Moderator: Carl A. Friedrich, FSA, MAAA. Presenters: Benjamin Goodman, FSA, MAAA Lane Kent

|

|

|

- Clinton McCoy

- 8 years ago

- Views:

Transcription

1 Session 39 PD, The Retirement Dilemma: Buying Longevity Products or Covering Your Health Care Costs Analysis from a Sales and Marketing Viewpoint Moderator: Carl A. Friedrich, FSA, MAAA Presenters: Benjamin Goodman, FSA, MAAA Lane Kent

2 Life Annuities 101 Benny Goodman PD 39 Monday, October 27 1:45PM 3PM

3 Life Expectancy 78? 85? 87? Probability 50% versus 75% Doing it on your own - 90%? 2

4 3 The Twin Sister Challenge - V1

5 Guarantee Periods Single Life Annuity $6,964 With 10 year guarantee $6,789 With 20 year guarantee $6,237 A 20 year guarantee ensures (and insures) your money back! 4

your")

6 5 The Twin Sister Challenge - V2

7 Framing Investment versus Consumption RoR versus spending Downside versus Upside Where is the real risk? Showing income on quarterly statements What is the plan really for? 6

8 The Income Floor Everyone has one Social Security is not enough Lifetime Annuity Floor varies by income level 7

9 Things to think about Health Who needs your money? Cognitive ability Live Longer! 8

10 Long Term Care Lane B. Kent, LTCP

11 The Long Term Care side of the Retirement dilemma Three big questions and then some discussion Why do we care? What s the problem? What can be done about it? 10

12 Why we care; The Chronic Care Risk The risk is real* 69% of those aged 65+ will require functional assistance before they die One-in-six will have costs of $100,000 or more One-in-twenty five will spend $250,000 or more The cost of care outweigh most families ability to self-insure the risk A private room cost an average of $248 daily, or more than $90,500 annually, according to a 2012 survey by MetLife. Home care costs anywhere from $18-$30 per hour depending upon location and provider experience/certification US Federal Government has acknowledged the problem, but has failed to provide a solution CLASS Act 2010 public insurance for disabled and aged, killed by legislative act in 2013 PPA 2007 clarified tax treatment of 1035 exchanges to certain policies with LTC benefit BBA 2003 expanded state/private Partnership plans HIPAA 1996 created Tax Qualified LTC insurance *Kemper P, Komisar HL, Alexcih L. Long-term care over an uncertain future: what can current retirees expect? Inquiry. 2006;42(4):

13 Why we care; US LTSS Landscape Total spend on LTSS is $363 billion* estimated to be ~$1 Trillion by 2050** ~7 Million covered with Private LTC insurance (of 309 Million = 2%) US Unfunded liabilities ~$127 Trillion Usdebtclock.org Dually eligible (Medicare & Medicaid) ~9 million, target of pilot programs evaluating the total of cost of care with patient-centered approach Graphic from SCAN foundation, as presented to LTC Discussion Group July 17, 2014 * Kemper, P. Komisar, H. and Alecxih, L **Frank RG. Long term care financing in the United States: sources and institutions.

14 Private LTCi, (not)trending Total claim payments of $3 billion in 2012, up 18% from 2011, but just 1% of the total costs. Reporting insurers have paid over $20 billion in claims through More Company exits in 2012; only 18 insurers reported new sales in 2013 and the top five writers account for over 75% of new premium. Product trends Gender-based pricing, removal of Life Time benefit period, just a few policies feature Cash benefit. Shift toward scheduled additional coverage purchases GPO/FPO (up from 13% to 20%), but compound inflation still being purchased despite the cost (56%), with 3% being bought now more than 5%. Average issue age has dropped to 56. Ages 45 to 59 account for just over 50% of all policies sold. Only 16% are over age 65 (this segment once accounted for over 70% of new sales) Average daily benefit amount is $160/day. Roughly 40% of couples bought shared care. The most popular duration for shared care is 4 years (1/3 of all shared care sales). Reflecting discontinuation of Lifetime benefits 2013 sales of ~175,000 new policies down 26% from 2012, pre 2003 levels 13 LIMRA 2012

, but compound inflation still being purchased despite the cost (56%), with 3% being bought now more than 5%.")

15 The problem; Private LTCi is in decline Challenging Regulatory framework (NAIC model, HIPAA) Benefit triggers for low level of dependence Mandate to offer inflation protection not reflective of economic realities Rate stability threshold is high Premium adjustment has political undercurrent Poor legacy product experience Missed lapse assumptions Underwriting too loose, then too stringent Bad actors exited business then engaged in extensive rerating Supply issues Little capacity (insurers and reinsurers) Low interest rate environment Rerating challenges Scarce domain knowledge (actuarial, underwriting, claims management, medical direction) Disenfranchised producers Demand issues Popular features withdrawn Product too expensive, average premium >$2300 annually Scarcity of discretionary funds to spend on insurance (the Retirement Dilemma) Lack of awareness of the need 14

Disenfranchised producers Demand issues Popular features withdrawn Product too expensive, average premium >$2300 annually Scarcity of")

16 What can be done; The discussion Leading Age and LTC commission, 7 Pathways Status Quo do nothing different Personal Responsibility reduce scope of government, everyone is on their own, figure it out Private Market take steps to strengthen private market (new tax incentives, mandate coverage, loosen regulation, etc.) Private Catastrophic redefine product as total loss of dependency, take steps to encourage purchase through private insurers Public Catastrophic same as Private Catastrophic with government as the insurer Common Good Government coverage for entire risk, funded through broad taxation Comprehensive elements of the above in some combination 15

17 What can be done Bias 20+ years in private industry, but material involvement in public policy efforts last 10 years Mandate coverage for working adults Supplement to Medicare for retirees Buy through workplace and exchanges Pretax, partial employee funded Progressive benefit triggers Cash model, emphasis on home based care, family support Cheaper and better product, deeper penetration Societal and Individual Preparedness Lift Medicare Lifetime SNF limit Standardize Home and Community Care waivers Standardize needs assessment process Reduce chronic care risk exposure for States, leaving them to focus on the poor and disabled Government care for total dependence 16

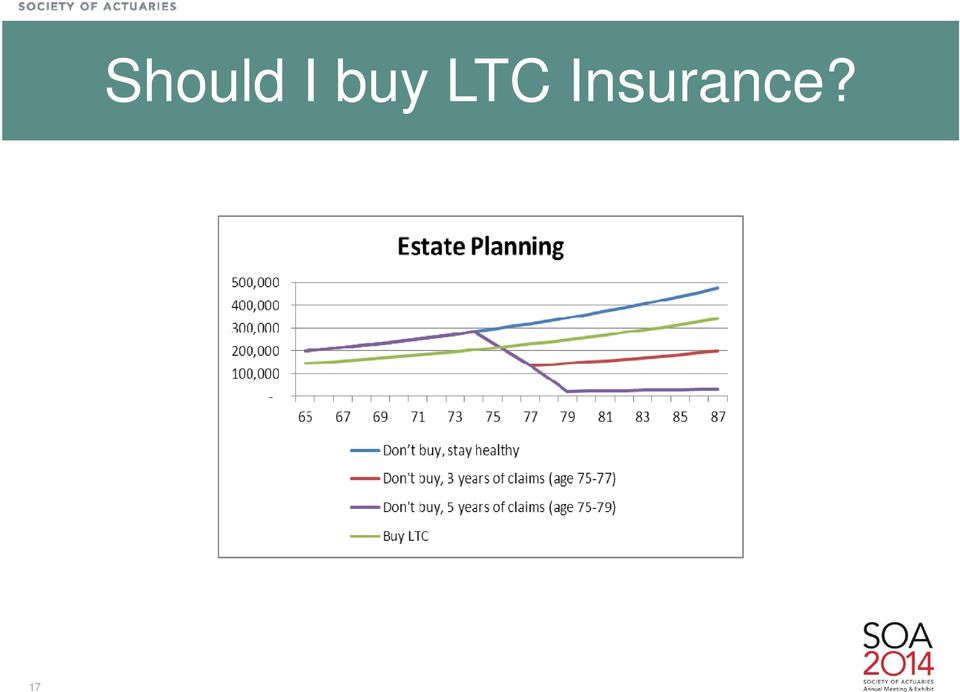

18 17 Should I buy LTC Insurance?

19 Combination Plans Several forms of coverage that package life or annuities with LTC First layer of coverage usually from acceleration of base plan assets As such, essentially represents a form of self-insurance Example 1: Deferred annuity coupled with LTC With no LTC event, policyholder can annuitize values for lifetime income With an LTC event, annuity values are drawn down, after which point independent monthly LTC benefits continue; the longevity concern is secondary in this scenario Example 2: Annuity doubler Payout annuity in place to provide lifetime income With an LTC event, payouts are doubled to address at least a portion of the cost of LTC The cost of the LTC coverage is reflected as a lower basic monthly payout (non-ltc claimants have a longer life expectancy, which should be reflected in the payouts) 18

20 Combination Plans Estate planning example 2 $150K nest egg to address LTC risk SPDA only, SPDA funding 6 year standalone LTC with 3% inflation, or Combo annuity with 2 year acceleration of AV and 4 year extension of benefit provision Issue age 65, claim age 80 19

21 Should I buy LTC or Combo Insurance? 400,000 Estate Planning 300, , ,000 (100,000) (200,000) (300,000) No LTC claim Annuity No LTC claim Annuity/LTC Combo Annuity paying LTC premium, with or without claim LTC Claim Annuity/LTC Combo LTC Claim with Annuity Only (400,000) (500,000) 20

22 Combination Plans Conclusions SPDA only is optimal if claims never occur, but $150K can be depleted in two years (or less) and the shortfall can be considerable with a longer term claim, depleting other assets or income Combo annuity reduces the nest egg gradually over time, caps the cost of LTC at the value of the nest egg, and covers excess costs thereafter LTC reduces the nest egg more quickly, but can cover the entire cost of LTC if purchased with inflation benefits Longevity concern is reduced after a LTC claim, but depletion of estate values and ability to cover LTC costs is the concern without some form of LTC insurance 21

23 The Dilemma The chronic care risk is real and must be addressed Longevity places new challenges on an already difficult problem to solve Addressing one risk while neglecting the other is nonsensical The insurance industry has yet to provide a complete solution so consumers are faced with this dilemma someone had to do something, its just incredibly pathetic it had to be us J. Garcia 22

Universal Life LTC Combinations & Annuity - LTC Combinations. Product Design, Distribution, Underwriting, and Marketing Considerations

Universal Life LTC Combinations & Annuity - LTC Combinations Product Design, Distribution, Underwriting, and Marketing Considerations Carl Friedrich November, 2007 II. Life/LTC Combination Products 2 Background

Universal Life LTC Combinations & Annuity - LTC Combinations Product Design, Distribution, Underwriting, and Marketing Considerations Carl Friedrich November, 2007 II. Life/LTC Combination Products 2 Background

... Life/Annuity Long-Term Care Combination Products. ... by Carl Friedrich +

Published in The Four Pillars Newsletter No. 51, September 2012....... Life/Annuity Long-Term Care Combination Products....... by Carl Friedrich + Despite the ageing of the American population and the

Published in The Four Pillars Newsletter No. 51, September 2012....... Life/Annuity Long-Term Care Combination Products....... by Carl Friedrich + Despite the ageing of the American population and the

Combination Products. Annuity Combos. Jeff Drake, OneAmerica. Jeff Funderburk, Genworth

Combination Products Annuity Combos Jeff Drake, OneAmerica Carl Friedrich, i Milliman Jeff Funderburk, Genworth March 23 3:45PM Combination Products Jeff Funderburk The Pension Protection Act (PPA) As

Combination Products Annuity Combos Jeff Drake, OneAmerica Carl Friedrich, i Milliman Jeff Funderburk, Genworth March 23 3:45PM Combination Products Jeff Funderburk The Pension Protection Act (PPA) As

Long-Term Care Insurance: Barriers to Purchase and Opportunities for Growth. Information Brief #2

Long-Term Care Insurance: Barriers to Purchase and Opportunities for Growth Information Brief #2 Presented to The Colorado Health Foundation By LifePlans, Inc. September, 2013 1 Introduction In an effort

Long-Term Care Insurance: Barriers to Purchase and Opportunities for Growth Information Brief #2 Presented to The Colorado Health Foundation By LifePlans, Inc. September, 2013 1 Introduction In an effort

How LTC Hybrid Products Really Work. Hybrids for Dummies

How LTC Hybrid Products Really Work Hybrids for Dummies AALTCI Producers Summit April 2011 Scott D. Boyd, LTCP, CSA V.P. LTC The National Benefit Corp This presentation is for Producer Use Only Not intended

How LTC Hybrid Products Really Work Hybrids for Dummies AALTCI Producers Summit April 2011 Scott D. Boyd, LTCP, CSA V.P. LTC The National Benefit Corp This presentation is for Producer Use Only Not intended

Financing Long Term Care Al Schmitz, FSA, MAAA Yung-Ping Chen, Ph.D. Bob Yee, FSA, MAAA

of the International Actuarial Association Financing Long Term Care Al Schmitz, FSA, MAAA Yung-Ping Chen, Ph.D. Bob Yee, FSA, MAAA Financing Proposal Summary* Private LTCI Promotion Standardized Policies

of the International Actuarial Association Financing Long Term Care Al Schmitz, FSA, MAAA Yung-Ping Chen, Ph.D. Bob Yee, FSA, MAAA Financing Proposal Summary* Private LTCI Promotion Standardized Policies

Request for Information Regarding Lifetime Income Options for Participants and Beneficiaries in Retirement Plans

Department of Labor and Department of the Treasury Re: RIN 1210 AB33 Request for Information Regarding Lifetime Income Options for Participants and Beneficiaries in Retirement Plans These comments are

Department of Labor and Department of the Treasury Re: RIN 1210 AB33 Request for Information Regarding Lifetime Income Options for Participants and Beneficiaries in Retirement Plans These comments are

Combination Products

Alternative Products Pi Pricing i Mechanics of Combination Products March 4, 2013 Dallas, Texas Moderator: Speakers: Missy Gordon, FSA, MAAA, Milliman Minneapolis Bruce Moon, ChFC, CLU, CASL, OneAmerica

Alternative Products Pi Pricing i Mechanics of Combination Products March 4, 2013 Dallas, Texas Moderator: Speakers: Missy Gordon, FSA, MAAA, Milliman Minneapolis Bruce Moon, ChFC, CLU, CASL, OneAmerica

Financing Options for Long Term Care Services and Supports

Financing Options for Long Term Care Services and Supports AARP National Policy Council Summer Meeting July 2013 LONG TERM CARE INSURANCE: INDUSTRY IN TRANSITION Talk about the industry s past, present

Financing Options for Long Term Care Services and Supports AARP National Policy Council Summer Meeting July 2013 LONG TERM CARE INSURANCE: INDUSTRY IN TRANSITION Talk about the industry s past, present

Life Insurance/LTC Combination Products A Pricing Perspective

Life Insurance/LTC Combination Products A Pricing Perspective Reid Settle, FSA, CERA, MAAA Core Life Product Development August 3, 2013 2013 Lincoln National Corporation The Need for Long-Term Care 70

Life Insurance/LTC Combination Products A Pricing Perspective Reid Settle, FSA, CERA, MAAA Core Life Product Development August 3, 2013 2013 Lincoln National Corporation The Need for Long-Term Care 70

Session 89 PD, Future of the Long-Term Care Insurance Industry Moderator: Allen J. Schmitz, FSA, MAAA

Session 89 PD, Future of the Long-Term Care Insurance Industry Moderator: Allen J. Schmitz, FSA, MAAA Presenters: Anthony C. Laudato, FSA, MAAA Allen J. Schmitz, FSA, MAAA The Future of the LTC Industry

Session 89 PD, Future of the Long-Term Care Insurance Industry Moderator: Allen J. Schmitz, FSA, MAAA Presenters: Anthony C. Laudato, FSA, MAAA Allen J. Schmitz, FSA, MAAA The Future of the LTC Industry

Mary, age 62, and Bob, age 65, have worked

Long-Term Care Insurance Could Montana s New Partnership Plan Have Helped the Smiths? by Jerry Furniss and Michael Harrington Editor s Note: On July 1, 2009, Montana joined 29 other states by having regulations

Long-Term Care Insurance Could Montana s New Partnership Plan Have Helped the Smiths? by Jerry Furniss and Michael Harrington Editor s Note: On July 1, 2009, Montana joined 29 other states by having regulations

Long Term Care Insurance Opportunities Under The Pension Protection Act

Long Term Care Insurance Opportunities Under The Pension Protection Act Presented [by/for]: [Type Your Name Here] Long Term Care Insurance Underwritten by Genworth Life Insurance Company, Richmond, VA

Long Term Care Insurance Opportunities Under The Pension Protection Act Presented [by/for]: [Type Your Name Here] Long Term Care Insurance Underwritten by Genworth Life Insurance Company, Richmond, VA

Is the LTC Market Dead? An Update on LTC. Introduction

Introduction Is the LTC Market Dead? An Update on LTC Steve Schoonveld, FSA, MAAA Head of Linked Benefit Product Solutions Lincoln Financial Group What is the Long-Term Care Insurance Market? Traditional

Introduction Is the LTC Market Dead? An Update on LTC Steve Schoonveld, FSA, MAAA Head of Linked Benefit Product Solutions Lincoln Financial Group What is the Long-Term Care Insurance Market? Traditional

The Current State of the Long-Term Care Insurance Market

The Current State of the Long-Term Care Insurance Market Presented to 14 th Annual Intercompany Long-Term Care Insurance Conference by Marc A. Cohen, PhD Ph.D. LifePlans, Inc. Rosen Centre Orlando, Florida

The Current State of the Long-Term Care Insurance Market Presented to 14 th Annual Intercompany Long-Term Care Insurance Conference by Marc A. Cohen, PhD Ph.D. LifePlans, Inc. Rosen Centre Orlando, Florida

Topics We ll Review. NGL background. Product design. Premiums. Underwriting

Product Overview The NGL product is pending state approval. National Guardian Life Insurance Company is not affiliated with The Guardian Life Insurance Company of America a.k.a. The Guardian or Guardian

Product Overview The NGL product is pending state approval. National Guardian Life Insurance Company is not affiliated with The Guardian Life Insurance Company of America a.k.a. The Guardian or Guardian

Comparing Long-Term Care Alternatives By Joe Tomlinson December 18, 2012

Comparing Long-Term Care Alternatives By Joe Tomlinson December 18, 2012 Should clients buy expensive long-term care insurance they might never need, or go without insurance and risk a big hit to their

Comparing Long-Term Care Alternatives By Joe Tomlinson December 18, 2012 Should clients buy expensive long-term care insurance they might never need, or go without insurance and risk a big hit to their

A Primer on Long-term Care Insurance

A Primer on Long-term Care Insurance What Is It? Long-term care insurance (LTCi) provides a daily financial benefit to cover the cost of long-term custodial care (LTC) for those who are unable to take

A Primer on Long-term Care Insurance What Is It? Long-term care insurance (LTCi) provides a daily financial benefit to cover the cost of long-term custodial care (LTC) for those who are unable to take

Alternative Products. Current LTC Alternatives: Short Term Care and Combination Products. Dawn Helwig, FSA, MAAA

Alternative Products Current LTC Alternatives: Short Term Care and Combination Products Dawn Helwig, FSA, MAAA Tony Laudato, FSA, MAAA Short Term Care Insurance Dawn E. Helwig, FSA, MAAA Milliman, Inc.

Alternative Products Current LTC Alternatives: Short Term Care and Combination Products Dawn Helwig, FSA, MAAA Tony Laudato, FSA, MAAA Short Term Care Insurance Dawn E. Helwig, FSA, MAAA Milliman, Inc.

Long Term Care Insurance: Factors Impacting Premiums and The Rationale for Rate Adjustments

Long Term Care Insurance: Factors Impacting Premiums and The Rationale for Rate Adjustments Amy Pahl, FSA, MAAA Principal and Consulting Actuary Milliman, Inc. Amy.Pahl@milliman.com (952) 820-2419 Prepared

Long Term Care Insurance: Factors Impacting Premiums and The Rationale for Rate Adjustments Amy Pahl, FSA, MAAA Principal and Consulting Actuary Milliman, Inc. Amy.Pahl@milliman.com (952) 820-2419 Prepared

Learning Objectives 26. What Is Insurance? 3. Coverage Concepts 8. Types of Insurance 10. Types of Insurers 11. Introduction 26

Contents u n i t 1 Introduction to Insurance 1 Introduction 2 Learning Objectives 2 What Is Insurance? 3 Risk 4 Coverage Concepts 8 Types of Insurance 10 Types of Insurers 11 Domicile and Authorization

Contents u n i t 1 Introduction to Insurance 1 Introduction 2 Learning Objectives 2 What Is Insurance? 3 Risk 4 Coverage Concepts 8 Types of Insurance 10 Types of Insurers 11 Domicile and Authorization

Quantification of the Natural Hedge Characteristics of Combination Life or Annuity Products Linked to Long- Term Care Insurance

Quantification of the Natural Hedge Characteristics of Combination Life or Annuity Products Linked to Long- Term Care Insurance Sponsored by The Society of Actuaries LTCI Section and The ILTCI Conference

Quantification of the Natural Hedge Characteristics of Combination Life or Annuity Products Linked to Long- Term Care Insurance Sponsored by The Society of Actuaries LTCI Section and The ILTCI Conference

The Current State of the. Private Long-Term Care Insurance Industry

The Current State of the Private Long-Term Care Insurance Industry Presented to The Long-Term Care Commission by Marc A. Cohen, Ph.D. LifePlans, Inc. June 27, 2013 Presentation Topics Current overview

The Current State of the Private Long-Term Care Insurance Industry Presented to The Long-Term Care Commission by Marc A. Cohen, Ph.D. LifePlans, Inc. June 27, 2013 Presentation Topics Current overview

Caution: Withdrawals made prior to age 59 ½ may be subject to a 10 percent federal penalty tax.

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Annuity Distributions What are annuity distributions? How are annuity distributions made? How are your annuity payouts computed if you elect to annuitize? Who are the parties to an annuity contract? How

Income Annuities: Market Opportunities & Product Trends

Income Annuities: Market Opportunities & Product Trends Atlanta Actuarial Club John Fenton David Beasley December 3, 2009 2009 Towers Perrin Overview of presentation Sizing the retirement market Product

Income Annuities: Market Opportunities & Product Trends Atlanta Actuarial Club John Fenton David Beasley December 3, 2009 2009 Towers Perrin Overview of presentation Sizing the retirement market Product

Alternative Products. Again? ILTCI Conference: March 5, 2013 3pm. Session 48: A Roundtable Discussion by Industry Experts.

Alternative Products Universal LTC: A New Product Idea Again? ILTCI Conference: March 5, 2013 3pm Session 48: A Roundtable Discussion by Industry Experts Moderator: Speakers: Jim Stoltzfus Carl Friedrich

Alternative Products Universal LTC: A New Product Idea Again? ILTCI Conference: March 5, 2013 3pm Session 48: A Roundtable Discussion by Industry Experts Moderator: Speakers: Jim Stoltzfus Carl Friedrich

Bridging the Gap LTC Combination Products

Bridging the Gap LTC Combination Products Session 28 : Current Topics in Mortality Tony Laudato, Vice President and Actuary Hannover Life Reassurance Company of America Valuation Actuary Symposium Indianapolis,

Bridging the Gap LTC Combination Products Session 28 : Current Topics in Mortality Tony Laudato, Vice President and Actuary Hannover Life Reassurance Company of America Valuation Actuary Symposium Indianapolis,

Findings. Who Buys Long-Term Care Insurance in 2010 2011?

Findings Who Buys Long-Term Care Insurance in 2010 2011? America s Health Insurance Plans Who Buys Long-Term Care Insurance in 2010-2011? is a twenty year study of the long-term care insurance marketplace

Findings Who Buys Long-Term Care Insurance in 2010 2011? America s Health Insurance Plans Who Buys Long-Term Care Insurance in 2010-2011? is a twenty year study of the long-term care insurance marketplace

Underwritten by Genworth Life Insurance Company

The Teacher Retirement System of Texas Group Long Term Care Insurance Program for New TRS Members Underwritten by Genworth Life Insurance Company 2007 Genworth Financial, Inc. All rights reserved. 45145

The Teacher Retirement System of Texas Group Long Term Care Insurance Program for New TRS Members Underwritten by Genworth Life Insurance Company 2007 Genworth Financial, Inc. All rights reserved. 45145

Valuation Actuary Symposium September 25-26, 2008. Session # 30 PD: Premium Deficiency Reserves for Health Insurance

Valuation Actuary Symposium September 25-26, 2008 Session # 30 PD: Premium Deficiency Reserves for Health Insurance Michael Weilant Norman Zwitter Moderator: Larry Pfannerstill Premium Deficiency Reserves

Valuation Actuary Symposium September 25-26, 2008 Session # 30 PD: Premium Deficiency Reserves for Health Insurance Michael Weilant Norman Zwitter Moderator: Larry Pfannerstill Premium Deficiency Reserves

What You Should Know About Long Term Care. Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

Long-term Care Insurance: A Product and Industry in Transition

Long-term Care Insurance: A Product and Industry in Transition Presented to NAIC Senior Issues Task Force by Marc A. Cohen, Ph.D. LifePlans, Inc. Gaylord Convention Center in National Harbor, Maryland

Long-term Care Insurance: A Product and Industry in Transition Presented to NAIC Senior Issues Task Force by Marc A. Cohen, Ph.D. LifePlans, Inc. Gaylord Convention Center in National Harbor, Maryland

Long-term Care. A product in transition. ASNY Spring Meeting

Long-term Care A product in transition ASNY Spring Meeting Agenda Section One Needs of LTCI Strong need due to increasing life expectancy Public options are not ideal Medicaid and Medicare are not enough

Long-term Care A product in transition ASNY Spring Meeting Agenda Section One Needs of LTCI Strong need due to increasing life expectancy Public options are not ideal Medicaid and Medicare are not enough

LTC/Combo Products on Life Insurance and Annuities- Understanding the Current Tax Laws and Defining Sales Opportunities

LTC/Combo Products on Life Insurance and Annuities- Understanding the Current Tax Laws and Defining Sales Opportunities Shawn Britt, CLU Director, Long-term Care Initiatives Advanced Consulting Group Nationwide

LTC/Combo Products on Life Insurance and Annuities- Understanding the Current Tax Laws and Defining Sales Opportunities Shawn Britt, CLU Director, Long-term Care Initiatives Advanced Consulting Group Nationwide

Corporate Benefit Funding

Corporate Benefit Funding > SECURE SOLUTIONS FOR TOMORROW AND BEYOND Corporate Benefit Funding > CBF > Corporate Benefit Funding > WHY METLIFE? For over 140 years, MetLife has been one of the country s

Corporate Benefit Funding > SECURE SOLUTIONS FOR TOMORROW AND BEYOND Corporate Benefit Funding > CBF > Corporate Benefit Funding > WHY METLIFE? For over 140 years, MetLife has been one of the country s

Deconstructing Long-Term Care Insurance

Insights November 2012 Deconstructing Long-Term Care Insurance In spite of the growing need for long-term care financing, two observations about the current state of long-term care insurance market are

Insights November 2012 Deconstructing Long-Term Care Insurance In spite of the growing need for long-term care financing, two observations about the current state of long-term care insurance market are

Moderator: Steven W. Schoonveld, FSA, MAAA. Presenters: John Cutler Anna M. Rappaport, FSA, MAAA Sandra Timmermann

Session 162 PD, Managing the Impact of Long-Term Care on Retirement Security Part 1: A Holistic and Multi-Generational View Moderator: Steven W. Schoonveld, FSA, MAAA Presenters: John Cutler Anna M. Rappaport,

Session 162 PD, Managing the Impact of Long-Term Care on Retirement Security Part 1: A Holistic and Multi-Generational View Moderator: Steven W. Schoonveld, FSA, MAAA Presenters: John Cutler Anna M. Rappaport,

Old versus New Insurance

Old versus New Insurance A Discussion of Chronic/LTC Riders Available Now Mike Pinkans, CFA, CFP Executive Vice President & CMO Life Insurance How many thought about the life insurance you own when you

Old versus New Insurance A Discussion of Chronic/LTC Riders Available Now Mike Pinkans, CFA, CFP Executive Vice President & CMO Life Insurance How many thought about the life insurance you own when you

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Provided to you by: H. Howard Rigg CFS,CRPS,RFC,CASL Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Written

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Provided to you by: H. Howard Rigg CFS,CRPS,RFC,CASL Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Written

Life and Annuity Market Update

Life and Annuity Market Update Southeastern Actuaries Club John Fenton, FSA, MAAA November 2014 OVERVIEW Overview of presentation U.S. Annuity Market Sales trends Key issues Products U.S. Life Market Sales

Life and Annuity Market Update Southeastern Actuaries Club John Fenton, FSA, MAAA November 2014 OVERVIEW Overview of presentation U.S. Annuity Market Sales trends Key issues Products U.S. Life Market Sales

Asset-based LTC solutions

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

The Truth About INSURANCE

INSURANCE The Truth About Annuities are one of the least known, least understood and most underutilized financial instruments. Yet as Paul Goldstein explains, in certain circumstances annuities should

INSURANCE The Truth About Annuities are one of the least known, least understood and most underutilized financial instruments. Yet as Paul Goldstein explains, in certain circumstances annuities should

A U.S. Perspective on Annuity Lifetime Income Guarantees

A U.S. Perspective on Annuity Lifetime Income Guarantees Jacob M. Herschler June 8, 2011 Mexico City Agenda Defined Benefit and Defined Contribution plan trends in the U.S. and prospects for longevity

A U.S. Perspective on Annuity Lifetime Income Guarantees Jacob M. Herschler June 8, 2011 Mexico City Agenda Defined Benefit and Defined Contribution plan trends in the U.S. and prospects for longevity

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011. Session 123 TS, Current Developments in Life Insurance Federal Income Tax

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011 Session 123 TS, Current Developments in Life Insurance Federal Income Tax Moderator: Christian J. DesRochers, FSA, MAAA Presenters: John T. Adney Christian

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011 Session 123 TS, Current Developments in Life Insurance Federal Income Tax Moderator: Christian J. DesRochers, FSA, MAAA Presenters: John T. Adney Christian

An Analysis of the Value of Private Long-Term Care Insurance

An Analysis of the Value of Private Long-Term Care Insurance Presented to Minnesota Department of Commerce Public Hearing Presented by: Marc A. Cohen, Ph.D. Chief Research and Development Officer August

An Analysis of the Value of Private Long-Term Care Insurance Presented to Minnesota Department of Commerce Public Hearing Presented by: Marc A. Cohen, Ph.D. Chief Research and Development Officer August

LTCI: Standard Products and new Developments

LTCI: Standard Products and new Developments Laure de MONTESQUIEU Scor Global Life Head of the International Research & Development Centre for Long Term Care Insurance Introduction: Long-Term Care, a problem

LTCI: Standard Products and new Developments Laure de MONTESQUIEU Scor Global Life Head of the International Research & Development Centre for Long Term Care Insurance Introduction: Long-Term Care, a problem

Asset-based LTC solutions

Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company I-21012 (IPR) For company use only. Not for

Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company I-21012 (IPR) For company use only. Not for

Annuity Owner Mistakes

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

thinking about your future? plan for your long-term care needs

Long-Term Care Services SM Rider thinking about your future? plan for your long-term care needs Life Insurance Products: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal

Long-Term Care Services SM Rider thinking about your future? plan for your long-term care needs Life Insurance Products: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal

The Hartford Income Security SM

The Hartford Income Security SM A Fixed Deferred Payout Annuity Prepare To Live SM For Use In All States, Except Florida Start Building Your Future Income Today There s never been a better time to begin

The Hartford Income Security SM A Fixed Deferred Payout Annuity Prepare To Live SM For Use In All States, Except Florida Start Building Your Future Income Today There s never been a better time to begin

Overview of Current Long-Term Care Financing Options

Overview of Current Long-Term Care Financing Options By Eileen J. Tell This series summarizes current issues in financing long-term care and outlines policy options for increasing affordable access to

Overview of Current Long-Term Care Financing Options By Eileen J. Tell This series summarizes current issues in financing long-term care and outlines policy options for increasing affordable access to

The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

Help your clients manage chronic illness costs with life insurance. Chronic Illness Rider Optional Living Benefits. Producer Guide

Help your clients manage chronic illness costs with life insurance. Chronic Illness Rider Optional Living Benefits Producer Guide Life insurance can leave a legacy. It can provide a living benefit too.

Help your clients manage chronic illness costs with life insurance. Chronic Illness Rider Optional Living Benefits Producer Guide Life insurance can leave a legacy. It can provide a living benefit too.

TAKING AN IN-DEPTH LOOK:

TAKING AN IN-DEPTH LOOK: LONG-TERM CARE RIDERS VS. CHRONIC ILLNESS RIDERS 1 TAKING AN IN-DEPTH LOOK: LONG-TERM CARE RIDERS VS. CHRONIC ILLNESS RIDERS FOR FINANCIAL PROFESSIONAL USE ONLY NOT FOR PUBLIC

TAKING AN IN-DEPTH LOOK: LONG-TERM CARE RIDERS VS. CHRONIC ILLNESS RIDERS 1 TAKING AN IN-DEPTH LOOK: LONG-TERM CARE RIDERS VS. CHRONIC ILLNESS RIDERS FOR FINANCIAL PROFESSIONAL USE ONLY NOT FOR PUBLIC

Chronic illness accelerated benefit riders

Prepared by: Carl Friedrich Teresa McNeela Chronic illness accelerated benefit riders is among the world's largest providers of actuarial and related products and services. The firm has consulting practices

Prepared by: Carl Friedrich Teresa McNeela Chronic illness accelerated benefit riders is among the world's largest providers of actuarial and related products and services. The firm has consulting practices

Partners in Planning: Life Insurance and Long-term Care

Partners in Planning: Life Insurance and Long-term Care From Nationwide Advanced Sales: The Specialists 1 hour CE Some things you need to know This presentation was not intended by the author to be used,

Partners in Planning: Life Insurance and Long-term Care From Nationwide Advanced Sales: The Specialists 1 hour CE Some things you need to know This presentation was not intended by the author to be used,

NAIC Center for Insurance Policy and Research Symposium

NAIC Center for Insurance Policy and Research Symposium Lifetime Income Insurance Products and Emerging Issues Mark Shemtob, MAAA, A.S.A., EA Member, Lifetime Income Risk Jt. Task Force May not be reproduced

NAIC Center for Insurance Policy and Research Symposium Lifetime Income Insurance Products and Emerging Issues Mark Shemtob, MAAA, A.S.A., EA Member, Lifetime Income Risk Jt. Task Force May not be reproduced

Americans love choice. We want the freedom to

Be Careful What Lump Sum From a Pension Plan May Not Be Best Choice Americans love choice. We want the freedom to choose everything what car to buy, where to live, what color to paint our houses. In retirement

Be Careful What Lump Sum From a Pension Plan May Not Be Best Choice Americans love choice. We want the freedom to choose everything what car to buy, where to live, what color to paint our houses. In retirement

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

NAIC Center for Insurance Policy and Research Symposium

NAIC Center for Insurance Policy and Research Symposium Lifetime Income Insurance Products and Emerging Issues Mark Shemtob, MAAA, A.S.A., EA Member, Lifetime Income Risk Jt. Task Force May not be reproduced

NAIC Center for Insurance Policy and Research Symposium Lifetime Income Insurance Products and Emerging Issues Mark Shemtob, MAAA, A.S.A., EA Member, Lifetime Income Risk Jt. Task Force May not be reproduced

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

billion, while annuity reserves (Table 8.2) increased 6 percent to $2.5 trillion.

increased 6 percent to $2.5 trillion.") 8annuities Annuities are financial contracts that pay a steady stream of income for either a fixed period of time or for the lifetime of the annuity owner (the annuitant). Most pension and retirement plan

8annuities Annuities are financial contracts that pay a steady stream of income for either a fixed period of time or for the lifetime of the annuity owner (the annuitant). Most pension and retirement plan

Designed for growth. Destined to provide. ULTRA INDEX SM UNIVERSAL LIFE INSURANCE LBL7376-2

Designed for growth. Destined to provide. PRODUCT OVERVIEW ULTRA INDEX SM UNIVERSAL LIFE INSURANCE Designed for growth. Destined to provide. Taking care of your family means more than protecting them.

Designed for growth. Destined to provide. PRODUCT OVERVIEW ULTRA INDEX SM UNIVERSAL LIFE INSURANCE Designed for growth. Destined to provide. Taking care of your family means more than protecting them.

Key to retiring with sufficient lifetime income is making good financial choices.

American Academy of Actuaries OCTOBER 2015 PLANNING THE RETIREMENT JOURNEY 1. When to retire 2. When to claim Social Security benefits 3. Planning for an unknown length of retirement 4. How much retirement

American Academy of Actuaries OCTOBER 2015 PLANNING THE RETIREMENT JOURNEY 1. When to retire 2. When to claim Social Security benefits 3. Planning for an unknown length of retirement 4. How much retirement

FAQ New Health Insurance Law

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

September 2014 Update. The Facts of Life and Annuities

September 2014 Update The Facts of Life and Annuities The Facts of Life and Annuities Introduction... 2 Key Facts... 2 Ownership Is Widespread, but Inadequate... 3-4 Most Individual Life Insurance Policies

September 2014 Update The Facts of Life and Annuities The Facts of Life and Annuities Introduction... 2 Key Facts... 2 Ownership Is Widespread, but Inadequate... 3-4 Most Individual Life Insurance Policies

Challenger Retirement Income Research. How much super does a retiree really need to live comfortably? A comfortable standard of living

14 February 2012 Only for use by financial advisers How much super does a retiree really need to live comfortably? Understanding how much money will be needed is critical in planning for retirement One

14 February 2012 Only for use by financial advisers How much super does a retiree really need to live comfortably? Understanding how much money will be needed is critical in planning for retirement One

The Benefits of Long-Term Care Insurance and What They Mean for Long-Term Care Financing. By LifePlans, Inc.

The Benefits of Long-Term Care Insurance and What They Mean for Long-Term Care Financing By LifePlans, Inc. November 214 LIST OF TABLES and figures Table 1. Key LTC Insurance Market Parameters, 212....

The Benefits of Long-Term Care Insurance and What They Mean for Long-Term Care Financing By LifePlans, Inc. November 214 LIST OF TABLES and figures Table 1. Key LTC Insurance Market Parameters, 212....

The State Life Insurance Company P. O. Box 6062 Indianapolis, IN 46206-6062

P. O. Box 6062 Indianapolis, IN 46206-6062 Life Insurance Illustration Single Premium Deferred Individual Retirement Annuity and Current Interest Whole Life Insurance with Long-Term Care Benefits for Either

P. O. Box 6062 Indianapolis, IN 46206-6062 Life Insurance Illustration Single Premium Deferred Individual Retirement Annuity and Current Interest Whole Life Insurance with Long-Term Care Benefits for Either

LONG-TERM CARE INSURANCE IN 2000-2001

Health Insurance Association of America EXECUTIVE SUMMARY RESEARCH FINDINGS LONG-TERM CARE INSURANCE IN 2000-2001 January 2003 1201 F Street, NW! Suite 500! Washington, D.C. 20004-1204! (202) 824-1600!

Health Insurance Association of America EXECUTIVE SUMMARY RESEARCH FINDINGS LONG-TERM CARE INSURANCE IN 2000-2001 January 2003 1201 F Street, NW! Suite 500! Washington, D.C. 20004-1204! (202) 824-1600!

LIFE TERM. Guaranteed Level Term. Protection. Flexibility. Value.

LIFE TERM Guaranteed Level Term Protection. Flexibility. Value. Life. your waysm Strive to live your dream and plan for the if in life. Discover the flexibility of life insurance protect and transfer wealth

LIFE TERM Guaranteed Level Term Protection. Flexibility. Value. Life. your waysm Strive to live your dream and plan for the if in life. Discover the flexibility of life insurance protect and transfer wealth

Taking the Long-Term Care Journey MANAGING RETIREMENT DECISIONS SERIES

Taking the Long-Term Care Journey MANAGING RETIREMENT DECISIONS SERIES Long-term care (Ltc) may not be the first thing people think about as they approach retirement, but it is a subject that may require

Taking the Long-Term Care Journey MANAGING RETIREMENT DECISIONS SERIES Long-term care (Ltc) may not be the first thing people think about as they approach retirement, but it is a subject that may require

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Eric J Malloy CRPC Annuity Owner Mistakes Written by Financial Educators Provided to you by Eric J Malloy CRPC 2

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Eric J Malloy CRPC Annuity Owner Mistakes Written by Financial Educators Provided to you by Eric J Malloy CRPC 2

SOA 2013 Life & Annuity Symposium May 6-7, 2013. Session 28 PD, Life Protection Product Update. Moderator: Robert P.

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 28 PD, Life Protection Product Update Moderator: Robert P. Stone, FSA, MAAA Presenters: Jeremy Allen Bill, FSA, MAAA Elizabeth H. MacGowan, FSA,

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 28 PD, Life Protection Product Update Moderator: Robert P. Stone, FSA, MAAA Presenters: Jeremy Allen Bill, FSA, MAAA Elizabeth H. MacGowan, FSA,

Northwestern Mutual Retirement Strategy. Retirement Income Planning with Confidence

Northwestern Mutual Retirement Strategy Retirement Income Planning with Confidence Over the past decade, the conventional approach to retirement planning has shifted. Retirement planning used to focus

Northwestern Mutual Retirement Strategy Retirement Income Planning with Confidence Over the past decade, the conventional approach to retirement planning has shifted. Retirement planning used to focus

CONGRESS What Do They Have In Store For Our 401(k) And 403(b) Plans? Richard S. Sych, F.S.A. President and Consulting Actuary April 2013

And 403(b) Plans? Richard S. Sych, F.S.A. President and Consulting Actuary April 2013") CONGRESS What Do They Have In Store For Our 401(k) And 403(b) Plans? Richard S. Sych, F.S.A. President and Consulting Actuary April 2013 Agenda Why All The Fuss? What s On The Table? What s Next? What

CONGRESS What Do They Have In Store For Our 401(k) And 403(b) Plans? Richard S. Sych, F.S.A. President and Consulting Actuary April 2013 Agenda Why All The Fuss? What s On The Table? What s Next? What

Long-Term Care Insurance:

The Prudential Insurance Company of America 2011 Long-Term Care Insurance: A Piece of the Retirement & Estate Planning Puzzle IRA Pension 401(k) Annuities Long-Term Care Insurance Life Insurance Social

The Prudential Insurance Company of America 2011 Long-Term Care Insurance: A Piece of the Retirement & Estate Planning Puzzle IRA Pension 401(k) Annuities Long-Term Care Insurance Life Insurance Social

Paying for Long-Term. Care. by Jon Caswell

F E A T U R E Paying for Long-Term by Jon Caswell Care any stroke families don t know how to care for a family member who can t handle a few activities of daily living (ADLs) but isn t so compromised that

F E A T U R E Paying for Long-Term by Jon Caswell Care any stroke families don t know how to care for a family member who can t handle a few activities of daily living (ADLs) but isn t so compromised that

What You Should Know About Long Term Care. Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

Chapter 14. Agenda. Individual Annuities. Annuities and Individual Retirement Accounts

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

Chapter 14 Annuities and Individual Retirement Accounts Agenda 2 Individual Annuities Types of Annuities Taxation of Individual Annuities Individual Retirement Accounts Individual Annuities 3 An annuity

Design your own retirement

Design your own retirement Lincoln Deferred Income Solutions SM Annuity Products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured May go down in value Not insured by

Design your own retirement Lincoln Deferred Income Solutions SM Annuity Products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured May go down in value Not insured by

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION TO THE SPECIAL COMMITTEE ON AGING AND THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION TO THE SPECIAL COMMITTEE ON AGING AND THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL

PORTFOLIO OVERVIEW. MutualCare Solutions Long-Term Care Insurance. Mutual of Omaha Insurance Company

MutualCare Solutions Long-Term Care Insurance Mutual of Omaha Insurance Company PORTFOLIO OVERVIEW M28381 For producer use only. Not for use with the general public. MutualCare Solutions It s a new approach

MutualCare Solutions Long-Term Care Insurance Mutual of Omaha Insurance Company PORTFOLIO OVERVIEW M28381 For producer use only. Not for use with the general public. MutualCare Solutions It s a new approach

Asset/liability Management for Universal Life. Grant Paulsen Rimcon Inc. November 15, 2001

Asset/liability Management for Universal Life Grant Paulsen Rimcon Inc. November 15, 2001 Step 1: Split the product in two Premiums Reinsurance Premiums Benefits Policyholder fund Risk charges Expense

Asset/liability Management for Universal Life Grant Paulsen Rimcon Inc. November 15, 2001 Step 1: Split the product in two Premiums Reinsurance Premiums Benefits Policyholder fund Risk charges Expense

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION CHOICE SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION CHOICE SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important

Indexed Annuity Care Producer Sales and Marketing Guide

Indexed Annuity Care Indexed Annuity Care Producer Sales and Marketing Guide Products and financial services provided by The State Life Insurance Company a OneAmerica company I-26075 For use with financial

Indexed Annuity Care Indexed Annuity Care Producer Sales and Marketing Guide Products and financial services provided by The State Life Insurance Company a OneAmerica company I-26075 For use with financial

10 MISTAKES PEOPLE MAKE IN RETIREMENT

10 MISTAKES PEOPLE MAKE IN RETIREMENT by Bill Elson, CFP 3705 Grand Avenue Des Moines, IA 50312 (515) 255-3306 or (800) 616-4392 belson@vsrfin.com KEYWORDS: RETIREMENT PLANNING, RETIREMENT INCOME, RETIREMENT

10 MISTAKES PEOPLE MAKE IN RETIREMENT by Bill Elson, CFP 3705 Grand Avenue Des Moines, IA 50312 (515) 255-3306 or (800) 616-4392 belson@vsrfin.com KEYWORDS: RETIREMENT PLANNING, RETIREMENT INCOME, RETIREMENT

Asset-based LTC solutions

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

California Department of Insurance Eight-Hour Mandatory Long-Term Care Course Attachment II

Tax Treatment of Long-Term Care Insurance & Expenses Introduction Federal and state tax codes have a purpose beyond raising revenue. Public policy is often served by providing economic relief to taxpayers

Tax Treatment of Long-Term Care Insurance & Expenses Introduction Federal and state tax codes have a purpose beyond raising revenue. Public policy is often served by providing economic relief to taxpayers

Life Settlements 101 Introduction to the Secondary Market in Life Insurance

Life Settlements 101 Introduction to the Secondary Market in Life Insurance Anita A Sathe, FSA, FCAS, MAAA Donald Solow, FSA, MAAA Michael Taht, FSA, FCIA, MAAA October 15, 2007 Presentation Outline History

Life Settlements 101 Introduction to the Secondary Market in Life Insurance Anita A Sathe, FSA, FCAS, MAAA Donald Solow, FSA, MAAA Michael Taht, FSA, FCIA, MAAA October 15, 2007 Presentation Outline History

Reinsurance Section News

Article from: Reinsurance Section News August 2005 Issue 56 A NEW MARKET FOR REINSURERS by David DiMartino challenges insurance companies face when participating in this immediate annuity market, and to

Article from: Reinsurance Section News August 2005 Issue 56 A NEW MARKET FOR REINSURERS by David DiMartino challenges insurance companies face when participating in this immediate annuity market, and to

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E B U Y E R S G U I D E TC27761(0906) Life is a journey. And while there are many unknowns along the way, you can be prepared. Preparations should

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E B U Y E R S G U I D E TC27761(0906) Life is a journey. And while there are many unknowns along the way, you can be prepared. Preparations should

GAO LONG-TERM CARE INSURANCE. Partnership Programs Include Benefits That Protect Policyholders and Are Unlikely to Result in Medicaid Savings

GAO United States Government Accountability Office Report to Congressional Requesters May 2007 LONG-TERM CARE INSURANCE Partnership Programs Include Benefits That Protect Policyholders and Are Unlikely

GAO United States Government Accountability Office Report to Congressional Requesters May 2007 LONG-TERM CARE INSURANCE Partnership Programs Include Benefits That Protect Policyholders and Are Unlikely

Ensuring Your Path. Solutions Protecting Life s Next Steps. The Guardian Life Insurance Company of America A LONG TERM CARE GUIDE FOR CONSUMERS

Ensuring Your Path Solutions Protecting Life s Next Steps Pub5889ICC (5/13) ICC13 LTCR 5889 2013 1438 The Guardian Life Insurance Company of America A LONG TERM CARE GUIDE FOR CONSUMERS The good news is

Ensuring Your Path Solutions Protecting Life s Next Steps Pub5889ICC (5/13) ICC13 LTCR 5889 2013 1438 The Guardian Life Insurance Company of America A LONG TERM CARE GUIDE FOR CONSUMERS The good news is

Planning for Long-Term Care

long-term care insuranceo october 2014 2 The Reality of Living Longer 4 Why Should You Consider Long-Term Care Coverage? 7 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care Summary

long-term care insuranceo october 2014 2 The Reality of Living Longer 4 Why Should You Consider Long-Term Care Coverage? 7 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care Summary

How To Use A Massmutual Whole Life Insurance Policy

An Educational Guide for Individuals Unlocking the value of whole life Whole life insurance as a financial asset Insurance Strategies Contents 3 Whole life insurance: A versatile financial asset 4 Providing

An Educational Guide for Individuals Unlocking the value of whole life Whole life insurance as a financial asset Insurance Strategies Contents 3 Whole life insurance: A versatile financial asset 4 Providing

For some reason, a majority of individuals

Life & Health Insurance Advisor info@mmibi.com momentousins.com Your future Our commitment Long-Term Care December 2010 Volume 8 Number 12 How to Get Long-Term Care Coverage Without Buying an LTC Policy

Life & Health Insurance Advisor info@mmibi.com momentousins.com Your future Our commitment Long-Term Care December 2010 Volume 8 Number 12 How to Get Long-Term Care Coverage Without Buying an LTC Policy