due to a 3.8-cent per litre tax reduction in October 2006 and tobacco tax is $11.1 million lower due to lowerthan-anticipated volumes. Taxes are up $302.6 million from the previous year. Personal income tax is up $111.5 million due to prioryear adjustments and strong growth in the tax base. Corporate income tax is up $67.3 million due to prioryear adjustments. Metallic minerals tax is up $109.7 million due to significant increases in world zinc prices, and prior-year adjustments. The harmonized sales tax has increased by $33.4 million as a result of economic growth. Provincial real property tax is $10.5 million higher than the previous year as a result of the growth in the assessment base. Similar to above, the increases have been partially offset by decreases in some other taxes. Gasoline and motive fuels tax is $16.9 million lower than the previous year largely due to a 3.8-cent per litre tax reduction in October 2006 and tobacco tax is $8.6 million lower due to lower volumes. Investment Income Investment income is up $76.3 million from budget mainly due to a $64.7 million improvement in net income for the New Brunswick Electric Finance Corporation (NBEFC). NBEFC net income was higher than budget as a result of NB Power experiencing an above-average year in with warm winter weather, high water levels and increased exports. The above-average results for NB Power more than offset the impact of an 8% cap on electricity rate increases. Investment income is down $101.1 million from the previous year primarily due to a $112.9 million decrease in net income for NBEFC. NBEFC net income was lower than the previous year as a result of the impact of a cap on electricity rate increases in and an extraordinary fiscal performance for NB Power in Other Provincial Revenue Other provincial revenue is up $62.6 million from budget reflecting increases in various sales of goods and services and other miscellaneous revenue as well as new public sector accounting guidelines to report the amortization of deferred capital contributions of $23.2 million. Other provincial revenue is up $21.7 million from the previous fiscal year. This reflects increases in various sales of goods and services and other miscellaneous revenue. Federal Sources Fiscal Equalization Payments Fiscal Equalization Payments are up $18.6 million from budget reflecting the fixed payment announced in the federal budget. Fiscal Equalization Payments are up $102.8 million year-over-year due to an increase in the fixed payment to the province.

13 2007 PROVINCE OF NEW BRUNSWICK 7 Unconditional Grants Unconditional Grants are up $10.6 million from the previous year mainly due to increased federal funding for the Canada Health Transfer and the Canada Social Transfer. Conditional Grants Conditional Grants are down $19.7 million from the previous fiscal year mainly due to lower federal funding related to health and education. EXPENSES Education and Training Education and Training expenses were $72.4 million higher than budget mainly due to an additional $68.0 million grant to universities. Education and Training expenses were $4.2 million lower than in mainly due to a decrease in the Assistance to Universities Program partially offset by additional expenses in School District Operations. Health Health expenses were $44.8 million higher than budget mainly due to increased expenses in Hospital Services related to the operations of the Regional Health Authorities, partially offset by lower Out-of- Province Hospital Payments expenses. Health expenses were $152.4 million higher than in mainly due to increased expenses in Hospital Services, Medicare, the Prescription Drug Program and Ambulance Services. Family and Community Services Family and Community Services expenses were $11.7 million higher than budget mainly due to additional expenses in Long Term Care and Nursing Homes. Family and Community Services expenses were $48.6 million higher than in mainly due to increased expenses in Long Term Care, Nursing Homes and Children Services. Protection Services Protection Services expenses were $61.6 million higher than budget mainly due to funding for Credit Union Stabilization and Support. Protection Services expenses were $72.4 million higher than in mainly due to funding for Credit Union Stabilization and Support and increases in Public Safety s provision for loss expense and Safety Services Program. Economic Development Economic Development expenses were $28.6 million higher than budget mainly due to an increase in Business New Brunswick's Strategic Assistance Program and provision for loss expense.

14 8 PROVINCE OF NEW BRUNSWICK 2007 Economic Development expenses were $24.4 million higher than in mainly due to an increase in the Regional Development Corporation's federal-provincial programs and Business New Brunswick's Strategic Assistance Program, partially offset by a decrease in Business New Brunswick s provision for loss expense. Labour and Employment Labour and Employment expenses were $1.1 million higher than budget mainly due to an increase in demand for employment support for the forest industry. Labour and Employment expenses were $3.0 million higher than in mainly due to an increase in demand for employment support for the forest industry. Resources Resource Sector expenses were $21.6 million higher than budget due to a $26.6 million contribution to Saint John Harbour Clean-up, partially offset by a decrease in the Energy Efficiency and Conservation Agency of New Brunswick due to the timing of program spending. Resource Sector expenses were $32.9 million higher than mainly due to a $26.6 million contribution to Saint John Harbour Clean-up and increased spending in the Environmental Trust Fund. Transportation Transportation expenses were $21.5 million higher than budget mainly due to increased amortization expense resulting from an accounting policy change. Transportation expenses were $11.2 million higher than in mainly due to increased funding to the New Brunswick Highway Corporation for the maintenance of new sections of highway, increased amortization expense, and increased expenses in the Permanent Bridges Program. Central Government Central Government expenses were $44.0 million lower than budget mainly due to lower than anticipated expense in General Government's Supplementary Funding Provision and pension expense. Central Government expenses were $15.3 million higher than in mainly due to costs associated with the 2006 Provincial Election and increased Provision for Loss expense partially offset by a decrease in pension expense. Service of the Public Debt Service of the Public Debt expenses were $15.7 million lower than budget due to a larger than anticipated one-time foreign exchange gain and lower short-term and long-term interest expense. Service of the Public Debt expenses were $32.0 million lower than in as a result of a large onetime foreign exchange gain, maturing debt and savings from refinancing at lower interest rates.

15

16

17 2007 PROVINCE OF NEW BRUNSWICK 11 STATEMENT OF OPERATIONS for the fiscal year ended Schedule Budget Actual Actual REVENUE Provincial Sources 14 Taxes $ 2,879.1 $ 3,120.2 $ 2, Licenses and Permits Royalties Investment Income Other Provincial Revenue Sinking Fund Earnings , , ,952.6 Federal Sources Fiscal Equalization Payments 1, , , Unconditional Grants Conditional Grants - Canada , , , , , ,323.1 EXPENSE 21 Education and Training 1, , , Health 2, , , Family and Community Services Protection Services Economic Development Labour and Employment Resources Transportation Central Government Service of the Public Debt (Note 13) , , ,088.1 ANNUAL SURPLUS ACCUMULATED DEFICIT - BEGINNING OF YEAR (1,738.8) (1,738.8) (1,973.8) ACCUMULATED DEFICIT - END OF YEAR $ (1,716.6) $ (1,502.0) $ (1,738.8) The accompanying notes are an integral part of these Financial Statements.

18 12 PROVINCE OF NEW BRUNSWICK 2007 STATEMENT OF CASH FLOW for the fiscal year ended OPERATING ACTIVITIES Surplus / (Deficit) $ $ Non Cash Items Amortization of Premiums, Discounts and Issue Expenses Foreign Exchange Expense (30.8) (7.8) Increase in Allowance for Doubtful Accounts Amortization of Tangible Capital Assets Loss on Disposal of Tangible Capital Assets Amortization of Deferred Contributions (23.1) (22.4) Sinking Fund Earnings (231.8) (226.4) Losses on Foreign Exchange Settlements Decrease in Pension Liability (Note 14) (156.6) (126.5) Increase in Deferred Revenue Increase in Working Capital (129.3) (80.0) Net Cash From Operating Activities INVESTING ACTIVITIES Increase in Investments, Loans and Advances (95.0) (401.5) Net Cash Used in Investing Activities (95.0) (401.5) CAPITAL TRANSACTIONS Acquisition of Capital Assets (365.0) (342.2) Revenue Received to Acquire Tangible Capital Assets Net Cash Used in Capital Transactions (321.5) (317.3) FINANCING ACTIVITIES Proceeds from Issuance of Funded Debt 1, ,387.9 Purchase of NB Power Debentures (560.0) (400.0) Received from Sinking Fund for Redemption of Debentures and Payment of Exchange Decrease in Obligations under Capital Leases (17.0) (15.2) Sinking Fund Instalments (129.1) (127.9) Funded Debt Matured (755.5) (453.2) Net Cash From Financing Activities INCREASE (DECREASE) IN CASH DURING YEAR (92.3) CASH POSITION - BEGINNING OF YEAR CASH POSITION - END OF YEAR $ $ 56.0 CASH REPRESENTED BY Cash Net of Short Term Borrowing $ $ 56.0 The accompanying notes are an integral part of these Financial Statements.

Losses on Foreign Exchange Settlements 16.6 19.1 Decrease in Pension Liability (Note 14) (156.6) (126.5) Increase in Deferred Revenue 41.9 5.4 Increase in Working Capital (129.3) (80.")

19 2007 PROVINCE OF NEW BRUNSWICK 13 STATEMENT OF CHANGE IN NET DEBT for the fiscal year ended Budget Actual Actual NET DEBT - BEGINNING OF YEAR As Previously Published $ (6,655.7) $ (6,655.7) $ (6,778.3) Prior Years' Adjustments Recognition of Retirement Allowance for Hospital Employees --- (58.5) (49.9) RESTATED NET DEBT - BEGINNING OF YEAR (6,655.7) (6,714.2) (6,828.2) CHANGES IN YEAR Annual Surplus Acquisition of Tangible Capital Assets (345.9) (365.0) (342.2) Amortization of Tangible Capital Assets Amortization of Deferred Contributions --- (23.1) (22.4) Loss on Disposal of Tangible Capital Assets Revenue Received to Acquire Tangible Capital Assets Net Change in Supplies Inventories --- (1.9) (2.0) Net Change in Prepaid Expenses (6.6) (INCREASE) DECREASE IN NET DEBT (87.0) NET DEBT - END OF YEAR $ (6,742.7) $ (6,577.9) $ (6,714.2) The accompanying notes are an integral part of these Financial Statements.

(22.4) Loss on Disposal of Tangible Capital Assets --- 0.3 0.4 Revenue Received to Acquire Tangible Capital Assets 27.6 43.5 24.")

20 14 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES a) Provincial Reporting Entity These financial statements include those entities which make up the Provincial Reporting Entity. The Provincial Reporting Entity is comprised of certain organizations that are controlled by the government. These organizations are the Consolidated Fund, the General Sinking Fund and the agencies, commissions and corporations listed below. b) Basis of Consolidation Transactions and balances of organizations are included in these financial statements through one of the following accounting methods: Consolidation method This method combines the accounts of distinct organizations. It requires uniform accounting policies for the organizations except that tangible capital asset policies of these organizations are not conformed to provincial policies. Inter-organizational balances and transactions are eliminated under this method. This method reports the organizations as if they were one organization. The organizations included through the consolidation method are: Algonquin Golf Limited; Algonquin Properties Limited; Arts Development Trust Fund; Environmental Trust Fund; Forest Protection Limited; New Brunswick Credit Union Deposit Insurance Corporation; New Brunswick Distance Education Network Inc.; New Brunswick Energy Efficiency and Conservation Agency New Brunswick Highway Corporation; New Brunswick Housing Corporation; New Brunswick Investment Management Corporation; New Brunswick Tire Stewardship Board; Regional Development Corporation; Regional Health Authorities; Service New Brunswick; Sport Development Trust Fund. Modified equity method This method is used for government enterprises. Government enterprises are defined in Note 8 to these financial statements. The modified equity method reports a government enterprise s net assets as an investment on the Province s Statement of Financial Position. The net income of the government enterprise is reported as investment income on the Province s Statement of Operations. Interorganizational transactions and balances are not eliminated. All gains or losses arising from interorganizational transactions between government enterprises and other government organizations are eliminated. The accounting policies of government enterprises are not adjusted to conform with those of other government organizations. The organizations have been included through modified equity accounting are: Lotteries Commission of New Brunswick; New Brunswick Municipal Finance Corporation; New Brunswick Electric Finance Corporation; New Brunswick Power Group; New Brunswick Liquor Corporation; New Brunswick Securities Commission. Transaction method This method records only transactions between the Province and the other organizations. The transaction method was used because the appropriate methods would not produce a materially different result. The determination of which entities to exclude because of materiality was made by Board of Management. The organizations included through the transaction method are:

Basis of Consolidation Transactions and balances of organizations are included in these financial statements through one of the following accounting methods: Consolidation method This method")

21 2007 PROVINCE OF NEW BRUNSWICK 15 NOTES TO THE FINANCIAL STATEMENTS Advisory Council on the Status of Women; Atlantic Education International Inc.; Fundy Linen Services Inc.; Kings Landing Corporation; New Brunswick Advisory Council on Youth; New Brunswick Arts Board; New Brunswick Crop Insurance Commission; New Brunswick Energy and Utilities Board New Brunswick Insurance Board; New Brunswick Legal Aid Services Commission; New Brunswick Museum; New Brunswick Public Libraries Foundation; New Brunswick Research and Productivity Council; Premier's Council on the Status of Disabled Persons; Provincial Holdings Ltd.; Strait Crossing Finance Inc. c) Specific Accounting Policies Accrual Accounting Expenses are recorded for all goods and services received or consumed during the fiscal year. Revenues and recoveries are recorded on an accrual basis with the exception of revenue from Canada under the Federal-Provincial Fiscal Arrangements and Federal Post-Secondary Education and Health Contributions Act, 1977, and the Canada-New Brunswick Tax Collection Agreement which is accrued based on information provided by Canada and is adjusted in subsequent years. Interest revenue is recorded on outstanding loan amounts due to the Province as the interest is earned. The major categories of loans receivable are Student Assistance, Economic Development, Agriculture Development and Fisheries. Amounts received or recorded as receivable but not earned by the end of the fiscal year are recorded as deferred revenue. Debt Charges Interest and other debt service charges are reported in the Statement of Operations as Service of the Public Debt except as described below: Because government enterprises are included in the Provincial Reporting Entity through modified equity accounting, the cost of servicing their debt is not included in the Service of the Public Debt expense. The cost of servicing the debt of government enterprises is an expense included in the calculation of their net profit or loss for the year. Interest costs imputed on the Province s Accrued Pension Liability are recorded as part of pension expense, which is included in various expense functions. Interest earned on the assets of the General Sinking Fund and on other provincial assets is reported as revenue. Note 13 to these financial statements reports the components of the Service of the Public Debt Expense function and total debt charges. Government Transfers Government transfers are transfers of money, such as grants, from a government to an individual, an organization or another government for which the government making the transfer does not receive any goods or services directly in return. Government transfers are recognized in the Province's financial statements as expenses or revenues in the period that the events underlying the transfer occurred. Liabilities have been established for any transfers due at 31

22 16 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS March 2007 for which the intended recipients have met the eligibility criteria. Receivables have been established for transfers to which the Province is entitled under governing legislation, regulation or agreement. Asset Classification Assets are classified as either financial or non financial. Financial assets are assets that could be used to discharge existing liabilities or finance future operations and are not to be consumed in the normal course of operations. Non-financial assets are acquired, constructed or developed assets that do not provide resources to discharge existing liabilities but are employed to deliver government services, may be consumed in normal operations and are not for resale. Non-financial assets include tangible capital assets, prepaid expenses and inventories of supplies. Short Term Investments Short term investments are recorded at cost with supplemental information related to market values of short term investments reported in note 6 to these financial statements. Concessionary Loans There are two situations where the Province charges loan disbursements entirely as expenses. These are: Loan agreements which commit the Province to provide future grants to the debtor to be used to repay the loan. Loan agreements which include forgiveness provisions if the forgiveness is considered likely. In both these situations, the loan is charged to expense when it is disbursed. Loans that are significantly concessionary because they earn a low rate of return are originally recorded as assets at the net present value of the expected future cash flows. The net present value is calculated using the Province s borrowing rate at the time the loan was issued. The difference between the nominal value of the loan and its net present value is recorded as an expense. Inventories Inventories are recorded at the lower of cost or net realizable value. Inventories include supplies for use, and goods and properties held for resale. Properties held for resale are reported as a financial asset and include land and fixtures acquired or constructed for the purpose of sale. Properties held for resale also include properties acquired through foreclosure. Inventories of supplies for use are reported as a non financial asset. Allowances Allowances have been established for accounts receivable, loan guarantees and other possible losses. These allowances are disclosed in the schedules to the financial statements. An allowance is established on outstanding loan guarantee amounts when it is considered likely the debtor will default on their loan and the Province will be required to pay out under the guarantee. As with all provisions for loss, this is an estimate and adjustments are made annually to the reflect management s best estimate of likely losses. Amounts due to the province but deemed uncollectible are written off from the accounts of the Province once the write-off has been approved by either the Board of Management or Secretary to the Board of Management depending on the dollar value involved.

23 2007 PROVINCE OF NEW BRUNSWICK 17 NOTES TO THE FINANCIAL STATEMENTS Tangible Capital Assets Tangible capital assets are assets owned by the Province which have useful lives greater than one year. Certain dollar thresholds have been established for practical purposes. Computer hardware and software have not been capitalized in the Province s financial statements. Tangible capital assets are reported at gross cost. Contributions received to assist in the acquisition of tangible capital assets are reported as Deferred Capital Contributions and amortized to income at the same rate as the related asset. Tangible capital assets policies of government entities which are consolidated in these financial statements are not adjusted to conform to Provincial policies. The types of items which could differ include amortization rates, estimates of useful lives and dollar thresholds for capitalization. Trusts under Provincial Administration Legally established trust funds which the Province administers but does not control are not included as Provincial assets or liabilities. Note 18 to these financial statements discloses the equity balances of the trust funds administered by the Province Borrowing on Behalf of New Brunswick Electric Finance Corporation The Province, as represented by the Consolidated Fund, has issued long term debt securities on behalf of New Brunswick Electric Finance Corporation in exchange for debentures with like terms and conditions. The New Brunswick Electric Finance Corporation debentures received by the Province are reported in Note 12 of these financial statements as a reduction of Funded Debt. This financing arrangement was used to obtain more favourable debt servicing costs. The transactions involving these securities, including the debt servicing costs, are not part of the budget plan of the Province s Consolidated Fund. Foreign Currency Translation and Risk Management The Province's assets, liabilities and contingent liabilities denominated in foreign currencies are translated to Canadian dollars at the year end rates of exchange, except where such items have been hedged or are subject to interest rate and currency swap agreements. In such cases, the rates established by the hedge or the agreements are used in the translation. Exchange gains and losses are included in the Statement of Operations except for the unrealized exchange gains and losses arising on the translation of long term items, which are deferred and amortized on a straight line basis over the remaining life of the related assets or liabilities. Revenue and expense items are translated at the rates of exchange in effect at the respective transaction dates. The Province borrows funds in both domestic and foreign capital markets and manages its existing debt portfolio to achieve the lowest debt costs within specified risk parameters. As a result, the Province may be exposed to foreign exchange risk. Foreign exchange or currency risk is the risk that the principal and interest payments on foreign debt will fluctuate in Canadian dollar terms due to fluctuations in foreign exchange rates. In accordance with risk management policy guidelines, the Province uses various financial instruments and techniques to manage exposure to foreign currency risk. These financial instruments include currency forwards, cross-currency swaps and purchases of foreign denominated assets into the Province s sinking fund. As at March 31, 2007, the Province had outstanding $1,064.5 million US$ denominated debt. Of this total, $714.5 million was hedged by entering into cross-currency swaps, which convert the interest and principal payable from US to Canadian dollars.

24 18 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS The Province s currency exposure was 4.4% of the total debt portfolio prior to netting out the US dollar denominated assets in the sinking fund. A one-cent change in the US/CDN$ foreign exchange rate as of March 31, 2007 would result in a $4.6 million change in the principal amount of Provincial-purpose long term-debt. The hypothetical change, a gain or loss, would be amortized over the remaining life of the related debt issue. A onecent change would also result in a change of $0.5 million on interest payments in Service of the Public Debt. The net currency exposure is 2.8% when the US dollar denominated assets held in the sinking fund are netted from the total Provincial-purpose debt portfolio. Sinking Funds The General Sinking Fund is maintained by the Minister of Finance under the authority of section 12 of the Provincial Loans Act ( Act ). This Act provides that the Minister shall maintain one or more sinking funds for the payment of funded debt either at maturity or upon redemption in advance of maturity. Typically, redemptions are only made after the related Provincial purpose portion of the debt has been outstanding a minimum of twenty years. Sinking fund investments in bonds and debentures are reported at par value less unamortized discounts less premiums and the unamortized balance of unrealized foreign exchange gains or losses. Short-term deposits are reported at cost. The Province s sinking fund may be invested in eligible securities as defined in the Act. Sinking fund installments are paid into the General Sinking Fund on or before the anniversary date of each issue of funded debt, at the prescribed rate of a minimum of 1% of the outstanding principal. New Brunswick Electric Finance Corporation (NBEFC) is contractually obligated to pay to the Province the amount of the sinking fund installment required each year in respect of the debentures issued by the Province on behalf of New Brunswick Power Corporation prior to October 1, 2004 and to NBEFC after September 30, The following table shows the allocation of various components of the Sinking Fund between the Consolidated Fund of the Province and NBEFC. Consolidated Fund NBEFC Total Fund Equity, beginning of year $ 3,984.0 $ $ 4,320.4 Sinking Fund Earnings Installments Paid for Debt Retirement (376.7) (83.2) (459.9) Fund Equity, end of year $ 3,968.2 $ $ 4,268.7 Leases Long term leases, under which the Province, as lessee, assumes substantially all the benefits and risks of ownership of leased property, are classified as capital leases although certain minimum dollar thresholds are in place for practical reasons. The present value of a capital lease is accounted for as a tangible capital asset and an obligation at the inception of the lease.

25 2007 PROVINCE OF NEW BRUNSWICK 19 NOTES TO THE FINANCIAL STATEMENTS All leases under which the Province does not assume substantially all the benefits and risks of ownership related to the leased property are classified as operating leases. Each rental payment required by an operating lease is recorded as an expense when it is due. Measurement Uncertainty Measurement uncertainty is uncertainty in the determination of the amount at which an item is recognized in financial statements. This uncertainty exists when there is a variance between the recognized amount and another reasonably possible amount. Many items in these financial statements have been measured using estimates. Those estimates have been based on assumptions that reflect economic conditions. Some examples of where measurement uncertainty exists are the establishment of allowances for doubtful accounts, the determination of pension expense and the calculation of transition balances for Tangible Capital Assets. NOTE 2 BUDGET The budget amounts included in these financial statements are the amounts published in the Main Estimates, adjusted for transfers from the Supplementary Funding Provision Program and elimination of inter-account transactions. The Supplementary Funding Provision Program is an appropriation which provides funding to other programs for costs associated with contract settlements and other requirements not budgeted in a specific program. Budget figures for the year ending reflect the acquisition of tangible capital assets and amortization expense. These amounts are disclosed in the Main Estimates as a separate schedule. NOTE 3 PRIOR PERIOD ADJUSTMENT An actuarial valuation was performed during the year to value the liability related to retirement allowances of employees in Regional Health Authorities (RHA s). The financial results of the RHA s are included in these financial statements using the consolidation method. As this was the first year this information was available, it has been accounted for retroactively as a first-time adoption of a Public Sector Accounting Board (PSAB) recommendation relating to these entities. This transaction resulted in a reduction of the reported surplus in 2006 of $8.6 million, an increase in opening Net Debt at 1 April 2005 of $49.9 million and an increase in liabilities in 2006 of $58.5 million. This also increased the opening Net Debt at 1 April 2006 by $58.5 million. The Province commenced in 2007 to report the gross cost of tangible capital assets in the financial statements rather than reporting these amounts net of deferred capital contributions. Deferred capital contributions are reported separately. The impact in the Statement of Financial Position is to increase both the cost of tangible capital assets and deferred contributions reported by $680.1 million ($659.7 million 2006). The impact on the Statement of Operations is to increase both amortization expense and other provincial revenue by $23.1 million ($22.4 million 2006). There is no impact on net debt. NOTE 4 FISCAL RESPONSIBILITY AND BALANCED BUDGET ACT The Fiscal Responsibility and Balanced Budget Act requires that total expenses not exceed total revenues for the period commencing 1 April 2004 and ending. That Act stipulates that any change made within the last fifteen months of the period from 1 April 2004 to 31 March 2007, or after completion of that period, in relation to the official estimates by the Government of Canada

26 20 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS for provincial entitlements under the Federal-Provincial Fiscal Arrangements Act (Canada), the Canada-New Brunswick Tax Collection Agreement or the Comprehensive Integrated Tax Coordination Agreement, shall not be taken into account. The surplus according to the Fiscal Responsibility and Balanced Budget Act for each of the years in the 3 year period ending is as follows: Actual Actual Actual Revenue $ 5,959.8 $ 6,300.7 $ 6,648.9 Adjustments as per section 4(1) of the Act --- (3.4) (121.4) Revenue as per Fiscal Responsibility and Balanced Budget Act 5, , ,527.5 Expense 5, , ,412.1 Surplus for the year Cumulative Surplus at beginning of year Cumulative Surplus at end of year $ $ $ The Province is required under the Act to report annually on the ratio of Net Debt to Gross Domestic Product (GDP). The following table presents the ratio for the years ended 31 March 2004 to Net Debt $ (6,965.5) $ (6,828.2) $ (6,714.2) $ (6,577.9) GDP (31 December) $ 22,346.0 $ 23,487.0 $ 24,162.0 $ 25,221.0 Ratio of Net Debt to GDP 31.2% 29.1% 27.8% 26.1%

27 2007 PROVINCE OF NEW BRUNSWICK 21 NOTES TO THE FINANCIAL STATEMENTS NOTE 5 SPECIAL PURPOSE ACCOUNTS Special Purpose Account revenue earned but not spent accumulates as a surplus in that account and may be spent in future years for the purposes specified. At, the accumulated surplus in all Special Purpose Accounts totaled $95.0 million ($85.7 million 2006). This total is a component of net debt and accumulated deficit. The following table summarizes the change in the accumulated Special Purpose Account surplus Accumulated Surplus Revenue Expense Accumulated Surplus Active Community School Sport Project $ --- $ 0.2 $ 0.2 $ --- Art Smart Project Arts Development Trust Fund Child Centered Family Justice Fund CMHC Funding Environmental Trust Fund Fish Stocking Fund Fred Magee Account Grand Lake Meadows Historic Places Hospital Liability Protection Account International Projects Johann Wordel Account Land Management Account Library Account Medical Research Assistance Account Municipal Police Assistance National Safety Code Agreement Natural Resources Recoverable Projects NB 911 Service Fund NB Community College Scholarship Account Parlee Beach Maintenance Public/Private Partnership Projects Renovation of Old Government House School District Scholarship and Trusts School District Self Sustaining Accounts Sport Development Trust Fund Strait Crossing Finance Inc Suspended Driver Alcohol Re-Education Trail Management Trust Fund Training Recoverable Projects Victim Services Account Wildlife Trust Fund $ 85.7 $ 62.5 $ 53.2 $ 95.0 Descriptions of Major Special Purpose Accounts CMHC Funding CMHC funding is used to provide funding for the operation of the programs that fall under the administration of the Social Housing Agreement. Assets consist of current assets held within the Consolidated Fund.

28 22 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS School District Self Sustaining Accounts Self Sustaining Accounts record school district revenue and expenses for non-educational services such as the rental of school facilities, cafeteria operations and foreign student tuition fees. These special purpose accounts also record partnership activities with third parties to provide resources, services or grants to students. NOTE 6 SHORT TERM INVESTMENTS The fair value of short-term investments at March 31, 2007 is not materially different from the carrying value. Short-term investments primarily consist of investments in banker s acceptances and depository notes. NOTE 7 OBLIGATIONS UNDER CAPITAL LEASES The total future principal and interest payments for capital leases amount to $1,616.7 million ($1,693.2 million 2006). That amount includes $817.1 million ($834.1 million 2006) in principal and $799.6 million ($859.1 million 2006) in interest. Minimum annual principal and interest payments in each of the next five years are as follows: Fiscal Year $ NOTE 8 GOVERNMENT ENTERPRISES A Government Enterprise is an organization accountable to the Legislative Assembly that has the power to contract in its own name, has the financial and operating authority to carry on a business, sells goods and services to customers outside the Provincial Reporting Entity as its principal activity, and that can, in the normal course of its operations, maintain its operations and meet its liabilities from revenues received from sources outside the Provincial Reporting Entity. The following is a list of Government Enterprises, and their fiscal year ends, which are included in the Provincial Reporting Entity as described in note 1 b) to these financial statements. In addition we have included summary information for the NB Power Group in the narrative section following the table below. The financial results of the NB Power Group are included in New Brunswick Electric Finance Corporation s financial statements using the modified equity method. Lotteries Commission of New Brunswick (Lotteries) New Brunswick Liquor Corporation (Liquor) New Brunswick Municipal Finance Corporation (Municipal Finance) New Brunswick Electric Finance Corporation (NB Electric Finance) New Brunswick Power Group (NB Power Group) New Brunswick Securities Commission (Securities) The following table presents condensed financial information of these Government Enterprises.

29 2007 PROVINCE OF NEW BRUNSWICK 23 NOTES TO THE FINANCIAL STATEMENTS Municipal Finance NB Electric Finance Securities Total Lotteries Liquor Assets Cash and Equivalents $ --- $ 3.0 $ 1.0 $ 94.6 $ 1.3 $ 99.9 Receivables Prepaids Inventories Investments Deferred Charges Fixed Assets Long Term Notes Receivable , ,214.8 Other Assets Total Assets $ 2.1 $ 37.3 $ $ 3,631.1 $ 2.8 $ 4,239.2 Liabilities Short Term Indebtedness $ --- $ --- $ --- $ 24.0 $ --- $ 24.0 Payables Long Term Debt , ,484.2 Sinking Funds (352.2) --- (352.2) Total Liabilities $ --- $ 18.2 $ $ 3,669.0 $ 0.6 $ 4,252.7 Equity Retained Earnings $ 2.1 $ 19.1 $ 1.0 $ (37.9) $ 2.2 $ (13.5) Total Liabilities and Equity $ 2.1 $ 37.3 $ $ 3,631.1 $ 2.8 $ 4,239.2 Net Income Revenue $ $ $ 25.3 $ $ 10.2 $ Expenses (7.8) (229.9) (0.2) (29.4) (3.8) (271.1) Interest and Related Expense (25.1) (243.9) --- (269.0) Net Income $ $ $ --- $ 19.4 $ 6.4 $ The financial information of Government Enterprises is prepared according to generally accepted accounting principles, using accounting policies that are appropriate for the industry segment in which they operate. These accounting policies may not be consistent with accounting policies used by other member organizations of the Provincial Reporting Entity. Because minor adjustments are required for timing differences, the net income amounts reported in the financial statements of government enterprises may vary slightly from the investment income reported in the Province s Statement of Operations.

30 24 PROVINCE OF NEW BRUNSWICK 2007 NOTES TO THE FINANCIAL STATEMENTS Lotteries Commission of New Brunswick The Lotteries Commission of New Brunswick is a shareholder in Atlantic Lottery Corporation Inc. and in the Interprovincial Lottery Corporation. Atlantic Lottery Corporation Inc. is jointly owned by the four Atlantic Provinces and is responsible to develop, organize, undertake, conduct and manage lotteries in Atlantic Canada. Atlantic Lottery Corporation Inc. also markets and handles the products of the Interprovincial Lottery Corporation. The Interprovincial Lottery Corporation is a corporation jointly owned by the ten Canadian provinces. New Brunswick Liquor Corporation The New Brunswick Liquor Corporation was established under the New Brunswick Liquor Corporation Act. Its business activity is the purchase, distribution and sale of alcoholic beverages throughout the Province of New Brunswick. New Brunswick Municipal Finance Corporation The Municipal Finance Corporation was established under the New Brunswick Municipal Finance Corporation Act. Its purpose is to provide financing for municipalities and municipal enterprises through a central borrowing authority. The Province is guarantor of all debt issued by the Corporation. New Brunswick Electric Finance Corporation New Brunswick Electric Finance Corporation (NBEFC) is a Crown Corporation formed to assume New Brunswick Power's existing debt, to capitalize the new companies with debt and equity to enable them to become financially independent of Government, and to receive interest, dividend and special payments (in lieu of taxes) to enable it to service and repay the debt it has assumed. NBEFC includes the NB Power Group using the modified equity method. At it had included $21.0 million of net income from the NB Power Group. The $229.7 million shown by NBEFC as an investment is equal to the amount of Capital Stock of the NB Power Group plus all earnings of the corporation subsequent to 30 September The amount of $3,214.8 million reported by NBEFC as long Term Notes Receivable is included by the NB Power Group as Long Term Debt. In addition, $3,709.1 million of the amount shown as Long Term Debt of NBEFC has been borrowed by the Province and is shown on the Statement of Financial Position as a reduction of Funded Debt. New Brunswick Power Group The New Brunswick Power Corporation was established as a Crown Corporation of the Province of New Brunswick in 1920 by enactment of the New Brunswick Electric Power Act. On October 1, 2004 the Province of New Brunswick proclaimed the Electricity Act which resulted in the reorganization of NB Power and the restructuring of the electricity industry in New Brunswick. NB Power was continued as New Brunswick Power Holding Corporation with four new subsidiary operating companies (NB Power Group) which commenced operations on that date. The NB Power Group provides for the continuous supply of energy adequate for the needs and future development of the Province, and promotes economy and efficiency in the distribution, supply, sale and use of power. The combined statements of the NB Power Group report net income of $21.0 million on total revenue of $1,512 million. Total assets reported were $4,186 million. Of this amount, $3,440 million related to the net book value of tangible capital assets. The statements also report total liabilities of $3,955 million of which $2,869 million is long term debt.

Public Accounts for the fiscal year ended 31 March 2000

Public Accounts for the fiscal year ended 31 March 2000 Volume 1 Financial Statements Printed by Authority of the Legislature Fredericton, N.B. Public Accounts for the fiscal year ended 31 March 2000

Public Accounts for the fiscal year ended 31 March 2000 Volume 1 Financial Statements Printed by Authority of the Legislature Fredericton, N.B. Public Accounts for the fiscal year ended 31 March 2000

Public Accounts. for the fiscal year ended 31 March. Volume 1. Financial Statements. Printed by Authority of the Legislature Fredericton, N.B.

Public Accounts for the fiscal year ended 31 March 2001 Volume 1 Financial Statements Printed by Authority of the Legislature Fredericton, N.B. Public Accounts for the fiscal year ended 31 March 2001

Public Accounts for the fiscal year ended 31 March 2001 Volume 1 Financial Statements Printed by Authority of the Legislature Fredericton, N.B. Public Accounts for the fiscal year ended 31 March 2001

Public Accounts. Volume 1 Consolidated Financial Statements. for the fiscal year ended 31 March 2013

Volume 1 Consolidated Financial Statements Public Accounts for the fiscal year ended Printed by Authority of the Legislature Fredericton, N.B. Volume 1 Consolidated Financial Statements Public Accounts

Volume 1 Consolidated Financial Statements Public Accounts for the fiscal year ended Printed by Authority of the Legislature Fredericton, N.B. Volume 1 Consolidated Financial Statements Public Accounts

Provincial Debt Summary (Unaudited)

") Provincial Debt Summary The following unaudited Provincial Debt Summary information is intended to provide additional information to financial statement readers. The accounting policies applied for this

Provincial Debt Summary The following unaudited Provincial Debt Summary information is intended to provide additional information to financial statement readers. The accounting policies applied for this

Province of Newfoundland and Labrador. Public Accounts Volume I Consolidated Summary Financial Statements

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements FOR THE YEAR ENDED MARCH 31, 2011 Province of Newfoundland and Labrador Public Accounts Volume I

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements FOR THE YEAR ENDED MARCH 31, 2011 Province of Newfoundland and Labrador Public Accounts Volume I

VANCOUVER COMMUNITY COLLEGE

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

Province of Newfoundland and Labrador. Public Accounts. Volume II. Consolidated Revenue Fund Financial Statements. For The Year Ended 31 March 2004

Province of Newfoundland and Labrador Public Accounts Volume II Consolidated Revenue Fund Financial Statements For The Year Ended 31 March 2004 PRINTED UNDER AUTHORITY OF THE HOUSE OF ASSEMBLY This Page

Province of Newfoundland and Labrador Public Accounts Volume II Consolidated Revenue Fund Financial Statements For The Year Ended 31 March 2004 PRINTED UNDER AUTHORITY OF THE HOUSE OF ASSEMBLY This Page

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

Financial Statements of

Financial Statements of For the year ended March 31, 2015 KPMG LLP Chartered Accountants Telephone (604) 854-2200 32575 Simon Avenue Fax (604) 853-2756 Abbotsford BC V2T 4W6 Internet www.kpmg.ca Canada

Financial Statements of For the year ended March 31, 2015 KPMG LLP Chartered Accountants Telephone (604) 854-2200 32575 Simon Avenue Fax (604) 853-2756 Abbotsford BC V2T 4W6 Internet www.kpmg.ca Canada

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

BRITISH COLUMBIA TRANSIT

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements. Trade Centre Limited March 31, 2014

Financial Statements Trade Centre Limited MANAGEMENT S REPORT The financial statements have been prepared by management in accordance with Canadian public sector accounting standards and the integrity

Financial Statements Trade Centre Limited MANAGEMENT S REPORT The financial statements have been prepared by management in accordance with Canadian public sector accounting standards and the integrity

Office of the Auditor General of New Brunswick. Financial Statements

Office of the Auditor General of New Brunswick Financial Statements Financial Statements CONTENTS Independent Auditor s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement of

Office of the Auditor General of New Brunswick Financial Statements Financial Statements CONTENTS Independent Auditor s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement of

$ 2,035,512 98,790 6,974,247 2,304,324 848,884 173,207 321,487 239,138 (117,125) 658,103

658,103") FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

MOUNTAIN EQUIPMENT CO-OPERATIVE

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY. FIRST QUARTER 2000 Consolidated Financial Statements (Non audited)

") INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

The Awa Bank, Ltd. Consolidated Financial Statements. The Awa Bank, Ltd. and its Consolidated Subsidiaries. Years ended March 31, 2011 and 2012

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2011 and 2012 Consolidated Balance Sheets (Note 1) 2011 2012 2012 Assets Cash and due from banks (Notes 3 and 4) \ 230,831 \

The Awa Bank, Ltd. Consolidated Financial Statements Years ended March 31, 2011 and 2012 Consolidated Balance Sheets (Note 1) 2011 2012 2012 Assets Cash and due from banks (Notes 3 and 4) \ 230,831 \

Nova Scotia Farm Loan Board. Financial Statements March 31, 2015

Nova Scotia Farm Loan Board Financial Statements March 31, Management's Responsibility for the Financial Statements The financial statements have been prepared by management in accordance with Canadian

Nova Scotia Farm Loan Board Financial Statements March 31, Management's Responsibility for the Financial Statements The financial statements have been prepared by management in accordance with Canadian

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

GOVERNMENT OF YUKON. Financial Statement Discussion and Analysis for the year ended March 31, 2007

1 2 Introduction The Public Accounts is a major accountability report of the Government of Yukon (the Government). The purpose of the financial statement discussion and analysis is to expand upon and explain

1 2 Introduction The Public Accounts is a major accountability report of the Government of Yukon (the Government). The purpose of the financial statement discussion and analysis is to expand upon and explain

Consolidated Financial Statements. Nippon Unipac Holding and Consolidated Subsidiaries

Consolidated Financial Statements Nippon Unipac Holding and Consolidated Subsidiaries Period from March 30, 2001 (date inception) to September 30, 2001 Nippon Unipac Holding and Consolidated Subsidiaries

Consolidated Financial Statements Nippon Unipac Holding and Consolidated Subsidiaries Period from March 30, 2001 (date inception) to September 30, 2001 Nippon Unipac Holding and Consolidated Subsidiaries

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Province of Newfoundland and Labrador. Public Accounts. Volume I. Consolidated Summary Financial Statements. For The Year Ended 31 March 2004

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements For The Year Ended 31 March 2004 PRINTED UNDER AUTHORITY OF THE HOUSE OF ASSEMBLY This Page Intentionally

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements For The Year Ended 31 March 2004 PRINTED UNDER AUTHORITY OF THE HOUSE OF ASSEMBLY This Page Intentionally

London District Catholic School Board. Consolidated Financial Statements August 31, 2014

London District Catholic School Board Consolidated Financial Statements August 31, 2014 MANAGEMENT REPORT Management s responsibility for the consolidated financial statements The accompanying consolidated

London District Catholic School Board Consolidated Financial Statements August 31, 2014 MANAGEMENT REPORT Management s responsibility for the consolidated financial statements The accompanying consolidated

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

Financial Statement Guide. A Guide to Local Government Financial Statements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000)

") Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

Ricoh Company, Ltd. INTERIM REPORT (Non consolidated. Half year ended September 30, 2000) *Date of approval for the financial results for the half year ended September 30, 2000, at the Board of Directors'

5N PLUS INC. Condensed Interim Consolidated Financial Statements (Unaudited) For the three month periods ended March 31, 2016 and 2015 (in thousands

For the three month periods ended March 31, 2016 and 2015 (in thousands") Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

The Kansai Electric Power Company, Incorporated and Subsidiaries

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

Investments and Other Assets: Investment Securities 11,145 10,339 135,694 Investments in Unconsolidated Subsidiaries and Associated Companies

Consolidated Balance Sheets IBJ Leasing Company, Limited and Consolidated Subsidiaries As of March 31, 2012 and 2011 Millions of yen Thousands of U.S. dollars (Note 1) ASSETS Current Assets: Cash and Cash

Consolidated Balance Sheets IBJ Leasing Company, Limited and Consolidated Subsidiaries As of March 31, 2012 and 2011 Millions of yen Thousands of U.S. dollars (Note 1) ASSETS Current Assets: Cash and Cash

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

Consolidated Financial Statements. Forestry Innovation Investment Ltd. March 31, 2014

Consolidated Financial Statements Forestry Innovation Investment Ltd. Contents Page Independent Auditor's Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of Operations

Consolidated Financial Statements Forestry Innovation Investment Ltd. Contents Page Independent Auditor's Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of Operations

Case Western Reserve University Consolidated Financial Statements for the Year Ending June 30, 2001

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

PSAB AT A GLANCE Section PS 1201 Financial Statement Presentation

PSAB AT A GLANCE Section PS 1201 Financial Statement Presentation November 2015 Section PS 1201 - Financial Statement Presentation GENERAL REPORTING PRINCIPLES Effective Date This Section applies in the

PSAB AT A GLANCE Section PS 1201 Financial Statement Presentation November 2015 Section PS 1201 - Financial Statement Presentation GENERAL REPORTING PRINCIPLES Effective Date This Section applies in the

R E P O R T O F T H E. Auditor General. New Brunswick

R E P O R T O F T H E Auditor General of New Brunswick 1996 Office of the Auditor General Bureau du vérificateur général The Honourable Donald (Danny) Gay Speaker of the Legislative Assembly Province of

R E P O R T O F T H E Auditor General of New Brunswick 1996 Office of the Auditor General Bureau du vérificateur général The Honourable Donald (Danny) Gay Speaker of the Legislative Assembly Province of

FUNDY MUTUAL INSURANCE COMPANY CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS INDEX Page INDEPENDENT AUDITORS' REPORT 1-2 CONSOLIDATED FINANCIAL STATEMENTS Statement 1 - Consolidated Balance Sheet 3 Statement 2 - Consolidated General Reserve and

CONSOLIDATED FINANCIAL STATEMENTS INDEX Page INDEPENDENT AUDITORS' REPORT 1-2 CONSOLIDATED FINANCIAL STATEMENTS Statement 1 - Consolidated Balance Sheet 3 Statement 2 - Consolidated General Reserve and

Financial Statements

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

Financial Statements Years ended March 31,2002 and 2003 Contents Consolidated Financial Statements...1 Report of Independent Auditors on Consolidated Financial Statements...2 Consolidated Balance Sheets...3

Holloway Lodging Corporation. Interim Consolidated Condensed Financial Statements (Unaudited) June 30, 2015 (in thousands of Canadian dollars)

June 30, 2015 (in thousands of Canadian dollars)") Interim Consolidated Condensed Financial Statements August 12, Management s Report The accompanying unaudited interim consolidated condensed financial statements of Holloway Lodging Corporation (the Company

Interim Consolidated Condensed Financial Statements August 12, Management s Report The accompanying unaudited interim consolidated condensed financial statements of Holloway Lodging Corporation (the Company

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS JUNE 30, 2010 BANKERS PETROLEUM LTD. CONSOLIDATED BALANCE SHEETS (Unaudited, expressed in thousands of US dollars) ASSETS June 30 2010 December 31 2009 Current assets

CONSOLIDATED FINANCIAL STATEMENTS JUNE 30, 2010 BANKERS PETROLEUM LTD. CONSOLIDATED BALANCE SHEETS (Unaudited, expressed in thousands of US dollars) ASSETS June 30 2010 December 31 2009 Current assets

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, 2012 and January 1, 2012 (in thousands of dollars)

") A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

COMMUNITY LIVING BRITISH COLUMBIA. Audited Financial Statements. March 31, 2014

Audited Financial Statements Management s Report Management s Responsibility for the Financial Statements The financial statements of Community Living British Columbia as at, and for the year then ended,

Audited Financial Statements Management s Report Management s Responsibility for the Financial Statements The financial statements of Community Living British Columbia as at, and for the year then ended,

How To Audit A Community Care Organization

Financial Statements August 31, 2013 Table of Contents Page Independent Auditors' Report 1 Statement of Operations 3 Statement of Changes in Net Assets 4 Statement of Financial Position 5 Statement of

Financial Statements August 31, 2013 Table of Contents Page Independent Auditors' Report 1 Statement of Operations 3 Statement of Changes in Net Assets 4 Statement of Financial Position 5 Statement of

Notes to Consolidated Financial Statements Notes to Non-Consolidated Financial Statements

[Translation: Please note that the following purports to be a translation from the Japanese original Notice of Convocation of the Annual General Meeting of Shareholders 2013 of Chugai Pharmaceutical Co.,

[Translation: Please note that the following purports to be a translation from the Japanese original Notice of Convocation of the Annual General Meeting of Shareholders 2013 of Chugai Pharmaceutical Co.,

Consolidated Financial Results

UFJ Holdings, Inc. November 25, 2003 For the Six Months Ended September 30, 2003 UFJ Holdings, Inc. today reported the company's consolidated financial results for the six months ended September 30, 2003.

UFJ Holdings, Inc. November 25, 2003 For the Six Months Ended September 30, 2003 UFJ Holdings, Inc. today reported the company's consolidated financial results for the six months ended September 30, 2003.

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

DTS CORPORATION and Consolidated Subsidiaries. Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008

DTS CORPORATION and Consolidated Subsidiaries Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008 DTS CORPORATION and Consolidated Subsidiaries Quarterly Consolidated

DTS CORPORATION and Consolidated Subsidiaries Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008 DTS CORPORATION and Consolidated Subsidiaries Quarterly Consolidated

SENECA COLLEGE OF APPLIED ARTS AND TECHNOLOGY

Consolidated Financial Statements of SENECA COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Telephone (416) 228-7000 Chartered Accountants Fax (416) 228-7123 Yonge Corporate Centre Internet www.kpmg.ca

Consolidated Financial Statements of SENECA COLLEGE OF APPLIED ARTS AND TECHNOLOGY KPMG LLP Telephone (416) 228-7000 Chartered Accountants Fax (416) 228-7123 Yonge Corporate Centre Internet www.kpmg.ca

UTILITY SPLIT TRUST. Annual Financial Statements for the year ended December 31, 2011

Annual Financial Statements for the year ended December 31, 2011 MANAGEMENT S RESPONSIBILITY FOR FINANCIAL REPORTING The accompanying financial statements of Utility Split Trust (the Fund ) are the responsibility

Annual Financial Statements for the year ended December 31, 2011 MANAGEMENT S RESPONSIBILITY FOR FINANCIAL REPORTING The accompanying financial statements of Utility Split Trust (the Fund ) are the responsibility

BRITISH COLUMBIA EMERGENCY HEALTH SERVICES CORPORATION

Financial Statements of BRITISH COLUMBIA EMERGENCY HEALTH June 26, 2014 Independent Auditor s Report To the Board of British Columbia Emergency Health Services Corporation We have audited the accompanying

Financial Statements of BRITISH COLUMBIA EMERGENCY HEALTH June 26, 2014 Independent Auditor s Report To the Board of British Columbia Emergency Health Services Corporation We have audited the accompanying

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER Illustrative PSAB Financial Statements The purpose of this publication is to assist colleges in preparing their first Public Sector

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER Illustrative PSAB Financial Statements The purpose of this publication is to assist colleges in preparing their first Public Sector

Financial Statements of RED RIVER COLLEGE. Year ended June 30, 2009

Financial Statements of RED RIVER COLLEGE KPMG LLP Telephone (204) 957-1770 Chartered Accountants Fax (204) 957-0808 Suite 2000 One Lombard Place Internet www.kpmg.ca Winnipeg MB R3B 0X3 Canada AUDITORS'

Financial Statements of RED RIVER COLLEGE KPMG LLP Telephone (204) 957-1770 Chartered Accountants Fax (204) 957-0808 Suite 2000 One Lombard Place Internet www.kpmg.ca Winnipeg MB R3B 0X3 Canada AUDITORS'

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Boston College Financial Statements May 31, 2007 and 2006

Financial Statements Index Page(s) Report of Independent Auditors... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities... 3 Statement of Cash Flows... 4...5-15 PricewaterhouseCoopers

Financial Statements Index Page(s) Report of Independent Auditors... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities... 3 Statement of Cash Flows... 4...5-15 PricewaterhouseCoopers

Notes to Consolidated Financial Statements Year ended March 31, 2014

Notes to Consolidated Financial Statements Year ended March 31, 2014 Mitsui Oil Exploration Co., Ltd. and Consolidated Subsidiaries 1. Basis of Presenting Consolidated Financial Statements The accompanying

Notes to Consolidated Financial Statements Year ended March 31, 2014 Mitsui Oil Exploration Co., Ltd. and Consolidated Subsidiaries 1. Basis of Presenting Consolidated Financial Statements The accompanying

FINANCIAL STATEMENT 2010

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

Centre for Addiction and Mental Health. Financial Statements March 31, 2014

Centre for Addiction and Mental Health Financial Statements June 4, Independent Auditor s Report To the Trustees of Centre for Addiction and Mental Health We have audited the accompanying financial statements