TILA/RESPA Integrated Disclosures. BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group

|

|

|

- Pierce Byrd

- 8 years ago

- Views:

Transcription

1 TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group

2 BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National consumer protection agency Enforcement and rulemaking authority consolidated within CFPB Dodd Frank required CFPB to use that authority in specific ways 2

CFPB TILA/RESPA Integrated Disclosures")

3 CONSOLIDATION OF AUTHORITY FRB Truth In Lending Act (TILA) HUD Real Estate Settlement & Procedures Act (RESPA) CFPB TILA/RESPA Integrated Disclosures (TRID) 3

4 Application Closing Truth In Lending Act TIL Initial Disclosure TIL Disclosure RESPA GFE HUD 1 4

5 TIL Initial Disclosure GFE GFE HUD 1 Loan Estimate Variances? Closing Disclosure 5

6 THE RULE: OVERVIEW The Loan Estimate ( LE ) replaces two documents: Good Faith Estimate designed by HUD under RESPA Early Truth in Lending Disclosure designed by the FRB under TILA The Closing Disclosure ( CD ) replaces: HUD-1 designed by HUD under RESPA Revised Truth in Lending Disclosure by FRB under TILA New pre-disclosure requirements New timing requirements for disclosures New tolerance (variance) levels for disclosed estimates 6

7 IMPLEMENTATION AND SCOPE New forms cannot be used before August 1, 2015 After August 1, 2015, forms must be used for most closed-end consumer mortgages, including: Construction-only loans Loans secured by vacant land or by 25 or more acres Credit extended to certain trusts for tax or estate planning purposes 7

8 IMPLEMENTATION AND SCOPE Exceptions - do not use the new forms for: HELOCs Reverse mortgages Mobile home mortgages Chattel-Dwelling Loans Loans made by a creditor who makes five or fewer mortgages in a year 8

9 PERMISSIVE/PROHIBITED USE OF FORMS You can use the forms for loans not covered by TILA or RESPA But you cannot use forms in place of HUD-1, GFE and TILA forms where the transaction is covered by TILA or RESPA (i.e., reverse mortgages) The rule exempts certain down payment assistance loans, but the transaction must meet criteria listed in the rule and corresponding RESPA exemptions 9

10 CONSUMMATION Consummation Not the same thing as closing or settlement May commonly occur at the same time as closing or settlement, but it is a legally distinct event Consummation occurs when the consumer becomes contractually obligated to the creditor on the loan, not, for example, when the consumer becomes contractually obligated to a seller on a real estate transaction. 10

11 THE PROCESS - SIMPLIFIED Borrower submits application Creditor provides LE within 3 days of application and at least 7 days before consummation Borrower accepts LE CD delivered to borrower at least 3 days before consummation CD errors corrected within 30 days Variance errors corrected within 60 days after consummation 11

12 LIMITATIONS ON PRE-LE CHARGES Cannot charge fees before the consumer has received the Loan Estimate and consented to proceed with the transaction Cannot require that consumers submit documents verifying information related to the application before providing the Loan Estimate Cannot provide written estimates of costs before issuing a Loan Estimate unless you provide a written statement that the terms and costs may change 12

13 DIFFERENCES BETWEEN PROPOSED RULE AND FINAL RULE Two proposed provisions omitted: No All-in APR No mandatory machine-readable record retention; the data standard wasn t specific enough Lenders must issue the Loan Estimate within 3 days of application Proposed rule included Saturdays in the 3-day period for LE Final Rule only counts days the lender is actually open for this purpose* * Does not apply when calculating time for CD 13

14 DIFFERENCES BETWEEN PROPOSED RULE AND FINAL RULE Proposed Rule required reissue CD/ restart 3-day waiting period whenever there was more than minor change Now 3-day waiting period restarts only if there are substantial changes to: APR Loan Product (fixed rate becomes adjustable rate or interest only mortgage) Prepayment penalty added 14

15 APPLICATION Submission of the application triggers obligation to provide Loan Estimate and consists of six pieces of information: Consumer s name Income Social Security Number Property address Estimated value of the property Mortgage loan amount sought Former catch-all provision ( any other information deemed necessary by the loan originator ) has been eliminated 15

16 APPLICATION Application can be complete without the consumer requesting a specific loan product or term CFPB expects creditors to be able to obtain additional information before issuing the LE If not specified, creditor can select product, term or other features to use when producing the LE (good faith still required) Creditor is not required to produce multiple Loan Estimates for different products 16

17 APPLICATION No special treatment of online applications Consumer can save an online application without submitting it Online application systems should not refuse applications for lack of preferred information Information from a previous or existing loan or loan application submission does not constitute submission 17

18 Application Submission 3 Days Issue Loan Estimate 18

19 LOAN ESTIMATE: SCOPE Loan Estimate required for any federally related mortgage loans Alternative Loan Estimate may be used if the transaction has no seller Must contain a good faith estimate of credit costs and: Be based on best information available at that time and due diligence Be In writing and contain the information described in

20 LOAN ESTIMATE: DELIVERY The creditor is responsible for delivering the Loan Estimate or placing it in the mail no later than 3 business days after receiving the application Mortgage broker may deliver the LE if the broker received the application Business day means a day on which the creditor s offices are open to the public for carrying out substantially all of its business functions. 20

21 LOAN ESTIMATE: DELIVERY If not delivered in person, the consumer is considered to have received it 3 business days after it is delivered or placed in the mail Loan Estimate must be delivered or placed in the mail no later than 7 business days before consummation (This does not apply to revised disclosures) 21

22 LOAN ESTIMATE: PROVIDER LIST When LE is delivered, creditor must also provide a written list of providers that corresponds to the settlement services for which the consumer can shop (as disclosed on the Loan Estimate) The creditor may also identify on the written list of providers those services for which the consumer is not permitted to shop Services must be clearly and conspicuously distinguished 22

23 INFORMATION BOOKLET Creditors must deliver or place in the mail the special information booklet not later than 3 business days after receiving the consumer s loan application Booklet is not required if the consumer mortgage loan is not for the purpose of purchasing a one-to-four family residential property: A refinancing A closed-end loan secured by a subordinate lien A reverse mortgage 23

24 Application Submission Within 3 Days Issue Loan Estimate At least 7 days before Consummation 24

25 LOAN ESTIMATE: WAIVER OF WAITING PERIOD Consumer can waive the 7-business-day waiting period for a bonafide personal financial emergency Consumer must give the creditor a dated written statement that Describes the emergency Specifically modifies or waives the waiting period Is signed by all consumers primarily liable on the legal obligation 25

26 LOAN ESTIMATE: CONSUMER CONSENT A consumer indicates intent to proceed with the transaction when The consumer communicates, in any manner, that the consumer chooses to proceed after the Loan Estimate has been delivered Unless a particular manner of communication is required by the creditor 26

27 LOAN ESTIMATE: REVISIONS PERMITTED Revised Loan Estimates permitted only in certain specific circumstances: 1. Changed circumstances that occur after the Loan Estimate is provided to the consumer cause estimated settlement charges to increase more than is permitted under the TILA-RESPA rule 2. Changed circumstances that occur after the Loan Estimate is provided to the consumer affect the consumer s eligibility for the terms for which the consumer applied or the value of the security for the loan 3. Revisions to the credit terms or the settlement are requested by the consumer 27

28 LOAN ESTIMATE: REVISIONS PERMITTED Conditions (continued): 4. The interest rate was not locked when the Loan Estimate was provided, and locking the rate causes the points or lender credits disclosed on the Loan Estimate to change 5. The consumer indicates an intent to proceed with the transaction more than 10 business days after the Loan Estimate was originally provided 6. The loan is a new construction loan, and settlement is delayed by more than 60 calendar days, if the original Loan Estimate states clearly and conspicuously that at any time prior to 60 calendar days before consummation, the creditor may issue revised disclosures 28

29 LOAN ESTIMATE: DOES RATE LOCK REQUIRE REVISION? CFPB has said that the revised LE must be provided on the same business day the creditor and consumer enter into the rate lock agreement (not necessarily the date the lock is requested) The Bureau does not believe that creditors need that much time in situations where the interest rate is locked because the creditor controls when it executes the rate lock agreement. Re-disclosure is not triggered when the interest rate has been set but a rate lock agreement does not yet exist: The Bureau intended that (e)(3)(iv)(D) only applies in situations where a rate lock agreement has been entered into between the creditor and the borrower or where such agreement has expired. 29

30 LOAN ESTIMATE: REVISIONS PERMITTED A creditor also may provide and use a revised Loan Estimate if 1. A changed circumstance affected the consumer s creditworthiness, or 2. A changed circumstance affected the value of the security for the loan, and 3. As a result of either condition, the consumer becomes ineligible for the disclosed estimated previously disclosed loan term 30

31 TIMELINE: REVISED LOAN ESTIMATE Creditor must deliver or place in the mail the revised LE no later than 3 business days after receiving the information that justifies revision The revised LE must be provided before the Closing Disclosure The creditor must ensure that the consumer receives the revised LE no later than 4 business days before consummation 31

32 LOAN ESTIMATE FORM

33 LOAN ESTIMATE PAGE 1 33

34 LOAN ESTIMATE PAGE 1 34

35 LOAN ESTIMATE PAGE 1 35

36 LOAN ESTIMATE PAGE 1 36

37 LOAN ESTIMATE PAGE 2 37

38 LOAN ESTIMATE PAGE 2 38

39 LOAN ESTIMATE PAGE 2 39

40 LOAN ESTIMATE PAGE 2 40

41 LOAN ESTIMATE PAGE 2 41

42 LOAN ESTIMATE PAGE 2 42

43 LOAN ESTIMATE PAGE 3 43

44 LOAN ESTIMATE PAGE 3 44

45 LOAN ESTIMATE PAGE 3 45

46 LOAN ESTIMATE PAGE 3 46

47 ALTERNATIVE LE FORM Creditors to use an alternative Loan Estimate and an alternative Closing Disclosure with fewer entries for transactions without a seller Adjusts and abbreviates two parts of the Loan Estimate: Cash to close amount on page 1 Calculating cash to close table on page 2 Discretionary in transactions without a seller 47

48 LOAN ESTIMATE AND GOOD FAITH Generally cannot issue revised LE due to technical errors, miscalculations, or underestimated charges Good Faith is determined by calculating the difference between: Estimated charges in the Loan Estimate and Actual charges imposed in the Closing Disclosure Always good faith if creditor charges less than the LE 48

49 VARIANCES There are some amounts that are permitted to increase between LE and CD Final Rule refers to variance (rather than tolerance ) Three categories of charges: No Cap on Variance 10% Cumulative Variance Allowed 0% Variance Allowed 49

50 NO CAP VARIANCES A creditor can charge more than the amount disclosed on the Loan Estimate (assuming otherwise in good faith) for the following: 1. Prepaid interest; property insurance premiums; amounts placed into an escrow, impound, reserve or similar account 2. For services required by the creditor if the creditor permits the consumer to shop and the consumer selects a third-party service provider not on the creditor s written list of service providers 3. Charges paid to third-party service providers for services not required by the creditor (may be paid to affiliates of the creditor) 50

51 10% CAP Charges for third-party services and recording fees paid by the consumer are subject to a 10% cumulative tolerance Creditor may charge more than the amount disclosed on the LE But only if the total charges added together does not exceed the total disclosed on the LE by more than 10% If a creditor failed to include a particular charge on the LE that is later imposed, it falls under the 10% cumulative variance rule 51

52 0% VARIANCE For all other charges, creditors are not permitted to charge consumers more than the amount disclosed on the Loan Estimate under any circumstances (absent certain changed circumstances): Fees paid to the creditor, mortgage broker, or an affiliate of either Fees paid to an unaffiliated third party if the creditor did not permit the consumer to shop for a third party service provider for a settlement service Transfer taxes 52

53 EXPANDED 0% CATEGORIES Reg X previously prohibited variations in between the estimated amounts and the actual amounts of Origination charges Transfer taxes Final Rule expands the current zero percent tolerance category of settlement costs to include Affiliate fees Fees charged lender required service providers Unless it is a legitimate cost revisions such as changed circumstances or borrower-requested changes 53

54 CHARGES PAID TO CREDITOR, BROKER, OR AFFILIATE The term affiliate means any company that controls, is controlled by, or is under common control with another company A charge is paid to the creditor, mortgage broker, or an affiliate of either if it is retained by that person or entity A charge is not paid to one of these entities when it receives money but passes it on to an unaffiliated third party 54

55 VARIANCE - OWNER S TITLE INSURANCE Generally speaking, owner s title insurance not required by the creditor is not subject to the 10% cumulative tolerance The 10% category only includes recording fees and charges paid to unaffiliated third-party service providers Where the consumer is permitted to shop and chooses a provider from the creditor s written list of providers 55

56 VARIANCE - OWNER S TITLE INSURANCE Owner s title insurance is not called out as a charge subject to any categorical treatment under the tolerance rules Its category will depend on the other rules: Whether it is required by the creditor If required, is shopping is permitted and/or did it occur If owner s title is not required and is disclosed as optional, it is a variation permitted charges - not subject to tolerance. 56

57 VARIANCE - THRESHOLD VIOLATION 60 DAY CURE PERIOD If the amounts paid by the consumer at closing exceed the amounts disclosed on the Loan Estimate beyond the applicable tolerance threshold, the creditor must refund the excess to the consumer no later than 60 calendar days after consummation 57

58 CLOSING DISCLOSURE Creditor required to ensure that the consumer receives the Closing Disclosure no later than 3 business days before consummation: Must be in writing Generally must contain the actual terms and costs of the transaction For any loans subject to the TILA-RESPA rule that are federally related mortgage (which will include most mortgages) creditors must use the form H-25 58

59 CLOSING DISCLOSURE: BUSINESS DAY DEFINED Business day has a different meaning for the Closing Disclosure than for the Loan Estimate For purposes of the Closing Disclosure, business day means all calendar days except Sundays and the legal public holidays The loan may not be consummated less than three business days after the Closing Disclosure is received by the consumer If a settlement is scheduled during the waiting period, the creditor generally must postpone settlement, unless a settlement within the waiting period is necessary to meet a bona fide personal financial emergency 59

60 CLOSING DISCLOSURE: DELIVERY/TIMING CD can be delivered via hand delivery, mail, or Creditor can use electronic signatures If provided in person, deemed received that day If mailed or delivered electronically, deemed received 3 business days after it is delivered or mailed If the creditor has evidence that the consumer received the CD earlier than 3 business days after mailing or delivery, it may rely on that evidence and deem it received on that date 60

61 CLOSING DISCLOSURE: DELIVERY/PREPARATION Creditors may contract with settlement agents to have the settlement agent provide the CD to consumer Creditors and settlement agents may divide responsibility for completing CD Creditor must communicate with agent to ensure requirements are satisfied Creditor remains legally responsible for any errors or defects The settlement agent is required to provide the seller with the Closing Disclosure reflecting the actual terms of the seller s transaction 61

62 CLOSING DISCLOSURE: ESTIMATED AMOUNTS Creditors may estimate disclosure amounts when the actual term or cost is not reasonably available when the disclosure is made if: Using the best information reasonably available Acting in good faith and using due diligence to obtain the information Creditor normally may rely on the representations of other parties in obtaining the information, including, for example, the settlement agent 62

63 CLOSING DISCLOSURE: USING AVERAGES An average charge can be used if it is no more than the average amount paid for that service by all consumers and sellers for a class of transactions Creditor or settlement service provider must: Define the class of transactions based on an appropriate period of time, geographic area, and type of loan Use the same average charge for every transaction within the defined class Do not use an average charge for any type of insurance, any charge based on the loan amount of property value, or as is prohibited by law 63

64 CLOSING DISCLOSURE: WAIVER OF WAITING PERIOD Consumers may waive or modify the three-business-day waiting period when: 1. The extension of credit is needed to meet a bona fide personal financial emergency 2. The consumer has received the Closing Disclosure 3. The consumer gives the creditor a dated written statement that: Describes the emergency Specifically modifies or waives the waiting period Bears the signature of all consumers who are primarily liable on the legal obligation 64

65 CLOSING DISCLOSURE: REDISCLOSURE Certain changes require creditors to re-disclose terms or costs on the CD Three categories of changes that require a corrected CD: 1. Changes that occur before consummation that require a new 3- business-day waiting period 2. Changes that occur before consummation and do not require a new 3-business-day waiting period 3. Changes that occur after consummation. 65

66 CLOSING DISCLOSURE: REDISCLOSURE/3-DAYS New 3-day waiting period required if there are substantial changes to: APR Loan Product (fixed rate becomes adjustable rate or interest only mortgage) Prepayment penalty added 66

67 CLOSING DISCLOSURE: REDISCLOSURE/NO 3-DAY PERIOD For any other changes before consummation that do not fall under the three categories above, the creditor still must: Provide a corrected Closing Disclosure with any terms or costs that have changed and ensure that the consumer receives it For these changes, there is no additional three-business-day waiting period required The creditor must ensure only that the consumer receives the revised Closing Disclosure at or before consummation 67

68 CLOSING DISCLOSURE: REDISCLOSURE FOR APR? Is an additional 3-business-day waiting period required if the APR decreases by more than ¼ or ⅛ percentage points? An additional three business day waiting period is required if the APR on the Closing Disclosure becomes inaccurate But assume an APR was overdisclosed due to an overdisclosed finance charge That situation should not require a new waiting period* * Based on oral guidance from CFPB 68

69 CLOSING DISCLOSURE: CONSUMER REQUEST TO INSPECT A consumer may request to inspect the Closing Disclosure the business day before consummation The corrected Closing Disclosure presented to the consumer must reflect any adjustments to the costs or terms that are known to the creditor at the time the consumer inspects it 69

70 CLOSING DISCLOSURE FOR SELLER In transactions with a seller, where the creditor may commonly have no relationship with the seller, the settlement agent shall provide the seller with the Closing Disclosures In this circumstance, the third-party settlement agent may provide the seller with the Closing Disclosure on a different document than that provided to the consumer by the creditor When the consumer and seller s disclosures are provided on separate documents, the settlement agent shall provide to the creditor, again assuming different parties, a copy of the disclosures provided to the seller 70

71 CLOSING DISCLOSURE AND RECORD RETENTION FOR SELLER The Rule does not does not state that settlement agents are required to provide the creditor with underlying records used to take the seller s disclosures Examples: Copies of agreements outside the purchase contract that may exist between the seller and buyer Any invoices or bills related to fees or costs paid by the seller but not on behalf of the borrower 71

72 CLOSING DISCLOSURE: CORRECTIONS REQUIRED Post-consummation, creditors must provide a corrected Closing Disclosure if, within 30-calendar days following consummation: An event in connection with the settlement occurs that causes the Closing Disclosure to become inaccurate And results in a change to an amount paid by the consumer from what was previously disclosed Creditor must deliver or place in the mail a corrected Closing Disclosure not later than 30 calendar days after receiving information sufficient to establish that such an event has occurred 72

73 CLOSING DISCLOSURE: CORRECTIONS POST-CONSUMMATION Settlement agents must provide a revised Closing Disclosure to seller if: An event related to the settlement occurs during the 30-day period after consummation that causes the Closing Disclosure to become inaccurate, and Results in a change to an amount actually paid by the seller from what was previously disclosed The settlement agent must deliver or place in the mail a corrected Closing Disclosure not later than 30 calendar days after receiving information sufficient to establish that such an event has occurred 73

74 CLOSING DISCLOSURE: CORRECTIONS FOR TOLERANCE VIOLATION Creditors must issue revised CD to correct non-numerical clerical errors and document refunds for tolerance violations no later than 60 calendar days after consummation An error is clerical if it does not affect a numerical disclosure and does not affect the timing and/or delivery If the creditor cures a tolerance violation by providing a refund to the consumer, the creditor must deliver or place in the mail a corrected Closing Disclosure that reflects the refund no later than 60 calendar days after consummation 74

75 CLOSING DISCLOSURE FORM

76 CLOSING DISCLOSURE PAGE 1 76

77 CLOSING DISCLOSURE PAGE 1 77

78 CLOSING DISCLOSURE PAGE 1 78

79 CLOSING DISCLOSURE PAGE 1 79

80 CLOSING DISCLOSURE PAGE 2 80

81 CLOSING DISCLOSURE PAGE 2 81

82 CLOSING DISCLOSURE PAGE 2 82

83 CLOSING DISCLOSURE PAGE 2 83

84 CLOSING DISCLOSURE PAGE 2 84

85 CLOSING DISCLOSURE PAGE 2 85

86 CLOSING DISCLOSURE PAGE 2 86

87 CD PAGE 2 RECORDING FEE ISSUES Difference in recording fees between the LE and the CD The LE requires recording fees to be disclosed as one item The CD requires the recording fees to be disclosed as one item, except: It requires that amounts for recording the deed and the mortgage be itemized Recording fees associated with any other documents, except for the deed and mortgage, are included in the total recording fees and not separately itemized 87

88 CLOSING DISCLOSURE PAGE 2 88

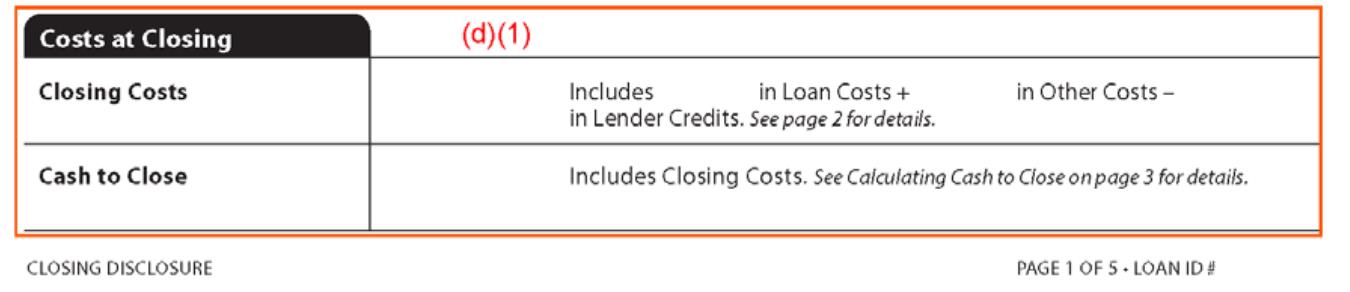

89 CLOSING DISCLOSURE PAGE 2 89

90 CLOSING DISCLOSURE PAGE 2 90

91 CLOSING DISCLOSURE PAGE 2 IDENTIFY TRANSFER TAXES How should creditors disclose the name of the government entity to whom a transfer tax is distributed? Creditors should disclose the name of the entity assessing the transfer tax, even if that is different from the payee of the check cut by the settlement agent. ( (g)(1)(ii)). 91

92 CLOSING DISCLOSURE PAGE 2 92

93 CLOSING DISCLOSURE PAGE 3 93

94 CLOSING DISCLOSURE PAGE 3 94

95 CLOSING DISCLOSURE PAGE 3 95

96 CLOSING DISCLOSURE PAGE 3 96

97 CLOSING DISCLOSURE PAGE 3 Summaries of Borrower and Seller transactions Similar to current page 1 of HUD-1 The closing disclosure given to the seller must also be provided to the creditor by the settlement agent Lender s credits will not appear in the borrower s transaction table Lender credit will either show as individual settlement services paid by others or as a generalized lender credit at the bottom of Page 2 97

98 CLOSING DISCLOSURE PAGE 4 98

99 CLOSING DISCLOSURE PAGE 4 99

100 CLOSING DISCLOSURE PAGE 4 100

101 CLOSING DISCLOSURE PAGE 4 101

102 CLOSING DISCLOSURE PAGE 4 102

103 CLOSING DISCLOSURE PAGE 5 103

104 CLOSING DISCLOSURE PAGE 5 104

105 CLOSING DISCLOSURE PAGE 5 105

106 CLOSING DISCLOSURE PAGE 5 106

107 CLOSING DISCLOSURE PAGE 5 107

108 ESCROW NOTICE Creditor must provide a consumer notice not later than three business days before the consumer s escrow account is cancelled For loans subject to the escrow account cancellation notice requirement, creditor or servicer must disclose: When and why the escrow account will be closed That an escrow account may also be called an impound or trust account That without an escrow account the consumer must directly pay all property costs (i.e., taxes, homeowner s insurance) 108

109 ESCROW NOTICE Escrow account cancellation notice requirements (continued): A Cost to you table itemizing the amount of any fee imposed on the consumer in connection with the closure of the escrow account A statement that the fee is for closing the escrow account and under In the future, consequences for failure to pay property costs A telephone number for additional information Whether escrow account can be kept open Whether there is a deadline to request that the escrow account be kept open. 109

110 RECORD RETENTION After consummation, Creditor must retain: Loan Estimate for 3 years Closing Disclosure and all related documents for 5 years Post-Consummation Escrow Cancellation Notice (Escrow Closing Notice) for 2 years Post-Consummation Partial Payment Policy Disclosure for two years 110

111 RECORD RETENTION If mortgage is sold (and the creditor does not retain servicing rights), creditor must provide a copy of the Closing Disclosure to the purchaser Both entities are required to keep copies of the Closing Disclosure for the five year period. The creditor or servicer, if applicable, must retain all records and/or evidence of compliance with the Integrated Disclosure Rules for three years after the consummation of the transaction 111

112 CLOSING DISCLOSURE AND RECORD RETENTION FOR SELLER CFPB guidance: Creditors not required to collect the seller-specific records from the third-party settlement agent or retain them along with the Closing Disclosure If the creditor receives documentation related to the seller s disclosure, the creditor should adhere to the normal record retention requirements and retain those records Such as when the creditor is the settlement agent When seller-related documents are provided to the creditor by a third-party settlement agent along with the completed disclosure 112

113 TRID TIMELINES CFPB SCENARIO

114 TIME LINE EXAMPLE Assumptions The Creditor is not open for business on Saturdays. The property is located in a State where consummation is the day of closing, or signing of documents, between the Consumer and Seller. All parties are targeting a closing date of October 29. The Consumer s application is received by the Creditor on Monday, August 3, From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014) 114

115 TIME LINE EXAMPLE For purposes of providing the Loan Estimate, or any revised Loan Estimate, a business day is a day on which the creditor s offices are open to the public for carrying out substantially all of its business functions. For all other purposes, business day means all calendar days except Sundays and legal public holidays specified in 5 U.S.C. 6103(a) such as, New Year s Day, the Birthday of Martin Luther King, Jr., Washington s Birthday, Memorial Day, Independence Day, Labor Day, Columbus Day, Veterans Day, Thanksgiving Day, and Christmas Day. From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014) 115

116 TIME LINE EXAMPLE This timeline shows the effect of the following events during the course of the origination of the loan: Receipt of an addendum to Contract modifying the allocation of transfer taxes between the Consumer and Seller. (August 28th) Appraisal provides a property value resulting in a loan-to-value ratio higher than 80%, triggering mortgage insurance. (September 4th) An updated credit report obtained by the Creditor shows a changed credit score, triggering a LLPA. (September 22nd) From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014) 116

117 TIME LINE EXAMPLE Events (continued): A rate lock is requested by the Consumer. (October 5th) The Consumer decides to obtain an Owner s Title Policy the week prior to consummation. (October 21st) During a walkthrough two days before consummation, a broken dishwasher is discovered. (October 27th) The recording fees collected were $100 more than needed when the documents are presented for recording after consummation. (October 30th) From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014) 117

118 118 From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014)

119 119 From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014)

120 120 From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014)

121 121 From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014)

122 122 From CFPB: TILA RESPA Integration Disclosure Timeline Example (September 2014)

123 CURING VIOLATIONS The Bureau believes that providing creditors with sufficient time to obtain revised cost information, revise the integrated disclosures, prepare payments for such revised costs or the cures to be paid to consumers, and deliver such payments to consumers will facilitate compliance and ensure accurate disclosures and payments for consumers The final rule removes the condition that refunds and revised disclosures be provided as soon as reasonably practicable in favor of a bright-line standard by which revised disclosures must be mailed or delivered The Bureau lengthened the cure period to 60 days after consummation 123

124 CURING VIOLATIONS Final (f)(2)(v) provides that: If amounts paid by the consumer exceed the amounts specified under ((e)(3)(i) or (ii), the creditor complies with (e)(1)(i) if: The creditor refunds the excess to the consumer no later than 60 days after consummation, and The creditor complies with (f)(1)(i) if the creditor delivers or places in the mail corrected disclosures that reflect such refund no later than 60 days after consummation. 124

125 CURING VIOLATIONS This proposed regulation will enable meaningful disclosure of credit terms, prevent circumvention and evasion of TILA, and will facilitate compliance with TILA by enabling creditors to refund amounts collected in excess of the good faith requirements, consistent with TILA section 105(a). This will also result in the meaningful advance disclosure of settlement costs and the elimination of kickbacks, referral fees, and other practices that tend to increase unnecessarily the costs of certain settlement services by enabling creditors to refund amounts collected in excess of the good faith requirements, thereby furthering the meaningfulness and reliability of the estimated disclosures, consistent with section 19(a) of RESPA. 125

126 GENERAL CONCERNS Challenges Significant challenge will be closing disclosure timing change - getting documents to consumer 3 days before consummation Today, a buyer might still be in negotiations with the seller, and things can change right up until the closing. Industry Integration Awareness and communication of expectations 126

127 TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney Regulatory Compliance Group LINDSEY R. JOHNSON Attorney Regulatory Compliance Group

TILA-RESPA Integrated Disclosures

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

Outlook Live Webinar- June 17, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued the

CFPB Integrated Mortgage Disclosures

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

TILA-RESPA Integrated Disclosure Rule * January 21, 2015

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP David.kantor@stinsonleonard.com 612-335-1620 1. Effective Date. The new Integrated Disclosures

FRESH. Agenda. Credit Union Integrated Mortgage Disclosures Are you Prepared?

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

When do I have to start following the TILA-RESPA rule and using the new Integrated Disclosures?

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

PRMG is Ramping Up for the TILA RESPA Rule

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders

CUNA s COMPLIANCE HIGHLIGHTS

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

TILA-RESPA Integrated Disclosure rule. Small entity compliance guide

TILA-RESPA Integrated Disclosure rule Small entity compliance guide September 2014 Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications to the rule which impacts

TILA-RESPA Integrated Disclosure rule Small entity compliance guide September 2014 Version Log The Bureau updates this guide on a periodic basis to reflect finalized clarifications to the rule which impacts

TILA-RESPA Integrated Disclosure rule. Small entity compliance guide

TILA-RESPA Integrated Disclosure rule Small entity compliance guide March 2014 Table of contents Table of contents... 2 1. Introduction... 10 1.1 What is the purpose of this guide?... 11 1.2 Who should

TILA-RESPA Integrated Disclosure rule Small entity compliance guide March 2014 Table of contents Table of contents... 2 1. Introduction... 10 1.1 What is the purpose of this guide?... 11 1.2 Who should

The Federal Register published the proposed rule on August 23, 2012.

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

Brief Walk Through of TRID. Presented by: Scott Meerstein MGIC Inside Sales

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

TILA-RESPA Integrated Disclosure Rule

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

How To Write A Disclosure Form

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

TRID. What are the Timing Requirements for Revisions to a Loan Estimate?

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

LOAN ESTIMATE TABLE. Definition of an application that triggers a Loan Estimate

LOAN ESTIMATE TABLE CATEGORY SYNOPSIS TIMING AND DELIVERY Timing & Delivery No later than the third-business-day after receiving the consumer s application. Must also be delivered or placed in the mail

LOAN ESTIMATE TABLE CATEGORY SYNOPSIS TIMING AND DELIVERY Timing & Delivery No later than the third-business-day after receiving the consumer s application. Must also be delivered or placed in the mail

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

Changes to Mortgage Loan Closing Process

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

bankerstitleshenandoah.com 1.888.259.7184

Delivered in partnership with your local title and settlement agency bankerstitleshenandoah.com 1.888.259.7184 About this Manual In an effort to provide a thorough condensed training reference, this manual

Delivered in partnership with your local title and settlement agency bankerstitleshenandoah.com 1.888.259.7184 About this Manual In an effort to provide a thorough condensed training reference, this manual

2015 Fidelity National Title Group

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

Know Before You Owe. TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

TRID Frequently Asked Questions

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!!

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements

TILA-RESPA Integrated Disclosure (TRID) Rule Requirements") Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

Loan Estimate (LE) TILA-RESPA Integrated Disclosure (TRID) Rule Requirements New Definitions; New Forms New Work Flow New Rule creates new definition of Covered Loan Loan Application Consummation (Closing)

CFPB Proposes New Mortgage Disclosure Rules

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

Overview The Regulation The Loan Estimate (LE) The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility

The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility") To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

TILA RESPA Integration disclosure timeline example. September 2014

TILA RESPA Integration disclosure timeline example September 2014 Disclaimer This document does not represent legal interpretation, guidance or advice of the Bureau. While efforts have been made to ensure

TILA RESPA Integration disclosure timeline example September 2014 Disclaimer This document does not represent legal interpretation, guidance or advice of the Bureau. While efforts have been made to ensure

TILA RESPA An Overview

TILA RESPA An Overview March 13, 2014 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. and Michael J. Coleman, Esq. NAFCU Director of Regulatory Affairs E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. 150

TILA RESPA An Overview March 13, 2014 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. and Michael J. Coleman, Esq. NAFCU Director of Regulatory Affairs E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. 150

TILA/RESPA Integrated Disclosure (TRID) Rule

Rule") TILA/RESPA Integrated Disclosure (TRID) Rule Ken Markison, Vice President, Regulatory Counsel, MBA Jerra H. Ryan, Vice President of Compliance, Cherry Creek Mortgage Alex Karram, Attorney, Weiner Brodsky

TILA/RESPA Integrated Disclosure (TRID) Rule Ken Markison, Vice President, Regulatory Counsel, MBA Jerra H. Ryan, Vice President of Compliance, Cherry Creek Mortgage Alex Karram, Attorney, Weiner Brodsky

TILA RESPA Integrated Disclosures. On October 3 rd, life as we know it will change forever. One of the new forms is.

TILA RESPA Integrated Disclosures The Loan Estimate and Miscellaneous Requirements Lynne Murphy Breen, Esquire Sue Ellen Rogal, Esquire September 16, 2015 On October 3 rd, life as we know it will change

TILA RESPA Integrated Disclosures The Loan Estimate and Miscellaneous Requirements Lynne Murphy Breen, Esquire Sue Ellen Rogal, Esquire September 16, 2015 On October 3 rd, life as we know it will change

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation

Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation") Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements

TILA- RESPA Integrated Disclosure (TRID) Rule Requirements") Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements The purpose of this document is to provide a reference guide for the Loan Estimate (LE) TILA-RESPA Integrated

Reference Guide: Loan Estimate (LE) TILA- RESPA Integrated Disclosure (TRID) Rule Requirements The purpose of this document is to provide a reference guide for the Loan Estimate (LE) TILA-RESPA Integrated

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Home Mortgage Loan Tips: TILA-RESPA Integrated Disclosures

PLEASE STAND BY Your webinar is about to begin. pncmortgage.com/agentalliance 1 2015 Home Lending Changes New Mortgage Rules Demystified: TILA RESPA Integrated Disclosures (TRID) Welcome to the webinar!

PLEASE STAND BY Your webinar is about to begin. pncmortgage.com/agentalliance 1 2015 Home Lending Changes New Mortgage Rules Demystified: TILA RESPA Integrated Disclosures (TRID) Welcome to the webinar!

TILA RESPA One of the Most Expensive Changes in Decades

Veronese 2405 Wednesday, July 23, 2014 1:00 2:00 p.m.; 2:15 3:15 p.m. TILA RESPA One of the Most Expensive Changes in Decades E. Andrew Keeney, Esq., Partner, Kaufman & Canoles, P.C. 1 TILA RESPA One of

Veronese 2405 Wednesday, July 23, 2014 1:00 2:00 p.m.; 2:15 3:15 p.m. TILA RESPA One of the Most Expensive Changes in Decades E. Andrew Keeney, Esq., Partner, Kaufman & Canoles, P.C. 1 TILA RESPA One of

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

CFPB and Lenders. A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Moderator Roger Blauvelt Vice President & National Agency Counsel WFG National Title Insurance Company

Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Webinar Thursday, January 16, 2014 2:00 3:30 pm ET Moderator Roger Blauvelt Vice President & National Agency Counsel WFG National Title Insurance Company

General Resources CFPB Resources ALTA Best Practices Closing Insight Notaries Business & Commercial Loans Foreign Consumers

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

TILA RESPA Procedural Impacts Are You Ready? Presenters. CUNA Mutual Group 2015 All rights reserved. 1. July 7, 2015

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 jonathan.bundy@cunamutual.com Theresa Reinke LOANLINER Compliance Consultant

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 jonathan.bundy@cunamutual.com Theresa Reinke LOANLINER Compliance Consultant

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

CFPB s RESPA TILA Integrated Disclosure. Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381

329-8381") CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

CFPB s RESPA TILA Integrated Disclosure Finley P. Maxson NAR Senior Counsel fmaxson@realtors.org (312) 329-8381 RESPA-TILA Integrated Disclosure A. Background I. Impetus for change a. Dodd-Frank directed

Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs

October 6, 2016 TO: State Directors Rural Development ATTN: Program Directors Single Family Housing FROM: Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs SUBJECT:

October 6, 2016 TO: State Directors Rural Development ATTN: Program Directors Single Family Housing FROM: Tony Hernandez /s/ Tony Hernandez Administrator Housing and Community Facilities Programs SUBJECT:

Update on CFPB s TILA- RESPA Integrated Disclosure Rule

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

INTEGRATED MORTGAGE DISCLOSURES

INTEGRATED MORTGAGE DISCLOSURES (TILA RESPA RULE) Financial Solutions Patti Blenden April 2015 1 CFPB Accomplishes Integration of GFE/eTILA After 30 years of encouraging HUD and the FRB to cooperate Dodd

INTEGRATED MORTGAGE DISCLOSURES (TILA RESPA RULE) Financial Solutions Patti Blenden April 2015 1 CFPB Accomplishes Integration of GFE/eTILA After 30 years of encouraging HUD and the FRB to cooperate Dodd

TRID: Caution Ahead. Katie Wechsler June, 2015. This article looks at the road ahead for homebuyers under the new TRID regime.

TRID: Caution Ahead Katie Wechsler June, 2015 When the Consumer Financial Protection Bureau s (CFPB) TILA-RESPA Integrated Disclosure Rule (TRID) is in effect, Americans seeking a home mortgage will be

TRID: Caution Ahead Katie Wechsler June, 2015 When the Consumer Financial Protection Bureau s (CFPB) TILA-RESPA Integrated Disclosure Rule (TRID) is in effect, Americans seeking a home mortgage will be

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

Key Components of TRID. Presented by: Benjamin K. Olson

Key Components of TRID Presented by: Benjamin K. Olson 1 TRID Effective Date and Enforcement June 17, 2015: CFPB Press Release CFPB Director announces proposal to delay effective date until October 1:

Key Components of TRID Presented by: Benjamin K. Olson 1 TRID Effective Date and Enforcement June 17, 2015: CFPB Press Release CFPB Director announces proposal to delay effective date until October 1:

PART 2: THE LOAN ESTIMATE. Integrated Disclosures Rule Effective August 1, 2015

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

Understanding the CFPB s TILA-RESPA Integrated Disclosures. Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp.

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

Mission: to make markets for consumer financial products and services work for Americans.

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

3/5/2015. Next Steps to prepare for compliance

NEW CLOSING DISCLOSURE FORMS Next Steps to prepare for compliance Presented by: Summary of where we are with the implementation of the new closing disclosure form promulgated by the CFPB Summary so far

NEW CLOSING DISCLOSURE FORMS Next Steps to prepare for compliance Presented by: Summary of where we are with the implementation of the new closing disclosure form promulgated by the CFPB Summary so far

TRID Consolidated Resources

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

TRID Consolidated Resources Annotated Forms for TILA RESPA Integrated Disclosure Closing Disclosure. 1 Annotated Forms for TILA RESPA Integrated Disclosure Loan Estimate.2 Closing Disclosure Form.. 3 Loan

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures. Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

INTEGRATED MORTGAGE DISCLOSURES CLOSING DISCLOSURE

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

INTEGRATED MORTGAGE DISCLOSURES TILA RESPA RULE CLOSING DISCLOSURE Financial Solutions Patti Blenden October 2014 1 September 2014 Guide The Loan Estimate and Closing Disclosure must be used for most closed

TILA-RESPA Integrated Mortgage Disclosures

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

7 business days after loan estimate delivery is the waiting period for consummation (loan closing) after the Loan Estimate Delivery

after the Loan Estimate Delivery") TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

CFPB Consumer Laws and Regulations

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

TRID Overview. Provided by Primary Capital Mortgage. Presented by Stacie Weider, Training Manager

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

THE NEW TILA/RESPA INTEGRATED DISCLOSURES

THE NEW TILA/RESPA INTEGRATED DISCLOSURES IN PLAIN ENGLISH TRID Workshop Finals E F F E C T I V E A U G U S T 1, 2 0 1 5 *PROPOSAL PENDING TO DELAY EFFECTIVE DATE UNTIL OCTOBER 3RD, 2015 WHAT YOU WILL

THE NEW TILA/RESPA INTEGRATED DISCLOSURES IN PLAIN ENGLISH TRID Workshop Finals E F F E C T I V E A U G U S T 1, 2 0 1 5 *PROPOSAL PENDING TO DELAY EFFECTIVE DATE UNTIL OCTOBER 3RD, 2015 WHAT YOU WILL

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

TILA-RESPA Integrated Mortgage Disclosures

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending NMLS #2129 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending NMLS #2129 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

Disclosure Process. 1 WSL:1241 Issued: 09/04/15

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

TRID Settlement Service Provider List (SSP List)

") TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TRID Survival Guide: Consumer Edition

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

TRID Survival Guide: Consumer Edition What you need to know about the TILA-RESPA Integrated Closing Disclosures. NFM Lending NMLS # 2893 Toll-Free: 1-888-233-0092 www.nfmlending.com Introduction NFM Lending

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS)

(CLOSED-END HOME MORTGAGE TRANSACTIONS)") QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

QUICK REFERENCE GUIDE TO DISCLOSURES TRUTH IN LENDING ACT AND REGULATION Z (1) (CLOSED-END HOME MORTGAGE TRANSACTIONS) Type of (2) Contents of Truth in Lending Statements 226.17 226.36 Early s 226.19(a)(1)

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015. Presenter: Bonnie S. Nachamie

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

Important Information Regarding TILA-RESPA Integrated Disclosure (TRID) Rule Notice to students: If your course contains information on the Truth in Lending Act (TILA) and the Real Estate Settlement Procedure

TRID In the Weeds. Article by Alice Alvey January 2015

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

July 2015. For questions or comments regarding this newsletter, contact Marketing@idsdoc.com 2015 IDS, Inc.

July 2015 For questions or comments regarding this newsletter, contact Marketing@idsdoc.com 2015 IDS, Inc. Still To Be TRID Ready Before August 1 Due to the recent press release from the CFPB of possibly

July 2015 For questions or comments regarding this newsletter, contact Marketing@idsdoc.com 2015 IDS, Inc. Still To Be TRID Ready Before August 1 Due to the recent press release from the CFPB of possibly

TILA-RESPA INTEGRATED DISCLOSURE RULE

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED

I. What is the CFPB? KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED For more than 30 years, federal law has required all lenders to provide two disclosure forms to consumers

I. What is the CFPB? KNOW BEFORE YOU CLOSE THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE EXPLAINED For more than 30 years, federal law has required all lenders to provide two disclosure forms to consumers

CFPB mortgage disclosure rules

www.pwc.com/consumerfinance www.pwcregulatory.com CFPB mortgage disclosure rules An analysis of the Consumer Financial Protection Bureau s Know Before You Owe disclosure forms March 2014 A joint point

www.pwc.com/consumerfinance www.pwcregulatory.com CFPB mortgage disclosure rules An analysis of the Consumer Financial Protection Bureau s Know Before You Owe disclosure forms March 2014 A joint point

Answer: ppddocs.com we don t endorse this site or this product, it is just a site we used to input examples for the webinar

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK FIS REGULATORY ADVISORY SERVICES

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

YOUR NEW MORTGAGE DISCLOSURE FORMS - AN IN-DEPTH LOOK BY FIS REGULATORY ADVISORY SERVICES 92012 Your New Mortgage Disclosure Forms An In Depth Look www.fisregulatoryservices.com i 1 Agenda Introduction

The Closing Disclosure

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

The Closing Disclosure Overview: The new TRID Regulation is effective for applications taken on October 3, 2015 and after. As a result, the GFE, TIL, and HUD-1 will no longer be issued. The Loan Estimate

FINANCE HELPLINE PRESENTS: TRID WHAT TO EXPECT ON AUG. 1ST finance.car.org (213) 739-8383 financehelpline@car.org

739-8383 financehelpline@car.org") FINANCE HELPLINE PRESENTS: TRID WHAT TO EXPECT ON AUG. 1ST finance.car.org (213) 739-8383 financehelpline@car.org Thank you for joining the Webinar! We will begin at 11:00 a.m. Your phone will be muted,

FINANCE HELPLINE PRESENTS: TRID WHAT TO EXPECT ON AUG. 1ST finance.car.org (213) 739-8383 financehelpline@car.org Thank you for joining the Webinar! We will begin at 11:00 a.m. Your phone will be muted,

CFPB-TRID Frequently Asked Questions April 29, 2015

CFPB-TRID Frequently Asked Questions April 29, 2015 Contents TILA-RESPA Integrated Disclosure Rule... 2 Effective Date(s)... 2 Impacted People, Property & Transaction Types... 2 Financing Type... 4 Seller

CFPB-TRID Frequently Asked Questions April 29, 2015 Contents TILA-RESPA Integrated Disclosure Rule... 2 Effective Date(s)... 2 Impacted People, Property & Transaction Types... 2 Financing Type... 4 Seller

Integrated Disclosure

Thursday, December 4, 2014 2 3 p.m. Central time Integrated Disclosure Sheldon Hendrix, CRCM Senior Managing Consultant BKD, LLP shendrix@bkd.com Michael Prince Senior Consultant II BKD, LLP mprince@bkd.com

Thursday, December 4, 2014 2 3 p.m. Central time Integrated Disclosure Sheldon Hendrix, CRCM Senior Managing Consultant BKD, LLP shendrix@bkd.com Michael Prince Senior Consultant II BKD, LLP mprince@bkd.com

PwC Perspectives CFPB s Integrated Mortgage Disclosures under RESPA/TILA Know Before You Owe Introduction Background of Know Before You Owe

PwC Perspectives CFPB s Integrated Mortgage Disclosures under RESPA/TILA Know Before You Owe Issue 1/September 2014 Implementing the simplified definition of an Application Introduction Welcome to the

PwC Perspectives CFPB s Integrated Mortgage Disclosures under RESPA/TILA Know Before You Owe Issue 1/September 2014 Implementing the simplified definition of an Application Introduction Welcome to the

Lesson 15: Closing Real Estate Transactions

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA TILA-RESPA INTEGRATED DISCLOSURE RULE BACKGROUND, TILA LIABILITIES & OPERATIONAL CONCERNS I. OVERVIEW

AMERICAN BAR ASSOCIATION CONSUMER FINANCIAL SERVICES COMMITTEE SPRING MEETING SAN FRANCISCO, CALIFIORNIA TILA-RESPA INTEGRATED DISCLOSURE RULE BACKGROUND, TILA LIABILITIES & OPERATIONAL CONCERNS I. OVERVIEW

November 6, 2012. The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702

November 6, 2012 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702 Re: Integrated Mortgage Disclosures under the Real Estate Settlement

November 6, 2012 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702 Re: Integrated Mortgage Disclosures under the Real Estate Settlement

Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID 1 TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID 1 TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

Provident Bank Mortgage Wholesale Operations FAQ s on TRID

Provident Bank Mortgage Wholesale Operations FAQ s on TRID General 1) Q: Can an email or other communication to the borrower provide a list of standard items that will be needed for the application (income/asset